UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2019

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission File Number 001-35370

(Exact Name of Registrant as Specified in Its Charter)

State or Other Jurisdiction of Incorporation or Organization | I.R.S. Employer Identification No. | |

Address of principal executive offices

Registrant’s telephone number, including area code: +44 (0) 161 -300-0700

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Symbol | Name of each exchange on which registered |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment to the Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See definition of "large accelerated filer", "accelerated filer", "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.:

Large accelerated filer ☐ Accelerated filer ☒

Non accelerated filer ☐ Smaller reporting company ☐

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of ordinary shares held by non-affiliates of the Registrant was approximately $640,603,954 based on the last reported sale price of such securities as of June 28, 2019, the last business day of the Registrant’s most recently completed second quarter.

The number of shares outstanding of Registrant’s only class of ordinary stock on December 31, 2019, was 27,431,283 .

DOCUMENTS INCORPORATED BY REFERENCE

Parts of the Registrant's definitive proxy statement for its annual general meeting to be held on June 3, 2020, to be filed no later than 120 days after the end of the fiscal year covered by this annual report, are incorporated by reference in this Form 10-K in response to Part III, Items 10, 11, 12, 13 and 14.

TABLE OF CONTENTS |

Page | ||||||

PART I | ||||||

Item 1. | Business | 1 | ||||

Item 1A. | Risk Factors | 8 | ||||

Item 1B. | Unresolved Staff Comments | 22 | ||||

Item 2. | Properties | 22 | ||||

Item 3. | Legal Proceedings | 22 | ||||

Item 4. | Mine Safety Disclosures | 22 | ||||

PART II | ||||||

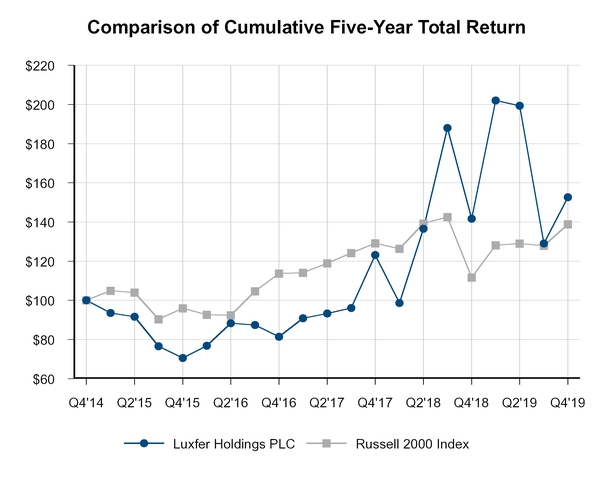

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 23 | ||||

Item 6. | Selected Financial Data | 25 | ||||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 26 | ||||

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 44 | ||||

Item 8. | Financial Statements and Supplementary Data | 46 | ||||

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 95 | ||||

Item 9A. | Controls and Procedures | 95 | ||||

Item 9B. | Other Information | 96 | ||||

PART III | ||||||

Item 10. | Directors, Executive Officers and Corporate Governance | 97 | ||||

Item 11. | Executive Compensation | 97 | ||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 97 | ||||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 97 | ||||

Item 14. | Principal Accountant Fees and Services | 97 | ||||

PART IV | ||||||

Item 15. | Exhibits and Financial Statement Schedules | 98 | ||||

Item 16. | Form 10-K Summary | 99 | ||||

Signatures | 100 | |||||

PART I

Item 1. Business

Background and business overview

Luxfer Holdings PLC ("Luxfer," "the Company," "we") is a global producer of highly-engineered industrial materials focused on sustained value creation using its broad array of technical knowhow and proprietary materials technologies. The company specializes in the design and manufacture of high-performance products for transportation, defense and emergency response, healthcare, and general industrial purposes. Luxfer customers include both end-users of its products and manufacturers that incorporate Luxfer products into finished goods.

We focus primarily on innovations related to magnesium alloys, zirconium chemicals, aluminum alloys and carbon composites. For example, we were the first to develop and patent a rare-earth-containing magnesium alloy (EZ33A) for use in high-temperature aerospace applications, including helicopter gearboxes; we were at the forefront of the commercial development of zirconia-rich mixed oxides for use in automotive catalysis; we were the first to manufacture a high-pressure gas cylinder out of a single piece of aluminum using cold-impact extrusion; and we developed and patented the superforming process and the first superplastic aluminum alloy (AA2004). We have a long history of innovation derived from our strong technical expertise, and we work closely with customers to apply innovative solutions to their most demanding product needs. Our proprietary technologies and technical expertise, coupled with strong customer service and global presence, provide competitive advantages and have established us as leaders in the global markets we serve. We believe that we have leading positions in key product areas, including magnesium aerospace alloys, photo-engraving plates, zirconium chemicals for automotive catalytic converters and high-pressure aluminum and composite cylinders for breathing applications and a wide variety of other uses.

We have a global presence, operating 16 manufacturing plants in the U.S., the U.K., Canada and China, and employ approximately 1,600 people, including temporary staff. We also have joint ventures in Japan and India. In 2019, our net sales were $443.5 million (2018: $487.9 million, 2017: $441.3 million) and our net income was $3.1 million (2018: $25.0 million, 2017: $16.6 million). In 2019, we manufactured and sold approximately 11,000 metric tons of our magnesium products, approximately 2,800 metric tons of our zirconium products (excluding water weight as sold as a solution) and approximately 1.7 million high-pressure gas cylinders.

The original Luxfer Group was formed in 1996 in connection with the management buy-in (the "Management Buy-in") of certain downstream assets of British Alcan. The Management Buy-in was financed by a syndicate of private equity investors. Largely through a leveraged reorganization in 1999, and finally a capital reorganization in 2007, these investors fully exited their original investments in the business.

In October 2012, Luxfer Holdings PLC successfully listed its shares (in the form of American Depositary Shares ("ADSs") evidenced by American Depositary Receipts or "ADRs") on the New York Stock Exchange. On December 11, 2017, we terminated the ADR facility and arranged for the exchange of outstanding ADSs for the underlying ordinary shares. The exchange allows Luxfer shareholders to directly own and publicly trade ordinary shares on the New York Stock Exchange under the symbol "LXFR."

On June 30, 2018, Luxfer Holdings PLC determined that the Company did not meet the criteria to continue as a Foreign Private Issuer, or "FPI." The result of which means, that as of January 1, 2019, the Company is now a Domestic Issuer, conforms with the full listing rules of the New York Stock Exchange and is in full compliance with applicable SEC regulations.

Luxfer operates in two business segments - Elektron and Gas Cylinders.

Elektron Segment

Our Elektron Segment focuses on specialty materials based primarily on magnesium and zirconium. In 2019, sales from our Elektron Segment represented approximately 50% (2018: 51%, 2017: 50%) of our consolidated net sales. Our top ten customers represented 31% of segment sales. No customer represented 10% or more of our Elektron Segment sales.

