U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

__________________

FORM 10-K

__________________

(Mark one)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2018 |

| o | TRANSITION REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 for the transition period from ________________ to________________________. |

Commission File Number: 000-27055

CANNAPHARMARX, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 27-4635140 | |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |

|

Suite 206 1180 Sunset Drive Kelowna, BC, Canada |

Z1Y 9W6 | 949-652-6838 |

| (Address of principal executive office) | (Zip Code) | (Registrant’s telephone number, Including area code) |

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act: Common Stock.

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $0.0001 par value | OTC Pink Sheets |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o Yes x No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one)

| Large accelerated filer o | Accelerated filer o |

| Non-accelerated filer o | Smaller Reporting Company x |

| Emerging growth company x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). x Yes o No

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter on June 30, 2018 was $17,422,378.

As of March 29, 2019, the Registrant had 26,791,371 shares of Common Stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s Proxy Statement for the Annual Meeting of Shareholders to be held on or about June 21, 2019, or such other date as may be selected in the future, are incorporated by reference in certain sections of PART III.

| i |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The statements regarding Cannapharmarx contained in this Report that are not historical in nature, particularly those that utilize terminology such as “may,” “will,” “should,” “likely,” “expects,” “anticipates,” “estimates,” “believes” or “plans,” or comparable terminology, are forward-looking statements based on current expectations and assumptions, and entail various risks and uncertainties that could cause actual results to differ materially from those expressed in such forward-looking statements.

Important factors known to us that could cause such material differences are identified in this Report. We undertake no obligation to correct or update any forward-looking statements, whether as a result of new information, future events or otherwise. You are advised, however, to consult any future disclosures we make on related subjects in future reports to the SEC.

| ii |

| ITEM 1. | BUSINESS. |

History

We were originally incorporated in the State of Colorado in August 1998 under the name “Network Acquisitions, Inc.” We changed our name to Cavion Technologies, Inc. in February 1999 and subsequently to Concord Ventures, Inc. in October 2006.

On December 21, 2000, we filed for protection under Chapter 11 of the United States Bankruptcy Code. In connection with the filing, on February 16, 2001, we sold our entire business, and all of our assets, for the benefit of our creditors. After the sale, we still had liabilities of $8.4 million and were subsequently dismissed by the Court from the Chapter 11 reorganization, effective March 13, 2001, at which time the last of our remaining directors resigned. On March 13, 2001, we had no business or other source of income, no assets, no employees or directors, outstanding liabilities of approximately $8.4 million and had terminated our duty to file reports under securities law. In February 2008, we were re-listed on the OTC Bulletin Board.

In April 2010, we re-domiciled in Delaware under the name CCVG, Inc. (“CCVG”). Effective December 31, 2010, CCVG completed an Agreement and Plan of Merger and Reorganization (the “Reorganization") which provided for the merger of two of our wholly-owned subsidiaries. As a result of this reorganization, our name was changed to “Golden Dragon Inc.”, which became the surviving publicly quoted parent holding company.

On May 9, 2014, we entered into a Share Purchase Agreement (the “Share Purchase Agreement”) with CannaPharmaRX, Inc., a Colorado corporation (“Canna Colorado”), and David Cutler, a former President, Chief Executive Officer, Chief Financial Officer and director of our Company. Under the Share Purchase Agreement, Canna Colorado purchased 1,421,120 shares of our common stock from Mr. Cutler and an additional 9,000,000 restricted common shares directly from us.

On May 15, 2014, as amended and effective January 29, 2015, we entered into an Agreement and Plan of Merger (the “Merger”) pursuant to which Canna Colorado became a subsidiary of our Company. In October 2014, we changed our legal name to “CannaPharmaRx, Inc.”

Pursuant to the Merger all of the shares of our common stock previously owned by Canna Colorado were canceled. As a result of the aforesaid transactions, we became an early-stage pharmaceutical company whose purpose was to advance cannabinoid research and discovery using proprietary formulation and drug delivery technology then under development.

In April 2016, we ceased operations. Our then management resigned their respective positions with our Company with the exception of Mr. Gary Herick, who remains as one of our officers and directors as of the date of this Report.

Description of Current Business

Effective November 19, 2018, we entered into a Securities Purchase Agreement with Alternative Medical Solutions, Inc., an Ontario, Canada corporation (“AMS”), its shareholders and Hanover CPMD Acquisition Corp., wherein we acquired all of the issued and outstanding securities of AMS. As part of the material terms of this transaction, we also agreed to acquire all of the outstanding shareholder loans held by the principal shareholder of AMS. The purchase price was CAD$12,700,000, of which CAD$1,012,982 was paid at closing and we assumed debt of approximately CAD$650,000. The principal shareholders of AMS elected to receive 971,765 shares of our Common Stock in lieu of CAD$985,000 in additional cash. We granted the holders of these shares “piggyback” registration rights. The balance of approximately CAD$10,000,000 is to be paid pursuant to the terms of a relevant subordinated non-interest bearing promissory note, secured only by the shares acquired in AMS Principal payments under the Promissory Note are due quarterly and are computed based upon 50% of AMS' cash flow, defined as EBITDA less all capital expenditures, taxes incurred, non-recurring items and other non-cash items for the relevant fiscal quarter, including the servicing of all senior debt payment obligations of the company. The Promissory Note matures the earlier of two years from the date AMS receives a license to cultivate or December 31, 2021, whichever is later.

| 3 |

Relevant thereto, in January 2019 we also entered into a two year Consulting Agreement with Stephen Barber, a founder and principal shareholder of AMS, to assist us in our ongoing discussions and negotiations with various governmental agencies, including the City of Hanover and Province of Ontario, whereby we agreed to pay (i) a consulting fee of US$225,000, payable on or before April 30, 2019, along with a monthly fee of CAD$1,500 and (ii) an option to purchase up to 500,000 shares of our common stock at an exercise price of USD$1.00 per share, which option shall expire November 19, 2020. Further, we agreed to repurchase 45,000 shares of the stock issued to him as part of the AMS acquisition for CAD$33,750 (USD$0.75 per share) on or before April 30, 2019.

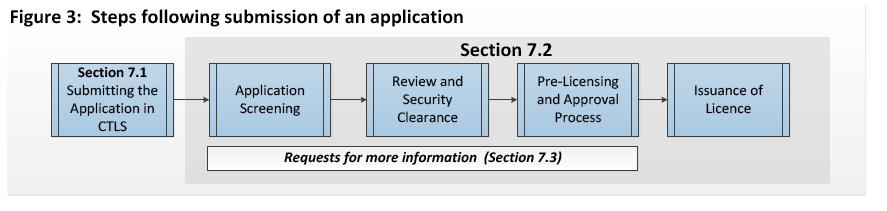

As a result of the AMS acquisition described above, we are again engaged in the cannabis business. AMS is a corporation organized under the laws of the Province of Ontario, Canada. AMS has filed a cultivation application. The application process is a phased approach with Health Canada issuing a Confirmation of Readiness letter during the late stages of the application process. This letter confirms that if the applicant builds out the facility, as described, Health Canada will review the documentation and further assess the applicant’s suitability in obtaining the License to Cultivate. At the completion of construction, the applicant submits an evidence package showing that the facility design and construction meets the Good Production Practices and Security Design described in the application. After review, Health Canada issues the License to Cultivate and then follows up with unannounced inspections as the company becomes operational. Following the successful completion of two batches Health Canada will inspect and issue the License to Sell. The AMS application was in the Confirmation of Readiness stage in the previous regulatory structure. On October 17, 2018, The Cannabis Regulations (SOR/2018-144) came into effect. With the new regulations, the AMS application will need to be transitioned to the Cannabis Tracking and Licensing System (CTLS). The new process will follow a similar process as described in the Cannabis Licensing Application Guide, below:

After the application is transitioned to the new regulations, Health Canada will review compliance with the new regulations and again issue the Confirmation of Readiness.

