![]()

![]()

![]()

| SUPPLEMENTARY INFORMATION AND MD&A For the three and twelve months ended August 31, 2011 |

|

Supplementary Information and MD&A

For the three

and twelve months ended August 31, 2011

MANAGEMENT DISCUSSION AND ANALYSIS

This management discussion and analysis (“MD&A”) of Platinum Group Metals Ltd. (“Platinum Group”, the “Company” or “PTM”) is dated as of November 21, 2011 focuses on the Company’s financial condition and results of operations for the three and twelve months ended August 31, 2011 and should be read in conjunction with the Company’s audited consolidated financial statements for the year ended August 31, 2011 together with the notes thereto (the “Financial Statements”).

The Company prepares it’s financial statements in accordance with generally accepted accounting principles in Canada (“Canadian GAAP”). All dollar figures included therein and in the following MD&A are quoted in Canadian Dollars unless otherwise noted.

PRELIMINARY NOTES

NOTE REGARDING FORWARD-LOOKING STATEMENTS:

This MD&A and the documents incorporated by reference herein contain “forward-looking information and “forward-looking statements” within the meaning of applicable Canadian and US securities legislation (collectively, “forward-looking statements”). All statements, other than statements of historical fact that address activities, events or developments that the Company believes, expects or anticipates will, may, could or might occur in the future (including without limitation, statements regarding estimates and/ or assumptions in respect of production, revenue, cash flows and costs, estimated project economics, mineral resource and mineral reserve estimates, potential mineralization, potential mineral resources and mineral reserves, projected timing of possible production, the Company’s exploration and development plans and objectives with respect to its projects are forward-looking statements.

These forward-looking statements reflect the current expectations or beliefs of the Company based on information currently available to the Company. Forward looking statements in respect of capital costs, operating costs, production rate, grade per tonne and smelter recovery are based upon the estimates in the Updated Feasibility Study (defined below) and the forward looking statements in respect of metal prices and exchange rate are based upon the three year trailing average prices and the assumptions contained in the Updated Feasibility Study.

Forward-looking statements are subject to a number of risks and uncertainties that may cause the actual events or results of the Company to differ materially from those discussed in the forward-looking statements, and even if such actual events or results were realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, the Company. Factors that could cause actual results or events of the Company to differ materially from current expectations include, among other things: metals price volatility; additional financing requirements; economic and political instability; the ability to obtain and maintain necessary permits; fluctuations in the relative values of the Canadian Dollar as compared to the South African Rand and the United States Dollar; the ability of the Company to purchase the necessary surface rights for its mineral properties; property title risks including defective title to mineral claims or property; the mineral exploration industry is extremely competitive; South African foreign exchange controls may limit repatriation of profits; the Company’s designation as a “passive foreign investment company”; discrepancies between actual and estimated reserves and resources, between actual and estimated development and operating costs, between actual and estimated metallurgical recoveries and between estimated and actual production; changes in national and local government legislation, taxation, controls, regulations and political or economic developments in Canada, South Africa or other countries in which the Company does or may carry out business in the future; success of exploration activities and permitting timelines; the speculative nature of mineral exploration, development and mining, including the risks of obtaining necessary licenses and permits; exploration, development and mining risks and the inherently dangerous nature of the mining industry, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, mine collapses, cave-ins or flooding and the risk of inadequate insurance or inability to obtain insurance to cover these risks and other risks and uncertainties; the Company’s limited experience with development-stage mining operations; the Company has a history of losses; most of the Company’s properties contain no proven reserves; the ability of the Company to retain its key management employees; conflicts of interest; dilution through the exercise of outstanding options and warrants; share price volatility and no expectation of paying dividends; any disputes or disagreements with the Company’s joint venture

Platinum Group Metals Ltd. (Exploration and Development Stage Company) P.21

SUPPLEMENTARY INFORMATION AND MD&A

For the three and

twelve months ended August 31, 2011

partners; socio economic instability in South Africa or regionally; the Company’s land in South Africa could be subject to land restitution claims; any adverse decision in respect of the Company’s prospecting or future mining rights and projects in South Africa; the introduction of South African State royalties where the Company’s current mineral reserves are located; and the other risks disclosed under the heading “Risk Factors” in the Company’s annual information form (“AIF”) dated November 21, 2011 which is available electronically at www.sedar.com.

Any forward-looking statement speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking statement, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking statements are reasonable, forward-looking statements are not guarantees of future performance and accordingly undue reliance should not be put on such statements due to the inherent uncertainty therein.

NOTE TO U.S. INVESTORS REGARDING RESOURCE ESTIMATES:

All r esource estimates contained in this report have been prepared in accordance withNational Instrument 43 101 and the Canadian Institute of Mining, Metallurgy and Petroleum Classification System in compliance with Canadian securities laws, which differ from the requirements of United States securities laws. Without limiting the foregoing, this report uses the terms “measured resources”, “indicated resources” and “inferred resources”. U.S. investors are advised that, while such terms are recognized and required by Canadian securities laws, the U.S. Securities and Exchange Commission (“SEC”) does not recognize them. Under U.S. standards, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. U.S. investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into reserves. Further, inferred resources have a great amount of uncertainty as to their existence and as to whether they can be mined legally or economically. It cannot be assumed that all or any part of the inferred resources will ever be upgraded to a higher category. U.S. investors are cautioned not to assume that all or any part of the inferred resources exists, or that they can be mined legally or economically. Information concerning descriptions of mineralization and resources contained in this report may not be comparable to information made public by U.S. companies subject to the reporting and disclosure requirements of the SEC.

1. DESCRIPTION OF BUSINESS

Pla tinum GroupMetals Ltd. is a British Columbia corporation incorporated on February 18, 2002 by an order of the Supreme Court of British Columbia approving an amalgamation between Platinum Group Metals Ltd. and New Millennium Metals Corporation. The Company is an exploration and development company conducting work primarily on mineral properties it has staked or acquired by way of option agreement in the Republic of South Africa and Ontario, Canada.

The Company’s complement of staff, consultants and casual workers in both Canada and South Africa currently consists of approximately 30 individuals. A further six people have been appointed as the owner’s team for the Project 1 Platinum Mine (“Project 1”) in South Africa. Engineering, Procurement and Construction Management, (“EPCM”) provider, DRA Mining Pty Ltd. (“DRA”) has assigned approximately 30 people to the project. Civil and underground mining contractors currently have approximately 300 people working on site at Project 1. General office space and support services in Canada and South Africa are being maintained at similar levels in 2011 as compared to 2010, but at Project 1, existing facilities at the Sundown Ranch property owned by the Company have been renovated to handle mine site administration, site induction and staff services. An information technology and communication upgrade is also underway in Canada and South Africa to enhance the efficiency of data transmission within the Company. The upgrade is near completion.

2. PROPERTIES

The Company defers all acquisition, exploration and development costs related to mineral properties The. recoverability of these amounts is dependent upon the existence of economically recoverable reserves, the ability of the Company to obtain the necessary financing to complete the development of the property, and any future profitable production; or alternatively upon the Company’s ability to dispose of its interests on an advantageous basis.

P.22 Platinum Group Metals Ltd. (Exploration and Development Stage Company)

| SUPPLEMENTARY INFORMATION AND MD&A For the three and twelve months ended August 31, 2011 |

|

The Company evaluates the carrying value of its property interests on a regular basis Any. properties management deems to be impaired are written down to estimated fair market value or are written off. During the period there were no material write-offs in deferred costs relating to South African or Canadian projects. For more information on mineral properties, see below and Note 4 of the Company’s Financial Statements.

SOUTH AFRICAN PROPERTIES

The Company conducts all of its SouthAfrican exploration work through its 100% owned subsidiary, Platinum Group Metals RSA (Pty.) Ltd. (“PTM RSA”). Development of Project 1 is conducted through Maseve Investments 11 (Pty.) Ltd. (“Maseve”), a company owned 74% by PTM RSA and 26% by Black Economic Empowerment company Africa Wide Mineral Prospecting and Exploration (Pty) Limited (“Africa Wide”), which is in turn owned 100% by JSE listed Wesizwe Platinum Limited (“Wesizwe”).

Project 1 and 3

Project 1- Financial Overview

The Company completed a definitive feasibility study FS”) in July 2008 and an updated feasibility study dated November 20, 2009(“ entitled “Updated Technical Report (Updated Feasibility Study) Western Bushveld Joint Venture (Elandsfontein and Frischgewaagd) (“UFS”) in October 2009 with respect to Project 1, which was at that time a portion of the Western Bushveld Joint Venture (“WBJV”) in South Africa. Included in each study is a declaration of four element or “4E” reserve ounces of combined platinum, palladium, rhodium and gold at the time of publication.

The Base Case for the UFS was modeled using 3 year trailing metal prices at September 2009, including US$1,343 per ounce platinum, an exchange rate of 8 Rand to the US Dollar and a 10% discount rate, resulting in a pre-tax net present value of US $475 million for the project on a 100% of project basis. Applying a 5% discount rate resulted in a pre-tax net present value of US $981 million on a 100% of project basis. The UFS model does not include escalation of costs or metal prices due to inflation. The Base Case also calculated a strong Internal Rate of Return “IRR” (pretax) of 23.54%.

