UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 1)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from _________to _________

Commission File Number 001-34502

Future FinTech Group Inc.

(Exact name of registrant as specified in its charter)

| Florida | 98-0222013 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification Number) | |

| Room 2103, 21st Floor, SK Tower 6A | ||

Jianguomenwai Avenue, Chaoyang District Beijing, PRC |

100022 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s Telephone Number: 86-10- 8589-9303

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $0.001 par value | Nasdaq Capital Market |

Securities registered pursuant to Section 12(g) of the Act:

| None | ||

| (Title of class) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy statement or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes ☐ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| Emerging growth company | ☐ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of voting and nonvoting stock held by non-affiliates of the registrant, based upon the closing price of $1.25 per share for shares of the registrant’s Common Stock on June 28, 2019, the last business day of the registrant’s most recently completed second fiscal quarter as reported by the NASDAQ Capital Market, was approximately $9.57 million.

The number of shares of Common Stock outstanding as of May 29, 2020 was 38,345,415.

EXPLANATORY NOTE

In response to a comment letter received from the Securities and Exchange Commission (the “SEC”), dated September 29, 2020, Future FinTech Group, Inc. (the “Company,” “we,” “us” or “our”) is filing this Amendment No. 1 on Form 10-K/A to our Annual Report on Form 10-K for the year ended December 31, 2019, originally filed with the SEC on June 2, 2020 (the “Original Form 10-K”) to correct typographical errors in Item 7 Management’s Discussion and Analysis of Financial Condition and Results of Operation and on page F-17 of the Original Form 10-K which incorrectly stated our long term investment in InUnion Chain Limited (“InUnion”) included the INU Digital Assets Token and 10% equity investment in InUnion, however, it should only be 10% equity investment in InUnion without any INU Digital Assets Token as the Company didn’t purchase or own any INU Digital Assets Token. Except as described above, this Form 10-K/A does not modify, amend, or otherwise supplement the Original Form 10-K.

This Form 10-K/A should be read in conjunction with the Company’s periodic filings made with the SEC subsequent to the filing date of the Original Form 10-K, including any amendments to those filings, as well as any Current Reports, filed on Form 8-K subsequent to the date of the Original Form 10-K. In addition, in accordance with applicable rules and regulations promulgated by the SEC, the Company’s Chief Executive Officer and Chief Financial Officer are providing currently dated certifications in connection with this Form 10-K/A. The certifications are filed as Exhibits 31.1, 31.2, 32.1 and 32.2. Because this Form 10-K/A sets forth the Original Form 10-K in its entirety, it includes both items that have been changed as a result of the amended disclosures and items that are unchanged from the Original Form 10-K. Other than the revision of the disclosures as discussed above, this Form 10-K/A speaks as of the original filing date of the Original Form 10-K and has not been updated to reflect other events occurring subsequent to the original filing date. This includes forward-looking statements and all other sections of this Form 10-K/A that were not directly impacted by this amendment, which should be read in their historical context.

FUTURE FINTECH GROUP INC.

Annual Report on Form 10-K for Fiscal Year Ended December 31, 2019

i

SPECIAL NOTE REGARDING RELIANCE ON RELIEF ORDER

On March 25, 2020 we filed a Current Report on Form 8-K in compliance with and in reliance upon the SEC Order issued pursuant to Section 36 of the Securities Exchange Act of 1934, as amended, granting Exemptions from Specified Provisions of the Exchange Act and Certain Rules thereunder (SEC Release No. 34-88465 on March 25, 2020) (the “Relief Order”). By way of filing the Current Report, we, among other things, extended the time of filing of our Annual Report on Form 10-K for the fiscal year ended December 31, 2019 (the “Annual Report”), until no later than May 14, 2020 in reliance on the Relief Order. The Current Report disclosed the reasons that our Annual Report could not be filed timely.

As required by the Relief Order, we hereby disclose that we were unable to timely file our Annual Report and had to avail ourselves of the Relief Order because of the following issues posed by the COVID-19 outbreak:

In December 2019, a novel strain of coronavirus was reported to have surfaced in Wuhan, China, which has and is continuing to spread throughout China and other parts of the world, including the United States. On January 30, 2020, the World Health Organization declared the outbreak of the coronavirus disease (COVID-19) a “Public Health Emergency of International Concern,” and on March 11, 2020, the World Health Organization characterized the outbreak as a “pandemic”. Xi’an City and Beijing City, where our headquarters are located, are among the most affected areas in China. The Company has been following the orders of local government and health authorities to minimize exposure risk for its employees, including the closures of its offices and having employees work remotely. Our offices were closed for the Lunar New Year Holiday Break in late January 2020 and remained closed as a result of the outbreak until late March 2020. As a result, the Company’s books and records were not easily accessible, resulting in a delay in the preparation, audit and completion of the Company’s financial statements for the Annual Report.

NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K for the fiscal year ended December 31, 2019 (“Annual Report”) of Future Fintech Group, Inc. (together with our direct or indirect subsidiaries, “we,” “us,” “our”, “the Company” or “Future FinTech”) includes forward-looking statements regarding, among other things, Future FinTech’s plans, strategies and prospects, both business and financial. Although Future FinTech believes that its plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, Future FinTech cannot assure you that we will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions including, without limitation, the factors described under “Risk Factors” from time to time in Future FinTech’s filings with the SEC. Many of the forward-looking statements contained in this presentation may be identified by the use of forward-looking words such as “believe”, “expect”, “anticipate”, “should”, “planned”, “will”, “may”, “intend”, “estimated”, “aim”, “on track”, “target”, “opportunity”, “tentative”, “positioning”, “designed”, “create”, “predict”, “project”, “seek”, “would”, “could”, “continue”, “ongoing”, “upside”, “increases” and “potential”, among others. Important factors that could cause actual results to differ materially from the forward-looking statements we make in this presentation are set forth in other reports or documents that we file from time to time with the SEC, and include, but are not limited to:

| ● | fluctuations in the supply of products from our suppliers; |

| ● | the expected growth of the online retail industry in China |

| ● | changes in general economic conditions and conditions adversely affecting the businesses in which Future FinTech is engaged; |

| ● | changes in U.S., China and global financial and equity markets, including market disruptions and significant interest rate fluctuations, which may impede our access to, or increase the cost of, external financing for our operations and investments; |

| ● | our success in implementing our business strategy or introducing new products and services; |

| ● | our ability to attract and retain customers; |

| ● | changes in tastes and preferences for, or the consumption of, our products and services; |

| ● | impact of competitive activities on our business; |

| ● | the result of future financing efforts; |

| ● | risks associated with the adverse effects of COVID-19 pandemic globally; |

| ● | risks associated with conducting business internationally and especially in the People’s Republic of China (“PRC”, or “China”), including currency fluctuations and devaluation, currency restrictions, local laws and restrictions and possible social, political and economic instability; and |

| ● | change of laws and regulations of blockchain technology and its application to business; |

| ● | other economic, financial and regulatory factors beyond the Company’s control. |

Any or all of our forward-looking statements in this report may turn out to be inaccurate. They can be affected by inaccurate assumptions we might make or by known or unknown risks or uncertainties. Consequently, no forward-looking statement can be guaranteed. Actual future results may vary materially as a result of various factors, including, without limitation, the risks outlined under “Item 1A. Risk Factors” in this Annual Report. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this filing will in fact occur. You should not place undue reliance on these forward-looking statements.

