Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

Annual Report for the fiscal year ended July 31, 2013

Zale Corporation

A Delaware Corporation

IRS Employer Identification No. 75-0675400

SEC File Number 1-04129

901 W. Walnut Hill Lane

Irving, Texas 75038-1003

(972) 580-4000

Zale Corporation's common stock, par value $0.01 per share, is registered pursuant to Section 12 (b) of the Securities Exchange Act of 1934 (the "Act") and is listed on the New York Stock Exchange. Zale Corporation does not have any securities registered under Section 12(g) of the Act. Zale Corporation is not a well-known seasoned issuer. Zale Corporation is required to file reports pursuant to Section 13 of the Act. Zale Corporation (1) has filed all reports required to be filed by Section 13 or 15(d) of the Act during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days.

Zale Corporation has submitted electronically and posted on the Company's website all Interactive Data Files required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Company was required to submit and post such files).

Disclosure of the delinquent filers pursuant to Item 405 of Regulation S-K will not be contained in our definitive Proxy Statement, portions of which are incorporated by reference in Part III of this Form 10-K.

Zale Corporation is an accelerated filer.

Zale Corporation is not a shell company.

The aggregate market value of Zale Corporation's common stock (based upon the closing sales price quoted on the New York Stock Exchange) held by non-affiliates as of January 31, 2013 was $157,946,032. For this purpose, directors and officers have been assumed to be affiliates. As of September 23, 2013, 32,764,729 shares of Zale Corporation's common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE.

Portions of Zale Corporation's definitive Proxy Statement for the 2013 Annual Meeting of Stockholders to be held on December 5, 2013 are incorporated by reference into Part III.

ZALE CORPORATION AND SUBSIDIARIES

General

References to the "Company," "we," "us," and "our" in this Form 10-K are references to Zale Corporation and its subsidiaries. We are, through our wholly owned subsidiaries, a leading specialty retailer of fine jewelry in North America. At July 31, 2013, we operated 1,064 specialty retail jewelry stores and 630 kiosks located mainly in shopping malls throughout the United States, Canada and Puerto Rico.

We were incorporated in Delaware in 1993. Our principal executive offices are located at 901 W. Walnut Hill Lane, Irving, Texas 75038-1003. Our telephone number at that address is (972) 580-4000, and our internet address is www.zalecorp.com.

During the fiscal year ended July 31, 2013, we generated $1.9 billion of revenues. We compete in the approximately $79 billion U.S. and Canadian retail jewelry industry by leveraging our established brand names, economies of scale and geographic and demographic diversity. We have significant brand name recognition as a result of each of our brands' long-standing presence in the industry and our national and regional marketing campaigns. We believe that brand name recognition is an important advantage in jewelry retailing and consumers must trust a retailer's reliability, credibility and commitment to customer service. In addition, exclusive merchandise is becoming an increasingly important part of the retail jewelry business and presents a significant opportunity to differentiate our merchandise from the competition.

Business Segments

We report our operations under three business segments: Fine Jewelry, Kiosk Jewelry and All Other. An overview of each business segment follows below. During fiscal year 2013, Fine Jewelry generated $1.6 billion, or 86.7 percent of our revenues and Kiosk Jewelry generated $239.7 million, or 12.7 percent of our revenues.

Fine Jewelry

Fine Jewelry is comprised of our three core national brands, Zales Jewelers®, Zales Outlet® and Peoples Jewellers® and our two regional brands, Gordon's Jewelers® and Mappins Jewellers®. Each brand specializes in fine jewelry and watches, with merchandise and marketing emphasis focused on diamond products. Zales Jewelers® is a value-oriented jeweler in the U.S. offering a broad range of bridal, diamond solitaire and fashion jewelry. Zales Outlet® operates in outlet malls and neighborhood power centers and capitalizes on Zales Jewelers'® national marketing and brand recognition. Gordon's Jewelers®, our regional brand in the U.S., provides moderately priced jewelry to a wide range of guests. Peoples Jewellers®, Canada's largest fine jewelry retailer, provides guests with an affordable assortment and an accessible shopping experience. Mappins Jewellers® offers Canadian guests a broad selection of merchandise from engagement rings to fashionable and contemporary fine jewelry. We have extended our reach of certain brands through the use of our webstores, mobile devices and social media to provide our guests access to our brands wherever and whenever they choose. In addition, we offer our guests the option to purchase warranty coverage on substantially all of our merchandise in Fine Jewelry. We also offer repair services to guests who do not purchase warranty coverage.

Zales Jewelers and Zales Outlet

Zales Jewelers ("Zales"), our U.S. based flagship, is a leading brand name in jewelry retailing in the U.S., operating 614 stores in 50 states and Puerto Rico with an average store size of 1,682 square feet. Zales is positioned as "The Diamond Store" given its emphasis on diamond jewelry, especially in the bridal and fashion segments. The Zales brand complements its merchandise assortments with promotional strategies to increase sales during traditional gift-giving periods and throughout the year. We believe that

1

the prominence of diamond jewelry in our product selection and Zales' reputation for customer service for close to 90 years fosters an image of product expertise, quality and trust among consumers. Zales accounted for 52 percent of total revenues in fiscal year 2013, with average sales per location of $1.6 million. Zales serves internet guests through the ecommerce site www.zales.com, which accounted for approximately four percent of our total revenues in fiscal year 2013. Internet sales totaled approximately $84 million in fiscal year 2013 compared to approximately $77 million in fiscal year 2012.

We operate 127 Zales Outlet ("Outlet") stores in 35 states and Puerto Rico, with an average store size of 2,361 square feet. The outlet concept has evolved into three differentiated formats: power strip centers, traditional outlet malls and destination centers. Outlet was established as an extension of the Zales brand and capitalizes on Zales' national marketing and brand recognition. Our stores feature items in every major jewelry category including exclusive bridal designs, branded watches, gemstones, gold merchandise, diamond fashion and solitaire products. Outlet accounted for 10 percent of total revenues in fiscal year 2013, with average sales per location of $1.5 million. Outlet also serves internet guests through the ecommerce sites www.zalesoutlet.com, which accounted for less than one percent of our total revenues in fiscal year 2013. Internet sales totaled approximately $2 million in fiscal years 2013 and 2012.

Revenues from our Zales branded stores, which includes Zales and Zales Outlet, accounted for 62 percent of total revenues in fiscal year 2013. Internet sales for Zales branded stores totaled approximately $86 million and $79 million in fiscal years 2013 and 2012, respectively.

Peoples Jewellers

Peoples Jewellers ("Peoples") is a leading brand name in jewelry retailing in Canada, operating 146 stores in nine provinces with an average store size of 1,630 square feet. Peoples is one of the most recognized brand names in Canada and enjoys the largest market share of any specialty jewelry retailer. Peoples was founded in 1919 and offers jewelry at affordable prices, attracting a wide variety of Canadian guests. Using the trademark "Peoples the Diamond Store", Peoples emphasizes its diamond business while also offering a wide selection of gold jewelry, gemstone jewelry and watches. The Peoples brand has built recognition through a marketing campaign that primarily includes television and print media. Peoples accounted for 14 percent of total revenues in fiscal year 2013, with average sales per location of $1.7 million. Peoples serves internet guests through the ecommerce site, www.peoplesjewellers.com. Internet sales totaled approximately $6 million in fiscal year 2013 compared to approximately $4 million in fiscal year 2012.

Gordon's Jewelers

Gordon's Jewelers ("Gordon's"), our regional brand in the U.S., was founded in 1905 and operates 122 stores in 24 states and Puerto Rico with an average store size of 1,546 square feet. Gordon's features items in every major jewelry category including exclusive bridal designs, branded watches, gemstones, gold merchandise, and diamond fashion and solitaire products. Gordon's accounted for eight percent of total revenues in fiscal year 2013, with average sales per location of $1.1 million. Gordon's serves internet guests through the ecommerce site www.gordonsjewelers.com. Internet sales totaled approximately $5 million in fiscal years 2013 and 2012.

