Blucora, Inc. 8-K

Exhibit 99.2

BUILDING LONG - TERM VALUE FOR SHAREHOLDERS March 2021 Privileged and Confidential Prepared at the Direction of Counsel Contains Input From Counsel for Purposes of Providing Legal Advice VoteBlucora.com DRAFT Subject to Completion

Important Information 2 Forward - Looking Statements T his presentation contains forward - looking statements within the meaning of Section 27 A of the Securities Act of 1933 , as amended, and Section 21 E of the Securities Exchange Act of 1934 , as amended , including statements with respect to the anticipated effects of the strategic plan of Blucora , Inc . (“ Blucora ” or the “ Company ”), expectations relating to the 2021 tax season, future marketing spend, expected cross - over opportunities between the Company’s two businesses and expectations with respect to any near - term sale of the Company’s Tax Preparation business . Forward - looking statements provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to any historical or current fact . Forward - looking statements can be identified by words such as “anticipates,” “believes,” “plans,” “expects,” “future,” “intends,” “may,” “will,” “would,” “could,” “should,” “estimates,” “predicts,” “potential,” “continues,” “target,” “outlook” and similar terms and expressions . Actual results may differ significantly from management’s expectations due to various risks and uncertainties including, but not limited to, the current COVID - 19 pandemic ; our ability to effectively implement our future business plans and growth strategy ; our ability to effectively compete within our industry ; our ability to attract and retain customers ; the availability of financing and our ability to meet our current and future debt service obligations and comply with our debt covenants ; our ability to generate strong investment performance for our customers and the impact of the financial markets on our customers’ portfolios ; political and economic conditions and events that directly or indirectly impact the wealth management and tax preparation industries ; our ability to attract and retain productive financial professionals ; our ability to successfully make technology enhancements and introduce new and improve on existing products and services ; our expectations concerning the revenues we generate from fees associated with the financial products that we distribute ; our ability to comply with laws and regulations, including, among others, those related to privacy protection and consumer data ; our ability to successfully transition our wealth management business to a new clearing platform and our expectations concerning the benefits that may be derived therefrom ; cybersecurity risks ; our ability to maintain our relationships with third party partners ; the seasonality of our business ; litigation risks ; our ability to attract and retain qualified employees ; our assessments and estimates that determine our effective tax rate ; the impact of new or changing tax legislation ; our ability to develop, establish and maintain strong brands ; our ability to protect our intellectual property ; and our ability to effectively integrate companies or assets that we acquire . A more detailed description of these and certain other factors that could affect actual results is included in the Risk Factors section of the Company’s Annual Report on Form 10 - K for the year ended December 31 , 2020 filed with the U . S . Securities and Exchange Commission (the “ SEC ”) on February 26 , 2021 . Readers are cautioned not to place undue reliance on forward - looking statements, which speak only as of the date of this presentation . Except as required by law, the Company undertakes no obligation to update any forward - looking statement to reflect events, new information or circumstances occurring after the date of this presentation . Non - GAAP Financial Information This presentation contains non - GAAP financial measures relating to our performance . You can find the reconciliation of these measures to the most directly comparable GAAP financial measure in the Appendix at the end of this presentation . The non - GAAP financial measures disclosed by the Company should not be considered a substitute for, or superior to, the financial measures prepared in accordance with GAAP . Important Additional Information and Where to Find It The Company has filed a definitive proxy statement, an accompanying BLUE proxy card and other relevant documents with the SEC in connection with the solicitation of proxies for the Company’s 2021 annual meeting of stockholders . BEFORE MAKING ANY VOTING DECISION, STOCKHOLDERS OF THE COMPANY ARE URGED TO READ THE DEFINITIVE PROXY STATEMENT, INCLUDING ANY AMENDMENTS AND SUPPLEMENTS THERETO, AND ALL RELEVANT DOCUMENTS FILED WITH OR FURNISHED TO THE SEC, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION . Investors and stockholders will be able to obtain a copy of the Company’s definitive proxy statement and other documents filed by the Company with the SEC free of charge from the SEC’s website at www . sec . gov . In addition, copies will be available at no charge by selecting “SEC Filings” under “Financial Information” in the “Investors” tab of the Company’s website at www . blucora . com .

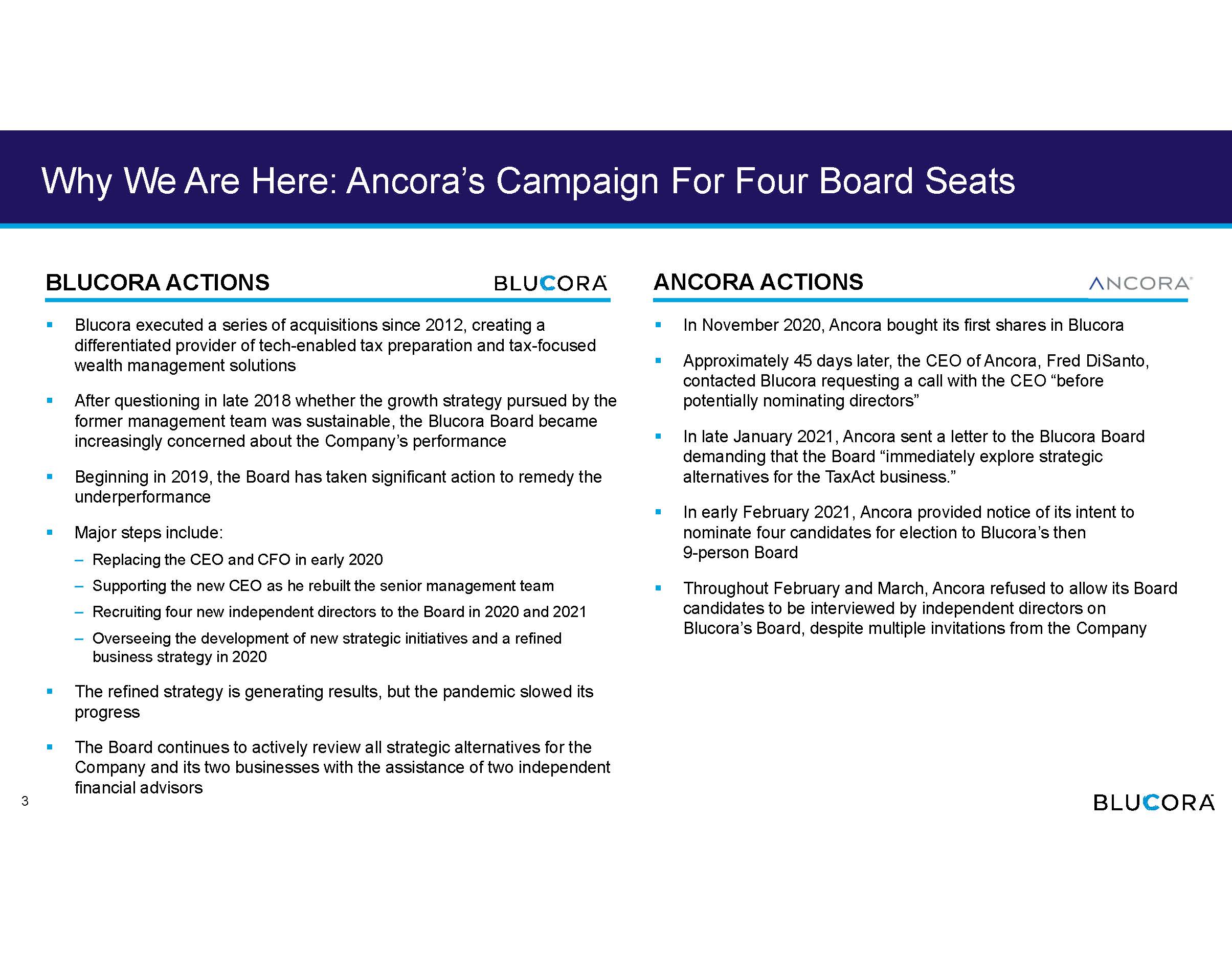

Why We Are Here: Ancora’s Campaign For Four Board Seats ▪ In November 2020, Ancora bought its first shares in Blucora ▪ Approximately 45 days later, the CEO of Ancora , Fred DiSanto, contacted Blucora requesting a call with the CEO “before potentially nominating directors” ▪ In late January 2021, Ancora sent a letter to the Blucora Board demanding that the Board “immediately explore strategic alternatives for the TaxAct business.” ▪ In early February 2021, Ancora provided notice of its intent to nominate four candidates for election to Blucora’s then 9 - person Board ▪ Throughout February and March, Ancora refused to allow its Board candidates to be interviewed by independent directors on Blucora’s Board, despite multiple invitations from the Company ▪ Blucora executed a series of acquisitions since 2012, creating a differentiated provider of tech - enabled tax preparation and tax - focused wealth management solutions ▪ After questioning in late 2018 whether the growth strategy pursued by the former management team was sustainable, the Blucora Board became increasingly concerned about the Company’s performance ▪ Beginning in 2019, the Board has taken significant action to remedy the underperformance ▪ Major steps include: ‒ Replacing the CEO and CFO in early 2020 ‒ Supporting the new CEO as he rebuilt the senior management team ‒ Recruiting four new independent directors to the Board in 2020 and 2021 ‒ Overseeing the development of new strategic initiatives and a refined business strategy in 2020 ▪ The refined strategy is generating results, but the pandemic slowed its progress ▪ The Board continues to actively review all strategic alternatives for the Company and its two businesses with the assistance of two independent financial advisors BLUCORA ACTIONS ANCORA ACTIONS 3

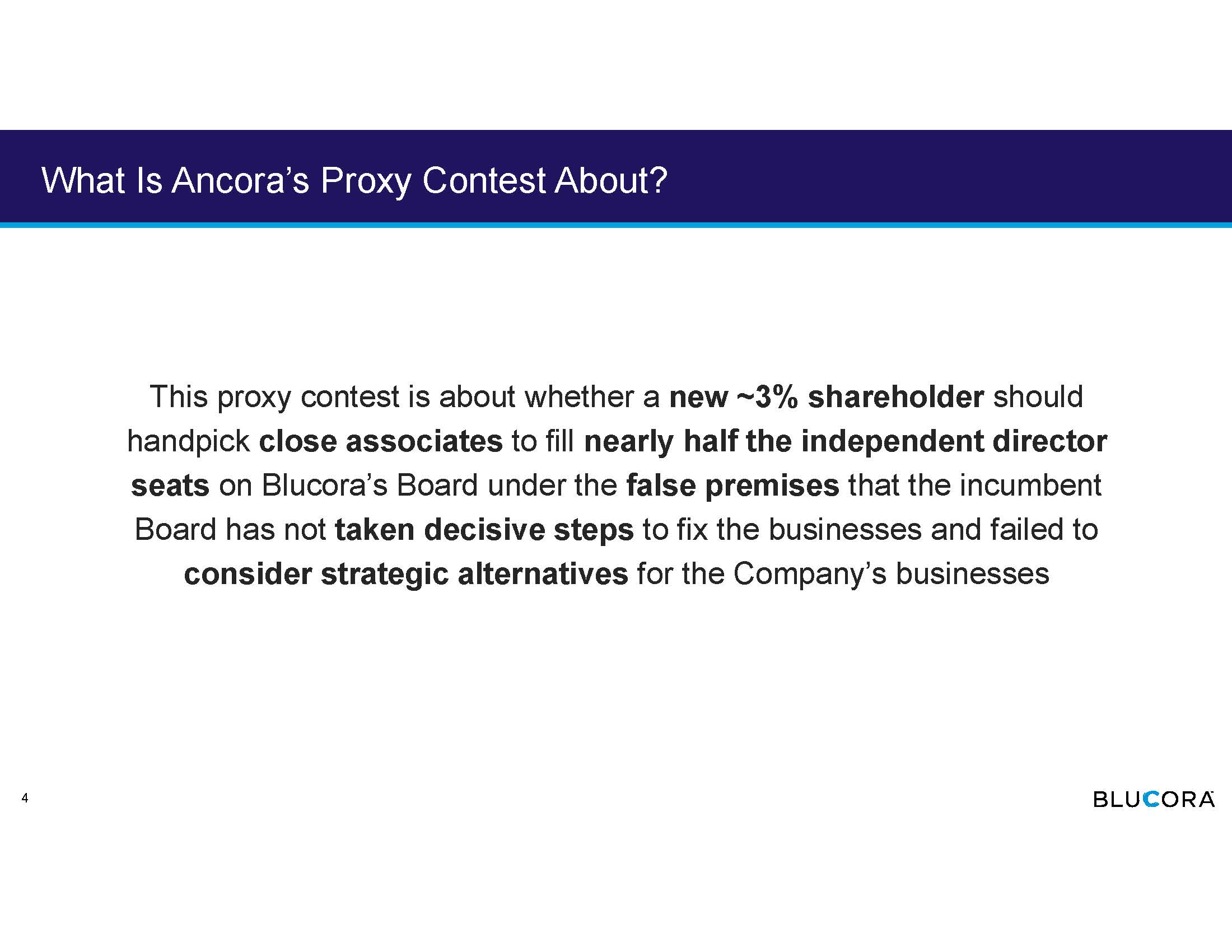

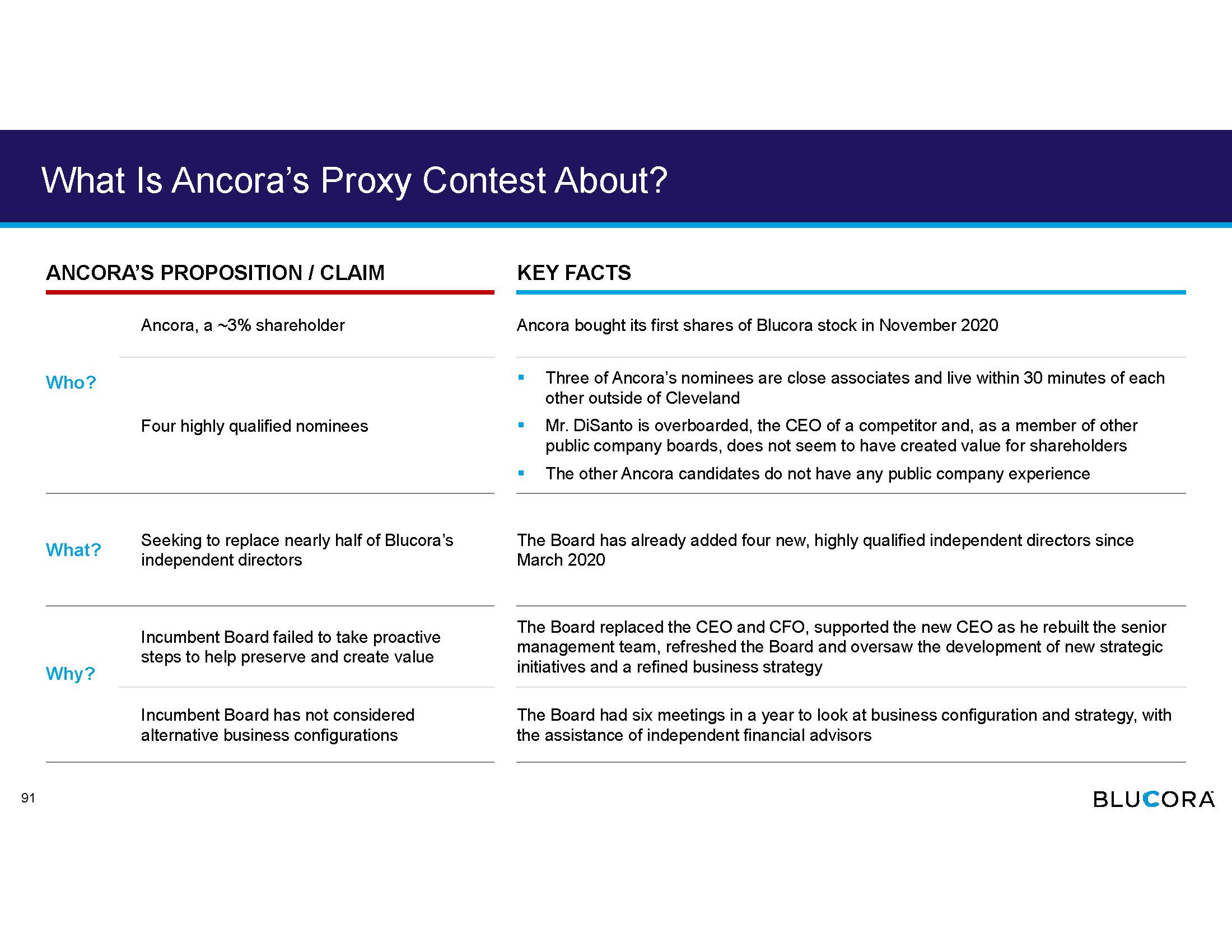

What Is Ancora’s Proxy Contest About? This proxy contest is about whether a new ~3% shareholder should handpick close associates to fill nearly half the independent director seats on Blucora’s Board under the false premises that the incumbent Board has not taken decisive steps to fix the businesses and failed to consider strategic alternatives for the Company’s businesses 4

Table of Contents I Executive Summary 6 II Overview of Blucora’s Businesses 15 III The Board Became Increasingly Concerned About the Company’s Performance in 2019 23 IV The Board Made Decisive Changes to Management and Board Composition and Oversaw a Refinement in Strategy 27 V Blucora Has the Right Board and Governance to Drive Change and Growth 46 VI Ancora’s Campaign is an Overreach; Its Nominees Are Not Additive 56 VII Conclusion 89 VIII Appendix 95 5

Executive Summary

Executive Summary By mid - 2019, it was evident to the Blucora Board that the Company was not pursuing a sustainable strategy ▪ Blucora was formed through a series of acquisitions and dispositions beginning in 2012 ▪ The acquisitions created two business units, each focused on helping American consumers with taxes – a tax preparation software business (“TaxAct”) and a tax - focused wealth management business (“Avantax”) ▪ The prior management team used price increases to drive TaxAct revenue, a strategy that was later determined by the Board to be unsustainable; TaxAct faced increasingly competitive pressure in 2018 and 2019 ▪ Wealth management acquisitions completed in 2015 and 2019 were not integrated in line with the Board’s expectations, and the prior strategy depended on further acquisitions and market appreciation of assets to drive growth ▪ The stock underperformed peers in 2019 ▪ Recognizing the suboptimal strategy, the Blucora Board took proactive steps in the fourth quarter of 2019 and early 2020 ▪ Since early 2020, nearly the entire senior management team has been changed, including a new CEO and CFO ▪ The rebuilt management team has a refined strategic plan that the Board believes will strengthen each of the businesses individually and reap cross - over benefits ▪ The Board saw the need for self refreshment and, since March 2020, has added four directors with relevant skills and experience ▪ Blucora’s governance and executive compensation practices were also enhanced and are shareholder - friendly ▪ In the Tax Preparation business, the Company is executing on several operational and strategy changes: driving increased functionality and useability while attracting new customers through improved marketing efforts ▪ In the Wealth Management business, the Company is integrating its three core acquisitions, driving efficiencies and selectively improving retention rates ▪ Blucora believes there are substantial cross - over opportunities between the two business units ▪ In 2020 and 2021, the pandemic impacted our business as the IRS extended the tax season and wealth management assets initially declined due to market volatility, while the reduction in the federal funds rate to 0% caused a decline in high - margin cash sweep revenue The Blucora Board took decisive action to rebuild the executive team, refresh the Board of Directors and oversee the development of new strategic initiatives Blucora is executing on a strategy that will create significant value, but the pandemic has impacted our business 7

Executive Summary, Continued The Blucora Board has been active in reviewing all strategic alternatives for the business ▪ The Board met numerous times throughout 2020 and 2021 to refine the Company’s strategy and address challenges related to the COVID - 19 pandemic ▪ The Board has confidence in the refined strategic plan and the opportunity for Blucora to create significant value for shareholders ▪ Nevertheless, since early 2020, Blucora’s refreshed Board has been actively evaluating strategic alternatives and the optimal timing for executing on any such alternatives ▪ The Board has received input from two independent financial advisors and continues to evaluate the best way to maximize value for all Blucora shareholders on an ongoing basis ▪ Ancora is a recent shareholder with a ~3% stake that has nominated several close associates to fill nearly half the independent director seats ▪ Ancora has refused to allow its nominees to be interviewed by Blucora ▪ Ancora seems focused on having Blucora immediately sell TaxAct and redeploying the proceeds to repay debt, repurchase stock and acquire wealth management assets ▪ We do not believe Ancora’s proposed strategy maximizes value for all Blucora shareholders ▪ Based on what we know, Ancora’s nominees are not well - suited to serve on Blucora’s Board and likely lack the relevant skills and experience necessary to evaluate Ancora’s own plan ▪ Blucora’s Board acted decisively to address performance issues by replacing the CEO and CFO, recruiting four new independent directors, and overseeing the development of a refined plan ▪ The Board has been actively evaluating strategic and business configuration alternatives and has exercised — and will continue to exercise — objective business judgment in working to maximize value for all shareholders ▪ Ancora’s nominees do not appear to bring new skills or experience to the Board, and the replacement of existing directors would be a net loss to the Board’s capabilities ▪ Blucora shareholders should support the Board’s nominees Ancora’s campaign is an overreach, and its candidates will not bring new relevant skills or experience to the Board Shareholders should support the refreshed Blucora Board and its actions to maximize value 8

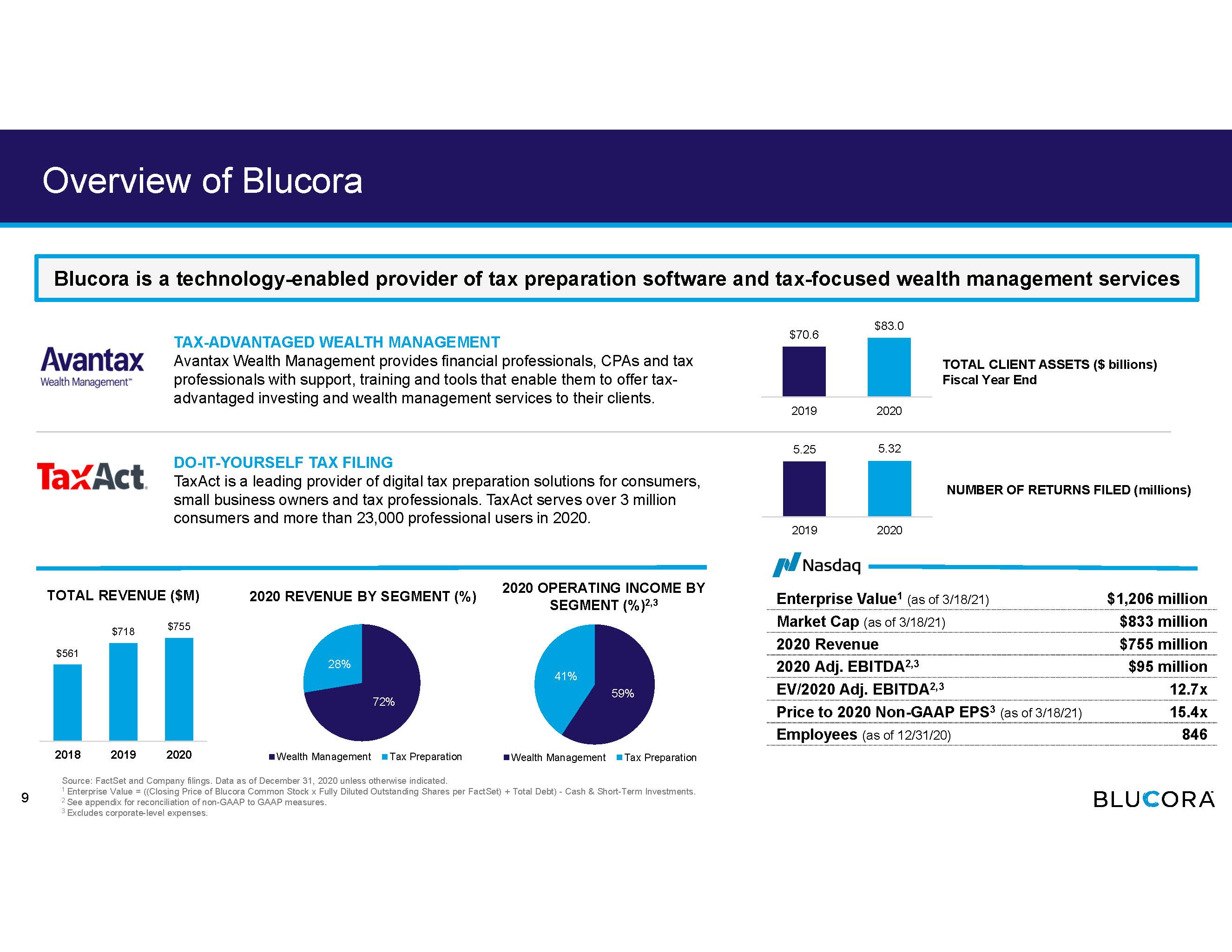

TAX - ADVANTAGED WEALTH MANAGEMENT Avantax Wealth Management provides financial professionals, CPAs and tax professionals with support, training and tools that enable them to offer tax - advantaged investing and wealth management services to their clients. DO - IT - YOURSELF TAX FILING TaxAct is a leading provider of digital tax preparation solutions for consumers, small business owners and tax professionals. TaxAct serves over 3 million consumers and more than 23,000 professional users in 2020. Overview of Blucora Enterprise Value 1 (as of 3/18/21) $1,206 million Market Cap (as of 3/18/21) $833 million 2020 Revenue $755 million 2020 Adj. EBITDA 2, 3 $95 million EV/2020 Adj. EBITDA 2, 3 12.7x Price to 2020 Non - GAAP EPS 3 (as of 3/18/21) 15.4x Employees (as of 12/31/20) 846 Blucora is a technology - enabled provider of tax preparation software and tax - focused wealth management services 72% 28% Wealth Management Tax Preparation 2020 REVENUE BY SEGMENT (%) TOTAL REVENUE ($M) $561 $718 $755 2018 2019 2020 2020 OPERATING INCOME BY SEGMENT (%) 2,3 Source: FactSet and Company filings. Data as of December 31, 2020 unless otherwise indicated. 1 Enterprise Value = ((Closing Price of Blucora Common Stock x Fully Diluted Outstanding Shares per FactSet) + Total Debt) - Cash & Short - Term Investments. 2 See appendix for reconciliation of non - GAAP to GAAP measures. 3 Excludes corporate - level expenses. NUMBER OF RETURNS FILED (millions) TOTAL CLIENT ASSETS ($ billions) Fiscal Year End 5.25 5.32 2019 2020 $70.6 $83.0 2019 2020 9 59% 41% Wealth Management Tax Preparation

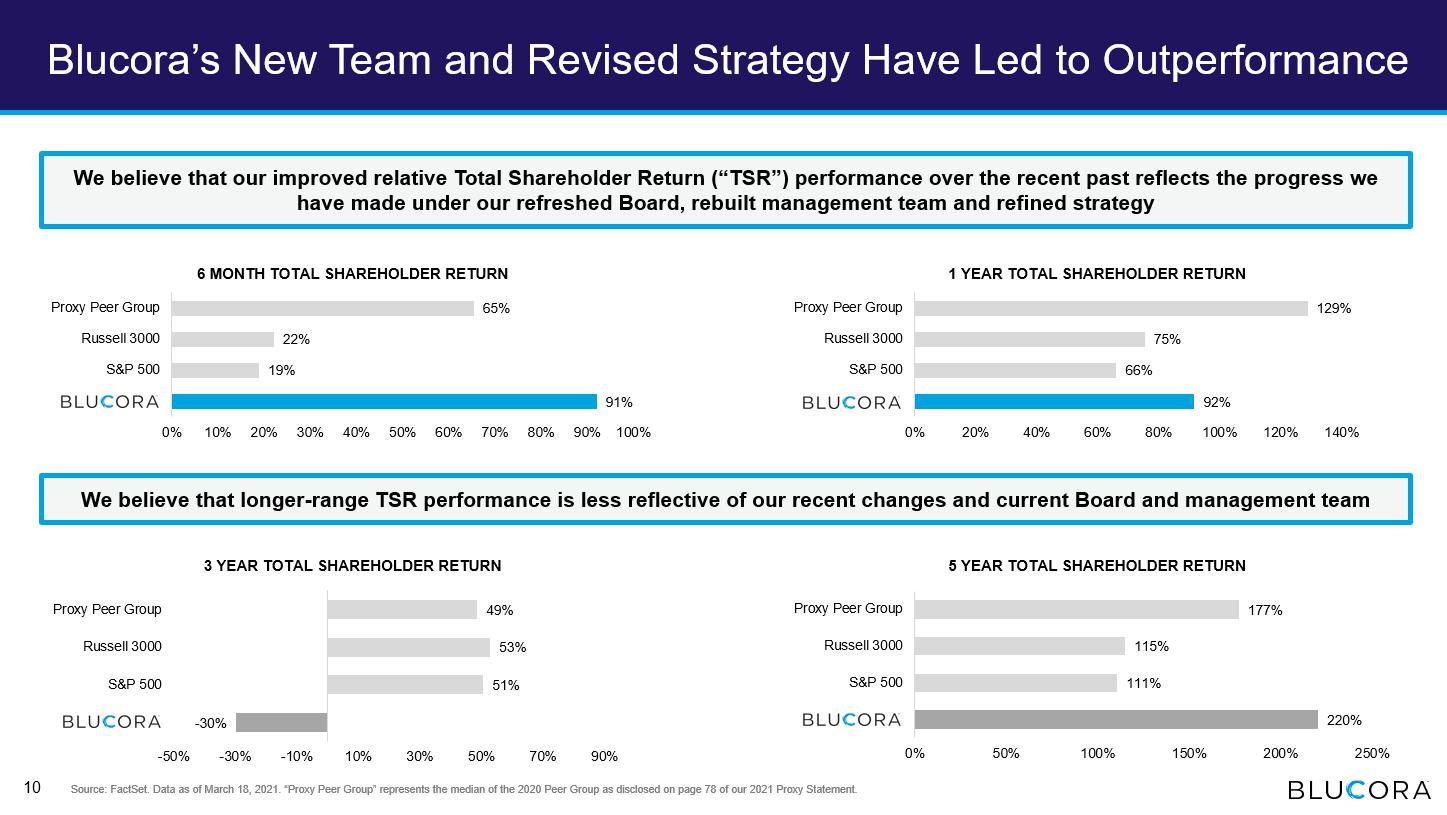

Blucora’s New Team and Strategy Have Led to Outperformance We believe that our improved relative Total Shareholder Return (“TSR”) performance over the recent past reflects the progress we have made under our refreshed Board, rebuilt management team and refined strategy Source: FactSet. Data as of March 18, 2021. “Proxy Peer Group” represents the median of the 2020 Peer Group as disclosed on p age 78 of our 2021 Proxy Statement. We believe that longer - range TSR performance is less reflective of our recent changes and current Board and management team 6 MONTH TOTAL SHAREHOLDER RETURN 1 YEAR TOTAL SHAREHOLDER RETURN 3 YEAR TOTAL SHAREHOLDER RETURN 5 YEAR TOTAL SHAREHOLDER RETURN 92% 66% 75% 129% 0% 20% 40% 60% 80% 100% 120% 140% S&P 500 Russell 3000 Proxy Peer Group 91% 19% 22% 65% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% S&P 500 Russell 3000 Proxy Peer Group - 30% 51% 53% 49% -50% -30% -10% 10% 30% 50% 70% 90% S&P 500 Russell 3000 Proxy Peer Group 220% 111% 115% 177% 0% 50% 100% 150% 200% 250% S&P 500 Russell 3000 Proxy Peer Group 10

