UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| [X] | QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended January 31, 2020

| [ ] | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________ to ________

Commission file number 001-36138

ADVAXIS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 02-0563870 | |

| (State or other jurisdiction | (IRS Employer | |

| of incorporation or organization) | Identification No.) |

| 305 College Road East, Princeton, NJ | 08540 | |

| (Address of principal executive offices) | (Zip Code) |

(609) 452-9813

(Registrant’s telephone number)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Stock, par value $0.001 per share | ADXS | NASDAQ Global Select Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | [ ] | Accelerated Filer | [ ] | |

| Non-accelerated Filer | [X] | Smaller Reporting Company | [X] | |

| Emerging growth company | [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.[ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The number of shares of the registrant’s Common Stock, $0.001 par value, outstanding as of February 29, 2020 was 60,244,843.

TABLE OF CONTENTS

| Page No. | ||

| PART I | FINANCIAL INFORMATION | 5 |

| Item 1. | Financial Statements (unaudited) | 5 |

| Condensed Balance Sheets | 5 | |

| Condensed Statements of Operations | 6 | |

| Condensed Statements of Cash Flows | 7 | |

| Notes to the Condensed Financial Statements | 8 | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 18 |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 24 |

| Item 4. | Controls and Procedures | 24 |

| PART II | OTHER INFORMATION | 25 |

| Item 1. | Legal Proceedings | 25 |

| Item 1A. | Risk Factors | 25 |

| Item 6. | Exhibits | 25 |

| SIGNATURES | 26 | |

| 2 |

CAUTIONARY NOTE REGARDING FORWARD LOOKING-STATEMENTS

This quarterly report on Form 10-Q (“Form 10-Q”) includes statements that are, or may be deemed, “forward-looking statements.” In some cases, these forward-looking statements can be identified by the use of such terms as “believes,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” “approximately” or, in each case, their negative or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. They appear in a number of places throughout this Form 10-Q and include statements regarding our intentions, beliefs, projections, outlook, analyses or current expectations concerning, among other things, our ongoing and planned discovery and development of drug candidates, the strength and breadth of our intellectual property, our ongoing and planned preclinical studies and clinical trials, the timing of and our ability to make regulatory filings and obtain and maintain regulatory approvals for our product candidates, the degree of clinical utility of our product candidates, particularly in specific patient populations, expectations regarding clinical trial data, our results of operations, financial condition, our available cash, liquidity, prospects, growth and strategies, the length of time that we will be able to continue to fund our operating expenses and capital expenditures, our expected financing needs and sources of financing, the industry in which we operate and the trends that may affect our industry or us.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events, competitive dynamics, and healthcare, regulatory and scientific developments and depend on the economic circumstances that may or may not occur in the future or may occur on longer or shorter timelines than anticipated. Although we believe that we have a reasonable basis for each forward-looking statement contained in this Form 10-Q, we caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and the development of the industry in which we operate, may differ materially from the forward-looking statements contained in this Form 10-Q. In addition, even if our results of operations, financial condition and liquidity, and the development of the industry in which we operate, are consistent with the forward-looking statements contained in this Form 10-Q, they may not be predictive of results or developments in future periods.

Some of the factors that we believe could cause actual results to differ from those anticipated or predicted include:

| ● | the success and timing of our clinical trials, including patient accrual; | |

| ● | our ability to obtain and maintain regulatory approval or reimbursement of our product candidates for marketing; | |

| ● | our ability to obtain the appropriate labeling of our products under any regulatory approval; | |

| ● | our ability to develop and commercialize our products; | |

| ● | the successful development and implementation of our sales and marketing campaigns; | |

| ● | the change of key scientific or management personnel; | |

| ● | the size and growth of the potential markets for our product candidates and our ability to serve those markets; | |

| ● | our ability to successfully compete in the potential markets for our product candidates, if commercialized; | |

| ● | regulatory developments in the United States and other countries; | |

| ● | the rate and degree of market acceptance of any of our product candidates; | |

| ● | new products, product candidates or new uses for existing products or technologies introduced or announced by our competitors and the timing of these introductions or announcements; | |

| ● | market conditions in the pharmaceutical and biotechnology sectors; | |

| ● | our available cash; | |

| ● | the accuracy of our estimates regarding expenses, future revenues, capital requirements and needs for additional financing; | |

| ● | our ability to obtain additional funding; | |

| ● | our ability to obtain and maintain intellectual property protection for our product candidates; | |

| ● | the success and timing of our preclinical studies, including IND enabling studies; |

| 3 |

| ● | the ability of our product candidates to successfully perform in clinical trials and to resolve any clinical holds that may occur; | |

| ● | our ability to obtain and maintain approval of our product candidates for trial initiation; | |

| ● | our ability to manufacture and the performance of third-party manufacturers; | |

| ● | our ability to identify license and collaboration partners and to maintain existing relationships; | |

| ● | the performance of our clinical research organizations, clinical trial sponsors, clinical trial investigators and collaboration partners for any clinical trials we conduct; and | |

| ● | our ability to successfully implement our strategy. |

Any forward-looking statements that we make in this Form 10-Q speak only as of the date of such statement, and we undertake no obligation to update such statements to reflect events or circumstances after the date of this Form 10-Q. You should also read carefully the factors described in the “Risk Factors” section of the Company’s annual report on Form 10-K for the fiscal year ended October 31, 2019, (as filed with the SEC on December 20, 2019, and amended by Amendment No. 1 thereto on Form 10-K/A filed on January 21, 2020 and by Amendment No. 2 thereto on Form 10-K/A filed on February 28, 2020, as so amended the “2019 Form 10-K/A”), to better understand the risks and uncertainties inherent in our business and underlying any forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this Form 10-Q will prove to be accurate.

This Form 10-Q includes statistical and other industry and market data that we obtained from industry publications and research, surveys and studies conducted by third parties. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe these industry publications and third-party research, surveys and studies are reliable, we have not independently verified such data.

We qualify all of our forward-looking statements by these cautionary statements. In addition, with respect to all of our forward-looking statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

| 4 |

PART I - FINANCIAL INFORMATION

ADVAXIS, INC.

(In thousands, except share and per share data)

| January 31, 2020 (Unaudited) | October 31, 2019 | |||||||

| ASSETS | ||||||||

| Current Assets: | ||||||||

| Cash and cash equivalents | $ | 34,156 | $ | 32,363 | ||||

| Deferred expenses | 2,032 | 2,353 | ||||||

| Prepaid expenses and other current assets | 965 | 1,433 | ||||||

| Total current assets | 37,153 | 36,149 | ||||||

| Property and equipment (net of accumulated depreciation) | 4,121 | 4,350 | ||||||

| Intangible assets (net of accumulated amortization) | 4,490 | 4,575 | ||||||

| Operating right-of-use asset (net of accumulated amortization) | 5,402 | - | ||||||

| Other assets | 182 | 183 | ||||||

| Total assets | $ | 51,348 | $ | 45,257 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | 444 | $ | 976 | ||||

| Accrued expenses | 2,657 | 3,478 | ||||||

| Common stock warrant liability | 54 | 19 | ||||||

| Current portion of operating lease liability | 857 | - | ||||||

| Other current liabilities | - | 48 | ||||||

| Total current liabilities | 4,012 | 4,521 | ||||||

| Operating lease liability, net of current portion | 5,788 | - | ||||||

| Other liabilities | - | 1,205 | ||||||

| Total liabilities | 9,800 | 5,726 | ||||||

| Commitments and contingencies – Note 10 | ||||||||

| Stockholders’ equity: | ||||||||

| Preferred stock, $0.001 par value; 5,000,000 shares authorized, 0 shares issued and outstanding at January 31, 2020 and October 31, 2019 Liquidation preference of $0 at January 31, 2020 and October 31, 2019 | - | - | ||||||

| Common stock, $0.001 par value, 170,000,000 shares authorized, 60,236,599 and 50,201,671 shares issued and outstanding at January 31, 2020 and October 31, 2019, respectively | 60 | 50 | ||||||

| Additional paid-in capital | 433,614 | 423,750 | ||||||

| Accumulated deficit | (392,126 | ) | (384,269 | ) | ||||

| Total stockholders’ equity | 41,548 | 39,531 | ||||||

| Total liabilities and stockholders’ equity | $ | 51,348 | $ | 45,257 | ||||

The accompanying notes should be read in conjunction with the financial statements.

| 5 |

ADVAXIS, INC.

