U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

Mark One

For the quarterly period ended

For the transition period from ______ to _______

COMMISSION FILE NO.

(Exact name of registrant as specified in its charter)

(State or Other Jurisdiction of | IRS Employer | Primary Standard Industrial |

Incorporation or Organization) | Identification Number | Classification Code Number |

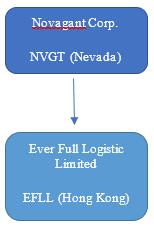

NOVAGANT CORP.

Tel.

(Address and telephone number of principal executive offices)

Indicate by checkmark whether the issuer: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant is a large accelerated filed, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

Large accelerated filer [ ] | Accelerated filer [ ] |

Smaller reporting company | |

Emerging growth company |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by checkmark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the most practicable date:

Class | Outstanding as of August 10, 2022 |

Common Stock, $0.001 |

1

Unless otherwise mentioned or unless the context requires otherwise, when used in this Form 10-Q, the terms “Company,” “we,” “us,” “our,” “EFLL” and “NVGT” refer to Novagant Corp. and/or its wholly-owned subsidiary, Ever Full Logistics Limited.

EXPLANATORY NOTE

NVGT is a holding company, incorporated in Nevada. Our operations are conducted through our wholly-owned subsidiary organized in Hong Kong, EFLL. EFLL’s operations are based in Hong Kong. We have no business operations in China. This structure presents unique risks as our investors may never directly hold equity interests in our Hong Kong subsidiary and will be dependent upon contributions from our subsidiaries to finance our cash flow needs. We may also become subject to foreign exchange regulations that might limit our ability to transfer cash between entities, across borders, to U.S. investors, to convert foreign currency into Renminbi, acquire other PRC companies or establish VIEs in the PRC. There are risks relating to PRC laws and regulations with respect to foreign exchange, for example, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the “Opinions on Severely Cracking Down on Illegal Securities Activities According to Law,” or the Opinions, which was made available to the public on July 6, 2021. The Opinions emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems will be taken to deal with the risks and incidents of China-concept overseas listed companies, and cybersecurity and data privacy protection requirements and similar matters. The Opinions and any related implementing rules to be enacted may subject us to compliance requirement in the future. Given the current regulatory environment in the PRC, we are still subject to the uncertainty of interpretation and enforcement of the rules and regulations in the PRC, which can change quickly with little advance notice, and any future actions of the PRC authorities. Moreover, we cannot assure you that relevant PRC government agencies would reach the same conclusion as we do or as advised by our PRC legal counsel. Our PRC legal counsel, China Commercial Law Firm. Guangdong. has provided the consent at Exhibit 23.3 to the Form 10-12G/A on June 7, 2022 accordingly. However, (i) if we inadvertently concluded that such permissions or approvals are not required, or (ii) if the CSRC, the Cyberspace Administration of China or other regulatory PRC agencies later promulgate new rules requiring that we obtain their approvals to issue the Company’s common stock to foreign investors, and we are unable to obtain a waiver of such approval requirements, if and when procedures are established to obtain such a waiver, then we may not be able to list on a U.S. exchange. In addition, any uncertainties and/or negative publicity regarding such an approval requirement could have a material adverse effect on the trading price of our securities. It is uncertain when and whether we will be required to obtain permission from the China Securities Regulatory Commission to list on U.S. exchanges, and even if such permission is obtained, whether it will be denied or rescinded. Although we concluded our subsidiary is currently not required to obtain permission from any of the PRC central or local government and has not received any denial to list on the U.S. exchange, our operations, financial conditions, and results of operations could be adversely affected, directly or indirectly, and the value of the Company’s common stock could significantly decline or become worthless, if we inadvertently conclude that such approvals are not required when they are, if we do not receive or maintain such permissions or approvals if and when required, or changes in applicable laws, regulations, or interpretations relating to our business or industry which would require us to obtain approvals in the future. If our subsidiary is unable to receive or maintain approvals when required for our business or industry under then applicable PRC laws, then such failure could limit or prohibit the ability of our subsidiary to operate in Hong Kong, and our operations, financial conditions, and the results of operations could be adversely affected, directly or indirectly, and the value of the Company’s common stock could significantly decline or become worthless.

Any restrictions and limitations on foreign exchange and the ability of our subsidiary to make payments to us, to transfer cash between entities, across borders, and to U.S. investors could have a material adverse effect on our ability to conduct business. We do not anticipate paying dividends in the foreseeable future; you should not buy our stock if you expect dividends. Please see ”Risk Factors - Our ability to pay dividends is limited because of our holding company structure creates restrictions on the payment of dividends.

Our holding company NVGT and Hong Kong subsidiary EFLL are currently not required to obtain permission or approval from the Chinese authorities including the China Securities Regulatory Commission, or CSRC, or the Cyberspace Administration of China, or CAC, to operate or to issue securities to foreign investors. Please refer to the consent provided by our PRC legal counsel at Exhibit 23.3 to the Form 10-12G/A on June 7, 2022. While this currently does not present any operational risks, interference from the government of the People’s Republic of China (“PRC”) could cause a material change in our operations and the value of the Company’s common stock. Recent statements by the government of the PRC, while not currently applicable to EFLL, could limit the Company’s use of variable interest entities, effect the Company’s data security, and hinder our ability to operate as planned. Further overreach by the Chinese government into Hong Kong could limit the Company’s ability to accept foreign investments or be quoted in the U.S.

We believe that there are certain risks and uncertainties involved in our operations, some of which are beyond our control. We believe a few of the more significant risks relating to our business are as follows summarized below and in “Risk Factors — Risks Of The Corporate Structure Based In Hong Kong.”

2

In light of China’s extension of its authority into Hong Kong, the Chinese government can change Hong Kong’s rules and regulations including its enforcement and interpretation at any time with little to no advance notice and can intervene at any time with little to no advance notice. NVGT and EFLL are currently not required to obtain permission or approval from Chinese authorities to list on U.S. exchanges. We have not been denied from any Chinese authorities with permissions or approvals to operate our business or to offer our securities so far. However, if our subsidiary or the holding company were required to obtain permission or approval in the future, or we erroneously conclude that permissions or approvals were not required, or we were denied permission or approval from Chinese authorities to operate or to list on U.S. exchanges, we will not be able to continue listing on a U.S. exchange and the value of our common stock would likely significantly decline or become worthless, which would materially affect the interest of the investors. There is a risk that the Chinese government may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in Hong Kong-based issuers, which could result in a material change in our operations and/or the value of our securities. Further, any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers and Hong Kong based issuers, would likely significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Please see Risk Factors - We face the risk that changes in the policies of the PRC government could have a significant impact upon the business we may be able to conduct in the Hong Kong and the profitability of such business. Substantial uncertainties and risks arising from the legal system in China, regarding the enforcement of laws and that rules and regulations in China can change quickly with respect to the political and economic policies of the PRC government and PRC laws and regulations could have a significant impact upon the business that we may be able to conduct in Hong Kong and accordingly on the results of our operations and financial condition. Adverse changes in economic and political policies of the PRC government could have a material and adverse effect on overall economic growth in China and Hong Kong, which could materially and adversely affect our business. General macroeconomic conditions may materially and adversely affect our business, prospects, results of operations and financial position. Occupation protest, demonstration or rioting causing mass disruption to business in Hong Kong may impose adverse impact on the economy of Hong Kong, which in turn may affect our business performance. The PRC government’s control over foreign currency conversion may adversely affect our business and results of operations and our ability to remit dividends. PRC regulations of loans to and direct investments in PRC entities by offshore holding companies may delay or prevent us from making loans or additional capital contributions to our operating subsidiary in Hong Kong, which could materially and adversely affect our liquidity and our ability to fund and expand business. The M&A Rules and certain other PRC regulations may make it more difficult for us to pursue growth through acquisitions. Under the Enterprise Income Tax Law, we may be classified as a “Resident Enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC shareholders and have a material adverse effect on our results of operations and the value of your investment. We face uncertainties with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies.