Key product lines include:

• | Advanced lightweight, corrosion-resistant and heat- and flame-resistant magnesium alloys including our dissolvable SoluMag® alloy. |

• | Magnesium powders used in countermeasure flares that protect aircraft from heat-seeking missiles and also for heating pads for self-heating meals used by the military and emergency-relief agencies. |

• | High-performance zirconium-based materials and oxides used as catalysts and in the manufacture of advanced ceramics, fiber-optic fuel cells, and many other performance products. |

1

• | Magnesium, copper, and zinc photoengraving plates for graphic arts and luxury packaging. |

Gas Cylinders Segment

Our Gas Cylinders Segment manufactures and markets specialized products using aluminum, titanium and carbon composites. In 2019, sales from our Gas Cylinders Segment represented approximately 50% (2018: 49%, 2017: 50%) of our consolidated net sales. Our top ten customers represented 46% of segment sales. One customer represented 11% of our Gas Cylinders Segment sales with no other customer greater than 10%.

Key product lines include:

• | Carbon composite cylinders for self-contained breathing apparatus (SCBA), used by firefighters and other emergency-responders. Our products are also used by scuba divers and personnel in potentially hazardous environments such as mines. |

• | Aluminum and composite cylinders used for containment of oxygen and other medical gases used by patients, healthcare facilities and laboratories. |

• | Carbon composite cylinders for compressed natural gas (CNG) and hydrogen containment in alternative fuel (AF) vehicles. |

• | Lightweight aluminum cylinders for a variety of industrial applications such as fire extinguishers and containment of high-purity specialty gases. |

• | Lightweight aluminum and titanium panels superformed into highly complex shapes used mainly in the Aerospace and Luxury-Auto industries. |

Financial Information about Segments and Geographic Areas

See Note 16 ("Segmental Information") to our consolidated financial statements for further information regarding our operating segments and our geographic areas.

Suppliers and raw materials

Elektron Segment

Key raw materials used by our Elektron Segment are magnesium, zircon sand and rare earths.

The world demand for magnesium is around one million metric tons per year. China provides about 70% of the world supply. Western primary production is, however, significant, from North American suppliers, Dead Sea Magnesium in Israel, RIMA Industrial in Brazil and two smelters in Russia. We purchase approximately half of our magnesium needs from China. We use only U.S.-sourced materials for our products sold to the U.S. military, for which U.S. and Canadian sourcing is mandatory.

We generally purchase raw materials from suppliers on a spot basis under standard terms and conditions. In 2017, we entered into a three-year supply contract with Rio Tinto Alcan for a substantial portion of our aluminum requirements. In addition, we have supply contracts in place with U.S. Magnesium for raw material purchases of magnesium ingot for both military and commercial applications. The military contract covers magnesium purchases through December 31, 2023, whereas the commercial contract covers through December 31, 2021.

We purchase and process zircon sand, which is found in heavy-minerals sand, titanium dioxide and other products. Global production of zircon is estimated at approximately 1.6 million metric tons. We source premium-grade zircon sand from suppliers in South Africa and Australia. We also purchase intermediate zirconium chemicals from suppliers in China; the level of these purchases is based on a number of factors, including required properties and relative market prices.

There are 17 rare earth metals that are reasonably common in nature. Usually found mixed together with other mineral deposits, these rare earths have magnetic and light-emitting properties that make them invaluable to high-technology manufacturers. As they are ingredients in our zirconium chemical and magnesium alloy products, our use of rare earths has expanded over the last few years. Our main requirement is for cerium, which we use in automotive catalysis compounds because of its unique oxygen-storage capabilities.

2

Gas Cylinders Segment

The largest single raw material purchased by the Gas Cylinders Segment is aluminum. In 2019, we purchased approximately 60% of our aluminum from Rio Tinto Alcan and its associated companies, and aluminum represented approximately 50% of the segment's raw material costs in the year.

The price of aluminum has been somewhat volatile in the past and while we pass on most price movements to our customers, sometimes through contractual cost-sharing formulas, doing so can be more difficult or time consuming with our higher-value products. Whilst we have historically hedged a portion of our exposure to fluctuations in aluminum pricing no hedges were taken out in 2019.

Another key material is high-strength carbon fiber used in our composite products. Our main suppliers are Toray and Mitsubishi. In recent years, carbon fiber shortages have occurred from increased demand for commercial aerospace and military applications. Over time, we have built relationships with our suppliers, providing them predictable requirements and fixed-price annual contracts to encourage successful procurement of our required quota of carbon fiber.

Our end-markets

Key end-markets for Luxfer products fall into four categories:

Transportation (32% of 2019 sales): Many Luxfer products serve a growing need to improve and safeguard the environment in the field of transportation, including our zirconium-based products that reduce automotive emissions; our lightweight magnesium alloys used in fuel-efficient aerospace and automotive designs; and our lightweight, high-pressure carbon composite alternative fuel cylinders that contain clean-burning compressed natural gas and hydrogen. We also superform single sheets of aluminum, magnesium or titanium to create complex, three-dimensional components used in automotive, aerospace and rail components.

Area of Focus | Product | End-market drivers | ||||

Alternative fuels | • Alternative fuel cylinders • Bulk gas transportation cylinders | • "Clean air" initiatives • Abundance of natural gas • Favorable tax treatment • Increasing CNG filling infrastructure | ||||

Environmental catalysts (cleaning of exhaust emissions) | • Zirconium compounds with specific properties used in auto-catalysis washcoats | • Emissions legislation and regulation generally • Cost effective for vehicle manufacturers as they reduce the use of precious metals • Increasing demand for gasoline-electric hybrid vehicles | ||||

Specialty / high-end automotive | • Superformed complex body panels, doors and trunk assemblies and other high-strength components • Magnesium extrusions | • Fuel efficiency for a given level of performance • Increased flexibility for vehicle designers in terms of complex shapes and strength • Strong demand for top-end cars from affluent customers, typically in emerging markets | ||||

Sensors, piezoelectrics and electro-ceramics | • Zirconium-based ceramic materials used in sensors of engine management systems | • Engine efficiency • Control of exhaust gases | ||||

Rail transport | • Superformed train front-cab and internal components | • Government investment in public transport • Fuel efficiency • Safety requirements for moving from plastic to metal for internal components | ||||

Civil aerospace | • Superform (wing leading edges, engine nacelle skins, winglets) • Elektron® aerospace alloys in cast, extruded, and sheet form | • Growing aircraft build rate • Increasing cost of fuel • Increased vehicle design / sophistication | ||||

Helicopters | • Magnesium sand-casting alloys, superformed panels | • Lightweighting • Fuel efficiency | ||||

3

Defense and emergency response (27% of 2019 sales) : Luxfer offers several products that address principal factors driving growth in this market, such as heightened societal expectations regarding protection of people, equipment and property during conflicts and emergencies. Our products include magnesium powders for countermeasure flares that defend aircraft against heat-seeking missile attack and for flameless heaters used in meals, life-support cylinders for firefighters and other emergency-service personnel, fire extinguisher cylinders, and chemical agent detection and decontamination products.

