Filed Pursuant to Rule 424(b)(3)

Registration No. 333-266887

Prospectus Supplement No. 1 dated April 12, 2023

(To Prospectus dated October 19, 2022)

BITECH TECHNOLOGIES CORPORATION

141,954,924 Shares of Common Stock for Resale by Selling Stockholders

This Prospectus Supplement is being filed by Bitech Technologies Corporation, a Delaware corporation (the “Company,” “we,” “our”, “us”) to update and supplement the information contained in the Prospectus dated October 19, 2022 (the “Prospectus”) relating to the resale from time to time of up to an aggregate of 141,954,924 shares of our common stock, par value $0.001 per share (“common stock”) held by the selling stockholders named in the Prospectus or their permitted transferees (“Selling Stockholders”).

This Prospectus Supplement is being filed to update and supplement the information contained in the Prospectus, which forms a part of our registration statement on Form S-1 (File No. 333-266887) with the information contained in the following reports filed by the Company with the Securities and Exchange Commission on the dates indicated below (collectively, the “Reports”). Each of the respective Reports are attached hereto.

| Report | Date Filed | |

| Current Report on Form 8-K | April 10, 2023 | |

| Annual Report on Form 10-K for the fiscal year ended December 31, 2022 | March 31, 2023 | |

| Current Report on Form 8-K | February 24, 2023 | |

| Current Report on Form 8-K | February 17, 2023 | |

| Current Report on Form 8-K | February 3, 2023 | |

| Current Report on Form 8-K | December 21, 2022 | |

| Quarterly Report on Form 10-Q for the period ended September 30, 2022 | November 10, 2022 |

This Prospectus Supplement is not complete without, and may not be delivered or utilized except in connection with the Prospectus, including any supplements and amendments thereto. This Prospectus Supplement should be read in conjunction with the Prospectus, which is to be delivered with this Prospectus Supplement. This Prospectus Supplement is qualified by reference to the Prospectus, except to the extent that the information in this Prospectus Supplement updates or supersedes the information contained in the Prospectus, including any supplements and amendments thereto.

Our Common Stock is quoted on the OTCQB under the ticker symbol “BTTC.”

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 19 of the Prospectus.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this Prospectus Supplement is April 12, 2023.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): April 3, 2023

BITECH TECHNOLOGIES CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 000-27407 | 98-0187705 | ||

(State or other jurisdiction of incorporation or organization) |

(Commission File No.) |

(IRS Employee Identification No.) |

895 Dove Street, Suite 300

Newport Beach, CA 92660

(Address of principal executive offices)

(Registrant’s telephone number, including area code: (855) 777-0888

Not applicable.

(Former name or former address, if changed since last report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

| ☐ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) |

Name of each exchange on which registered | ||

| None. |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 5.02 Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain Officers; Compensatory Arrangements of Certain Officers.

On April 3, 2023, the board of directors of Bitech Technologies Corporation (the “Company”) approved the grant of a nonstatutory stock option (the “Stock Option”) to purchase 5,000,000 shares of the Company’s common stock, $0.001 par value (the “Common Stock”) to each of Robert J. Brilon, the Company’s Chief Financial Officer and Gregory D. Trimarche, a director of the Company.

The exercise price of the Stock Options are $0.03 per share. The Stock Options subject to these grants vest 50% on the date of the grant and 50% on April 3, 2024 so long as the recipient of the award is providing services to the Company or one of its subsidiaries; provided, however, the vesting is subject to acceleration such that if the recipient is terminated from his role without cause (as defined in the Stock Option) the number of shares subject to their respective Stock Option in the year of termination shall vest plus the number of shares that would have vested in the following year. In the event the recipient’s service is terminated with cause, the number of shares subject to the Stock Option awarded to such recipient in the year of termination shall vest.

The Stock Option may be exercised for the earlier of (1) ten years from grant date or (2) five (5) years after termination as a member of the Company’s board of directors.

Item 9.01 Financial Statements and Exhibits.

| (d) | The following exhibits are filed with this Current Report: |

| Exhibit No. | Description | |

| 10.1† | Form of Stock Option Agreement (Incorporated by reference to Exhibit 10.2 from the Form 8-K filed with the SEC on December 21, 2022). | |

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document |

| † | Includes management contracts and compensation plans and arrangements |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this Report to be signed on its behalf by the undersigned hereunto duly authorized.

| BITECH TECHNOLOGIES CORPORATION | ||

| Dated: April 10, 2023 | By: | /s/ Benjamin Tran |

| Benjamin Tran | ||

| Chief Executive Officer | ||

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2022

or

☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ______________ to ______________

Commission file number: 000-27407

BITECH TECHNOLOGIES CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 98-0187705 | |

| (State or Other Jurisdiction of | (I.R.S. Employer | |

| Incorporation or Organization) | Identification No.) |

895 Dove Street, Suite 300

Newport Beach, CA 92660

(Address of principal executive offices, Zip Code)

Telephone: (855) 777-0888

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| None. |

Securities registered under Section 12(g) of the Exchange Act:

Common Stock ($0.001 Par Value)

(Title of Each Class)

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definition of “large accelerated filer,” accelerated filer” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☒ | Smaller reporting company ☒ |

| Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold was approximately $14,000,000 as of the last business day of the registrant’s most recently completed fiscal quarter. For purposes of this computation, all officers, directors, and 10% beneficial owners of the registrant are deemed to be affiliates. Such determination should not be deemed to be an admission that such officers, directors, or 10% beneficial owners are, in fact, affiliates of the registrant.

At March 31, 2023, there were 463,998,027 shares of the registrant’s common stock outstanding (the only class of voting common stock).

DOCUMENTS INCORPORATED BY REFERENCE

None.

NOTE ABOUT FORWARD-LOOKING STATEMENTS

The information in this Annual Report contains forward-looking statements and information within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which are subject to the “safe harbor” created by those sections. The words “anticipates,” “believes,” “estimates,” “expects,” “intends,” “may,” “plans,” “projects,” “will,” “should,” “could,” “predicts,” “potential,” “continue,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. We may not actually achieve the plans, intentions or expectations disclosed in the Company’s forward-looking statements and you should not place undue reliance on the Company’s forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements that we make. The forward-looking statements are applicable only as of the date on which they are made, and we do not assume any obligation to update any forward-looking statements. All forward-looking statements in this Annual Report on Form 10-K are made based on the Company’s current expectations, forecasts, estimates and assumptions, and involve risks, uncertainties and other factors that could cause results or events to differ materially from those expressed in the forward-looking statements. In evaluating these statements, you should specifically consider various factors, uncertainties and risks that could affect the Company’s future results or operations. These factors, uncertainties and risks may cause the Company’s actual results to differ materially from any forward-looking statement set forth in this Annual Report on Form 10-K. You should carefully consider these risk and uncertainties described and other information contained in the reports we file with or furnish to the Securities and Exchange Commission (the “SEC”) before making any investment decision with respect to the Company’s securities. All forward-looking statements attributable to us or persons acting on the Company’s behalf are expressly qualified in their entirety by this cautionary statement.

TABLE OF CONTENTS

| 3 |

PART I

ITEM 1. BUSINESS

Bitech Technologies Corporation (formerly, Spine Injury Solutions Inc.) (the “Company”, “we” or “us”) was incorporated under the laws of Delaware on March 4, 1998. In connection with the Company’s planned expansion of its business following the completion of the acquisition of Bitech Mining Corporation, a Wyoming corporation (“Bitech Mining”), it filed a Certificate of Amendment to its Certificate of Incorporation, as amended (the “Certificate of Amendment”) with the Secretary of State of the State of Delaware on April 29, 2022 to change its corporate name to Bitech Technologies Corporation.