We undertake no obligation to update forward-looking statements to reflect subsequent events, changed circumstances or the occurrence of unanticipated events except as required by law.

ii

Overview

Future FinTech is a holding company incorporated under the laws of the State of Florida. The Company historically engaged in the production and sale of fruit juice concentrates (including fruit purees and fruit juices), fruit beverages (including fruit juice beverages and fruit cider beverages) in the Peoples Republic of China (“PRC”). Due to drastically increased production costs and tightened environmental laws in China, the Company has been transforming its business from fruit juice manufacturing and distribution to a real-name blockchain e-commerce platform that integrates blockchain and internet technology. The main business of the Company includes a shopping platform, Chain Cloud Mall (CCM), which is based on blockchain technology; a cross-border e-commerce platform (NONOGIRL) which is online and has started its trial operation in March 2020 and is expected for a formal launch in the third quarter of 2020; a blockchain-based application incubator and a digital payment system (DCON); and the application and development of blockchain-based e-commerce technology and financial technology.

Chain Cloud Mall adopts a “multi-vendor hosted stores + platform self-hosted stores” model. The platform supports various marketing methods, including point rewards programs, coupons, live webcasts, game interaction, and social media sharing. Besides the blockchain-powered features, CCM is also fully equipped with the same functions and services that other Chinese leading traditional e-commerce platforms provide.

Based on blockchain technology, CCM is established to transform the relationship between companies and consumers from traditional selling and buying relationships to a value-sharing relationship. The platform will fairly distribute the benefit of the entire mall to users who engaged in the promotion, development, and consumption based on their contributions to the platform. The members of CCM are not only consumers and entrepreneurs but also participants, promoters and beneficiaries. The CCM shared shopping mall platform is designed to be a block-chain based shopping mall for merchants and goods, not the exchange of digital currencies, and it currently only accepts payment from credit cards, Alipay and Wechat.

Chain Cloud Mall is an enterprise customer interactive and comprehensive shopping and sales service platform. It is an open network promotion system with a blockchain based anti-counterfeit system including point issuance, point referral and discount points settlement. The brand-new business model creates a completely new source of data traffic for enterprises.

Merchants in the Chain Cloud Mall issue their own blockchain points and anti-counterfeiting QR codes. Every product comes with unique anti-counterfeiting QR codes. Customers collect the points of the enterprise by scanning products for anti-counterfeiting check with their mobile phones. The successful collection of the merchant points confirms that the authentication of product from such enterprise. It also enables the Chain Cloud Mall to record and provide Chain Cloud Mall points to its members upon a successful new member and/or product referral, which can be used as credit when making purchases on CCM. It incentivize its members to promote the platform and share the products with their social contacts, which in turn increases the sales through Chain Cloud Mall and helps the Company generate greater value.

The Company has three direct wholly-owned subsidiaries: SkyPeople Foods Holding Limited (“SkyPeople BVI”), a company organized under the laws of the British Virgin Islands, DigiPay FinTech Limited (“DigiPay,”) formerly known as Belkin Foods Holdings Group Limited, which changed its name on January 4, 2018), a company incorporated under the laws of the British Virgin Islands, and Digital Online Marketing Limited (“Digital Online”) (formerly known as FullMart Holding Limited, which changed its name on January 5, 2018), a company organized under the laws of the British Virgin Islands. In September 2017, all of Digital Online’s operations were transferred to a subsidiary of SkyPeople BVI, and Digital Online has no operational assets or businesses.

1

SkyPeople BVI holds 100% of the equity interest of HeDeTang Holdings (HK) Ltd. (“HeDeTang HK”), a company organized under the laws of the Hong Kong Special Administrative Region of the People’s Republic of China (“Hong Kong”), and HeDeTang HK holds 73.42% of the equity interest of SkyPeople Juice Group Co., Ltd., (“SkyPeople (China)”), a company incorporated under the laws of the PRC. SkyPeople (China) has eleven subsidiaries in the PRC, which are mainly involved in the production and sales of fruit juice concentrates, fruit juice beverages and other fruit-related products in the PRC and overseas markets. On February 27, 2020, SkyPeople BVI (the “Seller”) completed the transfer of its ownership of HeDeTang HK to New Continent International Co., Ltd. (the “Buyer”), an unrelated third party and a company incorporated in the British Virgin Islands for a total price of RMB 0.6 million (approximately $85,714), pursuant to a Share Transfer Agreement entered into by the Seller and the Buyer on September 18, 2019 and approved at the special shareholders meeting of the Company on February 26, 2020.

DigiPay holds 100% of the equity interest of Future FinTech (HongKong) Limited (“FinTech HK”), a company organized under the laws of Hong Kong. FinTech HK holds 100% of the equity interest of Hedetang Foods (China) Ltd. (“Hedetang Foods (China)”) which changed its name to China Agricultural Silkroad Finance Lease Ltd. (“Finance Lease”) on May 24, 2018. Finance Lease transferred two of its subsidiaries to Chain Cloud Mall Network and Technology (Tianjin) Co., Limited (“CCM Network” or “CCM Tianjin”), namely, Hedetang Farm Products Trading Market (Mei County) Co., Ltd and China Agricultural Silk Road Trading Center, which changed its name to Chain Cloud Mall Logistics Center (Shaanxi) Co., Limited (“CCM Logistics”) on April 17, 2019. CCM Network holds 90% of the equity interest of Hedetang Farm Products Trading Market (Mei County) Co., Ltd. (“Trading Market Mei County”), a company incorporated under the laws of the PRC. Chain Cloud Mall Logistics Center (Shaanxi) Co., Limited (“CCM Logistics”) holds the remaining 10% of the equity interest of Trading Market Mei County. Finance Lease also holds 80% of the equity interest of CCM Logistics. Finance Lease holds 55% of the equity interest of Zhonglian Hengxin Assets Management Co., Ltd. (“Zhonglian Hengxin”). CCM Logistics holds 100% of the equity interest of GlobalKey Supply Chain Limited (GlobalKey Supply Chain). CCM Logistics is located in the national kiwifruit Industrial Park of Baoji City. It provides kiwifruit distributors and farmers an integrated supply chain solution through its distribution network, including transportation, after-sale service and other customer services.

On July 31, 2019, Chain Cloud Mall Network and Technology (Tianjin) Co., Ltd., Chain Cloud Mall E-commerce (Tianjin) Co., Ltd., a limited liability company incorporated under the laws of the China (the “E-commerce Tianjin”), and Mr. Zeyao Xue and Mr. Kai Xu, citizens of China and shareholders of E-commerce Tianjin, entered into the following agreements, or collectively, the “Variable Interest Entity Agreements” or “VIE Agreements,” pursuant to which CCM Network has contractual rights to control and operate the business of E-commerce Tianjin (the “VIE”).

Pursuant to Chinese law and regulations, a foreign owned enterprise cannot apply for and hold a license for operation of certain e-commerce businesses, the category of business which the Company plans to expand in China. CCM Network is an indirectly wholly foreign owned enterprise of the Company. In order to comply with Chinese law and regulations, CCM Network agreed to provide E-commerce Tianjin an Exclusive Operation and Use Rights Authorization to operate and use the Chain Cloud Mall System owned by CCM Network.

The following is a summary of the currently effective contractual arrangements relating to E-commerce Tianjin.

Contractual Arrangements with Our Consolidated Affiliated Entity and Its Respective Shareholders

Our contractual arrangements with our VIE and their respective shareholders allow us to (i) exercise effective control over our VIE, (ii) receive substantially all of the economic benefits of our VIE, and (iii) have an exclusive option to purchase all or part of the equity interests in our VIE when and to the extent permitted by PRC law.

