UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2014

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 1-14287

USEC Inc.

Delaware | 52-2107911 |

(State of incorporation) | (I.R.S. Employer Identification No.) |

Two Democracy Center

6903 Rockledge Drive, Bethesda, Maryland 20817

(301) 564-3200

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | o | Accelerated filer | o | |

Non-accelerated filer | o | Smaller reporting company | ý | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No ý

As of April 30, 2014, there were 4,945,549 shares of the registrant’s Common Stock issued and outstanding.

TABLE OF CONTENTS

Page | ||

PART I – FINANCIAL INFORMATION | ||

Item 1. | Financial Statements: | |

PART II – OTHER INFORMATION | ||

This quarterly report on Form 10-Q, including “Management's Discussion and Analysis of Financial Condition and Results of Operations” in Part I, Item 2, contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934 - that is, statements related to future events. In this context, forward-looking statements may address our expected future business and financial performance, and often contain words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “will” and other words of similar meaning. Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For USEC, particular risks and uncertainties that could cause our actual future results to differ materially from those expressed in our forward-looking statements include, but are not limited to the impact of and risks related to USEC Inc.'s “pre-arranged” case under Chapter 11 of the bankruptcy code including risks related to obtaining approval and confirmation of USEC Inc.’s plan of reorganization, the impact of any delay or inability in obtaining such confirmation, the impact of a potential de-listing of our common stock on the NYSE, and the impact of our restructuring on the holders of our common stock, preferred stock and convertible notes; risks related to the ongoing transition of our business, including the impact of our ceasing enrichment at the Paducah gaseous diffusion plant and uncertainty regarding our ability to deploy the American Centrifuge project; uncertainty regarding funding for the American Centrifuge project and the potential for a demobilization or termination of the American Centrifuge project if additional government funding is not provided during the term of the agreement with UT-Battelle, LLC, the management and operating contractor for the Oak Ridge National Laboratory ("ORNL") for continued research, development and demonstration of the American Centrifuge technology (the "ACTDO Agreement"), including for any option periods, or upon completion of such agreement; risks related to our ability to perform the work required under the ACTDO Agreement at a cost that does not exceed the firm fixed funding provided thereunder; the impact of actions we have taken or may take (including as a result of the reduction in scope of work under the ACTDO Agreement) to reduce spending on the American Centrifuge project, including the potential loss of key suppliers

2

and employees, impacts to cost and schedule and the ability to remobilize for commercial deployment of the American Centrifuge plant, impacts on our liquidity as a result of demobilization or termination liabilities, and potential impacts on our proposed plan of reorganization; risks related to the underfunding of our defined benefit pension plans and potential actions the Pension Benefit Guarantee Corporation could pursue in connection with ceasing enrichment at the gaseous diffusion plants or with any demobilization or termination of the American Centrifuge project; the impact of uncertainty regarding our ability to continue as a going concern on our liquidity and prospects; our ability to reach an agreement with the U.S. Department of Energy (“DOE”) regarding the transition of the Paducah gaseous diffusion plant and uncertainties regarding the transition costs and other impacts of USEC ceasing enrichment at the Paducah gaseous diffusion plant and returning the plant to DOE; the continued impact of the March 2011 earthquake and tsunami in Japan on the nuclear industry and on our business, results of operations and prospects; the impact and potential extended duration of the current supply/demand imbalance in the market for low enriched uranium (“LEU”); the impact of enrichment market conditions, increased project costs and other factors on the economic viability of the American Centrifuge project without additional government support and on our ability to finance the project and the potential for a demobilization or termination of the project; uncertainty concerning the ultimate success of our efforts to obtain a loan guarantee from DOE and/or other financing for the American Centrifuge project or additional government support for the project and the timing and terms thereof; the dependency of government funding or other government support for the American Centrifuge project on Congressional appropriations or on actions by DOE or Congress; potential changes in our anticipated ownership of or role in the American Centrifuge project, including as a result of our role as a subcontractor to ORNL or as a result of the need to raise additional capital to finance the project in the future; the potential for DOE to seek to terminate or exercise its remedies under the 2002 DOE-USEC agreement; changes in U.S. government priorities and the availability of government funding or support, including loan guarantees; risks related to our ability to manage our liquidity without a credit facility; our dependence on deliveries of LEU from Russia under a commercial supply agreement (the “Russian Supply Agreement”) with a Russian government entity known as Techsnabexport (“TENEX”) and limitations on our ability to import the Russian LEU we buy under the Russian Supply Agreement into the United States and other countries; risks related to actions that may be taken by the U.S. Government, the Russian Government or other governments that could affect our ability or the ability of TENEX to perform the Russian Supply Agreement, including the imposition of sanctions, restrictions or other requirements; risks related to our ability to sell the LEU we procure under our fixed purchase obligations under the Russian Supply Agreement; the decrease or elimination of duties charged on imports of foreign-produced LEU; pricing trends and demand in the uranium and enrichment markets and their impact on our profitability; movement and timing of customer orders; changes to, or termination of, our agreements with the U.S. government; risks related to delays in payment for our contract services work performed for DOE, including our ability to resolve certified claims for payment filed by USEC under the Contracts Dispute Act; the impact of government regulation by DOE and the U.S. Nuclear Regulatory Commission; the outcome of legal proceedings and other contingencies (including lawsuits and government investigations or audits); the competitive environment for our products and services; changes in the nuclear energy industry; the impact of volatile financial market conditions on our business, liquidity, prospects, pension assets and credit and insurance facilities; the timing of recognition of previously deferred revenue; and other risks and uncertainties discussed in this and our other filings with the Securities and Exchange Commission, including our Annual Report on Form 10-K for the year ended December 31, 2013 (“10-K”). Revenue and operating results can fluctuate significantly from quarter to quarter, and in some cases, year to year. For a discussion of these risks and uncertainties and other factors that may affect our future results, please see Item 1A entitled “Risk Factors” and the other sections of this report and our 10-K, which are available on our website at www.usec.com. Readers are urged to carefully review and consider the various disclosures made in this report and in our other filings with the Securities and Exchange Commission that attempt to advise interested parties of the risks and factors that may affect our business. We do not undertake to update our forward-looking statements to reflect events or circumstances that may arise after the date of this quarterly report on Form 10-Q except as required by law.

3

USEC Inc.

(DEBTOR-IN-POSSESSION)

CONSOLIDATED CONDENSED BALANCE SHEETS

(Unaudited)

(millions)

March 31, 2014 | December 31, 2013 | ||||||

ASSETS | |||||||

Current Assets | |||||||

Cash and cash equivalents | $ | 85.1 | $ | 314.2 | |||

Accounts receivable, net | 38.0 | 163.0 | |||||

Inventories | 571.7 | 967.6 | |||||

Deferred costs associated with deferred revenue | 80.9 | 165.5 | |||||

Other current assets | 20.0 | 21.7 | |||||

Total current assets | 795.7 | 1,632.0 | |||||

Property, plant and equipment, net | 5.2 | 7.9 | |||||

Deposits for surety bonds | 39.2 | 39.8 | |||||

Other long-term assets | 25.8 | 25.8 | |||||

Total Assets | $ | 865.9 | $ | 1,705.5 | |||

LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) | |||||||

Current Liabilities | |||||||

Accounts payable and accrued liabilities | $ | 94.3 | $ | 114.5 | |||

Payables under Russian Contract | — | 340.7 | |||||

Inventories owed to customers and suppliers | 157.4 | 499.7 | |||||

Deferred revenue | 105.6 | 195.9 | |||||

Convertible senior notes | — | 530.0 | |||||

Convertible preferred stock | — | 113.9 | |||||

Total current liabilities | 357.3 | 1,794.7 | |||||

Postretirement health and life benefit obligations | 198.0 | 195.0 | |||||

Pension benefit liabilities | 113.8 | 121.2 | |||||

Other long-term liabilities | 51.7 | 52.8 | |||||

Liabilities subject to compromise | 653.6 | — | |||||

Total Liabilities | 1,374.4 | 2,163.7 | |||||

Commitments and Contingencies (Note 15) | |||||||

Stockholders’ Equity (Deficit) | (508.5 | ) | (458.2 | ) | |||

Total Liabilities and Stockholders’ Equity (Deficit) | $ | 865.9 | $ | 1,705.5 | |||

See notes to consolidated condensed financial statements.

4

USEC Inc.

(DEBTOR-IN-POSSESSION)

CONSOLIDATED CONDENSED STATEMENTS OF OPERATIONS

(Unaudited)

(millions, except per share data)

Three Months Ended March 31, | |||||||

2014 | 2013 | ||||||

Revenue: | |||||||

Separative work units | $ | 145.6 | $ | 290.2 | |||

Uranium | — | 27.6 | |||||

Contract services | 3.0 | 2.6 | |||||

Total revenue | 148.6 | 320.4 | |||||

Cost of Sales: | |||||||

Separative work units and uranium | 165.3 | 303.8 | |||||

Contract services | 4.2 | 3.3 | |||||

Total cost of sales | 169.5 | 307.1 | |||||

Gross profit (loss) | (20.9 | ) | 13.3 | ||||

Advanced technology costs | 33.3 | 59.3 | |||||

Selling, general and administrative | 11.7 | 12.9 | |||||

Special charges (credit) for workforce reductions and advisory costs | (0.5 | ) | 2.4 | ||||

Other (income) | (26.2 | ) | (47.6 | ) | |||

Operating (loss) | (39.2 | ) | (13.7 | ) | |||

Interest expense | 4.6 | 13.3 | |||||

Interest (income) | (0.4 | ) | (0.3 | ) | |||

Reorganization items, net | 8.4 | — | |||||

(Loss) from continuing operations before income taxes | (51.8 | ) | (26.7 | ) | |||

Provision (benefit) for income taxes | (1.0 | ) | (3.0 | ) | |||

Net (loss) from continuing operations | (50.8 | ) | (23.7 | ) | |||

Net income from discontinued operations | — | 21.7 | |||||

Net (loss) | $ | (50.8 | ) | $ | (2.0 | ) | |

Net income (loss) per share (Note 14): | |||||||

Net (loss) from continuing operations per share – basic and diluted | $ | (10.37 | ) | $ | (4.84 | ) | |

Net (loss) per share – basic and diluted | $ | (10.37 | ) | $ | (0.41 | ) | |

Weighted-average number of shares outstanding – basic and diluted | 4.9 | 4.9 | |||||

See notes to consolidated condensed financial statements.

