Exhibit 99.2

Q2 2021 FINANCIAL RESULTS July 29, 2021 1

F O R W A R D L OO K I N G S T A T E M E N T S 2 Certain statements in this presentation that are not historical facts may constitute forward - looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are intended to be covered by the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Statements contained in this presentation that do not describe historical or current facts are forward - looking statements, including statements regard the potential effects of the COVID - 19 pandemic on the Company’s business, credit quality, financial condition, liquidity and results of operations. Forward - looking statements made with regard to the potential effects of COVID - 19 on the Company’s business, credit quality, financial condition, liquidity and results of operation may differ, possibly materially, from what is included in this presentation due to factors and future developments that are uncertain and beyond the scope of the Company’s control. These included, but are not limited to the length and extent of the economic contraction as a result of the COVID - 19 pandemic; continued deterioration in employment levels, general business and economic conditions on a national basis and in the local markets in which the Company and its banking subsidiaries operate; changes in consumer behavior due to changing political, business and economic conditions or legislative or regulatory initiatives; the possibility that future credit losses may be higher than currently expected; reputational risk relating to the Company’s participation in the Paycheck Protection Program and other pandemic - related legislative and regulatory initiatives and programs; and turbulence in capital and debt markets. Forward - looking statements involve risks and uncertainties which are difficult to predict. Forward - looking statements involve risks and uncertainties. These statements include, among others, statements regarding our strategy, evaluations of future interest rate trends and liquidity, expectations as to growth in assets, deposits and results of operations, success of acquisitions, future operations, market position, financial position, and prospects, plans and objectives of management. You should not place undue reliance on the Company’s forward - looking statements. You should exercise caution in interpreting and relying on forward - looking statements because they are subject to significant risks, uncertainties and other factors which are, in some cases, beyond the Company’s control. Forward - looking statements are based on the current assumptions and beliefs of management and are only expectations of future results. The Company’s actual results could differ materially from those projected in the forward - looking statements as a result of, among other factors, changes in interest rates; competitive pressures from other financial institutions; the effects of continued weakness in general economic conditions and the impact of the COVID - 19 pandemic on a national basis or in the local markets in which the Company operates, including changes that adversely affect borrowers’ ability to service and repay our loans; changes in the value of securities in the Company’s investment portfolio, changes in loan default and charge - off rates, the adequacy of loan loss reserves, decreases in deposit levels necessitating increased borrowing to fund loans and investments; changes in government regulation, as well as the other risks and uncertainties detailed in the Company’s Annual Report on Form 10 - K, as updated by the Company’s Quarterly Reports on Form 10 - Q and other filings submitted to the Securities and Exchange Commission. Forward looking statements speak only as of the date on which they are made. The Company does not undertake any obligation to update any forward - looking statement to reflect circumstances or events that occur after the date the forward - looking statements are made.

OVERVIEW 3 • Record quarterly net income of $31.6 million resulted in earnings per share of $0.40. • Our credit quality remained stable during the quarter. Loans of $96 million had modifications under the CARES Act as of June 30 th . • The reserve for loan losses represents a coverage ratio of 160 basis points on outstanding non - PPP loans. The Company recorded a negative provision for credit losses of $3.3 million for Q2. • Continued strong deposit and lending activity masked by accelerated PPP forgiveness. Lending pipelines remain strong across all segments. • Our net interest margin increased to 3.52% and net interest income increased $2 million from Q1. • Fee income growth of $1.1 million on a linked - quarter basis. • Expenses declined $2.8 million due to a $2.1 million gain on sale of OREO, seasonally lower compensation costs and reduced FDIC assessments. • Our Board approved a quarterly dividend of $0.12 per share.

