UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number

(Exact name of registrant as specified in its charter)

|

MARYLAND |

|

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

(Address and zip code of principal executive office)

REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE: (

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

|

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

|

|

|

|

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of "large accelerated filer", "accelerated filer", "smaller reporting company", and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

☒ |

|

Accelerated filer |

☐ |

|

Non-accelerated filer |

☐ |

|

Smaller reporting company |

|

|

Emerging growth company |

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.). Yes

The aggregate market value of the shares of the registrant's Common Stock held by non-affiliates was approximately $

DOCUMENTS INCORPORATED BY REFERENCE:

CORECIVIC, INC.

FORM 10-K

For the fiscal year ended December 31, 2019

TABLE OF CONTENTS

|

Item No. |

|

Page |

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

5 |

|

|

|

5 |

|

|

|

Operating Procedures and Offender Services for Correctional, Detention, and Residential |

7 |

|

|

11 |

|

|

|

13 |

|

|

|

16 |

|

|

|

27 |

|

|

|

32 |

|

|

|

34 |

|

|

|

35 |

|

|

|

36 |

|

|

|

36 |

|

|

1A. |

37 |

|

|

1B. |

58 |

|

|

2. |

58 |

|

|

3. |

59 |

|

|

4. |

59 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of |

60 |

|

|

60 |

|

|

|

60 |

|

|

|

60 |

|

|

6. |

60 |

|

|

7. |

Management's Discussion and Analysis of Financial Condition and Results of Operations |

62 |

|

|

62 |

|

|

|

64 |

|

|

|

68 |

|

|

|

81 |

|

|

|

86 |

|

|

|

86 |

|

|

7A. |

87 |

|

|

8. |

87 |

|

|

9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

87 |

|

9A. |

87 |

|

|

9B. |

90 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10. |

91 |

|

|

11. |

91 |

|

|

12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

91 |

|

13. |

Certain Relationships and Related Party Transactions and Director Independence |

92 |

|

14. |

92 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15. |

93 |

|

|

16. |

96 |

|

|

|

97 |

2

CAUTIONARY STATEMENT REGARDING

FORWARD-LOOKING INFORMATION

This Annual Report on Form 10-K, or Annual Report, contains statements as to our beliefs and expectations of the outcome of future events that are forward-looking statements as defined within the meaning of the Private Securities Litigation Reform Act of 1995, as amended. All statements other than statements of current or historical fact contained in this Annual Report, including statements regarding our future financial position, business strategy, budgets, projected costs and plans, and objectives of management for future operations, are forward-looking statements. The words "anticipate," "believe," "continue," "could," "estimate," "expect," "intend," "may," "plan," "projects," "will," and similar expressions, as they relate to us, are intended to identify forward-looking statements. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made in this Annual Report. These include, but are not limited to, the risks and uncertainties associated with:

|

|

• |

general economic and market conditions, including, but not limited to, the impact governmental budgets can have on our contract renewals and renegotiations, per diem rates, and occupancy; |

|

|

• |

fluctuations in our operating results because of, among other things, changes in occupancy levels, competition, contract renegotiations or terminations, increases in costs of operations, fluctuations in interest rates, and risks of operations; |

|

|

• |

changes in the privatization of the corrections and detention industry, the acceptance of our services, the timing of the opening of new facilities, and the commencement of new management contracts (including the extent and pace at which new contracts are utilized), as well as our ability to utilize available beds; |

|

|

• |

our ability to obtain and maintain correctional, detention, and residential reentry facility management contracts because of reasons including, but not limited to, sufficient governmental appropriations, contract compliance, negative publicity and effects of inmate disturbances; |

|

|

• |

increases in costs to develop or expand real estate properties that exceed original estimates, or the inability to complete such projects on schedule as a result of various factors, many of which are beyond our control, such as weather, labor conditions, cost inflation, and material shortages, resulting in increased construction costs; |

|

|

• |

changes in government policy, legislation and regulations that affect utilization of the private sector for corrections, detention, and residential reentry services, in general, or our business, in particular, including, but not limited to, the continued utilization of the South Texas Family Residential Center by U.S. Immigration and Customs Enforcement, or ICE, under terms of the current contract, and the impact of any changes to immigration reform and sentencing laws. (Our company does not, under longstanding policy, lobby for or against policies or legislation that would determine the basis for, or duration of, an individual's incarceration or detention.); |

|

|

• |

our ability to successfully identify and consummate future acquisitions and our ability to successfully integrate the operations of our completed acquisitions and realize projected returns resulting therefrom; |

|

|

• |

our ability to meet and maintain qualification for taxation as a real estate investment trust, or REIT; and |

|

|

• |

the availability of debt and equity financing on terms that are favorable to us, or at all. |

Any or all of our forward-looking statements in this Annual Report may turn out to be inaccurate. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy, and financial needs. Our statements can be affected by inaccurate assumptions we might make or by known or unknown risks, uncertainties and assumptions, including the risks, uncertainties, and assumptions described in "Risk Factors" included elsewhere in this Annual Report and in other reports, documents, and other information we file with the Securities and Exchange Commission, or the SEC, from time to time.

3

In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this Annual Report may not occur and actual results could differ materially from those anticipated or implied in the forward-looking statements. When you consider these forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this Annual Report, including in "Management's Discussion and Analysis of Financial Condition and Results of Operations," "Business" and "Risk Factors."

Our forward-looking statements speak only as of the date made. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or circumstances or otherwise, except as required by law. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained in this Annual Report.

4

PART I.

|

ITEM 1. |

BUSINESS. |

Overview

We are a diversified government solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. Through three segments, CoreCivic Safety, CoreCivic Community, and CoreCivic Properties, we provide a broad range of solutions to government partners that serve the public good through corrections and detention management, a growing network of residential reentry centers to help address America's recidivism crisis, and government real estate solutions. We have been a flexible and dependable partner for government for more than 35 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good.

