Exhibit 99.1

Beijing Tongmei Xtal Technology Co., Ltd.

(No. 4, East 2nd Street, Tongzhou Industrial Development Zone, Beijing)

Reply to the Second Round Audit Inquiry Letter on Application for Initial Public Offering and STAR Market Listing of Shares by Beijing Tongmei Xtal Technology Co., Ltd.

Sponsor (Lead Underwriter)

(No. 689, Guangdong Road, Shanghai)

Exhibit 99.1

To Shanghai Stock Exchange,

The Second Round Audit Inquiry Letter on Application for Initial Public Offering and STAR Market Listing of Shares by Beijing Tongmei Xtal Technology Co., Ltd. (SZKS (Audit) [2022] No. 182) (the “Inquiry Letter”) issued by you on April 26, 2022 has been received, and Beijing Tongmei Xtal Technology Co., Ltd. (the “Issuer”, the “Company” or “Beijing Tongmei”), Haitong Securities Co., Ltd. (“Haitong Securities” or the “Sponsor”), King & Wood Mallesons (the “Issuer’s Attorney”), Ernst & Young Hua Ming LLP (the “Accountant” or “Reporting Accountant”) and other relevant parties have checked and verified the questions listed in the Inquiry Letter, and now reply as follows for your review.

Except as otherwise specially stated, all abbreviations used herein shall have the same meanings in the Prospectus of Beijing Tongmei in Respect of Initial Public Offering and STAR Market Listing of Shares (Declaration Draft).

Type | Typeface |

Boldface (in bold) | Questions listed in the Inquiry Letter |

SimSun (not in bold) | Reply to questions listed in the Inquiry Letter |

Simkai (in bold) | The contents additionally disclosed or amended in such application documents as prospectus |

In this reply to the Inquiry Letter, any difference in mantissa between the sum and the sum of sub-items is due to rounding.

8-1-1

Q1. Independence | 3 |

Q2. Business Reorganization | 94 |

Q3. Fundraising Projects and Relocation and Construction of Production Lines | 110 |

Q4. Sales Revenue and Gross Profit Margin | 133 |

Q5. Inventory | 217 |

Q6. R&D Personnel and R&D Expenses | 251 |

Q7. Legality and Compliance of Source of Core Technologies | 264 |

Q8. Disclosure of Industry Related Information and Risks | 287 |

Others. Explanation About Matters Related to the Holding Foreign Companies Accountable Act | 335 |

Overall Opinions of the Sponsor | 341 |

8-1-2

According to the reply to the Inquiry Letter, (1) the Issuer acquired AXT-Tongmei in May 2021, and AXT-Tongmei is now the Issuer’s overseas seller and purchaser. AXT, the controlling shareholder of the Issuer, established AXT-Tongmei in December 2020, and notified its customers and suppliers thereof via email or otherwise, and transferred AXT’s purchasing and selling business to AXT-Tongmei, whereupon the Issuer believes that it consummated the business transfer with AXT in March 2021; (2) The confirmation letter signed by and between AXT and its customers and suppliers clearly states that AXT will maintain the status as the controlling shareholder of the Issuer, and AXT-Tongmei Inc. is the new name adopted for AXT business, and the original address and contact information remain unchanged.

The Issuer is required to explain: (1) upon business transfer, whether the parties to the Company’s domestic and overseas sale and purchase contracts, goods transhippers and warehouses, sales proceeds recipients and purchasing cost payers are AXT or affiliates under its control; (2) upon the transfer of business from AXT to AXT-Tongmei, whether the Company is obligated to notify the relevant parties of change of AXT-Tongmei shareholder into the Issuer under such arrangements as original agreements, customer certifications and supply arrangements or industry practices; if yes, the impact of the Company’s performance of such obligation or acquisition of confirmation on the conduct of business; (3) the role of AXT in maintaining the status as the Company’s controlling shareholder during the process of business transfer, whether AXT’s status as the controlling shareholder of the Company constitutes a precondition or necessary requirement for the business transfer by taking into account the factors that the customer takes into account in establishing cooperation with the Company, and the method of management of its partners

8-1-3

and relevant agreement clauses; (4) new customers acquired by the Company and the amount of newly signed orders after the business transfer, and the method of acquiring new customers and newly signed orders, as well as whether the Company’s controlling shareholder and relevant personnel have actually provided any support or convenience for the Company to acquire customers; (5) the impact of the change of shareholder of AXT-Tongmei on sales and purchases by taking into account the relevant industry practices of the semiconductor industry and international trade policies; and (6) whether the Company relies upon AXT, satisfies independence requirements and has taken specified standard measures to guarantee the independence and the effectiveness thereof by taking into account the above questions.

Reply:

I. Explanations from the Issuer

(I) Upon business transfer, whether the parties to the Company’s domestic and overseas sale and purchase contracts, goods transhippers and warehouses, sales proceeds recipients and purchasing cost payers are AXT or affiliates under its control;

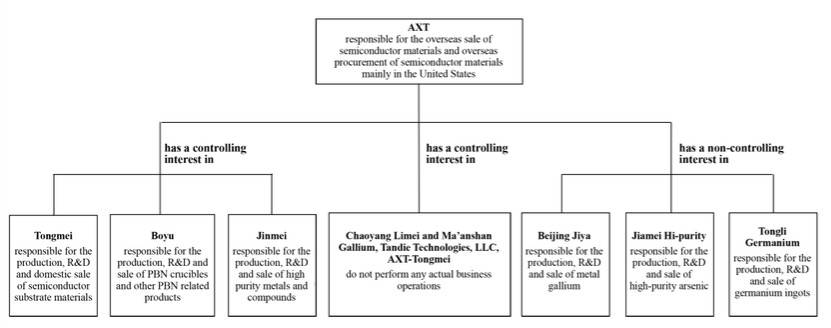

1. Business structure of AXT and the Issuer before and after reorganization and business transfer

(1) AXT’s business structure before and after reorganization and business transfer

1) Before reorganization and business transfer

Before reorganization and business transfer, the particulars of AXT and the enterprises in which AXT has a controlling interest or non-controlling interest as well as their businesses are as follows:

8-1-4

2) After reorganization and business transfer

After reorganization and business transfer, the particulars of AXT and the enterprises in which AXT has a controlling interest or non-controlling interest as well as their businesses are as follows:

3) Change of personnel before and after reorganization and business transfer

In March 2021, AXT transferred to AXT-Tongmei all of its business, procurement and R&D personnel and some of its financial and administrative personnel, and AXT-Tongmei entered into a new labor agreement with each of the said personnel; in May 2021, the Company completed the acquisition of AXT-Tongmei and also the transfer of relevant bodies and personnel. The particulars of the

8-1-5

relevant personnel of AXT and their responsibilities are set out in the table below:

AXT | Position | Before business transfer | After business transfer | ||

Number of personnel | Key responsibilities | Number of personnel | Key responsibilities | ||

Management | 2 | Managing the daily operations of AXT | 2 | Managing the daily operations of AXT | |

Sale | 8 | Sales to overseas customers | - | - | |

Procurement | 1 | Overseas procurement business mainly in the United States | - | - | |

R&D | 7 | Carrying out the R&D of growing and other processes, conducting technical communication with overseas customers, and providing assistance in the R&D of sample testing | - | - | |

Other back office positions | 9 | Performing all functions relating to finance, payments and receipts, recruitment, security and other back office support | 1 | Preparing consolidated financial statements and conducting daily finance work | |

Total | 27 | - | 3 | - | |

AXT-Tongmei | Position | Before transfer | After transfer | ||

Number of personnel | Key responsibilities | Number of personnel | Key responsibilities | ||

Sale | - | - | 8 | Sales to overseas customers | |

Procurement | - | - | 1 | Overseas procurement business mainly in the United States | |

R&D | - | - | 7 | Carrying out the R&D of growing and other processes, conducting technical communication with overseas customers, and providing assistance in the R&D of sample testing | |

Other back office positions | - | - | 8 | Performing all functions relating to finance, payments and receipts, recruitment, security and other back office support | |

Total | - | - | 24 | - | |

8-1-6

It can be seen from the above table that, AXT has three (3) employees upon business transfer, among whom MORRIS SHEN-SHIN YOUNG serves as CEO, Gary L. Fisher serves as CFO and Secretary, and Alan Chan serves as Vice President of Finance and Corporate Controller.