11% 11% 1% - 8% -10% -5% 0% 5% 10% 15% INTU BCOR HRB FRG TaxAct Has Strong Growth and Good Margins 11 REVENUE CAGR 2016 - 2020 LTM SEGMENT OPERATING MARGINS¹ 24% 19% 12% 8% 0% 5% 10% 15% 20% 25% BCOR FRG INTU HRB Corporate overhead Source: Company filings. Intuit revenue/margin reflects contributions from tax - focused “Consumer” and “Strategic Partner” segmen ts. Note: H&R Block, Intuit, and Liberty Tax (2016) data is calendarized to reflect contributions from November 1 through October 31 of each year. ¹ LTM (Last Twelve Months) segment operating margin equals segment operating income divided by segment revenue. Note: H&R Block only reports one segment, so operating margins reflect whole Company. TaxAct is a growing player in the tax preparation space with good margins

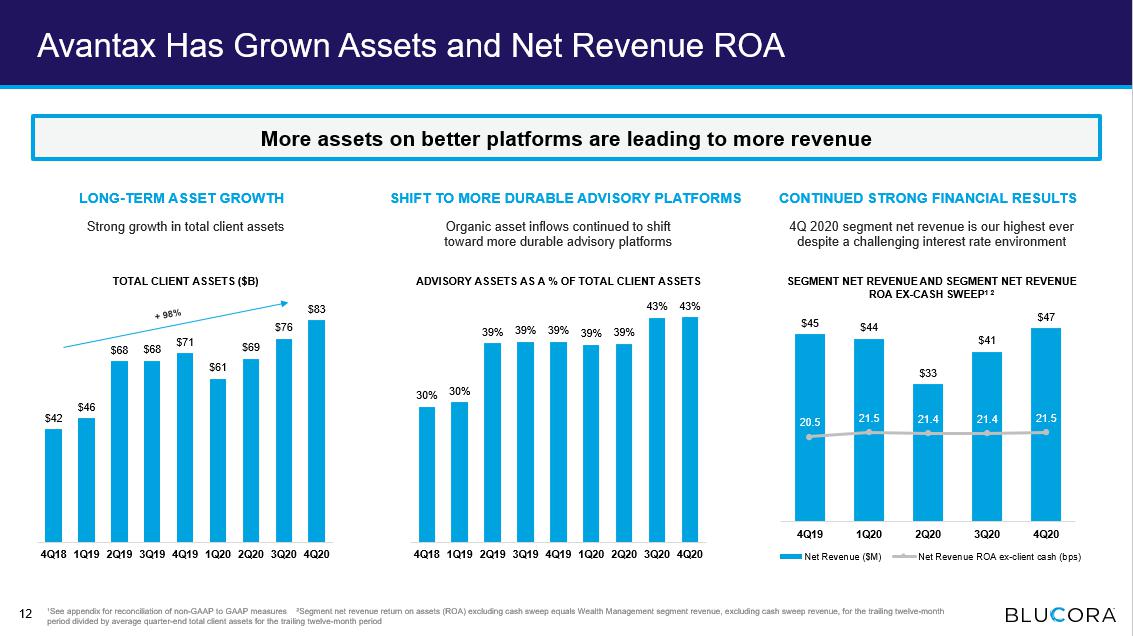

Organic asset inflows continued to shift toward more profitable advisory platforms LONG - TERM ASSET GROWTH CONTINUED STRONG FINANCIAL RESULTS SHIFT TO MORE DURABLE ADVISORY PLATFORMS Strong growth in total client assets 4Q 2020 segment net revenue is our highest ever despite a challenging interest rate environment Avantax Has Grown Assets and Net Revenue ROA TOTAL CLIENT ASSETS ($B) ADVISORY ASSETS AS A % OF TOTAL CLIENT ASSETS SEGMENT NET REVENUE AND SEGMENT NET REVENUE ROA EX - CASH SWEEP 1 2 $42 $46 $68 $68 $71 $61 $69 $76 $83 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 30% 30% 39% 39% 39% 39% 39% 43% 43% 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 $45 $44 $33 $41 $47 20.5 21.5 21.4 21.4 21.5 4Q19 1Q20 2Q20 3Q20 4Q20 Net Revenue ($M) Net Revenue ROA ex-client cash (bps) ¹See appendix for reconciliation of non - GAAP to GAAP measures ²Segment net revenue return on assets (ROA) excluding cash swee p equals Wealth Management segment revenue, excluding cash sweep revenue, for the trailing twelve - month period divided by average quarter - end total client assets for the trailing twelve - month period More assets on better platforms are leading to more revenue 12

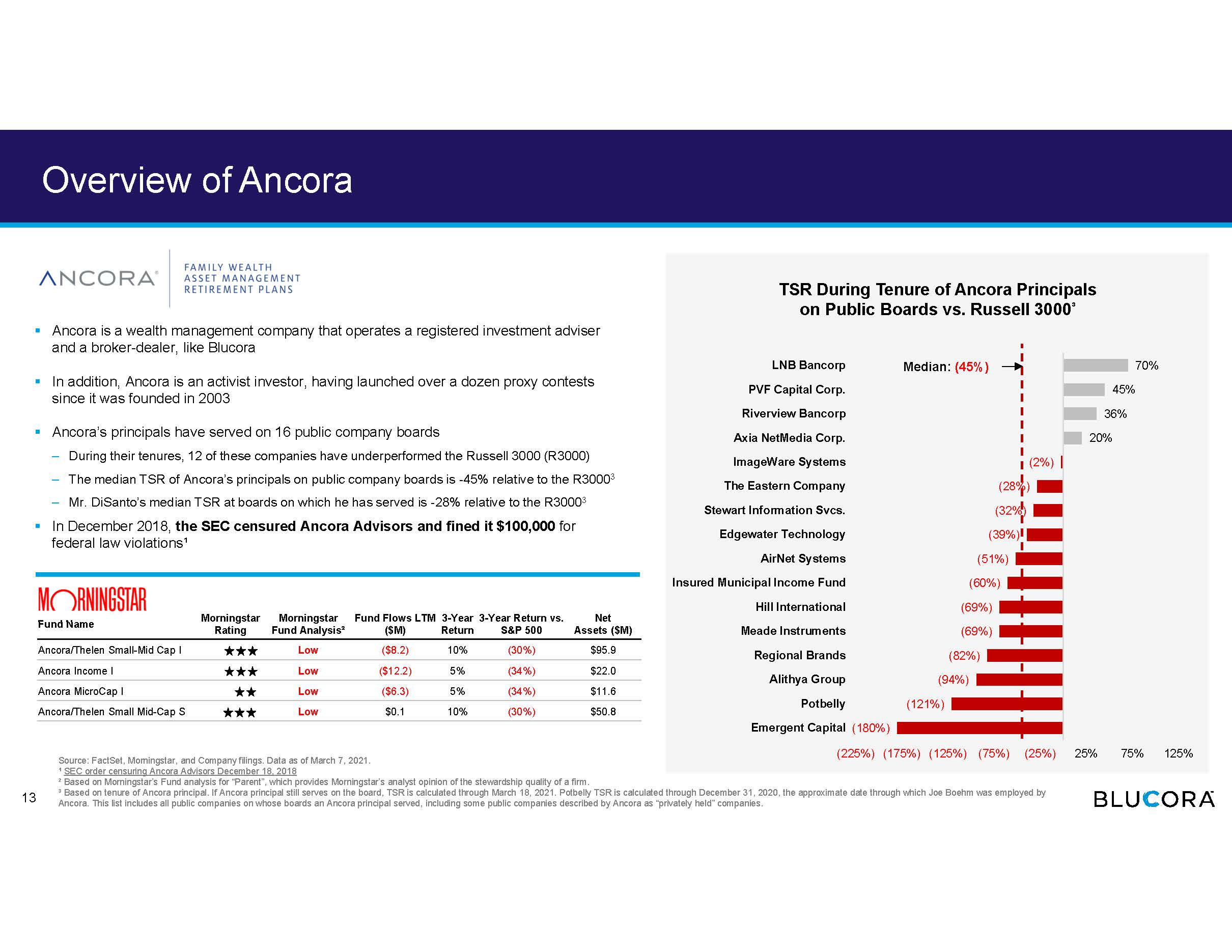

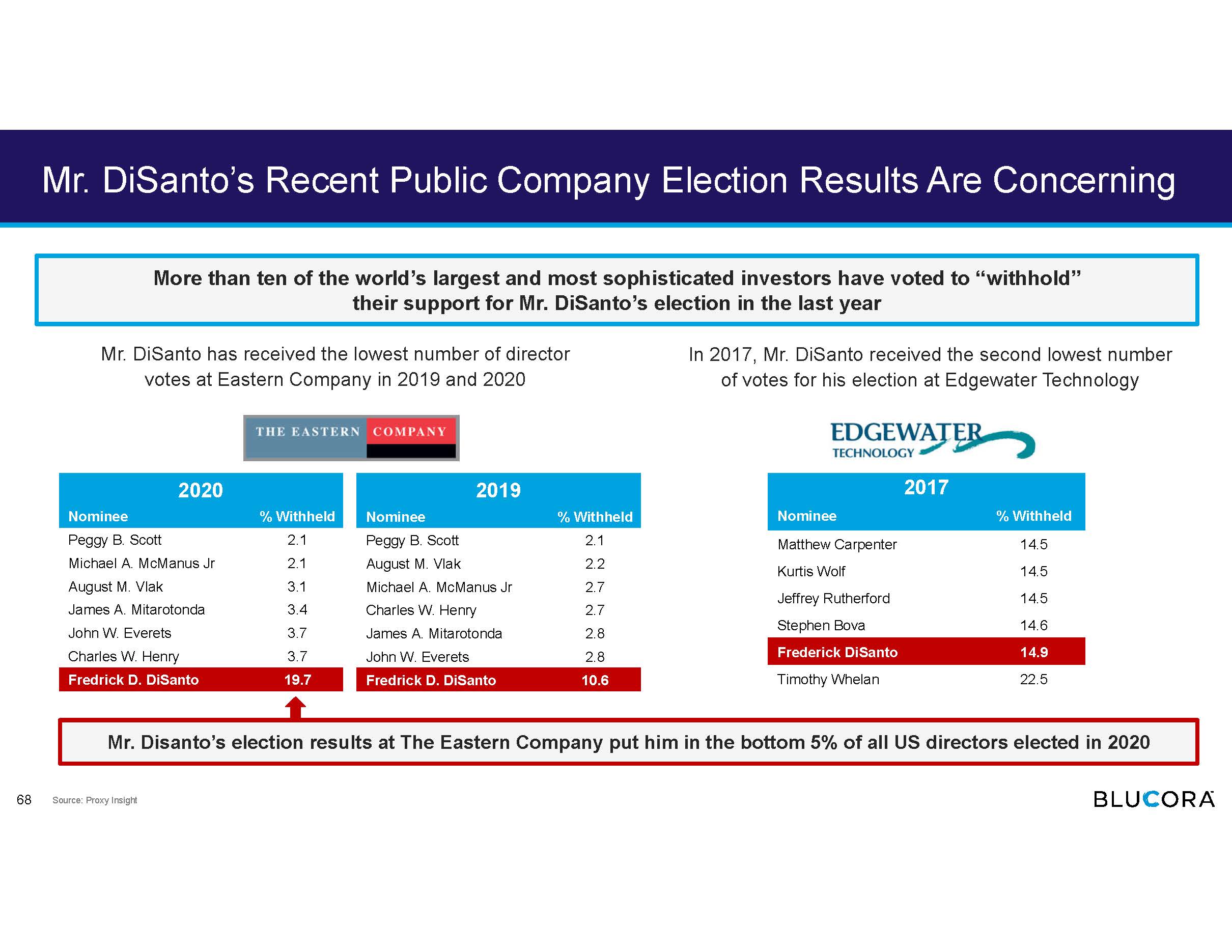

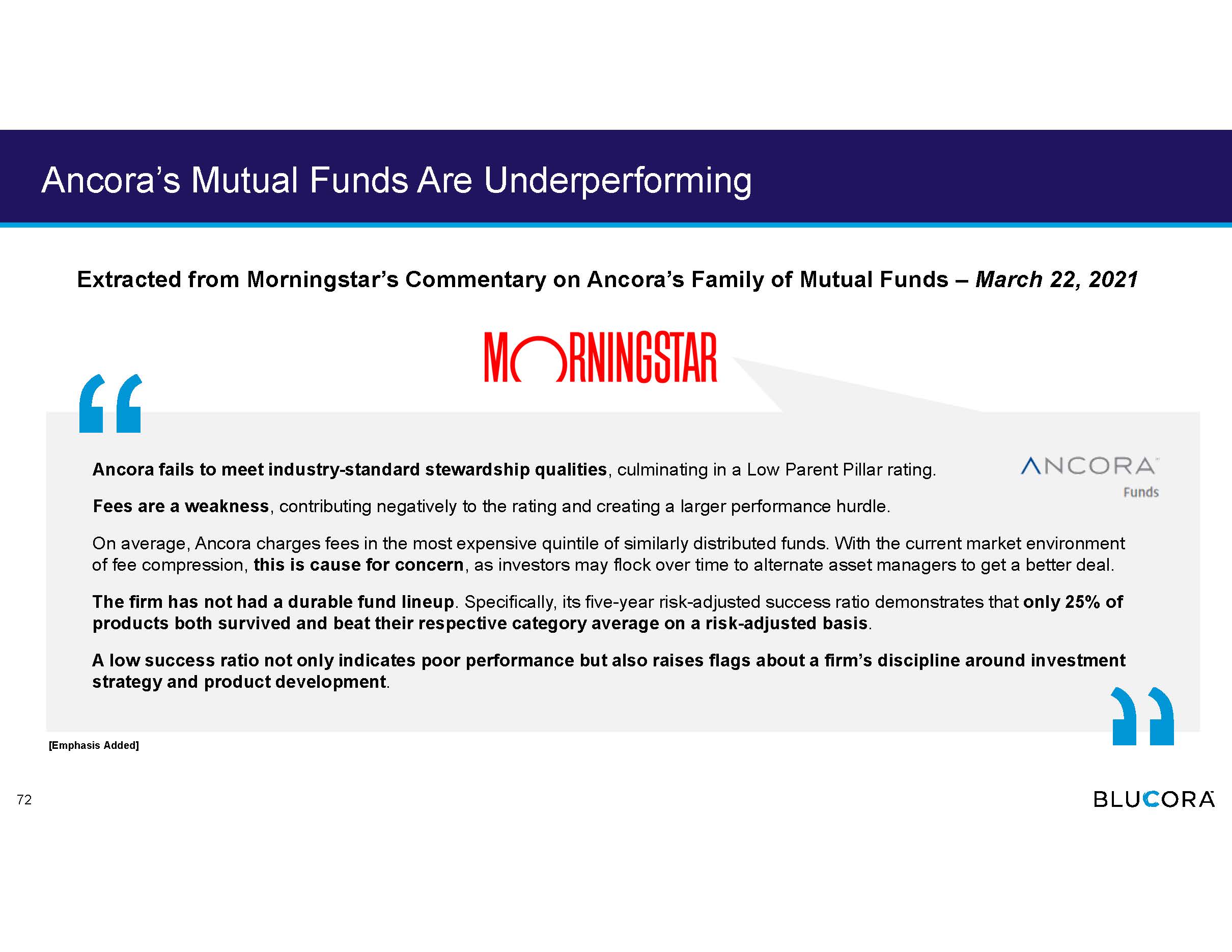

TSR During Tenure of Ancora Principals on Public Boards vs. Russell 3000 ³ Overview of Ancora ▪ Ancora is a wealth management company that operates a registered investment adviser and a broker - dealer, like Blucora ▪ In addition, Ancora is an activist investor, having launched over a dozen proxy contests since it was founded in 2003 ▪ Ancora’s principals have served on 16 public company boards ‒ During their tenures, 12 of these companies have underperformed the Russell 3000 (R3000) ‒ The median TSR of Ancora’s principals on public company boards is - 45% relative to the R3000 3 ‒ Mr. DiSanto’s median TSR at boards on which he has served is - 28% relative to the R3000 3 ▪ In December 2018, the SEC censured Ancora Advisors and fined it $100,000 for federal law violations ¹ Source: FactSet, Morningstar, and Company filings. Data as of March 7, 2021. ¹ SEC order censuring Ancora Advisors December 18, 2018 ² Based on Morningstar’s Fund analysis for “Parent”, which provides Morningstar’s analyst opinion of the stewardship quality of a firm. ³ Bas ed on tenure of Ancora principal. If Ancora principal still serves on the board, TSR is calculated through March 18, 2021. Potbelly TSR is calculated through December 31 , 2020, the approximate date through which Joe Boehm was employed by Ancora . This list includes all public companies on whose boards an Ancora principal served, including some public companies described by Ancora as “privately held” companies. Median: (45%) Fund Name Morningstar Rating Morningstar Fund Analysis ² Fund Flows LTM ($M) 3 - Year Return 3 - Year Return vs. S&P 500 Net Assets ($M) Ancora / Thelen Small - Mid Cap I Low ($8.2) 10% (30%) $95.9 Ancora Income I Low ($12.2) 5% (34%) $22.0 Ancora MicroCap I Low ($6.3) 5% (34%) $11.6 Ancora / Thelen Small Mid - Cap S Low $0.1 10% (30%) $50.8 13 70% 45% 36% 20% (2%) (28%) (32%) (39%) (51%) (60%) (69%) (69%) (82%) (94%) (121%) (180%) (225%) (175%) (125%) (75%) (25%) 25% 75% 125% LNB Bancorp PVF Capital Corp. Riverview Bancorp Axia NetMedia Corp. ImageWare Systems The Eastern Company Stewart Information Svcs. Edgewater Technology AirNet Systems Insured Municipal Income Fund Hill International Meade Instruments Regional Brands Alithya Group Potbelly Emergent Capital

Shareholders Should Support Blucora’s Nominees THE BOARD HAS DRIVEN CHANGE ▪ Beginning in early 2020, the Blucora Board has proactively changed the CEO and CFO and refreshed the Board ▪ The Blucora Board has supported the new CEO as he rebuilt the senior management team and has overseen the development of new strategic initiatives and a refined business strategy ▪ The Company has been executing a promising strategy amidst an unprecedented and unpredictable pandemic, which has masked results ▪ The Board is well constructed and actively evaluates operational and strategic alternatives, including with the help of independent financial advisors ▪ The Board continues to closely monitor the execution of the Company’s strategic plan with unfettered access to detailed performance data and forecasts THE BOARD IS BEST POSITIONED TO CONTINUE BLUCORA’S TRANSFORMATION ▪ The Board has added four new directors since March 2020 and is well - suited to oversee the execution of the Company’s long - term strategy and evaluate strategic alternatives ▪ The Board has been decisive and is committed to continuing to evaluate the business configuration and potential improvements ▪ Three of Ancora’s nominees do not have any public company executive or board experience and are not additive to the skills of the Board ▪ The fourth candidate – Ancora’s CEO Fred DiSanto – is overboarded 1 and may not be able to serve on Blucora’s Board under the Clayton Antitrust Act ▪ On the other hand, Blucora’s Board is engaged, active and well - rounded with the skills and experiences necessary to maximize value ¹ Mr. DiSanto is the CEO of a public company and already serves on three public company boards. 14

Overview of Blucora’s Businesses

Blucora’s Tax - Focused Solutions Empower Financial Wellness 16 The Solution Americans spend more on taxes than on their mortgage, groceries and clothing, combined Blucora empowers people to improve their financial wellness with data - and technology - enabled tax software and wealth management solutions Helps consumers with their financial lives by leveraging tax as the core: ▪ Enables more holistic financial advice ▪ Uncovers financial insights not readily apparent to taxpayers Helps tax professionals maximize their businesses to meet the financial needs of clients: ▪ Adds significant incremental revenue stream with wealth management ▪ Delivers on their core business with value - based tax preparation software The Opportunity Taxes are one of life’s largest expenses, yet: ▪ The Tax Prep industry focuses consumers on maximizing a once - a - year refund ▪ Historically, tax - focused wealth management advice has not been widely available to all Americans

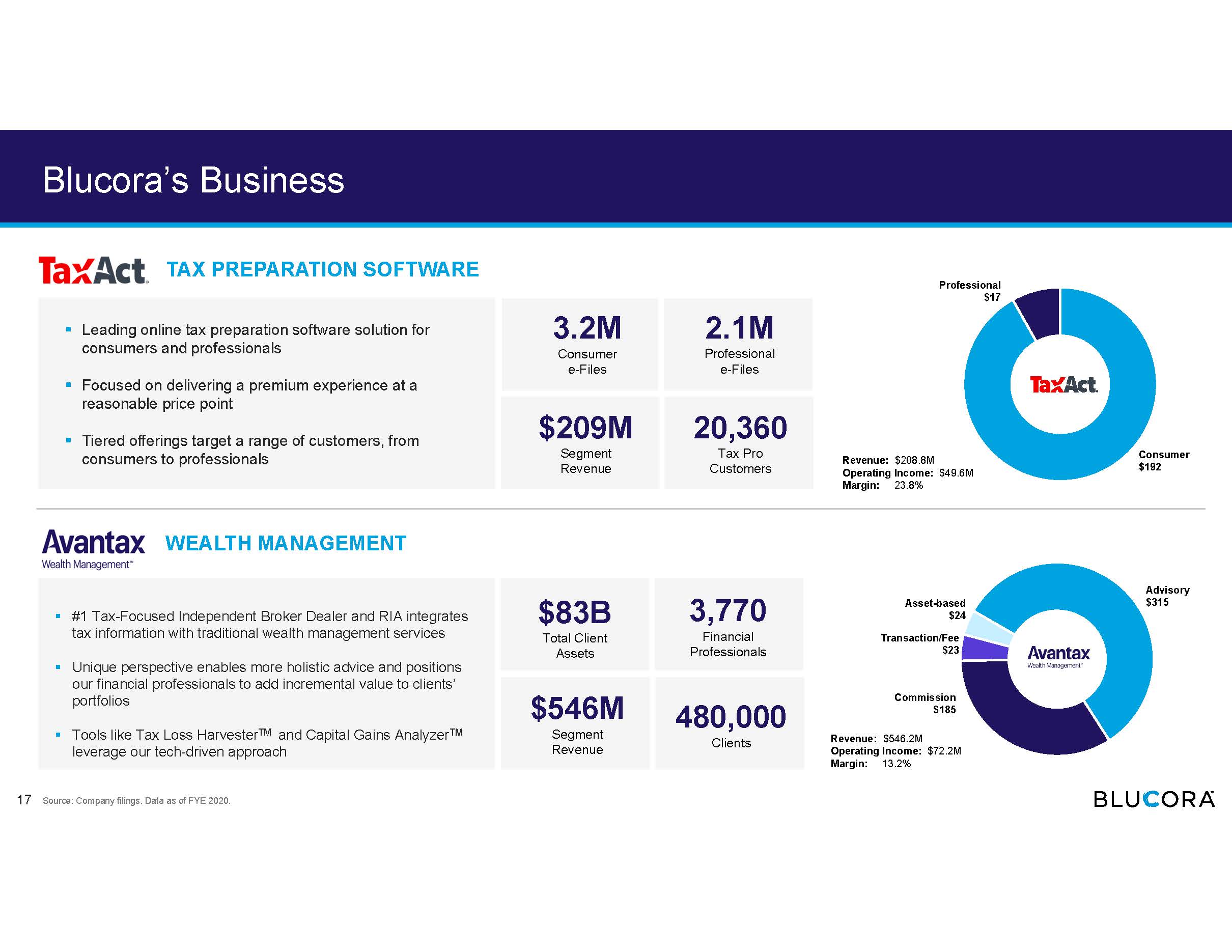

Blucora’s Business 17 ▪ Leading online tax preparation software solution for consumers and professionals ▪ Focused on delivering a premium experience at a reasonable price point ▪ Tiered offerings target a range of customers, from consumers to professionals ▪ #1 Tax - Focused Independent Broker Dealer and RIA integrates tax information with traditional wealth management services ▪ Unique perspective enables more holistic advice and positions our financial professionals to add incremental value to clients’ portfolios ▪ Tools like Tax Loss Harvester TM and Capital Gains Analyzer TM leverage our tech - driven approach Revenue: $208.8M Operating Income: $49.6M Margin: 23.8% Revenue: $546.2M Operating Income: $72.2M Margin: 13.2% 3.2M Consumer e - Files 2.1M Professional e - Files $209M Segment Revenue 20,360 Tax Pro Customers $83B Total Client Assets $546M Segment Revenue 480,000 Clients 3,770 Financial Professionals Source: Company filings. Data as of FYE 2020. Commission $185 Advisory $315 Asset - based $24 Transaction/Fee $23 Consumer $192 Professional $17 WEALTH MANAGEMENT TAX PREPARATION SOFTWARE

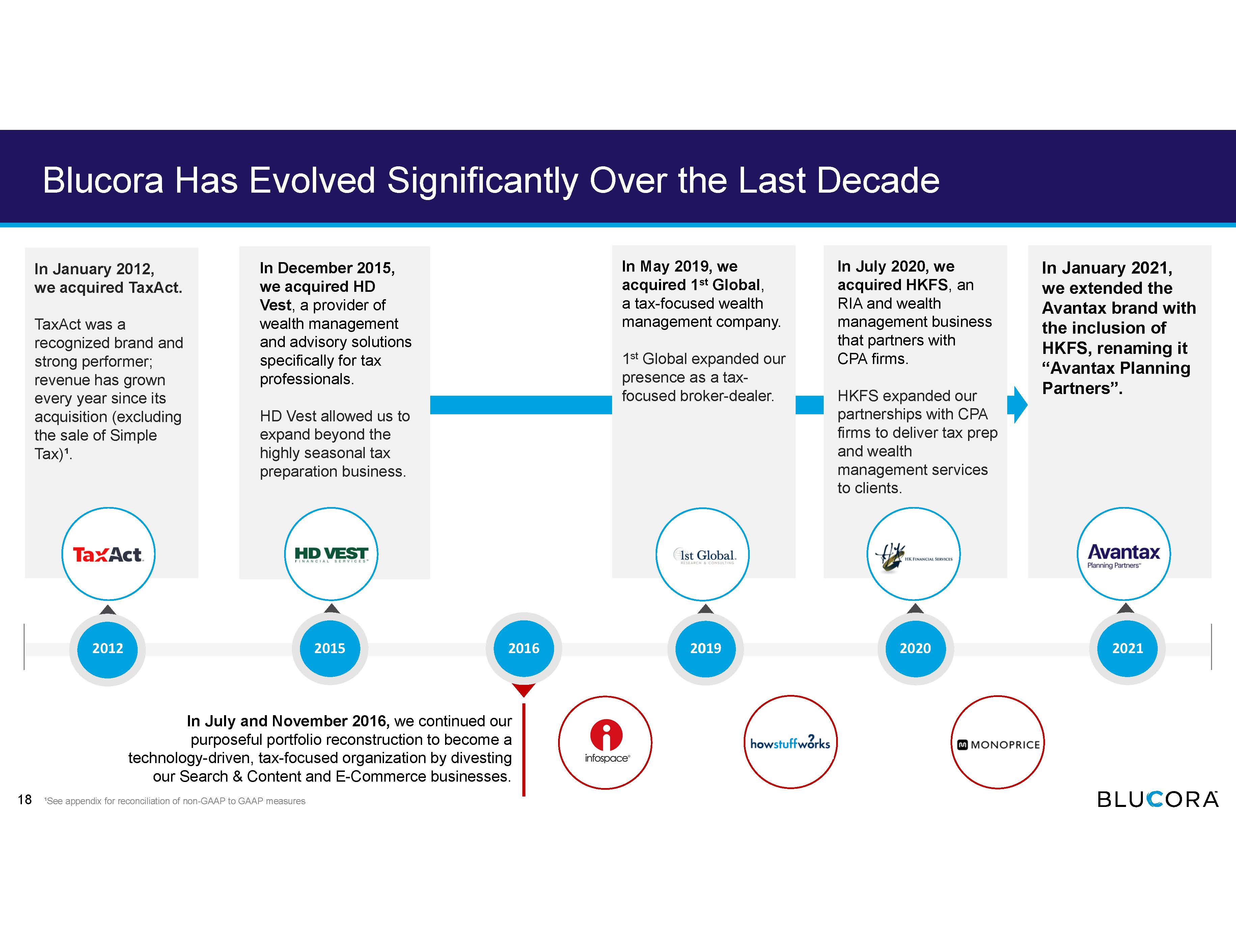

Blucora Has Evolved Significantly Over the Last Decade In January 2012, we acquired TaxAct. TaxAct was a recognized brand and strong performer; revenue has grown every year since its acquisition (excluding the sale of Simple Tax)¹. In May 2019, we acquired 1 st Global , a tax - focused wealth management company. 1 st Global expanded our presence as a tax - focused broker - dealer. In July 2020, we acquired HKFS , an RIA and wealth management business that partners with CPA firms. HKFS expanded our partnerships with CPA firms to deliver tax prep and wealth management services to clients. In January 2021, we extended the Avantax brand with the inclusion of HKFS, renaming it “Avantax Planning Partners”. In December 2015, we acquired HD Vest , a provider of wealth management and advisory solutions specifically for tax professionals. HD Vest allowed us to expand beyond the highly seasonal tax preparation business. 18 In July and November 2016, we continued our purposeful portfolio reconstruction to become a technology - driven, tax - focused organization by divesting our Search & Content and E - Commerce businesses. 2012 2015 2019 2020 2021 2016 ¹See appendix for reconciliation of non - GAAP to GAAP measures

