UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-K

| x | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2012, or

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from ............... to ...............

Commission file number 0-9068

WEYCO GROUP, INC.

(Exact name of registrant as specified in its charter)

| Wisconsin | 39-0702200 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

333 W. Estabrook Boulevard, P. O. Box 1188, Milwaukee, WI 53201

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, include area code: (414) 908-1600

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock - $1.00 par value per share | The NASDAQ Stock Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulations S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes ¨ No x

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant as of the close of business on June 29, 2012 was $153,484,000. This was based on the closing price of $23.18 per share as reported by NASDAQ on June 29, 2012, the last business day of the registrant’s most recently completed second fiscal quarter.

As of March 1, 2013, there were 10,783,805 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for its Annual Meeting of Shareholders scheduled for May 7, 2013, are incorporated by reference in Part III of this report.

WEYCO GROUP, INC.

Table of Contents to Annual Report on Form 10-K

Year Ended December 31, 2012

| Page | |||

| CAUTIONARY STATEMENTS FOR FORWARD-LOOKING INFORMATION | 4 | ||

| PART I. | |||

| ITEM 1. | BUSINESS | 5 | |

| ITEM 1A. | RISK FACTORS | 6 | |

| ITEM 1B. | UNRESOLVED STAFF COMMENTS | 9 | |

| ITEM 2. | PROPERTIES | 10 | |

| ITEM 3. | LEGAL PROCEEDINGS | 10 | |

| ITEM 4. | MINE SAFETY DISCLOSURES | 10 | |

| EXECUTIVE OFFICERS OF THE REGISTRANT | 11 | ||

| PART II. | |||

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER | ||

| MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 12 | ||

| ITEM 6. | SELECTED FINANCIAL DATA | 13 | |

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 14 | |

| ITEM 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 24 | |

| ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 25 | |

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 54 | |

| ITEM 9A. | CONTROLS AND PROCEDURES | 54 | |

| ITEM 9B. | OTHER INFORMATION | 54 | |

| PART III. | |||

| ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 55 | |

| ITEM 11. | EXECUTIVE COMPENSATION | 55 | |

| ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 55 | |

| ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 55 | |

| ITEM 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES | 55 | |

| PART IV. | |||

| ITEM 15. | EXHIBITS, FINANCIAL STATEMENT SCHEDULES | 56 |

| 2 |

[This page intentionally left blank.]

| 3 |

CAUTIONARY STATEMENTS FOR FORWARD-LOOKING INFORMATION

This report contains certain forward-looking statements with respect to the Company’s outlook for the future. These statements represent the Company's reasonable judgment with respect to future events and are subject to risks and uncertainties that could cause actual results to differ materially. The reader is cautioned that these forward-looking statements are subject to a number of risks, uncertainties, or other factors that may cause actual results to differ materially from those described in the forward-looking statements. These risks and uncertainties include, but are not limited to, the risk factors described under Item 1A, “Risk Factors.”

| 4 |

PART 1

| ITEM 1 | BUSINESS |

The Company is a Wisconsin corporation incorporated in the year 1906 as Weyenberg Shoe Manufacturing Company. Effective April 25, 1990, the name of the corporation was changed to Weyco Group, Inc.

Weyco Group, Inc. and its subsidiaries (the “Company”) engage in one line of business, the distribution of quality and innovative footwear. The Company designs and markets footwear principally for men, but also for women and children, under a portfolio of well-recognized brand names including: “Florsheim,” “Nunn Bush,” “Stacy Adams,” “BOGS,” “Rafters,” and “Umi.” The Company also has other brands, including “Brass Boot”, which is included within Nunn Bush sales figures, and “Florsheim by Duckie Brown” which is included within Florsheim sales figures. Trademarks maintained by the Company on these brands are important to the business. The Company’s products consist primarily of mid-priced leather dress shoes and casual footwear of man-made materials or leather. In addition, the Company added outdoor boots, shoes and sandals in 2011 with the acquisition of the BOGS and Rafters brands. The Company’s footwear is available in a broad range of sizes and widths, primarily purchased to meet the needs and desires of the general American population.

The Company purchases finished shoes from outside suppliers, primarily located in China and India. Almost all of these foreign-sourced purchases are denominated in U.S. dollars. Historically, there have been few inflationary pressures in the shoe industry and leather and other component prices have been stable. However, since 2007 there have been upward cost pressures from the Company’s suppliers, related to a variety of factors, including higher labor, materials and freight costs and changes in the strength of the U.S. dollar. The Company has worked to increase its selling prices to offset the effect of these increases.

The Company’s business is separated into two reportable segments – the North American wholesale segment (“wholesale”) and the North American retail segment (“retail”). The Company also has other wholesale and retail businesses overseas which include its businesses in Australia, South Africa and Asia Pacific (collectively, “Florsheim Australia”) and its wholesale and retail businesses in Europe.

In 2012, 2011 and 2010, sales of the North American wholesale segment, which include both wholesale sales and licensing revenues, constituted approximately 74%, 74% and 72% of total sales, respectively. At wholesale, shoes are marketed throughout the United States and Canada in more than 10,000 shoe, clothing and department stores. In 2012 and 2011, there were no single customers with sales above 10% of the Company’s total sales. In 2010, sales to the Company’s largest customer, JCPenney, were 12% of total sales. The Company employs traveling salespeople who sell the Company’s products to retail outlets. Shoes are shipped to these retailers primarily from the Company’s distribution center in Glendale, Wisconsin. In the men’s footwear business, there is generally no identifiable seasonality, although new styles are historically developed and shown twice each year, in spring and fall. With BOGS, there is some seasonality in its business due to the nature of the product; the majority of BOGS sales occur in the third and fourth quarters. Consistent with industry practices, the Company carries significant amounts of inventory to meet customer delivery requirements and periodically provides extended payment terms to customers. As of December 31, 2012, the Company had licensing agreements with third parties who sell its branded shoes outside of the United States, as well as licensing agreements with specialty shoe, apparel and accessory manufacturers in the United States.

In 2012, 2011 and 2010, sales of the North American retail segment constituted approximately 8%, 9% and 10% of total sales, respectively. As of December 31, 2012, the retail segment consisted of 23 company-operated stores in the United States and an Internet business. Sales in retail stores are made directly to the consumer by Company employees. In addition to the sale of the Company’s brands of footwear in these retail stores, other branded footwear and accessories are also sold in order to provide the consumer with a more complete selection.

Sales of the Company’s other businesses represented 18%, 17% and 18% of total sales in 2012, 2011, and 2010, respectively. These sales relate to the Company’s wholesale and retail operations in Australia, South Africa, Asia Pacific and Europe.

| 5 |

As of December 31, 2012, the Company had a backlog of $42 million of orders compared with $40 million as of December 31, 2011. This does not include unconfirmed blanket orders from customers, which account for the majority of the Company’s orders, particularly from its larger accounts. All orders are expected to be filled within one year.

As of December 31, 2012, the Company employed 633 persons, of whom 33 were members of collective bargaining units. Future wage and benefit increases under the collective bargaining contracts are not expected to have a significant impact on the future operations or financial position of the Company.

Price, quality, service and brand recognition are all important competitive factors in the shoe industry. The Company has a design department that continually reviews and updates product designs. Compliance with environmental regulations historically has not had, and is not expected to have, a material adverse effect on the Company’s results of operations, financial position or cash flows, although there can be no assurances.

The Company makes available, free of charge, copies of its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports upon written or telephone request. Investors can also access these reports through the Company’s website, www.weycogroup.com, as soon as reasonably practical after the Company files or furnishes those reports to the Securities and Exchange Commission (“SEC”). The information on the Company’s website is not a part of this filing. Also available on the Company’s website are various documents relating to the corporate governance of the Company, including its Code of Ethics.

| ITEM 1A | RISK FACTORS |

There are various factors that affect the Company’s business, results of operations and financial condition, many of which are beyond the Company’s control. The following is a description of some of the significant factors that might materially and adversely affect the Company’s business, results of operations and financial condition.

