EXHIBIT 21.1

v

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

x | QUARTERLY REPORT UNDER SECTION 13 OR 15 (D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE QUARTERLY PERIOD ENDED SEPTEMBER 30, 2019

OR

¨ | TRANSITION REPORT UNDER SECTION 13 OR 15 (D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______ to _______.

Commission file number: 000-29219

VIKING ENERGY GROUP, INC. |

(Formerly Viking Investments Group, Inc.) (Exact name of registrant as specified in its charter) |

Nevada |

| 98-0199508 |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

15915 Katy Freeway, Suite 450 Houston, TX 77094 (Address of principal executive offices) |

(281) 404 4387 (Registrant’s telephone number, including area code) |

______________________________________________________________

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Not applicable. | Note applicable. | Not applicable. |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer | ¨ | Accelerated Filer | ¨ |

Non-Accelerated Filer | ¨ | Smaller Reporting Company | x |

|

| Emerging Growth Company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

APPLICABLE ONLY TO CORPORATE ISSUERS

As of November 1, the registrant had 96,276,947 shares of common stock outstanding.

| 2 |

Consolidated Balance Sheets |

|

| September 30, |

|

| December 31, |

| ||

|

| 2019 |

|

| 2018 |

| ||

|

| (unaudited) |

|

|

|

| ||

ASSETS |

|

|

|

|

|

| ||

Current assets: |

|

|

|

|

|

| ||

Cash |

| $ | 1,555,390 |

|

| $ | 4,009,892 |

|

Restricted cash |

|

| 6,088,859 |

|

|

| - |

|

Accounts receivable – oil and gas - net |

|

| 2,653,653 |

|

|

| 258,300 |

|

Prepaid expenses |

|

| 136,404 |

|

|

| 124,443 |

|

Total current assets |

|

| 10,434,306 |

|

|

| 4,392,635 |

|

|

|

|

|

|

|

|

|

|

Oil and gas properties, full cost method |

|

|

|

|

|

|

|

|

Proved developed producing oil and gas properties, net |

|

| 75,675,548 |

|

|

| 81,331,986 |

|

Proved undeveloped and non-producing oil and gas properties, net |

|

| 48,143,115 |

|

|

| 50,492,906 |

|

Total oil and gas properties, net |

|

| 123,818,663 |

|

|

| 131,824,892 |

|

|

|

|

|

|

|

|

|

|

Fixed assets, net |

|

| 534,829 |

|

|

| 200,243 |

|

Derivative asset |

|

| 101,726 |

|

|

| 681,776 |

|

Other assets |

|

| 71,594 |

|

|

| 110,194 |

|

TOTAL ASSETS |

| $ | 134,961,118 |

|

| $ | 137,209,740 |

|

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS’ DEFICIT |

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

|

|

|

|

Accounts payable |

| $ | 2,431,858 |

|

| $ | 2,549,280 |

|

Accrued expenses and other current liabilities |

|

| 2,145,033 |

|

|

| 1,014,661 |

|

Undistributed revenues and royalties |

|

| 1,746,255 |

|

|

| 1,207,605 |

|

Derivative liability |

|

| 1,683,980 |

|

|

| 2,531,718 |

|

Amount due to director |

|

| 590,555 |

|

|

| 395,555 |

|

Current portion of long-term debt and other short-term borrowings – net of debt discount |

|

| 40,241,800 |

|

|

| 11,805,582 |

|

Total current liabilities |

|

| 48,839,481 |

|

|

| 19,504,401 |

|

Long term debt - net of current portion and debt discount |

|

| 66,231,506 |

|

|

| 92,076,857 |

|

Operating lease liability |

|

| 323,642 |

|

|

| - |

|

Asset retirement obligation |

|

| 3,377,424 |

|

|

| 4,413,465 |

|

TOTAL LIABILITIES |

|

| 118,772,053 |

|

|

| 115,994,723 |

|

|

|

|

|

|

|

|

|

|

Commitments and contingencies (Note 8) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

Preferred stock, $0.001 par value, 5,000,000 shares authorized, 28,092 shares issued and outstanding as of September 30, 2019 and December 31, 2018 |

|

| 28 |

|

|

| 28 |

|

Common stock, $0.001 par value, 500,000,000 shares authorized, 96,276,947 and 90,989,025 shares issued and outstanding as of September 30, 2019 and December 31, 2018 respectively. |

|

| 96,277 |

|

|

| 90,989 |

|

Additional paid-in capital |

|

| 36,204,678 |

|

|

| 32,015,913 |

|

Accumulated deficit |

|

| (20,111,918 | ) |

|

| (10,891,913 | ) |

TOTAL STOCKHOLDERS’ EQUITY |

|

| 16,189,065 |

|

|

| 21,215,017 |

|

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY |

| $ | 134,961,118 |

|

| $ | 137,209,740 |

|

The accompanying notes are an integral part of these unaudited consolidated financial statements.

| 3 |

| Table of Contents |

Consolidated Statements of Operations (Unaudited) |

|

| Three months ended |

|

| Nine months ended |

| ||||||||||

|

| September 30, |

|

| September 30, |

| ||||||||||

|

| 2019 |

|

| 2018 |

|

| 2019 |

|

| 2018 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Revenue |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Oil and gas sales |

|

| 9,000,591 |

|

| $ | 1,895,932 |

|

| $ | 27,081,506 |

|

| $ | 6,376,501 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lease operating costs |

|

| 3,547,662 |

|

|

| 913,331 |

|

|

| 9,004,334 |

|

|

| 2,957,073 |

|

General and administrative |

|

| 1,076,287 |

|

|

| 1,364,779 |

|

|

| 3,367,591 |

|

|

| 3,391,240 |

|

Stock based compensation |

|

| 402,451 |

|

|

| 680,156 |

|

|

| 444,533 |

|

|

| 1,898,255 |

|

Depreciation, depletion and amortization |

|

| 2,379,725 |

|

|

| 412,669 |

|

|

| 6,978,604 |

|

|

| 1,362,306 |

|

Accretion - ARO |

|

| 72,042 |

|

|

| 40,081 |

|

|

| 230,269 |

|

|

| 137,858 |

|

Total operating expenses |

|

| 7,478,167 |

|

|

| 3,411,016 |

|

|

| 20,025,331 |

|

|

| 9,746,732 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income (loss) from operations |

|

| 1,522,424 |

|

|

| (1,515,084 | ) |

|

| 7,056,175 |

|

|

| (3,370,231 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other income (expense) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense |

|

| (3,278,555 | ) |

|

| (255,999 | ) |

|

| (9,602,522 | ) |

|

| (1,217,383 | ) |

Amortization of debt discount |

|

| (2,364,357 | ) |

|

| (1,420,459 | ) |

|

| (6,947,607 | ) |

|

| (4,059,563 | ) |

Change in fair value of derivatives |

|

| 5,539,255 |

|

|

| (342,318 | ) |

|

| 267,688 |

|

|

| (1,330,102 | ) |

Gain on disposal of assets |

|

| - |

|

|

| 555,548 |

|

|

| - |

|

|

| 613,589 |

|

Interest and other income |

|

| 363 |

|

|

| - |

|

|

| 6,261 |

|

|

| - |

|

Total other income (expense) |

|

| (103,294 | ) |

|

| (1,463,228 | ) |

|

| (16,276,180 | ) |

|

| (5,993,459 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) before income taxes |

|

| 1,419,130 |

|

|

| (2,978,312 | ) |

|

| (9,220,005 | ) |

|

| (9,363,690 | ) |

Income tax benefit (expense) |

|

| - |

|

|

| 33,548 |

|

|

| - |

|

|

| 910,827 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Income (loss) |

| $ | 1,419,130 |

|

| $ | (2,944,764 | ) |

| $ | (9,220,005 | ) |

| $ | (8,452,863 | ) |

Earnings (loss) per common share |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

| $ | 0.02 |

|

| $ | (0.03 | ) |

| $ | (0.10 | ) |

| $ | (0.11 | ) |

Weighted average number of common shares outstanding |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

| 92,586,983 |

|

|

| 84,561,061 |

|

|

| 91,632,904 |

|

|

| 79,979,011 |

|

The accompanying notes are an integral part of these unaudited consolidated financial statements.