The AMS cultivation facility is a 48,750 square foot cannabis grow facility built on a 6.7-acre parcel of land located in Hanover, Ontario Canada. To date, exterior construction of the building has been completed, however, no interior construction has begun. Upon full completion, the facility will contain up to 20 separate growing rooms which we believe will provide annual production capacity of 9,500 kilos of cannabis (20,900 lbs.). Completion of the build-out of the facility is expected to take an estimated 20 weeks. Together with the remaining equipment needed to complete the grow we estimate that we will require approximately CAD$20 million in additional financing which we will seek to raise via equity and debt. While there can be no assurances that we will successfully raise the financing required to complete construction of the facility and begin cultivation, we have had several initial discussions with funding sources and while no assurances can be provided, we believe we will be able to obtain such financing. Failure to obtain such financing will have a significant negative impact on our ability to successfully implement our business plan.

A Cultivation License issued in Canada gives the licensee the right to produce, possess, ship, transport, deliver and destroy dried cannabis and cannabis plants, as well as cannabis oil extracts. The Cultivation License is issued to the licensee for use only at a designated facility. In the case of AMS, the Hanover Facility will be the designated location.

| 4 |

A Sales License may be obtained during the Cultivation License application process, and as a final step of that general process, as described below.

In 2018 AMS received its Confirmation of Readiness for a license under Canadian law. The Confirmation of Readiness is the result of a successful Initial Screening of the application by Health Canada. At the stage of the initial screening, the (i) the proposed business plan; (ii) the Security Clearance Application Form and (iii) record-keeping methods pertaining to security, Good Production Practices, inventory, and destruction methods of AMS were assessed and deemed satisfactory by Health Canada. In parallel to the Initial Screening process, Health Canada conducted the required security clearance process of the proposed personnel. AMS was notified by Health Canada that all members of proposed personnel had obtained the required security clearance. All of these people have been retained by us following the closing of the AMS acquisition.

In the course of the Detailed Review stage, AMS was asked to submit specific information to Health Canada, which was reviewed to:

| · | complete the assessment of the application to ensure that it met the requirements of applicable law and regulations; |

| · | establish that the issuance of the License was not likely to create risks to public health, safety or security, including the risk of cannabis being diverted to an illicit market or use; and |

| · | establish that there were no other grounds for refusing the application. |

As of the date of this report, the Officer of Medical Cannabis in Canada has asked AMS to confirm or provide evidence of the following items (the “Evidence Package”):

The perimeter of the site is in compliance with sections 43 to 45 of the MMPR, which include:

| · | operational visual recording device capable of recording any unauthorized access; | |

| · | operational intrusion monitoring systems to detect any attempted or actual unauthorized access to, or movement in, the site, or tampering with the system; and | |

| · | all systems are monitored by personnel at all times. |

The areas within a site where cannabis is present are in compliance with sections 46 to 49 of the MMPR, which include:

| · | all areas are capable of recording the identity of every person entering or exiting those areas; | |

| · | operational visual recording devices capable of detecting illicit conduct in those areas; | |

| · | operational intrusion monitoring system in those areas; | |

| · | operational system in those areas to prevent the escape of odors and, if present, pollen; and | |

| · | all systems are monitored by personnel at all times. |

The storage area is in compliance with security level 9 under the Security Directive for the storage of dried marihuana (cannabis, its preparations, derivatives, and similar synthetics).

In addition, it was requested that AMS confirm that the proposed sites comply with:

| · | all the Good Production Practices as required under Division 4; and | |

| · | all requirements for Record Keeping as required under Part 6 of the MMPR. |

| 5 |

In reviewing the Evidence Package, consideration is specifically given to AMS’s proposed security measures and the description of the storage area for cannabis as required by the Security Directive; the credentials of the proposed quality assurance person to meet the good production requirements under Canadian law and the details listed in the quality assurance report relating to premises, equipment and sanitation program. Physical security plans will also be reviewed and assessed in detail at this stage.

AMS will be in a position to begin assembling the Evidence Package as the construction of the Hanover Facility progresses, and once it is completed and the Hanover Facility becomes operational. To date, exterior construction of the building has been completed, but no interior construction has begun. We expect that we will be in a position to submit the Evidence Package to the Officer of Medical Cannabis shortly following the completion of the Hanover Facility.

Upon the completion of the Detailed Review stage, Health Canada is expected to issue a Cultivation License. As part of the terms and conditions on the license, a Licensed Producer is required to notify Health Canada once it begins cultivation. Once notified, Health Canada will schedule an initial inspection to verify that the Licensed Producer is meeting the requirements of applicable Canadian law including, but not limited to, the physical security requirements for the site, record-keeping practices, and Good Production Practices and to confirm that the activities being conducted by the Licensed Producer correspond to those indicated on their License.

Once AMS is issued a Cultivation License, in order to be authorized for the activity of sale specifically, AMS will have to undergo a Pre-Sale Inspection by Health Canada and submit an amendment application to the Office of Medical Cannabis. Health Canada will then schedule an inspection to verify that AMS, as a Licensed Producer, is meeting the requirements of applicable Canadian law including, but not limited to, Good Production Practices, packaging, labeling, shipping, and record keeping prior to allowing the sale or provision of product.

To complete the assessment of the requirements under Canadian law and establish that adding the activity of sale of cannabis products is not likely to create a risk to public health, safety or security, and to confirm that there are no other grounds for refusing the amendment application, the following information is reviewed

| · | results of the pre-sale inspection; |

| · | information submitted in the amendment application to add the activity of sale to the license; and |

| · | any other relevant information. |

When the review is completed, an amended license (i.e. the Sales License), including the activity of sale, may be issued to the Licensed Producer. The Licensed Producer may then begin supplying cannabis products to registered clients, other licensed producers and/or other parties named, depending on the activities licensed.

While no assurances can be provided, based on our knowledge of the licensing process under current Canadian law, we expect that we will be in a position to obtain a Cultivation License by the end of 2019, and a Sales License by the end of June 2020, subject to our ability to raise the funds necessary to complete the interior of the property, of which there is no assurance. The Detailed Review stage will be completed once we complete that construction of a site and production facility that is compliant with the requirements listed above. Based on our projected construction timeline we expect that the construction of the Hanover Facility will be completed by the end of 2019, and that at that time we will have satisfied all of the requirements found in the Confirmation of Readiness and will be in a position to submit the Evidence Package to the Officer of Medical Cannabis. This proposed timeline is only an estimate based on our observations and knowledge of the licensing process under applicable Canadian law and could vary significantly.

| 6 |

License Renewal Processes

Once we obtain the Licenses, any adverse changes or events affecting the construction of the Hanover Facility, or the facility itself once built, could have a material and adverse effect on our ability to continue producing cannabis, our business, financial condition, and prospects.