Changes in the U.S. and global economy may adversely affect the Company.

Spending patterns in the footwear market, particularly those in the moderate-priced market in which a good portion of the Company’s products compete, have historically been impacted by consumers’ disposable income. As a result, the success of the Company is impacted by changes in general economic conditions, especially in the United States. Factors affecting discretionary income for the moderate consumer include, among others, general business conditions, gas and energy costs, employment, consumer confidence, interest rates and taxation. Additionally, the economy and consumer behavior can impact the financial strength and buying patterns of retailers, which can also affect the Company’s results. Continued volatile, unstable or weak economic conditions, or a worsening of conditions, could adversely affect the Company’s sales volume and overall performance.

Changes in the U.S. and global credit markets could adversely affect the Company’s business.

U.S. and global financial markets recently have been, and continue to be, unstable and unpredictable, which has generally resulted in a tightening in the credit markets with heightened lending standards and terms. This volatility and instability in the credit markets pose various risks to the Company, including, among others, negatively impacting retailer and consumer confidence, limiting the Company’s customers’ access to credit markets and interfering with the normal commercial relationships between the Company and its customers. Increased credit risks associated with the financial condition of some customers in the retail industry affects their level of purchases from the Company and the collectability of amounts owed to the Company, and in some cases, causes the Company to reduce or cease shipments to certain customers who no longer meet the Company’s credit requirements.

In addition, weak economic conditions and unstable and volatile financial markets could lead to certain of the Company’s customers experiencing cash flow problems, which may force them into higher default rates or to file for bankruptcy protection which may increase the Company’s bad debt expense or further negatively impact the Company’s business.

| 6 |

The Company is subject to risks related to the retail environment that could adversely impact the Company’s business.

The Company is subject to risks associated with doing business in the retail environment, primarily in the United States. The U.S. retail industry has experienced a growing trend toward consolidation of large retailers. The merger of major retailers could result in the Company losing sales volume or increasing its concentration of business with a few large accounts, resulting in reduced bargaining power on the part of the Company, which could increase pricing pressures and lower the Company’s margins.

Changes in consumer preferences could negatively impact the Company.

The Company’s success is dependent upon its ability to accurately anticipate and respond to rapidly changing fashion trends and consumer preferences. Failure to predict or respond to current trends or preferences could have an adverse impact on the Company’s sales volume and overall performance.

The Company relies on independent foreign sources of production and the availability of leather, rubber and other raw materials which could have unfavorable effects on the Company’s business.

The Company purchases its products entirely from independent foreign manufacturers, primarily in China and India. Although the Company has good working relationships with its manufacturers, the Company does not have long-term contracts with them. Thus, the Company could experience increases in manufacturing costs, disruptions in the timely supply of products or unanticipated reductions in manufacturing capacity, any of which could negatively impact the Company’s business, results of operations and financial condition. The Company has the ability to move product to different suppliers; however, the transition may not occur smoothly and/or quickly and the Company could miss customer delivery date requirements and, consequently, could lose orders. Additional risks associated with foreign sourcing that could negatively impact the Company’s business include adverse changes in foreign economic conditions, import regulations, restrictions on the transfer of funds, duties, tariffs, quotas and political or labor interruptions, disruptions at U.S. or foreign ports or other transportation facilities, foreign currency fluctuations, expropriation and nationalization.

The Company’s use of foreign sources of production results in long production and delivery lead times. Therefore, the Company typically forecasts demand at least five months in advance. If the Company’s forecasts are wrong, it could result in the loss of sales if the Company does not have enough product on hand, or in reduced margins if the Company has excess inventory that needs to be sold at discounted prices.

Additionally, the Company’s products depend on the availability of raw materials, especially leather and rubber. Any significant shortages of quantities or increases in the cost of leather or rubber could have a material adverse effect on the Company’s business and results of operations.

The Company is subject to risks associated with its non-U.S. operations that could adversely affect its financial results.

As a result of the Company’s global presence, a portion of the Company’s revenues and expenses are denominated in currencies other than the U.S. dollar. The Company is therefore subject to foreign currency risks and foreign exchange exposure. The Company’s primary exposures are to the Australian dollar and the Canadian dollar. Exchange rates can be volatile and could adversely impact the Company’s financial results.

The Company operates in a highly competitive environment, which may result in lower prices and reduce its profits.

The footwear market is extremely competitive. The Company competes with manufacturers, distributors and retailers of men’s, women’s and children’s shoes, certain of which are larger and have substantially greater resources than the Company has. The Company competes with these companies primarily on the basis of price, quality, service and brand recognition, all of which are important competitive factors in the shoe industry. The Company’s ability to maintain its competitive edge depends upon these factors, as well as its ability to deliver new products at the best value for the consumer, maintain positive brand recognition, and obtain sufficient retail floor space and effective product presentation at retail. If the Company does not remain competitive, the Company’s future results of operations and financial condition could decline.

| 7 |

The Company is dependent on information and communication systems to support its business and Internet sales. Significant interruptions could disrupt its business.

The Company accepts and fills the majority of its larger customers’ orders through the use of Electronic Data Interchange (EDI). It relies on its warehouse management system to efficiently process orders. The corporate office relies on computer systems to efficiently process and record transactions. Significant interruptions in its information and communication systems from power loss, telecommunications failure or computer system failure could significantly disrupt the Company’s business and operations. In addition, the Company sells footwear on its websites, and failures of the Company’s or other retailers’ websites could adversely affect the Company’s sales and results.

The Company may not be able to successfully integrate new brands and businesses.

The Company has recently completed a number of acquisitions and intends to continue to look for new acquisition opportunities. Those search efforts could be unsuccessful and costs could be incurred in those failed efforts. Further, if and when an acquisition occurs, the Company cannot guarantee that it will be able to successfully integrate the brand into its current operations, or that any acquired brand would achieve results in line with the Company’s historical performance or its specific expectations for the brand.

Loss of the services of the Company’s top executives could adversely affect the business.

Thomas W. Florsheim, Jr., the Company’s Chairman and Chief Executive Officer, and John W. Florsheim, the Company’s President, Chief Operating Officer and Assistant Secretary, have a strong heritage within the Company and the footwear industry. They possess knowledge, relationships and reputations based on their lifetime exposure to and experience in the Company and the industry. The loss of either one or both of the Company’s top executives could have an adverse impact on the Company’s performance.

The cost to provide employee healthcare insurance and/or benefits could increase in the future

The Affordable Care Act (the “ACA”), which was adopted in 2010 and is being phased in over several years, significantly affects the provision of both healthcare services and benefits in the United States. It is possible that the ACA will negatively impact the Company’s cost of providing health insurance and/or benefits and may also impact various other aspects of the Company’s business. While the ACA did not have a material impact on the Company in 2012, 2011 or 2010, management is continuing to assess the future impact the ACA could have on the Company’s healthcare benefit costs.

The limited public float and trading volume for the Company’s stock may have an adverse impact on the stock price or make it difficult to liquidate.

The Company’s common stock is held by a relatively small number of shareholders. The Florsheim family owns over 35% of the stock and two institutional shareholders hold significant blocks. Other officers, directors, and members of management own stock or have the potential to own stock through previously granted stock options and restricted stock. Consequently, the Company has a relatively small float and low average daily trading volume, which could affect a shareholder’s ability to sell his stock or the price at which he can sell it. In addition, future sales of substantial amounts of the Company’s common stock in the public market by those larger shareholders, or the perception that these sales could occur, may adversely impact the market price of the stock and the stock could be difficult for the shareholder to liquidate.

| 8 |

The Company’s total assets include goodwill and other indefinite-lived intangible assets. If management determines these have become impaired in the future, net income could be materially adversely affected.