Currently, we have refocused our business development plans as we seek to position ourselves as a global technology solution enabler dedicated to providing a suite of green energy solutions with industry focus on green data centers, commercial and residential utility, EV infrastructure, and other renewable energy initiatives. We plan to pursue these innovative energy technologies through research and development, planned acquisitions of other green energy technologies and plans to become a grid-balancing operator using Battery Energy Storage System (BESS) solutions and applying new green technologies in power plants as a technology enabler in the green energy sector. While participating in the clean energy economy, we are seeking business partnerships with defensible technology innovators and renewable energy providers to facilitate investments, provide new market entries toward emerging-growth regions and implement or manufacture these innovative, scalable energy system solutions with technological focuses on smart grids, Building Energy Management System (BEMS), energy storage, and EV infrastructure.

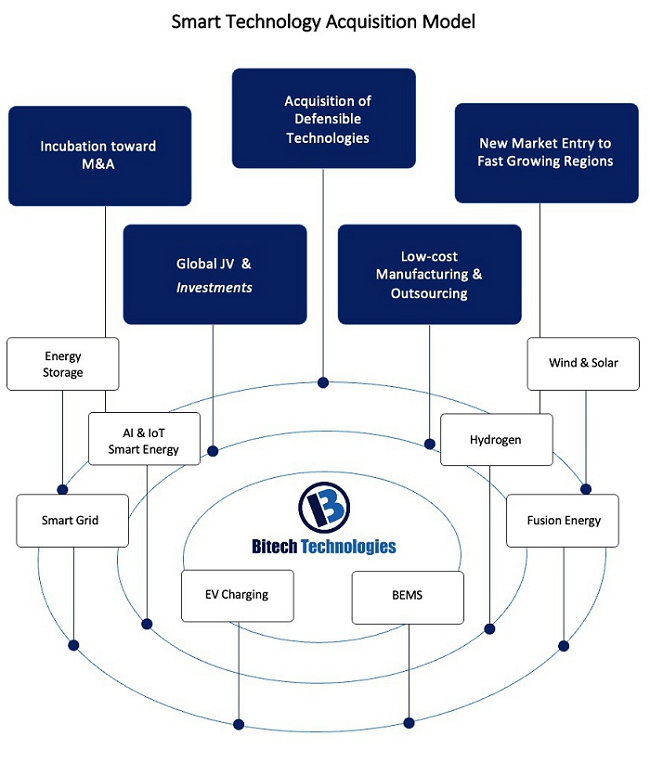

To accelerate growth of a planned intellectual property (IP) portfolio through acquisition strategies, we plan to execute our “Smart Acquisition Model” depicted in the diagram below with selected acquisitions of defensible technologies accompanied with visionary management teams who can demonstrate a common goal with us in order to unlock the full potential with capital infusion, accelerate growth. To achieve our development plans, we plan to incubate those acquired companies toward foreseeable plans for mergers and acquisitions, formation of global joint ventures, while facilitating new market entry to today’s fastest growing Southeast Asia region. With this acquisition model, we expect to build a valuable technology portfolio of IP assets in various innovative green energy technologies, leveraging our network of global capital partners with low-cost manufacturing capacity and oversea outsourcing technical talents from our niche sources in Vietnam.

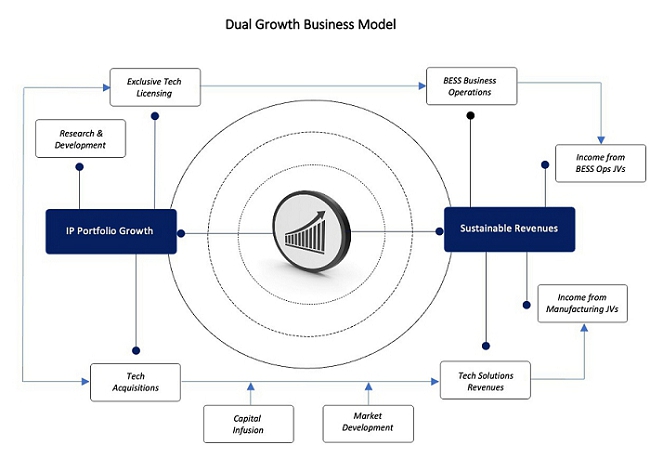

We plan to execute a “Dual Growth Business Model” as depicted in the diagram below encompassing (1) IP portfolio growth which includes technology licensing or technology acquisitions, enhanced with our plans to carry out research and development for specific applications, and (2) sustainable revenue growth by executing planned BESS acquisitions via joint ventures with capital partners to collect joint venture income from BESS operations or Vietnam-based manufacturing partners which can manufacture products derived from our technology solutions.

| 4 |

In light of these initiatives and other reasons noted below, the Company has, however, elected to discontinue its efforts to commercialize the electric power generation and charging system (the “Tesdison Technology”) it formerly licensed from SuperGreen Energy Corporation (“SuperGreen”) pursuant to the Patent & Technology Exclusive and Non-Exclusive License Agreement dated January 15, 2021, as amended, entered into between SuperGreen and the Company’s wholly owned subsidiary Bitech Mining Corporation (“Bitech Mining”) (the “SuperGreen License”). The Company has determined that the Tesdison Technology was not functional nor was it capable of being developed into a commercially viable product as had been represented to the Company by SuperGreen, its founder Calvin Cao, and his brother Michael Cao, leading up to Bitech Mining entering into the SuperGreen License. In addition, the Company will temporarily pause the further development of Intellisys-8, the Company’s planned chipset and related software that had been designed to reduce power consumption and heat in computer systems and accelerate their computational speed due to the currently unfavorable market conditions within the cryptocurrency market.

Acquisition of Bitech Mining Corporation

The Company acquired Bitech Mining on March 31, 2022 (the “Closing Date”) through a share exchange pursuant to a Share Exchange Agreement (the “Share Exchange Agreement”) by and among the Company, Bitech Mining, each of Bitech Mining’s shareholders (each, a “Seller” and collectively, the “Sellers”), and Benjamin Tran, solely in his capacity as Sellers’ Representative (“Sellers’ Representative”). The transaction contemplated by the Share Exchange Agreement is hereinafter referred to as the “Share Exchange”). The Share Exchange Agreement provides that the Company will acquire from the Sellers, an aggregate of 94,312,250 shares of Bitech Mining’s Common Stock, par value $0.001 per share, representing 100% of the issued and outstanding shares of Bitech Mining (collectively, the “Bitech Mining Shares”). In consideration of the Bitech Mining Shares, the Company issued to the Sellers an aggregate of 9,000,000 shares of the Company’s newly authorized Series A Convertible Preferred Stock, par value $0.001 per share (the “Series A Preferred Stock”). Each Bitech Mining Share shall be entitled to receive 0.09543 shares of Series A Preferred Stock. Each share of Series A Preferred Stock shall automatically convert into 53.975685 shares (an aggregate of approximately 485,781,300) of the Company’s Common Stock (the “Company Common Stock”) upon filing of an amendment to its Certificate of Incorporation increasing the number of the Company’s authorized common stock so that there are a sufficient number of shares of Company Common Stock authorized but unissued to permit a full conversion of all the Series A Preferred Stock. Effective as of June 27, 2022, the Series A Preferred Stock automatically converted into 485,781,168 shares of Company Common Stock following the June 27, 2022 filing of an amendment to its Certificate of Incorporation increasing the number of the Company’s authorized common stock to 1,000,000,000 shares. Upon conversion of the Series A Preferred Stock, the Sellers held, in the aggregate, approximately 96% of the issued and outstanding shares of Company capital stock on a fully diluted basis.