| 4 |

| Table of Contents |

Consolidated Statements of Cash Flows (Unaudited) |

|

| Nine Months Ended |

| |||||

|

| September 30, |

| |||||

|

| 2019 |

|

| 2018 |

| ||

|

|

|

|

|

|

| ||

Cash flows from operating activities: |

|

|

|

|

|

| ||

Net loss |

| $ | (9,220,005 | ) |

| $ | (8,452,863 | ) |

Adjustments to reconcile net loss to cash provided by (used in) operating activities: |

|

|

|

|

|

|

|

|

Change in fair value of derivative liability |

|

| (267,688 | ) |

|

| 1,330,102 |

|

Stock based compensation |

|

| 444,533 |

|

|

| 1,898,255 |

|

Depreciation, depletion and amortization |

|

| 6,978,604 |

|

|

| 1,362,306 |

|

Amortization of operational right-of-use assets |

|

| 2,997 |

|

|

| - |

|

Gain on disposal of assets |

|

| - |

|

|

| (613,589 | ) |

Accretion – Asset retirement obligation |

|

| 230,269 |

|

|

| 137,858 |

|

Amortization of debt discount |

|

| 6,947,607 |

|

|

| 4,059,563 |

|

Changes in operating assets and liabilities |

|

|

|

|

|

|

|

|

Accounts receivable |

|

| (2,307,266 | ) |

|

| (154,772 | ) |

Prepaid expenses and other assets |

|

| 26,639 |

|

|

| (368,542 | ) |

Other receivable |

|

| - |

|

|

| 548,714 |

|

Accounts payable |

|

| (806,594 | ) |

|

| (1,198,555 | ) |

Accrued expenses and other current liabilities |

|

| 1,753,034 |

|

|

| 349,156 |

|

Deferred tax liability |

|

| - |

|

|

| (910,827 | ) |

Undistributed revenues and royalties |

|

| 538,650 |

|

|

| 77,167 |

|

Amounts due to directors |

|

| - |

|

|

| 39,993 |

|

Net cash provided by (used) in operating activities |

|

| 4,320,780 |

|

|

| (1,896,034 | ) |

|

|

|

|

|

|

|

|

|

Cash flows from investing activities: |

|

|

|

|

|

|

|

|

Investment in and acquisition of oil and gas properties |

|

| (4,641,453 | ) |

|

| (3,600,528 | ) |

Acquisition of fixed assets |

|

| - |

|

|

| (130,000 | ) |

Proceeds from sale of fixed assets |

|

| - |

|

|

| 45,000 |

|

Proceeds from sale of oil and gas interests |

|

| 552,966 |

|

|

| 1,332,995 |

|

Net cash used in investing activities |

|

| (4,088,487 | ) |

|

| (2,352,533 | ) |

|

|

|

|

|

|

|

|

|

Cash flows from financing activities: |

|

|

|

|

|

|

|

|

Proceeds from amount due to director |

|

| 195,000 |

|

|

| 583,000 |

|

Repayment of amount due to director |

|

| - |

|

|

| (1,312,908 | ) |

Proceeds from long term debt |

|

| 6,372,383 |

|

|

| 16,047,458 |

|

Debt issuance costs |

|

|

|

|

|

| (791,385 | ) |

Short term advance |

|

| 693,706 |

|

|

| - |

|

Repayment of long-term debt |

|

| (3,859,025 | ) |

|

| (8,199,989 | ) |

Net cash provided by financing activities |

|

| 3,402,064 |

|

|

| 6,326,176 |

|

|

|

|

|

|

|

|

|

|

Net increase (decrease) in cash |

|

| 3,634,357 |

|

|

| 2,077,609 |

|

Cash and Restricted Cash, beginning of period |

|

| 4,009,892 |

|

|

| 5,735,259 |

|

|

|

|

|

|

|

|

|

|

Cash and Restricted Cash, end of period |

| $ | 7,644,249 |

|

| $ | 7,812,868 |

|

Supplemental Cash Flow Information: |

|

|

|

|

|

|

|

|

Cash paid for: |

|

|

|

|

|

|

|

|

Interest |

| $ | 7,664,537 |

|

| $ | 1,059,616 |

|

Income taxes |

| $ | - |

|

| $ | - |

|

|

|

|

|

|

|

|

|

|

Supplemental disclosure of Non-Cash Investing and Financing Activities: |

|

|

|

|

|

|

|

|

Recognition of asset retirement obligation |

| $ | 94,796 |

|

| $ | 231,053 |

|

Recognition of right-of-use asset and lease liability |

| $ | 367,365 |

|

| $ | - |

|

Amortization of right-of-use asset and lease liability |

| $ | 43,723 |

|

| $ | - |

|

Purchase of transportation equipment through direct financing |

| $ | 56,760 |

|

| $ | - |

|

Proceeds from sale of oil and gas properties paid directly to reduce debt |

| $ | 3,800,000 |

|

| $ | - |

|

Elimination of asset retirement obligation associated with sale of assets |

| $ | 1,361,106 |

|

| $ | - |

|

Issuance of shares as discount on debt |

| $ | - |

|

| $ | 2,231,331 |

|

Issuance of shares as payment of interest on debt |

| $ | 620,508 |

|

| $ | - |

|

Issuance of warrants for services |

| $ | 167,151 |

|

| $ | - |

|

Issuance of warrants as discount on debt |

| $ | 3,129,012 |

|

| $ | 1,716,039 |

|

Accrual of debt issuance costs |

| $ | - |

|

| $ | 1,187,428 |

|

Debt refinanced through new credit facility |

| $ | 3,310,000 |

|

| $ | 7,633,389 |

|

Private placement debt exchanged for new private placement |

| $ | - |

|

| $ | 5,314,000 |

|

Purchase of working interest through new debt |

| $ | - |

|

| $ | 165,000 |

|

Issuance of shares for contract services |

| $ | - |

|

| $ | 55,000 |

|

Cashless exercise of warrants |

| $ | - |

|

| $ | 447 |

|

Accrued expenses exchanged for long term debt |

| $ | - |

|

| $ | 177,771 |

|

The accompanying notes are an integral part of these unaudited consolidated financial statements.

