MANAGEMENT'S

DISCUSSION

AND ANALYSIS

| A. HOW WE REPORT OUR RESULTS | I. CAPITAL AND LIQUIDITY MANAGEMENT | ||||||||||

| 1. Capital | |||||||||||

| B. OVERVIEW | 2. Capital Adequacy | ||||||||||

| 1. Strategy | 3. Shareholder Dividends | ||||||||||

| 2. Financial Objectives | 4. Principal Sources and Uses of Funds | ||||||||||

| 3. Sustainability Plan | 5. Liquidity | ||||||||||

| 4. Acquisitions and Other | |||||||||||

| J. RISK MANAGEMENT | |||||||||||

| C. FINANCIAL SUMMARY | 1. Risk Management Framework | ||||||||||

| 2. Risk Governance | |||||||||||

| D. PROFITABILITY | 3. Risk Universe | ||||||||||

| 4. Risk Appetite | |||||||||||

| E. GROWTH | 5. Risk Management Policies | ||||||||||

| 1. Sales, Gross Flows and Value of New Business | 6. Risk Management Process | ||||||||||

| 2. Assets Under Management | 7. Three Lines of Defence | ||||||||||

| 8. Risk Culture and Philosophy | |||||||||||

| F. FINANCIAL STRENGTH | 9. Risk Categories | ||||||||||

| G. PERFORMANCE BY BUSINESS GROUP | K. ADDITIONAL FINANCIAL DISCLOSURE | ||||||||||

1. Canada | 1. Selected Annual Information | ||||||||||

2. U.S. | 2. Items related to Statement of Operations | ||||||||||

3. Asset Management | 3. Items related to Statement of Financial Position | ||||||||||

4. Asia | 4. Fourth Quarter 2022 Profitability | ||||||||||

| 5. Corporate | 5. Fourth Quarter 2022 Growth | ||||||||||

| 6. Previous Quarters | |||||||||||

| H. INVESTMENTS | |||||||||||

| 1. Investment Profile | L. NON-IFRS FINANCIAL MEASURES | ||||||||||

| 2. Debt Securities | |||||||||||

| 3. Equities | M. ACCOUNTING AND CONTROL MATTERS | ||||||||||

| 4. Mortgages and Loans | 1. Critical Accounting Policies and Estimates | ||||||||||

| 5. Derivatives | 2. Changes in Accounting Policies | ||||||||||

| 6. Investment Properties | 3. Disclosure Controls and Procedures | ||||||||||

| 7. Impaired Assets | |||||||||||

| 8. Asset Default Provision | N. LEGAL AND REGULATORY PROCEEDINGS | ||||||||||

| O. FORWARD-LOOKING STATEMENTS | |||||||||||

MANAGEMENT'S DISCUSSION & ANALYSIS Sun Life Financial Inc. December 31, 2022 9

Management's Discussion and Analysis

February 8, 2023

| A. How We Report Our Results | |||||

Sun Life is a leading international financial services organization providing asset management, wealth, insurance and health solutions to individual and institutional Clients. Sun Life has operations in a number of markets worldwide, including Canada, the United States, the United Kingdom, Ireland, Hong Kong, the Philippines, Japan, Indonesia, India, China, Australia, Singapore, Vietnam, Malaysia and Bermuda. As of December 31, 2022, Sun Life had total assets under management ("AUM") of $1.33 trillion. For more information please visit www.sunlife.com.

Sun Life Financial Inc. trades on the Toronto (TSX), New York (NYSE) and Philippine (PSE) stock exchanges under the ticker symbol SLF.

Sun Life Financial Inc. ("SLF Inc.") is a publicly traded company domiciled in Canada and is the holding company of Sun Life Assurance Company of Canada ("Sun Life Assurance"). In this management's discussion and analysis ("MD&A"), SLF Inc., its subsidiaries and, where applicable, its joint ventures and associates are collectively referred to as "the Company", "Sun Life", "we", "our", and "us". Unless otherwise indicated, all information in this MD&A is presented as at and for the year ended December 31, 2022 and the information contained in this document is in Canadian dollars.

Where information at and for the year ended December 31, 2022 is not available, information available for the latest period before December 31, 2022 is used. Except where otherwise noted, financial information is presented in accordance with International Financial Reporting Standards ("IFRS") and the accounting requirements of the Office of the Superintendent of Financial Institutions ("OSFI"). Reported net income (loss) refers to Common shareholders' net income (loss) determined in accordance with IFRS.

We manage our operations and report our financial results in five business segments: Canada, United States ("U.S."), Asset Management, Asia, and Corporate. Information concerning these segments is included in our annual and interim consolidated financial statements and accompanying notes ("Annual Consolidated Financial Statements" and "Interim Consolidated Financial Statements", respectively, and "Consolidated Financial Statements" collectively), and this MD&A document.

1. Use of Non-IFRS Financial Measures

We report certain financial information using non-IFRS financial measures, as we believe that these measures provide information that is useful to investors in understanding our performance and facilitate a comparison of our quarterly and full year results from period to period. These non-IFRS financial measures do not have any standardized meaning and may not be comparable with similar measures used by other companies. For certain non-IFRS financial measures, there are no directly comparable amounts under IFRS. These non-IFRS financial measures should not be viewed in isolation from or as alternatives to measures of financial performance determined in accordance with IFRS. Additional information concerning non-IFRS financial measures and, if applicable, reconciliations to the closest IFRS measures are available in section L - Non-IFRS Financial Measures in this document and the Supplementary Financial Information package that are available on www.sunlife.com under Investors - Financial results and reports.

2. Forward-looking Statements

Certain statements in this document are forward-looking statements within the meaning of certain securities laws, including the "safe harbour" provisions of the United States Private Securities Litigation Reform Act of 1995 and applicable Canadian securities legislation. Additional information concerning forward-looking statements and important risk factors that could cause our assumptions, estimates, expectations and projections to be inaccurate and our actual results or events to differ materially from those expressed in or implied by such forward-looking statements can be found in section O - Forward-looking Statements in this document.

3. Additional Information

Additional information about SLF Inc. can be found in the Consolidated Financial Statements, the annual and interim MD&A, and SLF Inc.'s Annual Information Form ("AIF") for the year ended December 31, 2022. These documents are filed with securities regulators in Canada and are available at www.sedar.com. SLF Inc.'s Annual Consolidated Financial Statements, annual MD&A and AIF are filed with the United States Securities and Exchange Commission ("SEC") in SLF Inc.'s annual report on Form 40-F and SLF Inc.'s interim MD&A and Interim Consolidated Financial Statements are furnished to the SEC on Form 6-Ks and are available at www.sec.gov.

4. COVID-19 Pandemic Considerations

In early 2020, the world was impacted by COVID-19, which was declared a pandemic by the World Health Organization. The overall impact of the COVID-19 pandemic is still uncertain and dependent on the progression of the virus and on actions taken by governments, businesses and individuals, which could vary by country and result in differing outcomes. Given the extent of the circumstances, it is difficult to reliably measure or predict the potential impact of this uncertainty on our future financial results.

For additional information, refer to section J - Risk Management - 9 - Risk Categories - vii - Other Risks - Risks relating to the COVID-19 pandemic in this document.

10 December 31, 2022 Sun Life Financial Inc. MANAGEMENT'S DISCUSSION & ANALYSIS

| B. Overview | |||||

1. Strategy

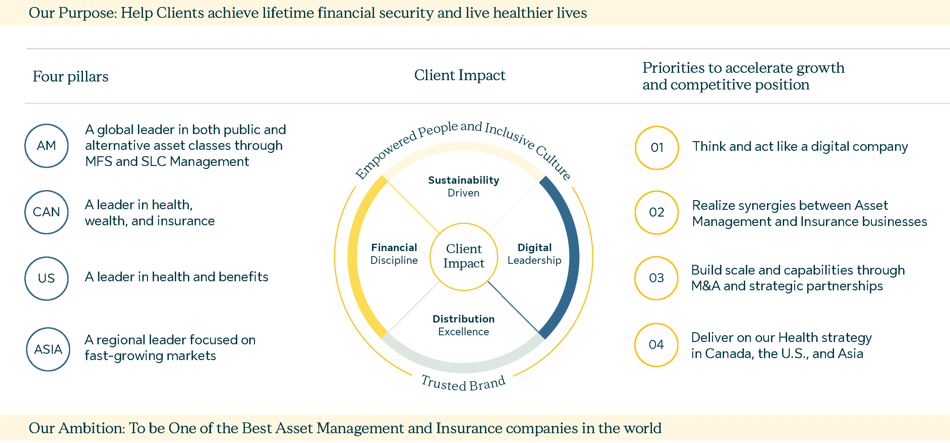

Our strategy places the Client at the centre of everything we do. Our enterprise strategy, as described below, reflects both our priorities and our diversified business mix. We believe by effectively executing on our strategy, we can fulfill our Purpose, create a positive impact for our Clients, and achieve our goal to be a leader in each of our four pillars.