The Share Exchange was treated as a recapitalization and reverse acquisition for financial reporting purposes, and Bitech Mining is considered the acquirer for accounting purposes. As a result of the Share Exchange and the change in our business and operations, a discussion of the past financial results of our predecessor, Spine Injury Solutions Inc., is not pertinent, and under applicable accounting principles, the historical financial results of Bitech Mining, the accounting acquirer, prior to the Share Exchange are considered our historical financial results.

| 5 |

The following agreements were entered into in connection with the acquisition of Bitech Mining:

Management Services Agreement. On the Closing Date, the Company, Quad and Peter L. Dalrymple (“Dalrymple”), a former director of the Company, entered into a Management Services Agreement (the “MSA”) whereby Dalrymple agreed to act as the general manager of the video recording operations of Quad and collect certain accounts receivable of the Company (the “Services”). In exchange for providing the Services, the Company agreed to pay Dalrymple a fee equal to the net revenues derived from these operations after payment of all operating expenses related to such operations. The term of the MSA commences on the Closing Date and continues until the earlier to occur of the following: (i) 90 days after the Closing Date; (ii) the Company and Dalrymple’s mutual written consent; or (iii) any material breach of the MSA by either party, provided that the breaching party has been provided written notice of such breach and has failed to cure such breach within ten (10) days of receipt of such written notice.

Amendment to the Note. On the Closing Date, the Company, Quad and Dalrymple, entered into an Amendment to the Secured Promissory Note (the “Note Amendment”) whereby Dalrymple agreed that (i) the principal and accrued interest outstanding under the Secured Promissory Note dated August 31, 2020 as amended on October 29, 2021 issued by the Company in favor of Dalrymple (collectively, the “Note”) is $95,000 as of the Closing Date, (ii) the date on which the outstanding principal and accrued interest is due is 90 days after the Closing Date, (iii) any obligations of (x) the Company that become due and owing to Bitech Mining or the Sellers under Section 4.07(c) of the Share Exchange Agreement or (y) that become due and owing under Section 6.12 of the MSA may be offset against any amounts owed by the Company or Quad under the Note and (iv) all claims or causes of action (whether in contract or in tort, in law or in equity) that may be based upon, arise out of or relate to the Note, or the negotiation, execution or performance of the Note (including any representation or warranty made in or in connection with the Note or as an inducement to enter into the Note or this Amendment), may be made only against Quad, and SPIN who is not a party to the Note as of the Closing Date, including without limitation any past, present or future director, officer, employee, incorporator, member, manager, partner, equity holder, affiliate, agent, attorney or representative of SPIN (“SPIN Parties”), shall have no liability (whether in contract or in tort, in law or in equity, or based upon any theory that seeks to impose liability of the SPIN Parties) for any obligations or liabilities arising under, in connection with or related to the Note or for any claim based on, in respect of, or by reason of the Note or its negotiation or execution, and Dalrymple waives and releases all such liabilities, claims and obligations against any such SPIN Parties.

Amendment to the Security Agreement. On the Closing Date, the Company, Quad and Dalrymple, entered into an Amendment to Security Agreement (the “Security Agreement Amendment”) whereby the parties to that agreement agreed that (i) Quad shall be included with the Company as an additional debtor for all purposes in the Security Agreement entered into between the Company and Dalrymple dated August 31, 2020 (the “Security Agreement”), (ii) Quad’s collateral obligations under the Security Agreement shall only relate to its accounts receivable, and the collateral described relating to “Pledged Securities” as defined in the Security Agreement shall not apply to Quad’s obligations under the Security Agreement, (iii) the Company’s pledge of its accounts receivables as provided for in the Security Agreement will be limited solely to the Company’s accounts receivables in existence as of March 27, 2022 at 11:59 P.M. ET, and shall not apply to any after acquired accounts receivables and (iv) the Company is authorized to file an amended financing statement to reflect the terms of Security Agreement Amendment and Quad shall promptly file a financing statement reflecting the terms set for in such amendment.

Disposition of Quad Video Assets

On June 30, 2022 (the “Effective Date”), we completed the sale of all of the assets of our wholly owned subsidiary Quad Video Halo, Inc. (“Quad Video”) pursuant to the terms of an Asset Purchase Agreement entered into among Quad Video, Quad Video Holdings Corporation (“Quad Holdings”) and Peter Dalrymple, a former officer, director and substantial shareholder of the Company (“Dalrymple,” together with Quad Holdings, collectively, the “Buyers”) dated as of the Effective Date (the “Quad Video APA”). Pursuant to the terms of the Quad Video APA, Quad Video sold all of its assets to Quad Holdings which included its accounts receivables, fixed assets, intangible assets and all customer lists associated with Quad Video’s business (the “Quad Video Assets”).

Under the terms of the Quad Video APA, the amount of the consideration paid to the Company for purchase of the Quad Video Assets was Mr. Dalrymple’s cancellation of a promissory note with an approximate principal balance of $8,789 plus accrued interest as of the Effective Date issued by the Company to Mr. Dalrymple and the cancellation of a security agreement securing payment of that note pursuant to a Secured Promissory Note and Security Agreement Cancellation Agreement and assumed all liabilities related the Quad Video’s operations and the Quad Video Assets and terminated the Management Services Agreement entered into among the Company, Quad Video and Dalrymple dated March 31, 2022 pursuant to a Management Services Termination Agreement.

In addition, on the Effective Date, we completed the sale of certain accounts receivables related to our spine pain management business pursuant to the terms of an Asset Purchase Agreement entered into among the Company, SPIN Collections LLC, a company owned or controlled by Dalrymple and Dalrymple (the “SPIN Accounts Receivable APA”). The consideration received by the Company in connection with the SPIN Accounts Receivable APA was $10.00 and other good and valuable consideration that was nominal and immaterial.

Prior to March 31, 2022, we were engaged in the business of owning, developing and leasing the Quad Video Halo video recording system (“QVH”) used to record medical procedures including the collection of accounts receivables related to previously provided spine injury diagnostic services (collectively, the “QVH Business”). On June 30, 2022, we sold the assets related to the QVH Business.

Effective as of June 27, 2022, we issued an aggregate of 485,781,168 shares (the “Conversion Shares”) of our common stock upon the conversion of 9,000,000 shares of our Series A Convertible Preferred Stock, $0.001 par value per share (the “Series A Preferred”). The shares of the Series A Preferred were issued to the former shareholders of Bitech Mining on March 31, 2022 in exchange for their shares in Bitech Mining representing 100% of the issued and outstanding shares of Bitech Mining. The Series A Preferred automatically converted into our common stock upon our filing of a Certificate of Amendment to our Certificate of Incorporation, as amended on June 27, 2022.

| 6 |

Employees

As of December 31, 2022, we had two full-time employees. To date, we have not experienced any work stoppages and we consider our relationship with our employees to be good. None of our employees are either represented by a labor union or are subject to a collective bargaining agreement.

ITEM 1A. RISK FACTORS

Smaller reporting companies are not required to provide the information required by this item.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not Applicable.

ITEM 2. PROPERTIES

Our principal executive offices are located at 895 Dove Street, Suite 300, Newport Beach, CA 92660. We occupy this location pursuant to a lease that may be terminated by us on 90 days prior notice.