| 5 |

| Table of Contents |

Consolidated Statements of Changes in Stockholders’ Equity (Unaudited) |

For the nine months ended September 30, 2019

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Retained |

|

|

|

| ||||||||||||

|

| Preferred Stock |

|

| Common Stock |

|

| Additional Paid-in |

|

| Prepaid Equity-Based |

|

| Earnings (Accumulated |

|

| Total Stockholders' |

| ||||||||||||||

|

| Number |

|

| Amount |

|

| Number |

|

| Amount |

|

| Capital |

|

| Compensation |

|

| Deficit) |

|

| Equity |

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Balances at December 31, 2018 |

|

| 28,092 |

|

| $ | 28 |

|

|

| 90,989,025 |

|

| $ | 90,989 |

|

| $ | 32,015,913 |

|

| $ | - |

|

| $ | (10,891,913 | ) |

| $ | 21,215,017 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shares issued for services |

|

|

|

|

|

|

|

|

|

| 1,637,876 |

|

|

| 1,638 |

|

|

| 275,144 |

|

|

|

|

|

|

|

|

|

|

| 276,782 |

|

Shares issued for interest |

|

|

|

|

|

|

|

|

|

| 3,650,046 |

|

|

| 3,650 |

|

|

| 616,858 |

|

|

|

|

|

|

|

|

|

|

| 620,508 |

|

Warrants issued for services |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 167,751 |

|

|

|

|

|

|

|

|

|

|

| 167,751 |

|

Warrants issued as debt discouint |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 3,129,012 |

|

|

|

|

|

|

|

|

|

|

| 3,129,012 |

|

Net loss for the nine months ended September 30, 2019 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (9,220,005 | ) |

|

| (9,220,005 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balances at September 30, 2019 |

|

| 28,092 |

|

| $ | 28 |

|

|

| 96,276,947 |

|

| $ | 96,277 |

|

| $ | 36,204,678 |

|

| $ | - |

|

| $ | (20,111,918 | ) |

| $ | 16,189,065 |

|

For the nine months ended September 30, 2018

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Retained |

|

|

| |||||||||||

|

| Preferred Stock |

|

| Common Stock |

|

| Additional Paid-in |

|

| Prepaid Equity-Based |

|

| Earnings (Accumulated |

|

| Total Stockholders' |

| ||||||||||||||

|

| Number |

|

| Amount |

|

| Number |

|

| Amount |

|

| Capital |

|

| Compensation |

|

| Deficit) |

|

| Equity |

| ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Balances at December 31, 2017 |

|

| 28,092 |

|

| $ | 28 |

|

|

| 72,347,990 |

|

| $ | 72,348 |

|

| $ | 19,029,892 |

|

| $ | (11,827 | ) |

| $ | 3,417,872 |

|

| $ | 22,508,313.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accounting principle change relative to certain derivative liabilities - Note 2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 807,762 |

|

|

| 807,762 |

|

Shares issued for consulting services |

|

|

|

|

|

|

|

|

|

| 5,029,443 |

|

|

| 5,030 |

|

|

| 1,172,979 |

|

|

|

|

|

|

|

|

|

|

| 1,178,009 |

|

Shares issued as prepaid equity-based compensation |

|

|

|

|

|

|

|

|

|

| 250,000 |

|

|

| 250 |

|

|

| 54,750 |

|

|

| (55,000 | ) |

|

|

|

|

|

| - |

|

Shares issued as debt discount |

|

|

|

|

|

|

|

|

|

| 10,323,356 |

|

|

| 10,323 |

|

|

| 2,221,008 |

|

|

|

|

|

|

|

|

|

|

| 2,231,331 |

|

Warrants issued for services |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 653,419 |

|

|

|

|

|

|

|

|

|

|

| 653,419 |

|

Shares issued in cashless exercise of warrants |

|

|

|

|

|

|

|

|

|

| 447,591 |

|

|

| 447 |

|

|

| (447 | ) |

|

|

|

|

|

|

|

|

|

| - |

|

Warrants issued as debt discount |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 1,716,039 |

|

|

|

|

|

|

|

|

|

|

| 1,716,039 |

|

Amortization of prepaid equity-based compensation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 66,827 |

|

|

|

|

|

|

| 66,827 |

|

Net loss for the nine months ended September 30, 2018 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (8,452,863 | ) |

|

| (8,452,863 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balances at September 30, 2018 |

|

| 28,092 |

|

| $ | 28 |

|

|

| 88,398,380 |

|

| $ | 88,398 |

|

| $ | 24,847,640 |

|

| $ | - |

|

| $ | (4,227,229 | ) |

| $ | 20,708,837 |

|

The accompanying notes are an integral part of these unaudited consolidated financial statements.

| 6 |

| Table of Contents |

Notes to Consolidated Financial Statements (Unaudited) |

Note 1 Nature of Business and Going Concern

Viking Energy Group, Inc. (“Viking” or the “Company”) is engaged in the acquisition, exploration, development and production of oil and natural gas properties, both individually and through collaborative partnerships with other companies in this field of endeavor. Since the beginning of 2018 the Company has had the following related activities:

| · | On January 12, 2018, the Company, through its subsidiary Mid-Con Drilling, LLC (“Mid-Con Drilling”) completed an acquisition of a 100% working interest in seven new oil and gas leases in Woodson and Allen Counties in Eastern Kansas. |

|

|

|

| · | Effective February 1, 2018, the Company, through Mid-Con Drilling, closed on the acquisition of a working interest in a lease with access to the mineral rights (oil and gas) concerning approximately 80 acres of property in Douglas County in eastern Kansas. |

|

|

|

| · | On December 28, 2018, the Company, through its subsidiary Ichor Energy, LLC (“Ichor Energy”) completed an acquisition (the “Ichor Energy Acquisition”) of working interests in certain oil and gas leases in Texas (primarily in Orange and Jefferson Counties) and Louisiana (primarily in Calcasiue Parish), which include 58 producing wells and 31 salt water disposal wells. The properties produce hydrocarbons from known reservoirs/sands in the on-shore Gulf Coast region, with an average well depth in excess of 10,600 feet. |

|

|

|

| · | On May 1, 2019, the Company’s subsidiary, Mid-Con Development, LLC sold all of its interests in the oil and gas assets Mid-Con Development, LLC owned in Ellis and Rooks Counties, Kansas, consisting of working interests in approximately 41 oil leases comprising several thousand acres. |

|

|

|

| · | On May 10, 2019, Petrodome Louisiana Pipeline LLC ("Petrodome LA"), a subsidiary of the Company’s subsidiary, Petrodome Energy, LLC, acquired a majority working interest in 6 gas wells (including 2 producing gas wells), 1 producing oil well and 1 salt water disposal well located in the East Mud Lake Field in Cameron Parish, Louisiana, with leases to mineral rights (oil and gas) concerning approximately 765 acres. |

These accompanying consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. Although the Company had net income of $1,419,130 for the three months ended September 30, 2019, the Company had a net loss of $9,220,005 for the nine months ended September 30, 2019. Furthermore, as of September 30, 2019, the Company has a working capital deficiency in excess of $38,000,000. The largest components of current liabilities creating this deficiency are (a) notes payable with a face value aggregating approximately $15,000,000 due in August of 2020 and (b) a promissory note payable to the seller of the certain oil and gas interests purchased on December 28, 2018 in the amount of $23,777,948 with all principal and accrued interest due on the earlier of (i) the date the Company or one of its affiliates completes an acquisition with one or more of the Sellers for a purchase price equal to or greater than $50,000,000 or (ii) January 31, 2020.