Purpose and Ambition

Our Purpose is to help our Clients achieve lifetime financial security and live healthier lives.

We seek to provide outstanding value and impact for our Clients in three ways:

Driving positive financial actions by:

•Helping Clients build and protect their wealth.

•Providing quality products and solutions that meet the needs of our Clients.

•Delivering timely and expert advice through consistently superior Client experiences.

Delivering solid long-term Client investment returns by:

•Leveraging our collective expertise to make better investment decisions.

•Sourcing broad investment capabilities to serve global Client needs.

•Actively engaging with our Clients to think and act sustainably.

Driving positive health actions by:

•Being a trusted payer of benefits.

•Helping Clients access, navigate, manage, and receive the care they need.

•Improving health outcomes, including physical and mental well-being, by providing health solutions.

Our Ambition is "to be one of the best asset management and insurance companies in the world". We aim to achieve our ambition by maintaining our balanced business mix and leading positions across our pillars, delivering on our Purpose and Client Impact strategy, and focusing on strong execution to meet our medium-term financial objectives(1)(2):

•Underlying Earnings Per Share growth: 8-10%.

•Underlying Return on Equity: 16%+.

•Underlying Dividend Payout Ratio: 40%-50%.

(1)For more information about our medium-term financial objectives, see section B - Overview - 2 - Financial Objectives in this document. Underlying earnings per share, underlying ROE and underlying dividend payout ratio are Non-IFRS financial measures. See section L - Non-IFRS Financial Measures in this document.

(2)Our medium-term financial objectives following the adoption of IFRS 17 and IFRS 9 remain consistent for underlying earnings per share and underlying dividend payout ratio. Our underlying ROE medium-term financial objective will change to 18%+ following the adoption of both standards, an increase from 16%+ prior to transition. We continue to assess the impact that the adoption of IFRS 17 and IFRS 9 will have on our Consolidated Financial Statements and estimates of the financial impacts are subject to change. For more information, see Section J - Risk Management - 9 - Risk Categories - vii - Other Risks in this document.

MANAGEMENT'S DISCUSSION & ANALYSIS Sun Life Financial Inc. December 31, 2022 11

Our Four Pillars

Our four pillars define the businesses and markets in which we operate. In each of these pillars, we focus on creating value and positively impacting our Clients through businesses that have strong growth prospects, favourable return on equity ("ROE"), and strong capital generation in attractive global markets. We are well-positioned across each of our pillars.

Asset Management: A global leader in both public and alternative asset classes through MFS and SLC Management

We deliver value and drive positive Client impact through our offering of quality investment products:

•MFS Investment Management ("MFS") is a long-standing premier active investment manager offering a comprehensive set of asset management products and services to retail and institutional investors around the world.

•SLC Management is an institutional investment manager delivering alternative fixed income, private credit, infrastructure and global real estate solutions to institutional investors.

Canada: A leader in health, wealth, and insurance

We deliver value and impact to over 6.6 million Clients via our group and individual businesses, helping Clients achieve lifetime financial security and live healthier lives by:

•Providing a wide range of asset management, wealth, health and protection solutions to retail Clients.

•Continuing to build a health business that focuses on helping Canadians live healthy lives, both as a major provider of group benefits and through a growing focus on innovative products and services that lead to better health outcomes.

•Remaining a market leader in group retirement services in the workplace, including defined contribution pensions, and defined benefit pension de-risking.

U.S.: A leader in health and benefits

We have deep expertise in the health care market, and help our Clients get the coverage they need while improving health outcomes. We are:

•The largest independent medical stop-loss provider in the U.S., offering protection against large medical claims for employers who self-insure their employee health plans and health care navigation services to help members improve outcomes.

•The second largest dental benefits provider in the U.S.(1), serving more than 37 million members(2) through government programs and commercial group dental and vision solutions for employers of all sizes.

•A top ten group life and disability provider in the U.S., offering a broad portfolio of group insurance products and services, as well as turnkey risk management solutions for health plans and other insurance carriers.

Asia: A regional leader focused on fast-growing markets

We are well-positioned in growing markets in Asia, with operations in key ASEAN markets (Philippines, Vietnam, Indonesia, and Malaysia), Hong Kong, India, China, and High-Net-Worth ("HNW") (International and Singapore). These markets account for approximately 65% of Asia’s GDP with high potential for future growth(3). We are:

•A provider of individual life and health insurance that delivers Client value across all of our markets.

•A provider, in select markets, of asset management and group retirement products and services.

•Among the global leaders in providing life insurance solutions to HNW Clients.

Our Client Impact Strategy

Our Client Impact strategy has seven areas of focus that we are pursuing across our four pillars. These areas of focus define how we compete in our markets, extend our competitive advantages, fulfill our Purpose and support our ambition to be one of the best asset management and insurance companies in the world.

Client Impact: Our Clients are at the centre of everything we do. Whether it is helping to navigate health concerns, save and plan for retirement or provide financial security for their families, our focus is on the positive impact we have on our Clients' lives. We believe this allows us to develop and offer the right solutions and experiences, build lasting and trusted Client relationships, and create value for Clients that also deliver better business outcomes for Sun Life. We are committed to helping Clients by driving positive health and financial actions, and delivering solid long-term investment returns.

Distribution Excellence: We have established an omni-channel approach to distribution that makes it easier for Clients to do business with us across all markets. To excel at distribution, we prioritize exceptional service, connecting with our Clients when and how they want to engage, and providing personalized and holistic solutions. We are focused on meeting our Clients' needs by being an exceptional distribution partner that empowers our advisors and partners to harness digital solutions to provide seamless Client experiences.

Digital Leadership: We are accelerating our digital, data and analytics capabilities and seek to think and act like a digital company. Our Digital Enterprise strategy brings our businesses and technology teams closer together and transforms how we work. Business and technology are working together in an agile way to deliver digital experiences, products, and solutions that meet our Clients’ needs and drive positive outcomes. We continue to adopt Client-centric solutions that incorporate our Clients’ perspectives in every stage of their lives, creating long-term relationships.

Our Digital Enterprise strategy is focused on:

•Creating deep Client relationships enabled by leading digital capabilities and analytics.

•Delivering personalized Client experiences harnessing our data to provide insights.

•Evolving how we work together to drive faster decisions that are made closer to the Client.

(1)Based on number of members as of December 31, 2021. Ranking based on data disclosed by competitors.

(2)Includes members who also have a Sun Life Group coverage.

(3)Source: International Monetary Fund, 2022.

12 December 31, 2022 Sun Life Financial Inc. MANAGEMENT'S DISCUSSION & ANALYSIS

Financial Discipline: Our strategy is underpinned by a continued commitment to strong financial performance and risk management, coupled with a focus on capital management. Sustained focus across these areas support our medium-term financial objectives and our aim of top quartile total shareholder returns. Specific areas of focus include:

•Delivering strong, stable earnings growth and disciplined expense management.

•Managing our capital to protect our policyholders and to maintain strong financial flexibility, to generate shareholder value.

•Disciplined investment and a programmatic M&A(1) approach focused on building scale and capabilities to drive future growth.

Sustainability Driven: Sustainability is essential to our long-term business success. We embed sustainability into our strategy, culture, and operations, to drive meaningful social and economic outcomes for our Clients, employees, advisors, investors and communities. We believe our actions will contribute to a healthier, more financially resilient, environmentally secure, and economically prosperous world. See Section B - Overview - 3 - Sustainability Plan in this document for more information about our approach to sustainability.

Empowered People and Inclusive Culture: Delivering on our strategy will require us to attract, retain, and develop the best talent, and to empower our people to drive results. It will also require us to preserve and strengthen our strong culture of Client focus, integrity, collaboration and inclusivity. Specifically, our focus is to:

•Empower employees and advisors to take action, make decisions, and be accountable.

•Develop talent that combines strong leadership skills with technological savvy, to support our transformation to a leading digital organization.

•Maintain momentum on our diversity, equity and inclusion (“DE&I”) commitment, embedding DE&I into our decision-making to reflect our values.

•Design our Future of Work with intent, offering employees choice and flexibility in how and where we work.

•Be the employer of choice for top talent.

