UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For the fiscal year ended

OR

For the Transition Period from _________ to _________

Commission File Number

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification Number) | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s Telephone Number:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

Securities registered pursuant to Section 12(g) of the Act:

| None | ||

| (Title of class) |

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy statement or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes ☐ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s

assessment of the effectiveness of its internal control over

financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that

prepared or issued its audit report.

Indicate by check mark whether the registrant

is a shell company (as defined in rule 12b-2 of the Exchange Act). Yes ☐

No

The aggregate market value of voting and nonvoting

stock held by non-affiliates of the registrant, based upon the closing price of $3.15 per share for shares of the registrant’s

Common Stock on June 30, 2021, the last business day of the registrant’s most recently completed second fiscal quarter as reported

by the NASDAQ Capital Market, was approximately $

The number of shares of Common Stock outstanding as of April 12, 2022

was

FUTURE FINTECH GROUP INC.

Annual Report on Form 10-K for Fiscal Year Ended December 31, 2021

i

NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K for the fiscal year ended December 31, 2021 (“Annual Report”) of Future Fintech Group, Inc. (together with our direct or indirect subsidiaries, “we,” “us,” “our”, “the Company” or “Future FinTech”) includes forward-looking statements regarding, among other things, Future FinTech’s plans, strategies and prospects, both business and financial. Although Future FinTech believes that its plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, Future FinTech cannot assure you that we will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions including, without limitation, the factors described under “Risk Factors” from time to time in Future FinTech’s filings with the SEC. Many of the forward-looking statements contained in this presentation may be identified by the use of forward-looking words such as “believe”, “expect”, “anticipate”, “should”, “planned”, “will”, “may”, “intend”, “estimated”, “aim”, “on track”, “target”, “opportunity”, “tentative”, “positioning”, “designed”, “create”, “predict”, “project”, “seek”, “would”, “could”, “continue”, “ongoing”, “upside”, “increases” and “potential”, among others. Important factors that could cause actual results to differ materially from the forward-looking statements we make in this presentation are set forth in other reports or documents that we file from time to time with the SEC, and include, but are not limited to:

| ● | fluctuations in the supply of products from our suppliers; | |

| ● | the expected growth of the online retail and supply chain industries in China, asset management business in Hong Kong and global financial technology industry; | |

| ● | changes in general economic conditions and conditions adversely affecting the businesses in which Future FinTech is engaged; | |

| ● | changes in U.S., China and global financial and equity markets, including market disruptions and significant interest rate fluctuations, which may impede our access to, or increase the cost of, external financing for our operations and investments; | |

| ● | our success in implementing our business strategy or introducing new products and services; | |

| ● | our ability to attract and retain customers; | |

| ● | changes in tastes and preferences for, or the consumption of, our products and services; | |

| ● | impact of competitive activities on our business; | |

| ● | the result of future financing efforts; | |

| ● | risks associated with the adverse effects of COVID-19 pandemic globally; | |

| ● | risks associated with conducting business internationally and especially in the People’s Republic of China (“PRC”, or “China”), including currency fluctuations and devaluation, currency restrictions, local laws and restrictions and possible social, political and economic instability; and | |

| ● | change of laws and regulations of blockchain technology and its application to business; | |

| ● | other economic, financial and regulatory factors beyond the Company’s control. |

Any or all of our forward-looking statements in this report may turn out to be inaccurate. They can be affected by inaccurate assumptions we might make or by known or unknown risks or uncertainties. Consequently, no forward-looking statement can be guaranteed. Actual future results may vary materially as a result of various factors, including, without limitation, the risks outlined under “Item 1A. Risk Factors” in this Annual Report. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this filing will in fact occur. You should not place undue reliance on these forward-looking statements.

We undertake no obligation to update forward-looking statements to reflect subsequent events, changed circumstances or the occurrence of unanticipated events except as required by law.

ii

Summary of Significant Risk Factors

The following is a summary of significant risk factors and uncertainties that may affect our business, which are discussed in more detail below in “Part I—Item 1A—Risk Factors” included in this Annual Report on Form 10-K:

Risks Related to Our Business

| ● | An occurrence of an uncontrollable event such as the COVID-19 pandemic may negatively affect our operations and financial results. |

| ● | The supply chain financing service industry is an emerging and rapidly evolving industry in China and we might not achieve the development as we expected. |

| ● | The supply chain financing service industry is increasingly competitive in China. If we fail to compete effectively, we may lose our customers and partners, which could materially and adversely affect our business, financial condition and results of operations. |

| ● | The asset management services that NTAM provides involve various risks, and failure to identify or fully appreciate such risks will negatively affect our reputation, client relationships, operations and prospects. |

| ● | Our operations of NTAM depend on key management and professional staff and our business may suffer if we are unable to recruit or retain them. |

| ● | The regulatory regime governing blockchain technologies, cryptocurrencies, digital assets, and offerings of digital assets is uncertain, and new regulations or policies may materially adversely affect the development of our blockchain related business. |

| ● | We are subject to cyber security risks and may incur increasing costs in an effort to minimize those risks and to respond to cyber incidents. |

| ● | Our business depends on our website, app, network infrastructure and transaction-processing systems. |

Risks Related to Doing Business in the PRC

| ● | Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our business and results of operations. |

| ● | Uncertainties and quick change in the interpretation and enforcement of Chinese laws and regulations with little advance notice could result in a material and negative impact our business operations, decrease the value of our shares of common stock and limit the legal protections available to us. |

iii

| ● | Uncertainties and quick change in the interpretation and enforcement of Chinese laws and regulations with little advance notice could result in a material and negative impact our business operations, decrease the value of our shares of common stock and limit the legal protections available to us. |

| ● | The Chinese government exerts substantial influence over the manner in which we must conduct our business as well as more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers, and may intervene or influence our operations at any time, which could result in a material change in our operations, and significantly limit or completely hinder our ability to offer or continue to offer securities to investors and, and cause the value of our shares of common stock to significantly decline or be worthless. |

| ● | There are uncertainties under the PRC Securities Law relating to the procedures and requisite timing for the U.S. securities regulatory agencies to conduct investigations and collect evidence within the territory of the PRC. |

| ● | The Holding Foreign Companies Accountable Act, or the HFCA Act, and the related regulations are evolving quickly. Further implementations and interpretations of or amendments to the HFCA Act or the related regulations, or a PCOAB’s determination of its lack of sufficient access to inspect our auditor, might pose regulatory risks to and impose restrictions on us because of our operations in mainland China. A potential consequence is that our shares of common stock may be delisted by the exchange. The delisting of our common stock, or the threat of our common stock being delisted, may materially and adversely affect the value of your investment. Additionally, the inability of the PCAOB to conduct full inspections of our auditor deprives our investors of the benefits of such inspections. |

Risks Relating to Our Corporate Structure

| ● | If the PRC government deems that the contractual arrangements in relation to our consolidated variable interest entity do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. |

| ● | The shareholders of our consolidated VIE may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition. |

| ● | Any failure by our consolidated VIE or their shareholders to perform their obligations under our contractual arrangements with them would have a material adverse effect on our business. |

| ● | Our contractual arrangements with our consolidated affiliated entity may not be as effective in providing operational control as direct ownership. |

Risks Related to Our Common Stock

| ● | We are authorized to issue blank check preferred stock, which may be issued without shareholder approval and which may adversely affect the rights of holders of our Common Stock. |

| ● | In recent years, our Common Stock has been in danger of being delisted from the NASDAQ Stock Market (“NASDAQ”). |

Other risks and uncertainties, including those listed under “Part I—Item 1A—Risk Factors”.