| 7 |

| Table of Contents |

Management has evaluated these conditions and has developed a plan which, in part, address these obligations as follows:

| · | The terms of the $15 million notes which were initially due in August 2019 allowed for 50% of the principal to be converted into shares of the Company’s common stock at $0.20 per share, and also contained a provision whereby the Company had the right to extend the Maturity Date for one additional year to August of 2020. Consideration for the one-year extension was payment of the accrued interest, an increase in the interest rate to 12% for the extension period and the issuance of a warrant to purchase an additional 115,000 common shares per $100,000 of outstanding principal of each note on a pro rata basis. The Company elected to extend the Maturity Date and accomplished the payment of the accrued interest through the issuance of approximately 3,650,000 common shares and approximately $900,000 in cash. Effective as of October 31, 2019, all the warrant holders associated with these notes consented to a modification to the exercise price of these warrants from $0.20 to $0.10. Multiple warrant holders then elected to exercise 20,416,350 warrants for an aggregate exercise price of $2,041,635. As to $1,860,635 of such exercise price consideration, the applicable warrant holders agreed to pay such exercise price by reducing the principal amount owing by the Company to the warrant holders under the Notes. As to the balance of $181,000 of such exercise price consideration, the applicable warrant holders agreed to pay such amount in cash to the Company. |

| · | The acquisition of oil and gas assets in Texas and Louisiana (the Ichor Energy Acquisition) at the end of 2018 is believed to provide cash flow sufficient to not only satisfy the Company’s debt service associated with this acquisition, but to also fund a $12,000,000 development program to increase this purchased production beyond its current average daily production of 2,300 BOE and provide a quicker principal reduction, resulting in an increased equity position relative to these assets. The acquisition of Petrodome Energy LLC in 2017 and the oil and gas expertise retained by Petrodome at the end of 2017 provided an internal lease operating company to efficiently evaluate development opportunities. |

| · | The Company has a revolving credit facility with CrossFirst Bank, which was approved for $30,000,000. The balance outstanding at September 30, 2019 is approximately $7,990,000. On May 10, 2019, the Company entered into an amendment to this revolving credit facility to extend the final maturity date from June 30, 2020 to May 10, 2021, which provides the Company with an additional year to meet the cash demands associated with maturity. Additional funds could be made available to the Company for projects reviewed and approved by the lender. |

These conditions raise substantial doubt regarding the Company’s ability to continue as a going concern. The Company’s ability to continue as a going concern is dependent upon its ability to utilize the resources in place to generate future profitable operations, to develop additional acquisition opportunities, and to obtain the necessary financing to meet its obligations and repay its liabilities arising from business operations when they come due. Management believes the Company will be able to continue to develop new opportunities and will be able to obtain additional funds through debt and / or equity financings to facilitate its development strategy; however, there is no assurance of additional funding being available. These consolidated financial statements do not include any adjustments to the recorded assets or liabilities that might be necessary should the Company have to curtail operations or be unable to continue in existence.

Note 2 Summary of Significant Accounting Policies

a) Basis of Presentation

The accompanying unaudited consolidated financial statements of the Company have been prepared in accordance with generally accepted accounting principles in the United States of America (“GAAP”) and the interim reporting rules of the Securities and Exchange Commission (“SEC”) and should be read in conjunction with the audited financial statements and notes thereto contained in Viking’s latest Annual Report filed with the SEC on Form 10-K. In the opinion of management, all adjustments, consisting of normal recurring adjustments (unless otherwise indicated), necessary for a fair presentation of the financial position and the results of operations for the interim periods presented have been reflected herein. The results of operations for interim periods are not necessarily indicative of the results to be expected for the full year.

| 8 |

| Table of Contents |

b) Basis of Consolidation

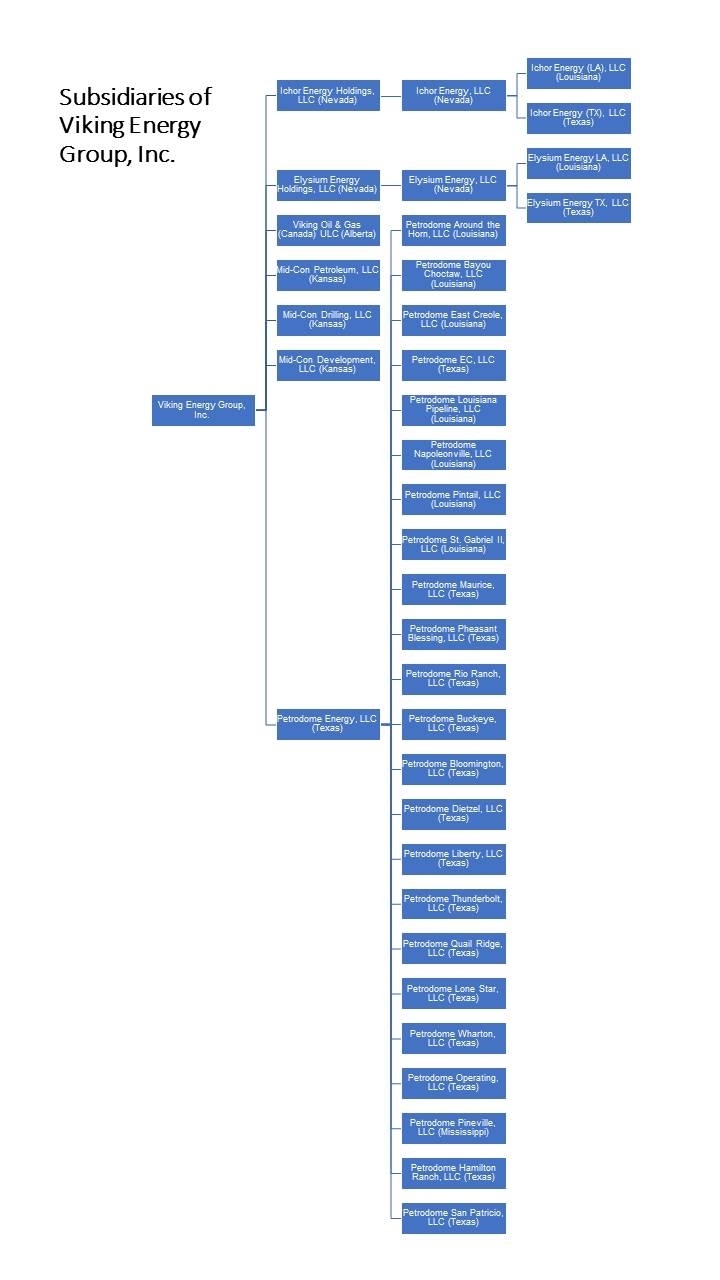

The financial statements presented herein reflect the consolidated financial results of the Company and its wholly owned subsidiaries: Viking Oil & Gas (Canada) ULC, a Canadian corporation formed to provide a base of operations for properties in Canada; Mid-Con Petroleum, LLC, Mid-Con Drilling, LLC, and Mid-Con Development, LLC, which were all formed to provide a base of operations for properties in the Central United States; and Petrodome Energy, LLC (and its subsidiaries) and Ichor Energy Holdings, LLC, its subsidiary Ichor Energy, LLC (Ichor Energy”), and Ichor Energy’s subsidiaries, Ichor Energy (TX), LLC, and Ichor Energy (LA), LLC, which provide a base of operations to facilitate property acquisitions in Texas, Louisiana and Mississippi. All significant intercompany transactions and balances have been eliminated.

c) Use of Estimates in the Preparation of Financial Statements

The preparation of consolidated financial statements in conformity with GAAP requires management to make certain estimates and assumptions that affect the reported amounts and timing of revenues and expenses, the reported amounts and classification of assets and liabilities, and disclosure of contingent assets and liabilities. Significant areas requiring the use of management estimates relate to impairment of long-lived assets, stock-based compensation, asset retirement obligations, and the determination of expected tax rates for future income tax recoveries.