ITEM 3. LEGAL PROCEEDINGS

As of the date of this Annual Report, to our knowledge, there are no legal proceedings or regulatory actions material to us to which we are a party, or have been a party to, or of which any of our property is or was the subject matter of, and no such proceedings or actions are known by us to be contemplated except as provided below:

Due to the misrepresentations and omissions of SuperGreen, Calvin C. Cao and Michael H. Cao, among other reasons, the Company filed a complaint in the U.S. District Court, Central District of California on February 2, 2023 against SuperGreen, Michael H. Cao, Linh T. Dao, Calvin C. Cao and entities affiliated with them alleging fraud-concealment, breach of contract, breach of fiduciary duty-duty of good faith, breach of fiduciary duty-undivided loyalty, conversion and violation of California Penal Code Sec. 496 (the “Cao Lawsuit”). This lawsuit seeks compensatory damages of at least $33.6 million, treble and punitive damages, imposition of a constructive trust over the defendants assets, pre-judgment and post-judgment interest, attorney’s fees and such other relief as determined by the court.

Effective February 20, 2023, the Company, together with its wholly owned subsidiary Bitech Mining Corporation entered into a Confidential Settlement, Mutual Release, and Share Transfer Agreement (the “C. Cao Settlement Agreement”) with Calvin Cao (“C. Cao”) and SuperGreen Energy Corporation (“SuperGreen,” together with C. Cao, the “C. Cao Parties”). The C. Cao Settlement Agreement settles as to the C. Cao Parties, the Cao Lawsuit. Pursuant to the C. Cao Settlement Agreement, the C. Cao Parties terminated the Patent & Technology Exclusive and Non-Exclusive License Agreement between Bitech Mining Corporation and SuperGreen dated January 15, 2021 as amended on January 15, 2021 and on March 26, 2022 (the “License Agreement”) and SuperGreen canceled 51,507,749 shares of the Company’s common stock, par value $0.001 per share issued by the Company to SuperGreen pursuant to the License Agreement. In addition, the parties to the Settlement Agreement agreed to a mutual general release of liabilities against each other, refrain from making any disparaging remarks about each other and the Company’s filing a dismissal with prejudice of the Cao Lawsuit as to the C. Cao Parties. The Settlement Agreement also contains additional covenants, representations and warranties that are customary of litigation settlement agreements. The Company intends to continue to pursue the Cao Lawsuit as to the remaining defendants in that case, namely Michael Cao, B&B Investment Holding, LLC (“B&B Investment”) and Linh Dao.

On March 6, 2023, Michael Cao and Linh Dao filed, without an attorney, a pro se Motion to Dismiss for Lack of Jurisdiction. No hearing has been set for this motion. On March 23, 2023, the Court entered a default against B&B Investment for failing to appear or otherwise defend itself in the case. B&B Investment is an affiliate of Michael Cao.

The Company intends to vigorously prosecute this case and believes the basis for the motion to dismiss the case lack merit. We cannot predict the outcome of this lawsuit, however.

Litigation Assessment

We have evaluated the foregoing Cao Lawsuit to assess the likelihood of any unfavorable outcome and to estimate, if possible, the amount of potential loss as it relates to the litigation. Based on this assessment and estimate, which includes an understanding of our intention to vigorously prosecute the Cao Lawsuit, we believe that the potential defenses of any of the remaining defendants lack merit, however, and we cannot predict the likelihood of any recoveries by any of our claims against the remaining defendants. This assessment and estimate is based on the information available to management as of the date of this Annual Report and involves a significant amount of management judgment, including the inherent difficulty associated with assessing litigation matters in their early stages. As a result, the actual outcome or loss may differ materially from those envisioned by the current assessment and estimate. Our failure to successfully prosecute, defend or settle the Cao Litigation with the remaining defendants could have a material adverse effect on our financial condition, revenue and profitability and could cause the market value of our common stock to decline.

ITEM 4. MINE SAFETY DISCLOSURES

Not Applicable.

| 7 |

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is quoted on the OTCQB tier of the OTC Markets Group, Inc. under the symbol, “BTTC.” The OTC Market is a network of security dealers who buy and sell stock. The dealers are connected by a computer network that provides information on current “bids” and “asks”, as well as volume information.

The following table sets forth trading information for our common stock for the periods indicated, as quoted on the OTCQB. These quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions.

| Low Trading Price | High Trading Price | |||||||

| Period | ($) | ($) | ||||||

| Year Ended December 31, 2022 | ||||||||

| Fourth Quarter (December 31, 2022) | 0.02 | 0.14 | ||||||

| Third Quarter (September 30, 2022) | 0.10 | 0.19 | ||||||

| Second Quarter (June 30, 2022) | 0.09 | 0.45 | ||||||

| First Quarter (March 31, 2022) | 0.07 | 0.18 | ||||||

| Year Ended December 31, 2021 | ||||||||

| Fourth Quarter (December 31, 2021) | 0.05 | 0.21 | ||||||

| Third Quarter (September 30, 2021) | 0.15 | 0.42 | ||||||

| Second Quarter (June 30, 2021) | 0.06 | 0.43 | ||||||

| First Quarter (March 31, 2021) | 0.03 | 0.19 | ||||||

Record Holders

As of December 31, 2022 there were approximately 115 record holders of our common stock. The number of record holders does not include beneficial owners of common stock whose shares are held in the names of banks, brokers, nominees or other fiduciaries. We believe there are approximately 550 shareholders as of December 31, 2022.

Dividend Policy

We have not declared or paid any dividends on our common stock since our inception. We currently intend to reinvest all cash resources to finance the development and growth of our business. As a result, we do not intend to pay dividends on our common stock in the foreseeable future. Any future determination to pay dividends will be at the discretion of our board of directors and will depend on the financial condition, earnings, legal requirements, restrictions in its debt agreements and any other factors that our board of directors deems relevant. In addition, as a holding company, our ability to pay dividends depends on our receipt of cash dividends from our operating subsidiaries, which may further restrict our ability to pay dividends as a result of the laws of their respective jurisdictions of organization, agreements of our subsidiaries or covenants under future indebtedness that we or our subsidiaries may incur.

[Unregistered Sales of Securities]

The following information represents securities sold by us that has not been previously included in a Quarterly Report on Form 10-Q or a Current Report on Form 8-K which were not registered under the Securities Act. Included are new issues, securities issued in exchange for property, services or other securities, securities issued upon conversion from our other share classes and new securities resulting from the modification of outstanding securities. We issued all of the securities listed below pursuant to the exemption from registration provided by Section 4(a)(2) of the Securities Act, or Regulation D or Regulation S promulgated thereunder.

On April 19, 2022, the Company issued 4,635,720 shares of its Common Stock to an individual as compensation for future services at a fair value price on the date of issuance of $0.10 per share. The shares vest 25% on each April 18 commencing on April 18, 2023 so long as the individual is providing services to the Company or one of its subsidiaries.

On April 14, 2022, the Company issued 3,348,000 shares of its Common Stock to an individual as compensation for future services at a fair value price on the date of issuance of $0.10 per share. 1,802,769 shares vest on April 13, 2023 and 515,077 shares vest on April 13, 2024, April 13, 2025, and April 13, 2026 so long as the individual is providing services to the Company or one of its subsidiaries.

During August 2022 and October 2022, the Company sold a total of 1,500,000 shares of its unregistered common stock to four accredited investors for $0.10 per share for total gross proceeds of $150,000.

Equity Compensation Plan Information

As of December 31, 2022, we do not have any compensation plans under which our equity securities are authorized for issuance.

