UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the Fiscal Year Ended September 30 , 2021

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from __________ to ___________

| Commission File No. | Name of Registrant, State of Incorporation, Address of Principal Offices, and Telephone No. | IRS Employer Identification No. | ||||||||||||

(a Delaware corporation)

(608 ) 275-3340

www.spectrumbrands.com

(a Delaware limited liability company)

3001 Deming Way, Middleton, WI 53562

(608) 275-3340

Securities registered pursuant to Section 12(b) of the Act:

| Registrant | Title of each class | Name of each exchange on which registered | ||||||||||||

| Spectrum Brands Holdings, Inc. | Common Stock, Par Value $0.01 | New York Stock Exchange | ||||||||||||

| SB/RH Holdings, LLC | None | None | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrants are well-known seasoned issuers, as defined in Rule 405 of the Securities Act.

| Spectrum Brands Holdings, Inc. | ☒ | No | ☐ | ||||||||||||||

| SB/RH Holdings, LLC | Yes | ☐ | ☒ | ||||||||||||||

Indicate by check mark if the registrants are not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| Spectrum Brands Holdings, Inc. | Yes | ☐ | ☒ | ||||||||||||||

| SB/RH Holdings, LLC | Yes | ☐ | ☒ | ||||||||||||||

Indicate by check mark whether the registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| Spectrum Brands Holdings, Inc. | ☒ | No | ☐ | ||||||||||||||

| SB/RH Holdings, LLC | ☒ | No | ☐ | ||||||||||||||

Indicate by check mark whether the registrants have submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

| Spectrum Brands Holdings, Inc. | ☒ | No | ☐ | ||||||||||||||

| SB/RH Holdings, LLC | ☒ | No | ☐ | ||||||||||||||

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

| Spectrum Brands Holdings, Inc. | |||||||||||||||||

| SB/RH Holdings, LLC | |||||||||||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company in Rule 12b-2 of the Exchange Act.:

Registrant | Accelerated Filer | Smaller Reporting Company | Emerging Growth Company | ||||||||||||||

| Spectrum Brands Holdings, Inc. | X | ||||||||||||||||

| SB/RH Holdings, LLC | X | ||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

| Spectrum Brands Holdings, Inc. | ☐ | ||||

| SB/RH Holdings, LLC | ☐ | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| Spectrum Brands Holdings, Inc. | Yes | No | ☒ | ||||||||||||||

| SB/RH Holdings, LLC | Yes | No | ☒ | ||||||||||||||

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

| Spectrum Brands Holdings, Inc. | Yes | ☒ | No | ☐ | |||||||||||||

| SB/RH Holdings, LLC | Yes | ☐ | No | ☒ | |||||||||||||

The aggregate market value of the voting stock held by non-affiliates of Spectrum Brands Holdings, Inc. was approximately $3,592 million based upon the closing price on the last business day of the registrant's most recently completed second fiscal quarter (April 4, 2021). For the sole purposes of making this calculation, term “non-affiliate” has been interpreted to exclude directors and executive officers and other affiliates of the registrant. Exclusion of shares held by any person should not be construed as a conclusion by the registrant, or an admission by any such person, or that such person is an “affiliate” of the Company, as defined by applicable securities law.

As of November 19, 2021, there were outstanding 41,190,355 shares of Spectrum Brands Holdings, Inc.’s Common Stock, par value $0.01 per share.

SB/RH Holdings, LLC meets the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K and has therefore omitted the information otherwise called for by Items 10 to 13 of Form 10-K as allowed under General Instruction I(2)(c).

DOCUMENTS INCORPORATED BY REFERENCE

1

SPECTRUM BRANDS HOLDINGS, INC.

SB/RH HOLDINGS, LLC

TABLE OF CONTENTS

Page | ||||||||

2

Forward-Looking Statements

We have made or implied certain forward-looking statements in this document. All statements, other than statements of historical facts included or incorporated by reference in this document, including the statements under Management’s Discussion and Analysis of Financial Condition and Results of Operations, without limitation, statements or expectations regarding our Global Productivity Improvement Program, our business strategy, future operations, financial condition, estimated revenues, projected costs, projected synergies, prospects, plans and objectives of management, information concerning expected actions of third parties are forward-looking statements. When used in this report, the words future, anticipate, pro forma, seek, intend, plan, envision, estimate, believe, belief, expect, project, forecast, outlook, goal, target, would, will, can, should, may and similar expressions are also intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words.

Since these forward-looking statements are based upon our current expectations of future events and projections and are subject to a number of risks and uncertainties, many of which are beyond our control and some of which may change rapidly, actual results or outcomes may differ materially from those expressed or implied herein, and you should not place undue reliance on these statements. Important factors that could cause our actual results to differ materially from those expressed or implied herein include, without limitation:

•the impact of the COVID-19 pandemic and economic, social and political conditions or civil unrest in the U.S. and other countries on our customers, employees (including our ability to retain and attract key personnel), manufacturing facilities, suppliers, capital markets, and our financial condition, and results of operations, all of which tend to aggravate the other risks and uncertainties we face;

•the impact of our indebtedness on our business, financial condition, and results of operations;

•the impact of restrictions in our debt instruments on our ability to operate our business, finance our capital needs or pursue or expand business strategies;

•any failure to comply with financial covenants and other provisions and restrictions of our debt instruments;

•the effects of general economic conditions, including the impact of, and changes to tariffs and trade policies, inflation, recession or fears of a recession, depression or fears of a depression, labor costs and stock market volatility or monetary or fiscal policies in the countries where we do business;

•the impact of fluctuations in transportation and shipment costs, commodity prices, costs or availability of raw materials or terms and conditions available from suppliers, including suppliers’ willingness to advance credit;

•interest rate and exchange rate fluctuations;

•the loss of, significant reduction in, or dependence upon, sales to any significant retail customer(s);

•competitive promotional activity or spending by competitors, or price reductions by competitors;

•the introduction of new product features or technological developments by competitors and/or the development of new competitors or competitive brands;

•the impact of actions taken by significant stockholders;

•changes in consumer spending preferences and demand for our products, particularly in light of the COVID-19 pandemic and economic stress;

•our ability to develop and successfully introduce new products, protect our intellectual property and avoid infringing the intellectual property of third parties;

•our ability to successfully identify, implement, achieve and sustain productivity improvements (including our Global Productivity Improvement Program), cost efficiencies (including at our manufacturing and distribution operations), and cost savings;

•the seasonal nature of sales of certain of our products;

•the effects of climate change and unusual weather activity as well as our ability to respond to future natural disasters and pandemics and to meet our environmental, social and governance goals;

•the cost and effect of unanticipated legal, tax or regulatory proceedings or new laws or regulations (including environmental, public health and consumer protection regulations);

•our discretion to conduct, suspend or discontinue our share repurchase program (including our discretion to conduct purchases, if any, in a variety of manners including open-market purchases or privately negotiated transactions);

•public perception regarding the safety of products that we manufacture and sell, including the potential for environmental liabilities, product liability claims, litigation and other claims related to products manufactured by us and third parties;

•the impact of existing, pending or threatened litigation, government regulation or other requirements or operating standards applicable to our business;

•the impact of cybersecurity breaches or our actual or perceived failure to protect company and personal data, including our failure to comply with new and increasingly complex global data privacy regulations;

•changes in accounting policies applicable to our business;

•our ability to utilize net operating loss carry-forwards to offset tax liabilities from future taxable income;

•the impact of expenses resulting from the implementation of new business strategies, divestitures or current and proposed restructuring activities;

•the ability to consummate the announced Hardware and Home Improvement ("HHI") divestiture on the expected terms and within the anticipated time period, or at all, which is dependent on the parties' ability to satisfy certain closing conditions and our ability to realize the benefits of the transaction, including reducing the leverage of the Company, invest in the organic growth of the Company, fund any future acquisitions, returning capital to shareholders, and/or maintain its quarterly dividends;

•the risk that regulatory approvals that are required to complete the proposed HHI divestiture may not be realized, may take longer than expected or may impose adverse conditions;

•our ability to realize the expected benefits of such transaction and to successfully separate the HHI business;

•our ability to successfully implement further acquisitions or dispositions and impact of any such transactions on our financial performance;

•the unanticipated loss of key members of senior management and the transition of new members of our management teams to their new roles;

•the impact of economic, social and political conditions or civil unrest in the U.S. and other countries;

•the effects of political or economic conditions, terrorist attacks, acts of war, natural disasters, public health concerns or other unrest in international markets;

•the ability to achieve our goals regarding environmental, social, and governance practices; and

•our increased reliance on third-party partners, suppliers, and distributors to achieve our business objectives.

