Annual Information Form of Platinum Group Metals Ltd.

For year ended: August 31, 2011

Annual Information Form – Filed November 22, 2011

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Table of Contents

2

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Preliminary Notes

DATE OF INFORMATION

All information in this Annual Information Form (“AIF”) of Platinum Group Metals Ltd. (“Platinum Group” or the “Company”) is as of August 31, 2011 unless otherwise indicated.

GLOSSARY OF TERMS

Schedule “B” attached hereto contains a glossary of mining terms used in this AIF.

DOCUMENTS INCORPORATED BY REFERENCE

Incorporated by reference into this AIF are the Consolidated Audited Financial Statements of the Company for the year ended August 31, 2011 (the ”Financial Statements”) as filed on SEDAR on November 21, 2011, a copy of which may be obtained online from SEDAR at www.sedar.com.

Any statement contained in a document incorporated or deemed to be incorporated by reference herein shall be deemed to be modified or superseded for the purposes of this AIF to the extent that a statement contained in this AIF or in any subsequently filed document that also is or is deemed to be incorporated by reference herein modifies or supersedes such statement. Any statement so modified or superseded shall not constitute a part of this AIF, except as so modified or superseded. The modifying or superseding statement need not state that it has modified or superseded a prior statement or include any other information set forth in the document that it modifies or supersedes.

The making of such a modifying or superseding statement shall not be deemed an admission for any purpose that the modified or superseded statement, when made, constituted a misrepresentation, an untrue statement of a material fact or an omission to state a material fact that is required to be stated or that is necessary to make a statement not misleading in light of the circumstances in which it was made.

All financial information in this AIF is prepared in accordance with generally accepted accounting principles in Canada.

FORWARD LOOKING STATEMENTS

This AIF and the documents incorporated by reference herein contain “forward-looking statements” and forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable Canadian and US securities legislation. All statements, other than statements of historical fact, that address activities, events or developments that the Company believes, expects or anticipates will, may, could or might occur in the future, including without limitation, statements regarding estimates and/or assumptions in respect of production, revenue, cash flows and costs, estimated project economics, mineral resource and mineral reserve estimates, potential mineralization, potential mineral resources and mineral reserves, projected timing of possible production, the Company’s exploration and development plans and objectives with respect to its projects and the successful exercise of the Maseve Subscription Right (as defined herein) are forward-looking statements.

These forward-looking statements reflect the current expectations or beliefs of the Company based on information currently available to the Company. Forward-looking statements in respect of capital costs, operating costs, production rate, grade per tonne and smelter recovery are based upon the estimates in the Updated Feasibility Study and the forward-looking statements in respect of metal prices and exchange rate are based upon the three year trailing average prices and the assumptions contained in the Updated Feasibility Study.

Forward-looking statements are subject to a number of risks and uncertainties that may cause the actual events or results of the Company to differ materially from those discussed in the forward-looking statements, and even if such actual events or results were realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, the Company. Factors that could cause actual results or events of the Company to differ materially from current expectations include, among other things: metals price volatility; additional financing requirements; economic and political instability; the ability to obtain and maintain necessary permits; fluctuations in the relative values of the Canadian Dollar as compared to the South African Rand and the United States Dollar; property title risks including defective title to mineral claims or property; the mineral exploration industry is extremely competitive; South African foreign exchange controls may limit repatriation of profits; the Company’s designation as a “passive foreign investment company”; discrepancies between actual and estimated reserves and resources, between actual and estimated development and operating costs, between actual and estimated metallurgical recoveries and between estimated and actual production; changes in national and local government legislation, taxation, controls, regulations and political or economic developments in Canada, South Africa or other countries in which the Company does or may carry out business in the future; success of exploration activities and permitting time lines; the speculative nature of mineral exploration, development and mining, including the risks of obtaining necessary licenses and permits; exploration, development and mining risks and the inherently dangerous nature of the mining industry, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, mine collapses, cave-ins or flooding and the risk of inadequate insurance or inability to obtain insurance to cover these risks and other risks and uncertainties; the Company’s limited experience with development-stage mining operations; the Company has a history of losses; most of the Company’s properties contain no proven reserves; the ability of the Company to retain its key management employees; conflicts of interest; dilution through the exercise of outstanding options and warrants; share price volatility and no expectation of paying dividends; any disputes or disagreements with the Company’s joint venture partners; socio-economic instability in South Africa or regionally; the Company’s land in South Africa could be subject to land restitution claims; any adverse decision in respect of the Company’s prospecting or future mining rights and projects in South Africa; the introduction of South African State royalties where the Company’s current mineral reserves are located; and the other risks disclosed under the heading “Risk Factors” in this AIF.

3

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Any forward-looking statement speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking statement, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking statements are reasonable, forward-looking statements are not guarantees of future performance and accordingly undue reliance should not be put on such statements due to the inherent uncertainty therein.

CURRENCY AND EXCHANGE

All dollar amounts in this AIF are expressed in Canadian Dollars unless otherwise indicated. The Company’s accounts are maintained in Canadian Dollars. All references to “U.S. Dollars” or to “US$” are to U.S. Dollars. All references to “ZAR” or to “R” or to “Rand” are to South African Rand.

The following table sets forth the rate of exchange for the Canadian Dollar expressed in United States Dollars in effect at the end of the indicated periods, the average of exchange rates during such periods, and the high and low exchange rates during such periods based on the noon rate of exchange as reported by the Bank of Canada.

| Canadian Dollars

to U.S. Dollars |

Year Ended August 31 | |||

| 2011 | 2010 | 2009 | 2008 | |

| Rate at end of period | US$1.0221 | US$0.9399 | US$0.9118 | US$0.9411 |

| Average rate for period | US$1.0115 | US$0.9565 | US$0.8484 | US$0.9961 |

| High for period | US$1.0583 | US$0.9950 | US$0.9711 | US$1.0905 |

| Low for period | US$0.9506 | US$0.9244 | US$0.7653 | US$0.9365 |

The noon rate of exchange on November 21, 2011 as reported by the Bank of Canada for the conversion of Canadian Dollars into United States Dollars was Canadian $1.00 equals US$0.9629.

The following table sets forth the rate of exchange for the South African Rand, expressed in Canadian Dollars in effect at the end of the periods indicated, the average of exchange rates during such periods, and the high and low exchange rates during such periods based on the noon rate of exchange as reported by the Bank of Canada.

4

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

South African Rand to Canadian Dollars |

Year Ended August 31 | ||

| 2011 | 2010 | 2009 | |

| Rate at end of period | $0.1397 | $0.1443 | $0.1409 |

| Average rate for period | $0.1428 | $0.1393 | $0.1304 |

| High for period | $0.1510 | $0.1358 | $0.1108 |

| Low for period | $0.1352 | $0.1441 | $0.1502 |

The rate of exchange on November 21, 2011 as reported by the Bank of Canada for the conversion of South African Rand into Canadian Dollars was one South African Rand equals Canadian $0.1247.

METRIC EQUIVALENTS

For ease of reference, the following factors for converting Imperial measurements into metric equivalents are provided:

| To convert from Imperial | To metric | Multiply by |

| Acres | Hectares | 0.404686 |

| Feet | Metres | 0.30480 |

| Miles | Kilometres | 1.609344 |

| Tons | Tonnes | 0.907185 |

| Ounces (troy)/ton | Grams/Tonne | 34.2857 |

Terms used and not defined in this AIF that are defined in National Instrument 51-102 - Continuous Disclosure Obligations (“NI 51-102”) shall bear that definition. Other definitions are set out in National Instrument 14-101 Definitions, as amended.

CAUTIONARY NOTE TO UNITED STATES READERS – DIFFERENCES REGARDING THE DEFINITIONS OF RESOURCE AND RESERVE ESTIMATES IN THE UNITED STATES AND CANADA

Mineral Reserve

The definitions of “mineral reserves”, “proven mineral reserves” and “probable mineral reserves,” as used in this report, are Canadian mining terms as defined in accordance with National Instrument 43-101 -Standards of Disclosure for Mineral Projects (“NI 43-101”) under the guidelines set out in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Standards on Mineral Resources and Mineral Reserves Definitions and guidelines adopted by the CIM Council on August 20, 2000. CIM standards differ from the standards in the United States.

