Exhibit 99.1 – Annual Information Form

GOLD RESERVE INC.

ANNUAL INFORMATION FORM

For The Year Ended December 31, 2016

As filed on April 28, 2017

Exhibit 99.1 Annual Information Form - Page 1

TABLE OF CONTENTS

Cautionary Statement Regarding Forward-Looking Statements and Information...7.

General Development and Description of the Business...8.

Dividends and Distributions...20.

Description of Capital Structure...21.

Escrowed Securities and Securities Subject to Contractual Restriction on Transfer...22

Audit Committee Information...26.

Legal Proceedings and Regulatory Actions...28.

Interest of Managament and Others in Material Transactions...28.

Transfer Agents and Registrars...28.

Exhibit 99.1 Annual Information Form - Page 2

Introductory Notes

In this Annual Information Form, the terms "Gold Reserve", the "Company" "we," "us," or "our," refer to Gold Reserve Inc. and its consolidated subsidiaries and affiliates, unless the context requires otherwise. When appropriate, capitalized terms are defined herein.

Gold Reserve, an exploration stage company, is engaged in the business of acquiring, exploring and developing mining projects. We were incorporated in 1998 under the laws of the Yukon Territory, Canada and continued to Alberta, Canada in September 2014. We are the successor issuer to Gold Reserve Corporation which was incorporated in 1956. We have only one operating segment, the exploration and development of mineral properties.

In February 1999, each Gold Reserve Corporation shareholder exchanged their shares for an equal number of Gold Reserve Inc. Class A common shares except in the case of certain U.S. holders who for tax reasons elected to receive equity units (each an "Equity Unit") in lieu of Gold Reserve Inc. Class A common shares. Each Equity Unit comprises one Gold Reserve Inc. Class B common share and one Gold Reserve Corporation Class B common share and is substantially equivalent to a Class A common share. At December 31, 2015, all Equity Units had been converted to Class A common shares.

Our recent activities, as more fully described herein, have included:

SETTLEMENT AGREEMENT

§ The signing of a Memorandum of Understanding (the "MOU") in February 2016, with the Bolivarian Republic of Venezuela ("Venezuela") represented by the Office of the Attorney General and the Ministry of Popular Power of Oil and Mining that contemplated settlement, including payment and resolution, of the International Centre for the Settlement of Investment Disputes ("ICSID") arbitral award (the "Award") granted in our favor by ICSID in respect of the Brisas Project and the transfer of our technical mining data related to the Brisas Project (the "Mining Data"). Efforts to come to an agreement with Venezuela commenced in October 2015 and in the spirit of that effort, the parties subsequently agreed to extend the MOU to allow for further efforts to agree on a formal settlement agreement;

§ The execution of a Settlement Agreement (as defined herein) in July 2016 with Venezuela which provided for payment of the Award (including accrued interest) in the amount of approximately $770 million in respect of the Brisas project and the acquisition by Venezuela of the Mining Data for $240 million. The Company agreed to temporarily suspend the legal enforcement of the Award until final payment is made by Venezuela, at which time we would permanently cease all legal activities related to the collection of the Award;

§ The execution of addendums to the Settlement Agreement in early November and again in early December 2016 whereby the parties agreed to revise the payment schedule. The payments for the Award and Mining Data continue to be contingent upon Venezuela obtaining the necessary financing, which has not occurred and, as a result, as of the date of this report no payments have been made by Venezuela. At the passing of the last agreed upon payment date, the board of directors chose to not formally terminate the Settlement Agreement as a result of the delay in the initial agreed upon payment(s), but instead instructed management to continue all efforts to work with Venezuela to complete the terms of the Settlement Agreement. Management has recently proposed and Venezuela is currently considering a third addendum to the Settlement Agreement, whereby the parties would agree, among other things, to revise the previously proposed payment schedule.

MIXED COMPANY AGREEMENT

· The parties agreed, during the first half of 2016, following extensive negotiations over a number of months with Venezuelan authorities, to significant terms, including economic conditions and various decrees and resolutions impacting the entity envisioned to develop the Brisas and the adjacent Cristinas gold-copper project (the "Brisas Cristinas Project"). Concurrent with those activities, we developed a business plan (the "Business Plan") for the Brisas Cristinas Project with broad input from our engineering consultants. Thereafter, we met with and reviewed the Business Plan with representatives of Venezuela. These discussions were key to our joint agreement to revise royalty and income tax rates related to the Brisas Cristinas Project resulting in the parties concluding initial formation negotiations, moving on to the negotiation of the various terms of the articles of incorporation and by-laws of the Mixed Company;

· The Company and Venezuela entered into an agreement ("Mixed Company Agreement") on August 7, 2016 for the formation of a jointly owned company ("Mixed Company") to develop the Brisas Cristinas Project;

Exhibit 99.1 Annual Information Form - Page 3

· In anticipation of the Mixed Company Agreement, GR Mining (Barbados) Inc. ("GR Mining") a wholly-owned subsidiary of Gold Reserve Inc. and GR Engineering (Barbados) Inc. ("GR Engineering"), a wholly-owned subsidiary of GR Mining were formed in early 2016. GR Mining was formed to hold our interest in Empresa Mixta Ecosocialista Siembra Minera, S.A. ("Siembra Minera"), the Venezuelan company formed to act as the Mixed Company and provide for the management of the development and operation of the Brisas Cristinas Project and GR Engineering was formed to provide technical services to Siembra Minera;

· Venezuela has granted the following decrees which have been published in the Official Gazette: The formation, in October 2016, of Siembra Minera, the entity that will develop the Brisas Cristinas Project, Delimitation of the Area, Transferring the Gold Rights, Transferring the Strategic Mineral Rights (including copper and silver). Venezuela has also committed to issuing the following decrees, resolutions and exchange agreement on or prior to the effective date of the new addendum of the Settlement Agreement: the BCV (Central Bank of Venezuela) Resolution to export doré and concentrate and sell product to other than the BCV and keep funds offshore; the Incentives Regime; the Special Tax Regime Decree; the Ministry Resolution in accordance with Article 16 of the Organic Gold Law; and the Exchange Agreement;

· The significant negotiated terms related to the formation of Siembra Minera and its development and operation of the Brisas Cristinas Project include:

· Siembra Minera is beneficially owned 55% by Corporacion Venezolano Minera (a Venezuelan government corporation) and 45% by GR Mining;

· Siembra Minera holds the rights to the gold, copper, silver and other strategic minerals contained within a 18,950 hectare area located in southeast Bolivar State which includes the Brisas Cristinas Project;

· GR Engineering, under a Technical Services Agreement, will provide engineering, procurement and construction services to Siembra Minera for a fee of 5% over all costs of construction and development and, thereafter, for a fee of 5% over operating costs during operations;

· Presidential Decrees, within the legal framework of the "Orinoco Mining Arc", have been, or will be issued to provide for tax and fiscal incentives for mixed companies operating in that area that include exemption from value added tax, stamp tax, municipal taxes and any taxes arising from the contribution of tangible or intangible assets, if any, to the mixed companies by the parties and the same cost of electricity, diesel and gasoline as that incurred by the government or related entities;

· Gold price participation, in accordance with an agreed upon formula resulting in specified respective percentages based on the sales price of gold per ounce. For sales up to $1600 per ounce, net profits will be allocated 55% to Venezuela and 45% to us. For sales greater than $1600 per ounce, the incremental amount will be allocated 70% to Venezuela and 30% to us. For example, with sales at $1600 and $3500 per ounce, net profits will be allocated 55.0% ̶ 45.0% and 60.5% ̶ 39.5%, respectively;

· Net smelter return royalty (“NSR”) to Venezuela on the sale of gold, copper, silver and any other strategic minerals of 5% for the first ten years of commercial production, 6% for the next ten years;

· Income tax rate of 14% for years one to five, 19% for years 6 to 10, 24% for years 11 to 15, 29% for years 16 to 20 and 34% thereafter;