Area of Focus | Product | End-market drivers | ||||

Life-support breathing apparatus | • Composite cylinders used in SCBA | • Increased awareness of importance of properly equipping firefighting services post 9/11 • Demand for lightweight products to upgrade from heavy all-metal cylinders • Periodic upgrade of new U.S. National Institute for Occupational Safety and Health (NIOSH) standards and natural replacement cycles • Asian and European fire services looking to adopt more modern SCBA equipment | ||||

Fire protection | • Cylinders (CO2 fire extinguishers) | • New commercial buildings • Cylinder replacement during annual servicing | ||||

Countermeasures | • Ultra-fine magnesium powders for flares used to protect aircraft from attack by heat-seeking missiles | • Use in combat and training • Maintenance of countermeasures reserves (shelf-life restrictions) | ||||

Military vehicles | • Elektron® magnesium alloys in cast rolled, and extruded forms | • Maintaining high level of protection while reducing weight to improve maneuverability and fuel economy | ||||

Military personnel and emergency relief agencies | • Self-heating meals used by military personnel and emergency-relief agencies • Chemical detection and chemical decontamination kits | • Ensuring protection and well-being for military personnel and victims of natural disasters • Use in combat and training and in response to terrorist activities | ||||

Healthcare (5% of 2019 sales): Luxfer has a long history serving the healthcare end-market, and we see this as a major area for the introduction of new products and solutions. These include lightweight aluminum and composite cylinders for containment of medical and laboratory gases; zirconium powders for pharmaceutical products; magnesium materials for lightweight orthopedic devices; specialized magnesium alloys for cardiovascular stents and implants; and zirconium materials for biomedical applications and dental implants.

Area of Focus | Product | End-market drivers | ||||

Medical gases | • Portable aluminum and composite cylinders • Portable oxygen concentrators | • Growing use of medical gases • Shift to paramedics, who need portable, lightweight products • Growing trend to provide oxygen therapy in the home and to keep patients mobile • Increasingly aging population • Increase in respiratory diseases | ||||

Medical equipment casings | • Superformed panels (e.g., for MRI scanners) | • Growing use of equipment using powerful magnets and consequent need for non-ferrous, hygienic casings | ||||

Pharmaceutical industry | • Magnesium powders as a catalyst for chemical synthesis (Grignard process) | • Growth in pharmaceutical industry | ||||

Orthopedics | • Magnesium sheets | • Improved mobility through use of easy-to-wear, lightweight braces and trusses | ||||

Sorbents | • MELsorb® material being developed as active ingredient in dialysis equipment and enterosorbents | • Growth in kidney problems • New technologies to remove noxious elements from the body | ||||

4

General industrial (36% of 2019 sales): Our core technologies have enabled us to serve various other markets and applications. Our products include zirconium-based compounds to purify drinking water and clean industrial exhausts; magnesium alloys shaped for use in various general engineering applications; and high-pressure gas cylinders used for high-purity specialty gases, beverage dispensing, scuba diving and performance racing. Metal foil-stamping and embossing dies are used primarily for luxury packaging, labels and greeting cards. Our high-quality magnesium, copper, brass and zinc plates are ideal for these and other graphic applications.

Area of Focus | Product | End-market drivers | ||||

Specialty gases | • Inert-interior aluminum cylinders for high-purity gases | • Semiconductor and electronics industries • Pharmaceutical industry growth • Specialized laboratory requirements • Oil exploration | ||||

Leisure activities | • Cylinders for SCUBA diving, car and boat racing | • Leisure time • Growth of middle class in emerging markets | ||||

General engineering | • Magnesium billets, sheets, coil, tooling plates • Zirconium ceramic compounds for hard working components | • Economic growth • Need for components to operate in more extreme environments for longer periods, such as underground or in the ocean | ||||

Hydraulic fracturing or "fracking" | • Dissolvable SoluMag® magnesium alloy | • Onshore shale gas exploration linked to increasing energy demand | ||||

Paper | • Bacote™ and Zirmel™, both formaldehyde-free insolubilizers that aid high-quality printing | • Elimination of toxic chemicals | ||||

Graphic arts | • Photo-engraving plates | • Luxury packaging as part of marketing high-end products | ||||

Our competitive advantages

Focus on innovation and product development for growing specialized end-markets. We continue to produce a steady stream of new products, including those developed in close collaboration with our customers.

Strong technical expertise and know-how. Using our expertise in metallurgy and material science, we specialize in advanced materials, developing products and materials with superior performance to satisfy the most demanding requirements in the most extreme environments. Further, we benefit from the fact that a growing number of our products are patented, including many of our alloys and compounds.

Diversified customer base with long-standing relationships. We put the customer at the heart of our strategy, and we have long-standing relationships with many of our customers, including global leaders in our key markets.

Our Business Excellence Standard Toolkit. The "Luxfer B.E.S.T. Model," consists of the following key themes:

• | A common set of values that drives accountability, innovation, customer first, personal development, teamwork and integrity. |

• | Disciplined capital allocation with the aim of maximizing organic growth and the product portfolio value through value-enhancing acquisitions and divestitures. |

• | Balanced score-card used in an effort to continuously improve employee performance in an effort to help translate our vision into actionable individual goals and ensure that employee compensation is commensurate with individual performance. |

• | A published Customer Charter designed to enable us to retain and grow our customer base and capture additional market share. |

• | A lean enterprise philosophy that helps drive operational process excellence in all functions including, sales, marketing, innovation, human resources, supply, manufacturing, information technology and finance. |

5

Seasonality

We have shutdown periods at most of our manufacturing sites during which we carry out maintenance work. Shutdowns typically last two weeks in the summer and one to two weeks around the year-end holidays, resulting in reduced levels of activity in the second half of the year compared to the first half. Third-quarter and fourth-quarter sales and operating profit can be affected by our own shutdowns and by shutdowns by various industrial customers. In particular, we have found that our fourth-quarter results are generally lower, since many customers reduce production activity from late November through December. We also operate in various geographic areas that are susceptible to bad weather during winter months, such as Calgary, Canada, and various U.S. eastern states. Bad weather can unexpectedly disrupt production and shipments from our manufacturing facilities, which can lead to reduced revenue and operating profits. We also manufacture products that are used in graphic arts and premium packaging, demand for which increases in the run up to the year-end holidays.

Research and Development

Luxfer recognizes the importance of research in materials science and the need to develop innovative new products to meet future needs of customers and to continue providing growth opportunities for the business. Each year, we invest in the development of new products and processes directed towards transportation, defense and emergency response, healthcare and general industrial end-markets. Direct expenditures on research and development amounted to $5.7 million in 2019 (2018: $6.4 million; 2017: $7.8 million). Our product development projects also include utilizing skills of our wider commercial technical sales staff and general management, many of whom are highly qualified scientists and engineers. A large proportion of senior sales and management time is spent overseeing development of products and working with customers on integrating our products and solutions into their product designs.

To provide customers with improving products and services, we invest in new technology and research and employ some of the world's leading specialists in materials science and metallurgy. Our engineers and metallurgists collaborate closely with our customers to design, develop and manufacture our products. We also co-sponsor ongoing research programs at major universities in the U.S., Canada and Europe. Thanks to the ingenuity of our own research and development teams, Luxfer has developed a steady stream of new products, most recently including:

• | soluble magnesium alloys, branded SoluMag®, for down-well oil and gas applications; |

• | ultra-lightweight large composite cylinders, branded G-StorTM, for containment of CNG, hydrogen, helium and other gases; |

• | enabling technologies for AF systems, including high-pressure valves, branded G-FloTM, and pressure- release devices; |

• | zirconium catalysts for large-scale industrial chemical applications; |

• | L7X® higher-strength aluminum alloy and carbon composite gas cylinders; |

• | Luxfer ECLIPSE, a new carbon composite cylinders for firefighter self-contained breathing apparatus (SCBA); |

• | bioresorbable magnesium alloys, branded SynerMag®; and |

• | zirconium sorbents, branded MELsorb®, being developed for use as an active ingredient in kidney dialysis equipment. |

We believe that our commitment to research and new product development, through dedicated resources and significant use of management's time, is the core of Luxfer's growth potential worldwide. This commitment reflects our strategy of focusing on high-performance, value-added product lines and markets and leveraging our collaboration with universities. We invest in developing products for end-markets that we believe have long-term growth potential.