CONDENSED STATEMENTS OF OPERATIONS (Unaudited)

(In thousands, except share and per share data)

| Three Months Ended January 31, | ||||||||

| 2020 | 2019 | |||||||

| Revenue | $ | 3 | $ | 19,689 | ||||

| Operating expenses: | ||||||||

| Research and development expenses | 4,859 | 6,707 | ||||||

| General and administrative expenses | 3,030 | 2,666 | ||||||

| Total operating expenses | 7,889 | 9,373 | ||||||

| (Loss) income from operations | (7,886 | ) | 10,316 | |||||

| Other income (expense): | ||||||||

| Interest income | 66 | 146 | ||||||

| Net changes in fair value of derivative liabilities | (37 | ) | 2,409 | |||||

| Other expense | - | (4 | ) | |||||

| Net (loss) income before benefit for income taxes | (7,857 | ) | 12,867 | |||||

| Income tax expense | - | 50 | ||||||

| Net (loss) income | $ | (7,857 | ) | $ | 12,817 | |||

| Net (loss) income per common share, basic and diluted | $ | (0.15 | ) | $ | 2.76 | |||

| Weighted average number of common shares outstanding, basic | 51,747,246 | 4,642,718 | ||||||

| Weighted average number of common shares outstanding, diluted | 51,747,246 | 4,642,817 | ||||||

The accompanying notes should be read in conjunction with the financial statements.

| 6 |

ADVAXIS, INC.

CONDENSED STATEMENTS OF CASH FLOWS (Unaudited)

(in thousands)

| Three Months Ended January 31, | ||||||||

| 2020 | 2019 | |||||||

| OPERATING ACTIVITIES | ||||||||

| Net (loss) income | $ | (7,857 | ) | $ | 12,817 | |||

| Adjustments to reconcile net (loss) income to net cash used in operating activities: | ||||||||

| Stock compensation | 242 | 622 | ||||||

| Employee stock purchase plan expense | - | 1 | ||||||

| Loss (gain) on change in value of warrants | 37 | (2,409 | ) | |||||

| Abandonment of intangible assets | 232 | 244 | ||||||

| Depreciation expense | 229 | 285 | ||||||

| Amortization expense of intangible assets | 91 | 96 | ||||||

| Amortization of right-of-use asset | 181 | - | ||||||

| Change in operating assets and liabilities: | ||||||||

| Accounts receivable | - | 143 | ||||||

| Prepaid expenses and other current assets | 789 | (660 | ) | |||||

| Other assets | 1 | - | ||||||

| Accounts payable and accrued expenses | (1,462 | ) | (4,707 | ) | ||||

| Deferred revenue | - | (18,318 | ) | |||||

| Operating lease liabilities | (191 | ) | - | |||||

| Other liabilities | - | 16 | ||||||

| Net cash used in operating activities | (7,708 | ) | (11,870 | ) | ||||

| INVESTING ACTIVITIES | ||||||||

| Purchase of property and equipment | - | (45 | ) | |||||

| Cost of intangible assets | (238 | ) | (507 | ) | ||||

| Net cash used in investing activities | (238 | ) | (552 | ) | ||||

| FINANCING ACTIVITIES | ||||||||

| Net proceeds of issuance of common stock | 9,737 | - | ||||||

| Proceeds from employee stock purchase plan | 2 | 14 | ||||||

| Employee tax withholdings paid on equity awards | - | (11 | ) | |||||

| Tax shares sold to pay for employee tax withholdings on equity awards | - | 11 | ||||||

| Net cash provided by financing activities | 9,739 | 14 | ||||||

| Net increase (decrease) in cash, cash equivalents and restricted cash | 1,793 | (12,408 | ) | |||||

| Cash, cash equivalents and restricted cash at beginning of year | 32,363 | 45,118 | ||||||

| Cash, cash equivalents and restricted cash at end of year | $ | 34,156 | $ | 32,710 | ||||

| SUPPLEMENTAL CASH FLOW INFORMATION | ||||||||

| Cash paid for taxes | $ | - | $ | 50 | ||||

| SUPPLEMENTAL DISCLOSURE OF NON-CASH AND FINANCING ACTIVITIES | ||||||||

| Amounts accrued for offering costs | 109 | - | ||||||

| Warrant liability reclassified into equity | 2 | - | ||||||

The accompanying notes should be read in conjunction with the financial statements.

| 7 |

ADVAXIS, INC.

NOTES TO THE CONDENSED FINANCIAL STATEMENTS

(Unaudited)

1. NATURE OF OPERATIONS

Advaxis, Inc. (“Advaxis” or the “Company”) is a clinical-stage biotechnology company focused on the development and commercialization of proprietary Listeria monocytogenes (“Lm”)-based antigen delivery products. The Company is using its Lm platform directed against tumor-specific targets in order to engage the patient’s immune system to destroy tumor cells. Through a license from the University of Pennsylvania, Advaxis has exclusive access to this proprietary formulation of attenuated Lm called Lm TechnologyTM. Advaxis’ proprietary approach is designed to deploy a unique mechanism of action that redirects the immune system to attack cancer in three distinct ways:

| ● | Alerting and training the immune system by activating multiple pathways in Antigen-Presenting Cells (“APCs”) with the equivalent of multiple adjuvants; | |

| ● | Attacking the tumor by generating a strong, cancer-specific T cell response; and | |

| ● | Breaking down tumor protection through suppression of the protective cells in the tumor microenvironment (“TME”) that shields the tumor from the immune system. This enables the activated T cells to begin working to attack the tumor cells. |

Advaxis’ proprietary Lm platform technology has demonstrated clinical activity in several of its programs and has been dosed in over 470 patients across multiple clinical trials and in various tumor types. The Company believes that Lm Technology immunotherapies can complement and address significant unmet needs in the current oncology treatment landscape. Specifically, its product candidates have the potential to work synergistically with other immunotherapies, including checkpoint inhibitors, while having a generally well-tolerated safety profile.

Liquidity and Financial Condition

The Company has not yet commercialized any human products and the products that are being developed have not generated significant revenue. As a result, the Company has experienced recurring losses and requires significant cash resources to execute its business plans. Historically, the Company’s major sources of cash have been comprised of proceeds from various public and private offerings of its common stock, clinical collaborations, option and warrant exercises, and interest income. From October 2013 through January 2020, the Company raised approximately $302.7 million in gross proceeds ($10.5 million in the first quarter of fiscal year 2020) from various public and private offerings of its common stock.

In Note 2 of the notes to the Company’s audited financial statements as of and for the year ended October 31, 2019, management stated that the Company had incurred significant losses, negative operating cash flows and as of those dates needed to raise additional funds to meet its obligations and sustain its operations. As a result, the Company concluded that there was substantial doubt as to the Company’s ability to continue as a going concern. As of January 31, 2020, the Company had approximately $34.2 million in cash and cash equivalents. The Company has significantly reduced its operating expenses to $38.9 million for the fiscal year ended October 31, 2019 as compared to $76.4 million during the fiscal year ended October 31, 2018. Furthermore, the Company expects cash requirements to approximate $29 million for fiscal year 2020, which includes approximately $6 million in non-recurring costs related to programs that are winding down. The Company believes to have sufficient capital to fund its obligations, as they become due, in the ordinary course of business until at least August 2021.

Given our cash balances including funds raised of $10.5 million (which yielded net proceeds of $9.6 million) in January 2020 and based on its budgeted, reduced cash flow requirements for the next twelve months from the date of filing, the Company believes such funds are sufficient to support ongoing operations at least one year after the issuance of these financial statements. Regardless of the results of any ongoing clinical trial, we have control over our expenditures and have the ability to adjust spending accordingly based on the budgeted cash flow requirements developed and the excess cash on hand.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND BASIS OF PRESENTATION

Basis of Presentation/Estimates

The accompanying unaudited interim condensed financial statements and related notes have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information, and in accordance with the rules and regulations of the Securities and Exchange Commission (“SEC”) with respect to Form 10-Q and Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete financial statements and the accompanying unaudited condensed balance sheet as of January 31, 2020 has been derived from the Company’s October 31, 2019 audited financial statements. In the opinion of management, the unaudited interim condensed financial statements furnished include all adjustments (consisting of normal recurring accruals) necessary for a fair statement of the results for the interim periods presented.

| 8 |

Operating results for interim periods are not necessarily indicative of the results to be expected for the full year. The preparation of financial statements in accordance with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues, expenses, and the related disclosures at the date of the financial statements and during the reporting period. Significant estimates include the timelines associated with revenue recognition on upfront payments received, fair value and recoverability of the carrying value of property and equipment and intangible assets, fair value of warrant liability, grant date fair value of options, deferred tax assets and any related valuation allowance and related disclosure of contingent assets and liabilities. On an on-going basis, the Company evaluates its estimates, based on historical experience and on various other assumptions that it believes to be reasonable under the circumstances. Actual results could materially differ from these estimates.