· The Parties agreed to work together to complete financing(s) to jointly fund the contemplated $2.1 billion anticipated capital costs of the Brisas Cristinas project on behalf of Siembra Minera, which is expected to be comprised of a combination of project financing, development agencies, equipment manufacturer, offtake and smelter financings. In order to facilitate the early startup of the pre-operation and construction activities, Venezuela agreed to advance $110.2 million to Siembra Minera, which will be repaid from the financing proceeds;

· Maintenance of funds associated with future capital cost financings in offshore US dollar accounts;

Exhibit 99.1 Annual Information Form - Page 4

· Authorization to export and sell concentrate and doré containing gold, copper, silver and other strategic minerals outside of Venezuela and maintain proceeds from such sales in a US dollar account. In addition, dividends and profit distributions, if any, will be directly paid to the shareholders;

· Funds to pay, as required, Venezuela income taxes and local annual operating and capital costs denominated in Bolivars for the Brisas Cristinas Project will be converted into local currency at the most favorable exchange rate offered by Venezuela to other entities;

· Venezuela agrees to use its best efforts to grant to Siembra Minera similar terms that would apply to the Brisas Cristinas Project in the event Venezuela enters into an agreement with a third party for the incorporation of a mixed company to perform similar activities with terms and conditions that are more favorable than the above tax and fiscal incentives;

· Venezuela will indemnify us and our affiliates against any future legal actions associated with the Brisas Cristinas Project; and

· The board of directors will be comprised of seven individuals, of which four will be appointed by Venezuela and three by us.

The primary activities of Siembra Minera since its formation has included:

§ Establishment of bank accounts in both offshore US$ accounts and Venezuelan Bolivars. Identification of external auditors which will be formally designated during upcoming board meetings. Engagement of certain key employees with additional initial interviews has been completed or is in process. Potential office locations in Caracas and Puerto Ordaz have been identified;

§ Initiated discussions whereby the parties are working on a draft Engineering Procurement Construction Management (“EPCM”) contract between GR Engineering and Siembra Minera;

§ Conducted preliminary meetings with CAMIMPEG, a Venezuelan Army construction company, to provide project information regarding the early works plan which includes man-camp and certain access roads;

§ Provided CVG-Tecmin, a state corporation that provides technical services and information with regard to the development of mineral resources, with the project description and related technical information to produce and file the Environmental Questionnaire leading to the granting of the Authorization to Occupy the Territory (AOT);

§ Sponsored several meetings with Mission Piar to initiate surveys and follow up on the activities of small miners groups currently working in certain parts of the 18,950 hectare property. Mission Piar is a Government instituted Mission under the authority of the Ministry of Mines in charge of providing assistance and coordination of small mining activities;

§ Held fact finding meetings with the Ministry of Mines and members of the Guayana REDI to provide inputs and assist in the establishment of a General Plan of Security for the Project Area. The security of the project area falls under the responsibility of the Region of Integral Defense Guayana (REDI) lead by General Carlos Augusto Leal Tellería;

§ Initiated efforts to define the Relocation Plan with the help of Venezuelan officials and REDI and supported by a census that is underway by Mission Piar. Several meetings have taken place between the Ministry of Mines and small miners as part of the relocation plan;

§ Initiated development of a Small Miner Project with input from entities such as Ministry of Mines, REDI, Mission Piar and others to provide alternatives to some of the small miners that currently operate in the project area. This project is intimately linked to the Relocation Plan and includes an Early Production Plan, training of miners in environmental protection and remediation, and in other disciplines so many of them can be incorporated in the project construction and operation; and

Exhibit 99.1 Annual Information Form - Page 5

§ Requested a High Definition Multispectral Satellite image of the Brisas Cristinas Project land position and its adjacent area at the end of 2016, which will be used to document existing conditions and as an aid for documenting and census of existing small miner activity. Completion will take several months due to multiple satellite passes to meet cloud cover requirement.

PRIVATE PLACEMENT

§ Completed a non-brokered private placement in May 2016 for the issuance of 8,562,500 Class A common shares at $4.00 per share for gross proceeds of $34.3 million.

AWARD ENFORCEMENT

§ Due to the rejection on February 7, 2017 by the Paris Court of Appeal of Venezuela’s annulment arguments and the issuance of a judgment dismissing the applications filed by Venezuela pending before the French courts in relation to the Award, we initiated service to accelerate Venezuela’s appeal before the French Cour de cassation, which is the court of final resort in the French judicial system. Regardless of whether Venezuela files an appeal to the Cour de cassation, the exequatur previously achieved by us remains in full force and effect; and

§ Continued legal efforts in the United States and Luxembourg to posture the Company for potential future legal activities related to enforcement of the Award in the event payment under Settlement Agreement is not received.

OTHER

§ Continued to pursue the sale of Brisas Project equipment; and

§ Pursued activities related to the LMS property in Alaska.

We have no commercial production and, as a result, we continue to experience losses from operations, a trend we expect to continue unless we collect, in part or whole, the Award and/or acquire and develop a mineral project which results in positive results from operations.

Historically we have financed our operations through the issuance of common stock, other equity securities and debt. Funds necessary for on-going corporate activities to pursue the collection of the Award, future investments and/or transactions if any, cannot be precisely determined at this time and are subject to available cash, proceeds related to the sale of remaining Brisas Project equipment, future financings and cash received from the collection of the Award, if any.

We currently employ eight individuals. Our Class A common shares are listed for trading on the TSX Venture Exchange (the "TSXV") and the OTC under the symbol "GRZ.V" and "GDRZF", respectively.

Our registered office is located at the office of Norton Rose Fulbright Canada LLP, 400 3rd Avenue SW, Suite 3700, Calgary, Alberta T2P 4H2, Canada. Telephone and fax numbers for our registered agent are 403.267.8222 and 403.264.5973, respectively. Our administrative office is located at 926 West Sprague Avenue, Suite 200, Spokane, WA 99201, U.S.A. and our telephone and fax numbers are 509.623.1500 and 509.623.1634, respectively.

We maintain our accounts in U.S. dollars and prepare our financial statements in accordance with accounting principles generally accepted in the United States. Our audited consolidated financial statements as at December 31, 2016 and 2015 and for the years ended December 31, 2016 and 2015 are available for review under our profiles at www.sedar.com and www.sec.gov. All information in this Annual Information Form is as of April 28, 2017, unless otherwise noted.

Exhibit 99.1 Annual Information Form - Page 6

Currency

Unless otherwise indicated, all references to "$", “U.S. $” or "U.S. dollars" in this Annual Information Form refer to U.S. dollars and references to "Cdn$" or "Canadian dollars" refer to Canadian dollars. The 12 month average rate of exchange for one Canadian dollar, expressed in U.S. dollars, for each of the last two calendar years equaled 0.7544 and 0.7820, respectively, and the exchange rate at the end of each such period equaled 0.7448 and 0.7226, respectively.

Cautionary Statement Regarding Forward-Looking Statements and Information

The information presented or incorporated by reference in this report contains both historical information and "forward-looking statements" (within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act) or "forward looking information" (within the meaning of applicable Canadian securities laws) (collectively referred to herein as "forward looking statements") that may state our intentions, hopes, beliefs, expectations or predictions for the future.

Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by us at this time, are inherently subject to significant business, economic and competitive uncertainties and contingencies that may cause our actual financial results, performance or achievements to be materially different from those expressed or implied herein and many of which are outside our control.

Forward-looking statements involve risks and uncertainties, as well as assumptions, including those set out herein, that may never materialize, prove incorrect or materialize other than as currently contemplated which could cause our results to differ materially from those expressed or implied by such forward-looking statements. The words "believe," "anticipate," "expect," "intend," "estimate," "plan," "may," "could" and other similar expressions that are predictions of or indicate future events and future trends, which do not relate to historical matters, identify forward-looking statements. Any such forward-looking statements are not intended to provide any assurances as to future results.