Mappins Jewellers

Mappins Jewellers ("Mappins"), our regional brand in Canada, was founded in 1935 and operates 55 stores in six provinces with an average store size of 1,560 square feet. Mappins differentiates itself by offering exclusive merchandise primarily in its bridal assortment and branded jewelry lines. Mappins accounted for three percent of total revenues in fiscal year 2013, with average sales per location of $1.1 million.

2

Kiosk Jewelry

Kiosk Jewelry operates under the brand names Piercing Pagoda®, Plumb Gold™, and Silver and Gold Connection® (collectively, "Piercing Pagoda") through mall-based kiosks and is focused on the opening price point guest. At July 31, 2013, Piercing Pagoda operated 630 locations in 41 states and Puerto Rico with an average kiosk size of 190 square feet. Kiosks are generally located in high traffic areas that are easily accessible and visible within regional shopping malls. At the entry-level price point, Piercing Pagoda services fashion conscious guests of all ages. Piercing Pagoda offers an extensive collection of bracelets, earrings, charms, rings, non-precious metal products and gold chains, as well as a selection of silver and diamond jewelry, all in basic styles at moderate prices. In addition, trained associates perform ear-piercing services on site. Piercing Pagoda accounted for 13 percent of total revenues in fiscal year 2013, with average sales per location of $0.4 million. Piercing Pagoda serves internet guests through the ecommerce site www.pagoda.com. Internet sales totaled approximately $2 million in both fiscal year 2013 and 2012.

All Other

We provide insurance and reinsurance services for various types of insurance coverage, which are marketed to our private label credit card guests, through Zale Indemnity Company, Zale Life Insurance Company and Jewel Re-Insurance Ltd. These three companies are the insurers (either through direct written or reinsurance contracts) of our guests' credit insurance coverage. In addition to providing merchandise replacement coverage for certain perils, credit insurance coverage provides protection to the creditor and cardholder for losses associated with the disability, involuntary unemployment, leave of absence or death of the cardholder. Zale Life Insurance Company also provides group life insurance coverage for our eligible employees. Zale Indemnity Company, in addition to writing direct credit insurance contracts, has certain discontinued lines of insurance that it continues to service. Credit insurance operations are dependent on our retail sales through our private label credit cards. In fiscal year 2013, 38 percent of our private label credit card purchasers purchased some form of credit insurance. Under the current private label agreement with Citibank (South Dakota), N.A. ("Citibank"), our insurance affiliates provide insurance to holders of our U.S. private label credit card and receive payments for such insurance products. Under the current private label agreement with TD Financing Services, Inc. ("TDFS"), TDFS provides credit insurance to holders of our Canadian private label credit card and receives 40 percent of the net profits and the remaining 60 percent is paid to us. In fiscal year 2013, All Other accounted for approximately one percent of our total revenues.

Ecommerce Business

The webstores for Zales, Zales Outlet, Gordon's, Peoples and Piercing Pagoda provide our guests with a source of information about the merchandise available, as well as the ability to buy online. The webstores allow guests to order merchandise online that may be delivered directly to the guest or picked up at a store. For the year ended July 31, 2013, approximately 28 percent of our guests chose to pick up the merchandise from a store. The websites make an important and growing contribution to the guest experience and are an integral part of our marketing programs. In fiscal year 2013, total internet sales were $100.0 million, an increase of 11.5 percent compared to revenues of $89.7 million in fiscal year 2012. Our guests also utilize our webstores to identify merchandise online that they subsequently purchase at a store.

We continue to expand our omnichannel business through mobile devices and social media to enable our guests to buy and receive products where, when and how they want and enhance their experience as they engage with us across all of our virtual and brick and mortar channels. Our omnichannel strategy allows guests to experience our brands by providing a seamless and high-quality approach to their shopping experience. We aim to deliver the best guest experience possible through an integration of all available shopping channels including stores, websites and through mobile devices. Our followers on Facebook and Twitter and views of our YouTube advertisements continue to increase and social media outlets are driving more traffic to our stores and ecommerce sites. We believe that our web marketing, social media and

3

mobile initiatives will be a significant contributor to our future sales growth. We plan to continue to invest in these initiatives by implementing new capabilities to provide guests with an enhanced shopping experience.

Our supplier relationships allow us to display suppliers' inventories on our websites for sale to customers without holding the items in our inventory until the products are ordered by guests, which are referred to as "virtual inventory". Virtual inventory expands the choice of merchandise available to guests both online and in our stores. Virtual inventory reduces our investment in inventory while increasing the selection available to the guest.

Industry and Competition

Jewelry retailing is highly fragmented and competitive. We compete with a large number of independent regional and local jewelry retailers, as well as with other national jewelry chains. We also compete with other types of retailers who sell jewelry and gift items such as department stores, discounters, direct mail suppliers, online retailers and television home shopping programs. Certain of our competitors are non-specialty retailers, which are larger and have greater financial resources than we do. The malls where most of our stores are located typically contain competing national chains, independent jewelry stores and/or department stores with jewelry departments. We believe that we generally compete for consumers' discretionary spending dollars and, therefore, compete with retailers who offer merchandise other than jewelry. Therefore, we compete primarily on the basis of our reputation for high quality products, brand recognition, store location, distinctive and value-oriented merchandise, personalized customer service and ability to offer a variety of credit programs to guests wishing to finance their purchases. Our success also is dependent on our ability to both create and react to guest demand for specific merchandise categories.

The U.S. and Canadian retail jewelry industry accounted for approximately $79 billion of sales in 2012 according to publicly available data, of which approximately $33 billion is specialty jewelry. We have a 5.7 percent market share in the combined U.S. and Canadian specialty jewelry markets. The largest jewelry retailer in the combined U.S. and Canadian markets is believed to be Wal-Mart Stores, Inc. Other significant segments of the fine jewelry industry include national chain department stores (such as J.C. Penney Company, Inc.), mass merchant discount stores (such as Wal-Mart Stores, Inc.), other general merchandise stores, specialty retail jewelers (such as Signet Jewelers Limited) and apparel and accessory stores. The remainder of the retail jewelry industry is comprised primarily of catalog and mail order houses, direct-selling establishments, TV shopping networks (such as QVC, Inc.) and online jewelers.

We hold no material patents, licenses, franchises or concessions; however, our established trademarks and trade names are essential to maintaining our competitive position in the retail jewelry industry.

4

Operations by Brand and Merchandise Mix

The following table presents revenues, comparable store sales and average sales per location for each of our brands for the periods indicated.

| |

Year Ended July 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

Revenues (in thousands)

|

2013 | 2012 | 2011 | |||||||

Zales |

$ | 982,409 | $ | 948,353 | $ | 852,362 | ||||

Outlet |

194,767 | 188,151 | 167,960 | |||||||

Peoples |

254,550 | 243,147 | 227,534 | |||||||

Gordon's |

143,278 | 168,179 | 174,865 | |||||||

Mappins |

62,355 | 69,854 | 70,573 | |||||||

Piercing Pagoda |

239,722 | 238,692 | 239,231 | |||||||

All Other |

10,935 | 10,502 | 10,038 | |||||||

|

$ | 1,888,016 | $ | 1,866,878 | $ | 1,742,563 | ||||

Comparable Store Sales(a)

|

||||||

Zales |

4.9% | 11.0% | 8.4% | |||

Outlet |

3.3% | 9.6% | 8.8% | |||

Peoples |

5.7% | 4.3% | 14.0% | |||

Gordon's |

(3.6)% | 1.7% | 3.6% | |||

Mappins |

(6.7)% | (1.5)% | 11.9% | |||

Piercing Pagoda |

1.3% | (1.0)% | 3.6% | |||

Total Company |

3.3% | 6.9% | 8.1% | |||

Comparable Store Sales (in constant currency)(a)

|

||||||

Peoples |

4.8% | 5.9% | 7.9% | |||

Mappins |

(7.5)% | 0.1% | 5.9% |

Average Sales Per Location (in thousands)(b):

|

||||||||||

Zales |

$ | 1,571 | $ | 1,470 | $ | 1,286 | ||||

Outlet |

1,521 | 1,418 | 1,239 | |||||||

Peoples |

1,713 | 1,623 | 1,490 | |||||||

Gordon's |

1,079 | 1,032 | 964 | |||||||

Mappins |

1,095 | 1,171 | 1,181 | |||||||

Piercing Pagoda |

377 | 361 | 356 |

- (a)

- Comparable

store sales include internet sales and repair sales but exclude revenue recognized from warranties and insurance premiums related to credit

insurance policies sold to guests who purchase merchandise under our proprietary credit programs. Stores closed for more than 90 days due to unforeseen events (e.g., hurricanes, etc.)

are excluded from the calculation of comparable store sales.