Once AMS receives the Licenses, before the expiration of the expiry date stipulated on the Licenses, AMS must submit an application for renewal to Health Canada containing information prescribed by the ACMPR.

Canadian law requires that the Minister of Health, after examining the application and any supplementary information requested, issue a renewed License, unless:

(a) the applicant is not an adult who ordinarily resides in Canada or a corporation that has its head office in Canada or operates a branch office in Canada and whose officers and directors are all adults;

(b) the requirements regarding notification of local authorities pursuant to the ACMPR have not been met (such notifications would only be required in connection with a renewal if there are changes to the information since the original application);

(c) an inspector, who has requested an inspection, has not been given the opportunity by the applicant to conduct an inspection;

(d) the Minister has reasonable grounds to believe that false or misleading information or false or falsified documents were submitted in or with the application;

(e) information received from a peace officer, a competent authority or the United Nations raises reasonable grounds to believe that the applicant has been involved in the diversion of a controlled substance or precursor to an illicit market or use;

(f) the applicant does not have in place the security measures set out in the applicable Canadian law in respect of an activity for which the License is sought;

(g) the applicant is in contravention of or has contravened in the past 10 years:

(i) a provision of the Controlled Drugs and Substances Act (the “CDSA”) or its regulations or the Food and Drugs Act, or

(ii) a term or condition of another Licensor a permit issued to it under any of those regulations;

(h) the renewal of the License would likely create a risk to public health, safety or security, including the risk of cannabis being diverted to an illicit market or use;

(i) any of the following persons do not hold a security clearance:

(i) the senior person in charge,

(ii) the responsible person in charge,

(iii) if applicable, the alternate responsible person in charge,

(iv) if the applicant is an individual, that individual, and

(v) if the applicant is a corporation, any of its officers or directors;

(j) the proposed method of record keeping does not meet the requirements of the ACMPR; or

(k) if applicable, any supplemental information requested has not been provided or is insufficient to process the application.

There can be no guarantee that Health Canada will extend or renew the Licenses as necessary or, if it extended or renewed, that the Licenses will be extended or renewed on the same or similar terms. Should Health Canada not extend or renew the Licenses, or should it renew the Licenses on different terms, the business, financial condition and results of the operation of AMS would be materially adversely affected.

| 7 |

Subsequent Event

Effective February 25, 2019, we acquired 3,712,500 shares and 2,500,000 Warrants to purchase 2,500,000 shares of Common Stock of GN Ventures, Ltd, Alberta, Canada, f/k/a Great Northern Cannabis, Ltd. (“GN”), in exchange for an aggregate of 7,988,963 shares of our Common Stock, from a former shareholder of GN who is now our President and CEO. These shares and warrants, when exercised, will represent 18% and 11%, respectively, of the issued and outstanding stock of GN. While no assurances can be provided, we believe this is the initial step in our efforts to acquire all of the issued and outstanding stock of GN. We anticipate making additional purchases of stock from other shareholders of GN during 2019. The seller of the GNC interests is the former President, CEO and a director of our Company, positions he assumed again after the acquisition. He had resigned his positions prior to the commencement of discussions on this acquisition in order to fully recuse himself from this matter.

GN owns a 60,000 square foot cannabis cultivation and grow facility located on 38 acres in Stevensville, Ontario, Canada. Once completed, GN estimates annual total production capacity from the Stevensville facility of up to 12,500 kilograms of cannabis. GN believes the Stevensville facility to be 95% complete and to receive a license to cultivate from the Canadian Ministry of Health prior to the end of the second quarter of 2019. If and when completed, GN believes it will begin cultivation activities and generate its initial harvest during the middle of 2019. Additionally, the plan is to increase cannabis production by building additional cannabis cultivation facilities on the excess land presently owned adjacent to the existing Stevensville facility, provided that additional funding can be obtained on commercially reasonable terms. GN does not have any firm commitment to provide any of the funds necessary for expansion as of the date of this release.

While there can be no assurances, we will be successful in acquiring all of the issued and outstanding stock of GN, we intend to dual list our common stock for trading on the Canadian Securities Exchange (“CSE”) as a precursor to consummating a transaction with GN. We anticipate filing our initial listing application with the CSE during April 2019 and, while no assurances can be provided, anticipate receiving approval for trading during the second quarter of 2019.

We estimate that in order to consummate the acquisition of GN, as well as to complete development of the cultivation facilities we presently own located in Hanover, Ontario, we will require up to CAD$20 million in additional financing. We cannot provide any assurances that we will be able to raise such funds or whether we would be able to raise such funds on terms that are favorable to us. We may seek to borrow monies from lenders at commercial rates, but such lenders will probably charge higher than bank rates, which higher rates could, depending on the amount borrowed, der the net operating income of any of our planned profitable businesses insufficient to cover the interest burden.

Currently, we have no committed source for any funds to allow us to complete the Hanover project. No representation is made that any funds will be available when needed. In the event funds cannot be raised if and when needed, we may not be able to carry out our business plan and could fail in business as a result of these uncertainties.

Growth by Acquisition

We also plan to grow through the acquisition of related, complementary businesses. In doing so we expect to increase revenues and profits by providing a broader range of services in vertical markets which are consolidated under one parent, thus realizing synergies between the brands to increase sales on multiple fronts; reducing overhead costs by streamlining operations; and eliminating duplicitous efforts and costs. There are no assurances that we will increase profitability if we are successful in acquiring other synergistic companies.

If we are successful, the acquisition of related, complementary businesses is expected to increase revenues and profits by providing a broader range of services in vertical markets which are consolidated under one parent, thus reducing overhead costs by streamlining operations and eliminating duplicitous efforts and costs. There are no assurances that we will increase profitability if we are successful in acquiring other synergistic companies.

| 8 |

Management continues to seek out and evaluate related, complementary businesses for acquisition. The integrity and reputation of any potential acquisition candidate will first be thoroughly reviewed to ensure it meets with management’s standards. Once targeted as a potential acquisition candidate, we will enter into negotiations with the potential candidate and commence due diligence evaluation, including its financial statements, cash flow, debt, location and other material aspects of the candidate’s business. It is our intention to utilize the issuance of our securities as part of the consideration that we will pay for these proposed acquisitions. If we are successful in our attempts to acquire synergistic companies utilizing our securities as part or all of the consideration to be paid, our current shareholders will incur dilution.

In implementing a structure for a particular acquisition, we may become a party to a merger, consolidation, reorganization, joint venture, or licensing agreement with another corporation or entity. We may also acquire stock or assets of an existing business.