The estimates of proved oil and gas reserves are used as significant inputs in determining the depletion of oil and gas properties and the impairment of proved oil and gas properties. There are numerous uncertainties inherent in the estimation of quantities of proved reserves and in the projection of future rates of production and the timing of development expenditures. Similarly, evaluations for impairment of proved oil and gas properties are subject to numerous uncertainties including, among others, estimates of future recoverable reserves and commodity price outlooks. Actual results could differ from the estimates and assumptions utilized.

d) Financial Instruments

The three levels of valuation hierarchy are defined as follows:

| · | Level 1: inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets. |

| · | Level 2: inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument. |

| · | Level 3: inputs to the valuation methodology are unobservable and significant to the fair value measurement. |

Assets and liabilities measured at fair value as of September 30, 2019 are classified below based on the three fair value hierarchy described above:

Description |

| Quoted Prices in Active Markets for Identical Assets (Level 1) |

|

| Significant Other Observable Inputs (Level 2) |

|

| Significant Unobservable Inputs (Level 3) |

|

| Total Gains (Losses) |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Financial Assets |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Commodity Derivative |

| $ | - |

|

| $ | 101,726 |

|

| $ | - |

|

| $ | (580,050 | ) |

|

| $ | - |

|

| $ | 101,726 |

|

| $ | - |

|

| $ | (580,050 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Financial liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commodity Derivative |

| $ |

|

|

| $ | 1,683,980 |

|

| $ | - |

|

| $ | 847,738 |

|

|

| $ | - |

|

| $ | 1,683,980 |

|

| $ | - |

|

| $ | 847,738 |

|

| 9 |

| Table of Contents |

Assets and liabilities measured at fair value as of December 31, 2018, are classified below based on the three-level fair value hierarchy described above:

Description |

| Quoted Prices in Active Markets for Identical Assets (Level 1) |

|

| Significant Other Observable Inputs (Level 2) |

|

| Significant Unobservable Inputs (Level 3) |

|

| Total Gains (Losses) |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Financial Assets |

|

|

|

|

|

|

|

|

|

|

|

| ||||

Commodity Derivative |

| $ | - |

|

| $ | 681,776 |

|

| $ | - |

|

| $ | 926,802 |

|

|

| $ | - |

|

| $ | 681,776 |

|

| $ | - |

|

| $ | 926,802 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Financial liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Commodity Derivative |

| $ | - |

|

| $ | 2,531,718 |

|

| $ | - |

|

| $ | (2,531,718 | ) |

|

| $ | - |

|

| $ | 2,531,718 |

|

| $ | - |

|

| $ | (2,531,718 | ) |

The Company has entered into certain commodity derivative instruments containing swaps and collars, which management believes are effective in mitigating commodity price risk associated with a portion of its future monthly natural gas and crude oil production and related cash flows. The Company does not designate its commodities derivative instruments as hedges and therefore does not apply hedge accounting. Changes in fair value of derivative instruments subsequent to the initial measurement are recorded as change in fair value on derivative liability, in other income (expense). The estimated fair value amounts of the Company’s commodity derivative instruments have been determined at discrete points in time based on relevant market information which resulted in the Company classifying such derivatives as Level 2. Although the Company’s commodity derivative instruments are valued using public indices, as well as the Black-Sholes model, the instruments themselves are traded with unrelated counterparties and are not openly traded on an exchange.

In a commodities swap agreement, the Company trades the fluctuating market prices of oil or natural gas at specific delivery points over a specified period, for fixed prices. As a producer of oil and natural gas, the Company holds these commodity derivatives to protect the operating revenues and cash flows related to a portion of its future natural gas and crude oil sales from the risk of significant declines in commodity prices, which helps reduce exposure to price risk and improves the likelihood of funding its capital budget. If the price of a commodity rises above what the Company has agreed to receive in the swap agreement, the amount that it agreed to pay the counterparty is expected to be offset by the increased amount it received for its production.

| 10 |

| Table of Contents |

The Company has also entered into collar agreements related to oil and gas production with established floors and ceilings. Upon settlement, if the current market price of the commodity is below the floor, the Company receives the difference. Conversely, if the current market price of the commodity is above the ceiling at settlement, the Company pays the excess over the ceiling price.

Although the Company is exposed to credit risk to the extent of nonperformance by the counterparties to these derivative contracts, the Company does not anticipate such nonperformance and monitors the credit worthiness of its counterparties on an ongoing basis.

The derivative assets were $101,726 and $681,776 as of September 30, 2019 and December 31, 2018, and the derivative liabilities were $1,683,980 and $2,531,718 as of September 30, 2019 and December 31, 2018 respectively. The change in the fair value of the derivative assets and liabilities for the nine months ended September 30, 2019 consisted of a decrease of $580,050 associated with existing commodity derivatives and an increase of $847,738 associated with the new commodity derivative related to the acquisition accomplished on December 28, 2018, and a gain recognized in the consolidated statement of operations in the amount of $267,688.

The table below is a summary of the Company’s commodity derivatives as of September 30, 2019:

Natural Gas |

| Period |

| Average MMBTU per Month |

| Fixed Price per MMBTU |

|

|

|

|

|

|

|

Swap |

| Dec-18 to Dec-22 |

| 118,936 |

| $2.715 |

|

|

|

|

|

|

|

Crude Oil |

| Period |

| Average BBL per Month |

| Price per BBL |

|

|

|

|

|

|

|

Swap |

| Dec-18 to Dec- 22 |

| 24,600 |

| $50.85 |

Swap |

| Dec-17 to Dec-19 |

| 1,400 |

| $54.77 |

Swap |

| Jan-20 to Jun-20 |

| 1,400 |

| $52.71 |

Collar |

| Dec-17 to Jun-20 |

| 4,000 |

| $55.00 / $72.00 |

Collar |

| Sep-17 to Sep-19 |

| 1,100 |

| $47.00 / $54.10 |

The carrying amounts reported in the consolidated balance sheets for accrued expenses and other current liabilities, accounts payable, derivative liabilities, amount due to director each qualify as financial instruments and are a reasonable estimate of their fair values because of the short period of time between the origination of such instruments and their expected realization and their current market rate of interest

e) Cash and Cash Equivalents

Cash and cash equivalents include cash in banks and highly liquid investment securities that have original maturities of three months or less. At September 30, 2019, the Company has cash deposits in excess of FDIC insured limits in the amounts of $6,314,524.