- (b)

- Average sales per location include merchandise sales, internet sales, repair revenue and warranties for locations open a full 12 months during the applicable year.

5

The following table presents the number of locations for each of our brands for the periods indicated.

| |

Locations by Brand | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

Year Ended July 31, 2013

|

Locations Opened During Period |

Locations Closed During Period |

Locations at End of Period |

|||||||

Zales |

— | 25 | 614 | |||||||

Outlet |

1 | 6 | 127 | |||||||

Peoples |

— | 1 | 146 | |||||||

Gordon's |

— | 25 | 122 | |||||||

Mappins |

— | 4 | 55 | |||||||

Piercing Pagoda |

12 | 36 | 630 | |||||||

|

13 | 97 | 1,694 | |||||||

Year Ended July 31, 2012

|

||||||||||

Zales |

9 | 20 | 639 | |||||||

Outlet |

1 | 1 | 132 | |||||||

Peoples |

— | 1 | 147 | |||||||

Gordon's |

— | 21 | 147 | |||||||

Mappins |

— | 6 | 59 | |||||||

Piercing Pagoda |

2 | 14 | 654 | |||||||

|

12 | 63 | 1,778 | |||||||

Year Ended July 31, 2011

|

||||||||||

Zales |

1 | 26 | 650 | |||||||

Outlet |

2 | 6 | 132 | |||||||

Peoples |

1 | — | 148 | |||||||

Gordon's |

— | 24 | 168 | |||||||

Mappins |

— | 3 | 65 | |||||||

Piercing Pagoda |

7 | 13 | 666 | |||||||

|

11 | 72 | 1,829 | |||||||

The following table presents Fine Jewelry's merchandise mix for the periods indicated (excludes repair sales, revenue recognized from warranties and insurance premiums related to credit insurance).

| |

Year Ended July 31, | |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2013 | 2012 | 2011 | |

|||||||||

Diamond jewelry |

68 | % | 68 | % | 68 | % | |||||||

Gold and silver jewelry, including beads |

15 | 15 | 14 | ||||||||||

Watches |

4 | 4 | 5 | ||||||||||

Other |

13 | 13 | 13 | ||||||||||

|

100 | % | 100 | % | 100 | % | |||||||

Business Segment Data

Information concerning sales, segment income and total assets attributable to each of our business segments is set forth below in Item 6, "Selected Financial Data," Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations," and in the "Notes to Consolidated Financial Statements," all of which are incorporated herein by reference.

6

Exclusive, Branded Merchandise

We believe that offering exclusive, branded merchandise to our guests raises the profile of our brands and helps to drive sales. Such merchandise also has significantly less exposure to competitive discounting. Our exclusive, branded merchandise includes our Vera Wang LOVE collection and our Celebration Diamond Collection™. The Vera Wang LOVE collection is designed by the most recognizable name in the wedding business, Vera Wang, and includes diamond engagement rings, wedding bands and diamond solitaires. As a result of the success of this merchandise, we intend to expand the collection during the fiscal year 2014 Holiday season. In fiscal year 2013, we reintroduced our Celebration Diamond Collection™, which consists of diamond jewelry that has been expertly cut to maximize its brilliance and beauty. The Celebration Diamond Collection™ offers a good, better and best selection of engagement rings and diamond solitaires with the Celebration 102™, Celebration Grand™ and Celebration Fire™ product lines. During fiscal year 2013, revenue associated with our exclusive, branded merchandise increased to 11 percent of Fine Jewelry's revenue, compared to 8 percent in the prior year. We expect to increase our exclusive, branded collections to over 13 percent of Fine Jewelry's revenue in fiscal year 2014.

Guest Experience

Our stores are designed to differentiate our brands, create an attractive environment, make shopping convenient and enjoyable, and maximize operating efficiencies, all of which enhance the guest experience. Our store layout is designed to optimize merchandise presentation, which provides particular focus on arrangement of showcases, lighting and materials. To support peak selling seasons, merchandise presentations are changed periodically.

Each of our stores is led by a store manager who is responsible for store-level operations, including overall store sales, store profitability and personnel matters. Administrative functions, including purchasing, distribution and payroll, are delivered from the corporate level to maintain efficiency and lower operating costs. To protect the investment in our fine jewelry, all stores also offer protection plans to our guests that provide extended warranty coverage that may be purchased at the guest's option, and competitive return and exchange policies. We also offer repair services to guests who do not purchase warranty coverage. To facilitate sales, we offer a layaway program, generally requiring a deposit of not less than 10 percent of the purchase price at the inception of the layaway transaction.

We believe it is important to provide knowledgeable and responsive guest service and we maintain a strong focus on connecting with the guest, both through our marketing and in-store communications and service. Our goal is to form and sustain an effective relationship with the guest from the first sale. We maintain a centralized customer service center to deliver efficient and effective service to our guests.

We consistently focus on the level and frequency of our employee education and training programs, particularly with store managers and jewelry consultants. We provide selling and merchandise product training for all store personnel. We continue to utilize our Engage training program to ensure our jewelry consultants across all brands provide a consistent guest experience. We offer Diamond Council of America ("DCA") training to our store managers, district managers, regional directors and full-time jewelry consultants to provide a more in-depth understanding of the technical aspects of selling diamonds. At July 31, 2013, 76 percent of our eligible full-time store personnel were DCA certified compared to 62 percent last year.

Purchasing and Inventory

We purchase the majority of our merchandise in finished form from a network of established suppliers and manufacturers located primarily in the United States, India, Southeast Asia and Italy. We purchase products from 28 countries and operate a manufacturing subsidiary that is our largest supplier of finished products. At the end of fiscal year 2013, approximately 16 percent of our total inventory represented raw materials and finished goods in our distribution centers. All purchasing is done through buying offices at

7

our corporate headquarters ("Store Support Center"). Consignment inventory has historically consisted of test programs, merchandise at higher price points or merchandise that otherwise does not warrant the risk of ownership. We had $149.1 million and $118.4 million of consignment inventory on hand at July 31, 2013 and 2012, respectively. During both fiscal years 2013 and 2012, we purchased approximately 22 percent of our finished merchandise from our top five vendors (excluding finished merchandise produced by our manufacturing subsidiary) with no single vendor exceeding ten percent. If our supply with these top vendors were disrupted, particularly at certain critical times during the year, our sales could be adversely affected in the short term until alternative supply arrangements could be established.

In fiscal year 2013, we began a comprehensive, multi-year program to review all aspects of merchandise sourcing including optimization of make-or-buy alternatives, more efficient diamond sourcing and an assessment of standard vendor payment terms. We expect to begin realizing benefits from this initiative in fiscal year 2014, with acceleration of those benefits in fiscal year 2015.

We maintain stringent inventory control systems, extensive security systems and loss prevention procedures to minimize inventory losses. We screen employment applicants and provide our store personnel with training in loss prevention. Despite such precautions, we experience theft losses from time to time, and maintain insurance to cover significant external losses.