The Chinese government exerts substantial influence over, and can intervene at any time with little to no advance notice in the manner in which we must conduct our business activities. The holding company NVGT and the subsidiary EFLL are currently not required to obtain permission or approval from Chinese authorities to list on U.S. exchanges. However, to the extent that the Chinese government exerts more control over offerings conducted overseas and/or foreign investment in Hong Kong based issuers over time and if our subsidiary or the holding company were required to obtain approval in the future and were denied permission from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on a U.S. exchange and the value of our common stock may significantly decline or become worthless, which would materially affect the interest of the investors in future. Please see Risk Factors - The Chinese government exerts substantial influence over the manner in which we must conduct our business activities. We are currently not required to obtain permission or approval from Chinese authorities to list on U.S exchanges. However, to the extent that the Chinese government exerts more control over offerings conducted overseas and/or foreign investment in China-based issuers and Hong Kong based issuers over time and if our PRC subsidiaries or the holding company were required to obtain permission or approval in the future and were denied permission from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange and the value of our common stock may significantly decline or become worthless, which would materially affect the interest of the investors.

U.S shareholders may face difficulties in effecting service of process against the Company and our officers and directors, as they are all based in Hong Kong. Even with proper service of process, the enforcement of judgments obtained in U.S. courts or foreign courts based on the civil liability provisions of the U.S. federal securities laws would be extremely difficult. Furthermore, there would be added costs and issues with bringing an original action in foreign courts to enforce liabilities based on the U.S. federal securities laws against the Company or any of the officers or directors, and they still may be fruitless.

The holding company and the subsidiary are not required to obtain any permission or approval for our operations from the Chinese government, including those required from the CSRC, CAC or any other entity at present. However, in light of the recent statements and regulatory actions by the PRC government, such as those related to Hong Kong’s national security, the promulgation of regulations prohibiting foreign ownership of Chinese companies operating in certain industries, which are constantly evolving, and anti-monopoly concerns, we may be subject to the risks of uncertainty of any future actions of the PRC government in this regard including the risk that we inadvertently conclude that such permissions or approvals are not required, that applicable laws, regulations or interpretations change such that we are required to obtain permission or approval in the future, or that the PRC government could disallow our holding company structure, which would likely result in a material change in our operations, including our ability to continue our

3

existing holding company structure, carry on our current business, accept foreign investments, and offer or continue to offer securities to our investors. These adverse actions would likely cause the value of our common stock to significantly decline or become worthless. We may also be subject to penalties and sanctions imposed by the PRC regulatory agencies, including the Chinese Securities Regulatory Commission, if we fail to comply with such rules and regulations, which would likely adversely affect the ability of the Company’s securities to continue to trade on the Over-the-Counter market, which would likely cause the value of our securities to significantly decline or become worthless.

Furthermore, there may be some prominent risks associated with our operations based in Hong Kong. For example, as a U.S.-listed Hong Kong public company, we may face heightened scrutiny, criticism and negative publicity, which could result in a material change in our operations and the value of our common stock. It could also significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Additionally, changes in Chinese internal regulatory mandates, such as the M&A rules, Anti-Monopoly Law, and the soon to be effective Data Security Law, may target the Company's corporate structure and impact our ability to conduct business in Hong Kong, accept foreign investments, or list on an U.S. or other foreign exchange. Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies and Hong Kong-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. In April 2020, the Cyberspace Administration of China and certain other PRC regulatory authorities promulgated the Cybersecurity Review Measures, which became effective in June 2020. Pursuant to the Cybersecurity Review Measures, operators of critical information infrastructure must pass a cybersecurity review when purchasing network products and services which do or may affect national security. On July 10, 2021, the Cyberspace Administration of China issued a revised draft of the Measures for Cybersecurity Review for public comments (“Draft Measures”), which required that, in addition to “operator of critical information infrastructure,” any “data processor” carrying out data processing activities that affect or may affect national security should also be subject to cybersecurity review, and further elaborated the factors to be considered when assessing the national security risks of the relevant activities. On January 4, 2022, the CAC, in conjunction with 12 other government departments, issued the New Measures for Cybersecurity Review (the "New Measures") on January 4, 2022. The New Measures amends the Draft Measures released on July 10, 2021 and became effective on February 15, 2022. For a detailed description regarding Measures for Cybersecurity Review, please also see Risk Factors - The Chinese government exerts substantial influence over the manner in which we must conduct our business activities. We are currently not required to obtain permission or approval from Chinese authorities to list on U.S exchanges. However, to the extent that the Chinese government exerts more control over offerings conducted overseas and/or foreign investment in China-based issuers and Hong Kong based issuers over time and if our PRC subsidiaries or the holding company were required to obtain permission or approval in the future and were denied permission from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange and the value of our common stock may significantly decline or become worthless, which would materially affect the interest of the investors.

The business of NVGT and EFLL until now are not subject to cybersecurity review with the Cyberspace Administration of China, or CAC, given that: (i) we do not have one million individual online users of our products and services in Hong Kong; (ii) we do not possess a large amount of personal information in our business operations.. In addition, we are not subject to merger control review by China’s anti-monopoly enforcement agency due to the level of our revenues which provided from us and audited by our auditor and the fact that we currently do not expect to propose or implement any acquisition of control of, or decisive influence over, any company with revenues within China of more than RMB400 million. Currently, these statements and regulatory actions have had no impact on our daily business operation, the ability to accept foreign investments and list our securities on an U.S. or other foreign exchange. However, since these statements and regulatory actions are the latest, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list our securities on an U.S. or other foreign exchange. For a detailed description of the legal and operational risks facing the Company and the offering associated with our operations in Hong Kong, please refer to the “Risk Factors — Risks Of The Corporate Structure Based In Hong Kong”.