ITEM 6. RESERVED

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This management discussion and analysis (“MD&A”) of the financial condition and results of operations of Bitech Technologies Corporation (the “Company,” “Bitech Technologies,” “our” or “we”) is for the years ended December 31, 2022 and 2021. It is supplemental to, and should be read in conjunction with, our financial statements for the period January 8, 2021 (inception) through December 31, 2022 and the accompanying notes for such period included in our Current Report on Form 8-K filed with the Securities and Exchange Commission, or SEC, on April 4, 2022. Our financial statements are prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). Financial information presented in this MD&A is presented in United States dollars (“$” or “US$”), unless otherwise indicated.

The information about us provided in this MD&A, including information incorporated by reference, may contain “forward-looking statements” and certain “forward-looking information” as defined under applicable United States securities laws. All statements, other than statements of historical fact, made by us that address activities, events or developments that we expect or anticipate will or may occur in the future are forward-looking statements, including, but not limited to, statements preceded by, followed by or that include words such as “may”, “will”, “would”, “could”, “should”, “believes”, “estimates”, “projects”, “potential”, “expects”, “plans”, “intends”, “anticipates”, “targeted”, “continues”, “forecasts”, “designed”, “goal”, or the negative of those words or other similar or comparable words and includes, among others, information regarding: our future business activities; our ability to generate revenues; our need for substantial additional financing to operate our current and future business and difficulties we may face acquiring additional financing on terms acceptable to us or at all; risks related to competition; risks related to our lack of internal controls over financial reporting and their effectiveness; increased costs we are subject to as a result of being a public company in the United States; and other events or conditions that may occur in the future.

Forward-looking statements may relate to future financial conditions, results of operations, plans, objectives, performance or business developments. These statements speak only as at the date they are made and are based on information currently available and on the then current expectations of the party making the statement and assumptions concerning future events, which are subject to a number of known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements to be materially different from that which was expressed or implied by such forward-looking statements.

| 8 |

Although we believe that the expectations and assumptions on which such forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements, because no assurance can be given that they will prove to be correct. Since forward-looking statements address future events and conditions, by their very nature, they involve inherent risks and uncertainties. Actual results could differ materially from those currently anticipated due to a number of factors and risks discussed above.

Consequently, all forward-looking statements made in this MD&A and other documents, as applicable, are qualified by such cautionary statements, and there can be no assurance that the anticipated results or developments will actually be realized or, even if realized, that they will have the expected consequences to or effects on us. The cautionary statements contained or referred to in this section should be considered in connection with any subsequent written or oral forward-looking statements that we and/or persons acting on its behalf may issue. We do not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, other than as required under securities legislation.

Overview of the Business

Currently, we have refocused our business development plans as we seek to position ourselves as a global technology solution enabler dedicated to providing a suite of green energy solutions with industry focus on green data centers, commercial and residential utility, EV infrastructure, and other renewable energy initiatives. We have been developing and evaluating the commercial viability of our Evirontek™ Integrated Platform to resolve the exorbitantly high cost of electricity in several industries. We plan to pursue these innovative energy technologies through research and development, planned acquisitions of other green energy technologies and plans to become a grid-balancing operator using Battery Energy Storage System (BESS) solutions and applying new green technologies in power plants as a technology enabler in the green energy sector. While participating in the clean energy economy, we are seeking business partnerships with defensible technology innovators and renewable energy providers to facilitate investments, provide new market entries toward emerging-growth regions and implement or manufacture these innovative, scalable energy system solutions with technological focuses on smart grids, Building Energy Management System (BEMS), energy storage, and EV infrastructure.

To accelerate growth of a planned intellectual property (IP) portfolio through acquisition strategies, we plan to execute our Smart Acquisition Model with selected acquisitions of defensible technologies accompanied with visionary management teams who can demonstrate a common goal with us in order to unlock the full potential with capital infusion, accelerate growth. To achieve our development plans, we plan to incubate those acquired companies toward foreseeable plans for mergers and acquisitions, formation of global joint ventures, while facilitating new market entry to today’s fastest growing Southeast Asia region. With this acquisition model, we expect to build a valuable technology portfolio of IP assets in various innovative green energy technologies, leveraging our network of global capital partners with low-cost manufacturing capacity and oversea outsourcing technical talents from our niche sources in Vietnam.

Further, we plan to execute a Dual Growth Business Model as depicted in the diagram below encompassing (1) IP portfolio growth which includes technology licensing or technology acquisitions, enhanced with our plans to carry out research and development for specific applications, and (2) sustainable revenue growth by executing planned BESS acquisitions via joint ventures with capital partners to collect joint venture income from BESS operations or Vietnam-based manufacturing partners which can manufacture products derived from our technology solutions.

In light of these initiatives and other reasons noted below, the Company has, however, elected to discontinue its efforts to commercialize the electric power generation and charging system (the “Tesdison Technology”) it licensed from SuperGreen pursuant to the SuperGreen License. The Company has determined that the Tesdison Technology was not functional nor was it capable of being developed into a commercially viable product as had been represented to the Company by SuperGreen, its founder Calvin Cao, and his brother Michael Cao, leading up to Bitech Mining entering into the SuperGreen License. In addition, the Company will temporarily pause the further development of Intellisys-8, the Company’s planned chipset and related software that had been designed to reduce power consumption and heat in computer systems and accelerate their computational speed due to the currently unfavorable market conditions within the cryptocurrency market.

The Company acquired Bitech Mining on March 31, 2022 pursuant to a Share Exchange Agreement. Pursuant to the Share Exchange Agreement we acquired an aggregate of 94,312,250 shares of Bitech Mining’s Common Stock representing 100% of the issued and outstanding shares of Bitech Mining in exchange for an aggregate of 9,000,000 shares of the Company’s newly authorized Series A Convertible Preferred Stock. Each share of Series A Preferred Stock automatically converted into 53.975685 shares (an aggregate of approximately 485,781,300) of the Company’s Common Stock (the “Company Common Stock”) upon filing of an amendment to its Certificate of Incorporation increasing the number of the Company’s authorized common stock so that there were a sufficient number of shares of Company Common Stock authorized but unissued to permit a full conversion of all the Series A Preferred Stock. Effective as of June 27, 2022, the Series A Preferred Stock automatically converted into 485,781,168 shares of Company Common Stock following the June 27, 2022 filing of an amendment to its Certificate of Incorporation increasing the number of the Company’s authorized common stock to 1,000,000,000 shares. Upon conversion of the Series A Preferred Stock, the Sellers held, in the aggregate, approximately 96% of the issued and outstanding shares of Company capital stock on a fully diluted basis.

The Share Exchange was treated as a recapitalization and reverse acquisition for financial reporting purposes, and Bitech Mining is considered the acquirer for accounting purposes. As a result of the Share Exchange and the change in our business and operations, a discussion of the past financial results of our predecessor, Spine Injury Solutions Inc., is not pertinent, and under applicable accounting principles, the historical financial results of Bitech Mining, the accounting acquirer, prior to the Share Exchange are considered our historical financial results.

The following agreements were entered into in connection with the acquisition of Bitech Mining:

Agreements involving Peter L. Dalrymple. On March 31, 2022, the Company, Quad and Peter L. Dalrymple (“Dalrymple”), a former director of the Company, entered into the MSA, Note Amendment and Security Agreement Amendment. See “Item 1 - Business – Acquisition of Bitech Mining Corporation.”

Disposition of Quad Video Assets. On June 30, 2022, we completed the sale of the Quad Video Assets pursuant to the terms of the Quad Video APA and the sale of certain accounts receivables related to our former spine pain management business pursuant to the terms of the SPIN Accounts Receivable APA. See “Item 1 - Business – Disposition of Quad Video Assets.”