6

Intellectual Property

We rely on a combination of patents, trade secrets, copyrights, trademarks, proprietary manufacturing processes and design rights, together with non-disclosure agreements and technical measures, to establish and protect proprietary rights in our products. Our Elektron Segment holds key patents related to protection applications, including numerous aerospace alloys and magnesium-gadolinium alloys, as well as patents related to environmental applications, including water-treatment products and our specialized G4 process used to manufacture zirconium-cerium oxides for emissions-control catalysts. The segment also has patented technology for magnesium-based flameless heater pads used to heat meals and beverages. Key patents held by our Gas Cylinders Segment relate to aluminum alloys for pressurized hollow bodies and superplastic-forming techniques.

In certain areas, we rely more heavily upon trade secrets and unpatented proprietary know-how than patent protection in order to establish and maintain our competitive advantage. We generally enter into non-disclosure and invention assignment agreements with our employees and subcontractors.

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q , Current Reports on Form 8-K and any exhibits or amendments to these are made available, free of charge on our website at http://www.luxfer.com as soon as reasonably practicable after we electronically file such reports with, or furnish them to, the Securities and Exchange Commission ("SEC"). Information on our website is not incorporated by reference herein and is not a part of this report.

Financial and other material information regarding the company is routinely posted and accessible on our website at http://www.luxfer.com/investors.

7

Item 1A. Risk Factors

The risks described below are not the only risks facing us. Any of the following risks could materially and adversely affect our business, financial condition or results of operations. Additional risks and uncertainties not currently known to us or those we currently view to be immaterial may also materially and adversely affect our business, financial condition or results of operations. See also "Information Regarding Forward-Looking Statements" for certain warnings regarding forward-looking information contained in this document.

Risks Relating to Our Operations

We depend on certain end-markets, including automotive, alternative fuels, self-contained breathing apparatus, aerospace and defense, healthcare, oil and gas and printing and paper. An economic downturn, or regulatory changes, in any of those end-markets, could reduce sales and profit margins on those end-markets.

We have significant exposures to certain end-markets, including some end-markets that are cyclical in nature or subject to high levels of regulatory control, including automotive, self-contained breathing apparatus ("SCBA"), aerospace and defense and printing and paper. Dependence of either of our segments on certain end-markets is even more pronounced.

To the extent that any of these cyclical end-markets are in decline, at a low point in their economic cycle, or subject to regulatory change, sales and margins on those sales may be adversely affected. It is possible that all or most of these end-markets could be in decline at the same time, such as during a recession. Any significant reduction in sales could have a material adverse impact on our results of operations, financial position and cash flows.

Our global operations expose us to economic conditions, potential tax costs, political risks and specific regulations or restrictions in the countries in which we operate, which could have a material adverse impact on our results of operations, financial position and cash flows.

We derive our sales and earnings from operations in many countries and are subject to risks associated with doing business internationally. We have wholly-owned operations in the U.S., the U.K., Canada, China and Australia; and joint venture facilities in India and Japan. Doing business in different countries has risks, including the potential for adverse changes in the local social, political, financial or regulatory climate, difficulty in staffing and managing geographically diverse operations, and the costs of complying with a variety of laws and regulations. For example the change in the political climate in the U.S. and imposition of tariffs could make it more challenging or expensive to import products manufactured in Europe.

Due to the fact we have operations in many countries, we are also liable to pay taxes in many fiscal jurisdictions. Our tax burden depends on the interpretation of local tax regulations, bilateral or multilateral international tax treaties and the administrative doctrines in each jurisdiction. Changes in these tax regulations may increase our tax burden, or otherwise affect our accounting for taxes. For example, as a result of the reduction in the statutory corporate income tax rate in the U.S. pursuant to the Tax Cut and Jobs Act (TCJA) enacted on December 22, 2017, we recorded a reduction in the value of our deferred tax assets in the U.S. of $4.0 million in 2017. Moreover, the principal markets for our products are located in North America, Europe and Asia, and any financial difficulties experienced in these markets may have a material adverse impact on our businesses. For example, the maturity of some of our markets, particularly the U.S. medical oxygen cylinder market and the European fire extinguisher market, could require us to increase sales in developing regions, which may involve greater economic and political risks. We cannot provide any assurances that we will be able to expand sales in these regions. Any of these factors could have a material adverse impact on our results of operations, financial position and cash flows.

On June 23, 2016, the U.K. held a referendum in which voters approved an exit from the European Union (the "E.U."), commonly referred to as 'Brexit'. On March 29, 2017, the U.K. Government invoked Article 50 of the Treaty on the European Union, which was expected to result in the U.K. leaving the E.U. on March 29, 2019 but was subsequently twice deferred with the Withdrawal Agreement taking effect on January 31, 2020. Following the exit there is an eleven month transition period during which existing E.U. rules and regulations will continue to apply to the U.K. pending agreement on the future trading arrangements, currently required to be achieved by December 31, 2020. It is possible that following agreement, the new relationship will result in greater restrictions on imports and exports between the U.K. and E.U. countries, the U.S. and other markets with increased regulatory complexity. There is also the potential for disruption to the movement of raw materials and finished goods in the event that no agreement is reached by the end of the transition period. These changes may adversely affect our operations and financial results. See also "—Changes in foreign exchange rates could reduce profit margins on our sales and reduce the reported sales of our non-U.S. operations and have a material adverse effect on our results of operations."

8

We may not be able to consummate, finance or successfully integrate future acquisitions into our business, which could hinder our strategy or result in unanticipated expenses, losses or charges.

As part of our strategy, we have supplemented and may continue to supplement organic growth by acquiring companies or operations engaged in similar or complementary businesses. If the consummation of future acquisitions, together with integration of acquired companies and businesses excessively diverts management's attention from the operations of our existing businesses, operating results could suffer. Any acquisition made could be subject to a number of risks, including:

• | failing to discover liabilities of the acquired company or business for which we may be responsible as a successor owner or operator, including litigation or environmental costs and liabilities; |

• | difficulties associated with the assimilation of operations and personnel of the acquired company or business, creating uncertainty for employees, customers and suppliers; |

• | increased debt service requirements as a result of increased indebtedness to complete acquisitions; |

• | the loss of key personnel in the acquired company or business; |

• | a negative effect on our financial results resulting from an impairment of acquired intangible assets, the creation of provisions, or write downs; and / or |

• | potential adverse effects on our stock price and dividend amount due to the issuance of additional stock. |

We cannot ensure that every acquisition will ultimately provide the benefits originally anticipated, which could ultimately have a material adverse impact on our results of operations, financial position and cash flows.

Our operations rely on a number of large customers in certain areas of our business, and the loss of any of our major customers could negatively impact our results of operations.