Structured as a REIT, we are the nation's largest owner of partnership correctional, detention, and residential reentry facilities and one of the largest prison operators in the United States. We also believe we are the largest private owner of real estate used by U.S. government agencies. As of December 31, 2019, through our CoreCivic Safety segment, we operated 50 correctional and detention facilities, 43 of which we owned, with a total design capacity of approximately 73,000 beds. Through our CoreCivic Community segment, we owned and operated 29 residential reentry centers with a total design capacity of approximately 5,000 beds. In addition, through our CoreCivic Properties segment, we owned 28 properties for lease to third parties and used by government agencies, totaling 2.4 million square feet.

In addition to providing fundamental residential services, our correctional, detention, and residential reentry facilities offer a variety of rehabilitation and educational programs, including basic education, faith-based services, life skills and employment training, and substance abuse treatment. These services are intended to help reduce recidivism and to prepare offenders for their successful reentry into society upon their release. We also provide or make available to offenders certain health care (including medical, dental, and mental health services), food services, and work and recreational programs.

We are a Maryland corporation formed in 1983. Our principal executive offices are located at 5501 Virginia Way, Brentwood, Tennessee, 37027, and our telephone number at that location is (615) 263-3000. Our website address is www.corecivic.com. We make our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, definitive proxy statements, and amendments to those reports under the Securities Exchange Act of 1934, as amended, or the Exchange Act, available on our website, free of charge, as soon as reasonably practicable after these reports are filed with or furnished to the SEC. Information contained on our website is not part of this Annual Report.

We began operating as a REIT effective January 1, 2013. We provide services and conduct other business activities through taxable REIT subsidiaries, or TRSs. A TRS is a subsidiary of a REIT that is subject to applicable corporate income tax and certain qualification requirements. Our use of TRSs enables us to comply with REIT qualification requirements while providing correctional services at facilities we own and at facilities owned by our government partners and to engage in certain other business operations. A TRS is not subject to the distribution requirements applicable to REITs so it may retain income generated by its operations for reinvestment.

As a REIT, we generally are not subject to federal income taxes on our REIT taxable income and gains that we distribute to our stockholders, including the income derived from our real estate and dividends we earn from our TRSs. However, our TRSs will be required to pay income taxes on their earnings at regular corporate income tax rates.

As a REIT, we generally are required to distribute annually to our stockholders at least 90% of our REIT taxable income (determined without regard to the dividends paid deduction and excluding net capital gains). Our REIT taxable income will not typically include income earned by our TRSs except to the extent our TRSs pay dividends to the REIT.

5

Our ongoing operations are organized into three principal business segments:

|

|

• |

CoreCivic Safety segment, consisting of the 50 correctional and detention facilities that are owned, or controlled via a long-term lease, and managed by CoreCivic, as well as those correctional and detention facilities owned by third parties but managed by CoreCivic. CoreCivic Safety also includes the operating results of our subsidiary that provides transportation services to governmental agencies, TransCor America, LLC, or TransCor. |

|

|

• |

CoreCivic Community segment, consisting of the 29 residential reentry centers that are owned, or controlled via a long-term lease, and managed by CoreCivic. CoreCivic Community also includes the operating results of our electronic monitoring and case management services. |

|

|

• |

CoreCivic Properties segment, consisting of the 28 real estate properties owned by CoreCivic for lease to third parties and used by government agencies. |

For the years ended December 31, 2019, 2018, and 2017, our total facility net operating income, which we define as a facility's revenues less operating expenses, was divided among our three business segments as follows:

|

|

|

For the Years Ended December 31, |

|

|||||||||

|

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|||

|

Segment: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Safety |

|

|

85.2 |

% |

|

|

87.1 |

% |

|

|

90.0 |

% |

|

Community |

|

|

5.0 |

% |

|

|

4.8 |

% |

|

|

4.4 |

% |

|

Properties |

|

|

9.8 |

% |

|

|

8.1 |

% |

|

|

5.6 |

% |

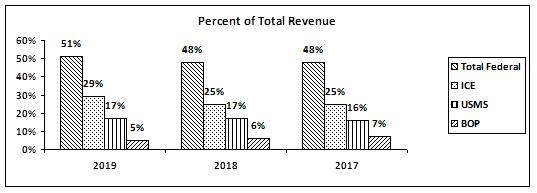

Our customers primarily consist of federal, state, and local government agencies. Federal correctional and detention authorities primarily consist of ICE, the United States Marshals Service, or the USMS, and the Federal Bureau of Prisons, or the BOP. Payments by federal correctional and detention authorities represented 51%, 48%, and 48% of our total revenue for the years ended December 31, 2019, 2018, and 2017, respectively.

Our customer contracts for providing bed capacity and correctional, detention, and residential reentry services in our CoreCivic Safety and CoreCivic Community segments typically have terms of three to five years and contain multiple renewal options. Most of our facility contracts also contain clauses that allow the government agency to terminate the contract at any time without cause, and our facility contracts are generally subject to annual or bi-annual legislative appropriations of funds. Notwithstanding these termination clauses, the contract renewal rate for properties we owned and operated in these segments was 94% over the five years ended December 31, 2019. The government lease agreements in our CoreCivic Properties segment typically have terms of five to twenty years including renewal options, and generally have more restrictive termination clauses. At December 31, 2019, the lease agreements in our CoreCivic Properties segment had a weighted average lease term of 4.2 years remaining.