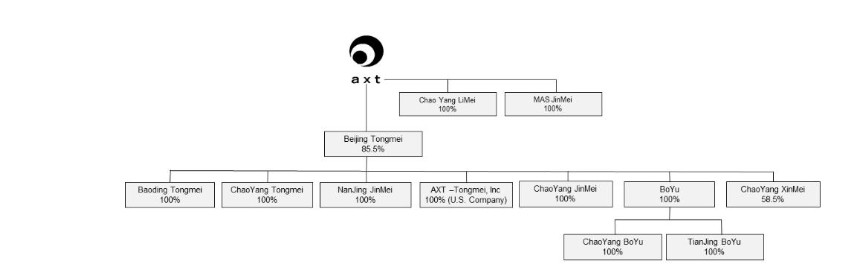

(2) Business structure of the Issuer before and after asset reorganization and business transfer

The business structure of AXT and the Issuer and changes thereof before and after asset reorganization and business transfer are set out in the table below:

Level | Entity | Responsibilities at the beginning of the reporting period | Change and transfer | Current responsibilities |

AXT | AXT’s parent company | Domestic sale, and procurement functions and some R&D functions in the United States | Transferring overseas procurement, sale and R&D functions, business orders and corresponding personnel to AXT-Tongmei | No actual business operations; only having three (3) employees responsible for maintaining daily operations |

The Issuer and companies under its control | Beijing Tongmei, Baoding Tongmei and Chaoyang Tongmei | R&D, production and domestic sale of InP, GaAs and Ge substrates | No significant change | Basically consistent with those at the beginning of the reporting period |

Nanjing Jinmei and Chaoyang Jinmei | R&D, production and sale of high-purity metals and compounds | |||

Beijing Boyu, Tianjin Boyu and Chaoyang Boyu | R&D, production and sale of PBN materials | |||

AXT-Tongmei | Not established yet | Receiving the original overseas procurement, sale and R&D functions, business | Overseas sale, and procurement functions and some applied R&D functions in |

8-1-7

orders and corresponding personnel from AXT’s parent company | the United States | |||

Chaoyang Xinmei | Not established yet | Newly established, to be responsible for the production and sale of high-purity gallium | No actual business operations |

Note: Tianjin Boyu and Chaoyang Boyu are subsidiaries of Beijing Boyu.

At the end of 2020, AXT contributed additional capital to Beijing Tongmei in the form of equity of Baoding Tongmei, Chaoyang Tongmei, Nanjing Jinmei, Chaoyang Jinmei and Beijing Boyu. In December 2020, AXT established AXT-Tongmei in the United States, which company was acquired by the Issuer in May 2021. Upon completion of the reorganization and business transfer, the Issuer established a complete industry chain for the R&D, production and sale of semiconductor substrate materials, PBN crucibles, key raw materials and high-purity metals.

8-1-8

2. Transfer of customers

AXT, as the overseas selling entity of semiconductor substrate materials, established AXT-Tongmei in the United States in December 2020; In March 2021, AXT notified its customers and suppliers by email that AXT would transfer its sales and procurement business and personnel to AXT-Tongmei; In May 2021, the Issuer completed the acquisition of ATX-Tongmei. During the reporting period, the proportion of the amount of proceeds from the performance of selling functions by AXT and AXT-Tongmei for the Company in the operating revenue of the Issuer is set out in the table below:

In RMB0’000

Item | 2021 | 2020 | 2019 | |||

Amount | Proportion | Amount | Proportion | Amount | Proportion | |

Overseas business revenue | 41,860.60 | 48.83% | 33,609.67 | 57.63% | 28,034.46 | 60.65% |

Including: Proceeds from the performance of selling functions by AXT and AXT-Tongmei under the control of AXT | 12,993.13 | 15.16% | 28,196.51 | 48.35% | 22,144.98 | 47.91% |

Domestic business revenue | 43,873.92 | 51.17% | 24,707.37 | 42.37% | 18,188.22 | 39.35% |

Operating revenue | 85,734.52 | 100.00% | 58,317.04 | 100.00% | 46,222.68 | 100.00% |

Note: In 2021, the proceeds from the performance of selling functions by AXT and AXT-Tongmei are proceeds obtained by the Company through AXT, and through AXT-Tongmei under the control of AXT prior to the end of May 2021.

① All customers involved in the domestic business are independently developed by the Issuer and its domestic subsidiaries, and perform the corresponding

8-1-9

production, sale, receipt and other functions, which has nothing to do with AXT.

② The overseas business mainly involves the sale of semiconductor substrate materials, PBN crucibles and other PBN products. The customers of PBN products involved in the overseas business are independently developed by Beijing Boyu, for which the sales are also implemented by Beijing Boyu. AXT is only responsible for the sale of semiconductor substrate materials to overseas customers.

③ There is no overlap between domestic customers and overseas customers, instead there is an overlap between some overseas customers of Beijing Boyu and AXT customers (who became the customers of AXT-Tongmei upon transfer). During the reporting period, the percentage of proceeds from the sale of PBN products by the overlapping customers (mainly including Sumitomo) in the proceeds from PBN products and business of the Company is 19.77%, 17.24% and 13.51% respectively, demonstrating a decrease year by year.

As the world-renowned telecommunication service provider and industrial manufacturer, Sumitomo is one of the Company’s competitors, and purchased semiconductor substrate materials from AXT through its subsidiary Sumika Electronic Materials, Inc., and also purchased PBN crucibles and PBN boards from Beijing Boyu through another subsidiary SUMIDEN SHOJI CO., LTD. These two customers are Sumitomo’s subsidiaries in different business segments, and make independent procurement decisions. They are not involved in any direct connection or incidental purchase.

④After transferring the business to AXT-Tongmei in March 2021, AXT will acquire no additional orders after completing orders on hand; in May 2021, after completing the acquisition of AXT-Tongmei, the Issuer incorporated the overseas sales of semiconductor substrates into the Issuer. In June 2021, the revenue realized through AXT by implementing orders on hand was RMB10,400. From July 2021, since all previous orders of AXT have been completed, the Issuer no longer made sales through AXT.

To sum up, the customers involved in the transfer are sellers of semiconductor

8-1-10

substrate materials in the overseas business, details of which are as follows:

AXT clearly notified its overseas customers via email and by telephone in March 2021 that given the fact Beijing Tongmei, the subsidiary in which AXT has a controlling interest, seeks to be listed on the STAR Market, Beijing Tongmei’s selling business and selling entity will be transferred from AXT to AXT-Tongmei. The Company received the confirmations from the customers via email, or the customer placed subsequent orders directly with AXT-Tongmei. In May 2021, the Company acquired AXT-Tongmei, and completed the business transfer.

During the process of business transfer, the letter sent by AXT to each customer states that: 1) AXT will maintain the status as the Issuer’s controlling shareholder; 2) AXT-Tongmei is a company incorporated in Delaware, and will conduct business on behalf of AXT; and 3) since AXT-Tongmei leased the original office space of AXT, and relevant sales personnel were transferred from AXT to AXT-Tongmei, the original address and contact information of the customer will remain unchanged, in order for the parties to maintain communication.

All original customers of AXT were transferred and continued to have business dealings with the Company based on their needs. The notices sent by the Company to end customers who achieved 90.50% of the sales proceeds through AXT and confirmations thereof are set out in the table below:

S/N | Name of major customer | Has the customer been notified of the reason for business transfer | Has the customer made confirmation | Discussion process | Confirmation date | Confirmation by the customer | Particulars of current transaction with AXT-Tongmei |

Type 1: Confirmation made by the customer via email | |||||||

1 | Customer C | √ | √ | Email + telephone | 2021/3/3 | Confirmation by email | Consistently placing orders |

2 | VPEC | √ | √ | Email + telephone | 2021/3/15 | Confirmation by email | Consistently placing orders |

3 | Osram | √ | √ | Email + | 2021/3/22 | Confirmation by | Consistently |

8-1-11

telephone | placing orders | ||||||

4 | IQE | √ | √ | Email + telephone | 2021/3/16 | Confirmation by email | Consistently placing orders |

5 | Win | √ | √ | Fill in supplier evaluation score sheet, supplier change application and supplier informed consent | 2021/5/17 | Confirmation by email | Consistently placing orders |

6 | LandMark Optoelectronics | √ | √ | Email + telephone | 2021/3/10 | Confirmation by email | Consistently placing orders |

Type 2: Confirmation by signing new orders with AXT-Tongmei | |||||||

1 | Mo Sangyo Co, Ltd. | √ | √ | Email + telephone | 2021/3/8 | By signing new orders with AXT-Tongmei | Consistently placing orders |