As a specialty retail jeweler, we are affected by industry-wide fluctuations in the prices of diamonds, gold, silver and other metals and stones. The supply and prices of diamonds in the principal world markets are significantly influenced by a single entity, Diamond Trading Company ("DTC"), a subsidiary of the De Beers group, which has traditionally controlled the sale of a substantial percentage of the world's supply of diamonds and sells rough diamonds to worldwide diamond cutters at prices determined in its sole discretion. The availability of diamonds to the DTC and our suppliers is to some extent dependent on the political environment in diamond-producing countries and on continuation of prevailing supply of rough diamonds. Any sustained interruption in the supply of diamonds could adversely affect us and the retail jewelry industry as a whole. The inverse is true with respect to any oversupply from diamond-producing countries, which could cause diamond prices to fall.

Customer Credit Programs

Our customer credit programs facilitate the sale of merchandise to guests who wish to finance their purchases rather than use cash or other payment sources. We offer revolving and interest free credit plans under our private label credit card programs, in conjunction with other alternative finance vehicles that allow our jewelry consultants to provide the guest with a variety of financing options. Approximately 35 percent of our U.S. sales were financed by customer credit in both fiscal years 2013 and 2012. Our Canadian propriety credit card sales represented approximately 18 percent and 19 percent of Canadian sales for fiscal years 2013 and 2012, respectively.

In September 2010, we entered into a five-year agreement to amend and restate various terms of the March 2001 Merchant Services Agreement with Citibank, to provide financing for our U.S. guests beginning October 1, 2010. Citibank issues private label credit cards branded with an appropriate trademark, and provides financing for our U.S. guests to purchase merchandise in exchange for payment by us of a merchant fee based on a percentage of each credit card sale. The merchant fee varies according to the credit plan that is chosen by the guest (i.e., revolving, interest free). The agreement also enables us to write credit insurance. In July 2013, the Company provided written notice to Citibank of its intent not to renew the agreement upon expiration in October 2015.

On July 9, 2013, we entered into a Private Label Credit Card Program Agreement (the "ADS Agreement") with an affiliate of Alliance Data Systems Corporation ("ADS") to provide financing to our U.S. guests to purchase merchandise through private label credit cards beginning no later than October 1, 2015. In addition, ADS will provide marketing, analytical and technical services and has the option to

8

participate in certain special financing programs prior to the commencement of the agreement. The ADS Agreement will replace our current agreement with Citibank which expires on October 1, 2015.

In May 2010, we entered into a five-year Private Label Credit Card Program Agreement with TDFS to provide financing for our Canadian guests to purchase merchandise through private label credit cards beginning July 1, 2010. The agreement with TDFS replaced the agreement with Citi Cards Canada Inc., which expired on June 30, 2010.

We also enter into agreements with certain other lenders to offer alternative financing options to our U.S. guests who have been declined by Citibank. During fiscal year 2013, we expanded our alternate credit program by entering into an agreement with Genesis Financial Solutions, Inc. to provide additional financing options to our U.S. guests.

Employees

As of July 31, 2013, we had approximately 11,900 employees, of whom approximately 13 percent were Canadian employees and less than one percent of whom were represented by unions. In addition, we typically hire temporary employees during November and December of each year, the Holiday season.

Seasonality

As a specialty retailer of fine jewelry, our business is seasonal in nature, with our second fiscal quarter, which includes the holiday months of November and December, accounting for a disproportionately greater percentage of annual sales and cash flow than the other three quarters. Other important periods include Valentine's Day and Mother's Day. We expect such seasonality to continue.

Information Technology

Our technology systems provide information necessary for: (i) store operations; (ii) inventory control; (iii) profitability monitoring; (iv) customer service; (v) expense control programs; and (vi) overall management decision support. Significant data processing systems include point-of-sale reporting, purchase order management, replenishment, warehouse management, merchandise planning and control, payroll, general ledger, sales audit and accounts payable. Bar code ticketing and scanning are used at all point-of-sale terminals to ensure accurate sales and margin data compilation and to provide for inventory control monitoring. Information is made available online to merchandising staff on a timely basis, thereby increasing the merchants' ability to be responsive to changes in guest behavior. In fiscal year 2013, we began an initiative to enhance store productivity through upgrades in information technology in our Fine Jewelry stores. The upgrades include new point-of-sale hardware and software and improved connectivity in our stores. We believe this technology will improve the guest experience and the efficiency of our communication and training to our stores. Investment in the digital environment such as websites and social media further adds to the guest's shopping choices.

Our information technology systems and processes allow management to monitor, review and control operational performance on a daily, monthly, quarterly and annual basis for each store and each transaction. Senior management can review and analyze activity by store, amount of sale, terms of sale or employees who sell the merchandise.

We have an operations services agreement with a third party for the management of our client server systems, local area network operations, wide area network management and technical support. The agreement commenced in June 2010 and requires fixed payments totaling $34.5 million over a 74-month period plus a variable amount based on usage. We believe that by outsourcing our data center operations, we are better able to focus our resources on developing and executing our strategic initiatives.

9

Regulation

Our operations are affected by numerous federal and state laws that impose disclosure and other requirements upon the origination, servicing and enforcement of credit accounts and limitations on the maximum amount of finance charges that may be charged by a credit provider. In addition to our private label credit cards, credit to our guests is provided primarily through bank cards such as Visa®, MasterCard®, and Discover®. Regulations implementing the Credit Card Accountability Responsibility and Disclosure Act of 2009 imposed new restrictions on credit card pricing, finance charges and fees, customer billing practices and payment. Any change in the regulation of credit which would materially limit the availability of credit to our customer base could adversely affect our results of operations or financial condition.

We are subject to the jurisdiction of various state and other taxing authorities. From time to time, these taxing authorities conduct reviews or audits of the Company.

The sale of insurance products is also regulated. Our wholly-owned insurance companies are required to file reports with various insurance commissions, and are also subject to regulations relating to capital adequacy, the payment of dividends and the operation of their businesses generally. State laws also impose registration and disclosure obligations with respect to the credit and other insurance products that we sell to our guests. In addition, the providers of our private label credit programs are subject to disclosure and other requirements under state and federal law and are subject to review by the Federal Trade Commission and the state and federal banking regulators. The sale of certain warranty products are also regulated by state laws that impose registration and disclosure obligations with respect to warranty products that we sell to our guests.

Merchandise in the retail jewelry industry is frequently sold at a discount off the "regular" or "original" price. We are subject to federal and state regulations requiring retailers offering merchandise at promotional prices to offer the merchandise at regular or original prices for stated periods of time. Additionally, we are subject to certain truth-in-advertising and various other laws, including consumer protection regulations that regulate retailers generally and/or the promotion and sale of jewelry in particular.

Diamonds extracted from certain regions in Africa, including Zimbabwe, and believed to be used to fund terrorist activities, are considered conflict diamonds. We support the Kimberley Process, an international initiative intended to ensure diamonds are not illegally traded to fund conflict. As part of this initiative, we require our diamond suppliers to acknowledge compliance with the Kimberley Process, and invoices received for diamonds purchased by us must include a certification from the vendor that the diamonds and diamond-containing jewelry are conflict free. Through this and other efforts, we believe that the suppliers from whom we purchase our diamonds exclude conflict diamonds from their inventories.

In August 2012, the Securities and Exchange Commission ("SEC") issued rules that require companies that manufacture products using certain minerals, including gold, to determine whether those minerals originated in the Democratic Republic of Congo ("DRC") or adjoining countries. If the minerals originate in the DRC, or if companies are not able to establish where they originated, extensive disclosure regarding the sources of those minerals, and in some instances an independent audit of the supply chain, is required. The costs of complying with the new rules are not expected to be material. The Company will be required to file its first disclosure report by May 31, 2014 for the calendar year ending December 31, 2013.

Available Information

We provide links to our filings with the SEC and to the SEC filings of our directors and executive officers under Section 16 (Forms 3, 4 and 5) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), free of charge, on our website at www.zalecorp.com, under the heading "Investor Relations" in the "SEC Filings" section. These links are automatically updated, so the filings are available

10

immediately after they are made publicly available by the SEC. These filings also are available through the SEC's EDGAR system at www.sec.gov.