Numerous factors could cause actual results to differ materially from those described in the forward-looking statements, including, without limitation:

· delay or failure by Venezuela to make payments or otherwise honor its commitments under the Settlement Agreement, including with respect to the sale of the Mining Data;

· the ability of the Company and Venezuela to (i) successfully overcome any legal, regulatory or technical obstacles to operate the Mixed Company and develop the Brisas Cristinas Project (as herein defined), (ii) obtain any remaining governmental approvals and (iii) obtain financing to fund the capital costs of the Brisas Cristinas Project;

· risks associated with exploration, delineation of adequate resources and reserves, regulatory and permitting obstacles and other risks normally incident to the exploration, development and operation of mining properties including our ability to achieve revenue producing operations in the future;

· local risks associated with the concentration of our future operations and assets in Venezuela, including operational, security, regulatory, political and economic risks;

· our ability to resume our efforts to enforce and collect the Award, including the associated costs of such enforcement and collection effort and the timing and success of that effort, if Venezuela fails to make payments under the Settlement Agreement, it is terminated and further efforts to consummate the Settlement Agreement are abandoned;

· pending the receipt of payments under the Settlement Agreement or otherwise, our continued ability to service or restructure our outstanding notes or other obligations as they come due and access future additional funding, when required, for ongoing liquidity and capital resources;

· shareholder dilution resulting from future restructuring, refinancing and/or conversion of our outstanding notes or from the sale of additional equity, if required;

· value realized from the disposition of the remaining Brisas Project related assets, if any;

· our prospects in general for the identification, exploration and development of additional mining projects;

· risks associated with the abilities and continued participation of key employees; and

Exhibit 99.1 Annual Information Form - Page 7

· Changes in U.S. and/or Canadian tax laws to which we are subject.

This list is not exhaustive of the factors that may affect any of our forward-looking statements. See the section entitled "Risk Factors" in our Management's Discussion and Analysis ("MD&A") for the fiscal year ended December 31, 2016 which is incorporated by reference herein. The MD&A has been filed on SEDAR and can be viewed at www.sedar.com.

Investors are cautioned not to put undue reliance on forward-looking statements, and investors should not infer that there has been no change in our affairs since the date of this report that would warrant any modification of any forward-looking statement made in this document, other documents periodically filed with the SEC or other securities regulators or presented on the Company’s website. Forward-looking statements speak only as of the date made. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by this notice. We disclaim any intent or obligation to update publicly or otherwise revise any forward-looking statements or the foregoing list of assumptions or factors, whether as a result of new information, future events or otherwise, subject to our disclosure obligations under applicable U.S. and Canadian securities regulations. Investors are urged to read the Company’s filings with U.S. and Canadian securities regulatory agencies, which can be viewed online at www.sec.gov and www.sedar.com, respectively.

Corporate Structure

We are domiciled in Alberta, Canada and conduct our business primarily through our wholly-owned subsidiaries. The following table lists the names of our significant subsidiaries, our ownership in each subsidiary and each subsidiary's jurisdiction of incorporation or organization.

|

Subsidiary |

Ownership |

Domicile |

|

Gold Reserve Corporation |

100% |

Montana USA |

|

GR Mining (Barbados) Inc. |

100% |

Barbados |

|

GR Engineering (Barbados) Inc. |

100% |

Barbados |

In September 2016, together with Venezuela, we established Siembra Minera of which we own 45%, to develop the Brisas Cristinas Project. We also have several dormant subsidiaries domiciled in Venezuela, Barbados and Canada which were previously formed to hold our interest in our foreign subsidiaries or for future transactions.

GENERAL Development and description of the BUSINESS

Brisas Award

SETTLEMENT AGREEMENT

In February 2016, we signed the MOU with Venezuela represented by the Office of the Attorney General and the Ministry of Popular Power of Oil and Mining that contemplated settlement, including payment and resolution, of the Award granted in our favor by ICSID in respect of the Brisas Project and the transfer of the Mining Data. In April 2016, in the spirit of providing continuity to the discussions begun in February, the parties agreed to extend the MOU to allow for further efforts to agree on a settlement.

At the urging of the board of directors, management had made numerous multi-weeks trips to Venezuela since late 2015 to meet face to face with the President of Venezuela, Minister of Mines, Attorney General, Central Bank President, and many other key administration officials and their staff to ensure that a settlement agreement with Venezuela was obtained.

In July 2016, we executed the Settlement Agreement with Venezuela which contemplated payment of the Award including accrued interest in the amount of approximately $770 million in respect of the Brisas Project, acquisition of our Mining Data by Venezuela for $240 million and, included, among other terms:

· Payment of the Award in respect of the Brisas Project of approximately $770 million, including accrued interest up to February 24, 2016, in two installments, $600 million due on or before October 31, 2016 and the remaining approximately $170 million on or before December 31, 2016. The Company agreed to temporarily suspend the legal enforcement of the Award until final payment is made by Venezuela, at which time we will permanently cease all legal activities related to the collection of the Award.

· The acquisition of our Mining Data by Venezuela for $240 million, payable in four quarterly installments of $50 million beginning October 31, 2016, with a fifth and final installment of $40 million due on or before October 31, 2017. After the final payment, the Mining Data will be transferred to the Venezuelan National Mining Database.

Exhibit 99.1 Annual Information Form - Page 8

· Venezuela agreed to use the proceeds from any financing it closes after the execution of the Settlement agreement to pay us the amounts owed under the Settlement Agreement in preference to any other creditor.

· Termination of the Settlement Agreement by written notice by us, without requiring any decision from any judicial authority if the two installments with respect to the payment of the Award are not received within the periods provided in the Settlement Agreement.

In early November 2016, and again in early December 2016, the parties executed addendums to the Settlement Agreement whereby the parties agreed to revise the payment schedule under which Venezuela would make payments related to the Award and Mining Data as follows: $300 million on or before December 15, 2016; $469.7 million on or before January 3, 2017; $50 million on or before January 31, 2017; $100 million on or before February 28, 2017 and $90 million on or before June 30, 2017. The payments for the Award and Mining Data continue to be contingent upon Venezuela obtaining the necessary financing, which has not occurred and, as a result, as of the date of this report no payments have been made by Venezuela. At the passing of the last agreed upon payment date, the board of directors chose to not formally terminate the Settlement Agreement as a result of the delay in the initial agreed upon payment(s), but instead instructed management to continue all efforts to work with Venezuela to complete the terms of the Settlement Agreement. Management has recently proposed and Venezuela is currently considering a third addendum to the Settlement Agreement, whereby the parties would agree, among other things, to revise the previously proposed payment schedule.

ENFORCEMENT AND COLLECTION EFFORTS

In October 2009, we initiated a claim (the "Brisas Arbitration") under the Additional Facility Rules of the ICSID of the World Bank to obtain compensation for the losses caused by the actions of Venezuela that terminated the Brisas Project in violation of the terms of the Treaty between the Government of Canada and the Government of Venezuela for the Promotion and Protection of Investments (the "Canada-Venezuela BIT"). (Gold Reserve Inc. v. Bolivarian Republic of Venezuela (ICSID Case No. ARB(AF)/09/1)).

In September 2014, the ICSID Tribunal unanimously awarded us the Award totaling (i) $713 million in damages, plus (ii) pre-award interest from April 2008 through the date of the Award based on the U.S. Government Treasury Bill Rate, compounded annually totaling, as of the date of the Award, approximately $22.3 million and (iii) $5 million for legal costs and expenses, for a total, as of September 22, 2014, of $740.3 million. The Award (less legal costs and expenses) accrues post-award interest at a rate of LIBOR plus 2%, compounded annually for a total estimated Award as of the date of the Settlement Agreement of $770 million.

Subsequent to the issuance of the Award, both parties filed requests for the ICSID Tribunal to correct what each party identified as "clerical, arithmetical or similar errors" in the Award as is permitted by the rules of ICSID’s Additional Facility. In December 2014, the Tribunal denied both parties’ requests for correction and reaffirmed the Award originally rendered in our favor on September 22, 2014. This proceeding marked the end of the Tribunal’s jurisdiction with respect to the Award.