2 | VISHAY SEMICONDUCTOR GmbH | √ | √ | Email + telephone | 2021/3/10 | By signing new orders with AXT-Tongmei | Consistently placing orders |

3 | AVAGO TECHNOLOGIES INT'L SALES | √ | √ | Email + telephone | 2021/4/21 | By signing new orders with AXT-Tongmei | Consistently placing orders |

4 | Azur Space | √ | √ | Email + telephone | 2021/3/15 | By signing new orders with AXT-Tongmei | Consistently placing orders |

5 | INTELLIGENT EPITAXY TECHNOLOGY | √ | √ | Email + telephone | 2021/6/2 | By signing new orders with AXT-Tongmei | Consistently placing orders |

6 | II-VI | √ | √ | Email + telephone | 2021/6/2 | By signing new orders with AXT-Tongmei | Consistently placing orders |

7 | KAGA TOSHIBA ELECTRONICS CO. | √ | √ | Email + telephone | 2021/4/7 | By signing new orders with AXT-Tongmei | Consistently placing orders |

8 | AUK | √ | √ | Email + | 2021/3/15 | By signing new | Consistently |

8-1-12

CORPORATION | telephone | orders with AXT-Tongmei | placing orders | ||||

9 | WAFER TECHNOLOGY | √ | √ | Email + telephone | 2021/3/9 | By signing new orders with AXT-Tongmei | Consistently placing orders |

The contract performance by the said customers upon business transfer is as follows:

S/N | Name of major customer | Was there any framework agreement before transfer | Is the original framework agreement still being implemented | Is there any new framework agreement entered with AXT-Tongmei upon transfer | Has any order been placed with AXT- Tongmei upon transfer | Has any new order been signed with AXT upon transfer |

1 | Customer C | No | Not involved | No | Yes | No |

2 | VPEC | No | Not involved | No | Yes | No |

3 | Osram | Yes | No | No | Yes | No |

4 | IQE | No | Not involved | No | Yes | No |

5 | Win | No | Not involved | No | Yes | No |

6 | LandMark Optoelectronics | No | Not involved | No | Yes | No |

7 | Mo Sangyo Co, Ltd. | Yes | No | Yes | Yes | No |

8 | VISHAY SEMICONDUCTOR GmbH | No | Not involved | No | Yes | No |

9 | AVAGO TECHNOLOGIES INT'L SALES | No | Not involved | No | Yes | No |

10 | Azur Space | No | Not involved | No | Yes | No |

11 | INTELLIGENT EPITAXY TECHNOLOGY | No | Not involved | No | Yes | No |

12 | II-VI | No | Not involved | No | Yes | No |

13 | KAGA TOSHIBA | No | Not involved | No | Yes | No |

8-1-13

ELECTRONICS CO. | ||||||

14 | AUK CORPORATION | No | Not involved | No | Yes | No |

15 | WAFER TECHNOLOGY | No | Not involved | No | Yes | No |

According to the industry practices, generally, all overseas customers of semiconductor substrate materials placed direct orders upon certification of the supplier’s products, without entering into a framework agreement. Osram entered into a framework agreement with AXT in April 2014, but due to the early execution of such agreement, the parties conducted the transaction as per the relevant order during the reporting period. Upon business transfer, Osram purchased goods by placing orders directly with AXT-Tongmei other than AXT. Mo Sangyo Co., Ltd. entered into a new framework agreement with AXT-Tongmei, and will not implement any agreement relating to AXT. Beyond that, the said customers have not entered into relevant framework agreements with the Company.

Upon transfer, all overseas customers placed orders with AXT-Tongmei, and will not place new orders with AXT.

The relevant situation after the completion of transfer of semiconductor substrate material business is as follows:

1) Domestic

All domestic purchases and sales, logistics and transportation, warehousing and receipts and payments have been executed by such domestic entities as Beijing Tongmei, Baoding Tongmei, Chaoyang Tongmei, Chaoyang Jinmei and Nanjing Jinmei, and remain unchanged before and after business transfer, and all domestic customers and suppliers are independently developed and acquired by the Company and its domestic subsidiaries.

2) Overseas

Before the business transfer, AXT is responsible for the overseas sale of the Company’s semiconductor substrates and the purchase of raw materials in the United

8-1-14

States, and domestic entities are responsible for purchases in other overseas regions, details of which are as follows:

Item | Parties to contract/order | Shipper/recipient Product/raw materials warehouse | Recipient | Payer |

Overseas sale | ||||

InP substrate and Germanium substrate | AXT | Beijing Tongmei and AXT | AXT | N/A |

GaAs substrate | AXT | Baoding Tongmei and AXT | AXT | |

Overseas purchase | ||||

Beijing Tongmei and AXT | Beijing Tongmei and AXT | N/A | Beijing Tongmei and AXT | |

GaAs substrate | Chaoyang Tongmei and AXT | Chaoyang Tongmei and AXT | Chaoyang Tongmei and AXT | |

Upon business transfer, AXT-Tongmei undertook the original functions of AXT, and AXT no longer undertook any functions, and the functions of other entities remain unchanged, details of which are as follows:

Item | Parties to contract/order | Shipper/recipient Product/raw materials warehouse | Recipient | Payer |

Overseas sale | ||||

InP substrate and Germanium substrate | AXT-Tongmei | Beijing Tongmei and AXT-Tongmei | AXT-Tongmei | N/A |

GaAs substrate | AXT-Tongmei | Baoding Tongmei and AXT-Tongmei | AXT-Tongmei | |

Overseas purchase | ||||

InP substrate and Germanium substrate | Beijing Tongmei and AXT-Tongmei | Beijing Tongmei and AXT-Tongmei | N/A | Beijing Tongmei and AXT-Tongmei |

GaAs substrate | Chaoyang Tongmei and AXT-Tongmei | Chaoyang Tongmei and AXT-Tongmei | Chaoyang Tongmei and AXT-Tongmei | |

Upon business transfer, relevant business personnel involved in overseas purchases and sales were transferred from AXT to AXT-Tongmei, the purchaser and entity placing product sale orders of raw materials relating to semiconductor substrates in the United States, and received remuneration from AXT-Tongmei, details of which are as follows:

① Overseas sale

A. Contracts/orders have been signed by AXT-Tongmei with respect to the overseas sale of semiconductor substrates in accordance with the requirements and arrangements of the Issuer; B. Beijing Tongmei and Baoding Tongmei have

8-1-15

respectively shipped the products subject to sale in the United States to AXT-Tongmei’s warehouse, and upon short-term storage at the warehouse, AXT-Tongmei shipped such products to the place designated by the relevant customer; C. Beijing Tongmei and Baoding Tongmei have directly shipped the products subject to sale in other countries or regions from the relevant warehouse to the place designated by the relevant customer; D. All overseas sale proceeds have been directly received by AXT-Tongmei, and then used to make payments to Beijing Tongmei and Baoding Tongmei for their respective purchases, pay wages of their employees and disburse rentals and other daily expenses. No funds have flowed to AXT.

During the process of business transfer, both AXT-Tongmei and AXT had accounts receivable from the same customer, and some customers remitted the amounts payable to AXT-Tongmei to AXT, which amounts were then remitted by AXT to AXT-Tongmei. As of September 2021, the total amount of accounts received by AXT on behalf of AXT-Tongmei was RMB10.2483 million, representing a small percentage in operating revenue. Upon receipt of the payment for goods of the Company, AXT promptly transferred the same to AXT-Tongmei, and does not possess any funds of the Company. The above situation does not involve the circulation of external funds. As of October 2021, the Company has never been involved in the above situation.

② Overseas purchase

Overseas purchase is quite similar to overseas sale: A. Orders have been placed by AXT-Tongmei with respect to the purchase of raw materials relating to semiconductor substrates in the United States, and orders have been directly placed by Beijing Tongmei and Chaoyang Tongmei with respect to purchases in other regions; B. The raw materials subject to purchases in the United States were shipped to Beijing Tongmei and Chaoyang Tongmei upon short-term storage at AXT-Tongmei’s warehouse, and the relevant supplier has directly shipped the products subject to sale in other countries or regions to Beijing Tongmei and Chaoyang Tongmei; C. All goods have been paid for by the entity placing orders.

To sum up, upon business transfer, the parties to the Company’s domestic and overseas sale and purchase contracts, goods transhippers and warehouses, sales proceeds recipients and purchasing cost payers are the Issuer and subsidiaries under its control, and are not AXT or the affiliates under AXT’s control. The production,

8-1-16

supply and distribution system of the Issuer is independent and complete, and the Issuer has taken over all end customers from AXT without losing customers.