As a result of our direct ownership in our WFOE and the contractual arrangements with our VIE, we are regarded as the primary beneficiary of our VIE, and we treat them and their subsidiaries as our consolidated affiliated entities under U.S. GAAP. We have consolidated the financial results of our VIE in our consolidated financial statements in accordance with U.S. GAAP.

2

Agreements that Provide us with Effective Control over our VIE

Exclusive Purchase Option Agreement.

Pursuant to the Exclusive Purchase Option Agreement, Mr. Zeyao Xue and Mr. Kai Xu granted to CCM Network and any party designated by CCM Network the exclusive right to purchase, at any time during the term of this agreement, all or part of the equity interests in E-commerce Tianjin, or the “Equity Interests,” at a purchase price equal to the registered capital paid by Mr. Zeyao Xue and Mr. Kai Xu for the Equity Interests, or, in the event that applicable law requires an appraisal of the Equity Interests, the lowest price permitted under applicable law. Pursuant to powers of attorney executed by Mr. Zeyao Xue and Mr. Kai Xu, they irrevocably authorized any person appointed by CCM Network to exercise all shareholder rights, including but not limited to voting on their behalf on all matters requiring approval of E-commerce Tianjin’s shareholder, disposing of all or part of the shareholder’s equity interest in E-commerce Tianjin, and electing, appointing or removing directors and executive officers. The person designated by CCM Network is entitled to dispose of dividends and profits on the equity interest without reliance on any oral or written instructions of Mr. Zeyao Xue and Mr. Kai Xu. The powers of attorney will remain in force for so long as Mr. Zeyao Xue and Mr. Kai Xu remain the shareholders of E-commerce Tianjin. Mr. Zeyao Xue and Mr. Kai Xu have waived all the rights which have been authorized to CCM Network’s designated person under the powers of attorney.

Equity Pledge Agreement.

Pursuant to the Equity Pledge Agreements, Mr. Zeyao Xue and Mr. Kai Xu pledged all of the Equity Interests to CCM Tianjin to secure the full and complete performance of the obligations and liabilities on the part of E-commerce Tianjin and them under this and the above contractual arrangements. If E-commerce Tianjin, Mr. Zeyao Xue, or Mr. Kai Xu breaches their contractual obligations under these agreements, then CCM Tianjin, as pledgee, will have the right to dispose of the pledged equity interests. Mr. Zeyao Xue and Mr. Kai Xu agree that, during the term of the Equity Pledge Agreements, they will not dispose of the pledged equity interests or create or allow any encumbrance on the pledged equity interests, and they also agree that CCM Tianjin’s rights relating to the equity pledge should not be interfered with or impaired by the legal actions of the shareholders of E-commerce Tianjin, their successors or designees. During the term of the equity pledge, CCM Tianjin has the right to receive all of the dividends and profits distributed on the pledged equity. The Equity Pledge Agreements will terminate on the second anniversary of the date when E-commerce Tianjin, Mr. Zeyao Xue and Mr. Kai Xu have completed all their obligations under the contractual agreements described above.

Agreements that Allow us to Receive Economic Benefits from our VIE

Exclusive Technology Consulting and Service Agreement.

Pursuant to the Exclusive Technology Consulting and Service Agreement, CCM Tianjin agreed to act as the exclusive consultant of E-commerce Tianjin and provide technology consulting and services to E-commerce Tianjin. In exchange, E-commerce Tianjin agreed to pay CCM Tianjin a technology consulting and service fee, the amount of which is to be equivalent to the amount of net profit before tax of E-commerce Tianjin, payable on a quarterly basis after making up losses of previous years (if necessary) and deducting necessary costs, expenses and taxes related to the business operations of E-commerce Tianjin. Without the prior written consent of CCM Tianjin, E-commerce Tianjin may not accept the same or similar technology consulting and services provided by any third party during the term of the agreement. All the benefits and interests generated from the agreement, including but not limited to intellectual property rights, know-how and trade secrets, will be CCM Tianjin’s sole and exclusive property. This agreement has a term of 10 years and may be extended unilaterally by CCM Tianjin with CCM Tianjin’s written confirmation prior to the expiration date. E-commerce Tianjin cannot terminate the agreement early unless CCM Tianjin commits fraud, gross negligence or illegal acts, or becomes bankrupt or winds up.

Agreements that Provide us with the Option to Purchase the Equity Interests in and Assets of our VIE

See Exclusive Purchase Option Agreement above

Spousal Consent Letters. The spouse of Mr. Kai Xu (Mr. Zeyao Xue is not married) of Chain Cloud Mall E-commerce (Tianjin) Co., Ltd. has signed a spousal consent letter agreeing that the equity interests in Chain Cloud Mall E-commerce (Tianjin) Co., Ltd. held by and registered under the name of the shareholder will be disposed pursuant to the contractual agreements with our WFOE. The spouse agreed not to assert any rights over the equity interest in Chain Cloud Mall E-commerce (Tianjin) Co., Ltd. held by the shareholder.

Through its subsidiaries, DigiPay is mainly involved blockchain based E-commerce platform and related business.

3

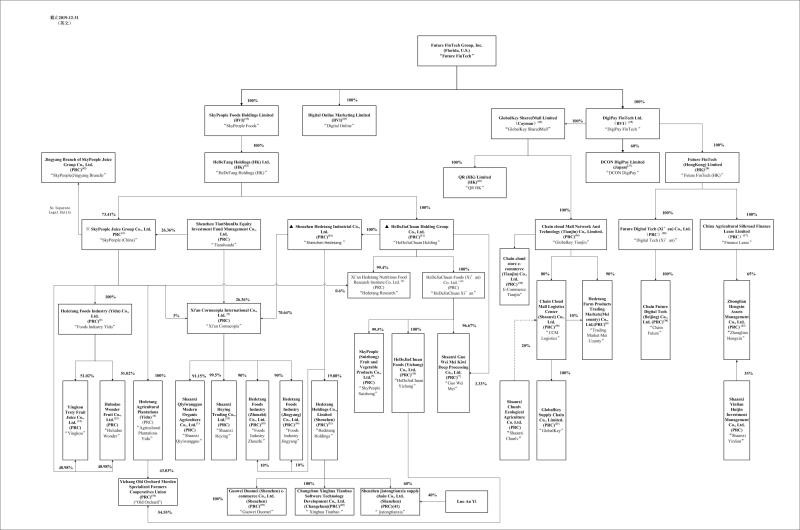

Organizational Structure

The following diagram illustrates our corporate structure, including our principal subsidiaries and our VIE as of the December 31, 2019.

