Exhibit 99.1

Annual Report

for the year ended

31 December 2014

Lauro Cinquantasette Group

Registered offices in Via del Lauro 7 - 20121 Milan

Share capital Euro 58,333,333.25 fully paid up

Fiscal Code 04849340965

(English language translation of the original Italian document)

Index

| Corporate bodies | 3 | |

| Directors’ Report | 4 | |

| Summary of Results | 5 | |

| Group Structure | 8 | |

| Significant events during the year 2014 | 9 | |

| Business Performance | 11 | |

| Research and development activities 2014 | 13 | |

| Analysis of the Group’s income statement | 15 | |

| Analysis of the Group’s equity and financial situation | 19 | |

| Human Resources | 25 | |

| Health, Safety and Environmental protection | 27 | |

| Risk Assessment | 28 | |

| Transactions with Group companies and other related parties | 32 | |

| Own shares | 32 | |

| Derivative Instruments | 32 | |

| Significant events after the year-end and Business outlook | 33 | |

| Consolidated Financial Statements as at 31 December 2014 | 35 | |

| Consolidated Statement of Financial Position | 36 | |

| Consolidated Income Statement | 37 | |

| Consolidated Statement of Comprehensive Income | 38 | |

| Consolidated Cash Flow Statement | 39 | |

| Consolidated Statement of Changes in Equity | 40 | |

| Explanatory Notes to the Consolidated Financial Statements | 41 | |

| 1. General Information | 41 | |

| 2. Summary of accounting principles adopted | 41 | |

| 3. Financial Risk Management | 61 | |

| 4. Estimates and assumptions | 67 | |

| 5. Business Combinations | 68 | |

| 6. Notes to the Consolidated Income Statement and Consolidated Statement of Financial Position headings | 70 | |

| 7. Criteria adopted for the transition from Italian Accounting Principles to the IFRS | 93 | |

| Appendix 1: List of subsidiary, associated and other companies | 105 |

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 2 |

Corporate bodies

Board of Directors of the Parent company Lauro Cinquantasette SpA

(appointed up until the date of the Shareholders Meeting called for the approval of the financial statements for the year ended 31 December 2014)

| Chairman | Dott. Gianmario Baccalini |

| Managing Director | Dott.ssa Margalit Fine |

| Director | Dott. Pierluca Antolini |

| Director | Dott. Ugo Belardi |

| Director | Dott. Marco Carotenuto |

| Director | Dott. Roberto Colussi |

| Director | Dott. Alberto Mangia |

| Director | Avv. Emiliano Nitti |

| Director | Dott. Alessandro Papetti |

| Director | Dott. Francesco Pilli |

| Director | Dott. Enrico Ricotta |

| Director | Dott. Carlo Luigi Rossi |

| Director | Dott.ssa Alessandra Stea |

Board of Statutory Auditors of the parent company Lauro Cinquantasette SpA

(appointed up until the date of the Shareholders Meeting called for the approval of the financial statements for the year ended 31 December 2014)

| Chairman | Dott. Piero Alonzo |

| Statutory Auditor | Dott. Paolo Fratta Pasini |

| Statutory Auditor | Dott. Guido Riccardi |

Independent auditors

Reconta Ernst & Young S.p.A

(appointed up until the date of the Shareholders Meeting called for the approval of the financial statements for the year ended 31 December 2014)

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 3 |

Directors’ Report

The present annual report for the year ended on 31 December 2014 has been prepared in conformity with accounting principles and valuation criteria established by the IFRS, by which we intend all of the “International Financial Reporting Standards”, all of the “International Accounting Standards” (IAS), all of the interpretations of the “International Reporting Interpretations Committee” (IFRIC), formerly called “Standing Interpretations Committee” (SIC) endorsed at that date by the European Union, in accordance with the Regulation EC No. 1606/2002 of the European Parliament and of the European Council dated 19 July 2002.

The IFRS have been applied consistently to all of the periods presented in this Annual Report. Given that these are the first set of Consolidated Financial Statements prepared by Lauro Cinquantasette Spa (hereinafter referred to as “Lauro”, the “Company” or the “Parent company”) in conformity with the IFRS, it has been necessary to carry out a process of conversion from Italian Accounting Principles to the IFRS in conformity with the requirements of IFRS1 “First time adoption of the International Financial Reporting Standards”; for this purpose and for the abovementioned reasons, the 1° January 2013 was chosen as the date for the transition to the IFRS (hereinafter referred to as the “Transition date”). As regards the disclosure requirements of IFRS 1 regarding the accounting effects linked to the transition from Italian Accounting Principles to the IFRS, reference should be made to note 7 of the Explanatory Notes to the Consolidated Financial Statements.

During the year 2014, the Lauro Cinquantasette Group recorded total revenues of Euro 186,113 thousand, representing a decrease of 7.8% with respect to the previous year. This decrease was due principally to the effect of a slowdown of the Generic drugs (API -Active Pharmaceutical Ingredients /Intermediates) business, which was only partly offset by the expansion of the CMO/CS business.

The drop in the turnover of the Fine Chemical business is linked mainly to the completion of the Macaba project in the USA, the effects of which were partially offset by an improvement in the product mix that, thanks above all to the growth of T3P in Germany, led to an increase in profit margins.

The Group achieved positive results in consolidating its:

| - | Product Portfolio: we would point out in fact that 71% of Group turnover is concentrated within our top 20 products; |

| - | Customer Portfolio: 40% of Group turnover is concentrated on the world’s principal pharmaceutical companies (Big Pharma companies). Management believes that this concentration represents an opportunity for the growth of our product portfolio in line with the Big Pharma’s growth. |

Faced with the drop in turnover during the year 2014, the Group has improved the range of products sold, which has led to an increase in the percentage Cash margin1. The decrease in absolute terms is attributable to the lower utilisation of production capacity related both to an overcapacity of our industrial plants and to a more efficient management of inventory levels.

The “adjusted” EBITDA, or rather, the operating result before depreciation, amortisation and other value adjustments as well as before non-recurring income and expenses, shows a profit of Euro 23,567 thousand, representing a decrease of Euro 7,597 thousand with respect to the year 2013. This decrease is mainly attributable to the drop in the sales volumes of the Generic drugs (API/Intermediates) and to a lower utilization of production capacity.

1 By Cash Margin we intend the margin calculated by deducting from sales revenues only the cost of those raw materials relative to the products sold. This indicator is used by management to evaluate the Group’s performance.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 4 |

The Net Operating Result (EBIT) shows a profit of Euro 119 thousand, representing an improvement of Euro 735 thousand with respect to the year 2013, in which the Group recorded a net operating loss of Euro 615 thousand.

The net financial position as at 31 December 2014 shows a net indebtedness of Euro 82,114 thousand, lower by Euro 6,072 thousand than that at 31 December 2013, which amounted to Euro 88,186 thousand; this decrease is due to a more efficient management of the Group’s operations and thanks to the proceeds realised on the sale of the minority shareholding in the company Pharmintraco Sagl, as described in greater detail in the section of this report relative to “Significant events during the year”.

The Group’s operations generated cash flows as a result also of the further improvement in credit control procedures introduced during the year 2013, to the reduction in capital expenditure and to the improvement in the management of stock levels, which enabled us to reduce trade payables.

For a detailed analysis of both the economic results and of the equity and financial performance and situation, reference should be made to the paragraphs “Business performance”, “Analysis of the Group’s income statement”, as well as “Analysis of the Group’s equity and financial position” contained in this Report. The figures shown in this Report, including certain percentage figures, have been rounded to the nearest thousands of Euro, except where indicated otherwise. Consequently, certain totals in the tables below may not coincide with the precise arithmetic sum of the table components.