In our CoreCivic Safety and CoreCivic Community segments, we are compensated for providing bed capacity and correctional, detention, and residential reentry services at a per diem rate based upon actual or minimum guaranteed occupancy levels. Occupancy rates for a particular facility are typically low when first opened or immediately following an expansion. However, beyond the start-up period, which typically ranges from 90 to 180 days, the occupancy rate tends to stabilize. The average compensated occupancy of our correctional, detention, and residential reentry facilities, based on rated capacity was as follows for the years 2019, 2018, and 2017:

|

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|||

|

CoreCivic Safety facilities |

|

|

82 |

% |

|

|

81 |

% |

|

|

80 |

% |

|

CoreCivic Community facilities |

|

|

76 |

% |

|

|

80 |

% |

|

|

80 |

% |

|

Total |

|

|

82 |

% |

|

|

81 |

% |

|

|

80 |

% |

The average compensated occupancy of our CoreCivic Safety and CoreCivic Community facilities, excluding idled facilities, was 93%, 93%, and 91% for the years 2019, 2018, and 2017, respectively.

6

In our CoreCivic Properties segment, we own properties for lease to third parties and used by government agencies where our occupancy percentage is based on leased square feet rather than bed capacity. The average occupancy of these facilities was as follows for the years 2019, 2018, and 2017:

|

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|||

|

Leased portfolio |

|

|

99 |

% |

|

|

100 |

% |

|

|

100 |

% |

Operating Procedures and Offender Services for Correctional, Detention, and Residential Reentry Facilities

Pursuant to the terms of our customer contracts, we are responsible for the overall operations of our facilities, including staff recruitment, general administration of the facilities, facility maintenance, security, and supervision of the offenders. We are required by our customer contracts to maintain certain levels of insurance coverage for general liability, workers' compensation, vehicle liability, and property loss or damage. We also are required to indemnify our customers for claims and costs arising out of our operations and, in certain cases, to maintain performance bonds and other collateral requirements.

Reentry programs.

We believe a focus on inmate reentry provides great benefits for our communities – more people living healthy and productive lives and contributing to strong families and local economies. We have committed to evolving our model with an increased focus on reentry services, and we are working hard to equip the men and women in our care with the services, support, and resources they need to be successful upon reentry.

We provide a wide range of evidence-based reentry programs and activities in our facilities. At most of the facilities we manage, offenders have the opportunity to enhance their basic education from literacy through earning a high school equivalency diploma endorsed by their respective state. In some cases, we also provide opportunities for postsecondary educational achievements and chances to participate in college degree programs. A number of our facilities that care for non-U.S. citizens offer adult education curricula recognized by several nations to which these offenders may return, including a curriculum offered in conjunction with the Mexican government. We also provide the Adult Education in Spanish program for offenders with that specific language need.

For the offenders who are close to taking their high school equivalency exam (either the GED or the HiSET), we have invested in the equipment needed to use the GED/HiSET Academy software program, which is an offline software program providing over 200 hours of individualized lessons up to the 12th grade. The GED/HiSET Academy incorporates teaching best practices and provides an atmosphere to engage and motivate students to learn everything they need to know to pass the GED/HiSET exam. As an example of the impact we are having, during 2019, the number of offenders in our facilities who passed high school equivalency exams totaled 1,376. According to research from the independent RAND Corporation, "Evaluating the Effectiveness of Correctional Education" published in 2013, inmates who obtain GEDs while in prison are 30% less likely to return to prison.

In addition, we offer a broad spectrum of career/technical education opportunities to help individuals learn marketable job skills. Our trade programs are certified by the National Center for Construction Education and Research, or NCCER. NCCER establishes the curriculum and certification for over 4,000 construction and trade organizations. Graduates of these programs enter the job market with certified skills that significantly enhance employability. According to research conducted by the RAND Corporation published in 2013, inmates who complete vocational training are 28% more likely to find a job after release. During 2019, 5,136 offenders in facilities we manage earned career and technical education certificates.

We are proud of the educational programs we offer and intend to maintain and continue to develop such programs. Examples of programs we've recently offered include:

7

|

|

• |

In 2019, we partnered with Persevere, a national non-profit organization, to offer offenders at our Trousdale Turner facility in Tennessee an opportunity to learn software coding and job readiness/employability skills specific to the technology field. The instructor-led, self-paced program utilizes both a coding instructor and a Technology Employability Specialist to ensure students are learning the craft and how to obtain and maintain a job in the field, post-incarceration. Additionally, the program is split into two phases that allows students to become certified Front-end Developers (phase 1) and Full Stack Developers (phase 2) upon completion. |

|

|

• |

In 2019, we increased our post-secondary educational offerings by growing our relationship with Ashland University, based in Ohio, to deliver college-level programming to offenders at our Jenkins, Wheeler, and Coffee correctional facilities in Georgia. This relationship allows enrollees to obtain an Associate's Degree in General Studies or a Bachelor's Degree in Communication Studies or Interdisciplinary Studies at no cost to them through Pell Grant funding. Students access coursework, tests, and interact with their instructors through a secure Learning Management System via a tablet computer. |

|

|

• |

In late 2019, we launched a NCCER plumbing program at our Metro-Davidson County facility in Nashville, Tennessee in conjunction with a regional company in Tennessee that offers comprehensive services, including HVAC, plumbing, and electrical. The program is taught once a week by an instructor of the service company and we provide the space and materials. Upon completion of the plumbing program and release from the Metro-Davidson County facility, some of the students will be interviewed for placement in the service company's four-year training and leadership program in order for them to complete programming and become an apprentice plumber with the service company. |

|

|

• |

In 2018, through a relationship with Fuel Education, a company that specializes in digital learning opportunities, we began offering an online Information Support and Services computer program at our Lee Adjustment Center in Kentucky. This program allows students to enhance their computer knowledge and was developed in coordination with the Commonwealth of Kentucky Department of Corrections, or KYDOC, our government partner at the Lee facility. Students who successfully complete the approximate 10-month program will be awarded a base National Occupational Competency Testing Institute, or NOCTI, credential with the opportunity to earn an advanced NOCTI credential in the future. |

|

|

• |

In 2016, our Coffee and Wheeler facilities in Georgia implemented state-of-the-art Diesel Maintenance and Welding programs in coordination with the Georgia Department of Corrections, enabling students to earn trade certificates from nearby community colleges. As of December 31, 2019, these programs graduated 50 from the Diesel Maintenance program and 83 from the Welding program. |