As part of our investigation, our officers and directors will meet personally with management and key personnel, may visit and inspect material facilities, obtain independent analysis of verification of certain information provided, check references of management and key personnel, and take other reasonable investigative measures, to the extent of our limited financial resources and management expertise. The manner in which we participate in an acquisition will depend on the nature of the opportunity, the respective needs, and desires of the parties, the management of the acquisition candidate and our relative negotiation strength.

We will participate in an acquisition only after the negotiation and execution of appropriate written agreements. Although the terms of such agreements cannot be predicted, generally such agreements will require some specific representations and warranties by all of the parties thereto, will specify certain events of default, will detail the terms of closing and the conditions which must be satisfied by each of the parties prior to and after such closing, will outline the manner of bearing costs, including costs associated with our attorneys and accountants, will set forth remedies on default and will include miscellaneous other terms.

Depending upon the nature of the acquisition, including the financial condition of the acquisition company, as a reporting company under the Securities Exchange Act of 1934 (the “34 Act”), it may be necessary for such acquisition candidate to provide independent audited financial statements. If so required, we will not acquire any entity which cannot provide independent audited financial statements within a reasonable period of time after closing of the proposed transaction. If such audited financial statements are not available at closing, or within time parameters necessary to ensure our compliance with the requirements of the 34 Act, or if the audited financial statements provided do not conform to the representations made by the candidate to be acquired in the closing documents, the closing documents will provide that the proposed transaction will be voidable, at the discretion of our present management. If such transaction is voided, the agreement will also contain a provision providing for the acquisition entity to reimburse us for all costs associated with the proposed transaction.

We intend to continue a focus on the acquisition of additional companies operating in jurisdictions where cannabis is legal on a national basis. Our focus is initially on Canadian Licensed Producers of marijuana but may extend to other cannabis-related products. If and when cannabis becomes legal in other foreign jurisdictions we will research acquisition or development opportunities. We intend to target opportunities which are revenue generating or will be in the immediate future, low-cost producers and either profitable or nearing profitability.

We are presently in discussion with other companies operating in the cannabis industry regarding a potential acquisition or other form of partnership. Relevant thereto, we have signed a non-binding letter of intent to acquire Great Northern Cannabis Ltd of Calgary, Alberta, Canada. However, there can be no assurance we will be successful consummating any additional acquisitions in the future, nor can there be any assurance we will have access available to equity and debt financing required to consummate any transaction in the future.

We do not engage in any U.S. cannabis-related activities unless and until federal laws on cannabis prohibition are eliminated and cannabis is no longer considered a Schedule I controlled substance. If this changes in the future we may review opportunities in the United States if such opportunities arise under acceptable terms and conditions. There are no assurances this will occur.

| 9 |

Employees

Until November 2018, we had no employees except our management at that time. Upon the closing of the AMS transaction we retained three of the former AMS employees, including individuals who shall continue to assist AMS with its pending Application and related issuance to AMS of a producer's license under Canadian law, who shall continue to act as a "senior person in charge", "responsible person in charge" or "alternate responsible person in charge" pursuant to applicable Canadian law.

We anticipate that we will retain additional employees as we close additional acquisitions in the future, of which there is no assurance. We believe that there are a sufficient number of potential qualified employees available. No employee is a member of any union. We believe our relationship with our employees is satisfactory.

Competition

We are competing with other companies, both publicly held and private, who are also seeking to acquire or otherwise consolidate with an existing Canadian cannabis business. Many of our competitors have greater resources, both financial and otherwise, than the resources presently available to us.

Intellectual Property

We currently do not hold any patents or patent applications. We hold one registered trademark, Recruit Registry™. This Report contains additional trademarks, service marks, or trade names of others. Our use or display of other parties’ trademarks, service marks or trade names is not intended to imply and does not imply a relationship with, or endorsement of, such parties. We seek to protect our proprietary information, including our trade secrets and proprietary know-how, by requiring our employees, consultants and other advisors to execute confidentiality agreements upon the commencement of their employment or engagement. These agreements generally provide that all confidential information developed or made known during the course of the relationship with us be kept confidential and not be disclosed to third parties except in specific circumstances. In the case of our employees, the agreements also typically provide that all inventions resulting from work performed for us, utilizing our property or relating to our business and conceived or completed during employment shall be our exclusive property to the extent permitted by law. Where appropriate, agreements we obtain with our consultants also typically contain similar assignment of invention provisions. Further, we generally require confidentiality agreements from business partners and other third parties that receive our confidential information.

Government Regulation

It is our intention to continue to emphasize the cannabis industry in our search for business opportunities, specifically in Canada. As of the date of this report we do not have any intention of engaging in the cannabis industry in the United States so long as marijuana remains a Schedule-I controlled substance and remains illegal under US federal law.

A Schedule I controlled substance is defined as a substance that has no currently accepted medical use in the United States, a lack of safety for use under medical supervision and a high potential for abuse. The Department of Justice defines Schedule 1 controlled substances as “the most dangerous drugs of all the drug schedules with potentially severe psychological or physical dependence.” If the applicable federal laws are repealed to eliminate cannabis as a controlled substance in the US we will consider potential cannabis acquisitions in the US.

| 10 |

Canadian Regulations

Summary of the Cannabis Act

On October 17, 2018, the Cannabis Act came into force as law with the effect of legalizing adult recreational use of cannabis across Canada. The Cannabis Act replaced the ACMPR and the IHR, both of which came into force under the Controlled Drugs and Substances Act (Canada) (the “CDSA”), which previously permitted access to cannabis for medical purposes for only those Canadians who had been authorized to use cannabis by their health care practitioner. The ACMPR replaced the Marihuana for Medical Purposes Regulations (Canada) (the “MMPR”), which was implemented in June 2013. The MMPR replaced the Marihuana Medical Access Regulations (Canada) (the “MMAR”) which was implemented in 2001. The MMPR and MMAR were initial steps in the Government of Canada’s legislative path towards the eventual legalization and regulating recreational and medical cannabis.

The Cannabis Act permits the recreational adult use of cannabis and regulates the production, distribution and sale of cannabis and related oil extracts in Canada, for both recreational and medical purposes. Under the Cannabis Act, Canadians who are authorized by their health care practitioner to use medical cannabis have the option of purchasing cannabis from one of the producers licensed by Health Canada and are also able to register with Health Canada to produce a limited amount of cannabis for their own medical purposes or to designate an individual who is registered with Health Canada to produce cannabis on their behalf for personal medical purposes.

Pursuant to the Cannabis Act, subject to provincial regulations, individuals over the age of 18 are be able to purchase fresh cannabis, dried cannabis, cannabis oil, and cannabis plants or seeds and are able to legally possess up to 30 grams of dried cannabis, or the equivalent amount in fresh cannabis or cannabis oil. The Cannabis Act also permits households to grow a maximum of four cannabis plants. This limit applies regardless of the number of adults that reside in the household. In addition, the Cannabis Act provides provincial and municipal governments the authority to prescribe regulations regarding retail and distribution, as well as the ability to alter some of the existing baseline requirements of the Cannabis Act, such as increasing the minimum age for purchase and consumption.