Trusted Brand: Preserving our long standing reputation of being a trusted brand is paramount in an increasingly complex and digitized world. Over the last 150 years, we have built and enjoyed strong, trusted relationships with our Clients in all Sun Life markets and through our distribution partnerships. Our brand informs the differentiated Sun Life experiences we create, the products and service experiences we deliver, and the culture we live by, to achieve our Purpose. Our forward-looking brand strategy will maintain focus on future competitive advantage and brand appeal with both new and existing Clients.

Key Strategic Priorities

Together with the strong foundation of our four pillars and key strategic areas of focus, our strategy emphasizes four key strategic priorities to accelerate growth and improve competitive positioning:

1.Think and act like a digital company.

2.Realize synergies between asset management and insurance businesses.

3.Build scale and capabilities through M&A and strategic partnerships.

4.Deliver on our health strategy in Canada, the U.S., and Asia.

We believe we are well-positioned to execute on each of these strategic priorities and that by doing so we will create positive Client Impact.

Our balanced four pillars, holistic Client Impact strategy, and focus on our strategic priorities combine elements that have been core to our success. Looking ahead, we are confident that our strategy will allow us to deliver on our Purpose, drive positive Client outcomes, create meaningful value for our shareholders, and support our ambition to be one of the best asset management and insurance companies in the world.

(1)Mergers & Acquisitions ("M&A").

MANAGEMENT'S DISCUSSION & ANALYSIS Sun Life Financial Inc. December 31, 2022 13

2. Financial Objectives

Our medium-term financial objectives are outlined as follows:

Measure(1)(2) | Medium-term financial objectives(3) | 5-Year(4) | 2022 results | ||||||||

Underlying EPS growth Growth in EPS reflects the Company's focus on generating sustainable earnings for shareholders. | 8%-10% | 9% | 4% | ||||||||

Underlying Return on Equity ("ROE") ROE is a significant driver of shareholder value and is a major focus for management across all businesses. | 16%+ | 14.7% | 15.1% | ||||||||

Underlying dividend payout ratio Payout of capital versus shareholder value, based on underlying net income. | 40%-50% | 41% | 44% | ||||||||

(1)Underlying earnings per share ("EPS"), underlying ROE and underlying dividend payout ratio are non-IFRS financial measures. See section L - Non-IFRS Financial Measures in this document. Underlying dividend payout ratio represents the ratio of common shareholders' dividends to diluted underlying EPS. See section I - Capital and Liquidity Management - 3 - Shareholder Dividends in this document for further information regarding dividends.

(2)Our medium-term financial objectives following the adoption of IFRS 17 and IFRS 9 remain consistent for underlying earnings per share and underlying dividend payout ratio. Our underlying ROE medium-term financial objective will change to 18%+ following the adoption of both standards, an increase from 16%+ prior to transition. We continue to assess the impact that the adoption of IFRS 17 and IFRS 9 will have on our Consolidated Financial Statements and estimates of the financial impacts are subject to change. For more information, see Section J - Risk Management - 9 - Risk Categories - vii - Other Risks in this document.

(3)Although considered reasonable, we may not be able to achieve our medium-term financial objectives as our assumptions may prove to be inaccurate. Accordingly, our actual results could differ materially from our medium-term financial objectives as described above. Our medium-term financial objectives do not constitute guidance. Our medium-term financial objectives are forward-looking non-IFRS financial measures and additional information is provided in this MD&A in section O - Forward-looking Statements - Medium-Term Financial Objectives.

(4)Underlying EPS growth is calculated using a compound annual growth rate. Underlying ROE and dividend payout ratio are calculated using an average.

In the year and over the medium-term, we have performed well against our medium-term financial objectives in a challenging operating environment reflecting economic and geopolitical uncertainties and global health concerns.

3. Sustainability Plan

Our sustainability plan is aligned directly with our Purpose of helping our Clients achieve lifetime financial security and live healthier lives, and is integrated into our enterprise strategy. We focus on three areas where we have the greatest opportunity to have a positive impact on society, while creating a competitive advantage for our business.

Increasing Financial Security: We provide Clients and employees with innovative solutions and services that increase their lifetime financial security. We empower and educate Clients to take positive financial action, improving access to and use of wealth and protection products, helping to build long-term wealth and close insurance coverage gaps.

Fostering Healthier Lives: We offer Clients and employees products, services and tools to help them live healthier lives. We positively impact health and wellness outcomes in society through our focus on increasing access to health care and health and disability insurance. Our investments in community health complement these efforts.

Advancing Sustainable Investing: We aspire to deliver sustainable returns for our Clients and drive the transition to a low-carbon, inclusive economy. We embed ESG factors in our investment processes, offering Clients sustainable investing opportunities. In addition, we invest our own assets in ways that support a low-carbon and more inclusive economy.

Our sustainability plan builds from our foundation as a Trusted and Responsible Business. We prioritize foundational sustainability considerations that are important to stakeholders: climate change, diversity, equity & inclusion, data security & privacy, talent management, governance & ethics, risk management, and reporting & disclosure. We recognize climate change as one of the defining issues of our time and commit to working together across industries, with our Clients, investees and other stakeholders to contribute to solving this global challenge. We are committed to the goal of achieving net zero greenhouse gas emissions by 2050, for our operations and investments.

Our sustainability plan is guided by the United Nations Sustainable Development Goals ("SDGs"). We focus primarily on supporting the five SDGs where we believe we can have the greatest impact. These are: #3 Good health & well-being, #5 Gender equality, #7 Affordable and clean energy, #8 Decent work and economic growth and #13 Climate action.

For additional information on our sustainability plan and recent progress, refer to www.sunlife.com/sustainability and the headings "2022 Highlights" throughout section G - Performance by Business Segment in this document. For more information on our approach to climate change, refer to the heading "Environmental and Social Risk Section" in section J - Risk Management - 9 - Business and Strategy Risks of this document, which includes our disclosure based on the recommendations of the Task Force on Climate-related Financial Disclosures ("TCFD").

14 December 31, 2022 Sun Life Financial Inc. MANAGEMENT'S DISCUSSION & ANALYSIS

4. Acquisitions and Other

The following developments occurred since January 1, 2022. Additional information concerning acquisitions and dispositions is provided in our 2022 Annual Consolidated Financial Statements.

On April 5, 2022, we announced an expansion to our existing bancassurance partnership with PT Bank CIMB Niaga Tbk ("CIMB Niaga") in Indonesia, which also extends our existing agreement by six years to 2039. Under the new agreement, for a term of 15 years effective January 2025, Sun Life will be the provider of insurance solutions to CIMB Niaga customers across all distribution channels, accelerating our growth ambitions in the country.

On June 1, 2022, we completed the acquisition of DentaQuest Group, Inc. ("DentaQuest"), the second-largest dental benefits provider in the U.S,(1) for approximately $3.3 billion (US$2.6 billion). DentaQuest is included in our U.S. business segment as part of the new “Dental” business unit, along with our existing dental and vision business, formerly within Group Benefits. DentaQuest is the largest provider of U.S. Medicaid dental benefits, with growing Medicare Advantage, commercial, and U.S. Affordable Care Act exchange businesses. The acquisition advances our strategy of being a leader in health and benefits in the U.S. while contributing to fee-based earnings and businesses which generate higher ROE.

On August 4, 2022, we entered into an agreement to sell SLF of Canada UK Limited ("Sun Life UK") to Phoenix Group Holdings plc ("Phoenix Group") for approximately $385 million (£248 million). Sun Life UK manages life and pension policies as well as payout annuities for UK Clients. Sun Life UK is closed to new sales and has operated as a run-off business since 2001. Under the agreement, we will retain our economic interest in the payout annuities business through a reinsurance treaty. Phoenix Group is the UK's largest long-term savings and retirement business, with £270 billion(2) of assets under administration and approximately 13 million customers. As part of the sale, we will establish a long-term partnership to become a strategic asset management partner to Phoenix Group. Our asset management companies, MFS and SLC Management, will continue to manage approximately $9 billion of Sun Life UK's general account upon the close of the sale. In addition, Phoenix Group has set a goal to invest approximately US$25 billion in North American public and private fixed income and alternative investments over the next five years. MFS and SLC Management will be material partners to Phoenix Group in achieving this goal. In Q3'22, we recognized an impairment charge of $170 million

(£108 million) pertaining to the attributed goodwill that is not expect to be recovered for through the sale. The transaction is expected to close in the first half of 2023, subject to regulatory approvals and customary closing conditions.

Subsequent Events

For additional information, refer to Note 28 of our 2022 Annual Consolidated Financial Statements.