Some of the above-mentioned factors are described in further detail in the sections entitled Risk Factors in our annual and quarterly reports (including this report), as applicable. You should assume the information appearing in this report is accurate only as of the end of the period covered by this report, or as otherwise specified, as our business, financial condition, results of operations and prospects may have changed since that date. Except as required by applicable law, including the securities laws of the United States (“U.S.”) and the rules and regulations of the United States Securities and Exchange Commission (“SEC”), we undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, to reflect actual results or changes in factors or assumptions affecting such forward-looking statements.

3

PART I

ITEM 1. BUSINESS

This combined Form 10-K is being filed by Spectrum Brands Holdings, Inc. (“SBH”) and SB/RH Holdings, LLC (“SB/RH”) (collectively, the “Company”). SB/RH is a wholly-owned subsidiary of SBH and represents substantially all of its assets, liabilities, revenues, expenses and operations. SB/RH is the parent guarantor for certain debt of Spectrum Brands, Inc., a wholly-owned subsidiary of SB/RH ("SBI"), and represents all of SBI assets, liabilities, revenues, expenses, and operations. Thus, all information contained in this report relates to, and is filed by, SBH. Information that is specifically identified in this report as relating solely to SBH, such as its financial statements and its common stock, does not relate to and is not filed by SB/RH. SB/RH makes no representation as to that information. The terms “the Company,” “we,” and “our” as used in this report, refer to both SBH and its consolidated subsidiaries and SB/RH and its consolidated subsidiaries, unless otherwise indicated.

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are available free of charge through our website at www.spectrumbrands.com as soon as reasonably practicable after such reports are filed with, or furnished to the SEC. The SEC also maintains a website that contains our reports, proxy statements and other information at www.sec.gov. In addition, copies of our (i) Corporate Governance Guidelines, (ii) charters for the Audit Committee, Compensation Committee, and Nominating and Corporate Governance Committee, (iii) Code of Business Conduct and Ethics and (iv) Code of Ethics for the Principal Executive Officer and Senior Financial Officers are available on our website at www.spectrumbrands.com under “Investor Relations—Corporate Governance.” Copies will also be provided to any stockholder upon written request to Spectrum Brands, Inc. at 3001 Deming Way, Middleton, Wisconsin 53562 or via electronic mail at investorrelations@spectrumbrands.com, or by telephone at (608) 275-4917.

General Overview

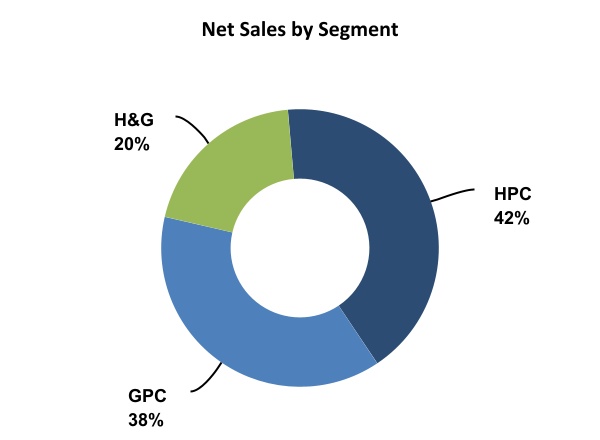

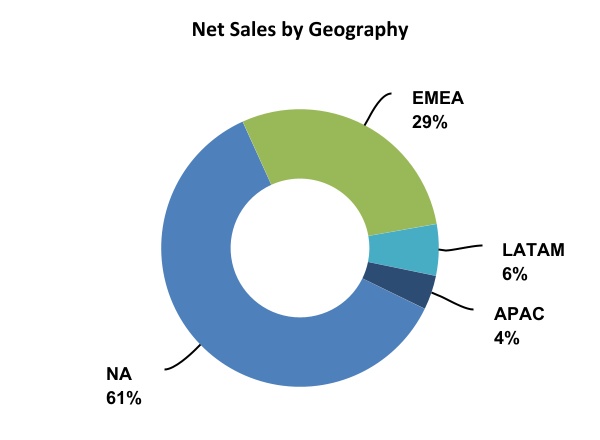

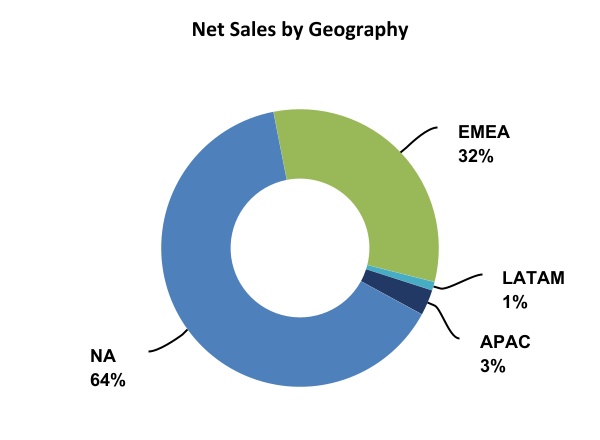

We are a diversified global branded consumer products and home essentials company. We manage the business in three vertically integrated, product focused segments: (i) Home and Personal Care (“HPC”), (ii) Global Pet Care (“GPC”), and (iii) Home and Garden (“H&G”). The Company manufactures, markets and distributes its products globally in the North America (“NA”), Europe, Middle East & Africa (“EMEA”), Latin America (“LATAM”) and Asia-Pacific (“APAC”) regions through a variety of trade channels, including retailers, wholesalers and distributors. We enjoy strong name recognition in our regions under our various brands and patented technologies across multiple product categories. Global and geographic strategic initiatives and financial objectives are determined at the corporate level. Each segment is responsible for implementing defined strategic initiatives and achieving certain financial objectives and has a president responsible for sales and marketing initiatives and the financial results for all product lines within that segment. The segments are supported through center-led corporate shared service operations consisting of finance and accounting, information technology, legal and human resources, supply chain and commercial operations. The following is an overview of the consolidated business showing net sales by segment and geographic region sold (based upon destination) as a percentage of consolidated net sales for the year ended September 30, 2021.

Our operating performance is influenced by a number of factors including: general economic conditions; foreign exchange fluctuations; trends in consumer markets; consumer confidence and preferences; our overall product line mix, including pricing and gross margin, which vary by product line and geographic market; pricing of certain raw materials and commodities; energy and fuel prices; and our general competitive position, especially as impacted by our competitors’ advertising and promotional activities and pricing strategies. See Management’s Discussion and Analysis of Financial Condition and Results of Operations, included in Item 7 to this Annual Report, for further discussion of the consolidated operating results and segment operating results.

On September 8, 2021, SBI entered into a definitive Asset and Stock Purchase Agreement with ASSA ABLOY AB to sell the Company's Hardware and Home Improvement ("HHI") segment. As a result, the Company's assets and liabilities associated with the HHI segment have been classified as held for sale, and the respective operations of the HHI segment classified as discontinued operations and reported separately for all periods presented as the planned disposition represents a strategic shift that will have a major effect on the Company's operations and financial results.