The UFS estimated average life-of-mine cash operating costs to produce concentrate at R525 (approximately US$65.63) per tonne of ore or R4,208 (approximately US$526) per 4E ounce. The Merensky Reef layer represents the first 15 years of production and the Merensky basket price per 4E ounce is modeled at US$1,185 (3 year trailing prices to September 2009) and US$1,025 (prices recent to September 2009). The UG2 layer represents the balance of modeled production. The UG2 basket price per 4E ounce was modeled at US$1,433 (3 year trailing prices to September 2009) and US$1,068 (prices recent to September 2009). The model includes a subsequent average 15.16% discount from the metal price to estimate the smelter pay discount.

The project, as described in the UFS, has an estimated life of 22 years with 9 years at steady state production of 234,000 to 300,000 4E ounces per year. Capital costs for the mine and concentrator are R3.55 billion or US$443.13 million for peak funding and R4.76 billion or US$595.04 million for life of mine funding, both at an exchange rate of 8 Rand to the USD.

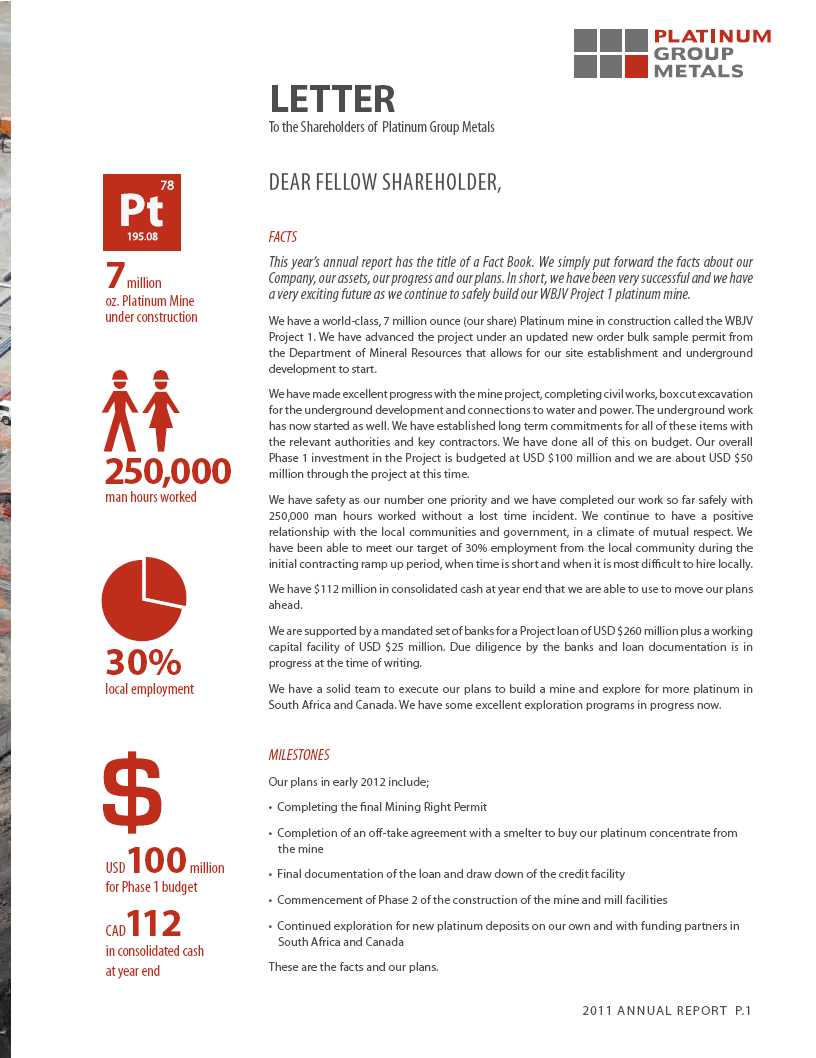

Currently, management believes the general outline of project implementation and timing is appropriate taking into account a delay to the effective project start from the dates in the UFS due to the time required to complete the restructuring of the WBJV (the “Restructuring”) and the two phase approach to development now being employed. Phase 1 development is underway, while Phase 2 of development will be dependent upon the grant of a final mining authorization, the completion of a concentrate off-take agreement and the arrangement of a commercial debt facility for the project, all three of which are currently in process.

In December 2010, the Company approved the $100 million Phase 1 budget for the development of twin central declines into the Project 1 deposit. The Company has committed $74 million against its 74% share of this budget. Phase 1 included the purchase of surface rights and facilities at a cost of R 130.0 million (approximately $18.81 million). The remainder of the Phase 1 budget is to be applied for surface and earth works, including pads, lay down areas, a box cut, twin decline access and limited level development. Work completed under Phase 1 is a component of the estimated US$443 million peak funding to build Project 1. In April 2011 the board of Maseve approved a disbursement from Maseve of $6.2 million (Rand 43 million) to cover reimbursement to PTM for past costs and value engineering.

Platinum Group Metals Ltd. (Exploration and Development Stage Company) P.23

SUPPLEMENTARY INFORMATION AND MD&A

For the three and

twelve months ended August 31, 2011

Project 1 - Activities in the Current Year

Dur ing the year endedAugust 31, 2011, the Company incurred exploration, engineering and development costs of $23.14 million for Projects 1 and 3 and invested approximately $20 million of property, plant and equipment towards the development of Project 1. In the prior year’s comparative period, this property was held in a joint venture arrangement and engineering and development costs for the Company’s account was $0.9 million.

In October 2010, the Company appointed Mr. Thys Uys, a Professional Engineer with more than 21 years of management experience in project feasibility and implementation in South Africa, as the Company’s representative and project manager for development of the Project 1. An owner’s team consisting of people who previously worked with Mr. Uys on large scale mining construction projects has also been appointed, including a dedicated quantity surveyor for cost engineering services, contract and capital control administrators and a permitting consultant responsible for the Company’s Environmental Impact Assessment and Management Plan.

In December 2010, the Company appointed DRA as EPCM contractor for surface infrastructure and underground development. DRA has assigned approximately 30 full time professionals to oversee and plan the execution of the development of surface infrastructure, power delivery, water delivery, civil works and excavations and the development of underground tunnels to access ore during Phase 1 construction. DRA’s scope of work includes engineering, design, construction management, administration and cost and schedule control.

In late March 2011, the Company received a positive record of decision from the Department of Mineral Resources of the Government of South Africa (“DMR”) for its detailed underground development plans and environmental management program, including the taking of a bulk sample. The consent of the DMR requires compliance with underlying regulations related to health, safety and environment. The final mining right application and social and labour program for Project 1 was filed in April 2011 and was later accepted for processing by the DMR. Application in terms of the National Environmental Management Act (NEMA) was also accepted by the DMR. An update to the public participation process, including project publication, placement of notices and public meetings with local government and interested and affected parties is underway.

During February, March and April 2011, the Company conducted approximately 16,850 metres of infill drilling on the near surface portions of the Project 1 platinum deposit in order to move resource blocks from the indicated to measured level of confidence and to gain more detailed information for metallurgical, geotechnical, mine planning and scheduling purposes. As a result of this work, refinements to the scheduled mining during the first three or four years of the planned Project 1 mine life of both UG2 and Merensky Reef tonnage are currently being modeled and implemented. New geo-statistical information resulting from the latest borehole data, combined with the modified modeling, mine planning and scheduling, could result in changes to the reported reserves and resources. During the execution of the development plan, changes to the estimated capital cost for the development of the Project 1 Platinum Mine may occur.

Civil construction for Phase 1 of Project 1 began in May 2011, with the mobilization of civil contractor Wilson Bailey Holmes (“WBH”), who is responsible for major surface infrastructure excavation and construction. An expenditure for civil construction of R 23.62 million (approximately $3.3 million) has been incurred to August 31, 2011 from a commitment of R35.6 million (approximately $5.09 million). The box cut excavation was completed in mid-September. WBH executed the first undercut blasts to commence underground development in October. WBH remains on site and is currently working to complete surface infrastructure.

In July 2011, JIC Mining Services (“JIC”) of Johannesburg, South Africa was awarded the contract to develop the twin 1,200 meter underground decline tunnels into the center of the Project 1 platinum deposit. JIC took over underground development from WBH in mid-October. JIC is operating as one of the underground mining contractors at the producing Bafokeng Rasimone Platinum Mine immediately adjacent to the Project 1 and currently operates as underground mining contractor on another six platinum mines and one chrome mine in South Africa, employing 7,200 people. JIC has a good safety record and have invested in an accredited training facility near Project 1. Total primary underground development cost for Phase 1 based on the JIC contract is estimated at R 206.85 million (approximately $28.90 million on August 31, 2011), resulting in an estimated cost per unit for underground development below the estimate in our Updated Feasibility Study. An initial pre-payment of R 25.0 million (approximately $3.50 million) was released to JIC after JIC provided an appropriate form of performance guarantee. A further retention amount of R 20.69 million ($2.90 million) was released to JIC approximately ten days later. JIC will be paid according to progress invoicing as work is completed over approximately seventeen months. Phase 1 is currently about 55% to 60% complete, is on budget and within 10 to 12 weeks of being on time.

P.24 Platinum Group Metals Ltd. (Exploration and Development Stage Company)

| SUPPLEMENTARY INFORMATION AND MD&A For the three and twelve months ended August 31, 2011 |

|

Ancillary servicing for the site including, buildings, piping, cabling, fencing and security have been initiated for a commitment of approximately R14.4 million (approximately $2.06 million). A temporary power supply of 1.5MVa has been installed on site and has been energized. A 10 MVa supply line is slated for completion and connection in 2012. Permanent power service for the remaining 30 MVa is being designed and engineered by Eskom to be supplied in 2013. The Company has paid Eskom R 51.71 million ($7.22 million at August 31, 2011) of an R 142.22 million (approximately $20.32 million) commitment for delivery of power.