|

Contractual Arrangements |

|

Equity Interest |

4

| (1) | Xi’an Qinmei Food Co., Ltd., an entity not affiliated with the Company, owns the remaining 8.85% of the equity interest in Shaanxi Qiyiwangguo Modern Organic Agriculture Co., Ltd. (“Shaanxi Qiyiwangguo”). (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (2) | SkyPeople Juice Group Co., Ltd., formerly known as Shaanxi Tianren Organic Food Co. Ltd. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (3) | Hedetang Foods Industry (Yidu) Co., Ltd. (“Foods Industry Yidu”), formerly known as SkyPeople Juice Group Yidu Orange Products Co., Ltd., was established on March 13, 2012. Its scope of business includes deep processing and sales of oranges. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (4) | Hedetang Agricultural Plantations (Yidu) Co., Ltd., formerly known as Hedetang Fruit Juice Beverages (Yidu) Co., Ltd., was established on March 13, 2012. Its scope of business includes the planting, acquisition and sales of vegetables, fruits, flowers, farm products; fresh fruit picking; research, training and promotion of planting and breeding technology. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (5) | SkyPeople (Suizhong) Fruit and Vegetable Products Co., Ltd. was established on April 26, 2012. Its scope of business includes the initial processing, quick-freezing and sales of agricultural products and related by-products. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (6) | Hedetang Farm Products Trading Market (Mei County) Co., Ltd., formerly known as SkyPeople Juice Group (Mei County) Kiwi Fruit and Farm Products Trading Market Co., Ltd. (“Kiwi Fruit & Farm Products”) was established on April 19, 2013. Its scope of business includes preliminary processing of agricultural and subsidiary products, establishment of trading markets for agriculture products, and similar activities. |

| (7) | Shaanxi Guo Wei Mei Kiwi Deep Processing Co., Ltd. was established on April 19, 2013. Its scope of business includes producing kiwi fruit juice, kiwi puree, cider beverages, and similar products. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (8) | Xi’an Hedetang Fruit Juice Beverages Co., Ltd. (“Xi’an Hedetang”) was established on March 31, 2014. Its scope of business includes the production and sales of fruit juice beverages. On August 10, 2017, it changed its name to Xi’an Hedetang Nutritious Food Research Institute Co., Ltd. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (9) | Xi’an Cornucopia International Co., Ltd. (“Cornucopia”) was established on July 2, 2014. Its scope of business includes the retail and wholesale of pre-packaged food. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

5

| (10) | Shaanxi Fruitee Fun Co., Ltd. (“Fruitee Fun”) was established on July 3, 2014. Its scope of business includes retail and wholesale of pre-packaged food. Shaanxi Fruitee Fun Co., Ltd. (also known as Shaanxi Guoweiduomei Beverage Co., Limited) changed its name to Hedetang Foods Industry (Xi’an) Co., Ltd. (“Foods Industry Xi’an”) on July 5, 2016. On June 6, 2017, it again changed its name to HedeJiachuan Foods (Xi’an) Co. Ltd. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (11) | Hedetang Holding Group Co., Ltd., formerly known as Hedetang Holding Co., Ltd., (“Hedetang Holding”) was established on July 21, 2014. Its scope of business includes corporate investment consulting, corporate management consulting, corporate image design and corporate marketing planning. On June 14, 2017, it changed its name to HedeJiachuan Holding Group Co. Ltd. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (12) | The Company acquired Huludao Wonder Co. Ltd. (“Huludao”) on September 10, 2008. Its scope of business mainly includes the manufacture and sale of concentrated fruit juice and fruit juice beverages. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (13) | The Company acquired Yingkou Trusty Fruits Co., Ltd. (“Yingkou”) on November 25, 2009. Its scope of business mainly includes the manufacture of concentrated fruit juice. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (14) | Hedetang Foods Industry (Jingyang) Co., Ltd. (“Foods Industry Jingyang”) was established on September 7, 2016. Its scope of business includes processing, storage and sales of farm products, fruits, tea and snacks; as well as research and promotion of processing technology of organic agriculture, fruit industry and agricultural products. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (15) | HedeJiachuan Foods (Yichang) Co. Ltd (“Hedejiachuan Yichang”), formerly known as Hedetang Farm Products Trading Market (Yidu) Co., Ltd., and Hedetang Foods Industry (Yichang) Co., Ltd, was established on March 23, 2016. Its scope of business includes construction, operation, and property management of a farm products trading market; e-commerce services for farm products; and construction and operation management of an e-commerce information platform. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (16) | Yichang Old Orchard Morden Specialized Farmers Cooperatives Union (“Old Orchard”) was established on April 8, 2016. Its main business scope is the purchase, sales, trading and reprocessing of farm products, development of products for the union, introducing new technology and new plants, and technology training for union members. Old Orchard dissolved in 2020 and canceled its registration with the State Administration for Industry and Commerce of the People’s Republic of China (the “SAIC”) on April 7, 2020. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (17) | The Company acquired Hedetang Foods (China) Co., Ltd. (“Hedetang Foods China”) on May 18, 2016 through the acquisition of DigiPay FinTech Limited (formerly known as Belking Foods Holdings Group Co., Ltd.), the 100% indirect shareholder of Hedetang Foods China, on the same date. It changed its name to China Agricultural Silkroad Finance Lease Ltd. on May 24, 2018. The scope of business of China Agricultural Silkroad Finance Lease Ltd. includes consulting services for corporate bankruptcy and liquidation, mergers and acquisitions, assets restructuring, corporate listing and disposal services of non-performing assets. |

6

| (18) | Hedetang Agricultural Plantations (Mei County) Co., Ltd. was established on September 2, 2016. Its scope of business includes the planting, acquisition and sales of vegetables, fruits, flowers, Chinese herbal medicine, and farm products; fresh fruit picking; research, training and promotion of planting and breeding technology, development and training for E-commerce and online sales of agricultural and sideline products. On September 6, 2017, it changed its name to Shaanxi China Agricultural Silk Road Farm Products Trading Center Co., Ltd. On April 17, 2019, it changed its name to Chain Cloud Mall Logistics Center. |

| (19) | Hedetang Foods Industry (Zhouzhi) Co., Ltd. (“Foods Industry Zhouzhi”) was established on November 29, 2016. Its scope of business includes production, processing and sales of kiwifruit wine, juice, puree and beverages; storage and sales of fresh fruits; and import and export of a variety of products and technology. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (20) | Future FinTech (HongKong) Limited (“FinTech HK”), formerly known as Future World Trading (Hong Kong) and SkyPeople International Trading (HK) Limited, was first established on July 27, 2016. It mainly engages in the import and export of food products. |

| (21) | GlobalKey Supply Chain Limited, formerly known as Shaanxi Quangoutong E-commerce Inc., was acquired on May 27, 2017. Its main business scope includes computer hardware and software development and sales, electronic products and communication equipment, computer network engineering design, business information consultation, online sales and online marketing, and investment management. |

| (22) | Shaanxi Heying Trading Co. Ltd was established on December 17, 2009. Its main business scope includes the sales of pre-packaged food and bulk food; import and export of goods and technology; food technology research and development; business management and consulting; and corporate planning services. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (23) | Zhonglian Hengxin Assets Management Co., Ltd. (“Zhonglian Hengxin”) was established in Xi’an in 2017. Its main business scope includes asset management (except for financial, securities, futures and other restricted items); asset acquisition, asset disposal and asset operation (except for financial, securities, futures and other restricted items); planning and advisory services for corporate restructures and mergers and acquisitions; equity and real estate investment (no public offerings, restricted to investment through assets of the company itself); financial business process outsourcing entrusted by financial institutions; financial information technology outsourcing entrusted by financial institutions; and financial knowledge process outsourcing. Any such businesses that require approval by government agencies shall only operate within the scope of such approval. |

| (24) | Shenzhen Hedetang Industrial Co., Ltd. (“Shenzhen Hedetang”) was established on September 29, 2017. Its main business scope includes industrial projects (specific items to be declared separately); domestic trade; and import and export businesses. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (25) | DigiPay FinTech Limited (“DigiPay FinTech”), formerly known as Belking Foods Holdings Group Co., Ltd., was established on May 3, 2016. |

| (26) | QR (HK) Limiter (“QR HK”), formerly known as GlobalKey Holdings Limited, was established on January 13, 2012 and its name was changed on October 23, 2018. It was established mainly to engage in product import and export. |

| (27) | DCON DigiPay Limited (“DCON DigiPay”) was established on February 5, 2018 in Tokyo, Japan. Its main business scope includes the development and marketing of a blockchain based payment system, computer software, asset management consulting, and business consulting. |