Under United States standards, a “mineral reserve” is defined as a part of a mineral deposit which could be economically and legally extracted or produced at the time the mineral reserve determination is made, where:

-

“reserve” means that part of a mineral deposit which can be economically and legally extracted or produced at the time of the reserve determination;

-

“economically” implies that profitable extraction or production has been established or analytically demonstrated to be viable and justifiable under reasonable investment and market assumptions; and

-

while “legally” does not imply that all permits needed for mining and processing have been obtained or that other legal issues have been completely resolved, for a reserve to exist, there should be a reasonable certainty based on applicable laws and regulations that issuance of permits or resolution of legal issues can be accomplished in a timely manner.

5

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Mineral reserves are categorized as follows on the basis of the degree of confidence in the estimate of the quantity and grade of the deposit.

Under United States standards, proven or measured reserves are defined as reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes, grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geographic character is so well defined that size, shape, depth and mineral content of reserves are well established.

Under United States standards, probable reserves are defined as reserves for which quantity and grade and/or quality are computed from information similar to that of proven reserves (under United States standards), but the sites for inspection, sampling, and measurement are further apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven mineral reserves, is high enough to assume continuity between points of observation.

Mineral Resource

While the terms “mineral resource,” “measured mineral resource,” “indicated mineral resource,” and “inferred mineral resource” are recognized and required by Canadian regulations, they are not defined terms under standards in the United States. As such, information contained in this report concerning descriptions of mineralization and resources under Canadian standards may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements of the United States Securities and Exchange Commission (“SEC”). “Indicated mineral resource” and “inferred mineral resource” have a great amount of uncertainty as to their existence and a great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an “indicated mineral resource” or “inferred mineral resource” will ever be upgraded to a higher category. Investors are cautioned not to assume that any part or all of mineral deposits in these categories will ever be converted into reserves .

Corporate Structure

The Company is a British Columbia corporation amalgamated on February 18, 2002 pursuant to an order of the Supreme Court of British Columbia approving an amalgamation between Platinum Group Metals Ltd. and New Millennium Metals Corporation. On January 25, 2005, the Company was transitioned under the Business Corporations Act (British Columbia). On February 22, 2005, the Company’s shareholders passed a special resolution to amend the authorized share capital from 1,000,000,000 common shares without par value (“Common Shares”) to an unlimited number of common shares without par value, to remove the Pre-existing Company Provisions and to adopt new articles.

| The Company’s head office is located at: | |

| 328 – 550 Burrard Street | |

| Vancouver, British Columbia | |

| Canada, V6C 2B5 | |

| The Company’s registered office is located at: | |

| Gowling Lafleur Henderson LLP | |

| 2300 - 550 Burrard Street | |

| Vancouver, British Columbia | |

| Canada, V6C 2B5 | |

6

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

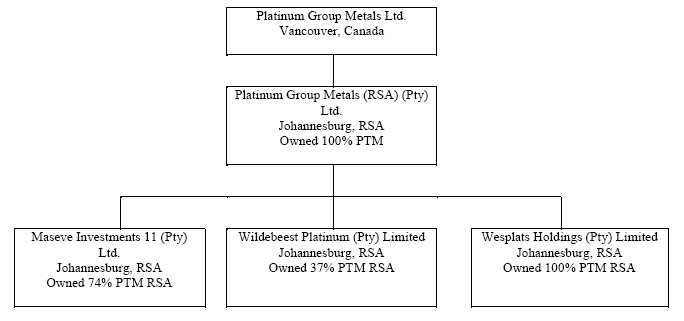

PLATINUM GROUP METALS AND ITS PRINCIPAL SUBSIDIARIES

The Company has two wholly-owned subsidiaries, one majority-owned subsidiary and a 37% holding in a fourth company, all of which are incorporated under the company laws of The Republic of South Africa. The Company also has a 100% owned subsidiary, Platinum Group Metals (Barbados) Ltd., incorporated under the laws of Barbados, which is currently inactive and not material to the affairs of the Company.

The Company conducts its South African exploration and development work through its wholly-owned direct subsidiary, Platinum Group Metals (RSA) (Proprietary) Limited (“PTM RSA”). PTM RSA holds the Company’s interests in Project 1 and Project 3 of what was formerly the Western Bushveld Joint Venture (the “WBJV”) through its majority 74% holdings in Maseve Investments 11 (Pty) Limited (“Maseve”). See details below “Projects 1 and 3 of the Western Bushveld Complex”

PTM RSA also holds 100% of the shares of a company named Wesplats Holding (Proprietary) Limited (“Wesplats”), a holding company set up to acquire surface rights over Project 1, and a 37% interest in Wildebeest Platinum (Pty) Limited (“Wildebeest”), a company set up to hold prospecting permits for the exploration joint venture between the Company and Sable Platinum (Pty) Ltd. (“Sable”).

The registered and records offices of PTM RSA, Maseve, Wesplats and Wildebeest are located at 4th Floor, Aloe Grove, 196 Louis Botha Avenue, Houghton Estate, Johannesburg, 2000, Gauteng Province, Republic of South Africa. The principal business address of PTM RSA is Technology House, Greenacres Office Park, Victory Park, Johannesburg 2193, Gauteng Province, South Africa.

General Development of the Business

Since its formation in 2002, the Company has been engaged in the acquisition, exploration and development of Platinum properties with interests in the western and northern limbs of the Bushveld Complex in South Africa and in Ontario, Canada. Currently, the Company’s primary focus is bringing its Project 1 Platinum Mine located in the Western Bushveld Complex of South Africa into production.

Three Year History

The following is a timeline summarizing the Company’s activities over the last three years:

7

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

| May 2008 |

The Company purchased surface rights adjacent to the east of the Project 1 deposit area measuring 216.27 hectares. |

Page 19 |

| May 2008 |

The Company purchased additional surface rights directly over a portion of the Project 1 deposit area measuring 358.79 hectares. |

Page 19 |

| July 2008 |

The Company published a Feasibility Study and revised resource estimation for the Project 1 area of the WBJV. |

Page 35 |

| September 2008 |

The Company announced that the parties of the WBJV entered into an agreement, subject to formal documentation and conditions precedent, to consolidate and rationalize the ownership of the mineral rights held by the WBJV. |

Page 13 |

| December 2008 |

On December 9, 2008, the Company announced the execution of definitive agreements (the “Consolidation Agreements”) by Anglo Platinum Limited (“Anglo”) and Wesizwe Platinum Limited (“Wesizwe”) to consolidate and rationalize the ownership of the mineral rights held by the WBJV (the “Consolidation Transaction”). The Consolidation Agreements were completed on April 22, 2010. |

Page 13 |

| March 2009 |

The Company entered into an option agreement with Japan Oil, Gas and Metals National Corporation (“JOGMEC”) whereby JOGMEC may earn 35% (one-half of the Company’s interest) of the War Springs Project. |

Page 38 |

| September 2009 |

The Company was granted prospecting rights for a 118 square kilometre area named the Waterberg Project north of the known North Limb of the Bushveld Complex. |

Page 38 |

| October 2009 |

The Company entered into an agreement with JOGMEC and empowerment company Mnombo Wethu Consultants CC (“Mnombo”) whereby JOGMEC may earn up to a 37% interest in the Waterberg project and Mnombo may earn a 26% interest. |

Page 39 |

| October 2009 |

The Company published the Updated Feasibility Study and revised resource estimate for the Project 1 area of the WBJV. |

Page 32 |

| April 2010 |

The Company paid an equalization amount due to Anglo of R 186.28 million (approximately $24.83 million at the time), including interest charges, as required under the terms of the original WBJV Agreement. |