Goodwill represents the excess of cost over the fair market value of net assets acquired in a business combination. Indefinite-lived intangible assets are comprised of certain trademarks on the Company’s principal shoe brands. The Company’s goodwill and trademarks were approximately $46 million as of December 31, 2012, or approximately 16% of total assets.

The Company analyzes goodwill for impairment on an annual basis or more frequently when, in the judgment of management, an event has occurred that may indicate that additional analysis is required. Impairment may result from, among other things, deterioration in the Company’s performance, adverse market conditions, adverse changes in applicable laws or regulations, including changes that restrict the activities of or affect the products sold by the Company, and a variety of other factors. The amount of any quantified impairment must be expensed as a charge to results of operations in the period in which the asset becomes impaired. The Company did not record any charges for impairment of goodwill or trademarks in 2012, 2011, or 2010. Depending on future circumstances, it is possible the Company may never realize the full value of its intangible assets. Any future determination of impairment of a significant portion of goodwill or other identifiable intangible assets could have an adverse effect on the Company’s financial condition and results of operations.

If the Company is unable to maintain effective internal control over its financial reporting, investors could lose confidence in the reliability of its financial statements, which could result in a reduction in the value of its common stock.

Under Section 404 of the Sarbanes-Oxley Act, public companies must include a report of management on the Company’s internal control over financial reporting in their annual reports; that report must contain an assessment by management of the effectiveness of the Company’s internal control over financial reporting. In addition, the independent registered public accounting firm that audits a company’s financial statements must attest to and report on the effectiveness of the company’s internal control over financial reporting.

If the Company is unable to maintain effective internal control over financial reporting, including in connection with changes in accounting rules and standards that apply to it, this could lead to a failure to meet its reporting obligations to the SEC. Such a failure in turn could result in an adverse reaction to the Company in the marketplace or a loss in value of the Company’s common stock, due to a loss of confidence in the reliability of the Company's financial statements.

Natural disasters and other events outside of the Company’s control, and the ineffective management of such events, may harm the Company’s business.

The Company’s facilities and operations, as well as those of the Company’s suppliers and customers, may be impacted by natural disasters. In the event of such disasters, and if the Company or its suppliers or customers are not adequately insured, the Company’s business could be harmed due to the event itself or due to its inability to effectively manage the effects of the particular event; potential harms include the loss of business continuity, the loss of inventory or business data and damage to infrastructure, warehouses or distribution centers.

| ITEM 1B | UNRESOLVED STAFF COMMENTS |

None

| 9 |

| ITEM 2 | PROPERTIES |

The following facilities were operated by the Company or its subsidiaries as of December 31, 2012:

| Owned/ | Square | ||||||||||||

| Location | Character | Leased | Footage | % Utilized | |||||||||

| Glendale, Wisconsin (2) | Two story office and distribution center | Owned | 1,025,000 | 85 | % | ||||||||

| Portland, Oregon (2) | One story office | Leased | (1) | 4,100 | 100 | % | |||||||

| Montreal, Canada (2) | Multistory office and distribution center | Leased | (1) | 75,800 | 100 | % | |||||||

| Florence, Italy (3) | Two story office and distribution center | Leased | (1) | 15,100 | 100 | % | |||||||

| Fairfield Victoria , Australia (3) | Office and distribution center | Leased | (1) | 54,000 | 100 | % | |||||||

| Strydom Park, South Africa (3) | Distribution center - Apparel | Leased | (1) | 3,700 | 100 | % | |||||||

| Strydom Park, South Africa (3) | Distribution center - Footwear | Leased | (1) | 3,700 | 100 | % | |||||||

| Hong Kong, China (3) | Office and distribution center | Leased | (1) | 14,000 | 100 | % | |||||||

| Shenzhen, China (3) | Office | Leased | (1) | 2,600 | 100 | % | |||||||

| Donguan City, China (3) | Office | Leased | (1) | 3,000 | 100 | % | |||||||

| (1) | Not material leases. |

| (2) | These properties are used principally by the Company's North American wholesale segment. |

| (3) | These properties are used principally by the Company's other businesses which are not reportable segments. |

In addition to the above-described offices and distribution facilities, the Company also operates retail shoe stores under various rental agreements. All of these facilities are suitable and adequate for the Company’s current operations. See Note 14 of the Notes to Consolidated Financial Statements and Item 1, “Business”, above.

| ITEM 3 | LEGAL PROCEEDINGS |

None

| ITEM 4 | MINE SAFETY DISCLOSURES |

Not Applicable

| 10 |

EXECUTIVE OFFICERS OF THE REGISTRANT

The following table lists the executive officers of the Company as of March 1, 2013:

| Officer | Age | Office(s) | Executive Officer Since |

Business Experience | |||||

| Thomas W. Florsheim, Jr. (1) | 54 | Chairman and Chief Executive Officer | 1996 | Chairman and Chief Executive Officer of the Company - 2002 to present; President and Chief Executive Officer of the Company - 1999 to 2002; President and Chief Operating Officer of the Company - 1996 to 1999; Vice President of the Company - 1988 to 1996 | |||||

| John W. Florsheim (1) | 49 | President, Chief Operating Officer and Assistant Secretary | 1996 | President, Chief Operating Officer and Assistant Secretary of the Company - 2002 to present; Executive Vice President, Chief Operating Officer and Assistant Secretary of the Company - 1999 to 2002; Executive Vice President of the Company - 1996 to 1999; Vice President of the Company 1994 to 1996 | |||||

| John F. Wittkowske | 53 | Senior Vice President, Chief Financial Officer and Secretary | 1993 | Senior Vice President, Chief Financial Officer and Secretary of the Company - 2002 to present; Vice President, Chief Financial Officer and Secretary of the Company - 1995 to 2002; Secretary and Treasurer of the Company 1993 - 1995 |

| (1) | Thomas W. Florsheim, Jr. and John W. Florsheim are brothers, and Chairman Emeritus Thomas W. Florsheim is their father. |

| 11 |

PART II

| ITEM 5 | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The shares of the Company’s common stock are traded on the NASDAQ Stock Market (“NASDAQ”) under the symbol

“WEYS.”

COMMON STOCK DATA

| 2012 | 2011 | |||||||||||||||||||||||

| Cash | Cash | |||||||||||||||||||||||

| Stock Prices | Dividends | Stock Prices | Dividends | |||||||||||||||||||||

| Quarter: | High | Low | Declared | High | Low | Declared | ||||||||||||||||||

| First | $ | 27.25 | $ | 22.49 | $ | 0.16 | $ | 25.68 | $ | 22.63 | $ | 0.16 | ||||||||||||

| Second | $ | 24.71 | $ | 22.01 | $ | 0.17 | $ | 25.00 | $ | 22.25 | $ | 0.16 | ||||||||||||

| Third | $ | 24.90 | $ | 22.53 | $ | 0.17 | $ | 25.89 | $ | 20.82 | $ | 0.16 | ||||||||||||

| Fourth | $ | 25.71 | $ | 22.62 | $ | 0.34 | $ | 25.08 | $ | 20.97 | $ | 0.16 | ||||||||||||

| $ | 0.84 | $ | 0.64 | |||||||||||||||||||||

There were 159 holders of record of the Company's common stock as of March 1, 2013.

The stock prices shown above are the high and low actual trades on the NASDAQ for the calendar periods indicated.

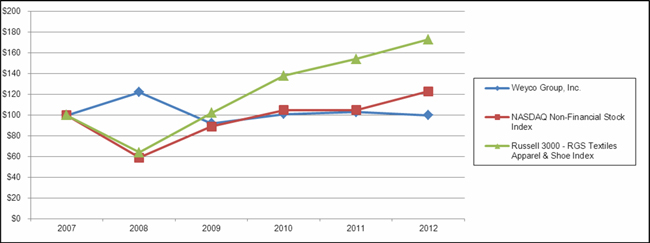

Stock Performance

The following line graph compares the cumulative total shareholder return on the Company’s common stock during the five years ended December 31, 2012 with the cumulative return on the NASDAQ Non-Financial Stock Index and the Russell 3000 - RGS Textiles Apparel & Shoe Index. The comparison assumes $100 was invested on December 31, 2007 in the Company’s common stock and in each of the foregoing indices and assumes reinvestment of dividends.