These unaudited interim condensed financial statements should be read in conjunction with the financial statements of the Company as of and for the fiscal year ended October 31, 2019 and notes thereto contained in the Company’s annual report on Form 10-K, as filed with the SEC on December 20, 2019.

Leases

Effective November 1, 2019, the Company adopted ASC Topic 842, Leases (“ASC 842”) using the modified retrospective transition approach by applying the new standard to all leases existing as of the date of initial application. Results and disclosure requirements for reporting periods beginning after November 1, 2019 are presented under ASC 842, while prior period amounts have not been adjusted and continue to be reported in accordance with the previous guidance in ASC 840, Leases.

At the inception of an arrangement, the Company determines whether an arrangement is or contains a lease based on the facts and circumstances present in the arrangement. An arrangement is or contains a lease if the arrangement conveys the right to control the use of an identified asset for a period of time in exchange for consideration. Most leases with a term greater than one year are recognized on the balance sheet as operating lease right-of-use assets and current and long-term operating lease liabilities, as applicable. The Company has elected not to recognize on the balance sheet leases with terms of 12 months or less. The Company typically only includes the initial lease term in its assessment of a lease arrangement. Options to extend a lease are not included in the Company’s assessment unless there is reasonable certainty that the Company will renew.

Operating lease liabilities and their corresponding right-of-use assets are recorded based on the present value of lease payments over the expected remaining lease term. Certain adjustments to the right-of-use asset may be required for items such as prepaid or accrued rent. The interest rate implicit in the Company’s leases is typically not readily determinable. As a result, the Company utilizes its incremental borrowing rate, which reflects the fixed rate at which the Company could borrow on a collateralized basis the amount of the lease payments in the same currency, for a similar term, in a similar economic environment. In transition to ASC 842, the Company utilized the remaining lease term of its leases in determining the appropriate incremental borrowing rates.

Recent Accounting Standards

Recently Adopted Accounting Standards

On November 1, 2019, the Company adopted Accounting Standards Update No. 2016-02, Leases (Topic 842) (ASU 2016-02), as amended, which establishes ASC 842 and supersedes the lease accounting guidance under ASC 840, and generally requires lessees to recognize operating and financing lease liabilities and corresponding right-of-use (ROU) assets on the balance sheet and to provide enhanced disclosures surrounding the amount, timing and uncertainty of cash flows arising from leasing arrangements. We adopted the new guidance using the modified retrospective transition approach by applying the new standard to all leases existing at the date of initial application and not restating comparative periods.

In adopting the new standard, the Company elected to utilize the available package of practical expedients permitted under the transition guidance within the new standard, which does not require the reassessment of the following: (i) whether existing or expired arrangements are or contain a lease, (ii) the lease classification of existing or expired leases, and (iii) whether previous initial direct costs would qualify for capitalization under the new lease standard. Additionally, the Company elected to combine lease and non-lease components and to exclude leases with a term of 12 months or less.

As of the November 1, 2019 effective date, the Company has identified one operating lease arrangement and one short-term lease in which it is a lessee. The adoption of ASC 842 resulted in the recognition of an operating lease liability and a right-of-use asset of approximately $6.8 million and $5.6 million, respectively, on the Company’s balance sheet relating to its leases, with the difference relating to reclassifications of the current accrued rent liability and the current lease incentive obligation of approximately $0.9 million and $0.3 million, respectively, as reductions to the right-of-use-asset for its operating lease. The adoption of the standard did not have a material effect on the Company’s condensed statements of operations or condensed statements of cash flows.

Management does not believe that any other recently issued, but not yet effective accounting pronouncements, if adopted, would have a material impact on the accompanying condensed financial statements.

| 9 |

3. PROPERTY AND EQUIPMENT

Property and equipment, net consists of the following (in thousands):

| January 31, 2020 | October 31, 2019 | |||||||

| Leasehold improvements | $ | 2,335 | $ | 2,335 | ||||

| Laboratory equipment | 3,405 | 3,405 | ||||||

| Furniture and fixtures | 744 | 744 | ||||||

| Computer equipment | 409 | 409 | ||||||

| Construction in progress | 83 | 83 | ||||||

| Total property and equipment | 6,976 | 6,976 | ||||||

| Accumulated depreciation and amortization | (2,855 | ) | (2,626 | ) | ||||

| Net property and equipment | $ | 4,121 | $ | 4,350 | ||||

Depreciation expense for the three months ended January 31, 2020 and 2019 was approximately $0.2 million and $0.3 milion, respectively.

4. INTANGIBLE ASSETS

Intangible assets, net consist of the following (in thousands):

| January 31, 2020 | October 31, 2019 | |||||||

| Patents | $ | 5,811 | $ | 5,833 | ||||

| Licenses | 777 | 777 | ||||||

| Software | 117 | 117 | ||||||

| Total intangibles | 6,705 | 6,727 | ||||||

| Accumulated amortization | (2,215 | ) | (2,152 | ) | ||||

| Intangible assets | $ | 4,490 | $ | 4,575 | ||||

The expirations of the existing patents range from 2020 to 2040 but the expirations can be extended depending upon market approval if granted and/or based on existing laws and regulations. Capitalized costs associated with patent applications that are abandoned without future value are charged to expense when the determination is made not to pursue the application. Patent applications having a net book value of approximately $0.2 million were abandoned and were charged to general and administrative expenses in the statement of operations for each of the three months ended January 31, 2020 and 2019, respectively. Amortization expense for intangible assets that was charged to general and administrative expense in the statement of operations aggregated approximately $0.1 million for each of the three months ended January 31, 2020 and 2019.

Management has reviewed its long-lived assets for impairment whenever events and circumstances indicate that the carrying value of an asset might not be recoverable. Net assets are recorded on the balance sheet for patents and licenses related to axalimogene filolisbac (AXAL), ADXS-HOT, ADXS-PSA and ADXS-HER2 and other products that are in development. However, if a competitor were to gain FDA approval for a treatment before us or if future clinical trials fail to meet the targeted endpoints, the Company would likely record an impairment related to these assets. In addition, if an application is rejected or fails to be issued, the Company would record an impairment of its estimated book value. Lastly, if the Company is unable to raise enough capital to continue funding its studies and developing its intellectual property, the Company would likely record an impairment to these assets.