LAURO CINQUANTASETTE GROUP– SUMMARY OF CONSOLIDATED RESULTS

| Year ended on | 31 December 2014 | 31 December 2013 | Variation | |||||||||||||||||||||

| Euro/1000 | % | Euro/1000 | % | Euro/1000 | % | |||||||||||||||||||

| Sales revenues | 186,113 | 100.0 | % | 201,809 | 100.0 | % | -15,696 | -7.8 | % | |||||||||||||||

| Normalised Ebitda | 23,567 | 12.7 | % | 31,164 | 15.0 | % | -7,597 | -24.4 | % | |||||||||||||||

| Ebitda | 21,628 | 11.6 | % | 21,383 | 14.4 | % | 244 | 1.1 | % | |||||||||||||||

| Ebit | 119 | 0.1 | % | -615 | -1.0 | % | 735 | -119.4 | % | |||||||||||||||

| Profit/(loss) before tax | -6,113 | -3.3 | % | -6,706 | -3.5 | % | 592 | -8.8 | % | |||||||||||||||

| Net profit/(loss) for the Group | -4,224 | -2.3 | % | -8,405 | -6.4 | % | 4,181 | -49.7 | % | |||||||||||||||

| (in thousands of Euro) | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Fixed assets | 196,808 | 204,552 | -7,745 | |||||||||

| Working capital | 76,941 | 78,622 | -1,681 | |||||||||

| Capital Invested | 273,749 | 283,175 | -9,426 | |||||||||

| Shareholders’ equity | -172,950 | -178,415 | 5,465 | |||||||||

| Medium/long term liabilities | -18,685 | -16,574 | -2,111 | |||||||||

| Net Financial Position | 82,114 | 88,186 | -6,072 | |||||||||

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 5 |

| (in thousands of Euro) | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Net cash flow generated / (absorbed) by operating activities | 18,595 | 11,807 | 6,788 | |||||||||

| Net cash flow generated / (absorbed) by investing activities | -11,116 | -5,091 | -6,025 | |||||||||

| Net cash flow generated / (absorbed) by financing activities | -9,231 | 625 | -9,855 | |||||||||

| Total cash flows generated / (absorbed) during the period | -1,753 | 7,340 | -9,093 | |||||||||

| Capital expenditure | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Euro/1000 | Euro/1000 | Euro/1000 | ||||||||||

| Property, plant and equipment | 8,069 | 8,621 | -552 | |||||||||

| Intangible assets | 5,495 | 3,294 | 2,201 | |||||||||

| Total | 13,564 | 11,915 | 1,649 | |||||||||

| Net working capital | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Euro/1000 | Euro/1000 | Euro/1000 | ||||||||||

| Inventories | 64,291 | 73,478 | -9,187 | |||||||||

| Trade receivables | 42,241 | 50,198 | -7,957 | |||||||||

| Trade payables | -30,038 | -38,785 | 8,747 | |||||||||

| Other current assets | 20,651 | 13,417 | 7,233 | |||||||||

| Other current liabilities | -20,204 | -19,686 | -518 | |||||||||

| Total | 76,941 | 78,622 | -1,681 | |||||||||

| Net Financial Position | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Euro/1000 | Euro/1000 | Euro/1000 | ||||||||||

| Cash and cash equivalents | 13,395 | 15,148 | -1,753 | |||||||||

| Current financial debt | -94,077 | -101,783 | 7,706 | |||||||||

| Non-current financial debt | -1,432 | -1,552 | 120 | |||||||||

| Total net indebtedness | -82,114 | -88,186 | 6,072 | |||||||||

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 6 |

| Workforce | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Italy | 550 | 571 | -21 | |||||||||

| France | 146 | 146 | 0 | |||||||||

| Germany | 66 | 64 | 2 | |||||||||

| UK | 0 | 0 | 0 | |||||||||

| USA | 73 | 74 | -1 | |||||||||

| Total | 835 | 855 | -20 | |||||||||

| Workforce | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Managers | 24 | 23 | 1 | |||||||||

| Supervisory staff | 115 | 113 | 2 | |||||||||

| Clerical staff | 294 | 305 | -11 | |||||||||

| Manual workers | 402 | 414 | -12 | |||||||||

| Total | 835 | 855 | -20 | |||||||||

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 7 |

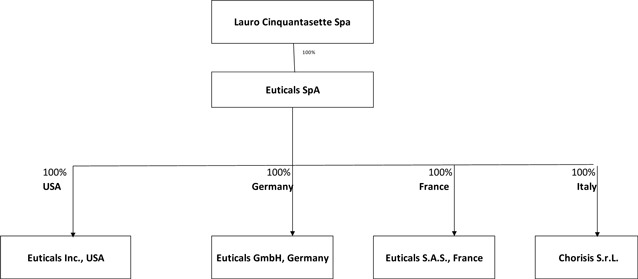

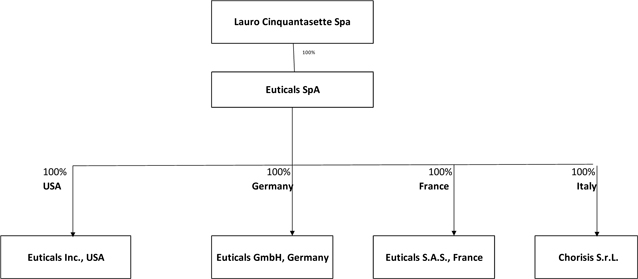

Group Structure

Lauro Cinquantasette Spa prepared its first Consolidated Financial Statements in the year 2012 following the acquisition of the Euticals Group which took place in April 2012. This operation entailed the acquisition of 100% of the share capital of the company Prime European Therapeuticals S.p.a. (Euticals Spa, hereinafter referred to as “Euticals”), which heads up the Euticals Group, comprised of the companies Euticals GMBH, Euticals SAS, Euticals INC and Archimica UK LTD, all of which operating in the API sector.

The acquisition of 100% of the share capital of the company Chorisis Srl, a company operating in the sector with significant experience the industrial development of the products contained in the Group’s product portfolio, is effective as from 1 July 2013.

At 31 December 2014 the subsidiary Archimica Ltd and its subsidiary were excluded from the consolidation area, given that these companies were placed into liquidation on 31 July 2013.

We would point out that the investment in the company Società Pharmintraco Sagl, 40%-owned by Euticals Spa, was sold on 13 February 2014; reference should be made to the paragraph “Significant events during the year” for further information thereon. .

The Group structure of the Lauro Cinquantasette Group (hereinafter referred to as “the Group”) as at 31 December 2014 is shown below.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 8 |

Significant events during the year 2014

From a strategic point of view, in February 2014 the Group completed the preparation of its Strategic Plan for the period 2014-2018, which was subject to amendment and integration during the latter part of the year.

This was followed by measures aimed at rationalisation of the corporate structure with the sale, on 13 February 2014, of the minority shareholding in the Swiss company Pharmintraco Sagl. In addition to the sale agreement, Euticals Spa and the purchaser have signed a “Manufacturing agreement” which shall allow Euticals to continue the production at the Swiss manufacturing plant of the oncological formulas developed, and whose dossiers (ANDA) have been submitted for approval to the FDA (Food Drug Administration).

On 31 March 2014 the Board of Directors of Euticals Spa appointed Dottoressa Margalit Fine as Managing Director; she has been entrusted to follow the process of the development, preparation and implementation of the 2014-2018 Strategic Plan. Formerly Head of the API Division of Teva in Europe, her arrival shall enrich the Company’s management through her significant experience and knowledge of the Pharmaceuticals sector and of API, as well as her wide network of contacts throughout the world market.

Therefore, in 2014, preparation continued for the corporate reorganisation, resulting in the drawing up of the Strategic Plan for the period 2015-2022 (hereinafter referred to as the “New Plan”), approved by the Board of Directors on 4 November 2014, which concentrated on four main areas:

| - | the consolidation of the existing business by means of greater valorisation of the “core” products with the highest margins and the rationalisation of the minor products; |

| - | the growth of the CMO/CS business as a driver for short/medium term growth, sustained through investment aimed at improving our reference sites; |

| - | the development of new API as a driver for medium/long term growth, sustained through an increase in R&D activity. |

| - | the industrial restructuring of those manufacturing sites most beneficial to the optimisation of the Group’s production and management. |

The current manufacturing structure is considered to be redundant both in terms of the number of production plants and in terms of complexity and of cost.

Following the approval of the New Plan, the Group has proceeded with the evaluation of the manufacturing sites, with the detailed planning of the process for the transfer of production of its reference products and with the estimate of the specific investments required, as described in greater detail in the paragraph “Significant events after the year-end and Business outlook”.

As from May 2014, in line with the guidelines contained in the New Plan, Euticals has commenced negotiations with a leader in the pharmaceuticals sector for the sale of the plant and buildings at the first manufacturing site chosen for rationalisation. This operation represents a first step in the process of restructuring of the industrial structure, while maintaining the continuity of the business thanks to the transfer of production to other manufacturing sites. The negotiations and the initial due diligence controls carried out resulted in the receipt, in October 2014, of a non-binding preliminary offer in preparation for the final phase of the due diligence and of the negotiations as described in greater detail in the paragraph “Significant events after the year-end and Business outlook”.

The growth of the business and of earnings shall also benefit from the strengthening:

| - | of the Sales structure with the appointment of Area managers for the target markets; |

| - | of the Quality structure in coincidence with the development of the CMO and of new API; |

| - | of the Research and Development structure, also with the acquisition of external expertise; |

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 9 |

as well as from a capital expenditure programme which is significantly higher than those of previous years aimed at the achievement of specific objectives both in terms of growth and in terms of restructuring.