7

| (28) | Future Digital FinTech (Xi’an) Co., Ltd. (“FinTech (Xi’an)”) was established on February 9, 2018 in Xi’an. Its main business scope includes software development and marketing, information consulting services, and financial information technology development. |

| (29) | GlobalKey SharedMall Limited (“GlobalKey SharedMall”) was established on March 6, 2018 in the Cayman Islands. Its main business scope includes an online trading and shopping platform for fresh fruits, juices and other products and services, using blockchain technology. |

| (30) | Chain Future Digital Tech (Beijing) Co., Ltd, (“Chain Future”) was established on July 10, 2018. Its main business scope includes technical services and technology transfer, development, promotion and consultation; wholesale of computers, software and auxiliary equipment, electronic products, and other related products. This company focuses its business on acting as an accelerator for blockchain projects and it provides basic support including technical support, whitepaper editing, solution design and financial management services for its clients. Its business also includes training and cultivating technicians for blockchain projects, providing consultation services regarding cryptocurrency exchanges and tokens listing matters, as well as marketing-related services. |

| (31) | Chain Future Digital Tech (Tianjin) Co., Ltd, (“Chain Future Tianjin”) was established on November 12, 2018. Its main business scope includes digital technology development, technology transfer, technical consultation and technical services; services in business incubation; development and sales of software technology; computer system integration services; company management consulting; financial information consulting; technology services on computer system, basic software, application software; exhibition services; meeting services; and advertisement business. Its business also includes training and cultivating technicians for blockchain projects, providing consultation services regarding cryptocurrency exchanges and tokens listing matters, as well as marketing-related services. Chain Future Tianjin dissolved in 2019 and canceled its registration with State Administration for Market Regulation (SAMR and formerly known as SAIC) on November 4, 2019. |

| (32) | The Company acquired 19.88% shares of Hedetang Holdings (Shenzhen) Co., Limited which is an NEEQ listed company, through Shenzhen Hedetang Industrial Co., Ltd on March 26, 2018. The business scope of Hedetang Holdings (Shenzhen) Limited is information consultation (excluding restricted projects and talent intermediary services); import and export business (except for the items prohibited by law, administrative regulations and the state council, which restricted items can only be operated after obtaining permission); venture capital business; business information consulting, financial, investment and enterprise management consulting (the above items do not include restricted items); research and development of prepackaged food and health food; pre-packaged food, health food production and sales; and information service business (internet information service business only). (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 26, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

According to USGAAP Code No. 810-10-15-8, for legal entities other than limited partnerships, the usual condition for a controlling financial interest is ownership of a majority voting interest, and, therefore, as a general rule, ownership by one reporting entity, directly or indirectly, of more than 50 percent of the outstanding voting shares of another entity is a condition pointing toward consolidation. The power to control may also exist with a lesser percentage of ownership, for example, by contract, lease, agreement with other stockholders, or by court decree.

As all the board members, General Manager and Financial Controller of Hedetang Holdings (Shenzhen) Co., Limited are appointed by the Company, Hedetang Holdings (Shenzhen) Co., Limited. is consolidated into the Company’s financial statements.

| (33) | SkyPeople Foods Holdings Limited, established in British Virgin Island in 2011. Its main business scope includes trading, import and export of food products. |

| (34) | HeDeTang Holdings (HK) Ltd. incorporated in Hong Kong, China in 2007. Its main business scope includes the research and development of food packages, food production techniques; the research and development of technology consultation and transfer. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

8

| (35) | Digital Online Marketing Limited was established in British Virgin Island in 2011. Its main business scope includes trading consultancy, corporation management, software development and marketing, and information consulting services. |

| (36) | GlobalKey Network Technology (Tianjin) Co., Ltd. which was changed to Chain Cloud Mall (CCM) Network and Technology (Tianjin) Co., Ltd. (“CCM Tianjin”), was established in January 2019. Its main business scope includes blockchain technology development, service, consultation and transfer; encryption technology; digital integral system technology; and e-commerce platform technology development. |

| (37) | GloblalKey Network and Technology (Beijing) Co., Ltd was established on March 20, 2018. Its main business scope is technology service, development, consultation, transfer and technology popularization; technology import and export, serving as agent for import and export, and import and export of goods. GloblalKey Network and Technology (Beijing) Co., Ltd dissolved in 2019 and canceled its registration with the SAMR on November 20, 2019. |

| (38) | Chain Cloud Mall E-commerce (Tianjin) Co., Ltd. (“E-commerce”) was established on April 4, 2019 by Mr. Zeyao Xue and Kai Xu and is a variable interest entity (“VIE”) of the Company. Its main business scope is sale of products through e-commerce. Mr. Zeyao Xue is a major shareholder of the Company and the son of Mr. Yongke Xue, our Chairman. Mr. Kai Xu is the Chief Operating Officer of the Company. |

| (39) | Guowei Duomei (Shenzhen) E-commerce Co., Ltd. was established on August 20, 2018. Its main business scope is the sale of health foods, local products, pre-packaged foods, agricultural and agricultural by-products, bulk foods and online sales. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (40) | Changchun Xinghua Tianbao Software Technology Development Co., Ltd. was established on August 7, 2018. Its main business scope is software development, technology transfer and software information consultation. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (41) | Shenzhen Jiatong Tianxia Supply Chain Co., Ltd. was established on March 19, 2018. Its main business scope is trading, import and export, supply chain management and the related support services, whole selling and retailing of pre-packaged foods, sale of dairy products (including infant formula milk powder), beverages, and health products. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

| (42) | Jiangyang Branch of Sky People Juice Group Co. Ltd. was established on September 26, 2016. Its main business scope is the production of beverages (fruit and vegetable juices, solid beverages and other beverages), the storage and sale of fresh fruit and vegetables, organic agriculture, research into the processing technology of the fruit industry, research on high grade production and technical services, processing and the sale of packaging products. (The ownership was transferred as a subsidiary of HeDeTang Holdings (HK) Ltd. to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang Holdings (HK) Ltd. and New Continent International Co., Ltd. on September 18, 2019) |

9

Certain Highlights For the Fiscal Year ended December 31, 2019

In January 2019, the Company established Chain Cloud Mall Network and Technology (Tianjin) Co., Ltd., (“CCM Tianjin”),formerly known as GlobalKey Network Technology (Tianjin) Co., Ltd.). Its main business scope includes blockchain technology development, service, consultation and transfer; Encryption technology, digital integral system technology, e-commerce platform technology development, etc.

On January 22, 2019, CCM Tianjin formally launched Chain Cloud Mall (CCM) v1.0, the real-name and membership-based blockchain shared shopping mall platform that integrates blockchain and internet technology and distinguishes itself by utilizing the automatic value distribution system of blockchain and sharing the value of the platform to all the participants in the system.