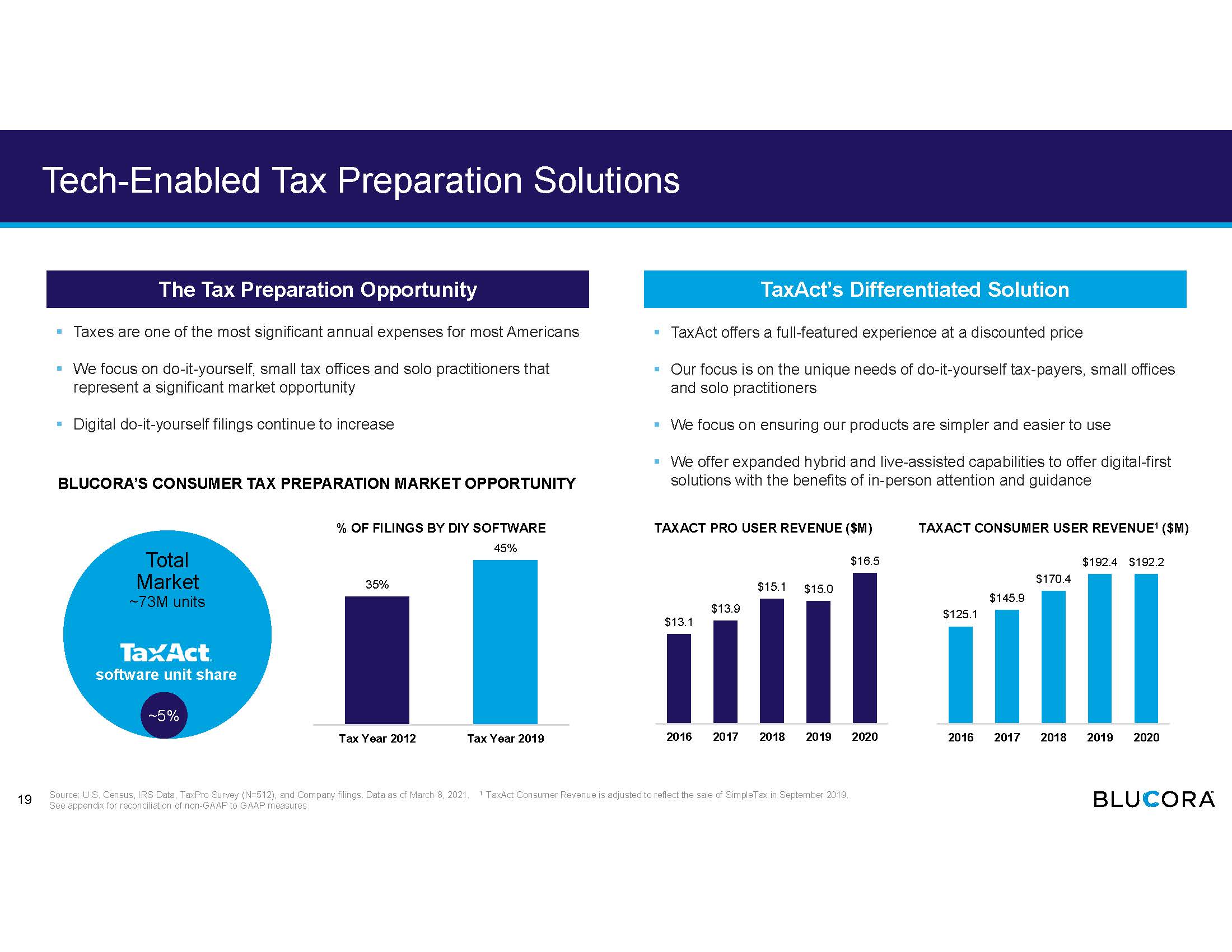

Tech - Enabled Tax Preparation Solutions 19 The Tax Preparation Opportunity TaxAct’s Differentiated Solution ▪ Taxes are one of the most significant annual expenses for most Americans ▪ We focus on do - it - yourself, small tax offices and solo practitioners that represent a significant market opportunity ▪ Digital do - it - yourself filings continue to increase ▪ TaxAct offers a full - featured experience at a discounted price ▪ Our focus is on the unique needs of do - it - yourself tax - payers, small offices and solo practitioners ▪ We focus on ensuring our products are simpler and easier to use ▪ We offer expanded hybrid and live - assisted capabilities to offer digital - first solutions with the benefits of in - person attention and guidance BLUCORA’S CONSUMER TAX PREPARATION MARKET OPPORTUNITY Source: U.S. Census, IRS Data, TaxPro Survey (N=512), and Company filings. Data as of March 8, 2021. 1 TaxAct Consumer Revenue is adjusted to reflect the sale of SimpleTax in September 2019. See appendix for reconciliation of non - GAAP to GAAP measures TAXACT PRO USER REVENUE ($M) TAXACT CONSUMER USER REVENUE 1 ($M) $13.1 $13.9 $15.1 $15.0 $16.5 2016 2017 2018 2019 2020 Total Market ~73M units ~5% software unit share % OF FILINGS BY DIY SOFTWARE 35% 45% Tax Year 2012 Tax Year 2019 $125.1 $145.9 $170.4 $192.4 $192.2 2016 2017 2018 2019 2020

Tax - Smart Wealth Management 20 ~45M Households Blucora’s Focus ▪ The captive Registered Investment Advisor (RIA) and Independent Broker Dealer (IBD) markets are large and growing ▪ We offer sophisticated, tax - focused approaches used by high - net worth wealth managers to our focused markets ▪ Our target market opportunity represents approximately 45 million households BLUCORA’S WEALTH MANAGEMENT MARKET OPPORTUNITY ▪ Avantax Wealth Management is the only firm that marries tax planning and preparation with financial planning and advisory for all Americans ▪ Avantax helps tax professionals maximize their business by adding a meaningful incremental revenue stream ▪ Avantax Financial Professionals are able to provide a more holistic suite of wealth management services that focus on minimizing taxes as well as maximizing returns SEGMENT OPERATING INCOME ($M) $46.3 $50.9 $53.1 $68.3 $72.2 2016 2017 2018 2019 2020 TOTAL CLIENT ASSETS ($B) $38.7 $44.2 $42.2 $70.6 $83.0 2016 2017 2018 2019 2020 Source: Cerulli Lodestar 2019; TaxPro Survey (N=512); Activate Consumer Survey 2020; IRS Tax Season Statistics for July 2020; data analysis of 2019 Tax Pro client re turns; and company filings. The Wealth Management Opportunity Avantax’s Differentiated Solution 83M 16M 11M 8M 10M Mass Market (<$75K Investable Net Worth) Lower Middle Market ($75K - 150K Investable Net Worth) Upper Middle Market ($250K - $500K Investable Net Worth) Mass Affluent ($500K - $1M Investable Net Worth) Affluent & Higher (>$1M Investable Net Worth) 45M

Our wealth management business is significantly more valuable today than the aggregate acquisition cost Our Wealth Management Acquisitions Have Created Value 21 Acquisitions Goodwill The combination of our larger wealth management acquisitions has created our Avantax business – a tax - focused Broker - Dealer combined with a tax - focused Registered Investment Advisor (RIA) ▪ We are working to have a more scalable platform to support organic growth by integrating the businesses ▪ We have harmonized pricing and fee structures to align the business to customers’ needs, where the industry is going and to create value for our financial professionals and Avantax ▪ We have retained key personnel (while refining a streamlined organization) and experienced expected attrition among financial professionals The goodwill impairment charge for these businesses in 2020 does not demonstrate that the acquisitions were overpriced or that the business is not more valuable today than when we acquired the companies ▪ The goodwill impairment test was conducted in March 2020, in accordance with GAAP accounting requirements, at the depth of the pandemic - related market decline in 2020, which negatively impacted key wealth management business drivers such as client asset levels and interest rates ▪ The goodwill impairment charge factored in conservative assumptions

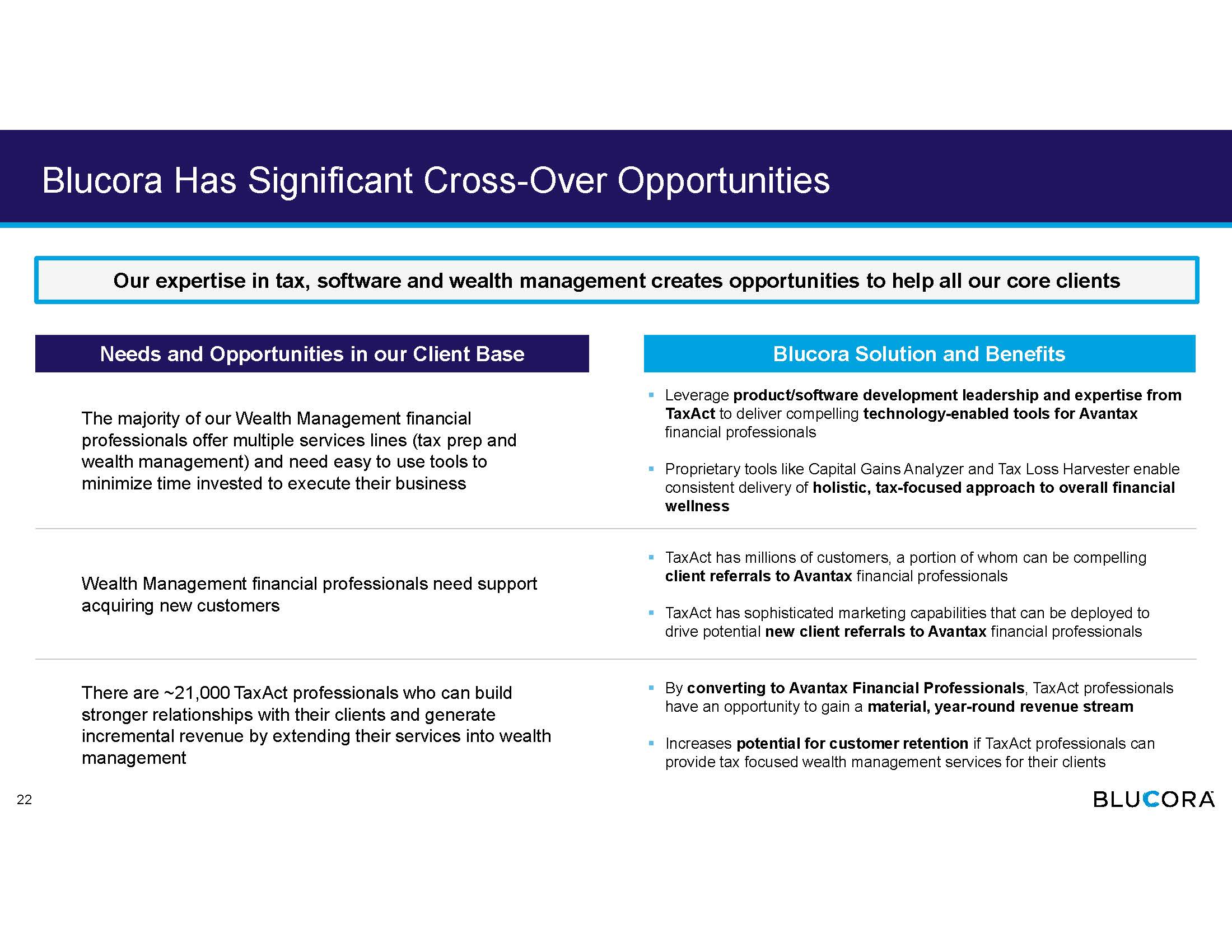

Blucora Has Significant Cross - Over Opportunities The majority of our Wealth Management financial professionals offer multiple services lines (tax prep and wealth management) and need easy to use tools to minimize time invested to execute their business ▪ Leverage product/software development leadership and expertise from TaxAct to deliver compelling technology - enabled tools for Avantax financial professionals ▪ Proprietary tools like Capital Gains Analyzer and Tax Loss Harvester enable consistent delivery of holistic, tax - focused approach to overall financial wellness Wealth Management financial professionals need support acquiring new customers ▪ TaxAct has millions of customers, a portion of whom can be compelling client referrals to Avantax financial professionals ▪ TaxAct has sophisticated marketing capabilities that can be deployed to drive potential new client referrals to Avantax financial professionals There are ~21,000 TaxAct professionals who can build stronger relationships with their clients and generate incremental revenue by extending their services into wealth management ▪ By converting to Avantax Financial Professionals , TaxAct professionals have an opportunity to gain a material, year - round revenue stream ▪ Increases potential for customer retention if TaxAct professionals can provide tax focused wealth management services for their clients Our expertise in tax, software and wealth management creates opportunities to help all our core clients 22 Needs and Opportunities in our Client Base Blucora Solution and Benefits

The Board Became Increasingly Concerned About the Company’s Performance in 2019

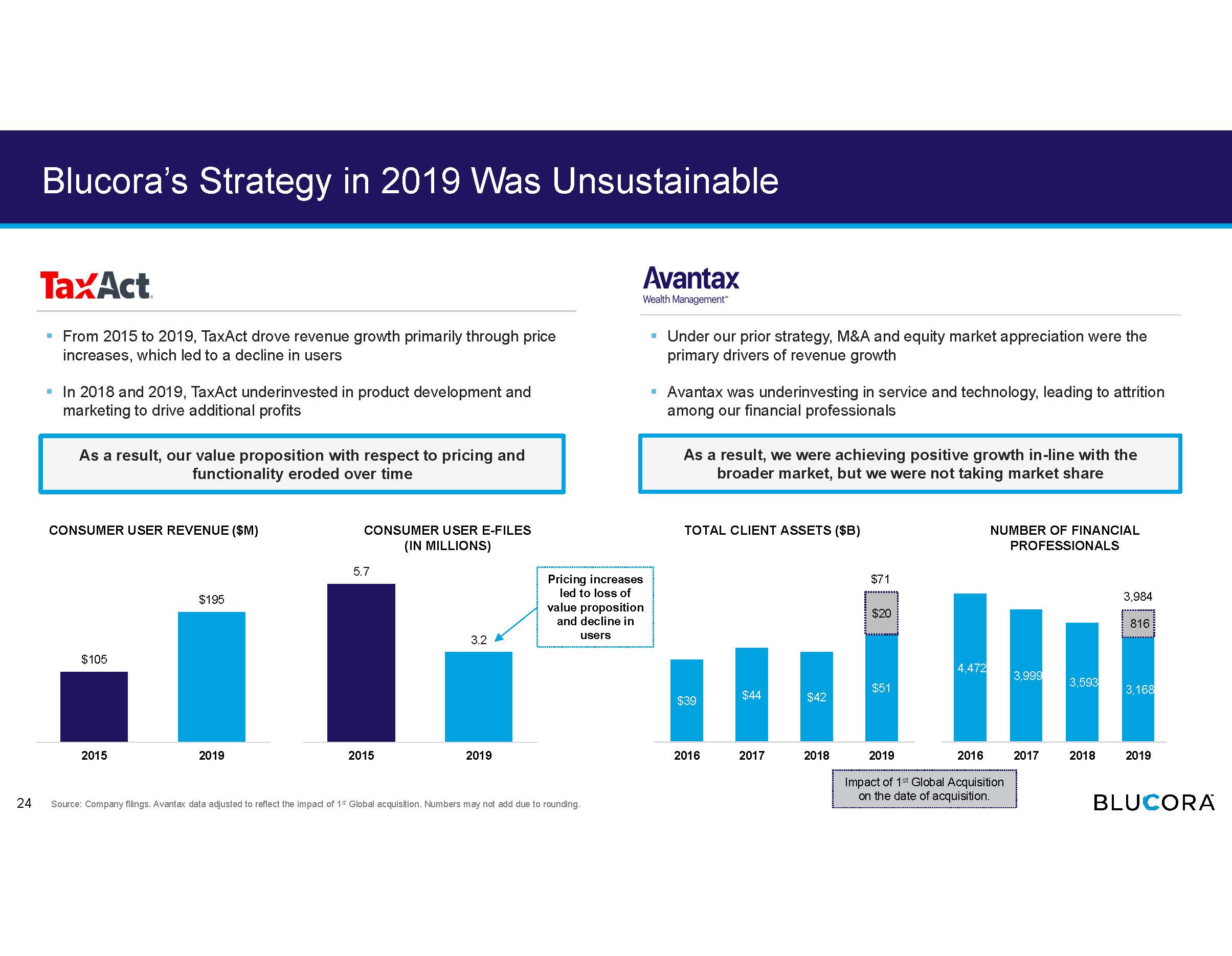

Blucora’s Strategy in 2019 Was Unsustainable CONSUMER USER REVENUE ($M) CONSUMER USER E - FILES (IN MILLIONS) $105 $195 2015 2019 5.7 3.2 2015 2019 ▪ From 2015 to 2019, TaxAct drove revenue growth primarily through price increases, which led to a decline in users ▪ In 2018 and 2019, TaxAct underinvested in product development and marketing to drive additional profits ▪ Under our prior strategy, M&A and equity market appreciation were the primary drivers of revenue growth ▪ Avantax was underinvesting in service and technology, leading to attrition among our financial professionals Pricing increases led to loss of value proposition and decline in users TOTAL CLIENT ASSETS ($B) NUMBER OF FINANCIAL PROFESSIONALS Source: Company filings. Avantax data adjusted to reflect the impact of 1 st Global acquisition. Numbers may not add due to rounding. As a result, our value proposition with respect to pricing and functionality eroded over time As a result, we were achieving positive growth in - line with the broader market, but we were not taking market share 24 3,984 $71 Impact of 1 st Global Acquisition on the date of acquisition. 4,472 3,999 3,593 3,168 816 2016 2017 2018 2019 $39 $44 $42 $51 $20 2016 2017 2018 2019

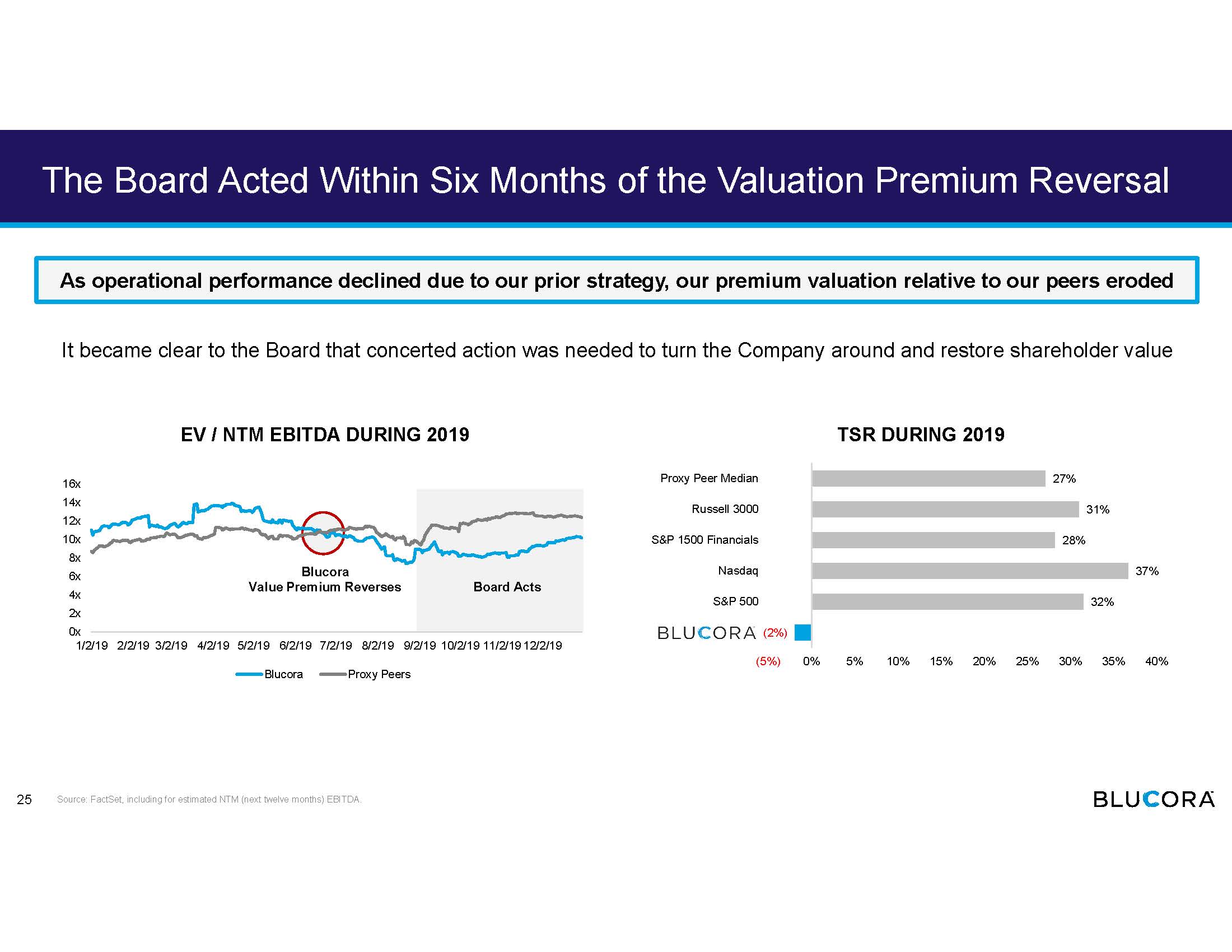

The Board Acted Within Six Months of the Valuation Premium Reversal EV / NTM EBITDA DURING 2019 TSR DURING 2019 It became clear to the Board that concerted action was needed to turn the Company around and restore shareholder value Source: FactSet, including for estimated NTM (next twelve months) EBITDA. 0x 2x 4x 6x 8x 10x 12x 14x 16x 1/2/19 2/2/19 3/2/19 4/2/19 5/2/19 6/2/19 7/2/19 8/2/19 9/2/19 10/2/19 11/2/19 12/2/19 Blucora Proxy Peers (2%) 32% 37% 28% 31% 27% (5%) 0% 5% 10% 15% 20% 25% 30% 35% 40% S&P 500 Nasdaq S&P 1500 Financials Russell 3000 Proxy Peer Median Board Acts Blucora Value Premium Reverses As operational performance declined due to our prior strategy, our premium valuation relative to our peers eroded 25

Board’s Aggressive Reset Has Put Blucora on the Right Track Source: FactSet. Data as of March 18, 2021. 1 2 3 4 2016 to September 2019 Growth fueled by unsustainable pricing/M&A September 2019 to January 2020 Board acts January 2020 to September 2020 Turbulence during pandemic September 2020 to Present Momentum as turnaround shows progress ▪ Loss of competitive advantage as the low - cost, value - oriented provider in the tax preparation space as prices increased ▪ Wealth management growth was fueled by M&A and market appreciation ▪ At a four - day strategy session, the Board begins to put into motion plans to change leadership and support a refined strategy ▪ Board replaces management team, supports management’s strategy and begins Board refreshment ▪ The IRS’ decision to extend the 2020 tax deadline from April 15 to July 15 results in significant and unplanned increased spe ndi ng on marketing and call center staff ▪ Decrease in federal funds rate to at or near zero negatively affects wealth management revenue and profitability ▪ Board continues refreshment ▪ Positive momentum in each business and across the Company ▪ Stock has outperformed the peers during this period $0 $5 $10 $15 $20 $25 $30 $35 $40 $45 12/31/15 12/31/16 12/31/17 12/31/18 12/31/19 12/31/20 2016 to September ‘19 TaxAct growth fueled by unsustainable pricing Wealth Management fueled by M&A Sept. ‘19 to Jan. ‘20 Board acts Jan ’20. to Sep. ‘20 Turbulence during Pandemic Sep ’20. to Present Momentum as turnaround shows progress 1 2 3 4 New CEO Appointed 1 - 30 - 2020 26

The Board Made Decisive Changes to Management and Board Composition and Oversaw a Refinement in Strategy

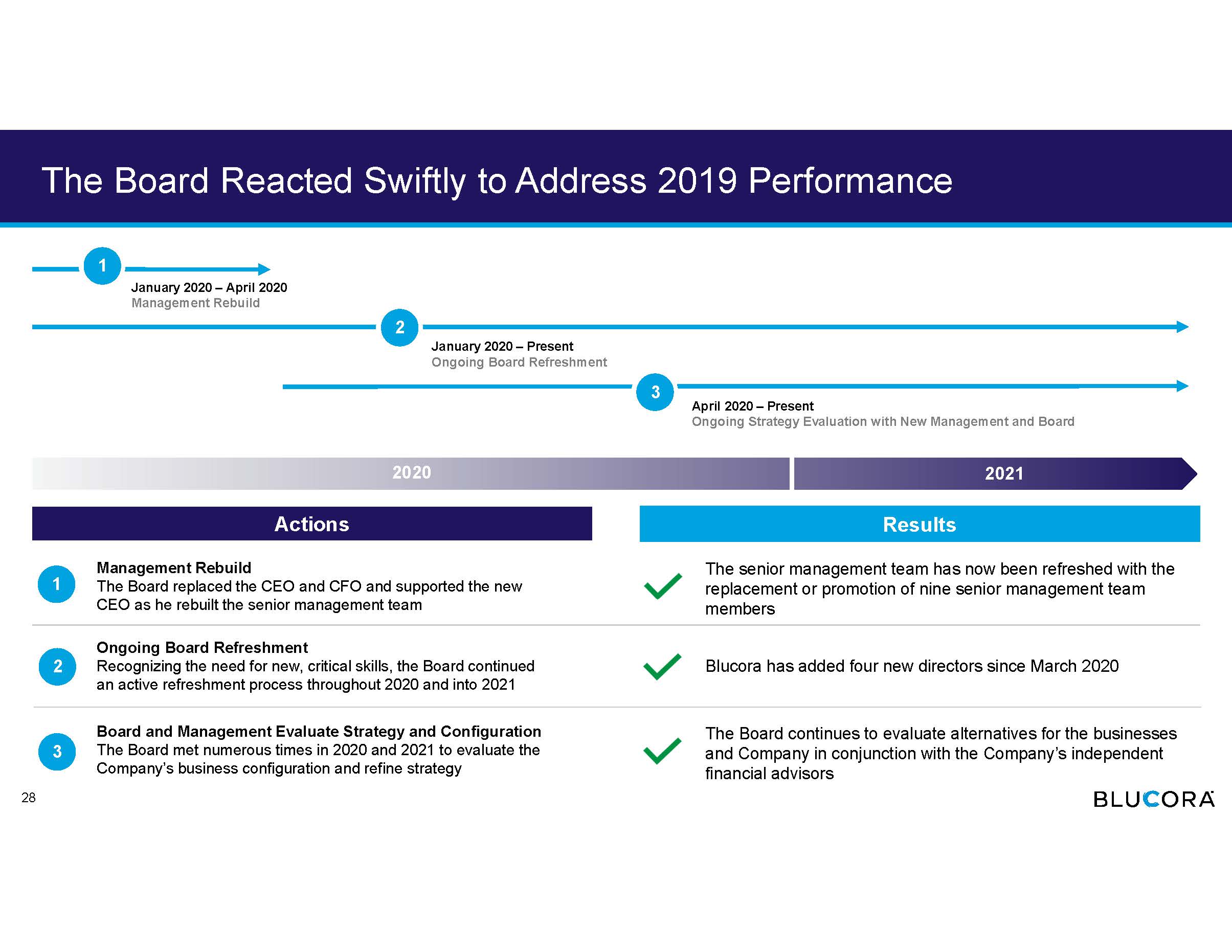

The Board Reacted Swiftly to Address 2019 Performance 28 2020 2021 1 3 2 April 2020 – Present Ongoing Strategy Evaluation with New Management and Board January 2020 – Present Ongoing Board Refreshment January 2020 – April 2020 Management Rebuild 1 2 3 Actions Results Management Rebuild The Board replaced the CEO and CFO and supported the new CEO as he rebuilt the senior management team Board and Management Evaluate Strategy and Configuration The Board met numerous times in 2020 and 2021 to evaluate the Company’s business configuration and refine strategy Ongoing Board Refreshment Recognizing the need for new, critical skills, the Board continued an active refreshment process throughout 2020 and into 2021 The senior management team has now been refreshed with the replacement or promotion of nine senior management team members The Board continues to evaluate alternatives for the businesses and Company in conjunction with the Company’s independent financial advisors Blucora has added four new directors since March 2020