5

USEC Inc.

(DEBTOR-IN-POSSESSION)

CONSOLIDATED CONDENSED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Unaudited)

(millions)

Three Months Ended March 31, | |||||||

2014 | 2013 | ||||||

Net (loss) | $ | (50.8 | ) | $ | (2.0 | ) | |

Other comprehensive income, before tax (Note 16): | |||||||

Amortization of actuarial (gains) losses, net | 0.3 | 6.8 | |||||

Amortization of prior service costs (credits) | (0.1 | ) | 0.2 | ||||

Other comprehensive income, before tax | 0.2 | 7.0 | |||||

Income tax expense related to items of other comprehensive income | (0.1 | ) | (2.6 | ) | |||

Other comprehensive income, net of tax | 0.1 | 4.4 | |||||

Comprehensive income (loss) | $ | (50.7 | ) | $ | 2.4 | ||

See notes to consolidated condensed financial statements.

6

USEC Inc.

(DEBTOR-IN-POSSESSION)

CONSOLIDATED CONDENSED STATEMENTS OF CASH FLOWS

(Unaudited)

(millions)

Three Months Ended March 31, | |||||||

2014 | 2013 | ||||||

Cash Flows from Operating Activities | |||||||

Net (loss) | $ | (50.8 | ) | $ | (2.0 | ) | |

Adjustments to reconcile net (loss) to net cash (used in) operating activities: | |||||||

Depreciation and amortization | 2.8 | 9.4 | |||||

Reorganization items, non-cash | 1.6 | — | |||||

Deferred income taxes | — | (2.6 | ) | ||||

Convertible preferred stock dividends payable-in-kind | — | 3.2 | |||||

Gain on sale of subsidiary | — | (35.6 | ) | ||||

Changes in operating assets and liabilities: | |||||||

Accounts receivable – (increase) decrease | 125.0 | (15.1 | ) | ||||

Inventories, net – decrease | 53.6 | 57.1 | |||||

Payables under Russian Contract – (decrease) | (340.7 | ) | (209.8 | ) | |||

Deferred revenue, net of deferred costs – increase (decrease) | (5.7 | ) | 41.9 | ||||

Accounts payable and other liabilities – (decrease) | (16.3 | ) | (3.4 | ) | |||

Restricted cash – (increase) | — | (15.1 | ) | ||||

Other, net | 0.8 | (3.3 | ) | ||||

Net Cash (Used in) Operating Activities | (229.7 | ) | (175.3 | ) | |||

Cash Flows Provided by Investing Activities | |||||||

Deposits for surety bonds - net (increase) decrease | 0.6 | (0.3 | ) | ||||

Proceeds from sale of subsidiary | — | 39.9 | |||||

Net Cash Provided by Investing Activities | 0.6 | 39.6 | |||||

Cash Flows Used in Financing Activities | |||||||

Repayment of credit facility term loan | — | (83.2 | ) | ||||

Payments for deferred financing costs | — | (2.0 | ) | ||||

Common stock issued (purchased), net | — | (0.1 | ) | ||||

Net Cash (Used in) Financing Activities | — | (85.3 | ) | ||||

Net (Decrease) | (229.1 | ) | (221.0 | ) | |||

Cash and Cash Equivalents at Beginning of Period | 314.2 | 292.9 | |||||

Cash and Cash Equivalents at End of Period | $ | 85.1 | $ | 71.9 | |||

Supplemental Cash Flow Information: | |||||||

Interest paid | $ | — | $ | 3.2 | |||

Income taxes paid, net of refunds | — | 0.4 | |||||

See notes to consolidated condensed financial statements.

7

USEC Inc.

(DEBTOR-IN-POSSESSION)

CONSOLIDATED CONDENSED STATEMENTS OF

STOCKHOLDERS’ EQUITY (DEFICIT)

(Unaudited)

(millions, except per share data)

Common Stock, Par Value $.10 per Share | Excess of Capital over Par Value | Retained Earnings (Deficit) | Treasury Stock | Accumulated Other Comprehensive Income (Loss) | Total | ||||||||||||||||||

Three Months Ended March 31, 2013 | |||||||||||||||||||||||

Balance at December 31, 2012 | $ | 0.5 | $ | 1,213.3 | $ | (1,361.8 | ) | $ | (33.0 | ) | $ | (291.9 | ) | $ | (472.9 | ) | |||||||

Other comprehensive income, net of tax (Note 16) | — | — | — | — | 4.4 | 4.4 | |||||||||||||||||

Restricted and other common stock issued, net of amortization | — | 1.0 | — | (0.1 | ) | — | 0.9 | ||||||||||||||||

Net (loss) | — | — | (2.0 | ) | — | — | (2.0 | ) | |||||||||||||||

Balance at March 31, 2013 | $ | 0.5 | $ | 1,214.3 | $ | (1,363.8 | ) | $ | (33.1 | ) | $ | (287.5 | ) | $ | (469.6 | ) | |||||||

Three Months Ended March 31, 2014 | |||||||||||||||||||||||

Balance at December 31, 2013 | $ | 0.5 | $ | 1,216.4 | $ | (1,520.7 | ) | $ | (34.3 | ) | $ | (120.1 | ) | $ | (458.2 | ) | |||||||

Other comprehensive income, net of tax (Note 16) | — | — | — | — | 0.1 | 0.1 | |||||||||||||||||

Restricted and other common stock issued, net of amortization | — | 0.4 | — | — | — | 0.4 | |||||||||||||||||

Net (loss) | — | — | (50.8 | ) | — | — | (50.8 | ) | |||||||||||||||

Balance at March 31, 2014 | $ | 0.5 | $ | 1,216.8 | $ | (1,571.5 | ) | $ | (34.3 | ) | $ | (120.0 | ) | $ | (508.5 | ) | |||||||

See notes to consolidated condensed financial statements.

8

USEC Inc.

(DEBTOR-IN-POSSESSION)

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

(Unaudited)

1. BASIS OF PRESENTATION

The unaudited consolidated condensed financial statements of USEC Inc. ("USEC" or the "Company") as of and for the three months ended March 31, 2014 and 2013 have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission. The unaudited consolidated condensed financial statements reflect all adjustments which are, in the opinion of management, necessary for a fair statement of the financial results for the interim period. Certain information and notes normally included in financial statements prepared in accordance with generally accepted accounting principles in the United States (“GAAP”) have been omitted pursuant to such rules and regulations. Certain amounts in the consolidated condensed financial statements have been reclassified to conform to the current presentation.

In March 2013, USEC’s wholly owned subsidiary NAC International, Inc. (“NAC”) was acquired by Hitz Holdings U.S.A. Inc., a subsidiary of Hitachi Zosen Corporation. USEC recorded a gain on the sale of $35.6 million in the first quarter of 2013. Results for NAC through the date of divestiture of March 15, 2013 are segregated from continuing operations and reported as discontinued operations.

Operating results for the three months ended March 31, 2014 are not necessarily indicative of the results that may be expected for the year ending December 31, 2014. The unaudited consolidated condensed financial statements should be read in conjunction with the consolidated financial statements and related notes and management's discussion and analysis of financial condition and results of operations included in the annual report on Form 10-K for the year ended December 31, 2013.

Chapter 11 Filing

On March 5, 2014, USEC Inc. filed a voluntary petition for relief (the "Bankruptcy Filing") under Chapter 11 of the United States Bankruptcy Code in the United States Bankruptcy Court for the District of Delaware (the "Bankruptcy Court"). The Bankruptcy Filing was a “pre-arranged” filing which included the filing of a proposed reorganization plan which is supported by certain holders of the claims and interests impaired under the reorganization plan. The Bankruptcy Filing is intended to strengthen the Company’s balance sheet, enhance its ability to sponsor the American Centrifuge project and improve its long-term business opportunities. Additional details are provided in Note 2.