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |||||||||||||||||||

| Weyco Group, Inc. | 100 | 122 | 92 | 101 | 103 | 100 | ||||||||||||||||||

| NASDAQ Non-Financial Stock Index | 100 | 59 | 89 | 105 | 105 | 123 | ||||||||||||||||||

| Russell 3000 - RGS Textiles Apparel & Shoe Index | 100 | 64 | 102 | 138 | 154 | 173 | ||||||||||||||||||

| 12 |

In April 1998, the Company’s Board of Directors first authorized a stock repurchase program to repurchase 1,500,000 shares of its common stock in open market transactions at prevailing prices. In April 2000 and again in May 2001, the Company’s Board of Directors extended the stock repurchase program to cover the repurchase of 1,500,000 additional shares. In February 2009, the Board of Directors extended the stock repurchase program to cover the repurchase of 1,000,000 additional shares, bringing the total authorized since inception to 5,500,000. The table below presents information pursuant to Item 703 of Regulation S-K regarding the repurchase of the Company’s common stock by the Company in the three-month period ended December 31, 2012.

| Maximum Number | ||||||||||||||||

| Total | Average | Total Number of | of Shares | |||||||||||||

| Number | Price | Shares Purchased as | that May Yet Be | |||||||||||||

| of Shares | Paid | Part of the Publicly | Purchased Under | |||||||||||||

| Period | Purchased | Per Share | Announced Program | the Program | ||||||||||||

| 10/01/2012 - 10/31/2012 | - | $ | - | - | 861,569 | |||||||||||

| 11/01/2012 - 11/30/2012 | 30,382 | $ | 23.00 | 30,382 | 831,187 | |||||||||||

| 12/01/2012 - 12/31/2012 | 7,662 | $ | 22.96 | 7,662 | 823,525 | |||||||||||

| Total | 38,044 | $ | 22.99 | 38,044 | ||||||||||||

| ITEM 6 | SELECTED FINANCIAL DATA |

The following selected financial data reflects the results of operations, balance sheet data and common share information for the years ended December 31, 2008 through December 31, 2012.

| Years Ended December 31, | ||||||||||||||||||||

| (in thousands, except per share amounts) | ||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| Net Sales | $ | 293,471 | $ | 271,100 | $ | 229,231 | $ | 225,305 | $ | 221,432 | ||||||||||

| Net earnings attributable to Weyco Group, Inc. | $ | 18,957 | $ | 15,251 | $ | 13,668 | $ | 12,821 | $ | 17,025 | ||||||||||

| Diluted earnings per share | $ | 1.73 | $ | 1.37 | $ | 1.19 | $ | 1.11 | $ | 1.45 | ||||||||||

| Weighted average diluted shares outstanding | 10,950 | 11,159 | 11,493 | 11,510 | 11,757 | |||||||||||||||

| Cash dividends per share | $ | 0.84 | $ | 0.64 | $ | 0.63 | $ | 0.59 | $ | 0.53 | ||||||||||

| Total assets | $ | 285,321 | $ | 273,508 | $ | 223,435 | $ | 207,153 | $ | 190,640 | ||||||||||

| Bank borrowings | $ | 45,000 | $ | 37,000 | $ | 5,000 | $ | - | $ | 1,250 | ||||||||||

| 13 |

| ITEM 7 | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

GENERAL

The Company designs and markets quality and innovative footwear for men, women and children under a portfolio of well-recognized brand names including: “Florsheim,” “Nunn Bush,” “Stacy Adams,” “BOGS,” “Rafters,” and “Umi.” Inventory is purchased from third-party overseas manufacturers. The majority of foreign-sourced purchases are denominated in U.S. dollars. The Company has two reportable segments, North American wholesale operations (“wholesale”) and North American retail operations (“retail”). In the wholesale segment, the Company’s products are sold to leading footwear, department and specialty stores, primarily in the United States and Canada. As of December 31, 2012, the Company also had licensing agreements with third parties who sell its branded apparel, accessories and specialty footwear in the United States, as well as its footwear in Mexico and certain markets overseas. Licensing revenues are included in the Company’s wholesale segment. The Company’s retail segment consisted of 23 Company-owned retail stores in the United States and an Internet business as of December 31, 2012. Sales in retail outlets are made directly to consumers by Company employees. The Company’s “other” operations include the Company’s wholesale and retail businesses in Australia, South Africa and Asia Pacific (collectively, “Florsheim Australia”) and Europe. The majority of the Company’s operations are in the United States, and its results are primarily affected by the economic conditions and the retail environment in the United States.

This discussion summarizes the significant factors affecting the consolidated operating results, financial position and liquidity of the Company for the three-year period ended December 31, 2012. This discussion should be read in conjunction with Item 8, “Financial Statements and Supplementary Data” below.

EXECUTIVE OVERVIEW

Sales and Earnings Highlights

Consolidated net sales in 2012 were $293.5 million, up 8% over last year’s net sales of $271.1 million. Operating earnings were $29.8 million this year, up from $23.2 million in 2011. Consolidated net earnings attributable to Weyco Group, Inc. were $19.0 million in 2012 compared with $15.3 million last year. Diluted earnings per share for the year ended December 31, 2012 were $1.73 per share, up from $1.37 per share in 2011. Earnings for the year included $3.4 million ($2.1 million after tax, or $0.19 per share) of income resulting from a reduction in the estimated liability for future payments to be made as a result of the 2011 acquisition of Bogs.

The majority of the Company’s operations are in its North American wholesale segment, and its consolidated results primarily reflect the results of that business. North American wholesale net sales increased $18.8 million in 2012 compared to 2011. This increase was primarily due to higher sales volumes across all of the Company’s wholesale brands, which included increased Bogs sales volumes due to the takeover of Bogs distribution in Canada during 2012. The 2011 acquisition of Bogs also contributed to the wholesale sales increase, as 2012 net sales included twelve months of Bogs sales while 2011 net sales only included ten months of Bogs sales, based on the March 2, 2011 acquisition date.

The Company’s North American wholesale segment operating earnings increased $6.6 million in 2012 compared to 2011. The increase in operating earnings was due to higher sales volumes as well as an adjustment to reduce the estimated liability for future payments due to the former owners of the BOGS and Rafters brands. See Note 11.

| 14 |

Financial Position Highlights

At December 31, 2012, cash and marketable securities totaled $61.5 million and outstanding debt totaled $45.0 million. At December 31, 2011, cash and marketable securities totaled $61.9 million and outstanding debt totaled $37.0 million. The Company’s main sources of cash in 2012 were from operations, the maturities of marketable securities, and borrowings under the revolving line of credit. The Company’s main uses of cash in 2012 were for the payment of dividends, common stock repurchases, and the payment of an indemnification holdback to the former shareholders of Bogs. The Company also had increased capital expenditures in 2012 due to construction to connect a new building that was acquired in 2011 to the Company’s Glendale, Wisconsin distribution center.

Recent Acquisitions

Bogs

On March 2, 2011, the Company acquired 100% of the outstanding shares of The Combs Company (“Bogs”) from its former shareholders for $29.3 million in cash plus assumed debt of approximately $3.8 million and contingent payments after two and five years (in 2013 and 2016), which are dependent on Bogs achieving certain performance measures. In accordance with the agreement, $2.0 million of the cash portion of the purchase price was held back to be used to help satisfy any claims of indemnification by the Company, and any amounts not used therefore were to be paid to the seller 18 months from the date of acquisition. This holdback was paid in full to the former shareholders of Bogs in 2012. At the acquisition date, the Company’s estimate of the fair value of the contingent payments was approximately $9.8 million in aggregate. At December 31, 2012, the Company’s estimate of the fair value of the contingent payments was approximately $6.3 million in aggregate. The change in fair value was recognized in earnings. See Note 11 in the Notes to Consolidated Financial Statements.