Prior to March 31, 2022, we were engaged in the business of owning, developing and leasing the Quad Video Halo video recording system (“QVH”) used to record medical procedures including the collection of accounts receivables related to previously provided spine injury diagnostic services (collectively, the “QVH Business”). On June 30, 2022, we sold the assets related to the QVH Business.

| 9 |

Historically, the Company acquired Bitech Mining Corporation, a Wyoming corporation (“Bitech Mining”) on

| 10 |

Comparison of the years ended December 31, 2022 and 2021.

The Company has not generated any revenues from its primary business for the year ended December 31, 2022. We invoiced and collected $26,197 from QVH legacy business and recorded other income of $50,275 generated from accounts receivable previously written-off as uncollectible for the year ended December 31, 2022. There was no revenue for the year ended December 31, 2021.

During the year ended December 31, 2022, we incurred $888,106 of general and administrative expenses compared to $284,959 for the same period in 2021. General and administrative expenses have increased during 2022 compared to 2021 as the Company moves from development stage to revenue generation.

As a result of the foregoing, we had net loss of ($811,635) for the year ended December 31, 2022, compared to a net loss of ($284,959) for the year ended December 31, 2021.

Working Capital

The calculation of Working Capital provides additional information and is not defined under GAAP. We define Working Capital as current assets less current liabilities. This measure should not be considered in isolation or as a substitute for any standardized measure under GAAP. This information is intended to provide investors with information about our liquidity.

Other companies in our industry may calculate this measure differently than we do, limiting its usefulness as a comparative measure.

Liquidity and Capital Resources

As of December 31, 2022 and December 31, 2021, we had total current liabilities of $11,397 and $11,106, respectively, and current assets of $210,723 and $976,947, respectively, to meet our current obligations. As of December 31, 2022, we had working capital of $199,326, a decrease of working capital of $766,515 as compared to December 31, 2021, driven primarily by cash used in operations.

For the year ended December 31, 2022, cash used in operations was ($789,344) which primarily included the net loss of ($811,635) partially offset by a $35,000 full amortization of exclusive license agreement.

We have a history of operating losses. We have not yet achieved profitable operations and expect to incur further losses. We have funded our operations primarily from equity financing. As of December 31, 2022, cash generated from financing activities was not sufficient to fund our growth strategy in the short-term or long-term. The primary need for liquidity is to fund working capital requirements of the business, including operational expenses in connection with our efforts to become a provider of a suite of green energy solutions. The primary source of liquidity has primarily been private financing transactions. The ability to fund operations and pursue opportunities within the green energy industry depends on our ability to raise funds from debt and/or equity financing which is subject to prevailing economic conditions and financial, business and other factors, some of which are beyond our control. There can be no assurance that additional financing will be available to us when needed or, if available, that it can be obtained on commercially reasonable terms.

Off-Balance Sheet Arrangements

As of the date of this Annual Report on Form 10-K, we do not have any off-balance-sheet arrangements that have, or are reasonably likely to have, a current or future effect on our results of operations or financial condition, including, and without limitation, such considerations as liquidity and capital resources.

Changes in or Adoption of Accounting Practices

There were no material changes in or adoption of new accounting practices during the year ended December 31, 2022.

Critical Accounting Policies

See Note 2 of the accompanying notes to unaudited condensed consolidated financial statements, which note is incorporated herein by reference.

Income Tax Expense (Benefit)

We have not made a provision for income taxes in 2022 or 2021, which reflects our valuation allowance established against our benefits from net operating loss carryforwards.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not Applicable.

| 11 |

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA.

Our financial statements for the fiscal years ended December 31, 2022 and 2021 are attached hereto.

TABLE OF CONTENTS

| 12 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and

Stockholders of Bitech Technologies Corporation

Opinion on the Financial Statements

We have audited the accompanying consolidated balance sheet of Bitech Technologies Corporation (“the Company”) as of December 31, 2022, and the related consolidated statements of operations, changes in shareholders’ deficit, and cash flows for year then ended, and the related notes (collectively referred to as the financial statements). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2022, and the results of its operations and its cash flows for the year ended December 31, 2022, in conformity with accounting principles generally accepted in the United States of America.

The Company’s Ability to Continue as a Going Concern

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the financial statements, the Company has suffered recurring losses from operations and negative cash flows from operating activities, therefore, the Company has stated that substantial doubt exists about its ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 2. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audit we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provide a reasonable basis for our opinion.

Critical Audit Matters

The critical audit matters communicated below are matters arising from the current period audit of the financial statements that were communicated or required to be communicated to the audit committee and that: (1) relate to accounts or disclosures that are material to the financial statements and (2) involved our especially challenging, subjective, or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the financial statements, taken as a whole, and we are not, by communicating the critical audit matters below, providing separate opinions on the critical audit matters or on the accounts or disclosures to which they relate.

Going Concern

As described further in Note 2 to the consolidated financial statements, the Company has incurred losses each year from inception through December 31, 2022 and expects to incur additional losses in the future.

We determined the Company’s ability to continue as a going concern is a critical audit matter due to the estimation and uncertainty regarding the Company’s future cash flows and the risk of bias in management’s judgments and assumptions in estimating these cash flows.

Our audit procedures related to the Company’s assertion on its ability to continue as a going concern included the following, among others:

We reviewed the Company’s working capital and liquidity ratios and forecasted revenue, operating expenses, and uses and sources of cash used in management’s assessment of whether the Company has sufficient liquidity to fund operations for at least one year from the financial statement issuance date. This testing included inquiries with management, comparison of prior period forecasts to actual results, consideration of positive and negative evidence impacting management’s forecasts, the Company’s financing arrangements in place as of the report date, market and industry factors and consideration of the Company’s relationships with its financing partners.

| /s/ Fortune CPA, Inc | |

| We have served as the Company’s auditor since 2022. | |

Huntington Beach, CA |

|

| March 31, 2023 | |

| PCAOB # 6901 |

| 13 |

BITECH TECHNOLOGIES CORPORATION

CONSOLIDATED BALANCE SHEETS

AUDITED

| December 31, | December 31, | |||||||

| 2022 | 2021 | |||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | 197,723 | $ | 976,947 | ||||

| Prepaid expense | 13,000 | - | ||||||

| Total current assets | 210,723 | 976,947 | ||||||

| Intangible Asset – Exclusive License | - | 35,000 | ||||||

| Total assets | $ | 210,723 | $ | 1,011,947 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: | ||||||||

| Note payable to shareholder | - | - | ||||||

| Accounts payable and accrued liabilities | 11,397 | 11,106 | ||||||

| Total current liabilities | 11,397 | 11,106 | ||||||

| Stockholders’ equity | ||||||||

| Preferred stock, $0.001 par value, 10,000,000 shares authorized, 0 shares issued and outstanding at December 31, 2022 and December 31, 2021, respectively | - | - | ||||||

| Series A Convertible Preferred stock; $0.001 par value, 9,000,000 shares authorized, no shares issued and outstanding at December 31, 2022 and December 31, 2021 | - | - | ||||||

| Common stock: $0.001 par value, 1,000,000,000 shares authorized, 515,505,770 and 20,240,882 shares issued and outstanding at December 31, 2022 and December 31, 2021, respectively | 515,506 | 20,241 | ||||||

| Additional paid-in capital | 780,414 | 1,265,559 | ||||||

| Accumulated deficit | (1,096,594 | ) | (284,959 | ) | ||||

| Total stockholders’ equity | 199,326 | 1,000,841 | ||||||

| Total liabilities and stockholders’ equity | $ | 210,723 | $ | 1,011,947 | ||||