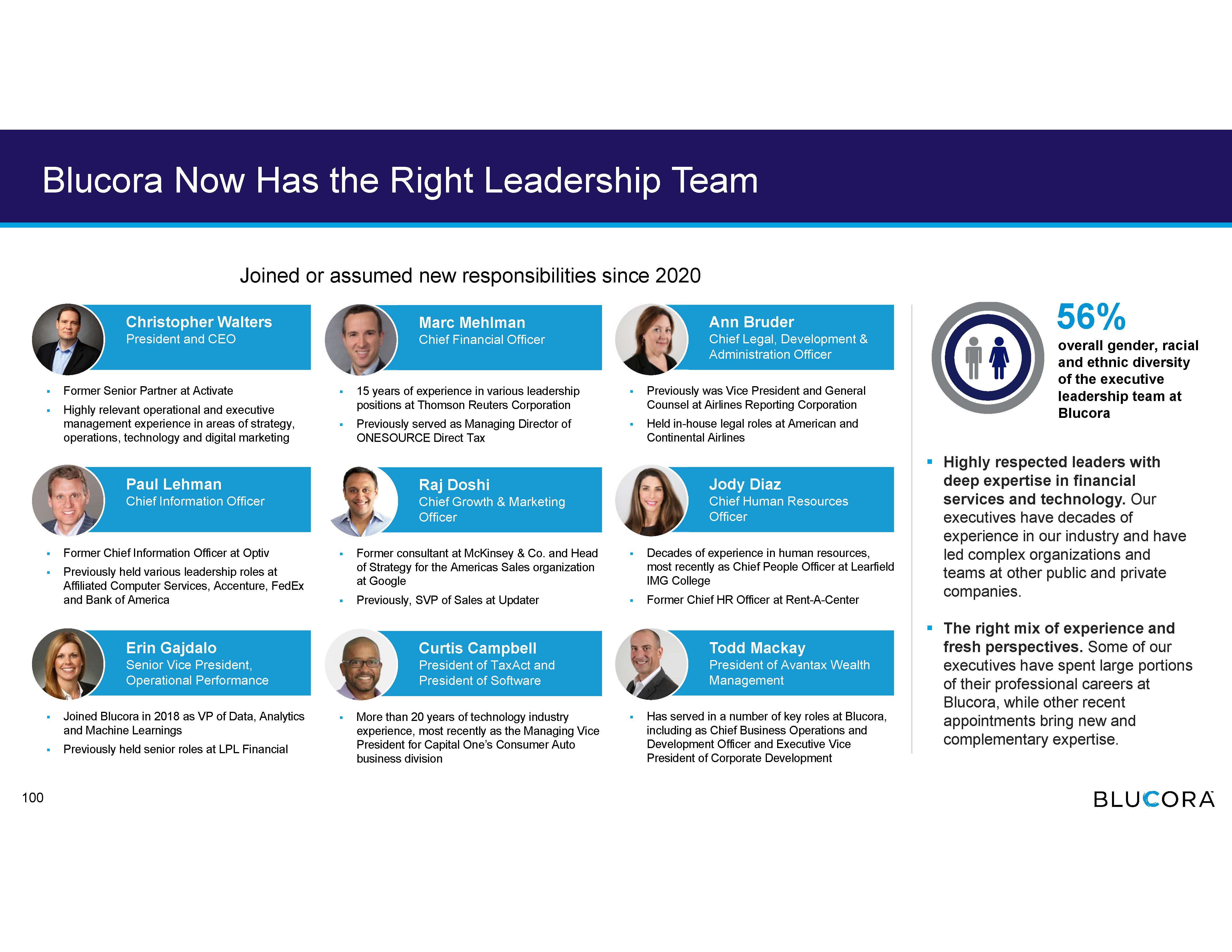

Blucora Has a Rebuilt Management Team DECEMBER 2019 John Clendening CEO Davinder Athwal CFO Ann Bruder Chief Legal Officer & Secretary Todd Mackay Chief Business Operations and Development Officer Mike Hogan Chief Marketing Officer Enrique Vazquez President of Wealth Management Curtis Campbell President of TaxAct Tran Taylor Chief Human Resources Officer Christopher Walters CEO 2020 1 Marc Mehlman CFO 2020 Ann Bruder Chief Legal & Administration Officer 2017 2 Paul Lehman Chief Information Officer 2020 Raj Doshi Chief Growth & Marketing Officer 2020 Jody Diaz Chief Human Resources Officer 2020 Erin Gajdalo Sr. Vice President, Operational Performance 2018 2 Curtis Campbell President of TaxAct and President of Software 2018 2 Todd Mackay President of Avantax Wealth Management 2019 2 Source: Company filings and LinkedIn. 1 Mr. Walters has also served on the Board since 2014. 2 Promoted to new role and/or assumed additional responsibilities in 2020. 1 In January and April 2020, we did a “hard reset” of our management team and organizational structure in order to add and promote new talent, streamline our management and ensure accountability DECEMBER 2020 29

Why Christopher Walters is the Right CEO to Lead Blucora Now 1 30 Christopher Walters President & CEO Since January 30, 2020 Board Member since 2014 ▪ Understanding of the Board’s concerns and his familiarity with the businesses positioned him to make rapid progress on a turnaround ▪ As a leading critic of the prior management team and its ability to execute the strategy , Mr. Walters had a strong point of view about what refinements needed to be made to the strategy, culture and execution to realize the Company’s potential ▪ Demonstrated executive leadership success with a history of driving performance improvement and growth fueled by technology and data ▪ Extensive experience driving large - scale technology development initiatives that included leading applications for businesses and consumers ▪ Deep knowledge of media and marketing, which is critical to drive growth in both of Blucora’s businesses and is the Company’s second largest expense after compensation of employees and financial professionals ▪ Ability to recruit a strong management team ▪ Experience navigating the federal government based on founding Bloomberg Government, which has become one of the most important digital information sources in Washington DC – experience is valuable given the regulated nature of both businesses ▪ Significant knowledge of the tax industry based on six years on the Blucora board and the acquisition and integration of BNA, one of the leading providers of tax information and software while at Bloomberg ▪ Broad knowledge of the financial services industry . Leadership experience at Bloomberg, one of the leading providers of information and technology services to the financial services sector including traders, wealth and asset managers – information and tools used by more than 300,000 decision makers in the financial services space every day and media properties informed millions of leaders in the financial sector The Board determined Mr. Walters was the best choice for the CEO role: Blucora’s Board considered potential external and internal candidates with the assistance of a top - tier executive search firm

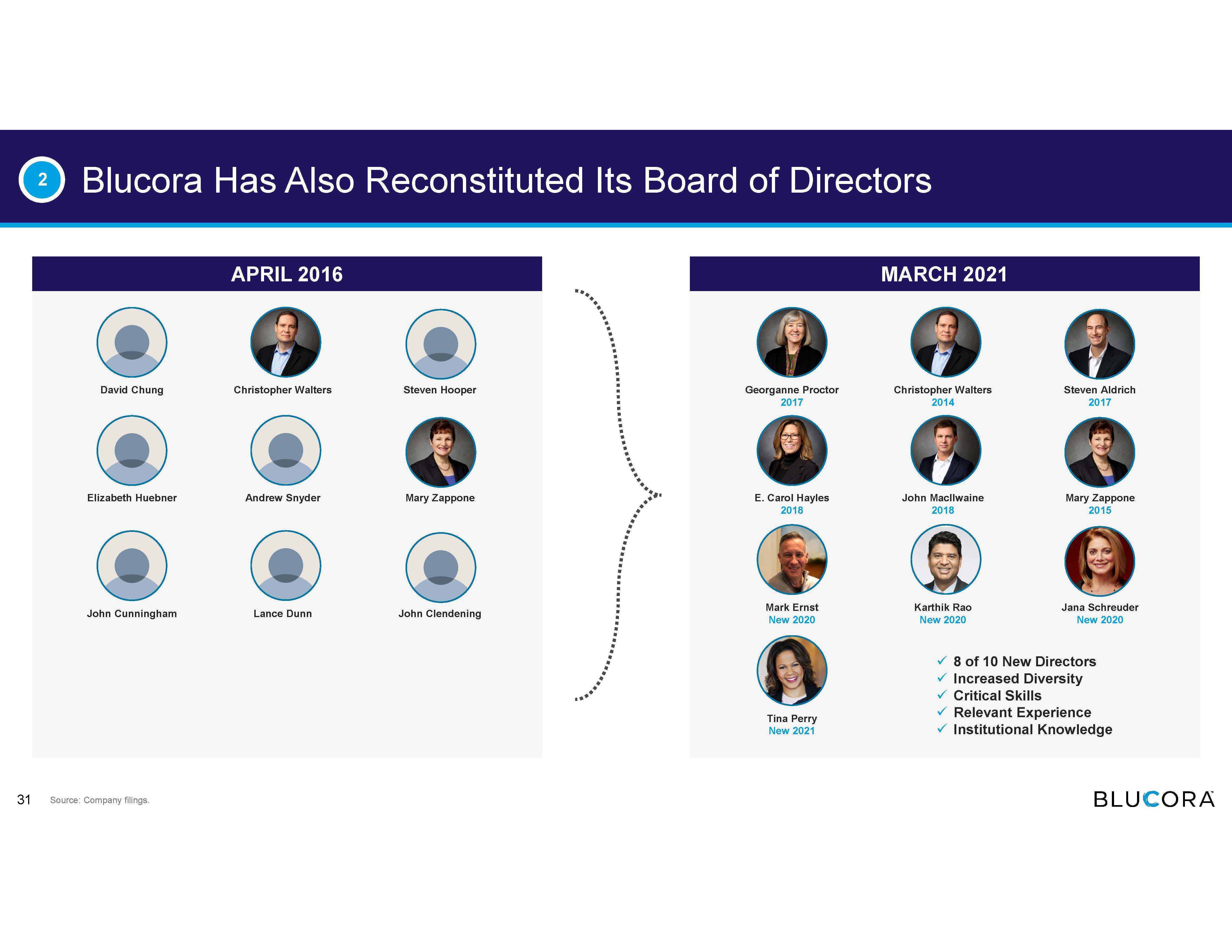

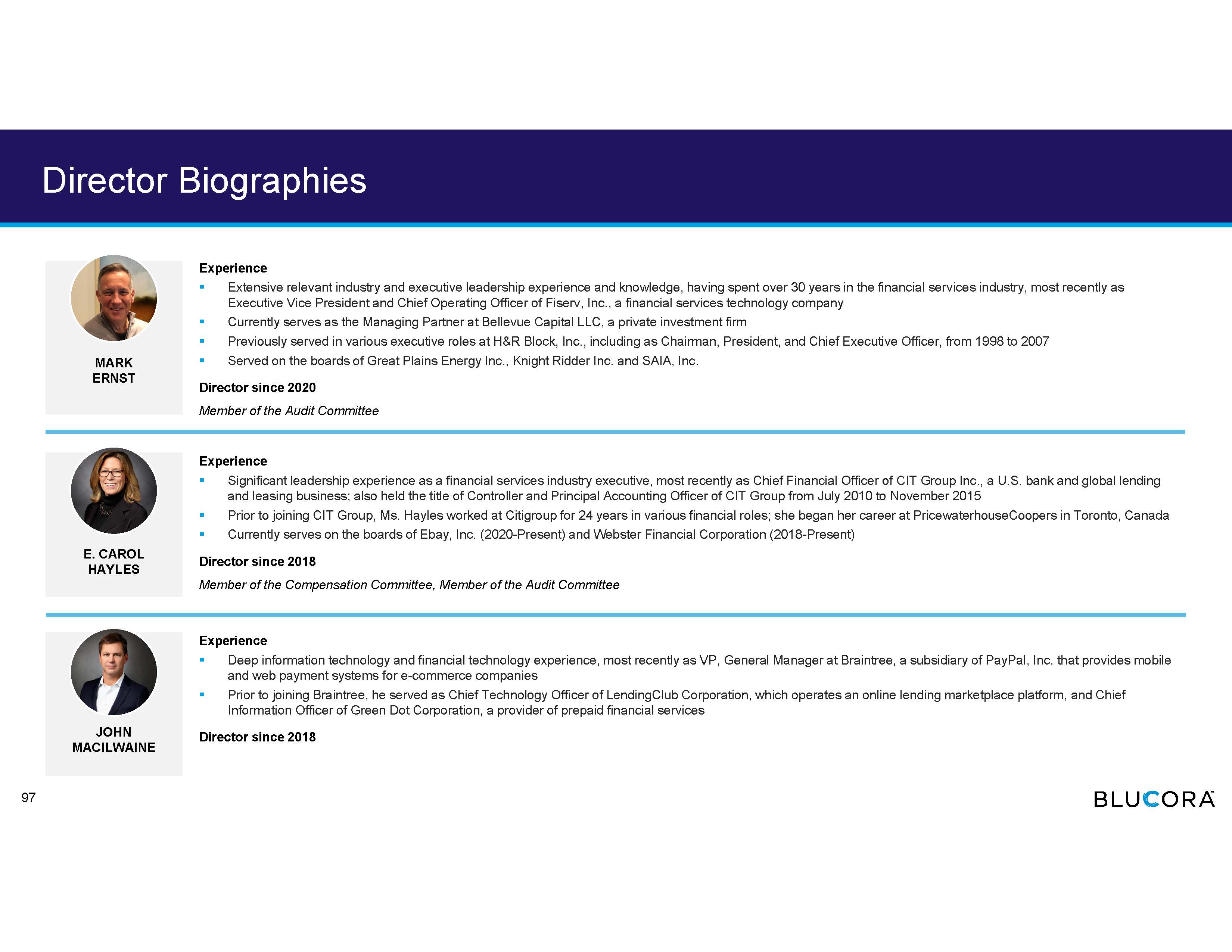

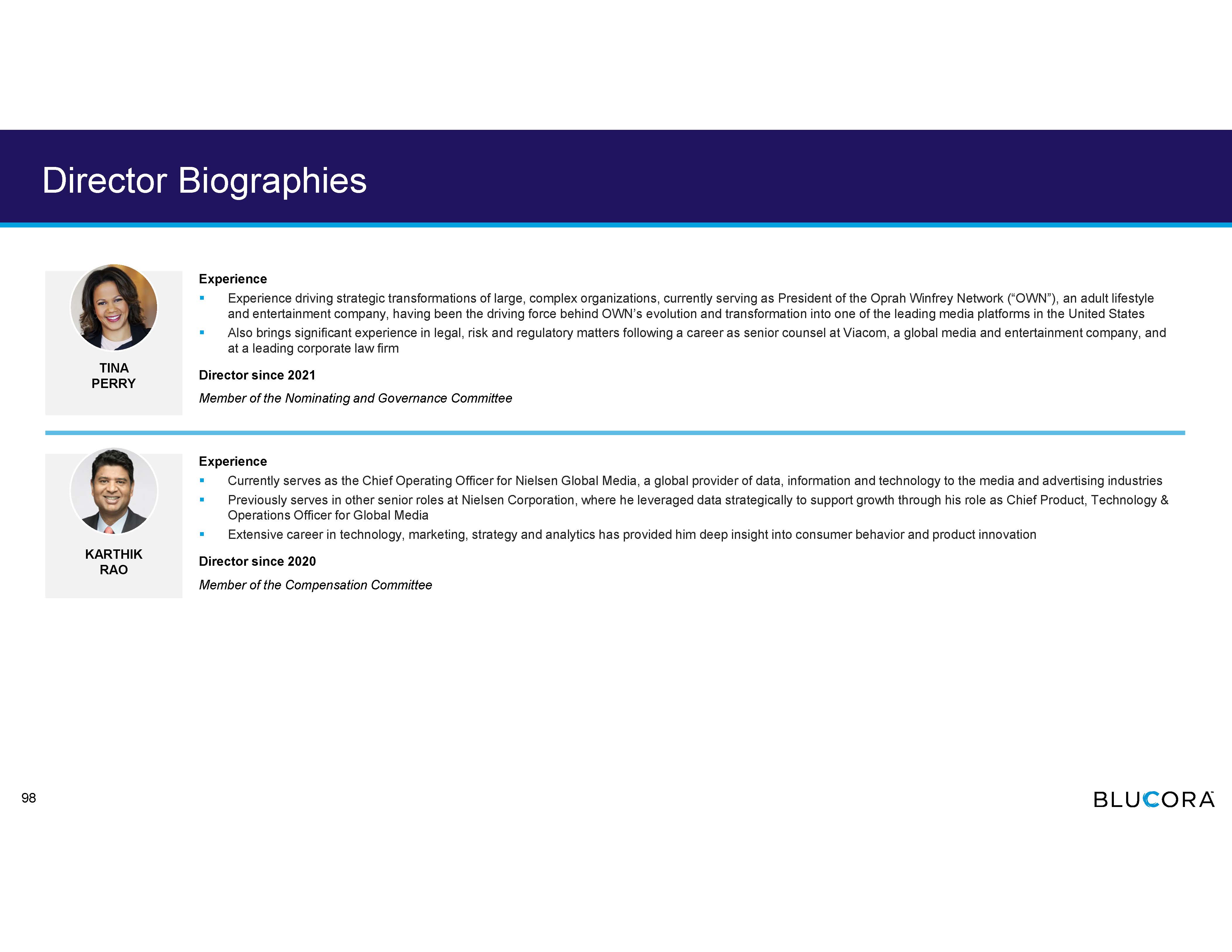

APRIL 2016 MARCH 2021 David Chung Christopher Walters Steven Hooper Elizabeth Huebner Andrew Snyder Mary Zappone John Cunningham Lance Dunn John Clendening x 8 of 10 New Directors x Increased Diversity x Critical Skills x Relevant Experience x Institutional Knowledge Source: Company filings. Blucora Has Also Reconstituted Its Board of Directors 2 Georganne Proctor 2017 Christopher Walters 2014 Steven Aldrich 2017 E. Carol Hayles 2018 John MacIlwaine 2018 Mary Zappone 2015 Mark Ernst New 2020 Karthik Rao New 2020 Jana Schreuder New 2020 Tina Perry New 2021 31

DIRECTORS ADDED SINCE 2020 ENHANCED SKILL SETS Wealth Management Tax Digital / Technology / Software Strategy / Turnaround Audit / Finance / Risk Sales / Marketing Human Capital Public Company Board Executive Leadership ▪ Former EVP and COO of Fiserv , a financial services technology company, Deputy Commissioner at the IRS and former CEO of H&R Block ▪ 30 - year career in the financial services industry, including the tax preparation business, as well as operational, capital allocation, and strategy development experience ▪ Chief Operating Officer of Nielsen Global Media , a global provider of data, information and technology ▪ Background in driving product innovation; deep technology and operational expertise ▪ Former EVP and COO of Northern Trust Corporation , a financial services company ▪ Extensive technology, operations and wealth management experience ▪ President of OWN : Oprah Winfrey Network , a leading cable channel and media company ▪ Experience successfully leading turnaround initiatives, fostering healthy organizational cultures and driving growth Recent Board Appointments Bring Relevant Skills and Experiences 2 Each of our recent Board appointments is the culmination of a thoughtful refreshment process and followed a months - long vetting process to assess their skills, qualifications and strategic fit Karthik Rao Director Since 2020 Tina Perry Director Since 2021 Mark Ernst Director Since 2020 Jana Schreuder Director Since 2020 Audit Committee Nominating and Governance Committee Compensation Committee Compensation Committee (Chair) 32

Extracted from the Board of Directors’ Strategy Meetings ▪ In March 2020 , the Board considered the Company’s strategy and, in particular, which businesses were critical to the Company’s portfolio ▪ In May and June 2020, at the direction of the Board, the Company undertook an in - depth review of the Company’s strategy, financing options and configuration, with the assistance of two separate independent financial advisors ▪ In September 2020 , the Board reviewed with management the strategy with respect to each of the Company’s businesses and the Company’s configuration and alternatives, with the assistance of one of the Company’s independent financial advisors ▪ In November 2020 , the Board continued the strategic review session that had commenced in September 2020. Over the course of three days, the Board conducted a comprehensive review of the Company’s businesses, configuration and alternatives, with the assistance of one of the Company’s independent financial advisors ▪ In February 2021, the Board received input from two independent financial advisors with respect to alternatives to the Company’s current strategy, configuration and capital allocation The Board Has Actively Reviewed the Company’s Strategy and Configuration 3 33

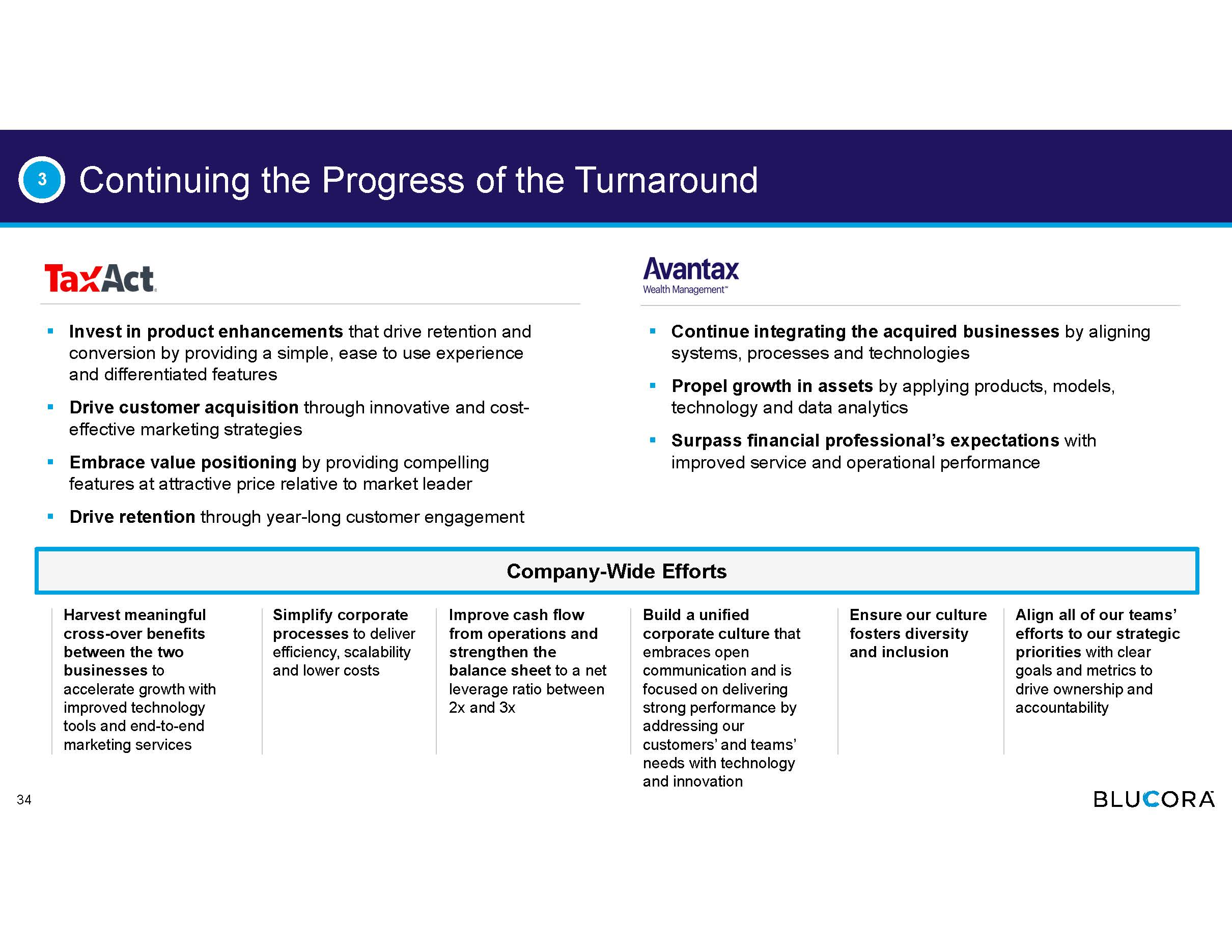

▪ Invest in product enhancements that drive retention and conversion by providing a simple, ease to use experience and differentiated features ▪ Drive customer acquisition through innovative and cost - effective marketing strategies ▪ Embrace value positioning by providing compelling features at attractive price relative to market leader ▪ Drive retention through year - long customer engagement ▪ Continue integrating the acquired businesses by aligning systems, processes and technologies ▪ Propel growth in assets by applying products, models, technology and data analytics ▪ Surpass financial professional’s expectations with improved service and operational performance Continuing the Progress of the Turnaround 3 34 Harvest meaningful cross - over benefits between the two businesses to accelerate growth with improved technology tools and end - to - end marketing services Simplify corporate processes to deliver efficiency, scalability and lower costs Improve cash flow from operations and strengthen the balance sheet to a net leverage ratio between 2x and 3x Build a unified corporate culture t hat embraces open communication and is focused on delivering strong performance by addressing our customers’ and teams’ needs with technology and innovation Ensure our culture fosters diversity and inclusion Align all of our teams’ efforts to our strategic priorities with clear goals and metrics to drive ownership and accountability Company - Wide Efforts

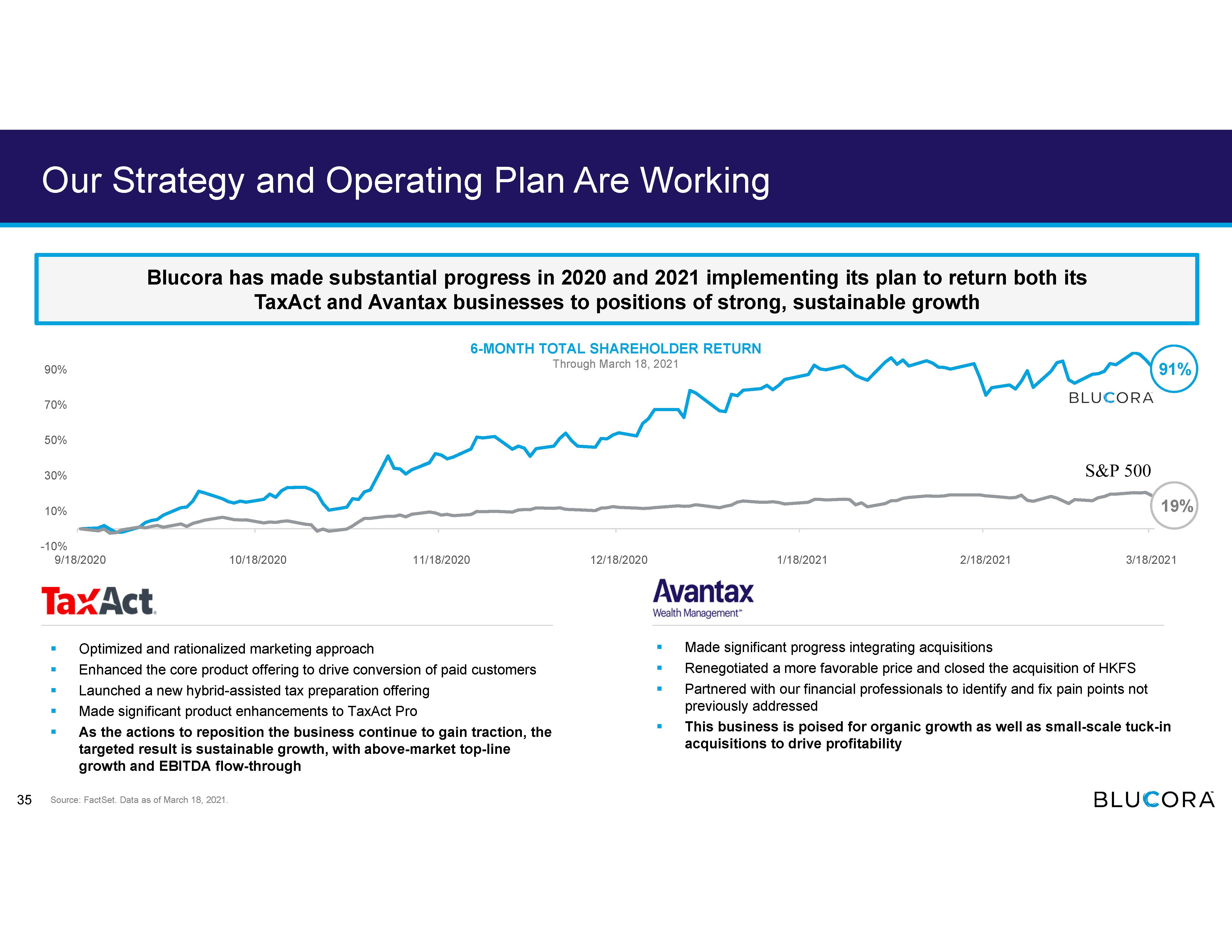

-10% 10% 30% 50% 70% 90% 9/18/2020 10/18/2020 11/18/2020 12/18/2020 1/18/2021 2/18/2021 3/18/2021 Our Strategy and Operating Plan Are Working ▪ Optimized and rationalized marketing approach ▪ Enhanced the core product offering to drive conversion of paid customers ▪ Launched a new hybrid - assisted tax preparation offering ▪ Made significant product enhancements to TaxAct Pro ▪ As the actions to reposition the business continue to gain traction, the targeted result is sustainable growth, with above - market top - line growth and EBITDA flow - through ▪ Made significant progress integrating acquisitions ▪ Renegotiated a more favorable price and closed the acquisition of HKFS ▪ Partnered with our financial professionals to identify and fix pain points not previously addressed ▪ This business is poised for organic growth as well as small - scale tuck - in acquisitions to drive profitability Source: FactSet. Data as of March 18, 2021. Blucora has made substantial progress in 2020 and 2021 implementing its plan to return both its TaxAct and Avantax businesses to positions of strong, sustainable growth 91% 6 - MONTH TOTAL SHAREHOLDER RETURN Through March 18, 2021 35 19%