Bogs operations have been consolidated into the Company’s wholesale segment since the date of acquisition. Accordingly, the Company’s 2012 results included Bogs operations for the entire year while 2011 only included Bogs operations from March 2 through December 31, 2011. Bogs net sales were $36.4 million in 2012 compared to $28.0 million in 2011. See Note 3 in the Notes to Consolidated Financial Statements.

On June 1, 2012, the Company took over the sales and distribution of the BOGS and Rafters brands in Canada from a third-party licensee. Consequently, Bogs wholesale net sales increased and its licensing revenues decreased in 2012.

Umi

On April 28, 2010, the Company acquired certain assets, including the Umi brand name, intellectual property and accounts receivable from Umi LLC (“Umi”), a children’s footwear company, for an aggregate price of approximately $2.6 million. The operating results of Umi have been consolidated into the Company’s wholesale segment since the date of acquisition. Accordingly, the Company’s 2012 and 2011 results included Umi’s operations for the entire year while 2010 only included Umi’s operations from April 28 through December 31, 2010. See Note 3 in the Notes to Consolidated Financial Statements.

| 15 |

2012 vs. 2011

SEGMENT ANALYSIS

Net sales and earnings from operations for the Company’s segments, as well as its “other” operations, in the years ended December 31, 2012 and 2011 were as follows:

| Years ended December 31, | ||||||||||||

| 2012 | 2011 | % Change | ||||||||||

| (Dollars in thousands) | ||||||||||||

| Net Sales | ||||||||||||

| North American Wholesale | $ | 217,908 | $ | 199,087 | 9 | % | ||||||

| North American Retail | 24,348 | 24,740 | -2 | % | ||||||||

| Other | 51,215 | 47,273 | 8 | % | ||||||||

| Total | $ | 293,471 | $ | 271,100 | 8 | % | ||||||

| Earnings from Operations | ||||||||||||

| North American Wholesale | $ | 22,214 | $ | 15,673 | 42 | % | ||||||

| North American Retail | 1,662 | 1,554 | 7 | % | ||||||||

| Other | 5,920 | 5,970 | -1 | % | ||||||||

| Total | $ | 29,796 | $ | 23,197 | 28 | % | ||||||

North American Wholesale Segment

Net Sales

Net sales in the Company’s North American wholesale segment for the years ended December 31, 2012 and 2011 were as follows:

| Years ended December 31, | ||||||||||||

| 2012 | 2011 | % Change | ||||||||||

| (Dollars in thousands) | ||||||||||||

| North American Net Sales | ||||||||||||

| Stacy Adams | $ | 59,217 | $ | 53,904 | 10 | % | ||||||

| Nunn Bush | 64,325 | 63,619 | 1 | % | ||||||||

| Florsheim | 50,055 | 46,344 | 8 | % | ||||||||

| BOGS/Rafters | 36,428 | 27,959 | 30 | % | ||||||||

| Umi | 4,543 | 3,812 | 19 | % | ||||||||

| Total North American Wholesale | $ | 214,568 | $ | 195,638 | 10 | % | ||||||

| Licensing | 3,340 | 3,449 | -3 | % | ||||||||

| Total North American Wholesale Segment | $ | 217,908 | $ | 199,087 | 9 | % | ||||||

The Company’s Stacy Adams and Florsheim brands both had solid sales growth during 2012 with department and chain stores, and Internet and mail order retailers. Nunn Bush net sales were up slightly in 2012. Net sales of the BOGS and Rafters brands increased $8.5 million due mainly to the takeover by the Company of the Canadian distribution of the brands in 2012. Bogs sales in Canada were $6.9 million in 2012. Bogs also had increased sales in the United States due to twelve months of sales in 2012 compared to ten months in 2011 due to the March 2011 acquisition of the brands.

Licensing revenues were down slightly in 2012 as compared to 2011. This resulted from decreased Bogs licensing revenues offset by increased Florsheim revenues. Bogs licensing revenues decreased in 2012 due to the takeover by the Company of the distribution of the BOGS and Rafters brands in Canada, which had previously been licensed to a third party. Florsheim licensing revenues increased due the collection of past due licensing revenues from the Company’s Mexican licensee of amounts that had previously been reserved for.

| 16 |

Earnings from Operations

Earnings from operations in the North American wholesale segment were $22.2 million in 2012 compared with $15.7 million in 2011. The 2012 reduction in the estimated liability for future payments to be made as a result of the Bogs acquisition caused $3.4 million of the increase. The remainder of the increase was achieved through higher sales volumes across all wholesale brands as well as slightly higher gross margins as a percent of net sales, partially offset by higher selling and administrative costs related to the Canadian distribution of Bogs as well as higher pension and advertising expenses in 2012. Wholesale gross earnings were 32.2% of net sales in 2012 compared to 31.8% in 2011.

The Company’s cost of sales does not include distribution costs (e.g., receiving, inspection or warehousing costs). The Company’s distribution costs were $10.0 million and $8.6 million in the years ended December 31, 2012 and 2011, respectively. These costs were included in selling and administrative expenses. The Company’s gross earnings may not be comparable to other companies, as some companies may include distribution costs in cost of sales.

North American wholesale segment selling and administrative expenses include, and are primarily related to, distribution costs, salaries and commissions, advertising costs, employee benefit costs and depreciation. As a percent of net sales, wholesale selling and administrative expenses were 22% this year compared to 24% in 2011. The decrease in selling and administrative expenses as a percent of net sales was largely due to the impact of the $3.4 million of income from the reduction of the estimated liability for future payments due to the former owners of the BOGS and Rafters brands. The reduction of this liability was primarily due to a decrease in the Company’s estimate of the 2013 contingent payment which was based on 2011 and 2012 gross margin dollars. The Company lowered its estimate of 2012 gross margin dollars relative to its original projections, primarily because sales of Bogs products were less than expected due to the mild winters experienced in the United States since the brands were acquired.

North American Retail Segment

Net Sales

Net sales in the Company’s North American retail segment decreased $392,000 or 2% in 2012 compared to 2011. There were seven fewer stores at December 31, 2012 than at December 31, 2011, as the Company has been closing unprofitable stores. Same store sales, which include retail store sales and Internet sales, were up 8% in 2012. Stores are included in same store sales beginning in the store’s 13th month of operations after its grand opening. The increase in same store sales was driven in part by increases in the Company’s Internet business.

Earnings from Operations

Retail earnings from operations increased $108,000 in 2012 compared to 2011. Gross earnings as a percent of net sales were 64% in 2012 and 2011. Selling and administrative expenses for the retail segment decreased in 2012 and were primarily related to rent and occupancy costs, employee costs and depreciation. Selling and administrative expenses as a percent of net sales were 57.6% in 2012 and 58.1% in 2011.

The Company reviews its long-lived assets for impairment in accordance with Accounting Standards Codification (ASC) 360, Property Plant and Equipment (“ASC 360”). See Note 2 in the Notes to Consolidated Financial Statements for further information. In 2012 and 2011, impairment charges of $93,000 and $165,000, respectively, were recognized within selling and administrative expenses to write down the fixed assets of certain retail locations that were unprofitable. Those locations have closed or are slated to close when their respective lease terms expire. In 2012, seven retail locations closed and in 2011, five locations closed. In general, earnings from operations for the retail segment have improved as fixed assets have been written down and underperforming stores have closed. In 2013, the Company expects to close three more locations.