3. Transfer of suppliers

During the reporting period, the particulars of key raw materials and equipment purchased by the Company from related and non-related parties are as follows:

During the reporting period, the proportion of key raw materials required for the production activities and operation of the Company from related and non-related parties respectively is set out in the table below:

In RMB0’000

Item | Supplier | 2021 | 2020 | 2019 | |||

Amount | Percentage | Amount | Percentage | Amount | Percentage | ||

Metal gallium | Non-related party | 8,190.77 | 53.71% | 3,274.44 | 51.57% | 367.39 | 37.59% |

Related party | 7,059.32 | 46.29% | 3,075.53 | 48.43% | 609.98 | 62.41% | |

Total | 15,250.09 | 100.00% | 6,349.97 | 100.00% | 977.37 | 100.00% | |

Germanium ingots | Non-related party | 4,149.61 | 89.84% | 3,989.59 | 86.38% | 1,943.00 | 67.48% |

Related party | 469.50 | 10.16% | 628.89 | 13.62% | 936.19 | 32.52% | |

Total | 4,619.11 | 100.00% | 4,618.48 | 100.00% | 2,879.19 | 100.00% | |

Quartz material | Non-related party | 3,849.18 | 100.00% | 2,965.95 | 100.00% | 1,574.30 | 100.00% |

Related party | - | - | - | - | - | - | |

Total | 3,849.18 | 100.00% | 2,965.95 | 100.00% | 1,574.30 | 100.00% | |

High-purity arsenic | Non-related party | 1,112.49 | 66.41% | - | - | - | - |

Related party | 562.68 | 33.59% | 1,214.61 | 100.00% | 991.72 | 100.00% | |

Total | 1,675.17 | 100.00% | 1,214.61 | 100.00% | 991.72 | 100.00% | |

Boron trichloride | Non-related party | 1,009.54 | 100.00% | 915.83 | 100.00% | 1,042.18 | 100.00% |

Related party | - | - | - | - | - | - | |

Total | 1,009.54 | 100.00 | 915.83 | 100.00 | 1,042.1 | 100.00 | |

8-1-17

% | % | 8 | % | ||||

Indium phosphide polycrystalline | Non-related party | 1,230.59 | 100.00% | 693.76 | 100.00% | 1,485.51 | 100.00% |

Related party | - | - | - | - | - | - | |

Total | 1,230.59 | 100.00% | 693.76 | 100.00% | 1,485.51 | 100.00% | |

Key raw materials | Non-related party | 19,542.18 | 70.72% | 11,839.57 | 70.65% | 6,412.38 | 71.64% |

Related party | 8,091.51 | 29.28% | 4,919.03 | 29.35% | 2,537.90 | 28.36% | |

Total | 27,633.69 | 100.00% | 16,758.61 | 100.00% | 8,950.28 | 100.00% |

Note: The purchases from the said affiliates include those from companies in which AXT has a controlling interest, from companies in which the Issuer has a controlling interest, and from third parties through AXT.

Generally speaking, the key raw materials required for the production activities and operations of the Company are sourced from related parties, accounting for a relatively low proportion. Only metal gallium, germanium ingots and high-purity arsenic in the key raw materials are involved in the connected purchases, and the supply capacity of the non-related parties of and the quality of such three types of key raw materials may be seen in “Q1 “1.2 I. (I). 2. Analyze the role of related suppliers in the Company’s raw materials supply and its impact on supply stability according to the actual supply of upstream raw materials, the supply capacity and quality of non-related parties and other factors;” in this Reply.

During the reporting period, the key raw materials purchased in a connected transaction through AXT are germanium ingots and high-purity arsenic, in which the purchase amount of germanium ingots is RMB1,716,200, RMB6,288,900 and RMB0 respectively, and the purchase amount of high-purity arsenic is RMB2,017,500, RMB3,080,700 and RMB970,300.

During the reporting period, the fact that the Company has a non-controlling interest in some qualified suppliers effectively guarantees the supply stability of the raw materials. However, given small difference in the quality of products provided by the non-related supplier of the said raw materials, if its raw materials have passed the Company’s test and been accepted by downstream customers, the Company can purchase relevant products from non-related parties. In addition, upon transfer of the

8-1-18

overseas suppliers in the United States, the said connected purchase between the Company and AXT has been solved.

During the reporting period, the proportion of equipment required for the production activities and operations of the Company from related and non-related parties respectively is set out in the table below:

In RMB0’000

Supplier | 2021 | 2020 | 2019 | |||

Amount | Proportion | Amount | Proportion | Amount | Proportion | |

Non-related party | 6,224.48 | 91.53% | 1,929.59 | 76.20% | 3,271.07 | 73.83% |

Related party | 576.05 | 8.47% | 602.54 | 23.80% | 1,159.69 | 26.17% |

Total | 6,800.53 | 100.00% | 2,532.13 | 100.00% | 4,430.76 | 100.00% |

Note: The purchases from the said affiliates are those from third parties through AXT.

At the early stage of the Company’s development, the domestic III-V compound semiconductor material industry was just starting, and the number of qualified suppliers (in particular key equipment suppliers) was very small. For the convenience of procurement, and in order to guarantee the production stability of products, the Company purchased single crystal polishing machine, single crystal furnace, vacuum furnace controller and other equipment with daily high energy consumption mainly through AXT. For the convenience of procurement, the Company continued to import the equipment with daily high energy consumption through AXT; in 2021, after AXT implemented the original equipment purchase order, the Company directly purchased equipment from suppliers or through AXT-Tongmei other than AXT.

During the reporting period, the equipment purchased by the Issuer from AXT is mainly germanium ingots, high-purity arsenic, single crystal polishing machine, single crystal furnace, vacuum furnace controller and other equipment with daily high energy consumption. There is a wide selection of domestic suppliers of germanium ingots, and the Company has completed the transfer with respect to the purchase of high-purity arsenic and single crystal polishing machine, details of which are as follows:

AXT clearly notified its overseas suppliers via email and by telephone in March 2021 that given the fact Beijing Tongmei, the subsidiary in which AXT has a

8-1-19

controlling interest, seeks to be listed on the STAR Market, the purchase business and purchasing entity will be transferred from AXT to AXT-Tongmei. The Company received the confirmations from the customers via email. In May 2021, the Company acquired AXT-Tongmei, and completed the transfer of the purchase business.

During the process of business transfer, the letter sent by AXT to each supplier states that: 1) AXT will maintain the status as the Issuer’s controlling shareholder; 2) AXT-Tongmei is a company incorporated in Delaware, and will conduct purchase business on behalf of AXT; and 3) since AXT-Tongmei leased the original office space of AXT, and relevant sales personnel were transferred from AXT to AXT-Tongmei, the original address and contact information of the customer will remain unchanged, in order for the parties to maintain communication.

As far, AXT has notified all suppliers of the matters relating to business transfer via email, and details of the transfer of top five (5) suppliers before purchase of raw materials by AXT are set out in the table below:

S/N | Name of major customer | Has the letter of CEO been sent? | Has the order been issued concurrently? | Communication process | Symbol for completion of transfer | Particulars of current transaction with AXT-Tongmei |

1 | H-SQUARE CORPORATION | √ | √ | Telephone | Confirmation by the supplier via email | Still consistently placing orders |

2 | KNF CLEAN ROOM PRODUCTS | √ | √ | Telephone | Confirmation by the supplier via email | Still consistently placing orders |

3 | ENTEGRIS, Inc. | √ | √ | Telephone | Confirmation by the supplier via email | Still consistently placing orders |

4 | CONAX TECHNOLOGIES LLC | √ | √ | Telephone | Confirmation by the supplier via email | Still consistently placing orders |

5 | SAINT-GOBAIN ADVANCED CERAMICS | √ | √ | Telephone | Confirmation by the supplier via email | Still consistently placing orders |

(II) Upon the transfer of business from AXT to AXT-Tongmei, whether the Company is obligated to notify the relevant parties of change of AXT-Tongmei shareholder into the Issuer under such arrangements as original agreements,

8-1-20

customer certifications and supply arrangements or industry practices; if yes, the impact of the Company’s performance of such obligation or acquisition of confirmation on the conduct of business;

1. The Company has no obligation to notify the relevant parties (other than Osram)

According to Osram’s supplier manual, any supplier that experiences change of control shall notify it thereof; AXT clearly notified Osram via email and by telephone in March 2021, and received the confirmation from Osram via email. Currently, the Issuer and the intermediary have confirmed with Osram the change of the controlling shareholder of AXT-Tongmei into Beijing Tongmei, and Osram procurement manager confirmed as follows through Osram official email:

(1) The change of the controlling shareholder of AXT-Tongmei into Beijing Tongmei does not affect the cooperation between Osram and AXT-Tongmei;

(2) Osram selects suppliers mainly relying on the production environment and other relevant quality and system certificates of suppliers;

(3) With the production sites, production lines, and other factors remaining unchanged, the choice of the selling entity will not affect Osram’s procurement of products produced by Beijing Tongmei; and

(4) Generally, there is only one supplier under one group in Osram’s list of suppliers; by now, Osram has changed AXT to AXT-Tongmei in its supplier system, and will no longer retain AXT.