For those with assessed substance use disorders, we offer cognitive behavioral evidence-based treatment programs with proven clinical outcomes, such as the Residential Drug Abuse Program. We offer both therapeutic community models and intensive outpatient programs. We also offer drug and alcohol use education/DWI programs at some of our locations. Our goal in providing substance use treatment is to stimulate internal motivation for change and progress through the stages of change so that lasting behavioral change can occur. Our drug and alcohol education programs help participants understand their relationships with drugs and alcohol and the links between drug and alcohol use and crime, as well as assisting them in making better choices that can lead to healthier relationships in their lives. According to a study by the Florida State University College of Criminology and Criminal Justice, "An Assessment of Substance Abuse Treatment Programs in Florida's Prisons Using a Random Assignment Experimental Design" submitted to the National Institute of Justice, Office of Justice Programs, U.S. Department of Justice in 2016, inmates who completed addiction treatment in prison have significantly lower recidivism levels regardless of the treatment model used. In 2019, 1,900 offenders in our care completed substance use disorder programming.

8

Additional program offerings include our Victim Impact Programs, available at a number of our facilities, which seek to educate offenders about the negative effects their criminal conduct can have on others. Currently, 24 of our facilities have received training to offer Victim Impact Programs to offenders at both Safety and Community sites. In 2019, 1,247 offenders successfully completed Victim Impact Programs. All of our facility chaplains facilitate diverse and inclusive opportunities for those in our care to engage in the practice of spirituality and to exercise individual religious freedom. In several facilities, we offer faith-based programs with an emphasis on character development, spiritual growth, and successful reentry. Presently, we utilize Threshold, as an innovative, evidence-based inter-faith component of comprehensive reentry services. In 2019, 721 offenders in our care successfully completed the Threshold program.

Our Reentry and Life Skills programs prepare individuals for life after incarceration by teaching them how to successfully conduct a job search, how to manage their budget and financial matters, parenting skills, and relationship and family skills. Equally significant, we offer cognitive behavioral programs aimed at changing anti-social attitudes and behaviors in offenders, with a focus on altering the level of criminal thinking. In 2017, we introduced a comprehensive reentry strategy we call "Go Further", a forward thinking, process approach to reentry. "Go Further" encompasses all facility reentry programs, adds a proprietary cognitive/behavioral curriculum, and encourages staff and offenders to take a collaborative approach to assist in reentry preparation. "Go Further" is currently in place in 21 of our facilities, with plans to add additional facilities in 2020. In 2019, offenders in our care completed 5,355 cognitive/behavioral evidence-based journals in preparation for returning to their communities.

Across the country, our dedicated staff, along with the assistance of thousands of volunteers, work to provide guidance, direction, and post-incarceration services to the men and women in our care. We believe these critical reentry programs help fight the serious challenge of recidivism facing the United States.

Through our community corrections facilities, we provide an array of services to defendants and offenders who are serving their full sentence, the last portion of their sentence, waiting to be sentenced, or awaiting trial while supervised in a community environment. We offer housing and programs with a key focus on employment, job readiness, life skills and various substance abuse treatment programs, in order to help offenders successfully reenter their communities and reduce the risk of recidivism. In some of our community corrections facilities, we offer housing and program services to parolees who have completed their sentence but lack a viable reentry plan. Through a focus on employment and skill development, we provide a means for these parolees to successfully reintegrate into their communities.

In addition, we provide day-reporting and substance abuse treatment programs at some of our community corrections facilities. These programs, depending on the needs of the offender, can provide cognitive behavioral-based programs to assist in the offender's successful reentry while holding the individual accountable while living in the community.

9

Lastly, we also provide a number of non-residential correctional alternative services, including electronic monitoring and case management services, under our CoreCivic Community segment. Governmental customers use electronic monitoring products and services to monitor low risk offenders as a way to help reduce overcrowding in correctional facilities, as a monitoring and sanctioning tool, and to promote public safety by imposing restrictions on movement and serving as a deterrent for alcohol usage. Providing these non-residential services is a natural complement to our broad network of residential reentry facilities and can help keep individuals from going back to prison or being incarcerated in the first place.

Ultimately, the work we do is intended to give people the tools to reintegrate with their communities permanently. We are proud of the teachers, counselors, case managers, chaplains, and other offender support service professionals who provide these services to the men and women entrusted in our care.

To further underscore our long-term commitment to reducing recidivism, in October 2017, we announced that we launched a nationwide initiative to advocate for a range of government policies that will help former offenders successfully reenter society and stay out of prison. We believe that as successful as we may be with our work inside our facilities, offenders still face embedded societal barriers when they return to their communities. Supporting recidivism-reducing policies is one way we can bridge the gap and give the men and women entrusted in our care a better opportunity at never returning to prison. As part of the initiative, we apply government relations resources and expertise to advocate for the following policies:

|

|

• |

"Ban-the-Box" proposals to help improve former inmates' chances at getting a job; |

|

|

• |

Reduced legal barriers to make it easier and less risky for companies to hire former inmates; |

|

|

• |

Increased funding for reentry programs in areas such as education, addiction treatment, faith-based offerings, victim impact and post-release employment; and |

|

|

• |

Social impact bond pilot programs that tie contractor payments to positive outcomes. |

Operating guidelines.

The American Correctional Association, or ACA, is an independent organization comprised of corrections professionals that establishes accreditation standards for correctional and detention facilities around the world. Outside agency standards, such as those established by the ACA, provide us with the industry's most widely accepted operational guidelines. ACA accredited facilities must be audited and re-accredited at least every three years. We have sought and received ACA accreditation for 38, or approximately 95%, of the eligible facilities we operated as of December 31, 2019, excluding our residential reentry facilities and our Eden Detention Center and our Torrance County Detention Facility. We have not yet sought accreditation at the previously idled Eden and Torrance facilities because they were only recently activated, although we currently intend to pursue accreditation. During 2019, 14 of the facilities we manage were re-accredited by the ACA with an average score of 99.6%, making our portfolio average 99.6%.