At the same time, a series of initiatives has been launched aimed at a greater corporate effectiveness and efficiency, in particular these regard (i) the integrated supply chain project in order to guarantee a better management of the purchasing function and of working capital; (ii) the review and updating of the manufacturing processes and (iii) the rationalization of the industrial plants in line with the requirements of the principal customers in this sector (Big Pharma). These initiatives, backed up by a significant capital expenditure programme, should enable the Group to stabilise its high added value activities and return to the path of growth outlined in the 2014-2018 Strategic Business Plan and confirmed by the New Plan.

As regards compliance, in 2014 the Group has passed all of the AIFA and FDA inspections.

*******************

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 10 |

Business Performance

Total revenues amounted to Euro 186.1 million for the year 2014, representing a decrease of 7.8% with respect to the revenues for the year 2013, which amounted to Euro 201.8 million.

This drop in turnover with respect to the previous year is mainly linked to the following:

| (i) | a reduction in the business related to the Generics drugs produced in Italy, which was negatively affected by the downsizing of certain markets and of the regulatory changes introduced by the EMA (European Medicine Agency); |

| (ii) | to the completion of the Fine Chemical contracts in the USA; |

| (iii) | to a drop in the turnover of the French subsidiary attributable to the redefinition of the terms of the contract for a specific product which registered a drop in volumes in favour of an improvement in country operating margins. |

These negative effects were compensated for in part by the following:

| - | the excellent performance of the German subsidiary, which more than doubled the volumes of its main products, has significantly increased Custom Synthesis revenues; |

| - | the growth in the volumes of controlled substances in the USA which has largely compensated for the drop in the volumes of Fine Chemicals, enabling the American subsidiary to improve its margin levels. |

The analysis of revenues by geographical area is shown in the table below:

| Total Revenues | 31 December 2014 | 31 December 2013 | Variation | |||||||||||||||||||||

| Euro/1000 | % | Euro/1000 | % | Euro/1000 | % | |||||||||||||||||||

| Italy | 125,014 | 67.2 | % | 142,857 | 70.8 | % | -17,843 | -12.5 | % | |||||||||||||||

| USA | 15,184 | 8.2 | % | 16,638 | 8.2 | % | -1,454 | -8.7 | % | |||||||||||||||

| Germany | 20,285 | 10.9 | % | 11,750 | 5.8 | % | 8,535 | 72.6 | % | |||||||||||||||

| France | 30,776 | 16.5 | % | 32,884 | 16.3 | % | -2,108 | -6.4 | % | |||||||||||||||

| UK | 0 | 0.0 | % | 1,162 | 0.6 | % | -1,162 | -100.0 | % | |||||||||||||||

| Intercompany | -5,146 | -2.8 | % | -3,482 | -1.7 | % | -1,664 | 47.8 | % | |||||||||||||||

| Total | 186,113 | 100.0 | % | 201,809 | 100.0 | % | -15,696 | -7.8 | % | |||||||||||||||

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 11 |

The table below analyses revenues by product type:

| Total Revenues | 31 December 2014 | 31 December 2013 | Variation | |||||||||||||||||||||

| Euro/1000 | % | Euro/1000 | % | Euro/1000 | % | |||||||||||||||||||

| Generic drugs (API / Intermediates) | 113,106 | 60.8 | % | 126,271 | 62.6 | % | -13,165 | -10.4 | % | |||||||||||||||

| Cmo/Custom Synthesis | 38,173 | 20.5 | % | 36,942 | 18.3 | % | 1,231 | 3.3 | % | |||||||||||||||

| Fine Chemicals | 34,834 | 18.7 | % | 36,566 | 18.1 | % | -1,732 | -4.7 | % | |||||||||||||||

| Other | 0 | 0.0 | % | 2,030 | 1.0 | % | -2,030 | -100.0 | % | |||||||||||||||

| Total | 186,113 | 100.0 | % | 201,809 | 100.0 | % | -15,696 | -7.8 | % | |||||||||||||||

The sales of GENERIC drugs amounted to Euro 113.1 million, showing a decrease of Euro 13.2 million with respect to the previous year; this decrease was due in part to the downsizing of certain markets and to the regulatory changes introduced by the EMA.

The weak performance of Generic drugs was in part compensated for (i) by the growth in Contract manufacturing (CMO/Custom synthesis) linked in particular to the development of new projects in Germany and in Italy; (ii) by the stability of the Fine Chemical business which, despite the conclusion of a major contract, managed to replace the revenues lost with the relaunching of a reference product, whose revenues more than doubled with respect to the year 2013, contributing significantly to the increase in the Group’s earnings.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 12 |

Research and Development activities 2014

During the year 2014 the Research and Development (R&D) department completed the reorganisation process launched in 2013, with the introduction of a project management function aimed at improving its capacity to manage projects and achieve the predetermined goals in terms of sales volume.

Research and Development activities are focused on:

| - | Development of new API (generics) in order to extend and diversify the product portfolio; |

| - | Custom synthesis: projects/products to be developed and/or produced upon the specific indication of customers and/or with the customer’s own technology; |

| - | Continuous Improvement, or rather, the optimisation of existing manufacturing processes with the aim of increasing the quality and the profitability of the products linked thereto; |

| - | Trouble shooting: resolving problems regarding products and manufacturing processes. |

The resources dedicated to research and development are equivalent to approximately 4% of turnover, this amount is in addition to Group investments.

New API

The Group offers its services as manufacturer of API for the Generics market thanks to the availability of manufacturing plants in various geographical areas and supplies a wide range of potential products.

Our customers are generic pharmaceutical companies and/or the creators of the original drugs.

During the year 2014, the Group concentrated on the development of the active pharmaceutical ingredients necessary for the manufacture of the following therapeutic areas:

| - | anti-cancer drugs, which represent a cornerstone of the Group’s production and for which the Group has 2 manufacturing plants dedicated respectively to oral cancer drugs and intravenous cancer drugs; |

| - | immunosuppressants, for which the starting materials are produced internally in designated sites within the Group using fermentation and subsequent chemical transformation of fermentation products; |

| - | hormone replacements; |

| - | slow release bronchodilators ; these are products with a high margin and low production volumes, with a complex crystalline structure, that renders the development thereof extremely difficult, due principally to the low dosage which is measured in micrograms; |

| - | antibiotics; |

| - | controlled substances produced at the American manufacturing plant at Springfield. |

All of these products strategically expand the Group’s product portfolio, in certain cases strengthening the specific activities that distinguish the Group within the API market.

In 2014 the Group deposited two patents relative to new API with an excellent potential in terms of profit margins and of future sales volumes on the worldwide market.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 13 |

Further API have been developed in order to optimise the productive capacity of those manufacturing plants not dedicated to a specific family of products and to the further enrichment of the Group’s commercial portfolio.

Custom Synthesis/Contract manufacturing

The Group’s skill and experience place it among the key operators in the sector for the development and manufacture of new products for the large pharmaceutical companies and destined for the clinical trials phase prior to commercialisation. These types of product are developed with the aim of optimising the use of the plants’ production capacity.

In particular, in 2014 new projects were launched relative to new antibiotics, which, together with the products developed in previous years, enabled the Group to strengthen its collaboration with the principal leading pharmaceutical companies on the world market.

Continuous Improvement

This type of activity is aimed towards improving the quality and the competitivity of our products.

The generics market is in continuous evolution as a result of national politics and/or of insurance companies who define pharmaceutical prices for reimbursable or life saving drugs, usually imposing gradually decreasing price curves.

The complexity of the industrial processes and the growing presence in the market of competitors, render it necessary to dedicate expert resources.

During the year 2014 the Group’s activities were concentrated on the improvement of the principal products contained in its product portfolio, such as Minocycline, 4FBA, Propofol, Hydroxyurea, GPC, Dihydroergotamine mesylate.

Trouble shooting

The manufacture of API for sale may be subject to involuntary deviations from normal processes or to sub-standard products. In this case the research department is involved for the resolution of the problem.