4

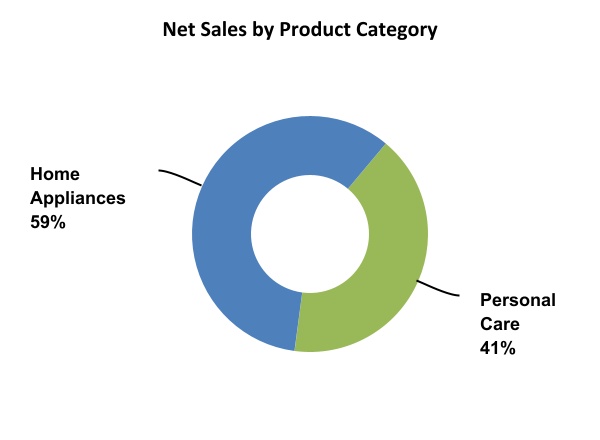

Home and Personal Care (HPC)

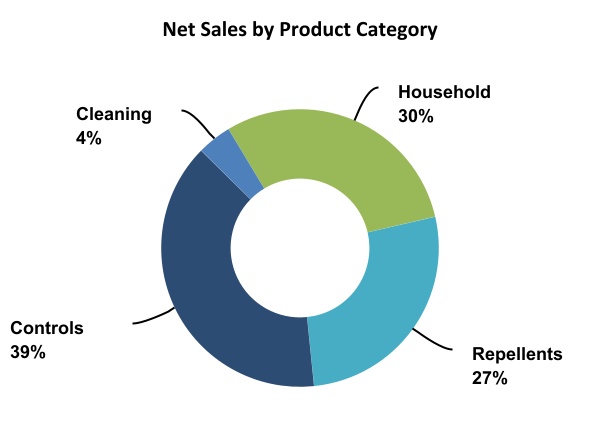

The following is an overview of net sales by product category and geographic region sold by destination for the year ended September 30, 2021.

Product Category | Products | Brands | ||||||||||||

Home Appliances | Small kitchen appliances including toaster ovens, coffeemakers, slow cookers, blenders, hand mixers, grills, food processors, juicers, toasters, irons, kettles, and breadmakers | Black & Decker®, Russell Hobbs®, George Foreman®, Toastmaster®, Juiceman®, Farberware®, and Breadman® | ||||||||||||

Personal Care | Hair dryers, flat irons and straighteners, rotary and foil electric shavers, personal groomers, mustache and beard trimmers, body groomers, nose and ear trimmers, women's shavers, haircut kits and intense pulsed light hair removal systems | Remington®, LumaBella® | ||||||||||||

We have a trademark license agreement (the "License Agreement") with Stanley Black & Decker ("BDC") pursuant to which we license the Black & Decker® brand in North America, Latin America (excluding Brazil) and the Caribbean for four core categories of household appliances: beverage products, food preparation products, garment care products and cooking products through December 31, 2021. Under the terms of the License Agreement, we agree to pay BDC royalties based on a percentage of sales, with minimum annual royalty payments of $15.0 million. The License Agreement also requires us to comply with maximum annual return rates for products. Total revenue under the License Agreement was $400.2 million for the year ended September 30, 2021.

As of the date of this report, we are in discussions with BDC to replace the current License Agreement with a new multi-year trademark license agreement, but there can be no assurances that we will be able to do so. In the event that we cannot reach a new agreement, we believe the current License Agreement, provides us until June 30, 2023 to transition out of the BDC brand and prohibits BDC from competing in the four categories for five years after the end of the transition period. BDC has asserted that it believes the transition period and non-competition provisions in the License Agreement are no longer applicable. For additional information please see our Risk Factors set forth in this Annual Report, including the risk factor entitled "We may not be able to adequately establish and protect our intellectual property rights, and the infringement or loss of our intellectual property rights could harm our business."

We own the right to use the Remington® trademark for electric shavers, shaver accessories, grooming products and personal care products; and Remington Arms Company, Inc. (“Remington Arms”) owns the rights to use the trademark for firearms, sporting goods and products for industrial use, including industrial hand tools. The terms of a 1986 agreement between Remington Products, LLC and Remington Arms provides for the shared rights to use the trademark on products which are not considered “principal products of interest” for either company. We retain the trademark for nearly all products which we believe can benefit from the use of the brand name in our distribution channels.

HPC products are sold primarily to large retailers, online retailers, wholesalers, distributors, warehouse clubs, food and drug chains and specialty trade or retail outlets such as consumer electronics stores, department stores, discounters and other specialty stores. International distribution varies by region and is often executed on a country-by-country basis. Our sales generally are made through the use of individual purchase orders. A significant percentage of our sales are attributable to a limited group of retailer customers, including Walmart and Amazon, which represent approximately 35% of segment sales for the year ended September 30, 2021.

Primary competitors for home appliances include Newell Brands (Sunbeam, Mr. Coffee, Crockpot, Oster), De’Longhi America (DeLonghi, Kenwood, Braun), SharkNinja (Shark, Ninja), Hamilton Beach Holding Co. (Hamilton Beach, Proctor Silex), Sensio, Inc. (Bella); SEB S.A.(T-fal, Krups, Rowenta), Whirlpool Corporation (Kitchen Aid), Conair Corporation (Cuisinart, Waring), Koninklijke Philips N.V. (Philips), Glen Dimplex (Morphy Richards) and private label brands for major retailers. Primary competitors in personal care include Koninklijke Philips Electronics N.V. (Norelco), The Procter & Gamble Company (Braun), Conair Corporation, Wahl Clipper Corporation, and Helen of Troy Limited.

Sales from electric personal care product categories tend to increase during the December holiday season (the Company's fiscal first quarter), while small appliances sales typically increase from July through December primarily due to the increased demand by customers in the late summer for “back-to-school” sales (the Company's fiscal fourth quarter) and in December for the holiday season. Our sales by quarter as a percentage of annual net sales during the years ended September 30, 2021, 2020, and 2019 are as follows:

| 2021 | 2020 | 2019 | ||||||||||||||||||

First Quarter | 30 | % | 29 | % | 30 | % | ||||||||||||||

Second Quarter | 24 | % | 21 | % | 20 | % | ||||||||||||||

Third Quarter | 22 | % | 23 | % | 23 | % | ||||||||||||||

Fourth Quarter | 24 | % | 27 | % | 27 | % | ||||||||||||||

5

Substantially all of our home appliances and personal care products are manufactured by third-party suppliers that are primarily located in the APAC region, the prices of which may be susceptible to changes in transportation costs, government regulations and tariffs, and changes in currency exchange rates. We maintain ownership of most of the tooling and molds used by our suppliers.

We continuously monitor and evaluate our supplier network for quality, cost, and manufacturing capacity. Our research and development strategy is focused on new product development and performance enhancements of our existing products. We plan to continue to use our brand names, customer relationships and research and development efforts to introduce innovative products that offer enhanced value to consumers through new designs and improved functionality.

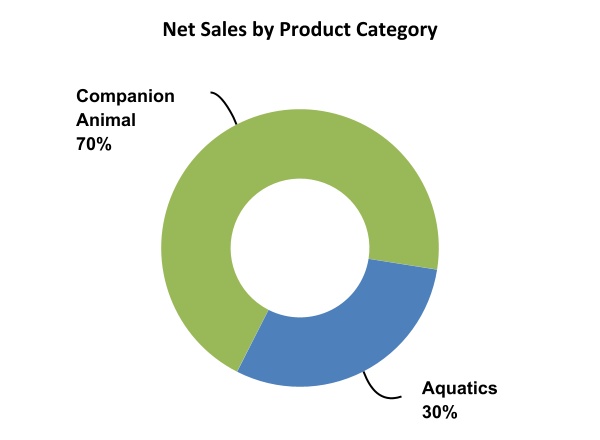

Global Pet Care (GPC)

The following is an overview of GPC net sales by product category and geographic region sold by destination for the year ended September 30, 2021.