The Company incurred a net loss for the three months ended March 31, 2014 and for the years ended December 31, 2013, 2012 and, 2011, and had a shareholders’ deficit as of March 31, 2014. USEC’s business is in a state of significant transition and is subject to numerous risks and uncertainties. The increasingly competitive industry conditions under which USEC operates have negatively impacted the Company’s results of operations and cash flows and may continue to do so in the future. These factors raise substantial doubt about the Company’s ability to continue as a going concern. The consolidated condensed financial statements have been prepared assuming that USEC will continue as a going concern and contemplate the realization of assets and the satisfaction of liabilities in the normal course of business. USEC Inc.’s ability to continue as a going concern is contingent upon the Bankruptcy Court’s approval of the proposed reorganization plan and the Company’s ability to successfully implement the proposed reorganization plan, among other factors. As a result of the Bankruptcy Filing, the realization of assets and the satisfaction of liabilities are subject to uncertainty. While operating as a debtor-in-possession under Chapter 11, USEC Inc. may sell or otherwise dispose of or liquidate assets or settle liabilities, subject to the approval of the Bankruptcy Court or as otherwise permitted in the ordinary course of business (subject to restrictions), for amounts other than those reflected in the consolidated condensed financial statements. Further, USEC's reorganization could materially change the amounts and classifications of assets and liabilities reported in the consolidated condensed financial statements. The consolidated condensed financial statements do not include any adjustments related to the recoverability and classification of assets or the amounts and

9

classification of liabilities or any other adjustments that might be necessary should the Company be unable to continue as a going concern or as a consequence of the Bankruptcy Filing, including confirmation of a plan of reorganization or emergence from bankruptcy.

Financial Reporting in Reorganization

Liabilities subject to compromise in the Chapter 11 proceedings are distinguished from liabilities of the Company's subsidiaries that were not part of the Bankruptcy Filing and from post-petition liabilities in the accompanying Consolidated Condensed Balance Sheet as of March 31, 2014. Under Section 362 of the Bankruptcy Code, the filing of a voluntary bankruptcy petition by USEC Inc. automatically stayed most actions against USEC Inc., including most actions to collect indebtedness incurred prior to March 5, 2014 or to exercise control over USEC Inc.’s property. Accordingly, although the Bankruptcy Filing triggered defaults for certain of USEC Inc.’s obligations, creditors are stayed from taking any actions as a result of such defaults. Absent an order of the Bankruptcy Court, substantially all of USEC Inc.’s pre-petition liabilities are subject to settlement under the proposed reorganization plan.

Expenses, gains and losses directly associated with reorganization proceedings are reported as Reorganization Items, Net in the accompanying Consolidated Condensed Statement of Operations. Reorganization Items are indicated as cash or non-cash items in the accompanying Consolidated Condensed Statement of Cash Flows.

New Accounting Standards

In July 2013, the Financial Accounting Standards Board ("FASB") issued guidance requiring an entity to present unrecognized tax benefits as a reduction to deferred tax assets when a net operating loss carryforward, similar tax loss or a tax credit carryforward exists, with limited exceptions. This pronouncement is effective beginning in the first quarter of 2014. USEC has historically presented uncertain tax positions in accordance with the new guidance and the implementation of the guidance did not have a material impact on its consolidated financial statements.

In April 2014, the FASB issued amendments to guidance for reporting discontinued operations and disposals of components of an entity. The amended guidance changes the definition of a discontinued operation to include only those disposals of components of an entity that represent a strategic shift that has, or will have, a major effect on an entity’s operations and financial results. The amendments also expand the disclosure requirements for discontinued operations and add new disclosures for individually significant dispositions that do not qualify as discontinued operations. The amendments are effective prospectively beginning in the first quarter of 2015 (early adoption is permitted only for disposals that have not been previously reported). The implementation of the amended guidance is not expected to have a material impact on USEC's results of operations, cash flows or financial position.

10

2. CHAPTER 11 FILING

On March 5, 2014 (the “Petition Date”), USEC Inc. (the "Debtor") filed a voluntary petition for relief under Chapter 11 of the United States Bankruptcy Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the District of Delaware case number 14-10475. The Bankruptcy Filing was a “pre-arranged” filing which, as described further below, included the filing of a proposed Plan of Reorganization (the “Proposed Plan”) which is supported by certain holders of the claims and interests impaired under the Proposed Plan. USEC Inc.’s subsidiaries (collectively, the “Non-Filing Entities”), including United States Enrichment Corporation ("Enrichment"), which is our primary operating subsidiary, were not part of the Bankruptcy Filing. USEC Inc. will continue to operate its business as “debtor-in-possession” under the jurisdiction of the Bankruptcy Court and in accordance with the applicable provisions of the Bankruptcy Code and the orders of the Bankruptcy Court. The Non-Filing Entities will continue to operate in the ordinary course of business.

The Bankruptcy Filing is intended to strengthen the Company’s balance sheet, enhance its ability to sponsor the American Centrifuge project and improve its long-term business opportunities. USEC Inc. has reached an agreement on the terms of a financial restructuring plan with the holders (the “Consenting Noteholders”) of approximately 65% of the principal amount of its convertible senior notes (the “Convertible Notes”). Under the terms of the agreement described in more detail below, USEC Inc. will replace the approximately $530 million of Convertible Notes that are scheduled to mature in October 2014 with new debt and equity. USEC Inc. has also reached an agreement with Babcock & Wilcox Investment Company (“B&W”) and Toshiba America Nuclear Energy Corporation (“Toshiba” and together with B&W, the “Preferred Investors”) to restructure their preferred convertible equity investment (each of the agreements with the Consenting Noteholders, Toshiba and B&W, respectively, a "Plan Support Agreement"; and collectively, the "Plan Support Agreements").

Proposed Reorganization Plan

The material terms of the Proposed Plan include, among other things, that, upon the effective date of the Proposed Plan (the “Effective Date”):

• | The holders of the Convertible Notes will receive, on a pro rata basis, in exchange for claims on account of their $530 million in outstanding principal amount of Convertible Notes: |

◦ | 79.04% of the common stock of reorganized USEC Inc. (“New Common Stock”), subject to dilution on account of a new management incentive plan; |

◦ | cash for interest payable on the Convertible Notes accrued from October 1, 2013, the date of the last semi-annual interest payment, to the Effective Date; and |

◦ | $200 million in principal amount of new notes issued by reorganized USEC Inc. on terms described in the Proposed Plan’s implementing documents (the “New Notes”), with the New Notes being guaranteed and secured on a subordinated and limited basis by Enrichment. |

• | B&W and Toshiba will each receive in exchange and on account of their shares of USEC’s Series B-1 12.75% convertible preferred stock (the “Preferred Stock”) (as of December 31, 2013, there were 85,903 shares of Preferred Stock outstanding with an aggregate liquidation preference of $113.9 million including accrued paid-in-kind dividends) and warrants dated September 2, 2010 to purchase up to 250,000 shares of USEC’s common stock (the “Warrants”): |

◦ | 7.98% of the New Common Stock (15.96% in the aggregate), subject to dilution on account of a new management incentive plan; and |

◦ | $20.19 million in principal amount of New Notes ($40.38 million in the aggregate). |

11

◦ | The Preferred Investors have agreed to enter into good faith negotiations to each invest $20.19 million (for an aggregate investment of $40.38 million) of equity in the American Centrifuge project in the future, upon mutually agreed upon terms and conditions, but in any event contingent upon the funding for the American Centrifuge Plant ("ACP") of not less than $1.5 billion of debt supported by the U.S. Department of Energy ("DOE") loan guarantee program or other government support or funding in such amount. |

◦ | In connection with USEC Inc.’s compliance with regulatory requirements, the New Common Stock issued to the Preferred Investors would be structured in a similar manner to the Class B Common Stock contemplated to be issuable to the Preferred Investors upon conversion of the Preferred Stock. As contemplated, Class B Common Stock will have the same rights, powers, preferences and restrictions and rank equally in all matters with the common stock of the reorganized USEC Inc., except voting. Holders of Class B Common Stock shall be entitled to elect two members of the Board of Directors of USEC Inc., consistent with their current arrangements. |

• | If the Noteholders and Preferred Investors vote by requisite majorities to accept the Proposed Plan, the holders of USEC Inc.’s common stock will receive, on a pro rata basis, 5% of the New Common Stock, subject to dilution on account of a new management incentive plan. |

• | All secured claims will be reinstated and otherwise not impaired and all liens shall be continued until the claims are paid in full. |

• | All other general unsecured claims of the Company will be unimpaired and will be either reinstated or paid in full in the ordinary course of business upon the later of the Effective Date or when such obligation becomes due according to its terms. |

USEC believes that the Proposed Plan meets the standards for confirmation under the Bankruptcy Code, but that determination will rest with the Bankruptcy Court. Confirmation of the Proposed Plan could materially alter the classifications and amounts reported in USEC’s consolidated condensed financial statements, which do not give effect to any adjustments to the carrying values of assets or amounts of liabilities that might be necessary as a consequence of a confirmation of the Proposed Plan or other arrangement or the effect of any operational changes that may be implemented.

Operation and Implication of the Bankruptcy Filing

Throughout the restructuring process, both USEC Inc. and the Non-Filing Entities expect to continue operations and meet obligations to stakeholders, including suppliers, partners, customers and employees, subject to limitations on the ability of USEC Inc. to pay certain pre-petition obligations pending confirmation and implementation of the Proposed Plan. USEC also anticipates the continuation of research, development and demonstration activities for the American Centrifuge technology subject to the availability of continued government funding. As a non-debtor, Enrichment’s operations, which include the transition of the Paducah gaseous diffusion plant ("Paducah GDP") back to DOE and the sale of SWU from its inventory and purchases of Russian low enriched uranium ("LEU"), are expected to continue unaffected by the bankruptcy.