On January 20, 2023, we announced a 15-year exclusive bancassurance partnership in Hong Kong with Dah Sing Bank ("Dah Sing"). Under this partnership, Sun Life will be the exclusive provider of life insurance solutions to Dah Sing's 570,000 retail banking customers, helping to fulfill their savings and protection needs at different life stages. This is Sun Life's first exclusive bancassurance partnership in Hong Kong and will be a valuable complement to our existing network of over 2,500 expert insurance advisors. Hong Kong is a thriving life insurance hub in Asia and bancassurance is a key distribution channel, accounting for more than 50% of the life insurance distribution mix. Following the completion of regulatory processes and approvals, distribution of Sun Life products is anticipated to start in July 2023.

On February 1, 2023, we completed the acquisition of a 51%(3) interest in Advisors Asset Management, Inc. ("AAM"), a leading independent U.S. retail distribution firm. AAM provides access to U.S. retail distribution for SLC Management, Sun Life's institutional fixed income and alternatives asset manager. This allows SLC Management to meet the growing demand among U.S. HNW investors for alternative assets. AAM provides a range of solutions and products to financial advisors at wirehouses, registered investment advisors and independent broker-dealers, overseeing US$40.5 billion (approximately C$55 billion) in assets as at December 31, 2022, with 10 offices across nine U.S. states.

On February 1, 2023, we completed the sale of our sponsored markets business from Sun Life Assurance Company of Canada ("SLA"), a wholly owned subsidiary of SLF Inc., to Canadian Premier Life Insurance Company ("Canadian Premier"). Sponsored markets include a variety of association & affinity, and group creditor clients.

(1)Based on number of members as of December 31, 2021. Ranking based on data disclosed by competitors.

(2)As at June 30, 2022.

(3)On a fully diluted basis.

MANAGEMENT'S DISCUSSION & ANALYSIS Sun Life Financial Inc. December 31, 2022 15

| C. Financial Summary | |||||

| ($ millions, unless otherwise noted) | |||||||||||

| Profitability | 2022 | 2021 | |||||||||

| Net income (loss) | |||||||||||

Reported net income (loss) - Common shareholders | 3,060 | 3,934 | |||||||||

Underlying net income (loss)(1) | 3,674 | 3,533 | |||||||||

| Diluted earnings per share ("EPS") ($) | |||||||||||

Reported EPS (diluted) | 5.21 | 6.69 | |||||||||

Underlying EPS (diluted)(1) | 6.27 | 6.03 | |||||||||

| Reported basic EPS ($) | 5.22 | 6.72 | |||||||||

| Return on equity ("ROE") (%) | |||||||||||

Reported ROE(1) | 12.5 | % | 17.1 | % | |||||||

Underlying ROE(1) | 15.1 | % | 15.4 | % | |||||||

| Growth | 2022 | 2021 | |||||||||

| Sales | |||||||||||

Insurance sales(1) | 4,321 | 3,674 | |||||||||

Wealth sales and asset management gross flows(1) | 204,113 | 228,408 | |||||||||

Value of new business ("VNB")(1) | 1,253 | 1,346 | |||||||||

Assets under management(1) | |||||||||||

| General fund assets | 205,614 | 205,374 | |||||||||

| Segregated funds | 125,292 | 139,996 | |||||||||

Other AUM(1) | 994,953 | 1,099,358 | |||||||||

Total AUM(1) | 1,325,859 | 1,444,728 | |||||||||

| Financial Strength | 2022 | 2021 | |||||||||

LICAT ratios(2) | |||||||||||

| Sun Life Financial Inc. | 130 | % | 145 | % | |||||||

Sun Life Assurance(3) | 127 | % | 124 | % | |||||||

Financial leverage ratio(1)(4) | 25.1 | % | 25.5 | % | |||||||

| Dividend | |||||||||||

Dividend payout ratio(1) | 44 | % | 38 | % | |||||||

| Dividends per common share ($) | 2.760 | 2.310 | |||||||||

| Capital | |||||||||||

Subordinated debt(4) | 6,676 | 6,425 | |||||||||

Innovative capital instruments(5) | 200 | 200 | |||||||||

| Participating policyholders' equity | 1,837 | 1,700 | |||||||||

| Non-controlling interest equity | 90 | 59 | |||||||||

| Preferred shares and other equity instruments | 2,239 | 2,239 | |||||||||

Common shareholders' equity(6) | 25,211 | 24,075 | |||||||||

Total capital(4) | 36,253 | 34,698 | |||||||||

| Weighted average common shares outstanding for basic EPS (millions) | 586 | 586 | |||||||||

| Closing common shares outstanding (millions) | 586 | 586 | |||||||||

(1)Represents a non-IFRS financial measure. For more details, see section L - Non-IFRS Financial Measures in this document.

(2)Life Insurance Capital Adequacy Test ("LICAT") ratio. Our LICAT ratios are calculated in accordance with OSFI-mandated guideline, Life Insurance Capital Adequacy Test.

(3)Sun Life Assurance Company of Canada ("Sun Life Assurance") is SLF Inc.’s principal operating life insurance subsidiary.

(4)For 2021, amount included $2.0 billion of proceeds from the subordinated debt offerings completed in November 2021, of which $1.5 billion did not qualify as LICAT capital at issuance as it was subject to contractual terms requiring us to redeem the underlying securities in full, if the closing of the DentaQuest acquisition did not occur. We completed the acquisition of DentaQuest on June 1, 2022.

(5)Innovative capital instruments consist of Sun Life ExchangEable Capital Securities ("SLEECS"), which qualify as regulatory capital. However, under IFRS they are reported as Senior debentures in the Consolidated Financial Statements. For additional information, see section I - Capital and Liquidity Management in this document.

(6)Common shareholders’ equity is equal to Total shareholders’ equity less Preferred shares and other equity instruments.

16 December 31, 2022 Sun Life Financial Inc. MANAGEMENT'S DISCUSSION & ANALYSIS

| D. Profitability | ||||||||||||||

The following table reconciles our Common shareholders' net income ("reported net income") and underlying net income. The table also sets out the impacts that other notable items had on reported net income and underlying net income. All factors discussed in this document that impact underlying net income are also applicable to reported net income.

| ($ millions, after-tax) | 2022 | 2021 | |||||||||

| Reported net income - Common shareholders | 3,060 | 3,934 | |||||||||

Less: Market-related impacts(1) | (410) | 627 | |||||||||

Assumption changes and management actions(1) | 62 | 74 | |||||||||

Other adjustments(1)(2) | (266) | (300) | |||||||||

Underlying net income(3) | 3,674 | 3,533 | |||||||||

Reported ROE(3) | 12.5 | % | 17.1 | % | |||||||

Underlying ROE(3) | 15.1 | % | 15.4 | % | |||||||

Experience-related items attributable to reported and underlying net income(3)(4) | |||||||||||

| Impacts of investment activity on insurance contract liabilities ("investing activity") | 247 | 144 | |||||||||

| Credit | 81 | 114 | |||||||||

| Mortality | (97) | (111) | |||||||||

| Morbidity | 141 | 39 | |||||||||

| Lapse and other policyholder behaviour ("policyholder behaviour") | (30) | (31) | |||||||||

| Expenses | 22 | (170) | |||||||||

| Other experience | (71) | (56) | |||||||||

Total of experience-related items(3)(4) | 293 | (71) | |||||||||

(1)Represents an adjustment made to arrive at a non-IFRS financial measure. For more details, see section L - Non-IFRS Financial Measures in this document for a breakdown of components within this adjustment, including pre-tax amounts.

(2)Other adjustments to arrive at a non-IFRS financial measure include other items that are unusual or exceptional in nature. See section L - Non-IFRS Financial Measures L - Non-IFRS Financial Measures in this document.

(3)Represents a non-IFRS financial measure. For more details, see section L - Non-IFRS Financial Measures in this document.

(4)Experience-related items reflect the difference between actual experience during the reporting period and best estimate assumptions used in the determination of our insurance contract liabilities. Experience-related items are a part of the Sources of Earnings framework, and are calculated in accordance with OSFI Guideline D-9, Sources of Earnings Disclosures. Experience-related items from our India, China and Malaysia joint ventures and associates are recorded within other experience.

2022 vs. 2021

Reported net income of $3,060 million decreased $874 million or 22%, reflecting unfavourable market-related impacts, a prior year gain on the IPO of our India asset management joint venture, a $170 million charge related to the sale of Sun Life UK(1) and DentaQuest acquisition and integration costs, partially offset by fair value changes on MFS'(2) share-based payment awards and the impact of the Canada Tax Rate Change(3).