Provincial and territorial governments in Canada have made varying announcements on the proposed regulatory regimes for the distribution and sale of cannabis for adult-use purposes. For example, Québec, New Brunswick, Nova Scotia, Prince Edward Island, Yukon and the Northwest Territories have chosen the government-regulated model for distribution, whereas Saskatchewan and Newfoundland & Labrador have opted for a private sector approach. Alberta, Ontario, Manitoba, Nunavut and British Columbia have announced plans to pursue a hybrid approach of public and private sale and distribution.

In connection with the new framework for regulating cannabis in Canada, the Federal Government has introduced new penalties under the Criminal Code (Canada), including penalties for the illegal sale of cannabis, possession of cannabis over the prescribed limit, production of cannabis beyond personal cultivation limits, taking cannabis across the Canadian border, giving or selling cannabis to a youth and involving a youth to commit a cannabis-related offence.

On July 11, 2018, the Federal Government published regulations in the Canada Gazette to support the Cannabis Act, including the Cannabis Regulations, the new Industrial Hemp Regulations, along with proposed amendments to the Narcotic Control Regulations and certain regulations under the Food and Drugs Act (Canada). The Industrial Hemp Regulations and the Cannabis Regulations, among other things, outline the rules for the legal cultivation, processing, research, analytical testing, distribution, sale, importation and exportation of cannabis and hemp in Canada, including the various classes of licenses that can be granted, and set standards for cannabis and hemp products. The Industrial Hemp Regulations and the Cannabis Regulations include strict specifications for the plain packaging and labeling and analytical testing of all cannabis products as well as stringent physical and personnel security requirements for all federally licensed production sites. The Industrial Hemp Regulations and the Cannabis Regulations also maintain a distinct system for access to cannabis. With the Cannabis Act now in force, cannabis has ceased to be regulated under the CDSA and is instead regulated under the Cannabis Act, and both the ACMPR and the IHR have been repealed effective October 17, 2018.

| 11 |

On June 7, 2018, Bill-C45 passed the third reading in the Senate with a number of amendments to the language of the Cannabis Act. More specifically, the Senate proposed:

| · | establishing a committee of the Senate and a committee of the House of Commons to undertake a comprehensive review of the administration and operation of the Cannabis Act; |

| · | assisting provinces and territories to facilitate the development of workplace impairment policies; |

| · | allowing provinces to place restrictions on the ability of individuals to engage in home cultivation; |

| · | that law enforcement be provided with the appropriate tools and resources to address concerns about continued illicit production, diversion, and sale of cannabis to youth, including preventing the sharing of marihuana among young adults by rendering it a ticketable offense; |

| · | that the prices set for cannabis products and the applicable taxes reflect the dual objective of minimizing the health dangers of cannabis consumption and undercutting the illicit market of cannabis; |

| · | mandatory health warnings for cannabis products, including warnings about the danger of smoking cannabis, the danger of exposure to second-hand cannabis smoke, and the risks of combining cannabis and tobacco; |

| · | testing procedures for THC content be standardized to ensure accurate measurement to better protect consumer health and safety; |

| · | that forthcoming regulations for edible products and other forms of cannabis ensure that product packaging is child-resistant and does not appeal to young people and that the type of available products should be strictly limited; |

| · | adequate and ongoing funding for sustained, evidence-based cannabis education and prevention programs to provide Canadians, especially young Canadians, with knowledge about the health risks of cannabis use, including on-going research initiatives on the impact of cannabis use on the developing brain; and that the federal government commit to on-going educational initiatives to ensure youth are informed on the effects of cannabis use; |

| · | to prohibit licensees under the Cannabis Act to distribute branded merchandise, such as T-shirts and baseball caps and imposing a moratorium on loosening the regulations on the branding, marketing, and promotion of cannabis for 10 years; |

| · | to set aggressive targets, comparable to the successful Federal Tobacco Control Strategy, to reduce the number of youth and adult cannabis users; and |

| · | to ensure that the Cannabis Tracking System be operational upon the coming-into-force of the Cannabis Act. |

Security Clearances

The Cannabis Regulations require that certain people associated with cannabis licensees, including individuals occupying a “key position” directors, officers, large shareholders and individuals identified by the Minister of Health, must hold a valid security clearance issued by the Minister of Health. Officers and directors of a parent corporation must be security cleared.

Under the Cannabis Regulations, the Minister of Health may refuse to grant security clearances to individuals with associations to organized crime or with past convictions for, or an association with, drug trafficking, corruption or violent offenses. Individuals who have histories of nonviolent, lower-risk criminal activity (for example, simple possession of cannabis, or small-scale cultivation of cannabis plants) are not precluded from participating in the legal cannabis industry, and the grant of security clearance to such individuals is at the discretion of the Minister of Health and such applications will be reviewed on a case-by-case basis.

Cannabis Tracking System

Under the Cannabis Act, the Minister of Health is authorized to establish and maintain a national cannabis tracking system. The Cannabis Regulations set out a national cannabis tracking system to track cannabis throughout the supply chain to help prevent diversion of cannabis into, and out of, the illicit market. The Cannabis Regulations also provides the Minister of Health with the authority to make a ministerial order that would require certain persons named in such order to report specific information about their authorized activities with cannabis, in the form and manner specified by the Minister of Health.

| 12 |

Cannabis Products

The Cannabis Regulations set out the requirements for the sale of cannabis products at the retail level permit the sale of dried cannabis, cannabis oil, fresh cannabis, cannabis plants, and cannabis seeds, including in such forms as “pre-rolled” and in capsules. The THC content and serving size of cannabis products is limited by the Cannabis Regulations. The sale of edibles containing cannabis and cannabis concentrates was not initially permitted, however, such products are expected to be legalized by the fall of 2019.

Description of Canadian Licenses and Licensing Requirements

Laws and regulations affecting the medical marijuana industry are constantly changing, which could detrimentally affect our proposed operations. Local, state and federal medical marijuana laws and regulations are broad in scope and subject to evolving interpretations, which could require us to incur substantial costs associated with compliance or alter our business plan. In addition, violations of these laws, or allegations of such violations, could disrupt our business and result in a material adverse effect on our operations. It is also possible that regulations may be enacted in the future that will be directly applicable to our business. These ever-changing regulations could even affect federal tax policies that may make it difficult to claim tax deductions on our returns. We cannot predict the nature of any future laws, regulations, interpretations or applications, nor can we determine what effect additional governmental regulations or administrative policies and procedures, when and if promulgated, could have on our business.

| Item 1A. | Risk Factors. |

We are a smaller reporting company and not required to include this disclosure in our Form 10-K annual report.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS. |

None.

| ITEM 2. | PROPERTIES. |

During our fiscal year ended December 31, 2017, Mr. Herick provided office space at his home at no cost to the Company.

On April 1, 2018 we changed our principal place of business to 2 Park Plaza, Suite 1200 – B. Irvine, CA. 92614, phone: 949-652-6838. This space is provided to us on a twelve-month term by a company to which Mr. Nicosia, one of our directors, serves as Chief Executive Officer. Our monthly rent is $1,000, however, as of the date of this filing, we have not made any rent payments and continue to accrue those amounts as accounts payable.