Our certificate of incorporation and bylaws as well as the charters for the compensation, audit, nominating and corporate governance committees of our Board of Directors and the corporate governance guidelines are available on our website at www.zalecorp.com, under the heading "About Zale Corporation" in the "Corporate Governance" section.

We have a Code of Business Conduct and Ethics (the "Code"). All of our directors, executive officers and employees are subject to the Code. The Code is available on our web site at www.zalecorp.com, under the heading "About Zale Corporation" in the "Corporate Governance" section. Waivers of the Code, if any, for directors and executive officers would be disclosed in a SEC filing on Form 8-K or, to the extent permitted by law, on our website.

We make forward-looking statements in this Annual Report on Form 10-K and in other reports we file with the SEC. In addition, members of our senior management make forward-looking statements orally in presentations to analysts, investors, the media and others. Forward-looking statements include statements regarding our objectives and expectations with respect to our financial plan (including expectations for earnings, comparable store sales, gross margin, selling, general and administrative expenses, operating margin, interest expense, income tax expense and capital expenditures for fiscal year 2014), merchandising and marketing strategies, acquisitions and dispositions, share repurchases, store openings, renovations, remodeling and expansion, inventory management and performance, liquidity and cash flows, capital structure, capital expenditures, development of our information technology and telecommunications plans and related management information systems, ecommerce initiatives, human resource initiatives and other statements regarding our plans and objectives. In addition, the words "plans to," "anticipate," "estimate," "project," "intend," "expect," "believe," "forecast," "can," "could," "should," "will," "may," or similar expressions may identify forward-looking statements, but some of these statements may use other phrasing. These forward-looking statements are intended to relay our expectations about the future, and speak only as of the date they are made. We disclaim any obligation to update or revise publicly or otherwise any forward-looking statements to reflect subsequent events, new information or future circumstances.

Forward-looking statements are not guarantees of future performance and a variety of factors could cause our actual results to differ materially from the anticipated or expected results expressed in or suggested by these forward-looking statements.

If the general economy performs poorly, discretionary spending on goods that are, or are perceived to be, "luxuries" may not grow and may decrease.

Jewelry purchases are discretionary and may be affected by adverse trends in the general economy (and consumer perceptions of those trends). In addition, a number of other factors affecting consumers such as employment, wages and salaries, business conditions, energy costs, credit availability and taxation policies, for the economy as a whole and in regional and local markets where we operate, can impact sales and earnings.

A serious economic downturn could have a material and adverse effect on our business and financial condition.

Declining confidence in either the U.S. or Canadian economies where we are active could adversely affect consumers' ability and willingness to purchase our products in those regions. Should either of these economies suffer a serious economic downturn, it could have a material and adverse effect on our business and financial condition.

11

The concentration of a substantial portion of our sales in three relatively brief selling periods means that our performance is more susceptible to disruptions.

A substantial portion of our sales are derived from three selling periods—Holiday (Christmas), Valentine's Day and Mother's Day. Because of the briefness of these three selling periods, the opportunity for sales to recover in the event of a disruption or other difficulty is limited, and the impact of disruptions and difficulties can be significant. For instance, adverse weather (such as a blizzard or hurricane), a significant interruption in the receipt of products (whether because of vendor or other product problems), or a sharp decline in mall traffic occurring during one of these selling periods could materially impact sales for the affected period and, because of the importance of each of these selling periods, commensurately impact overall sales and earnings.

Any disruption in the supply of finished goods from our largest merchandise vendors could adversely impact our sales.

We purchase substantial amounts of finished goods from our five largest merchandise vendors. If our supply with these top vendors was disrupted, particularly at certain critical times of the year, our sales could be adversely affected in the short-term until alternative supply arrangements could be established.

Most of our sales are of products that include diamonds, precious metals and other commodities. A substantial portion of our purchases and sales occur outside the United States. Fluctuations in the availability and pricing of commodities or exchange rates could impact our ability to obtain, produce and sell products at favorable prices.

The supply and price of diamonds in the principal world market are significantly influenced by the DTC, which has traditionally controlled the marketing of a substantial majority of the world's supply of diamonds and sells rough diamonds to worldwide diamond cutters at prices determined in its sole discretion. The DTC's share of the diamond supply chain has decreased over recent years, which may result in more volatility in rough diamond prices. The availability of diamonds also is somewhat dependent on the political conditions in diamond-producing countries and on the continuing supply of raw diamonds. Any sustained interruption in this supply could have an adverse affect on our business.

We also are affected by fluctuations in the price of diamonds, gold and other commodities. A significant change in prices of key commodities could adversely affect our business by reducing operating margins or decreasing consumer demand if retail prices are increased significantly. In the past, our vendors have experienced significant increases in commodity costs, especially diamond, gold and silver costs. If significant increases in commodity prices occur in the future, it could result in higher merchandise costs, which could materially impact our earnings. In addition, foreign currency exchange rates and fluctuations impact costs and cash flows associated with our Canadian operations and the acquisition of inventory from international vendors.

A substantial portion of our raw materials and finished goods are sourced in countries generally described as having developing economies. Any instability in these economies could result in an interruption of our supplies, increases in costs, legal challenges and other difficulties.

In August 2012, the SEC issued rules that require companies that manufacture products using certain minerals, including gold, to determine whether those minerals originated in the DRC or adjoining countries. If the minerals originate in the DRC, or if companies are not able to establish where they originated, extensive disclosure regarding the sources of those minerals, and in some instances an independent audit of the supply chain, is required. The costs of complying with the new rules are not expected to be material. The Company will be required to file its first disclosure report by May 31, 2014 for the calendar year ending December 31, 2013.

12

There may also be reputational risks with guests and other stakeholders if, due to the complexity of the global supply chain, we are unable to sufficiently verify the origin for the relevant metals. Also, if the responses of portions of our supply chain to the verification requests are adverse, it may harm our ability to obtain merchandise and add to compliance costs. Other minerals, such as diamonds, could be added to those currently covered by these rules.

Our sales are dependent upon mall traffic.

Our stores and kiosks are located primarily in shopping malls throughout the U.S., Canada and Puerto Rico. Our success is in part dependent upon the continued popularity of malls as a shopping destination and the ability of malls, their tenants and other mall attractions to generate customer traffic. Accordingly, a significant decline in this popularity, especially if it is sustained, would substantially harm our sales and earnings. In addition, even assuming this popularity continues, mall traffic can be negatively impacted by mall renovations, weather, gas prices and similar factors.

We operate in a highly competitive and fragmented industry.

The retail jewelry business is highly competitive and fragmented, and we compete with nationally recognized jewelry chains as well as a large number of independent regional and local jewelry retailers and other types of retailers who sell jewelry and gift items, such as department stores and mass merchandisers. We also compete with internet sellers of jewelry. Because of the breadth and depth of this competition, we are constantly under competitive pressure that both constrains pricing and requires extensive merchandising efforts in order for us to remain competitive.

Any failure by us to manage our inventory effectively, including judgments related to consumer preferences and demand, will negatively impact our financial condition, sales and earnings.

We purchase much of our inventory well in advance of each selling period. In the event we do not stock merchandise consumers wish to purchase or misjudge consumer demand, we will experience lower sales than expected and will have excessive inventory that may need to be written down in value or sold at prices that are less than expected, which could have a material adverse impact on our business and financial condition.

Omnichannel retailing is rapidly evolving and our inability to keep pace with consumer preferences and expectations could adversely affect our financial performance.

Our guests are increasingly using computers, tablets, mobile phones and other devices to shop in our stores and online for our products. There are various risks relating to omnichannel retailing, including the need to keep pace with rapid technological change, internet security risks, risks of systems failure or inadequacy and increased competition. If we are unable to timely and appropriately respond to these risks, including through maintenance of customer service and guest relationships, demand for our products and services and our financial performance could be adversely affected. Further, governmental regulation of internet-based commerce continues to evolve in areas such as taxation, privacy, data protection and mobile communications. Unfavorable changes to regulations in these areas could have a negative effect on our business.

