UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| þ |

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2012 |

OR

| ¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____ to ____ |

Commission file number 000-33393

Northwest Biotherapeutics, Inc.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 94-3306718 |

| (State or other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

| 4800 Montgomery Lane, Suite 800 | 20814 |

| Bethesda, Maryland 20814 | (Zip Code) |

| (Address of Principal Executive Offices) |

(240) 497-9024

(Registrant’s Telephone Number, Including Area Code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o | Smaller reporting company þ |

| (do not check if a smaller reporting company) |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes ¨ No þ

As of May 9, 2012, the total number of shares of common stock, par value $0.001 per share, outstanding was 162,806,546.

NORTHWEST BIOTHERAPEUTICS, INC.

TABLE OF CONTENTS

| Page | |

| PART I — FINANCIAL INFORMATION | |

| Item 1. Financial Statements | |

| Condensed Consolidated Balance Sheets as of December 31, 2011 and March 31, 2012 (unaudited) | 3 |

| Condensed Consolidated Statements of Operations (unaudited) for the three months ended March 31, 2011 and 2012 and the period from March 18, 1996 (inception) to March 31, 2012 | 4 |

| Condensed Consolidated Statements of Comprehensive Loss (unaudited) for the three months ended March 31, 2011 and 2012 and the period from March 18, 1996 (inception) to March 31, 2012 | 5 |

| Condensed Consolidated Statements of Cash Flows (unaudited) for the three months ended March 31, 2011 and 2012 and the period from March 18, 1996 (inception) to March 31, 2012 | 6 |

| Notes to Condensed Consolidated Financial Statements | 7 |

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | 16 |

| Item 4. Controls and Procedures | 19 |

| PART II — OTHER INFORMATION | |

| Item 1. Legal Proceedings | 19 |

| Item 2. Unregistered Sales of Equity Securities and Use of Proceeds | 20 |

| Item 6. Exhibits | 21 |

| SIGNATURES | 22 |

| INDEX TO EXHIBITS | 23 |

| 2 |

Part I — Financial Information

NORTHWEST BIOTHERAPEUTICS, INC.

(A Development Stage Company)

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands)

| December 31, 2011 | March 31, 2012 | |||||||

| (unaudited) | ||||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash | $ | 24 | $ | 37 | ||||

| Prepaid expenses and other current assets | 94 | 79 | ||||||

| Total current assets | 118 | 116 | ||||||

| Property and equipment: | ||||||||

| Laboratory equipment | 29 | 29 | ||||||

| Office furniture and other equipment | 172 | 172 | ||||||

| 201 | 201 | |||||||

| Less accumulated depreciation and amortization | (123 | ) | (125 | ) | ||||

| Property and equipment, net | 78 | 76 | ||||||

| Deposit and other non-current assets | 16 | 34 | ||||||

| Total assets | $ | 212 | $ | 226 | ||||

| LIABILITIES AND STOCKHOLDERS' EQUITY (DEFICIT) | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | 2,219 | $ | 3,855 | ||||

| Accounts payable, related party | 1,589 | 1,005 | ||||||

| Accrued expenses | 2,185 | 2,560 | ||||||

| Accrued expenses, related party | 630 | 961 | ||||||

| Notes payable | 3,149 | 3,306 | ||||||

| Note payable to related parties | 2,056 | 2,067 | ||||||

| Convertible notes payable, net | 4,832 | 5,270 | ||||||

| Convertible notes payable to related party, net | 3,588 | 4,672 | ||||||

| Embedded derivative liability | 601 | 253 | ||||||

| Liability for reclassified equity contracts | 29,903 | - | ||||||

| Total current liabilities | 50,752 | 23,949 | ||||||

| Long term liabilities: | ||||||||

| Notes payable | 200 | 200 | ||||||

| Convertible notes payable, net | 1,433 | 896 | ||||||

| Total long term liabilities | 1,633 | 1,096 | ||||||

| Total liabilities | 52,385 | 25,045 | ||||||

| Stockholders’ equity (deficit): | ||||||||

| Preferred stock, $0.001 par value; 20,000,000 shares authorized and none issued and outstanding | ||||||||

| Common stock, $0.001 par value; 150,000,000 and 450,000,000 shares authorized, and 149,345,623 and 159,278,036 shares issued and outstanding at December 31, 2011 and March 31, 2012, respectively | 150 | 160 | ||||||

| Additional paid-in capital | 199,605 | 237, 140 | ||||||

| Deficit accumulated during the development stage | (251,778 | ) | (261,929 | ) | ||||

| Cumulative translation adjustment | (150 | ) | (190 | ) | ||||

| Total stockholders’ equity (deficit) | (52,173 | ) | (24,819 | ) | ||||

| Total liabilities and stockholders’ equity (deficit) | $ | 212 | $ | 226 | ||||

See accompanying notes to the condensed consolidated financial statements

| 3 |

NORTHWEST BIOTHERAPEUTICS, INC.

(A Development Stage Company)

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share data)

(Unaudited)

| Three Months Ended | Period from March | |||||||||||

| March 31, | 18, 1996 (Inception) | |||||||||||

| 2011 | 2012 | to March 31, 2012 | ||||||||||

| Revenues: | ||||||||||||

| Research material sales | $ | - | $ | - | $ | 580 | ||||||

| Contract research and development from related parties | - | - | 1,128 | |||||||||

| Research grants and other | - | - | 1,061 | |||||||||

| Total revenues | - | - | 2,769 | |||||||||

| Operating cost and expenses: | ||||||||||||

| Cost of research material sales | - | - | 382 | |||||||||

| Research and development | 4,440 | 3,580 | 93,844 | |||||||||

| General and administration | 2,316 | 2,183 | 77,507 | |||||||||

| Depreciation and amortization | - | 2 | 2,365 | |||||||||

| Loss on facility sublease | - | - | 895 | |||||||||

| Asset impairment loss and other (gain) loss | - | - | 2,445 | |||||||||

| Total operating costs and expenses | 6,756 | 5,765 | 177,438 | |||||||||

| Loss from operations | (6,756 | ) | (5,765 | ) | (174,669 | ) | ||||||

| Other income (expense): | ||||||||||||

| Valuation of reclassified equity instruments | - | 491 | 16,071 | |||||||||

| Conversion inducement expense | - | - | (18,234 | ) | ||||||||

| Derivative valuation gain/(loss) | (161 | ) | 348 | 1,130 | ||||||||

| Gain on sale of intellectual property and property and equipment | - | - | 3,664 | |||||||||

| Interest expense | (1,491 | ) | (5,225 | ) | (46,789 | ) | ||||||

| Interest income and other | - | - | 1,707 | |||||||||

| Net loss | (8,408 | ) | (10,151 | ) | (217,120 | ) | ||||||

| Issuance of common stock in connection with elimination of Series A and Series A-1 preferred stock preferences | - | - | (12,349 | ) | ||||||||

| Modification of Series A preferred stock warrants | - | - | (2,306 | ) | ||||||||

| Modification of Series A-1 preferred stock warrants | - | - | (16,393 | ) | ||||||||

| Series A preferred stock dividends | - | - | (334 | ) | ||||||||

| Series A-1 preferred stock dividends | - | - | (917 | ) | ||||||||

| Warrants issued on Series A and Series A-1 preferred stock dividends | - | - | (4,664 | ) | ||||||||

| Accretion of Series A preferred stock mandatory redemption obligation | - | - | (1,872 | ) | ||||||||

| Series A preferred stock redemption fee | - | - | (1,700 | ) | ||||||||

| Beneficial conversion feature of Series D preferred stock | - | - | (4,274 | ) | ||||||||

| Net loss applicable to common stockholders | $ | (8,408 | ) | $ | (10,151 | ) | $ | (261,929 | ) | |||

| Net loss per share applicable to common stockholders — basic | $ | (0.11 | ) | $ | (0.07 | ) | ||||||

| Weighted average shares used in computing basic loss per share | 77,087 | 153,584 | ||||||||||