8-1-21

In addition, in accordance with the practices of the semiconductor materials industry and the regulations of the Company, in the event of any of the following major changes, the Company needs to re-certify customers, obtain the consent from customers and re-sign the Process Change Notification as the case may be. Details of the changes and processing methods are as follows:

Level of change | Definition | Specific change | Processing method |

First level | Key changes in production processes | Change of production site | The Process Change Notification needs to be re-signed and obtain the consent of the customer, and the customer needs to be re-certified. |

Change of key raw materials | |||

Second level | Key changes in process or materials | Overall change of cleaning equipment | The Process Change Notification needs to be re-signed and obtain the consent of the customer. |

Change of cleaning reagent | |||

Change of polishing solution | |||

Packaging change | |||

Change of testing method | |||

Third level | Change of product information or label | Revision of change level classification or standard format | The Process Change Notification needs to be re-signed. |

Change of label information | |||

Fourth level | Minor process changes | Minor adjustment or optimization of process parameters that do not fall in the columns of first, second and third levels of change | The Process Change Notification does not need to be re-signed. |

As shown in the above table, the change of controlling shareholder of AXT-Tongmei from AXT to the Issuer does not involve change of production site, change of key raw materials, major changes in process or materials, change of product information or label information and minor changes of processes, and does not fall under any of the above four circumstances.

To sum up, AXT has notified Osram and obtained its confirmation based on the relevant agreements between the Company and customers and suppliers, the agreements on customer certification and supply arrangements; in addition, the

8-1-22

Company is not obligated to notify the relevant parties of the change of the shareholder of AXT-Tongmei into the Issuer.

2. The Company has performed the obligation of notification

In August 2021, AXT disclosed in the “Basic Information” section in 2021 Semi-Annual Report published on NASDAQ that: “AXT sold AXT-Tongmei to Beijing Tongmei for $1”. Upon the announcement of the Company’s acquisition of AXT-Tongmei, the composition of AXT’s subsidiaries is as follows:

In addition, AXT promptly announced the prospectus reviewed and disclosed on the STAR Market and the reply to questions, and also announced the business transfer.

So far, AXT-Tongmei has maintained a good partnership with overseas customers, and the relevant parties have not raised any objection to the cooperation between the parties in relation to this business transfer and the announcement.

3. Good business conduct upon transfer

In March 2021, AXT-Tongmei completed the business transfer with AXT and started overseas procurement and sales; in May 2021, the Issuer completed the acquisition of AXT-Tongmei.

At the end of June 2021, AXT-Tongmei had the total assets of RMB125.7014 million, mainly including the accounts receivable, monetary funds, and other assets formed after the business transfer is completed in March 2021 and subsequent overseas procurement and sales; from Marth to June 2021, AXT-Tongmei realized the revenue of RMB108.3759 million, with the closing balance

8-1-23

of RMB114.9253 million in total for accounts receivable, monetary funds, and inventories. While making sales to others, AXT-Tongmei needs to purchase semiconductor substrate materials from a domestic entity of the Issuer; therefore, AXT-Tongmei makes monthly payment to the domestic entity according to the billing cycle. As of December 31, 2021, AXT-Tongmei had the balance of monetary funds in the amount of RMB27.5767 million.

So far, it has been nearly twelve (12) months since the Company’s acquisition of AXT-Tongmei, and the operation of AXT-Tongmei upon business transfer goes well. The changes in the amount of revenue and sales achieved by overseas customers of the Company in 2020 and 2021 are set out in the table below:

In RMB0’000 or 0’000 units

Name of customer | 2021 | 2020 | ||

Amount | Sales | Amount | Sales | |

Osram | 10,668.93 | 98.35 | 9,389.14 | 87.84 |

LandMark Optoelectronics | 2,430.77 | 9.14 | 2,804.49 | 10.71 |

Mo Sangyo Co, Ltd. | 3,626.34 | 25.62 | 2,208.70 | 18.19 |

IQE | 3,973.88 | 24.81 | 2,252.91 | 16.59 |

VPEC | 3,471.19 | 20.68 | 1,366.78 | 3.24 |

Customer C | 1,015.61 | 3.22 | 813.45 | 2.36 |

Others | 8,986.11 | 181.82 | 9,383.22 | 138.93 |

Total | 34,172.83 | 255.43 | 28,218.69 | 220.04 |

Note: The revenue received in 2021 is estimated based on the sales volume and the average selling price of the products sold in 2020; the sales volume is determined based on 2-inch substrate products.

It can be seen from the above table that, upon business transfer, there was a significant increase in the revenue obtained by major overseas customers, and that the Company can maintain a good partnership with the said customers, and has not experienced a great decline in its business performance due to business transfer.

To sum up, the Company has performed the obligation to notify Osram and obtained Osram’s confirmation in accordance with the relevant agreements signed with its

8-1-24

customers and suppliers, the agreement on customer certification and supply arrangement, but has no obligation to notify the relevant parties of the change of the shareholder of AXT-Tongmei into the Issuer; in order to avoid the misunderstanding of overseas customers and suppliers, AXT published an announcement on the NASDAQ, so that customers, suppliers and global investors can better understand relevant conditions; upon business transfer, AXT-Tongmei has maintained a good partnership with overseas customers, and the purchase quantity and orders placed by the customers have increased; the Issuer has successfully accepted the relevant overseas customers from AXT.

(III) The role of AXT in maintaining the status as the Company’s controlling shareholder during the process of business transfer, whether AXT’s status as the controlling shareholder of the Company constitutes a precondition or necessary requirement for the business transfer by taking into account the factors that the customer takes into account in establishing cooperation with the Company, and the method of management of its partners and relevant agreement clauses;

AXT’s status as the controlling shareholder of the Company has a positive impact on the successful business transfer, but does not constitute a precondition or necessary requirement for successful business transfer, nor does it constitute a precondition or necessary requirement for continuous cooperation with the Company.

1. Customers

(1) Factors that the customer takes into account in establishing cooperation with the Company

8-1-25

Based on the practices in the semiconductor substrate industry and the Company’s actual situation, the factors that a downstream customer takes into account in establishing cooperation with the Company mainly include product performance, product stability and ability to continuously supply products, details of which are as follows:

No. | Major factor | Particular case |

1 | Product performance | The customer will consider whether the size and performance parameters of the products supplied by the Company can meet its requirements in establishing cooperation with the Company, and the size and performance parameters of the products are closely related to the Company’s R&D and technological level. |

2 | Product stability | The customer elects to focus on the stability of the Company’s products in establishing cooperation with the Company, and product stability is mainly reflected in the continuous production by the downstream customer using the substrates supplied by the Company, and in the stable performance and parameters of epitaxial wafers produced by the customer. There will be no major difference between batches of products. Product stability is closely associated with production lines and processes. Thus, the customer generally will verify the Company’s production lines and processes in establishing cooperation with the Company. Meanwhile, the customer will also verify with its downstream customer whether the substrate-based epitaxial wafers and chips can meet its final requirements for product performance; only upon verification will the customer place a formal order to the Company. |

3 | Ability to continuously supply products | Since the Company’s ability to timely deliver a certain quantity of its substrate products will directly affect the customer’s production and operation rhythm, the customer needs to maintain long-term and good partnership with the Company, and to regularly inspect the production capability and level of the Company. The quantity of products supplied by the Company may be reasonably determined only after the parties establish a close and trusted partnership, thus the customer will maintain close communication with the Company’s sales personnel. |

Except for the above factors, the customer will also consider the Company’s position in the industry, types of other users of the products and product positioning in the market, and subsequent ability to continuously provide services.