Beyond the standards provided by the ACA, our facilities are operated in accordance with a variety of company and facility-specific policies and procedures, as well as various contractual requirements. Many of these policies and procedures reflect the high standards generated by a number of sources, including the ACA, the National Commission on Correctional Healthcare, the Occupational Safety and Health Administration, as well as federal, state, and local government codes and regulations and longstanding correctional procedures.

In addition, our facilities are operated in compliance with the Prison Rape Elimination Act, or PREA, standards, which became effective in August 2013. All confinement facilities covered under the PREA standards must be audited at least every three years to maintain compliance with the PREA standards. Covered facilities include adult prisons and jails, juvenile facilities, lockups (facilities housing detainees overnight), and community confinement facilities, whether operated by the United States Department of Justice, or DOJ, or by a state, local, corporate, or nonprofit authority. We utilize DOJ-certified PREA auditors to help ensure that all facilities operate in compliance with applicable PREA regulations.

10

Our facilities operate under these established standards, policies, and procedures, and also are subject to annual audits by our Quality Assurance Division, or QAD, which operates under, and reports directly to, our Office of General Counsel and independently from our Operations Division. Through the QAD, we have devoted significant resources to ensuring that our facilities meet outside agency and accrediting organization standards and guidelines.

The QAD employs a team of full-time auditors, who are subject matter experts from all major disciplines within institutional operations. Annually, without advance notice, QAD auditors conduct on-site evaluations of each CoreCivic Safety facility we operate using specialized audit tools, typically containing more than 1,000 audit indicators across all major operational areas. In most instances, these audit tools are tailored to facility and partner specific requirements. In addition, audit teams provide guidance to facility staff on operational best practices and assist staff with addressing specific areas of need, such as meeting requirements of new partner contracts and providing detailed training on compliance requirements for new departmental managers.

The QAD management team coordinates overall operational auditing and compliance efforts across all correctional, detention, and residential reentry facilities we manage. In conjunction with subject matter experts and other stakeholders having risk management responsibilities, the QAD management team develops performance measurement tools used in facility audits. The QAD management team provides governance of the corrective action plan process for any items of nonconformance identified through internal and external facility reviews. Our QAD also contracts with teams of ACA certified correctional auditors to evaluate compliance with ACA standards at accredited facilities. Similarly, the QAD routinely incorporates a review of facility compliance with key PREA regulations during annual audits of company facilities.

In addition to our own internal audit and contract compliance efforts, we are also subject to oversight by our government partners. As part of their standard monitoring and compliance programs, approximately 70% of our federal and state government partners conduct formal contract-compliance audits and inspections at least annually at CoreCivic Safety facilities. In addition to these annual audits of our facilities, many partners conduct additional area-specific operational audits and inspections on a more frequent basis, including monthly, quarterly, and semi-annually. Some of these audits and facility inspections by our partners are conducted on an unannounced basis. In 2019, our government partners conducted over 230 annual, semi-annual, quarterly, and monthly compliance audits and inspections at our CoreCivic Safety facilities. In addition, the majority of our federal and state government partners employ on-site contract monitors who monitor performance and contract compliance at our facilities on a full- or part-time basis. In 2019, approximately 84% of the CoreCivic Safety facilities we manage have an onsite contract monitor.

Business Development

We believe we own, or control via a long-term lease, approximately 58% of all privately owned prison beds in the United States, manage nearly 39% of all privately managed prison beds in the United States, and are currently the second largest private owner and provider of community corrections services in the nation. We also believe that we are the largest private owner of real estate used by U.S. government agencies. Under the direction of our partnership development department, we market our facilities and services to government agencies responsible for federal, state, and local correctional, detention, and residential reentry facilities in the United States. Under the direction of our real estate department, we intend to continue pursuing the acquisition and development of additional correctional, detention, and residential reentry facilities, as well as other government-leased real estate assets with a bias toward those used to provide mission-critical governmental services that we believe have a favorable investment return, diversify our cash flows, and increase value to our stockholders.

We execute cross-departmental efforts to market CoreCivic Safety solutions to government partners that seek corrections and detention management services, CoreCivic Community solutions to government partners seeking residential reentry services, and CoreCivic Properties solutions to customers that need real estate and maintenance services.

As indicated by the following chart, business from our federal customers, including primarily ICE, the USMS, and the BOP, continues to be a significant component of our business, although the source of revenue is derived from many contracts at various types of properties, i.e. correctional, detention, reentry, and leased. ICE and the USMS each accounted for 10% or more of our total revenue during the last three years.

11

Certain of our contracts with federal partners contain clauses that guarantee the federal partner access to a minimum bed capacity in exchange for a fixed monthly payment. However, these contracts also generally provide the government the ability to cancel the contract for non-appropriation of funds or for convenience. The solutions we provide to our federal customers continue to be a significant component of our business. We believe our ability to provide flexible solutions and fulfill emergent needs of our federal customers would be very difficult and costly to replicate in the public sector.

State revenues from contracts at correctional, detention, and residential reentry facilities that we operate constituted 34%, 39%, and 41% of our total revenue during 2019, 2018, and 2017, respectively, and decreased 4.7% from $706.8 million during 2018 to $673.4 million during 2019, largely due to declines in populations from the state of California, as further described in Management's Discussion and Analysis of Financial Condition and Results of Operations. No state partner accounted for 10% or more of our total revenue during these years.