See accompanying notes to the condensed consolidated financial statements

| 4 |

NORTHWEST BIOTHERAPEUTICS, INC.

(A Development Stage Company)

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(in thousands)

(Unaudited)

| Period from March | ||||||||||||

| Three Months Ended | 18, 1996 | |||||||||||

| March 31, | (Inception) to | |||||||||||

| 2011 | 2012 | March 31, 2012 | ||||||||||

| Net loss | $ | (8,408 | ) | $ | (10,151 | ) | $ | (217,120 | ) | |||

| Other comprehensive loss | ||||||||||||

| Foreign currency translation adjustment loss | (20 | ) | (40 | ) | (190 | ) | ||||||

| Total comprehensive loss | $ | (8,428 | ) | $ | (10,151 | ) | $ | (217,310 | ) | |||

See accompanying notes to the condensed consolidated financial statements

| 5 |

NORTHWEST BIOTHERAPEUTICS, INC.

(A Development Stage Company)

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

(Unaudited)

| Period from | ||||||||||||

| March 18, | ||||||||||||

| 1996 | ||||||||||||

| (Inception) to | ||||||||||||

| Three Months Ended | March 31, | |||||||||||

| March 31, | 2012 | |||||||||||

| 2011 | 2012 | |||||||||||

| Cash Flows from Operating Activities: | ||||||||||||

| Net Loss | $ | (8,408 | ) | $ | (10,151 | ) | $ | (217,120 | ) | |||

| Reconciliation of net loss to net cash used in operating activities: | ||||||||||||

| Depreciation and amortization | - | 2 | 2,365 | |||||||||

| Amortization of deferred financing costs | - | - | 320 | |||||||||

| Amortization debt discount | 1,066 | 4,634 | 34,859 | |||||||||

| Derivative valuation (gain) loss | 161 | (348 | ) | (1,130 | ) | |||||||

| Accrued interest converted to stock | - | - | 260 | |||||||||

| Accreted interest on convertible promissory note | - | - | 1,484 | |||||||||

| Stock-based compensation costs | 493 | 1,042 | 20,901 | |||||||||

| Stock and warrants issued for services and other expenses | 3,262 | - | 20,269 | |||||||||

| Loan conversion inducement | - | - | 10,415 | |||||||||

| Valuation of reclassified equity contracts | - | (491 | ) | (16,070 | ) | |||||||

| Asset impairment loss and loss (gain) on sale of properties | - | - | (936 | ) | ||||||||

| Loss on facility sublease | - | - | 895 | |||||||||

| Increase (decrease) in cash resulting from changes in assets and liabilities: | - | |||||||||||

| Prepaid expenses and other current assets | 26 | (3 | ) | 613 | ||||||||

| Accounts payable and accrued expenses | 650 | 2,027 | 9,173 | |||||||||

| Related party accounts payable and accrued expenses | 1,249 | (253 | ) | 12,816 | ||||||||

| Accrued loss on sublease | - | - | (265 | ) | ||||||||

| Deferred rent | - | - | 410 | |||||||||

| Net Cash used in Operating Activities | (1,501 | ) | (3,541 | ) | (120,741 | ) | ||||||

| Cash Flows from Investing Activities: | ||||||||||||

| Purchase of property and equipment, net | - | - | (5,093 | ) | ||||||||

| Proceeds from sale of property and equipment | - | - | 258 | |||||||||

| Proceeds from sale of intellectual property | - | - | 1,816 | |||||||||

| Proceeds from sale of marketable securities | - | - | 2,000 | |||||||||

| Refund of security deposit | - | - | (3 | ) | ||||||||

| Transfer of restricted cash | - | - | (1,035 | ) | ||||||||

| Net Cash used in Investing Activities | - | - | (2,057 | ) | ||||||||

| Cash Flows from Financing Activities: | ||||||||||||

| Proceeds from issuance of note payable | 2,072 | 500 | 8,480 | |||||||||

| Proceeds from issuance of convertible notes payable to related parties | 500 | 2,955 | 4,855 | |||||||||

| Proceeds from issuance of note payable to related parties | - | - | 11,250 | |||||||||

| Repayment of note payable to related parties | - | - | (8,050 | ) | ||||||||

| Proceeds from issuance of convertible promissory note and warrants, net of issuance costs | (350 | ) | - | 23,333 | ||||||||

| Repayment of convertible promissory note | - | - | (1,069 | ) | ||||||||

| Borrowing under line of credit, Northwest Hospital | - | - | 2,834 | |||||||||

| Repayment of line of credit, Northwest Hospital | - | - | (2,834 | ) | ||||||||

| Payment on capital lease obligations | - | - | (323 | ) | ||||||||

| Payments on note payable | - | - | (420 | ) | ||||||||

| Proceeds from issuance preferred stock, net | - | - | 28,708 | |||||||||

| Proceeds from exercise of stock options and warrants | - | - | 228 | |||||||||

| Proceeds from issuance common stock, net | 210 | 139 | 59,214 | |||||||||

| Proceeds from sale of stock warrant | 4 | - | 90 | |||||||||

| Payment of preferred stock dividends | - | - | (1,251 | ) | ||||||||

| Series A preferred stock redemption fee | - | - | (1,700 | ) | ||||||||

| Deferred financing costs | - | - | (320 | ) | ||||||||

| Net Cash provided by Financing Activities | 2,436 | 3,594 | 123,025 | |||||||||

| Effect of exchange rates on cash | (20 | ) | (40 | ) | (190 | ) | ||||||

| Net increase (decrease) in cash | 915 | 13 | 37 | |||||||||

| Cash at beginning of period | 153 | 24 | - | |||||||||

| Cash at end of period | $ | 1,068 | $ | 37 | $ | 37 | ||||||

| Supplemental disclosure of cash flow information — Cash paid during the period for interest | $ | - | $ | - | $ | 1,879 | ||||||

| Supplemental schedule of non-cash financing activities: | ||||||||||||

| Equipment acquired through capital leases | $ | - | $ | - | $ | 285 | ||||||

| Issuance of common stock in connection with elimination of Series A and Series A-1 preferred stock preferences | - | - | 12,349 | |||||||||