Product Category | Products | Brands | ||||||||||||

Companion Animal | Rawhide chews, dog and cat clean-up, training, health and grooming products, small animal food and care products, rawhide-free dog treats, and wet and dry pet food for dogs and cats | 8IN1® (8-in-1), Dingo®, Nature's Miracle®, Wild Harvest™, Littermaid®, Jungle®, Excel®, FURminator®, IAMS® (Europe only), Eukanuba® (Europe only), Healthy-Hide®, DreamBone®, SmartBones®, ProSense®, Perfect Coat®, eCOTRITION®, Birdola®, Good Boy®, Meowee!®, Wildbird®, and Wafcol®. | ||||||||||||

Aquatics | Consumer and commercial aquarium kits, stand-alone tanks; aquatics equipment such as filtration systems, heaters and pumps; and aquatics consumables such as fish food, water management and care | Tetra®, Marineland®, Whisper®, Instant Ocean®, GloFish®, OmegaOne® and OmegaSea®. | ||||||||||||

We sell primarily to large retailers, pet superstores, online retailers, food and drug chains, warehouse clubs and other specialty retail outlets. International distribution varies by region and is often executed on a country-by-country basis. Our sales generally are made through the use of individual purchase orders. In addition to product sales, we also perform installation and maintenance services on commercial aquariums. Live fish under our GloFish® brand are produced, marketed, and sold by independent third-party breeders through a supply and licensing agreement with the Company. On October 26, 2020, the Company completed the acquisition of Armitage Pet Care Ltd. ("Armitage"), a premium pet treats and toys business in Nottingham, United Kingdom including a portfolio of brands that include Armitage's dog treats brand, Good Boy®, cat treats brand, Meowee!®, and Wildbird® bird feed products, among others, that are predominantly sold within the United Kingdom. A significant percentage of our sales are attributable to a limited group of retailer customers, including Walmart and Amazon, which represent approximately 32% of segment sales for the fiscal year ended September 30, 2021.

Primary competitors are Mars Corporation, the Hartz Mountain Corporation, and Central Garden & Pet Company all of which sell a comprehensive line of pet supplies that compete across our product categories. The pet supplies product category is highly fragmented with no competitor holding a substantial market share and consists of small companies with limited product lines, including private label products and suppliers.

Sales remain fairly consistent throughout the year with little variation. Our sales by quarter as a percentage of annual net sales during the years ended September 30, 2021, 2020, and 2019 are as follows:

| 2021 | 2020 | 2019 | ||||||||||||||||||

First Quarter | 24 | % | 21 | % | 24 | % | ||||||||||||||

Second Quarter | 26 | % | 25 | % | 25 | % | ||||||||||||||

Third Quarter | 23 | % | 25 | % | 25 | % | ||||||||||||||

Fourth Quarter | 27 | % | 29 | % | 26 | % | ||||||||||||||

Rawhide products and certain companion animal products are produced at third-party suppliers in the APAC region and Mexico. Aquatics products are produced in our manufacturing plants located in the U.S. and Germany and are also produced at third-party suppliers in the APAC region. On March 29, 2020, the Company sold its dog and cat food (“DCF”) production facility and distribution center in Coevorden, Netherlands (the “Coevorden Operations”) pursuant to an agreement with United Petfood Producers NV (“UPP”) that continues to produce DCF products for the Company sold and distributed in EMEA under the IAMS® and Eukanuba® brands.

We maintain ownership of most of the tooling and molds used by third-party suppliers. We continually evaluate capacity at our manufacturing facilities and related utilization. In general, we believe our existing facilities are adequate for our present and foreseeable operating needs. Product purchased from third-party suppliers, especially those from the APAC regions, are susceptible to fluctuations in transportation costs, government regulations and tariffs, and changes in currency exchange rates. We continuously monitor and evaluate our supplier network for quality, cost, and manufacturing capacity.

6

Our research and development strategy is focused on new product development and performance enhancements of our existing products. We plan to continue to use our brand names, customer relationships and research and development efforts to introduce innovative products that offer enhanced value to consumers through new designs and improved functionality.

Home and Garden (H&G)

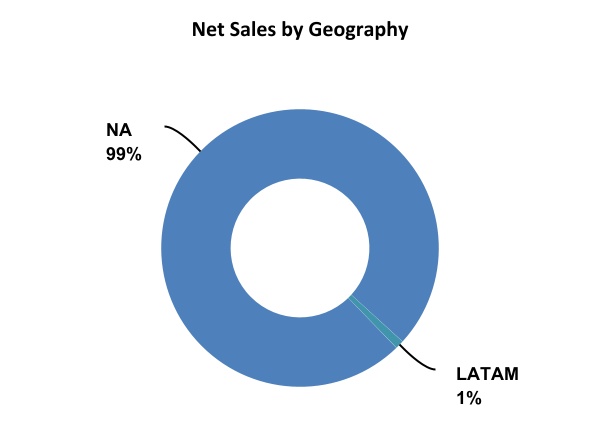

The following is an overview of H&G net sales by product category and geographic region sold by destination for the year ended September 30, 2021.

Product Category | Products | Brands | ||||||||||||

Household | Household pest control solutions such as spider and scorpion killers; ant and roach killers; flying insect killers; insect foggers; wasp and hornet killers; and bedbug, flea and tick control products | Hot Shot®, Black Flag®, Real-Kill®, Ultra Kill®, The Ant Trap® (TAT), and Rid-A-Bug®. | ||||||||||||

Controls | Outdoor insect and weed control solutions, and animal repellents such as aerosols, granules, and ready-to-use sprays or hose-end ready-to-sprays | Spectracide®, Garden Safe®, Liquid Fence®, and EcoLogic®. | ||||||||||||

Repellents | Personal use pesticides and insect repellent products, including aerosols, lotions, pump sprays and wipes, yard sprays and citronella candles | Cutter® and Repel®. | ||||||||||||

| Cleaning | Household surface cleaning, maintenance, and restoration products, including bottled liquids, mops, wipes, and markers. | Rejuvenate® | ||||||||||||

We sell primarily to large retailers, home improvement centers, mass merchants, dollar stores, hardware stores, lawn and garden distributors, food and drug retailers, and e-commerce. We sell primarily in the U.S. with some distribution in LATAM and the Caribbean. On May 28, 2021, the Company acquired 100% of the membership interest in For Life Products, LLC ("FLP"); a leading manufacturer of household cleaning, maintenance, and restoration sold under the Rejuvenate® brand, expanding the product categories provided by the H&G segment. Our sales generally are made through the use of individual purchase orders. A significant percentage of our sales are attributable to a limited group of retailer customers, including Lowe’s, Home Depot, and Walmart, which represent approximately 65% segment sales for the year ended September 30, 2021.

Primary competitors include The Scotts Miracle-Gro Company (Ortho, Roundup, Tomcat), S.C. Johnson & Son, Inc. (Raid, OFF!), Central Garden & Pet (AMDRO, Sevin), SBM Company (BioAdvanced), and Henkel AG & Co. KGaA (Combat).

Sales typically peak during the first six months of the calendar year (the Company’s second and third fiscal quarters) and are lowest in the last three months of the calendar year (the Company's first quarter) due to customer purchasing patterns, and timing of promotional activities. Our sales by quarter as a percentage of annual net sales during the years ended September 30, 2021, 2020, and 2019 are as follows:

| 2021 | 2020 | 2019 | ||||||||||||||||||

First Quarter | 14 | % | 8 | % | 10 | % | ||||||||||||||

Second Quarter | 29 | % | 25 | % | 27 | % | ||||||||||||||

Third Quarter | 35 | % | 38 | % | 40 | % | ||||||||||||||

Fourth Quarter | 22 | % | 29 | % | 23 | % | ||||||||||||||

H&G currently produces the majority of its products in one facility in St. Louis, Missouri, with production primarily consisting of liquids and aerosols, and the remaining portion of products being produced by various third-party manufacturers, consisting of granulates, candles, baits & traps, and wipes. Products produced for the Rejuvenate business are primarily provided by third-party manufacturers. The main raw materials purchased are plastic bottles, steel aerosol cans, corrugate, active ingredients, and bulk chemicals. The prices of these raw materials are susceptible to fluctuations due to supply and demand trends, energy costs, transportation costs, inflation, government regulations, and tariffs. We continuously monitor and evaluate our supplier network for quality, cost, and manufacturing capacity.