Underlying net income of $3,674 million(4) increased $141 million or 4%, driven by business growth and experience in protection and health, contribution from the DentaQuest acquisition, and lower incentive compensation expenses. This was partially offset by lower wealth and asset management earnings reflecting declines in global equity markets, a higher effective tax rate compared to prior year and lower available-for-sale ("AFS") gains.

Foreign exchange translation led to an increase of $67 million and $52 million in reported net income and underlying net income, respectively.

1.Market-related impacts

Market-related impacts resulted in a decrease of $410 million to reported net income (2021 - an increase of $627 million), reflecting interest rate movements and lower equity markets, partially offset by an increase in the value of real estate investments. See section L - Non-IFRS Financial Measures in this document for a breakdown of the components of market-related impacts.

(1)On August 4, 2022, we entered into an agreement to sell SLF of Canada UK Limited ("Sun Life UK") to Phoenix Group Holdings plc ("Phoenix Group"). In Q3'22, we recognized an impairment charge of $170 million (£108 million) pertaining to the attributed goodwill that is not expected to be recovered through the sale ("sale of Sun Life UK"). For more details, see section B - Overview - 4 - Acquisitions and Other in this document.

(2)MFS Investment Management ("MFS").

(3)On December 15, 2022, legislation implementing an additional surtax of 1.5% applicable to banks and life insurers’ taxable income in excess of $100 million was enacted in Canada ("Canada Tax Rate Change"). This legislation applies retroactively to the Federal Budget date of April 7, 2022. As a result, reported net income increased by $127 million in the fourth quarter, reflected in Assumption changes and management actions ("ACMA") and Other adjustments. Refer to section D - Profitability - 5 - Income taxes in this document for more information.

(4)Refer to section L - Non-IFRS Financial Measures in this document for a reconciliation between reported net income and underlying net income.

MANAGEMENT'S DISCUSSION & ANALYSIS Sun Life Financial Inc. December 31, 2022 17

2.Assumption changes and management actions

Due to the long-term nature of our business, we make certain judgments involving assumptions and estimates to value our obligations to policyholders. The valuation of these obligations is recorded in our financial statements as insurance contract liabilities and investment contract liabilities and requires us to make assumptions about equity market performance, interest rates, asset default, mortality and morbidity rates, policyholder behaviour, expenses and inflation and other factors over the life of our products. We review assumptions each year, generally in the third quarter, and revise these assumptions if appropriate. We consider our actual experience in current and past periods relative to our assumptions as part of our annual review.

The net impact of ACMA was an increase of $62 million to reported net income (2021 - an increase of $74 million). See section L - Non-IFRS Financial Measures in this document for more details.

Assumption Changes and Management Actions by Type

The following table sets out the impacts of ACMA on our reported net income in 2022.

| As at December 31, 2022 | ||||||||

| ($ millions, after-tax) | Impacts on reported net income(1) | Comments | ||||||

| Mortality / morbidity | 90 | Updates to reflect mortality/morbidity experience in all jurisdictions. The largest items were favourable mortality impacts in the UK in Corporate and in Group Retirement Services ("GRS") in Canada offset partially by adverse morbidity impacts in Sun Life Health in Canada. | ||||||

Policyholder behaviour | (65) | Updates to lapse and policyholder behaviour in all jurisdictions. The largest item was an adverse lapse impact in Vietnam in Asia. | ||||||

| Expenses | (11) | Updates to reflect expense experience. | ||||||

| Investment returns | (10) | Updates to various investment-related assumptions. | ||||||

| Model enhancements and other | 58 | Various enhancements and methodology changes. | ||||||

Total impacts on reported net income(2) | 62 | |||||||

(1)ACMA is included in reported net income and is presented as an adjustment to arrive at underlying net income.

(2)In this table, ACMA represents the shareholders' reported net income impacts (after-tax) including management actions. In Note 10.A of our 2022 Consolidated Financial Statements for the period ended December 31, 2022, the impacts of method and assumptions changes represents the change in shareholders' and participating policyholders' insurance contract liabilities net of reinsurance assets (pre-tax) and does not include management actions. Further information can be found in section L - Non-IFRS Financial Measures in this document.

Additional information on estimates relating to our policyholder obligations, including the methodology and assumptions used in their determination, can be found in this MD&A under section M - Accounting and Control Matters - 1 - Critical Accounting Policies and Estimates and Note 10 of our 2022 Annual Consolidated Financial Statements.

3.Other adjustments

Other adjustments decreased reported net income $266 million (2021 - a decrease of $300 million), reflecting a $170 million charge related to the sale of Sun Life UK(1), DentaQuest acquisition and integration costs, an increase in SLC Management's acquisition-related liabilities(2) and a charge reflecting the resolution of a matter related to reinsurance pricing for our U.S. In-force Management business, partially offset by fair value changes on MFS' share-based payment awards, an increase in the value of deferred tax assets related to the Canada Tax Rate Change(3), and a gain on the sale-leaseback of the Wellesley office in the U.S.

4. Experience-related items

The notable experience-related items, which impact current year reported and underlying net income, are as follows:

•Favourable investing activity gains across the businesses;

•Favourable credit across the businesses;

•Unfavourable mortality which primarily included COVID-19-related experience;

•Favourable morbidity driven by U.S. medical stop-loss;

•Unfavourable policyholder behaviour primarily in Asia;

•Favourable expense experience, driven by lower corporate expenses and incentive compensation costs; and

•Unfavourable other experience reflecting higher project spend.

(1)On August 4, 2022, we entered into an agreement to sell SLF of Canada UK Limited ("Sun Life UK") to Phoenix Group Holdings plc ("Phoenix Group"). In Q3'22, we recognized an impairment charge of $170 million (£108 million) pertaining to the attributed goodwill that is not expected to be recovered through the sale ("sale of Sun Life UK"). For more details, see section B - Overview - 4 - Acquisitions and Other in this document.

(2)Reflects the changes in estimated future payments for acquisition-related contingent considerations and options to purchase remaining ownership interests of SLC Management affiliates.

(3)On December 15, 2022, legislation implementing an additional surtax of 1.5% applicable to banks and life insurers’ taxable income in excess of $100 million was enacted in Canada ("Canada Tax Rate Change"). This legislation applies retroactively to the Federal Budget date of April 7, 2022. As a result, reported net income increased by $127 million in the fourth quarter, reflected in ACMA and Other adjustments. Refer to section D - Profitability - 5 - Income taxes in this document for more information.

18 December 31, 2022 Sun Life Financial Inc. MANAGEMENT'S DISCUSSION & ANALYSIS

5.Income taxes

The effective tax rate is impacted by various tax benefits, such as lower taxes on income subject to tax in foreign jurisdictions, a range of tax-exempt investment income, and other sustainable tax benefits.

On December 15, 2022, legislation implementing an additional surtax of 1.5% applicable to banks and life insurers’ taxable income in excess of $100 million was enacted in Canada. This legislation applies retroactively to the Federal Budget date of April 7, 2022. As a result, reported net income increased by $127 million in the fourth quarter, reflected in ACMA and Other adjustments. The increase was comprised of after-tax income of $22 million ($31 million pre-tax) in ACMA in Canada, and income of $115 million on the remeasurement of deferred tax assets, partially offset by the impact of the retroactive increase in the tax rate of $10 million in Canada and Corporate in Other adjustments.

The effective tax rates on reported net income and underlying net income(1) were 15.8% and 16.8%, respectively (2021 - 14.3% and 13.5%, respectively). In 2022, the effective tax rate on underlying net income was within our expected range of 15% to 20%. In 2021, the effective tax rate on underlying net income was slightly below the expected range primarily due to higher tax-exempt investment income and resolutions of prior years' tax matters. For additional information, refer to Note 20 of our 2022 Annual Consolidated Financial Statements.

6.Impacts of foreign exchange translation

We operate in many markets worldwide, including Canada, the United States, the United Kingdom, Ireland, Hong Kong, the Philippines, Japan, Indonesia, India, China, Australia, Singapore, Vietnam, Malaysia and Bermuda, and generate revenues and incur expenses in local currencies in these jurisdictions, which are translated to Canadian dollars.

Items impacting our Consolidated Statements of Operations are translated into Canadian dollars using average exchange rates for the respective period. For items impacting our Consolidated Statements of Financial Position, period end rates are used for currency translation purposes.