At January 31, 2020, the estimated amortization expense by fiscal year based on the current carrying value of intangible assets is as follows (in thousands):

| Fiscal Year ended October 31, | ||||

| 2020 (Remaining) | $ | 249 | ||

| 2021 | 332 | |||

| 2022 | 332 | |||

| 2023 | 332 | |||

| 2024 | 332 | |||

| Thereafter | 2,913 | |||

| Total | $ | 4,490 | ||

| 10 |

5. ACCRUED EXPENSES

The following table represents the major components of accrued expenses (in thousands):

| January 31, 2020 | October 31, 2019 | |||||||

| Salaries and other compensation | $ | 1,108 | $ | 158 | ||||

| Vendors | 1,189 | 3,194 | ||||||

| Professional fees | 360 | 126 | ||||||

| Total accrued expenses | $ | 2,657 | $ | 3,478 | ||||

6. COMMON STOCK PURCHASE WARRANTS AND WARRANT LIABILITY

Warrants

As of January 31, 2020, there were outstanding warrants to purchase 5,405,726 shares of our common stock with exercise prices ranging from $0 to $281.25 per share. Information on the outstanding warrants is as follows:

| Exercise Price | Number of Shares Underlying Warrants | Expiration Date | Summary of Warrants | |||||||

| $ | - | 334,838 | July 2024 | July 2019 Public Offering | ||||||

| $ | 281.25 | 25 | N/A | Other Warrants | ||||||

| $ | 0.372 | 70,863 | September 2024 | September 2018 Public Offering | ||||||

| $ | 1.25 | 5,000,000 | July 2025 | January 2020 Public Offering | ||||||

| Grand Total | 5,405,726 | |||||||||

As of October 31, 2019, there were outstanding warrants to purchase 432,142 shares of our common stock with exercise prices ranging from $0 to $281.25 per share. Information on the outstanding warrants is as follows:

| Exercise Price | Number of Shares Underlying Warrants | Expiration Date | Summary of Warrants | |||||||

| $ | - | 359,838 | July 2024 | July 2019 Public Offering | ||||||

| $ | 281.25 | 25 | N/A | Other Warrants | ||||||

| $ | 0.372 | 72,279 | September 2024 | September 2018 Public Offering | ||||||

| Grand Total | 432,142 | |||||||||

A summary of warrant activity was as follows (In thousands, except share and per share data):

| Shares | Weighted Average Exercise Price | Weighted Average Remaining Contractual Life In Years | Aggregate Intrinsic Value | |||||||||||||

| Outstanding and exercisable warrants at October 31, 2019 | 432,142 | $ | 0.08 | 4.76 | $ | 114,069 | ||||||||||

| Issued | 5,000,000 | $ | 1.25 | |||||||||||||

| Exercised* | (26,416 | ) | $ | 0.24 | ||||||||||||

| Outstanding and exercisable warrants at January 31, 2020 | 5,405,726 | $ | 1.16 | 5.40 | $ | 322,542 | ||||||||||

* Includes the cashless exercise of 25,000 warrants that resulted in the issuance of 25,000 shares of common stock.

As of January 31, 2020, the Company had 5,334,863 of its total 5,405,726 outstanding warrants classified as equity (equity warrants). At October 31, 2019, the Company had 359,863 of its total 432,142 outstanding warrants classified as equity (equity warrants). At issuance, equity warrants are recorded at their relative fair values, using the relative fair value method, in the stockholders’ equity section of the balance sheet.

| 11 |

Warrant Liability

As of January 31, 2020, the Company had 70,863 of its total 5,405,726 outstanding warrants classified as liabilities (liability warrants). At October 31, 2019, the Company had 72,279 of its total 432,142 outstanding warrants classified as liabilities (liability warrants). These warrants contain a down round feature, except for exempt issuances as defined in the warrant agreement, in which the exercise price would immediately be reduced to match a dilutive issuance of common stock, options, convertible securities and changes in option price or rate of conversion. As of January 31, 2020, the down round feature was triggered three times and the exercise price of the warrants were reduced from $22.50 to $0.372. The warrants require liability classification as the warrant agreement requires the Company to maintain an effective registration statement and does not specify any circumstances under which settlement in other than cash would be permitted or required. As a result, net cash settlement is assumed and liability classification is warranted. For these liability warrants, the Company utilized the Monte Carlo simulation model to calculate the fair value of these warrants at issuance and at each subsequent reporting date.

In measuring the warrant liability at January 31, 2020 and October 31, 2019, the Company used the following inputs in its Monte Carlo simulation model:

| January 31, 2020 | October 31, 2019 | |||||||

| Exercise Price | $ | 0.37 | $ | 0.37 | ||||

| Stock Price | $ | 0.86 | $ | 0.32 | ||||

| Expected Term | 4.62 years | 4.87 years | ||||||

| Volatility % | 103.18 | % | 100.99 | % | ||||

| Risk Free Rate | 1.32 | % | 1.51 | % | ||||

7. SHARE BASED COMPENSATION

The following table summarizes share-based compensation expense included in the condensed statements of operations (in thousands):

| Three Months Ended January 31, | ||||||||

| 2020 | 2019 | |||||||

| Research and development | $ | 91 | $ | 323 | ||||

| General and administrative | 151 | 299 | ||||||

| Total | $ | 242 | $ | 622 | ||||

Restricted Stock Units (RSUs)

A summary of the Company’s RSU activity and related information for the three months ended January 31, 2020 is as follows:

| Number of RSUs | Weighted-Average Grant Date Fair Value | |||||||

| Unvested as of October 31, 2019 | 14,706 | $ | 47.62 | |||||

| Vested | (2,957 | ) | 124.77 | |||||

| Cancelled | (105 | ) | 101.72 | |||||

| Unvested as of January 31, 2020 | 11,644 | $ | 27.53 | |||||

As of January 31, 2020, there was approximately $0.2 million of unrecognized compensation cost related to non-vested RSUs, which is expected to be recognized over a remaining weighted average vesting period of 1.05 years.

As of January 31, 2020, the aggregate fair value of non-vested RSUs was approximately $10,000.

Employee Stock Awards

Common Stock issued to executives and employees related to vested incentive retention awards, employment inducements, management purchases and employee excellence awards totaled 2,957 shares and 9,847 shares during the three months ended January 31, 2020 and 2019, respectively. Total stock compensation expense associated with employee awards for the three months ended January 31, 2020 and 2019 was approximately $56,000 and $0.3 million, respectively.

| 12 |

Stock Options

A summary of changes in the stock option plan for the three months ended January 31, 2020 is as follows:

| Number of Options | Weighted-Average Exercise Price | |||||||

| Outstanding at October 31, 2019 | 560,490 | $ | 71.56 | |||||

| Canceled or Expired | (7,044 | ) | 24.10 | |||||

| Outstanding at January 31, 2020 | 553,446 | 72.17 | ||||||

| Vested and Exercisable at January 31, 2020 | 268,371 | $ | 141.37 | |||||

Total compensation cost related to the Company’s outstanding stock options, recognized in the condensed statement of operations for the three months ended January 31, 2020 and 2019 was approximately $0.2 million and $0.3 million, respectively.

As of January 31, 2020, there was approximately $1.1 million of unrecognized compensation cost related to non-vested stock option awards, which is expected to be recognized over a remaining weighted average vesting period of 1.41 years.

As of January 31, 2020, the aggregate intrinsic value of vested and exercisable options was $0.

In determining the fair value of the stock options granted during the three months ended January 31, 2019, the Company used the following inputs in its Black-Scholes Merton (“BSM”) model (no options were granted during the three months ended January 31, 2020):

| Three Months Ended January 31, 2019 | ||||

| Expected Term | 5.50-6.51 years | |||

| Expected Volatility | 90.29%-99.32 | % | ||

| Expected Dividends | 0 | % | ||

| Risk Free Interest Rate | 2.65%-3.15 | % | ||

2018 Employee Stock Purchase Plan

During the three months ended January 31, 2020, the Company issued 5,555 shares that were purchased under the 2018 Employee Stock Purchase Plan (“ESPP”).

8. NET INCOME (LOSS) PER SHARE

Basic and diluted earnings per share is calculated as follows (in thousands, except share and per share data):

| Three Months Ended January 31, | ||||||||

| 2020 | 2019 | |||||||

| Numerator : | ||||||||

| Net (loss) income | $ | (7,857 | ) | $ | 12,817 | |||

| Earnings attributable to common stockholders – basic and diluted | (7,857 | ) | 12,817 | |||||

| Denominator: | ||||||||

| Weighted-average number of common shares used in earnings per share - basic | 51,412,408 | 4,642,718 | ||||||

| Effect of dilutive stock options | - | 99 | ||||||

| Weighted-average number of common shares used in earnings per share - diluted | 51,412,408 | 4,642,817 | ||||||

| Earnings per share – basic and diluted | $ | (0.15 | ) | $ | 2.76 | |||

The following potentially dilutive securities, prior to the use of the treasury stock method, have been excluded from the computation of diluted weighted-average shares outstanding, as they would be anti-dilutive:

| As of January 31, | ||||||||

| 2020 | 2019 | |||||||

| Warrants | 5,405,726 | 944,636 | ||||||

| Stock Options | 553,446 | 383,292 | ||||||

| Restricted Stock Units | 11,644 | 20,258 | ||||||

| Total | 5,970,816 | 1,348,186 | ||||||

| 13 |

9. COLLABORATION AND LICENSING AGREEMENTS

Elanco Animal Health (formerly Aratana Therapeutics)

During the year fiscal year ended October 31, 2018, the USDA’s Center for Veterinary Biologics granted Aratana conditional approval for its canine osteosarcoma vaccine using Advaxis’ technology. During the three months ended January 31, 2020 and 2019, Advaxis recognized royalty revenue totaling approximately $3,000 and $2,000, respectively, from Aratana’s sales of the canine osteosarcoma vaccine. On July 16, 2019, Aratana announced their shareholders approved a merger agreement with Elanco Animal Health (“Elanco”) whereby Elanco will be the majority shareholder of Aratana. All of the terms of the Aratana Agreement remain in effect.