Several of our state partners have experienced improvements in their budgets which has helped us secure recent per diem increases at certain facilities. Further, several of our existing state partners, as well as prospective state partners, are experiencing growth in offender populations and overcrowded conditions, are considering alternative correctional capacity for their aged and inefficient infrastructure, or are seeking cost savings by utilizing the private sector. Although we can provide no assurance that we will enter into any new contracts, we believe we are well positioned to provide states with needed bed capacity, as well as the programming and reentry services they are seeking. Since the beginning of 2018, we have completed the intake of new inmate populations as a result of new contracts with Kansas, Kentucky, Ohio, Nevada, South Carolina, and Vermont, while Wyoming began utilizing an existing contract it had not utilized in nearly a decade. In January 2020, we signed a new management contract with Mississippi.

We believe the long-term growth opportunities of our business remain attractive as government agencies consider their emergent needs, as well as the efficiency and offender programming opportunities we provide, as flexible solutions to satisfy our partners' needs. Further, we expect our partners to continue to face challenges in maintaining old facilities, developing new facilities, and expanding current facilities for additional capacity, which could result in increased future demand for the solutions we provide.

We believe that we can further develop our business by, among other things:

|

|

• |

Maintaining and expanding our existing customer relationships and filling existing beds within our facilities, while maintaining an adequate inventory of available beds that we believe provides us with flexibility and a competitive advantage when bidding for new management contracts; |

|

|

• |

Enhancing the terms of our existing contracts and expanding the services we provide under those contracts; |

|

|

• |

Pursuing additional opportunities to lease our facilities to government and other third-party operators in need of correctional, detention, and residential reentry capacity; |

|

|

• |

Pursuing mission-critical real estate solutions for government agencies including, but not limited to, corrections and detention real estate assets; |

12

|

|

• |

Pursuing other asset acquisitions and business combinations through transactions with non-government third parties; |

|

|

• |

Maintaining and expanding our focus on community corrections and reentry programming that align with the needs of our government partners; |

|

|

• |

Pursuing additional opportunities that expand the scope of non-residential correctional alternative solutions we provide to government agencies; and |

|

|

• |

Establishing relationships with new customers that have either previously not outsourced their correctional facility management needs or have utilized other private enterprises. |

We generally receive inquiries from or on behalf of government agencies that are considering outsourcing the ownership and/or management of certain facilities or that have already decided to contract with a private enterprise. When we receive such an inquiry, we determine whether there is an existing need for our correctional, detention, and residential reentry facilities and/or services and whether the legal and political climate in which the inquiring party operates is conducive to serious consideration of outsourcing. Based on these findings, an initial cost analysis is conducted to further determine project feasibility.

Frequently, government agencies responsible for correctional, detention, and residential reentry facilities and services procure space and services through solicitations or competitive procurements. As part of our process of responding to such requests, members of our management team meet with the appropriate personnel from the agency making the request to best determine the agency's needs. If the project fits within our strategy, we submit a written response. A typical solicitation or competitive procurement requires bidders to provide detailed information, including, but not limited to, the space and services to be provided by the bidder, its experience and qualifications, and the price at which the bidder is willing to provide the facility and services (which services may include the purchase, renovation, improvement or expansion of an existing facility or the planning, design and construction of a new facility). The requesting agency selects a provider believed to be able to provide the requested bed capacity, if needed, and most qualified to provide the requested services, and then negotiates the price and terms of the contract with that provider.

2019 Accomplishments

In 2019, we entered into a number of new contracts, renewed several other significant contracts, and completed numerous other transactions and milestones, including the following:

CoreCivic Safety:

|

|

• |

1,376 offenders in our care passed high school equivalency exams, 5,136 earned career and technical education certificates, 1,900 completed substance use disorder programming, 1,247 completed Victim Impact Programs, 721 completed the Threshold program, and 5,355 completed cognitive/behavioral evidence-based journals in our "Go Further" program in preparation for successfully returning to their communities. |

13

|

|

• |

Increased our post-secondary educational offerings by growing our relationship with Ashland University, based in Ohio, to deliver college-level programming to offenders at our Jenkins, Wheeler, and Coffee facilities in Georgia. This relationship allows enrollees to obtain an Associate's Degree in General Studies or Bachelor's Degree in Communication Studies or Interdisciplinary Studies at no cost to them through Pell Grant funding. |

|

|

• |

Introduced a new computer coding program at our Trousdale Turner Correctional Center in Hartsville, Tennessee. The program is offered by Persevere, a national nonprofit organization, and provides an opportunity for those in our care at the facility to learn software coding and job readiness/employability skill specific to the technology field. Students participating in the new program take classes and earn industry certifications, which helps prepare them to find and maintain jobs in the technology field, post-incarceration. |

|

|

• |

Executed a new contract with ICE to care for up to 2,348 adult detainees at our Adams County Correctional Center in Mississippi. The new management contract has an initial term of 60 months, with unlimited extension options thereafter upon mutual agreement. |

|

|

• |

Executed a new contract with ICE to activate our 910-bed Torrance County Detention Facility in New Mexico. The Torrance facility had previously been idle since 2017. The new management contract has an initial term of 60 months, with unlimited extension options thereafter upon mutual agreement. |

|

|

• |

Executed a new contract with the USMS to activate our 1,422-bed Eden Detention Center in Texas. The Eden facility had previously been idle since 2017. The new management contract, which also permits ICE to utilize capacity at the facility at any time in the future, has an indefinite term. |

|

|

• |

Executed a new contract with the Kansas Department of Corrections, or KDOC, to care for offenders at our Saguaro Correctional Facility. The new management contract has an initial term of one year, with two additional one-year extension options upon mutual agreement. The new contract with the KDOC also provides that, upon mutual agreement, we may transfer offenders held under the contract to another correctional facility that we operate. |

|

|

• |

Completed the $39.0 million, 512-bed expansion of our Otay Mesa Detention Center in California and extended the contract with the federal government through December 2034, including two five-year extension options. The expansion was a result of long-standing demand from the USMS and ICE, and limited detention capacity in the Southwest region of the United States. Both the USMS and ICE currently utilize the Otay Mesa facility under an existing contract that enables both agencies to utilize the additional capacity. |