If we fail to maintain our relationships with our major customers, or fail to replace lost customers, or if there is reduced demand from our customers or for products produced by our customers, such failures or reduced demand could materially reduce our sales. In addition, we could experience a reduction in sales if any of our customers fail to perform or default on any payment pursuant to our contracts with them. Long-term relationships with customers are especially important for suppliers of intermediate materials and components such as ourselves. We often work closely with customers to develop products that meet particular specifications as part of the design of a product intended for an end-user market. The bespoke nature of many of our products could make it difficult to replace lost customers. Our top 10 customers accounted for approximately 25% of our net sales in 2019. Any significant reduction in sales or customer payment default could have an adverse material impact on our results of operations, financial position and cash flows.

Competitive pressures could materially and adversely affect our sales and profit margins.

The markets for many of our products are now increasingly global and highly competitive, especially in terms of quality, price and service. Due to the highly competitive nature of some markets in which we operate, we may have difficulty raising prices to offset increases in the costs of raw materials. For example, the U.S. medical oxygen cylinder market has a number of dedicated producers with excess capacity, making it very difficult for us to raise customer prices to offset aluminum cost increases. In addition, rising aluminum costs could lead to the development of alternative products that use lower cost materials, which could become favored by end-market users and thereby lead to a decline in the demand for our products.

We also experience competition from developing countries where manufacturers may benefit from lower labor costs. We are also affected by Western-based competitors that have chosen to relocate production to Asia to take advantage of lower labor costs. Competitors with operations in these regions may be able to produce goods at a relatively lower cost, which may enable them to offer highly competitive selling prices.

Competition with respect to less-complex zirconium chemicals has been particularly intense, with Chinese suppliers providing low-cost feedstock to specialist competitors, making it especially difficult to compete in commodity products such as paper-making additives. Chinese magnesium also continues to be imported into Europe in large volumes, which may impact our competitive position in Europe regarding certain magnesium alloys. More generally, we may face potential competition from producers that manufacture products similar to our aluminum-based, magnesium-based and zirconium-based products using other materials, such as steel, plastics, composite materials or other metals, minerals and chemicals. Products manufactured by competitors using different materials might compete with our products in terms of price, weight, engineering characteristics, recyclability or other grounds.

We may also enter new markets in which there are established competitors. We expect to face new and significant challenges in our effort to enter into these highly competitive markets in which we did not have a presence historically. For example, in recent years, we have entered markets focused on the containment of compressed natural gas (CNG) and incurred startup costs along with strong competitive pressures from existing

9

providers of similar cylinder technologies. Even if we are able to enter into these new markets initially, we may not be able to sustain the effort on a long-term basis or establish sufficient market share to achieve meaningful returns from our investment.

Other parts of our operations manufacture and sell products that satisfy customer specifications. Competitors may develop lower cost or better performing products, and customers may not be willing to pay a premium for advantages offered by our products.

In addition, governments may impose import and export restrictions, grant subsidies to local companies and implement tariffs and other trade protection regulations and measures that may give competitive advantages to certain of our competitors and adversely affect our business.

Any of these factors could have a material adverse impact on our results of operations, financial position and cash flows.

We depend upon our larger suppliers for a significant portion of our raw materials, and a loss of one of these suppliers, or a significant supply interruption could negatively impact our financial performance.

We rely, to varying degrees, on major suppliers for some of the principal raw materials of our engineered products, including aluminum, zirconium and carbon fiber. For example, in 2019, we obtained approximately 60% of our aluminum, the largest single raw material purchased by the Gas Cylinders Segment, from Rio Tinto Alcan and its associated companies. Moreover, demand for carbon fiber is increasing, which has led to occasional periods of short supply in recent years with a number of expanding applications competing for the same supply of this specialized raw material. Our largest suppliers of carbon fiber are Toray and Grafil, a subsidiary of Mitsubishi Chemical. For additional details of some of our major suppliers (see ITEM 1 - Suppliers and raw materials).

We generally purchase raw materials from suppliers on a spot basis under standard terms and conditions. In 2017, we entered into a three-year supply contract with Rio Tinto Alcan for a substantial portion of our aluminum requirements. In addition, we have supply contracts in place with U.S. Magnesium for raw material purchases of magnesium ingot for both military and commercial applications. The military contract covers magnesium purchases through December 31, 2023, whereas the commercial contract covers through December 31, 2021.

An interruption in the supply of essential raw materials used in our production processes or an increase in the costs of raw materials due to market shortages, supplier financial difficulties, government quotas or natural disturbances such as the recent outbreak of the covid-19 coronavirus, could significantly affect our ability to provide competitively priced products to customers in a timely manner. In the event of a significant interruption in the supply of any materials used in our production processes, or a significant increase in their prices (as we have experienced, for example, at different times with aluminum, magnesium and rare earths), we may have to purchase these materials from alternative sources, build additional inventory of raw materials, increase our prices, reduce our margins or possibly fail to fill customer orders by deadlines required in contracts, which could result in, among other things, contractual penalties. We can provide no assurance that we would be able to obtain replacement materials quickly on similar terms or at all. Failure to maintain relationships with key suppliers or to develop relationships with alternative suppliers could have a material adverse effect on our results of operations, financial position and cash flows.

We are exposed to fluctuations in the costs of the raw materials that are used to manufacture our products, and such fluctuations could lead us to incur unexpected costs and could affect our margins and / or working capital requirements.

The primary raw material we use to manufacture gas cylinders and superformed panels is aluminum supplied in billet and sheet form. The cost of aluminum is subject to both significant short-term price fluctuations and to longer-term cyclicality as a result of international supply and demand relationships. In 2019, the London Metal Exchange ("LME") three-month cost of aluminum reached a high of just below $2,000 per metric ton and a low of just above $1,700 per metric ton. The delivery premiums added by suppliers to the LME price also fluctuate, for example: the Midwest Aluminum Premium for physical supply of aluminum billet in the U.S. has historically averaged around $200 per metric ton, but in 2015 rose to a high of $535 per metric ton then fell to a low of $155 per metric ton. We have experienced significant volatility in other raw material costs in the last few years, such as primary magnesium, carbon fiber, zircon sand and rare earths. See ITEM 1.

Fluctuations in the costs of these raw materials could affect margins and working capital requirements in the businesses in which we use them, see ITEM 7. We cannot always pass on cost increases or increase our prices to offset these cost increases immediately or at all, whether because of fixed-price agreements with customers, competitive pressures that restrict our ability to pass on cost increases or increase prices, or other factors. It can be particularly difficult to pass on cost increases or increase prices in product areas such as gas cylinders, where competitors offer similar products made from alternative materials, such as steel, if those materials are

10

not subject to the same cost increases. Higher prices necessitated by large increases in raw material costs could make our current or future products unattractive compared to competing products made from alternative materials that have not been so affected by raw material cost increases, or compared to products produced by competitors who have not incurred such large increases in their raw material costs.