Other

The Company’s other businesses include its wholesale and retail operations in Australia, South Africa, Asia Pacific and Europe. In 2012, net sales of the Company’s other businesses were $51 million, compared with $47 million in 2011. The majority of the increase was at Florsheim Australia, whose wholesale and retail net sales both increased 12%, or $4.7 million collectively. Earnings from operations in the Company’s other businesses were flat.

| 17 |

Other income and expense and taxes

The majority of the Company’s interest income is from its investments in marketable securities. Interest income for 2012 was down approximately $380,000 compared with 2011, primarily due to lower average investment balances this year compared with last year.

Interest expense was $561,000 in 2012 compared with $611,000 in 2011.

The effective tax rate for 2012 was 34.1% compared with 34.3% in 2011.

2011 vs. 2010

SEGMENT ANALYSIS

Net sales and earnings from operations for the Company’s segments, as well as its “other” operations, in the years ended December 31, 2011 and 2010 were as follows:

| Years ended December 31, | ||||||||||||

| 2011 | 2010 | % Change | ||||||||||

| (Dollars in thousands) | ||||||||||||

| Net Sales | ||||||||||||

| North American Wholesale | $ | 199,087 | $ | 166,021 | 20 | % | ||||||

| North American Retail | 24,740 | 22,497 | 10 | % | ||||||||

| Other | 47,273 | 40,713 | 16 | % | ||||||||

| Total | $ | 271,100 | $ | 229,231 | 18 | % | ||||||

| Earnings from Operations | ||||||||||||

| North American Wholesale | $ | 15,673 | $ | 15,742 | 0 | % | ||||||

| North American Retail | 1,554 | (400 | ) | 488 | % | |||||||

| Other | 5,970 | 3,439 | 74 | % | ||||||||

| Total | $ | 23,197 | $ | 18,781 | 24 | % | ||||||

| 18 |

North American Wholesale Segment

Net Sales

Net sales in the Company’s North American wholesale segment for the years ended December 31, 2011 and 2010 were as follows:

| Years ended December 31, | ||||||||||||

| 2011 | 2010 | % Change | ||||||||||

| (Dollars in thousands) | ||||||||||||

| North American Net Sales | ||||||||||||

| Stacy Adams | $ | 53,904 | $ | 53,392 | 1 | % | ||||||

| Nunn Bush | 63,619 | 63,401 | 0 | % | ||||||||

| Florsheim | 46,344 | 45,883 | 1 | % | ||||||||

| BOGS/Rafters | 27,959 | - | n/a | |||||||||

| Umi | 3,812 | 1,167 | 227 | % | ||||||||

| Total North American Wholesale | $ | 195,638 | $ | 163,843 | 19 | % | ||||||

| Licensing | 3,449 | 2,178 | 58 | % | ||||||||

| Total North American Wholesale Segment | $ | 199,087 | $ | 166,021 | 20 | % | ||||||

Net sales of Stacy Adams and Florsheim grew 1% in 2011 due to slightly higher sales volumes across several trade channels. Nunn Bush net sales remained flat in 2011. Net sales for the BOGS/Rafters brands were $28 million in 2011, following the acquisition of Bogs on March 2, 2011 (see Note 3 of the Notes to Consolidated Financial Statements). Umi was acquired on April 28, 2010. Accordingly, the Company’s 2011 results included Umi’s operations from January 1 through December 31, 2011, while 2010 only included Umi’s operations for the period April 28 through December 31, 2010.

In 2011 and 2010, licensing revenues consisted of royalties earned on sales of branded apparel, accessories and specialty footwear in the United States and on branded footwear in Canada, Mexico and certain overseas markets. In 2011, the Company’s licensing revenues increased 58%, primarily due to the addition of Bogs which contributed $1.2 million in new licensing revenues during the period.

Earnings from Operations

Earnings from operations in the North American wholesale segment were $15.7 million in each of the years 2011 and 2010. Higher net sales in 2011 were offset by slightly lower gross margins and increased selling and administrative costs, which included nonrecurring acquisition and transition costs related to the Bogs acquisition as well as other increased operating costs.

Wholesale gross earnings as a percent of net sales were 31.8% in 2011 compared with 32.5% in 2010. The decrease was due to increased pricing from the Company’s third-party overseas factories resulting primarily from higher labor and material costs.

The Company’s cost of sales does not include distribution costs (e.g., receiving, inspection or warehousing costs). The Company’s distribution costs were $8.6 million and $7.9 million in the years ended December 31, 2011 and 2010, respectively. These costs were included in selling and administrative expenses. The Company’s gross earnings may not be comparable to other companies, as some companies may include distribution costs in cost of sales.

North American wholesale segment selling and administrative expenses include, and are primarily related to, distribution costs, salaries and commissions, advertising costs, employee benefit costs and depreciation. Wholesale selling and administrative expenses were up approximately $9.4 million in 2011 compared with 2010. As a percent of wholesale net sales, wholesale selling and administrative expenses were 24% in 2011 compared with 23% in 2010.

North American Retail Segment

Net Sales

In the North American retail segment, net sales in 2011 were $24.7 million, up 10% from $22.5 million in 2010. There were five fewer stores in 2011 compared with 2010. Same store sales, which include the Company’s retail store sales and the Company’s Internet sales, were up 18%. Stores are included in same store sales beginning in the store’s 13th month of operations after its grand opening.

| 19 |

Earnings from Operations

Earnings from operations in the North American retail segment increased $1.9 million in 2011 compared to 2010. The increase was primarily due to higher sales volumes in the Company’s Internet business and across the majority of the retail locations and improvement in same store performance as well as the closing of five underperforming stores during 2011. Gross earnings as a percent of net sales in the retail segment were flat at 64% in 2011 and 2010.

Retail selling and administrative expenses were down approximately $497,000 in 2011 compared with 2010. As a percent of net retail sales, retail selling and administrative expenses were 58% in 2011 compared with 66% in 2010. In 2011 and 2010, impairment charges of $165,000 and $310,000 respectively, were recognized within selling and administrative expenses to write down the fixed assets of certain retail locations that were deemed unprofitable. Those locations have closed or are slated to close when their respective lease terms expire. In 2011, five retail locations closed and in 2010, one location closed. In general, earnings from operations for the retail segment improved as fixed assets were written down and underperforming stores were closed.

Other

In 2011, net sales of the Company’s other operations were $47 million, compared with $41 million in 2010. The majority of the increase was at Florsheim Australia, whose net sales increased $6.5 million, or 20%. In local currency, Florsheim Australia’s sales increased 7%, and the weaker U.S. dollar in 2011 relative to the Australian dollar caused the rest of the sales increase. Earnings from operations in the Company’s other businesses in 2011 were up $2.5 million, due mainly to Florsheim Australia’s increased retail sales and gross earnings as a percent of sales. The improvement in gross earnings was due to the strengthening of the Australian dollar relative to the U.S. dollar, as Florsheim Australia’s purchases of inventory are denominated in U.S. dollars.

Other income and expense and taxes

The majority of the Company’s interest income is from its investments in marketable securities. Interest income for 2011 was down approximately $70,000 compared with 2010, primarily due to a lower average investment balance in 2011 compared with 2010.

Interest expense was $611,000 in 2011 compared with $120,000 in 2010. The increase was due to additional debt outstanding during 2011 following the Bogs acquisition.

The effective tax rate for 2011 was 34.3% compared with 33.7% in 2010. The increase in 2011 was primarily due to higher effective rates at certain of the Company’s foreign businesses.

LIQUIDITY & CAPITAL RESOURCES

The Company’s primary sources of liquidity are its cash and short-term marketable securities, which aggregated $25.3 million at December 31, 2012 and $15.1 million at December 31, 2011, and its revolving line of credit. In 2012, the Company generated $18.0 million in cash from operating activities, compared with $17.1 million and $98,000 in 2011 and 2010, respectively. Fluctuations in net cash from operating activities have mainly resulted from changes in net earnings and operating assets and liabilities, and most significantly the year-end inventory and accounts receivable balances.