Effective in March 2019, we changed our principal place of business to Suite 206 1180 Sunset Drive, Kelowna, BC, Canada Z1Y 9W6, which we have rented pursuant to an oral sublease from PLC International Investments Inc, a company owned and controlled by Dominic Colvin, our current CEO, President and a director. This location consists of approximately 500 sq. feet. We pay a monthly rent of $1500 (CAD). We believe this location will be sufficient for our current business purposes.

| 13 |

| ITEM 3. | LEGAL PROCEEDINGS. |

As part of our acquisition of AMS we assumed an action filed against AMS by Ataraxia Canada, Inc., alleging breach of contract, specifically, breach of a nonbinding term sheet providing for Ataraxia to acquire controlling interest in AMS and they are seeking $15 million in damages. A Statement of Claim was prepared by Ataraxia Canada, Inc., as plaintiff, and circulated to Alternative Medical Solutions Inc., as defendant, on August 2, 2017 under the Ontario Superior Court of Justice (Court file no. CV-17-580157). The pleadings have closed and the parties are now expected to schedule examinations for discovery. Counsel has advised that it believes it is premature to speculate on any outcome of this litigation, including the likelihood of success or potential liability at this time.

Our agreement to acquire AMS contained a provision requiring us to diligently defend against the claims brought forth in, and assume full and complete control of, the Ataraxia litigation, provided that we shall not enter into any compromise or settlement in respect of the Ataraxia litigation without the prior written consent of the sellers, which consent is not to be unreasonably withheld, conditioned or delayed. The sellers are obligated to cooperate fully and make available to us all pertinent information and witnesses under their control, make such assignments and take such other steps as in the opinion of our counsel are reasonably necessary to enable us to defend against the claims brought forth in the Ataraxia litigation.

In the event we are not successful in defending this action, the AMS Agreement also provides that the Purchase Price (and the amount owing under the Purchaser Notes) we paid for AMS shall be reduced by an amount equal to any judgment or order awarded against (and payable by) and all costs and expenses incurred by us in defending the Ataraxia litigation including, without limitation, all legal and other professional fees and any and all costs and expenses of any appeal of any judgment or order.

In addition, we had previously been party to an action filed by Gary M. Cohen, a former officer and director of our Company in 2014. In March 2015, we entered into a Settlement Agreement with Mr. Cohen wherein we agreed to repurchase 2,250,000 shares of our Common Stock from Mr. Cohen in consideration for $350,000. Mr. Cohen passed away while there was a remaining balance of $190,000 remaining to be paid in accordance with the Settlement Agreement. We have taken the position that his death has discharged any obligation we might have to make the balance of the payments. We have not received any demand for payment or otherwise been involved in any attempt to collect this balance as of the date of this report.

We are not a party to any other legal proceeding or aware of any other threatened action as of the date of this report.

| ITEM 4. | MINE SAFETY DISCLOSURES. |

Not Applicable.

| 14 |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Market Information

Our Common Stock is quoted on the over the counter “pink sheets” under the trading symbol “CPMD.” Trading volume in our Common Stock is very limited. As a result, the trading price of our Common Stock is subject to significant fluctuations.

There can be no assurance that a liquid market will develop in the foreseeable future.

Transfer of our common stock may also be restricted under the securities or blue sky laws of certain states and foreign jurisdictions. Consequently, investors may not be able to liquidate their investments and should be prepared to hold the common stock for an indefinite period of time.

The following table sets forth the high and low bid quotations for our Common Stock as reported on the pink sheets for the periods indicated.

| High | Low | |||||||

| Fiscal 2018 | $ | $ | ||||||

| First Quarter | $ | 2.01 | $ | 0.51 | ||||

| Second Quarter | 1.65 | 0.55 | ||||||

| Third Quarter | 2.55 | 0.51 | ||||||

| Fourth Quarter | 4.00 | 1.20 | ||||||

| Fiscal 2017 | ||||||||

| First Quarter | 1.00 | 0.40 | ||||||

| Second Quarter | 0.60 | 0.35 | ||||||

| Third Quarter | 0.39 | 0.15 | ||||||

| Fourth Quarter | 0.55 | 0.15 | ||||||

As of March 29, 2019, the closing price of our Common Stock was. $1.65 per share.

The Securities Enforcement and Penny Stock Reform Act of 1990

The Securities and Exchange Commission has also adopted rules that regulate broker-dealer practices in connection with transactions in penny stocks. Penny stocks are generally equity securities with a price of less than $5.00 (other than securities registered on certain national securities exchanges or quoted on the NASDAQ system, provided that current price and volume information with respect to transactions in such securities is provided by the exchange or system).

As of the date of this Report, our Common Stock is defined as a “penny stock” under the Securities and Exchange Act. It is anticipated that our Common Stock will remain a penny stock for the foreseeable future. The classification of penny stock makes it more difficult for a broker-dealer to sell the stock into a secondary market, which makes it more difficult for a purchaser to liquidate his/her investment. Any broker-dealer engaged by the purchaser for the purpose of selling his or her shares in us will be subject to Rules 15g-1 through 15g-10 of the Securities and Exchange Act. Rather than creating a need to comply with those rules, some broker-dealers will refuse to attempt to sell penny stock.

| 15 |

The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from those rules, to deliver a standardized risk disclosure document prepared by the Commission, which:

| · | contains a description of the nature and level of risk in the market for penny stocks in both public offerings and secondary trading; |

| · | contains a description of the broker's or dealer's duties to the customer and of the rights and remedies available to the customer with respect to a violation to such duties or other requirements of the Securities Act of 1934, as amended; |

| · | contains a brief, clear, narrative description of a dealer market, including "bid" and "ask" prices for penny stocks and the significance of the spread between the bid and ask price; |

| · | contains a toll-free telephone number for inquiries on disciplinary actions; |

| · | defines significant terms in the disclosure document or in the conduct of trading penny stocks; and |

| · | contains such other information and is in such form (including language, type, size, and format) as the Securities and Exchange Commission shall require by rule or regulation. |

The broker-dealer also must provide, prior to effecting any transaction in a penny stock, to the customer:

| · | the bid and offer quotations for the penny stock; |

| · | the compensation of the broker-dealer and its salesperson in the transaction; |

| · | the number of shares to which such bid and ask prices apply, or other comparable information relating to the depth and liquidity of the market for such stock; and |

| · | monthly account statements showing the market value of each penny stock held in the customer's account. |

In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from those rules; the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written acknowledgment of the receipt of a risk disclosure statement, a written agreement to transactions involving penny stocks, and a signed and dated copy of a written suitability statement. These disclosure requirements will have the effect of reducing the trading activity in the secondary market for our stock because it will be subject to these penny stock rules. Therefore, stockholders may have difficulty selling their securities.