*******************

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 14 |

Analysis of the Group’s Income Statement

The table below shows, in thousands of euro, the principal components of the reclassified consolidated income statement of the Lauro Cinquantasette Group for the years 2014 and 2013.

| Income statement | Year ended on 31 December 2014 | % | Year ended on 31 December 2013 | % | Variation in Euro | % | ||||||||||||||||||

| Sales revenues | 186,113 | 98.5 | % | 201,809 | 99.5 | % | -15,696 | -7.8 | % | |||||||||||||||

| Other income and revenues | 2,761 | 1.5 | % | 1,094 | 0.5 | % | 1,668 | 152.5 | % | |||||||||||||||

| Total Revenues | 188,875 | 100.0 | % | 202,903 | 100.0 | % | -14,028 | -6.9 | % | |||||||||||||||

| Variation in inventories | -3,243 | -1.7 | % | 8,868 | 4.4 | % | -12,111 | -136.6 | % | |||||||||||||||

| Value of production | 185,632 | 98.3 | % | 211,770 | 104.4 | % | -26,138 | -12.3 | % | |||||||||||||||

| Raw materials and other related costs | -69,695 | -36.9 | % | -90,550 | -44.6 | % | 20,855 | -23.0 | % | |||||||||||||||

| Added value (Gross Margin) | 115,937 | 61.4 | % | 121,220 | 59.7 | % | -5,283 | -4.4 | % | |||||||||||||||

| Personnel costs | -53,648 | -28.4 | % | -54,978 | -27.1 | % | 1,330 | -2.4 | % | |||||||||||||||

| R&D and other internal costs capitalised | 5,631 | 3.0 | % | 3,647 | 1.8 | % | 1,984 | 54.4 | % | |||||||||||||||

| Other operating costs | -46,292 | -24.5 | % | -48,506 | -23.9 | % | 2,214 | -4.6 | % | |||||||||||||||

| Gross operating margin (EBITDA) | 21,628 | 11.5 | % | 21,383 | 10.5 | % | 244 | 1.1 | % | |||||||||||||||

| Depreciation, amortisation and writedowns | -21,508 | -11.4 | % | -21,998 | -10.8 | % | 490 | -2.2 | % | |||||||||||||||

| Net operating result (EBIT) | 119 | 0.1 | % | -615 | -0.3 | % | 735 | -119.4 | % | |||||||||||||||

| Financial income and expenses | -6,233 | -3.3 | % | -6,090 | -3.0 | % | -142 | 2.3 | % | |||||||||||||||

| Result before tax | -6,113 | -3.2 | % | -6,706 | -3.3 | % | 592 | -8.8 | % | |||||||||||||||

| Income tax | 1,889 | 1.0 | % | -1,699 | -0.8 | % | 3,589 | -211.2 | % | |||||||||||||||

| Result after tax | -4,224 | -2.2 | % | -8,405 | -4.1 | % | 4,181 | -49.7 | % | |||||||||||||||

| Reconciliation EBITDA | ||||||||||||||||||||||||

| Gross operating margin (EBITDA) | 21,628 | 11.5 | % | 21,383 | 10.5 | % | 244 | 1.1 | % | |||||||||||||||

| Non-recurring income/expenses | 1,939 | 1.0 | % | 9,781 | 4.8 | % | -7,842 | -80.2 | % | |||||||||||||||

| Adjusted EBITDA | 23,567 | 12.5 | % | 31,164 | 15.4 | % | -7,597 | -24.4 | % | |||||||||||||||

Sales revenues for the year 2014 amounted to Euro 186.1 million, representing a decrease of 7.8% with respect to 2013.

The year 2014 was characterised by the continuation of the project for the relaunching of the foreign subsidiaries, which showed a significant growth in revenues, in particular (i) in Germany with the relaunching of T3P and the growth of Custom Synthesis, (ii) in the USA where the controlled substances business continued to expand, enabling it to compensate for the drop in turnover following the completion of the Macaba project, (iii) in France where the development of higher-margin products (Generics and CMO) led to an improvement in the profitability of Fine Chemicals (Generics and CMO), compensating for the decrease in the volumes of Generics. The lower revenues in Italy are attributable to contingent situations linked to the cyclical nature of certain Generics products, as illustrated in greater detail in the section “Business Performance”.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 15 |

“Other income and revenues” rose from Euro 1,094 thousand in the year 2013 to Euro 2,761 thousand in the year 2014, due principally to the effect of the revenues related to product development or regulatory activities or to other services commissioned by sector customers.

The significant reduction in the consumption of raw materials and work in progress was due to (i) the drop in sales revenues, (ii) the improvement in production mix and (iii) the improvement in the management of stock levels.

The added value (Gross Margin) relative to the year 2014 amounted to Euro 115,937 thousand, compared to Euro 121,220 thousand in the previous year.

The decrease in personnel costs is due to the implementation of the voluntary early retirement procedure and to efficiency measures implemented, offset in part by the strengthening of the managerial and business structures, as indicated in the paragraph “Significant events during the year”.

| Personnel costs | 31 December 2014 | 31 December 2013 | Variation | |||||||||||||||||||||

| Euro/1000 | % | Euro/1000 | % | Euro/1000 | % | |||||||||||||||||||

| Italy | -35,414 | 66.0 | % | -36,476 | 62.7 | % | 1,062 | -2.9 | % | |||||||||||||||

| USA | -4,150 | 7.7 | % | -4,322 | 7.8 | % | 172 | -4.0 | % | |||||||||||||||

| Germany | -5,317 | 9.9 | % | -5,213 | 9.7 | % | -104 | 2.0 | % | |||||||||||||||

| France | -8,767 | 16.3 | % | -8,807 | 15.9 | % | 40 | -0.5 | % | |||||||||||||||

| UK | 0 | 0.0 | % | -160 | 3.9 | % | 160 | -100.0 | % | |||||||||||||||

| Total | -53,648 | 100.0 | % | -54,978 | 100.0 | % | 1,330 | -2.4 | % | |||||||||||||||

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 16 |

| Workforce | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Italy | 550 | 571 | -21 | |||||||||

| France | 146 | 146 | 0 | |||||||||

| Germany | 66 | 64 | 2 | |||||||||

| UK | 0 | 0 | 0 | |||||||||

| USA | 73 | 74 | -1 | |||||||||

| Total | 835 | 855 | -20 | |||||||||

| Workforce | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Managers | 24 | 23 | 1 | |||||||||

| Supervisory staff | 115 | 113 | 2 | |||||||||

| Clerical staff | 294 | 305 | -11 | |||||||||

| Manual workers | 402 | 414 | -12 | |||||||||

| Total | 835 | 855 | -20 | |||||||||

The decrease in Other operating costs is due principally to the reduction in the volume of production. Significant savings were also made in the cost of services rendered by third parties, in particular for environmental costs and utilities.

The gross operating result (EBITDA) for the year 2014 is substantially in line with that of the year 2013, given that the effect of the drop in sales volumes was partially offset by the reduction in manufacturing costs.

The “Adjusted” EBITDA, or rather, the EBITDA before non-recurring income and expenses, shows a decrease of Euro 7,597 thousand, dropping from Euro 31,164 thousand at 31 December 2013 to Euro 23,567 thousand at 31 December 2014.

The decrease of Euro 490 thousand in Depreciation, amortisation and write downs is linked to the significant write downs charged to the income statement in the year 2013 mainly as a result of (i) the placing into liquidation of the UK subsidiary in July 2013 and (ii) the write-down of the carrying value of the minority shareholding in the Swiss company Pharmintraco Sagl: The write downs for the year 2014 regarded (i) the write-down of the carrying value of the assets available for sale in accordance with the industrial rationalisation project identified in the New Strategic Plan, as detailed in the paragraph “Significant events after the year-end and Business outlook” and (ii) the write-down in the value of certain R&D costs linked to projects no longer considered to be of strategic importance for the Group.