Page 13 |

| April 2010 |

On April 22, 2010, the Consolidation Transaction was completed and the WBJV was dissolved. The mineral rights underlying Project 1 and 3 were transferred into project operating company, Maseve. Wesizwe received a 45.25% initial interest in Maseve in exchange for the mineral rights it transferred to Maseve and the Company owned the remaining 54.75%. Under the terms of the Consolidation Agreements, the Company acquired the right to subscribe for a further 19.25% interest in Maseve (the “Maseve Subscription Right”). Company exercised the Maseve Subscription Right in January 2011. See “Acquisition and Reorganization – Project 1 and 3”. |

Page 13 |

| August 2010 |

The Company purchased surface rights covering 1,713 hectares overlaying the area of Project 1 for R 130.0 million (approximately $18.80 million). |

Page 19 |

| October 2010 |

The Company raised gross proceeds of $143.81 million on the issue of 70.15 million shares. The net proceeds were approximately $135.6 million after deducting the underwriters’ fee of $7.91 million and expenses of the offering of $0.3 million. |

Page 10 |

8

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

| December 2010 |

The Company appointed DRA Mining Pty Ltd. (“DRA”) as Engineering, Procurement, Construction and Management (“EPCM”) contractor for surface infrastructure and underground development at Project 1. |

Page 14 |

| January 2011 |

On January 14, 2011, the Company exercised its Maseve Subscription Right and acquired a further 19.25% interest in Maseve for subscriptions in the amount of approximately $59 million (R 408.81 million), thereby increasing its shareholding to 74%. |

Page 13 |

| February 2011 |

The Company acquired a right to earn up to a 75% interest (the “Bark Lake Option”) in Benton Resources Corp’s ("Benton"), Bark Lake platinum-palladium project, comprised of 19 mineral claims located west of Thunder Bay, Ontario. The Company stakes additional claims near Thunder Bay and commences exploration programs and drilling in the region. |

Page 39 |

| March 2011 |

The Company received a positive record of decision from the Department of Mineral Resources of the Government of South Africa (“DMR”) for the detailed underground development plans and environmental management program, including the taking of a bulk sample. |

Page 14 |

| May 2011 |

The Company commenced the Phase 1 civil construction work at Project 1 (“Phase 1.”) |

Page 14 |

| July 2011 |

The Company awarded the contract to develop the Phase 1 underground decline tunnels at Project 1 to JIC Mining Services (“JIC”) of Johannesburg, South Africa. |

Page 14 |

| August 2011 |

The Company acquired 100% ownership in the Providence Lake Nickel (Ni)-Copper (Cu)-Platinum Group Elements (PGE) property located in the Northwest territories, Canada. |

Page 39 |

| August 2011 |

The Company entered into a mandate letter with Barclays Capital, the investment banking division of Barclays Bank PLC (together with its affiliate Absa Capital, the corporate & investment banking division of Absa Bank Limited), The Standard Bank of South Africa Limited, West LB AG and Caterpillar Financial SARL for a US $260 million project finance loan to develop the Project 1 Platinum Mine. The proposal has preliminary credit committee approval from each of the proposed lenders, but is subject to certain legal and technical due diligence, final credit approval and execution of a formal loan agreement. Completion of due diligence and the documentation is currently in process. |

Page 10 |

Description of the Company’s Business

General

The Company’s business is conducted primarily in South Africa, and to a lesser extent, in Ontario and the Northwest Territories in Canada. The Company’s flagship, Project 1, in the Western Bushveld Complex of South Africa, is currently in development. The proceeds from the October 2010 Financing were utilized to execute the initial Phase 1 development and bulk sample program, including beginning to sink twin declines into the central part of the Project 1 deposit. Phase 1 is budgeted at USD $100 million. The Company is in the process of obtaining further financing to continue the development of Project 1. Phase 1 is approximately 55% to 60% complete with estimated completion by late calendar 2012. Subject to the grant of a final mining right from the Government of South Africa, once funding from both debt and equity sources is complete, the Company plans to commence Phase 2, including an additional southern decline access to the deposit and a milling, concentrating and tailings facility. Plant and facility construction and commissioning are estimated to take two years to complete. First production is currently projected to occur in late mid-2014. Full commercial production is estimated to occur after a two to three year ramp up period subsequent to the commissioning of the plant.

9

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

The Company also holds interests in various early stage exploration projects located in Canada and in South Africa. The Company continues to evaluate exploration opportunities both on currently owned properties and on new prospects. Details of these projects may be found in the “Mineral Property Interests” section below and in Note 6 of the Financial Statements.

To conduct its exploration and development, the Company is dependent on sub-contractors for certain construction, engineering, geological services, drilling equipment and supplies. These are generally available but vary in price and immediacy of availability subject to demand. For recent development regarding key personnel and contractors for Project 1 see “Recent Development – Project 1”

At present the Company has no debt other than trade payables in the normal course. The Company holds its cash at a major Canadian chartered bank, a major London Bank or with a major South African bank in current accounts and interest bearing deposits. The Company currently owns no marketable securities.

Recent Financing

In October 2010, the Company raised gross proceeds of $143.81 million on the issue of 70.15 million shares on a bought deal basis. The net proceeds received by the Company from the offering were approximately $135.6 million (determined after deducting the underwriters’ fee of $7.91 million and estimated expenses of the offering of $300,000). The Company’s 2009 Updated Feasibility Study estimates the total capital cost to build the Project 1 Platinum Mine at US$443 million (at 8.0 Rand to the USD). The net proceeds of the offering allowed the Company to initiate development, but further financing will be required to complete the project, likely from a combination of debt financing and the issuance of additional equity.

The Company entered into a mandate letter with Barclays Capital, the investment banking division of Barclays Bank PLC (together with its affiliate Absa Capital, the corporate & investment banking division of Absa Bank Limited), The Standard Bank of South Africa Limited, West LB AG and Caterpillar Financial SARL for a US $260 million project finance loan to develop the Project 1 Platinum Mine. The proposal has preliminary credit committee approval from each of the proposed lenders, but is subject to certain legal and technical due diligence, final credit approval and execution of a formal loan agreement. Completion of due diligence and the documentation is currently in process. Draw down on the facility would be subject to certain conditions, including the completion of a concentrate off take agreement and the grant of a final mining authorization for Project 1 by the DMR. Based on the current timelines to completion of documentation, hedging facilities, off take agreements, updated implementation engineering and the grant of a final mining right, the Company now anticipates that completion of formal loan arrangements will occur in Q1 and Q2 of calendar 2012.

Platinum and Palladium Trends

-

The platinum market was close to balance in 2010, with a surplus of just 20,000 oz. Supplies remained almost flat at 6.06 million ounces, while gross demand increased by 16% to 7.88 million ounces. Recycling of platinum increased by almost a third to 1.84 million ounces.

-

Gross demand for platinum in autocatalysts increased by 43% to 3.13 million ounces in 2010 as the global automotive sector bounced back from a poor 2009. Increased vehicle production in Europe in particular benefited platinum.

-

Gross industrial demand for platinum increased by 48% to 1.69 million ounces in 2010, led by growth in the glass and chemical sectors.

-

Gross demand for platinum from the jewelry sector fell by 14% to 2.42 million ounces in 2010 mainly due to softer Chinese demand. Purchasing of platinum by the jewelry industry in other regions remained fairly stable.

-

Identifiable physical investment demand for platinum remained almost flat in 2010 at 650,000 oz.

10

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

-

The palladium market was in a fundamental deficit of 490,000 oz in 2010. Supplies of palladium increased by a modest 3% to 7.29 million ounces. Gross demand increased by 23% to 9.63 million ounces, its highest ever level. Recycling of palladium increased by 29% to 1.85 million ounces.

-

A strongly performing automotive sector in all regions pushed up gross demand for palladium in autocatalysts by 35% to 5.45 million ounces in 2010.

-

Gross industrial demand for palladium increased by 70,000 oz in 2010 to 2.47 million ounces. Gross palladium demand in the jewelry sector softened by 20% in 2010 to 620,000 oz.

-

Net identifiable physical investment demand for palladium increased by a remarkable 74% in 2010 due to strong demand for various palladium exchange traded funds (ETFs).