8-1-26

(2) Method of the customer’s management of suppliers

1) Customer C

According to the interview with Customer C, Customer C adopts dual supplier management of “entity subject to product certification + order placement entity”, details of which are as follows:

① Management of entities subject to product certification

With respect to product certification, only the entity whose products have been certified by Customer C may be included in its list of eligible suppliers. The entity who has passed the product certification needs to complete and maintain the eligible supplier review procedures in accordance with its supplier management rules and regulations. According to the practices in the semiconductor materials industry, generally, the downstream customer will certify the manufacturer’s products, details of which are as follows:

No. | Main process | Particular case |

1 | Provide relevant materials | Provide the manufacturer’s information (e.g. business license, relevant certificates and supplier questionnaire), and confirm whether such information meets the customer’s requirements. |

2 | Provide assistance in production line assessment | Assist the customer’s quality, production, procurement and other departments to conduct an audit of the manufacturer’s production lines and processes. |

3 | Multiple delivery of samples for testing | The manufacturer needs to deliver the products multiple times to the customer for testing purposes. After the samples so delivered pass the test, the customer will purchase a small batch of the Company’s products; after such batch of products pass the test, the Issuer will include the manufacturer in the list of eligible suppliers and officially commence the cooperation with the manufacturer. |

4 | Assist the customer to identify production problems | The manufacturer needs to promptly respond to the customer if any production problem has been identified, and to assist the customer to determine the root cause of the problem. If the problem lies in the substandard substrate product, the customer will request replacement or return. |

5 | Assist the customer to pay regular return visits | Due to long certification cycle and high certification costs, once the supplier passes the certification, the downstream customer usually does not easily change the supplier. During years of cooperation, most overseas customers will regularly and irregularly go to China to inspect production lines, so as to confirm whether the production process and quality management system of the Company’s products meet the customer’s standards. |

Note: The certification process for different customers may differ. For instance, some customers with small purchases only certify product performance and parameters without assessing production lines.

8-1-27

② Management of contracted supplier (being seller)

According to the interview with Customer C, the contracted supplier needs to provide Customer C with its name, tax identification number, bank account number and other information, in order for Customer C to enter the same into Customer C’s supplier system. Upon business transfer, Customer C only maintains Beijing Tongmei and AXT-Tongmei (other than AXT) under its dual supplier management system in its supplier system.

In addition, as shown in the monthly statement sent by Osram to the Company upon business transfer, its supplier has also been changed from AXT to AXT-Tongmei, and it has changed the supplier code in its system.

③ Business relationship under the dual supplier management system

Upon business transfer, the business relationship among Beijing Tongmei (entity subject to product certification), AXT-Tongmei (seller) and the customer (for instance, Customer C) is as follows:

2) Osram, IQE, Visual Photonics Epitaxy (VPEC), Landmark Optoelectronics, VISHAY SEMICONDUCTOR GmbH, Mo Sangyo Co, Ltd. and AUK CORPORATION

8-1-28

According to the interview with Osram, IQE, VPEC, LandMark Optoelectronics, VISHAY SEMICONDUCTOR GmbH, Mo Sangyo Co, Ltd. and AUK CORPORATION, they have a supplier catalog and accept only an individual entity under the control of the same group as its supplier, and upon business transfer, such customers have deleted AXT from its supplier catalog and system, and replaced AXT with AXT-Tongmei, and entered AXT-Tongmei’s enterprise name, tax identification number, bank account number and other information in the system.

(3) Relevant agreement clauses

Osram (the global innovation promoter in the LED field), Customer C, IQE (the world’s leading compound semiconductor epitaxial wafer designer and manufacturer) and VPEC (the world-renowned epitaxial wafer manufacturer) from top ten overseas customers of the Company are selected for analysis. In their supplier management manuals or agreements, specific agreements on process, product quality and changes are as follows:

Customer | Agreed clauses | Agreement on process and product quality | Agreement on changes |

Osram | Osram’s purchase rules | 1. The supplier agrees not to change any specifications, form, coordination, functions, design, appearance, materials and technologies and manufacturing processes or facilities of deliverables, or to make any other revision to the warranties provided in GPC that affects or is likely to reasonably affect the quality, performance or compliance of the products without the prior written approval of the company; 2. In case of any unreasonable oversupply or shortfall, or any quality deviation, the supplier shall indemnify and hold the Company harmless from all expenses incurred by the Company due to extra inspections, packaging, return or storage. In any case, returns in excess of ordered quantity or unordered quantity shall be at the supplier’s cost and risk. | In case of any change of the control of the supplier, the supplier shall immediately notify Osram. Osram reserves the right to cancel orders for such change of ownership, without bearing further obligations and responsibilities. |

Customer C | Customer C’s supplier compliance manual | To ensure compliance with agreement clauses, reduce supply chain risks to the maximum extent, ensure quality and supply or secure the items purchased from or sold by the supplier, the supplier will conduct comprehensive cooperation with Customer C or any third party designated by Customer C, and Customer C or such third party may at any time inspect the supplier’s work, documents, property, assets, records and communication in a reasonable manner. The supplier may, upon Customer C’s written request, carry out in good faith such inspection in accordance with agreement clauses, which inspection shall not cause | N/A |

8-1-29

unreasonable interference with its normal business activities or operations. Within two (2) weeks after receipt of Customer C’s written request for such inspection, the supplier will make commercially reasonable efforts to disclose, provide or obtain the request and give any necessary consent, in order for Customer C, any third party or competent government authority to carry out the inspection. In addition, if any third party discovers upon inspection the supplier’s non-compliance with agreement clauses, the supplier will reimburse Customer C for all expenses in connection with such inspection. | |||

IQE | IQE’s standard supplier terms and conditions | 1. The supplier warrants that, within one (1) year following IQE’s acceptance of any goods and/or services, the goods and/or services shall: (i) fit their description and conform to any IQE regulations and applicable specifications determined with the supplier (the “Specifications”); (ii) be of satisfactory quality and fit for any purpose proposed by the supplier or expressly or impliedly notified by the supplier to IQE, and be based on the supplier’s expertise and judgment; (iii) in the case of finished goods, be free from defects in design, material and workmanship; and (iv) comply with all applicable laws, regulations and regulatory requirements; 2.1 IQE may inspect and test any goods at any time before shipment. Despite that IQE has conducted any such inspection or testing, the supplier shall also be held fully liable with respect to any goods, and any such inspection or test shall not diminish or otherwise affect the supplier’s obligations; 2.2 If, upon such inspection or testing, IQE deems that the goods do not conform to or are unlikely to comply with the supplier’s undertakings in Clause 2.1, IQE shall notify the supplier, and the supplier shall immediately take necessary remedial measures to ensure compliance; 2.3 After the supplier takes remedial measures, IQE may conduct further inspections and tests; | The supplier shall not assign or transfer any of its rights or obligations hereunder without the prior written consent of IQE (which shall not be unreasonably withheld or delayed). IQE may assign its rights and delegate its obligations. The supplier shall not subcontract any or all of its rights or obligations hereunder without the prior written consent of IQE; |

VPEC | Supplier quality manual | 1. The supplier is responsible for implementing all test and inspection requirements provided in the purchase documents. VPEC reserves the right to witness or carry out any such tests and inspections provided in the purchase documents, and to review the data generated during the course of the supplier carrying out such tests and inspections; 2. The supplier may be invited to participate in VPEC’s quality plans, including quality management system, process chart, production part approval process, failure mode and impact analysis, process control plan, rectification measures, failure analysis and continuous improvement plan. | Upon product certification, any change that requires VPEC’s comment is likely to be re-certified. The supplier shall follow the PCN process and provide support data, and shall not make any revision before VPEC’s comment. |

The Company needs to maintain regular communication with the customer in terms of production management, product quality, process and relevant changes in

8-1-30

accordance with the supplier management manuals of Osram, Customer C, IQE, VPEC and other key overseas customers or the provisions of relevant agreements regarding the Company. According to Osram’s supplier manual, any supplier that experiences change of control shall notify it thereof. The Company has notified Osram, and received its confirmation. So far, the Company has maintained good partnership with the above customers, and relevant agreements or orders signed by such parties are in the process of being performed.