The Financial income and expenses are in line with the previous year. The net financial expenses decreased due to the effect of the lower average financial debt during the year. This heading was positively influenced by the gains on exchange, due in particular to the strengthening/revaluation of the US dollar against the Euro. The other financial expenses relate to the discounting to present value of the provision for environmental risks in the USA.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 17 |

| Net financial expenses | 31 December 2014 | 31 December 2013 | Variation | |||||||||||||||||||||

| Euro/1000 | Euro/1000 | Euro/1000 | % | |||||||||||||||||||||

| Financial income | 11 | -0.2 | % | 8 | -0.1 | % | 3 | 33.8 | % | |||||||||||||||

| Financial charges | -4,722 | 75.8 | % | -5,778 | 94.9 | % | 1,056 | -18.3 | % | |||||||||||||||

| Exchange differences | 890 | -14.3 | % | -619 | 10.2 | % | 1,509 | -243.7 | % | |||||||||||||||

| Other charges | -2,411 | 38.7 | % | 299 | -4.9 | % | -2,710 | -906.5 | % | |||||||||||||||

| Total | -6,233 | 100.0 | % | -6,090 | 100.0 | % | -142 | 2.3 | % | |||||||||||||||

The Income tax shows a tax credit for the year of Euro 1,889 thousand, due to the deferred tax assets recorded by the subsidiary Euticals SpA in consideration of the expected future recovery of prior year tax losses in view of the forecasts of future profitability in the New Plan, as described in greater detail in the Explanatory Notes to the Consolidated Financial Statements.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 18 |

Analysis of the Group’s equity and financial situation

The table below shows the reclassified and condensed balance sheet of the Lauro Cinquantasette Group at 31 December 2014 and at 31 December 2013, in thousands of euro.

| Balance Sheet | 31 December 2014 | 31 December 2013 | Variation | % Variation | ||||||||||||

| Intangible assets | 117,839 | 116,282 | 1,557 | 1.3 | % | |||||||||||

| Property, plant and equipment | 77,152 | 86,426 | -9,274 | -10.7 | % | |||||||||||

| Financial fixed assets | 1,816 | 1,844 | -27 | -1.5 | % | |||||||||||

| Total Fixed Assets | 196,808 | 204,552 | -7,745 | -3.8 | % | |||||||||||

| Inventories | 64,291 | 73,478 | -9,187 | -12.5 | % | |||||||||||

| Trade receivables | 42,241 | 50,198 | -7,957 | -15.9 | % | |||||||||||

| Other current assets | 20,651 | 13,417 | 0 | |||||||||||||

| CAPITAL INVESTED | 323,991 | 341,646 | -17,655 | -5.2 | % | |||||||||||

| NET FINANCIAL DEBT | -82,114 | -88,186 | 6,072 | -6.9 | % | |||||||||||

| Shareholders’ equity | -172,950 | -178,415 | 5,465 | -3.1 | % | |||||||||||

| Medium/long term liabilities | -18,685 | -16,574 | -2,111 | 12.7 | % | |||||||||||

| Trade payables | -30,038 | -38,785 | 8,747 | -22.6 | % | |||||||||||

| Short term liabilities | -20,204 | -19,686 | -518 | 2.6 | % | |||||||||||

| SOURCES OF FINANCE | -323,991 | -341,646 | 17,655 | -5.2 | % | |||||||||||

The variation in fixed assets, net of the amortisation and depreciation charge for the year, is linked principally to the following:

| - | to the investments in Research and Development which amounted to Euro 4,957 thousand. |

| - | to the investments in Property, plant and equipment for a total of Euro 8,069 thousand, related principally to work carried out to comply with environmental protection and safety legislation and with REACH regulations, and for the revamping of the manufacturing sites and for the increase in production capacity. |

The tables below give details of the capital expenditure carried out during the period, analysed by geographic area and by the principal Italian manufacturing plants.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 19 |

Italy

| Capital expenditure | Year | Year | ||||||

| (in thousands of Euro) | 2014 | 2013 | ||||||

| Lodi | 1,264 | 2,068 | ||||||

| Varese | 149 | 183 | ||||||

| Ambrosia | 169 | 10 | ||||||

| Casaletto | 284 | 1,016 | ||||||

| Rozzano | 909 | 789 | ||||||

| Origgio | 2,402 | 1,621 | ||||||

| Chorisis Srl | 55 | - | ||||||

| TOTAL | 5,232 | 5,688 | ||||||

| Investments (in thousands of Euro) | Year 2014 | Year 2013 | ||||||

| ESHA | 1,423 | 2,089 | ||||||

| Revamping | 1,667 | 3,022 | ||||||

| R&D (tangible) | - | - | ||||||

| Production Capacity | 1,052 | 471 | ||||||

| Quality | 1,044 | 78 | ||||||

| IT | 46 | 28 | ||||||

| TOTAL | 5,232 | 5,688 | ||||||

Lodi

Work was carried out to update the fire detection equipment and, in particular, the system of optical and acoustic alarm signals, with the aim of significantly improving the alarm system at the site. The containment measures necessary for the safety of the production of anti-cancer drugs have been completed through the purchase of isolation systems.

The compartmentalisation with HVAC (Heating, Ventilation and Air Conditioning) plant of the unloading area of the Sulphapiridine dryer and of the filter press for Sucralfate, comprising also the wet products unloading area, was carried out in accordance with the Iso 8 standards.

Extraordinary maintenance work was carried out at the plant regarding services, utilities, laboratories and production buildings, in order to improve compliance with health and safety standards.

Lastly, investments were made for the rectification plant for pyridine solvent, in order to replace the existing equipment.

Varese

The necessary work was carried out in preparation of the AIFA inspection. The TOC control system for the industrial wastewater has been replaced,

Work was carried out for the lining of cisterns and effluent tanks in order to increase the level of safety thereof.

In addition a tender has been launched for the purchase of a refrigeration unit in order to comply with the deadlines set for the utilisation of the R22 fluid.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 20 |

Casaletto

The capital expenditure at this site mainly regarded the extraordinary maintenance of the C5 centrifuge and work was carried out for the optimisation of the process plant.

Ambrosia

The principal capital expenditure at this site regarded the utilities, in particular an extraordinary revamping of the plant for the treatment of off-gasses (Post-combustor system), the purchase of an industrial refrigeration unit in order to comply with the deadlines set for the prohibition of the use of R22 fluid and the work necessary to obtain the Fire Prevention Certificate required by the authorities.

Rozzano - Quinto de’ Stampi

Capital expenditure at this site comprised mainly the purchase of a high containment level insulator filter for the High Potency production, an air compressor with a view to energy saving, while the equipment containing R22 has been replaced in order to comply with current legislation.

Work has begun to implement the changes requested by the AIFA following their inspection of the site; this work involves the realisation of an area for the Sampling and dispensing of raw materials in compliance with current legislative standards and the improvement of the existing sampling area at the finished products warehouse. This work shall be completed during the course of the year 2015.

As regards new products, the purchase and installation of equipment for the development of Limus have been completed.

Origgio

Significant engineering work was carried out at this site, aimed at satisfying both customers’ requirements and the legal quality standards.

In particular, a new finishing department was realised for Propofol, a bottom discharge centrifuge was installed in an ISO 8 clean room, the flooring and certain airlocks in the Minocycline finishing department have also been improved.

Also, as part of the measures to improve quality standards, a gap analysis was completed for the realisation of the necessary improvements in the Syntesis 1 finishing department.

In addition work was carried out for debottlenecking with a view to increasing the efficiency and the productive capacity of Minocycline.

As part of the process of compliance with the legislation relative to the R22 refrigeration units, purchase orders have been issued for the necessary equipment.

As regards IT systems, an infrastructural project has been developed for the entire Group which shall be implemented as from the year 2015.

Abroad

Capital expenditure (in thousands of Euro) | Year 2014 | Year 2013 | ||||||

| USA | 1,063 | 1,018 | ||||||

| France | 1,189 | 1,206 | ||||||

| Germany | 585 | 708 | ||||||

| TOTAL | 2,837 | 2,932 | ||||||

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 21 |

Capital expenditure (in thousands of Euro) | Year 2014 | Year 2013 | ||||||

| ESHA | 559 | 543 | ||||||

| Production Capacity | 1,127 | 1,267 | ||||||

| Revamping | 623 | 729 | ||||||

| Quality | 502 | 325 | ||||||

| IT | 26 | 68 | ||||||

| TOTAL | 2,837 | 2,932 | ||||||

France

The work carried out was aimed principally at obtaining the approval by the FDA of the Tonneins site, necessary for the expansion of this subsidiary’s business. In particular the following were carried out:

| - | the realisation of a centrifuge room in conformity with the quality standards for pharmaceutical chemical finished products, as required by the Authorities and by our customers. |

| - | revamping of the services, utilities and process equipment. The plants PLC systems have been revamped and work has commenced to improve the “solvent handling” procedures, as also requested by the Authorities, with a particular attention to the containment measures for the utilisation of POCL3. |

Environmental and safety work has been completed in order to meet safety standards for a scrubber and for the improvement of the collection tank for the waste water at the Tonneins site.

USA

The American subsidiary has carried out work throughout the entire plant aimed at Energy Saving and for the prevention of damages caused by caused by ice and frost.

It has also replaced various pieces of obsolete equipment such as vacuum pumps, pumps and condensers.

It has set up the R&D laboratory and the pilot plant for the manufacture of Regadenoson, including the purchase of a glove box insulator.

The project for an area of filtration, drying and finishing in the S28 building for API products has been completed and the investment for the debottlenecking of the pilot unit by means of the installation of a filter dryer in the S19 department has been authorised. This investment, which is considered as a Special Project due to its strategic importance, shall be completed in 2015.

Germany

The major capital expenditure during the year regarded the completion of the work carried out in order to increase production capacity for our main products.