USEC Inc. has received approval from the Bankruptcy Court to pay or otherwise honor certain pre-petition obligations generally designed to stabilize its operations. These obligations were primarily related to certain employee wages, salaries and benefits, certain governmental taxes and fees, and certain insurance commitments. Pre-petition obligations not authorized to be paid currently by the Bankruptcy Court will be treated under the plan of reorganization. Post-petition obligations will be paid when due in the ordinary course of business, without prior payment authorization from the Bankruptcy Court. USEC Inc. has retained, pursuant to Bankruptcy Court approval, legal and financial professionals to advise it in connection with the Bankruptcy Filing and certain other professionals to provide services and advice in the ordinary course of business. USEC Inc. may retain additional

12

ordinary course professionals without further order of the Bankruptcy Court and from time to time may seek Bankruptcy Court approval to retain additional Chapter 11 professionals if needed.

USEC Inc. also received approval from the Bankruptcy Court to enter into a Debtor-In-Possession Credit Facility (the “DIP Facility”). This $50 million revolving credit facility is provided by Enrichment, USEC Inc.’s subsidiary. It accrues interest at an annual rate of 10.5% and is secured by substantially all of USEC Inc.’s assets. The DIP Facility requires mandatory prepayments from USEC Inc. when cost sharing reimbursements for research, development and demonstration work performed under the June 2012 cooperative agreement with DOE ("the Cooperative Agreement") have been received from DOE. It matures at the earlier of the Effective Date of the Proposed Plan or 120 days, and is expected to be repaid with a draw on the Exit Facility described below. Borrowings must be consistent with a budget satisfactory to Enrichment. USEC Inc. is also required to manage its cash flows pursuant to this budget on a weekly basis with a limitation on variance from the budget. Enrichment’s obligations to make funds available include certain conditions precedent such as commencement of solicitation of acceptance of a reorganization plan within 50 days of the Petition Date, USEC shall not have demobilized all or substantially all American Centrifuge activities, and DOE shall not have suspended or terminated the American Centrifuge research, development and demonstration program under the Cooperative Agreement or associated funding. Events of default include termination of any of the Plan Support Agreements prior to confirmation of a reorganization plan, USEC Inc. filing a plan that has not been consented to by Enrichment, as well as other events of default common to such facilities. In the first quarter of 2014, USEC Inc. borrowed and repaid $3.0 million under the DIP Facility.

As of April 17, 2014, USEC Inc. entered into a first amendment to the DIP Facility amending the conditions precedent to funding to provide for an extension of the time to commence solicitation of acceptances of a reorganization plan to 103 days from the Petition Date from 50 days from the Petition Date. This amendment was entered into to be consistent with amendments to certain termination conditions to the Plan Support Agreements as described below. In addition, on May 9, 2014, USEC Inc. filed a motion with the Bankruptcy Court seeking an order from the Bankruptcy Court authorizing USEC Inc. to enter into an Amended and Restated Credit Agreement. The Amended and Restated Credit Agreement would modify the DIP Facility to reflect the transition of the American Centrifuge research, development and demonstration program from the Cooperative Agreement to the new agreement with Oak Ridge National Laboratory discussed below. The other proposed modifications include extending the maturity date of the DIP Facility to the earlier of the Effective Date of the Proposed Plan or September 30, 2014 (which date may be extended by Enrichment in its sole discretion). A hearing on USEC Inc.'s motion has been scheduled for June 2, 2014. On May 14, 2014, USEC Inc. and Enrichment entered into a limited waiver to the DIP Facility that provides a waiver of certain conditions precedent that are no longer relevant in order to enable USEC Inc. to draw limited funds prior to the scheduled hearing.

Reorganization Plan Approval Process

In order for USEC Inc. to emerge successfully from Chapter 11, USEC Inc. must obtain the Bankruptcy Court’s approval of the Proposed Plan, which will enable the Company to transition from Chapter 11 into ordinary course operations outside of bankruptcy. In connection with the Proposed Plan, USEC Inc. expects to enter into a new credit facility (the “Exit Facility”) with Enrichment. USEC Inc.’s ability to obtain such approval and financing will depend on, among other things, the timing and outcome of various ongoing matters related to the Bankruptcy Filing including issues relating to continued U.S. government funding for the American Centrifuge technology and issues relating to demobilization costs and potential contract termination liabilities resulting from the reduced scope of work of the American Centrifuge research, development and demonstration program under the new contract with Oak Ridge National Laboratory. As summarized above, the Proposed Plan determines the rights and satisfaction of claims of various creditors and security holders, and is subject to the ultimate outcome of events, negotiations and Bankruptcy Court decisions ongoing through the date on which the Proposed Plan is confirmed.

13

Only creditors impaired under the Proposed Plan are entitled to vote on the Proposed Plan. As described above, USEC Inc. has already entered into agreements with the Consenting Noteholders and Preferred Investors pursuant to which the Consenting Noteholders and Preferred Investors have agreed to vote in favor of the Proposed Plan. The Plan Support Agreements may be terminated by USEC Inc., a majority of the Consenting Noteholders, or the Preferred Investors following written notice and the occurrence of certain events including:

• | Upon a good faith determination of the Board of Directors of USEC Inc. that proceeding with the Proposed Plan would be inconsistent with the exercise of its fiduciary duties; |

• | DOE terminates or suspends (or announces its intent to terminate or suspend) its 80% cost share funding for work performed under the research, development and demonstration program or a successor program; |

• | There is a termination or suspension or material delay in completion of the research, development and demonstration program or a successor program (other than, in the case of USEC’s right to terminate, as a result of action or inaction by USEC); and |

• | If the Russian transitional supply agreement between Enrichment and Joint Stock Company Techsnabexport is terminated, suspended or materially adversely modified. |

In April, the Consenting Noteholders and the Preferred Investors agreed to amend their respective Plan Support Agreements providing for an extension to certain dates which provide rights to terminate such Plan Support Agreements. A court order was entered on April 21, 2014 assuming the Plan Support Agreements in USEC Inc.’s bankruptcy case including these amendment changes. As amended, a majority of Consenting Noteholders or the Preferred Investors can also terminate their respective Plan Support Agreements following written notice and the occurrence of certain events including:

• | Failure to commence solicitation of the Proposed Plan within 103 days of the Petition Date (i.e., June 16, 2014); |

• | Failure to have a Confirmation Order entered by the Bankruptcy Court within 153 days of the Petition Date (i.e., August 5, 2014); |

• | Failure to have the occurrence of the Effective Date within 173 days of the Petition Date (i.e., August 25, 2014); and |

• | If USEC Inc. experiences any circumstance, change or other event that has had or is reasonably likely to have a short-term or long-term material adverse effect on the financial condition or operations of USEC Inc. and its subsidiaries. |

Further, the Proposed Plan is subject to revision in response to creditor claims and objections, the requirements of the Bankruptcy Code or the Bankruptcy Court, material changes in U.S. government funding for the American Centrifuge technology and in the event USEC incurs material demobilization or termination liabilities related to the American Centrifuge program. While USEC expects to emerge successfully from bankruptcy with approval of the Proposed Plan from the Bankruptcy Court during the summer of 2014, there can be no assurance that USEC will be able to secure approval for the Proposed Plan within that period or at all.

14

3. LIABILITIES SUBJECT TO COMPROMISE

The following table reflects pre-petition liabilities that were unpaid as of the Petition Date and are subject to compromise (in millions).

March 31, 2014 | |||

Accounts payable and accrued liabilities | $ | 1.5 | |

3% convertible senior notes and accrued interest (a) | 538.2 | ||

Convertible preferred stock and paid-in-kind dividends payable (b) | 113.9 | ||

Liabilities subject to compromise | $ | 653.6 | |

(a) | Subsequent to the Petition Date, interest is accrued at 3% plus 50 basis points based on the default rate defined in the notes. |

(b) | The convertible preferred stock are currently subject to a share issuance limitation. If a share issuance limitation were to exist at the time of share conversion or sale, any preferred stock shares subject to the share issuance limitation would be subject to optional or mandatory redemption for, at USEC's option, cash or SWU consideration. However, USEC’s ability to redeem may be limited by Delaware law and the Bankruptcy Code. Interest on the convertible preferred stock, in the form of dividends payable-in-kind, ceased in connection with the Proposed Plan. |

4. REORGANIZATION ITEMS, NET

The following is a summary of charges related to our bankruptcy filing and reorganization (in millions).

Three Months Ended March 31, 2014 | |||

Advisory fees | $ | 7.2 | |

Expense of deferred financing costs | 1.2 | ||

Reorganization items, net | $ | 8.4 | |

For debt that is subject to compromise, associated deferred financing costs are expensed so that the net carrying amount of the debt equals the amount of the allowed claim. Previously deferred financing costs of $1.2 million related to our convertible senior notes were expensed in the three months ended March 31, 2014.

For the three months ended March 31, 2014, cash payments for reorganization items totaled $7.0 million.

15

5. CONDENSED DEBTOR-IN-POSSESSION FINANCIAL INFORMATION

The financial statements below represent the unconsolidated condensed financial statements of the Debtor, USEC Inc. excluding subsidiaries. The statement of operations begins with operating expenses since USEC Inc. does not have revenue-generating activities.