These factors should not be construed as exhaustive, and should be read with the other cautionary statements, and other information in this Annual Report on Form 10-K, and our other filings with the SEC.

iv

PART I

ITEM 1 – BUSINESS

Overview

Future FinTech is a holding company incorporated under the laws of the State of Florida. The Company historically engaged in the production and sale of fruit juice concentrates (including fruit purees and fruit juices), fruit beverages (including fruit juice beverages and fruit cider beverages) in People’s Republic of China (“PRC” or “China”). Due to drastically increased production costs and tightened environmental laws in China, the Company had transformed its business from fruit juice manufacturing and distribution to a real-name blockchain based e-commerce platform, supply chain financing services and trading business and financial technology business. The main business of the Company includes an online shopping platform, Chain Cloud Mall (“CCM”), which is based on blockchain technology; supply chain financing services and trading, financial technology service business and the application and development of blockchain-based technology in financial technology services. The Company has also expanded into financial services and cryptocurrency market data and information service businesses.

On May 11, 2021, the Company established Future Supply Chain (Chengdu) Co., Ltd. Its business is coal and aluminum ingots supply chain financing services and trading.

On May 12, 2021, the Company established Future Big Data (Chengdu) Co., Ltd. in Chengdu, China. Its business includes big data technology and industrial internet data services.

On June 8, 2021, the Company established Tianjin Future Private Equity Fund Management Partnership (Limited Partnership) in Tianjin, China. Its main business is external equity investment.

On June 24, 2021, the Company established FTFT Capital Investments L.L.C. in Dubai, United Arab Emirates. In December 2021, FTFT Capital Investments, LLC (“FTFT Dubai”), a subsidiary of the Company, officially launched FTFTX, a cryptocurrency market data platform that provides investors with real-time cryptocurrency market data and trading information from a large number of cryptocurrency exchanges. The market data is available for Bitcoin, ETH, EOS, Litecoin, TRON and other cryptocurrencies at https://www.ftftx.com and via the FTFTX App on iOS and Android devices. The FTFTX app is free to download on Google Play and the Apple Store.

June 14, 2021, the Company established Future FinTech Labs Inc. in New York to serve as its global R&D and technical support center.

On July 2, 2021, the Company established Future Fintech Digital Number One US, LP. which is an investment fund.

On July 6, 2021, the Company established Future Fintech Digital Capital Management, LLC., which provides investment advisory services and investment fund management.

On July 6, 2021, the Company established Future Fintech Digital Number One GP, LLC., which is an off-shore investment fund.

On August 2, 2021, the Company incorporated FTFT UK Limited in United Kingdom as serve as its operating base to develop fintech business in Europe.

On August 6, 2021, the Company completed acquisition of 90% of the issued and outstanding shares of Nice Talent Asset Management Limited (“NTAM”), a Hong Kong-based asset management company, from Joy Rich Enterprises Limited (“Joy Rich”). NTAM is licensed under the Securities and Futures Commission of Hong Kong (“SFC”) to carry out regulated activities in Type 4: Advising on Securities and Type 9: Asset Management.

On August 11, 2021, the Company established Future Private Equity Fund Management (Hainan) Co., Ltd. Its business is investment fund management.

On September 1, 2021, FTFT UK Limited, a company organized under the laws of United Kingdom and a wholly owned subsidiary of the Company (“FTFT UK”) entered into a Share Purchase Agreement with Rahim Shah, a resident of United Kingdom (“Seller”) to acquire 100% of the issued and outstanding shares (the “Sale Shares”) of Khyber Money Exchange Ltd., which is a money transfer company with a platform for transferring money through one of its agent locations or via its online portal, mobile platform or over the phone. Khyber Money Exchange Ltd. is regulated by the UK Financial Conduct Authority (FCA) and the parties are waiting for the approval by the FCA before formal closing of the transaction.

On August 11, 2021, the Company established Future Private Equity Fund Management (Hainan) Co., Ltd. Its business is investment fund management.

On November 22, 2021, the Company established FTFT Digital Number One, Ltd., an investment fund.

On November 22, 2021, the Company established Future Fintech Digital Number One Offshore, LLC., an investment fund.

On December 15, 2021, the Company established FTFT Super Computing Inc. Its business is bitcoin and other cryptocurrency mining and related services.

In March 2022, FTFT UK received has received approval to operate as an Electronic Money Directive (“EMD”) Agent and has been registered as such with the Financial Conduct Authority (FCA), a UK regulator. This status grants FTFT UK the ability to distribute or redeem e-money and provide certain financial services on behalf of an e-money institution (registration number 903050).

Currently, Chain Cloud Mall adopts an “Enterprise Communication as A Service” or eCAAS platform which is a part of 3.15 China Responsible Brand Program run by the Anti-Counterfeiting Committee of China Foundation of Consumer Protection (the “Anti-Counterfeiting Committee”). Anti-Counterfeiting Committee reviews and accepts the companies to join its 3.15 China Responsible Brand Program. After acceptance, these companies are authorized to use anti-counterfeiting labels on their products which have authenticated signatures of these companies and Anti-Counterfeiting Committee recorded on the blockchain quality and safety traceability system controlled by the Anti-Counterfeiting Committee. The companies will sell such products on our eCAAS platform. The companies can also use sales agents to sell their products on our eCAAS platform and parties can negotiate the commission percentages for the products sold. Any new sales agent must be recommended by existing agents and pay a one-time fee to the eCAAS platform to be admitted as the authorized agent to provide sales agent services on the platform.

The Company started its trial operation of NONOGIRL, a cross-border e-commerce platform, in March 2020 and formally launched it in July 2020. The cross-border e-commerce platform aimed to build a new s2b2c (supplier to business and consumer) outsourcing sales platform dominated by social media influencers. It was aimed at the growing female consumer market, with the ability to broadcast, short video, and all forms communication through the platform. It could also create a sales oriented sharing ecosystem with other major social media used by customers, etc. The Company’s promotion strategy previously mainly relied on the training of members and distributors through meetings and conferences. Due to the outbreak of COVID-19, the Chinese government put a restriction on large gatherings. These restrictions made the promotion strategy for our online e-commerce platforms difficult to implement and the Company has experienced difficulties to subscribe new members for its online e-commerce platforms. Due to the lack of new subscribers, in June 2021, the Company suspended its cross-border e-commerce platform (NONOGIRL). Also, since the second quarter of 2021, the Company has transformed its member-based business model of Chain Cloud Mall to a sale agent based “Enterprise Communication as A Service” or eCAAS platform and began to provide supply chain financing services and trading of coal for coal mines and power generation plants as well as aluminum ingots.