10. COMMITMENTS AND CONTINGENCIES:

Legal Proceedings

Stendhal

On September 19, 2018, Stendhal filed a Demand for Arbitration before the International Centre for Dispute Resolution (Case No. 01-18-0003-5013) relating to the Co-development and Commercialization Agreement with Especificos Stendhal SA de CV (the “Stendhal Agreement”). In the demand, Stendhal alleged that (i) the Company breached the Stendhal Agreement when it made certain statements regarding its AIM2CERV program, (ii) that Stendhal was subsequently entitled to terminate the Agreement for cause, which it did so at the time and (iii) that the Company owes Stendhal damages pursuant to the terms of the Stendhal Agreement. Stendhal is seeking to recover $3 million paid to the Company in 2017 as support payments for the AIM2CERV clinical trial along with approximately $0.3 million in expenses incurred. Stendhal is also seeking fees associated with the arbitration and interest. The Company has answered Stendhal’s Demand for Arbitration and denied that it breached the Stendhal Agreement. The Company also alleges that Stendhal breached its obligations to the Company by, among other things, failing to make support payments that became due in 2018 and that Stendhal therefore owes the Company $3 million. Advaxis is also seeking fees associated with the arbitration and interest.

On April 2, 2019, the Arbitrator denied the Company’s early application for summary disposition of Stendhal’s claims. No reasoning was provided. From October 21-23, 2019, an evidentiary hearing for the arbitration was conducted, and on November 23, 2019, the arbitrator requested that the parties submit post-hearing briefs which were submitted on January 15, 2020. On February 20, 2020, the parties were notified that the hearings have been declared closed as of February 1, 2020. At this time, the Company is unable to predict the likelihood of an unfavorable outcome.

11. LEASES

Operating Leases

The Company leases its corporate office and manufacturing facility in Princeton, New Jersey under an operating lease that expires in November 2025. The Company has the option to renew the lease term for two additional five-year terms. The renewal periods were not included the lease term for purposes of determining the lease liability or right-of-use asset. The Company has provided a security deposit of approximately $182,000, which is recorded as Other Assets in the condensed balance sheet.

The Company identified and assessed the following significant assumptions in recognizing its right-of-use assets and corresponding lease liabilities:

| ● | As the Company does not have sufficient insight to determine an implicit rate, the Company estimated the incremental borrowing rate in calculating the present value of the lease payments. The Company utilized a synthetic credit rating model to determine a benchmark for its incremental borrowing rate for its leases. The benchmark rate was adjusted to arrive at an appropriate discount rate for the lease. | |

| ● | Since the Company elected to account for each lease component and its associated non-lease components as a single combined component, all contract consideration was allocated to the combined lease component. | |

| ● | Renewal option periods have not been included in the determination of the lease terms as they are not deemed reasonably certain of exercise. | |

| ● | Variable lease payments, such as common area maintenance, real estate taxes, and property insurance are not included in the determination of the lease’s right-of-use asset or lease liability. |

| 14 |

Supplemental balance sheet information related to leases as of January 31, 2020 was as follows (in thousands):

| Operating Leases: | ||||

| Operating lease right-of-use assets | $ | 5,402 | ||

| Operating lease liability | $ | 857 | ||

| Operating lease liability, net of current portion | 5,788 | |||

| Total operating lease liabilities | $ | 6,645 | ||

Supplemental lease expense related to leases was as follows (in thousands):

| Lease Cost (in thousands) | Statements of Operations Classification | For the Three Months Ended January 31, 2020 | ||||

| Operating lease cost | General and administrative | 290 | ||||

| Short-term lease cost | General and administrative | 85 | ||||

| Variable lease cost | General and administrative | $ | 141 | |||

| Total lease expense | $ | 516 | ||||

Other information related to leases where the Company is the lessee is as follows:

| For the Three Months Ended January 31, 2020 | ||||

| Weighted-average remaining lease term | 5.8 years | |||

| Weighted-average discount rate | 6.5 | % | ||

Supplemental cash flow information related to operating leases was as follows:

| For the Three Months Ended January 31, 2020 | ||||

| Cash paid for operating lease liabilities | $ | 300 | ||

Future minimum lease payments under non-cancellable leases as of January 31, 2020 were as follows:

| Fiscal Year ended October 31, | ||||

| 2020 (Remaining) | $ | 933 | ||

| 2021 | 1,318 | |||

| 2022 | 1,369 | |||

| 2023 | 1,395 | |||

| 2024 | 1,419 | |||

| Thereafter | 1,564 | |||

| Total minimum lease payments | 7,998 | |||

| Less: Imputed interest | (1,353 | ) | ||

| Total | $ | 6,645 | ||

Under ASC 840, future minimum payments under the Company’s operating lease were as follows (in thousands):

| Fiscal Year ended October 31, | ||||

| 2020 | $ | 1,233 | ||

| 2021 | 1,318 | |||

| 2022 | 1,369 | |||

| 2023 | 1,395 | |||

| 2024 | 1,419 | |||

| Thereafter | 1,564 | |||

| Total | $ | 8,298 | ||

Under ASC 840, rent expense for each of the years ended October 31, 2019 and 2018 was approximately $1.2 million.

| 15 |

12. STOCKHOLDERS’ EQUITY

A summary of the changes in stockholders’ equity for the three months ended January 31, 2020 and 2019 is presented below (in thousands, except share data):

| Preferred Stock | Common Stock | Additional Paid-In | Accumulated | Total Shareholders’ | ||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Capital | Deficit | Equity | ||||||||||||||||||||||

| Balance at November 1, 2018 | - | $ | - | 4,634,189 | $ | 5 | $ | 391,703 | $ | (367,657 | ) | $ | 24,051 | |||||||||||||||

| Stock based compensation | - | - | 9,811 | - | 622 | - | 622 | |||||||||||||||||||||

| Tax withholdings paid on equity awards | - | - | - | - | (11 | ) | - | (11 | ) | |||||||||||||||||||

| Tax shares sold to pay for tax withholdings on equity awards | - | - | - | - | 11 | - | 11 | |||||||||||||||||||||

| Issuance of shares to employees under ESPP Plan | - | - | 2,007 | - | 9 | - | 9 | |||||||||||||||||||||

| ESPP Expense | - | - | - | - | 1 | 1 | ||||||||||||||||||||||

| Net Income | - | - | - | - | - | 12,817 | 12,817 | |||||||||||||||||||||

| Balance at January 31, 2019 | - | $ | - | 4,646,007 | $ | 5 | $ | 392,335 | $ | (354,840 | ) | $ | 37,500 | |||||||||||||||

| Preferred Stock | Common Stock | Additional Paid-In | Accumulated | Total Shareholders’ | ||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Capital | Deficit | Equity | ||||||||||||||||||||||

| Balance at November 1, 2019 | - | $ | - | 50,201,671 | $ | 50 | $ | 423,750 | $ | (384,269 | ) | $ | 39,531 | |||||||||||||||

| Stock based compensation | - | - | 2,957 | - | 242 | - | 242 | |||||||||||||||||||||

| Advaxis public offerings | - | - | 10,000,000 | 10 | 9,618 | - | 9,628 | |||||||||||||||||||||

| Warrant exercises | - | - | 26,416 | - | 2 | - | 2 | |||||||||||||||||||||

| Issuance of shares to employees under ESPP Plan | - | - | 5,555 | - | 2 | - | 2 | |||||||||||||||||||||

| Net Income | - | - | - | - | - | (7,857 | ) | (7,857 | ) | |||||||||||||||||||

| Balance at January 31, 2020 | - | $ | - | 60,236,599 | $ | 60 | $ | 433,614 | $ | (392,126 | ) | $ | 41,548 | |||||||||||||||