Unfavorable consumer responses to price increases or misjudgments about the level of markdowns could have a material adverse impact on our sales and earnings.

From time to time, and especially in periods of rising raw material costs, we increase the retail prices of our products. Significant price increases could impact our earnings depending on, among other factors, the pricing by competitors of similar products and the response by the guest to higher prices. Such price increases may result in lower unit sales and a subsequent decrease in gross margin and adversely impact

13

earnings. In addition, if we misjudge the level of markdowns required to sell our merchandise at acceptable turn rates, sales and earnings could be negatively impacted.

Any failure of our pricing and promotional strategies to be as effective as desired will negatively impact our sales and earnings.

We set the prices for our products and establish product specific and store-wide promotions in order to generate store traffic and sales. While these decisions are intended to maximize our sales and earnings, in some instances they do not. For instance, promotions, which can require substantial lead time, may not be as effective as desired or may prove unnecessary in certain economic circumstances. Where we have implemented a pricing or promotional strategy that does not work as expected, our sales and earnings will be adversely impacted.

Any inability to recruit, train, motivate and retain suitably qualified sales associates could adversely impact sales and earnings.

In specialty jewelry retailing, the level and quality of customer service is a key competitive factor as nearly every in-store transaction involves the sales associate taking a piece of jewelry or a watch out of a display case and presenting it to the potential guest. Competition for suitable individuals or changes in labor and healthcare laws could require us to incur higher labor costs. Therefore an inability to recruit, train, motivate and retain suitably qualified sales associates could adversely impact sales and earnings.

Because of our dependence upon a small concentrated number of landlords for a substantial number of our locations, any significant erosion of our relationships with those landlords or their financial condition would negatively impact our ability to obtain and retain store locations.

We are significantly dependent on our ability to operate stores in desirable locations with capital investment and lease costs that allow us to earn a reasonable return on our locations. We depend on the leasing market and our landlords to determine supply, demand, lease cost and operating costs and conditions. We cannot be certain as to when or whether desirable store locations will become or remain available to us at reasonable lease and operating costs. Several large landlords dominate the ownership of prime malls, and we are dependent upon maintaining good relations with those landlords in order to obtain and retain store locations on optimal terms. From time to time, we do have disagreements with our landlords and a significant disagreement, if not resolved, could have an adverse impact on our business. In addition, any financial weakness on the part of our landlords could adversely impact us in a number of ways, including decreased marketing by the landlords and the loss of other tenants that generate mall traffic.

Any disruption in, or changes to, our private label credit card arrangements may adversely affect our ability to provide consumer credit and write credit insurance.

We rely on third party credit providers to provide financing for our guests to purchase merchandise and credit insurance through private label credit cards. Any disruption in, or changes to, our credit card agreements could adversely affect our sales and earnings.

Significant restrictions in the amount of credit available to our guests could negatively impact our business and financial condition.

Our guests rely heavily on financing provided by credit lenders to purchase our merchandise. The availability of credit to our guests is impacted by numerous factors, including general economic conditions and regulatory requirements relating to the extension of credit. Numerous federal and state laws impose disclosure and other requirements upon the origination, servicing and enforcement of credit accounts and limitations on the maximum amount of finance charges that may be charged by a credit provider.

14

Regulations implementing the Credit Card Accountability Responsibility and Disclosure Act of 2009 imposed restrictions on credit card pricing, finance charges and fees, customer billing practices and payment application. Future regulations or changes in the application of current laws could further impact the availability of credit to our guests. If the amount of available credit provided to our guests is significantly restricted, our sales and earnings would be negatively impacted.

We are dependent upon our revolving credit agreement, senior secured term loan and other third party financing arrangements for our liquidity needs.

We have a revolving credit agreement and a senior secured term loan that contain various financial and other covenants. Should we be unable to fulfill the covenants contained in these loans, we would be in default, all outstanding amounts would be immediately due, and we would be unable to fund our operations without a significant restructuring of our business.

If the credit markets deteriorate, our ability to obtain the financing needed to operate our business could be adversely impacted.

We utilize a revolving credit agreement to finance our working capital requirements, including the purchase of inventory, among other things. If our ability to obtain the financing needed to meet these requirements was adversely impacted as a result of a deterioration in the credit markets, our business could be significantly impacted. In addition, the amount of available borrowings under our revolving credit agreement is based, in part, on the appraised liquidation value of our inventory. Any declines in the appraised value of our inventory could impact our ability to obtain the financing necessary to operate our business.

Any security breach with respect to our information technology systems could result in legal or financial liabilities, damage to our reputation and a loss of guest confidence.

During the course of our business, we regularly obtain and transmit through our information technology systems customer credit and other data. If our information technology systems are breached due to the actions of outside parties, or otherwise, an unauthorized third party may obtain access to confidential guest information. Any breach of our systems that results in unauthorized access to guest information could cause us to incur significant legal and financial liabilities, damage to our reputation and a loss of customer confidence. In each case, these impacts could have an adverse effect on our business and results of operations.

Acquisitions and dispositions involve special risk, including the risk that we may not be able to complete proposed acquisitions or dispositions or that such transactions may not be beneficial to us.

We have made significant acquisitions and dispositions in the past and may in the future make additional acquisitions and dispositions. Difficulty integrating an acquisition into our existing infrastructure and operations may cause us to fail to realize expected return on investment through revenue increases, cost savings, increases in geographic or product presence and guest reach or other projected benefits from the acquisition. In addition, we may not achieve anticipated cost savings or may be unable to find attractive investment opportunities for funds received in connection with a disposition. Additionally, attractive acquisition or disposition opportunities may not be available at the time or pursuant to terms acceptable to us and we may be unable to complete the acquisition or disposition.

Our net operating loss carryforwards could be subject to limitations under the Internal Revenue Code.

If we were to experience an "ownership change" under Section 382 of the Internal Revenue Code, our net operating loss carryforwards ("NOLs") would be subject to annual limitations that could impact the timing of the utilization of our NOLs as well as our ability to fully utilize our NOLs prior to their

15

expiration. The determination of whether an ownership change has occurred is complex and depends upon a number of factors, including new issuances of shares by the Company and purchases and sales of shares by large stockholders, including the exercise of the outstanding warrants.

Litigation and claims can adversely impact us.

We are involved in various legal proceedings as part of the normal course of our business. Where appropriate, we establish reserves based on management's best estimates of our potential liability in these matters. While management believes that all current litigation and claims will be resolved without material effect on our financial position or results of operations, as with all litigation it is possible that there will be a significant adverse outcome.

Ineffective internal controls can have adverse impacts on the Company.

Under Federal law, we are required to maintain an effective system of internal controls over financial reporting. Should we not maintain an effective system, it would result in a violation of those laws and could impair our ability to produce accurate and timely financial statements. In turn, this could result in increased audit costs, a loss of investor confidence, difficulties in accessing the capital markets, and regulatory and other actions against us. Any of these outcomes could be costly to both our shareholders and us.

Changes in estimates, assumptions and judgments made by management related to our evaluation of goodwill and other long-lived assets for impairment could significantly affect our financial results.

Evaluating goodwill and other long-lived assets for impairment is highly complex and involves many subjective estimates, assumptions and judgments by our management. For instance, management makes estimates and assumptions with respect to future cash flow projections, terminal growth rates, discount rates and long-term business plans. If our actual results are not consistent with our estimates, assumptions and judgments made by management, we may be required to recognize impairments.

Changes in estimates related to the recognition of revenue associated with lifetime warranty sales could significantly affect our financial results.

We recognize revenue related to lifetime warranty sales in proportion to when the expected costs will be incurred, which we estimate will be over an eight-year period. A significant change in estimates related to the time period or pattern in which warranty-related costs are expected to be incurred could adversely affect our revenues and earnings.

Additional factors may adversely affect our financial performance.