4

Transfers of Cash to and from Our Subsidiary

NVGT is permitted under the Nevada laws to provide funding to our subsidiary in Hong Kong through loans or capital contributions without restrictions on the amount of the funds, subject to satisfaction of applicable government registration, approval and filing requirements. Likewise, EFLL is permitted under the laws of Hong Kong to provide funding to NVGT through earnings distribution without restrictions on the amount of the funds. As of the date of this prospectus, there have been no dividends or distributions among the holding company or the subsidiary and no transfers of cash between the holding company and the subsidiary.

We currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying any dividends in the foreseeable future. We have not paid any dividends in the past. Any future determination related to our dividend policy will be made at the discretion of our board of directors after considering our financial condition, results of operations, capital requirements, contractual requirements, business prospects and other factors the board of directors deem relevant, and subject to the restrictions contained in any future financing instruments.

Subject to the Nevada Revised Statutes and our bylaws, our board of directors may authorize and declare a dividend to shareholders at such time and of such an amount as they think fit if they are satisfied, on reasonable grounds, that immediately following the dividend the value of our assets will exceed our liabilities and we will be able to pay our debts as they become due. There is no further Nevada statutory restriction on the amount of funds which may be distributed by us by dividend.

Under the current practice of the Inland Revenue Department of Hong Kong, no tax is payable in Hong Kong in respect of dividends paid by us. The laws and regulations of the PRC do not currently have any material impact on transfers of cash from NVGT to EFLL or from EFLL to NVGT. There are no restrictions or limitation under the laws of Hong Kong imposed on the conversion of HK dollar into foreign currencies and the remittance of currencies out of Hong Kong or across borders and to U.S investors.

Current PRC regulations permit PRC subsidiaries to pay dividends to Hong Kong subsidiaries only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation. As of the date of this prospectus, we do not have any PRC subsidiaries.

The PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenues from our operations, we may be unable to pay dividends on our common stock. As of the date of this prospectus, we do not have any PRC subsidiaries.

Cash dividends, if any, on our common stock will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10.0%.

Pursuant to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC entity. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied, including, without limitation, that (a) the Hong Kong entity must be the beneficial owner of the relevant dividends; and (b) the Hong Kong entity must directly hold no less than 25% share ownership in the PRC entity during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong entity must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot assure you that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by a PRC subsidiary to its immediate holding company. As of the date of this prospectus, we do not have any PRC subsidiaries. In the event that we acquire or form a PRC subsidiary in the future and such PRC subsidiary desires to declare and pay dividends to our Hong Kong subsidiary, our Hong Kong subsidiary will be required to apply for the tax resident certificate from the relevant Hong Kong tax authority. In that case, we will update our investors by SEC filing of disclosure, e.g. a current report on Form 8-K, prior to such actions.

All our cash is paid directly to our Hong Kong company, EFLL. $0 has passed from EFLL to the parent company. EFLL has made no distributions to the holding company. There have been no transfers of cash between the holding company and the subsidiary.

5

The recent joint statement by the SEC and PCAOB, and the Holding Foreign Companies Accountable Act all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. Trading in our securities may be prohibited under the Holding Foreign Companies Accountable Act as the PCAOB has determined that it is unable to inspect or investigate completely our auditor Zhen Hui Certified Public Accountants (“ZHCPA”). We expect to be added to the list of Commission-Identified Issuers under the HFCAA subsequent to the filing of our annual report, and this could materially affect the trading price of our common stock, cause our common stock to be prohibited from trading and that as a result, the exchange may determine to delist our securities. In future, if we do not engage an auditor that is subject to regular inspection by the PCAOB, the Company’s common stock may be delisted under the HFCAA. Please see Risk Factors – The audit report included in this Amendment is prepared by an auditor who is not inspected by the Public Company Accounting Oversight Board and as such, our investors are deprived of the benefits of such inspection. The Company could be delisted if it is unable to timely meet the PCAOB inspection requirements established by the Holding Foreign Companies Accountable Act.

On December 16, 2021, Public Company Accounting Oversight Board (PCAOB) issued a report on its determinations that the PCAOB is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, a Special Administrative Region of the People’s Republic of China (PRC), because of positions taken by PRC authorities in those jurisdictions. The PCAOB made these determinations pursuant to PCAOB Rule 6100, which provides a framework for how the PCAOB fulfills its responsibilities under the Holding Foreign Companies Accountable Act (HFCAA). The report further listed in its Appendix A and Appendix B, Registered Public Accounting Firms Subject to the Mainland China Determination and Registered Public Accounting Firms Subject to the Hong Kong Determination, respectively. Our auditor Zhen Hui Certified Public Accountants (“ZHCPA”) was included on such list. Our auditor Zhen Hui Certified Public Accountants (“ZHCPA”) is subject to the determinations announced by the PCAOB on December 16, 2021. Consequently, the PCAOB is unable to inspect or investigate completely ZHCPA headquartered in Hong Kong, the lack of access to the PCAOB inspection in China prevents the PCAOB from fully evaluating audits and quality control procedures of the auditors based in China, as a result, the investors may be deprived of the benefits of such PCAOB inspections. The inability of the PCAOB to conduct inspections of auditors in China makes it more difficult to evaluate the effectiveness of these accounting firms’ audit procedures or quality control procedures as compared to auditors outside of China that are subject to the PCAOB inspections.

In addition, under the HFCAA, our securities may be prohibited from trading on the U.S. stock exchanges or in the over the counter trading market in the U.S. if our auditor is not inspected by the PCAOB for three consecutive years, and this ultimately could result in the Company’s common stock being delisted. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act (“AHFCAA”), which, if enacted, would amend the HFCAA and require the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges or in the over the counter trading market in the U.S. if its auditor is not subject to PCAOB inspections for two consecutive years instead of three. In future, if we do not engage an auditor that is subject to regular inspection by the PCAOB, the Company’s common stock may be delisted. Also, such as the potential for such determination would materially affect the trading price of our common stock, and the potential that such determination could cause our common stock to be prohibited from trading.

Furthermore, due to the recent developments in connection with the implementation of the Holding Foreign Companies Accountable Act, we cannot assure you whether the SEC or other regulatory authorities would apply additional and more stringent criteria to us after considering the effectiveness of our auditor’s audit procedures and quality control procedures, adequacy of personnel and training, or sufficiency of resources, geographic reach or experience as it relates to the audit of our financial statements. The requirement in the HFCA Act that the PCAOB is unable to inspect the issuer’s public accounting firm within two or three years, may result in the delisting of our securities from applicable trading markets in the U.S. Please see Risk Factors - The Holding Foreign Companies Accountable Act requires the Public Company Accounting Oversight Board (PCAOB) to be permitted to inspect the issuer's public accounting firm within three years. There are uncertainties under the PRC Securities Law relating to the procedures and requisite timing for the U.S. securities regulatory agencies to conduct investigations and collect evidence within the territory of the PRC. If the U.S. securities regulatory agencies are unable to conduct such investigations, they may suspend or de-register our registration with the SEC and delist our securities from applicable trading market within the US.