Although the process of getting the Award recognized and enforced is different in each jurisdiction, the process in general is-we file a petition or application to confirm the Award with the competent court; Venezuela has the right to oppose such petition for confirmation or recognition; thereafter there are a number of filings made by both parties and in some cases hearings before the court. If the court subsequently confirms the enforcement of the Award then the court will issue a judgment against Venezuela. Thereafter we will begin the process of executing the judgment by identifying and attaching specific property owned by Venezuela that is not protected by sovereign immunity.

Legal Activities in France

The Award was issued by a Tribunal constituted pursuant to the arbitration rules of ICSID’s Additional Facility and, by agreement of the parties the seat of the Tribunal was in Paris. As a consequence, the Award is subject to review by the French courts.

In October 2014, we filed an application before the Paris Court of Appeal (the "Paris Court") to obtain an Order of exequatur for the recognition of the Award in France. Venezuela opposed our application and requested a stay of execution pending the determination of its application for annulment of the Award, discussed below. On January 29, 2015, the Paris Court granted our application for exequatur and dismissed Venezuela’s request to stay the execution of the Award pending the outcome of its application to annul the Award. Since Venezuela was denied its motion to stay the execution of the Award, the exequatur or recognition of our Award granted on January 29, 2015 remains in full force and effect.

Exhibit 99.1 Annual Information Form - Page 9

In late October 2014 and in May 2015, Venezuela filed applications before the Paris Court, declaring its intent to have the Award and the December 15th decision (described above) annulled or set aside. At that time, we expected a ruling on Venezuela’s applications sometime in May 2016. As a result of the subsequent temporary suspension of the legal enforcement of the Award pursuant to the Settlement Agreement, the Paris Court did not make a ruling until February 2017.

On February 7, 2017, the Paris Court rejected all of Venezuela’s annulment arguments and issued a judgment dismissing the applications filed by Venezuela pending before the French courts in relation to the Award. In addition to the Award remaining enforceable in France, the Paris Court ordered Venezuela to pay an amount of €150,000 for our legal fees and costs. Venezuela can consider appealing the judgment before the French Cour de cassation, which is the court of final resort in the French judicial system. Regardless of whether Venezuela files an appeal, the exequatur remains in full force and effect.

Legal Activities in the District of Columbia – US District Court and US Court of Appeals

In November 2014, we filed in the U.S. District Court for the District of Columbia (the "district court") a petition to confirm the Award. In June 2015, Venezuela filed a motion to dismiss and in the alternative, Venezuela asked for a stay of enforcement of the Award pending the annulment determinations by the Paris Court. In November 2015, the district court entered an Order denying Venezuela’s motions, confirming the Award, and entering judgment for us against Venezuela for the Award, pre-award interest and legal fees totaling $740,331,576, plus post-award interest on the total amount awarded, exclusive of legal fees, at a rate of LIBOR plus 2%, compounded annually, from September 22, 2014, until payment in full (collectively, the "Judgment").

In December 2015, we filed a motion for an Order by the district court under 28 U.S.C. § 1610(c) determining that a "reasonable period of time" had elapsed since entry of the Judgment and in January 2016, the district court granted the motion, thus allowing us to pursue further efforts to enforce and collect on the Judgment. Venezuela filed a notice of appeal of the Judgment to the United States Court of Appeals for the District of Columbia Circuit. Filing of the appeal did not automatically stay enforcement of the Judgment.

Thereafter, in January 2016, we filed a motion for an Order by the district court permitting registration of the Judgment in federal district courts outside the District of Columbia and Venezuela filed a motion for a stay of execution of the Judgment pending appeal without an appeal bond, which was later denied by the district court. In same month, we served Venezuela with requests for written discovery (interrogatories and requests for production of documents) in aid of enforcement of the Judgment. The original date for Venezuela to respond to the discovery requests was in February 2016.

In February 2016, the parties filed a stipulation with the district court stating that Venezuela consented to the relief requested in our motion for an Order permitting registration of the Judgment outside the District of Columbia, that we would not so register the Judgment prior to March 2016, and that Venezuela’s due date to respond to our January 2016 discovery requests would be extended to March 2016. Shortly thereafter, the district court entered an Order enforcing the terms of this stipulation.

In March 2016, the parties agreed that Venezuela’s due date to respond to our January 2016 discovery requests would be further extended to April 2016, and that we would not register the Judgment in other federal district courts prior to April 2016.

In May 2016, the appellate court denied Venezuela's motion for a stay of execution pending appeal, the parties agreed to extend the above-referenced April 2016 deadlines to May 22, 2016, and the appellate court issued a schedule for the appeal. Thereafter, as a result of the Settlement Agreement, the parties have entered into a series of agreed or unopposed extensions of the appeal briefing schedule, which have been approved by the appellate court. Most recently, in March 2017, the court approved an extension that schedules the briefing to occur between May 2017 and July 2017.

Exhibit 99.1 Annual Information Form - Page 10

Legal Activities in Luxembourg

In October 2014, we were granted an exequatur for the recognition and execution of the Award by the Tribunal d’arrondissement de et à Luxembourg allowing us to proceed with conservatory or attachment actions against Venezuela’s assets in the Grand Duchy of Luxembourg. In January 2015, Venezuela filed a notice of appeal of this decision in the Cour d’appel de Luxembourg (the "Luxembourg Court of Appeal") asking for a stay of execution pending the determination of its application to annul the Award before the Paris Court of Appeal. In June 2015, the Luxembourg Court of Appeal stayed Venezuela's appeal of the October 28, 2014 order granting the exequatur (recognition and execution) of the Award in Luxembourg, on the basis that the Paris Court of Appeal was scheduled to hear Venezuela’s application to annul within a few months. The exequatur remains in full effect allowing us to proceed with seizure filings if and when we deem it appropriate. In light of the February 2017 ruling by the Paris Court, Venezuela must inform the Luxembourg Court of Appeal whether it wants to maintain the suspension of its appeal. The exequatur continues to allow for seizures in the form of conservatory actions to be taken while the appeal is pending.

Legal Activities in England

In May 2015, we filed in the High Court (Queen Bench’s Division - Commercial Court) an application for leave to enforce the Award pursuant to s. 101(2) of the Arbitration Act. In the English courts, such application is made by way of an Arbitration Claim Form (the "Claim"). In that same month, the Court granted leave to enforce the Award as a judgment or Order of the court, and entered judgment in the amount of the Award (the "Order and Judgment"). In September 2015 (prior to formal service), Venezuela made an application to the Court for declarations that the Court had no jurisdiction over the Claim, and for Orders that (i) the Claim be set aside, (ii) service of the Claim (if any) be dismissed and (iii) the Order and Judgment be set aside (the "Jurisdiction Application").

The hearing for the Jurisdiction Application took place in London in January 2016 and judgment was handed down the first of February 2016. The Court dismissed the Jurisdiction Application and ordered that, among other things, Venezuela did not have sovereign immunity and we followed the correct procedure in relation to the Claim. On February 23, 2016, Venezuela filed an Appeal with the Court of Appeal. Venezuela originally requested permission to appeal on an additional ground, which was denied by the Jurisdiction Application judge and the Court of Appeal at first instance, however the Court of Appeal has granted Venezuela an oral hearing in respect of this request. The permission to appeal hearing is listed for October 11, 2017. The Appeal itself is listed for October 16 to 18, 2017, with October 19, 2017 held in reserve depending on the outcome of Venezuela’s permission request (referred to above).

The parties have agreed by consent to extend the time for Venezuela to make any further application to set aside the Order and Judgment until 14 days following resolution of the Appeal of the Jurisdiction Application by Venezuela. We intend to continue to take all available steps to ensure that Appeal of the Jurisdiction Application is resolved as quickly as possible, and that any further application that Venezuela may make will be dealt with expeditiously, so that enforcement can proceed without further delay. Enforcement cannot proceed while the Appeal is pending.

Obligations Due Upon Collection of the Award and Sale of Brisas Technical Mining Data

We have outstanding Contingent Value Rights ("CVRs"), which are obligations arising from the disposition of a portion of the rights to future proceeds of the Award against Venezuela and/or the sale of the Brisas Project technical mining data (the "Mining Data").