Our research and development strategy is focused on new product development and performance enhancements of our existing products. We plan to continue to use our brand names, customer relationships, and research and development efforts to introduce innovative products that offer enhanced value to consumers through new designs and improved functionality.

7

Discontinued Operations

Hardware and Home Improvement ("HHI")

On September 8, 2021, the Company entered into a definitive Asset and Stock Purchase Agreement (the "Purchase Agreement") with ASSA ABLOY AB ("ASSA") to sell its HHI segment for cash proceeds of $4.3 billion, subject to customary purchase price adjustments. The Company's assets and liabilities associated with HHI have been classified as held for sale, and the respective operations have been classified as discontinued operations and reported separately for all periods presented. HHI consists of residential locksets and door hardware, including knobs, levers, deadbolts, handle sets, and electronic and connected locks under the Kwikset®, Weiser®, Baldwin®, Tell Manufacturing®, and EZSET® brands; kitchen and bath faucets and accessories under the Pfister® brand; and builders' hardware consisting of hinges, metal shapes, security hardware, rack and sliding door hardware, and gate hardware under the National Hardware® and FANAL® brands. Refer to Note 3 - Divestitures to the Consolidated Financial Statements, included elsewhere in this Annual Report, for further discussion pertaining the HHI divestiture.

Global Batteries and Lighting (“GBL”)

On January 2, 2019, the Company completed the sale of its GBL business pursuant to the GBL acquisition agreement with Energizer Holdings, Inc. (“Energizer”) for cash proceeds of $1,956.2 million, resulting in a pre-tax gain on sale of $989.8 million, during the year ended September 30, 2019, including the estimated settlement of customary purchase price adjustments for working capital and assumed indebtedness, recognition of tax and legal indemnifications under the acquisition agreement and a contingent purchase price adjustment for the settlement of the divestiture of the Varta® consumer batteries business by Energizer. The Company’s assets and liabilities associated with GBL have been classified as held for sale and the respective operations have been classified as discontinued operations; and reported separately for all periods presented. GBL consists of consumer batteries products including alkaline batteries, zinc carbon batteries, nickel metal hydride (NiMH) rechargeable batteries, hearing aid batteries, battery chargers, battery-powered portable lighting products including flashlights and lanterns, and other specialty battery products primarily under the Rayovac® and Varta® brand, and other proprietary brand names pursuant to licensing arrangements with third parties. Refer to Note 3 – Divestitures to the Consolidated Financial Statements, included elsewhere in this Annual Report, for further discussion pertaining to the GBL divestiture.

Global Auto Care (“GAC”)

On January 28, 2019, the Company completed the sale of its GAC business pursuant to the GAC acquisition agreement with Energizer for $938.7 million in cash proceeds and $242.1 million in stock consideration of common stock of Energizer, resulting in a loss on sale of business of $111.0 million, during the year ended September 30, 2019, including the estimated settlement of customary purchase price adjustments for working capital and assumed indebtedness, and recognition of tax and legal indemnifications in accordance with the GAC acquisition agreement. The Company’s assets and liabilities associated with GAC have been classified as held for sale and the respective operations have been classified as discontinued operations; and reported separately for all periods presented. GAC consists of appearance products, including protectants, wipes, tire and wheel care products, glass cleaners, leather care products, air fresheners and washes designed to clean, shine, refresh and protect interior and exterior automobile surfaces under the Armor All® brand; performance products including STP® branded fuel and oil additives, functional fluids and automotive appearance products; A/C recharge products that consist of do-it-yourself automotive air conditioner recharge products under the A/C Pro® brand, along with other refrigerant and oil recharge kits, sealants and accessories. Refer to Note 3 – Divestitures to the Consolidated Financial Statements, included elsewhere in this Annual Report, for further discussion pertaining to the GAC divestiture.

Human Resources

Employee Profile

At Spectrum Brands, we are led by our values of trust, accountability, and collaboration to serve others through this common mission: We Make Living Better at Home. We strive to live our core values of trust, accountability and collaboration every day by serving our customers, consumers, and communities. Our workplace culture is centered around practices that support our communities and promote sustainable practices and a diverse, equitable, and inclusive workforce.

Employee Wellness

We encourage our employees to “Speak Up,” “Be Accountable,” “Take Action,” and “Grow Talent,” promote innovation, trust, accountability and collaboration. The result is a work environment that encourages the well being of our employees wholistically - mind and body.

Employee Health and Safety

We are committed to the Environmental Health and Safety (EHS) safety of our employees. We continuously strive to maintain our strong safety performance as we continue to grow our business around the globe. The keys to our EHS success are a workforce that is engaged, a management team who supports and invests in employee safety, and the leadership of our skilled EHS team. In the last several years, the team has added dedicated EHS professionals to individual sites to train employees and ensure compliance with applicable safety standards and regulations. The team hosts regular meetings to share information and discuss best practices across plants.

Talent Development

Spectrum Brands is committed to developing our future leaders at every level. Our talent processes start with understanding what current and future talent is needed to deliver business goals, followed by a talent review process to assist managers with evaluating talent.

Learning and development is a critical part of creating Spectrum Brands’ culture of high performance, innovation, and inclusion. We believe on-the-job experience is an outstanding way to learn, and performance and development plans ensure that managers and employees have conversations about career aspirations, mobility, developmental goals and interests.

Employee Communication and Feedback

In an ongoing effort to understand our employees needs, and deliver on our values of trust, accountability and collaboration, we listen. We regularly host company-wide and business unit town halls to offer employees an opportunity to ask questions about Company activities and policies that impact them. We solicit and receive questions and feedback from our employees through this process.

COVID-19 Response

In response to COVID-19, our Company took swift and effective action to protect the health and safety of our global employees. The Company implemented a number of robust COVID-19 safety practices, including, by way of example:

8

•Temperature screenings and masks were required at all sites prior to admittance;

•Weekly audits using a list of safety requirements, including social distancing, personal protective equipment, sanitation, hygiene education, etc.;

•Guidelines and procedures for the deep cleaning of HVAC systems to prevent the spread of germs;

•Contact tracing practices with mandatory quarantine for individuals with confirmed close contact cases;

•Requirement that all non-essential employees to work from home; and

•Suspension of travel restrictions for all unnecessary travel.

Our Company also began producing and selling Cutter® Hand Sanitizer during the initial peak of the pandemic, which were eventually sent to employee homes for personal use and donated to health facilities.

Diversity, Equity and Inclusion

Spectrum Brands is committed to fostering a diverse, equitable, and inclusive workplace for employees of every race, color, gender identity, sexual orientation, age, physical or mental ability and background. At Spectrum Brands, we strive to make our employees feel valued and respected and given the opportunity to thrive as their authentic selves. To further that objective we have implemented a diversity, equity, and inclusion program.

ITEM 1A. RISK FACTORS

Any of the following factors could materially and adversely affect our business, financial condition and results of operations. The risks described below are not the only risks that we may face. Additional risks and uncertainties not currently known to us or that we currently view as immaterial may also materially and adversely affect our business, financial condition or results of operations.

We are subject to a variety of risks, including those described below. In particular, these risks include, but are not limited to:

•Risks related to our business operations: We participate in very competitive markets and we may not be able to compete successfully, causing us to lose market share and sales.

•Risks related to our indebtedness and financing abilities: Our substantial indebtedness may limit our financial and operating flexibility, and we may incur additional debt, which could increase the risks associated with our substantial indebtedness.

•Risks related to our international operations: We are subject to significant international business risks that could hurt our business and cause our results of operations to fluctuate.

•Risks related to Data Privacy and Intellectual Property: We may not be able to adequately establish and protect our intellectual property rights, and the infringement or loss of our intellectual property rights could harm our business.