Increases in expenses that are beyond our control including items such as increases in interest rates, inflation, fluctuations in foreign currency rates, higher tax rates and changes in laws and regulations (such as the Patient Protection and Affordable Care Act), may negatively impact our operating results.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

We lease a 430,000 square foot facility, which serves as our corporate headquarters and primary distribution facility. The lease for this facility extends through March 2018. The facility is located in Las Colinas, a planned business development in Irving, Texas, near the Dallas/Fort Worth International Airport. Our Canadian distribution operation is conducted in a leased 26,000 square foot facility in Toronto, Ontario. The lease expires in November 2014 and has a five-year renewal option.

16

We rent our store retail space under leases that generally range in terms from 5 to 10 years and may contain minimum rent escalation clauses, while kiosk leases generally range from 3 to 5 years. Most of the store leases provide for the payment of base rentals plus real estate taxes, insurance, common area maintenance fees and merchants association dues, as well as percentage rents based on the store's gross sales. In fiscal year 2013, most of our stores and kiosks only made base rental payments.

We lease 21 percent of our store and kiosk locations from Simon Property Group and 11 percent of our store and kiosk locations from General Growth Management, Inc. No other lessor accounts for 10 percent or more of our store and kiosk locations. No store lease is individually material to our U.S. or Canadian operations.

The following table indicates the expiration dates of our leases as of July 31, 2013:

Term Expires (Fiscal Year) |

Stores | Kiosks | Other(a) | Total | Percentage of Total |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

2014 |

235 | 173 | — | 408 | 24.0 | % | ||||||||||

2015 |

182 | 226 | 1 | 409 | 24.1 | |||||||||||

2016 |

156 | 74 | — | 230 | 13.6 | |||||||||||

2017 |

170 | 40 | — | 210 | 12.4 | |||||||||||

2018 and thereafter |

321 | 117 | 2 | 440 | 25.9 | |||||||||||

|

1,064 | 630 | 3 | 1,697 | 100.0 | % | ||||||||||

- (a)

- Other includes the Store Support Center, Canada distribution center and storage facilities.

Management believes that substantially all of the store leases expiring in fiscal year 2014 that it wishes to renew (including leases which expired earlier and are currently being operated under month-to-month extensions) will be renewed. We expect that leases will be renewed on terms not materially different than the terms of the expiring or expired leases. Management believes our facilities are suitable and adequate for our business as presently conducted.

ITEM 3. LEGAL PROCEEDINGS AND OTHER MATTERS

Information regarding legal proceedings is incorporated by reference from Note 18 to our consolidated financial statements set forth, under the heading, "Contingencies," in Part IV of this report.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

17

ITEM 4A. EXECUTIVE OFFICERS OF THE REGISTRANT

The following individuals serve as the executive officers of the Company. Executive officers are elected by the Board of Directors annually, each to serve until his or her successor is elected and qualified, or until his or her earlier resignation, removal from office or death.

Name

|

Age | Position | |||

|---|---|---|---|---|---|

Executive Officers |

|||||

Theo Killion |

62 | Chief Executive Officer | |||

Matthew W. Appel |

57 | Chief Administrative Officer | |||

Gilbert P. Hollander |

60 | Executive Vice President, Chief Merchant and Sourcing Officer | |||

Richard A. Lennox |

48 | Executive Vice President, Chief Marketing Officer | |||

Thomas A. Haubenstricker |

51 | Senior Vice President, Chief Financial Officer | |||

Other Officers |

|||||

Jeannie Barsam |

52 | Senior Vice President, Merchandise Planning and Allocation | |||

Ken Brumfield |

49 | Senior Vice President, Financial Products | |||

Brad Furry |

54 | Senior Vice President, Chief Information Officer | |||

Richard J. Golden |

48 | Senior Vice President, Real Estate | |||

John A. Legg |

52 | Senior Vice President, Supply Chain | |||

Becky Mick |

51 | Senior Vice President, Chief Stores Officer | |||

Toyin Ogun |

53 | Senior Vice President, Human Resources | |||

Jamie Singleton |

52 | Senior Vice President and General Manager of Piercing Pagoda | |||

Bridgett Zeterberg |

49 | Senior Vice President, General Counsel and Secretary | |||

Executive Officers

The following is a brief description of the business experience of the Company's executive officers for at least the past five years.

Mr. Theo Killion has served as Chief Executive Officer of the Company since September 23, 2010. He served as President of the Company from August 5, 2008 to September 23, 2010, and as Interim Chief Executive Officer from January 13, 2010 to September 23, 2010. From January 23, 2008 to August 5, 2008, Mr. Killion served as Executive Vice President of Human Resources, Legal and Corporate Strategy. From May 2006 to January 2008, Mr. Killion was employed with the executive recruiting firm Berglass+Associates, focusing on companies in the retail, consumer goods and fashion industries. From April 2004 through April 2006, Mr. Killion served as Executive Vice President of Human Resources at Tommy Hilfiger. From 1996 to 2004, Mr. Killion served in various management positions with Limited Brands. Mr. Killion serves on the board of Express, Inc.

Mr. Matthew W. Appel was appointed Chief Administrative Officer of the Company effective May 5, 2011. Mr. Appel was named Executive Vice President of the Company effective May 2009 and appointed Chief Financial Officer of the Company on June 15, 2009. From March 2007 to May 2009, Mr. Appel served as Vice President and Chief Financial Officer of ExlService Holdings, Inc. Prior to ExlService Holdings, Inc, Mr. Appel was Vice President, BPO Product Management from 2006 to 2007 and Vice President, Finance and Administration BPO from 2003 through 2005 at Electronic Data Systems Corporation. From 2001 to 2003, Mr. Appel was the Senior Vice President, Finance and Accounting BPO at Affiliated Computer Services, Inc. Mr. Appel began his career with Arthur Andersen, where he spent seven years in their audit practice. Mr. Appel is a certified public accountant and certified management accountant.

Mr. Gilbert P. Hollander was appointed Executive Vice President and Chief Sourcing Officer in September 2007, and was given the additional title of Chief Merchandising Officer on January 13, 2010. Prior to that appointment, Mr. Hollander served as President, Corporate Sourcing/Piercing Pagoda

18

beginning in May 2006, and was given the additional title of Group Senior Vice President in August 2006. From January 2005 to August 2006, he served as President, Piercing Pagoda. Prior to and up until that appointment, Mr. Hollander served as Vice President of Divisional Merchandise for Piercing Pagoda, to which he was appointed in August 2003. Mr. Hollander served as Senior Vice President of Merchandising for Piercing Pagoda from February 2000 to August 2003. Prior to February 2000, Mr. Hollander held various management positions within Piercing Pagoda beginning in May of 1997.

Mr. Richard A. Lennox was appointed Executive Vice President, Chief Marketing Officer of the Company effective August 2009. Prior to joining the Company, Mr. Lennox served as Executive Vice President, Marketing Director at J. Walter Thompson–New York. Mr. Lennox started at J. Walter Thompson in 1989 and held various senior level marketing positions. He began his career in 1987 with AGB–London.

Mr. Thomas A. Haubenstricker was appointed Senior Vice President, Chief Financial Officer effective October 2011. Prior to joining the Company, Mr. Haubenstricker served as Managing Director at Turnberry Advisors from January 2010 to October 2011. Prior to that, Mr. Haubenstricker spent 24 years at Electronic Data Systems (later acquired by Hewlett-Packard) in various finance and strategy leadership roles including Co-Chief Financial Officer, Vice President and Chief Financial Officer, EMEA Region, and Vice President, Finance for the combined Hewlett-Packard and EDS Business Services Group.

Other Officers

Ms. Jeannie Barsam was appointed Senior Vice President, Merchandise Planning and Allocation in March 2011. Prior to joining the Company, Ms. Barsam served as Senior Vice President, Planning and Allocation of Charlotte Russe, Inc. from November 2009 to February 2011. From December 2007 to November 2009, Ms. Barsam served as Senior Vice President, Merchandise Planning and Allocation of The Talbots, Inc. Prior to The Talbots, Inc., Ms. Barsam held various senior management positions with Gap, Inc. from August 2000 to December 2007.