(4) The role of AXT in maintaining the status as the Company’s controlling shareholder

1) The role of AXT in maintaining the status as the Company’s controlling shareholder

Through comprehensive analysis, the role of AXT in maintaining the status as the Company’s controlling shareholder is summarized as follows:

Item | Key indicator to be taken into consideration | Core factor | The role of AXT in maintaining the status as the Company’s controlling shareholder during the process of business transfer | Whether or not customer certification is involved |

Factors taken into consideration in establishing cooperation | Product performance | Company’s R&D and technological level | No material impact; AXT’s status as the Company’s controlling shareholder is not directly associated with the Company’s R&D and technological level | Yes |

Product stability | Product production process | No material impact; AXT’s status as the Company’s controlling shareholder is not directly associated with the stability of the Company’s production and processes | Yes | |

Ability to continuously supply products | Partnership with the Company; cooperation history; the Company’s capability for production | AXT has maintained cooperation with overseas customers for many years, and AXT’s status as the Company’s controlling shareholder is not directly associated with the Company’s production capacity and ability to continuously supply products | No |

8-1-31

and prompt response | ||||

Management method | Some customers have a catalog of eligible suppliers | Complete and maintain the customer’s eligibility review procedures in accordance with the customer’s supplier management mode and relevant regulations | No material impact; AXT’s status as the Company’s controlling shareholder is not directly associated with the Company’s ability to complete and maintain the customer’s eligibility review procedures in accordance with the customer’s supplier management rules and relevant regulations | Yes |

Relevant agreement clauses | Quality management, process requirements and change notification | Comply with the customer’s supplier management manual or agreement | No material impact; AXT’s status as the Company’s controlling shareholder is not directly associated with whether the Company complies with the customer’s supplier management manual or agreement | Yes |

Based on the analysis in the above table, AXT has been maintaining cooperation with key overseas customers for many years, and at the time of business transfer, maintaining its status as the Company’s controlling shareholder has reduced the costs of communication of the Company and the customer, which enables the customer to provide coordination and assistance to a greater extent. However, when it comes to customer certification, AXT’s status as the Company’s controlling shareholder will not directly affect the Company’s actual production lines or the performance and process stability of its products. Thus, despite the change of controlling shareholder, the customer does not need to re-certify the Company’s products. In addition, the Company has not made any covenant to the customer that AXT will maintain the status as its controlling shareholder in any contract or order signed by and between the Company and the customer.

8-1-32

2) Take Mo Sangyo Co, Ltd. for example

By taking the Company’s customer Mo Sangyo Co, Ltd. for example, according to the statement issued by Mo Sangyo Co, Ltd., as a trader in Japan, it provides semiconductor substrates mainly to Dowa Holdings Co., Ltd. (the world-renowned semiconductor materials enterprise established in 1937), ROHM (the world-renowned semiconductor enterprise established in 1958) and SONY (the world-renowned tech company established in 1946).

Mo Sangyo Co, Ltd. has executed agreements with the said customer, and has purchased relevant products from the Company. The Company does not have any direct business dealing with its downstream customers. The said end customer needs products that meet its performance and parameter requirements, and the relevant delivery obligations, risks and responsibilities are for the account of Mo Sangyo Co, Ltd., the trader in Japan. Based on the above judgment, it has relatively low requirements for sellers.

(5) The Company has not obtained any business by relying on the controlling shareholder

1) AXT-Tongmei is not obligated to notify any customer (other than Osram) of any change of control

Based on the management of the semiconductor substrates industry, the customer’s management of suppliers and the relevant agreements with the customer, AXT-Tongmei is not obligated to notify any customer (other than Osram) of any change of control. According to Osram’s supplier manual, any supplier that experiences change of control shall notify it thereof; AXT clearly notified Osram via email and by telephone in March 2021, and received the confirmation from Osram via email. Currently, the Issuer and the intermediary have confirmed with Osram the change of the controlling shareholder of AXT-Tongmei into Beijing Tongmei, and obtained confirmation from Osram that: the above matter will not affect the cooperation between Osram and AXT-Tongmei.

To sum up, the Company is not required to notify overseas customers (other than

8-1-33

Osram) of change of control of AXT-Tongmei, and the change of control of its supplier does not affect the normal course of the transaction between the parties. Thus, it can be seen that the choice of the customer to purchase products from the supplier does not depend on the background of the customer, the supplier or the de facto controller, but mainly depends on whether its products can pass customer certification.

2) Confirmation of interviews with key overseas customers

The intermediary interviewed Osram, Customer C, LandMark Optoelectronics, VPEC, VISHAY SEMICONDUCTOR GmbH, Mo Sangyo Co, Ltd., IQE, WIN Semiconductors and AUK CORPORATION (the revenue of such customers in 2020 represents, in aggregate, 76.52% of the sales generated by the Company through AXT) respectively from May 3 to 8, 2022, details of which upon confirmation of such customers are as follows:

① The cooperation between the customer and the Issuer mainly depends on the certification of the Issuer’s products, and the stable performance, good quality and timely supply of the products manufactured by the Issuer.

② If the production site and production line of the Issuer remain unchanged, the selection of any entity to sell the products manufactured by the Issuer does not affect the cooperation between the Issuer and the customer.

③ The Issuer is not required to notify the customer of the change of shareholder of AXT-Tongmei. (Osram has re-confirmed and informed that such matter does not affect its cooperation with AXT-Tongmei)

④ AXT has been replaced by AXT-Tongmei in the customer’s supplier system.

3) Industry particulars

The prospectus of National Silicon Industry Group (“NSIG”) demonstrates that: “Semiconductor silicon wafer is the core material for chip manufacturing, and the chip manufacturer has extremely high requirements in terms of the quality of semiconductor silicon wafers and is very prudent in supplier selection. According to industry practices, a manufacturer may only be included in the supply chain after certification of the semiconductor silicon wafer products. Once the products pass the

8-1-34

certification, the chip manufacturer will not easily change the supplier.”

The reply to the first-round feedbacks given by SICC shows that: “During the verification of 4-inch semi-insulating silicon carbide substrates, the Company discussed with the customer with respect to specific product parameters, e.g. microtubule, warpage and bending, and used the product parameters to benchmark the testing equipment and testing standards of the parties. After the product and technical parameters of the Company met any key customer’s standards, the Company supplied a small batch of goods to the key customer, and the customer conducted internal certification of such goods, so as to verify whether its epitaxial wafer and chip tape-out meet its product performance requirements. During the certification process, the parties continued to conduct technical communication, and the customer placed orders in batch upon such verification.

Thus, it can be seen that the choice of the customer to purchase products from the supplier mainly depends on whether its products can pass customer certification.

To sum up, AXT’s status as the controlling shareholder of the Company has a positive impact on the successful business transfer, but does not constitute a precondition or necessary requirement for successful business transfer, nor does it constitute a precondition or necessary requirement for continuous cooperation with the Company. The Company has not obtained any business by relying on the controlling shareholder.

2. Supplier

(1) Factors that the supplier takes into account in establishing cooperation with the Company

The factors that the supplier takes into account in establishing cooperation with the Company mainly include purchasing stability, the Company’s market position, purchasing price and payment cycle, details of which are as follows:

No. | Key factor | Particular case |

1 | Purchasing stability | The supplier will take into account the Company’s purchasing stability in choosing to cooperate with the Company. The purchasing stability involves purchase quantity and amount and is closely associated with |

8-1-35

the Company’s production lines, production capacity and production yield. | ||

2 | The Company’s market position | The supplier will take into account the Company’s market position in choosing to cooperate with the Company. Generally, the supplier’s products need to pass the verification and test by the downstream customer or ultimate brand in terms of reliability, function, resistance in harsh environment before inclusion in its supplier catalog. Thus, if the supplier can be included in the supplier catalog of well-known customers, its industry reputation will also be enhanced. |

3 | Purchasing price and payment cycle | The supplier will consider the purchasing price of the Company in choosing to cooperate with the Company. Generally, the supplier would prefer to cooperate with price-insensitive customers. On the other hand, customers with short payment period are able to alleviate the financial pressure of the supplier to a great extent, thus the supplier will prefer to cooperate with customers with short payment period. |

(2) Method of the customer’s management of suppliers

The Company implements management measures with respect to overseas suppliers, and conducts certification of the suppliers’ products. The Company will coordinate global sourcing by taking into account such factors as supplier quotation, supply capacity and product quality.

