of these provisions effectively inhibits certain mergers or other business combinations, which, in turn, could adversely affect the market price of our common stock.

ITEM 1B — UNRESOLVED STAFF COMMENTS

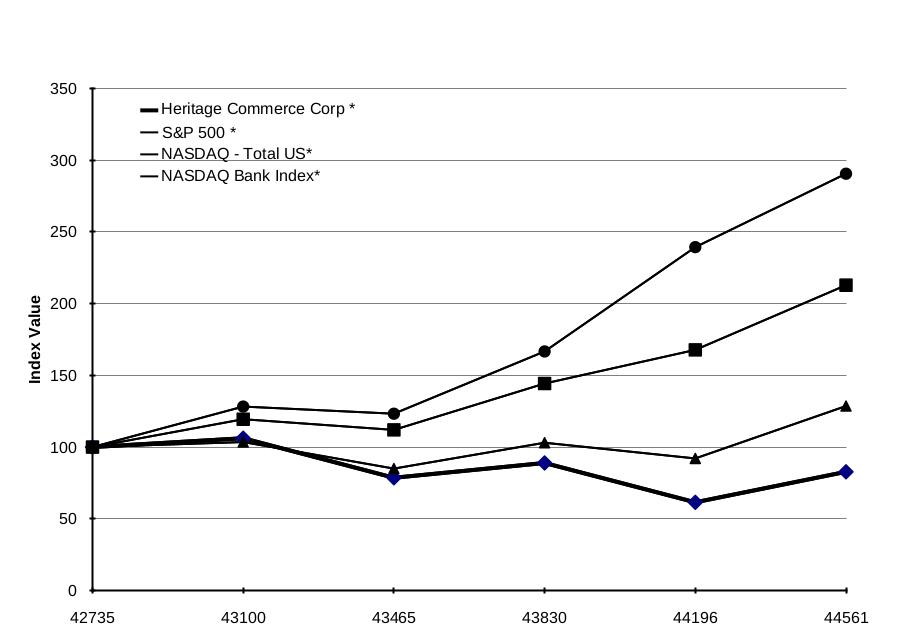

None.

ITEM 2 — PROPERTIES

The main and executive offices of Heritage Commerce Corp and Heritage Bank of Commerce are located at 224 Airport Parkway in San Jose, California 95110, with branch offices located at 15575 Los Gatos Boulevard in Los Gatos, California 95032, at 3137 Stevenson Boulevard in Fremont, California 94538, at 387 Diablo Road in Danville, California 94526, at 300 Main Street in Pleasanton, California 94566, at 1990 N. California Boulevard in Walnut Creek, California 94596, at 1987 First Street in Livermore, California 94550, at 18625 Sutter Boulevard in Morgan Hill, California 95037, at 7598 Monterey Street in Gilroy, California 95020, at 351 Tres Pinos Road in Hollister, California 95023, at 419 S. San Antonio Road in Los Altos, California 94022, at 333 W. El Camino Real in Sunnyvale, California 94087, at 325 Lytton Avenue in Palo Alto, California 94301, at 400 S. El Camino Real in San Mateo, California, 94402, at 2400 Broadway in Redwood City, California 94063, at 120 Kearny Street in San Francisco, California 94108, at 999 5th Avenue in San Rafael, California 94901 and at 1111 Broadway in Oakland, California 94607. Bay View Funding’s administrative offices are located at 224 Airport Parkway, San Jose, California 95110.

Main Offices

The main office of HBC, the San Jose branch office of HBC and the Bay View Funding administrative office are located at 224 Airport Parkway in San Jose, consisting of approximately 54,910 square feet in a six-story Class-A type office building, which are subject to a direct lease dated June 27, 2019, which expires on July 31, 2030. The current monthly rent is $209,714, subject to 3% annual increases.

Branch Offices

In June of 2007, as part of the acquisition of Diablo Valley Bank, the Company took ownership of an 8,285 square foot one-story commercial office building, including the land, located at 387 Diablo Road in Danville, California.

In February 2020, the Company renewed its lease for approximately 3,172 square feet in a one-story multi-tenant multi-use building located at 3137 Stevenson Boulevard in Fremont, California. The monthly rent payment is $10,432, subject to annual increases of 3% until the lease expires on February 29, 2024. The Company has reserved the right to extend the term of the lease for one additional period of three years.

In July of 2017, the Company extended its lease for approximately 5,213 square feet on the first floor in a two-story multi-tenant office building located at 419 S. San Antonio Road in Los Altos, California. The current monthly rent payment is $31,037, subject to annual increases of 3% until the lease expires on April 30, 2023.

In March of 2018, the Company extended its lease for approximately 3,022 square feet on the first floor of a three-story multi-tenant office building located at 333 West El Camino Real in Sunnyvale, California. The current monthly rent payment is $18,255, subject to annual increases of 3% until the lease expires on May 31, 2023.

In May of 2018, as part of the acquisition of United American Bank, the Company assumed a lease for approximately 2,369 square feet on the first floor of a two-story multi-tenant multi-use building located at 2400 Broadway in Redwood City, California. The current monthly rent payment is $14,398 until the lease expires on October 31, 2022. The Company has reserved the right to extend the lease for one additional period of two years.

In November of 2018, the Company extended its lease for approximately 1,920 square feet in a one-story stand-alone building located in an office complex at 15575 Los Gatos Boulevard in Los Gatos, California. The current monthly rent payment is $7,343, subject to annual increases of 3% until the lease expires on November 30, 2023. The Company has reserved the right to extend the term of the lease for one additional period of five years.