The CVRs entitle each holder that participated in the note restructuring completed in 2012 to receive, net of certain deductions (including income tax calculation and the payment of our then current obligations), a pro rata portion of a maximum aggregate amount of 5.468% of the proceeds actually received by us with respect to the Award or disposition of the Mining Data. The proceeds associated with the Award or sale of the Mining Data, if any, could be cash, commodities, bonds, shares and/or any other consideration we receive and if such proceeds are other than cash, the fair market value of such non-cash proceeds, net of any required deductions (e.g., for taxes) will be subject to the CVRs and will become our obligation only as the Award is collected and/or the Mining Data is sold.

The Board of Directors (the "Board") approved a Bonus Pool Plan (the "Bonus Plan") in May 2012, which is intended to compensate the participants, including executive officers, employees, directors and consultants, for their past and future contributions including their past efforts related to the development of the Brisas Project, execution of the Brisas Arbitration and the collection of an award and/or sale of the Mining Data. The bonus pool under the Bonus Plan is comprised of the gross proceeds collected or the fair value of any consideration realized (calculated on substantially the same terms as the CVR) related to such transactions less applicable taxes multiplied by 1% of the first $200 million and 5% thereafter. The Bonus Plan is administered by a committee of independent directors who selected the individual participants in the Bonus Plan and fixed the relative percentage of the total pool to be distributed to each participant. Participation in the Bonus Plan by existing participants is fully vested, subject to voluntary termination of employment or termination for cause.

Exhibit 99.1 Annual Information Form - Page 11

We also maintain the Gold Reserve Director and Employee Retention Plan (the "Retention Plan") (See Note 10 to the audited consolidated financial statements). Each Unit (the "Retention Units") granted entitles such participant to receive a cash payment equal to the fair market value of one Class A: Share (a) on the date the Unit was granted or (b) on the date any such participant becomes entitled to payment, whichever is greater. Units previously granted under the plan become fully vested upon: (1) collection of proceeds from the Award and/or sale of the Mining Data totaling at least $200 million and we agree to distribute a substantial majority of the proceeds to our shareholders or, (2) the event of a change of control. A “Change of Control”, as it relates to the Retention Plan, means one or more of the following: the acquisition by any individual, entity or group, of beneficial ownership of the Company of 25 percent of the voting power of the outstanding Common Shares; a change in the composition of the Board that causes less than a majority of the current directors of the Board to be members of the incoming board; solicitation of proxies or consents by or on behalf of a person other than the board; reorganization, merger or consolidation or sale or other disposition of all or substantially all of the assets of the Company; liquidation or dissolution of the Company; or any other event the Board reasonably determines constitutes a Change of Control.

As of December 31, 2016 an aggregate of 1,457,500 unvested units have been granted to directors and executive officers of the Company and 315,000 units have been granted to other employees. We currently do not accrue a liability for the Bonus Plan or Retention Plan as events required for payment under the Plans have not yet occurred. The minimum value of these units, based on the grant date value of the Class A common shares, was approximately $7.8 million. An estimated $1.8 million of contingent legal fees will also become due upon the collection of the Award.

Upon payment of the Award or receipt of proceeds from the disposition of the Mining Data, subject to certain limitations, we are obligated to make an offer to existing holders to redeem the 2018 Notes (as defined herein) at a price equal to 120% of the principal amount of 2018 Notes then outstanding. See "Description of Capital Structure".

Our Intent to Distribute Collection of the Award or Sale of Mining Data to Shareholders

Subject to applicable regulatory requirements regarding capital and reserves for operating expenses, accounts payable and income taxes, and any obligations arising as a result of the collection of the Award or sale of the Mining Data including payments pursuant to the terms of the 2018 Convertible Notes (as defined herein) (if not otherwise converted), Interest Notes (as defined herein), CVRs, Bonus Plan and Retention Plan or undertakings made to a court of law, our current plans are to distribute to our shareholders, in the most cost efficient manner, a substantial majority of any net proceeds.

Convertible Notes Restructuring:

During the fourth quarter of 2015, we issued approximately $13.4 million of new 2018 Convertible Notes (the “New Notes”) and modified, amended and extended the maturity date of approximately $43.7 million of our previously outstanding convertible notes and interest notes from previous financings and restructurings in 2007, 2012 and 2014 (the “Modified Notes”). The newly issued 2018 Convertible Notes comprised of approximately $12.3 million aggregate principal amount of 2018 Convertible Notes, issued with an original issue discount of 2.5% of the aggregate principal amount, and approximately $1.1 million aggregate principal amount of additional 2018 Convertible Notes, representing 2.5% of the extended principal and interest amount due to the note holders as a restructuring fee.

Exhibit 99.1 Annual Information Form - Page 12

Properties

Brisas Cristinas Project

Empresa Mixta Ecosocialista Siembra Minera, S.A.

In August 2016, we executed an agreement with Venezuela for the formation of a jointly owned Mixed Company to develop and operate the Brisas Cristinas Project. On September 29, 2016 a Presidential Decree was issued authorizing the formation of Siembra Minera.

In anticipation of the Mixed Company Agreement, GR Mining and GR Engineering were formed in early 2016. GR Mining was formed to hold our interest in Siembra Minera and provide for the management of the development and operation of the Brisas Cristinas Project and GR Engineering was formed to provide technical services to Siembra Minera. Siembra Minera is owned 55% by Venezuela through Corporacion Venezolana De Mineria, S.A. (a Venezuelan government corporation) and 45% by GR Mining.

The completion of the Mixed Company Agreement was based upon extensive long-term negotiations with Venezuelan authorities, related to significant business terms, including economic conditions and various decrees and resolutions impacting the entity envisioned to develop the Brisas Cristinas Project. Concurrent with those activities, we developed the Business Plan for the Brisas Cristinas Project with broad input from our engineering consultant. Thereafter we met with and reviewed the Business Plan with PDVSA Development. These discussions were central to our joint agreement to revise royalty and income tax rates related to the Project resulting in parties concluding negotiations and coming to an agreement. Thereafter, from April to July 2016, we negotiated the various terms of the articles of incorporation and by-laws of Siembra Minera. On October 4th, Siembra Minera was duly incorporated before the Register Office in Puerto Ordaz, Bolivar state and published its incorporation in Official Gazzete No. 41.002 of that same date.

On October 31, 2016, the Ministry of Mines issued Resolution 000030 which was published in the Official Gazzette No. 41.022 on November 2, 2016, assigning the area (approximately 18,950 hectares) including the Brisas Cristinas area to Siembra Minera. On March 27, 2017, Presidential Decrees were issued transferring all of the gold and strategic minerals (including copper and silver) rights to Siembra Minera.

These Decrees also authorized a term of twenty years plus extensions, a NSR royalty of five percent for the first 10 years of production and six percent for the following 10 years, a special advantage to Venezuela of three percent of gross sales and authorization to export and sell concentrate and doré containing gold, copper, silver and other strategic minerals outside of Venezuela and maintain foreign currency balances associated with sales proceeds.