(3) Relevant agreement clauses

The relevant agreement clauses agreed between the Company and key overseas suppliers and orders signed by and between the parties provide as follows:

Supplier | Management clauses | International trade arrangements | Supply cycle | Quality management | Obligations to be assumed by the Company |

TOKO SHOJI&CO,LTD | Supplier Management Regulations and orders signed by the parties | 1. Sea transport; 2. Notification before shipment; 3. The supplier shall deliver all products and provide all services in compliance with all applicable national and international export control, customs and foreign trade regulations (the “Foreign Trade Regulations”). The | 1. If any order cannot be executed, the supplier shall notify the Company within three (3) days thereof; 2. In case of damaged packaging of, collision against or rain damage to the imported goods and materials during transport, the Company shall | 1. The product packing list shall indicate the supplier’s name, material description, specifications, quantity, place of arrival, transportation method and pricing clause; 2. Coordinate with the purchaser and IQC to confirm the quality of the products that have arrived at the place of arrival. IQC shall confirm the quality of Type A and Type B key materials in accordance with the Inspection Procedures for | The Company shall make timely payments as per the relevant order; |

8-1-36

supplier shall obtain all necessary export permits; | coordinate with the carrier to deal with claims. In the event of delayed delivery or other transportation problems, the Company shall pursue a claim in accordance with contractual clauses based on the degree of impact caused thereby to the production schedule of the Company; | Incoming Materials. In case the products supplied by any non-ASL supplier do not meet the quality requirements, the Company may replace or return such products or pursue a claim therefor; | |||

YONEDA CORPORATION | Supplier Management Regulations and orders signed by the parties | 1. CIP; 2. The supplier shall deliver all products and provide all services in compliance with all applicable national and international export control, customs and foreign trade regulations (the “Foreign Trade Regulations”). The supplier shall obtain all necessary export permits; | 1. If any order cannot be executed, the supplier shall notify the Company within three (3) days thereof; 2. In case of damaged packaging of, collision against or rain damage to the imported goods and materials during transport, the Company shall coordinate with the carrier to deal with claims. In the event of delayed delivery or other transportation problems, the Company shall pursue a claim in accordance with contractual clauses based on the degree of impact caused thereby to the production schedule of the Company; | 1. The product packing list shall indicate the supplier’s name, material description, specifications, quantity, date and place of arrival, transportation method and pricing clause; 2. Coordinate with the purchaser and IQC to confirm the quality of the products that have arrived at the place of arrival. IQC shall confirm the quality of Type A and Type B key materials in accordance with the Inspection Procedures for Incoming Materials. In case the products supplied by any non-ASL supplier do not meet the quality requirements, the Company may replace or return such products or pursue a claim therefor; | 1. Payment 30 days after arrival; 2. The Company shall make timely payments as per the relevant order; |

By taking into account the clauses of relevant agreements executed by and

8-1-37

between TOKO SHOJI&CO,LTD, YONEDA CORPORATION and other key overseas suppliers and the Company, the cooperation between the Company and the supplier mainly focuses on the Foreign Trade Regulations, price, date of arrival, product quality and payment method, and the Company is not obligated to notify the supplier of the change of shareholder of AXT-Tongmei. Upon completion of the business transfer, the Company still has a global sourcing system and keeps close cooperation with overseas suppliers.

(4) The role of AXT in maintaining the status as the Company’s controlling shareholder

Through comprehensive analysis, the role of AXT in maintaining the status as the Company’s controlling shareholder during the transfer of the supplier’s business is summarized as follows:

Item | Key indicator to be taken into consideration | Core factor | The role of AXT in maintaining the status as the Company’s controlling shareholder during the transfer of the supplier’s business | Whether or not the supplier’s core interests are involved |

Factors taken into account in establishing cooperation | Purchasing stability | Production lines, production capacity and production yield | No material impact; AXT’s status as the Company’s controlling shareholder is not directly associated with production lines, production capacity and production yield | Yes |

The Company’s market position | The Customer’s industry reputation | The capacity as a qualified supplier of AXT, a company listed on NASDAQ, can enhance the industry reputation of the supplier. | No | |

Purchasing price and payment cycle | The Company’s willingness and ability to make payments | No material impact; AXT’s status as the Company’s controlling shareholder is not directly associated with the Company’s willingness and ability to make payments | Yes | |

Management method | The supplier does not have any | N/A | No material impact; the Company has coordinated global sourcing and provided alternative solutions | No |

8-1-38

management requirements for the Company | by taking into account purchasing price, exchange rate impact, supply cycle and other factors, and has cooperated with overseas suppliers in the purchaser’s market | |||

Relevant agreement clauses | Agreement clauses regarding the Company’s management of the supplier | Whether or not the supplier complies with the Company’s supplier management regulations | No material impact; AXT’s status as the Company’s controlling shareholder is not directly associated with whether the supplier complies with the Company’s supplier management regulations | Yes |

Based on the analysis in the above table, the status of AXT (a company listed on NASDAQ) as the controlling shareholder of the Company can enhance the supplier’s industry reputation. During the process of business transfer, the supplier will give full consideration to AXT’s market positioning and brand effect, and the costs of communication between the parties will be reduced. In addition, AXT’s status as the controlling shareholder of the Company will not affect the business transfer between the Company and the supplier.

(5) US-based suppliers do not have special requirements for the background of shareholders of their customers

Upon business transfer, the Company arranges for its subsidiary AXT-Tongmei to purchase products in the United States, and domestic purchases and purchases in other overseas regions are for the account of the Company and domestic subsidiaries. The Company’s suppliers in the United States are relatively dispersed. The raw materials supplied by such suppliers are mainly auxiliary materials for production lines, and the suppliers do not have special requirements for the background of shareholders of their customers.

(IV) New customers acquired by the Company and the amount of newly signed orders after the business transfer, and the method of acquiring new customers and newly signed orders, as well as whether the Company’s

8-1-39

controlling shareholder and relevant personnel have actually provided any support or convenience for the Company to acquire customers;

1. New customers acquired by the Company and the amount of newly signed orders after the business transfer, and the method of acquiring new customers and newly signed orders

After the business transfer, AXT-Tongmei signed new contracts or orders with all overseas customers to continue the cooperative relationships. In 2021, the Company achieved revenues of RMB341.7283 million with its overseas semiconductor substrate material business (calculated based on the current sales volume as well as the annual average export selling price of substrate materials of various sizes in 2020), a YoY growth of 21.10%. The acquisition of new orders came from the continuation of the cooperative relationships.

After the business transfer, the Company also acquired some new customers both at home and abroad. However, as the Company is the world’s mainstream III-V compound semiconductor substrate supplier, most of the downstream manufacturers with a certain scale around the world have become the Company’s customers, details of which are as follows:

Main downstream application sectors | Name of customer | Position in the industry | Some of its major downstream customers |

5G, data centers, and optical fiber communications | LandMark Optoelectronics | The world’s largest III-V compound semiconductor epitaxy manufacturer | Lumentum and Apple |

Win Semiconductors | The world’s largest GaAs wafer foundry | Apple, Broadcom | |

IQE | A listed British company, and the world’s second largest III-V compound semiconductor epitaxy manufacturer | Apple | |

Broadcom | A world-renowned supplier of semiconductor and infrastructure products in the sectors of RF, communications and LED | Apple | |

Qorvo | A world-renowned communications and RF chip company | Apple | |

Skyworks | A world-renowned communications and RF chip company | Apple, Samsung, Xiaomi, OPPO and |

8-1-40

VIVO | |||

New-generation displays (including Mini LED and Micro LED) | Osram | One of the world’s top two optoelectronic semiconductor manufacturers, with outstanding products in the LED sector | Volkswagen Group, BMW Group, Daimler Group, GM Group and Toyota Group |

Broadcom | A world-renowned supplier of semiconductor and infrastructure products in the sectors of RF, communications and LED | Siemens | |

Epistar | A world-renowned LED fab | Apple | |

San’an Optoelectronics | A world-renowned LED company | TCL and CSOT | |

AI and unmanned driving | LandMark Optoelectronics | The world’s largest III-V compound semiconductor epitaxy manufacturer | Apple and Broadcom |

Win Semiconductors | The world’s largest GaAs wafer foundry | Apple and Broadcom | |

Visual Photonics Epitaxy | One of the world’s top three GaAs wafer foundries | Broadcom, Qorvo and San’an Optoelectronics | |

Meta | Formerly known as Facebook, a world-renowned social media platform company | | |

Wearable devices | Masimo | A world-renowned medical technology company | Philips, Atom, Mindray and GE |

Alta Devices | A world-renowned solar thin film manufacturer | - | |

Aerospace | SolAero | A world-renowned solar panel manufacturer | - |

Azur Space | A world-renowned solar panel manufacturer | - | |

Nanchang Kingsoon | China’s largest germanium epitaxy manufacturer | - | |

Industrial laser | IPG | A world-renowned fiber laser manufacturer | Han’s Laser |

Trumpf | The world’s largest laser device manufacturer | ASML | |