Holders

As of December 31, 2018, there were 18,942,506 shares of our common stock issued and outstanding, which were held by 212 stockholders of record, not including those persons holding shares in “street name.” As of the date of this Report, there were 26,798,371 Common Shares issued and outstanding, held by 214 holders of record, not including those persons holding shares in “street name.”

| 16 |

In April 2018 we issued 60,000 shares of our Series A Convertible Preferred Stock at a price of $1.00 per share to two persons who subsequently became our management team. Each share of Series A Convertible Preferred Stock is convertible into 1,250 shares of common stock and vote on an as-converted basis. The rights and designations of these Preferred Shares include the following:

| · | entitles the holder thereof to 1,250 votes on all matters submitted to a vote of the shareholders; | |

| · | The holders of outstanding Series A Convertible Preferred Stock shall only be entitled to receive dividends upon declaration by the Board of Directors of a dividend payable on our Common Stock whereupon the holders of the Series A Convertible Preferred Stock shall receive a dividend on the number of shares of Common Stock in to which each share of Series A Convertible Preferred Stock is convertible; | |

| · | Each Series A Preferred Share is convertible into 1,250 shares of Common Stock; and | |

| · | is not redeemable. |

Stock Transfer Agent

Our stock transfer agent for our securities is Mountain Share Transfer, Inc., 2030 Powers Ferry Road SE, Suite 212, Atlanta, GA 30339. Their telephone number is (303) 460-1149.

Dividends

We have never declared or paid any cash dividends on our common stock. We currently intend to retain future earnings, if any, to finance the expansion of our business. As a result, we do not anticipate paying any cash dividends in the foreseeable future.

Reports

We are subject to certain reporting requirements and furnish annual financial reports to our stockholders, certified by our independent accountants, and furnish unaudited quarterly financial reports in our quarterly reports filed electronically with the SEC. All reports and information filed by us can be found at the SEC website, www.sec.gov.

| Item 6. | Selected Financial Data. |

As a smaller reporting company, we are not required to provide this information.

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations. |

The following discussion should be read in conjunction with our audited financial statements and notes thereto included herein. In connection with, and because we desire to take advantage of, the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, we caution readers regarding certain forward-looking statements in the following discussion and elsewhere in this Report and in any other statement made by, or on our behalf, whether or not in future filings with the Securities and Exchange Commission. Forward-looking statements are statements not based on historical information and which relate to future operations, strategies, financial results or other developments. Forward-looking statements are necessarily based upon estimates and assumptions that are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond our control and many of which, with respect to future business decisions, are subject to change. These uncertainties and contingencies can affect actual results and could cause actual results to differ materially from those expressed in any forward-looking statements made by, or on our behalf. We disclaim any obligation to update forward-looking statements.

| 17 |

Overview and History

We were originally incorporated in the State of Colorado in August 1998 under the name “Network Acquisitions, Inc.” We changed our name to Cavion Technologies, Inc. in February 1999 and subsequently to Concord Ventures, Inc. in October 2006.

On December 21, 2000, we filed for protection under Chapter 11 of the United States Bankruptcy Code. In connection with the filing, on February 16, 2001, we sold our entire business, and all of our assets, for the benefit of our creditors. After the sale, we still had liabilities of $8.4 million and were subsequently dismissed by the Court from the Chapter 11 reorganization, effective March 13, 2001, at which time the last of our remaining directors resigned. On March 13, 2001, we had no business or other source of income, no assets, no employees or directors, outstanding liabilities of approximately $8.4 million and had terminated our duty to file reports under securities law. In February 2008, we were re-listed on the OTC Bulletin Board.

In April 2010, we re-domiciled in Delaware under the name CCVG, Inc. (“CCVG”). Effective December 31, 2010, CCVG completed an Agreement and Plan of Merger and Reorganization (the “Reorganization") which provided for the merger of two of our wholly-owned subsidiaries. As a result of this reorganization, our name was changed to “Golden Dragon Inc.”, which became the surviving publicly quoted parent holding company.

On May 9, 2014, we entered into a Share Purchase Agreement (the “Share Purchase Agreement”) with CannaPharmaRX, Inc., a Colorado corporation (“Canna Colorado”), and David Cutler, a former President, Chief Executive Officer, Chief Financial Officer and director of our Company. Under the Share Purchase Agreement, Canna Colorado purchased 1,421,120 shares of our common stock from Mr. Cutler and an additional 9,000,000 restricted common shares directly from us.

On May 15, 2014, as amended and effective January 29, 2015, we entered into an Agreement and Plan of Merger (the “Merger”) pursuant to which Canna Colorado became a subsidiary of our Company. In October 2014, we changed our legal name to “CannaPharmaRx, Inc.”

Pursuant to the Merger, all of the shares of our common stock previously owned by Canna Colorado were canceled. As a result of the aforesaid transactions, we became an early-stage pharmaceutical company whose purpose was to advance cannabinoid research and discovery using proprietary formulation and drug delivery technology then under development.

In April 2016, we ceased operations. Our then management resigned their respective positions with our Company, with the exception of Mr. Gary Herick, who remained as one of our officers and directors until March 2019.

As a result, we are currently classified as a “shell” company as defined by Rule 12b-2 under the Securities Exchange Act of 1934, as amended. Relevant thereto, in February 2019 we filed a report on Form 8-K/A advising that we had taken all steps necessary and disclosed all required information with the SEC so as to allow us to no longer be considered a “shell” company effective February 13, 2020.

Our principal place of business is located at Suite 206, 1180 Sunset Drive, Kelowna, BC, Canada Z1Y 9W6, phone 949-652-6838. Our website address is www.cannapharmarx.com.

Because we have not generated any revenues during our prior two years, the following is our Plan of Operation.

PLAN OF OPERATION

See “Part 1, Item 1, Business,” above for a detailed discussion of our current business activities and plan of operation, the contents of which are incorporated herein as if set forth.

| 18 |

LIQUIDITY AND CAPITAL RESOURCES

As of December 31, 2018, we had $464,118 in cash.

In April 2018, we issued 60,000 shares of our Series A Convertible Preferred Stock at a price of $1.00 per share to our current management. Each share of Series A Convertible Preferred Stock is convertible into 1,250 shares of common stock and vote on an as-converted basis. The rights and designations of these Preferred Shares include the following:

| · | entitles the holder thereof to 1,250 votes on all matters submitted to a vote of the shareholders; |

| · | The holders of outstanding Series A Convertible Preferred Stock shall only be entitled to receive dividends upon declaration by the Board of Directors of a dividend payable on our Common Stock whereupon the holders of the Series A Convertible Preferred Stock shall receive a dividend on the number of shares of Common Stock in to which each share of Series A Convertible Preferred Stock is convertible; |

| · | Each Series A Preferred Share is convertible into 1,250 shares of Common Stock; and |

| · | not redeemable. |

During 2018 we conducted a private offering of 12% Convertible Debentures where we accepted subscriptions in the aggregate amount of $2,072,000 from 35 accredited investors, as that term is defined in Rule 501 of Regulation D. Each Convertible Debenture is convertible into shares of our common stock at the lesser of $0.40 or a 50% of the closing market price on the date a business combination valued at greater than $5,000,000 is completed. We relied upon the exemption from registration provided by Rule 506 of Regulation D to issue the Convertible Debentures. We used the proceeds from this offering for the purchase of AMS, as well as working capital, including costs associated with the preparation of over three years of reports that had not been filed with the SEC.