1

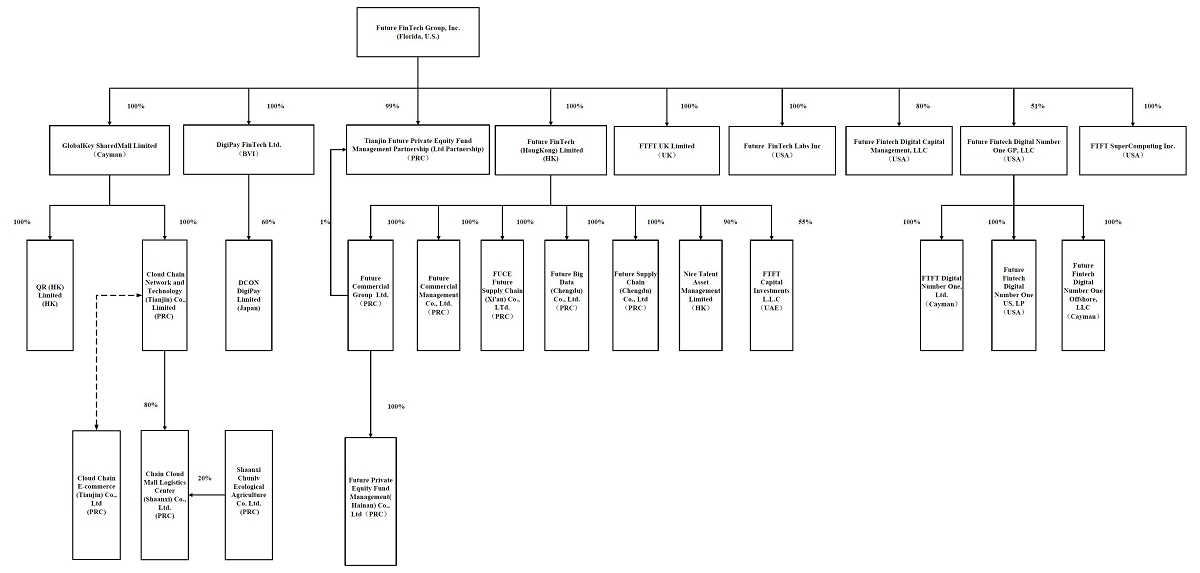

The Company currently has nine direct wholly-owned subsidiaries: DigiPay FinTech Limited (“DigiPay”), a company incorporated under the laws of the British Virgin Islands, Future FinTech (Hong Kong) Limited, a company incorporated under the laws of Hong Kong, GlobalKey Shared Mall Limited, a company incorporated under the laws of Cayman Islands (“GlobalKey Shared Mall”), Tianjin Future Private Equity Fund Management Partnership, a Limited Partnership under the laws of China, FTFT UK Limited, a company incorporated under the laws of United Kingdom, Future Fintech Digital Capital Management, LLC, a company incorporated under the laws of Connecticut, Future Fintech Digital Number One GP, LLC, a company incorporated under the laws of Connecticut, Future FinTech Labs Inc., a company incorporated under the laws of New York and FTFT SuperComputing Inc. a company incorporated under the laws of Ohio.

SkyPeople Foods Holdings Limited (“SkyPeople BVI”) was a wholly owned subsidiary of the Company and a company organized under the laws of the British Virgin Islands, which held 100% of the equity interest of HeDeTang Holdings (HK) Ltd. (“HeDeTang HK”), a company organized under the laws of the Hong Kong Special Administrative Region of the People’s Republic of China (“Hong Kong”), and HeDeTang HK held 73.42% of the equity interest of SkyPeople Juice Group Co., Ltd., (“SkyPeople (China)”), a company incorporated under the laws of the PRC. SkyPeople (China) had eleven subsidiaries in the PRC, which were mainly involved in the production and sales of fruit juice concentrates, fruit juice beverages and other fruit-related products in the PRC and overseas markets. On February 27, 2020, SkyPeople BVI (the “Seller”) completed the transfer of its ownership of HeDeTang HK to New Continent International Co., Ltd. (the “Buyer”), an unrelated third party and a company incorporated in the British Virgin Islands for a total price of RMB 0.6 million (approximately $85,714), pursuant to a Share Transfer Agreement entered into by the Seller and the Buyer on September 18, 2019 and approved at the special shareholders meeting of the Company on February 26, 2020 (the “Sale Transaction”). SkyPeople BVI had no operational assets or business after the transfer and the Company dissolved SkyPeople BVI on July 27, 2020.

Our organizational structure as of the date of this report is set forth in the diagram:

Contractual

Arrangements

Contractual

Arrangements

Equity

Interest

Equity

Interest

2

Our VIE Contractual Arrangements

On July 31, 2019, Cloud Chain Network and Technology (Tianjin) Co., Limited (“CCM Network” or “CCM Tianjin”, formerly known as Chain Cloud Mall Network and Technology (Tianjin) Co., Limited), Cloud Chain E-Commerce (Tianjin) Co., Ltd., formerly known as Chain Cloud Mall E-Commerce (Tianjin) Co., Ltd. (“E-Commerce Tianjin”), a limited liability company incorporated under the laws of China, and Mr. Zeyao Xue and Mr. Kai Xu, citizens of China and together 100% shareholders of E-Commerce Tianjin, entered into the following agreements, or collectively, the “Variable Interest Entity Agreements” or “VIE Agreements,” pursuant to which CCM Network has contractual rights to control and operate the business of E-commerce Tianjin (the “VIE”). Mr. Zeyao Xue is a major shareholder of the Company and the son of Mr. Yongke Xue, the President of the Company. Mr. Kai Xu was the Chief Operating Officer of the Company then and currently is the Deputy General Manager of FT Commercial Group Ltd., a wholly owned subsidiary of the Company and the vice president of blockchain division of the Company.

Pursuant to Chinese law and regulations, a foreign owned enterprise cannot apply for and hold a license for operation of certain e-commerce businesses. CCM Network is an indirectly wholly foreign owned enterprise of the Company (“WFOE”). In order to comply with Chinese law and regulations, CCM Network agreed to provide E-Commerce Tianjin an Exclusive Operation and Use Rights Authorization to operate and use the Chain Cloud Mall System owned by CCM Network. Although the VIE Contractual Arrangements have been widely adopted by PRC companies seeking for listing aboard, such arrangements have not been truly tested in any of the PRC courts. There are very few precedents as to how contractual arrangements in the context of a consolidated variable interest entity should be interpreted or enforced under PRC laws.

The following is a summary of the currently effective contractual arrangements relating to E-Commerce Tianjin.

Contractual Arrangements with Our Consolidated Affiliated Entity and Its Respective Shareholders

Our contractual arrangements with our VIE and its shareholders allow us to (i) exercise effective control over our VIE, (ii) receive substantially all of the economic benefits of our VIE, and (iii) have an exclusive option to purchase all or part of the equity interests in our VIE when and to the extent permitted by PRC law.

As a result of the contractual arrangements with our VIE, we are regarded as the primary beneficiary of our VIE, and we treat the VIE and its subsidiaries as our consolidated affiliated entities under U.S. GAAP. We have consolidated the financial results of our VIE in our consolidated financial statements in accordance with U.S. GAAP.

Agreements that Allow us to Receive Economic Benefits from our VIE

Exclusive Technology Consulting and Service Agreement.

Pursuant to the Exclusive Technology Consulting and Service Agreement, CCM Network agreed to act as the exclusive consultant of E-Commerce Tianjin and provide technology consulting and services to E-Commerce Tianjin. In exchange, E-Commerce Tianjin agreed to pay CCM Network a technology consulting and service fee, the amount of which is to be equivalent to the amount of net profit before tax of E-Commerce Tianjin, payable on a quarterly basis after making up losses of previous years (if necessary) and deducting necessary costs and expenses related to the business operations of E-Commerce Tianjin. Without the prior written consent of CCM Network, E-Commerce Tianjin may not accept the same or similar technology consulting and services provided by any third party during the term of the agreement. All the benefits and interests generated from the agreement, including but not limited to intellectual property rights, know-how and trade secrets, will be CCM Network’s sole and exclusive property. This agreement has a term of 10 years and may be extended unilaterally by CCM Network with CCM Network’s written confirmation prior to the expiration date. E-Commerce Tianjin cannot terminate the agreement early unless CCM Network commits fraud, gross negligence or illegal acts, or becomes bankrupt or winds up.

3

Agreements that Provide us with Effective Control over our VIE

Exclusive Purchase Option Agreement and Power of Attorney.