Debtor's Condensed Balance Sheet (millions) | |||

March 31, 2014 | |||

ASSETS | |||

Current Assets | |||

Cash and cash equivalents | $ | 13.9 | |

Accounts receivable, net | 17.4 | ||

Inventories | 0.2 | ||

Receivable from non-filing entity | 2.5 | ||

Other current assets | 11.3 | ||

Total current assets | 45.3 | ||

Property, plant and equipment, net | 1.6 | ||

Deposits for surety bonds | 29.4 | ||

Investment in non-filing entities | 484.8 | ||

Total Assets | $ | 561.1 | |

LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) | |||

Current Liabilities | |||

Accounts payable and accrued liabilities | $ | 18.0 | |

Total current liabilities | 18.0 | ||

Pension benefit liabilities | 26.2 | ||

Other long-term liabilities | 24.6 | ||

Liabilities subject to compromise | 1,000.8 | ||

Total Liabilities | 1,069.6 | ||

Stockholders’ Equity (Deficit) | (508.5 | ) | |

Total Liabilities and Stockholders’ Equity (Deficit) | $ | 561.1 | |

Components of liabilities subject to compromise follow (in millions):

March 31, 2014 | |||

Accounts payable and accrued liabilities | $ | 1.5 | |

Convertible senior notes and accrued interest | 538.2 | ||

Convertible preferred stock and paid-in-kind dividends payable | 113.9 | ||

Intercompany services payable | 203.1 | ||

Intercompany loan payable | 144.1 | ||

Liabilities subject to compromise | $ | 1,000.8 | |

16

Debtor's Condensed Statement of Operations and Comprehensive (Loss) (millions) | |||

Three Months Ended March 31, 2014 | |||

Gross profit (loss) | $ | — | |

Advanced technology costs | 33.3 | ||

Selling, general and administrative | 11.0 | ||

Other (income) expense, net | (26.5 | ) | |

Intercompany cost recovery | (13.5 | ) | |

Operating (loss) | (4.3 | ) | |

Interest expense | 7.5 | ||

Reorganization items, net | 8.4 | ||

Equity in earnings (loss) of non-filing entities | (31.6 | ) | |

(Loss) from continuing operations before income taxes | (51.8 | ) | |

Provision (benefit) for income taxes | (1.0 | ) | |

Net (loss) | $ | (50.8 | ) |

Other comprehensive income, net of tax | — | ||

Comprehensive income (loss) | $ | (50.8 | ) |

Debtor's Condensed Statement of Cash Flows (millions) | |||

Three Months Ended March 31, 2014 | |||

Cash Flows from Operating Activities | |||

Net (loss) | $ | (50.8 | ) |

Adjustments to reconcile net (loss) to net cash (used in) operating activities | 35.8 | ||

Net Cash (Used in) Operating Activities | (15.0 | ) | |

Cash Flows Provided by Investing Activities | |||

Net Cash Provided by Investing Activities | — | ||

Cash Flows Provided by Financing Activities | |||

Proceeds from debtor-in-possession credit facility | 3.0 | ||

Repayments of debtor-in-possession credit facility | (3.0 | ) | |

Proceeds from intercompany loan | 50.7 | ||

Repayments of intercompany loan | (27.1 | ) | |

Net Cash Provided by Financing Activities | 23.6 | ||

Net Increase | 8.6 | ||

Cash and Cash Equivalents at Beginning of Period | 5.3 | ||

Cash and Cash Equivalents at End of Period | $ | 13.9 | |

17

6. TRANSITION CHARGES

Non-Production Expenses Related to Ceasing Enrichment at the Paducah Plant

USEC ceased uranium enrichment at the Paducah GDP at the end of May 2013 and is in discussions with DOE regarding the timing of USEC’s de-lease of the facility from DOE. Under the terms of the lease, USEC can terminate the lease prior to June 2016 upon two years' notice. Also, as USEC's requirements change, USEC can de-lease portions of the property under lease upon 60 days' notice with DOE's consent, which cannot be unreasonably withheld. However, the right of partial de-lease does not include the right of USEC to terminate the lease in its entirety or with respect to the Paducah GDP, which termination is permitted only in accordance with the two-year termination provision of the lease. On August 1, 2013, USEC provided notice to DOE that USEC exercised its rights to terminate the lease with respect to the Paducah GDP and USEC has been in discussions with DOE regarding the timing of USEC’s de-lease. USEC anticipates being ready to complete the return of leased premises and to terminate the Paducah GDP lease as early as July 2014. However, based on USEC's current discussions with DOE, the return of the leased premises appears unlikely before October 2014 and USEC and DOE have not reached agreement on a lease termination date prior to August 1, 2015. DOE has indicated that its ability to agree to such an earlier date will depend on its ability to award a contract for deactivation services and be prepared to assume responsibility for the leased areas, among other things. In the event that USEC is unable to agree with DOE on a schedule for termination prior to two years, USEC plans to exercise its rights under the lease and submit a 60-day notification to return portions of the leased premises no longer required to meet its business needs. In addition, while DOE has stated that it continues to be willing to work with USEC to develop a transition plan and schedule for the safe and secure return of the Paducah GDP, DOE has taken the position that USEC is foreclosed from invoking its rights to a partial return of facilities under the lease. While USEC strongly disagrees with this DOE position, USEC believes it will be able to reach agreement with DOE on a mutually agreeable date to return the leased areas. Disputes could also arise regarding the requirements of the lease and responsibility for associated turnover costs.

The Paducah GDP operated for more than 60 years. Environmental liabilities associated with plant operations by agencies of the U.S. government prior to USEC's privatization on July 28, 1998 are the responsibility of the U.S. government. The USEC Privatization Act and the lease for the plant provide that DOE remains responsible for decontamination and decommissioning of the Paducah site.

As USEC accelerated the expected productive life of plant assets and ceased uranium enrichment at the Paducah GDP, USEC has incurred a number of expenses unrelated to production that have been charged directly to cost of sales. Non-production expenses totaled $34.9 million in the three months ended March 31, 2014 and $5.8 million in the corresponding period in 2013 as follows:

- | Site expenses, including lease turnover activities and Paducah and Portsmouth retiree benefit costs, of $27.0 million in the three months ended March 31, 2014. Following the cessation of enrichment at the Paducah GDP, costs for plant activities that formerly were capitalized as production costs are now charged directly to cost of sales including inventory management and disposition, ongoing regulatory compliance, utility requirements for operations, security, and other site management activities related to transition of facilities and infrastructure. Non-production expenses in the three months ended March 31, 2013 include $3.0 million of Portsmouth retiree benefit costs; |

- | Accelerated asset charges of $1.3 million in the three months ended March 31, 2014 and $2.8 million in the three months ended March 31, 2013. Beginning in the fourth quarter of 2012, the expected productive life of property, plant and equipment at the Paducah GDP was reduced from the lease term ending June 2016 to an accelerated basis ending December 2014. In addition, beginning in the third quarter of 2012, costs that would have been previously treated as construction work in progress are treated similar to maintenance and repair costs because of the shorter expected productive life of the Paducah GDP. The expected productive life of the Paducah GDP was further reduced following the ceasing of enrichment at the end of May 2013. In general, these assets, depending on their continuing economic life, are now expected to be useful only through the first half of 2014; and |

18

- | Inventory charges of $6.6 million in the three months ended March 31, 2014. These inventories are intended to be transferred to DOE upon final de-lease, including residual uranium in cylinders and inventories deployed for cascade drawdown, assay blending and repackaging. USEC determined that it was currently uneconomic to recover resulting residual quantities for resale. |

USEC may incur additional non-production expense and special charges in future periods based on the results of the planning and execution of the Paducah transition and assessments of evolving business needs.

Special Charges Summary

A summary of special charges recorded in the year ended December 31, 2013 and the three months ended March 31, 2014, and changes in the related balance sheet accounts, follow (in millions):

Liability Balance to Be Paid, Dec. 31, 2012 | 2013 Special Charges | 2013 Paid | Liability Balance to Be Paid, Dec. 31, 2013 | First Qtr. 2014 Special Charges | First Qtr. 2014 Paid | Liability Balance to Be Paid, Mar. 31, 2014 | |||||||||||||||||||||

Workforce reductions, primarily severance payments | $ | — | $ | 25.2 | $ | (4.0 | ) | $ | 21.2 | $ | 0.1 | $ | (2.7 | ) | $ | 18.6 | |||||||||||

Less: Amounts billed to DOE | — | (1.2 | ) | na | na | (0.6 | ) | na | na | ||||||||||||||||||

Pension and postretirement benefit charges, non-cash | — | 22.2 | na | na | — | na | na | ||||||||||||||||||||

Advisory costs | 0.1 | 11.0 | (9.9 | ) | 1.2 | — | (1.2 | ) | — | ||||||||||||||||||

$ | 0.1 | $ | 57.2 | $ | (13.9 | ) | $ | 22.4 | $ | (0.5 | ) | $ | (3.9 | ) | $ | 18.6 | |||||||||||

na - not applicable

Special Charges for Workforce Reductions

Beginning in May 2013, USEC has notified its Paducah employees of potential layoffs following the cessation of enrichment at the Paducah GDP. The notifications are provided under the Worker Adjustment and Retraining Notification Act ("WARN Act"), a federal statute that requires an employer to provide advance notice to its employees of potential layoffs in certain circumstances. Termination benefits, consisting primarily of severance payments, are estimated to total $25.2 million. The special charge of $24.0 million in the year ended December 31, 2013 is net of $1.2 million of severance paid by USEC and invoiced to DOE. In the first quarter of 2014, an additional $0.6 million was invoiced to DOE for its portion of severance paid to date, and is reflected as a credit to special charges in the three months ended March 31, 2014. Accounts receivable as of March 31, 2014 include DOE's share of severance paid by USEC. DOE’s liability for its share of severance paid is pursuant to the USEC Privatization Act.