The Company has entered into an agreement with regional water supplier, Magalies, for a temporary 0.5 ML/day water supply and have expended R 2.0 million (approximately $0.29 million). The construction of this supply is complete. The agreement for permanent water supply of 6 ML/day is being finalized and service is slated to be provided by 2013.

The Company has committed to Wrap-around Liability and Course of Construction insurance for Project 1 for a three year estimated cost of approximately $440,000. Additional insurance will be required for Phase 2 construction and mine operation. During fiscal 2011, the Company completed a comprehensive risk assessment for Project 1 with the assistance of an international insurance broking firm.

The Company has contracted the services of an experienced and professional HR company, Requisite Business Solutions (“RBS”), to provide site and office human resources, organization design and planning services to Project 1. RBS specializes in the mining industry, and their team of Professional Engineers, Psychologists and Practitioners has an intimate understanding of organization design & development, including knowledge of the applied legislation, mining techniques and associated labour practices. RBS has assisted the Company to complete a Local Skills Assessment in six communities to help identify candidates for leadership and staff positions as per the Company’s Social and Labour Plan and Human Resources Development obligations. Community members have already been hired and more are currently undergoing medicals, training and induction.

Project 1 - Mineral Resources and Reserves

The Company provided a statement of reserves Projectfor 1 in the Updated Feasibility Study and an updated statement of resources for Project 1 in a NI 43 101 technical report dated November 20, 2009 entitled “An Independent Technical Report on Project Areas 1 and 1A of the Western Bushveld Joint Venture (WBJV) Located on the Western Limb of the Bushveld Igneous Complex, South Africa” (the “Project 1 Report”). An updated NI 43 101 technical report dated August 31, 2010 entitled “Technical Report on Project 3 Resource Cut Estimation of the Western Bushveld Joint Venture (WBJV) Located on the Western Limb of the Bushveld Igneous Complex, South Africa” (the “Project 3 Report”) was filed with respect to Project 3. Project 1 hosts an estimated 2.801 million measured four element or “4E” ounces of platinum, palladium, rhodium and gold, 5.361 million indicated 4E ounces and 0.047 million inferred 4E ounces. Project 3 hosts an estimated 1.939 million indicated 4E ounces and 0.076 million inferred 4E ounces. Of the resources stated above for Project 1, there are 1.756 million 4E ounces categorized as proven reserves and 2.91 million 4E ounces categorized as probable reserves. The Company holds a 74% interest in the 4E ounces attributable to Project 1 and Project 3 as described above. New geo statistical information and ongoing mine design parameters resulting from recent infill borehole data, combined with modified modeling, mine construction steps and scheduling being completed at the time of writing of this MD&A, could result in changes to the reported reserves and resources for Project 1.

Additional information regarding grades, prill splits, sampling and reserve and resource calculations can be found in the technical reports described above as filed on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Reserves are a sub set of measured and indicated resources included in the UFS and take into account mining factors and are not in addition to the resources.

Project 1 - Infrastructure and Metal Recovery

The UFS design for metallurgical extraction utilizes a standard plant design similar to other nearby plants in the Bushveld complex operating on the same reefs. The plant is designed with circuits that can process Merensky Reef, UG2 Reef or a blended feed. The Merensky Reef is the target of initial mining because of its higher grade and low chrome content. The concentrator has been designed and costed in the UFS based on a treatment rate 160,000 tonnes per month, rather than on 140,000 tonnes per month as in the FS. For the concentrator to treat this increased quantity of reef, the recovery has been reduced with a discount of up to 2.5% for treatment in excess of nominal “name plate” capacity.

Metallurgical testing and the published experience of the adjacent operating mines support a “name plate” capacity plant recovery rate estimate of 87.5% of platinum, palladium, rhodium and gold on the Merensky Reef and 82.5% on the UG2 Reef. Recoveries

Platinum Group Metals Ltd. (Exploration and Development Stage Company) P.25

SUPPLEMENTARY INFORMATION AND MD&A

For the three and

twelve months ended August 31, 2011

of 45% for nickel and 70% for copper are also modeled for the Merensky Reef. Ruthenium and Iridium are also included as minor contributors. Additional metallurgical study is under way at the time of writing in order to refine the Company’s data in advance of formal off take negotiations.

The mine infrastructure in the estimates includes the entire required surface infrastructure for a standalone mine including water, power, underground access and ventilation to establish full production.

Project 1 - History of Acquisition

On October 26, 2004, the Company entered into the WBJV with a subsidiary Anglo Platinum Limited (“Anglo”) and Africa Wideof to pursue platinum exploration and development on combined mineral rights that would eventually cover approximately 72 square kilometres on the Western Bushveld Complex of South Africa. The Company and Anglo Platinum each held a 37% working interest in the WBJV, while Africa Wide held a 26% working interest. The area of the WBJV was comprised of three functional areas described as Project 1 (100% WBJV), Project 2 (50% WBJV: 50% Wesizwe Platinum Ltd.) and Project 3 (100% WBJV). In April 2007 the shareholders of Africa Wide sold 100% of their company to Wesizwe.

Also, in 2004, the Company acquired the surface rights to the 365.64 hectares Elandsfontein farm and its underlying mineral rights. The Elandsfontein mineral titles were transferred to project operating company, Maseve on April 22, 2010 while the surface rights, valued at half of the original acquisition cost, remain under title to the Company.

During 2008, the Company purchased surface rights adjacent to the Project 1 deposit area measuring 216.27 hectares for R 8.0 million (approximately $1.09 million) and the Company also acquired surface rights directly over a portion of the Project 1 deposit area measuring 358.79 hectares for a total of R 15.69 (approximately $2.14 million). The rights and title to the above two properties remain with the Company.

Based on the WBJV resource estimate contained in the FS, and under the terms of the original WBJV agreement, on April 22, 2010 the Company paid an equalization amount due to Anglo in the amount of $24.83 million (R 186.26 million).

Also on April 22, 2010, the partners of the WBJV completed the restructuring, a transaction dissolving the WBJV and reorganizing its underlying assets. Wesizwe acquired all of Anglo’s mineral interests underlying the WBJV, retained Anglo’s interests to Project 2, and then transferred all of Anglo’s interests underlying Projects 1 and 3 into project operating company Maseve. The Company transferred its interests in the mineral rights underlying Projects 1 and 3 into Maseve, and rescinded its interests in Project 2 to Wesizwe. As a result Wesizwe retained 100% of Project 2 and Maseve obtained 100% of Projects 1 and 3.

In exchange for its 18.5% interest in Project 2 the Company effectively received a 17.75% interest in Maseve. The Company also received a 37% interest in exchange for its share of Projects 1 and 3, bringing its holdings in Maseve to 54.75%. Wesizwe received a 45.25 % initial interest in Maseve.

The sale of the Company’s 18.5% interest in Project 2 was accounted at an estimated fair value of $65.42 million on April 22, 2010, versus an historic cost of $19.80 million, for a gain of $45.62 million. The transfer of the Company’s 37% interest in Projects 1 and 3 into Maseve was accounted for as a reorganization of existing business and was transferred into Maseve at book cost.

The Company acquired a further 19.25% interest in Maseve in exchange for subscriptions in the amount of approximately $59 million as of January 14, 2011 (R 408.81 million), thereby increasing its shareholding to 74%. The subscription funds are held in escrow for application towards Wesizwe’s 26% share of expenditures for Projects 1 and 3.

After the WBJV Restructuring, the Company carries total deferred costs related to Projects 1 and 3 of $138.5 million at August 31, 2011. The non-controlling interest related to Wesizwe’s 26% holding of Maseve is recorded at $11.7 million as of August 31, 2011. In August 12, 2010 the Company acquired surface rights covering 1,713 hectares, including accommodation facilities overlaying the area of the planned Project 1 Platinum Mine, for approximately $18.8 million (R 130.0 million). The Company has assigned this property to Maseve and the purchase price was part of the Phase 1 development budget for Project 1 as described above.

P.26 Platinum Group Metals Ltd. (Exploration and Development Stage Company)

| SUPPLEMENTARY INFORMATION AND MD&A For the three and twelve months ended August 31, 2011 |

|

Other South Africa Properties

Exploration expenditures during the year on projects in South Africa other than Project 1 and Project 3 totaled $1.68 million (2010 - $1.99 million). Cost recoveries during the period in the amount of $1.69 million (2010 -$1.94 million) were received from joint venture partners.

Northern Limb, Bushveld - War Springs and Tweespalk Properties

In March 2008, the Company reported an inferred resource on a 100% basis of 1.676 million ounces E (platinum,3 palladium and gold) at a grade of 1.11 g/t with a minor credit for copper and nickel. Additional information regarding grade, prill splits, sampling and resource calculations can be found in NI 43-101 technical report dated June 18, 2009 entitled “Revised Inferred Mineral Resource Declaration War Springs (Oorlogsfontein 45K2), Northern Limb Platinum Property, Limpopo Province, Republic of South Africa” (the “War Springs Report”) filed on SEDAR and on EDGAR at www.sec.gov.