The subsidiary also repaired and updated the main sewerage system and purchased a centrifuge as a first step towards increasing the production capacity for the CMO – CS projects. This latter project, which is of significant importance for the implementation of the Group’s strategy, shall be completed in the first six months of 2015.

**************

The table below shows the composition of net working capital as at 31 December 2014, together with the variations therein with respect to the previous year-end.

The decrease of Euro 1,681 thousand in net working capital is due to multiple factors, the more important of which are illustrated below.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 22 |

| Net working capital | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Euro/1000 | Euro/1000 | Euro/1000 | ||||||||||

| Inventories | 64,291 | 73,478 | -9,187 | |||||||||

| Trade receivables | 42,241 | 50,198 | -7,957 | |||||||||

| Trade payables | -30,038 | -38,785 | 8,747 | |||||||||

| Other current assets | 20,651 | 13,417 | 7,233 | |||||||||

| Other current liabilities | -20,204 | -19,686 | -518 | |||||||||

| Total | 76,941 | 78,622 | -1,681 | |||||||||

The value of Inventories, net of the relative provision for obsolescence, fell by Euro 9,187 thousand as a result of the following factors:

| (i) | the decrease in turnover volumes with respect to budget; |

| (ii) | the improvement in the planning process; |

| (iii) | the lower level of utilisation of production capacity; |

| (iv) | the variation in the provision for obsolescence, as detailed in paragraph 6.6 of the Explanatory Notes to the Consolidated Financial Statements. |

| Inventories | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Euro/1000 | Euro/1000 | Euro/1000 | ||||||||||

| Italy | 49,474 | 58,700 | -9,226 | |||||||||

| France | 6,325 | 6,827 | -502 | |||||||||

| Germany | 2,054 | 3,505 | -1,451 | |||||||||

| UK | 0 | 0 | ||||||||||

| USA | 7,019 | 5,117 | 1,902 | |||||||||

| Consolidation adjustments | -581 | -671 | 90 | |||||||||

| Total | 64,291 | 73,478 | -9,187 | |||||||||

The more significant decreases in inventory values were registered (i) in Italy, due principally to the effect of the increase of sales of the product T BOC , which contributed significantly to the increase in stock levels at the end of 2013 ; and (ii) in Germany, as a result of the significant increase in the volume of sales. In contrast, inventory levels in the USA showed a slight increase, in preparation for the sales of the first quarter of 2015.

The Receivables decreased by Euro 8 million as a result of (i) the drop in sales volumes as well as (ii) a more effective customer relations and credit collection management. In fact we would point out that the total value of overdue receivables has fallen from Euro 13 million at 31 December 2013 to Euro 4.7 million at 31 December 2014.

Net Financial Indebtedness fell by Euro 6.1 million. This decrease is principally due to a better management of trade receivables as well as to the sale of the minority shareholding in the company Pharmintraco Sagl which has brought a financial benefit of Euro 2.4 million.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 23 |

| Net Financial Position | 31 December 2014 | 31 December 2013 | Variation | |||||||||

| Euro/1000 | Euro/1000 | Euro/1000 | ||||||||||

| Cash and cash equivalents | 13,395 | 15,148 | -1,753 | |||||||||

| Current financial debt | -94,077 | -101,783 | 7,706 | |||||||||

| Non-current financial debt | -1,432 | -1,552 | 120 | |||||||||

| Total net indebtedness | -82,114 | -88,186 | 6,072 | |||||||||

The table below gives details of the Group’s net financial position:

| Net Financial Position | 31 December 2014 | 31 December 2013 | 01 January 2013 | |||||||||

| Cash and cash equivalents | -13,396 | -15,148 | -7,808 | |||||||||

| Short term loans | 93,656 | 100,764 | 99,691 | |||||||||

| Other current financial payables/(receivables) | 421 | 1,019 | 744 | |||||||||

| Current net financial position | 80,681 | 86,634 | 92,627 | |||||||||

| Long term loans | 0 | 0 | 0 | |||||||||

| Other non-current financial payables/(receivables) | 1,433 | 1,552 | 2,146 | |||||||||

| CAPITAL INVESTED | 82,114 | 88,186 | 94,773 | |||||||||

The “Other non-current financial payables/(receivables)” refer to payables for financial leasing contracts.

********************

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 24 |

Human Resources

The year 2014 was characterised principally by three events:

| - | the strengthening of the Corporate structure with the arrival of the new Managing Director; |

| - | the completion of the business structure of the Sales & Marketing (S&M) and Research and Development (R&D) departments ; |

| - | the closure of the voluntary redundancy procedure in the provinces of Lodi and Rozzano aimed at encouraging generational turnover in the relative manufacturing plants. |

The arrival of the new Managing Director, with an international background, has encouraged the globalisation of the Group’s corporate and business structure.

The Corporate structure was strengthened in the R&D area, where a greater emphasis was placed on planning, and a team was set up for the management of a pilot plant in Italy. In addition, a Global Project Manager was appointed at the beginning of the year 2015 for the Custom Synthesis and Custom Manufacturing products.

In the S&M structure the Group has employed (i) Area Managers in order to reinforce the staff dedicated to the North American, South American and Russian markets; (ii) Market Analysts for the analysis and monitoring of new products/markets.

In Italy, the completion of the voluntary procedure for generational turnover, carried out with the consensus of the trade union representatives, proved to be an effective and relatively inexpensive instrument.

This project had collected a very significant consensus and resulted in an effective reduction in costs due to the decision not to replace certain positions.

Personnel costs showed a decrease with respect to the year 2013, thanks to a strategy of cost control and to the active cooperation of every department within the Group.

From a legislative point of view, in Italy, 2014 was the year of the Jobs Act. Pending the implementative decree, this law was a source of great discussion and tension, especially regarding the abolition of article 18 of the Italian Constitution and the introduction of the employment contract with gradually increasing employee protection rights. The identity crisis of the trade unions is becoming increasingly apparent and leaves room for the more extremist fringes, even in the pharmaceutical chemicals sector, which has always in the past represented an example of constructive Industrial Relations.

In general the labour market varies greatly from country to country and is inevitably linked to the economic situation. The USA has experienced a strong recovery which has, in our case, led to a high turnover; Germany and France are starting to show signs of recovery while Italy is still lagging behind, hoping to finally benefit from the long-awaited economic boost.

Overall, the year 2014 proved to be a constructive one, especially from a structural point of view. The Group has completely changed its organisation and the composition of its staff, enabling it to redefine its structure and acquiring new highly qualified and experienced professionals from outwith the Group and giving, therefore, a new boost to the desire for corporate growth.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 25 |

Workforce at 31 December 2014

| Manufacturing site | Managers | Supervisors | Clerical staff | Manual work | Total workforce | Internships | ||||||

| Ambrosia | 0 | 3 | 2 | 5 | 10 | 0 | ||||||

| Casaletto | 1 | 2 | 20 | 26 | 49 | 0 | ||||||

| Rozzano QDS | 9 | 20 | 56 | 57 | 142 | 0 | ||||||

| Lodi | 2 | 8 | 39 | 47 | 96 | 0 | ||||||

| Origgio | 6 | 29 | 96 | 92 | 223 | 0 | ||||||

| Varese | 1 | 5 | 16 | 8 | 30 | 0 | ||||||

| Italy Total | 19 | 67 | 229 | 235 | 550 | 0 | ||||||

| France Be | 1 | 23 | 9 | 74 | 107 | 0 | ||||||

| France To | 0 | 1 | 5 | 31 | 37 | 0 | ||||||

| France Paris | 0 | 1 | 1 | 0 | 2 | 0 | ||||||

| Frankfurt | 3 | 7 | 29 | 27 | 66 | 3 | ||||||

| Us Springfield | 1 | 16 | 21 | 35 | 73 | 1 | ||||||

| Uk SandyCroft | 0 | 0 | 0 | 0 | 0 | 0 | ||||||

| Foreign Total | 5 | 48 | 65 | 167 | 285 | 4 | ||||||

| Group Total | 24 | 115 | 294 | 402 | 835 | 4 |

Workforce at 31 dicembre 2013

| Manufacturing site | Managers | Supervisors | Clerical staff | Manual work | Total workforce | Internship | ||||||

| Ambrosia | 0 | 4 | 2 | 7 | 13 | 0 | ||||||

| Casaletto | 0 | 3 | 20 | 28 | 51 | 0 | ||||||

| Rozzano QDS | 8 | 18 | 61 | 49 | 136 | 0 | ||||||

| Lodi | 1 | 11 | 43 | 61 | 116 | 0 | ||||||

| Origgio | 7 | 28 | 95 | 92 | 222 | 0 | ||||||

| Varese | 2 | 3 | 20 | 8 | 33 | 0 | ||||||

| Italy Total | 18 | 67 | 241 | 245 | 571 | 0 | ||||||

| France Be | 1 | 23 | 9 | 74 | 107 | 0 | ||||||

| France To | 0 | 1 | 5 | 31 | 37 | 0 | ||||||

| France Paris | 0 | 1 | 1 | 0 | 2 | 0 | ||||||

| Frankfurt | 3 | 5 | 29 | 27 | 64 | 2 | ||||||

| Us Springfield | 1 | 16 | 20 | 37 | 74 | 1 | ||||||

| Uk SandyCroft | 0 | 0 | 0 | 0 | 0 | 0 | ||||||

| Foreign Total | 5 | 46 | 64 | 169 | 284 | 3 | ||||||

| Group Total | 23 | 113 | 305 | 414 | 855 | 3 |

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 26 |

Health, safety and the environment

In Italy certain critical safety procedures have been reviewed and, where necessary, updated and integrated.