Pursuant to the Exclusive Purchase Option Agreement, Mr. Zeyao Xue and Mr. Kai Xu granted to CCM Network and any party designated by CCM Network the exclusive right to purchase, at any time during the term of this agreement, all or part of the equity interests in E-Commerce Tianjin, or the “Equity Interests,” at a purchase price equal to the registered capital paid by Mr. Zeyao Xue and Mr. Kai Xu for the Equity Interests, or, in the event that applicable law requires an appraisal of the Equity Interests, the lowest price permitted under applicable law. Pursuant to powers of attorney executed by Mr. Zeyao Xue and Mr. Kai Xu, they irrevocably authorized any person appointed by CCM Network to exercise all shareholder rights, including but not limited to voting on their behalf on all matters requiring approval of E-Commerce Tianjin’s shareholder, disposing of all or part of the shareholder’s equity interest in E-Commerce Tianjin, and electing, appointing or removing directors and executive officers. The person designated by CCM Network is entitled to dispose of dividends and profits on the equity interest without reliance on any oral or written instructions of Mr. Zeyao Xue and Mr. Kai Xu. The powers of attorney will remain in force for so long as Mr. Zeyao Xue and Mr. Kai Xu remain the shareholders of E-Commerce Tianjin. Mr. Zeyao Xue and Mr. Kai Xu have waived all the rights which have been authorized to CCM Network’s designated person under the powers of attorney.

Equity Pledge Agreement.

Pursuant to the Equity Pledge Agreements, Mr. Zeyao Xue and Mr. Kai Xu pledged all of the Equity Interests to CCM Network to secure the full and complete performance of the obligations and liabilities on the part of E-Commerce Tianjin and them under this and the above contractual arrangements. If E-Commerce Tianjin, Mr. Zeyao Xue, or Mr. Kai Xu breaches their contractual obligations under these agreements, then CCM Network, as pledgee, will have the right to dispose of the pledged equity interests. Mr. Zeyao Xue and Mr. Kai Xu agree that, during the term of the Equity Pledge Agreements, they will not dispose of the pledged equity interests or create or allow any encumbrance on the pledged equity interests, and they also agree that CCM Network’s rights relating to the equity pledge should not be interfered with or impaired by the legal actions of the shareholders of E-Commerce Tianjin, their successors or designees. During the term of the equity pledge, CCM Network has the right to receive all of the dividends and profits distributed on the pledged equity. The Equity Pledge Agreements will terminate on the second anniversary of the date when E-Commerce Tianjin, Mr. Zeyao Xue and Mr. Kai Xu have completed all their obligations under the contractual agreements described above.

Spousal Consent Letters. The spouse of Mr. Kai Xu (Mr. Zeyao Xue is not married), the shareholder of E-Commerce Tianjin has signed a spousal consent letter agreeing that the equity interests in E-Commerce Tianjin held by and registered under the name of such shareholder will be disposed pursuant to the contractual agreements with CCM Network. The spouse of such shareholder agreed not to assert any rights over the equity interest in E-Commerce Tianjin held by such shareholder.

We are a holding company incorporated in Florida. As a holding company with no material operations of our own, we conduct a substantial majority of our operations through our subsidiaries and contractual arrangements with our VIE (E-Commerce Tianjin) based in China. The VIE structure is subject to various risks. For example, the contractual arrangements may not be as effective as direct ownership in providing us with control over E-Commerce Tianjin. We expect to rely on the performance by the VIE shareholders of their respective obligations under the contracts to exercise control over E-Commerce Tianjin. The VIE shareholders may not act in the best interests of our company or may not perform their obligations under these contracts. Such risks will exist throughout the period in which we operate related e-commerce platform business through the contractual arrangements. If any dispute relating to these contracts remains unresolved, we will have to enforce our rights under these contracts through the operations of PRC law and arbitration, litigation or other legal proceedings which could be a lengthy process and very costly.

Our PRC operating entities receive a substantial part of our revenue in the RMB. Under our current corporate structure, to fund any cash and financing requirements we may have, the Company may rely on dividend payments from its nine direct wholly-owned subsidiaries. CCM Network will receives payment from E-Commerce Tianjin when it starts to generate profits, pursuant to the VIE Agreements. Under existing PRC foreign exchange regulations, payments of current account items, such as profit distributions and trade and service-related foreign exchange transactions, can be made in foreign currencies without prior approval from State Administration of Foreign Exchange or the SAFE by complying with certain procedural requirements. Therefore, our Chinese subsidiaries are able to pay dividends in foreign currencies to us without prior approval from SAFE, subject to the condition that the remittance of such dividends outside of the PRC complies with certain procedures under PRC foreign exchange regulation, such as the overseas investment registrations by our shareholders or the ultimate shareholders of our corporate shareholders who are PRC residents. Approval from or registration with appropriate government authorities is, however, required where the RMB is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. For the Company and our subsidiaries in Hong Kong, BVI, UK, Dubai and U.S. (“Non-PRC Entities”), there is no restrictions on foreign exchange for such entities and they are able to transfer cash among these entities across borders. Also, there is no restrictions and limitations on the abilities of Non-PRC Entities to distribute earnings from their businesses, including from subsidiaries to the parent company or from the Company to the U.S. investors.

4

Impact of COVID-19 on our Business

In December 2019, a novel strain of coronavirus was reported and has spread throughout China and other parts of the world. On March 11, 2020, the World Health Organization characterized the outbreak as a “pandemic”. In early 2020, Chinese government took emergency measures to combat the spread of the virus, including quarantines, travel restrictions, and the temporary closure of office buildings and facilities in China. In response to the evolving dynamics related to the COVID-19 outbreak, the Company is following the guidelines of local authorities as it prioritizes the health and safety of its employees, contractors, suppliers and business partners. Our offices in China were closed and the employees worked from home at the end of January until late March 2020 and was closed again in January 2022 due to the COVID-19 outbreak. The quarantines, travel restrictions, and the temporary closure of office buildings have materially negatively impacted our business. Our suppliers were negatively affected, and could continue to be negatively affected in their ability to supply and ship products to our customers in case of any resurgence of COVID-19. Our customers that have been negatively impacted by the outbreak of COVID-19 may reduce their budgets to purchase products and services from us, which may materially adversely impact our revenue. The business operations of the third parties’ stores on our e-commerce platform have been and continue to be negatively impacted by the outbreak, which in turn adversely affects the business of our platform as a whole as well as our financial condition and operating results. The outbreak has had and continues to have disruption to our supply chain, logistics providers, customers or our marketing activities with the new variants of COVID-19, which could materially adversely impact our business and results of operations. Although China has already begun to recover from the outbreak of COVID-19, there are still outbreak in various cities and provinces due to new variants, including the recent outbreak of Omicron variant in Xi’an city, Hong Kong and Shanghai city in 2022 which have resulted quarantines, travel restrictions, and temporary closure of office buildings and facilities in these cities. The Company’s promotion strategy of CCM Shopping Mall previously mainly relied on the training of members and distributors through meetings and conferences. Chinese government still puts a restriction on large gatherings. These restrictions made the promotion strategy for our online e-commerce platforms difficult to implement and the Company has experienced difficulties to subscribe new members for its online e-commerce platforms. Due to the lack of new subscribers, in June 2021, the Company suspended its cross-border e-commerce platform NONOGIRL. Also, since the second quarter of 2021, the Company has transformed its member-based Chain Cloud Mall to a sale agent based eCAAS platform and began to provide supply chain financing services.