| Issuance of common stock in connection conversion of liabilities | 2,528 | 3,738 | 22,793 | |||||||||

| Modification of Series A preferred stock warrants | - | - | 2,306 | |||||||||

| Modification of Series A-1 preferred stock warrants | - | - | 16,393 | |||||||||

| Warrants issued on Series A and Series A-1 preferred stock dividends | - | - | 4,664 | |||||||||

| Liability for reclassified equity contracts | 5,753 | 29,412 | 16,070 | |||||||||

| Accretion of mandatorily redeemable Series A preferred stock redemption obligation | - | - | 1,872 | |||||||||

| Debt discount on promissory notes | 1,435 | 3,213 | 22,714 | |||||||||

| Conversion of convertible promissory notes and accrued interest to Series D preferred stock | - | - | 5,324 | |||||||||

| Conversion of convertible promissory notes and accrued interest to Series A-1 preferred stock | - | - | 7,707 | |||||||||

| Conversion of convertible promissory notes and accrued interest to common stock | - | - | 269 | |||||||||

| Issuance of Series C preferred stock warrants in connection with lease agreement | - | - | 43 | |||||||||

| Issuance of common stock to settle accounts payable | - | - | 4 | |||||||||

| Liability for and issuance of common stock and warrants to Medarex | - | - | 840 | |||||||||

| Issuance of common stock to landlord | - | - | 35 | |||||||||

| Deferred compensation on issuance of stock options and restricted stock grants | - | - | 759 | |||||||||

| Cancellation of options and restricted stock | - | - | 849 | |||||||||

| Financing of prepaid insurance through note payable | - | - | 491 | |||||||||

| Stock subscription receivable | - | - | 480 | |||||||||

See accompanying notes to the condensed consolidated financial statements

| 6 |

Northwest Biotherapeutics, Inc.

(A Development Stage Company)

Notes to Condensed Consolidated Financial Statements

(Unaudited)

1. Basis of Presentation

The accompanying unaudited condensed consolidated financial statements include the accounts of Northwest Biotherapeutics, Inc. and its subsidiaries, NW Bio Europe Sarl and NW Bio GmBh (collectively, the “Company”, “we”, “us”, and “our” ). All material intercompany balances and transactions have been eliminated. The accompanying unaudited condensed consolidated financial statements should be read in conjunction with the financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2011. The year-end condensed balance sheet data was derived from audited financial statements, but does not include all disclosures required by accounting principles generally accepted in the United States of America (“GAAP”). All normal recurring adjustments which are necessary for the fair presentation of the results for the interim periods are reflected herein. Operating results for the three month periods ended March 31, 2011 and 2012 are not necessarily indicative of results to be expected for a full year.

The independent registered public accounting firm’s report on the financial statements for the fiscal year ended December 31, 2011 states that because of recurring operating losses, net operating cash flow deficits, and a deficit accumulated during the development stage, there is substantial doubt about the Company’s ability to continue as a going concern. A “going concern” opinion indicates that the financial statements have been prepared assuming the Company will continue as a going concern and do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result from the outcome of this uncertainty.

2. Summary of Significant Accounting Policies

The Company implemented the following accounting policy during the period ended March 31, 2012.

In June 2011, the Financial Accounting Standards Board issued ASU No. 2011-05, Comprehensive Income, or ASU 2011-05. The guidance in ASU 2011-05 revises the manner in which entities present comprehensive income in their financial statements. An entity is required to report the components of comprehensive income in either one or two consecutive financial statements:

| · | A single, continuous statement must present the components of net income and total net income, the components of other comprehensive income and total other comprehensive income, and a total for comprehensive income; or |

| · | In a two-statement approach, an entity must present the components of net income and total net income in the first statement. That statement must be immediately followed by a financial statement that presents the components of other comprehensive income, a total for other comprehensive income, and a total for comprehensive income. |

ASU 2011-05 does not change the items that must be reported in other comprehensive income. The amendments in ASU 2011-05 are effective for fiscal years beginning after December 15, 2011 and the Company adopted this guidance during the three months ended March 31, 2012, and implemented the two-statement approach.

The other significant accounting policies used in the preparation of the Company’s condensed consolidated financial statements are disclosed in Note 3 to our consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2011.

3. Stock-Based Compensation

Compensation expense for all stock-based awards is measured at the grant date based on the fair value of the award and is recognized as an expense, on a straight-line basis, over the employee's requisite service period (generally the vesting period of the equity award). The fair value of each option award is estimated on the date of grant using a Black-Scholes option valuation model. Stock-based compensation expense is recognized only for those awards that are expected to vest using an estimated forfeiture rate. We estimate pre-vesting option forfeitures at the time of grant and reflect the impact of estimated pre-vesting option forfeitures in compensation expense recognized. For options and warrants issued to non-employees, the Company recognizes stock compensation costs utilizing the fair value methodology over the related period of benefit.

| 7 |

Stock-based compensation expense was as follows for the three months ended March 31 (in thousands):

| 2011 | 2012 | |||||||

| Research and development | $ | 164 | $ | 158 | ||||

| General and administrative | 329 | 884 | ||||||

| Total stock- based compensation expense | $ | 493 | $ | 1,042 | ||||

There were no options to purchase common stock granted during the three month periods ended March 31, 2011 and 2012. At March 31, 2012, the unrecognized compensation expense related to stock options was $3.6 million which is to be recognized over a weighted average period of approximately 3 years.

4. Fair Value Measurements

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. U.S. GAAP establishes a three tier fair value hierarchy which prioritizes the inputs used in measuring fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). These tiers include:

| 8 |

| · | Level 1, defined as observable inputs such as quoted prices for identical instruments in active markets; |

| · | Level 2, defined as inputs other than quoted prices in active markets that are either directly or indirectly observable such as quoted prices for similar instruments in active markets or quoted prices for identical or similar instruments in markets that are not active; and |

| · | Level 3, defined as unobservable inputs in which little or no market data exists, therefore requiring an entity to develop its own assumptions, such as valuations derived from valuation techniques in which one or more significant inputs or significant value drivers are unobservable. |

The Company's liability for reclassified equity contracts were measured using significant unobservable (Level 3) inputs. There were no assets measured at fair value using unobservable inputs either as of or during the three months ended March 31, 2011 or as of or during the three months ended March 31, 2012.

As a result of the Company entering into convertible promissory notes and issuing warrants to purchase common stock, the Company's total potential outstanding common stock exceeded the Company’s authorized shares by approximately 109 million shares as of December 31, 2011, as also discussed in Note 7. As a result the Company was required to value a number of shares equal to the excess issuable on exercise of warrants and options and on conversion of convertible notes and recognize the value as a liability. The Company’s stockholders approved an increase in the number of authorized shares sufficient to cover the excess as of February 6, 2012. At that time, the liability was remeasured, with changes in value included in other income/(expense), and then reclassified to additional paid-in capital.