Between June and December 2013, the Paducah GDP workforce was reduced by 202 employees through layoffs. In the first quarter of 2014, the Paducah GDP workforce was reduced by an additional 134 employees through layoffs. Additional layoffs occurred in April and are expected in stages in 2014 including at other locations, depending on business needs. Information on these additional layoffs would be communicated to affected employees in future notices and may also result in additional charges.

USEC froze benefit accruals under its defined benefit pension plans, effective August 5, 2013, for active employees other than those who are covered by a collective bargaining agreement at the Paducah GDP. Pension benefits will no longer increase for these employees to reflect changes in compensation or company service. However, these employees will not lose any benefits earned through August 4, 2013 under the pension plans and continue to accrue service credits toward vesting and qualifying for early or unreduced retirement benefits under the plans. Unamortized prior service costs related to those pension plan participants were accelerated. In addition, as discussed above, layoffs of the remaining Paducah workforce are expected to occur in stages through 2014, but no later than the lease termination date of August 1, 2015. The layoffs are expected to accelerate retirement obligations

19

in the GDP pension plan and GDP postretirement health and life benefit plans. Unamortized prior service costs related to affected plan participants were accelerated due to these terminations. Moreover, and in accordance with plan documents, certain affected plan participants were credited additional plan service credits based on their involuntary termination of employment. The net impact recorded in special charges for the year ended December 31, 2013 for these plans was $22.2 million.

Special Charges for Advisory Costs

Since late 2012, USEC has been engaged with advisors on the restructuring of its balance sheet. Special charges recorded for these advisors totaled $2.4 million in the three months ended March 31, 2013 and $11.0 million for the year ended December 31, 2013.

In the three months ended March 31, 2014, USEC incurred $7.2 million in advisory costs related to the Bankruptcy Filing and these charges are included in Reorganization Items, Net, as detailed in Note 4.

7. ADVANCED TECHNOLOGY COSTS AND OTHER INCOME

Since June 2012, USEC performed work under the Cooperative Agreement for the American Centrifuge technology with cost-share funding from DOE. The objectives of the Cooperative Agreement were (1) to demonstrate the American Centrifuge technology through the construction and operation of a commercial demonstration cascade of 120 centrifuge machines and (2) sustain the domestic U.S. centrifuge technical and industrial base for national security purposes and potential commercialization of the American Centrifuge technology. This included activities to reduce the technical risks and improve the future prospects of deployment of the American Centrifuge technology. USEC achieved or exceeded all of the program milestones and performance indicators on or ahead of schedule and on or under budget.

The Cooperative Agreement, as amended, defined the scope, funding and technical goals for the centrifuge research, development and demonstration program. The Cooperative Agreement provided for 80% DOE and 20% USEC cost sharing for work performed June 1, 2012 through April 30, 2014. The Total Estimated Cost was $350 million and the Total Estimated Government Share was $280 million. The Cooperative Agreement was incrementally funded since 2012, and the final $23.0 million of government funding was provided through amendments to the Cooperative Agreement on January 28, 2014, February 12, 2014 and April 1, 2014. The Cooperative Agreement was subsequently extended on April 14 to April 30, 2014, at no additional cost to the U.S. government beyond the $280 million. The Cooperative Agreement expired in accordance with its terms on April 30, 2014.

As of March 31, 2014, USEC has made cumulative qualifying American Centrifuge expenditures of $341.0 million. DOE’s cost share is 80% or $272.8 million. Of the $272.8 million, $255.3 million was received by USEC and DOE’s remaining funding share of $17.5 million is included in current accounts receivable as of March 31, 2014. DOE’s cost share of 80% is recognized as other income.