14

CoreCivic Community:

|

|

• |

Completed the integration of Rocky Mountain Offender Management Systems, LLC into Recovery Monitoring Solutions Corporation, which provides non-residential correctional alternatives, including electronic monitoring and case management services, to municipal, county, and state governments in multiple states. This integration strengthens our focus on rehabilitation and recidivism and completes the spectrum of correctional services we offer to government agencies. |

|

|

• |

Completed the acquisition of the South Raleigh Reentry Center, a 60-bed residential reentry center in Raleigh, North Carolina. In connection with the acquisition, we provide reentry services for both male and female residents under custody of the BOP. |

|

|

• |

Completed the acquisition of certain assets of Rehabilitation Services, Inc., resulting in the addition of two residential reentry centers in Virginia. The Ghent Residential Reentry Center, a 36-bed residential reentry center in Norfolk, Virginia and the James River Residential Reentry Center, an 84-bed residential reentry center in Newport News, Virginia, provide reentry services for residents under custody of the BOP. The residential reentry facilities can also serve an additional 34 home confinement clients on behalf of the BOP. |

CoreCivic Properties:

|

|

• |

Completed the acquisition of a 37,000 square-foot office building in Detroit, Michigan that was built-to-suit for the state of Michigan's Department of Health and Human Services, or MDHHS, in 2002. The property is 100% leased to the Michigan Department of Technology, Management and Budget, or MDTMB, on behalf of MDHHS through June 2028, and includes one six-year renewal option at the sole discretion of the MDTMB. |

|

|

• |

Entered into a lease with the KYDOC for our previously idled 656-bed Southeast Correctional Complex in Wheelwright, Kentucky, formerly known as the Southeast Kentucky Correctional Facility. The lease is expected to commence in mid-2020 and has an initial term of ten years and includes five two-year renewal options. |

|

|

• |

Continued construction of the new Lansing Correctional Facility in Kansas, and in December 2019, began accepting offenders into the 512-bed minimum security complex ahead of schedule, with the remaining 1,920-bed medium/maximum security complex completed in January 2020. |

Corporate and Other:

|

|

• |

Issued our first Environmental, Social and Governance, or ESG, report which details how we are helping to tackle the national crisis of recidivism and provides quantified evidence of progress being made toward company-wide reentry goals. We are the first company in our industry to release an ESG report, demonstrating our commitment to transparency and accountability. |

|

|

• |

Partnered with other leaders in the private sector corrections and detention industry to launch the "Day 1 Alliance", or D1A, a newly formed trade and advocacy organization. The D1A is a unified voice dedicated to educating Americans on the small but valued role the private sector plays in addressing corrections and detention challenges in the United States. The D1A will not advocate on policies, regulations, or legislation that impact the basis for or duration of an individual's incarceration or detention. |

|

|

• |

Entered into a new $250.0 million Senior Secured Term Loan B, or Term Loan B, which bears interest at the London Interbank Offered Rate, or LIBOR, plus 4.50%, with a 1.00% LIBOR floor (or, at our option, a base rate plus 3.50%), and has a five-year maturity. Proceeds from the issuance of the Term Loan B were used to partially fund the early redemption of the $325.0 million in aggregate principal amount of 4.125% senior notes due in April 2020, or the 4.125% Senior Notes. |

15

Facility Portfolio

CoreCivic Safety and Community Facilities and Facility Management Contracts

Our correctional, detention, and residential reentry facilities can generally be classified according to the level(s) of security at such facility. Minimum security facilities have open housing within an appropriately designed and patrolled institutional perimeter. Medium security facilities have either cells, rooms or dormitories, a secure perimeter, and some form of external patrol. Maximum security facilities have cells, a secure perimeter, and external patrol. Multi-security facilities have various areas encompassing minimum, medium or maximum security.

Our CoreCivic Safety and Community facilities can also be classified according to their primary function. The primary functional categories are:

|

|

• |

Correctional Facilities. Correctional facilities care for and provide contractually agreed upon programs and services to sentenced adult prisoners, typically prisoners on whom a sentence in excess of one year has been imposed. |

|

|

• |

Detention Facilities. Detention facilities care for and provide contractually agreed upon programs and services to (i) individuals being detained by ICE, (ii) individuals who are awaiting trial who have been charged with violations of federal criminal law (and are therefore in the custody of the USMS) or state criminal law, and (iii) prisoners who have been convicted of crimes and on whom a sentence of one year or less has been imposed. |

|

|

• |

Residential Facilities. Residential facilities provide space and residential services in an open and safe environment to adults with children who have been detained by ICE and are awaiting the outcome of immigration hearings. As contractually agreed upon, residential facilities offer services including, but not limited to, educational programs, medical care, recreational activities, counseling, and access to religious and legal services. |

|

|

• |

Community Corrections. Community corrections/residential reentry facilities offer housing and programs to offenders who are serving the last portion of their sentence or who have been assigned to the facility in lieu of a jail or prison sentence, with a key focus on employment, job readiness, and life skills. |

16

As of December 31, 2019, through our CoreCivic Safety segment, we operated 50 correctional and detention facilities, 43 of which we owned and managed and seven of which we managed, but were owned by our government partners. Through our CoreCivic Community segment, we also owned and managed 29 residential reentry centers. Owned and managed facilities include facilities placed into service that we own or control via a long-term lease and manage. The following table includes certain information regarding each facility, including the term of the primary customer contract related to such facility.