The following table represents the activity for the Company’s liability for reclassified equity contracts for the periods ended March 31, 2011 and 2012:

| 2011 | 2012 | |||||||

| Beginning balance | $ | - | $ | 29,903,000 | ||||

| Liabilities reclassified | 5,753,000 | 693,000 | ||||||

| Change in value of reclassified liabilities | - | (491,000 | ) | |||||

| Liabilities reclassified to equity | - | (30,105,000 | ) | |||||

| Ending balance | $ | 5,753,000 | $ | - | ||||

The Company concluded that certain conversion features and warrant agreements included down-round provisions and were not indexed to the Company’s stock (and are therefore recorded as derivative liabilities). The Company recognizes the derivative liabilities at their respective fair values using a binomial model adjusted for the probability of issuance using a Monte Carlo simulation. Changes in the fair value are recorded in “Derivative valuation gain (loss)” in the condensed consolidated statements of operations. Key assumptions for determining fair values during the period presented included expected terms ranging from between 6 and 18 months, volatility ranging from between 95% and 190% and risk-free interest rate of 0.18%.

The Company's embedded derivative liability was measured using significant unobservable (Level 3) inputs. The following table represents the Company’s embedded derivative liability activity for the three months ended March 31, 2011 and 2012:

| 2011 | 2012 | |||||||

| Beginning balance | $ | 839,000 | $ | 601,000 | ||||

| Reclassification to stockholders' equity upon conversion and expiration of derivative | (168,000 | ) | - | |||||

| Net change in fair value of embedded derivative liabilities | 161,000 | (348,000 | ) | |||||

| Ending balance | $ | 832,000 | $ | 253,000 | ||||

| 9 |

5. Liquidity and Going Concern

The Company has experienced recurring losses from operations, and, as of March 31, 2012, had a working capital deficit of $23.8 million and a deficit accumulated during the development stage of $261.9 million.

Since 2004, Toucan Capital Fund II, L.P. (“Toucan Capital”), Toucan Partners LLC (“Toucan Partners”), entities controlled by Ms. Linda Powers, the managing director of Toucan Capital and managing member of Toucan Partners, and Ms. Linda Powers (collectively “Toucan”) have provided substantial funding to the Company. During the period from 2004 to 2007, the funding consisted of various loans and the purchase of common stock. Under a Conversion Agreement during 2007, all loans payable to Toucan outstanding at the time were converted to preferred stock and the preferred stock was subsequently converted to common stock. As a result of additional loans, as of March 31, 2012, notes payable include $4.6 million convertible notes payable to Toucan. The notes payable to Toucan outstanding as of March 31, 2012, are convertible at prices ranging from $0.20 to $0.57.

In addition, the Company utilizes the services of Cognate BioServices, Inc., an entity controlled by Toucan, for manufacturing DCVax product candidates, regulatory advice, research and development preclinical activities, and managing clinical trials. Accounts payable to Cognate BioServices, Inc. amounted to $0.8 million at March 31, 2012. As of March 31, 2012, the Company has a loan payable to Artecel, an entity also controlled by Toucan, amounting to $734,000. The Company and Artecel have not yet agreed to payment terms.

As a result of this financing activity, as of March 31, 2012, Toucan held 71,202,148 shares of common stock, representing approximately 44.7% of the common stock outstanding. Further, as of March 31, 2012, Toucan, beneficially owned (including unexercised warrants) 111,580,839 shares of common stock, representing a beneficial ownership interest of approximately 69.3%.

| 10 |

In addition to financing obtained from Toucan and related entities, the Company has raised additional capital by issuing common stock and debt securities. As of May 7, 2012 the Company had approximately $0.3 million of cash on hand. The Company will need to raise additional capital in the near future to continue to fund its clinical trials and other operating activities and there can be no assurance that its efforts to seek such funding will be successful. The Company may seek funding from Toucan Capital or Toucan Partners or their affiliates or other third parties. Such parties are under no obligation to provide the Company with any additional funds, and any such funding may be dilutive to stockholders and may contain restrictive covenants. The Company is currently exploring additional financings with several other parties; however, there can be no assurance that the Company will be able to complete any such financings or that the terms of such financings will be attractive to the Company. If the Company’s capital raising efforts are unsuccessful, its inability to obtain additional cash as needed could have a material adverse effect on the Company’s financial position, results of operations and the Company’s ability to continue its existence.

6. Notes Payable

Convertible Notes Payable to Related Parties

Al Rajhi converted the note payable with a principal balance of $2,523,201 into 4,426,670 shares of common stock on February 9, 2012.

The Company received proceeds of $1,500,000 in connection with issuing a convertible note to Toucan Partners on February 9, 2012. Warrants to purchase 4,687,500 shares of common stock at an exercise price of $0.57 for five years were issued in connection with the note. The note is unsecured, but will become secured if the Company enters into any secured financing or if there is an event of default, as defined. The note is payable on demand with 14 days written notice and carried an original issue discount of 10% and a one time interest charge of 10%. The conversion price of the note is 95% of the average five day closing price of the Company's common stock for ten days prior to conversion. The relative fair value of the warrants and beneficial conversion feature (based on the effective conversion price of the note payable) amounted to $761,240 and $792,055, respectively. The debt discount associated with the warrants and beneficial conversion feature was immediately written off to interest expense.

The Company received proceeds of $1,255,000 in connection with issuing unsecured convertible notes to Toucan Partners on dates between January 3, 2012 and March 6, 2012. Warrants to purchase 4,470,938 shares of common stock at an exercise price of $0.57 and terms between three and five years were issued in connection with the notes. The notes are payable on demand with between 7 and 14 days written notice and carried an original issue discount of 10% and a one-time interest charge of 10%. The conversion prices of the notes are 95% of the average five day closing price of the Company's common stock for twenty days prior to conversion. The relative fair value of the warrants and beneficial conversion feature (based on the effective conversion price of the notes payable) amounted to $616,315 and $673,632, respectively. The debt discount associated with the warrants and beneficial conversion feature was immediately written off to interest expense.

The Company received proceeds of $200,000 in connection with issuing an unsecured convertible note to an officer of the Company on January 3, 2012. Warrants to purchase 712,500 shares of common stock at an exercise price of $0.57 for three years were issued in connection with the note. The note is payable on demand with 7 days written notice and carried an original issue discount of 10% and a one time interest charge of 10%. The conversion price of the note is 95% of the average five day closing price of the Company's common stock for 20 days prior to conversion. The relative fair value of the warrants and beneficial conversion feature (based on the effective conversion price of the note payable) amounted to $94,653 and $101,650, respectively. The debt discount associated with the warrants and beneficial conversion feature was immediately written off to interest expense.

Convertible Notes Payable

The Company received proceeds of $500,000 in connection with issuing a 9% unsecured convertible note on January 24, 2012. The note is payable on January 24, 2013 and carried an original issue discount of $220,000. The conversion price of the note ranges from between 80% and 85% of the average five day closing price of the Company's common stock for 10 days prior to conversion. The debt discount related to the beneficial conversion feature amounted to $173,859 and will be amortized over the term of the note.