The global economy has also been materially negatively affected by the COVID-19 and there is continued severe uncertainty about the duration and intensity of its impacts. The Chinese and global growth forecast is extremely uncertain, which would seriously affect our business.

While the potential economic impact brought by, and the duration of COVID-19 and its new variants may be difficult to assess or predict, a widespread pandemic could result in significant disruption of global financial markets, reducing our ability to access capital, which could negatively affect our liquidity. In addition, a recession or market correction resulting from the spread of COVID-19 and its new variants could materially negatively affect our business and the value of our common stock.

Further, as we do not have access to a revolving credit facility, there can be no assurance that we would be able to secure commercial debt financing in the future in the event that we require additional capital. We currently believe that our financial resources will be adequate to see us through the outbreak. However, in the event that we do need to raise capital in the future, outbreak-related instability in the securities markets could adversely affect our ability to raise additional capital.

Consequently, our results of operations have been materially and adversely affected by COVID-19 pandemic. Any potential further impact to our results will depend on, to a large extent, future developments and new information that may emerge regarding the duration and severity of the COVID-19, new variants of COVID-19, the efficacy and distribution of COVID-19 vaccines and the actions taken by government authorities and other entities to contain the COVID-19 or treat its impact, almost all of which are beyond our control.

Company Strategy and Principal Products and Services

Our core business historically has been in the production and sale of fruit juice concentrates (including fruit purees and fruit juices), fruit beverages (including fruit juice beverages and fruit cider beverages) in the PRC and internationally. Due to drastically increased production cost and tightened environmental laws in China, the Company has transformed its main business from fruit juice manufacturing and distribution to a real-name blockchain e-commerce platform that integrates blockchain and internet technology in fiscal year 2019. The e-commerce platform contributed 93.7% to the total revenue for fiscal year 2020. Due to the outbreak of COVID-19, the Chinese government put a restriction on large gatherings. These restrictions made the promotion strategy for our online e-commerce platforms difficult to implement and the Company has experienced difficulties to subscribe new members for its online e-commerce platforms. Due to the lack of new subscribers, since the second quarter of 2021, the Company has transformed its member-based business model of Chain Cloud Mall to a sale agent based eCAAS platform and began to provide supply chain financing services and trading of coal for coal mines and power generation plants as well as aluminum ingots. Also, the Company acquired 90% of the issued and outstanding shares of NTAM, a Hong Kong-based asset management company in August 2021. NTAM is licensed under the Securities and Futures Commission of Hong Kong (“SFC”) to carry out regulated activities in Type 4: Advising on Securities and Type 9: Asset Management. During the fiscal year of 2021, the supply chain financing and wealth management business of NTAM contributed 78.75% and 21.22% of our revenues, respectively.

5

On September 1, 2021, FTFT UK entered into a Share Purchase Agreement with Rahim Shah, a resident of United Kingdom (“Seller”) to acquire 100% of the issued and outstanding shares (the “Sale Shares”) of Khyber Money Exchange Ltd., which is a money transfer company with a platform for transferring money through one of its agent locations or via its online portal, mobile platform or over the phone. Khyber Money Exchange Ltd. is regulated by the UK Financial Conduct Authority (FCA) and the parties are waiting for the approval by the FCA before formal closing of the transaction.

In December 2021, FTFT Capital Investments, LLC officially launched FTFTX, a cryptocurrency market data platform that provides investors with real-time cryptocurrency market data and trading information from a large number of cryptocurrency exchanges. The market data is available for Bitcoin, ETH, EOS, Litecoin, TRON and other cryptocurrencies at https://www.ftftx.com and via the FTFTX App on iOS and Android devices. The FTFTX app is free to download on Google Play and the Apple Store.

In March 2022, FTFT UK FTFT UK received has received approval to operate as an Electronic Money Directive (“EMD”) Agent and has been registered as such with the Financial Conduct Authority (FCA), a UK regulator. This status grants FTFT UK the ability to distribute or redeem e-money and provide certain financial services on behalf of an e-money institution (registration number 903050).

The Company is in the process of transition and developing its financial technology related business, including asset management, supply chain financial services, digital banking and payment services, blockchain based e-commerce, and cryptocurrency market data services.

Chain Cloud Mall (CCM)

The trial operation of CCM started on December 26, 2018. On January 22, 2019, the Company formally launched Chain Cloud Mall, the real-name and membership-based blockchain shared shopping mall platform that integrates blockchain and internet technology. On June 1, 2019, CCM v2.0 was launched and on May 1, 2020, CCM v3.0 was launched. The blockchain technology enables CCM to record every event or transaction on a distributed ledger and makes the whole process traceable. It also enables the CCM to record and provide CCM points to its members upon a successful new member and/or product referral, which can be used as credit when making purchases on CCM. It incentivizes its members to promote the platform and share the products with their social contacts, which in turn increases the sales through CCM.

Due to the outbreak of COVID-19, the Chinese government put a restriction on large gatherings. These restrictions made the promotion strategy for our online e-commerce platforms difficult to implement and the Company has experienced difficulties to subscribe new members for its online e-commerce platforms. Due to the lack of new subscribers, since the second quarter of 2021, the Company has transformed its member-based business model of CCM to a sale agent based eCAAS platform.

Currently, Chain Cloud Mall adopts an “Enterprise Communication as A Service” or eCAAS platform which is a part of 3.15 China Responsible Brand Program run by the Anti-Counterfeiting Committee of China Foundation of Consumer Protection (the “Anti-Counterfeiting Committee”). Anti-Counterfeiting Committee reviews and accepts the companies to join its 3.15 China Responsible Brand Program. After acceptance, these companies are authorized to use anti-counterfeiting labels on their products which have authenticated signatures of these companies and Anti-Counterfeiting Committee recorded on the blockchain quality and safety traceability system controlled by the Anti-Counterfeiting Committee. The companies will sell such products on our eCAAS platform. The companies can also use sales agents to sell their products on our eCAAS platform and parties can negotiate the commission percentages for the products sold. Any new sales agent must be recommended by existing agents and pay a one-time fee to the eCAAS platform to be admitted as the authorized agent to provide sales agent services on the platform.

6

Coal and Aluminum Ingots Supply Chain Financing Service and Trading

Since the second quarter of 2021, we started coal supply chain financing service and trading business. Since the third quarter of 2021, we started aluminum ingots supply chain financing service and trading business.

Our supply chain finance business mainly serves the receivables and payables of industrial customers, obtains the creditor’s rights or commodity goods rights of large state-owned enterprises through trade execution, provides customers with working capital, accelerates capital turnover, and then expands the business scale and improves the industrial value.

Through our supply chain service ability and customer resources, we can tap into low-risk assets, flexibly carry out financial services around the actual financial needs of certain industries, and reduce the overall risk of the business by using the control of business flow, goods logistics and capital flow in the process of commodity circulation.

We focus on bulk coal and aluminum ingots an take large state-owned or listed companies as the core service targets; We use our own funds as the operation basis, actively uses a variety of channels and products for financing, such as banks, commercial factoring companies, accounts receivable, asset-backed securities, and other innovative financing methods to obtain sufficient funds.

We sign purchase and sale agreements with suppliers and buyers. The suppliers are responsible for the supply and transportation of coal to the end users’ designated freight yard or transfer the title of aluminum ingots to us in certain warehouses. We select the customers and suppliers that have good credit and reputation.

Asset Management Service.

NTAM was founded in 2018 and it engages asset management and advisory services. NTAM is licensed under the Securities and Futures Commission of Hong Kong (SFC) for carrying out regulated activities in “Advising on Securities” and “Asset Management”. NTAM offers diversified asset management portfolio for professional investors. Assets of NTAM’s clients are held in banks, where clients gave the banks their authorization allowing NTAM to place trading instructions on behalf of the clients in order to manage the clients’ assets.