The Company’s capital expenditures were $9.5 million, $8.2 million and $1.5 million in 2012, 2011 and 2010, respectively. Capital expenditures in 2012 included a project to connect a neighboring building, acquired in December 2011, to the Company’s existing distribution center in Glendale, Wisconsin. This project was completed in the fourth quarter of 2012. The Company expects capital expenditures to decrease to approximately $4 million to $6 million in 2013, and to $1 million to $3 million thereafter.

In 2011, the Company used cash of approximately $30.8 million for its acquisition of Bogs including $3.8 million to repay the debt assumed in the transaction. The Company borrowed a net of $32 million in 2011 under its revolving line of credit to fund the Bogs acquisition and related capital expenditures and inventory purchases. In 2010, the Company used cash of approximately $2.6 million for its acquisition of Umi.

| 20 |

The Company paid cash dividends of $10.9 million, $7.2 million and $7.0 million in 2012, 2011 and 2010, respectively. On December 31, 2012, the Company paid two quarterly cash dividends. The Company accelerated its first and second quarter 2013 dividends, each for $0.17 per share, into 2012 and paid them on December 31st. Both dividends were paid early in anticipation of potential tax law changes effective January 1, 2013. The Company plans to resume its regular quarterly dividend payment schedule in July 2013.

The Company continues to repurchase its common stock under its share repurchase program when the Company believes market conditions are favorable. In 2012, the Company repurchased 285,422 shares for a total cost of $6.6 million. In 2011, the Company repurchased 175,606 shares for a total cost of $4.0 million through its share repurchase program and 400,319 shares for a total cost of $9.0 million in a private transaction. In 2010, the Company repurchased 101,192 shares for a total cost of $2.3 million. At December 31, 2012, the total shares available to purchase under the program was approximately 824,000 shares.

At December 31, 2012, the Company had a $60 million unsecured revolving line of credit with a bank expiring April 30, 2013. The line of credit allows for up to $60 million in borrowings at a rate of LIBOR plus 100 basis points (“LIBOR loans”). At December 31, 2012, outstanding borrowings were $45 million in LIBOR loans at an interest rate of approximately 1.2%. At December 31, 2011, outstanding borrowings were $37 million in LIBOR loans at an interest rate of approximately 1.0%. The Company’s line of credit includes a financial covenant that specifies a minimum level of net worth. As of December 31, 2012, the Company was in compliance with the covenant.

In connection with the Bogs acquisition, the Company held back $2.0 million of the purchase price to be used to help satisfy any claims of indemnification. This holdback amount was paid in full to the former shareholders of Bogs in 2012. The Company also has two contingent payments due to the former shareholders of Bogs in 2013 and 2016. For additional information, see Note 11 in the Notes to Consolidated Financial Statements.

The Company will continue to evaluate the best uses for its available liquidity, including, among other uses, continued stock repurchases and additional acquisitions.

The Company believes that available cash and marketable securities, cash provided by operations, and available borrowing facilities will provide adequate support for the cash needs of the business in 2013, although there can be no assurances.

Off-Balance Sheet Arrangements

The Company does not utilize any special purpose entities or other off-balance sheet arrangements.

| 21 |

Commitments

The Company’s significant contractual obligations are its supplemental pension plan, its operating leases, and the contingent payments that may result from the Bogs acquisition, as described above. These obligations are discussed further in the Notes to Consolidated Financial Statements. The Company also has significant obligations to purchase inventory. The pension obligations and contingent consideration were recorded on the Company’s Consolidated Balance Sheets. Future obligations under operating leases are disclosed in Note 14 of the Notes to Consolidated Financial Statements. The table below provides summary information about these obligations as of December 31, 2012.

| Payments Due by Period (dollars in thousands) | ||||||||||||||||||||

| Total | Less Than a Year | 2 - 3 Years | 4 - 5 Years | More Than 5 Years | ||||||||||||||||

| Pension obligations | $ | 30,951 | $ | 373 | $ | 788 | $ | 848 | $ | 28,942 | ||||||||||

| Operating leases | $ | 39,440 | 9,251 | 14,269 | 7,868 | 8,052 | ||||||||||||||

| Contingent consideration (undiscounted) | $ | 6,424 | 1,270 | 5,154 | ||||||||||||||||

| Purchase obligations* | $ | 50,182 | 50,182 | |||||||||||||||||

| Total | $ | 126,997 | $ | 61,076 | $ | 20,211 | $ | 8,716 | $ | 36,994 | ||||||||||

* Purchase obligations relate entirely to commitments to purchase inventory.

OTHER

Critical Accounting Policies

The Company’s accounting policies are more fully described in Note 2 of the Notes to Consolidated Financial Statements. As disclosed in Note 2, the preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions about future events that affect the amounts reported in the consolidated financial statements and accompanying notes. Future events and their effects cannot be determined with absolute certainty. Therefore, the determination of estimates requires the exercise of judgment. Actual results inevitably will differ from those estimates, and such differences may be material to the consolidated financial statements. The following policies are considered by management to be the most critical in understanding the significant accounting estimates inherent in the preparation of the Company’s consolidated financial statements and the uncertainties that could impact the Company’s results of operations, financial position and cash flows.

Sales Returns, Sales Allowances and Doubtful Accounts

The Company records reserves and allowances (“reserves”) for sales returns, sales allowances and discounts, and accounts receivable balances that it believes will ultimately not be collected. The reserves are based on such factors as specific customer situations, historical experience, a review of the current aging status of customer receivables and current and expected economic conditions. The reserve for doubtful accounts includes a specific reserve for accounts identified as potentially uncollectible, plus an additional reserve for the balance of accounts. The Company evaluates the reserves and the estimation process and makes adjustments when appropriate. Historically, actual write-offs against the reserves have been within the Company’s expectations. Changes in these reserves may be required if actual returns, discounts and bad debt activity varies from the original estimates. These changes could impact the Company’s results of operations, financial position and cash flows.

| 22 |

Pension Plan Accounting

The Company’s pension expense and corresponding obligation are determined on an actuarial basis and require certain actuarial assumptions. Management believes the two most critical of these assumptions are the discount rate and the expected rate of return on plan assets. The Company evaluates its actuarial assumptions annually on the measurement date (December 31) and makes modifications based on such factors as market interest rates and historical asset performance. Changes in these assumptions can result in different expense and liability amounts, and future actual experience can differ from these assumptions.

Discount Rate – Pension expense and projected benefit obligation both increase as the discount rate is reduced. See Note 12 of the Notes to Consolidated Financial Statements for discount rates used in determining the net periodic pension cost for the years ended December 31, 2012, 2011 and 2010 and the funded status of the plans at December 31, 2012 and 2011. The rates are based on the plan’s projected cash flows. The Company utilizes the cash flow matching method, which discounts each year’s projected cash flows at the associated spot interest rate back to the measurement date. A 0.5% decrease in the discount rate would increase annual pension expense and the projected benefit obligation by approximately $416,000 and $4,300,000, respectively.

Expected Rate of Return – Pension expense increases as the expected rate of return on pension plan assets decreases. In estimating the expected return on plan assets, the Company considers the historical returns on plan assets and future expectations of asset returns. The Company utilized an expected rate of return on plan assets of 7.75% in 2012 and 8.0% in 2011 and 2010. This rate was based on the Company’s long-term investment policy of equity securities: 20% - 80%; fixed income securities: 20% - 80%; and other, principally cash: 0% - 20%. A 0.5% decrease in the expected return on plan assets would increase annual pension expense by approximately $135,000.

Goodwill and Trademarks

Goodwill and trademarks are tested for impairment on an annual basis and more frequently when significant events or changes in circumstances indicate that their carrying values may not be recoverable. Conditions that would trigger an impairment assessment include, but are not limited to, a significant adverse change in legal factors or business climate that could affect the value of the asset.