•Risks related to litigation and regulatory compliance: We are subject to a number of claims and litigation and may be subject to future claims and litigation, any of which may adversely affect our business.

•Risks related to investment in our common stock: The market price of the Company’s common stock is likely to be highly volatile and could fluctuate widely in price in response to various factors, many of which are beyond our control.

Risks Related to our Business Operations

The COVID-19 pandemic is a serious threat to the health and economic well-being affecting our customers, employees, sources of supply and our financial condition and results of operations.

In March 2020, the World Health Organization announced that COVID-19 had become a pandemic and a National Emergency relating to COVID-19 was announced in the U.S. There is a possibility of continued widespread infection in the U.S. and abroad, with the potential for substantial commercial impact. National, state, and local authorities recommended social distancing and imposed, or were considering imposing, quarantine and isolation measures, on large portions of the population, including mandatory business closures. These measures are expected to have serious adverse impacts on domestic and foreign economies of uncertain severity and duration. The effectiveness of economic stabilization efforts, including potential government payments to affected citizens and industries, is uncertain.

The sweeping nature of COVID-19 makes it extremely difficult to predict the long-term ramifications on our financial condition and results of operations. However, the likely overall economic impact of COVID-19 is viewed as highly negative to the general economy. These impacts may include, but are not limited to:

•significant reductions in, or volatility of, demand for our products, which may be caused by the inability or unwillingness of consumers to purchase our products due to illness, quarantine, travel restrictions, store closures, general financial hardship, decreased consumer confidence or changes in consumer spending and shopping habits;

•inability to meet customers’ needs or achieve cost targets due to disruptions in our manufacturing and supply arrangements caused by the loss or disruption of essential manufacturing or availability or cost of key product components, transportation, workforce, or other manufacturing and distribution capability;

•failure of third parties on which we rely, including our suppliers, contract manufacturers, distributors, contractors, commercial banks, and other business partners, to meet their obligations to us, or significant disruptions in their ability to do so, which may be caused by their own financial or operational difficulties and may adversely impact our operations;

•significant change in the political conditions in markets in which we manufacture, sell or distribute our products, including governmental or regulatory actions such as quarantines, closures or other restrictions, that limit or close our operating and manufacturing facilities, restrict our employees’ ability to travel or perform necessary business functions, or otherwise prevent our third-party partners, suppliers, or customers from sufficiently staffing operations, including operations necessary for the production, distribution, sale and support of our products, which could adversely impact our results or impairment of the Company’s net assets;

•disruptions and stress in capital markets that could impact the cost and availability of capital for us and for our customers, suppliers and other business partners;

•quarantines, stay-at-home orders and other limitations can disrupt our product development, branding, research and administrative functions, regardless of whether we are actually forced to close our own facilities and similar disruptions that may also effect other organizations and persons that we collaborate with or whose services we are dependent on; or

•the need for our employees and business partners to work remotely in these circumstances also creates greater potential for risks related to cybersecurity, confidentiality and data privacy.

9

As of the date of this report, we have been classified as an essential business in the jurisdictions that have mandated closure of non-essential businesses, and therefore have generally been allowed to remain open. However, we can give no assurance that this will not change in the future. Despite our efforts to manage and remedy the impact of COVID-19 on our financial condition and results of operations, the ultimate impact also depends on factors beyond our knowledge or control, including the duration and severity of the COVID-19 pandemic and actions taken by governmental authorities to contain its spread and mitigate its public health effects. Additionally, as the COVID-19 pandemic conditions wane, we cannot predict how quickly the marketplaces in which we operate will return to normal. Any of the foregoing factors, or other cascading effects of the COVID-19 pandemic that are not currently foreseeable, could materially increase our costs, negatively impact our sales and damage our results of operations and liquidity position. The duration of any such impacts cannot be predicted. See further discussion in Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations.

Reliance on third-party relationships and outsourcing arrangements could adversely affect our business.

We rely on third parties, including suppliers, distributors, alliances with other companies, and third-party service providers, for selected aspects of product development, manufacture, commercialization, support for information technology systems, product distribution, and certain financial transactional processes. Additionally, we have outsourced certain functions to third-party service providers to leverage leading specialized capabilities and achieve cost efficiencies. Outsourcing these functions involves the risk that third-party service providers may not perform to our standards or legal requirements, may not produce reliable results, may not perform in a timely manner, may not maintain the confidentiality of our proprietary information, or may fail to perform at all. Additionally, any disruption, such as a government shutdown, war, natural disaster or global pandemic (including the current COVID-19 pandemic), could affect the ability of our third-party service providers to meet their contractual obligations to us. Failure of these third parties to meet their contractual, regulatory, confidentiality or other obligations to us could result in material financial loss, higher costs, regulatory actions, and reputational harm.

Uncertain global economic conditions may adversely impact demand for our products or cause our customers and other business partners to suffer financial hardship, which could adversely impact our business.

Our business could be negatively impacted by reduced demand for our products related to one or more significant local, regional or global economic disruptions, the risk of which are aggravated by the COVID-19 pandemic, such as: a slow-down in the general economy; reduced market growth rates; increased inflation rates, tighter credit markets for our suppliers, vendors or customers; a significant shift in government policies; the deterioration of economic relations between countries or regions, including potential negative consumer sentiment toward non-local products or sources; or the inability to conduct day-to-day transactions through our financial intermediaries to pay funds to, or collect funds from, our customers, vendors and suppliers. Additionally, economic conditions may cause our suppliers, distributors, contractors or other third-party partners to suffer financial difficulties that they cannot overcome, resulting in their inability to provide us with the materials and services we need, in which case our business and results of operations could be adversely affected. Customers may also suffer financial hardships due to economic conditions such that their accounts become uncollectible or are subject to longer collection cycles. In addition, if we are unable to generate sufficient income and cash flow, it could affect the Company’s ability to achieve expected share repurchase and dividend payments.

Disruption in our global supply chain may negatively impact our business results.

Our ability to meet our customers’ needs and achieve cost targets depends on our ability to maintain key manufacturing and supply arrangements, including execution of supply chain optimizations and certain sole supplier or sole manufacturing plant arrangements. The loss or disruption of such manufacturing and supply arrangements, including for issues such as labor disputes, labor shortages, loss or impairment of key manufacturing sites, discontinuity in our internal information and data systems, inability to procure sufficient raw or input materials, significant changes in trade policy, natural disasters, increasing severity or frequency of extreme weather events due to climate change or otherwise, acts of war or terrorism, the COVID-19 pandemic or other disease outbreaks or other external factors over which we have no control, including inflation, have interrupted product supply and, if not effectively managed and remedied, could have an adverse impact on our business, financial condition or results of operations.

We participate in very competitive markets and we may not be able to compete successfully, causing us to lose market share and sales.

We compete for consumer acceptance and limited shelf space based upon brand name recognition, perceived product quality, price, performance, product features and enhancements, product packaging and design innovation, as well as creative marketing, promotion and distribution strategies, and new product introductions. Additional discussion over the segments, product categories, and markets in which we compete are included under Item 1 above. Our ability to compete in these consumer product markets may be adversely affected by a number of factors, including, but not limited to, the following:

•We compete against many well-established companies that may have substantially greater financial and other resources, including personnel and research and development, and greater overall market share than us.

•In some key product lines, our competitors may have lower production costs and higher profit margins than us, which may enable them to compete more aggressively in offering retail discounts, rebates and other promotional incentives.

•Technological advancements, product improvements or effective advertising campaigns by competitors may weaken consumer demand for our products.

•Consumer purchasing behavior may shift to distribution channels, including to online retailers, where we and our customers do not have a strong presence.

•Consumer preferences may change to lower margin products or products other than those we market.

•We may not be successful in the introduction, marketing and manufacture of any new products or product innovations or be able to develop and introduce, in a timely manner, innovations to our existing products that satisfy customer needs or achieve market acceptance.