NTAM mainly engages in following asset management services for its clients:

(1) Equity Investment

NTAM manages clients’ investment portfolio in stocks of the companies listed on the international market with strong liquidity. At the same time, it selects companies that have unique or differentiated businesses, realizing above average profit growth.

(2) Debt investment

When NTAM manages clients’ investment portfolio in bonds that are denominated in major international currencies such as US dollar, euro and sterling, the issuer of debts shall have good credit rating and asset liability ratio. Through active management, NTAM focus in bonds with higher yield to maturity among bonds with the same maturity and credit rating.

(3) Precious metals and currencies investment

NTAM also manages clients’ investment portfolio in major international currencies and precious metals, including US dollar, euro, British pound, Japanese yen, Australian dollar and offshore Chinese yuan. Precious metals include gold, platinum and silver. With research on the fundamentals of market supply and demand to predict the trend of commodity prices, NTAM endeavors to improve the rate of return for clients through dual currency investment, options and structured products.

(4) Derivative Investment

NTAM also manages clients’ investment portfolio in financial derivatives in different asset classes, such as options and structured products.

7

(5) External Asset Management Services (EAM)

This business takes customer demand as the service purpose, cooperates with several private banks which provide asset custody services, and innovatively introduces the function of investment bank to provide exclusive private solutions for our clients.

NTAM’s main revenue is generated from providing professional advices to clients and management fees for managing the investment of the clients. As of March 15, 2022, NTAM has approximately US$260 million assets under its management.

Competition and our Competitive Advantages

E-Commerce Market in China

The e-commerce industry in China is intensely competitive. Our competitors include all major e-commerce companies in China, and other internet companies that engage in social e-commerce businesses.

We anticipate that the e-commerce industry will continually evolve and will continue to experience rapid technological change, evolving industry standards, shifting customer requirements, and frequent innovation. We must continually innovate to remain competitive.

We have a unique real-name based blockchain e-commerce shopping platform that integrates blockchain, internet technology and distinguishes itself through its eCAAS platform which is a part of 3.15 China Responsible Brand Program run by the Anti-Counterfeiting Committee of China Foundation of Consumer Protection. Our platform utilizes technologies that read the authenticated signatures of the companies and Anti- Counterfeiting Committee on the products that are recorded on the blockchain quality and safety traceability system controlled by the Anti-Counterfeiting Committee. We work closely with Anti-Counterfeiting Committee of the China Foundation of Consumer Protection which is the first and only organization that is approved by China’s Ministry of Civil Affairs that specializes in anti- counterfeiting in China. .

Asset Management Market in Hong Kong

We believe NTAM has the following competitive advantages in the asset management market in Hong Kong:

(1) Provide customers with comprehensive and professional financial services

NTAM currently holds Type 4 (Securities Advisory) and Type 9 (Asset Management) regulated activity licenses issued by the Hong Kong Securities and Futures Commission. It can provide a series of professional financial services for customers, including providing financial advisory services, and various capital entrusted investment management services for the investment in the companies and instruments listed or unlisted on the stock exchanges in Hong Kong, mainland China and worldwide.

(2) Simple and efficient management structure

Compared with the multi-level structure with multiple approval procedures by other large firms, NTAM adopts a more concise and efficient direct reporting system. Each business team can directly report the business to the board of directors of NTAM, which provides fast and efficient services for the company’s customers, quickly responds to the changes of market conditions, timely seizes market investment opportunities and responds to adverse factors.

(3) An experienced and diligent management team

The senior managers in NTAM have many years of experience in private banks and accounting firms and some of them have been in the asset management industry for more than 10 years. The management team has a comprehensive vision and efficient execution ability, and can bring more incremental business to the company with their professional advantages and personal resources.

8

(4) Maintain close and stable relationship with customers

NTAM has established a close and stable business relationship with its existing customers and understood their long-term business objectives, strategies and preferences, so that it can provide customized advisory and asset management services to the customers. NTAM believes its market reputation and existing customers’ confidence in the company can promote customers to introduce and bring new customers.

Supply Chain Finance Market in China

We believe our supply chain finance business has the following competitive strengths and set us apart from our competitors:

(1) Independent risk control management system

At the beginning of its establishment, we established a complete and independent risk control management system for our supply chain fiancé business, and have strictly implemented the unified and comprehensive risk control management for customer access, contract signing, business execution, and capital allocation.

(2) High-quality customer groups

The criteria for our corporate clients are generally the wholly owned or controlled subsidiaries of large state-owned companies or publicly listed companies. At present, our customers are mainly in the coal and metal industries, power generation and heating industries, which includes subsidiary of China Datang Corporation, one of the five large-scale power generation enterprises in China and Shanxi Lu’an Environmental Protection Energy Development Co., Ltd. (a public company listed on Shanghai Stock Exchange).

(3) Standardization of financing process and system

To improve operational efficiency and decision-making timeliness, we have established a standardized financing process and system to provide supply chain finance and services.

(4) Access to capital market

One of the key elements to the supply chain finance is to have access to sufficient funds in order to expand its business and increase number of clients. Our supply chain business will take the advantage as a subsidiary of the public company of Future FinTech as well as its other financial technology business development to obtain enough funds for its further development and provide comprehensive financial services to its clients.

Industry and Principal Markets

E-Commerce Market in China

According to emarketer data, the global e-commerce market is expected to reach US$4.89 trillion in 2021. China is leading the global e-commerce market, with online sales of nearly $2.8 trillion in 2021, accounting for half of the total global e-commerce market. The United States, which ranks second in the world, is expected to have a total e-commerce market of about US$843 billion in 2021. In addition, China’s digital consumers reached 792.5 million, accounting for 33.3% of the global total, ranking first in the world. In terms of retail, 52.1% of China’s retail transactions come from e-commerce, and China will become the first country in history where online retail sales exceed offline retail sales.

9

Asset Management Market in Hong Kong

According to a report by Research Office Information Services Division Legislative Council Secretariat on April 30, 2021, asset management is an important pillar for Hong Kong as an international financial center. While Hong Kong serves as the gateway for overseas investors to invest in the mainland China, it also serves as the gateway for the mainland investors to invest in overseas markets at the same time. This has contributed to the rapid development of the asset management industry in Hong Kong. According to the latest available information, asset management accounted for 1.0% of Hong Kong’s Gross Domestic Product in 2017. As at end-2020, there were 1,914 companies licensed by or registered with the Securities and Futures Commission (“SFC”) to carry out asset management business, representing an increase of 78% over 2014. Over the same period, the number of individuals licensed for asset management also grew from 7,729 to 13,074. The thriving development of the sector is also reflected in the rising trend in the revenue received by the industry. According to the Census and Statistics Department of Hong Kong, the business receipts index for the industry increased to 135 in 2020, representing an increase of 45% over 2014. According to a survey by SFC, Hong Kong’s asset management business amounted to HK$17.9 trillion (approximately US$2.29 trillion) as at end-2019. Within the industry, licensed corporations (e.g. fund houses) were the major market players, accounting for 87% of the total business. This was followed by registered institutions (i.e. banks engaging in asset management business) (7%) and insurance companies (6%).

Supply Chain Finance Market in China

Supply chain finance has become an important financing channel for small and medium-sized enterprises in China. Although China started late in supply chain finance, thanks to the favorable regulatory environment and good economic development, the scale of China’s supply chain financial market is expected reach RMB 29 trillion (approximately US$4.46 trillion) in 2022 according to the Overview Survey and Development Strategy Research Consulting Report for China Supply Chain Finance Industry 2021-2025 by Zhongyan Puhua Industry Research Institute.