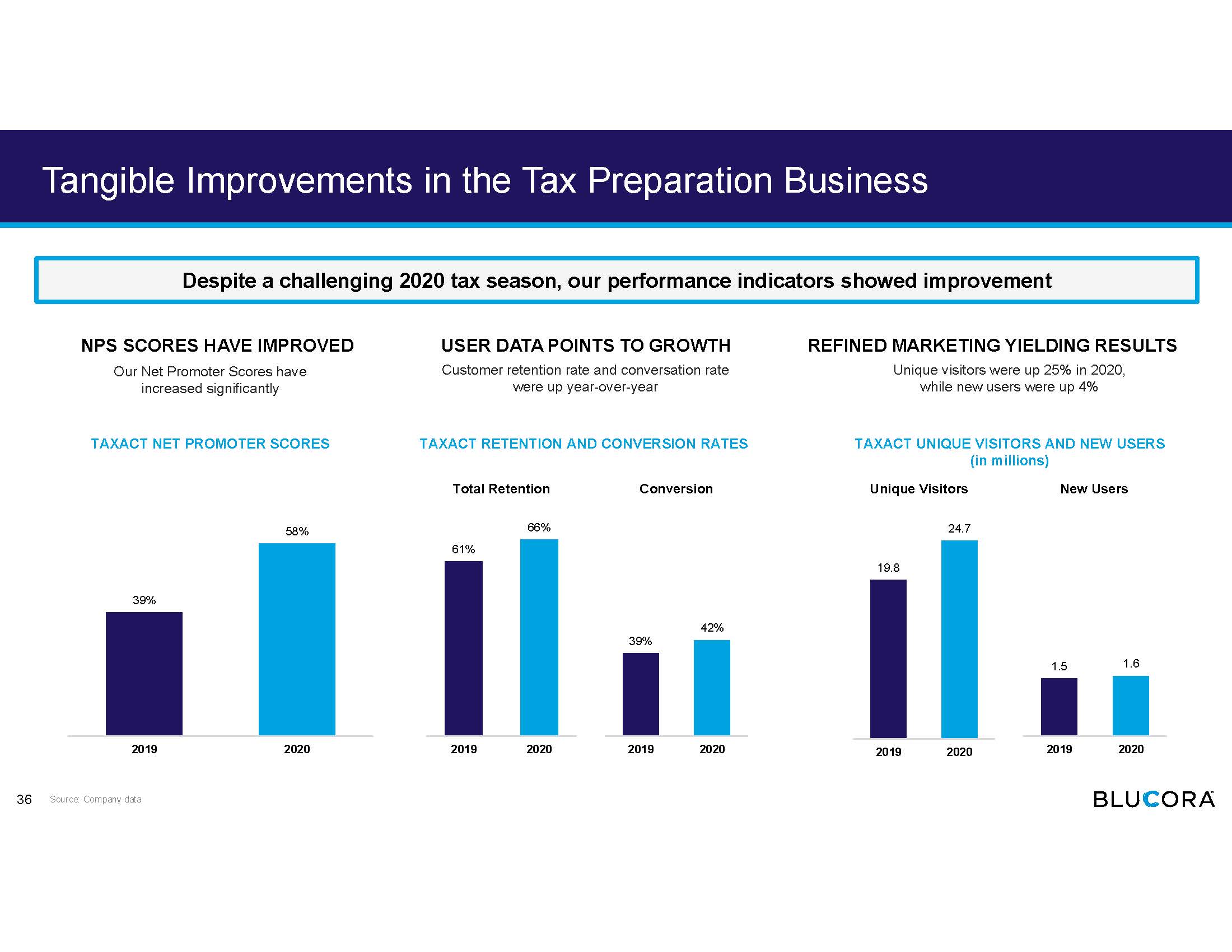

Tangible Improvements in the Tax Preparation Business 19.8 24.7 2019 2020 39% 42% 2019 2020 Source: Company data 1.5 1.6 2019 2020 61% 66% 2019 2020 Despite a challenging 2020 tax season, our performance indicators showed improvement Customer retention rate and conversation rate were up year - over - year NPS SCORES HAVE IMPROVED TAXACT NET PROMOTER SCORES REFINED MARKETING YIELDING RESULTS USER DATA POINTS TO GROWTH TAXACT RETENTION AND CONVERSION RATES TAXACT UNIQUE VISITORS AND NEW USERS (in millions) Our Net Promoter Scores have increased significantly Unique visitors were up 25% in 2020, while new users were up 4% 36 Total Retention Conversion Unique Visitors New Users 39% 58% 2019 2020

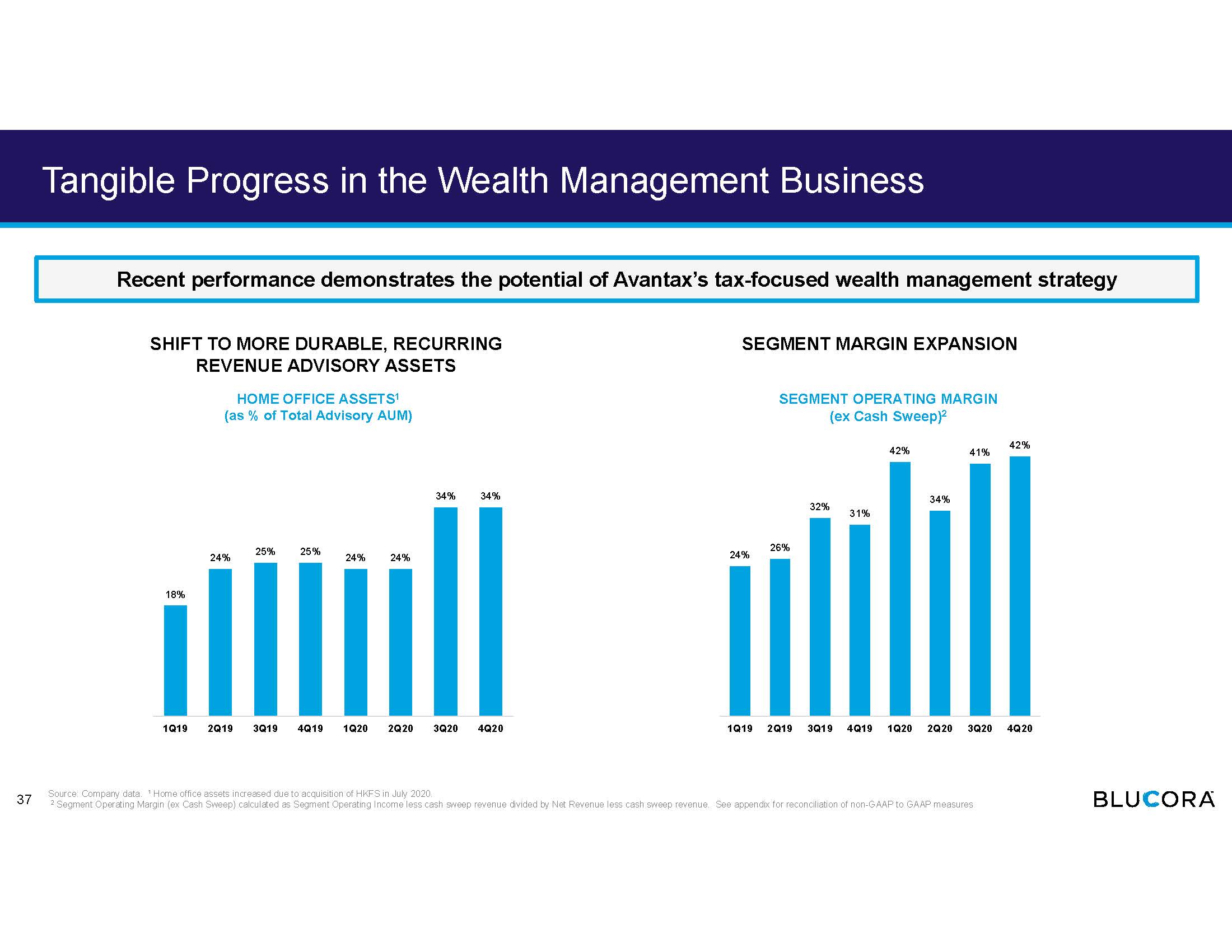

Tangible Progress in the Wealth Management Business Source: Company data. ¹ Home office assets increased due to acquisition of HKFS in July 2020. 2 Segment Operating Margin (ex Cash Sweep) calculated as Segment Operating Income less cash sweep revenue divided by Net Revenu e less cash sweep revenue. See appendix for reconciliation of non - GAAP to GAAP measures Recent performance demonstrates the potential of Avantax’s tax - focused wealth management strategy SHIFT TO MORE DURABLE, RECURRING REVENUE ADVISORY ASSETS HOME OFFICE ASSETS 1 (as % of Total Advisory AUM) 37 SEGMENT OPERATING MARGIN (ex Cash Sweep) 2 SEGMENT MARGIN EXPANSION 24% 26% 32% 31% 42% 34% 41% 42% 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 18% 24% 25% 25% 24% 24% 34% 34% 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20

We Retain a High - Level of Financial Professionals and Revenues Source: Company data 1 Reflects retention of commission and advisory revenues of independent Financial Professionals (“FPs”), calculated by deductin g t he prior year production of the annualized year - to - year attrition rate, over the prior year total production. Production is advisor - driven revenue the includes transactions, trailers and fee - based revenue RETENTION OF HIGH - PRODUCING FINANCIAL PROFESSIONALS ATTRITION OF FPs BY REVENUE PRODUCTION (2019 – 2020) 38 PRODUCTION RETENTION RATE 1 99% 99% 99% 98% 99% 98% 99% 96% 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 82% 6% 12% < $50k $50k to $100k > $100k ATTRITION IS PRIMARILY DRIVEN BY FOUR FACTORS: 1. An affirmative determination to cull inactive and less productive FPs to improve overall profitability 2. Expected post - acquisition attrition, which is a standard feature in the industry (and predictably runs at 10 - 20% of FPs associated with businesses that are acquired). Avantax is trending better than the industry’s post - acquisition attrition rate 3. Some tax professionals that add wealth management services later determine they prefer to refocus on tax 4. When tax professionals retire or leave wealth management, assets are often transferred to other financial professionals, reducing FP count but not assets in the business HIGH PORTION OF REVENUES ARE RETAINED Some attrition among Financial Professionals is natural, healthy for the business and expected 210 new Financial Professionals affiliated with Avantax in 2020

Pricing Models Position Avantax For Future Growth Source: Company data 39 OUR PRICING MODEL AIMS TO: ▪ Incentivize the shift to a more durable fee model, which is the future direction of the industry and allows for greater compliance oversight — Create potential for financial professionals to operate in a manner that offers the most diversified opportunity for financial planning and advisory for their clients — Offer competitive advisory and brokerage solutions that are distinct and compelling ▪ Harmonize the pricing across our consolidated businesses ▪ Encourages Financial Professionals to grow their business over time so that they can achieve higher payouts and have lower fees ▪ Align success of Financial Professionals with the success of Avantax Pricing strategies in Wealth Management are the result of extensive market studies and interaction with financial professionals, with a focus on maximizing value We balance offering industry leading pricing on our brokerage and advisory products and services with optimizing the economic value to the business that can be used for investments in Avantax and our Financial Professionals for future growth.”

We have spent a considerable amount of time with the current Avantax leadership team. They listen to us, and are always interested in our feedback. Though change is never easy, we have all the confidence in the world that this group is the right group to lead us into the future.” Our Financial Professionals Are Supportive of Our Progress 40 John Lammers MRK Financial Solutions What made me become an advocate of Avantax? Our colleagues at the home office who are always there and willing to assist us whether it be operational issues or client matters. Even though we are independent advisors, we are in the journey together.” Stan Warner Warner Finance I am thrilled with where Avantax is headed and the progress you all have made. I am particularly happy with the home office support I am getting which is the best it has been in 15 years.” Richard Reiser Chapter Director The transition has been incredible for us. We love Avantax and we love how things are going with the transition. The technology is much easier for us to navigate, service has been amazing… honestly, I couldn’t be happier.” Luke Funk Luke Funk Wealth Management My support has only grown as the bigger vision across the Blucora portfolio really seems to be hitting stride. My conviction is evident in our recent transition… I knew the right move was doubling - down and becoming a deeper - connected part of the vision of bringing what we do to even more families.” Davin Carey Avantax Planning Partners Avantax is defining the future of holistic financial planning. Their approach to tax - smart investment management puts them light years ahead of traditional advisors.” Stephen Moore KCS Wealth Advisors

COVID - 19 Has Temporarily Impacted Our Business Source: Company data. 1 Asset - based revenue primarily includes fees from financial product manufacturer sponsorship programs, cash sweep programs, and other asset - based revenues. Asset - based revenue excludes commission and advisory fee revenues. $23 $26 $31 $48 $24 2016 2017 2018 2019 2020 $46 $83 2019 2020 ▪ As a result of the COVID - 19 pandemic, the IRS extended the filing and payment deadline for tax year 2019 federal returns to July 15, 2020 ▪ The extension resulted in elevated sales and marketing expenses (in addition to previously committed marketing initiatives), and the longer season necessitated additional customer service costs TAXACT SALES & MARKETING EXPENSES ($M) BLUCORA ASSET - BASED REVENUE 1 ($M) ▪ The financial market disruption negatively impacted the value of some of our clients’ assets (in the first half of 2020), leading to a decline in our wealth management revenue ▪ With federal funds rate at ~ 0%, our cash sweep revenue declined 41

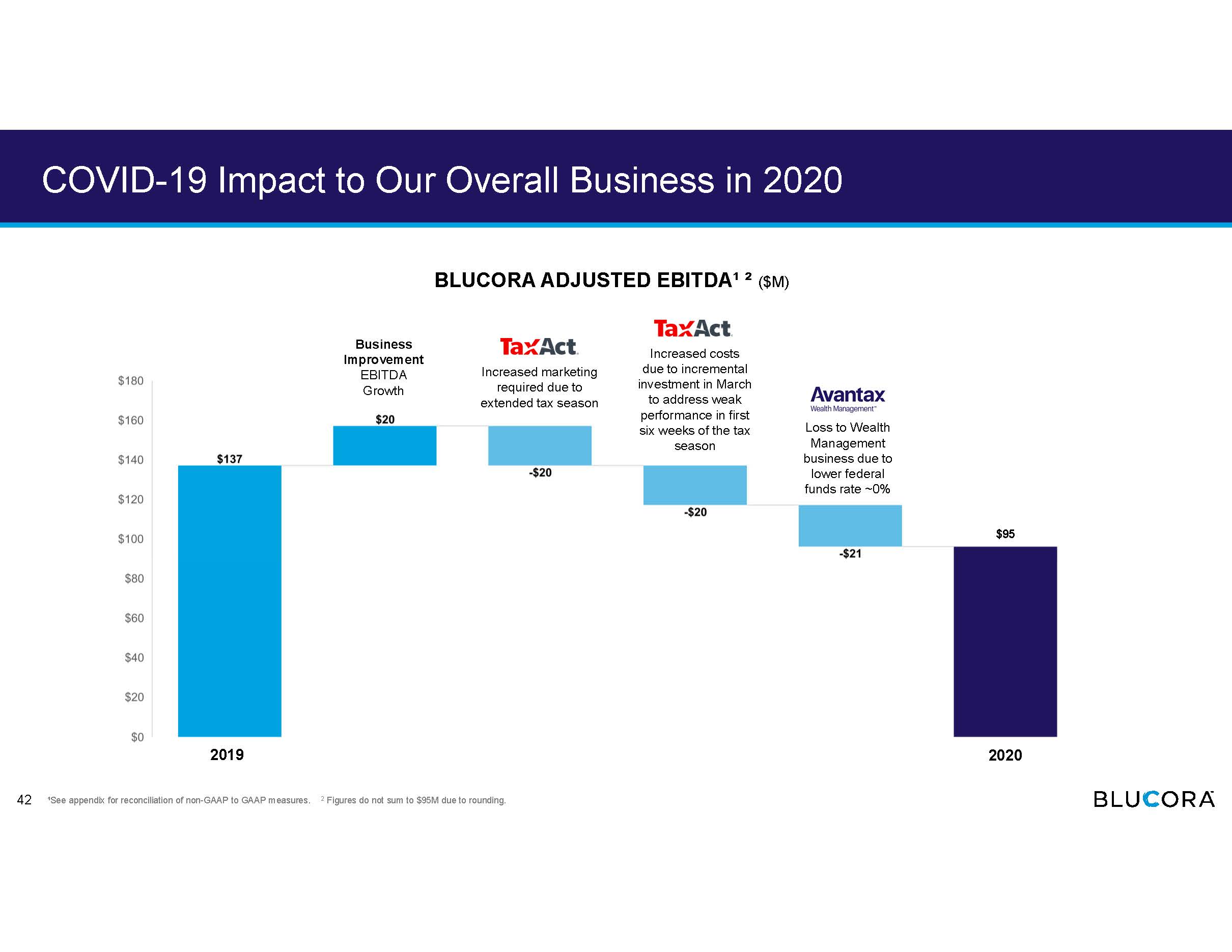

COVID - 19 Impact to Our Overall Business in 2020 42 BLUCORA ADJUSTED EBITDA ¹ ² ($M) 2019 Business Improvement EBITDA Growth Increased marketing required due to extended tax season Increased costs due to incremental investment in March to address weak performance in first six weeks of the tax season Loss to Wealth Management business due to lower federal funds rate ~0% 2020 ¹See appendix for reconciliation of non - GAAP to GAAP measures. 2 Figures do not sum to $95M due to rounding. $95

Blucora Has Carefully Considered and Managed Expenses Source: FactSet and Company filings. Data as of March 8, 2021. 3.8% 3.5% 2019 2020 4.3% 3.6% 2019 2020 17.6% 23.5% 2019 2020 Blucora is driving to an improved cost structure An extended 2020 tax season necessitated an increased marketing spend, but this should abate CORPORATE - LEVEL CORPORATE - LEVEL COSTS (as a % of revenue) ENGINEERING & TECHNOLOGY SALES & MARKETING SALES & MARKETING COSTS (as a % of revenue) ENGINEERING & TECHNOLOGY COSTS (as a % of revenue) Corporate - level general and administrative expense margin is lower than at any point in the last five years Improved efficiency in engineering and technology drove costs down even while continuing high - priority product enhancements 43

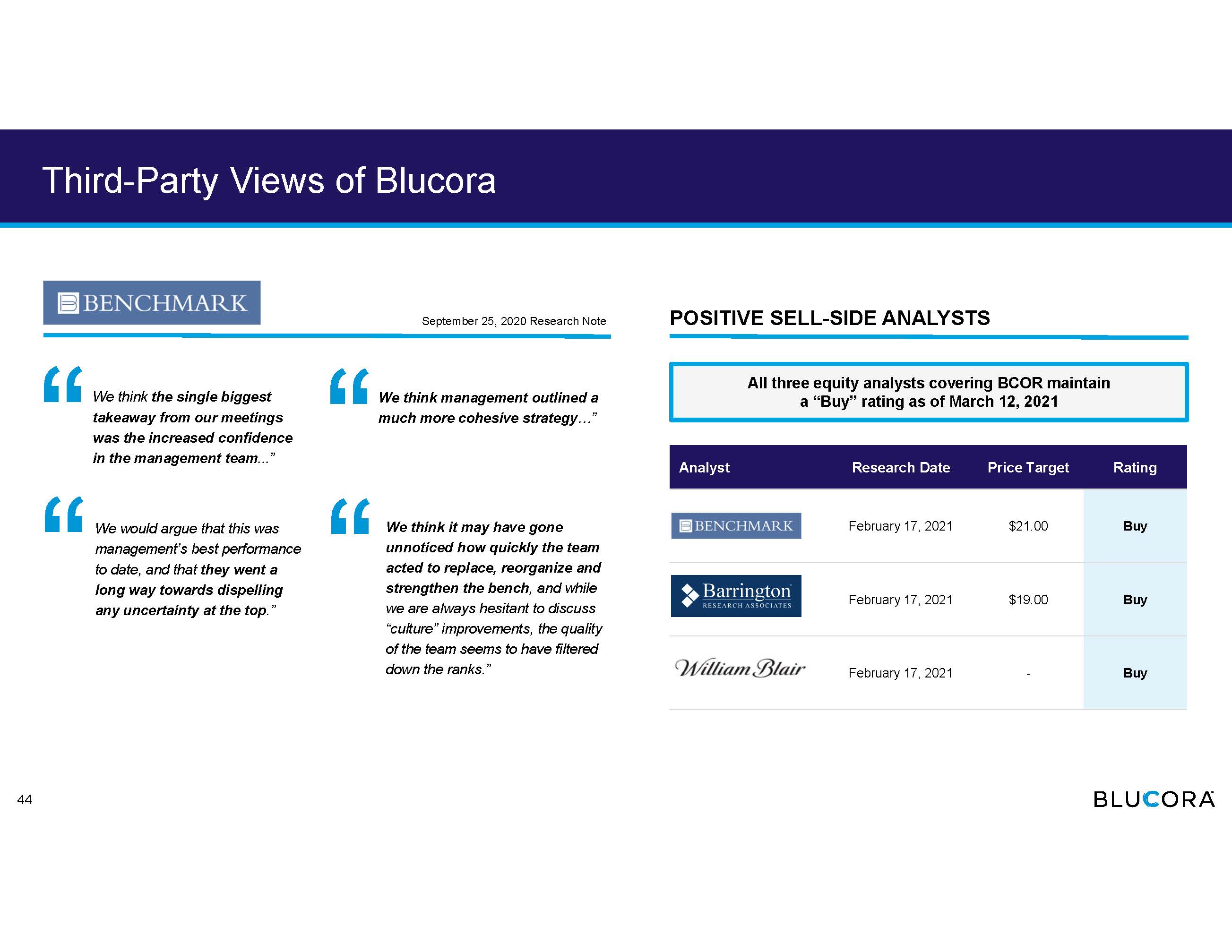

We think management outlined a much more cohesive strategy …” We think it may have gone unnoticed how quickly the team acted to replace, reorganize and strengthen the bench , and while we are always hesitant to discuss “culture” improvements, the quality of the team seems to have filtered down the ranks.” We think the single biggest takeaway from our meetings was the increased confidence in the management team ...” We would argue that this was management’s best performance to date, and that they went a long way towards dispelling any uncertainty at the top .” September 25, 2020 Research Note Analyst Research Date Price Target Rating February 17, 2021 $21.00 Buy February 17, 2021 $19.00 Buy February 17, 2021 - Buy POSITIVE SELL - SIDE ANALYSTS Third - Party Views of Blucora All three equity analysts covering BCOR maintain a “Buy” rating as of March 12, 2021 44

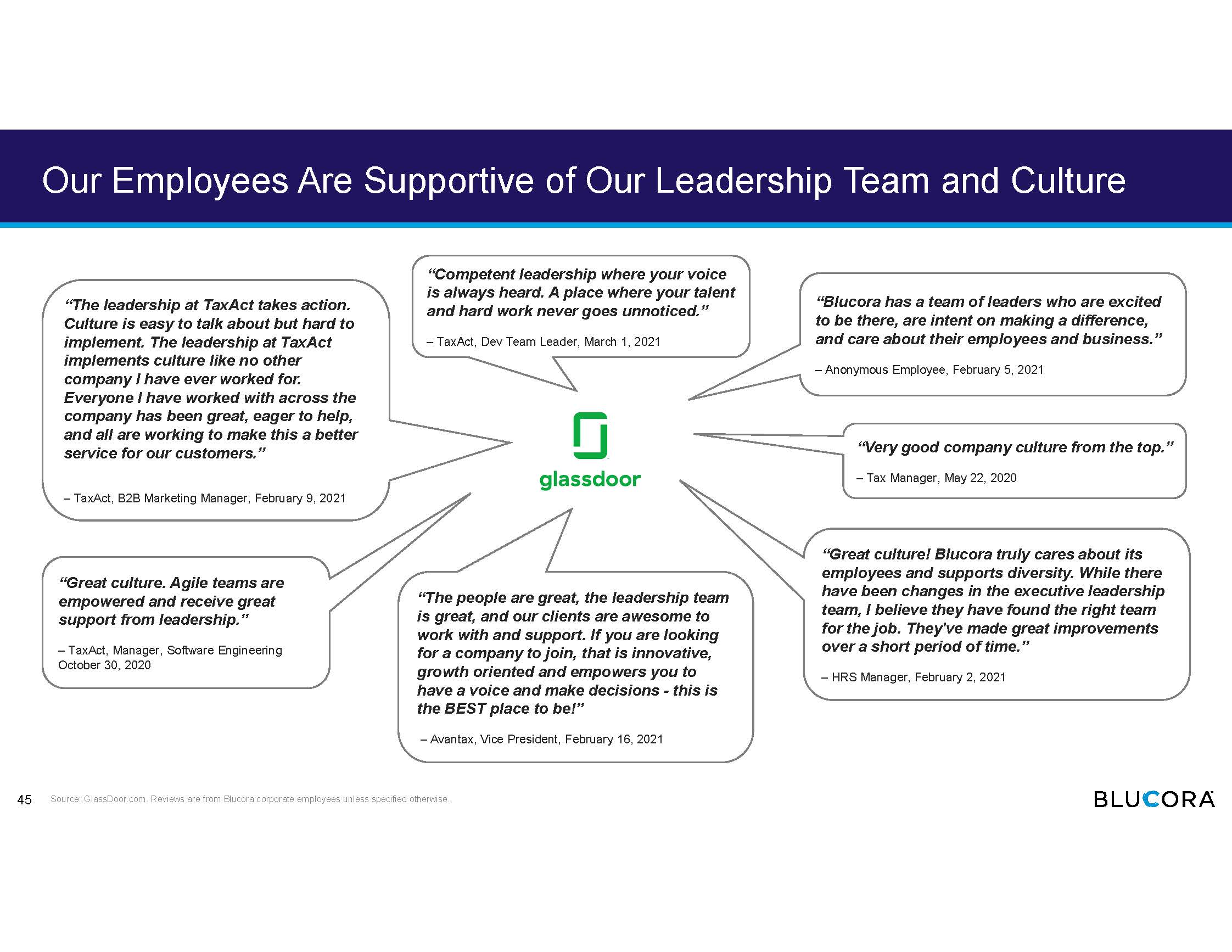

Our Employees Are Supportive of Our Leadership Team and Culture “The leadership at TaxAct takes action. Culture is easy to talk about but hard to implement. The leadership at TaxAct implements culture like no other company I have ever worked for. Everyone I have worked with across the company has been great, eager to help, and all are working to make this a better service for our customers.” – TaxAct, B2B Marketing Manager, February 9, 2021 Source: GlassDoor.com . Reviews are from Blucora corporate employees unless specified otherwise. “ Blucora has a team of leaders who are excited to be there, are intent on making a difference, and care about their employees and business.” – Anonymous Employee, February 5, 2021 “Great culture. Agile teams are empowered and receive great support from leadership.” – TaxAct, Manager, Software Engineering October 30, 2020 “Competent leadership where your voice is always heard. A place where your talent and hard work never goes unnoticed.” – TaxAct, Dev Team Leader, March 1, 2021 “Very good company culture from the top.” – Tax Manager, May 22, 2020 “The people are great, the leadership team is great, and our clients are awesome to work with and support. If you are looking for a company to join, that is innovative, growth oriented and empowers you to have a voice and make decisions - this is the BEST place to be!” – Avantax, Vice President, February 16, 2021 “Great culture! Blucora truly cares about its employees and supports diversity. While there have been changes in the executive leadership team, I believe they have found the right team for the job. They've made great improvements over a short period of time.” – HRS Manager, February 2, 2021 45

Blucora has the Right Board and Governance to Drive Change and Growth

Blucora’s Board Has the Skills Needed to Drive Change Tenure (Years) Industry Strategic Leadership Wealth Management Tax Digital, Technology, Software Strategy, Turnaround Audit, Finance, Risk Sales, Marketing Legal, Regulatory Human Capital Public Company Board Executive Leadership Steven Aldrich 4 ✓ ✓ ✓ ✓ ✓ ✓ ✓ E. Carol Hayles 3 ✓ ✓ ✓ ✓ ✓ John MacIlwaine 3 ✓ ✓ ✓ ✓ ✓ Georganne Proctor 4 ✓ ✓ ✓ ✓ ✓ Christopher Walters 7 ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ Mary Zappone 6 ✓ ✓ ✓ Joined Blucora in 2020 Mark Ernst 1 ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ Karthik Rao 1 ✓ ✓ ✓ ✓ ✓ Jana Schreuder 1 ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ Joined Blucora in 2021 Tina Perry - ✓ ✓ ✓ ✓ ✓ Our directors have a balanced and complementary set of skills and experiences 47