The War Springs mineral resource is characterised by two distinct reef layers, termed the “B” and “C” reefs. Both reefs are typically greater than 6 metres thick. The reefs outcrop on surface and extend down dip in parallel sheets at a 65 degree angle to a depth of 400 metres, remaining open at depth. Of the 22 boreholes drilled to February 2006, and which were used in the resource calculation, 15 boreholes intersected the “B” Reef and 8 boreholes intersected the “C” Reef. A total of 9,926 samples were taken for analysis. Drilling results from Phase 1 and 2 covering approximately 2,200 metres of strike length on 250 metre spacing, combined with a review of economic cut-off, form the basis of the updated Inferred Mineral Resource estimate reported in the War Springs Report. Since March 2009 a total of 17,222 metres of drilling in 20 boreholes have been completed on the War Springs project with JOGMEC funding. Total expenditures incurred by Japan Oil, Gas and Metals National Corporation (“JOGMEC”) to August 31, 2011 on War Springs amounted to approximately $2.9 million. Subsequent to year end the 2011 drilling program was completed and JOGMEC indicated that they do not plan to fund further work on this project.

Black Economic Empowerment groups Africa Wide, a subsidiary of Wesizwe, and Taung Minerals (Pty) Ltd., a subsidiary of Platmin Limited, have each acquired a 15% interest in the Company’s rights to the War Springs project carried to bankable feasibility. Africa Wide also holds a 30% participating interest in the Tweespalk property. The Company retains a net 70% project interest in both the War Springs and the Tweespalk properties.

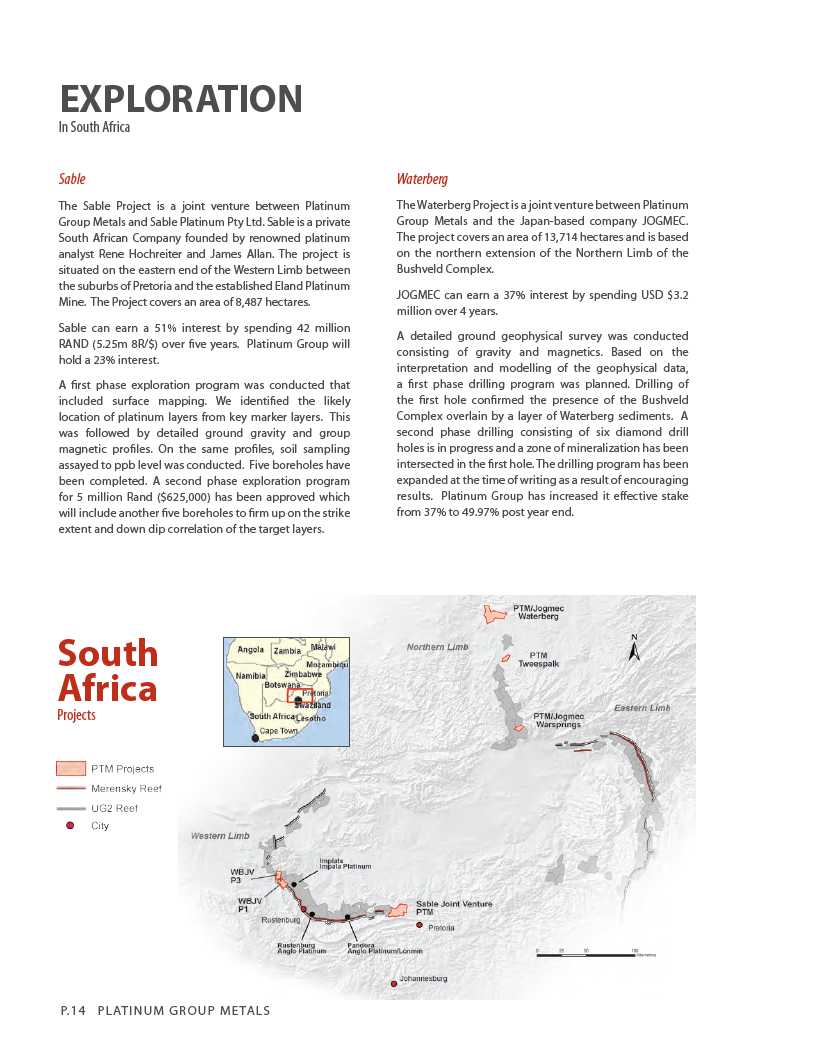

Sable Joint Venture, South Africa

During 2009, the Company acquired by staking various prospecting permits west Pretoria along the trend of the south easternof part of the Western Limb. The territory, named the Sable Joint Venture project area, is under agreement to a black economic empowerment group for a 26% interest and Sable Platinum Mining (Pty) Limited (“Sable”) as to a 51% interest in exchange for Sable funding approximately $6.0 million (R 42.0 million) in work on the project. Exploration work consisting of mapping, soil sampling, geophysical surveys and drilling has been undertaken to date. Drilling is underway at the time of writing. Results will be released in the months ahead. To the time of writing a total of 4,134 metres have been drilled in 5 boreholes on the project area. The Company is the operator of the project. Total cumulative expenditures incurred by Sable Platinum to August 31, 2011 amounted to approximately R 5.8 million ($0.8) million.

Waterberg Venture, South Africa

During September 2009, the Company was granted prospecting rights for a 137 square kilometre area named the Waterberg Project north of the known North Limb of the Bushveld Complex. The Company holds an initial 74% interest in the project and private South African Black Economic Empowerment firm, Mnombo, holds a 26% interest. Magnetic, gravity, and general trends all indicate that the North Limb extends under shallow cover in this area and initial geochemical sampling confirmed this interpretation. Drilling in early 2011 confirmed the presence of BIC sequences and results announced on November 9, 2011 confirmed the presence of two PGE bearing zones or reefs with significant values. Reported drill intercepts included 3.47 g/t platinum, palladium and gold (2 PGE+Au) over 3.5 metres and 7.00 g/t 2PGE+Au over 5.0 metres at vertical depth of approximately 660 metres. At the time of writing assay values for these intercepts for rhodium, copper and nickel remained outstanding. Drilling on the Waterberg Project continued in November 2011 with two drill rigs and at the time of writing the Company is planning to deploy another two rigs in order to accelerate the project.

Platinum Group Metals Ltd. (Exploration and Development Stage Company) P.27

SUPPLEMENTARY INFORMATION AND MD&A

For the three and

twelve months ended August 31, 2011

In October 2009, the Company entered an agreement with OGMEC and Mnombo whereby JOGMEC may earn up to a 37% interestJ in the Waterberg project for an optional work commitment of US$3.2 million over 4 years, while at the same time Mnombo is required to match JOGMEC’s expenditures on a 26/74 basis. If required, the Company agreed to loan Mnombo their first $87,838 in project funding. To the time of writing, a total of 3,331 metres have been drilled in 2 completed boreholes and 2 boreholes underway on the project area. The Company is the operator of the project. Total cumulative expenditures incurred by JOGMEC to August 31, 2011 amounted to approximately R 6.4 million ($0.89 million) and to October 31, 2011 JOGMEC had funded approximately R 6.85 million ($0.92 million).

On November 7, 2011 the Company entered into an agreement with Mnombo whereby the Company will acquire 49.9% of the issued and outstanding shares of Mnombo in exchange for a cash payment of R 1.2 million and for the Company paying for Mnombo’s 26% share of Waterberg Project costs to feasibility. When combined with the Company’s 37% direct interest in the Waterberg Project (after JOGMEC earn-in), the 12.974% indirect interest to be acquired through Mnombo will bring the Company’s project interest to 49.974%.

CANADIAN PROPERTIES

Mineral property acquisition and capital costs deferred during the year on projects in Canada totaled $0.35 million (2010 - $0.03 million). Exploration costs incurred in the year for Canadian properties totaled $1.05 million (2010 - $0.24 million). The Company hired a Canadian exploration manager at the beginning of January 2011 to run these exploration programs.