The holders of notes payable with an aggregate principal balance of $1,175,195 converted notes payable into 5,014,773 shares of common stock during the three months ended March 31, 2012.

| 11 |

Notes payable consist of the following at December 31, 2011 and March 31, 2012 (in thousands):

| 2011 | 2012 | |||||||

| Notes payable - current | ||||||||

| 12% unsecured originally due July 2011 | $ | 935 | $ | 935 | ||||

| 6% unsecured due May 16, 2012 (net of discount of $236 in 2011 and $79 in 2012) | 1,764 | 1,921 | ||||||

| 12% unsecured originally due March 2011 | 450 | 450 | ||||||

| $ | 3,149 | $ | 3,306 | |||||

| Notes payable related parties - current | ||||||||

| 12% unsecured due June 2012 (net of discount of $21 in 2011 and $10 in 2012) | $ | 2,056 | $ | 2,067 | ||||

| Convertible notes payable, net - current | ||||||||

| 6% unsecured originally due March 2011 | $ | 110 | $ | 110 | ||||

| 6% unsecured due between March 2011 and February 2012 (net of discount of $34 in 2011 and $0 in 2012) | 2,566 | 2,409 | ||||||

| 6% unsecured due between April 2011 and February 2012 (net of discount of $0 in 2011 and $55 in 2012) | 100 | 50 | ||||||

| 11% unsecured due December 2011 (net of discount of $38 in 2011 and $38 in 2012) | 50 | 50 | ||||||

| 10% unsecured convertible note due November 2012 (net of discount of $1,833 in 2011 and $1,333 in 2012) | 1,167 | 1,667 | ||||||

| 6% unsecured due June 2012 (net of discount of $182 in 2011 and $310 in 2012) | 839 | 984 | ||||||

| $ | 4,832 | $ | 5,270 | |||||

| Convertible Notes payable related party, net - current | ||||||||

| 12% unsecured due June 2012 (net of discount of $93 in 2011) | $ | 2,430 | $ | - | ||||

| 6% due July 2011 and November 2011 and on demand (net of discount of $92 in 2011 and $69 in 2012) | 1,158 | 4,672 | ||||||

| $ | 3,588 | $ | 4,672 | |||||

| Long term notes payable | ||||||||

| 6% unsecured note due October 2012 | 200 | 200 | ||||||

| $ | 200 | $ | 200 | |||||

| Long term convertible notes, net | ||||||||

| 4% unsecured due November 15, 2013 (net of discount of $42 in 2011 and $36 in 2012) | $ | 402 | $ | 408 | ||||

| 4% unsecured due June 30, 2013 (net of discount of $9 in 2011) | 67 | - | ||||||

| 11% unsecured convertible note due December 2013 (net of discount of $321 in 2011 and $98 in 2012) | 964 | 488 | ||||||

| $ | 1,433 | $ | 896 | |||||

| Total notes payable, net | $ | 15,258 | $ | 16,411 | ||||

| 12 |

7. Reclassified Equity Contracts

The Company accounts for potential shares that can be converted to common stock and if converted, will be in excess of authorized shares, as a liability that is recorded on the balance sheet (at fair value) only until the authorized number of shares is increased (at which time the whole liability will be remeasured, with changes in value included in other income/(expense), and then reclassified to additional paid-in capital). The value of the liability was computed by valuing the securities that management believed were most likely to be converted. This liability is revalued at each reporting date with any change in value included in other income/(expense) until such time as enough shares are authorized to cover all potentially convertible instruments.

As a result of the Company entering into convertible promissory notes and issuing, stock options, and warrants to purchase common stock, the Company's total potential outstanding common stock exceeded the Company's authorized shares by approximately 109 million shares at December 31, 2011. During 2012, the number of potential shares in excess of authorized shares increased to approximately112 million. Effective February 6, 2012, the number of authorized common shares was increased to 450 million and the liability for potential shares in excess of total authorized shares was revalued at that date. This valuation resulted in non-cash gain of approximately $0.5 million during the three months ended March 31, 2012. The liability reclassified to additional paid in capital, during the three months ended March 31, 2012 amounted to approximately $30 million.

8. Net Income (Loss) Per Share Applicable to Common Stockholders

Basic net loss per share is calculated based on the weighted average number of common shares outstanding during the reporting period. Diluted loss per share is computed on the basis of the weighted average number of common shares plus dilutive potential common shares outstanding using the treasury stock method. The potentially dilutive securities are antidilutive due to the Company's net losses and are as follows for all periods presented (in thousands):

| Three Months Ended March 31 | ||||||||

| 2011 | 2012 | |||||||

| Common stock options | 3,257 | 25,179 | ||||||

| Common stock warrants | 46,726 | 67,237 | ||||||

| Convertible notes | 29,750 | 34,638 | ||||||

| Excluded potentially dilutive securities | 79,733 | 127,054 | ||||||

9. Related Party Transactions

Cognate Agreement

During the quarter ended June 30, 2011, the Company entered into a new service agreement with Cognate Therapeutics, Inc. (“Cognate”), a contract manufacturing and services organization in which Toucan Capital has a majority interest. In addition, two of the principals of Toucan Capital are members of Cognate’s board of directors and Linda Powers who is a director of Cognate and managing director of Toucan Capital is Chairperson of the Company’s Board of Directors and Chief Executive Officer of the Company. This agreement replaces the agreement dated May 17, 2007 between the Company and Cognate, which had expired. Under the service agreement, the Company agreed to continue to utilize Cognate’s services, for certain consulting and manufacturing services to the Company for its ongoing DCVax®-Brain Phase II clinical trial. The scope of services and the economics are comparable to the prior agreement, and the structure and process for payments are simplified. Under the terms of the new agreement the Company will pay Cognate a monthly facility fee and a fixed fee (in lieu of cost-plus charges) for each patient in the study, subject to specified minimum number of patients per month, plus charges for certain patient and product data services if such services are requested by the Company. The current service agreement expires on March 31, 2016.

| 13 |

During the quarters ending March 31, 2011 and 2012, respectively, the Company recognized approximately $1.7 million and $2.2 million of research and development costs related to these service agreements. As of March 31, 2011 and 2012, the Company owed Cognate approximately $6.2 million and $0.8 million, respectively.

Toucan Capital

In accordance with a recapitalization agreement between the Company and Toucan Capital, as amended, pursuant to which Toucan Capital agreed to recapitalize the Company by making loans to the Company, Toucan paid certain legal and other administrative costs on the Company’s behalf. Pursuant to the terms of the Conversion Agreement discussed above, the recapitalization agreement was terminated on June 22, 2007. Subsequent to the termination of the recapitalization agreement, Toucan Capital continues to incur costs on behalf of the Company. These costs primarily relate to consulting costs and travel expenses incurred in support of the Company’s international expansion efforts. In addition, since July 1, 2007 the Company has accrued and recorded rent expense due to Toucan Capital Corp. an affiliate of Toucan Capital for its office space in Bethesda, Maryland.