We estimate that in order to consummate the acquisition of Great Northern, as well as to complete development of the cultivation facilities, we will require up to $20 million (CAD) in additional financing, which we will seek to raise via equity and debt. While there can be no assurances that we will successfully raise the financing required to complete construction of the facility and begin cultivation, we have had several initial discussions with funding sources and while no assurances can be provided, we believe we will be able to obtain such financing. We cannot provide any assurances that we will be able to raise such funds or whether we would be able to raise such funds on terms that are favorable to us. We may seek to borrow monies from lenders at commercial rates, but such lenders will probably be at higher than bank rates, which higher rates could depend on the amount borrowed, render the net operating income of any of our planned profitable businesses insufficient to cover the interest burden.

Currently, we have no committed source for any funds as of the date hereof. No representation is made that any funds will be available when needed. In the event funds cannot be raised if and when needed, we may not be able to carry out our business plan and could fail in business as a result of these uncertainties.

Subsequent Event

In February 2019, we commenced an offering of up to $3 million in principal amount of Units at a price of $1.00 per Unit, each Unit consisting of one share of Series “B” Convertible Preferred Stock, each Convertible Preferred Share convertible into one share of the Company’s Common Stock at the election of the holder and one Common Stock Purchase Warrant exercisable to purchase one share of Common Stock at an exercise price of $2.00 per share, which offering is to be offered only to “accredited investors,” as that term is defined in Rule 501 of Regulation D. As of the date of this report, we have accepted $169,000 in subscriptions in this offering.

| 19 |

Inflation

Although our operations are influenced by general economic conditions, we do not believe that inflation had a material effect on our results of operations during the year ended December 31, 2018.

Critical Accounting Policies and Estimates

Critical Accounting Estimates

Our financial statements and accompanying notes have been prepared in accordance with U.S. GAAP. The preparation of these financial statements requires management to make estimates, judgments, and assumptions that affect reported amounts of assets, liabilities, revenues and expenses. We continually evaluate the accounting policies and estimates used to prepare the financial statements. The estimates are based on historical experience and assumptions believed to be reasonable under current facts and circumstances. Actual amounts and results could differ from these estimates made by management.

RECENTLY ISSUED ACCOUNTING PRONOUNCEMENTS

Management has reviewed all other recently issued, but not yet effective, accounting pronouncements and do not believe the future adoption of any such pronouncements may be expected to cause a material impact on our financial condition or the results of our operations.

Off-Balance Sheet Arrangements

We have not entered into any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources and would be considered material to investors.

| Item 7a. | Quantitative And Qualitative Disclosures About Market Risk |

As a smaller reporting company, we are not required to provide this information.

| Item 8. | Financial Statements And Supplementary Data |

The financial statements and supplementary financial information required by this Item are set forth immediately following the signature page and are incorporated herein by reference.

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. |

On June 11, 2018, we engaged BF Borgers CPA PC as our independent registered public accounting firm, and effective June 11, 2018, we dismissed KLJ & Associates, LLP (“KLJ”), as our independent registered public accounting firm. The decision to dismiss KLJ and to appoint BF Borgers CPA PC was approved by our board of directors. No audit or audit-related services were performed between us and Borgers prior to their appointment.

| 20 |

KLJ’s report on our financial statements for either of the two fiscal years ended December 31, 2014 and 2013 did not contain an adverse opinion or disclaimer of opinion, or qualification or modification as to uncertainty, audit scope, or accounting principles, except that such report on our financial statements contained an explanatory paragraph in respect to the substantial doubt about our ability to continue as a going concern.

During the two fiscal years ended December 31, 2014 and 2013 and in the subsequent interim period through the date of dismissal, there were no disagreements, resolved or not, with KLJ on any matter of accounting principles or practices, financial statement disclosure, or audit scope and procedures, which disagreement(s), if not resolved to the satisfaction of KLJ, would have caused KLJ to make reference to the subject matter of the disagreement(s) in connection with its report. During the two fiscal years ended December 31, 2014 and 2013 and in the subsequent interim period through the date of dismissal, there were no reportable events as described in Item 304(a)(1)(v) of Regulation S-K.

The audit report of KLJ on our financial statements as of and for the years ended December 31, 2014 and 2013 did not contain an adverse opinion or disclaimer of opinion, nor was it qualified or modified as to uncertainty, audit scope, or accounting principles, except relevant to the audit reports for the years ended December 31, 2014 and 2013, which stated as follows:

“The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the financial statements, the Company has suffered net losses and has had negative cash flows from operating activities during the years ended December 31, 2014 and 2013. These matters raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans concerning these matters are also described in Note 2. The financial statements do not include any adjustments to the recoverability and classification of asset carrying amounts or the amount and classification of liabilities that might result should the Company be unable to continue as a going concern.”

| ITEM 9A. | CONTROLS AND PROCEDURES. |

Disclosure Controls and Procedures

Disclosure Controls and Procedures–Our management, with the participation of our Chief Executive Officer and Chief Financial Officer, has evaluated the effectiveness of our disclosure controls and procedures (as such term is defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) as of the end of the period covered by this Report.

These controls are designed to ensure that information required to be disclosed in the reports we file or submit pursuant to the Securities Exchange Act of 1934 is recorded, processed, summarized and reported within the time periods specified in the rules and forms of the Securities and Exchange Commission, and that such information is accumulated and communicated to our management, including our CEO/CFO to allow timely decisions regarding required disclosure.

Based on this evaluation, our CEO and CFO have concluded that our disclosure controls and procedures were effective as of December 31, 2018, at reasonable assurance levels.

We believe that our financial statements presented in this annual report on Form 10-K fairly present, in all material respects, our financial position, results of operations, and cash flows for all periods presented herein.

| 21 |

Inherent Limitations – Our management, including our Chief Executive Officer and Chief Financial Officer, does not expect that our disclosure controls and procedures will prevent all error and all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. The design of any system of controls is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within our company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdown can occur because of simple error or mistake. In particular, many of our current processes rely upon manual reviews and processes to ensure that neither human error nor system weakness has resulted in erroneous reporting of financial data.

Changes in Internal Control over Financial Reporting – There were no changes in our internal control over financial reporting during our fiscal year ended December 31, 2018, which were identified in conjunction with management’s evaluation required by paragraph (d) of Rules 13a-15 and 15d-15 under the Exchange Act, that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

This Annual Report does not include an attestation report of our registered public accounting firm regarding internal control over financial reporting. Management’s report was not subject to attestation by our registered public accounting firm pursuant to temporary rules of the Securities and Exchange Commission that permit us to provide only management’s report in this Annual Report.

Management Report on Internal Control over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting as defined in Rule 13a-15(f) or 15d-15(f) promulgated under the Exchange Act. Those rules define internal control over financial reporting as a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles and includes those policies and procedures that:

| · | Pertain to the maintenance of records that in reasonable detail accurately and fairly reflect the transactions and dispositions of the assets of the Company; | |

| · | Provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and the receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the Company; and | |

| · | Provide reasonable assurance regarding prevention or timely detection of unauthorized acquisitions, use or disposition of the company’s assets that could have a material effect on the financial statements. |

Because of its inherent limitations, internal controls over financial reporting may not prevent or detect misstatements. Projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.