The significant negotiated terms related to the formation of Siembra Minera and its development and operation of the Brisas Cristinas Project include:

§ Siembra Minera is beneficially owned 55% by Corporacion Venezolana de Mineria, S.A. and 45% by GR Mining;

§ Siembra Minera holds the rights to the gold, copper, silver and other strategic minerals contained within a 18,950 hectare area located in the Km 88 gold mining district of southeast Bolivar State which includes the Brisas Cristinas Project;

§ GR Engineering, under a Technical Services Agreement, will provide engineering, procurement and construction services to Siembra Minera for a fee of 5% over all costs of construction and development and, thereafter, for a fee of 5% over operating costs during operations;

§ Presidential Decrees, within the legal framework of the "Orinoco Mining Arc" (created on February 24, 2016 under Presidential Decree No. 2.248 as an area for national strategic development Official Gazzette No. 40.855), will or have been issued to provide for tax and fiscal incentives for mixed companies operating in that area that include exemption from value added tax, stamp tax, municipal taxes and any taxes arising from the contribution of tangible or intangible assets, if any, to the mixed companies by the parties and the same cost of electricity, diesel and gasoline as that incurred by the government or related entities;

§ Gold price participation, in accordance with an agreed upon formula resulting in specified respective percentages based on the sales price of gold per ounce. For sales up to $1,600 per ounce, net profits will be allocated 55% to Venezuela and 45% to us. For sales greater than $1,600 per ounce, the incremental amount will be allocated 70% to Venezuela and 30% to us. For example, with sales at $1,600 and $3,500 per ounce, net profits will be allocated 55.0% ̶ 45.0% and 60.5% ̶ 39.5%, respectively;

Exhibit 99.1 Annual Information Form - Page 13

§ Net smelter return royalty (“NSR”) to Venezuela on the sale of gold, copper, silver and any other strategic minerals of 5% for the first ten years of commercial production, 6% for the next ten years;

§ Income tax rate of 14% for years one to five, 19% for years 6 to 10, 24% for years 11 to 15, 29% for years 16 to 20 and 34% thereafter;

§ The parties agreed to work together to complete financing(s) to jointly fund the contemplated $2.1 billion anticipated capital costs of the Brisas Cristinas project on behalf of Siembra Minera, which is expected to be comprised of a combination of project financing , development agencies, equipment manufacturer, offtake and smelter financings. In order to facilitate the early startup of the pre-operation and construction activities, Venezuela agreed to advance $110.2 million to Siembra Minera, which will be repaid from the financing proceeds;

§ Funds associated with future capital cost financings will be held in offshore US dollar accounts and dividends and profit distributions, if any, will be directly paid to the shareholders;

§ All funds will be converted into local currency at the most favorable exchange rate offered by Venezuela to other entities to pay, as required, Venezuela income taxes and annual operating and capital costs denominated in Bolivars for the Brisas Cristinas Project. Venezuela agrees to use its best efforts to grant to Siembra Minera similar terms that would apply to the Brisas Cristinas Project in the event Venezuela enters into an agreement with a third party for the incorporation of a mixed company to perform similar activities with terms and conditions that are more favorable than the above tax and fiscal incentives;

§ Venezuela will indemnify us and our affiliates against any future legal actions associated with the Brisas Cristinas Project; and

§ The board of directors is comprised of seven individuals, of which four are appointed by Venezuela and three by us.

Exhibit 99.1 Annual Information Form - Page 14

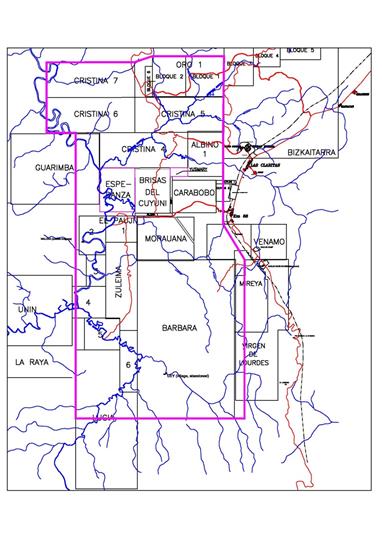

Brisas Cristinas Location

The Brisas Cristinas Project is located in the Guyana region, in the Kilometer (Km) 88 gold mining district of Bolivar State in southeast Venezuela. The name Kilometer 88 for the district came from the area being located near kilometer 88 marker of the road linking El Dorado (Km 0) with the Brazilian border (Pan American Highway or Highway 10). Las Claritas is the closest town to the property. The closest nearby large city is Puerto Ordaz situated on the Orinoco River near its confluence with the Caroní River. Puerto Ordaz is home to most of the major industrial facilities like the aluminum smelters and port facilities accessible to ocean-going vessels from the Atlantic Ocean via the Orinoco River, a distance of about 200 kilometers.

Exhibit 99.1 Annual Information Form - Page 15

Exhibit 99.1 Annual Information Form - Page 16

Brisas Cristinas History

Gold was first discovered in the Brisas Cristinas region in 1920. Gold mining at the site was initiated in the 1930's and continued sporadically on a minor scale until the early 1980’s when a gold rush occurred. During this period it has been reported that several thousand small miners worked alluvial and saprolite-hosted gold deposits using hydraulic mining techniques. This material was processed in sluices and small hammer mills. Since the early 1960’s the mining ministry granted gold mining concessions in the Guayana region, including the 1964 Las Cristinas and the 1988 Brisas concessions with small scale mining activities continuing under a legal framework.

Also, in the late 1980’s the mining ministry assigned to CVG, a state owned development corporation for the Guayana Region, the rights to grant gold mining operating contracts in the whole Guayana region, excluding the areas already under concession. Since Las Cristinas concessions had by then elapsed, CVG cleared the area of small miners and in 1991 established a joint venture with Placer Dome Inc. ("Placer") named Minera Las Cristinas (MINCA), for the development of the property. At approximately the same time, in 1992 we acquired the Brisas concession initiating the exploration and development of the Brisas property. The amount of gold recovered over the years is unknown and much of the Brisas Cristinas Project area now held by Siembra Minera is now void of any substantial vegetation and covered with tailings.

Las Cristinas

Based on publicly available information, Placer conducted essentially all of the modern exploration on Cristinas during their tenure on the property from 1991 to 2001. Placer completed line cutting, mapping, rock and soil sampling, geophysics, and drilling of 1,174 drill holes for a total of 158,738 meters of drilling, resulting in a significant presence of gold and copper in the deposit. Placer’s drilling was conducted in essentially three phases – shallow drilling to test saprolite, bedrock drilling and infill drilling in saprolite, and finally infill drilling of the pit area. Placer completed a comprehensive feasibility study on the project in 1996 that was updated in 1998.

After extensive exploration, Placer announced commencement of construction of the project in August 1997. However, in January 1998, Placer announced it had decided to suspend construction. Construction resumed once again in May 1999 but was again suspended in July 1999 due to uncertainties with respect to gold prices and legal security of title. Up until that time, Placer had reportedly spent US$168 million on the project.

CVG took possession of the property in 2001 and in 2002 signed a mine operating agreement with Crystallex International ("Crystallex") to explore, mine, and produce gold at Las Cristinas. Crystallex reportedly drilled 90 holes for a total of 28,427 meters from 2003 through early 2007. Crystallex’s 2003 drilling program twinned selected Placer holes to independently evaluate Placer’s drill-hole data and assay base. Crystallex’s subsequent drilling, conducted from 2004 through 2007, focused on infill drilling, drilling down-dip extensions of the stratiform mineralized zone, and exploring strike extensions of the deposit.

Brisas

The Brisas concession was acquired by us in August 1992 with the acquisition of Compañia Aurifera Brisas del Cuyuni C.A. Prior to 1992, no known drill holes existed on the Brisas site. Initial work included surface mapping, regional geophysical surveys, and geochemical sampling. Several anomalies were identified on the property and drilling and assaying began in 1993. The presence of a large strata bound gold-copper mineralization was discovered in both alluvial and hard rock material early in the drilling program. Additional work followed with petrology, mineral studies, density tests, metallurgical sample collection, and laboratory test work.

We commenced initial exploration drilling in 1993 utilizing both auger and core drilling methods. A majority of the exploration and development drilling took place in 1996 and 1997. From 1996 on, all exploration drilling was completed utilizing diamond drill core rigs. Additional exploration drilling was completed in 1999, 2003, 2004, and 2005. As of 2005, 802 exploration holes had been drilled of which 731 were diamond core holes. This represented 186,094 meters of exploration core drilling, and 189,985 total meters of exploration drilling, core and auger. Subsequent to 2005, 76 additional holes were drilled on the Brisas property for geotechnical and other studies.