The following table provides the foreign exchange rates for the U.S. dollar, which generates the most significant impact of foreign exchange translation, over the past four quarters and two years.

| Exchange rate | Quarterly | Full year | ||||||||||||||||||

| Q4'22 | Q3'22 | Q2'22 | Q1'22 | 2022 | 2021 | |||||||||||||||

U.S. Dollar - Average | 1.358 | 1.304 | 1.276 | 1.267 | 1.301 | 1.254 | ||||||||||||||

| U.S. Dollar - Period end | 1.355 | 1.383 | 1.287 | 1.250 | 1.355 | 1.263 | ||||||||||||||

The relative impacts of foreign exchange translation in any given period are driven by the movement of foreign exchange rates as well as the proportion of earnings generated in our foreign operations. In general, net income benefits from a weakening Canadian dollar and is adversely affected by a strengthening Canadian dollar as net income from the Company's international operations is translated back to Canadian dollars. Conversely, in a period of losses, the weakening of the Canadian dollar has the effect of increasing losses in foreign jurisdictions. We generally express the impacts of foreign exchange translation on net income on a year-over-year basis.

The impacts of foreign exchange translation led to an increase of $67 million and $52 million in reported net income and underlying net income, respectively.

(1)Our effective income tax rate on reported net income is calculated using Total income (loss) before income taxes, as detailed in Note 20 in our 2022 Consolidated Financial Statements for the period ended December 31, 2022. Our effective income tax rate on underlying net income is calculated using pre-tax underlying net income, as detailed in section L - Non-IFRS Financial Measures in this document, and the associated income tax expense.

MANAGEMENT'S DISCUSSION & ANALYSIS Sun Life Financial Inc. December 31, 2022 19

| E. Growth | |||||

1. Sales, Gross Flows and Value of New Business

| ($ millions) | 2022 | 2021 | ||||||

Insurance sales by business segment(1) | ||||||||

| Canada | 1,029 | 852 | ||||||

| U.S. | 1,948 | 1,564 | ||||||

| Asia | 1,344 | 1,258 | ||||||

Total insurance sales(1) | 4,321 | 3,674 | ||||||

Wealth sales and gross flows by business segment(1) | ||||||||

Canada | 20,092 | 19,854 | ||||||

| Asia | 11,140 | 15,491 | ||||||

| Total wealth sales | 31,232 | 35,345 | ||||||

Asset Management gross flows(1) | 172,881 | 193,063 | ||||||

Total wealth sales and asset management gross flows(1) | 204,113 | 228,408 | ||||||

Value of New Business(1) | 1,253 | 1,346 | ||||||

(1)Represents a non-IFRS financial measure. For more details, see section L - Non-IFRS Financial Measures in this document.

Total insurance sales increased $647 million or 18% from prior year ($548 million or 15%(1), excluding foreign exchange translation).

•Canada insurance sales increased 21%,driven by large case group benefits sales in Sun Life Health.

•U.S. insurance sales increased 18%(1), driven by growth in dental(2) and employee benefit sales partially offset by lower medical stop-loss sales.

•Asia insurance sales increased 8%(1), driven by higher sales in India, Vietnam, the Philippines, Singapore and Malaysia, partially offset by lower sales in Hong Kong and International.

Total wealth sales and asset management gross flows decreased $24,295 million or 11% from prior year ($29,330 million or 13%(1), excluding foreign exchange translation).

•Canada wealth sales were in line with prior year as higher defined contribution(3) sales in GRS were mostly offset by lower individual wealth sales.

•Asia wealth sales decreased 26%(1), reflecting lower sales in India, Hong Kong and the Philippines.

•Asset Management gross flows decreased 13%(1), reflecting lower retail gross flows in MFS and lower institutional gross flows in SLC Management.

Total VNB of $1,253 million decreased 7% from prior year, driven by lower wealth sales.

(1)This percentage change excludes the impacts of foreign exchange translation. For more information about these non-IFRS financial measures, see section L - Non-IFRS Financial Measures in this document.

(2)Dental sales include sales from DentaQuest, acquired on June 1, 2022.

(3)Defined contribution sales include retained business sales.

20 December 31, 2022 Sun Life Financial Inc. MANAGEMENT'S DISCUSSION & ANALYSIS

2. Assets Under Management

AUM consists of general funds, the investments for segregated fund holders ("segregated funds") and other AUM, which is comprised of other third-party assets managed by the Company.

| ($ millions) | 2022 | 2021 | ||||||

Assets under management(1) | ||||||||

| General fund assets | 205,614 | 205,374 | ||||||

| Segregated funds | 125,292 | 139,996 | ||||||

Other assets under management(1) | ||||||||

Retail(2)(3) | 527,617 | 623,611 | ||||||

Institutional and managed funds(2)(3) | 507,673 | 517,591 | ||||||

| Consolidation adjustments and other | (40,337) | (41,844) | ||||||

Total other AUM(1) | 994,953 | 1,099,358 | ||||||

Total assets under management(1) | 1,325,859 | 1,444,728 | ||||||

(1)Represents a non-IFRS financial measure. See section L - Non-IFRS Financial Measures in this document.

(2)Effective January 1, 2022, these components were renamed to Retail and Institutional and managed funds. Previously, these components of Other AUM were referred to as Mutual funds and Managed funds, respectively, in our interim and annual MD&A.

(3)Effective October 1, 2022, the classification of a MFS fund has changed from Institutional and managed funds to Retail. Other retail and trust accounts have also been reclassified from Institutional and managed funds to Retail. Prior periods have been restated.

AUM decreased $118.9 billion or 8% from December 31, 2021, primarily driven by:

(i)unfavourable market movements on the value of segregated, retail, institutional and managed funds of $159.9 billion;

(ii)net outflows from segregated, retail, institutional and managed funds of $21.5 billion; and

(iii)Client distributions of $4.6 billion; partially offset by

(iv)an increase of $57.3 billion from foreign exchange translation (excluding the impacts of general fund assets); and

(v)an increase of $9.5 billion from other business activities.

Segregated, retail, institutional and managed fund net outflows of $21.5 billion in 2022 were largely driven by net outflows of $43.4 billion in MFS, partially offset by net inflows of $21.5 billion in SLC Management.

Retail, Institutional and managed funds and other AUM decreased by $104.4 billion or 9% from December 31, 2021, primarily driven by:

(i)unfavourable market movements of $144.6 billion;

(ii)net outflows of $23.5 billion; and

(iii)Client distributions of $4.6 billion; partially offset by

(iv)foreign exchange translation of $57.6 billion; and

(v)other business activities of $10.7 billion.

MANAGEMENT'S DISCUSSION & ANALYSIS Sun Life Financial Inc. December 31, 2022 21

| F. Financial Strength | |||||

| ($ millions, unless otherwise stated) | 2022 | 2021 | ||||||

LICAT ratio(1) | ||||||||

Sun Life Financial Inc. | 130 | % | 145 | % | ||||

Sun Life Assurance | 127 | % | 124 | % | ||||

Financial leverage ratio(2)(3) | 25.1 | % | 25.5 | % | ||||

| Dividend | ||||||||

Underlying dividend payout ratio(2) | 44 | % | 38 | % | ||||

| Dividends per common share ($) | 2.760 | 2.310 | ||||||

Capital | ||||||||

Subordinated debt(3) | 6,676 | 6,425 | ||||||

Innovative capital instruments(4) | 200 | 200 | ||||||

| Participating policyholders' equity | 1,837 | 1,700 | ||||||

| Non-controlling interests | 90 | 59 | ||||||

| Preferred shares and other equity instruments | 2,239 | 2,239 | ||||||

Common shareholders' equity(5) | 25,211 | 24,075 | ||||||

Total capital(3) | 36,253 | 34,698 | ||||||

(1)Our LICAT ratios are calculated in accordance with OSFI-mandated guideline, Life Insurance Capital Adequacy Test.

(2)Represents a non-IFRS financial measure. For more details, see section L - Non-IFRS Financial Measures in this document.

(3)For 2021, amount included $2.0 billion of proceeds from the subordinated debt offerings completed in November 2021, of which $1.5 billion did not qualify as LICAT capital at issuance as it was subject to contractual terms requiring us to redeem the underlying securities in full, if the closing of the DentaQuest acquisition did not occur. We completed the acquisition of DentaQuest on June 1, 2022.

(4)Innovative capital instruments consist of SLEECS and qualify as regulatory capital. However, under IFRS they are reported as Senior debentures in our Consolidated Financial Statements. For additional information, see section I - Capital and Liquidity Management - 1 - Capital in this document.

(5)Common shareholders’ equity is equal to Total shareholders’ equity less Preferred shares and other equity instruments.

Life Insurance Capital Adequacy Test

The Office of the Superintendent of Financial Institutions has developed the regulatory capital framework referred to as the Life Insurance Capital Adequacy Test for Canada. LICAT measures the capital adequacy of an insurer using a risk-based approach and includes elements that contribute to financial strength through periods when an insurer is under stress as well as elements that contribute to policyholder and creditor protection wind-up.