The Group has identified the priority areas of its plants on which to intervene in order to guarantee the continual improvement of the safety and environmental compliance for all of the Group’s sites.

At the Casaletto site the action requested by the authorities has been integrated into the project for the reclamation of the land and the analytical results recorded to date confirm the progress achieved.

The inspection of the safety management system at the Lodi site, pursuant to Law No. 334, led to the creation of a plan of action that is already being carried out.

The necessary steps have been undertaken in order to obtain the CPI (Fire Prevention Certificate) for the Rozzano – Ambrosia plant.

The Rozzano site was awarded the renewal of its CPI (Fire Prevention Certificate) and the Origgio site was also awarded the CPI certificate.

The renewal of the (Integrated Pollution Prevention and Control) certification was obtained for Lodi and Casaletto, while the Rozzano (Quinto De Stampi and Ambrosia) and Origgio sites are undergoing investigation by the appointed authorities and MSDS and OEL safety analyses were carried out on certain processes in order to programme any improvements required.

The 18001 Health and safety management system certification has been obtained for the Origgio plant,which has also passed the controls carried out during the surveillance period, while the Rozzano site has also adopted a health and safety management system in line with OHSAS 18001 standard.

On 22 January 2015 a fatal accident took place at the Euticals Varese manufacturing plant, involving an employee working in the production plant.

Euticals, with the support of the Press Office of Federchimica, issued a statement to the press that same night, in which it expressed its sorrow for the event, its solidarity with the family and it confirmed its intention to fully collaborate in identifying the cause of the accident. Euticals also halted production at the site in question.

In the weeks following the accident, the local ASL conducted a series of interviews with the persons involved, as a result of which it prescribed certain operational measures to be carried out and issued various fines following the ascertainment of certain violations (the total sum for all of the persons interested parties amounted to less than Euro 20 thousand).

The reconstruction of the event and the allegations formalised have been transmitted to the appropriate authorities appointed for the definition of the framework of the investigation and the eventual legal action to be taken against the persons/entities involved.

Euticals has appointed prominent consultants from the Politecnico di Milano to carry out a risks assessment and a study of the measures to be carried out on machinery in order to minimise the risks associated with the use of the equipment.

As regards the US sites, the subsidiary is continuing to keep the appropriate authorities informed regarding the status of the land reclamation project.

In addition, safety analyses have been carried out on certain production processes, such as for example Regadenoson.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 27 |

The French manufacturing site completed a “gap analysis” with regard to the corporate guidelines programming the relative measures required to conform thereto and the regulatory requirements were implemented in full.

In general the updating of the material data safety sheets (MSDS) was carried out at all of the Group’s manufacturing sites.

The EHS audits carried out with customers showed positive results in terms of compliance and of management at both Group and local levels. The monitoring activities carried out have confirmed the level of compliance requested.

Risks Assessment

The principal risks and uncertainties to which the Group is exposed are described below.

Credit risk

The Group’s capacity to operate and to fulfil its obligations towards the banking system and towards its suppliers is dependent upon the regular cash flows deriving from the payments received from customers. The Group has always carried out a careful monitoring of trade receivables and has reduced to a minimum the positions of risk, the nominal values of which have, however, been written down to estimated realisable value. On these grounds and in consideration of the fact that the default rate for trade receivables is lower than 1%, the Group has not adopted any external measures for hedging against credit risk.

As a result of the financial embargo imposed on Iran by the OFAC at the beginning of the year 2012, the credit risk towards customers was highly concentrated on the receivables due from Iranian customers. At 31 December 2012 Euticals Spa had a gross exposure towards Iranian customers of approximately Euro 9 million, against which a specific provision for bad debts of Euro 3 million had been accrued.

We would point out that at 31 December 2014 the Group’s credit collection process had enabled it to collect the entire balance of the overdue receivable from its Iranian customers.

Further information is provided in paragraph 3 of the Explanatory Notes to the Consolidated Financial Statements.

Liquidity risk

Liquidity risk represents the risk that the available financial resources may be insufficient to cover commitments due and includes the risk that lenders who have granted loans and/or credit facilities may request the repayment thereof. Upon the entrance of a leading investment company as a shareholder at the beginning of the year 2012, the Group renegotiated the terms of the contracts signed with the Pool of banks in February 2011.

During the year the Group continued negotiations with the Pool of banks aimed principally at the rescheduling of the repayment plan.

As illustrated in the paragraph “Significant events after the year-end and Business Outlook”, on 1 April 2015 Euticals and the banks in the Pool signed an agreement amending the 2011 loan contract; this agreement specifies, amongst other things, the significant reduction in the repayment instalment foreseen for the year 2015, providing an increase in the liquidity available for normal business operations and for the projects of restructuring and of business development.

In general, the financial management function continues to place great importance on the management of cash flows and of financial debt, seeking to maximise the cash flows generated from operations. This has enabled us to reimburse all of the loans which matured during the year 2014.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 28 |

Therefore, at the moment the Group’s access to financial sources is sufficient to cover its requirements.

With regard to the failure, at 31 December 2014, to respect the financial parameters specified in the loan contract, reference should be made to the paragraph “Evaluation of business going concern” below and to the further comments contained in the Explanatory Notes to the Consolidated Financial Statements.

Market risks

Interest rate risk

The interest charged on the loans and other credit facilities provided by the banking system are almost entirely linked to the Euribor 3 monthly or 6 monthly rates. At 31 December 2014, the Group’s exposure with the Pool of banks on medium-long term “amortising” loans has been partially hedged through the utilisation of IRS contracts.

Further information is provided in paragraph 3 of the Explanatory Notes to the Consolidated Financial Statements.

Exchange rate risk

Approximately 40% of the Group’s turnover takes place with countries in the US dollar zone and therefore it is subject to exchange rate risk. In order to reduce the risk deriving its exposure to fluctuations in Exchange rates, the Group has adopted hedging measures through the recourse to bank borrowings and invoicing from suppliers denominated in US dollars.

Further information is provided in paragraph 3 of the Explanatory Notes to the Consolidated Financial Statements.

Product risk

The Group has evaluated the risk linked to the non-conformity of its products to be relatively remote, based on its past experience and on its high levels of customer satisfaction. However the Group has stipulated specific insurance policies that adequately cover the Group against the possible occurrence of such risk and that are subject to review on an annual basis.

Risks linked to the legislative and regulatory evolution in the pharmaceutical sector

The pharmaceuticals sector is characterised by a high level of local, national and international regulation that has an effect at all levels of the Group’s business. The pharmaceuticals sector is also subject to national and international technical legislation governing the research, development, manufacture and distribution of pharmaceuticals and the relative scientific information disclosure requirements. The Group carries out a policy of constant monitoring of the legislative developments in all of the markets in which it operates in order to indentify changes and adapt thereto in a timely and appropriate manner.

Emerging country risk

The Group strategy for the future includes the expansion of its activities into emerging economies with a high potential for future development and characterised by solid rates of growth (e.g. Central and Eastern Europe, Middle East and North Africa). These countries could present risks linked to the political instability and economic, currency, legislative or fiscal uncertainty.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 29 |

Competitive risk

Just like any other company operating in the pharmaceuticals sector, the Group is subject to competition from other products that could lead to a reduction of its market share. The Group manages this risk by adopting a policy of progressive diversification and enrichment of its product portfolio, in order to reduce its dependence upon a limited number of products. In the pharmaceuticals sector there exists the risk that delays in the process of development or of the granting of the necessary authorisation by the Regulatory Authorities could prevent the Group from fulfilling the planned time schedules for the launch of new products, with a consequent potential impact on the profitability of these products and/or delays in the achievement of the budgeted growth objectives. In order to mitigate such risk, the Group adopts both a strategy of the enrichment and balancing of its pipeline of products between products linked to dossiers still in the registration phase and products already registered and yet others at different stages of development, as well as strategies of geographical diversification designed to limit the Group’s dependency upon the Regulatory Authorities of any single country.