In addition, in a number of our product lines, we compete with our retail customers, who use their own private label brands, and with distributors and foreign manufacturers of unbranded products. Significant new competitors or increased competition from existing competitors, including specifically private label brands, may adversely affect our business, financial condition and results of our operations.

Some competitors may be willing to reduce prices and accept lower profit margins to compete with us. As a result of this competition, we could lose market share and sales, or be forced to reduce our prices to meet competition. If our product offerings are unable to compete successfully, our sales, results of operations and financial condition could be materially and adversely affected. In addition, we may be unable to implement changes to our products or otherwise adapt to changing consumer trends. If we are unable to respond to changing consumer trends, our operating results and financial condition could be adversely affected.

10

Changes in consumer shopping trends and changes in distribution channels could significantly harm our business

We sell our products through a variety of trade channels with a significant portion dependent upon retail partnerships, through both traditional brick-and-mortar retail channels and e-commerce channels. We are seeing the emergence of strong e-commerce channels generating more online competition and declining in-store traffic in brick-and-mortar retailers. Consumer shopping preferences have shifted and may continue to shift in the future to distribution channels other than traditional retail that may have more limited experience, presence and developed, such as e-commerce channels. If we are not successful in developing and utilizing e-commerce channels that future consumers may prefer, we may experience lower than expected revenues.

We are also seeing more traditional brick-and-mortar retailers closing physical stores, and filing for bankruptcy, which could negatively impact our distribution strategies and/or sales if such retailers decide to significantly reduce their inventory levels for our products or to designate more floor space to our competitors. Further consolidation, store closures and bankruptcies could have a material adverse effect on our business, prospects, financial condition, results of operations, cash flows, as well as the trading price of our securities.

Consolidation of retailers and our dependence on a small number of key customers for a significant percentage of our sales may negatively affect our business, financial condition and results of operations.

As a result of consolidation of retailers that has occurred during the past several years, particularly in the United States and the EU, and consumer trends toward national mass merchandisers, a significant percentage of our sales are attributable to a limited group of customers. As these mass merchandisers and retailers grow larger and become more sophisticated, they may demand lower pricing, special packaging or impose other requirements on product suppliers. These business demands may relate to inventory practices, logistics or other aspects of the customer-supplier relationship. Because of the importance of these key customers, demands for price reductions or promotions, reductions in their purchases, changes in their financial condition or loss of their accounts could have a material adverse effect on our business, financial condition and results of operations. Our success is dependent on our ability to manage our retailer relationships, including offering mutually acceptable trade terms.

Although we have long-established relationships with many of our customers, we generally do not have long-term agreements with them and purchases are normally made through the use of individual purchase orders. Any significant reduction in purchases, failure to obtain anticipated orders or delays or cancellations of orders by any of these major customers, or significant pressure to reduce prices from any of these major customers, could have a material adverse effect on our business, financial condition and results of operations. Additionally, a significant deterioration in the financial condition of the retail industry in general, the bankruptcy of any of our customers or any of our customers ceasing operations could have a material adverse effect on our sales and profitability.

As a result of retailers maintaining tighter inventory control, we face risks related to meeting demand and storing inventory.

As a result of the desire of retailers to more closely manage inventory levels, there is a growing trend among them to purchase products on a “just-in-time” basis. Due to a number of factors, including (i) manufacturing lead-times, (ii) seasonal purchasing patterns, and (iii) the potential for material price increases, we may be required to shorten our lead-time for production and more closely anticipate our retailers’ and customers’ demands, which could in the future require us to carry additional inventories and increase our working capital and related financing requirements. This may increase the cost of warehousing inventory or result in excess inventory becoming difficult to manage, unusable or obsolete. In addition, if our retailers significantly change their inventory management strategies, we may encounter difficulties in filling customer orders or in liquidating excess inventories or may find that customers are cancelling orders or returning products, which may have a material adverse effect on our business.

Furthermore, we primarily sell branded products and a move by one or more of our large customers to sell significant quantities of private label products, which we do not produce on their behalf and which directly compete with our products, could have a material adverse effect on our business, financial condition and results of operations.

Sales of certain of our products are seasonal and may cause our operating results and working capital requirements to fluctuate.

On a consolidated basis our financial results are approximately equally weighted across our quarters, however, sales of certain product categories tend to be seasonal. Further discussion over the seasonality of our sales is included under Item 1 above. As a result of this seasonality, our inventory and working capital needs fluctuate significantly throughout the year. In addition, orders from retailers are often made late in the period preceding the applicable peak season, making forecasting of production schedules and inventory purchases difficult. If we are unable to accurately forecast and prepare for customer orders or our working capital needs, or there is a general downturn in business or economic conditions during these periods, our business, financial condition and results of operations could be materially and adversely affected.

Adverse weather conditions during our peak selling seasons for our home and garden products could have a material adverse effect on our home and garden business.

Weather conditions have a significant impact on the timing and volume of sales of certain of our lawn and garden and household insecticide and repellent products. For example, periods of dry, hot weather can decrease insecticide sales, while periods of cold and wet weather can slow sales of herbicides. Adverse weather conditions during the first six months of the calendar year (the Company’s second and third fiscal quarters), when demand for home and garden control products typically peaks, could have a material adverse effect on our home and garden business and our financial results during such period.

Our products utilize certain key raw materials; any significant increase in the price of, or change in supply and demand for, these raw materials could have a material and adverse effect on our business, financial condition and profits.

The principal raw materials used to produce our products, including petroleum-based plastic materials and corrugated materials (for packaging), are sourced either on a global or regional basis by us or our suppliers, and the prices of those raw materials are susceptible to price fluctuations due to supply and demand trends, energy costs, transportation costs, government regulations, duties and tariffs, changes in currency exchange rates, price controls, general economic conditions, inflation, and other unforeseen circumstances. Although we may seek to increase the prices of certain of our goods to our customers, we may not be able to pass all of these cost increases on to our customers. As a result, our margins may be adversely impacted by such cost increases. We cannot provide any assurance that our sources of supply will not be interrupted due to changes in worldwide supply of or demand for raw materials or other events that interrupt material flow, which may have an adverse effect on our profitability and results of operations.

If we are not effective in managing our exposure to above average costs for an extended period of time, and we are unable to pass our raw materials costs on to our customers, our future profitability may be materially and adversely affected. Furthermore, with respect to transportation costs, certain modes of delivery are subject to fuel surcharges which are determined based upon the current cost of diesel fuel in relation to pre-established agreed upon costs. We may be unable to pass these fuel surcharges on to our customers, which may have an adverse effect on our profitability and results of operations.

11

In addition, we have exclusivity arrangements and minimum purchase requirements with certain of our suppliers for the home and garden business, which increase our dependence upon and exposure to those suppliers. Some of those agreements include caps on the price we pay for our supplies and in certain instances these caps have allowed us to purchase materials at below market prices. When we attempt to renew those contracts, the other parties to the contracts may not be willing to include or may limit the effect of those caps and could even attempt to impose above market prices in an effort to make up for any below market prices paid by us prior to the renewal of the agreement. Any failure to timely obtain suitable supplies at competitive prices could materially adversely affect our business, financial condition and results of operations.

Our dependence on a few suppliers for certain of our products makes us vulnerable to a disruption in the supply of our products.

Although we have long-standing relationships with many of our suppliers, we generally do not have long-term contracts with them. An adverse change in any of the following could have a material adverse effect on our business, financial condition and results of operations:

•our ability to identify and develop relationships with qualified suppliers;

•the terms and conditions upon which we purchase products from our suppliers, including applicable exchange rates, transport and other costs, our suppliers’ willingness to extend credit to us to finance our inventory purchases and other factors beyond our control;

•the financial condition of our suppliers;

•political and economic instability in the countries in which our suppliers are located, as a result of war, terrorist attacks, pandemics, natural disasters or otherwise;

•our ability to import outsourced products;

•our suppliers’ noncompliance with applicable laws, trade restrictions and tariffs; or

•our suppliers’ ability to manufacture and deliver outsourced products according to our standards of quality on a timely and efficient basis.