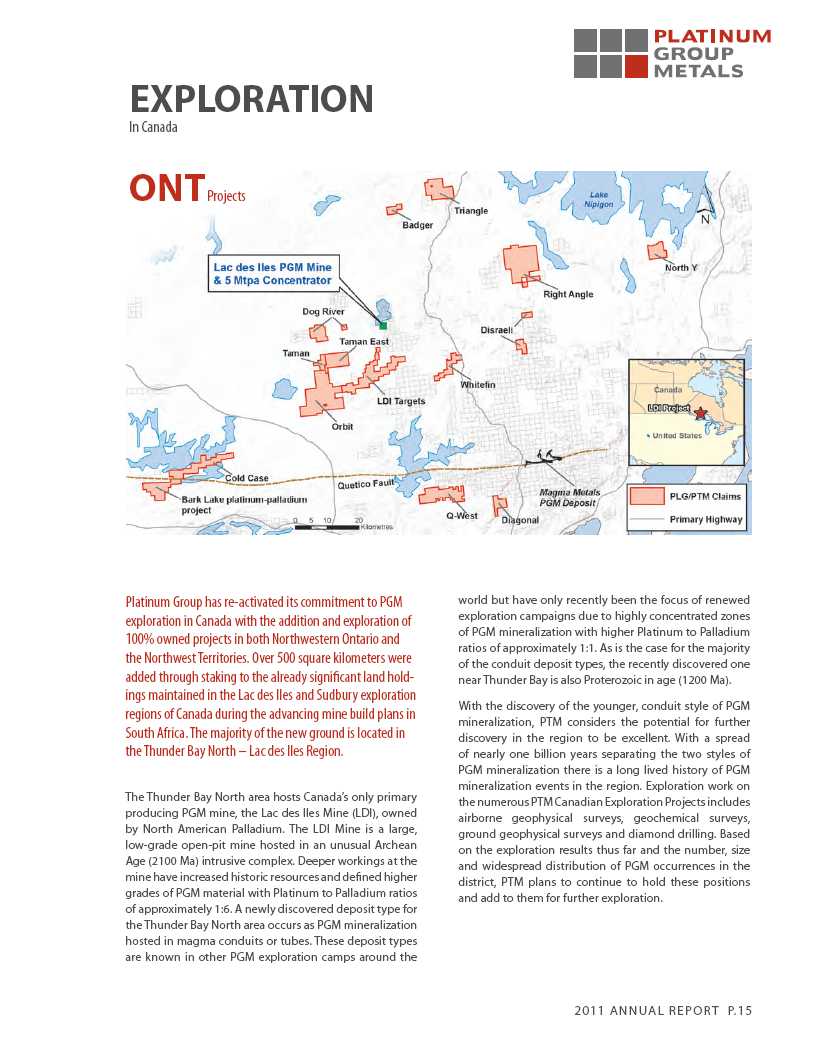

Lac des Iles - Thunder Bay North Properties, Ontario

The Company maintains a large mineral rights position in Lac des Iles – Thunder Bay North area, Ontario as a strategic holdingthe against increasing prices for palladium and platinum. Included in these holdings are claims staked in early 2011 and continued 100% interests in the Lac Des Iles River, Shelby Lake and South Legris properties, all subject to 2.0% NSR royalties, which the Company may buy back.

The Company’s Canadian exploration program was active in the period and 12 new properties have been acquired in the Thunder Bay Mining District, Ontario. The acquired ground covers at total of 532 square kilometres, bringing the company’s holdings in the Lac des Iles – Thunder Bay North region to 657 square kilometres. The majority of these new properties were acquired by staking, utilizing in-house compilation and modeling of geophysics, geochemistry and work completed by the company in the area over the past 10 years. In addition, the Company retains a majority interest in the 73 square kilometre Agnew lake property near Sudbury, Ontario.

The properties acquired in the current period by the Company include a right to earn up to a 75% interest in Benton Resources Corp’s (“Benton”) Bark Lake platinum-palladium project, comprised of 19 mineral claims totaling 3,884 hectares located approximately 120 km west of Thunder Bay, Ontario. To earn a 70% interest the Company must make staged option payments of $145,000 in cash ($35,000 paid) and 215,000 shares (none issued to date) and complete $1,625,000 in exploration ($242,800 complete to August 31, 2011) over a 7 year period. The Company may earn a further 5% (75% total) by completing a pre-feasibility study.

All of the newly acquired properties In the Thunder Bay District are targeted on a new mineralization type in younger intrusive rocks where contained platinum is equal or greater than palladium. Platinum Group’s older projects are targeted on older intrusive rock types like that at North American Palladium’s Lac des Iles Mine where palladium is the dominant platinum group metal, or “PGM”. Historically, North American deposits have been dominated by palladium rather than rarer and more valuable platinum. Some new exploration in the Thunder Bay area has demonstrated previously unexplored potential for platinum in pipe like intrusions or conduits. Platinum Group plans to be a major participant in exploration for this new deposit type in this area.

The Company is currently conducting exploration programs on all the Lac des Iles - Thunder Bay District properties. Prospecting, geophysical surveys, soil and rock chip sampling, mapping and drilling have all been part of the 2011 work program. Three of the 100% owned properties and the Bark Lake Option were drill tested based on airborne geophysical survey results, geological ground work, geochemistry and compilation of historic data. A total of 2,759 metres have been drilled in 13 holes to date.

P.28 Platinum Group Metals Ltd. (Exploration and Development Stage Company)

| SUPPLEMENTARY INFORMATION AND MD&A For the three and twelve months ended August 31, 2011 |

|

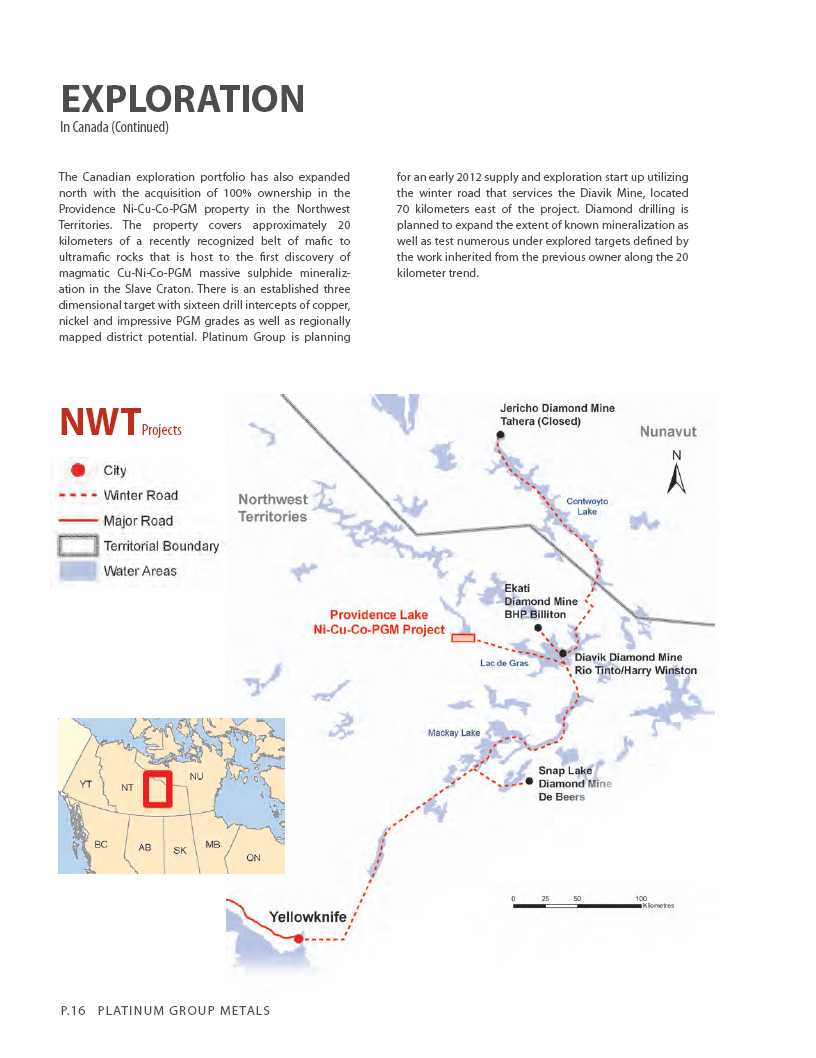

Northwest Territories Property

The Company has purchased Providencethe Nickel, Copper, Cobalt and Platinum Group Metals Property from Arctic Star Exploration (Arctic Star) for a payment of $50,000 and a 1.0% NSR royalty. The claims that comprise the Providence property will be brought to lease once a crown survey has been completed in 2012 at an estimated cost of $100,000. To date the first year lease payment and application fees have been paid. Total acquisition costs for the period are $78,216.

The camp and associated Land Use Permit will be purchased for an additional $20,000 once the Company has re-activated the corporate registration in the Northwest Territories. An extension has been granted by the Northwest Territories Mining Recorder for the completion of the survey of the claims to lease until September 28, 2012.

Exploration costs incurred during the period at Providence were $9,200 and include research and a site visit. The property is comprised of 13 mineral claims totaling 133.66 square kilometres and is located approximately 70 km west of the Diavik Diamond Mine, NWT. The property covers approximately 20 kilometres of a recently recognized belt of mafic to ultramafic rocks that is host to the first discovery of magmatic Copper-Nickel-Cobalt-Platinum Group Metals, “Cu-Ni-Co-PGM” massive sulphide mineralization in the Slave Craton. Drilling by Arctic Star has shown that the Ni-Cu-Co-PGM mineralization is hosted within, and at the base of the ultramafic flow/intrusive sill sequence. The dimensions of the massive sulphide mineralization defined to date ranges in thickness from 0.3m to 5.0m and exceeds 450 m strike length and 150 m (vertical) depth. The mineralized horizons remain open along strike in either direction and to depth.

The Company is currently compiling the large amount of data supplied by Arctic Star and will be drill testing any un-tested targets derived from the compilation work as well as planning a step out drill program to define the extents of known Ni-Cu-Co-PGM mineralized zone. Work on the property will commence in the Spring of 2012.

3. DISCUSSION OF OPERATIONS AND FINANCIAL CONDITION

A) RESULTS OF OPERATIONS

Three Months Ended August 31, 2011

For the three months August 31, 2011, the Company incurred a net loss before taxes of $3.12 ended million (August 31, 2010 – $1.73 million). General and administrative expenses totaled $1.8 million (August 31, 2010 - $1.8 million). The current year’s costs aren’t materially different than the comparative period as the Company has maintained the same level of corporate staff and utilized similar consulting services compared to the same period last year. Stock based compensation expenses totaled $0.31 million (August 31, 2010 - $Nil). Stock options were not issued during the 2010 comparative period. Foreign exchange loss during the period was $2.7 million (August 31, 2010 – loss $0.1 million). The loss in the current period resulted from the decreased value of the Rand and its impact on the cash balances held in Rand and an intercompany loan to a South African subsidiary denominated in CAD. Interest earned in the fourth quarter totaled $1.8 million versus $0.009 million in the comparative three month period in 2010. The increase in interest earned is due to greater cash holdings.