Evaluation of business going concern

As illustrated in the previous paragraphs of this Directors’ Report, the continuation of the difficult economic situation and the increased complexity and international nature of the Lauro Cinquantasette Group prevented the Group from fully respecting its financial parameters in previous years. These factors also had a negative influence on the results for the year 2014, which were lower than those forecast in the 2014-2018 Strategic Business Plan attached to the Amending Agreement signed in the year 2012 (hereinafter referred to as the “Original Plan”) and to the financial parameters indicated in the draft of the Amending Agreement to the loan contract linked to the Original Plan.

In accordance with the terms of the loan contract, following the failure by the Group to respect the abovementioned financial parameters, the lender banks would have had the right to demand the immediate repayment of the entire loan amount.

In view of the evolution of the business during the last year, the Board of Directors of Euticals has undertaken a series of steps, in particular:

| - | the strengthening of the internal functions and the rationalisation of the organisational structure, in order to render it more efficient and more appropriate to the current requirements, dimensions and operations of the Group. |

| - | The revision of the Original Plan and preparation of an updated Plan, approved by the Board of Directors on 4 November 2014 (“New Plan”), aimed at identifying the industrial and financial intervention considered necessary in order to achieve a balance and to redefine the growth strategy. |

| - | The launch, as from November 2014 of the review of the existing agreements regarding the financial operations with the Pool of banks. |

In particular, among the various financial measures considered necessary in order to fulfil the revised liquidity requirements for the years 2015 and 2016, the New Plan foresees the recourse to further sources of finance, to be obtained (i) by means of the recapitalisation, by the shareholders, of the parent company and of the subsidiary Euticals Spa; and (ii) through the remodelling of the loan repayment plan and the prolonging/extension of the repayment period.

On 31 March 2015 Euticals received confirmation of the unanimous resolution by the Pool of Banks approving (i) the waiver of the right to the penalties prescribed for the failure to comply with certain contractual clauses; (ii) the request for amendments to the loan contract.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 30 |

On 1 April 2015 Euticals and the Pool of Banks signed an agreement containing amendments to the terms of the original loan contract stipulated in the year 2011 (hereinafter referred to as the “Amending Agreement”).

The more significant terms and conditions of the Amending Agreement are shown below:

| A) | Rescheduling of the debt |

The Amending Agreement foresees the rescheduling of the loan repayment plan as follows:

| Year (in millions of Euro) | Repayment instalments Amending Agreement | Repayment instalments Original Contract | ||||||

| 2015 | 2.0 | 13.9 | ||||||

| 2016 | 2.5 | 35 | ||||||

| 2017 | 9.5 | 13.6 | ||||||

| 2018 | 17.5 | - | ||||||

| 2019 | 19.5 | - | ||||||

| 2020 | 11.5 | - | ||||||

| Total | 62.5 | 62.5 | ||||||

| B) | Financial parameters |

The Amending Agreement foresees the revision, in conformity with the New Plan, of the financial parameters on which to measure the Group’s performance during the loan repayment period as indicated in point A).

| C) | Capitalisation |

The Amending Agreement contains the obligation for the financial shareholders to underwrite a share capital increase in the Parent company, to be used for the capitalisation of the subsidiary Euticals, (i) of Euro 12.5 million, to be paid in at the time of the stipulation of the Amending Agreement, following the explicit waiver on the part of the Pool of Banks to the obligatory advance repayment of the loan received, as foreseen by the original loan contract; (ii) of a further Euro 5 million, to be paid in the event of the non-occurrence of certain events specified in the Amending Agreement.

On 15 April 2015, in accordance with the terms of the Amending Agreement, the financial shareholders of Lauro Cinquantasette Spa paid in the share capital increase of Euro 12.5 million. This sum was immediately paid by the parent company to the subsidiary Euticals in the form of increase in equity reserves.

In consideration of the above, the Directors of Lauro Cinquantasette and of Euticals have prepared the financial statements on a going concern basis.

The Group is proceeding with the path of industrial restructuring outlined in the New Plan, as described in greater detail in the paragraph “Significant events after the year-end and Business outlook”.

In consideration of the above, the table below shows the net indebtedness according to the terms of the current loan agreement and, in the column “Pro-forma at 31 December 2014” we show the expected effects of the rescheduling of the loan repayments:

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 31 |

| Net Financial Position | 31 December 2014 | 31 December 2014 | 31 December 2013 | |||||||||

| proforma - Euro/1000 | Euro/1000 | Euro/1000 | ||||||||||

| Cash and cash equivalents | 13,395 | 13,395 | 15,148 | |||||||||

| Current financial debt | -33,851 | -94,077 | -101,783 | |||||||||

| Non-current financial debt | -61,658 | -1,432 | -1,552 | |||||||||

| Total | -82,114 | -82,114 | -88,186 | |||||||||

Transactions with Group companies and Other related parties

All of the commercial and financial transactions between the Group companies during the year 2014 took place on an arm’s length basis at normal market conditions.

No significant transactions took place with other related parties.

Further information is provided in Note 6.27 of the Explanatory Notes to the Consolidated Financial Statements.

Own shares

The Company does not hold any own shares.

Derivative Financial Instruments

In accordance with the requirements of art. 2428, paragraph 3, point 6-bis of the Italian Civil Code, we inform you that on 12 May 2011 the Company stipulated a hedging contract against the risk of fluctuations in the interest rates (Euribor 3 months + Spread) on certain components of the Loan which matures on 31 December 2016. Reference should be made to Note 2.4 of the Explanatory Notes to the Consolidated Financial Statements for a detailed description of the characteristics and value of the derivate instruments as at 31 December 2014.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 32 |

Significant events after the year-end and Business outlook.

On 22 January 2015 a fatal accident took place at the Euticals Varese manufacturing plant, involving an employee working in the production plant.

Euticals, with the support of the Press Office of Federchimica, issued a statement to the press that same night, in which it expressed its sorrow for the event, its solidarity with the family and it confirmed its intention to fully collaborate in identifying the cause of the accident. Euticals also halted production at the site in question.

In the weeks following the accident, the local ASL conducted a series of interviews with the persons involved, as a result of which it prescribed certain operational measures to be carried out and issued various fines following the ascertainment of certain violations (the total sum for all of the persons interested parties amounted to less than Euro 20 thousand).

The reconstruction of the event and the allegations formalised have been transmitted to the appropriate authorities appointed for the definition of the framework of the investigation and the eventual legal action to be taken against the persons/entities involved.

Euticals has (i) appointed prominent consultants from the Politecnico di Milano to carry out a risks assessment and a study of the work to be carried out on machinery in order to minimise the risks associated with the use of the equipment, (ii) activated the insurance guarantees and (iii) as from 25 February has launched a back-up production plan at another Italian manufacturing plant in order to overcome the possibility of being unable to recommence production at the Varese plant in the short term. It should be noted that the production suspended accounts for approximately 5 million of total annual turnover.

From a financial point of view, on 13 February 2015 the Shareholders’ meeting of Lauro Cinquantasette resolved a share capital increase of Euro 17.5 million, to be paid in as specified in the paragraph “Evaluation of Business going concern”, necessary for the achievement of the objectives of the New Plan and to the reaching of an agreement to amend the terms of the contract for the loan with the Pool of Banks.

On 31 March 2015 Euticals received confirmation of the unanimous resolution by the Pool of Banks approving (i) the waiver by the banks of the covenant penalties for the failure to comply with certain contractual clauses; (ii) the request for amendments to the loan contract.

On 1 April 2015 Euticals and the Pool of Banks signed an agreement modifying the original loan contract stipulated in 2011 (hereinafter referred to as the “Amending Agreement”).

On 15 April 2015, in accordance with the terms of the Amending Agreement, the institutional investor shareholders of Lauro Cinquantasette Spa paid in the share capital increase of Euro 12.5 million. This sum was immediately paid by the parent company to the subsidiary Euticals in the form of an increase in the subsidiary’s equity reserves.

| Gruppo Lauro Cinquantasette – Bilancio consolidato al 31 dicembre 2014 | Pag. 33 |

From a strategic and industrial point of view, as part of the implementation of the New Plan, the Group is in the process of finalising the activities necessary for the sale of the first manufacturing plant to a leading company in the pharmaceuticals market interested in an Italian manufacturing plant for its own production.