Employees

As at August 31, 2011, the Company’s complement of staff, consultants and casual workers in both Canada and South Africa consists of approximately 30 individuals. A further six people have been appointed as the owner’s team for the Project 1 Platinum Mine in South Africa. EPCM provider, DRA has assigned approximately 30 people to the project. Civil and underground mining contractors currently have approximately 300 people working on site at Project 1. Of these 300 people more than 30% are people from the local community surrounding Project 1.

Specialized Skills and Knowledge

Due to the specialized skills and knowledge required for a company in the development phase and moving into the production phase, the Company has contracted the services of Requisite Business Solutions (“RBS”), an experienced and professional Human Resources Company, to provide services to both the site and office for Project 1. These services include human resources, organization design and human resource planning services. For recent development regarding key personnel and contractors for Project 1 see “Recent Development – Project 1”.

Competition

The global platinum group metals (“PGM”) mining industry is characterised by long term rising demand from global automotive and fabrication sectors on one hand and constrained supply sources on the other. South Africa’s PGM mining sector is the largest and fastest growing sector in the South African mining industry, representing approximately 80% of global supply. Almost all of the South African platinum supply comes from the geographic constraints of the Western and Eastern Limbs of the Bushveld Igneous Complex, resulting in a high degree of competition for mineral rights and projects. Notwithstanding its geographic superiority, the South African sector remains beholden to economic developments in the global automotive industry which accounts for approximately 50% of the total global demand for platinum. A prolonged downturn in global automobile and light truck sales, resulting in depressed platinum prices, often results in declining production as unprofitable mines are shut down. Alternatively, strong automobile and light truck sales combined with strong fabrication demand for platinum, most often results in a more robust industry, creating competition for resources, including funding, labour, technical experts, power, water, materials and equipment. The South African industry is dominated by three or four producers, who also control smelting and refining facilities. As a result there is general competition for access to these facilities on a contract basis. As the Company moves towards production from its Project 1 it will become exposed to many of the risks of competition as outlined herein and as set out below. See further discussion in “Risk Factors” below.

Environmental Compliance

The Company’s current and future exploration and development activities, as well as future mining and processing operations, if warranted, are subject to various federal, state and local laws and regulations in the countries in which the Company conducts its activities. These laws and regulations govern the protection of the environment, prospecting, development, production, taxes, labour standards, occupational health, mine safety, toxic substances and other matters. Company management expects to be able to comply with those laws and does not believe that compliance will have a material adverse effect on the Company’s competitive position. The Company intends to obtain all licenses and permits required by all applicable regulatory agencies in connection with our mining operations and exploration activities. The Company intends to maintain standards of compliance consistent with contemporary industry practice.

11

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Foreign Operations

The Company conducts the majority of its business in South Africa. South Africa has a large and well-developed mining industry, particularly in the area where the Project 1 is located. This, among other factors, means the infrastructure in the area is well established, with well-maintained roads and highways as well as electricity distribution networks, water supply and telephone systems. There is also excellent access to materials and skilled labour in the region, due to the existence of many platinum and chrome mines in the immediate vicinity. Smelter complexes and refining facilities are also located in the area. South Africa has a well-established government, police force and judiciary as well as financial, health care and social institutions. The system of mineral tenure was overhauled by new legislation in 2002. Since the fall of Apartheid and the free elections of 1994, South Africa is considered an emerging democracy. For a discussion of risks associated with operating in South Africa, please see “Risk Factors” below.

Mineral Property Interests

Under Canadian GAAP, the Company defers all acquisition, exploration and development costs related to mineral properties. The recoverability of these amounts is dependent upon the existence of economically recoverable reserves, the ability of the Company to obtain the necessary financing to complete the development of the property, and any future profitable production; or alternatively upon the Company’s ability to dispose of its interests on an advantageous basis.

Projects 1 and 3 of the Western Bushveld Complex

Readers are encouraged to read the following technical reports, from which the disclosure in this section has been derived:

| 1. |

Technical report dated August 31, 2010 entitled “Technical Report on Project 3 Resource Cut Estimation of the Western Bushveld Joint Venture (WBJV) Located on the Western Limb of the Bushveld Igneous Complex, South Africa” (the “Project 3 Report”), filed on SEDAR October 5, 2010; | |

| 2. |

Technical report dated November 20, 2009 entitled “Updated Technical Report (Updated Feasibility Study) Western Bushveld Joint Venture (Elandsfontein and Frischgewaagd)” (the “Updated Feasibility Study”), filed on SEDAR November 25, 2009; | |

| 3. |

Technical report dated November 20, 2009 entitled “An Independent Technical Report on Project Areas 1 and 1A of the Western Bushveld Joint Venture (WBJV) Located on the Western Limb of the Bushveld Igneous Complex, South Africa (the “Project 1 Report”) filed on SEDAR November 24, 2009; |

Acquisition and Reorganization– Project 1 and 3

On October 26, 2004, the Company entered into a joint venture agreement (the “WBJV Agreement”) forming the WBJV with Anglo and Africa Wide Mineral Prospecting and Exploration (Pty) Limited (“Africa Wide”) in relation to a platinum exploration and development project on combined mineral rights covering approximately 67 square kilometers on the Western Bushveld Complex of South Africa. In April 2007, Anglo contributed a further 5 square kilometer area into the WBJV. The WBJV was divided into three distinct project areas, namely Projects 1, 2 and 3. The ownership interests of the WBJV were originally structured as 37% by Rustenburg Platinum Mines Ltd. (“RPM”), a subsidiary of Anglo; 26% by Africa Wide (which was acquired in 2007 by Johannesburg Stock Exchange listed Black Economic Empowerment company, Wesizwe Platinum (Pty) Ltd. (“Wesizwe”)); and 37% by PTM RSA. PTM -RSA was the operator of the joint venture.

Under the terms of the original WBJV Agreement, upon a decision to mine, the respective deemed capital contribution of each party would be credited a dollar amount, based on their contribution of measured, indicated and inferred PGM ounces from the contributed properties comprising the WBJV. The ounces contributed would be determined based upon, and at the time of, the first bankable feasibility study for the WBJV, in accordance with the South African SAMREC Code and agreed amongst the parties on a “Determination Date” as defined in the WBJV agreement.

12

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

On September 2, 2008, the Company announced that the parties to the WBJV had agreed to terms with respect to the Consolidation Transaction and on December 9, 2008, the Company announced it had executed the definitive Consolidation agreements in this regard.

On April 22, 2010, the Company paid an equalization amount due to Anglo of R 186.28 million (approximately $24.83 million at the time), including interest charges, as required under the terms of the original WBJV Agreement.

On April 22, 2010, the Consolidation Transaction was completed and the WBJV was dissolved. The parties had agreed that upon dissolution the equalization due under the original WBJV Agreement would be paid and settled between the parties. At the moment of dissolution, Wesizwe acquired all of Anglo’s rights and interests to the mineral rights underlying the WBJV, retained Anglo’s mineral rights to Project 2, and transferred all of Anglo’s mineral rights underlying Projects 1 and 3 into project operating company, Maseve. The Company also transferred its mineral rights underlying Project 1 into Maseve, the result being that Wesizwe retained 100% of Project 2 and Maseve obtained 100% of Projects 1 and 3. The combined area covered by the mineral rights for Projects 1 and 3 held through Maseve, comprises approximately 53 square kilometres.

Although the Company did not hold any of the mineral rights comprising Project 2, the Company had an 18.5% interest in Project 2 through the WBJV. In exchange for rescinding its 18.5% of Project 2, the Company effectively received a 17.75% interest in Maseve. For accounting purposes under Canadian GAAP, this was treated as a deemed sale of 18.5% of Project 2 and was valued at estimated fair market value of $65.42 million, resulting in an accounting gain of $45.62 million. For accounting purposes, the Company has also accrued a deferred income tax liability of $22.5 million in relation to the deemed sale. This is a non-cash accrual for accounting purposes only, as the Company and its advisors have determined the deemed transaction is not a taxable event under the Income Tax Act of South Africa.