Twelve Months Ended August 31, 2011

Any reference to “period” hereafter refers to the twelve months endedAugust 31, 2011.

During the year, the Company incurred a net loss before taxes $13.25 million (2010 – income of $41.2 million). The net income in 2010 was primarily due to the disposition of the Company’s 18.5% interest in Project 2 of the WBJV to Wesizwe on April 22, 2010 for a gain on disposition of $45.62 million and an accrual for future income tax expense related to the transaction of $14.58 million. The accrual for future income tax expense is a non-cash item. A future income tax recovery was recorded in 2011 for $2.07 million, primarily relating to the Company’s mineral property expenditures. In 2010, the Company also realized a gain of $2.80 million on sale of marketable securities.

General and administrative expenses totaled $6.53 million (August 31, 2010 - $6.54 million). The current year’s costs aren’t materially different from the comparative period as the Company has maintained the same level of corporate staff and utilized similar consulting services compared to the same period last year. Stock based compensation expenses totaled $6.90 million (2010 - $0.14 million). Stock options were not issued during the 2010 comparative period; therefore the only stock-based compensation

Platinum Group Metals Ltd. (Exploration and Development Stage Company) P.29

SUPPLEMENTARY INFORMATION AND MD&A

For the three and

twelve months ended August 31, 2011

recorded for 2010 was resulting from the vesting of stock options issued in prior periods. The Company issued 7,691,500 stock options in 2011 of which 350,000 stock options are unvested. Foreign exchange loss during the year was $3.34 million (August 31, 2010 – loss $1.0 million). The loss in the current period resulted from the decreased value of the Rand and its impact on the cash balances held in Rand and an intercompany loan to a South African subsidiary denominated in CAD. Interest earned in the year totaled $3.8 million (2010 - $0.44 million).The increase in interest earned is due to greater cash holdings.

Annual Financial Information

The f ollowing tables set forth selected financial data from the Company’s annual audited financial statements and should be read in conjunction with those financial statements:

| Year ended Aug 31, 2011 | Year ended Aug 31, 2010 | Year ended Aug 31, 2009 | |

| Interest income | $ 3,785,298 (1) | $ 442,142 (1) | $ 139,548 |

| Net (loss) income | ($12,216,926)(2) | $26,660,174 (2) | ($6,963,384) |

| Basic (loss) earnings per share | ($0.07) (3) | $0.29 (3) | ($0.10) |

| Diluted earnings (loss) per share | ($0.07) (3) | $0.28 (3) | ($0.10) |

| Total assets | $286,713,122 (4) | $126,991,003 (4) | $67,070,797 |

| Long term debt | Nil | Nil | Nil |

| Dividends | Nil | Nil | Nil |

Explanatory Notes:

| (1) |

The Company’s only significant source of income during the years ending August 31, 2009 to 2011 was interest income from interest bearing accounts held by the Company. The amount of interest earned correlates directly to the interest rate at the time and the amount of cash on hand during the year referenced. |

| (2) |

In the year ended August 31, 2010, the Company recorded net income of $26.66 million. This was primarily due to gains of $2.80 million on sale of marketable securities and $45.62 million on the deemed sale for accounting purposes of an 18.5% interest in Project 2 of what was the WBJV. A $14.58 million future income tax charge was also associated with this gain. |

| (3) |

Basic earnings (loss) per common share are calculated using the weighted average number of common shares outstanding. The Company uses the treasury stock method for the calculation of diluted earnings per share. Diluted per share amounts reflect the potential dilution that could occur if securities or other contracts to issue common shares were exercised or converted to common shares. In periods when a loss is incurred, the effect of potential issuances of shares under options and share purchase warrants would be anti-dilutive, and accordingly basic and diluted loss per share are the same. |

| (4) |

Total assets had been increasing year-on-year primarily as a result of the Company’s increasing cash balance and continued investment in mineral properties funded by completion of private placement equity financings. At August 31, 2011 the Company held $64.12 million (2010 - $2.37 million; 2009 - $32.97 million) in cash and cash equivalents. The Company’s cash balance at August 31, 2011 was higher than in prior years due to equity financings completed in October and November, 2010. |

P.30 Platinum Group Metals Ltd. (Exploration and Development Stage Company)

| SUPPLEMENTARY INFORMATION AND MD&A For the three and twelve months ended August 31, 2011 |

|

Quarterly Financial Information

The following table sets forth selected quarterly financial information for each of the last eight quarters.

| Quarter Ending | Interest & Other Income (1) | Net (Loss) Income (2) | Net Basic (Loss) Earnings per Share |

| August 31, 2011 | $1,805,073 | ($1,823,756) | ($0.01) |

| May 31, 2011 | $1,084,648 | ($2,072,031) | ($0.01) |

| February 28, 2011 | $730,640 | ($3,982,628) | ($0.02) |

| November 30, 2010 | $164,937 | ($4,338,511) | ($0.03) |

| August 31, 2010 | $9,352 | ($4,140,280) | ($0.04) |

| May 31, 2010 | $220,145 | $31,183,948 | $0.33 |

| February 28, 2010 | $177,201 | ($975,747) | ($0.01) |

| November 30, 2009 | $35,444 | $592,253 | $0.01 |

Explanatory Notes:

| (1) |

The Company earned interest income from interest bearing accounts held by the Company. The amount of interest income earned correlates directly to the amount of cash on hand during the period referenced. Quarterly interest income was higher in 2011 than in past years due to higher cash balances on hand. |

| (2) |

Net income (loss) by quarter is often materially affected by the timing and recognition of large non-cash income, expense or write-off charges. The quarter ended August 31, 2011 included a foreign exchange loss of $3.37 million due to the increased value of the South African Rand and an accrual for a future income tax recovery of $2.07 million related to mineral property expenditures. The quarter ended May 31, 2011 included a non-cash charge for stock based compensation in the amount of $2.9 million. The quarter ended November 30, 2010 included a non-cash charge for stock based compensation in the amount of $3.5 million. The quarter ended May 31, 2010 included a non-cash realized gain for the deemed sale for accounting purposes of the Company’s 18.5% interest in Project 2 of the WBJV at an estimated fair market value of $45.6 million and a future income tax expense accrual for $11.9 million. The quarter ended November 30, 2009 included a non-cash charge for stock based compensation in the amount of $0.14 million, and a non- cash gain realized on marketable securities of $2.1 million. After adjusting out these non-cash charges, the results for the quarters listed show a more consistent trend, with a general growth in expenses over time in accordance with the Company’s increased exploration, development and corporate activities over the past several years as described above at “Discussion of Operations and Financial Condition”. |

B) DIVIDENDS

The Company has not declared nor paid dividends on its common shares.The Company has no present intention of paying dividends on its common shares, as it anticipates that all available funds will be invested to finance the growth of its business.

C) TREND INFORMATION

Other than the financial obligations as set out in the table provided at Item f) below, there are no demands or commitments that will result in, or that are reasonably likely to result in, the Company’s liquidity either increasing or decreasing at present or in the foreseeable future. The Company will require additional capital in the future to meet both its contractual and non-contractual project related expenditures. It is unlikely that the Company will generate sufficient operating cash flow to meet all of these expenditures in the foreseeable future. Accordingly, the Company will need to raise additional capital through debt financing, by issuance of securities, or by a sale or partnering of project interests in order to meet its ongoing cash requirements. See discussions at item 3. a) “Results of Operations” above and at item f). “Liquidity and Capital Resources” following.

Platinum Group Metals Ltd. (Exploration and Development Stage Company) P.31

SUPPLEMENTARY INFORMATION AND MD&A

For the three and

twelve months ended August 31, 2011

D) RELATED PARTY TRANSACTIONS

During the period the Company provided accounting, secretarial and reception services at market rates for day-to-day administration and accounting to Nextraction Energy Corp. (“Nextraction”), a company with three common directors (R. Michael Jones, Frank Hallam and Eric Carlson). Fees received have been credited by the Company against its own administrative costs. The Company received service fees of $126,000 (2010 - $59,500) during the period from NE.

During the period the Company provided accounting, secretarial and reception services at market rates for day-to-day administration and accounting to West Kirkland Mining (“WKM”), a company with three common directors (R. Michael Jones, Frank Hallam and Eric Carlson) and two common officers (R. Michael Jones and Frank Hallam). Fees received have been credited by the Company against its own administrative costs. The Company received service fees of $102,000 (2010 - $46,750) during the period from WKM.

Until early 2010 the Company provided accounting, secretarial and reception services at market rates for day-to-day administration to MAG Silver, a company with three common directors (R. Michael Jones, Frank Hallam, Eric Carlson). Fees received have been credited by the Company against its own administrative costs. The Company received service fees of $Nil (2010 - $64,347) during the period from MAG.

During the year ended August 31, 2005, the Company entered into an office lease agreement with Anthem Works Ltd. (“Anthem”), a company with a common director (Eric Carlson). During the period the Company accrued or paid Anthem $86,844 under the office lease agreement (2010 - $86,879).

All of the above transactions are in the normal course of business and are measured at the exchange amount which is the consideration established and agreed to by the noted parties.

E) OFF-BAL SHEET ARRANGEMENTSANCE

The Company does not have any special purpose entities nor is it party to any arrangements that would be excluded from the balance sheet.

F) LIQUIDITY AND CAPITAL RESOURCES

Accounts receivable at year end totaled $1.9 million (2010 - $1.3 million) being comprised mainly of value added taxes and transfer duties refundable in South Africa. Accounts payable at period end totaled $5.5 million (2010 - $2.3 million). The increase in accounts payable in 2011 compared to 2010 is due to increased expenditures on the development of Project 1.