For detailed discussions on such risks, please see the section captioned “Risk Factors” in our Annual Report on Form 10-K (the “Annual Report” or “Form 10-K”), filed with the SEC on June 29, 2022.

6

TABLE OF CONTENTS

| EXPLANATORY NOTE | 1 |

PART I | 8 | |

ITEM 1 | 8 | |

| 8 | |

| 9 | |

| CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY | 10 |

| 11 | |

| 12 | |

ITEM 2 | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 26 |

ITEM 3 | 31 | |

ITEM 4 | 31 | |

|

|

|

PART II | 31 | |

ITEM 1 | 31 | |

ITEM 2 | 31 | |

ITEM 3 | 31 | |

ITEM 4 | 31 | |

ITEM 5 | 31 | |

ITEM 6 | 32 | |

| 33 |

7

PART I. FINANCIAL INFORMATION

This Quarterly Report includes forward-looking statements within the meaning of the Securities Exchange Act of 1934 (the “Exchange Act”). These statements are based on management’s beliefs and assumptions, and on information currently available to management. Forward-looking statements include the information concerning our possible or assumed future results of operations set forth under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements also include statements in which words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” “consider” or similar expressions are used.

ITEM 1. FINANCIAL STATEMENTS

Condensed Consolidated Balance Sheets

|

| June 30, | March 31, |

| 2022 | 2022 | |

|

| US$ | US$ |

|

| (unaudited) | (audited) |

|

|

|

|

ASSETS |

|

|

|

|

|

|

|

Non-Current Assets |

|

|

|

Plant and equipment |

| ||

Right-of-use assets |

| | |

Total Non-Current Assets |

| ||

|

|

|

|

Current Assets |

|

|

|

Deposits |

| ||

Accounts receivables |

| ||

Cash and cash equivalents |

| ||

Total Current Assets |

| ||

|

|

|

|

TOTAL ASSETS |

| ||

|

|

|

|

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

|

|

|

|

Current Liabilities |

|

|

|

Creditors, other payables and accrual |

| ||

Lease liabilities |

| | |

Total Current Liabilities |

| ||

|

|

|

|

Shareholders’ Equity |

|

|

|

Preferred stock, |

|

|

|

Series A Preferred stock, $ |

| ||

Series B Preferred stock, $ |

| ||

Common stock, $ |

| ||

Additional paid-in capital |

| ||

Accumulated deficit |

| ( | ( |

Total Shareholders’ Equity |

| ( | ( |

|

|

|

|

TOTAL LIABILITIES AND SHAREHOLDER’S EQUITY |

|

The accompanying notes are an integral part of these consolidated financial statements.

8

Consolidated Statements of Operations

(unaudited)

|

| Three months | Three months | ||

|

| Ended June 30, | Ended June 30, | ||

|

|

| 2022 |

| 2021 |

|

|

| $ |

| $ |

|

|

|

|

|

|

Revenue – air/ocean freight service income |

|

| |

| |

Cost of services – air/ocean freight service direct cost |

|

| ( |

| ( |

|

|

|

|

|

|

|

|

| |

| |

|

|

|

|

|

|

Operating expenses: |

|

|

|

|

|

General and administrative expenses |

|

| ( |

| ( |

Finance costs |

|

| ( |

| ( |

|

|

|

|

|

|

Total expenses |

|

| ( |

| ( |

|

|

|

|

|

|

Profit (Loss) before provision for income taxes |

|

| |

| ( |

|

|

|

|

|

|

Provision for income taxes |

|

| |

| |

|

|

|

|

|

|

Net profit (loss) for the period |

|

| |

| ( |

9

Consolidated Statements of Changes in Stockholders' Equity

(unaudited)

|

Series A Preferred stock: |

Series B Preferred stock: |

Common stock: | Additional paid-in capital | Accumulated deficit | Total | |||

Shares | Amount | Shares | Amount | Shares | Amount | ||||

|

| $ |

| $ |

| $ | $ | $ | $ |

|

|

|

|

|

|

|

|

|

|

Balances at March 31, 2021 | ( | ( | ( | ||||||

|

|

|

|

|

|

|

|

|

|

Net loss for the period | ( | ( | |||||||

|

|

|

|

|

|

|

|

|

|

Balances at June 30, 2021 | ( | ( | ( | ||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balances at March 31, 2022 | ( | ( | |||||||

|

|

|

|

|

|

|

|

|

|

Net profit for the period | |||||||||

|

|

|

|

|

|

|

|

|

|

Balances at June 30, 2022 | ( | ( | |||||||

10

Consolidated Statements of Cash Flows

(Unaudited)

|

| Three months ended June 30, | |

|

| 2022 | 2021 |

|

| $ | $ |

|

|

|

|

Cashflow from Operating Activities |

|

|

|

Profit (Loss) for the period |

| | ( |

Adjustments for: |

|

|

|

Finance costs |

| | |

Depreciation |

| | |

Operating cash flows before working capital change |

| | ( |

|

|

|

|

Changes in Working Capital: |

|

|

|

Accounts receivables |

| | ( |

Deposit |

| ( | |

Creditors, Accruals and Other Payables |

| ( | |

Total |

| ( | |

|

|

|

|

Cash generated (used in) from Operating Activities |

| ( | |

|

|

|

|

Cashflow from Financing Activities |

|

|

|

Repayment of lease liabilities |

| ( | ( |

Interest paid |

| ( | ( |

Total |

| ( | ( |

|

|

|

|

Net change in cash and cash equivalents |

| ( | |

|

|

|

|

Cash & Cash equivalents at the beginning of the period |

| | |

Cash & Cash equivalents at the end of the period |

| | |

11

Notes to the Financial Statements

For the three months ended June 30, 2022, 2022 and 2021

Note 1 - Nature of Operations and Basis of Presentation

Legal Status and Nature of Operations

This summary of significant accounting policies of Novagant Inc. (the “Company”) and Ever Full Logistics Limited (“EFLL”) (together with the Company collectively referred to as the “Group”) is presented to assist in understanding the Group’s unaudited consolidated financial statements for the three months ended June 30, 2022. The consolidated financial statements and notes are representations of the Company's management who is responsible for their integrity and objectivity. These accounting policies conform to generally accepted accounting principles and have been consistently applied in the preparation of the financial statements.