The Company also received a 37% interest in Maseve in exchange for its share of Projects 1 and 3, bringing its holdings in Maseve to 54.75% . This part of the transaction was treated as a transfer of a business interest between controlled entities and was transferred at cost for accounting purposes. Wesizwe received a 45.25% initial interest in Maseve in exchange for the mineral rights it transferred to Maseve.

Under the terms of the Consolidation Agreements, the Company acquired the Maseve Subscription Right entitling it to subscribe for a further 19.25% interest in Maseve, from treasury, in exchange for a subscription amount of R 408.81 million. This right had to be exercised and funded within 270 days of the closing of the Consolidation Transaction, which occurred on April 22, 2010. This subscription would take the Company’s interest in Maseve to 74%.

Under the terms of the Consolidation Agreement, Anglo will hold a 60 day first right of refusal on the sale of ore or concentrate over the original WBJV mineral rights.

On January 14, 2011, the Company exercised the Maseve Subscription Right in the amount of approximately. $59 million (R 408.81 million), thereby increasing its shareholding in Maseve to 74%. The subscription funds are held in escrow for application towards Wesizwe’s 26% share of expenditures for Projects 1 and 3 (the “Escrowed Maseve Funds.”)

Recent Developments – Project 1

Upon completion of the October 2010 Financing, the Company approved and initiated the Phase 1 development and bulk sample program for the sinking of a twin decline into the central part of the Project 1 deposit. The Phase 1 program was budgeted at approximately $100 million, of which the Company will contribute $74 million and $26 million will be drawn down from the escrowed Maseve Funds held for Wesizwe’s share of costs. On November 21, 2011, the Company held remaining cash on hand, including earned interest, in escrow for Wesizwe of approximately R 259 million ($32.5 million).

13

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

In October 2010, the Company appointed Mr. Thys Uys, a Professional Engineer with more than 21 years of management experience in project feasibility and implementation in South Africa, as the Company’s representative and project manager for development of Project 1. An owner’s team consisting of people who have previously worked with Mr. Uys on large scale mining construction projects has also been appointed, including a dedicated quantity surveyor for cost engineering services, contract and capital control administrators and a permitting consultant responsible for the Company’s Environmental Impact Assessment and Management Plan.

In December 2010, the Company appointed DRA as EPCM contractor for surface infrastructure and underground development. DRA has assigned approximately 30 full time professionals to oversee and plan the execution of the development of surface infrastructure, power delivery, water delivery, civil works and excavations and the development of underground tunnels to access ore during Phase 1 construction. DRA’s scope of work includes engineering, design, construction management, administration and cost and schedule control.

In late March 2011, the Company received a positive record of decision from the DMR for its detailed underground development plans and environmental management program, including the taking of a bulk sample. The consent of the DMR requires compliance with underlying regulations related to health, safety and environment. The final mining right application and social and labour program for Project 1 was filed in April 2011 and was later accepted for processing by the DMR. Application in terms of the National Environmental Management Act (NEMA) was also accepted by the DMR. An update to the public participation process, including project publication, placement of notices and public meetings with local government and interested and affected parties is underway.

During February, March and April 2011, the Company conducted approximately 16,850 metres of infill drilling on the near surface portions of the Project 1 platinum deposit in order to gain more detailed information for metallurgical, geotechnical, mine planning and scheduling purposes. As a result of this work, refinements to the scheduled mining during the first three or four years of the planned Project 1 mine life of both UG2 and Merensky Reef tonnage, are currently being modeled and implemented. New geo-statistical information and ongoing mine design parameters resulting from recent infill borehole data, combined with the modified modeling, mine construction steps and scheduling being completed at the time of writing, could result in changes to the reported reserves and resources for Project 1. During the execution of the development plan, changes to the estimated capital cost for the development of the Project 1 Platinum Mine may occur.

Civil construction for Phase 1 began in May 2011, with the mobilization of civil contractor Wilson Bailey Holmes (“WBH”), who is responsible for major surface infrastructure excavation and construction. An expenditure for civil construction of R 23.62 million (approximately $3.3 million) has been incurred to August 31, 2011 from a commitment of R35.6 million (approximately $5.09 million). The box cut excavation was completed in mid-September. WBH executed the first undercut blasts to commence underground development in October. WBH remains on site and is currently working to complete surface infrastructure.

In July 2011, the Company awarded JIC the contract to develop the twin 1,200 meter underground decline tunnels into the center of the Project 1 platinum deposit. JIC took over underground development from WBH in mid-October. JIC is operating as one of the underground mining contractors at the producing Bafokeng Rasimone Platinum Mine immediately adjacent to the Project 1 and currently operates as underground mining contractor on another six platinum mines and one chrome mine in South Africa, employing 7,200 people. JIC has a good safety record and has invested in an accredited training facility near to Project 1. Total primary underground development cost for Phase 1 based on the JIC contract is estimated at R 206.85 million (approximately $28.90 million on August 31, 2011), resulting in an estimated cost per unit for underground development below the estimate in the Updated Feasibility Study. An initial pre-payment of R 25.0 million (approximately $3.55 million on July 11, 2011) was released to JIC after JIC provided an appropriate form of performance guarantee. A further retention amount of R 20.69 million ($2.94 million on July 11, 2011) was released to JIC approximately ten days later. JIC will be paid according to progress invoicing as work is completed over approximately seventeen months. Phase 1 is currently about 55% to 60% complete, is on budget, with approximately $52.0 million incurred to date, and within approximately 10 to 12 weeks of being on time.

14

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Ancillary servicing for the site including, buildings, piping, cabling, fencing and security have been initiated for a commitment of approximately R14.4 million (approximately $2.06 million.) A temporary power supply of 1.5MVa has been installed on site and has been energized. A 10 MVa supply line is slated for completion and connection in 2012. Permanent power service for the remaining 30 MVa is being designed and engineered by Eskom to be supplied in 2013. The Company has paid Eskom R 51.71 million ($7.22 million at August 31, 2011) of an R 142.22 million (approximately $20.32 million) commitment for delivery of power.

The company has entered into an agreement with regional water supplier, Magalies, for a temporary 0.5 ML/day water supply and have expended R 2.0 million (approximately $0.29 million). The construction of this supply is complete. The agreement for permanent water supply of 6 ML/day is being finalized and service is slated to be provided by 2013.

The Company has purchased an owner-controlled “Wrap-Around Liability” insurance policy covering contractors and sub-contractors on the Project 1 work site for the duration of all construction phases until plant completion and commercial production. The Wrap-Around policy provides coverage for up to USD $25.0 million of liability per incident, subject to industry standard terms, conditions and deductibles. The Company has also purchased “Course of Construction” insurance for Project 1 to cover up to R 630 million in property value in the event of loss or damage during all construction phases, once again subject to industry standard terms, conditions and deductibles. The estimated cost for approximately three years of coverage for the above two policies is approximately $440,000. Additional insurance will still be required once Phase 2 construction commences and for mine operation. During 2011, the Company completed a comprehensive risk assessment for Project 1 with the assistance of an international insurance broking firm.

The Company has contracted the services of an experienced and professional HR company, RBS, to provide site and office human resources, organization design and planning services to Project 1. RBS specializes in the mining industry, and their team of Professional Engineers, Psychologists and Practitioners has an intimate understanding of organization design & development, including knowledge of the applied legislation, mining techniques and associated labour practices. RBS has assisted the Company to complete a Local Skills Assessment in six communities to help identify candidates for leadership and staff positions as per the Company’s Social and Labour Plan and Human Resources Development obligations. Community members have already been hired and more are currently undergoing medicals, training and induction.

Project Description and Location

The approximately 53 square kilometres of mineral rights comprising Projects 1 and 3 are owned 100% by project operating company Maseve. PTM RSA owns 74% of Maseve while Wesizwe owns the remaining 26%. Maseve is operated by PTM RSA in accordance with the terms of a shareholders’ agreement (the “Maseve Shareholder’s Agreement.”) The property is divided into two distinct project areas, namely Projects 1 and 3. Project “1A” as discussed below is simply a subdivision of Project 1.