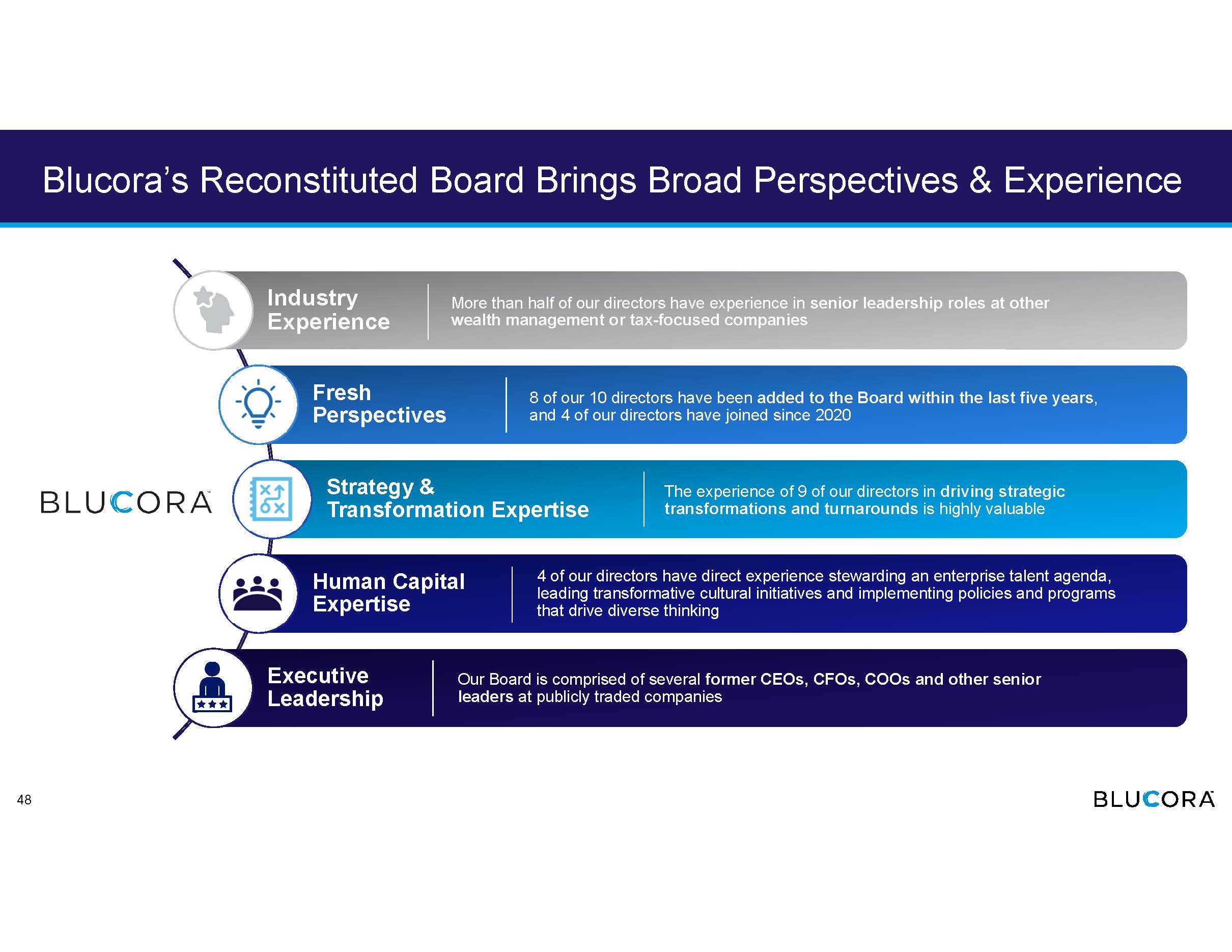

Blucora’s Reconstituted Board Brings Broad Perspectives & Experience Industry Experience Fresh Perspectives Strategy & Transformation Expertise Human Capital Expertise Executive Leadership More than half of our directors have experience in senior leadership roles at other wealth management or tax - focused companies 8 of our 10 directors have been added to the Board within the last five years , and 4 of our directors have joined since 2020 The experience of 9 of our directors in driving strategic transformations and turnarounds is highly valuable 4 of our directors have direct experience stewarding an enterprise talent agenda, leading transformative cultural initiatives and implementing policies and programs that drive diverse thinking Our Board is comprised of several former CEOs, CFOs, COOs and other senior leaders at publicly traded companies 48

Blucora Now Has a Balanced, Diverse Board of Directors ▪ Former CFO of TIAA - CREF ▪ Extensive experience, particularly as an executive and board member within the financial sector Georganne Proctor Independent Chair Director Since 2017 ▪ Former CFO of CIT Group ▪ Current board member of eBay and Webster Financial Corporation ▪ Valuable financial and accounting expertise as well as experience in operations and strategy E. Carol Hayles Director Since 2018 ▪ Former Senior Partner at Activate ▪ Highly relevant operational and executive management experience in areas of strategy, operations, technology and digital marketing Christopher Walters President & CEO Director Since 2014 ▪ Former Chief Product Officer of GoDaddy; Former VP of strategy and innovation at Intuit ▪ Deep product management experience with a unique understanding of operations, strategy, company growth and management Steven Aldrich Director Since 2017 ▪ CEO of Bay1; Former VP & General Manager of Braintree ▪ Unique experience in information technology, cybersecurity, operations, strategy, company growth and management John MacIlwaine Director Since 2018 ▪ CEO of Brace Industrial Group ▪ Significant executive leadership experience in operations, strategy, people management, business development and company growth and expansion Mary Zappone Director Since 2015 Collectively, our directors have expertise gained at some of the world’s most respected companies 49

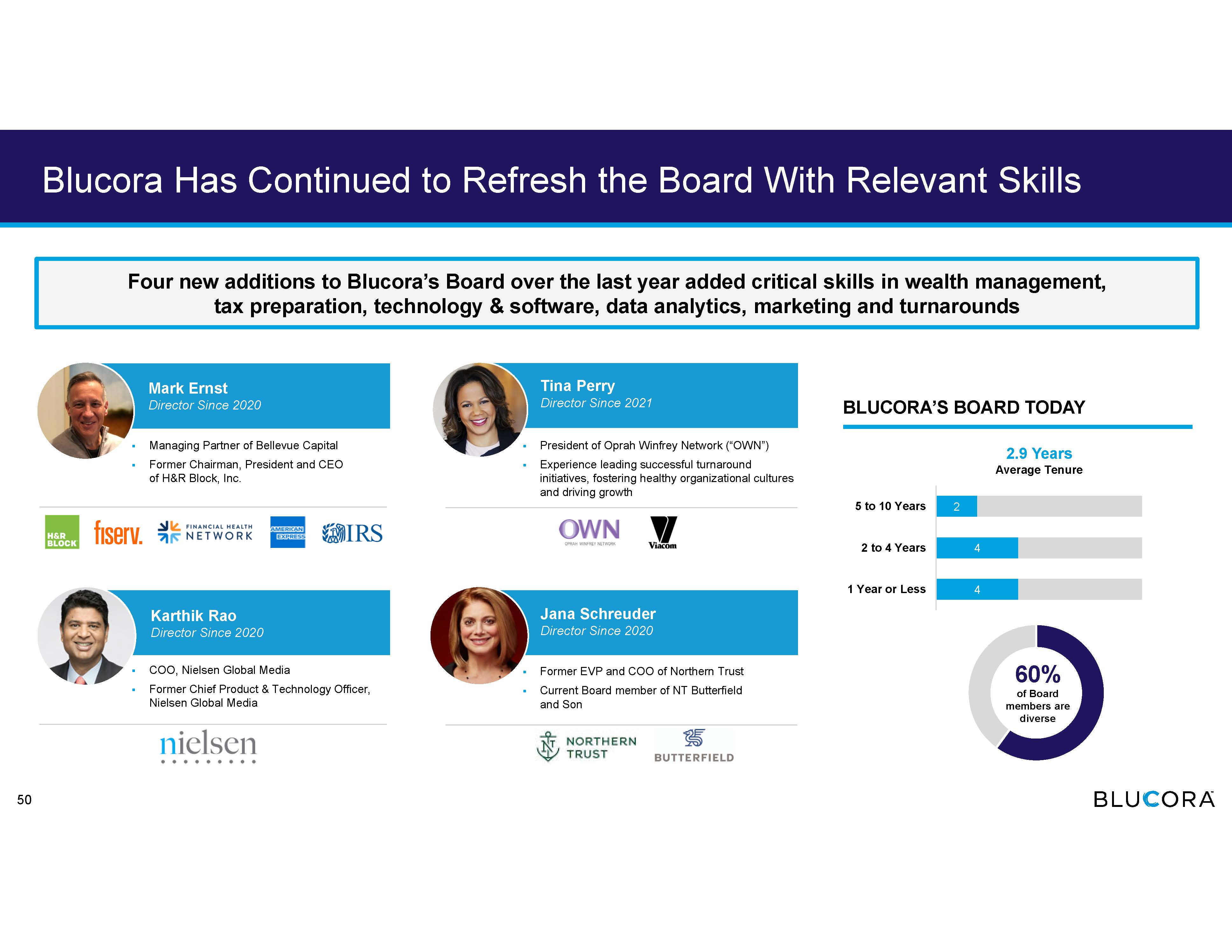

Karthik Rao Director Since 2020 Tina Perry Director Since 2021 Blucora Has Continued to Refresh the Board With Relevant Skills 2.9 Years Average Tenure 4 4 2 1 Year or Less 2 to 4 Years 5 to 10 Years 60 % of Board members are diverse ▪ Managing Partner of Bellevue Capital ▪ Former Chairman, President and CEO of H&R Block, Inc. ▪ COO, Nielsen Global Media ▪ Former Chief Product & Technology Officer, Nielsen Global Media ▪ President of Oprah Winfrey Network (“OWN”) ▪ Experience leading successful turnaround initiatives, fostering healthy organizational cultures and driving growth ▪ Former EVP and COO of Northern Trust ▪ Current Board member of NT Butterfield and Son Four new additions to Blucora’s Board over the last year added critical skills in wealth management, tax preparation, technology & software, data analytics, marketing and turnarounds Mark Ernst Director Since 2020 Jana Schreuder Director Since 2020 BLUCORA’S BOARD TODAY 50

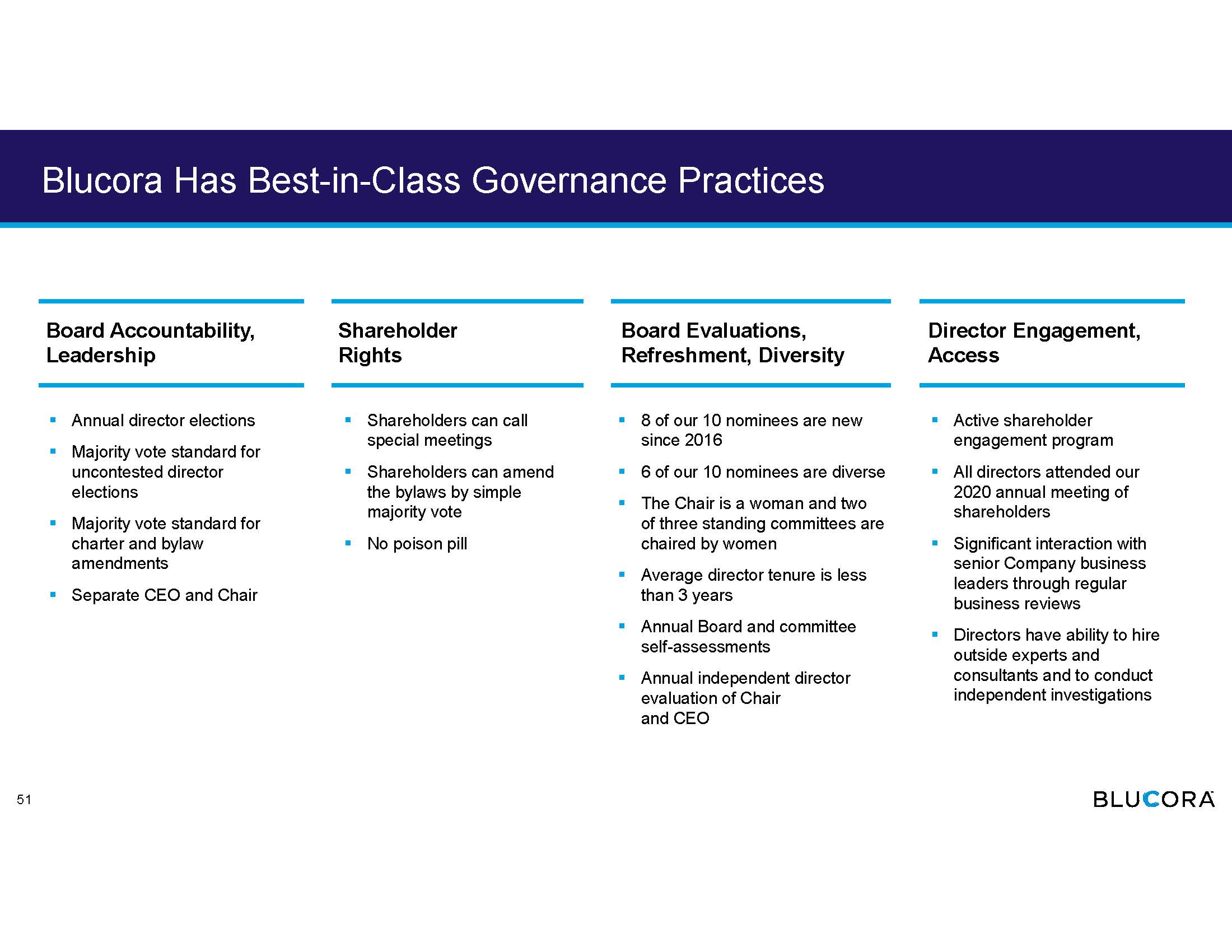

Blucora Has Best - in - Class Governance Practices Board Accountability, Leadership ▪ Annual director elections ▪ Majority vote standard for uncontested director elections ▪ Majority vote standard for charter and bylaw amendments ▪ Separate CEO and Chair Shareholder Rights ▪ Shareholders can call special meetings ▪ Shareholders can amend the bylaws by simple majority vote ▪ No poison pill Board Evaluations, Refreshment, Diversity ▪ 8 of our 10 nominees are new since 2016 ▪ 6 of our 10 nominees are diverse ▪ The Chair is a woman and two of three standing committees are chaired by women ▪ Average director tenure is less than 3 years ▪ Annual Board and committee self - assessments ▪ Annual independent director evaluation of Chair and CEO Director Engagement, Access ▪ Active shareholder engagement program ▪ All directors attended our 2020 annual meeting of shareholders ▪ Significant interaction with senior Company business leaders through regular business reviews ▪ Directors have ability to hire outside experts and consultants and to conduct independent investigations 51

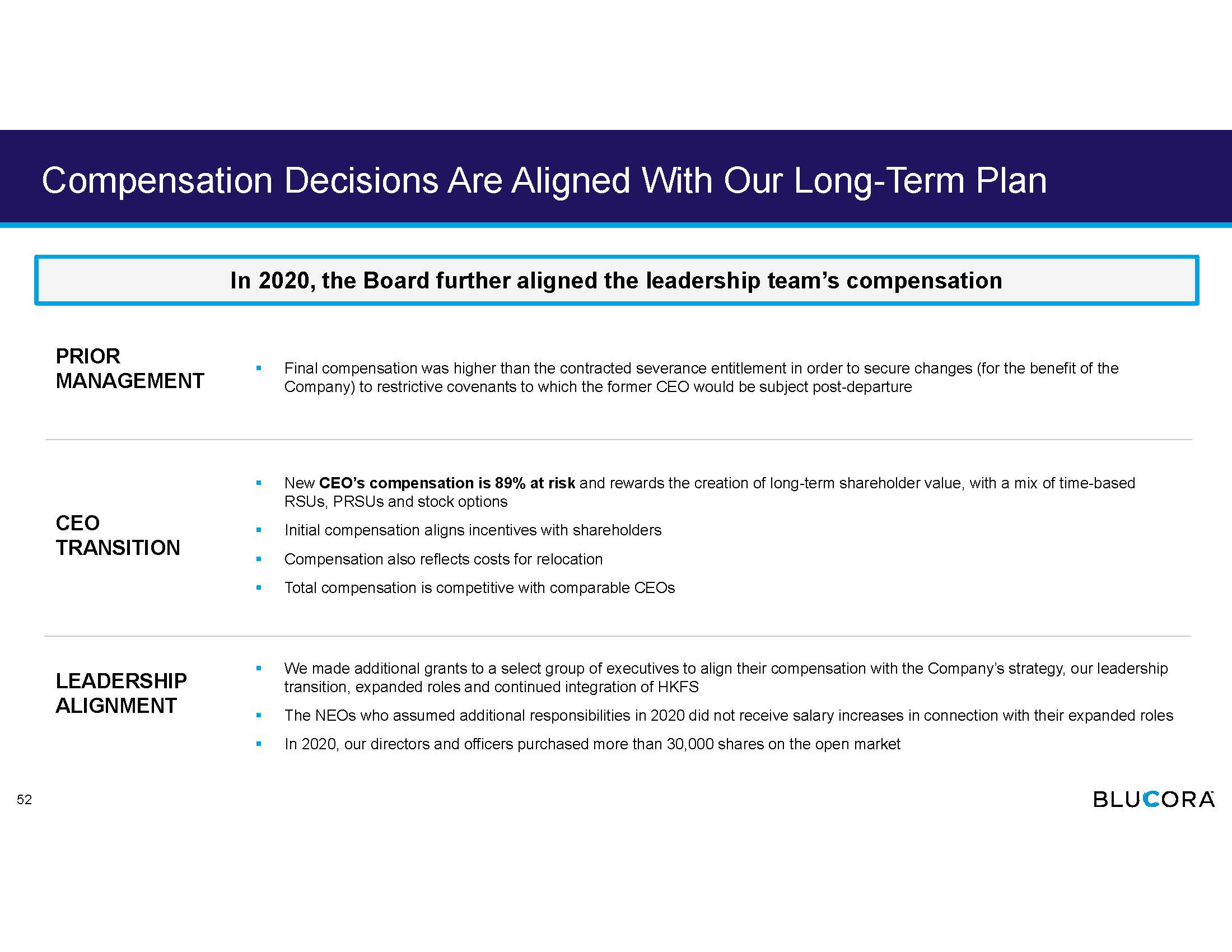

Compensation Decisions Are Aligned With Our Long - Term Plan CEO TRANSITION ▪ New CEO’s compensation is 89% at risk and rewards the creation of long - term shareholder value, with a mix of time - based RSUs, PRSUs and stock options ▪ Initial compensation aligns incentives with shareholders ▪ Compensation also reflects costs for relocation ▪ Total compensation is competitive with comparable CEOs LEADERSHIP ALIGNMENT ▪ We made additional grants to a select group of executives to align their compensation with the Company’s strategy, our leader shi p transition, expanded roles and continued integration of HKFS ▪ The NEOs who assumed additional responsibilities in 2020 did not receive salary increases in connection with their expanded r ole s ▪ In 2020, our directors and officers purchased more than 30,000 shares on the open market PRIOR MANAGEMENT ▪ Final compensation was higher than the contracted severance entitlement in order to secure changes (for the benefit of the Company) to restrictive covenants to which the former CEO would be subject post - departure In 2020, the Board further aligned the leadership team’s compensation 52

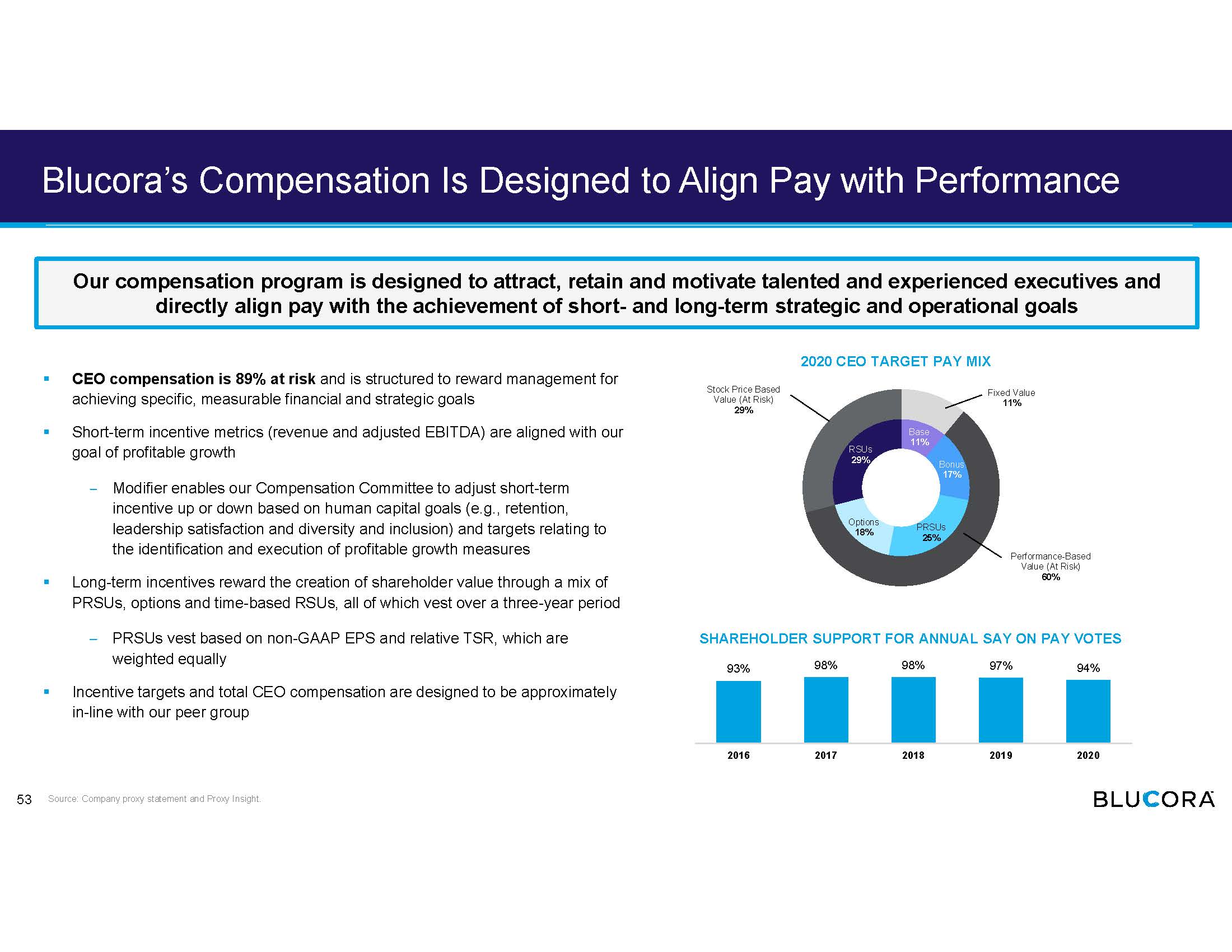

Blucora’s Compensation Is Designed to Align Pay with Performance ▪ CEO compensation is 89% at risk and is structured to reward management for achieving specific, measurable financial and strategic goals ▪ Short - term incentive metrics (revenue and adjusted EBITDA) are aligned with our goal of profitable growth ‒ Modifier enables our Compensation Committee to adjust short - term incentive up or down based on human capital goals (e.g., retention, leadership satisfaction and diversity and inclusion) and targets relating to the identification and execution of profitable growth measures ▪ Long - term incentives reward the creation of shareholder value through a mix of PRSUs, options and time - based RSUs, all of which vest over a three - year period – PRSUs vest based on non - GAAP EPS and relative TSR, which are weighted equally ▪ Incentive targets and total CEO compensation are designed to be approximately in - line with our peer group SHAREHOLDER SUPPORT FOR ANNUAL SAY ON PAY VOTES 93% 98% 98% 97% 94% 2016 2017 2018 2019 2020 Source: Company proxy statement and Proxy Insight. Base 11% Bonus 17% PRSUs 25% Options 18% RSUs 29% Fixed Value 11% Performance - Based Value (At Risk) 60% Stock Price Based Value (At Risk) 29% Our compensation program is designed to attract, retain and motivate talented and experienced executives and directly align pay with the achievement of short - and long - term strategic and operational goals 2020 CEO TARGET PAY MIX 53

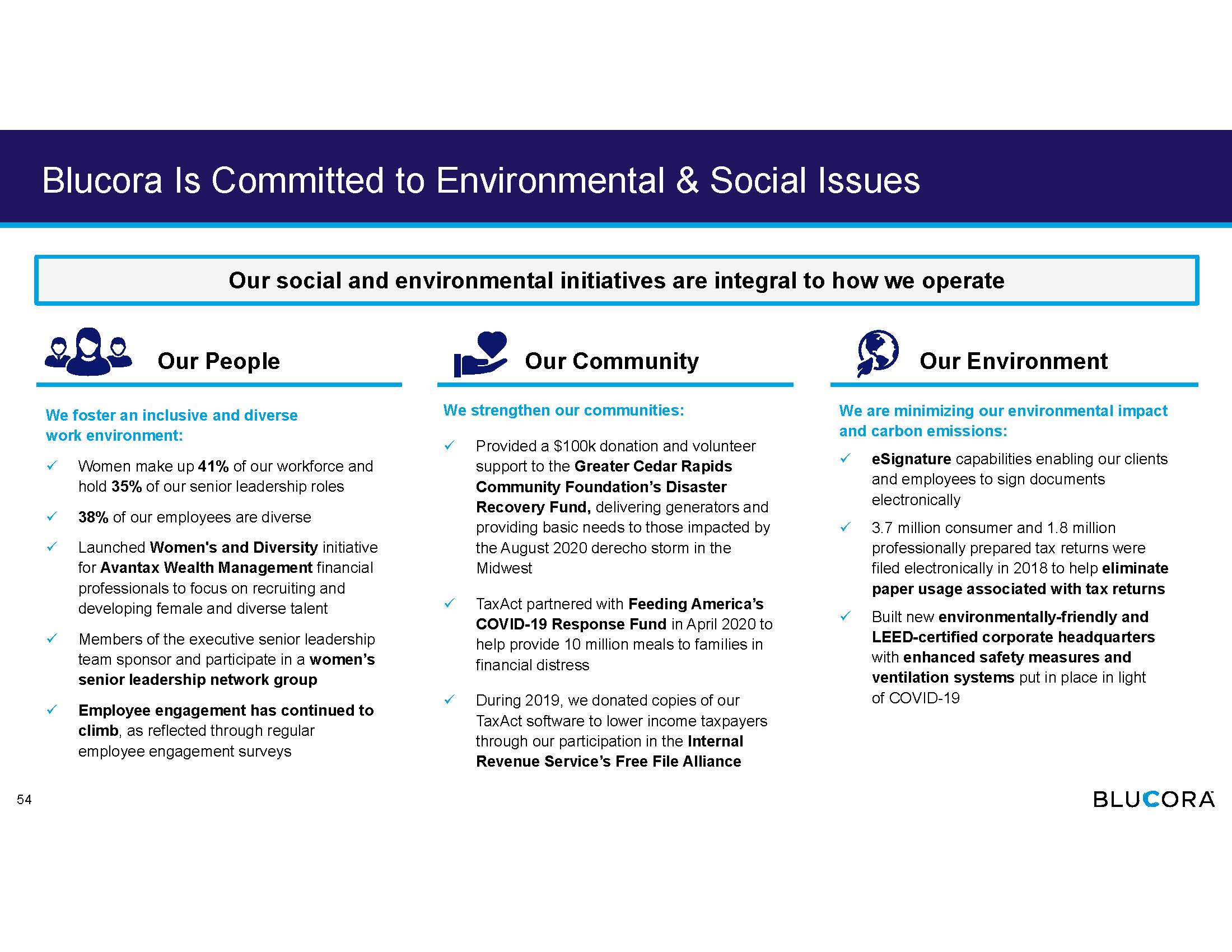

Blucora Is Committed to Environmental & Social Issues Our People Our Community Our Environment We foster an inclusive and diverse work environment: x Women make up 41% of our workforce and hold 35% of our senior leadership roles x 38% of our employees are diverse x Launched Women's and Diversity initiative for Avantax Wealth Management financial professionals to focus on recruiting and developing female and diverse talent x Members of the executive senior leadership team sponsor and participate in a women’s senior leadership network group x Employee engagement has continued to climb , as reflected through regular employee engagement surveys We strengthen our communities: x Provided a $100k donation and volunteer support to the Greater Cedar Rapids Community Foundation’s Disaster Recovery Fund, delivering generators and providing basic needs to those impacted by the August 2020 derecho storm in the Midwest x TaxAct pa rtnered with Feeding America’s COVID - 19 Response Fund in April 2020 to help provide 10 million meals to families in financial distress x During 2019, we donated copies of our TaxAct software to lower income taxpayers through our participation in the Internal Revenue Service’s Free File Alliance We are minimizing our environmental impact and carbon emissions: x eSignature capabilities enabling our clients and employees to sign documents electronically x 3.7 million consumer and 1.8 million professionally prepared tax returns were filed electronically in 2018 to help eliminate paper usage associated with tax returns x Built new environmentally - friendly and LEED - certified corporate headquarters with enhanced safety measures and ventilation systems put in place in light of COVID - 19 Our social and environmental initiatives are integral to how we operate 54

Our Response to COVID - 19 ▪ Implemented a Company - wide work - from - home policy well before state and local officials mandated it ▪ Implemented hazard pay for our essential employees ▪ Increased pace and depth of communication across the employee base ▪ Designed safety protocols for client - facing financial professionals ▪ Increased TaxAct’s customer service resources for the extended duration of the tax season ▪ Developed a Business Continuity Planning Group , for a variety of consequences in the long - term for Blucora and its independent financial professionals ▪ The group has developed continuity plans and responses for a variety of potential crises Our Employees Our Clients Long - Term Business Continuity Planning Our commitment to the safety and health of our workforce and our clients guides us as we address the unprecedented challenges of the global pandemic we are all facing 55