On June 1, 2019, CCM Tianjin formally launched CCM v2.0. Compared to the 1.0 version, CCM v2.0 has a wider variety of product categories, easier user interface, more transparent information, more stable operations, a higher security level, and faster logistics. The CCM v2.0 adopts a “multi-vendor hosted stores + platform self-hosted stores” model. The platform supports various marketing methods, including point rewards programs, coupons, live webcasts, game interaction, and social media sharing. Besides the blockchain-powered features, CCM v2.0 is also fully equipped with the same functions and services that other Chinese leading traditional e-commerce platforms provide.

On July 30, 2019, the Company announced E-commerce Tianjin adopted the QRO anti-counterfeiting code to all products under the Company’s Hedetang brand. By adopting the QRO anti-counterfeit code technology, each Hedetang product will be issued an unalterable anti-counterfeit code that records every event or transaction on a distributed ledger, which makes the whole process from manufacturing to delivering traceable. On August 2, 2019, the Company announced the adoption of the QRO anti-counterfeit code technology for the entire CCM Mall platform.

On July 31, 2019, CCM Tianjin, E-commerce Tianjin, and Mr. Zeyao Xue and Mr. Kai Xu, citizens of China and shareholders of E-commerce Tianjin, entered into the “Variable Interest Entity Agreements” or “VIE Agreements,” pursuant to which CCM Tianjin has contractual rights to control and operate the business of E-commerce Tianjin (the “VIE”).

On September 18, 2019, SkyPeople BVI, entered into a Share Transfer Agreement (the “Agreement”) with New Continent International Co., Ltd., a company incorporated in the British Virgin Islands (the “Buyer”). Pursuant to the terms of the Agreement, SkyPeople BVI will sell all of the issued and outstanding shares of HeDeTang HK, a wholly owned subsidiary of SkyPeople BVI, to the Buyer for a total of RMB 600,000, or approximately US$85,714. The above-mentioned share transfer was approved by the Company’s shareholders on February 27, 2020. On February 27, 2020, SkyPeople BVI completed the transfer of its ownership of HeDeTang HK to the Buyer.

On November 8, 2019, GlobalKey SharedMall entered into a Three-Party Cooperation Agreement (the “Agreement”) with Fan Zhang, a citizen of China, and Caixia Wang, a citizen of China. Pursuant to the Agreement, the three parties agreed to make cash contributions totaling RMB 1,000,000 (approximately $142,857) to QR(HK) Limited (“QR HK”), a wholly owned subsidiary of GlobalKey SharedMall. Of this total, GlobalKey SharedMall shall contribute RMB 510,000 (approximately $72,857); Fan Zhang shall contribute RMB 300,000 (approximately $42,857); and Caixia Wang shall contribute RMB 190,000 (approximately $27,143). GlobalKey SharedMall agreed to loan Fan Zhang RMB 300,000 for his cash contribution obligation, which shall be repaid from dividends of QR HK in the future. If QR HK is terminated by the parties before the loan is paid off from the dividends or by liquidation of Fan Zhang’s ownership of QR HK, Fan Zhang shall repay the loan to GlobalKey SharedMall in two years. Fan Zhang shall be responsible for the operations and daily management of QR HK’s cross-border e-commerce platform NONOGIRL and shall be paid RMB 12,000 (approximately $1,714) per month. GlobalKey SharedMall is responsible for accounting, supervision of Fan Zhang’s management, and auditing the financials of QR HK, and additionally has the right to veto material business decisions of QR HK.

On November 18, 2019, E-Commerce Tianjin entered a cooperation agreement with Chifeng Supply and Marketing E-commerce Co., Ltd. to develop a blockchain contract farming platform focusing on sheep farming.

10

Company strategy and Principal Products and Services

Our core business historically has been in the production and sale of fruit juice concentrates (including fruit purees and fruit juices), fruit beverages (including fruit juice beverages and fruit cider beverages) in the PRC and internationally. Revenue from the sale of fruit juice concentrates and fruit beverages accounted for 18% and 72% of our total revenue for fiscal years 2019 and 2018 respectively. Due to drastically increased production cost and tightened environmental laws in China, the Company has transformed its main business from fruit juice manufacturing and distribution to a real-name blockchain e-commerce platform that integrates blockchain and internet technology in fiscal year 2019. The e-commerce platform contributed 96.4% and 0% to the total revenue for fiscal 2019 and 2018 respectively.

On February 27, 2020, the Company completed the transfer of its ownership of HeDeTang HK to New Continent International Co., Ltd. (the “Buyer”), a company incorporated in the British Virgin Islands, pursuant to a Share Transfer Agreement (the “Agreement”) entered on September 18, 2019. Pursuant to the terms of the Agreement, the Buyer purchased 100% ownership of HeDeTang HK. (the “Sale Transaction”)

Following the completion of the Sale Transaction, the main business operations of the Company are focused on our real-name and membership-based blockchain shared shopping mall platform and cross-border e-commerce platform NONO Girl to be formally launched in 2020.

As the Company sold its juice related segment, the financial position and operating results of HeDeTang HK have been classified as discontinued operations within the accompanying consolidated financial statements of the Company.

Shared Shopping Mall

The Company has transformed its business from fruit juice manufacturing and distribution to a real-name and membership-based blockchain e-commerce platform that integrates blockchain and internet technology. On March 6, 2018, the Company established GlobalKey SharedMall Limited in the Cayman Islands to operating its global business service center based on blockchain technology.

The trial operation of GlobalKey ShareMall, also known as Chain Cloud Mall (CCM) started on December 26, 2018. On January 22, 2019, the Company formally launched Chain Cloud Mall, the real-name and membership-based blockchain shared shopping mall platform that integrates blockchain and internet technology and distinguishes itself by utilizing the automatic value distribution system of blockchain and sharing the value of the platform to all the participants in the system.

On June 1, 2019, CCM v2.0 was launched. Compared to the 1.0 version, CCM v2.0 has a wider variety of product categories, easier user interface, more transparent information, more stable operations, a higher security level, and faster logistics. Currently, CCM v2.0 adopts a “multi-vendor hosted stores + platform self-hosted stores” model. The platform supports various marketing methods, including point rewards programs, coupons, live webcasts, game interaction, and social media sharing. Besides the blockchain-powered features, CCM v2.0 is also fully equipped with the same functions and services that other Chinese leading traditional e-commerce platforms provide.

On August 2, 2019, CCM adopted the QRO anti-counterfeit code on the CCM. QRO code is a blockchain-powered unalterable Quick Response One (QRO) anti-counterfeit code issued by the manufacturer. It ensures the authenticity of products and directly links manufacturers with their targeted customers as a way of precision marketing. The system includes point issuance, point referral and discount points settlement. The brand-new business model creates a completely new source of data traffic for enterprises. Merchants in the Chain Cloud Mall issue their own blockchain points and anti-counterfeiting QR codes. Every product comes with unique anti-counterfeiting QR codes. Customers collect the points of the enterprise by scanning products for anti-counterfeiting check with their mobile phones. The successful collection of the merchant points confirms that the authentication of product from such enterprise.

On May 1, 2020, CCM v3.0 was launched. It creates a new value cycle system of online shopping mall with the real-name blockchain system. There are four major functions:

| 1. | Tracking reward points provided to its members. |

| 2. | Blockchain anti-counterfeiting system. |

| 3. | Member community system. |

| 4. | Points promotion system. |

11

The blockchain technology enables CCM to record every event or transaction on a distributed ledger and makes the whole process traceable. It also enables the CCM to record and provide CCM points to its members upon a successful new member and/or product referral, which can be used as credit when making purchases on CCM. It incentivizes its members to promote the platform and share the products with their social contacts, which in turn increases the sales through CCM.