Apart from net interest earned on cash deposits during the year of $3.79 million (2010 - $0.44 million), the Company had no sources of income. The Company’s primary source of capital has been from the sale of equity. At August 31, 2011 the Company had cash and cash equivalents on hand of $64.12 million compared to $2.37 million at August 31, 2010. Cash increased during the period primarily due to a bought deal financing in November 2010 for gross proceeds of $143.81 million. At August 31, 2011 the Company held a further $47.72 million (2010 - $Nil) classified as restricted cash in project operating company Maseve in escrow for Wesizwe. Wesizwe holds 26% of Maseve and the escrowed funds can be accessed for project expenditures at a ratio of 74:26, where for every $74 spent by the Company, $26 can be removed from escrow to cover Wesizwe’s share of costs. To August 31, 2011 a total of $11.0 million (2010 – nil) has been withdrawn from escrow against Wesizwe’s share of project expenditures.

During the year, the Company issued a total of 83,619,750 (2010 – 1,149,125) common shares for net cash proceeds of $158.76 million (2010 - $1.15 million). Included in this total, in October and November of 2010 the Company closed a bought deal financing and an over-allotment option for gross proceeds of $143.81 million on the issue of 70.15 million shares. Issue costs, including a 5.5% commission to the Agents and their legal costs, totaled $8.44 million. Cash proceeds from equity issuances are primarily spent on mineral property and surface right acquisitions, exploration and development as well as for general working capital purposes. The balance of cash outflows is made up of management and consulting fees and salaries, and other general and administrative expenses.

In January 2011, the Company used proceeds from equity issuances to acquire a further 19.25% interest in Maseve for subscriptions in the amount of R 408.8 million (approximately $59 million as of January 14, 2011), thereby increasing the Company’s shareholding

P.32 Platinum Group Metals Ltd. (Exploration and Development Stage Company)

| SUPPLEMENTARY INFORMATION AND MD&A For the three and twelve months ended August 31, 2011 |

|

in Maseve to 74%. According to the terms of the April 22, 2010 re-organization of the WBJV, this subscription amount was placedto 74%. into escrow in Maseve in order to fund Wesizwe’s 26% ongoing share of project costs. The Company is also funding its 74% share of a Phase 1 development budget for Project 1 of $100 million into Maseve.

The Company receives lump sum cash advances at various times as laid out in agreed budgets from its partners to cover the costs of joint venture projects.

The following table discloses the Company’s continual obligations for optional mineral property acquisition payments and contracted office and equipment lease obligations. Apart from a possible buy-out of the War Springs and Tweespalk projects, which optional acquisition payments are included in explanatory notes to the following table, the Company has no other property acquisition payments due to vendors under mineral property option agreements. The Company has no long term debt or loan obligations.

| Payments by period in Canadian Dollars | |||||||||||||||

| Total | < 1 Year | 1 – 3 Years | 3 – 5 Years | > 5 Years | |||||||||||

| Payments (War Springs & Tweespalk)(1) | $ | 72,915 | $ | 14,583 | $ | 29,166 | $ | 29,166 | $ | - | |||||

| Lease Obligations | 406,238 | 130,790 | 216,313 | 59,135 | - | ||||||||||

| Eskom–Power (2) | 12,640,885 | 8,452,435 | 4,188,450 | - | - | ||||||||||

| Insurance contracts | 435,890 | 302,667 | 133,223 | - | - | ||||||||||

| Other miscellaneous | 110,338 | 110,338 | - | - | |||||||||||

| Totals | $ | 13,666,266 | $ | 9,010,813 | $ | 4,567,152 | $ | 88,301 | $ | - | |||||

Explanatory Notes:

| (1) |

The Company pays annual prospecting fees to the vendors of US$3.25 per hectare. The Company has the option to settle the vendors’ residual interests in these mineral rights at any time for US$690 per hectare. |

| (2) |

The Company’s project operating subsidiary Maseve has entered into a long term electricity supply agreement with South African power utility Eskom. Under the agreement the Company is scheduled to receive connection and service for a 10 MVa construction power supply in 2012 and a total 40 MVa production power supply in later calendar 2013 in exchange for connection fees and guarantees totaling Rand 90,508,735 ($12,640,885 at August 31, 2011). |

Cash at August 31, 2011 is sufficient to fund the estimated general and development operations of the Company for calendar 2011 and into the first quarter of 2012, but will be insufficient to complete construction of the mine at Project 1. On August 2, 2011 the Company announced the appointment of four international commercial banks to the role of mandated lead arrangers for the placement of a USD $260 million project finance loan, representing approximately 60% of the estimated Project 1 capital cost requirements. The October 2009 UFS estimated a capital cost to build the Project 1 at US $443 million on a 100% basis at a rate of 8 Rand to the US Dollar. The banks have all received preliminary credit committee approval for the loan and are currently in process of completing loan documentation and due diligence. The project financing is planned to include a USD $25.0 million working capital facility. Completion of the project financing will be subject to certain items, including the completion of an off take agreement and the formal grant of a mining right from the Government of South Africa. The Company anticipates the probable need for additional equity funding for the project from the Company in 2012, depending on USD to Rand exchange rates and the actual costs to complete Phase 1 of the project.

G) OUTSTANDING SHARE DATA

The Company has an unlimited number of common shares authorized for issuance without par value At August. 31, 2011, there were 177,584,542 common shares outstanding, 11,250,500 incentive stock options outstanding at exercise prices of $1.40 to $4.40. At November 21, 2011, there were 177,584.542 common shares outstanding and 15,364,500 incentive stock options outstanding. Subsequent to August 31, 2011, nil common share purchase options were exercised. During the period ending August 31, 2011, the Company made no changes to the exercise price of outstanding options through cancellation and reissuance or otherwise.

Platinum Group Metals Ltd. (Exploration and Development Stage Company) P.33

SUPPLEMENTARY INFORMATION AND MD&A

For the three and

twelve months ended August 31, 2011

4. RISK FACTORS

The Company’s securities should be considered a highly speculative investment and investors should carefully consider all of the information disclosed in the Company’s Canadian and U.S. regulatory filings prior to making an investment in the Company. For a discussion of risk factors applicable to the Company, see the section entitled “Risk Factors” in the Company’s most recent annual information form filed with Canadian provincial securities regulators, which is also filed as part of the Company’s most recent annual report on Form 40-F with the U.S. Securities & Exchange Commission.

Without limiting the foregoing, the most significant risks and uncertainties faced by the Company are: the inherent risk associated with mineral exploration and development activities; the uncertainty of mineral resources and their development into mineable reserves; uncertainty as to potential project delays from circumstances beyond the Company’s control; the timing of production; title risks; political risks; risks associated with fluctuations in foreign exchange rates; risks associated with fluctuations in metal prices; risks associated with joint venture agreements and the possible failure to obtain mining licenses and/or to obtain the capital required for project and mine development.

GENERAL

Resource exploration and development is a speculative business, characterized by a number of significant risks including, among other things, unprofitable efforts resulting not only from the failure to discover mineral deposits but also from finding mineral deposits, which, though present, are insufficient in quantity and/or quality to return a profit from production.

ADDITIONAL FUNDING MAY BE REQUIRED

The Company may not have sufficient cash resources on hand to meet all of the Company’s future financial requirements relating to the exploration, development and operation of the Company’s projects. The Company will require additional financing from external sources, such as joint ventures, debt financing or equity financing in order to meet certain requirements and carry out the future development of the Company’s projects and external growth opportunities. The success and the pricing of any such capital raising and/or debt financing will be dependent upon the prevailing market conditions at that time. There can be no assurance that such financing will be available to the Company or, if it is, that it will be offered on acceptable terms. If additional financing is raised through the issuance of equity or convertible debt securities of the Company, this may have a depressive effect on the price of the Company’s securities and the interests of shareholders in the net assets of the Company may be diluted. Any failure by the Company to obtain required financing on acceptable terms could cause the Company to delay development of its material projects and could have a material adverse effect on the Company’s financial condition, results of operations and liquidity.

METAL PRICES AFFECT THE SUCCESS OF THE COMPANY’S BUSINESS

Metal prices have historically been subject to significant price fluctuations in recent No assurance. years may be given that metal prices will remain stable. Significant price fluctuations over short periods of time may be generated by numerous factors beyond the control of the Company, including domestic and international economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global or regional consumption patterns, speculative activities and increases or decreases in production due to improved mining and production methods. Significant or continued reductions or volatility in metal prices may have an adverse effect on the Company’s business, including the amount of the Company’s reserves, the economic attractiveness of the Company’s projects, the Company’s ability to obtain financing and develop projects and, if the Company’s projects enter the production phase, the amount of the Company’s revenues or profit or loss.

THE COMPANY’S BUSINESS IS SUBJECT TO EXPLORATION AND DEVELOPMENT RISKS

With the exception of Project 1, all of the Company’s properties are in the exploration stage and no known reserves have been discovered on such properties. At this stage, favourable drilling results, estimates and studies are subject to a number of risks, including:

-

the limited amount of drilling and testing completed to date;

P.34 Platinum Group Metals Ltd. (Exploration and Development Stage Company)

| SUPPLEMENTARY INFORMATION AND MD&A For the three and twelve months ended August 31, 2011 |

|

- the preliminary nature of any operating and capital cost estimates;

- the difficulties inherent in scaling up operations and achieving expected metallurgical recoveries;

- the likelihood of cost estimates increasing in the future; and

- the possibility of difficulties procuring needed supplies of electrical power and water.