Projects 1 and 3 are located on the south-western limb of the Bushveld Igneous Complex (“BIC”), 110km west-northwest of Pretoria and 120km from Johannesburg. The BIC is unique and well known for its layering and continuity of economic horizons mined for platinum, palladium and other platinum group elements (“PGEs”), chrome and vanadium.

15

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

![]()

The total area includes portions of the Company’s properties, namely Elandsfontein 102JQ, Mimosa 81JQ and Onderstepoort 98JQ, and also certain portions of Elandsfontein 102JQ, Onderstepoort 98JQ, Frischgewaagd 96JQ, Mimosa 81JQ and Koedoesfontein 94JQ originally contributed by RPM. These properties are centred on Longitude 27o 00’ 00’’ (E) and Latitude 25o 20’ 00’’ (S) and the mineral rights now cover approximately 53km2 or 5,300ha.

Project Area 1 and 1A covers an area of 10.87km 2 or 1,087ha in extent. Specifically, Project Area 1 and 1A consist of a section of Portion (“Ptn”) 18, the Remaining Extent (“Re”), Ptn 13, Ptn 8, Re of Ptn 2, Ptn 7, Ptn 15 and Ptn 16 of the farm Frischgewaagd 96JQ, sections of Ptn 2, Ptn 9 and Ptn 12 of the farm Elandsfontein 102JQ and a small section of the Re of the farm Mimosa 81JQ. Project Area 3 covers an area of 224.28ha in extent and is located on a section of the farm Koedoesfontein 94JQ.

16

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

![]()

The resources of Project Area 1 and 1A are located approximately 1km to 6km along strike from the active Merensky Reef (sometimes referred to as “MR”) mining face at the operating Bafokeng Rasimone Platinum Mine (“BRPM”). BRPM completed opencast mining on the Upper Group 2 (“UG2”) Reef within 100m of the property boundary.

The potential economic horizons in Project Area 1 and 1A are the Merensky Reef and UG2 Chromitite seam situated in the Critical Zone (“CZ”) of the Rustenburg Layered Suite (“RLS”) of the BIC; these horizons are known for their continuity. The Merensky Reef and UG2 Chromitite seam are mined at the BRPM adjoining the property as well as on other contiguous platinum-mine properties. In general, the layered package dips at less than 20 degrees and local variations in the reef attitude have been modeled. The Merensky Reef and UG2 Chromitite seam, in the Project Area, dip between 4 and 42 degrees, with an average dip of 14 degrees.

17

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Drilling, in the form of diamond drilling, has been carried out over the Project Area and to-date 231 boreholes have been drilled for the purposes of understanding the geology, structure and metallurgy of the ore body in the Project Area. PTM RSA has established a site office to the south of the Project Area, and all core is stored in the core yard on site. All logging and sampling of the core is undertaken at the site office core yard and the samples have been sent to Genanalysis (Perth), ALS Chemex (South Africa) and currently samples are sent to Set Point Laboratories (South Africa). To the time of the Updated Feasibility Study in October 2009, a total of 32,020 samples had been assayed and utilised in the estimation of the Mineral Resources over the Project Area.

Licences

The Consolidation Transaction was subject to ministerial approval of the cession of various prospecting rights in accordance with the provisions of section 11 South Africa’s Mineral and Petroleum Resources Development Act 2002 (“MPRDA”). The required cession of the prospecting rights was duly approved by the Minister of Mineral Resources on April 22, 2010. The result of the ministerial approval of the cessions was that the prospecting rights would be grouped into 3 projects referred as Project 1, Project 2 and Project 3. The prospecting rights in respect of Project 2 were ceded to Bakubung Minerals (Proprietary) Limited, a subsidiary of Wesizwe. The prospecting rights in respect of Project 1 and Project 3 were ceded to Maseve.

As a result of the transaction Maseve now holds 9 separate new order prospecting rights which are recorded below as follows:

| 1. |

Elandsfontein 102 JQ - |

DMR 18 PR - Portion 12, Remaining Extent of Portion 1 and Remaining Extent of Portion 14. |

| 2. |

Elandsfontein 102 JQ– |

DMR 1274 PR – Portions 8 and 9 |

| 3. |

Onderstepoort 98 JQ - |

DMR 1327 PR – Portions 4, 5 and 6 |

| 4. |

Onderstepoort 98 JQ - |

DMR 1328 PR –Portions 3 and 8. |

| 5. |

Onderstepoort 98 JQ - |

DMR 19 PR - Portions 14 and 15 |

| 6. |

Onderstepoort 98 JQ - |

DMR 558 PR - Portions Portion 9 –Mineral Area 1 Ruston 97 JQ (Now Mimosa 81) and Mineral Area 2 Ruston 97 (Now Mimosa 81) |

| 7. |

Frischgewaagd 98 JQ - |

DMR 1109 PR- Remaining Extent-Remaining Extent of Portion 2-Remaining Extent of Portion 6,Portions 7,8,13,15,16 and 18. Remaining Extent of Portion 2 (Former Mineral Area 2) |

| 8. |

Koedoesfontein 94 JQ - |

DMR 1264 PR - Portion of the farm Koedoesfontein. |

| 9. |

Koedoesfontein 94 JQ - |

DMR 1682 PR - Portion of the farm Koedoesfontein. |

The prospecting rights for PGMs, nickel, chrome and gold are all current and are held in the Regional Office of the Department of Mineral Resources in Klerksdorp, North West Province. Licence specifications for these prospecting permits may be found in the technical reports filed on SEDAR as detailed above under the heading “Project 1 and 3 of the Western Bushveld Complex”. Under the MPRDA, the holders of valid new order prospecting permits have the exclusive right to apply for transition of such prospecting rights into mining rights.

Rights to Surface and Minerals

The Company has acquired all surface rights it believes will be necessary to execute construction and operation of the Project 1 Platinum Mine. These surface rights are intended for purposes of tailings placements, surface infrastructure, location of shaft infrastructure, mill facilities, concentrator facilities and waste sites. Details of acquisition follow below:

PTM RSA acquired an option to purchase 100% of the surface and mineral rights to portions of the farm Elandsfontein 102 JQ in December 2002. The rights to Elandsfontein portions Re 1, 12 and Re 14 measure an aggregate 364.6357 Ha. By December 2005, the Company had purchased these surface and mineral rights in exchange for total payments of approximately $1.7 million. One half of this cost was applied to the surface rights and the other half was applied to the mineral rights. The acquired mineral rights were contributed to the WBJV under the terms of the original WBJV Agreement and were later transferred to Maseve under the Consolidation Transaction. The acquired mineral surface rights remain the property of the Company, after payment to Wesizwe for their share in accordance with the Consolidation Transaction.

18

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

PTM RSA acquired its original interests in respect of the mineral rights on portions of the farm Onderstepoort 4, 5 and 6; Onderstepoort 3 and 8; and Onderstepoort 14 and 15 by way of option agreements. All of the Onderstepoort option agreements were later bought out by way of settlement agreements in 2007 and 2008. PTM RSA contributed its interests in these properties to the WBJV.

The remainder of the WBJV mineral properties, being certain portions of Elandsfontein 102JQ, Onderstepoort 98JQ, Frischgewaagd 96JQ, Mimosa 81JQ and Koedoesfontein 94JQ, were contributed to the original WBJV by Anglo.

During the year ended August 31, 2008, the Company purchased surface rights adjacent to the Project 1 deposit area measuring 216.27 hectares for R 8.0 million (approximately $1.09 million) and also purchased surface rights directly over a portion of the Project 1 deposit area measuring 358.79 hectares for R 15.07 million (approximately $2.07 million). The surface rights to these two properties are held to the benefit of the Company or its subsidiaries only.