Restricted cash in the amount of $6,088,859 as of September 30, 2019 represents the balance of cash held by Ichor Energy, LLC (the “Borrower”) and/or its subsidiaries, generated through the operations of those subsidiaries. Pursuant to the Term Loan Credit Agreement to which the Borrower and its subsidiaries are parties, following March 31, 2019 the Borrower is required at all times to maintain a minimum cash balance of $2,000,000 (the “MLR”). Within 30 days of the end of each quarter, commencing with the quarter ended June 30, 2019, the Borrower is required to pay the lenders, as an additional principal payment on the debt, any cash in excess of (i) the MLR and (ii) any funds necessary for the capital expenditures contemplated to be expended in the next six month period by an approved plan of development (“APOD Capex Amount”). At September 30, 2019, the restricted cash did not exceed the MLR and the APOD Capex Amount.

| 11 |

| Table of Contents |

f) Accounts receivable

Accounts receivable consist of oil and gas receivables. The Company evaluates these accounts receivable for collectability and, when necessary, records allowances for expected unrecoverable amounts. The Company has recorded an allowance for doubtful accounts of $217,057 at September 30, 2019 and December 31, 2018 respectively.

g) Oil and Gas Properties

The Company uses the full cost method of accounting for its investment in oil and natural gas properties. Under this method of accounting, all costs associated with acquisition, exploration and development of oil and gas reserves, including directly related overhead costs, are capitalized. General and administrative costs related to production and general overhead are expensed as incurred.

All capitalized costs of oil and gas properties, including the estimated future costs to develop proved reserves, are amortized on the unit of production method using estimates of proved reserves. Disposition of oil and gas properties are accounted for as a reduction of capitalized costs, with no gain or loss recognized unless such adjustment would significantly alter the relationship between capitalized costs and proved reserves of oil and gas, in which case the gain or loss is recognized in operations. Unproved properties and major development projects are not amortized until proved reserves associated with the projects can be determined or until impairment occurs. If the results of an assessment indicate that the properties are impaired, the amount of the impairment is included in loss from operations before income taxes and the adjusted carrying amount of the unproved properties is amortized on the unit-of-production method.

Depreciation, depletion and amortization expense utilizing the unit-of-production method for the Company’s oil and gas properties for the three and nine months ended September 30, 2019 and 2018 were as follows:

|

| Three months ended |

|

| Nine months ended |

| ||||||||||

|

| September 30, |

|

| September 30, |

| ||||||||||

Cost Center |

| 2019 |

|

| 2018 |

|

| 2019 |

|

| 2018 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Canada |

| $ | - |

|

| $ | - |

|

| $ | - |

|

| $ | 21,387 |

|

United States |

|

| 2,379,725 |

|

|

| 412,669 |

|

|

| 6,978,604 |

|

|

| 1,340,919 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| $ | 2,379,725 |

|

| $ | 412,669 |

|

| $ | 6,978,604 |

|

| $ | 1,362,306 |

|

| 12 |

| Table of Contents |

h) Limitation on Capitalized Costs

Under the full-cost method of accounting, we are required, at the end of each reporting date, to perform a test to determine the limit on the book value of our oil and natural gas properties (the Ceiling test). If the capitalized costs of our oil and natural gas properties, net of accumulated amortization and related deferred income taxes, exceed the Ceiling, this excess or impairment is charged to expense. The expense may not be reversed in future periods, even though higher oil and natural gas prices may subsequently increase the Ceiling. The Ceiling is defined as the sum of:

(a) the present value, discounted at 10 percent, and assuming continuation of existing economic conditions, of 1) estimated future gross revenues from proved reserves, which is computed using oil and natural gas prices determined as the unweighted arithmetic average of the first-day-of-the-month price for each month within the 12-month hedging arrangements pursuant to SAB 103, less 2) estimated future expenditures (based on current costs) to be incurred in developing and producing the proved reserves, plus

(b) the cost of properties not being amortized; plus

(c) the lower of cost or estimated fair value of unproven properties included in the costs being amortized, net of

(d) the related tax effects related to the difference between the book and tax basis of our oil and natural gas properties.

i) Oil and Gas Reserves

Reserve engineering is a subjective process that is dependent upon the quality of available data and the interpretation thereof, including evaluations and extrapolations of well flow rates and reservoir pressure. Estimates by different engineers often vary sometimes significantly. In addition, physical factors such as the results of drilling, testing and production subsequent to the date of an estimate, as well as economic factors such as changes in product prices, may justify revision of such estimates. Because proved reserves are required to be estimated using recent prices of the evaluation, estimated reserve quantities can be significantly impacted by changes in product prices.

j) Income (loss) per Share

Basic net income (loss) per share is computed by dividing the net income (loss) by the weighted-average number of common shares outstanding during the period. Diluted net income (loss) per share is computed by dividing the net income (loss) by the weighted-average number of common shares outstanding and adjusted by any effects of warrants and options outstanding during the period, if dilutive. For the three months ended September 30, 2019 there were approximately 1,481 common stock equivalents that were dilutive; these dilutive shares were immaterial and omitted from the calculation of income per share for such period. For the nine months ended September 30, 2019 and 2018 there were approximately 109,649,190 and 40,807,159 common stock equivalents respectively, that were anti-dilutive.

k) Revenue Recognition

Sales of crude oil, natural gas, and natural gas liquids (NGLs) are included in revenue when production is sold to a customer in fulfillment of performance obligations under the terms of agreed contracts. Performance obligations primarily comprise delivery of oil, gas, or NGLs at a delivery point, as negotiated within each contract. Each barrel of oil, million BTU (MMBtu) of natural gas, or other unit of measure is separately identifiable and represents a distinct performance obligation to which the transaction price is allocated. Performance obligations are satisfied at a point in time once control of the product has been transferred to the customer. The Company considers a variety of facts and circumstances in assessing the point of control transfer, including but not limited to: whether the purchaser can direct the use of the hydrocarbons, the transfer of significant risks and rewards, the Company’s right to payment, and transfer of legal title. In each case, the time between delivery and when payments are due is not significant.

| 13 |

| Table of Contents |

The following table disaggregates the Company’s revenue by source for the nine months ended September 30, 2019 and 2018:

|

| Three months ended |

|

| Nine months ended |

| ||||||||||

|

| September 30, |

|

| September 30, |

| ||||||||||

|

| 2019 |

|

| 2018 |

|

| 2019 |

|

| 2018 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

| Oil |

| $ | 7,481,016 |

|

| $ | 1,872,636 |

|

| $ | 22,407,578 |

|

| $ | 6,145,546 |

|

| Natural gas and natural gas liquids |

|

| 1,519,575 |

|

|

| 23,296 |

|

|

| 4,673,928 |

|

|

| 230,955 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| $ | 9,000,591 |

|

| $ | 1,895,932 |

|

| $ | 27,081,506 |

|

| $ | 6,376,501 |

|

l) Income Taxes

The Company accounts for income taxes under the asset and liability method, which requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the consolidated financial statements. Under this method, the Company determines deferred tax assets and liabilities on the basis of the differences between the consolidated financial statements and the tax basis of assets and liabilities by using estimated tax rates for the year in which the differences are expected to reverse.

The Company recognizes deferred tax assets and liabilities to the extent that we believe that these assets and/or liabilities are more likely than not to be realized. In making such a determination, we consider all available positive and negative evidence, including future reversals of existing taxable temporary differences, projected future taxable income, tax planning strategies, and results of recent operations. If we determine that the Company would be able to realize our deferred tax assets in the future in excess of their net recorded amount, we would make an adjustment to the deferred tax asset valuation allowance, which would reduce the provision for income taxes.

In assessing the realizability of its deferred tax assets, management evaluated whether it is more likely than not that some portion, or all of its deferred tax assets, will be realized. The realization of its deferred tax assets relates directly to the Company’s ability to generate taxable income. The valuation allowance is then adjusted accordingly.