Based on blockchain technology, CCM is established to transform the relationship between companies and consumers from a traditional selling and buying relationship to a value-sharing relationship. The platform will fairly distribute the benefits of the entire mall to users who engage in promotion, development, and consumption based on their contributions to the platform. The members of CCM are not only consumers and entrepreneurs but also participants, promoters and beneficiaries.

CCM has attracted a growing base of users, including members and non-members. These users are actively purchasing products on the platform. Members are the key participants on CCM and drivers of its growth. Our members typically pay to gain access to a dedicated app that provides access to a curated selection of products, exclusive membership benefits, and features, including discounted prices and point rewards. Members can refer others to become members and are rewarded for doing so. Members can also promote products on various social platforms and are rewarded if those users purchase our products.

Currently, there are three kinds of membership programs with different membership Fees. The members are required to log onto Chain Cloud Mall (CCM) app or web portal in order to download some of their rewarding points each day. The member could download all his/her rewarding points if he/she log onto the app or web portal for at least 200 days within the membership valid period which is 365 days. Members must renew their membership before expiration to continue earning points and enjoy the discounts. A non-member user can purchase products from the platform but does not enjoy the above mentioned benefits.

Membership benefits are as follows:

| 1) | Receive a merchandise gift package |

| 2) | Exclusive discounts for merchandise sold on the Chain Cloud Mall (CCM) Web and App |

| 3) | Receive CCM-Points upon a successful new member and product referral |

CCM-Points can be used as coupons for the member’s future purchases on our app and website.

Since the trial operations of CCM began on December 26, 2018, CCM had approximately 164 and 6,401 users as of December 31, 2018 and December 31, 2019, respectively.

We currently generate revenues primarily from fixed membership fees and selling products on our platform to users, including both members and non-members. Membership revenue is recognized when a member registers and makes his/her first order on CCM app or web portal.

For the year ended December 31, 2019, approximately $0.54 million was recognized for fixed membership fees revenue from 6,401 members and approximately $0.39 million for merchandise sales revenue from orders on the Company’s own sales platform, which in total account for 56.7% of our total revenue.

Fruit Juice Concentrates and Fruit Beverages

There are two general categories of fruit and vegetable juices available in the market. One is fresh juice that is canned directly upon filtering and sterilization after being squeezed out of fresh fruits or vegetables. The other general category is juice drinks made out of concentrated fruit and vegetable juices. Concentrated fruit and vegetable juices are produced through the pressing, filtering, sterilization and evaporation of fresh fruits or vegetables. Concentrated juices are not drinkable. Instead, they are used as a basic ingredient for manufacturing juice drinks and as an additive to fruit wine, fruit jam, cosmetics and medicines.

12

The core products for the juice business are (1) fruit juice concentrates, mainly including concentrated apple, pear, and kiwi juices; (2) fruit beverages, including pure fruit beverages and fruit cider beverages; and (3) other fruit-related products, including, for example, fresh fruits, vegetables and fructose.

Fruit Juice Concentrate

Our family of fruit juice concentrate products mainly includes concentrated apple, pear, and kiwi juices. Our concentrated kiwifruits are made of three different categories: kiwifruit puree, concentrated kiwifruit puree and concentrated kiwifruit juice. Kiwifruit puree is prepared from clean, sound kiwifruits that have been washed and sorted prior to processing. The kiwifruits are crushed and pressed and the pulp of the kiwifruit is kept. All of the water and some of the pulp are then removed from the kiwifruit puree and the sugar level is increased in order to produce concentrated kiwifruit puree. We use advanced technologies to maintain the natural flavors and nutrients of the kiwifruit puree. Kiwifruit puree and concentrated kiwifruit puree are ideal raw materials used in the production of concentrated kiwifruit juices, kiwifruit beverages, kiwifruit flavored ice creams, smoothies and health care products. Concentrated kiwifruit juice is made from concentrated kiwifruit puree by removing all of the remaining pulp. Concentrated apple juice and concentrated pear juice are prepared from fresh fruits during the “squeezing season” of a year, when fresh fruits are available in the market. Generally, the squeezing season for apples is from August through January or February of the following year, the squeezing season for pears is from July or August through April of the following year, and the squeezing season for kiwifruits is from September through December or January of the following year.

Our production line at the Shaanxi Qiyiwangguo factory can only produce puree and concentrated puree. We use the production line that produces concentrated apple and pear juice in the facility of the Jingyang branch of SkyPeople BVI to produce concentrated clear kiwifruit juice.

Fruit Juice Beverages

As compared to our fruit juice concentrate products, which experience seasonality, fruit juice beverages can be produced and sold year-round.

The manufacturing process for fruit juice beverages involves further processing of fruit juice concentrates. Our fruit juice beverages are divided into two categories: pure fruit juice and fruit cider beverages. Currently we produce five flavors of fruit beverages in 236 ml glass bottles, 258 ml glass bottles, 280 ml glass bottles, 418 ml glass and 500 ml glass bottles, 888 ml glass bottles, 1.21 L glass bottles and BIB (bag in box) packages, including kiwifruit juice, mulberry juice, peach juice, pomegranate juice and fruit and vegetable juice. We also produce two flavors of lactobacillus fruit beverages in 268 ml glass bottles, including lactobacillus kiwifruit juice and lactobacillus mulberry juice, as well as three beverages with rich dietary fiber in 330 ml glass bottles, including kumquat and grapefruit juice, kiwifruit juice and mulberry juice. Our products are sold through distributors in stores.

Competition and our Competitive Advantages

The e-commerce industry in China is intensely competitive. Our competitors include all major e-commerce companies in China, and other internet companies that engage in social e-commerce businesses.

We anticipate that the e-commerce industry will continually evolve and will continue to experience rapid technological change, evolving industry standards, shifting customer requirements, and frequent innovation. We must continually innovate to remain competitive.

We compete primarily on the basis of the following factors: (i) our ability to attract and retain a large number of members and other users and establish strong community bonding and maintain member loyalty through social interaction effectively; (ii) our shared shopping platform that enables users to buy products easily; (iii) strong fulfillment capabilities, including logistics and online payment, (iv) advanced technology infrastructure, and (v) reliable and flexible supply chain and strong manufacturing partner network.

13

We have a unique real-name and membership–based blockchain e-commerce shopping platform that integrates blockchain, internet technology and distinguishes itself by utilizing the automatic value distribution system of the blockchain and sharing the value of the platform to all the participants in the system. In addition to providing value and convenience to our members, we reward them for referring new members and promoting our products and helping to generate transactions. Based on blockchain technology, CCM is established to transform the relationship between companies and consumers from traditional selling and buying relationship to a value-sharing relationship. The platform will fairly distribute the benefit of the entire mall to users who engage in promotion, development, and consumption based on their contributions to the platform.