SLF Inc. is a non-operating insurance company and is subject to the LICAT guideline. As of December 31, 2022, SLF Inc.'s LICAT ratio was 130%, 15 percentage points lower than December 31, 2021, primarily reflecting the DentaQuest acquisition, market-related impacts and dividend payments, partially offset by reported net income, net subordinated debt issuance, net management actions and the smoothing impact of the interest rate scenario switch in North America for participating businesses.

Sun Life Assurance, SLF Inc.'s principal operating life insurance subsidiary, is also subject to the LICAT guideline. As of December 31, 2022, Sun Life Assurance's LICAT ratio was 127%, 3 percentage points higher than December 31, 2021, primarily reflecting reported net income, net management actions and the smoothing impact of the interest rate scenario switch in North America for participating businesses, partially offset by market-related impacts and dividend payments to SLF Inc.

The Sun Life Assurance LICAT ratio at the end of 2022 and 2021 was well above OSFI's supervisory ratio of 100% and regulatory minimum ratio of 90%.

Capital

Our total capital consists of subordinated debt and other capital instruments, participating policyholders' equity and total shareholders' equity which includes common shareholders' equity, preferred shares and other equity instruments, and non-controlling interests. As at December 31, 2022, our total capital was $36.3 billion, an increase of $1.6 billion compared to December 31, 2021. The increase to total capital included reported net income of $3,060 million, the favourable impacts of foreign exchange translation of $934 million included in other comprehensive income (loss) ("OCI"), and the issuance of $650 million principal amount of Series 2022-1 Subordinated Unsecured 4.78% Fixed/Floating Debentures, which is detailed below. This was partially offset by net unrealized losses on AFS assets of $1,290 million, the payment of $1,614 million of dividends on common shares of SLF Inc. ("common shares"), and the redemption of $400 million principal amount of Series 2017-1 Subordinated Unsecured 2.75% Fixed/Floating Debentures, which is detailed below.

Our capital and liquidity positions remain strong with a LICAT ratio of 130% at SLF Inc., a financial leverage ratio of 25.1%(1)(2) and $1.1 billion in cash and other liquid assets(1)(2) as at December 31, 2022 in SLF Inc. (the ultimate parent company), and its wholly-owned holding companies (December 31, 2021 - $4.7 billion).

(1)Represents a non-IFRS financial measure. For more details, see section L - Non-IFRS Financial Measures in this document.

(2)For 2021, amount included $2.0 billion of proceeds from the subordinated debt offerings completed in November 2021, of which $1.5 billion did not qualify as LICAT capital at issuance as it was subject to contractual terms requiring us to redeem the underlying securities in full, if the closing of the DentaQuest acquisition did not occur. We completed the acquisition of DentaQuest on June 1, 2022.

22 December 31, 2022 Sun Life Financial Inc. MANAGEMENT'S DISCUSSION & ANALYSIS

Capital Transactions

On August 10, 2022, SLF Inc. issued $650 million principal amount of Series 2022-1 Subordinated Unsecured 4.78% Fixed/Floating Debentures due 2034. The net proceeds will be used for general corporate purposes of the Company, which may include investments in subsidiaries, repayment of indebtedness and other strategic investments.

On November 23, 2022, SLF Inc. redeemed all of the outstanding $400 million principal amount of Series 2017-1 Subordinated Unsecured 2.75% Fixed/Floating Debentures, in accordance with the redemption terms attached to such debentures. The redemptions were funded from existing cash and other liquid assets in SLF Inc.

During the fourth quarter, a matter related to reinsurance pricing for our U.S. In-force Management business was resolved. Sun Life recaptured the reinsurance treaty, which resulted in a net reduction to the SLF Inc. LICAT ratio of approximately two percentage points.

Financial Strength Ratings

Independent rating agencies assign credit ratings to securities issued by companies and assign financial strength ratings to financial institutions such as Sun Life Assurance.

The financial strength ratings assigned by rating agencies are intended to provide an independent view of the creditworthiness and financial strength of a financial institution. Each rating agency has developed its own methodology for the assessment and subsequent rating of life insurance companies.

Rating agencies do not assign a financial strength rating for SLF Inc., however, credit ratings are assigned to the securities issued by SLF Inc. and its subsidiaries and are described in SLF Inc.'s AIF under the heading Security Ratings.

The following table summarizes the financial strength ratings for Sun Life Assurance as at January 31, 2023 and January 31, 2022.

| A.M. Best | DBRS | Moody's | Standard & Poor's | |||||||||||

| January 31, 2023 | A+ | AA | Aa3 | AA | ||||||||||

| January 31, 2022 | A+ | AA | Aa3 | AA | ||||||||||

Most recent rating agency actions on the financial strength rating of Sun Life Assurance:

•March 23, 2022 - Standard and Poor's ("S&P") affirmed the financial strength rating with a stable outlook.

•April 1, 2021 - Moody's affirmed the financial strength rating with a stable outlook.

•October 27, 2022 - DBRS affirmed the financial strength rating with a stable outlook.

•January 28, 2022 - A.M. Best affirmed the financial strength rating with a stable outlook.

Subsequent Events

For additional information, refer to Note 28 of our 2022 Annual Consolidated Financial Statements.

On January 20, 2023, we announced a 15-year exclusive bancassurance partnership in Hong Kong with Dah Sing Bank ("Dah Sing"). Under this partnership, Sun Life will be the exclusive provider of life insurance solutions to Dah Sing's 570,000 retail banking customers, helping to fulfill their savings and protection needs at different life stages. This is Sun Life's first exclusive bancassurance partnership in Hong Kong and will be a valuable complement to our existing network of over 2,500 expert insurance advisors. Hong Kong is a thriving life insurance hub in Asia and bancassurance is a key distribution channel, accounting for more than 50% of the life insurance distribution mix. Following the completion of regulatory processes and approvals, distribution of Sun Life products is anticipated to start in July 2023.

On February 1, 2023, we completed the acquisition of a 51%(1) interest in Advisors Asset Management, Inc. ("AAM"), a leading independent U.S. retail distribution firm. AAM provides access to U.S. retail distribution for SLC Management, Sun Life's institutional fixed income and alternatives asset manager. This allows SLC Management to meet the growing demand among U.S. HNW investors for alternative assets. AAM provides a range of solutions and products to financial advisors at wirehouses, registered investment advisors and independent broker-dealers, overseeing US$40.5 billion (approximately C$55 billion) in assets as at December 31, 2022, with 10 offices across nine U.S. states.

On February 1, 2023, we completed the sale of our sponsored markets business from Sun Life Assurance Company of Canada ("SLA"), a wholly owned subsidiary of SLF Inc., to Canadian Premier Life Insurance Company ("Canadian Premier"). Sponsored markets include a variety of association & affinity, and group creditor clients.

(1)On a fully diluted basis.

MANAGEMENT'S DISCUSSION & ANALYSIS Sun Life Financial Inc. December 31, 2022 23

| G. Performance by Business Segment | |||||

Sun Life's business is well-diversified across geographies and business types, supported by our four pillar strategy and diversified offerings of wealth and insurance products.

| ($ millions) | 2022 | 2021 | ||||||

| Reported net income (loss) - Common shareholders | ||||||||

| Canada | 1,000 | 1,558 | ||||||

| U.S. | 586 | 499 | ||||||

| Asset Management | 1,141 | 892 | ||||||

| Asia | 515 | 1,075 | ||||||

| Corporate | (182) | (90) | ||||||

| Total reported net income (loss) - Common shareholders | 3,060 | 3,934 | ||||||

Underlying net income (loss)(1) | ||||||||

| Canada | 1,266 | 1,131 | ||||||

| U.S. | 728 | 518 | ||||||

| Asset Management | 1,204 | 1,346 | ||||||

| Asia | 627 | 586 | ||||||

| Corporate | (151) | (48) | ||||||

Total underlying net income (loss)(1) | 3,674 | 3,533 | ||||||

(1)Represents a non-IFRS financial measure. For more details, see section L - Non-IFRS Financial Measures in this document.

All factors discussed in this document that impact our underlying net income are also applicable to reported net income.