The Company was initially incorporated as Kendrex Systems, Inc in Nevada. on February 23, 1987. Kendrex Systems, Inc. changed to HLHKWorld Group, Inc. on November 18, 1996. HLHK World Group, Inc. changed to Trimfast Group, Inc. in Nevada on September 4, 1998. On December 21, 1998, the Company completed a 1 for 10 reverse stock split. In 2001 the Company filed for protection under Chapter 7 of the United States Bankruptcy Code and ceased all activities. On October 21, 2002, the Company completed a 1 for 200reverse stock split. During the period 2002 thru 2006, the Company was known as TrimFast Group, Inc. On November 9, 2004, the Company completed a 1 for 9 reverse stock split. On November 21, 2006, in conjunction with a one for 30 share reverse split of it’s common stock, the Company changed its’ name to EDollars, Inc. On September 18, 2007 the Company changed its’ name to Forex, Inc. and completed a one for 20 reverse stock split. On March 26, 2008, the Company changed its’ name to Petrogulf, Inc. On April23, 2012, the Company acquired 100% of Neeksom, Inc., a Nevada Corporation. On November 26, 2013 the Company changed its name to Novagant, Inc. During 2014, the Company exited its business products business and returned the Neeksom, Inc. subsidiary to its prior owners. The Company previously elected to pursue selling financial products. Trimfast Group, Inc. changed to Edollars, Inc. in Nevada on November, 2006. Edollars, Inc. changed to Forex, Inc. in June, 2007. Forex, Inc. changed to Petrogulf Corp. on March26, 2008. Petrogulf Inc. changed to Novagant, Inc. on November 26, 2013. On January 1, 2014, the Company changed its symbol from PTRF to NVGT.

In 2015, the Company ceased operations and reporting. On December 9, 2019, in Case No. A-19-804454-B, Eight Judicial DistrictCourt, Clark County, Nevada, GrassRoots Advisory, LLC (“GrassRoots”) was granted custodianship of the Company. On January 8, 2020, GrassRoots sold the controlling interest in the Company to Alexander M. Woods-Leo.

On January 8, 2020, GrassRoots agreed to assist Alexander M. Woods-Leo in acquiring control block of a custodian PubCo OTC: NVGT (Novagant Corp). Doug DiSanti Agrees to give 500,000 Preferred B. Shares to Alexander M Woods-Leo in exchange for the amount of $15,000 which was paid. The Preferred B shares will be Non-convertible and equal to 1,000 common votes per 1 Preferred share. A total of 500,000,000 common votes will be given to Alexander M. Woods-Leo. GrassRoots sold the controlling interest in the Company to Alexander M. Woods-Leo.

As of April 21, 2021, Pacific Corporate Advisory Services Limited who represents, Mr. WeiQun Chen, purchased the Preferred B Control block from Mr. Alexander M. Woods-Leo. As per escrow agreement, Mr. Alexander M. Woods- Leo had submitted the proper stock power with respect to the change of control to escrow. On May 6, 2021, Mr. Alexander M. Woods-Leo resigned as an officer and director and appointed Mr. WeiQun Chen as Chairman, CEO and Director, Mr. HongZhen Xu as Secretary, Treasurer and Director, and Haiyan Zeng as a Director.

EFLL is a limited company incorporated in Hong Kong. The address of its registered office and principal place of business are Unit A, Room V28, 5/F., Victory Industrial Building, 151-157 Wo Yi Hop Road, Kwai Chung, New Territories. The principal activity of the Company during the year was provision of logistics services.

On September 21, 2021, the Company entered into a Share Exchange Agreement (the “Exchange Agreement”) with Ever Full Logistics Limited (“EFLL”), registered and incorporated as a private limited liability company in Hong Kong. The Company received 100% of the issued and outstanding shares of EFLL in exchange for newly issued 300,000,000 shares of common stock of the Company, thus causing EFLL to become a direct wholly-owned subsidiary of the Company. This transaction resulted in the owner of EFLL obtaining a majority voting interest in the Company. The merger of EFLL into the Company results in EFLL having control of the combined entity.

12

Notes to the Financial Statements

For the three months ended June 30, 2022 and 2021

Note 1 - Nature of Operations and Basis of Presentation – continued

For financial reporting purposes, the transaction represents a "reverse merger" rather than a business combination and the Company is deemed to be the accounting acquiree in the transaction. The transaction is being accounted for as a reverse merger and recapitalization. The Company is the legal acquirer but accounting acquiree for financial reporting purposes and EFLL is the acquired company but accounting acquirer. Consequently, the assets and liabilities and the operations that will be reflected in the historical financial statements prior to the transaction will be those of EFLL and will be recorded at the historical cost basis of EFLL, and no goodwill will be recognized in this transaction. The consolidated financial statements after completion of the transaction will include the assets and liabilities of EFLL and the Company, and the historical operations of the Company and the combined operations of EFLL from the initial closing date of the transaction.

Basis of Presentation

The consolidated financial statements include all of the assets, liabilities, revenues, expenses and cash flows of entities in which the Company has a controlling interest (“subsidiaries”). Intercompany accounts and transactions between consolidated companies have been eliminated in consolidation.

Consolidated financial statements prepared following a reverse acquisition are issued under the name of the legal parent (accounting acquiree) but as a continuation of the financial statements of the legal subsidiary (accounting acquirer), with one adjustment, which is to retroactively adjust the accounting acquirer’s legal capital to reflect the legal capital of the accounting acquiree. That adjustment is required to reflect the capital of the legal parent (the accounting acquiree). Therefore the consolidated financial statements are those of EFLL as of and for the three months period ended June 30, 2021 and 2022. On the other hand, the comparative information on shareholders’ equity presented in those consolidated financial statements is retroactively adjusted to reflect the legal capital of the legal parent (accounting acquiree).

The accompanying consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”), and include the financial statements of the Company and EFLL. All material intercompany transactions and balances have been eliminated in the consolidation.

The consolidated financial statements include the accounts of Novagant Corp. and Ever Full Logistics Limited, a wholly-owned subsidiary of the Company incorporated in Hong Kong as a private company on June 3, 2020.

All significant inter-company balances and transactions within the Company have been eliminated upon consolidation.

The accompanying consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”), and include the financial statements of the Company and EFLL. All material intercompany transactions and balances have been eliminated in the consolidation.

These consolidated financial statements have been prepared under the historical cost convention and all transactions have been accounted for on accrual basis.

Going concern

As at June 30, 2022, the Company and EFLL (collectively referred to as the “Group”) had net current liabilities and net liabilities of $222,107 and $219,618, respectively. These conditions indicate the existence of a material uncertainty which may cast significant doubt about the Group’s ability to continue as a going concern. Therefore, the Group may be unable to realise its assets and discharge its liabilities in the normal course of business.

13

These consolidated financial statements have been prepared on a going concern basis, the validity of which depends upon the financial support from the shareholders at a level sufficient to finance the working capital requirements of the Group. The shareholders have agreed to provide adequate funds for the Group to meet its liabilities as they fall due for the foreseeable future. The directors of the Company is therefore of the opinion that it is appropriate to prepare the consolidated financial statements on a going concern basis. Should the Group be unable to continue as going concern, adjustments would have to be made to the consolidated financial statements to adjust the value of the Group’s assets to their recoverable amounts, to reclassify non-current assets as current assets and to provide for any further liabilities which might arise. The effect of these adjustments has not been reflected in the consolidated financial statements.

14

Notes to the Financial Statements

For the three months ended June 30, 2022 and 2021

Note 2 - Summary of Significant Accounting and Reporting Policy

Use of judgment and estimates

The preparation of the consolidated financial statements is in conformity with approved accounting standards which requires management to make judgments, estimates and assumptions that affect the application of policies and reported amounts of assets, liabilities, income and expenses. The estimates and related assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances. The estimates and related assumptions are reviewed on an ongoing basis. Accounting estimates are revised in the period in which such revisions are made and in any future periods affected.