In January 2020, the Company closed on an underwritten public offering of 10,000,000 shares of its common stock at a public offering price of $1.05, for gross proceeds of $10.5 million. In addition, the Company also undertook a concurrent private placement of warrants to purchase up to 5,000,000 shares of common stock. The warrants have an exercise price per share of $1.25, are exercisable during the period beginning on the six-month anniversary of the date of its issuance (the “Initial Exercise Date”) and will expire on the fifth anniversary of the Initial Exercise Date. The warrants also provide that if there is no effective registration statement registering, or no current prospectus available for, the issuance or resale of the warrant shares, the warrants may be exercised via a cashless exercise. After deducting the underwriting discounts and commissions and other offering expenses, the net proceeds from the offering were approximately $9.6 million.

| 16 |

13. FAIR VALUE

The authoritative guidance for fair value measurements defines fair value as the exchange price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or the most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. Market participants are buyers and sellers in the principal market that are (i) independent, (ii) knowledgeable, (iii) able to transact, and (iv) willing to transact. The guidance describes a fair value hierarchy based on the levels of inputs, of which the first two are considered observable and the last unobservable, that may be used to measure fair value which are the following:

● Level 1 — Quoted prices in active markets for identical assets or liabilities.

● Level 2— Inputs other than Level 1 that are observable, either directly or indirectly, such as quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or corroborated by observable market data or substantially the full term of the assets or liabilities.

● Level 3 — Unobservable inputs that are supported by little or no market activity and that are significant to the value of the assets or liabilities.

The following table provides the assets and liabilities carried at fair value measured on a recurring basis as of January 31, 2020 and October 31, 2019:

| January 31, 2020 | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Common stock warrant liability, warrants exercisable at $0.372 through September 2024 | - | - | $ | 54 | $ | 54 | ||||||||||

| October 31, 2019 | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Common stock warrant liability, warrants exercisable at $0.372 through September 2024 | - | - | $ | 19 | $ | 19 | ||||||||||

The following table sets forth a summary of the changes in the fair value of the Company’s warrant liabilities:

| January 31, 2020 | ||||

| Beginning balance | $ | 19 | ||

| Warrant Exercises | (2 | ) | ||

| Change in fair value | 37 | |||

| Ending Balance | $ | 54 | ||

| 17 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis contains forward-looking statements about our plans and expectations of what may happen in the future. Forward-looking statements are based on a number of assumptions and estimates that are inherently subject to significant risks and uncertainties, and our results could differ materially from the results anticipated by our forward-looking statements as a result of many known or unknown factors, including, but not limited to, those factors discussed in “Risk Factors” and incorporated by reference herein. See also the “Special Cautionary Notice Regarding Forward-Looking Statements” set forth at the beginning of this report.

You should read the following discussion and analysis in conjunction with the unaudited financial statements, and the related footnotes thereto, appearing elsewhere in this report, and in conjunction with management’s discussion and analysis and the audited financial statements included in our annual report on Form 10-K for the fiscal year ended October 31, 2019. In addition, we intend to use our media and investor relations website (www.advaxis.com/investor-relations), SEC filings, press releases, public conference calls and webcasts to communicate the public about Advaxis, its services and other issues.

Overview

Advaxis, Inc. (“Advaxis”) is a clinical-stage biotechnology company focused on the development and commercialization of proprietary Listeria monocytogenes (“Lm”)-based antigen delivery products. We are using our Lm platform directed against tumor-specific targets in order to engage the patient’s immune system to destroy tumor cells. Through a license from the University of Pennsylvania, we have exclusive access to this proprietary formulation of attenuated Lm called Lm TechnologyTM. Our proprietary approach is designed to deploy a unique mechanism of action that redirects the immune system to attack cancer in three distinct ways:

| ● | Alerting and training the immune system by activating multiple pathways in Antigen-Presenting Cells (“APCs”) with the equivalent of multiple adjuvants; | |

| ● | Attacking the tumor by generating a strong, cancer-specific T cell response; and | |

| ● | Breaking down tumor protection through suppression of the protective cells in the tumor microenvironment (“TME”) that shields the tumor from the immune system. This enables the activated T cells to begin working to attack the tumor cells. |

Our proprietary Lm platform technology has demonstrated clinical activity in several of our programs and has been dosed in over 470 patients across multiple clinical trials and in various tumor types. We believe that Lm Technology immunotherapies can complement and address significant unmet needs in the current oncology treatment landscape. Specifically, our product candidates have the potential to work synergistically with other immunotherapies, including checkpoint inhibitors, while having a generally well-tolerated safety profile.

The Advaxis Corporate Strategy

Our strategy is to advance the Lm Technology platform and leverage its unique capabilities to design and develop an array of cancer treatments. We are currently conducting or have conducted clinical studies of Lm Technology immunotherapies in HPV-associated cancers (including cervical and head and neck), prostate cancer, non-small cell lung cancer and other solid tumor types. We are working with, or are in the process of identifying, collaborators for many of our programs.

Moving forward, we expect that we will continue to invest in our core clinical program areas and will also remain opportunistic in evaluating Investigator Sponsored Trials (“ISTs”) as well as licensing opportunities. The Lm Technology platform is protected by a range of patents, covering both product and process, some of which we believe can be maintained into 2040.

Advaxis Pipeline of Product Candidates

| 18 |

Disease focused hotspot/’off the shelf’ neoantigen therapies (ADXS-HOT)

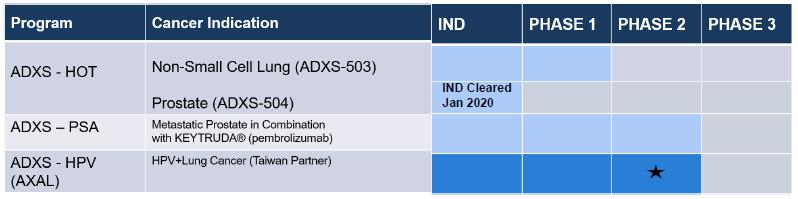

We are creating a new group of immunotherapy constructs for major solid tumor cancers that combines our optimized Lm Technology vector with promising targets designed to generate potent anti-cancer immunity. The ADXS-HOT program is a series of novel cancer immunotherapies that will target somatic mutations, or hotspots, cancer testis antigens, or CTAs, and oncofetal antigens, or OFAs. These three types of targets form the basis of the ADXS-HOT program because they are designed to be more capable of generating potent, tumor specific, and high strength killer T cells, versus more traditional over-expressed native sequence tumor associated antigens. Most hotspot mutations and OFA/CTA proteins play critical roles in oncogenesis; targeting both at once could significantly impair cancer proliferation. The ADXS-HOT products will combine many of the potential high avidity targets that are expressed in all patients with the target disease into one “off-the-shelf,” ready to administer treatment. We believe the ADXS-HOT technology has a strong intellectual property, or IP, position, with potential protection into 2040, and an IP filing strategy providing for broad coverage opportunities across multiple disease platforms and combination therapies.

In July 2018, we announced that the U.S. Food and Drug Administration, or FDA, allowed our investigational new drug, or IND, application for its ADXS-HOT drug candidate (ADXS-503) for non-small cell lung cancer, or NSCLC. ADXS-503 is currently being evaluated in a Phase 1/2 clinical trial, enrolling patients at five sites throughout the U.S. The first and second dose levels with monotherapy in Part A, (1 X108 and 5 X108 CFU) have been completed, and Part B in combination with a checkpoint inhibitor is currently open to enrollment. In February 2020, we announced the initial clinical data from the study, which showed that ADXS-503 has been safe and tolerable with potential signs of clinical activity in 4 of 7 evaluable patients achieving stable disease in the refractory setting. In addition, the first two patients evaluated in Part B who previously progressed on pembrolizumab showed stable disease with a 25% reduction in site lesion in the first patient and the second patient in Part B achieved a partial response. We are continuing to enroll patients in Part B and anticipate entering Part C, in combination with a checkpoint inhibitor as a first-line therapy, later in 2020.

Additionally, in January 2020, we announced that the FDA has allowed our IND for the initiation for a Phase 1 clinical study of ADXS-504, our ADXS-HOT drug candidate for prostate cancer.