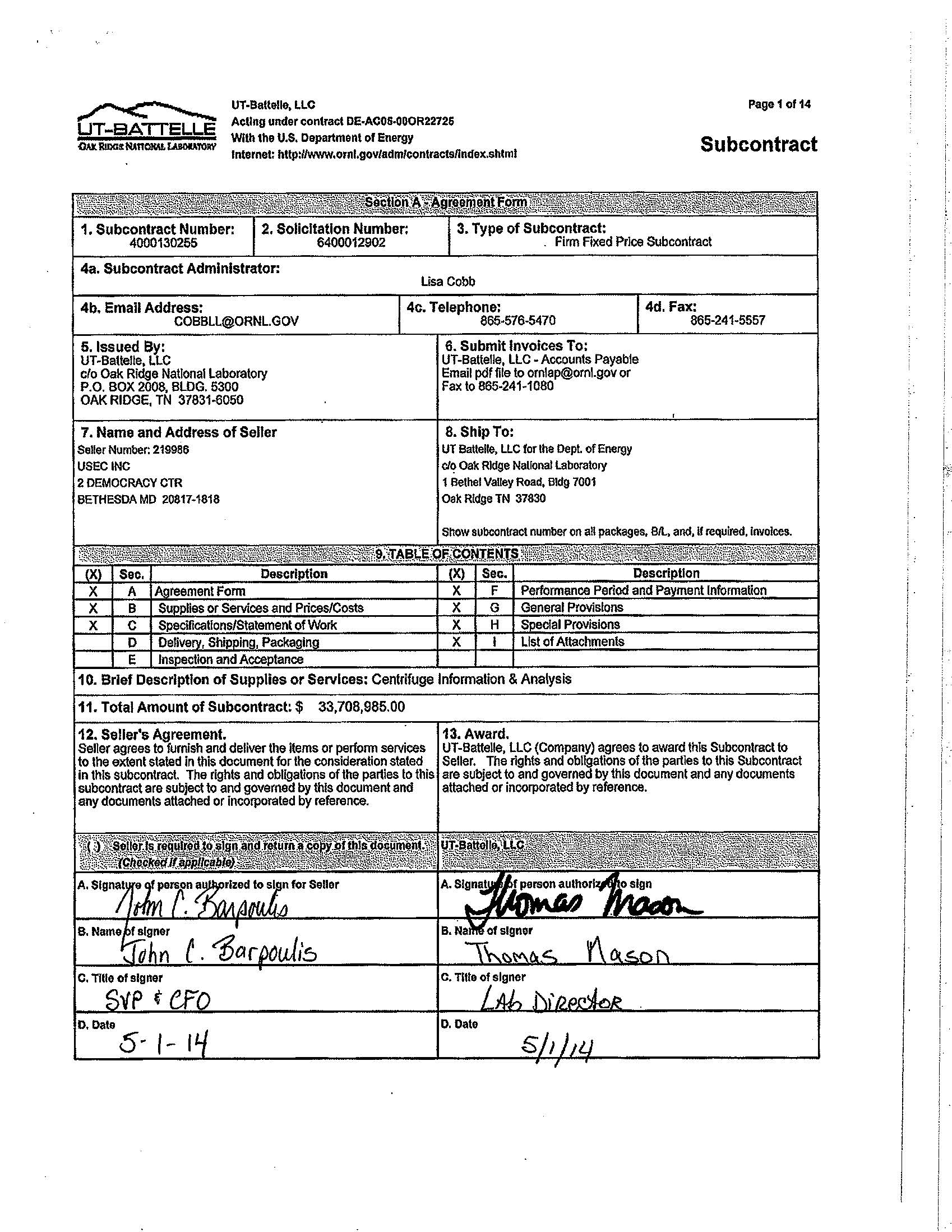

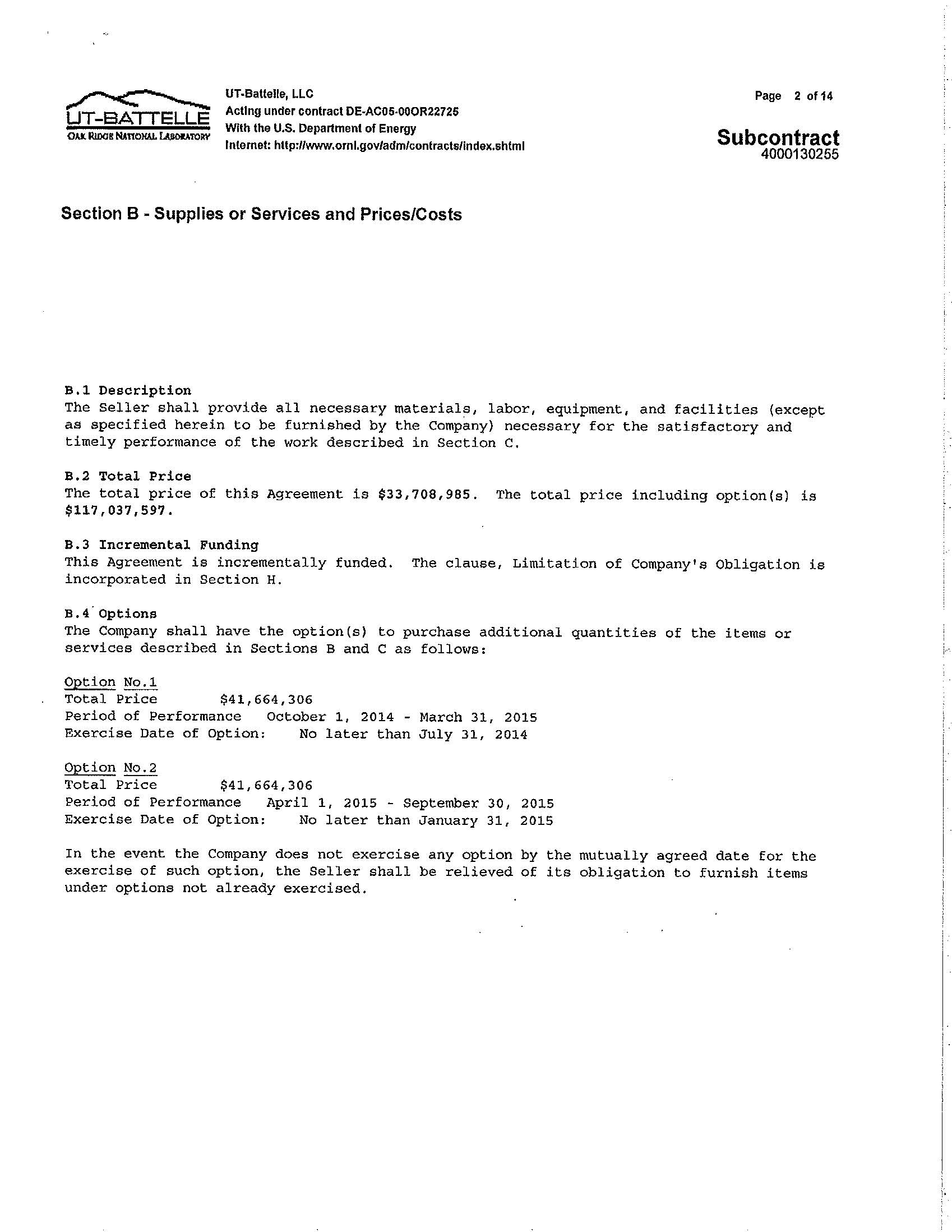

As described in Note 15, on May 1, 2014 USEC signed an agreement with UT-Battelle, LLC ("UT-Battelle"), the management and operating contractor for the Oak Ridge National Laboratory ("ORNL"), for continued cascade operations and continuation of core American Centrifuge research and technology activities and the furnishing of related reports to ORNL (the "American Centrifuge Technology Demonstration and Operations Agreement", or "ACTDO Agreement"). The new agreement is a fixed-price contract with a contract price of approximately $33.7 million for the period from May 1, 2014 to September 30, 2014 for USEC to maintain the American Centrifuge technology capability as a subcontractor to ORNL. The scope of the overall work under the ACTDO Agreement is reduced from the scope of work that was being conducted by USEC under the Cooperative Agreement.

20

8. RECEIVABLES

March 31, 2014 | December 31, 2013 | ||||||

(millions) | |||||||

Accounts Receivable: | |||||||

Utility customers | $ | 6.2 | $ | 129.3 | |||

DOE cost share of Cooperative Agreement funding | 17.5 | 20.1 | |||||

Contract services, primarily DOE: | |||||||

Billed revenue | 16.2 | 15.7 | |||||

Unbilled revenue | 2.7 | 1.9 | |||||

Contract services, primarily DOE | 18.9 | 17.6 | |||||

Accounts receivable, gross | 42.6 | 167.0 | |||||

Less: valuation allowances and allowances for doubtful accounts | 4.6 | 4.0 | |||||

Accounts receivable, net | $ | 38.0 | $ | 163.0 | |||

DOE Receivables included in Other Long-Term Assets: | |||||||

DOE long-term receivables, gross | $ | 80.8 | $ | 80.8 | |||

Less: valuation allowances and allowances for doubtful accounts | 55.0 | 55.0 | |||||

DOE long-term receivables, net | $ | 25.8 | $ | 25.8 | |||

Billings for contract services related to DOE are generally invoiced based on provisional billing rates approved by DOE. Unbilled revenue represents the difference between actual costs incurred, prior to incurred cost audit and notice by DOE authorizing final billing, and provisional billing rate invoiced amounts. Unbilled amounts are invoiced to DOE as billing rates are revised, submitted to and approved by DOE.

Certain receivables from DOE are included in other long-term assets based on the extended timeframe expected to resolve claims for payment. USEC believes DOE has breached its agreements by failing to establish appropriate provisional billing and final indirect cost rates on a timely basis and USEC has filed claims with DOE for payment under the Contract Disputes Act ("CDA"). DOE denied USEC's initial claim for payment of $38.0 million, and on May 30, 2013, USEC appealed the DOE's denial of its claims to the U.S. Court of Federal Claims.

On August 30, 2013, USEC submitted an additional claim to DOE under the CDA for payment of $42.8 million, representing DOE's share of pension and postretirement benefits costs related to the transition of Portsmouth site employees to DOE's decontamination and decommissioning ("D&D") contractor. As noted in Note 15, USEC has potential pension plan funding obligations under Section 4062(e) of the Employee Retirement Income Security Act (“ERISA”) related to USEC's de-lease of the Portsmouth gaseous diffusion facilities and transition of employees to DOE's D&D contractor and related to the transition of employees in connection with the Paducah GDP transition. USEC believes that DOE is responsible for a significant portion of any pension and postretirement benefit costs associated with the transition of employees at Portsmouth. The receivable for DOE's share of pension and postretirement benefits costs has a full valuation allowance due to the lack of a resolution with DOE and uncertainty regarding the amounts owed and the timing of collection. The amounts owed by DOE may be more than the amounts invoiced by USEC to date.

USEC has unapplied payments from DOE included in other long-term liabilities pending resolution of the long-term receivables from DOE described above. DOE funded a portion of USEC's contract services work through an arrangement whereby DOE transferred uranium to USEC which USEC immediately sold. USEC completed six competitive sales of uranium between the fourth quarter of 2009 and the first quarter of 2011. The net cash proceeds from the uranium sales are to be applied, at the direction of DOE, (a) as revenue is recognized in USEC’s contract services segment as services are provided or (b) to existing receivables balances due from DOE in USEC’s contract services segment. The remaining payment balance included in other long-term liabilities is $19.7 million as of March 31, 2014 and December 31, 2013.

21

9. INVENTORIES

USEC is a supplier of LEU for nuclear power plants. LEU consists of two components: separative work units (“SWU”) and uranium. SWU is a standard unit of measurement that represents the effort required to transform a given amount of natural uranium into two components: enriched uranium having a higher percentage of U235 and depleted uranium having a lower percentage of U235. The SWU contained in LEU is calculated using an industry standard formula based on the physics of enrichment. The amount of enrichment deemed to be contained in LEU under this formula is commonly referred to as its SWU component and the quantity of natural uranium deemed to be used in the production of LEU under this formula is referred to as its uranium component.

USEC holds uranium at the Paducah GDP and other NRC-licensed locations in the form of natural uranium and as the uranium component of LEU. USEC holds SWU as the SWU component of LEU. USEC may also hold title to the uranium and SWU components of LEU at fabricators to meet book transfer requests by customers. Fabricators process LEU into fuel for use in nuclear reactors. Costs included in inventory include purchase costs and previous production costs associated with the Paducah GDP.

Components of inventories follow (in millions):

March 31, 2014 | December 31, 2013 | ||||||||||||||||||||||

Current Assets | Current Liabilities (a) | Inventories, Net | Current Assets | Current Liabilities (a) | Inventories, Net | ||||||||||||||||||

Separative work units | $ | 468.5 | $ | 67.2 | $ | 401.3 | $ | 628.4 | $ | 200.0 | $ | 428.4 | |||||||||||

Uranium | 101.0 | 90.2 | 10.8 | 335.4 | 299.7 | 35.7 | |||||||||||||||||

Materials and supplies | 2.2 | — | 2.2 | 3.8 | — | 3.8 | |||||||||||||||||

$ | 571.7 | $ | 157.4 | $ | 414.3 | $ | 967.6 | $ | 499.7 | $ | 467.9 | ||||||||||||

(a) | Inventories owed to customers and suppliers, included in current liabilities, consist primarily of SWU and uranium inventories owed to fabricators. |

Uranium Provided by Customers and Suppliers

USEC held uranium with estimated values of approximately $954 million at March 31, 2014, and $1.3 billion at December 31, 2013, to which title was held by customers and suppliers and for which no assets or liabilities were recorded on the balance sheet. The reduction reflects a 23% decline in quantities and a 3% decline in the uranium spot price indicator. Utility customers provide uranium to USEC as part of their enrichment contracts. Title to uranium provided by customers generally remains with the customer until delivery of LEU at which time title to LEU is transferred to the customer, and title to uranium is transferred to USEC.

10. PROPERTY, PLANT AND EQUIPMENT

A summary of changes in property, plant and equipment follows (in millions):

December 31, 2013 | Capital Expenditures (Depreciation) | Retirements | March 31, 2014 | ||||||||||||

Leasehold improvements | $ | 141.1 | $ | — | $ | (109.9 | ) | $ | 31.2 | ||||||

Machinery and equipment | 164.0 | — | (36.5 | ) | 127.5 | ||||||||||

305.1 | — | (146.4 | ) | 158.7 | |||||||||||

Accumulated depreciation and amortization | (297.2 | ) | (2.5 | ) | 146.2 | (153.5 | ) | ||||||||

$ | 7.9 | $ | (2.5 | ) | $ | (0.2 | ) | $ | 5.2 | ||||||

22

11. FAIR VALUE MEASUREMENTS

Pursuant to the accounting guidance for fair value measurements, fair value is defined as the price that would be received from selling an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. When determining the fair value measurements for assets and liabilities required or permitted to be recorded at fair value, consideration is given to the principal or most advantageous market and assumptions that market participants would use when pricing the asset or liability.