On August 12, 2010, the Company acquired the right to purchase the Sundown Ranch surface rights covering 1,713 hectares, including accommodation facilities and overlaying the area of the planned Project 1 Platinum Mine for R 130.0 million (approximately $18.57 million at the time). A deposit of R 13.0 million (approximately $1.85 million at the time) was paid to the vendor on August 26, 2010. The purchase price balance of R 117.0 million was paid in January 2011 (approximately $17.03 million at that time). Title was subsequently transferred into Maseve at the Company’s direction. The Company received credit for the purchase price against its share of ongoing project costs. All business and operation of the hotel and recreation facilities at the Sundown Ranch have been contracted to a former manager of the property in exchange for a monthly rental fee and a small revenue participation amount payable to Maseve.

Mineralized Zones

The BIC in general is well known for containing a large share of the world's platinum and palladium resources. There are two very prominent economic deposits within the BIC. Firstly, the Merensky Reef and the UG2 chromitite, which together can be traced on surface for 300km in two separate areas and secondly, the Northern Limb (“Platreef”), which extends for over 120km in the area north of Mokopane.

The platinum and palladium bearing reefs of the BIC have been estimated at about 770 and 480 million ounces respectively (down to a depth of 2,000 metres). These estimates do not distinguish between the categories of Proven and Probable Reserves and Inferred Resource. Recent calculations suggest about 204 and 116 million ounces of Proven and Probable Reserves of platinum and palladium respectively, and 939 and 711 million ounces of Inferred Resources. Mining is already taking place at 2km depth in the BIC. Inferred and ultimately mineable ore resources can almost certainly be regarded as far greater than the calculations suggest. These figures represent about 75% and 50% of the world's platinum and palladium resources respectively. Reserve figures for the Proven and Probable categories alone in the BIC appear to be sufficient for mining during the next 40 years at the current rate of production. However, estimated world resources are such as to permit extraction at a rate increasing by 6% per annum over the next 50 years. Expected extraction efficiency is less for palladium. Thereafter, down-dip extensions of existing BIC mines, as well as lower-grade areas of the Platreef and the Middle Group chromitite layers (sometimes referred to as “CL”), may become payable. Demand, and hence price, will be the determining factor in such mining activities rather than availability of ore.

Exploration drilling in the area has shown that both economic reefs (Merensky and UG2) are present and economically exploitable on the Western Bushveld properties. The separation between these reefs tends to increase from the subcrop environment (less than five metres apart) to depths exceeding 650 metres (up to 50 metres apart) towards the northeast. The subcrops of both reefs generally strike southeast to northwest and dip on average 14 degrees to the northeast. The reefs locally exhibit dips from 4 to 42 degrees (average 14 degrees) as observed from borehole information.

19

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

The most pronounced PGM mineralisation along the western limb of the BIC occurs within the Merensky Reef and is generally associated with a 0.1 –1.2m -thick pegmatoidal feldspathic pyroxenite unit. The second important mineralized unit is the UG2 CL, which is on average 0.6 –2.0m thick.

Environmental Liabilities and Prospecting Permits

There are known environmental issues relating to the Company’s or Maseve’s properties.

Mining and exploration companies in South Africa operate with respect to environmental management principles and environmental management programmes more fully set out in section 39 of the MPRDA and the regulations published in respect thereof.

In addition to the environmental requirements of the MPRDA, the principles as set out in section 2 of the Environmental Management Act 1998 apply to all prospecting and mining operations, as the case may be, and any matter relating to such operation.

In terms of the environmental regulations to the MPRDA, the Company and Maseve as the holders of prospecting rights must:

-

As part of the general terms and conditions for a prospecting right and in order to ensure compliance with the Environmental Management Programme or Environmental Management Plan and to assess the continued appropriateness and adequacy of the Environmental Management Programme and the Environmental Management Plan, the holder of a prospecting right must;

-

Conduct monitoring on a continuous basis.

-

Conduct the performance assessments of the Environmental Management Plan or Environmental Programme as required.

-

Compile and submit a performance assessment report to the Minister in which compliance is demonstrated.

Regular site inspections are conducted on the Company’s and Maseve’s prospecting activities and the aim of these site inspections are:

- To determine the compliance with all legislation pertaining to the environment.

- Advice on environmental management measures to be undertaken during the prospecting phase.

- Site rehabilitation monitoring.

In August 2010, independent compliance inspections were conducted over each prospecting site of the Company and Maseve.

The purpose of an Environmental Compliance Report is to indicate the state of the prospecting when measured against the commitments of the Environmental Management Plan. This Environmental Compliance Report is required in terms of the environmental regulations to the MPRDA.

It was reported that all of the drilling sites and the immediate areas that were affected by prospecting had adequately complied with commitments as recorded in the Environmental Management Programmes. It was further reported that all rehabilitation of prospecting boreholes and related infrastructure was completed and that no further rehabilitation is necessary.

Independent rehabilitation certificates were issued for each borehole and are on record at the site offices.

Subsequent to the compliance inspection an Environmental Compliance Report was issued on August 31, 2010 for each of the Company and Maseve’s prospecting rights and duly lodged with the respective Regional Manager’s offices Mineral Development at the DMR.

20

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Accessibility, Climate, Local Resources, Infrastructure and Physiography

South Africa has a large and well-developed mining industry in the area where the Project 1 and 3 are located. This, among other factors, means that the infrastructure in the area is well established, with well-maintained roads and highways as well as electricity distribution networks and telephone systems.

The project area is located on the southwestern limb of the BIC, some 35km northwest of the North West Province town of Rustenburg. The town of Boshoek is situated 10km to the south along the tar road that links Rustenburg with Sun City and crosses the project area. The project area adjoins the Anglo managed BRPM to the southeast. A railway line linking BRPM to the national network passes the project area immediately to the east with a railway siding at Boshoek. Projects 1 and 3 are readily accessible from Johannesburg by traveling 120km northwest on Regional Road 24 to the town of Rustenburg and then a further 35km. Both BRPM to the south of the project area and Styldrift, a joint venture between the Royal Bafokeng Nation and Anglo, which lies directly to the east of the property, have modern access roads and services. Numerous gravel roads crossing the properties provide easy access to all portions.

The major population centre is the town of Rustenburg, about 35km to the southeast of the project. Pretoria lies approximately 100km to the east and Johannesburg about 120km to the southeast. A popular and unusually large hotel and entertainment centre, Sun City, lies about 10km to the north of the project area. The Sundown Ranch Hotel lies in close proximity to the project area and offers rooms and chalets as accommodation. The properties fall under the jurisdiction of the Moses Kotane Municipality. A paved provincial road crosses the property. Access across most of the property can be achieved by truck without the need for significant road building.

With low rainfall (the area is considered semi-arid with an annual rainfall of 520mm) and high summer temperatures, the area is typical of the Highveld Climatic Zone. The climate of the area does not hinder the operating season and exploration can continue all year long.

All project areas are close to major towns and informal settlements as a potential source of labour with paved roads being the norm. Power lines (400kV) cross both project areas and water is, as a rule, drawn from boreholes. As several platinum mines are located adjacent to and within 50km of the property, there is excellent access to materials and skilled labour. One of the smelter complexes of Anglo is located within 60km of the property.

Topographically, the project area is located on a central plateau characterized by extensive savannah with vegetation consisting of grasses and shrubs with a few trees. The total elevation relief is greater as prominent hills occur in the northern most portions, but variations in topographical relief are minor and limited to low, gently sloped hills. On Project Area 1, elevations range from 1,080 metres above mean sea level (“AMSL”) towards the Elands River in the north to 1,156m AMSL towards the farm Onderstepoort in the southwest, with an average of 1,100 AMSL. The section of the Koedoesfontein property covered by the Project 3 Area gently dips in a north-easterly direction toward a tributary of the Elands River. On Project 3 Area, elevations range from 1,060m AMSL towards the Sandspruit River in the north to 1100m AMSL towards the south eastern corner of the property.

History

Elandsfontein (PTM RSA), Onderstepoort (Portions 4, 5 and 6), Onderstepoort (Portions 3 and 8) and

Onderstepoort (Portions 14 and 15) were all privately owned. Previous work done on these properties has not been fully researched and is largely unpublished. Such academic work as has been done by the Council for Geoscience (government agency) is generally not of an economic nature. PTM RSA acquired these rights and then contributed them to the WBJV in 2004.