We completed and filed in August 2005 a Venezuelan Environmental and Social Impact Assessment (V-ESIA) for the Ministry of Environment and Natural Resources ("MARN"), with the assistance of a number of independent consultants. At the time the V-EISA satisfied Venezuelan requirements to obtain an “Administrative Authorization to Affect Natural Resources for Construction of Infrastructure and Exploitation of Alluvial and Vein Deposits of Gold and Copper,” which was granted by MARN. In addition, an International Environmental and Social Impact Assessment (I-ESIA) meeting World Bank Standards, the Equator Principles and any requirements desired by financing institutions was completed in draft form during the subsequent months.

Exhibit 99.1 Annual Information Form - Page 17

Detailed engineering, including construction drawings, site layout, manpower requirements, construction planning, and many other functions required in a project of this magnitude were substantially advanced through 2008 by SNC Lavalin and was approximately 85% complete by mid-2008. This was the final step in the engineering process for mine development work and is expected to be an important resource for the development of the Brisas Cristinas project.

Brisas Cristinas Combined

Brisas and Cristinas properties are immediately adjacent to each other. Historical studies for both projects show their respective pit designs coming within a few hundred meters of each other and mineralization continuing in-line along strike over a distance of 5 to 6 kilometers covering both areas. The void between the projects, the Potaso area, had never been significantly drilled due to a large man-made lake that was a result of historical small miner activity. However, based on historical small miner activities in the immediate area and the alignment of strike and dip of mineralization being almost identical on both properties, we believed that it was highly likely that the mineralization continued between the pits.

The concept of combining the Brisas and Cristinas properties was first evaluated in the year 2000 and as part of that effort we studied additional economic aspects of developing and exploiting the mineralization on the properties. It was determined that not only did the adjoining properties share one large, continuous mineral deposit, but developing and exploiting this mineralization in a combined project would have less impact on the environment than two separate projects, and as a result would create efficiencies and economies of scale that would enhance the combined project economics. The concept was developed utilizing Brisas information combined with available Cristinas data from public records and permit documents.

In 2001 INGEOMIN, the Venezuelan government's Geological & Mining Institute prepared a comprehensive report evaluating the environmental, social and economic impacts of the combined project being proposed by us and strongly recommended its implementation. However, Venezuela decided to move forward, on a standalone basis, with the Las Cristinas project with Crystallex while we continued our work on the combined project in parallel with our efforts to develop the Brisas Project.

Multiple mineral resource estimates and feasibility studies, that are no longer current, have been completed on each individual property in the past and Siembra Minera plans to complete a new resource estimate on the combined properties in the future with a view to preparing a Preliminary Economic Assessment ("PEA") in accordance with National Instrument 43-101- Standards of Disclosure for Mineral Projects ("NI 43-101").

We believe that based on previous studies the Brisas Cristinas Project has the potential to be a large open pit mining project. Our base plan is to combine the Brisas and Cristinas properties into one project and utilize the 2008 Brisas design and layout as an initial blue print. This concept eliminates the duplication of infrastructure facilities and staff from the previously independent project plans. It reduces the project footprint or disturbed ground by 30 to 40% of the area from what was anticipated for the independently developed projects. As a result, it allows the down-dip expansion of the pit area for increased recovery of addition potential ore resources while reducing related environmental impacts significantly. The Brisas site would be the starting point for the project due to its advanced stage of design, environmental permitting and readiness for construction activity.

Brisas Cristinas Project Completed Activities

Siembra Minera held its first meeting of shareholders and its board of directors in October 2016 where the appointment of the directors was confirmed and key strategic issues associated with the startup of the initial activities of Siembra Minera were discussed. A second board meeting was held in early 2017, in the office of the Ministry of Mines, with the presence of the Directors, Legal Consultant, and Secretary of Siembra Minera, and again the discussions covered key strategic issues.

Subsequent to the October board meeting, we traveled to Germany with Venezuelan representatives to meet with a German smelter company resulting in a signed letter of intent through which the smelter expressed its interest in a future service agreement including possible financing conditions and offering the plant's available capacity to process 60 to 100% of the copper concentrate for 10 to 15 years.

The primary activities of Siembra Minera since its formation has included:

· Established bank accounts in both offshore US$ accounts and Venezuelan Bolivars. External auditors have been identified and formal designation will occur during upcoming board meetings. Certain key employees have been engaged and additional initial interviews completed. Potential office locations in Caracas and Puerto Ordaz have been identified;

· Initiated discussions whereby the parties are working on a draft EPCM contract between GR Engineering and Siembra Minera;

Exhibit 99.1 Annual Information Form - Page 18

· Conducted preliminary meetings with CAMIMPEG, a Venezuelan Army construction company, to provide project information regarding the early works plan which include man-camp and certain access roads;

· Provided CVG-Tecmin, a state corporation that provides technical services and information with regard to the development of mineral resources, with the project description and related technical information to produce and file the Environmental Questionnaire leading to the granting of the Authorization to Occupy the Territory (AOT);

· Sponsored several meetings with Mission Piar to initiate surveys and follow up on the activities of small miners groups currently working in certain parts of the 18,950 hectare property. Mission Piar is a Government instituted Mission under the Ministry of Mines in charge of providing assistance and coordination of small mining activities;

· Held fact finding meetings with the Ministry of Mines and members of the Guayana REDI to provide inputs and assist in the establishment of a General Plan of Security for the Project Area. The security of the project area falls under the responsibility of the Region of Integral Defense Guayana (REDI) lead by General Carlos Augusto Leal Tellería;

· Initiated efforts to define the Relocation Plan with the help of Venezuelan officials and REDI and supported by a census that is underway by Mission Piar. Several meetings have taken place between the Ministry of Mines and small miners as part of the relocation plan;

· Initiated development of a Small Miner Project with input from entities such as Ministry of Mines, REDI, Mission Piar and others to provide alternatives to some of the small miners that currently operate in the project area. This project is intimately linked to the Relocation Plan and includes an Early Production Plan, training of miners in environmental protection and remediation, and in other disciplines so many of them can be incorporated in the project construction and operation; and

· Requested a High Definition Multispectral Satellite image of the Project land position and its adjacent area at the end of 2016 which will be used to document existing conditions and as an aid for documenting and census of existing small miner activity. Completion will take several months due to multiple satellite passes to meet cloud cover requirement.

Brisas Cristinas Initial Scope of work

Siembra Minera will focus its initial staffing efforts towards providing the future management group the required organization structure, policies and facilities to support its workforce and expects to employ a project director and a general manager as soon as is possible. Thereafter, additional key staff positions are expected to be filled and the following tasks will be implemented:

· Identify and lease secure office facilities with reliable access to utilities such as electrical power, telephone and secure high speed internet and source office furniture and IT hardware.

· Engage professional consultants with very proven success in technical matters, engineering, design, operations experience and international environmental & social standards required to conduct data research, studies, resource estimates, pit design, mine plans, complete engineering & design work, prepare drawings, specifications, procurement documents and other documents for permits and reports.

· Engage consultants to assist in acquiring Venezuela visas, provide for incoming/outgoing transportation, day to day office work and transportation, living accommodations or housing assistance.

· Prepare and implement security policies, transportation and housing policies, hire and train security staff, acquire vehicles and equipment. It will be necessary to determine number of security people including those required for rotating shift assignments and number and type of vehicles.

· Complete initial contractual agreement between GR Engineering and Siembra Minera for EPCM services which will allow for the engagement of consultants and early-works contractors. A more extensive contract document will be completed as significant detail engineering, procurement and construction takes place.

Exhibit 99.1 Annual Information Form - Page 19

· Prepare and submit updated permit applications for approval of early-works construction which will include timber clearing, road building and sediment control structures in areas of the access roads, overland conveyor corridor, powerline corridor, process plant, man camp area, rock quarry and tailings dam area. In conjunction with the permit application; we expect to prepare and submit a draft scope of work, design specifications and drawings for construction.

· Assemble a temporary work facility and temporary housing or man camp for Company employees and consultants associated with the early-works and field data collection required for the International ESIA.

· Prepare and implement long-term small miner consultation, relocation and education program.

· Implement public consultation regarding the plans for construction, operations, reclamation, project size & magnitude providing for mitigation of the impact upon the general public and communities surrounding the project area.