Significant management estimates in these consolidated financial statements relate to the useful life of plant and equipment, provisions and doubtful receivables. However, the management believes that the change in outcome of estimates would not have a material effect on the amounts disclosed in the consolidated financial statements.

Judgment made by management in the application of approved standards that have significant effect on the consolidated financial statements and estimates with a risk of material adjustment in subsequent year are as follows:

Depreciation method, rates and useful lives of property, plant and equipment

The management of the Company reassesses useful lives, depreciation method, and rates for each item of plan and equipment annual by considering expected pattern of economic benefits that the Group expects to derive from those items.

Provisions

Provisions are based on best estimate of the expenditure required to settle the present obligation at the reporting date, that is, the amount that the Group would rationally pay to settle the obligation at the reporting date or to transfer it to a third party.

Impairment

The carrying amounts of the Group's assets are reviewed at each balance sheet date to determine whether there is any indication of impairment loss. If any such indication exists, recoverable amount is estimated in order to determine the extent of the impairment loss, if any. Impairment loss is recorded on judgmental basis, for which provision may differ in the future years based on the actual expense.

Basis of consolidation

The consolidated financial statements include the accounts of the Company and EFLL. All significant inter-company balances and transactions within the Company have been eliminated upon consolidation.

Cash and cash equivalents

The Group considers all highly liquid investments with a maturity of three months or less at the date of acquisition to be cash equivalents.

15

Notes to the Financial Statements

For the three months ended June 30, 2022 and 2021

Note 2 - Summary of Significant Accounting and Reporting Policy - continued

Revenue recognition

ASU No. 2014-09, Revenue from Contracts with Customers (“Topic 606”), became effective for the Company on April 1, 2018 and were adopted using the modified retrospective method. The adoption of the new revenue standards as of April 1, 2018 did not change the Group’s revenue recognition as there were no revenues during the period.

Under the new revenue standards, the Group recognizes revenues when its customer obtains control of promised goods or services, in an amount that reflects the consideration which it expects to receive in exchange for those goods. The Company recognizes revenues following the five step model prescribed under ASU No. 2014-09: (i) identify contract(s) with a customer; (ii) identify the performance obligations in the contract; (iii) determine the transaction price; (iv) allocate the transaction price to the performance obligations in the contract; and (v) recognize revenues when (or as) we satisfy the performance obligation.

The Group’s revenue is derived from provision of air or ocean freight services to the customers located in Hong Kong, and are recognized when the services are performed in accordance with the agreed terms.

Accounts receivable

The Group reviews accounts receivable periodically for collectability and establishes an allowance for doubtful accounts and records bad debt expense when deemed necessary. The allowance for doubtful accounts is maintained to provide for losses arising from customers’ inability to make required payments. If there is deterioration of our customers’ credit worthiness and/or there is an increase in the length of time that the receivables are past due greater than the historical assumptions used, additional allowances may be required. The management of the Company considered as of June 30, 2022, and March 31, 2022, no allowance for doubtful accounts is necessary.

Foreign currency translation

The functional currency of the Company is United States Dollars (“US$”). The functional currency of EFLL is Hong Kong dollars (“HK$”). The Group maintains its consolidated financial statements in US$. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency at rates of exchange prevailing at the balance sheet dates. Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchanges rates prevailing at the dates of the transaction. During the three months ended June 30, 2022, the exchange rate being use to translate amount in HK$ is fixed at 7.8 to US$1 for the purpose of preparing the consolidated financial statements which is derived from October 17, 1983 monetary policy from Hong Kong Monetary Authority where the Hong Kong dollar was pegged at a rate of 7.8 HK$ = 1 US$, through the currency board system with a limited floating range from 7.85 to 7.75. Exchange gains or losses arising from foreign currency transactions are included in the determination of net income for the respective periods.

For financial reporting purposes, the financial statements of the Group which are prepared using the functional currency have been translated into US$. Assets and liabilities are translated at the exchange rates at the balance sheet dates and revenue and expenses are translated at the average exchange rates and stockholders’ equity is translated at historical exchange rates. Any translation adjustments resulting are not included in determining net income but are included in foreign exchange adjustment to other comprehensive income, a component of stockholders’ equity.

Income taxes

The Group provides for income taxes under Statement of Financial Accounting Standards No. 109, Accounting for Income Taxes. SFAS No. 109 requires the use of an asset and liability approach in accounting for income taxes. Deferred tax assets and liabilities are recorded based on the differences between the financial statement and tax bases of assets and liabilities and the tax rates in effect when these differences are expected to reverse. SFAS No. 109 requires the reduction of deferred tax assets by a valuation allowance if, based on the weight of available evidence, it is more likely than not that some or all of the deferred tax assets will not be realized.

16

Notes to the Financial Statements

For the three months ended June 30, 2022 and 2021

Note 2 - Summary of Significant Accounting and Reporting Policy – continued

The provision for income taxes includes income taxes currently payable and those deferred as a result of temporary differences between the financial statements and the income tax basis of assets and liabilities. Deferred income tax assets and liabilities are measured using enacted income tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect of a change in income tax rates on deferred income tax assets and liabilities is recognized in income or loss in the period that includes the enactment date. A valuation allowance is provided to reduce deferred tax assets to the amount of future tax benefit when it is more likely than not that some portion or all of the deferred tax assets will not be realized. Projected future taxable income and ongoing tax planning strategies are considered and evaluated when assessing the need for a valuation allowance. Any increase or decrease in a valuation allowance could have a material adverse or beneficial impact on the Group’s income tax provision and net income or loss in the period the determination is made.

The Company has approximately $

Fair Value Measurements

ASC 820, Fair Value Measurement and Disclosures, defines fair value as the exchange price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. This topic also establishes a fair value hierarchy which requires classification based on observable and unobservable inputs when measuring fair value. There are three levels of inputs that may be used to measure fair value:

Level 1: Observable inputs such as quoted prices (unadjusted) in an active market for identical assets or liabilities.

Level 2: Inputs other than quoted prices that are observable, either directly or indirectly. These include quoted prices for similar assets or liabilities in active markets and quoted prices for identical or similar assets or liabilities in markets that are not active.

Level 3: Unobservable inputs that are supported by little or no market activity; therefore, the inputs are developed by the Group using estimates and assumptions that the Group expects a market participant would use, including pricing models, discounted cash flow methodologies, or similar techniques.

The carrying value of the Group’s financial instruments, including cash and cash equivalents, loan receivables, loan interest receivables, deposit paid, accounts payable and accrued expenses and due to a related party approximate to their fair value because of the short-term maturity of these financial instruments.

Pension Plans

During the three months ended June 30, 2022, the Group participates in a defined contribution pension scheme under the Mandatory Provident Fund Schemes Ordinance (“MPF Scheme”) for all its eligible employees in Hong Kong.