In addition, pricing of raw materials, such as aluminum, may be impacted by the level of tariffs imposed on imports. President Trump announced in March 2018 a 10% tariff on aluminum imported into the U.S. The Company uses a substantial amount of aluminum in its products, with imports into the U.S. primarily originating from Canada. The tariffs were subsequently suspended in May 2019, paving the way for ratification of the United States-Mexico-Canada agreement ("USMCA"), which was approved by the United States on January 29, 2020. While the imposition of the temporary tariff did not have a major adverse impact on our business, if the tariff were to be reimposed at a higher level, then the price of affected imported materials could increase substantially and the price of U.S.-made aluminum could also increase substantially.

If the cost of aluminum were to rise, we may not be able pass those cost increases on to our customers or manage the exposure effectively through hedging instruments. From time to time we use derivative financial instruments to hedge our exposures to fluctuations in aluminum costs. Although it is our treasury policy to enter into these transactions only for hedging and not for speculative purposes, we are exposed to market risk and credit risk with respect to the use of these derivative financial instruments, see ITEM 7A. In addition, if we have hedged our metal position, a fall in the cost of aluminum might give rise to hedging margin calls to the detriment of our borrowing position.

In the past several years we have made additional purchases of large stocks of magnesium alloys in an effort to delay the effect of potentially increased costs in the future. However, even though such purchases are not made for speculative purposes, there can be no assurance that costs will move as expected.

Moreover, these strategic purchases increase our working capital needs, thus reducing our liquidity and cash flow.

Accordingly, a substantial increase in raw material costs could have a material adverse effect on our results of operations, financial position and cash flows.

We are exposed to fluctuations in costs of utilities that are used in the manufacture of our products, and such fluctuations could lead us to incur unexpected costs and could affect our margins and results of operations.

Our utility costs, which constitute another major input cost of our total expenses and include costs related to electricity, natural gas and water, may be subject to significant variations. Increased taxation and other factors have contributed in the past to a significant increase in utility costs for us, particularly with respect to the price that we pay for our U.K. energy supplies.

Fluctuations in the costs of these utilities could affect margins in our businesses in which we use them. We cannot always pass on cost increases or increase our prices to offset cost increases immediately or at all, whether because of fixed-price agreements with customers, competitive pressures that restrict our ability to pass on cost increases or increase prices, or other factors. It can be particularly difficult to pass on cost increases or increase prices in product areas such as gas cylinders, where competitors offer similar products made from alternative materials, such as steel, if those materials are not subject to the same cost increases. As a result, a substantial increase in utility costs could have a material adverse effect on our results of operations, financial position and cash flows.

Changes in foreign exchange rates could reduce profit margins on our sales and reduce the reported sales of our non-U.S. operations and have a material adverse effect on our results of operations.

We conduct a large portion of our commercial transactions, purchases of raw materials and sales of goods in various countries and regions, including the U.S., the U.K., continental Europe, Australia and Asia. Our manufacturing operations based in the U.S., continental Europe and Asia usually purchase raw materials and sell goods denominated in their local currency, but our manufacturing operations in the U.K. often purchase raw materials and sell products in different currencies. Changes in the relative values of currencies can decrease the profits of our subsidiaries when they incur costs in currencies that are different from the currencies in which they generate all or part of their revenue. These transaction risks principally arise as a result of purchases of raw materials in U.S. dollars, coupled with sales of products to customers in euros. This impact is most pronounced in our exports to continental Europe from the U.K. In 2019, our U.K. operations sold approximately €70 million of goods into the Eurozone. Our policy is to hedge a portion of our net exposure to fluctuations in exchange rates with forward foreign currency exchange contracts. Therefore, we are exposed to market risk and credit risk through the use of derivative financial instruments. Moreover, any failure of hedging policies could negatively impact our profits, and thus damage our ability to fund our operations and to service our indebtedness. Further

11

exchange rate volatility has been experienced during 2019 with GBP sterling reaching a five-year low against both the U.S. dollar and euro in August and until the terms of the U.K.'s future relationship with the E.U. are known, continued volatility is to be expected.

In addition to subsidiaries and joint ventures in the U.S., we have operating subsidiaries located in the U.K., Canada, China and Australia, as well as joint ventures in Japan and India, whose revenue, costs, assets and liabilities are denominated in local currencies. As our consolidated financial statements are reported in U.S. dollars, we are exposed to fluctuations in those currencies when those amounts are translated to U.S. dollars for purposes of reporting our consolidated financial statements, which may cause declines in results of operations. The largest risk is from our operations in the U.K., which in 2019 generated an operating profit of $1.9 million and net sales of $156.0 million. Fluctuations in exchange rates, particularly between the U.S. dollar and GBP sterling (which has been subject to significant fluctuations, as described above), can have a material effect on our consolidated income statement and consolidated balance sheet. In 2019, movements in the average U.S. dollar exchange rate had a negative impact on net sales of $9.5 million; in 2018 movements in the average U.S. dollar exchange rate had a positive impact on net sales of $2.5 million. Changes in translation exchange rates increased net assets by $3.1 million in 2019, compared to a decrease of $6.4 million in 2018.

These foreign exchange risks could have a material adverse effect on our results of operations, financial position and cash flows. For additional information on these risks, and the historical impact on our results, see ITEM 7A.

Our defined benefit pension plans have funding deficits and are exposed to market forces that could require us to make increased ongoing cash contributions in response to changes in market conditions, actuarial assumptions and investment decisions These market forces could expose us to significant short-term liabilities if a wind-up trigger occurred in relation to such plans, each of which could have a material adverse impact on our results of operations and financial position.

We have defined benefit pension arrangements in the U.K. and in the U.S., see ITEM 8, note 13. Our largest defined benefit plan, the Luxfer Group Pension Plan, which closed to new members in 1998, remained open for accrual of future benefits based on career-average salary until April 5, 2016. However, following a consultation, it was agreed with the trustees and plan members to close the Luxfer Group Pension Plan in the U.K. to future accrual of benefits, effective from April 5, 2016. Moreover, for the purpose of increasing pensions in payment, it was agreed to use the CPI as the reference index, in place of the RPI where applicable. The Luxfer Group Pension Plan is funded according to the regulations in effect in the U.K. and, as of December 31, 2019, and December 31, 2018, had an accounting deficit of $30.5 million and $31.8 million, respectively. Luxfer Group Limited is the principal employer under the Luxfer Group Pension Plan, and other U.K. subsidiaries also participate under the plan. Our other defined benefit plans are less significant than the Luxfer Group Pension Plan and, as of December 31, 2019, and December 31, 2018, had aggregate accounting deficits of $4.7 million and $8.2 million, respectively. The largest of these additional plans is the BA Holdings, Inc. Pension Plan in the U.S., which was closed to further benefit accruals in December 2005, and merged with the much smaller Luxfer Hourly Pension Plan, effective January 1, 2016. According to the actuarial valuation of the Luxfer Group Pension Plan as of April 5, 2018, being the date of the last triennial valuation, the Luxfer Group Pension Plan had a deficit of £26.5 million on a plan-specific basis. Should a wind-up trigger occur in relation to the Luxfer Group Pension Plan, the buy-out deficit of that plan will become due and payable by the employers. The aggregate deficit of the Luxfer Group Pension Plan on a buy-out basis was estimated at £145 million as of April 5, 2018. The trustees have the power to wind-up the Luxfer Group Pension Plan if they consider that in the best interests of members there is no reasonable purpose in continuing the Luxfer Group Pension Plan.