The market participants in supply chain finance business in China are diversified, among which supply chain management service companies, internet financial platforms and business sections of commercial banks have a total market share of nearly 60%, according to the 2021 China Supply Chain Finance Market Forecast and Investment Strategy Planning Analyst Report by Qianzhan Industry Research Institute.

Since 2021, the performance of bulk commodities has been particularly strong. Affected by COVID-19 pandemic and related supply chain disruption, economic recovery, monetary easing and the carbon emission control goal, the prices of bulk commodities have been rising, among which the price of coal has reached a new high in 2021. In this context, the active trading situation and market demand provide a good business environment for commodity supply chain enterprises.

Commodity supply chain is an important part of modern economic system. The development of China’s bulk commodity supply chain is conducive to the optimal allocation of bulk commodity resources and further enhance China’s competitiveness and voice in the global bulk commodity market.

In recent years, thanks to good economic development and favorable policy support, China’s supply chain financial market has developed rapidly. The scale of supply chain financial market in China has increased from RMB 16.7 trillion in 2016 to RMB 28.6 trillion in 2021, with an average annual compound growth rate of 10.5%. The market scale in 2022 is expected to be the same as that in 2021, according to the Overview Survey and Development Strategy Research Consulting Report for China Supply Chain Finance Industry 2021-2025 by Zhongyan Puhua Industry Research Institute.

The Chinese government has regarded the development of supply chain finance as an effective way to promote the real economy and supply chain industry. The Guideline Opinions of Promoting Supply Chain Finance to Serve the Real Economy issued by China Banking and Insurance Regulatory Commission in 2019 and the Opinions on Management of the Development of Supply Chain Finance to Support the Stable Business Cycle and Optimized Upgrade for Supply Chain Industry jointly issued by the People’s Bank of China, the Ministry of Industry and Information Technology (“MIIT”), the Ministry of Commerce, China Banking and Insurance Regulatory Commission and four other regulatory departments in 2020 are designed to encourage and promote the development of supply chain industry.

10

Marketing and Sales

Due to the lack of new member subscriptions caused by restrictions on our promotion strategy for the control of spread of COVID-19, we have transformed the CCM shopping mall to an “Enterprise Communication as A Service” or eCAAS platform. The eCAAS platform is entrusted by the Anti-Counterfeiting Committee of the China Foundation of Consumer Protection (the “Anti-Counterfeiting Committee”) to run its 3.15 China Responsible Brand Program.

Anti-Counterfeiting Committee will review and accept the companies to join its 3.15 China Responsible Brand Program. After acceptance, these companies are authorized to use anti-counterfeiting labels on their products and sell them on our eCAAS platform. The companies can also use sales agents to sell their products on our eCAAS platform and parties can negotiate the commission percentages for the products sold. Any new sales agent must be recommended by existing agents and pay a one-time fee to the eCAAS platform to be admitted as the authorized agent to provide sales agent services on the platform.

We market our supply chain financing services to large state-owned or controlled enterprises and public company, with a focus on energy and metal industries. Our supply chain finance business has established a high-quality team that fully understands our strategy and market situation and is sensitive to market changes to find target customers and expand our business. Based on standardized operation, our team has established a good reputation in the cooperation with existing customers, and to reach out to their respective upstream and downstream business partners to expand our business scope.

NTAM has multidimensional flexible layout for its business development. It manages clients’ investment portfolio in a diversified manner across multiple asset classes in global markets . The type and proportion of positions are determined according to the long-term and short-term investment goals of investors and other market factors. In terms of specific operation, NTAM relies on solid investment and research ability to flexibly adjust its position and avoid the price fluctuation of its subject matter caused by risk events. NTAM also uses “License + talent” to maintain core competitiveness. With its Type 4 (Securities Advisory) and Type 9 (Asset Management) licenses issued by the Hong Kong Securities and Futures Commission, NTAM continues to take the advantages of such licenses to optimize its business structure, expand the business scale, actively expand business opportunities in different regions, continue to recruit outstanding talents in the industry, and introduce incentive measures for the senior management, so as to maintain the development vitality of the company, continuously strengthening the core competitiveness. NTAM runs its risk management system throughout its core business operations and continuously evaluates the potential risks that may cause impact in the daily operation of its business segment, including evaluating the effectiveness of existing internal control measures, whether they are sufficient to deal with potential risks and whether they need to be supplemented. The relevant review results are entered in time to analyze the potential strategic impact, so that the internal control measures can be more effective and timely, and ensure the steady operation of the company while developing rapidly.

11

Government Regulations

Regulations on Cybersecurity Review

On December 28, 2021, Cybersecurity Review Measures was published by Cyberspace Administration of China or the CAC, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, Ministry of State Security, Ministry of Finance, Ministry of Commerce, People’s Bank of China, State Administration of Radio and Television, China Securities Regulatory Commission, State Secrecy Administration and State Cryptography Administration, effective on February 15, 2022, which provides that, Critical Information Infrastructure Operators (“CIIOs”) that intend to purchase internet products and services and Data Processing Operators (“DPOs”) engaging in data processing activities that affect or may affect national security shall be subject to the cybersecurity review by the Cybersecurity Review Office. On November 14, 2021, CAC published the Administration Measures for Cyber Data Security (Draft for Public Comments), or the “Cyber Data Security Measure (Draft)”, which requires cyberspace operators with personal information of more than 1 million users who want to list abroad to file a cybersecurity review with the Office of Cybersecurity Review. Our e-commerce platform currently is not a cyberspace operator with personal information of more than 1 million users or has activities that affect or may affect national security.

Regulations Relating to E-Commerce

In January 2014, State Administration for Market Regulation or SAMR (formerly known as State of Administration of Industry and Commerce) adopted the Administrative Measures for Online Trading, or the Online Trading Measures, which took effect in March 2014. Under the Online Trading Measures, e-commerce platform operators are required to examine, register and archive the identity information of the merchants applying for access to their platforms as sellers, and verify and update such information regularly. The Online Trading Measures also provide that e-commerce platform operators must make publicly available (i) the link to or the information contained in the business licenses of the merchants, in the case of business entities, or (ii) a label confirming the verified identity of the merchants, in the case of individuals. A consumer is entitled to return the commodities within seven days after receipt of the commodities without giving a reason, except for the following commodities: customized commodities, fresh and perishable commodities, audio-visual products downloaded online or unpackaged by consumers and computer software and other digital commodities, and newspapers and journals that have been delivered. E-commerce platform operators must, within seven days upon receipt of the returned commodities, provide full refunds to consumers. In addition, operators are prohibited from setting forth provisions in contracts or other terms that are not fair or reasonable to consumers such as those excluding or restraining consumers’ rights, relieving or exempting operators’ responsibilities, and increasing the consumers’ responsibilities, or conducting transactions in a forcible manner taking advantage of contractual terms or technical means.

In March 2016, the State Administration of Taxation, or the SAT, the Ministry of Finance, or the MOF, and the General Administration of Customs jointly issued the Circular on Tax Policy for Cross-Border E-Commerce Retail Imports, which took effect in April 2016. Pursuant to this circular, goods imported through the cross-border e-commerce retail are subject to tariff, import value-added tax, and consumption tax based on the types of goods. Individuals purchasing any goods imported through cross-border e-commerce retail are taxpayers, and e-commerce companies, companies operating e-commerce transaction platforms or logistic companies are required to withhold the taxes.