|

Facility Name |

|

Primary Customer |

|

|

Design Capacity (A) |

|

|

Security Level |

|

|

Facility Type (B) |

|

|

Term |

|

|

Remaining Renewal Options (C) |

|

||||||

|

CoreCivic Safety Facilities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Safety - Owned and Managed: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Central Arizona Florence Correctional Complex |

|

USMS |

|

|

|

4,128 |

|

|

Multi |

|

|

Detention |

|

|

Sep-23 |

|

|

(1) 5 year |

|

|||||

|

Florence, Arizona |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Eloy Detention Center |

|

ICE |

|

|

|

1,500 |

|

|

Medium |

|

|

Detention |

|

|

Indefinite |

|

|

|

— |

|

||||

|

Eloy, Arizona |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

La Palma Correctional Center |

|

ICE |

|

|

|

3,060 |

|

|

Multi |

|

|

Detention |

|

|

Indefinite |

|

|

|

— |

|

||||

|

Eloy, Arizona |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Red Rock Correctional Center (D) |

|

State of Arizona |

|

|

|

2,024 |

|

|

Medium |

|

|

Correctional |

|

|

Jul-26 |

|

|

(2) 5 year |

|

|||||

|

Eloy, Arizona |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Saguaro Correctional Facility |

|

State of Hawaii |

|

|

|

1,896 |

|

|

Multi |

|

|

Correctional |

|

|

Jun-20 |

|

|

(1) 1 year |

|

|||||

|

Eloy, Arizona |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leo Chesney Correctional Center |

|

|

— |

|

|

240 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

Live Oak, California |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Otay Mesa Detention Center |

|

ICE |

|

|

|

1,994 |

|

|

Minimum/ |

|

|

Detention |

|

|

Dec-24 |

|

|

(2) 5 year |

|

|||||

|

San Diego, California |

|

|

|

|

|

|

|

|

|

Medium |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Bent County Correctional Facility |

|

State of Colorado |

|

|

|

1,420 |

|

|

Medium |

|

|

Correctional |

|

|

Jun-20 |

|

|

|

— |

|

||||

|

Las Animas, Colorado |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Crowley County Correctional Facility |

|

State of Colorado |

|

|

|

1,794 |

|

|

Medium |

|

|

Correctional |

|

|

Jun-20 |

|

|

|

— |

|

||||

|

Olney Springs, Colorado |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Huerfano County Correctional Center |

|

|

— |

|

|

752 |

|

|

Medium |

|

|

Correctional |

|

|

|

— |

|

|

|

— |

|

|||

|

Walsenburg, Colorado |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Kit Carson Correctional Center |

|

|

— |

|

|

|

1,488 |

|

|

Medium |

|

|

Correctional |

|

|

|

— |

|

|

|

— |

|

||

|

Burlington, Colorado |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Coffee Correctional Facility (E) |

|

State of Georgia |

|

|

|

2,312 |

|

|

Medium |

|

|

Correctional |

|

|

Jun-20 |

|

|

(14) 1 year |

|

|||||

|

Nicholls, Georgia |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17

|

Facility Name |

|

Primary Customer |

|

|

Design Capacity (A) |

|

|

Security Level |

|

|

Facility Type (B) |

|

|

Term |

|

|

Remaining Renewal Options (C) |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Jenkins Correctional Center (E) |

|

State of Georgia |

|

|

|

1,124 |

|

|

Medium |

|

|

Correctional |

|

|

Jun-20 |

|

|

(15) 1 year |

|

|||||

|

Millen, Georgia |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

McRae Correctional Facility |

|

BOP |

|

|

|

1,978 |

|

|

Medium |

|

|

Correctional |

|

|

Nov-20 |

|

|

(1) 2 year |

|

|||||

|

McRae, Georgia |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stewart Detention Center |

|

ICE |

|

|

|

1,752 |

|

|

Medium |

|

|

Detention |

|

|

Indefinite |

|

|

|

— |

|

||||

|

Lumpkin, Georgia |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Wheeler Correctional Facility (E) |

|

State of Georgia |

|

|

|

2,312 |

|

|

Medium |

|

|

Correctional |

|

|

Jun-20 |

|

|

(14) 1 year |

|

|||||

|

Alamo, Georgia |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leavenworth Detention Center |

|

USMS |

|

|

|

1,033 |

|

|

Maximum |

|

|

Detention |

|

|

Dec-21 |

|

|

(1) 5 year |

|

|||||

|

Leavenworth, Kansas |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lee Adjustment Center |

|

Commonwealth of |

|

|

816 |

|

|

Multi |

|

|

Correctional |

|

|

Jun-20 |

|

|

(1) 1 year |

|

||||||

|

Beattyville, Kentucky |

|

Kentucky |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Marion Adjustment Center |

|

|

— |

|

|

826 |

|

|

Minimum/ |

|

|

Correctional |

|

|

|

— |

|

|

|

— |

|

|||

|

St. Mary, Kentucky |

|

|

|

|

|

|

|

|

|

Medium |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Prairie Correctional Facility |

|

|

— |

|

|

|

1,600 |

|

|

Medium |

|

|

Correctional |

|

|

|

— |

|

|

|

— |

|

||

|

Appleton, Minnesota |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adams County Correctional Center |

|

ICE |

|

|

|

2,232 |

|

|

Medium |

|

|

Detention |

|

|

Aug-24 |

|

|

Indefinite |

|

|||||

|

Adams County, Mississippi |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tallahatchie County Correctional Facility (F) |

|

USMS |

|

|

|

2,672 |

|

|

Multi |

|

|

Correctional |

|

|

Jun-20 |

|

|

Indefinite |

|

|||||

|

Tutwiler, Mississippi |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Crossroads Correctional Center (G) |

|

State of Montana |

|

|

664 |

|

|

Multi |

|

|

Correctional |

|

|

Jun-21 |

|

|

(1) 2 year |

|

||||||

|

Shelby, Montana |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nevada Southern Detention Center |

|

USMS |

|

|

|

1,072 |

|

|

Medium |

|

|

Detention |

|

|

Sep-20 |

|

|

(2) 5 year |

|

|||||

|

Pahrump, Nevada |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|