Ancora’s Campaign is an Overreach; Its Nominees Are Not Additive

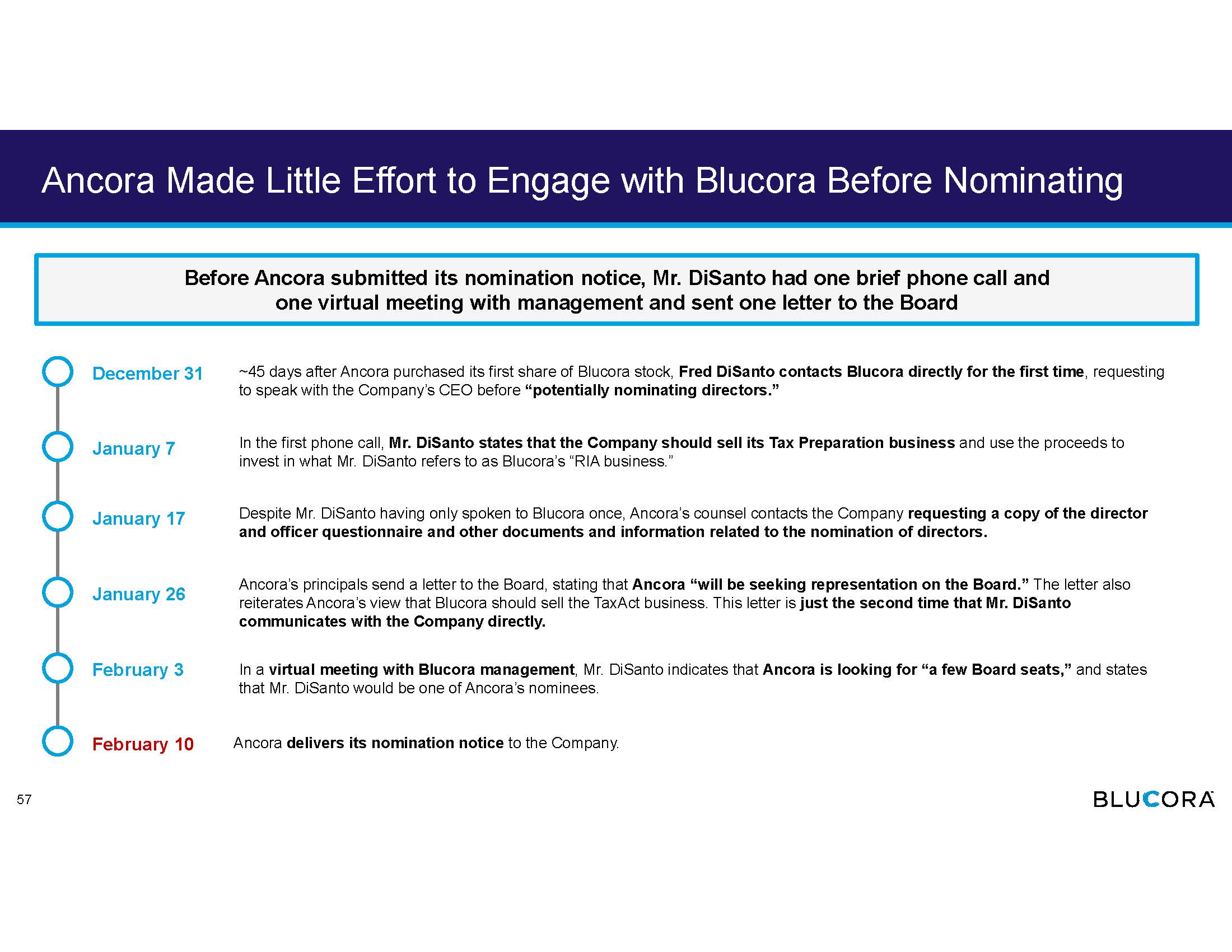

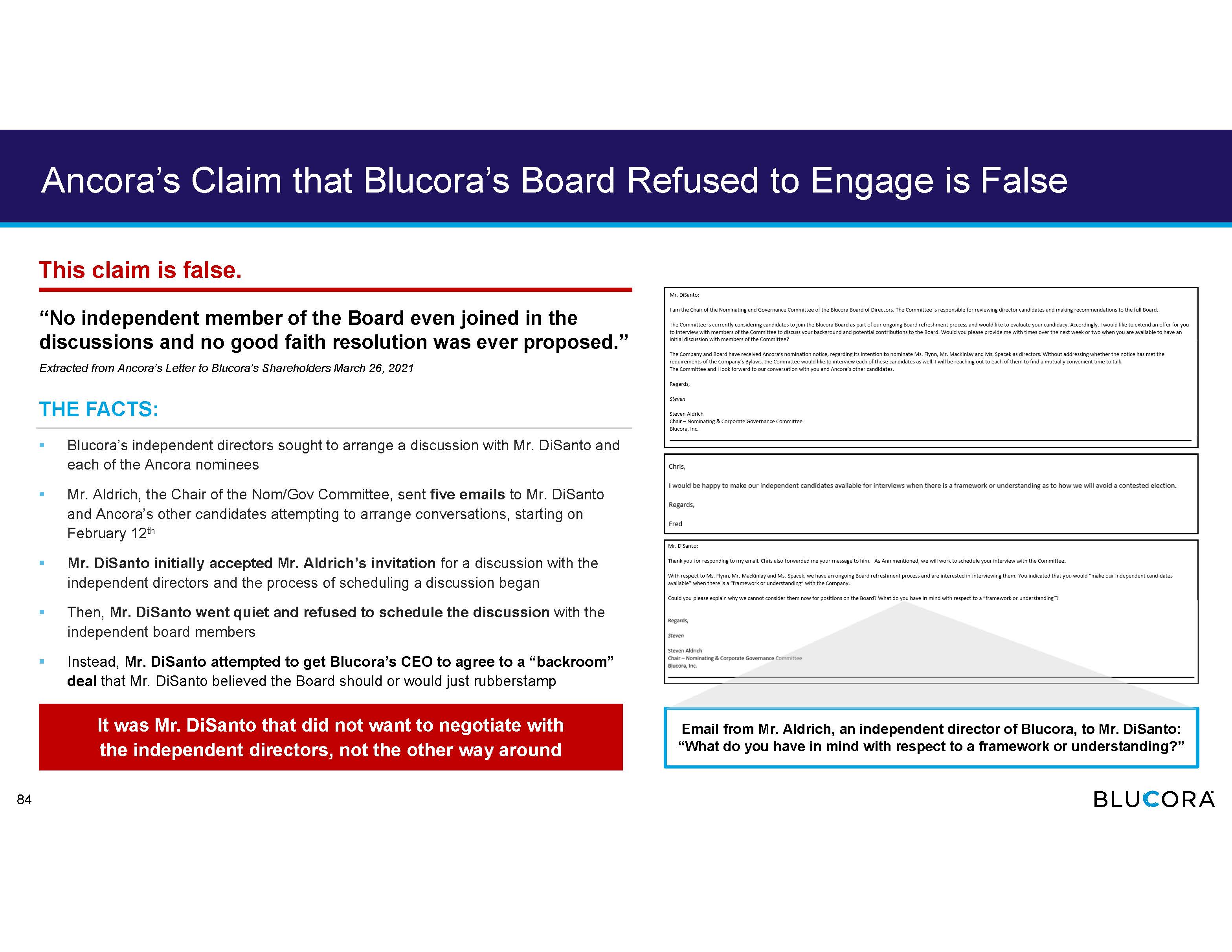

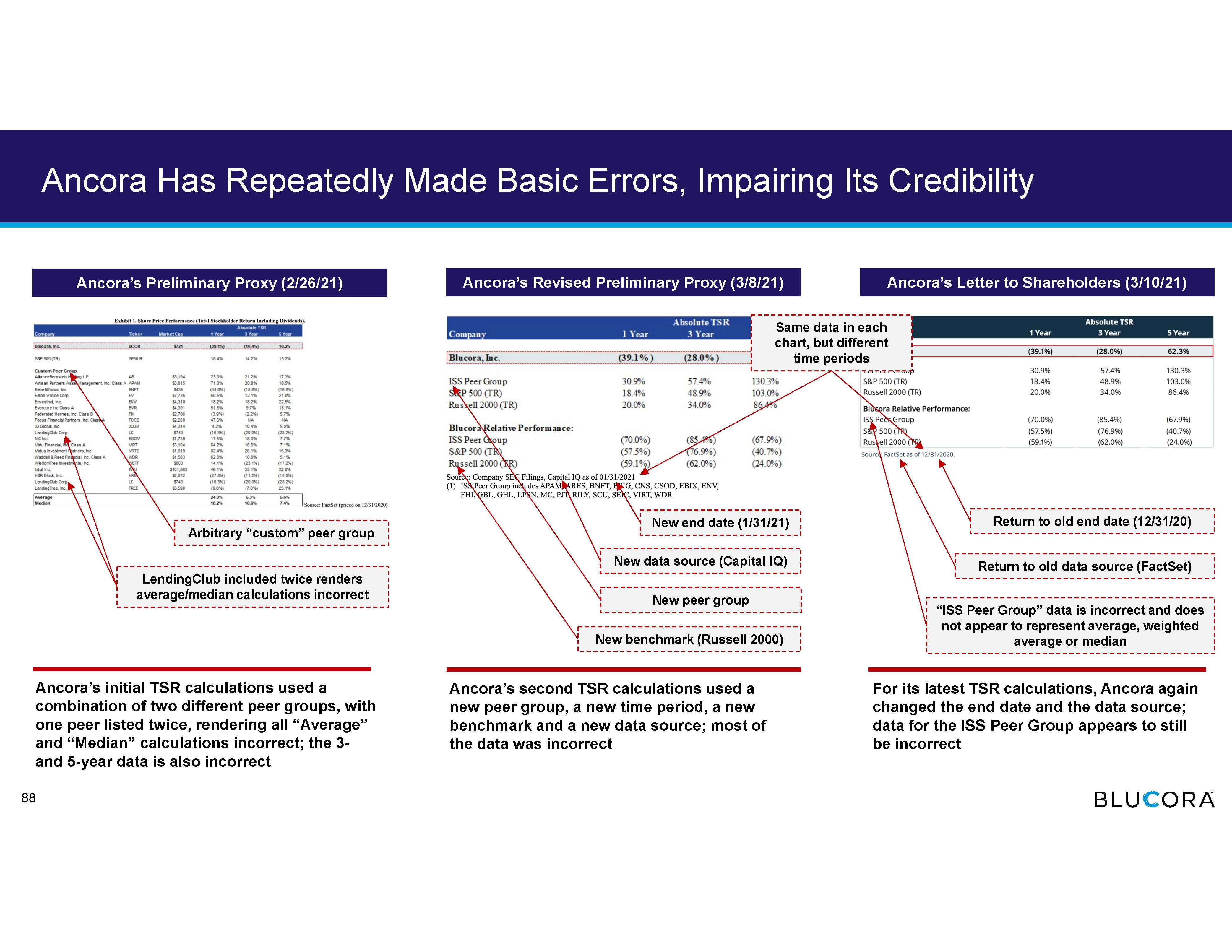

Ancora Made Little Effort to Engage with Blucora Before Nominating December 31 January 7 January 17 January 26 February 3 February 10 ~45 days after Ancora purchased its first share of Blucora stock, Fred DiSanto contacts Blucora directly for the first time , requesting to speak with the Company’s CEO before “potentially nominating directors.” In the first phone call, Mr. DiSanto states that the Company should sell its Tax Preparation business and use the proceeds to invest in what Mr. DiSanto refers to as Blucora’s “RIA business.” Despite Mr. DiSanto having only spoken to Blucora once, Ancora’s counsel contacts the Company requesting a copy of the director and officer questionnaire and other documents and information related to the nomination of directors. Ancora’s principals send a letter to the Board, stating that Ancora “will be seeking representation on the Board.” The letter also reiterates Ancora’s view that Blucora should sell the TaxAct business. This letter is just the second time that Mr. DiSanto communicates with the Company directly. In a virtual meeting with Blucora management , Mr. DiSanto indicates that Ancora is looking for “a few Board seats,” and states that Mr. DiSanto would be one of Ancora’s nominees. Ancora delivers its nomination notice to the Company. Before Ancora submitted its nomination notice, Mr. DiSanto had one brief phone call and one virtual meeting with management and sent one letter to the Board 57

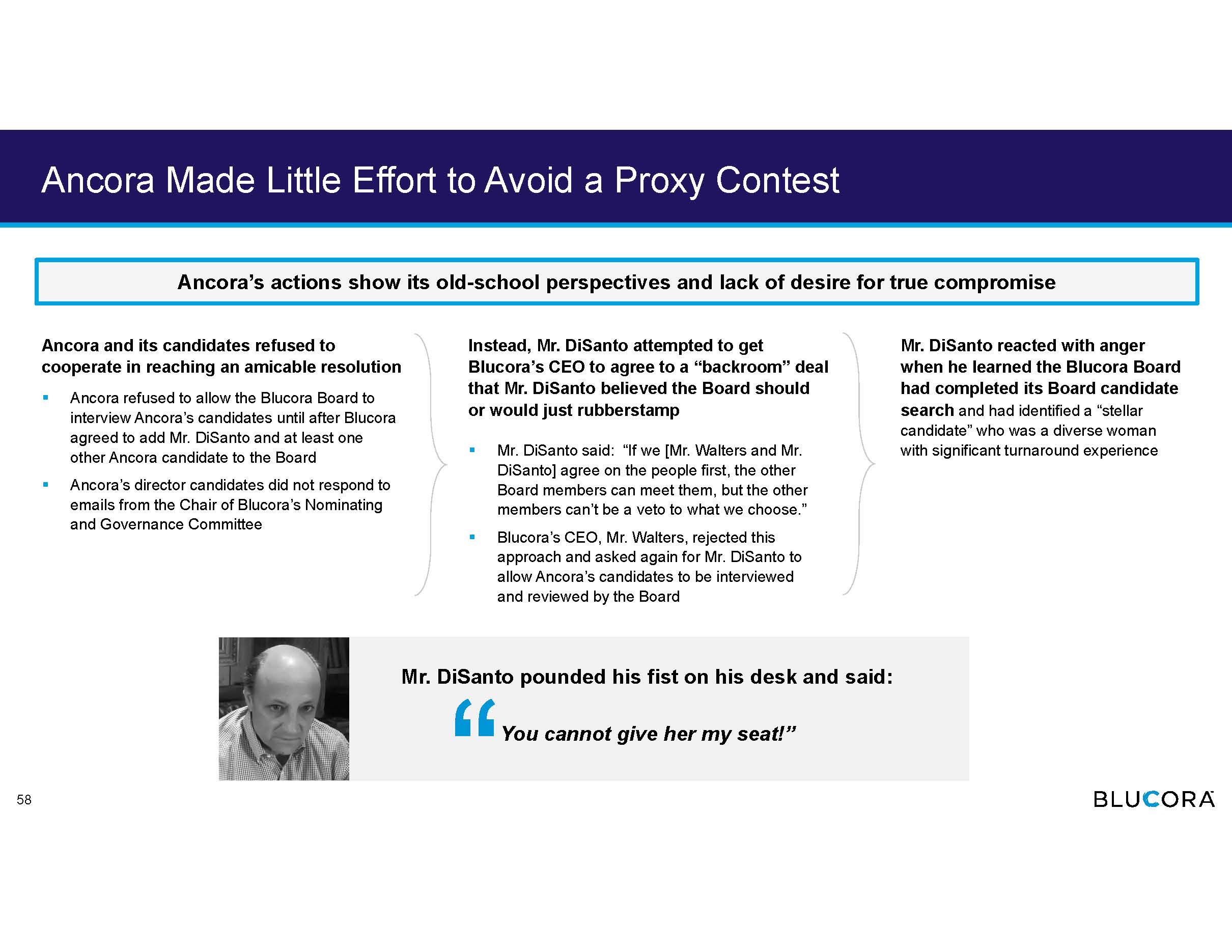

Ancora Made Little Effort to Avoid a Proxy Contest Ancora and its candidates refused to cooperate in reaching an amicable resolution ▪ Ancora refused to allow the Blucora Board to interview Ancora’s candidates until after Blucora agreed to add Mr. DiSanto and at least one other Ancora candidate to the Board ▪ Ancora’s director candidates did not respond to emails from the Chair of Blucora’s Nominating and Governance Committee Ancora’s actions show its old - school perspectives and lack of desire for true compromise 58 Mr. DiSanto reacted with anger when he learned the Blucora Board had completed its Board candidate search and had identified a “stellar candidate” who was a diverse woman with significant turnaround experience Instead, Mr. DiSanto attempted to get Blucora’s CEO to agree to a “backroom” deal that Mr. DiSanto believed the Board should or would just rubberstamp ▪ Mr. DiSanto said: “If we [Mr. Walters and Mr. DiSanto] agree on the people first, the other Board members can meet them, but the other members can’t be a veto to what we choose.” ▪ Blucora’s CEO, Mr. Walters, rejected this approach and asked again for Mr. DiSanto to allow Ancora’s candidates to be interviewed and reviewed by the Board Mr. DiSanto pounded his fist on his desk and said: You cannot give her my seat!”

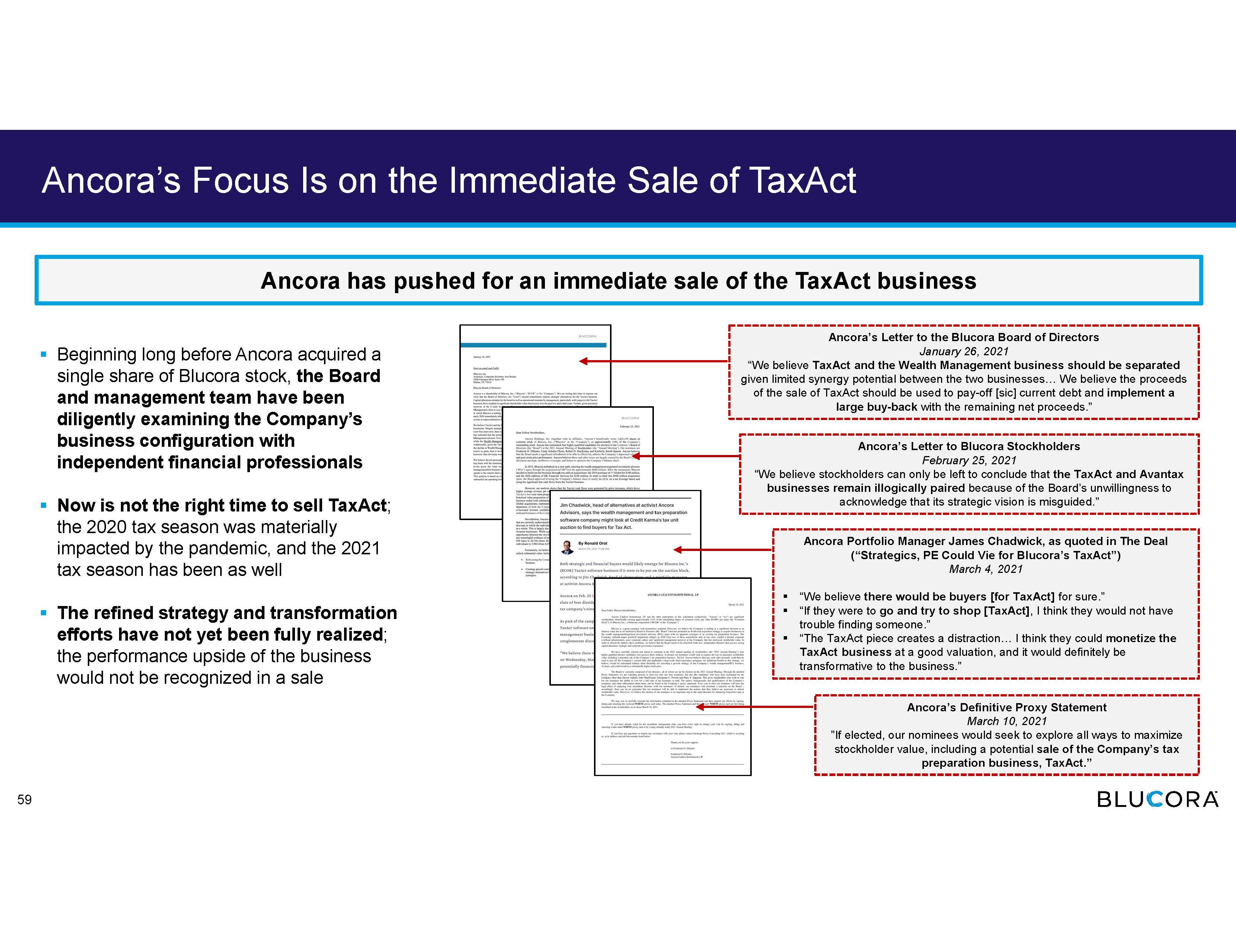

Ancora’s Focus Is on the Immediate Sale of TaxAct ▪ Beginning long before Ancora acquired a single share of Blucora stock, the Board and management team have been diligently examining the Company’s business configuration with independent financial professionals ▪ Now is not the right time to sell TaxAct ; the 2020 tax season was materially impacted by the pandemic, and the 2021 tax season has been as well ▪ The refined strategy and transformation efforts have not yet been fully realized ; the performance upside of the business would not be recognized in a sale Ancora’s Letter to the Blucora Board of Directors January 26, 2021 “We believe TaxAct and the Wealth Management business should be separated given limited synergy potential between the two businesses… We believe the proceeds of the sale of TaxAct should be used to pay - off [sic] current debt and implement a large buy - back with the remaining net proceeds.” Ancora’s Letter to Blucora Stockholders February 25, 2021 “We believe stockholders can only be left to conclude that the TaxAct and Avantax businesses remain illogically paired because of the Board’s unwillingness to acknowledge that its strategic vision is misguided.” Ancora’s Definitive Proxy Statement March 10, 2021 ”If elected, our nominees would seek to explore all ways to maximize stockholder value, including a potential sale of the Company’s tax preparation business, TaxAct.” Ancora Portfolio Manager James Chadwick, as quoted in The Deal (“Strategics, PE Could Vie for Blucora’s TaxAct”) March 4, 2021 ▪ “We believe there would be buyers [for TaxAct] for sure.” ▪ “If they were to go and try to shop [TaxAct] , I think they would not have trouble finding someone.” ▪ “The TaxAct piece creates a distraction… I think they could monetize the TaxAct business at a good valuation, and it would definitely be transformative to the business.” Ancora has pushed for an immediate sale of the TaxAct business 59

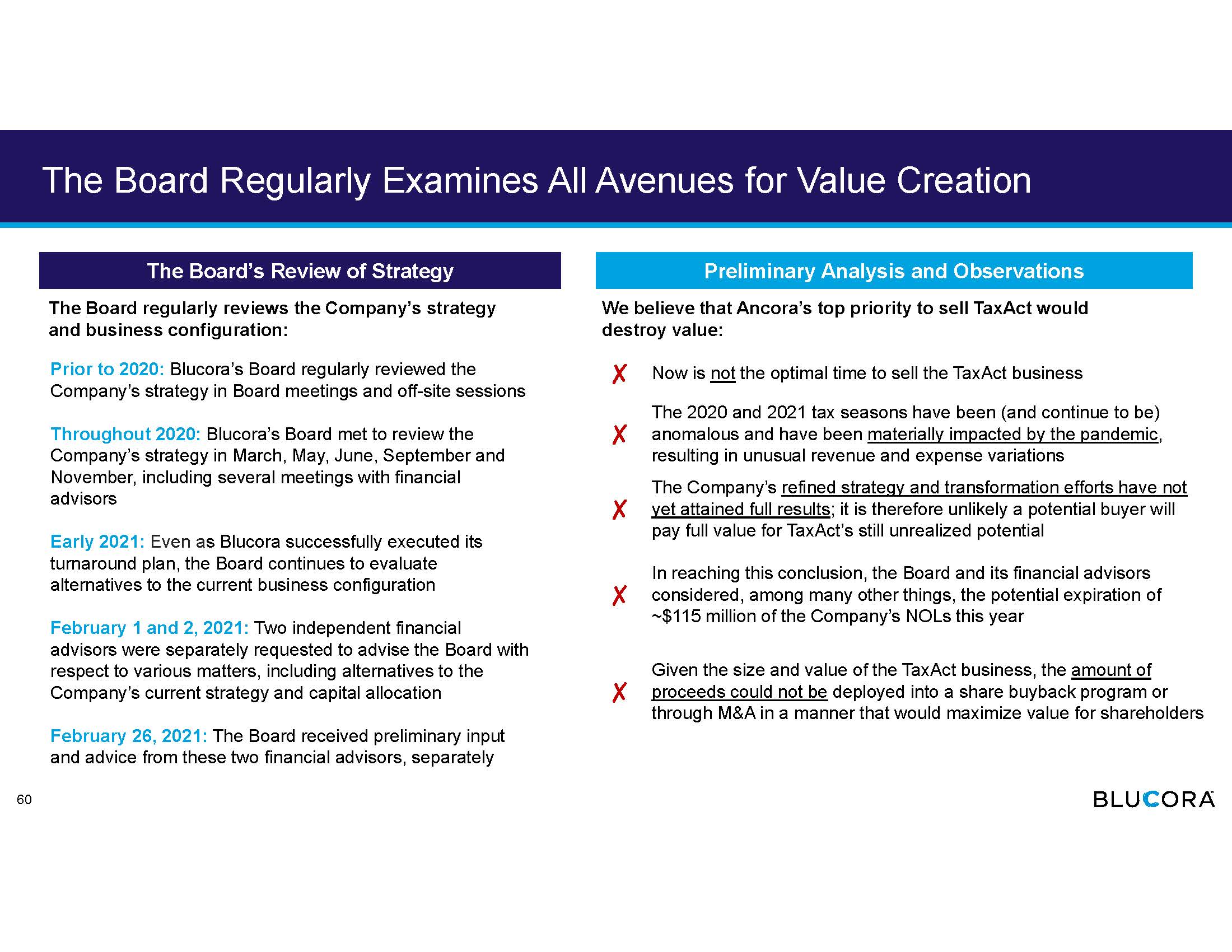

The Board Regularly Examines All Avenues for Value Creation 60 We believe that Ancora’s top priority to sell TaxAct would destroy value: ✗ Now is not the optimal time to sell the TaxAct business ✗ The 2020 and 2021 tax seasons have been (and continue to be) anomalous and have been materially impacted by the pandemic , resulting in unusual revenue and expense variations ✗ The Company’s refined strategy and transformation efforts have not yet attained full results ; it is therefore unlikely a potential buyer will pay full value for TaxAct’s still unrealized potential ✗ In reaching this conclusion, the Board and its financial advisors considered, among many other things, the potential expiration of ~$115 million of the Company’s NOLs this year ✗ Given the size and value of the TaxAct business, the amount of proceeds could not be deployed into a share buyback program or through M&A in a manner that would maximize value for shareholders Prior to 2020: Blucora’s Board regularly reviewed the Company’s strategy in Board meetings and off - site sessions Throughout 2020: Blucora’s Board met to review the Company’s strategy in March, May, June, September and November, including several meetings with financial advisors Early 2021: Even a s Blucora successfully executed its turnaround plan, the Board continues to evaluate alternatives to the current business configuration February 1 and 2, 2021: Two independent financial advisors were separately requested to advise the Board with respect to various matters, including alternatives to the Company’s current strategy and capital allocation February 26, 2021: The Board received preliminary input and advice from these two financial advisors, separately The Board regularly reviews the Company’s strategy and business configuration: The Board’s Review of Strategy Preliminary Analysis and Observations