On August 31, 2018, the Standing Committee of the National People’s Congress promulgated the E-Commerce Law, which became effective on January 1, 2019. The E-Commerce Law sets forth a series of requirements on e-commerce platform operators. According to the E-Commerce Law, e-commerce platform operators shall verify and register platform merchants, and cooperate with the market regulatory administrative department and tax administrative department to conduct industry and commerce registrations and tax registrations for merchants. The e-commerce platform operators shall also prepare a contingency plan for cybersecurity events and take technological measures and other measures to prevent online illegal and criminal activities. The E-Commerce Law also expressly requires platform operators to take necessary actions to ensure fair dealing on their platforms to safeguard the legitimate rights and interests of consumers, including to prepare platform service agreements and transaction information record-keeping and transaction rules, to prominently display such documents on the platform’s website, and to keep such information for no fewer than three years following the completion of a transaction. To legally handle intellectual property infringement disputes, upon receipt of the notice specifying preliminary evidence for alleged infringement, the platform operators are required to take necessary measures in a timely manner, such as deleting, blocking and disconnecting the hyperlinks, terminating transactions and services, and forwarding notices to merchants on its platform. If an e-commerce platform operator fails to take necessary measures when it knows or should have known that a merchant on the platform infringes any third-party intellectual property rights, products or services provided by a merchant on its platform do not meet the requirements regarding personal or property safety, or any merchant otherwise impairs the lawful rights and interests of consumers, the e-commerce platform operator will be held jointly liable with the merchants on its platform.

12

Moreover, the E-Commerce Law imposes a requirement on operators of e-commerce platforms to assist in tax collection with respect to income generated by sellers from transactions conducted on e-commerce platforms, including among others, submitting to the tax authority information on the identities of sellers on e-commerce platforms and other information relating to tax payment. Failure to comply with the requirement may result in operators of e-commerce platform being subject to fines and, in severe circumstances, suspension of business operations of e-commerce platforms. If the merchants on our platform were deemed to be selling our products on consignment basis, the PRC tax authorities may require our members to make tax registration and request our assistance in these efforts, pursuant to the new E-Commerce Law, and the merchants may be subject to more stringent tax compliance requirements. See “Risk Factors— Failure to comply with the relatively new E-Commerce Law may have a material adverse impact on our business, financial conditions and results of operations.” According to the EIT Law, the VAT Law and other applicable regulations, sellers that conduct transactions on e-commerce platforms are generally subject to enterprise income tax at a rate of 25%, and value-added tax at a rate of 13% or 9% for services or products sold on the e-commerce platforms. Certain sellers that are deemed as small taxpayers under PRC law are subject to reduced value-added tax at a rate of 3%.

Value-Added Telecommunication Business Operating Licenses

The PRC Telecommunications Regulations, or the Telecom Regulations, which were issued by the State Council in 2000 and were most recently amended in February 2016 are the primary governing law on telecommunication services. The Telecom Regulations set out the general framework for the provision of telecommunication services by PRC entities. Under the Telecom Regulations, telecommunications service providers are required to procure operating licenses prior to their commencement of operations. The Telecom Regulations draw a distinction between “basic telecommunications services” and “value-added telecommunications services.” A “Catalog of Telecommunications Business” was issued as an attachment to the Telecom Regulations to categorize telecommunications services as basic or value-added. In December 2015, MIIT released the Catalog of Telecommunication Business (2015 Revision), or the 2015 Telecom Catalog, implemented in March 2016. Under the 2015 Telecom Catalog, both the online data processing and transaction processing business (i.e., operating e-commerce business) and information service business, continue to be categorized as value-added telecommunication services.

In March 2009, MIIT issued the Administrative Measures for Telecommunications Business Operating Permit, or the Telecom Permit Measures, which was implemented in 2009 and most recently amended in 2017. Pursuant to the Telecom Permit Measures, the operation scope of the value-added telecommunication business operating license, or VATS license, shall detail the permitted activities of the enterprise to which it is granted. An approved telecommunication services operator shall conduct its business in accordance with the specifications recorded on its VATS License. The VATS Licenses can be further categorized based on the specific business operations permitted to be carried out under such licenses, including among others, the VATS Licenses for internet information services, or the ICP License, and the VATS License for electronic data interchange business, or the EDI License. In addition, a VATS License holder is required to obtain approval from the original permit-issuing authority prior to any change to its shareholders, business scope or other information recorded on such license. In February 2015, the State Council issued the Decisions on Cancelling and Adjusting a Batch of Administrative Approval Items, which, among other things, replaced the pre-registration approval requirement for telecommunications businesses with a post-registration approval requirement.

In September 2000, the State Council promulgated the Administrative Measures on Internet Information Services, or the Internet Measures, most recently amended in January 2011. Under the Internet Measures, “internet information services” refer to the provision of information through the internet to online users, and are divided into “commercial internet information services” and “non-commercial internet information services”. Commercial internet information services operators shall obtain an ICP License, from the relevant government authorities within China. E-commerce (Tianjin), our VIE, holds our VATS License for our Value-Added Telecommunication businesses.

13

Regulations Relating to Internet Information Security and Privacy Protection

Internet information in China is regulated from a national security standpoint. The National People’s Congress, or the NPC, enacted the Decisions on Preserving Internet Security in December 2000 and amended in August 2009, which subject violators to potential criminal punishment in China for any attempt to: (i) gain improper entry into a computer or system of strategic importance; (ii) disseminate politically disruptive information; (iii) leak state secrets; (iv) spread false commercial information; or (v) infringe intellectual property rights. The Ministry of Public Security of the PRC, or the MPS, promulgated the Administrative Measures for the Computer Information Network and Internet Security Protection in December 1998 and amended in January 2011, which prohibits use of the internet in ways which, among other things, result in a leak of state secrets or a spread of socially destabilizing content. If an internet information service provider violates these measures, the MPS and its local branches may issue a warning, confiscate the illegal gains, impose fines, and, in severe cases, advise competent authority to revoke its operating license or shut down its websites.

Under the Several Provisions on Regulating the Market Order of Internet Information Services, issued by the MIIT in December 2011 and implemented in March 2012, an internet information service provider may not collect any user personal information or provide any such information to third parties without the consent of the user. An internet information service provider must expressly inform the users of the method, content and purpose of the collection and processing of such user personal information and may only collect such information necessary for the provision of its services. An internet information service provider is also required to properly maintain the user’s personal information, and in case of any leak or likely leak of the user’s personal information, the internet information service provider must take immediate remedial measures and, in severe circumstances, immediately report to the telecommunications authority. Moreover, pursuant to the Ninth Amendment to the Criminal Law issued by Standing Committee of the National People’s Congress (the “SCNPC”) in August 2015 and implemented in November 2015, any internet service provider that fails to fulfill the obligations related to internet information security administration as required by applicable laws and refuses to rectify such failure upon orders, shall be subject to criminal penalty for the result of (i) any dissemination of illegal information in large scale; (ii) any severe effect due to the leakage of the client’s information; (iii) any serious loss of criminal evidence; or (iv) other severe situation. Any individual or entity that (i) sells or provides personal information to others in a way violating the applicable law, or (ii) steals or illegally obtains any personal information, shall be subject to criminal penalty in severe situation. In addition, the Interpretations of the Supreme People’s Court and the Supreme People’s Procuratorate of the PRC on Several Issues Concerning the Application of Law in Handling Criminal Cases of Infringing Personal Information, issued in May 2017 and implemented in June 2017, clarified certain standards for the conviction and sentencing of the criminals in relation to personal information infringement.