The Company has estimated net operating losses in excess of $12,000,000 at September 30, 2019. The potential benefit of these net operating losses has not been recognized in these financial statements because the Company cannot be assured it is more likely than not that it will utilize the net operating losses carried forward in future years. In December 2017, tax legislation was enacted limiting the deduction for net operating losses from taxable years beginning after December 31, 2017 to 80% of current year taxable income and eliminating net operating loss carrybacks for losses arising in taxable years ending after December 31, 2017 (though any such tax losses may be carried forward indefinitely). Net operating losses originating in taxable years beginning prior to January 1, 2018 are still subject to former carryover rules. The net operating loss carryforwards generated prior to this date of approximately $11,000,000, will expire between 2019 through 2038.

| 14 |

| Table of Contents |

m) Stock-Based Compensation

The Company may issue stock options to employees and stock options or warrants to non-employees in non-capital raising transactions for services and for financing costs. The cost of stock options and warrants issued to employees and non-employees is measured on the grant date based on the fair value. The fair value is determined using the Black-Scholes option pricing model. The resulting amount is charged to expense on the straight-line basis over the period in which the Company expects to receive the benefit, which is generally the vesting period.

The fair value of stock options and warrants is determined at the date of grant using the Black-Scholes option pricing model. The Black-Scholes option model requires management to make various estimates and assumptions, including expected term, expected volatility, risk-free rate, and dividend yield. The expected term represents the period of time that stock-based compensation awards granted are expected to be outstanding and is estimated based on considerations including the vesting period, contractual term and anticipated employee exercise patterns. Expected volatility is based on the historical volatility of the Company’s stock. The risk-free rate is based on the U.S. Treasury yield curve in relation to the contractual life of stock-based compensation instrument. The dividend yield assumption is based on historical patterns and future expectations for the Company dividends.

The following table represents stock warrant activity as of and for the nine months ended September 30, 2019:

|

| Number of Shares |

|

| Weighted Average Exercise Price |

|

| Weighted Average Remaining Contractual Life |

|

| Aggregate Intrinsic Value |

| ||||

Warrants Outstanding – December 31, 2018 |

|

| 54,821,690 |

|

| $ | 0.26 |

|

| 6.0 years |

|

| $ | - |

| |

Granted |

|

| 20,922,500 |

|

|

| 0.22 |

|

| 4.9 years |

|

|

| - |

| |

Exercised |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

Forfeited/expired/cancelled |

|

| - |

|

|

|

|

|

|

| - |

|

|

| - |

|

Warrants Outstanding – September 30, 2019 |

|

| 75,744,190 |

|

| $ | 0.25 |

|

| 5.2 years |

|

| $ | - |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Outstanding Exercisable – September 30, 2019 |

|

| 73,244,190 |

|

| $ | 0.25 |

|

| 5.2 years |

|

| $ | - |

| |

n) Impairment of long-lived assets

The Company is required to review its long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable through the estimated undiscounted cash flows expected to result from the use and eventual disposition of the assets. Whenever any such impairment exists, an impairment loss will be recognized for the amount by which the carrying value exceeds the fair value.

Assets are grouped and evaluated at the lowest level for their identifiable cash flows that are largely independent of the cash flows of other groups of assets. The Company considers historical performance and future estimated results in its evaluation of potential impairment and then compares the carrying amount of the asset to the future estimated cash flows expected to result from the use of the asset. If the carrying amount of the asset exceeds estimated expected undiscounted future cash flows, the Company measures the amount of impairment by comparing the carrying amount of the asset to its fair value. The estimation of fair value is generally determined by using the asset's expected future discounted cash flows or market value. The Company estimates fair value of the assets based on certain assumptions such as budgets, internal projections, and other available information as considered necessary. There is no impairment of long-lived assets during the nine months ended September 30, 2019 and 2018.

| 15 |

| Table of Contents |

o) Accounting for Asset Retirement Obligations

Asset retirement obligations (“ARO”) primarily represent the estimated present value of the amount the Company will incur to plug, abandon and remediate its producing properties at the projected end of their productive lives, in accordance with applicable federal, state and local laws. The Company determined its ARO by calculating the present value of estimated cash flows related to the obligation. The retirement obligation is recorded as a liability at its estimated present value as of the obligation’s inception, with an offsetting increase to proved properties.

The following table describes the changes in the Company’s asset retirement obligations for the nine months ended September 30, 2019:

|

| Nine months ended September 30, 2019 |

| |

|

|

|

| |

Asset retirement obligation – beginning |

| $ | 4,413,465 |

|

Oil and gas purchases |

|

| 94,796 |

|

Adjustments through disposals and settlements |

|

| (1,361,106 | ) |

Accretion expense |

|

| 230,269 |

|

|

|

|

|

|

Asset retirement obligation – ending |

| $ | 3,377,424 |

|

p) Undistributed Revenues and Royalties

The Company records a liability for cash collected from oil and gas sales that have not been distributed. The amounts get distributed in accordance with the working interests of the respective owners.

q) Recent Accounting Pronouncements

In February 2016, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update No. 2016-02 “Leases” (ASU 2016-02) and subsequently issued supplemental adoption guidance and clarification (collectively, Topic 842). Topic 842 amends a number of aspects of lease accounting, including requiring lessees to recognize right-of-use assets and lease liabilities for operating leases with a lease term greater than one year. Topic 842 supersedes Topic 840 “Leases.” On January 1, 2019, the Company adopted Topic 842 using the modified retrospective approach. Results for reporting periods beginning after January 1, 2019 are presented under Topic 842, while prior period amounts are not adjusted and continue to be reported in accordance with our historical accounting under Topic 840. We elected the package of practical expedients permitted under the transition guidance within Topic 842, which allowed us to carry forward the historical lease classification, retain the initial direct costs for any leases that existed prior to the adoption of the standard and not reassess whether any contracts entered into prior to the adoption are leases. We also elected to account for lease and non-lease components in our lease agreements as a single lease component in determining lease assets and liabilities. In addition, we elected not to recognize the right-of-use assets and liabilities for leases with lease terms of one year or less. Upon adoption of Topic 842, we recorded $367,365 of right-of-use assets and operating lease liabilities as of January 1, 2019. The adoption did not have a material impact on our Consolidated Statements of Operations or Consolidated Statements of Cash Flows

| 16 |

| Table of Contents |

r) Subsequent events

The Company has evaluated all subsequent events from September 30, 2019, through the date of filing this report, and determined there are no additional items to disclose other than those described in Note 9.