The MPF Scheme is available to all employees aged 18 to 64 with at least 60 days of service in the employment in Hong Kong. Contributions are made by the Group’s subsidiary operating in Hong Kong at 5% of the participants’ relevant income with a ceiling of HK$30,000. The participants are entitled to 100% of the Group’s contributions together with accrued returns irrespective of their length of service with the Group, but the benefits are required by law to be preserved until the retirement age of 65. The only obligation of the Group with respect to MPF Scheme is to make the required contributions under the plan.

17

Notes to the Financial Statements

For the three months ended June 30, 2022 and 2021

Note 2 - Summary of Significant Accounting and Reporting Policy - continued

Leases

Definition of a lease

A contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

For contracts entered into or modified on or after the date of initial application, the Group assesses whether a contract is or contains a lease based on the definition under GAAP ASC 842 at inception or modification date. Such contract will not be reassessed unless the terms and conditions of the contract are subsequently changed.

The Group as a lessee

Allocation of consideration to components of a contract

For a contract that contains a lease component and one or more additional lease or non-lease components, the Group allocates the consideration in the contract to each lease component on the basis of the relative stand-alone price of the lease component and the aggregate stand-alone price of the non-lease components.

The Group also applies practical expedient not to separate non-lease components from lease component, and instead account for the lease component and any associated non-lease components as a single lease component.

Short-term leases and leases of low-value assets

The Group applies the short-term lease recognition exemption to leases that have a lease term of 12 months or less from the commencement date and do not contain a purchase option. It also applies the recognition exemption for lease of low-value assets. Lease payments on short-term leases and leases of low-value assets are recognised as expense on a straight-line basis or another systematic basis over the lease term.

Right-of-use assets

The cost of right-of-use asset includes:

·the amount of the initial measurement of the lease liability;

·any lease payments made at or before the commencement date, less any lease incentives received; and

·any initial direct costs incurred by the Group.

Right-of-use assets are measured at cost, less any accumulated depreciation and impairment losses, and adjusted for any remeasurement of lease liabilities.

Right-of-use assets in which the Group is reasonably certain to obtain ownership of the underlying leased assets at the end of the lease term are depreciated from commencement date to the end of the useful life. Otherwise, right-of-use assets are depreciated on a straight-line basis over the shorter of its estimated useful life and the lease term.

The Group presents right-of-use assets that do not meet the definition of investment property as a separate line item on the statement of financial position.

18

Notes to the Financial Statements

For the three months ended June 30, 2022 and 2021

Note 2 - Summary of Significant Accounting and Reporting Policy - continued

Lease liabilities

At the commencement date of a lease, the Group recognises and measures the lease liability at the present value of lease payments that are unpaid at that date. In calculating the present value of lease payments, the Group uses the incremental borrowing rate at the lease commencement date if the interest rate implicit in the lease is not readily determinable.

The lease payments include:

·fixed payments less any lease incentives receivable;

·variable lease payments that depend on an index or a rate; and

·amounts expected to be payable by the Group under residual value guarantees;

After the commencement date, lease liabilities are adjusted by interest accretion and lease payments.

The Group remeasures lease liabilities (and makes a corresponding adjustment to the related right-of-use assets) whenever:

·the lease term has changed or there is a change in the assessment of exercise of a purchase option, in which case the related lease liability is remeasured by discounting the revised lease payments using a revised discount rate at the date of reassessment.

·the lease payments change due to changes in expected payment under a guaranteed residual value, in which cases the related lease liability is remeasured by discounting the revised lease payments using the initial discount rate.

Lease modifications

The Group accounts for a lease modification as a separate lease if:

·the modification increases the scope of the lease by adding the right to use one or more underlying assets; and

·the consideration for the leases increases by an amount commensurate with the stand-alone price for the increase in scope and any appropriate adjustments to that stand-alone price to reflect the circumstances of the particular contract.

For a lease modification that is not accounted for as a separate lease, the Group remeasures the lease liability based on the lease term of the modified lease by discounting the revised lease payments using a revised discount rate at the effective date of the modification.

The Group accounts for the remeasurement of lease liabilities and lease incentives from lessor by making corresponding adjustments to the relevant right-of-use asset. When the modified contract contains a lease component and one or more additional lease or non-lease components, the Group allocates the consideration in the modified contract to each lease component on the basis of the relative stand-alone price of the lease component and the aggregate stand-alone price of the non-lease components.

Plant and equipment

Plant and equipment is stated at cost less accumulated depreciation and accumulated impairment losses, if any. Expenditures for maintenance and repairs are charged to earnings as incurred. Major additions are capitalized. When assets are retired or otherwise disposed of, the related cost and accumulated depreciation are removed from the respective accounts, and any gain or loss is included in operations. Depreciation of plant and equipment is provided using the straight-line method for substantially all assets with estimated lives as follows:

|

| Estimated Useful Life |

Office equipment |

|

19

Impairment of long-lived assets

The Group evaluates long lived assets, including equipment, for impairment at least once per year and whenever events or changes in circumstances indicate that the carrying value may not be recoverable from its estimated future cash flows. Based on the existence of one or more indicators of impairment, the Group measures any impairment of long-lived assets by comparing the asset's estimated fair value with its carrying value, based on cash flow methodology. If the net book value of the asset exceeds the related undiscounted cash flows, the asset is considered impaired and an impairment loss equal to an amount by which the carrying value exceeds the fair value of the asset is recognized.

Comprehensive income

U.S. GAAP generally requires that recognized revenue, expenses, gains and losses be included in net income or loss. Although certain changes in assets and liabilities are reported as separate components of the equity section of the consolidated balance sheet, such items, along with net income, are components of comprehensive income or loss.

Recent Accounting Pronouncements

Accounting pronouncement adopted

In July 2017, the FASB issued ASU No. 2017-11, Earnings Per Share (Topic 260), Distinguishing Liabilities from Equity (Topic 480); Derivatives and Hedging (Topic 815): (Part I) Accounting for Certain Financial Instruments with Down Round Features, (Part II) Replacement of the Indefinite Deferral for Mandatorily Redeemable Financial Instruments of Certain Nonpublic Entities and Certain Mandatorily Redeemable Noncontrolling Interests with a Scope Exception (“ASU 2017-11”). ASU 2017-11 is intended to simplify the accounting for financial instruments with characteristics of liabilities and equity. Among the issues addressed are: (i) determining whether an instrument (or embedded feature) is indexed to an entity’s own stock; (ii) distinguishing liabilities from equity for mandatorily redeemable financial instruments of certain nonpublic entities; and (iii) identifying mandatorily redeemable non-controlling interests. The Group adopted ASU 2017-11 on April 1, 2019 and determined that this ASU does not have a material impact on the financial statements.