During the three months ending March 31, 2011 and 2012, respectively, the Company recognized approximately $0.8 million and $0.1 million of general and administrative costs related to this recapitalization agreement, rent expense, as well as legal, travel and other costs incurred by Toucan Capital, Toucan Partners and Linda Powers on the Company’s behalf. At December 31, 2011 and March 31, 2012, accrued expenses payable to Toucan Capital and related parties amounted to $0.6 million and $0.6 million, respectively, and are included as part of accounts payable to related parties in the accompanying consolidated balance sheets.

During 2009, the Company agreed with Toucan Capital, Toucan Partners and Linda Powers that some or all of the accrued expenses owed by the Company to these parties for certain expense reimbursements will be converted into shares of common stock instead of paid in cash. The parties agreed that these accrued expenses will be converted into common stock at a conversion rate equal to the price per share paid by unrelated investors at that time, and no less favorable than the conversion rate applied to any other creditor of the Company ($0.20 per share). The parties are in the process of determining the amounts of unbilled accrued expenses. The impact of the conversion will result in a reduction of liabilities for the amount converted. In addition, the Company will recognize the value of common stock issued in excess of the amount of the accrued expenses converted, if any, as a charge to operations when the conversion takes place. Finalization of these arrangements is in process.

The Company terminated its lease with Toucan Capital Corporation on December 31, 2009. The Company's obligation will be approximately $127,000 in 2012. There are no amounts due after 2012.

Artecel

During 2011, the Company received an operational loan from an entity controlled by Toucan Capital. Artecel, a stem cell research company, provided the Company with $734,000 to be used as funding for ongoing clinical trials. The Company and Artecel have not yet agreed to repayment terms.

10. Stockholders’ Equity (Deficit)

Common Stock Issuances

Issuances of common stock during 2012 were as follows:

During the three months ended March 31, 2012 the Company sold to private investors 216,667 shares of common stock at $0.27 per share for net proceeds of $65,000.

During the three months ended March 31, 2012 the Company sold to private investors 227,273 shares of common stock at $0.33 per share for net proceeds of $75,000.

During the three months ended March 31, 2012, the Company issued 9,441,443 shares of common stock as a result of the conversion of $3.7 million of notes payable.

During three months ended March 31, 2012, the Company issued 47,031 shares of common stock to settle accounts payable with a balance of $15,000.

| 14 |

Stock Purchase Warrants

Issuances of warrants during 2012 were as follows:

In January 2012, the Company issued warrants to purchase 56,250 shares of common stock at an exercise price of $0.40 per share in connection with the purchase of shares of the Company’s common stock.

In February 2012, the Company issued warrants to purchase 216,666 shares of common stock at an exercise price of $0.30 per share connection with the purchase of shares of the Company’s common stock.

In connection with the issuance of convertible notes payable to Toucan and an officer of the Company, the Company issued warrants to purchase 9,870,938 shares of common stock at an exercise price of $0.57 per share with an exercise period between three and five years.

11. Subsequent Events

Four M Purchasers and matching funds

During April and May 2012, the Company received $2.5 million related to the issuance of an 8% secured convertible note payable to Four M Purchasers. The note is payable on April 2, 2013, and is convertible at a price of $ 0.40 per share. Warrants to purchase 3,212,500 shares of common stock at an exercise price of $0.40 for five years were issued in connection with the note. The agreement provided that Four M Purchasers advanced the Company $500,000 upon executing the agreement and advanced the remaining $2 million (on a 2:1 basis) when the funds were matched by other investors (the Company received $1,142,000 from the issuance of notes payable and common stock to other investors and received the remaining $2 million from Four M Purchasers).

The funds matched from other investors resulted in the issuance of 8% convertible notes with an aggregate principal balance of $935,000 due in April 2013. In connection with the convertible notes, the Company also issued 4,025,000 warrants to purchase shares of common stock at an exercise price of $0.40 per share for five years. In addition, the Company issued 900,000 shares of common stock for proceeds of $207,000.

In connection with the execution of the $2.5 million secured convertible note payable, Four M Purchasers agreed to extend the maturity date for the $2 million note payable issued to Four M Purchasers on November 10, 2011. The $2 million note was originally due on May 10, 2012 and the extended due date is April 2, 2013. Also, the Company agreed to grant a security interest in the Company's intellectual property (all patents and licenses) to secure the repayment under the $2.5 million convertible note and the $2 million note payable.

Other

Between April and May 2012, the Company converted $507,000 of liabilities into 2,618,142 shares of common stock. Additionally, 10,368 shares of the Company’s common stock were issued in consideration of consulting services rendered in April.

| 15 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited condensed consolidated financial statements and the notes to those statements included with this report. In addition to historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those projected. The words “believe,” “expect,” “intend,” “anticipate,” and similar expressions are used to identify forward-looking statements, but some forward-looking statements are expressed differently. Many factors could affect our actual results, including those factors described under “Risk Factors” elsewhere in this report. These factors, among others, could cause results to differ materially from those presently anticipated by us. You should not place undue reliance on these forward-looking statements.

Overview

We are a development stage biotechnology company focused on discovering, developing and commercializing immunotherapy products that generate and enhance immune system responses to treat cancer. Data from our clinical trials suggest that our cancer therapies significantly extend both the time to tumor recurrence and patient survival time, while providing a superior quality of life with no debilitating side effects when compared with current therapies.

Our financing activities are described below under “— Liquidity and Capital Resources”. We will need to raise additional capital to fund our operations, including our Phase II DCVax ® -L clinical trial. If the results of our Phase II trial are positive, we plan to seek early product approval for DCVax ® -L, at the end of this trial.

We have experienced recurring losses from operations and as of March 31, 2012 we have a deficit accumulated during the development stage of $261.9 million. In addition, our independent registered public accounting firm’s report on the financial statements for the year ended December 31, 2011, states that because of recurring operating losses, net operating cash flow deficits, and a deficit accumulated during the development stage, there is substantial doubt about the Company’s ability to continue as a going concern.

Critical Accounting Policies and Estimates

Our discussion and analysis of our financial condition and results of operations are based upon our financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses and related disclosure of contingent assets and liabilities. The critical accounting policies that involve significant judgments and estimates used in the preparation of our financial statements are disclosed in our Annual Report on Form 10-K for the year ended December 31, 2011.

Recent Accounting Pronouncements

See Note 2 to Condensed Consolidated Financial Statements in this Form 10-Q.

Results of Operations

Operating costs:

Operating costs and expenses consist primarily of research and development expenses, including clinical trial expenses which increase when we are actively participating in clinical trials, and general and administrative expenses.

Research and development:

Discovery and preclinical research and development expenses include scientific personnel-related salary and benefit expenses, costs of laboratory supplies used in our internal research and development projects, travel, regulatory compliance, and expenditures for preclinical and clinical trial operation and management when we are actively engaged in clinical trials.