There is no certainty that the expenditures to be made by the Company or by its joint venture partners in the exploration of the properties described herein will result in discoveries of precious metals in commercial quantities or that any of the Company’s properties will be developed. Most exploration projects do not result in the discovery of precious metals and no assurance can be given that any particular level of recovery of precious metals will in fact be realized or that any identified resource will ever qualify as a commercially mineable (or viable) resource which can be legally and economically exploited. The resource and reserve estimates contained herein have been determined and valued based on assumed future prices, cut-off grades and operating costs that may prove to be inaccurate. Estimates of reserves, mineral deposits and production costs can also be affected by such factors as environmental permit regulations and requirements, weather, environmental factors, unforeseen technical difficulties, unusual or unexpected geological formations and work interruptions. In addition, the grade and/or quantity of precious metals ultimately recovered may differ from that indicated by drilling results. There can be no assurance that precious metals recovered in small-scale tests will be duplicated in large-scale tests under on-site conditions or in production scale. Extended declines in market prices for platinum, palladium, rhodium and gold may render portions of the Company’s mineralization uneconomic and result in reduced reported mineralization. Any material reductions in estimates of mineralization, or of the Company’s ability to extract this mineralization, could have a material adverse effect on the Company’s results of operations or financial condition. Amendments to the mine plans and production profiles may be required as the amount of resources changes or upon receipt of further information during the implementation phase of the project.

THE COMPANY REQUIRES VARIOUS PERMITS IN ORDER TO CONDUCT ITS CURRENT AND ANTICIPATED FUTURE OPERATIONS, AND DELAYS OR A FAILURE TO OBTAIN SUCH PERMITS, OR A FAILURE TO COMPLY WITH THE TERMS OF ANY SUCH PERMITS THAT THE COMPANY HAS OBTAINED, COULD HAVE A MATERIAL ADVERSE IMPACT ON THE COMPANY

The Company’s current and anticipated future operations, including further exploration, development activities and commencement of production on the Company’s properties, require permits from various national, provincial, territorial and local governmental authorities. In particular, the Company must obtain a water use licence and mining right for Project 1 and an environmental impact assessment must be completed there can be no absolute assurance that all licenses and permits which the Company requires for the construction of mining facilities and the conduct of mining operations will be obtainable on reasonable terms, or at all. Delays or a failure to obtain such licenses and permits, or a failure to comply with the terms of any such licenses and permits that the Company has obtained, could have a material adverse impact on the Company.

THE COMPANY IS SUBJECT TO THE RISK OF FLUCTUATIONS IN THE RELATIVE VALUES OF THE CANADIAN DOLLAR AS COMPARED TO THE SOUTH AFRICAN RAND AND THE UNITED STATES DOLLAR

The Company may be adversely affected by foreign currency fluctuations. The Company is primarily funded through equity investments into the Company denominated in Canadian Dollars. In the normal course of business the Company enters into transactions for the purchase of supplies and services denominated in South African Rand. The Company also has cash and certain liabilities denominated in South African Rand. Several of the Company’s options to acquire properties or surface rights in the Republic of South Africa may result in payments by the Company denominated in South African Rand or in U.S. Dollars. Exploration, development and administrative costs to be funded by the Company in South Africa will also be denominated in South African Rand. Fluctuations in the exchange rates between the Canadian Dollar and the South African Rand or U.S. Dollar may have an adverse or positive affect on the Company.

THE MINERAL EXPLORATION INDUSTRY IS EXTREMELY COMPETITIVE

The resource industry is intensely competitive in all of its phases, and the Company competes with many companies that possess greater financial resources and technical facilities. Competition could adversely affect the Company’s ability to acquire suitable new producing properties or prospects for exploration in the future. Competition could also affect the Company’s ability to raise financing to fund the exploration and development of its properties or to hire qualified personnel.

Platinum Group Metals Ltd. (Exploration and Development Stage Company) P.35

SUPPLEMENTARY INFORMATION AND MD&A

For the three and

twelve months ended August 31, 2011

SOUTH AFRICAN FOREIGN EXCHANGE CONTROLS MAY LIMIT REPATRIATION OF PROFITS

Loan capital or equity capital may be introduced into South Africa through a formal system of exchange control. Proceeds from the sale of assets in South Africa owned by a non-resident are remittable to the non-resident. Approved loan capital is generally remittable to a non-resident company from business profits. Dividends declared by a non-listed South African company are remittable to non-resident shareholders. However, there can be no assurance that restrictions on repatriation of earnings from the Republic of South Africa will not be imposed in the future.

JUDGMENTS BASED UPON THE CIVIL LIABILITY PROVISIONS OF THE UNITED STATES FEDERAL SECURITIES LAWS MAY BE DIFFICULT TO ENFORCE

The ability of investors to enforce judgments United States courts based upon the civil liability provisions of the United Statesof federal securities laws against the Company, its directors and officers, and the experts named herein may be limited due to the fact that the Company is incorporated outside of the United States, a majority of such directors, officers, and experts reside outside of the United States and their assets are located outside the United States. There is uncertainty as to whether foreign courts would: (i) enforce judgments of United States courts obtained against the Company or such person predicated upon the civil liability provisions of the United States federal securities laws, or (ii) entertain original actions brought in foreign courts against the Company or such persons predicated upon the federal securities laws of the United States, as such laws may conflict with foreign laws.

THE COMPANY IS SUBJECT TO SIGNIFICANT GOVERNMENTAL REGULATION

The Company’s operations and exploration and development activities in SouthAfrica and Canada are subject to extensive federal, state, provincial, territorial and local laws and regulation governing various matters, including:

- environmental protection;

- management and use of toxic substances and explosives;

- management of natural resources;

- exploration, development of mines, production and post-closure reclamation;

- exports;

- price controls;

- taxation;

- regulations concerning business dealings with local communities;

- labour standards and occupational health and safety, including mine safety; and

- historic and cultural preservation.

Failure to comply with applicable laws and regulations may result in civil or criminal fines or penalties or enforcement actions, including orders issued by regulatory or judicial authorities enjoining or curtailing operations or requiring corrective measures, installation of additional equipment or remedial actions, any of which could result in the Company incurring significant expenditures. The Company may also be required to compensate private parties suffering loss or damage by reason of a breach of such laws, regulations or permitting requirements. It is also possible that future laws and regulations, or a more stringent enforcement of current laws and regulations by governmental authorities, could cause additional expense, capital expenditures, restrictions on or suspensions of the Company’s operations and delays in the development of the Company’s properties.

THE COMPANY’S OPERATIONS ARE SUBJECT TO ENVIRONMENTAL LAWS AND REGULATION THAT MAY INCREASE THE COMPANY’S COSTS OF DOING BUSINESS AND RESTRICT ITS OPERATIONS

Environmental legislation on a global basis is evolving in a manner that will ensure stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessment of proposed development and a higher level of responsibility for companies and their officers, directors and employees. There can be no assurance that future changes to environmental legislation in Canada or South Africa will not adversely affect the Company’s operations. Environmental hazards may exist on the Company’s properties which are unknown at present and which have been caused by previous or existing owners or operators. Future compliance with environmental reclamation, closure and other requirements may involve significant costs and other liabilities. In particular, the Company’s operations and exploration activities are subject to Canadian and South African national and provincial laws and regulations governing protection of the environment. Such laws are continually changing and, in general, are becoming more restrictive.

P.36 Platinum Group Metals Ltd. (Exploration and Development Stage Company)

| SUPPLEMENTARY INFORMATION AND MD&A For the three and twelve months ended August 31, 2011 |

|

Amendments to current laws, regulations and permits governing operations and activities of mining companies, or more stringent implementation thereof, could have a material adverse impact on the Company and cause increases in capital expenditures or production costs or reduction in levels of production at producing properties or require abandonment or delays in development of new mining properties.

The Company has not made any material expenditure for environmental compliance to date. However, there can be no assurance that environmental laws will not give rise to significant financial obligations in the future and such obligations could have a material adverse effect on the Company’s financial performance.

MINING IS INHERENTLY DANGEROUS AND SUBJECT TO CONDITIONS OR EVENTS BEYOND THE COMPANY’S CONTROL, WHICH COULD HAVE A MATERIAL ADVERSE EFFECT ON THE COMPANY’S BUSINESS

In the course of exploration, development and production of mineral properties, certain risks, and in particular, unexpected or unusual geological operating conditions including rock bursts, cave-ins, fire, flooding and earthquakes may occur. It is not always possible to fully insure against such risks as a result of high premiums or other reasons. Should such liabilities arise, they could reduce or eliminate any future profitability and result in increasing costs and a decline in the value of the Company’s securities.

THE COMPANY HAS LIMITED EXPERIENCE WITH DEVELOPMENT-STAGE MINING OPERATIONS

Although there are personnel within the Company who have experience with development stage mining operations, the Company’s ability to place projects into production will be dependent upon using the services of both mining contractors and additional appropriately experienced personnel or entering into agreements with other major resource companies that can provide such expertise. There can be no assurance that the Company will have available the necessary expertise should the Company place a mineral property into production.

THE COMPANY HAS A HISTORY OF LOSSES AND IT ANTICIPATES CONTINUING TO INCUR LOSSES FOR THE FORESEEABLE FUTURE