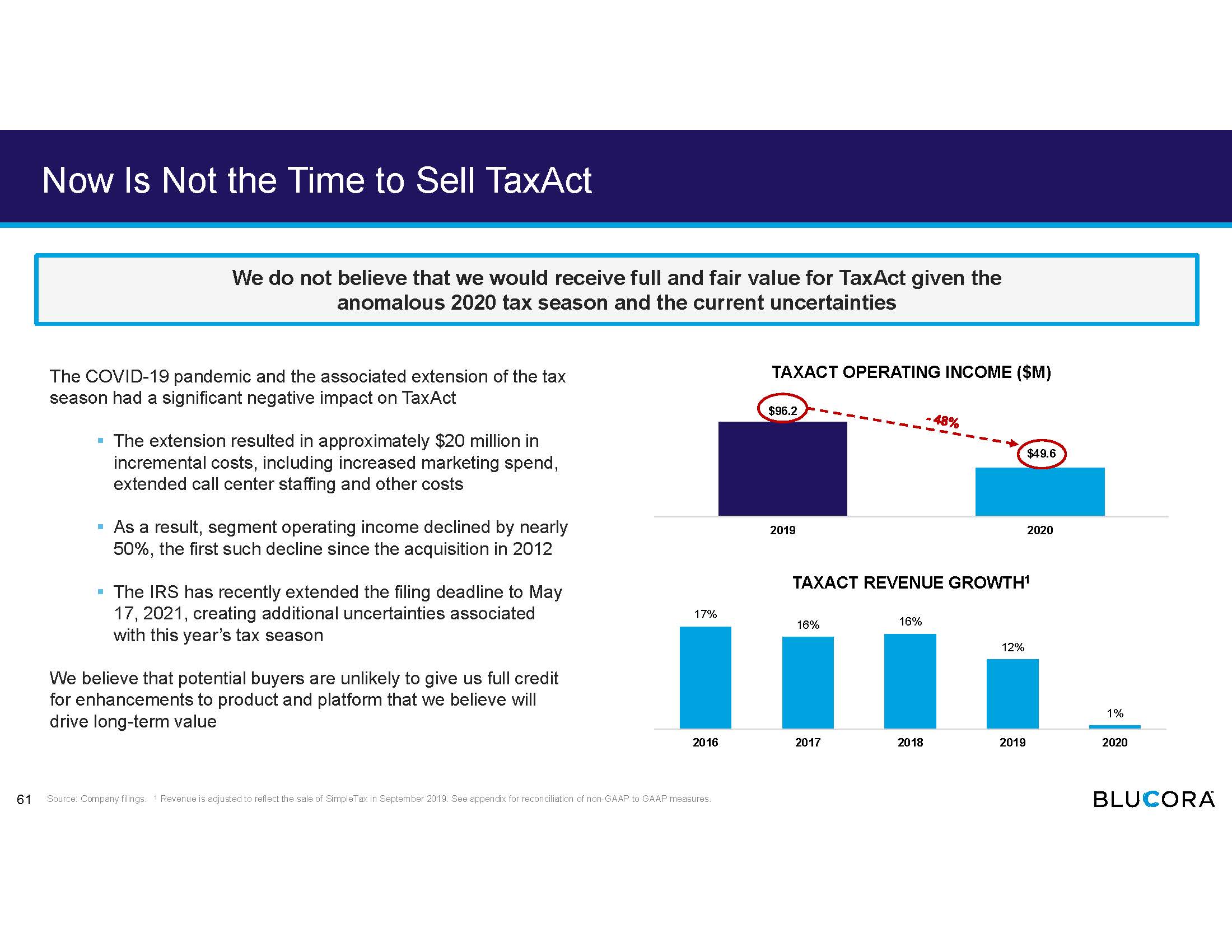

Now Is Not the Time to Sell TaxAct The COVID - 19 pandemic and the associated extension of the tax season had a significant negative impact on TaxAct ▪ The extension resulted in approximately $20 million in incremental costs, including increased marketing spend, extended call center staffing and other costs ▪ As a result, segment operating income declined by nearly 50%, the first such decline since the acquisition in 2012 ▪ The IRS has recently extended the filing deadline to May 17, 2021, creating additional uncertainties associated with this year’s tax season We believe that potential buyers are unlikely to give us full credit for enhancements to product and platform that we believe will drive long - term value TAXACT OPERATING INCOME ($M) TAXACT REVENUE GROWTH 1 $96.2 $49.6 2019 2020 Source: Company filings. 1 Revenue is adjusted to reflect the sale of SimpleTax in September 2019. See appendix for reconciliation of non - GAAP to GAAP measures. We do not believe that we would receive full and fair value for TaxAct given the anomalous 2020 tax season and the current uncertainties 61 17% 16% 16% 12% 1% 2016 2017 2018 2019 2020

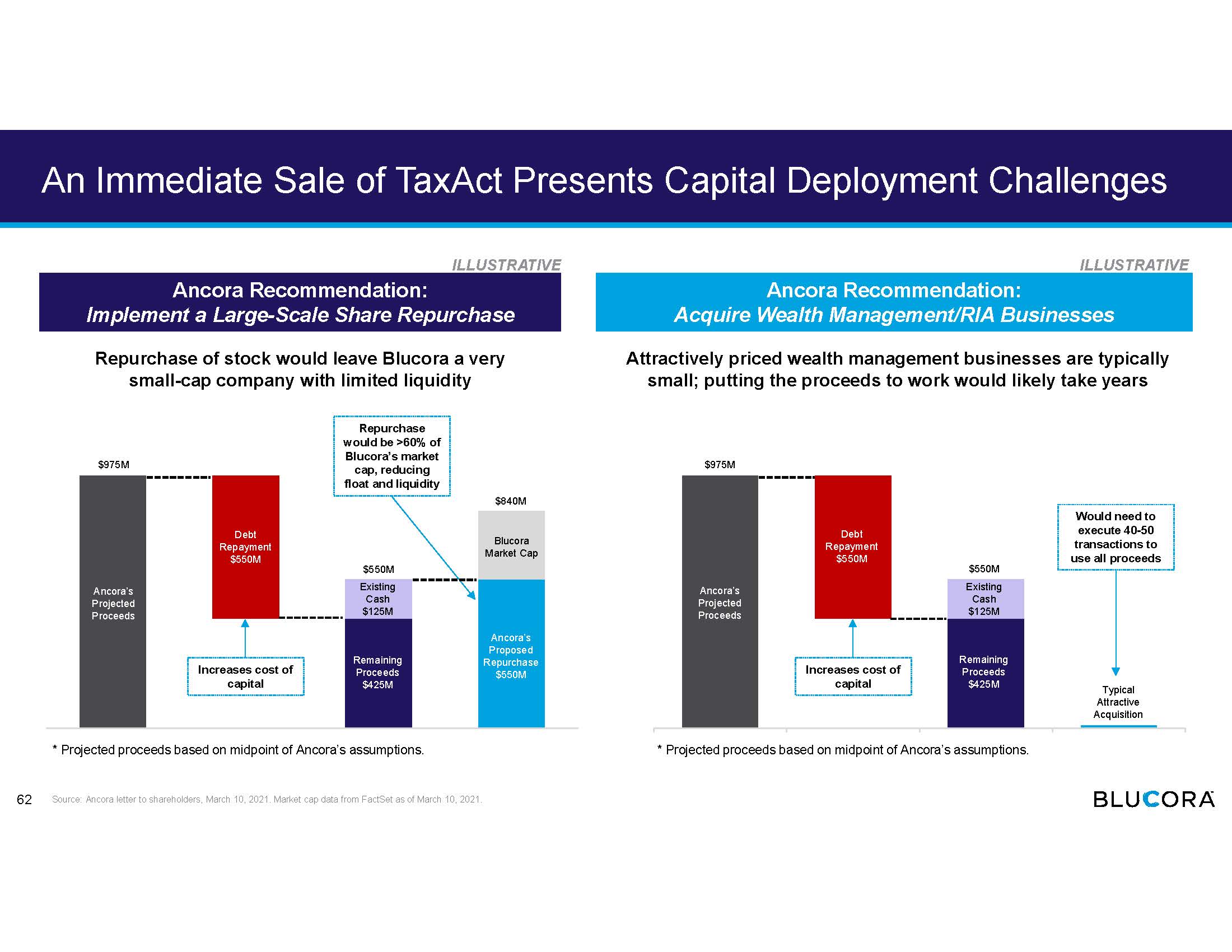

Ancora Recommendation: Implement a Large - Scale Share Repurchase Ancora Recommendation: Acquire Wealth Management/RIA Businesses An Immediate Sale of TaxAct Presents Capital Deployment Challenges Repurchase of stock would leave Blucora a very small - cap company with limited liquidity Attractively priced wealth management businesses are typically small; putting the proceeds to work would likely take years Projected Proceeds Debt Repayment Remaining Proceeds Blucora Market Cap Projected Proceeds Debt Repayment Remaining Proceeds Typical Acquisition ILLUSTRATIVE ILLUSTRATIVE * Projected proceeds based on midpoint of Ancora’s assumptions. * Projected proceeds based on midpoint of Ancora’s assumptions. Ancora’s Projected Proceeds Debt Repayment $550M Existing Cash $125M Remaining Proceeds $425M Blucora Market Cap Ancora’s Proposed Repurchase $550M $975M Ancora’s Projected Proceeds Debt Repayment $550M Existing Cash $125M Remaining Proceeds $425M $975M Typical Attractive Acquisition $550M $550M Repurchase would be >60% of Blucora’s market cap, reducing float and liquidity Would need to execute 40 - 50 transactions to use all proceeds Increases cost of capital Increases cost of capital Source: Ancora letter to shareholders, March 10, 2021. Market cap data from FactSet as of March 10, 2021. $840M 62

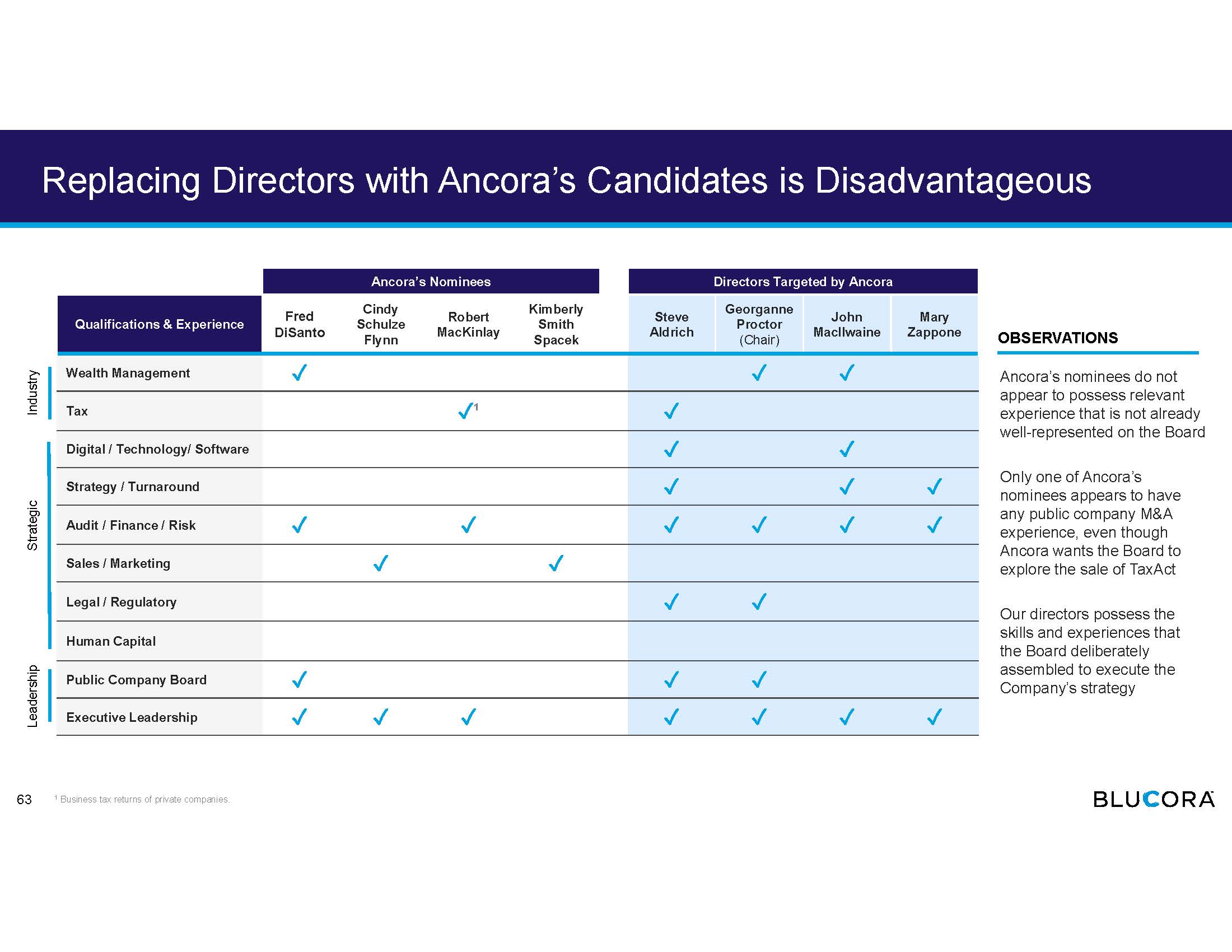

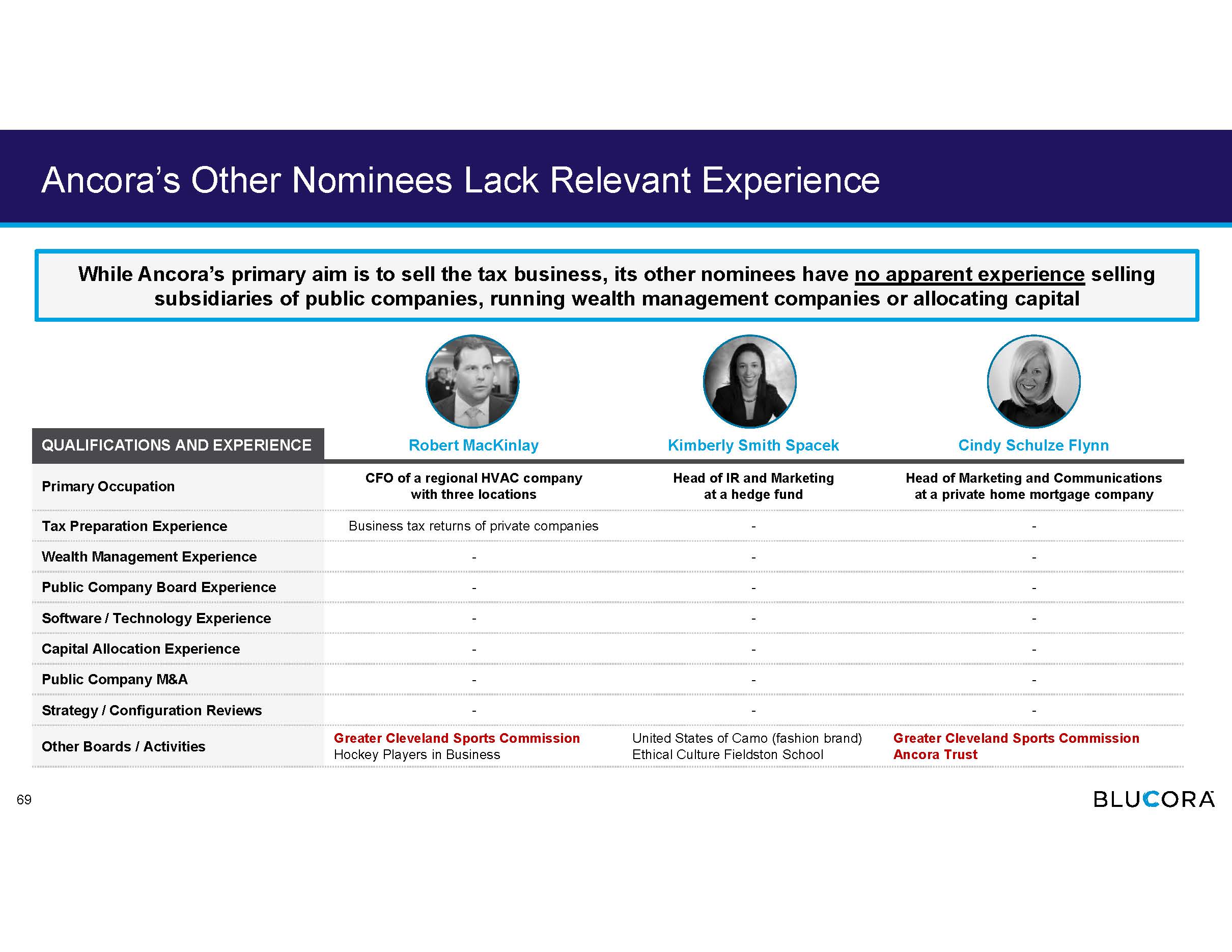

Replacing Directors with Ancora’s Candidates is Disadvantageous Ancora’s Nominees Directors Targeted by Ancora Qualifications & Experience Fred DiSanto Cindy Schulze Flynn Robert MacKinlay Kimberly Smith Spacek Steve Aldrich Georganne Proctor (Chair) John MacIlwaine Mary Zappone Wealth Management ض ض ض Tax ض 1 ض Digital / Technology/ Software ض ض Strategy / Turnaround ض ض ض Audit / Finance / Risk ض ض ض ض ض ض Sales / Marketing ض ض Legal / Regulatory ض ض Human Capital Public Company Board ض ض ض Executive Leadership ض ض ض ض ض ض ض OBSERVATIONS Ancora’s nominees do not appear to possess relevant experience that is not already well - represented on the Board Only one of Ancora’s nominees appears to have any public company M&A experience, even though Ancora wants the Board to explore the sale of TaxAct Our directors possess the skills and experiences that the Board deliberately assembled to execute the Company’s strategy Industry Strategic Leadership 63 1 Business tax returns of private companies.

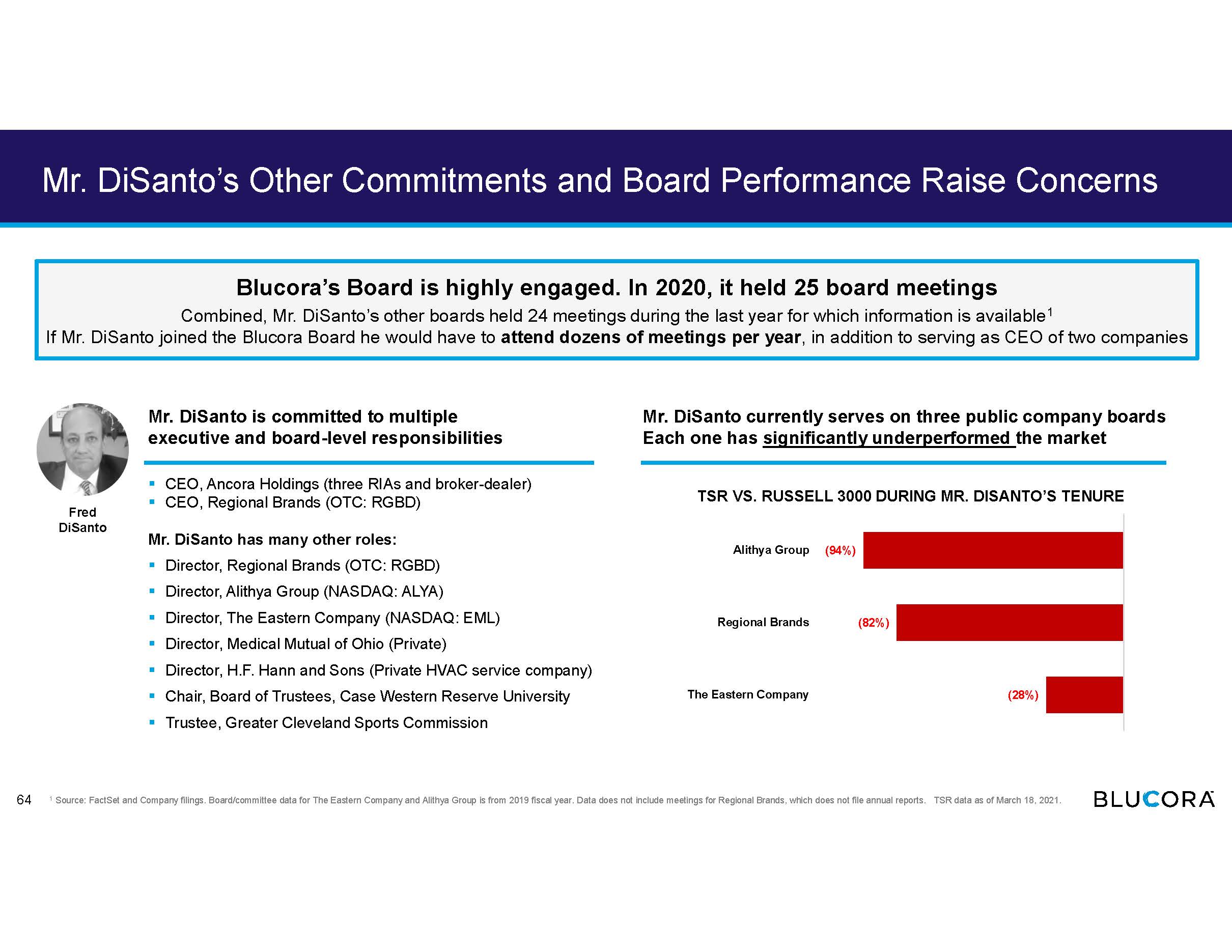

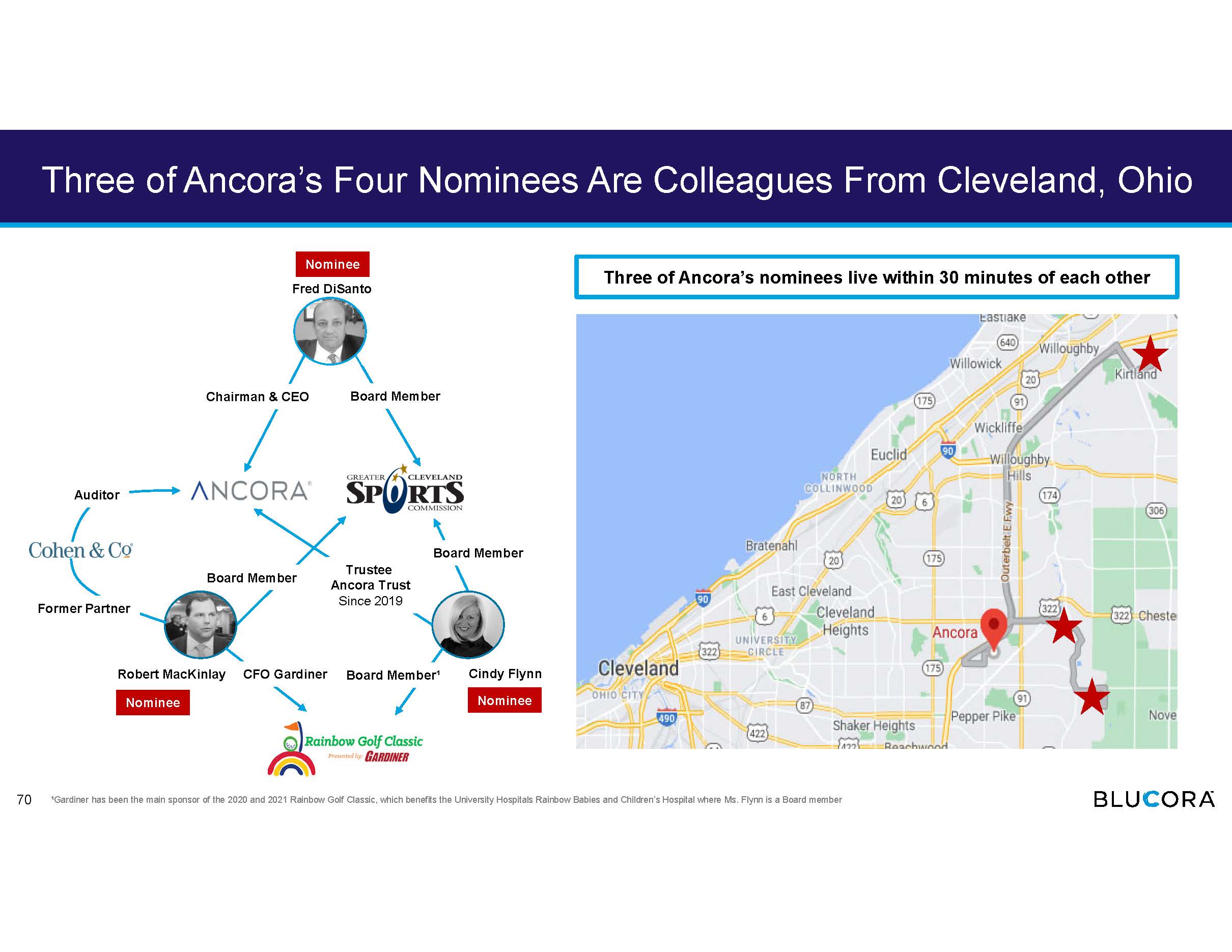

Mr. DiSanto’s Other Commitments and Board Performance Raise Concerns ▪ CEO, Ancora Holdings (three RIAs and broker - dealer) ▪ CEO, Regional Brands (OTC: RGBD) Mr. DiSanto has many other roles: ▪ Director, Regional Brands (OTC: RGBD) ▪ Director, Alithya Group (NASDAQ: ALYA) ▪ Director, The Eastern Company (NASDAQ: EML) ▪ Director, Medical Mutual of Ohio (Private) ▪ Director, H.F. Hann and Sons (Private HVAC service company) ▪ Chair, Board of Trustees, Case Western Reserve University ▪ Trustee, Greater Cleveland Sports Commission Fred DiSanto TSR VS. RUSSELL 3000 DURING MR. DISANTO’S TENURE Mr. DiSanto currently serves on three public company boards Each one has significantly underperformed the market Mr. DiSanto is committed to multiple executive and board - level responsibilities 1 Source: FactSet and Company filings. Board/committee data for The Eastern Company and Alithya Group is from 2019 fiscal year. Data does not include meetings for Regional Brands, which does not file annual reports. TSR d ata as of March 18, 2021. 64 Blucora’s Board is highly engaged. In 2020, it held 25 board meetings Combined, Mr. DiSanto’s other boards held 24 meetings during the last year for which information is available 1 If Mr. DiSanto joined the Blucora Board he would have to attend dozens of meetings per year , in addition to serving as CEO of two companies (94%) (82%) (28%) Alithya Group Regional Brands The Eastern Company

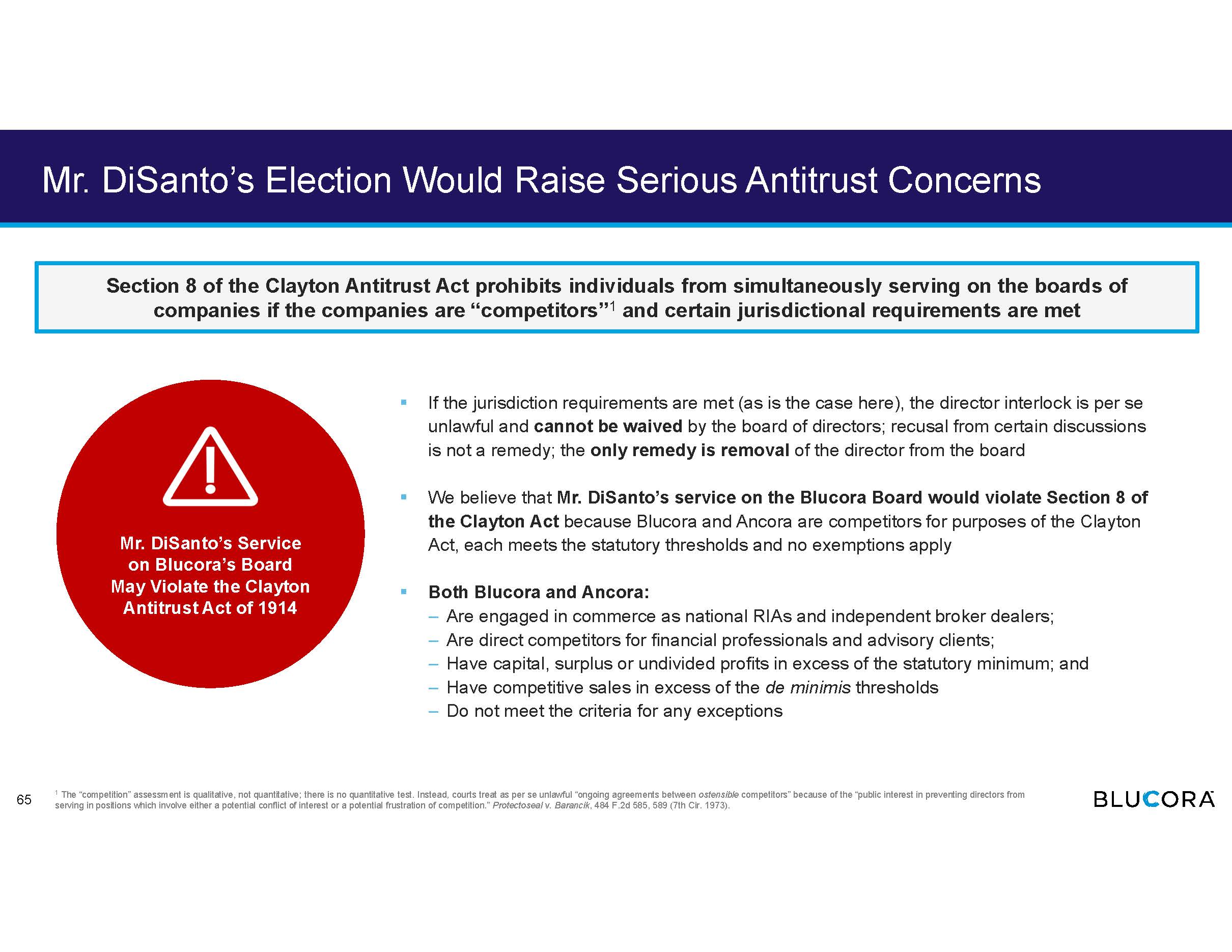

Mr. DiSanto’s Election Would Raise Serious Antitrust Concerns ▪ If the jurisdiction requirements are met (as is the case here), the director interlock is per se unlawful and cannot be waived by the board of directors; recusal from certain discussions is not a remedy; the only remedy is removal of the director from the board ▪ We believe that Mr. DiSanto’s service on the Blucora Board would violate Section 8 of the Clayton Act because Blucora and Ancora are competitors for purposes of the Clayton Act, each meets the statutory thresholds and no exemptions apply ▪ Both Blucora and Ancora : ‒ Are engaged in commerce as national RIAs and independent broker dealers; ‒ Are direct competitors for financial professionals and advisory clients; ‒ Have capital, surplus or undivided profits in excess of the statutory minimum; and ‒ Have competitive sales in excess of the de minimis thresholds ‒ Do not meet the criteria for any exceptions Mr. DiSanto’s Service on Blucora’s Board May Violate the Clayton Antitrust Act of 1914 1 The “competition” assessment is qualitative, not quantitative; there is no quantitative test. Instead, courts treat as per se u nlawful “ongoing agreements between ostensible competitors” because of the “public interest in preventing directors from serving in positions which involve either a potential conflict of interest or a potential frustration of competition.” Protectoseal v. Barancik , 484 F.2d 585, 589 (7th Cir. 1973). 65 Section 8 of the Clayton Antitrust Act prohibits individuals from simultaneously serving on the boards of companies if the companies are “competitors” 1 and certain jurisdictional requirements are met