As a result of the actuarial valuation as of April 5, 2018, we are required to continue to make ongoing cash contributions, over and above normal contributions required to meet the cost of future accrual, to the Luxfer Group Pension Plan. These additional payments are intended to reduce the funding deficit. We have agreed with the trustees to a schedule of annual payments of £4.1 million ($5.3 million at current exchange rates) to reduce the deficit. These contributions are to apply until the deficit is eliminated (which is expected to occur by the end of 2022), but in practice the schedule will be reviewed and may be revised following the next triennial actuarial valuation in April 2021. Regulatory burdens have also proved to be a significant risk, such as the U.K.'s Pension Protection Fund Levy, which was £0.3 million in 2019.

We are exposed to various risks related to our defined benefit plans, including the risk of loss of market value of the plan assets, the risk of actual investment returns being less than assumed rates of return, the trustees of the Luxfer Group Pension Plan switching investment strategy (which does require consultation with the employer) and the risk of actual experience deviating from actuarial assumptions for such things as mortality of plan participants. In addition, fluctuations in interest rates cause changes in the annual cost and benefit obligations. Any of these risks could have a material adverse impact on our results of operations, financial position and cash flows.

12

The Pensions Regulator in the U.K. has the power in certain circumstances to issue contribution notices or financial support directions that, if issued, could result in significant liabilities arising for us.

The Pensions Regulator may issue a contribution notice to the employers that participate in the Luxfer Group Pension Plan, or any person who is connected with, or is an associate of, these employers where the Pensions Regulator is of the opinion that the relevant person has been a party to an act, or a deliberate failure to act, which had as its main purpose (or one of its main purposes) the avoidance of pension liabilities or where such act has a materially detrimental effect on the likelihood of payment of accrued benefits under the Luxfer Group Pension Plan being received. A person holding alone or together with his or her associates, directly or indirectly, one-third or more of our voting power, could be the subject of a contribution notice. The terms "associate" and "connected person," which are taken from the Insolvency Act 1986, are widely defined and could cover our significant shareholders and others deemed to be shadow directors. If the Pensions Regulator considers that a plan employer is "insufficiently resourced" or a "service company" (which terms have statutory definitions), it may impose a financial support direction requiring such plan's employer or any member of the Group, or any person associated or connected with an employer, to put in place financial support in relation to the Luxfer Group Pension Plan. Liabilities imposed under a contribution notice or financial support direction may be up to the difference between the value of the assets of the Luxfer Group Pension Plan and the cost of buying out the benefits of members and other beneficiaries of the Luxfer Group Pension Plan. In practice, the risk of a contribution notice being imposed may restrict our ability to restructure or undertake certain corporate activities. Additional security may also need to be provided to the trustees of the Luxfer Group Pension Plan before certain corporate activities can be undertaken (such as the payment of an unusual dividend), and any additional funding of the Luxfer Group Pension Plan may have a material adverse effect on our financial position and cash flows.

Our ability to remain profitable depends on our ability to protect and enforce our intellectual property, and any failure to protect and enforce such intellectual property could have a material adverse impact on our results of operations and financial position.

We cannot ensure that we will always have the ability to protect proprietary information and our intellectual property rights. We protect our intellectual property rights (within the U.S., Europe and other countries) through various means, including patents and trade secrets. Due to the difference in foreign trademark, patent and other laws concerning proprietary rights, our intellectual property rights may not receive the same degree of protection in other countries as they would in the U.S. or the U.K. The patents we own could be challenged, invalidated or circumvented by others and may not be of sufficient scope or strength to provide us with any meaningful protection or commercial advantage. Further, competitors may infringe our patents and the costs of protecting our patents could be significant. We cannot assure you that we will have adequate resources to enforce our patents. Our patents will only be protected for the duration of the patent. Some of our older key patents have expired, and others will expire over the next few years. As a result, our competitors may introduce products using the technology previously protected, and these products may have lower prices than our products, which may negatively affect our market share. To compete, we may need to reduce our prices for those products. Additionally, the expiry of certain of those patents has reduced, or will reduce, barriers to entry to possible competitors for certain products and end-markets. With respect to our unpatented proprietary technology, it is possible that others will independently develop the same or similar technology or obtain access to our unpatented technology. To protect our trade secrets and other proprietary information, we require employees, consultants, advisors and collaborators to enter into confidentiality agreements. Nevertheless, we cannot assure you that these agreements will provide meaningful protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use, misappropriation or disclosure of such trade secrets, know-how or other proprietary information. We rely on our trademarks, trade names and brand names to distinguish our products from the products of our competitors, and we have registered or applied to register many of these trademarks. Third parties may also oppose our trademark applications, or otherwise challenge our use of the trademarks. In the event that our trademarks are successfully challenged, we could be forced to rebrand our products, which could result in loss of brand recognition and could require us to devote resources to advertising and marketing new brands. Further, we cannot assure you that competitors will not infringe our trademarks or that we will have adequate resources to enforce our trademarks.

Any failure to maintain, protect and enforce our intellectual property or the expiry of patent protection could have a material adverse impact on our results of operations, financial position and cash flows.

13

Expiration or termination of our right to use certain intellectual property granted by third parties, the right of those third parties to grant the right to use the same intellectual property to our competitors, and the right of certain third parties to use certain intellectual property used as part of our business, could have a material adverse impact on our results of operations, financial position and cash flows.

We have negotiated, and may from time to time in the future negotiate, licenses with third parties with respect to third party proprietary technologies used in certain of our manufacturing processes and products. If any of these licenses expire or terminate, we will no longer retain the rights to use the relevant third party proprietary technologies in our manufacturing processes and products, which could have a material adverse effect on our results of operations, financial position and cash flows. Further, the rights granted to us might be non-exclusive, which could result in our competitors gaining access to the same intellectual property.

Some of our patents may cover inventions that were conceived or first reduced to practice under, or in connection with, government contracts or other government funding agreements or grants. With respect to inventions conceived or first reduced to practice under such government funding agreements, a government may retain a non-exclusive, irrevocable, royalty-free license to practice, or have practiced for or on behalf of the relevant country, the invention throughout the world. In addition, if we fail to comply with our reporting obligations, or to adequately exploit the developed intellectual property under these government funding agreements, the relevant country may obtain additional rights to the developed intellectual property, including the right to take title to any patents related to government funded inventions or to license the same to our competitors. Furthermore, our ability to exclusively license or assign the intellectual property developed under these government funding agreements to third parties may be limited or subject to the relevant government's approval or oversight. These limitations could have a significant impact on the commercial value of the developed intellectual property.

We often enter into research and development agreements with academic institutions whereby they generally retain certain rights to the developed intellectual property. The academic institutions generally retain rights over the technology for use in non-commercial academic and research fields, including in some cases the right to license the technology to third parties for use in those fields. It is difficult to monitor and enforce such non-commercial academic and research uses, and we cannot predict whether the third party licensees would comply with the use restrictions of these licenses. We could incur substantial expenses to enforce our rights against such licensees. In addition, even though the rights that academic institutions obtain are generally limited to the non-commercial academic and research fields, they may obtain rights to commercially exploit developed intellectual property in certain instances. Under research and development agreements with academic institutions, our rights to intellectual property developed thereunder are not always certain, but instead may be in the form of an option to obtain license rights to such intellectual property. If we fail to exercise our option rights in a timely way and / or we are unable to negotiate a license agreement, the academic institution may offer a license to the developed intellectual property to third parties for commercial purposes. Any such commercial exploitation could adversely affect our competitive position and have a material adverse effect on our business.