Prostate Cancer (ADXS-PSA)

According to the American Cancer Society, prostate cancer is the second most common type of cancer found in American men and is the second leading cause of cancer death in men, behind only lung cancer. More than 191,000 men are estimated to be diagnosed with prostate cancer in 2020, with approximately 33,000 deaths each year. Unfortunately, in about 10-20% of cases, men with prostate cancer will go on to develop castration-resistant prostate cancer, or CRPC, which refers to prostate cancer that progresses despite androgen deprivation therapy. Metastatic CRPC, or mCRPC, occurs when the cancer spreads to other parts of the body and there is a rising prostate-specific antigen, PSA, level. This stage of prostate cancer has an average survival of 9-13 months, is associated with deterioration in quality of life, and has few therapeutic options available.

We have entered into a clinical trial collaboration and supply agreement with Merck & Co., or Merck, to evaluate the safety and efficacy of ADXS-PSA as monotherapy and in combination with KEYTRUDA®, Merck’s anti PD-1 antibody, in a Phase 1/2, open-label, multicenter, dose determination and expansion trial in patients with previously treated metastatic, castration-resistant prostate cancer (KEYNOTE-046). ADXS-PSA was tested alone or in combination with KEYTRUDA in an advanced and heavily pretreated patient population who had progressed on androgen deprivation therapy. A total of 13 and 37 patients were evaluated on monotherapy and combination therapy, respectively. For the ADXS-PSA monotherapy dose escalation and determination portion of the trial, cohorts were started at a dose of 1 x 109 cfu (n=7) and successfully escalated to higher dose levels of 5x109 cfu (n=3) and 1x1010 cfu (n=3) without achieving a maximum tolerated dose. Treatment-related adverse events, or TRAEs, noted at these higher dose levels were generally consistent with those observed at the lower dose level (1 x 109 cfu) other than a higher occurrence rate of Grade 2/3 hypotension. The Recommended Phase II Dose of ADXS-PSA monotherapy was determined to be 1x 109 cfu based on a review of the totality of the clinical data. This dose was used in combination with 200mg of pembrolizumab in a cohort of six patients to evaluate the safety of the combination before moving into an expanded cohort of patients. The safety of the combination was confirmed and enrollment in the expansion cohort phase was initiated. Enrollment in the study was completed in January 2017.

Data regarding checkpoint inhibitor monotherapy (KEYNOTE-199) has shown some antitumor activity that provides disease control in a subset of patients with bone-predominant mCRPC previously treated with next generation hormonal agents and docetaxel. Data from the KEYNOTE-199 trial in bone-predominant mCRPC patients treated with KEYTRUDA®, or pembrolizumab, was presented at the ASCO GU meeting in 2019. In this trial, the total stable disease/disease stabilization rate was 39% with no responses reported so far, and only one patient with ≥50% decrease in the post-baseline PSA value. It is hypothesized that the limited activity in mCRPC may be due to 1) the inability of the checkpoint inhibitor to infiltrate the tumor microenvironment and 2) the presence of an immunosuppressive tumor micro-environment, or TME. The combination therapy with agents—like Lm constructs—that induce T cell infiltration within the tumor and decrease negative regulators in the TME may improve performance of checkpoints in prostate cancer.

| 19 |

For KEYNOTE-046, as of the final data cutoff, September 16, 2019, the median overall survival (mOS) for 37 patients in the combination arm was 33.7 months (95% CI, range 15.4-33.7 months) and the median overall survival (95% CI) of 16.4 months (4.0-NR) for patients with prior visceral metastasis (n=11; 10 pts with prior docetaxel). This updated median overall survival is an increase from the previous data presented at the American Association for Cancer Research Annual Meeting in April 2019, where median overall survival was 21.1 months in the combination arm. The majority of TRAEs consisted of transient and reversible Grade 1-2 chills/rigors, fever, hypotension, nausea and fatigue. The combination of ADXS-PSA and KEYTRUDA® has appeared to be well-tolerated to date, with no additive toxicity observed. We are in discussions with potential partners regarding opportunities to expand or advance this mCRPC program.

HPV-Related Cancers

We conducted several studies evaluating axalimogene filolisbac, or AXAL, for HPV-related cancers. AXAL is an Lm-based antigen delivery product directed against HPV and designed to target cells expressing HPV.

In June 2019, we announced the closing of our AIM2CERV Phase 3 clinical trial with axalimogene filolisbac (AXAL) in high-risk locally advanced cervical cancer. The decision to close the study was based on the estimated remaining cost to complete the AIM2CERV trial of $80 million to $90 million, in addition to the timing to complete the study. The initial efficacy data was not anticipated for at least three years. No results from the clinical trial were to be available for at least three more years and therefore, results of the study were not the basis for the decision to close the study, nor was safety as the trial recently underwent its third Independent Data Monitoring Committee (IDMC) review with no safety issues noted. We are in the process of winding down the study and plan to publish the results in a medical journal in the future. We have no plans to further fund studies using AXAL.

In 2014, Advaxis granted Global BioPharma, or GBP, an exclusive license for the development and commercialization of AXAL in Asia, Africa, and the former Soviet Union territory, exclusive of India and certain other countries. GBP is responsible for all development and commercial costs and activities associated with the development in their territories. GBP anticipates initiating its Phase 2, open-label controlled trial in HPV-associated NSCLC in patients following first-line chemotherapy by the end of 2019. The study will be assessing the effects of AXAL when combined with pemetrexed in patients with HPV+ NSCLC, following first line induction therapy.

Personalized Neoantigen-directed Therapies (ADXS-NEO)

ADXS-NEO is an individualized Lm Technology antigen delivery product developed using whole-exome sequencing of a patient’s tumor to identify neoantigens. ADXS-NEO is designed to work by presenting a large payload of neoantigens directly into dendritic cells within the patient’s immune system and stimulating a T cell response against cancerous cells. In October 2019, we announced that we dosed our last patient in Part A, in monotherapy, and we do not intend to continue into Part B, in combination with a checkpoint inhibitor. As a result, we are in the process of winding down this study and we intend to publish the final results from Part A of the ADXS-NEO study in a medical journal in the future.

Other Lm Technology Products

HER2 Expressing Solid Tumors

HER2 is overexpressed in a percentage of solid tumors including osteosarcoma. According to published literature, up to 60% of osteosarcomas are HER2 positive, and this overexpression is associated with poor outcomes for patients. ADXS-HER2 is an Lm Technology antigen delivery product candidate designed to target HER2 expressing solid tumors including human and canine osteosarcoma. ADXS-HER2 has received FDA and EMA orphan drug designation for osteosarcoma and has received Fast Track designation from the FDA for patients with newly-diagnosed, non-metastatic, surgically-resectable osteosarcoma.

In September 2018, we announced that we had granted a license to OS Therapies, LLC, or OS Therapies, for the use of ADXS31-164, also known as ADXS-HER2, for evaluation in the treatment of osteosarcoma in humans. Under the terms of the license agreement, OS Therapies will be responsible for the conduct and funding of a clinical study evaluating ADXS-HER2 in recurrent, completely resected osteosarcoma. Pursuant to the agreement, upon OS Therapies’ successful completion of a financing, Advaxis expects to receive an upfront payment, reimbursement for product supply and other support, clinical, regulatory, and sales-based milestone payments, and royalties on future product sales. Additional details of the financial terms have not been disclosed.