The Company uses a two-step process to test goodwill for impairment. First, the applicable reporting unit’s fair value is compared to its carrying value. If the reporting unit’s carrying amount exceeds its fair value, an indication exists that the reporting unit’s goodwill may be impaired, and the second step of the impairment test would be performed. The second step of the goodwill impairment test is to measure the amount of the impairment loss, if any. In the second step, the implied fair value of the reporting unit’s goodwill is determined by allocating the reporting unit’s fair value to all of its assets and liabilities similar to a purchase price allocation. The implied fair value of the goodwill that results from the application of this second step is then compared to the carrying amount of the goodwill and an impairment charge would be recorded for the difference if the carrying value exceeds the implied fair value of the goodwill.

The Company conducted its annual impairment test of goodwill as of December 31, 2012. For goodwill impairment testing, the Company determined the applicable reporting unit is its wholesale segment. Fair value of the wholesale segment was estimated based on a weighted analysis of discounted cash flows (“income approach”) and a comparable public company analysis (“market approach”). The rate used in determining discounted cash flows is a rate corresponding to the Company’s weighted average cost of capital, adjusted for risk where appropriate. In determining the estimated future cash flows, current and future levels of income were considered as well as business trends and market conditions. The testing determined that the estimated fair value of the wholesale segment substantially exceeded its carrying value therefore there was no impairment of goodwill in 2012.

The Company conducted its annual impairment test of trademarks as of December 31, 2012. The Company uses a discounted cash flow methodology to determine the fair value of its trademarks, and a loss would be recognized if the carrying values of the trademarks exceeded their fair values. In fiscal 2012, 2011 and 2010, there was no impairment of the Company’s trademarks.

The Company can make no assurances that the goodwill or trademarks will not be impaired in the future. When preparing a discounted cash flow analysis, the Company makes a number of key estimates and assumptions. The Company estimates the future cash flows based on historical and forecasted revenues and operating costs. This, in turn, involves further estimates such as estimates of future growth rates and inflation rates. The discount rate is based on the estimated weighted average cost of capital for the business and may change from year to year. Weighted average cost of capital includes certain assumptions such as market capital structures, market beta, risk-free rate of return, and estimated costs of borrowing. Changes in these key estimates and assumptions, or in other assumptions used in this process, could materially affect the Company’s impairment analysis for a given year. Additionally, since the Company’s goodwill measurement also considers a market approach, changes in comparable public company multiples can also materially impact the Company’s impairment analysis.

| 23 |

Contingent Consideration

The Company recorded its estimate of the fair value of contingent consideration that may result from the Bogs acquisition. The contingent consideration is formula-driven and is based on Bogs achieving certain levels of gross margin dollars between January 1, 2011 and December 31, 2015. There are no restrictions as to the amount of consideration that could become payable under the arrangement. The calculation of the 2013 payment has been finalized and the Company will pay the former shareholders of Bogs approximately $1.27 million on or before March 31, 2013. Management estimates that the range of reasonably possible potential amounts for the second payment (due in 2016) will be between $2 million and $8 million. The Company recorded $5.0 million, which is management’s best estimate of the fair value of the second payment.

The Company determined the fair value of the contingent consideration using a probability-weighted model which included estimates related to Bogs future sales levels and gross margins. On a quarterly basis, the Company revalues the obligation and records increases or decreases in its fair value as an adjustment to operating earnings. Changes to the contingent consideration obligation can result from adjustments to the discount rate, accretion of the discount due to the passage of time, or changes in assumptions regarding the future performance of Bogs. The assumptions used to determine the value of contingent consideration include a significant amount of judgment, and any changes in the assumptions could have a material impact on the amount of contingent consideration expense or income recorded in a given period.

Recent Accounting Pronouncements

See Note 2 of the Notes to Consolidated Financial Statements.

| ITEM 7A | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

The Company is exposed to market risk from changes in foreign exchange and interest rates. To reduce the risk from changes in foreign exchange rates, the Company selectively uses forward exchange contracts. The Company does not hold or issue financial instruments for trading purposes. The Company does not have significant market risk on its marketable securities as those investments consist of high-grade securities and are held to maturity. The Company reviewed its portfolio of investments as of December 31, 2012 and determined that no other-than-temporary market value impairment exists.

The Company is also exposed to market risk related to the assets in its defined benefit pension plan. The Company reduces that risk by having a diversified portfolio of equity, fixed income and alternative investments and periodically reviews this allocation with its investment consultants.

Foreign Currency

The Company’s earnings are affected by fluctuations in the value of the U.S. dollar against foreign currencies, primarily as a result of the sale of product to Canadian customers, Florsheim Australia’s purchases of its inventory in U.S. dollars and the Company’s intercompany loans with Florsheim Australia. At December 31, 2012, Florsheim Australia had forward exchange contracts outstanding to buy $3.5 million U.S. dollars at a total price of approximately $3.4 million Australian dollars. Based on December 31, 2012 exchange rates, there were no significant gains or losses on these contracts. All contracts expire in less than one year. Based on the Company’s outstanding forward contracts and intercompany loans, a 10% appreciation in the U.S. dollar at December 31, 2012 would not have a material effect on the Company’s financial statements.

Interest Rates

The Company is exposed to interest rate fluctuations on borrowings under its revolving line of credit. At December 31, 2012, the Company had $45 million of outstanding borrowings under the revolving line of credit. The interest expense related to borrowings under the line during 2012 was $435,000. A 10% increase in the Company’s interest rate on borrowings outstanding as of December 31, 2012 would not have a material effect on the Company’s financial position, results of operations or cash flows.

| 24 |

ITEM 8 FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

Index to Consolidated Financial Statements

| Page | ||

| Management’s Report on Internal Control Over Financial Reporting | 26 | |

| Report of Independent Registered Public Accounting Firm | 27 | |

| Consolidated Statements of Earnings | 28 | |

| Consolidated Statements of Comprehensive Income | 29 | |

| Consolidated Balance Sheets | 30 | |

| Consolidated Statements of Equity | 31 | |

| Consolidated Statements of Cash Flows | 32 | |

| Notes to Consolidated Financial Statements | 33 |

| 25 |

Management’s Report on Internal Control Over Financial Reporting

The Company’s management is responsible for establishing and maintaining effective internal control over financial reporting. The Company’s management, with the participation of the Company’s Chief Executive Officer and Chief Financial Officer, assessed the effectiveness of the Company’s internal control over financial reporting as of December 31, 2012. In making this assessment, management used the criteria set forth by the Committee of Sponsoring Organizations of the Treadway Commission in Internal Control – Integrated Framework. Based on the assessment, the Company’s management has concluded that, as of December 31, 2012, the Company’s internal control over financial reporting was effective based on those criteria.

The Company’s internal control system was designed to provide reasonable assurance to the Company’s management and Board of Directors regarding the preparation and fair presentation of published financial statements. All internal control systems, no matter how well designed, have inherent limitations. Therefore, even those systems determined to be effective can provide only reasonable assurance with respect to financial statement preparation and presentation.

The Company’s independent registered public accounting firm has audited the Company’s consolidated financial statements and the effectiveness of internal controls over financial reporting as of December 31, 2012 as stated in its report below.

| 26 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and Board of Directors of

Weyco Group, Inc.:

We have audited the accompanying consolidated balance sheets of Weyco Group, Inc. and subsidiaries (the "Company") as of December 31, 2012 and 2011, and the related consolidated statements of earnings, comprehensive income, equity, and cash flows for each of the three years in the period ended December 31, 2012. We also have audited the Company's internal control over financial reporting as of December 31, 2012, based on the criteria established in Internal Control — Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. The Company's management is responsible for these consolidated financial statements, for maintaining effective internal control over financial reporting, and for its assessment of the effectiveness of internal control over financial reporting, included in the accompanying Management’s Report on Internal Control Over Financial Reporting. Our responsibility is to express an opinion on these financial statements and an opinion on the Company's internal control over financial reporting based on our audits.