Mr. Ken Brumfield has served as Senior Vice President, Financial Products since February 2012. He served as Vice President of Financial Products from May 2011 to January 2012 and as Vice President of Credit from September 2010 to April 2011. Prior to joining the Company, Mr. Brumfield served as Director of Sales at Alliance Data Systems, Inc. from September 2003 through September 2010. From November 1997 to September 2003, Mr. Brumfield served as Senior Vice President of Credit Services at Stage Stores, Inc. From September 1986 to November 1997, Mr. Brumfield held various management positions with Zale Corporation.

Mr. Brad Furry was appointed Senior Vice President, Chief Information Officer effective September 2011. Prior to joining the Company, Mr. Furry served as Vice President of Enterprise Services at The Neiman Marcus Group from December 2009 to September 2011. From March 1990 to December 2009, Mr. Furry held various Information Technology management positions with The Neiman Marcus Group.

Mr. Richard J. Golden was appointed Senior Vice President, Real Estate in May 2013. Prior to joining the Company, Mr. Golden served as Managing Partner of the R. Golden Group from August 2012 to April 2013 providing real estate consulting services to Private Equity and Venture Capital groups. From September 2008 to August 2012, Mr. Golden served as Director of Real Estate at HEB Grocery Company. From January 2005 to September 2008, Mr. Golden served as Senior Vice President of Real Estate at Designer Shoe Warehouse ("DSW"). Prior to DSW, Mr. Golden served as a Vice President of Real Estate at Gap Inc. from 1992 to 2004.

Mr. John A. Legg was appointed Senior Vice President, Supply Chain in August 2010. Prior to joining the Company, Mr. Legg served as Managing Director of Management Services International, LLC from 2008 to 2010. From 2007 to 2008, Mr. Legg was Senior Vice President, Global Distribution and Logistics of

19

The Warnaco Group, Inc. Prior to The Warnaco Group, Inc., Mr. Legg was Vice President, International Distribution of Liz Claiborne, Inc., from 1999 to 2007.

Ms. Becky Mick was appointed Senior Vice President, Chief Stores Officer in July 2010. Ms. Mick served as Vice President Zale North America since joining the Company in September 2008. Prior to joining the Company, Ms. Mick served as Vice President, Director of Stores and Operations of The Disney Store from May 2006 to April 2008. Ms. Mick served as Vice President of The Children's Place from August 2005 to May 2006. From 1997 to 2005, Ms. Mick held various management positions with Old Navy.

Mr. Toyin Ogun was appointed Senior Vice President, Human Resources in March 2011. Prior to joining the Company, Mr. Ogun served as Vice President, Human Resources of L.L. Bean, Inc. from October 2009 to March 2010. Mr. Ogun served as Senior Vice President and Chief Talent Officer of Sears Holdings from August 2007 to August 2009. Prior to Sears Holdings, Mr. Ogun held various senior management positions with Limited Brands, Inc. from February 1998 to August 2007.

Ms. Jamie Singleton was appointed Senior Vice President and General Manager of Piercing Pagoda effective March 2012. Prior to joining Zale Corporation, Ms. Singleton served as Senior Vice President, Business Expansion at CPI Corp from May 2010 to April 2012. From May 2007 to May 2010, she owned and operated Custom Brands International, Inc. She served as Senior Vice President, General Merchandising Manager from May 2004 to April 2007 and Vice President of Merchandising from March 2002 to May 2004 at the David's Bridal and After Hours Formalwear divisions of May Company's Bridal Group.

Mrs. Bridgett Zeterberg was appointed Senior Vice President, General Counsel and Secretary in July 2013. She served as Vice President, General Counsel and Secretary from February 2012 to July 2013 and as Associate General Counsel from September 2011 to February 2012. From September 2010 to September 2011, Mrs. Zeterberg served as a Senior Attorney of the Company. Prior to joining the Company, Mrs. Zeterberg served in various Director and Vice President positions in the legal and human resource functions of Accor North America from January 1995 to December 2009.

20

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is listed on the New York Stock Exchange under the symbol "ZLC." The following table sets forth the high and low closing prices as reported on the NYSE for our common stock for each fiscal quarter during the two most recent fiscal years.

| |

2013 | 2012 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

High | Low | High | Low | |||||||||

First |

$ | 7.31 | $ | 3.02 | $ | 6.16 | $ | 2.26 | |||||

Second |

$ | 7.50 | $ | 3.93 | $ | 4.01 | $ | 2.83 | |||||

Third |

$ | 5.12 | $ | 3.81 | $ | 3.47 | $ | 2.57 | |||||

Fourth |

$ | 9.68 | $ | 4.36 | $ | 3.16 | $ | 2.20 | |||||

As of September 23, 2013, the Company's outstanding shares of common stock were held by approximately 417 holders of record. We have not paid dividends on the common stock since its initial issuance on July 30, 1993, and do not anticipate paying dividends on the common stock in the foreseeable future. In addition, our revolving credit agreement and our senior secured term loan limit our ability to pay dividends or repurchase our common stock. The Company has the right to pay dividends if, after giving effect to the dividend payment, the Company satisfies: (i) a minimum pro forma borrowing availability requirement equal to the lesser of 17.5 percent of the aggregate commitments or the aggregate borrowing base under the revolving credit agreement and (ii) a minimum pro forma fixed charge coverage ratio of 1.1. At July 31, 2013, we had borrowing availability under the terms of the revolving credit agreement of approximately $242 million and a fixed charge coverage ratio of 2.72. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources" and "Notes to Consolidated Financial Statements—Long-Term Debt" for additional information related to our revolving credit agreement and senior secured term loan.

21

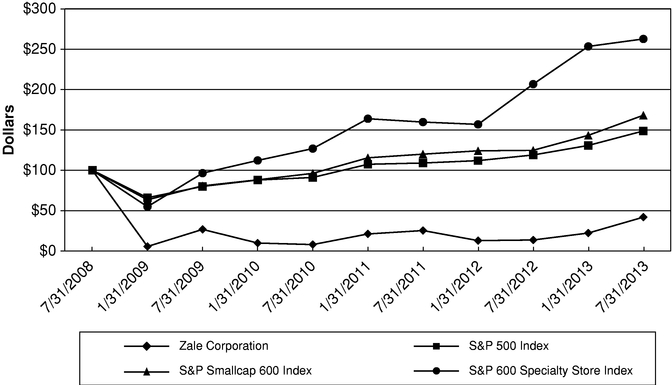

Corporate Performance Graph

The following graph shows a comparison of cumulative total returns for the Company, the S&P 500 Index, the S&P 600 Specialty Store Index and the S&P 600 Smallcap Index for the period from July 31, 2008 to July 31, 2013. The comparison assumes $100 was invested on July 31, 2008 in the Company's common stock and in each of the three indices and, for the S&P 500 Index, the S&P 600 Specialty Store Index and the S&P 600 Smallcap Index, assumes reinvestment of dividends. The Company has not paid any dividends during this period.

| |

7/31/2008 | 1/31/2009 | 7/31/2009 | 1/31/2010 | 7/31/2010 | 1/31/2011 | 7/31/2011 | 1/31/2012 | 7/31/2012 | 1/31/2013 | 7/31/2013 | |||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Zale Corporation |

$ | 100.00 | $ | 5.61 | $ | 26.76 | $ | 9.86 | $ | 7.96 | $ | 21.11 | $ | 25.36 | $ | 12.88 | $ | 13.65 | $ | 22.24 | $ | 41.95 | ||||||||||||

S&P 500 |

100.00 | 66.05 | 80.04 | 87.94 | 91.11 | 107.45 | 109.02 | 111.98 | 118.97 | 130.77 | 148.72 | |||||||||||||||||||||||

S&P Smallcap 600 |

100.00 | 63.45 | 80.73 | 88.18 | 96.21 | 115.46 | 119.99 | 124.11 | 124.78 | 143.29 | 168.17 | |||||||||||||||||||||||

S&P 600 Specialty Store |