Canine Osteosarcoma

On March 19, 2014, we entered into a definitive Exclusive License Agreement, or Aratana Agreement, with Aratana Therapeutics, Inc., or Aratana, where we granted Aratana an exclusive, worldwide, royalty-bearing license, with the right to sublicense, certain of our proprietary technology that enables Aratana to develop and commercialize animal health products that will be targeted for treatment of osteosarcoma and other cancer indications in animals. A product license request was filed by Aratana for ADXS-HER2 (also known as AT-014 by Aratana) for the treatment of canine osteosarcoma with the United States Department of Agriculture, or USDA. Aratana received communication in December 2017 that the USDA granted Aratana conditional licensure for AT-014 for the treatment of dogs diagnosed with osteosarcoma, one year of age or older.

| 20 |

Under the terms of the Aratana Agreement, Aratana paid an upfront payment to Advaxis in the amount of $1,000,000 upon signing of the Aratana Agreement. Aratana will also pay Advaxis: (a) up to $36.5 million based on the achievement of milestone relating to the advancement of products through the approval process with the USDA in the United States and the relevant regulatory authorities in the European Union, or E.U., in all four therapeutic areas and up to an additional $15 million in cumulative sales milestones based on achievement of gross sales revenue targets for sales of any and all products for use in non-human animal health applications, or the Aratana Field, (regardless of therapeutic area), and (b) tiered royalties starting at 5% and going up to 10%, which will be paid based on net sales of any and all products (regardless of therapeutic area) in the Aratana Field in the United States. Royalties for sales of products outside of the United States will be paid at a rate equal to half of the royalty rate payable by Aratana on net sales of products in the United States (starting at 2.5% and going up to 5%). Royalties will be payable on a product-by-product and country-by-country basis from first commercial sale of a product in a country until the later of (a) the 10th anniversary of first commercial sale of such product by Aratana, its affiliates or sub licensees in such country or (b) the expiration of the last-to-expire valid claim of our patents or joint patents claiming or covering the composition of matter, formulation or method of use of such product in such country. Aratana will also pay us 50% of all sublicense royalties received by Aratana and its affiliates. In fiscal year 2019, we received approximately $8,000 in royalty revenue from Aratana. Additionally, in July 2019, Aratana announced that their shareholders approved a merger agreement with Elanco Animal Health, or Elanco, whereby Elanco is now the majority shareholder of Aratana. All of the terms of the Aratana Agreement remain in effect.

Results of Operations for the Three Months Ended January 31, 2020 and 2019

Discussions of January 31, 2018 activity and period-to-period comparisons between 2019 and 2018 that are not included in this Form 10-Q can be found in Part I, Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations of our Form 10-Q for the quarterly period ended January 31, 2019.

Revenue

Revenue decreased $19.7 million to approximately $3,000 for the three months ended January 31, 2020 compared to the three months ended January 31, 2019. The reduction is attributable to revenue recognized in connection with the termination of the collaboration agreement with Amgen. On December 10, 2018, we received a written notice of termination from Amgen with respect to the Amgen Agreement, which termination was effective as of February 8, 2019. As a result, in the quarter ended January 31, 2019, we recognized the remaining upfront payments under ASC 606.

Research and Development Expenses

We invest in research and development to advance our Lm Technology through our pre-clinical and clinical development programs. Research and development expenses for the three months ended January 31, 2020 and January 31, 2019 were categorized as follows (in thousands):

Research and Development (in thousands)

Three Months Ended January 31, | Increase (Decrease) | |||||||||||||||

| 2020 | 2019 | $ | % | |||||||||||||

| Hotspot/Off-the-Shelf therapies | $ | 553 | $ | 717 | $ | (164 | ) | (30 | )% | |||||||

| Prostate cancer | 378 | 578 | (200 | ) | (53 | ) | ||||||||||

| HPV-associated cancers | 1,735 | 1,213 | 552 | 30 | ||||||||||||

| Personalized neoantigen-directed therapies | 350 | 1,206 | (856 | ) | (245 | ) | ||||||||||

| Other expenses | 1,843 | 2,993 | (1,150 | ) | (62 | ) | ||||||||||

| Total research & development expense | $ | 4,859 | $ | 6,707 | $ | (1,848 | ) | (38 | )% | |||||||

| Stock-based compensation expense included in research and development expense | $ | 91 | $ | 323 | $ | (232 | ) | (255 | )% | |||||||

| 21 |

Hotspot/Off-the-Shelf Therapies (ADXS-HOT)

Research and development costs associated with our hotspot mutation-based therapies for the three months ended January 31, 2020 decreased approximately $0.2 million to $0.6 million compared to the same period in 2019. The decrease is attributable to the startup costs associated with the initiation of the Phase 1/2 clinical trial in the first quarter of fiscal 2019. We have completed enrollment in Part A, in monotherapy, and the study is currently open for enrollment in combination with pembrolizumab at five sites across the U.S. In February 2020, we announced the initial clinical data from the study which showed that ADXS-503 has been safe and tolerable with potential signs of clinical activity in 4 of 7 evaluable patients achieving stable disease in the refractory setting. In addition, the first patient evaluated in Part B who previously progressed on pembrolizumab showed stable disease with a 25% reduction in a site lesion. We anticipate reporting additional information from this study as it becomes available throughout 2020.

Prostate Cancer Therapy (ADXS-PSA)

Research and development costs associated with our prostate cancer therapy for the three months ended January 31, 2020 decreased approximately $0.2 million, or 53%, compared to the same period in 2019. The decrease is attributable to the wrapping up of the study. The Phase 1/2 study of our ADXS-PSA compound is in combination with KEYTRUDA® (pembrolizumab), Merck’s humanized monoclonal antibody. During 2020, we presented updated data from this study which demonstrated an increase in the median overall survival, or mOS, to 33.7 months for patients in the combination arm of this study and mOS of 16.4 for patients with visceral metasteses (n=11). We are in discussions with potential partners on the next step for this therapy.

HPV-Associated Cancers

The majority of the HPV-associated research and development costs include clinical trial and other related costs associated with our axalimogene filolisbac, or AXAL, programs in cervical and head and neck cancers. HPV-associated costs for the three months ended January 31, 2020 increased approximately $0.6 million, or 30%, compared to the same period in 2019. The increase resulted from the partial hold by the FDA on our AIM2CERV study during the first quarter of 2019, which resulted in limited clinical activity as we worked to respond to the FDA’s questions surrounding their CMC requests. No new patients were enrolled during that time. In April 2019, we announced the clinical hold was lifted and in June 2019, we announced that we were closing the AIM2CERV study. We anticipate that our costs surrounding HPV-associated studies will continue to decline as we wrap up the remaining clinical and regulatory obligations of the program. We currently do not anticipate funding any new AXAL studies.

Personalized Neoantigen-Directed Therapies

Research and development costs associated with personalized neoantigen-directed therapies for the three months ended January 31, 2020 decreased approximately $0.9 million, or 245%, compared to the same period in 2019. In October 2019, we announced that we have enrolled our last patient in the ADXS-NEO program in monotherapy and will not continue into Part B of this study. As a result, the costs incurred for ADXS-NEO during the three months ended January 31, 2020 consisted of wind down costs associated with terminating the study. We anticipate that we will incur wind down costs for this study until late 2020 and plan to publish the results of this program in a future medical journal.

Other Expenses

Other expenses include salary and benefit costs, stock-based compensation expense, professional fees, laboratory costs and other internal and external costs associated with our research & development activities. Other expenses for the three months ended January 31, 2020 decreased approximately $1.2 million, or 62%, compared to the same period in 2019. The decrease was primarily attributable to a decrease in salary related expenses, including stock compensation, and travel expenses resulting from cost control measures put in place beginning in June 2018. In addition, there were decreases in laboratory and manufacturing costs, as we are focused on the clinical development of our HOT program and less on early research programs. Additionally, we announced in October 2019 that we are winding down ADXS-NEO and therefore no longer incurring costs to manufacture ADXS-NEO.

General and Administrative Expenses

General and administrative expenses primarily include salary and benefit costs and stock-based compensation expense for employees included in our finance and administrative departments. Also included in general and administrative expenses are outside legal, professional services and facilities costs. General and administrative expenses for the three months ended January 31, 2020 and January 31, 2019 were as follows (in thousands):

| Three Months Ended January 31, | Increase (Decrease) | |||||||||||||||

| 2020 | 2019 | $ | % | |||||||||||||

| General and administrative expense | $ | 3,030 | $ | 2,666 | $ | 364 | 12 | % | ||||||||

| Stock-based compensation expense included in general and administrative expense | $ | 151 | $ | 299 | $ | (147 | ) | (97 | )% | |||||||

| 22 |

General and administrative expenses for the three months ended January 31, 2020 increased approximately $0.4 million, or 12%, compared to the same period in 2019. The increase is attributable to higher legal fees, employee bonus accruals and business development costs. The aforementioned was partially offset by a decrease in stock-based compensation due to forfeitures of award and limitations of the granting of new awards due to the limited amount of available shares under the 2015 Incentive Plan, in addition to an insurance refund from a worker’s compensation audit.

Changes in Fair Values