1. Canada

| Our Canada business segment is a leading provider of protection, health, asset management and wealth solutions, providing products and services that deliver value to over 6.6 million Clients. We are the largest provider of benefits and pensions in the workplace, and offer a wide range of products to individuals via retail channels. We are focused on helping Canadians achieve lifetime financial security and live healthier lives. | ||||||||

| Business Units | ||||||||

| • Individual Insurance & Wealth | • Sun Life Health | • Group Retirement Services | ||||||

2022 Highlights

Putting Client Impact at the centre of everything we do, driving positive financial and health actions and outcomes

•As part of the Net Zero Asset Manager’s(1) ("NZAM") Initiative, SLGI Asset Management Inc. supports the goal of net zero greenhouse gas ("GHG") emissions by 2050, and set out an initial target to have, by 2030, 24% of total AUM(2) to be net zero aligned or aligning(3). This will be achieved by executing on investment strategies that drive long-term sustainable outcomes while helping our Clients build wealth and secure their financial futures.

•Expanded our suite of sustainable wealth and asset management product offerings including our first green bond fund(4), which seeks to provide members a direct way to participate in the transition to a low-carbon economy and our first Shariah-based pool fund(5), which gives members an option that reflects Islamic principles.

•Created over 65,000 financial roadmaps using our Sun Life One Plan digital tool, contributing to our ambition for all Canadians to have a financial plan. We also enhanced our tools with a digital navigation portal, making it easier for Clients to track progress and build flexible scenarios into financial plans.

•Advanced our Diabetes Signature Solutions program helping address a major health concern in Canada. The program helps Canadians with type 2 diabetes get access to affordable life insurance coverage. In addition, access to a specialized diabetes clinic and wellness platform for some regions in Canada provides content to help Clients achieve their health goals.

•Recognizing that Canadians build families in different ways, Sun Life Health launched a new Family Building Program as an optional benefit that will provide plan members medical and non-medical coverage for fertility treatments, surrogacy arrangements and adoption.

(1)An international group of asset managers committed to supporting the goal of achieving net zero greenhouse gas emissions by 2050 or sooner.

(2)The target assumes the mix of AUM will not materially change.

(3)Aligning towards or aligned to a net zero pathway as defined by criteria set out in the Net Zero Investment Framework. Criteria are asset class-specific. Pathways is the term used to describe the emissions, technologies and investment trajectories that will be needed to deliver net zero. (Paris Aligned Investment Initiative. “Net Zero Investment Framework: Implementation Guide”. 2021).

(4)AlphaFixe Green Bond Fund.

(5)BlackRock MSCI ACWI Islamic Equity Index Fund.

24 December 31, 2022 Sun Life Financial Inc. MANAGEMENT'S DISCUSSION & ANALYSIS

Shaping the market and driving growth

•Maintained our leading position in the group retirement market(1) with defined contribution assets under administration of over $133 billion. We extended our digital leadership in this space with innovations like our Sun Life One Plan and an enhanced mobile experience. In the pension risk transfer business, Defined Benefit Solutions, we achieved $2.1 billion in sales, assisting Canadian employers to de-risk their pension plans.

•Sun Life Health maintained its market leadership position in group benefits(2), with over $12.8 billion of business-in-force, continuing to proactively advance our focus on mental health in workplaces across Canada. We introduced Lumino Health Virtual Care’s Stress Management and Well-Being program providing members access to mental health and medical specialists 24/7.

•In Individual Wealth, broadened the product shelf, expanded distributor access, deepened advisor relationships, and attracted strong talent.

•In a challenging year for mutual fund industry net sales, SLGI Asset Management Inc. improved market share rank by six places to 9th (3). We also launched a sustainable credit private pool fund(4), providing Clients access to an alternative investment strategy.

•Recognized as one of the 2022 Best Workplaces in Canada by Great Place to Work® Canada, celebrating our commitment to our people. We maintain an equitable environment where diversity is championed, as well as offer resources and flexibility to support mental, physical and professional well-being.

Thinking and acting like a digital company

•Launched Prospr by Sun Life, a hybrid advice solution combining a best-in-class digital platform with a team of licensed advisors, to meet Canadians' personalized and holistic financial planning needs. Prospr by Sun Life makes it easier for Canadians to select, prioritize and track their financial goals all in one place.

•Launched Employee Assistance Program ("EAP") platform through Lumino Health Virtual Care. This all-in-one solution provides members access to professional support, the ability to get a personalized assessment within minutes and 24/7 access to online Cognitive Behavioural Therapy ("iCBT").

•Positively engaged Clients over 27 million times through Ella, our digital coach, an increase of 34% over prior year. Ella delivers proactive and personalized interactions to help our Clients achieve their health and financial goals.

•Made it easier for Clients to do business with us by digitally processing 93% of our retail insurance applications, 85% of retail wealth transactions and 96% of group benefits health and dental claims throughout the year.

•Introduced a new Voluntary Benefit eApp which consolidates our voluntary benefit products into a single resource, reducing the application process time for Clients by up to 50%.

Strategy and Outlook

Canada is a growth market for Sun Life. We have a unique opportunity to address health, wealth and protection holistically with our diversified products and services. We will continue to shape the market and deliver on our Purpose through an integrated approach that helps Canadians achieve lifetime financial security and live healthier lives. We aspire to achieve our strategic ambition and further our market differentiation by focusing on Client impact, enabled by digital leadership and distribution excellence. We look to incorporate sustainability into our culture and decision making to deliver a positive social impact, increase Client and employee engagement, and introduce new, innovative products. Our focus for the Canadian businesses will be to:

Advance our One Sun Client strategy

•Offer customized solutions for our Clients to help them achieve their health, wealth, and protection goals.

•Build and scale an omni-channel advice and service model to meet all Client needs and expand our reach in the market. This includes combining face-to-face advisors and best-in-class digital platforms to offer Clients flexibility to move across channels seamlessly, including direct access through self-serve platforms and capabilities.

Accelerate our wealth strategy

•Scale and accelerate SLGI Asset Management Inc. as a growth engine within Canada, empowering Clients with more convenient access to investment solutions and a holistic product suite to meet their asset management needs.

•Accelerate progress towards being the retirement income provider of choice by leveraging our scale and understanding Client goals while providing member and sponsor tools.

•Provide Clients with seamless planning, asset consolidation capabilities, and a unified experience across our wealth channels.

•Continue to be a market leader in the growing Canadian pension risk transfer market, with customized solutions to meet employers’ needs in managing and de-risking their defined benefit pension plans.

Strengthen and expand our health business

•Offer innovative solutions by leveraging our relationships with millions of group and retail Clients, to empower Canadians to act earlier to prevent and mitigate physical and mental health risks.

•To promote early intervention for mental disorders, we will engage at-risk group benefits plan members by prompting access to care through our virtual Mental Health Coach.

•Expand our virtual care options, powered by Lumino Health provider platform, to help members digitally access virtual primary care, employee assistance program, and stress management and well-being programs so that they can achieve better health outcomes, and reduce costs.

•Develop targeted insurance solutions for Canadians living with chronic conditions, for example diabetes, to improve insurability.

•Leveraging the Toronto Raptors' health and wellness experts and Sun Life's health ecosystem, we will motivate fans and communities to focus on their health and wellness through Sun Life's health offerings.

(1)Fraser Pension Universe Report, year-ended December 2021.

(2)Revenue for year ended December 2021 from 2022 Group Benefits Provider Report.

(3)ISS Market Intelligence Simfund, September 2022.

(4)Sun Life Crescent Specialty Private Pool Fund.

MANAGEMENT'S DISCUSSION & ANALYSIS Sun Life Financial Inc. December 31, 2022 25

Transform retail distribution

•Strengthen and modernize our dedicated face-to-face advice model by updating digital tools and enhancing financial planning capabilities.

•Effectively integrate our direct-to-consumer distribution channels under Prospr by Sun Life to offer Clients the flexibility to move across channels seamlessly, based on their individual needs.

Sustain financial discipline

•Enhance advisor and Client experiences and drive operational efficiencies through digital initiatives such as straight-through processing and data consolidation.

•Continue to augment predictive underwriting models, utilizing advanced data analytics and predictive modelling to enhance our Client experience with easier access to products, while minimizing underwriting risk.

•Seek low-cost, innovative opportunities focusing on capital and risk optimization.

Outlook

Our diversified business, which address Clients' needs in asset and wealth management, as well as life and health protection and multi-channel distribution, positions us well to deepen Client relationships and capture opportunities as they arise. We expect to continue to reach more Clients through investing in enhancements to our products, systems, distribution and digital capabilities. We will meet our Clients' needs by providing diverse offerings, holistic advice and a personalized plan throughout their wealth and health journeys. We are confident that our leadership position in Canada will continue to generate value and positive outcomes for Clients.

We are well positioned to manage through macroeconomic uncertainty, including equity market downturn and rising inflation and interest rates, through pricing discipline, diversified Client centric businesses, and prudent risk management.

Business Units | ||||||||||||||

| Business | Description | Market position | ||||||