Elandsfontein (RPM), Frischgewaagd, Onderstepoort (RPM) and Koedoesfontein have generally been in the hands of major mining groups resident in South Africa. Portions of Frischgewaagd previously held by Impala Platinum Mines Limited were acquired by Johannesburg Consolidated Investment Company Limited, which in turn has since been acquired by Anglo through RPM. RPM contributed these rights into the WBJV in 2004.

21

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Previous geological exploration and resource estimation assessments were done by Anglo as the original owner of some of the mineral rights. Anglo managed the exploration drilling programme for the Elandsfontein and Frischgewaagd borehole series in the area of interest on Project Area 1, and for the Koedoesfontein borehole series in the area of interest on Project Area 3. Geological and sampling logs and an assay database are available.

Prior to the establishment of the WBJV and commencement of drilling for the pre-feasibility study, PTM RSA had drilled 36 boreholes on the Elandsfontein property, of which the geological and sampling logs and assay databases are available.

Existing gravity and ground magnetic survey data were helpful in the interpretation of the regional and local geological setting of the reefs. A distinct increase in gravity values occurs from the southwest to the northwest, most probably reflecting the thickening of the Bushveld sequence in that direction. Low gravity trends in a southeastern to northwestern direction. The magnetic survey reflects the magnetite-rich Main Zone and some fault displacements and late-stage intrusives in the area.

Previous drilling on the Project 3 area conducted by Anglo consisted of three boreholes (KD1, KD2 and KD3). Boreholes KD1 and KD3 were drilled beyond the Merensky Reef and UG2 CL subcrop, and terminated in sediments of the Transvaal Supergroup. Drilling of borehole KD2 was stopped short of the Merensky Reef subcrop.

There has been no previous production from any of the Company’s properties in the Western Bushveld Complex.

Geological Setting

Regional Geology of the BIC

The stable Kaapvaal and Zimbabwe Cratons in southern Africa are characterised by the presence of large mafic-ultramafic layered complexes. These include the Great Dyke of Zimbabwe, the Molopo Farms Complex in Botswana and the well-known BIC.

The BIC was intruded about 2,060 million years ago into rocks of the Transvaal Supergroup along an unconformity between the Magaliesberg quartzites (Pretoria Group) and the overlying Rooiberg felsites (a dominantly felsic volcanic precursor). The BIC is by far the most economically important of these deposits as well as the largest in terms of preserved lateral extent, covering an area of over 66,000km2. It has a maximum thickness of 8km, and is matched in size only by the Windimurra intrusion in Western Australia and the Stillwater intrusion in the USA (Cawthorn, 1996). The mafic component of the Complex hosts layers rich in PGEs, nickel, copper, chromium and vanadium. The BIC is reported to contain about 75% and 50% of the world’s platinum and palladium resources respectively (Vermaak, 1995). The mafic component of the BIC is subdivided into several generally arcuate segments/limbs, each associated with a pronounced gravity anomaly. These include the western, eastern, northern/Potgietersrus, far western/Nietverdient and southeastern/Bethal limbs.

Local Geology

Projects 1 and 3 are underlain by the lower portion of the RLS, the Critical Zone and the lower portion of the Main Zone. The ultramafic Lower Critical Zone and the Mafic Upper Critical Zone and the Main Zone weather to dark, black clays with very little topography. The underlying Transvaal Supergroup comprises shale and quartzite of the Magaliesberg Formation, which creates a more undulating topography. Gravity, magnetic, LANDSAT, aerial photography and geochemistry have been used to map out lithological units. In parts of the project area the MR outcrops, as does the UG2 Reef, beneath a relatively thick (2-5m) overburden of red Hutton to darker Swartland soil forms. The sequence strikes northwest to southeast and dips between 4° and 42° with an average of 14° in the Project 1 and 1A areas, and with an average dip of ~10° in the Project 3 area. The top 32m of rock formation below the soil column is characterized by a highly weathered rock profile (regolith) consisting mostly of gabbro within the Main Zone. Thicknesses of this profile increase near intrusive dykes traversing the area.

22

| Platinum Group Metals Ltd. |

| 2011 Annual Information Form |

Stratigraphy

The RLS intruded into the rocks of the Transvaal Supergroup, largely along an unconformity between the Magaliesberg quartzite of the Pretoria Group and the overlying Rooiberg felsites, which is a dominantly felsic volcanic formation. The mafic rocks of the RLS are subdivided into the following five zones:

-

Marginal Zone comprising finer-grained gabbroic rocks with abundant country-rock fragments.

-

Lower Zone – the overlying Lower Zone is dominated by darker, more iron and magnesium bearing rocks (orthopyroxenite with associated olivine-rich cumulates (harzburgite, dunite)).

-

Critical Zone – its commencement is marked by first appearance of well-defined cumulus chromitite layers. Seven Lower Group chromitite layers have been identified within the lower Critical Zone. Two further chromitite layers – Middle Group (“MG”) – mark the top of the lower Critical Zone. From this stratigraphic position upwards, plagioclase becomes the dominant cumulus phase and lighter coloured (noritic) rocks predominate. The MG3 and MG4 chromitite layers occur at the base of the upper Critical Zone, which is characterised from here upwards by a number of cyclical units. The cycles commence in general with narrow, darker (pyroxenitic) horizons (with or without olivine and chromitite layers); these invariably pass up into norites, which in turn pass into near white layers (leuconorites and anorthosites). The UG1 – first of the two Upper Group chromitite layers – is a cyclical unit consisting of chromitite layers with overlying footwall units that are supported by an underlying anorthosite. The overlying UG2 chromitite layer is of considerable importance because of its economic concentrations of PGEs. The two uppermost cycles of the Critical Zone include the Merensky and Bastard cycles. The Merensky Reef is found at the base of the Merensky cycle, which consists of a pyroxenite and pegmatoidal feldspathic pyroxenite assemblage with associated thin chromitite layers that rarely exceed one metre in thickness. The top contact of the Critical Zone is defined by a giant mottled anorthosite that forms the top of the Bastard cyclic unit.

-

Main Zone – consists of norites grading upwards into gabbronorites. It includes several distinctive mottled anorthosite units towards the base and a distinctive pyroxenite, the Pyroxenite Marker, two thirds of the way up. This marker-unit does not occur in the project area, but is evident in the adjacent BRPM. The middle to upper part of the Main Zone is very resistant to erosion and gives rise to distinctive hills, which are currently being mined for dimension stone (black granite).

-

Upper Zone – the base is defined by the appearance of cumulus magnetite above the Pyroxenite Marker. The Upper Zone is divided into Subzone A at the base; Subzone B, where cumulus iron-rich olivine appears; and Subzone C, where apatite appears as an additional cumulus phase.

Local Geological Setting –Western Bushveld Limb

Exposures of the BIC located on the western limb include the stratigraphic units of the RLS. The local geology includes the classic layered sequence of the RLS and the footwall rocks of the Transvaal Supergroup. The Merensky Reef is believed to be present within much of this lobe. The position of the Merensky Reef is fairly closely defined by seismic reflectors associated with the cyclic units of the upper Critical Zone.

The sequence of the BIC within the project area is confined to the lower part of the Main Zone (Porphyritic Gabbro Marker) and the Critical Zone (HW5–1 and Bastard Reef to UG1 footwall sequence). The rock sequence thins towards the southwest (subcrop) including the marker horizons with concomitant middling of the economic reefs or total elimination thereof. The UG2 Reef and, more often, the UG1 Reef are not developed in some areas owing to the irregular and elevated palaeo-floor of the Transvaal sediments.

Reefs

The MR is a well-developed seam along the central part and towards the north eastern boundary of the Project 1 area. Islands of thin reef and relatively low-level mineralization are present. The better-developed reef package, in which the intensity of chromitite is generally combined with pegmatoidal feldspathic pyroxenite development, occurs as larger island domains along a wide central strip in a north south orientation from subcrop to deeper portions.