The accompanying notes are an integral part of the audited consolidated financial statements.

| 14 |

BITECH TECHNOLOGIES CORPORATION

CONSOLIDATED STATEMENTS OF OPERATIONS

AUDITED

For the Year ended December 31, 2022 | For the Year ended December 31, 2021 | |||||||

| REVENUE | $ | 26,197 | - | |||||

| COST OF REVENUE | - | - | ||||||

| GROSS PROFIT | 26,197 | - | ||||||

| OPERATING EXPENSES | ||||||||

| General & Administrative | 888,106 | 284,959 | ||||||

| Total Operating Expenses | 888,106 | 284,959 | ||||||

| LOSS FROM OPERATIONS | (861,910 | ) | (284,959 | ) | ||||

| OTHER INCOME (EXPENSE) | ||||||||

| Interest and Other Income | 50,475 | - | ||||||

| Interest Expense | (200 | ) | - | |||||

| Total Other Income (Expense) | 50,275 | - | ||||||

| LOSS BEFORE INCOME TAXES | (811,635 | ) | (284,959 | ) | ||||

| BENEFIT (PROVISION) FOR INCOME TAXES | - | - | ||||||

| NET LOSS | $ | (811,635 | ) | $ | (284,959 | ) | ||

| BASIC AND DILUTED LOSS PER SHARE | $ | (0.00 | ) | $ | (0.00 | ) | ||

| WEIGHTED AVERAGE SHARES | 284,808,907 | 20,240,882 | ||||||

The accompanying notes are an integral part of the audited consolidated financial statements.

| 15 |

BITECH TECHNOLOGIES CORPORATION

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

As of December 31, 2022

| Common Stock | Preferred Stock | Additional Paid-In | Accumulated | Total Stockholders’ Equity | ||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Capital | Deficit | (Deficit) | ||||||||||||||||||||||

| Balances, January 21, 2021 (inception) | 20,240,882 | 20,241 | - | - | 1,265,559 | - | 1,285,800 | |||||||||||||||||||||

| Net loss | - | - | - | - | (284,959 | ) | (284,959 | ) | ||||||||||||||||||||

| Balances, December 31, 2021 | 20,240,882 | $ | 20,241 | - | - | $ | 1,265,559 | $ | (284,959 | ) | $ | 1,000,841 | ||||||||||||||||

| Recapitalization | (139,880 | ) | (139,880 | ) | ||||||||||||||||||||||||

| Restricted Stock Awards | 7,983,720 | 7,984 | (7,984 | ) | ||||||||||||||||||||||||

| Series A Preferred Shares issued in Share Exchange | 9,000,000 | 9,000 | 9,000 | |||||||||||||||||||||||||

| Shares issued upon conversion of Series A Preferred Stock | 485,781,168 | 485,781 | (9,000,000 | ) | (9,000 | ) | (485,781 | ) | (9,000 | ) | ||||||||||||||||||

| Sale of Common Stock | 1,500,000 | 1,500 | 148,500 | 150,000 | ||||||||||||||||||||||||

| Net loss | - | - | - | - | - | (811,635 | ) | (811,635 | ) | |||||||||||||||||||

| Balances, December 31, 2022 | 515,505,770 | $ | 515,506 | - | $ | - | $ | 780,414 | $ | (1,176,594 | ) | $ | 199,326 | |||||||||||||||

The accompanying notes are an integral part of the audited consolidated financial statements.

| 16 |

BITECH TECHNOLOGIES CORPORATION

CONSOLIDATED STATEMENTS OF CASH FLOWS

AUDITED

| YEAR ENDED DECEMBER 31, | ||||||||

| 2022 | 2021 | |||||||

| Cash flows from operating activities: | ||||||||

| Net loss | $ | (811,635 | ) | $ | (284,959 | ) | ||

| Adjustments to reconcile net loss to net cash provided by operating activities: | ||||||||

| Impairment Write-off – Exclusive License | 35,000 | - | ||||||

| Common Stock issued for services | 111,200 | |||||||

| Changes in operating assets and liabilities: | ||||||||

| Prepaid expenses and other assets | (13,000 | ) | - | |||||

| Accounts payable and accrued liabilities | 291 | 11,106 | ||||||

| Net cash provided by (used in) operating activities | (789,344 | ) | (162,653 | ) | ||||

| Cash flows from investing activities: | ||||||||

| Purchase Intangible Asset – Exclusive License | - | (25,000 | ) | |||||

| Net cash used in investing activities | - | (25,000 | ) | |||||

| Cash flows from financing activities: | ||||||||

| Cash from Sale of Common Stock, net | 150,000 | 1,164,600 | ||||||

| Recapitalization | (139,880 | ) | ||||||

| Net cash provided by (used in) financing activities | 10,120 | 1,164,600 | ||||||

| Net increase (decrease) in cash and cash equivalents | (779,224 | ) | 976,947 | |||||

| Cash and cash equivalents at beginning of period | 976,947 | - | ||||||

| Cash and cash equivalents at end of period | $ | 197,723 | $ | 976,947 | ||||

| Supplemental disclosure of non-cash Investing and Financing | ||||||||

| Activities: | ||||||||

| Common Stock Issued for Intangible Asset – Exclusive License | $ | - | $ | 10,000 | ||||

| Supplementary disclosure of cash flow information: | ||||||||

| Interest paid | $ | 200 | $ | - | ||||

| Taxes paid | $ | - | $ | - | ||||

The accompanying notes are an integral part of the audited consolidated financial statements.

| 17 |

BITECH TECHNOLOGIES CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1. DESCRIPTION OF BUSINESS

Bitech Technologies Corporation (formerly, Spine Injury Solutions Inc.) (the “Company”, “we” or “us”) was incorporated under the laws of Delaware on March 4, 1998. In connection with the Company’s planned expansion of its business following the completion of the acquisition of Bitech Mining Corporation, a Wyoming corporation (“Bitech Mining”), it filed a Certificate of Amendment to its Certificate of Incorporation, as amended (the “Certificate of Amendment”) with the Secretary of State of the State of Delaware on April 29, 2022 to change its corporate name to Bitech Technologies Corporation.

As a development-stage company, we are a global technology solution enabler dedicated to providing a suite of green energy solutions with industry focus on green data centers, commercial and residential utility, EV infrastructure, and other renewable energy initiatives. Bitech has been developing and evaluating the commercial viability of its Evirontek™ Integrated Platform to resolve the exorbitantly high cost of electricity in several industries. Bitech innovates energy technologies through research and development, planned acquisitions of other green energy technologies and plans to become a grid-balancing operator using Battery Energy Storage System (BESS) solutions and applying new green technologies in power plants to save electricity. While participating in the Clean Energy Economy, we seek business partnerships with defensible technology innovators and renewable energy providers to facilitate investments, provide new market entries toward emerging-growth regions and implement or manufacture these innovative, scalable energy system solutions with technological focuses on smart grid, Building Energy Management System (BEMS), energy storage, and EV infrastructure.