Note 3. Business Acquisition

Proforma unaudited condensed selected financial data for the nine months ended September 30, 2018 as though the Ichor Energy Acquisition had taken place at January 1, 2018 are as follows:

|

| Nine Months Ended September 30, 2018 |

| |

|

|

|

| |

Revenues |

| $ | 36,869,285 |

|

|

|

|

|

|

Net Income (excludes unrealized gains / losses) |

| $ | 2,819,852 |

|

|

|

|

|

|

Income per share |

| $ | 0.03 |

|

Note 4. Oil and Gas Properties

The following table summarizes the Company’s oil and gas activities by classification and geographical cost center for the nine months ended September 30, 2019:

|

| December 31, 2018 |

|

| Adjustments |

|

| Impairments |

|

| September 30, 2019 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

Proved developed producing oil and gas properties |

|

|

|

|

|

|

|

|

|

|

|

| ||||

United States cost center |

| $ | 81,936,721 |

|

| $ | (578,384 | ) |

| $ | - |

|

| $ | 81,358,337 |

|

Accumulated depreciation, depletion and amortization |

|

| (604,735 | ) |

|

| (5,078,054 | ) |

|

| - |

|

|

| (5,682,789 | ) |

Proved developed producing oil and gas properties, net |

| $ | 81,331,986 |

|

| $ | (5,656,438 | ) |

| $ | - |

|

| $ | 75,675,548 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Undeveloped and non-producing oil and gas properties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

United States cost center |

| $ | 51,973,719 |

|

| $ | (496,028 | ) |

| $ | - |

|

| $ | 51,477,691 |

|

Accumulated depreciation, depletion and amortization |

|

| (1,480,813 | ) |

|

| (1,853,763 | ) |

|

| - |

|

|

| (3,334,576 | ) |

Undeveloped and non-producing oil and gas properties, net |

| $ | 50,492,906 |

|

| $ | (2,349,791 | ) |

| $ | - |

|

| $ | 48,143,115 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Oil and Gas Properties, Net |

| $ | 131,824,892 |

|

| $ | (8,006,229 | ) |

| $ | - |

|

| $ | 123,818,663 |

|

| 17 |

| Table of Contents |

Note 5. Related Party Transactions

The Company’s CEO and director, James Doris has incurred expenses on behalf of, and made advances to, the Company in order to provide the Company with funds to carry on its operations. Additionally, Mr. Doris has made several loans through promissory notes to the Company, all accruing interest at 12%, and payable on demand. As of September 30, 2019, the total amount due to Mr. Doris for these loans is $590,555. Accrued interest of $84,642 is included in accrued expenses and other current liabilities at September 30, 2019.

The Company’s CFO, Frank W. Barker, Jr., renders professional services to the Company through FWB Consulting, Inc., an affiliate of Mr. Barker’s. As of September 30, 2019, the total amount due to FWB Consulting, Inc. is $173,216 and is included in accounts payable.

Note 6. Capital Stock and Additional Paid-in Capital

(a) Preferred Stock

The Company is authorized to issue 5,000,000 shares of Preferred Stock, par value $0.001 per share (the “Preferred Stock”), of which 50,000 have been designated as Series C Preferred Stock (the “Series C Preferred Stock”). Pursuant to the amended Certification of Designation of the Series C Preferred Stock filed on September 5, 2019, each share of Series C Preferred Stock entitles the holder thereof to 32,500 votes on all matters submitted to the vote of the stockholders of the Company. Each share of Series C Preferred Stock is convertible, at the option of the holder, at any time after the date of issuance of such share, at the office of the Company or any transfer agent for such stock, into one share of fully paid and non-assessable common stock.

(b) Common Stock

On November 5, 2018, the Company amended its Articles of Incorporation to increase the number of shares of common stock the Company is authorized to issue from 100,000,000 to 500,000,000.

During the nine months ended September 30, 2019, the Company issued shares of its common stock as follows:

· 1,637,876 shares of common stock issued for services valued at fair market value on the date of the transactions, totaling $276,782. · 3,650,046 shares of common stock issued for accrued interest on promissory notes.

During the nine months ended September 30, 2018, the Company issued shares of its common stock as follows:

| · | 5,029,443 shares of common stock issued for services valued at fair market value on the date of the transactions, totaling $1,178,009. |

|

|

|

| · | 250,000 shares of common stock issued as prepaid equity-based compensation valued at fair market value at the date of the transaction, totaling $55,000. |

|

|

|

| · | 10,323,356 shares of common stock issued as debt discount valued at fair market value on the date of each transactions, totaling $2,231,331. |

|

|

|

| · | 447,591 shares of common stock issued in a cashless exercise of warrants. |

| 18 |

| Table of Contents |

Note 7. Long Term Debt and other short-term borrowings

Long term debt and other short-term borrowings consisted of the following at September 30, 2019 and December 31, 2018:

|

| September 30, 2019 |

|

| December 31, 2018 |

| ||

|

|

|

|

|

|

| ||

Long-term debt: |

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

During June through December of 2018, the Company borrowed $9,459,750 from private lenders, and exchanged $5,514,000 of amounts due lenders from prior borrowings as well as $191,250 in accrued interest, pursuant to a 10% Secured Promissory Note with 50% of the principal convertible into the Company’s common stock at $0.20 per share, all principal and accrued interest payable on the initial maturity date of August 31, 2019. Concurrently, the Company issued the Note holders 11,373,750 warrants (5-year term and an exercise price of $0.20 per share). On August 31, 2019, the Company, pursuant to the terms of the notes, elected to extend the maturity date to August 31, 2020, by increasing the interest rate to 12%, and issuing the Note holders an additional 115,000 warrants (5-year term and an exercise price of $0.20 per share) for every $100,000 invested, resulting in an additional 17,422,500 new warrants. The fair value of all these warrants was recorded as a debt discount and amortized over the life of the notes. The balance shown is net of unamortized discount of $2,872,536 at September 30, 2019 and $5,981,012 at December 31, 2018. |

|

| 12,277,464 |

|

|

| 9,168,988 |

|

|

|

|

|

|

|

|

|

|

On June 13, 2018, the Company borrowed $12,400,000 pursuant to a revolving line of credit facility with a maximum principal amount of $30,000,000 from Crossfirst Bank, bearing interest 1.5% above a base rate equal to the prime rate of interest published by the Wall Street Journal, interest only for June and July of 2018, at which time Principal is payable at $100,000 monthly through the maturity date of May 10, 2021, at which time all remaining unpaid principal and accrued interest shall be due. The balance shown is net of unamortized discount of $51,805 at September 30, 2019 and $103,421 at December 31, 2018 |

|

| 7,938,195 |

|

|

| 11,728,911 |

|

|

|

|

|

|

|

|

|

|

On December 28, 2018, to facilitate the acquisition of certain oil and gas assets, the Company, through one of its subsidiaries, Ichor Energy LLC, entered into a Term Loan Credit Agreement with various lenders represented by ABC Funding, LLC as administrative agent. The agreement provides for a total loan amount of $63,592,000, bearing interest at a rate per annum equal to the greater of (i) a floating rate of interest equal to 10% plus LIBOR, and (ii) a fixed rate of interest equal to 12%, payable monthly on the last day of each calendar month, commencing January 31, 2019. Principal payments are made quarterly at 1.25% of the initial loan amount, commencing on the last business day of the fiscal quarter ending June 30, 2019. Cash generated from the operation of these assets is restricted to lease operating expenses, the payment of debt service on the Term Loan, approximately $12,000,000 of oil and gas development projects approved by the lender, and distributions to the Company of $65,000 per month for general and administrative expenses, and a quarterly tax distribution at the current statutory rates. Within 30 days of the end of each quarter, commencing with the quarter ended June 30, 2019, Ichor Energy, LLC is required to pay, as an additional principal payment on the debt, any cash in excess of the MLR and the APOD Capex Amount. To the extent not previously paid, all loans under the Loan Agreement shall be due and payable on the December 28, 2023 (the Maturity Date). The balance shown is net of unamortized discount of $3,728,679 at September 30, 2019 and $4,385,408 at December 31, 2018. |

|

| 58,273,523 |

|

|

| 59,206,592 |

|

| 19 |

| Table of Contents |

|

|

|

|

|

|

|

|

|