Because we are a development stage company, we do not allocate research and development costs on a project basis. We adopted this policy, in part, due to the unreasonable cost burden associated with accounting at such a level of detail and our limited number of financial and personnel resources.

| 16 |

General and administrative:

General and administrative expenses include administrative personnel related salary and benefit expenses, cost of facilities, insurance, travel, legal support, property and equipment and amortization of stock options and warrants.

Three Months Ended March 31, 2012 and 2011

We recognized a net loss of $10.2 million for the three months ended March 31, 2012 compared to a net loss of $8.4 million for the three months ended March 31, 2011. The increased loss was primarily attributable to the Company’s increased borrowing costs during the three months ended March 31, 2012.

Research and Development Expense. Research and development expense decreased from $4.4 million for the three months ended March 31, 2011 to $3.6 million for the three months ended March 31, 2012. The decrease was primarily attributable to the declining costs associated with the resumption of enrollment in the brain cancer clinical trials.

General and Administrative Expense. General and administrative expense was $2.1 million for the three months ended March 31, 2012 compared to $2.3 million for the three months ended March 31, 2011. The decrease was primarily due to a reduction in travel and related consultant expenses.

Valuation of reclassified equity contracts. During the three months ended March 31, 2012, the Company recognized a non-cash gain amounting to $491,000 from the decrease in value of reclassified equity contracts. There was no gain or loss for reclassified equity contracts during the same period a year ago, since there were no contracts required to be accounted for as liabilities during the period in 2011.

Derivative valuation gain and loss. During the three months ended March 31, 2012 the Company recognized a gain on derivative liabilities of $348,000 due to the change in value of the financial instruments.

Interest (Expense). Interest expense increased to $5.2 million for the three months ended March 31, 2012 from $1.5 million for the three months ended March 31, 2011. Interest expense increased for the three-month period ended March 31, 2012 primarily related to the increased borrowing costs and terms of the convertible notes payable that were initiated during the three month period ended March 31, 2012.

Liquidity and Capital Resources

At March 31, 2012, cash totaled $37,000, compared to $24,000 at December 31, 2011. Working capital was a deficit of $23.7 million at March 31, 2012, compared to a deficit of $50.6 million at December 31, 2011. The working capital deficit decreased as of March 31, 2012 as compared to March 31, 2011 primarily due to the decrease in the liability for reclassified equity contracts in 2012. Cash balances increased during the quarter ended March 31, 2012 as compared to the quarter ended March 31, 2011 due primarily to the financing transactions discussed below that were executed in 2012.

The change in cash for the periods presented was comprised of the following (in thousands):

| March 31, 2011 | March 31, 2012 | Change | ||||||||||

| Net cash provided by (used in): | ||||||||||||

| Operating activities | $ | (1,501 | ) | $ | (3,541 | ) | $ | (2,040 | ) | |||

| Investing activities | - | - | - | |||||||||

| Financing activities | 2,436 | 3,594 | 1,158 | |||||||||

| Effect of exchange rates on cash | (20 | ) | (40 | ) | 20 | |||||||

| Increase in cash | $ | 915 | $ | 13 | $ | (862 | ) | |||||

Operating Activities

We used $3.5 million in cash for operating activities during the three months ended March 31, 2012. The increase in cash used in operating activities was a result of an increase in activities related to the Company’s ongoing Phase II clinical trials in the United States.

Investing Activities

Investing activities for the periods presented are not material.

| 17 |

Financing Activities

During the three months ended March 31, 2012, our financing activities consisted of net proceeds from notes payable amounting to $3.5 million and proceeds from the issuance of common stock amounting to $0.1 million. The increase in the Company's debt financing activities was largely due to the need to raise funding for costs associated with the ongoing Phase II clinical trials in the United States.

We estimate that our current funding is sufficient to enable us to proceed with our current activities under our DCVax ® -L program. Our ongoing funding requirements will depend on many factors, including the number of staff we employ, the pace of patient enrollment in our brain cancer trial, the cost of establishing clinical studies and compassionate use/named patient programs in other countries, and unanticipated developments. Without additional capital, we will not be able to proceed with significant enrollment in our DCVax ® -L clinical trial or move forward with compassionate use/named patients programs or with any of our other product candidates for which investigational new drug applications have been cleared by the FDA. We will also be constrained in developing our second generation manufacturing processes, which offer the potential for significant reduction in product costs.

Additional funding will be required in the near future and there can be no assurance that our efforts to seek such funding will be successful. If our capital raising efforts are unsuccessful, our inability to obtain additional cash as needed could have a material adverse effect on our financial position, results of operations and our ability to continue our existence. We may seek additional funds through the issuance of additional common stock or other securities (equity or debt) convertible into shares of common stock, which could dilute the ownership interest of our stockholders. We may seek funding from Toucan Capital or Toucan Partners or their affiliates or other third parties. Such parties are under no obligation to provide us any additional funds, and any such funding may be dilutive to stockholders and may contain restrictive covenants that could limit our ability to take certain actions.

| 18 |

Item 4. Controls and Procedures

Evaluation of Disclosure Controls and Procedures

Under the supervision and with the participation of our management, including our principal executive, financial and accounting officer, we conducted an evaluation of our disclosure controls and procedures, as such term is defined under Rule 13a-15(e) promulgated under the Securities Exchange Act of 1934, as amended. Based on this evaluation, our principal executive, financial and accounting officer concluded that, as of March 31, 2012, in light of the material weaknesses identified in our management report on internal controls and procedures contained in our Form 10-K for the fiscal year ended December 31, 2011, Item 9A filed on April 13, 2012, our disclosure controls and procedures were not effective to ensure that the information required to be disclosed by us in the reports that we file or submit under the Securities Exchange Act of 1934 is accumulated and communicated to management, including our chief executive officer, financial and accounting officer, to allow timely decisions regarding required disclosure, and that such information is recorded, processed, summarized and reported within the time periods prescribed by the SEC.

Changes in Internal Control over Financial Reporting

There has been no change in our internal controls over financial reporting that occurred during the fiscal quarter ended March 31, 2012 that has materially affected, or is reasonably expected to materially affect, our internal controls over financial reporting.

Part II — Other Information

Item 1. Legal Proceedings

From time to time, we are involved in claims and suits that arise in the ordinary course of our business. Although management currently believes that resolving any such claims against us will not have a material adverse impact on our business, financial position or results of operations, these matters are subject to inherent uncertainties and management’s view of these matters may change in the future.

| 19 |

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds

On January 20, 2012, the Company issued 227,273 shares of common stock to an affiliated investor at $0.33 per share for net proceeds of $75,000.

On February 27, 2012, the Company issued 216,666, shares of common stock to a private investor at $0.27 per share for net proceeds of $65,000.