The Company acquired Bitech Mining on March 31, 2022 (the “Closing Date”) through a share exchange pursuant to a Share Exchange Agreement (the “Share Exchange Agreement”) by and among the Company, Bitech Mining, each of Bitech Mining’s shareholders (each, a “Seller” and collectively, the “Sellers”), and Benjamin Tran, solely in his capacity as Sellers’ Representative (“Sellers’ Representative”). The transaction contemplated by the Share Exchange Agreement is hereinafter referred to as the “Share Exchange”). The Share Exchange Agreement provides that the Company will acquire from the Sellers, an aggregate of 94,312,250 shares of Bitech Mining’s Common Stock, par value $0.001 per share, representing 100% of the issued and outstanding shares of Bitech Mining (collectively, the “Bitech Mining Shares”). In consideration of the Bitech Mining Shares, the Company issued to the Sellers an aggregate of 9,000,000 shares of the Company’s newly authorized Series A Convertible Preferred Stock, par value $0.001 per share (the “Series A Preferred Stock”). Each Bitech Mining Share shall be entitled to receive 0.09543 shares of Series A Preferred Stock. Each share of Series A Preferred Stock shall automatically convert into 53.975685 shares (an aggregate of approximately 485,781,300) of the Company’s Common Stock (the “Company Common Stock”) upon filing of an amendment to its Certificate of Incorporation increasing the number of the Company’s authorized common stock so that there are a sufficient number of shares of Company Common Stock authorized but unissued to permit a full conversion of all the Series A Preferred Stock. Effective as of June 27, 2022, the Series A Preferred Stock automatically converted into 485,781,168 shares of Company Common Stock following the June 27, 2022 filing of an amendment to its Certificate of Incorporation increasing the number of the Company’s authorized common stock to 1,000,000,000 shares. Upon conversion of the Series A Preferred Stock, the Sellers held, in the aggregate, approximately 96% of the issued and outstanding shares of Company capital stock on a fully diluted basis.

The Share Exchange was treated as a recapitalization and reverse acquisition for financial reporting purposes, and Bitech Mining is considered the acquirer for accounting purposes. As a result of the Share Exchange and the change in our business and operations, a discussion of the past financial results of our predecessor, Spine Injury Solutions Inc., is not pertinent, and under applicable accounting principles, the historical financial results of Bitech Mining, the accounting acquirer, prior to the Share Exchange are considered our historical financial results.

Prior to March 31, 2022, we were engaged in the business of owning, developing and leasing the Quad Video Halo video recording system (“QVH”) used to record medical procedures including the collection of accounts receivables related to previously provided spine injury diagnostic services (collectively, the “QVH Business”). On June 30, 2022, we sold the assets related to the QVH Business.

| 18 |

BITECH TECHNOLOGIES CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 2. CRITICAL ACCOUNTING POLICIES

The following are summarized accounting policies considered to be critical by our management:

Going Concern

Since our inception, our expenses substantially exceeded our revenue, resulting in continuing losses and an accumulated deficit of $1,096,594 as of December 31, 2022. Presently, we are trying to limit all operating expenses as much as possible. If in the future we decide to increase our service development, marketing efforts and/or brand building activities, we will need to increase our operating expenses and our general and administrative functions to support such growth in operations. No such growth in operations is presently planned. We are also actively seeking a private company with which to enter into a strategic business transaction, including without limitation a merger; however, we cannot predict the ultimate outcome of our efforts. Our continued existence is dependent upon our ability to successfully merge with a financially viable company, or our ability to obtain additional capital from borrowing and/or selling securities, as needed, to fund our operations. There is no assurance that additional capital can be obtained or that it can be obtained on terms that are favorable to us and our existing stockholders. Any expectation of future profitability is likely dependent upon our ability to successfully merge with another company, of which there can be no assurances.

We were not involved in any procedures in 2022 and have no plans to do so in the future. The previous service revenues earned has resulted in longer settlement times, which has created a slowdown in cash collections.

Basis of Consolidation

The accompanying consolidated financial statements include the accounts of Bitech Technologies Corporation. and its wholly owned subsidiary, Quad Video Halo, Inc. All material intercompany transactions have been eliminated upon consolidation.

Revenue recognition

The Company adopted Accounting Standards Codification (“ASC”) 606. ASC 606, Revenue from Contracts with Customers, establishes principles for reporting information about the nature, amount, timing and uncertainty of revenue and cash flows arising from the entity’s contracts to provide goods or services to customers. The core principle requires an entity to recognize revenue to depict the transfer of goods or services to customers in an amount that reflects the consideration that it expects to be entitled to receive in exchange for those goods or services recognized as performance obligations are satisfied.

The Company has assessed the impact of the guidance by performing the following five steps analysis:

Step 1: Identify the contract

Step 2: Identify the performance obligations

Step 3: Determine the transaction price

Step 4: Allocate the transaction price

Step 5: Recognize revenue

Substantially all of the Company’s revenue is derived from leasing equipment. The Company considers a signed lease agreement to be a contract with a customer. Contracts with customers are considered to be short-term when the time between signed agreements and satisfaction of the performance obligations is equal to or less than one year, and virtually all of the Company’s contracts are short-term. The Company recognizes revenue when services are provided to customers in an amount that reflects the consideration to which the Company expects to be entitled in exchange for those services. The Company typically satisfies its performance obligations in contracts with customers upon delivery of the services. The Company does not have any contract assets since the Company has an unconditional right to consideration when the Company has satisfied its performance obligation and payment from customers is not contingent on a future event. Generally, payment is due from customers immediately at the invoice date, and the contracts do not have significant financing components nor variable consideration. There are no returns and there is no allowances. All of the Company’s contracts have a single performance obligation satisfied at a point in time and the transaction price is stated in the contract, usually as a price per unit. All estimates are based on the Company’s historical experience, complete satisfaction of the performance obligation, and the Company’s best judgment at the time the estimate is made.

| 19 |

BITECH TECHNOLOGIES CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Fair Value of Financial Instruments

Cash, accounts receivable, accounts payable, accrued liabilities and notes payable as reflected in the consolidated financial statements, approximates fair value. Fair value estimates are made at a specific point in time, based on relevant market information and information about the financial instrument. These estimates are subjective in nature and involve uncertainties and matters of significant judgment and therefore cannot be determined with precision. Changes in assumptions could significantly affect the estimates.

Cash and Cash Equivalents

Cash and cash equivalents consist of liquid investments with original maturities of three months or less. Cash equivalents are stated at cost, which approximates fair value. We maintain cash and cash equivalents in banks which at times may exceed federally insured limits. We have not experienced any losses on these deposits.

Property and Equipment

Property and equipment are carried at cost. When retired or otherwise disposed of, the related carrying cost and accumulated depreciation are removed from the respective accounts, and the net difference, less any amount realized from the disposition, is recorded in operations. Maintenance and repairs are charged to operating expenses as incurred. Costs of significant improvements and renewals are capitalized.

Property and equipment consist of computers and equipment and are depreciated over their estimated useful lives of three years, using the straight-line method.

Long-Lived Assets

We periodically review and evaluate long-lived assets when events and circumstances indicate that the carrying amount of these assets may not be recoverable. In performing our review for recoverability, we estimate the future cash flows expected to result from the use of such assets and its eventual disposition. If the sum of the expected undiscounted future operating cash flows is less than the carrying amount of the related assets, an impairment loss is recognized in the consolidated statements of operations. Measurement of the impairment loss is based on the excess of the carrying amount of such assets over the fair value calculated using discounted expected future cash flows.

Concentrations of Credit Risk

Assets that expose us to credit risk consist primarily of cash and accounts receivable. Our accounts receivable arise from a diversified customer base and, therefore, we believe the concentration of credit risk is minimal. We evaluate the creditworthiness of customers before any services are provided. We record a discount based on the nature of our business, collection trends, and an assessment of our ability to fully realize amounts billed for services. We have no accounts receivable to warrant any allowance at December 31, 2022 or December 31, 2021.

| 20 |

BITECH TECHNOLOGIES CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Stock Based Compensation