In August 2018, the FASB issued ASU 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework: Changes to the Disclosure Requirements for Fair Value Measurement (“ASU 2018-13”). ASU 2018-13 is intended to improve the effectiveness of fair value measurement disclosures. ASU 2018-13 is effective for fiscal years beginning after December 15, 2019, and interim periods within those fiscal years. Early adoption is permitted. The Group determined that ASU 2018-13 did not have a material impact on its financial statements.

In December 2019, the Financial Accounting Standards Board (FASB) issued Accounting Standard Update No. 2019-12, Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes (ASU 2019-12), which simplifies the accounting for income taxes. This guidance will be effective for us in the first quarter of 2021 on a prospective basis, with early adoption permitted. The Group determined that the adoption of this guidance to have a material impact on our consolidated financial statements.

20

Notes to the Financial Statements

For the three months ended June 30, 2022 and 2021

Note 2 - Summary of Significant Accounting and Reporting Policy - continued

In response to the COVID-19 pandemic, the Coronavirus Aid, Relief and Economic Security Act (“CARES Act”) was signed into law in March 2020. The CARES Act lifts certain deduction limitations originally imposed by the Tax Cuts and Jobs Act of 2017 (“2017 Tax Act”). Corporate taxpayers may carryback net operating losses (NOLs) originating between 2018 and 2020 for up to five years, which was not previously allowed under the 2017 Tax Act. The CARES Act also eliminates the 80% of taxable income limitations by allowing corporate entities to fully utilize NOL carryforwards to offset taxable income in 2018, 2019 or 2020. Taxpayers may generally deduct interest up to the sum of 50% of adjusted taxable income plus business interest income (30% limit under the 2017 Tax Act) for 2019 and 2020. The CARES Act allows taxpayers with alternative minimum tax credits to claim a refund in 2020 for the entire amount of the credits instead of recovering the credits through refunds over a period of years, as originally enacted by the 2017 Tax Act.

In addition, the CARES Act raises the corporate charitable deduction limit to 25% of taxable income and makes qualified improvement property generally eligible for 15-year cost-recovery and 100% bonus depreciation. The enactment of the CARES Act did not result in any material adjustments to our income tax provision for the year ended June 30, 2022.

In June 2016, the FASB issued ASU 2016-13, Financial Instruments–Credit Losses (Topic 326), which modifies the measurement of expected credit losses of certain financial instruments. The Group will adopt this ASU on April 1, 2023. Management is currently evaluating this ASU to determine its impact to the Group's financial statements.

In December 2019, The FASB issued ASU 2019-12, Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes. The amendments in this Update simplify the accounting for income taxes by removing certain exceptions to the general principles in Topic 740. The amendments also improve consistent application of and simplify GAAP for other areas of Topic 740 by clarifying and amending existing guidance. For non-public companies, the amendments in this Update are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2021. The Group is currently evaluating the impact of ASU 2020-04 on its future financial statements.

In March 2020, the FASB issued ASU 2020-04, Reference Rate Reform (Topic 848): Facilitation of Reference Rate Reform on Financial Reporting. The amendments in this Update provide optional expedients and exceptions for applying generally accepted accounting principles (GAAP) to contracts, hedging relationships, and other transactions affected by reference rate reform if certain criteria are met. The amendments in this Update apply only to contracts, hedging relationships, and other transactions that reference LIBOR or another reference rate expected to be discontinued because of reference rate reform. The Group’s line of credit agreement provides procedures for determining a replacement or alternative rate in the event that LIBOR is unavailable. The amendments in this Update are effective for all entities as of March 12, 2020 through December 31, 2022. The Group is currently evaluating the impact of ASU 2020-04 on its future financial statements.

The Group has implemented all new accounting pronouncements that are in effect and that may impact its financial statements and does not believe that there are any other new accounting pronouncements that have been issued that might have a material impact on its financial position or results of operations.

Provisions

Provisions are recognised when the Group has a present obligation (legal or constructive) as a result of a past event, it is probable that the Group will be required to settle that obligation, and a reliable estimate can be made of the amount of the obligation. The amount recognised as a provision, is the best estimate of the consideration required to settle the present obligation at the end of the reporting period, taking into account the risks and uncertainties surrounding the obligation. When a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows (where the effect of the time value of money is material).

21

Notes to the Financial Statements

For the three months ended June 30, 2022 and 2021

Note 2 - Summary of Significant Accounting and Reporting Policy – continued

Segment Reporting

The Group uses the “management approach” in determining reportable operating segments. The management approach considers the internal organization and reporting used by the Company’s chief operating decision maker for making operating decisions and assessing performance as the source for determining the Group’s reportable segments. Management, including the chief operating decision maker, reviews operating results solely by monthly revenue from air/ocean freight services (but not by sub-services/product type or geographic area) and operating results of the Group and, as such, the Group has determined that the Group has one operating segment as defined by ASC Topic 280 “Segment Reporting”.

Note 3 – Revenue

|

|

| Three months ended | |

|

|

| June 30, | |

|

|

| 2022 | 2021 |

|

|

| $ | $ |

|

|

|

|

|

Air/ocean freight services income |

|

| ||

Note 4 – General and Administrative Expenses

|

|

| Three months ended | |

|

|

| June 30, | |

|

|

| 2022 | 2021 |

|

|

| $ | $ |

|

|

|

|

|

Courier |

|

| ||

Depreciation |

|

| ||

Electricity and water |

|

| ||

Entertainment |

|

| ||

Medical |

|

| ||

MPF contributions |

|

| ||

Printing and stationery |

|

| ||

Professional fee |

|

| ||

Rental expenses |

|

| ||

Salaries and wages |

|

| ||

Staff welfare |

|

| ||

Telecommunication and IT |

|

| ||

Sundry expenses |

|

| ||

Transportation expenses |

|

| ||

|

|

|

|

|

|

|

| ||

22

Notes to the Financial Statements

For the three months ended June 30, 2022 and 2021

Note 5 – Plant and Equipment

|

|

| June 30, | March 31, |

|

|

| 2022 | 2022 |

|

|

| $ | $ |

|

|

|

|

|

Office equipment |

|

| ||

Less: accumulated depreciation |

|

| ( | ( |

|

|

|

|

|

|

|

|

Depreciation expense for the three months ended June 30, 2022 and 2021 amounted to $

Note 6 – Right-of-use Assets

|

|

| June 30, | March 31, |

|

|

| 2022 | 2022 |

|

|

| $ | $ |

|

|

|

|

|

Leased property |

|

|

The Group lease an office property for its operations. Lease contract is entered into for fixed term of within 2 years. Lease terms are negotiated on an individual basis and contain a wide range of different terms and conditions. In determining the lease term and assessing the length of the non-cancellable period, the Group applies the definition of a contract and determines the period for which the contract is enforceable.

Note 7 – Creditors, accruals and other payables

|

|

| June 30, | March 31, |

|

|

| 2022 | 2022 |

|

|

| $ | $ |

|

|

|

|

|

Creditors |

|

| ||

Accruals |

|

| ||

Notes payable |

|

| ||

Due to a related party |

|

| ||

Shareholders’ loan payable |

|

| ||

|