Our latest CCM v3.0 creates a new value cycle system of online shopping mall with the real-name blockchain system with following characteristics:

| 1. | Blockchain anti-counterfeiting |

Using real-name blockchain technology to carry out anti-counterfeiting for products produced by the enterprises. The essence of anti-counterfeiting is to determine the person responsible for the product. Using real-name blockchain system, it provides the assurance to our customers to the authentication of the products they purchase and solve the problem of counterfeiting products in online shopping mall.

| 2. | Blockchain points settlement leads to secondary data traffic |

Blockchain points are also discount coupons for enterprises, guiding customers to the platform of the enterprises, and provide them discounts when purchasing. This process is called secondary data traffic. Every company is aware of the importance of maintaining old customers. Blockchain anti-counterfeiting technology through scanning of QR codes by the customers helps companies identify such customers and allows them to systematically maintain contacts with such customers.

| 3. | Points promotion system |

Points promotion system brings secondary data traffic comes with volume and high turnover ratio. All such sales are directed to the enterprise platform when customers possess and use enterprise coupons. With a high level of user stickiness, customers are likely to purchase products again and collect more blockchain points.

| 4. | Member community system to build a high value community |

Anti-counterfeiting technology plus the Company’s secondary data traffic platform have created great value for the enterprises that have stores on our platform. By gathering all loyal customers to an enterprise platform, we can build a standard value community.With the same experiences and common interest, the value community of an enterprise can form a self-organizing system of customer groups to maximize the interests of such enterprise.

For our juice products, we believe that a number of companies are producing juice products that compete directly with our product offerings and some of our competitors have significantly more financial resources than we possess. Our apple juice concentrate competitors include Sdic Zhounglu Fruit Juice Co., Ltd., Yantai North Andre Juice Co., Ltd., Shaanxi Hengxing Fruit Juice and Shaanxi Haisheng Juice Holdings Co., Ltd. We also compete with fruit juice companies such as Wahaha, Huiyuan, Nongfu Guoyuan, Tongyi and Meizhiyuan. We believe our competitive advantages include the modern equipment and technology employed at our production factories in Shaanxi Province and the strategic locations of our manufacturing facilities. Our equipment and technology help us to improve product quality, control costs and allow us to meet international fruit juice production standards such as ISO9001, HACCP, and Kosher certifications, and those imposed by the United States Food and Drug Administration. In addition, our manufacturing facilities are strategically located near regional fruit production centers. For example, Shaanxi Province, where two of our manufacturing facilities are located, is known in the PRC for pear and kiwi production. Our proximity to regional fruit production centers enables us to purchase fresh fruits directly from farmers, avoid the need of transporting fresh fruit over long distances to processing facilities, reduce our transportation expenses and damage to fresh fruit during transportation, and helps us maintain a high quality of finished products by preserving freshness.

We believe that our management team, which includes Vincent Xue, our Chairman of Board of Directors, Shanchun Huang, Chief Executive Officer, Veronica Chen, our Chief Financial Officer, Yan Zhi, our Chief Technology Officer, and a seasoned team of senior managers with significant experience in the areas of operations, marketing, technology and finance, is one of the strongest management teams in e-commerce and blockchain technology and integrated fruit-related products industry.

14

Production Capacity

The following table sets forth our production capacity as of December 31, 2019.

| Subsidiary/branch | Location | Products | Production capacity | Notes | |||||

| Shaanxi Qiyiwangguo* | Zhouzhi county, Shaanxi province | Kiwi puree, concentrated kiwi puree and fruit beverages |

(1)

|

Sorting fresh fruits: 10 tons fresh fruits per hour; | Approximately 1.5 tons of fresh fruits are used to produce 1 ton of puree; 4 to 4.5 tons of fresh fruits are used to produce 1 ton of concentrated puree | ||||

| (2) | Puree/concentrated puree: processing 20 tons of fresh fruits per hour; | ||||||||

| (3) | Fruit beverages: producing 6,000 bottles per hour | ||||||||

| Jingyang branch of SkyPeople (China)* | Jingyang County, Xianyang City, Shaanxi Province |

Concentrated apple and pear juice, concentrated kiwifruit juice and fruit-related products | (1)

|

Concentrated apple/kiwi/pear juice: processing 40 tons of fresh fruits per hour; | All concentrated juice products are manufactured using the same type of production line with slight variations in processing methods | ||||

| (2) | Fructose: processing 10 tons of fresh fruits per hour | ||||||||

| Yingkou* | Gaotai Town, Gaizhou, Liaoning Province | Concentrated apple juice | (1) | Processing 20 tons of fresh fruits per hour | All concentrated juice products are manufactured using the same type of production line with slight variations in processing methods. | ||||

* All these are the subsidiaries of HeDeTang HK and were transferred along with the transfer of HeDeTang HK to New Continent International Co., Ltd. on February 27, 2020 pursuant to a Share Transfer Agreement entered into by HeDeTang HK and New Continent International Co., Ltd. on September 18, 2019.

15

Industry and Principal Markets

E-commerce Industry and Social e-commerce Platforms in China

According to digital data and research company eMarketer, China has the most mobile users in the world and more e-commerce activity than any other country in the world. In 2017, Chinese consumers spent more than $750 billion online – more than the UK and US combined. And in June 2019, retail e-commerce spend in China for 2019 was said to increase 27.3% to $1.935 trillion – making up 36.6% of total retail sales, according to digital data and research company eMarketer. eMarketer also forecast Chinese retail e-commerce sales to maintain its strong growth through the end of its forecast in 2023.

Blockchain Technology and Digital Economy Development

In 2016, the China State Council included blockchain technology as a new technology and started the promotion and development of blockchain technology and applications. Since then, the central and local governments have issued relevant supervision and support policies to support blockchain technology and industry development to enable commercialization. In April 2020, the Chinese Ministry of Industry and Information Technology (“MITT”) announced that it will strongly support technological innovation and industrial applications such as blockchain technology. Blockchain technology is now widely used by Chinese leading financial organizations and institutions. In early 2020, Alibaba announced its integration of a full-link traceability blockchain system into its importation e-commerce platform, Kaola.

2020 is a year of China-ASEAN digital economic cooperation. Leading high-quality development with a credible digital economy is becoming a new highlight in the development of cooperation between China and ASEAN countries. In the field of digital economy, China and ASEAN countries have a good foundation and environment of cooperation. We believe it is a good time to create application demonstration projects through the construction of digital infrastructure, support for 5G networks, the advancement of artificial intelligence, the initiation of innovative applications of blockchain and other emerging technologies.

At present, ASEAN countries hope to keep up with the development of the digital economy in order to start the digitalization of border markets, e-commerce, cross-border settlement, smart logistics, supply chain finance and traditional industries as soon as possible. As a basic and systematic technology and facility, the application of blockchain is expected to become an important force for future industrial revolution.

Market of Fruit Juice

Fruit juices in the Chinese market are mainly dominated by juice mixtures, smoothies & orange juice. The Chinese market of fruit and high pressure processing (HPP) vegetable juices is very competitive. Forecasts indicate likely coconut and other plant water booms; and demand for HPP juices is on the rise. According to website of www.China juice.net, revenue in the juice market amounted in China to US$4,639 million in 2019.

Marketing, Sales and Distribution

For our CCM shared shopping mall, we incentivize our members to recommend and market products through their own social networks and communities. Customers tend to find recommendations by influencers, including friends and families, who customers tend to deem trustworthy. Members who promote products are rewarded if other users purchase our products based on that promotion.

We market our juice products through two primary methods: attendance at international exhibitions and sales made through distributors and trade websites. Our marketing and sales teams work closely together to maintain a consistent message to our customers.

The sales team is divided into three subdivisions, focusing on the sales of fruit juice concentrates, fruit beverage products and derivative products including foods. We sell our products either indirectly through distributors with good credit histories or directly to end-users.

16

The Chinese market drives our fruit beverage sales, with most beverages sold through provincial, city and county-level agents.

Raw Materials and Other Supplies

Historically, fresh fruits, including apples, pears and kiwifruits were the primary raw materials for our juice related products. The continuous supply of high quality fresh fruit was necessary for the fruit juice related operations.