If third parties claim that intellectual property used by us infringes upon their intellectual property, our operating profits could be adversely affected.

We may, from time to time, be notified of claims that we are infringing upon patents, copyrights, or other intellectual property rights owned by third parties, and we cannot provide assurances that other companies will not in the future pursue such infringement claims against us or any third party proprietary technologies we have licensed. If we were found to infringe upon a patent or other intellectual property right, or if we failed to obtain or renew a license under a patent or other intellectual property right from a third party, or if a third party from whom we are licensing technologies was found to infringe upon a patent or other intellectual property rights of another third party, we may be required to pay damages, suspend the manufacture of certain products or re-engineer or rebrand our products, if feasible, or we may be unable to enter certain new product markets. Any such claims could also be expensive and time consuming to defend and could divert management's attention and resources. In addition, if we have omitted to enter into a valid non-disclosure or assignment agreement for any reason, we may not own the invention or our intellectual property and may not be adequately protected. Our competitive position could suffer as a result of any of these events and have a material adverse impact on our results of operations, financial position and cash flows.

Any failure of our research and development activity to improve our existing products and develop new products could cause us to lose market share.

Our products are highly technical in nature, and in order to maintain and improve our market position, we depend on successful research and development activity to continue to improve our existing products and develop new products. We cannot be certain that we will have sufficient research and development capability to respond to changes in the industries in which we operate. These changes could include changes in the technological environment in which we currently operate, increased demand for new products or the development of alternatives to our products. For example, the development of lighter weight steel alloys has

14

made the use of steel in gas cylinders a more competitive alternative to aluminum than it had been previously. In addition, our superformed aluminum components compete with new high-performance composite materials developed for use in the aerospace industry. In our efforts to develop and market new products and enhancements to our existing products, we may fail to identify new product opportunities or timely bring new products to market. We may also experience delays in completing development of, enhancements to or new versions of our products and product innovations may not achieve the market penetration or price stability necessary for profitability. In addition to benefiting from our research collaboration with universities, we spent $5.7 million, $6.4 million and $7.8 million in 2019, 2018 and 2017 respectively, on our own research and development activities. We expect to fund our future research and development expenditure requirements through operating cash flows and restricted levels of indebtedness, but if operating profit decreases, we may not be able to invest in research and development or continue to develop new products or enhancements.

Without the timely introduction of new products or enhancements to existing products, our products could become obsolete over time, in which case our results of operations, financial position and cash flows could be adversely affected.

Some of our key operational equipment is relatively old and may require significant capital expenditures for repair or replacement.

We incur considerable expense on maintenance, including preventative maintenance and repairs. Higher levels of maintenance and repair costs could result from the need to maintain our older plants, property and equipment, and machinery breakdowns could result in interruptions to the business, causing lost production time and reduced output. Machinery breakdowns or equipment failures may hamper or cause delays in the production and delivery of products to our customers and increase our operating costs, thus reducing cash flows from operations. In particular, the breakdown of some of our older equipment, such as the large hot-rolling mill at our Madison, Illinois plant, could be difficult to repair and would be very costly should it need to be replaced. Any failure to deliver products to our customers in a timely manner could adversely affect our customer relationships and reputation. Any failure to implement required investments, due to the need to divert funds to repair existing physical infrastructure, service debt obligations, unanticipated liquidity constraints or other factors, could have a material adverse effect on our results of operations, financial position and cash flows.

Our operations may prove harmful to the environment resulting in reputational damage and clean-up or other related costs.

We are exposed to substantial environmental costs and liabilities, including liabilities associated with divested assets and prior activities performed on sites before we acquired an interest in them. Our operations, including the production and delivery of our products, are subject to a broad range of continually changing environmental laws and regulations in each of the jurisdictions in which we operate. These laws and regulations increasingly impose more stringent environmental protection standards on us with respect to, among other things, air emissions, wastewater discharges, the use and handling of hazardous materials, noise levels, waste disposal practices, soil and groundwater contamination and environmental clean-up. Complying with these regulations involves significant and recurring costs.

We cannot predict our future environmental liabilities and cannot assure investors that our management is aware of every fact or circumstance regarding potential liabilities, or that the amounts provided and budgeted to address such liabilities will be adequate for all purposes. In addition, future developments, such as changes in regulations, laws or environmental conditions, may result in reputational damage or increase environmental costs and liabilities that could have a material adverse effect on our results of operations, financial position and cash flows.

The health and safety of our employees and the safe operation of our business is subject to various health and safety regulations in each of the jurisdictions in which we operate. These regulations impose various obligations on us, including the provision of safe working environments and employee training on health and safety matters. Complying with these regulations involves recurring costs.

Certain of our operations are highly regulated by different agencies that require products to comply with their rules and procedures and can subject our operations to penalties or adversely affect production.

Certain of our operations are in highly regulated industries that require us to maintain regulatory approvals and, from time to time, obtain new regulatory approvals from various countries. This can involve substantial time and expense. In turn, higher costs of compliance reduce our cash flows from operations. For example, manufacturers of gas cylinders throughout the world must comply with high local safety and health standards and obtain regulatory approvals in the markets in which they sell their products. Furthermore, military organizations require us to comply with applicable government regulations and specifications when providing products or services to them directly or as subcontractors. In addition, we are required to comply with U.S. and other export regulations with respect to certain products and materials. The E.U. has also passed legislation governing the registration,

15

evaluation and authorization of chemicals, known as REACH, pursuant to which we are required to register chemicals and gain authorization for the use of certain substances. In the U.S. there is similar legislation under the Toxic Substance Control Act 1976 ("TSCA") which was substantially amended in 2016. Although we make reasonable efforts to obtain all licenses and certifications that are required by countries in which we operate, there is always a risk that we may be found not to comply with certain required procedures. This risk grows with increased complexity and variance in regulations across the globe. As regulatory schemes vary by country, we may also be subject to regulations of which we are not presently aware and could be subject to sanctions by a foreign government that could materially and adversely affect our operations in the relevant country.

Governments and their agencies have considerable discretion to determine whether regulations have been satisfied. They may also revoke or limit existing licenses and certifications or change the laws and regulations to which we are subject at any time. If our operations fail to obtain, experience delays in obtaining or lose a needed certification or approval, we may not be able to sell our products to our customers, expand into new geographic markets or expand into new product lines. In addition, new or more stringent regulations, if imposed, could result in us incurring significant costs in connection with compliance. Non-compliance with these regulations could result in administrative, civil, financial, criminal or other sanctions against us, which could have negative consequences on our business and financial position. Furthermore, if we begin to operate in new countries, we may need to obtain new licenses, certifications and approvals.

Our customers are also often subject to similar regulations and risks. We therefore face the risk that our customers may have the demand for their products reduced as a result of regulatory matters that fall outside our direct control. This would in turn reduce demand for our products and have a negative financial impact on our operating results.

Any of these factors could have a material adverse impact on our results of operations, financial position and cash flows.

We are subject to legislation and regulations to reduce carbon dioxide and other greenhouse gas emissions.