· Prepare a preliminary ESIA document using existing information from the Brisas Project, which would exclude updated field data and the result of the small miner and public consultation, but would allow for the initiation of discussions with institutions for project financing and for preparation of Venezuela environmental permits. A more substantial final ESIA would be completed when the Cristinas field data is collected, combined project engineering and design is substantially complete and the small miner and public consultations with mitigation plans are complete.

· Initiate the preparation of a Preliminary Economic Assessment NI 43-101 document by an independent engineering company allowing for the public disclosure of resource tonnages, metal grade, annual production and any economic projections and providing support for obtaining international bank or financial institution project financing.

· Engage an international engineering contractor and initiate detail engineering work which will provide information regarding engineering, design and cost estimates for completion of a feasibility study. This effort will also provide design specification and pricing information that is needed for ordering long lead time equipment. The work would also support public consultations activities, permitting efforts, and completion of an updated NI 43-101 document. The new NI 43-101 will include the feasibility study results and provide a proven and probable reserve estimate for public disclosure and financing.

LMS Gold Project

On March 1, 2016, we completed the acquisition of certain wholly-owned mining claims known as the LMS Gold Project (the "Property"), together with certain personal property for $350,000, pursuant to a Purchase and Sale Agreement with Raven Gold Alaska Inc. ("Raven"), a wholly-owned subsidiary of Corvus Gold Inc.

Raven retains a royalty interest with respect to (i) "Precious Metals" produced and recovered from the Property equal to 3% of "Net Smelter Returns" on such metals (the "Precious Metals Royalty") and (ii) "Base Metals" produced and recovered from the Property equal to 1% of Net Smelter Returns on such metals, provided that we have the option, for a period of 20 years from the date of closing of the acquisition, to buy back a one-third interest (i.e. 1 %) in the Precious Metals Royalty at a price of $4 million. The Property consists of 36 contiguous State of Alaska mining claims covering 61 km² in the Goodpaster Mining District situated approximately 25 km north of Delta Junction and 125 km southeast of Fairbanks, Alaska.

The Property remains at an early stage of exploration and is the subject of a National Instrument 43-101 Technical Report entitled "Technical Report on the LMS Gold Project, Goodpaster Mining District, Alaska" dated February 19, 2016 prepared for us by Ed Hunter, BSc., P. Geo and Gary H. Giroux, M.A. Sc., P. Eng.

We have not declared or paid any dividends on our Class A common shares since 1984. We may declare cash dividends or make distributions in the future only if our earnings and capital are sufficient to justify the payment of such dividends or distributions. Regarding the collection of the Award and/or payment for the Mining Data, subject to applicable regulatory requirements regarding capital and reserves for operating expenses, accounts payable and taxes, we expect to distribute, in the most cost efficient manner, a substantial majority of any net proceeds received after fulfillment of our corporate obligations.

Exhibit 99.1 Annual Information Form - Page 20

Description of Capital Structure

We are authorized to issue an unlimited number of Class A common shares without par value of which 89,848,104 Class A common shares were issued and outstanding as at the date hereof. Shareholders are entitled to receive notice of and attend all meetings of shareholders with each Class A common share held entitling the holder to one vote on any resolution to be passed at such shareholder meetings. Shareholders are entitled to dividends if, as and when declared by the Board. Shareholders are entitled upon liquidation, dissolution or winding up of the Company to receive the remaining assets available for distribution to shareholders.

Equity Units

Equity Units were issued in February 1999, when Gold Reserve Corporation became our subsidiary, and we became the successor issuer. Generally, each shareholder of Gold Reserve Corporation received one of our Class A common shares for each common share owned in Gold Reserve Corporation. For tax reasons, certain U.S. holders elected to receive Equity Units in lieu of Class A common shares. An Equity Unit comprised one Class B common share of Gold Reserve Inc. and one Gold Reserve Corporation Class B common share, which were substantially equivalent to a Gold Reserve Inc. Class A common share and was generally immediately convertible into Class A common shares. As of December 31, 2016 and 2015 all Equity Units had been converted to Class A common shares.

We are authorized, subject to the limitations prescribed by law and our articles of incorporation, from time to time, to issue an unlimited number of serial preferred shares and to determine variations, if any, between any series so established as to all matters, including, but not limited to: the rate of dividend and whether dividends shall be cumulative or non-cumulative; the voting power of holders of such series; the rights of such series in the event of our dissolution or upon any distribution of our assets; whether the shares of such series shall be convertible; and such other designations, rights, privileges, and relative participating, optional or other special rights, and such restrictions and conditions thereon as are permitted by law. There are no preferred shares issued or outstanding as of the date hereof.

Share Purchase Warrants

We issued 1,750,000 share purchase warrants in 2013 to acquire for a two-year period one-half of one Class A common share (875,000 whole warrants) at a price of $4.00 per share. The share purchase warrants expired on September 20, 2015.

Share Purchase Options

We maintain the 2012 Equity Incentive Plan (the "2012 Plan") which provides for the grant of stock options of up to 8,750,000 of our Class A common shares. As of December 31, 2016, there were 3,357,000 options outstanding and 5,393,000 remaining options available for grant. Grants are made for terms of up to ten years with vesting periods as required by the TSXV and as may be determined by a committee established pursuant to the 2012 Plan, or in certain cases, by the Board.

Convertible Notes and Interest Notes

At December 31, 2016, we had $50.9 million aggregate principal amount of convertible notes outstanding, which are comprised of (i) approximately $49.9 million aggregate principal amount of 11% Senior Secured Convertible Notes due December 31, 2018 (the “2018 Convertible Notes”) and approximately $1.0 million aggregate principal amount of 5.50% Senior Subordinated Convertible Notes due June 15, 2022 (the “2022 Convertible Notes”). Interest on the 2018 Convertible Notes accrues and is capitalized quarterly and is payable in a new series of 11% Senior Secured Interest Notes due December 31, 2018 (the “Interest Notes” and together with the 2018 Convertible Notes, the “2018 Notes”). Interest on the Interest Notes is also payable in additional Interest Notes. We had $6.2 million aggregate principal amount of Interest Notes outstanding at December 31, 2016. The 2018 Notes mature on December 31, 2018. (See Note 11 to the audited consolidated financial statements).

Holders of the 2018 Convertible Notes may convert them into 333.3333 Class A common shares per $1,000 principal amount (which is equivalent to a conversion price of $3.00 per common share), subject to adjustment upon the occurrence of certain events. The Interest Notes are not convertible into Class A common shares or any other security. We paid, in the case of the New Notes, a fee of 2.5% of the principal in the form of an original issue discount, and in the case of the Modified Notes, an extension fee of 2.5% of the extended principal and interest notes in the form of additional 2018 Convertible Notes. For a more detailed description of the terms of the 2018 Notes, see "Material Contracts". The 2022 Convertible Notes subject to certain conditions can be redeemed, repurchased or converted into our Class A common shares at a conversion price of $7.54 per common share.

Exhibit 99.1 Annual Information Form - Page 21

Market for Securities

Our Class A common shares are traded in Canada on the TSXV under the symbol "GRZ.V". Our Class A common shares are also traded in the United States on the OTC under the symbol "GDRZF". The Notes are not listed for trading on any exchange. The following table sets forth for the periods indicated the high and low sales prices of our Class A common shares as reported on the TSXV and the OTC during 2016.

|

|

Cdn $ |

U.S. $ |

||||

|

|

High |

Low |

Volume |

High |

Low |

Volume |

|

January |

3.76 |

3.06 |

72,100 |

2.60 |

2.19 |

896,700 |

|

February |

6.23 |

3.35 |

1,012,500 |

4.54 |

2.35 |

3,238,000 |

|

March |

8.00 |

4.95 |

1,214,000 |

5.90 |

3.45 |

2,252,700 |

|

April |

6.50 |

5.52 |

306,100 |

5.20 |

4.24 |

1,234,400 |

|

May |

6.49 |

3.28 |

599,800 |

5.05 |