As a result of USEC Inc.'s bankruptcy filing on March 5, 2014, the realization of assets and the satisfaction of liabilities are subject to uncertainty. Further, USEC's reorganization could materially change the amounts and classifications of assets and liabilities reported in the consolidated condensed financial statements.

Fair Value Hierarchy

The accounting guidance for fair value measurement also requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. The standard establishes a fair value hierarchy based on the level of independent, objective evidence surrounding the inputs used to measure fair value. A financial instrument’s categorization within the fair value hierarchy is based upon the lowest level of input that is significant to the fair value measurement. The fair value hierarchy is as follows:

• | Level 1 – quoted prices in active markets for identical assets or liabilities. |

• | Level 2 – inputs other than Level 1 that are observable, either directly or indirectly, such as quoted prices in active markets for similar assets or liabilities, quoted prices for identical or similar assets or liabilities in markets that are not active, or model-derived valuations in which significant inputs are observable or can be derived principally from, or corroborated by, observable market data. |

• | Level 3 – unobservable inputs in which little or no market data exists. |

Financial Instruments Recorded at Fair Value

Fair Value Measurements (in millions) | |||||||||||||||||||||||||||

March 31, 2014 | December 31, 2013 | ||||||||||||||||||||||||||

Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||

Assets: | |||||||||||||||||||||||||||

Cash equivalents (a) | — | $ | 80.1 | — | $ | 80.1 | — | $ | 312.7 | — | $ | 312.7 | |||||||||||||||

Deferred compensation asset (b) | — | 3.1 | — | 3.1 | — | 3.1 | — | 3.1 | |||||||||||||||||||

Liabilities: | |||||||||||||||||||||||||||

Deferred compensation obligation (b) | — | 2.9 | — | 2.9 | — | 3.0 | — | 3.0 | |||||||||||||||||||

(a) | Cash equivalents consist of funds invested in institutional money market funds. These investments are classified within Level 2 of the valuation hierarchy because the publicly reported Net Asset Value (“NAV”) of one dollar does not necessarily reflect the fair value of the underlying securities. |

(b) | The deferred compensation obligation represents the balance of deferred compensation plus net investment earnings. The deferred compensation plan is informally funded through a rabbi trust using variable universal life insurance. The cash surrender value of the life insurance policies is designed to track the deemed investments of the plan participants. Investment crediting options consist of institutional and retail investment funds. The deemed investments are classified within Level 2 of the valuation hierarchy because (i) of the indirect method of investing and (ii) unit prices of institutional funds are not quoted in active markets. |

23

Other Financial Instruments

As of March 31, 2014 and December 31, 2013, the balance sheet carrying amounts for accounts receivable, accounts payable and accrued liabilities (excluding the deferred compensation obligation described above) approximate fair value because of the short-term nature of the instruments.

The balance sheet carrying amounts and estimated fair values of USEC’s convertible senior notes follow (in millions):

March 31, 2014 | December 31, 2013 | ||||||||||||||

Carrying Value | Fair Value | Carrying Value | Fair Value | ||||||||||||

Convertible senior notes, excluding accrued interest | $ | 530.0 | $ | 185.5 | $ | 530.0 | $ | 184.1 | |||||||

The estimated fair value of the convertible notes is based on the trading price as of the balance sheet date, and is classified as using Level 1 inputs in the fair value measurement. In connection with our voluntary petition for relief under Chapter 11 of the United States Bankruptcy Code, USEC Inc. has reached an agreement on the terms of a financial restructuring plan with the holders of approximately 65% of the principal amount of our convertible senior notes. Under the terms of the agreement, USEC will replace the approximately $530 million of convertible senior notes that are scheduled to mature in October 2014 with new debt and equity. As further detailed in Note 2, the $530 million in the outstanding principal amount of convertible senior notes would be exchanged for new common stock, cash for accrued and unpaid interest, and $200 million in principal amount of new notes issued by the reorganized USEC Inc. on terms described in the Plan’s implementing documents.

12. PENSION AND POSTRETIREMENT HEALTH AND LIFE BENEFITS

The components of net benefit costs for pension and postretirement health and life benefit plans were as follows (in millions):

Defined Benefit Pension Plans | Postretirement Health and Life Benefit Plans | ||||||||||||||

Three Months Ended March 31, | Three Months Ended March 31, | ||||||||||||||

2014 | 2013 | 2014 | 2013 | ||||||||||||

Service costs | $ | 0.6 | $ | 3.7 | $ | 0.5 | $ | 0.9 | |||||||

Interest costs | 10.5 | 11.0 | 2.5 | 2.2 | |||||||||||

Expected returns on plan assets (gains) | (12.8 | ) | (12.8 | ) | (0.5 | ) | (0.6 | ) | |||||||

Amortization of actuarial (gains) losses, net | 0.3 | 6.1 | — | 0.7 | |||||||||||

Amortization of prior service costs (credits) | — | 0.2 | (0.1 | ) | — | ||||||||||

Net benefit costs (credit) | $ | (1.4 | ) | $ | 8.2 | $ | 2.4 | $ | 3.2 | ||||||

USEC expects to contribute $28.7 million to the defined benefit pension plans in 2014, including $26.5 million of required contributions under ERISA and $2.2 million to non-qualified plans. USEC has contributed $5.8 million in the three months ended March 31, 2014.

There is no required contribution for the postretirement health and life benefit plans under ERISA and USEC does not expect to contribute in 2014. USEC receives federal subsidy payments for sponsoring prescription drug benefits that are at least actuarially equivalent to Medicare Part D.

Net periodic benefit costs related to continued operations are allocated to cost of sales, selling, general and administrative expense, and advanced technology costs.

24

The defined benefit pension plans were amended to allow a lump sum payment option to active employees who are not covered by a collective bargaining agreement at the Paducah GDP who are terminated as a result of participation in a reduction in force from August 5, 2013 through December 31, 2014. Any lump sum distributions in connection with this program would fully settle USEC's long-term pension obligations related to those benefits. Total lump sum benefits paid in the first quarter of 2014 were $5.0 million. Settlement accounting, which requires immediate recognition of a portion of amounts deferred in accumulated other comprehensive income, need not be followed if the sum of the settlements for the year is less than the service cost and interest cost components of the net periodic benefit cost for the plan year, determined on a plan by plan basis. Total lump sum payments in the first quarter of 2014 fell below the minimum settlement accounting thresholds for the plans and therefore settlement accounting was not required.

13. STOCK-BASED COMPENSATION

Three Months Ended March 31, | |||||||

2014 | 2013 | ||||||

(millions) | |||||||

Total stock-based compensation costs: | |||||||

Restricted stock and restricted stock units | $ | 0.4 | $ | 0.9 | |||

Stock options, performance awards and other | — | 0.1 | |||||

Expense included in selling, general and administrative and advanced technology costs | $ | 0.4 | $ | 1.0 | |||

Total recognized tax benefit | $ | — | $ | — | |||

The total recognized tax benefit is reported at the federal statutory rate net of the tax valuation allowance.

Stock-based compensation cost is measured at the grant date, based on the fair value of the award, and is recognized over the requisite service period, which is either immediate recognition if the employee is eligible to retire, or on a straight-line basis until the earlier of either the date of retirement eligibility or the end of the vesting period. There was no stock-based compensation granted in the three months ended March 31, 2014. As of March 31, 2014, there was $0.5 million of unrecognized compensation cost, adjusted for estimated forfeitures, related to non-vested restricted shares and restricted stock units granted in prior years. That cost is expected to be recognized over a weighted-average period of 1.0 year.

14. NET INCOME (LOSS) PER SHARE

Basic net income (loss) per share is calculated by dividing net income (loss) by the weighted average number of shares of common stock outstanding during the period, excluding any unvested restricted stock. In calculating diluted net income per share, the numerator is increased by interest expense on the convertible notes and convertible preferred stock dividends, net of amount capitalized and net of tax, and the denominator is increased by the weighted average number of shares resulting from potentially dilutive securities, assuming full conversion, consisting of stock compensation awards, convertible notes, convertible preferred stock and warrants. No dilutive effect is recognized in a period in which a net loss has occurred or in which the assumed conversion effect of convertible securities is antidilutive.

25

Three Months Ended March 31, | |||||||

2014 | 2013 | ||||||

(millions) | |||||||

Numerators for basic and diluted calculations (a): | |||||||

Net (loss) from continuing operations | $ | (50.8 | ) | $ | (23.7 | ) | |

Net income from discontinued operations | — | 21.7 | |||||

Net (loss) | $ | (50.8 | ) | $ | (2.0 | ) | |

Denominator: | |||||||

Weighted average common shares | 5.0 | 5.0 | |||||

Less: Weighted average unvested restricted stock | 0.1 | 0.1 | |||||

Denominator for basic calculation | 4.9 | 4.9 | |||||

Weighted average effect of dilutive securities: | |||||||

Convertible notes | 1.8 | 1.8 | |||||

Convertible preferred stock: | |||||||

Equivalent common shares (b) | 17.1 | 7.8 | |||||

Less: share issuance limitation (c) | 16.2 | 6.9 | |||||

Net allowable common shares | 0.9 | 0.9 | |||||

Subtotal | 2.7 | 2.7 | |||||

Less: shares excluded in a period of a net loss or antidilution | 2.7 | 2.7 | |||||

Weighted average effect of dilutive securities | — | — | |||||

Denominator for diluted calculation | 4.9 | 4.9 | |||||