The sales of the securities identified above were made pursuant to privately negotiated transactions that did not involve a public offering of securities and, accordingly, we believe that these transactions were exempt from the registration requirements of the Securities Act pursuant to Section 4(2) of the Securities Act and Rule 506 of Regulation D. The agreements executed in connection with this sale contain representations to support the Company’s reasonable belief that the Investor had access to information concerning the Company’s operations and financial condition, the Investor acquired the securities for their own account and not with a view to the distribution thereof in the absence of an effective registration statement or an applicable exemption from registration, and that the Investor are sophisticated within the meaning of Section 4(2) of the Securities Act and are “accredited investors” (as defined by Rule 501 under the Securities Act). In addition, the issuances did not involve any public offering; the Company made no solicitation in connection with the sale other than communications with the Investor; the Company obtained representations from the Investor regarding their investment intent, experience and sophistication; and the Investor either received or had access to adequate information about the Company in order to make an informed investment decision. All of the foregoing securities are deemed restricted securities for purposes of the Securities Act.

| 20 |

Item 6. Exhibits

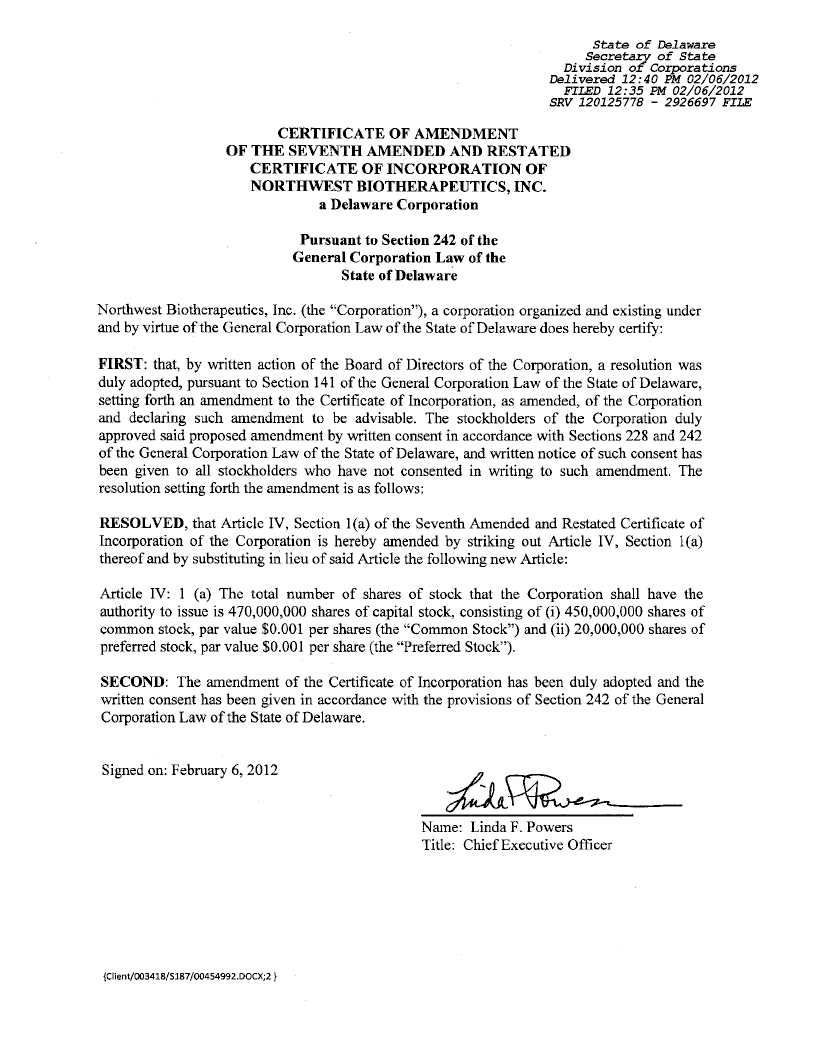

| *3.1 | Certificate of Amendment of the Seventh Amended and Restated Certificate of Incorporation of Northwest Biotherapeutics, Inc. | |

| *31.1 | Certification of President (Principal Executive Officer and Principal Financial and Accounting Officer), Pursuant to Exchange Act Rules 13a-14(a) and 15d-14(a), as Adopted Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. | |

| *32.1 | Certification of President, Chief Executive Officer and Principal Financial and Accounting Officer Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. |

| * | Filed herewith. |

| 21 |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| NORTHWEST BIOTHERAPEUTICS, INC | ||

| Dated: May 18, 2012 | By: | /s/ Linda M. Powers |

| Name: Linda M. Powers | ||

| Title: President and Chief Executive Officer | ||

| Principal Executive Officer | ||

| Principal Financial and Accounting Officer | ||

| 22 |

NORTHWEST BIOTHERAPEUTICS, INC.

(A Development Stage Company)

EXHIBIT INDEX

| *3.1 | Certificate of Amendment of the Seventh Amended and Restated Certificate of Incorporation of Northwest Biotherapeutics, Inc. | |

| *31.1 | Certification of President (Principal Executive Officer and Principal Financial and Accounting Officer), Pursuant to Exchange Act Rules 13a-14(a) and 15d-14(a), as Adopted Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. | |

| *32.1 | Certification of President, Chief Executive Officer and Principal Financial and Accounting Officer Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. |

| * | Filed herewith. |

| 23 |

EXHIBIT 31.1

SECTION 302 CERTIFICATION

I, Linda M. Powers, certify that:

| (1) | I have reviewed this quarterly report on Form 10-Q of Northwest Biotherapeutics, Inc.; |

| (2) | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| (3) | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report; |

| (4) | I am responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)), and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15 (f)), for the registrant and have: |

| (a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

| (b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

| (c) | Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and |

| (d) | Disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal quarter (the registrant’s fourth fiscal quarter in the case of an annual report) that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and |

| (5) | I have disclosed, based on my most recent evaluation of internal control over financial reporting, to the registrant’s auditors and the audit committee of the registrant’s Board of Directors (or persons performing the equivalent functions): |

| (a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant’s ability to record, process, summarize and report financial information; and |

| (b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal control over financial reporting. |

| Date: May 18, 2012 | ||

| By: | /s/ Linda M. Powers | |

| Name: Linda M. Powers | ||

| Title: President and Chief Executive Officer | ||

| Principal Executive Officer | ||

| Principal Financial and Accounting Officer | ||

EXHIBIT 32.1

CERTIFICATION PURSUANT TO

18 U.S.C. SECTION 1350,

AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

In connection with the quarterly report of Northwest Biotherapeutics, Inc. (the “Company”) on Form 10-Q for the period ended March 31, 2012, as filed with the Securities and Exchange Commission (the “Report”), I, Linda M. Powers, certify, pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, that:

| (1) | The Report fully complies with the requirements of section 13(a) or 15(d) of the Securities Exchange Act of 1934; and |

| (2) | The information contained in the Report fairly presents, in all material respects, the financial condition and results of operations of the Company. |

| Date: May 18, 2012 | ||

| /s/ Linda M. Powers | ||

| Name: | Linda M. Powers | |

| Title: | President and Chief Executive Officer | |

| Principal Executive Officer | ||

| Principal Financial and Accounting Officer | ||