If our relationship with one of our key suppliers is adversely affected, we may not be able to quickly or effectively replace such supplier and may not be able to retrieve tooling, molds or other specialized production equipment or processes used by such supplier in the manufacture of our products. The loss of one or more of our suppliers, a material reduction in their supply of products or provision of services to us or extended disruptions or interruptions in their operations could have a material adverse effect on our business, financial condition and results of operations.

Our home and garden products are mainly manufactured from our St. Louis, MO, facility and our aquatics products and certain companion animal products are manufactured in Blacksburg, VA, Bridgeton, MO, Noblesville IN and Melle, Germany. We are dependent upon the continued safe operation of these facilities.

Our facilities are subject to various hazards associated with the manufacturing, handling, storage, and transportation of chemical materials and products, including human error, leaks and ruptures, explosions, floods, fires, inclement weather and natural disasters, power loss or other infrastructure failures, mechanical failure, unscheduled downtime, regulatory requirements, the loss of certifications, technical difficulties, labor disputes, inability to obtain material, equipment or transportation, environmental hazards such as remediation, chemical spills, discharges or releases of toxic or hazardous substances or gases, and other risks. Many of these hazards could cause personal injury and loss of life, severe damage to, or destruction of, property and equipment and environmental contamination. In addition, the occurrence of material operation problems at our facilities due to any of these hazards could cause a disruption in the production of products. We may also encounter difficulties or interruption as a result of the application of enhanced manufacturing technologies or changes to production lines to improve throughput or to upgrade or repair its production lines. The Company’s insurance policies have coverage in case of significant damage to its manufacturing facilities but may not fully compensate for the cost of replacement for any such damage and any loss from business interruption. As a result, we may not be adequately insured to cover losses resulting from significant damage to its manufacturing facility. Any damage to its facility or interruption in manufacturing could result in production delays and delays in meeting contractual obligations which could have a material adverse effect on relationships with customers and on its results of operations, financial condition or cash flows in any given period.

We face risks related to our sales of products obtained from third-party suppliers.

We sell a significant number of products that are manufactured by third-party suppliers over which we have no direct control. While we have implemented processes and procedures to try to ensure that the suppliers we use are complying with all applicable regulations, there can be no assurances that such suppliers in all instances will comply with such processes and procedures or otherwise with applicable regulations. Noncompliance could result in our marketing and distribution of contaminated, defective or dangerous products which could subject us to liabilities and could result in the imposition by governmental authorities of procedures or penalties that could restrict or eliminate our ability to purchase products. Any or all of these effects could adversely affect our business, financial condition, and results of operations.

Additionally, the impact of economic conditions of our suppliers cannot be predicted and our suppliers may be unable to access financing or become insolvent and thus become unable to supply us with products. Development in tax policy, such as the imposition of tariffs on imported goods, could further have a material adverse effect on our results of operations and liquidity.

In addition, the Dodd-Frank Wall Street Reform and Consumer Protection Act includes provisions regarding certain minerals and metals, known as conflict minerals, mined from the Democratic Republic of Congo and adjoining countries. These provisions require companies to undertake due diligence procedures and report on the use of conflict minerals in its products, including products manufactured by third parties. Compliance with these provisions causes us to incur costs to certify that our supply chain is conflict free and we may face difficulties if our suppliers are unwilling or unable to verify the source of their materials. Our ability to source these minerals and metals may also be adversely impacted. In addition, our customers may require that we provide them with a certification and our inability to do so may disqualify us as a supplier.

If we are unable to negotiate satisfactory terms to continue existing or enter into additional collective bargaining agreements, we may experience an increased risk of labor disruptions and our results of operations and financial condition may suffer.

While we currently expect to negotiate continuations to the terms of these agreements, there can be no assurances that we will be able to obtain terms that are satisfactory to us or otherwise to reach agreement at all with the applicable parties. In addition, in the course of our business, we may also become subject to additional collective bargaining agreements. These agreements may be on terms that are less favorable than those under our current collective bargaining agreements. Increased exposure to collective bargaining agreements, whether on terms more or less favorable than our existing collective bargaining agreements, could adversely affect the operation of our business, including through increased labor expenses. While we intend to comply with all collective bargaining agreements to which we are subject, there can be no assurances that we will be able to do so and any noncompliance could subject us to disruptions in our operations and materially and adversely affect our results of operations and financial condition. For additional information see the discussion over the Company’s labor force subject to collective bargaining agreements under the caption Employees in Item 1 above.

12

Significant changes in actual investment return on pension assets, discount rates, and other factors could affect our results of operations, equity and pension contributions in future periods.

Our results of operations may be positively or negatively affected by the amount of income or expense we record for our defined benefit pension plans. Accounting Principles Generally Accepted in the United States (“GAAP”) requires that we calculate income or expense for the plans using actuarial valuations. These valuations reflect assumptions about financial markets and other economic conditions, which may change based on changes in key economic indicators. The most significant assumptions we use to estimate pension income or expense are the discount rate and the expected long-term rate of return on plan assets. In addition, we are required to make an annual measurement of plan assets and liabilities, which may result in a significant change to equity. Although pension expense and pension funding contributions are not directly related, key economic factors that affect pension expense would also likely affect the amount of cash we would contribute to pension plans as required under the Employee Retirement Income Security Act of 1974, as amended.

Our business may be materially affected by changes to fiscal and tax policies that could adversely affect our results of operations and cash flows.

We operate globally and changes in tax laws could adversely affect our results. On December 22, 2017, the Tax Cuts and Jobs Act (the “Tax Reform Act”) was signed into law. The legislation, which became effective on January 1, 2018, significantly changed U.S. tax law by, among other things, lowering corporate income tax rates, implementing a dividends received deduction for dividends from foreign subsidiaries, imposing a repatriation tax on deemed repatriated earnings of foreign subsidiaries, a minimum tax on foreign earnings, limitations on deduction of business interest expense and limits on deducting compensation to certain executive officers. Additional tax regulations and interpretations of the Tax Reform Act have been, and continue to be, issued, some with retroactive application dates and some which materially impacted the Company. The Company understands that other U.S. taxpayers have or plan to challenge the constitutionality of a set of regulations that had a material impact on the Company. If the regulations were ruled unconstitutional, the Company could be favorably impacted. New or revised interpretations of the Tax Reform Act and state conformity with its provisions could have a material impact on the valuation allowance recorded on U.S. state net operating losses. Certain of these changes could have a negative or adverse impact on the operating results and cash flows of the Company. See Note 16 – Income Taxes in the Notes to the Consolidated Financial Statements included elsewhere in this Annual Report for further discussion on the impact from the Tax Reform Act.

We may not be able to fully utilize our U.S. tax attributes.

The Company has accumulated a substantial amount of U.S. federal and state net operating loss (“NOLs”) carryforwards, and federal and state tax credits that will expire if unused. We have concluded that it is more likely than not that the majority of the federal and state deferred tax assets will create tax benefits in the future. As a consequence of earlier business combinations and issuances of common stock, the Company and its subsidiaries have had various changes of ownership that continue to subject a significant amount of the Company’s U.S. NOLs and other tax attributes to certain limitations; and therefore a valuation allowance is still recognized on certain federal and state tax asset carryforwards that are expected to expire due to the ownership change limitations or because we do not believe we will earn enough taxable income to utilize. Changes to state conformity to the provisions of the Tax Reform Act could have a material impact on the valuation allowance recorded on U.S. state net operating losses. If we are unable to fully utilize our NOLs to offset taxable income generated in the future, our future cash taxes could be materially and negatively impacted. For further discussion on the Company’s federal and state NOLs, credits, and applicable valuation allowance as of September 30, 2021, see Note 16 – Income Taxes in the Notes to the Consolidated Financial Statements included elsewhere in this Annual Report.

Our strategic initiatives including acquisitions and divestitures may not be successful and may divert our management’s attention away from operations and could create general customer uncertainty.