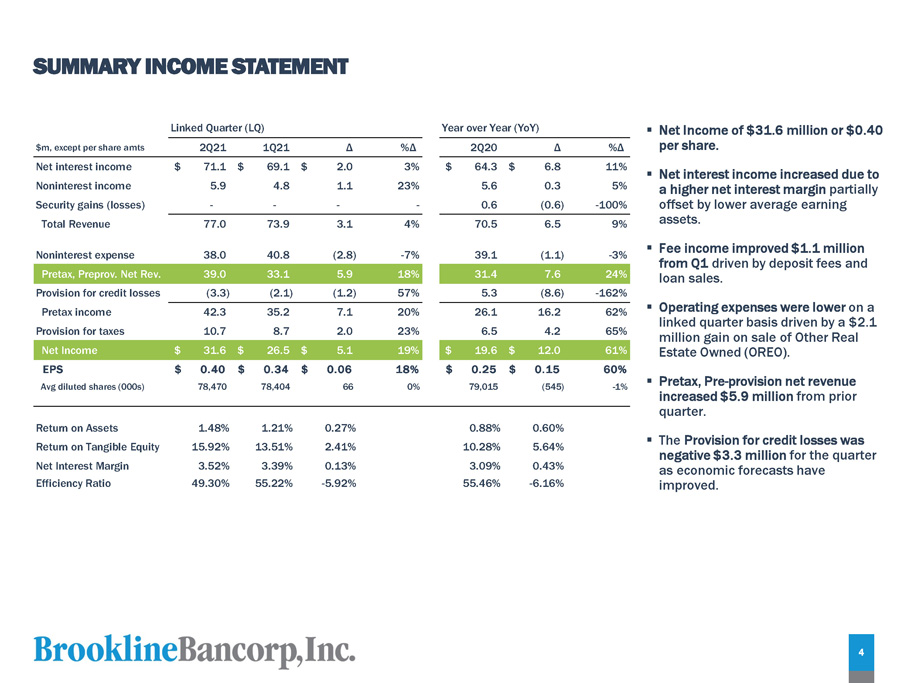

S U MM A R Y I N C O M E S T A T E M E N T ▪ Net Income of $31.6 million or $0.40 per share. ▪ Net interest income increased due to a higher net interest margin partially offset by lower average earning assets. ▪ Fee income improved $ 1 . 1 million from Q 1 driven by deposit fees and loan sales . ▪ Operating expenses were lower on a linked quarter basis driven by a $2.1 million gain on sale of Other Real Estate Owned (OREO). ▪ Pretax, Pre - provision net revenue increased $ 5 . 9 million from prior quarter . ▪ The Provision for credit losses was negative $3.3 million for the quarter as economic forecasts have improved. $m, except per share amts 2Q21 1Q21 Δ %Δ 2Q20 Δ %Δ Net interest income $ 71.1 $ 69.1 $ 2.0 3% $ 64.3 $ 6.8 11% Noninterest income 5.9 4.8 1.1 23% 5.6 0.3 5% Security gains (losses) - - - - 0.6 (0.6) - 100% Total Revenue 77.0 73.9 3.1 4% 70.5 6.5 9% Noninterest expense 38.0 40.8 (2.8) - 7% 39.1 (1.1) - 3% Pretax, Preprov. Net Rev. 39.0 33.1 5.9 18% 31.4 7.6 24% Provision for credit losses (3.3) (2.1) (1.2) 57% 5.3 (8.6) - 162% Pretax income 42.3 35.2 7.1 20% 26.1 16.2 62% Provision for taxes 10.7 8.7 2.0 23% 6.5 4.2 65% Net Income $ 31.6 $ 26.5 $ 5.1 19% $ 19.6 $ 12.0 61% EPS $ 0.40 $ 0.34 $ 0.06 18% $ 0.25 $ 0.15 60% Avg diluted shares (000s) 78,470 78,404 66 0% 79,015 (545) - 1% Return on Assets 1.48% 1.21% 0.27% 0.88% 0.60% Return on Tangible Equity 15.92% 13.51% 2.41% 10.28% 5.64% Net Interest Margin 3.52% 3.39% 0.13% 3.09% 0.43% Efficiency Ratio 49.30% 55.22% - 5.92% 55.46% - 6.16% Linked Quarter (LQ) Year over Year (YoY) 4

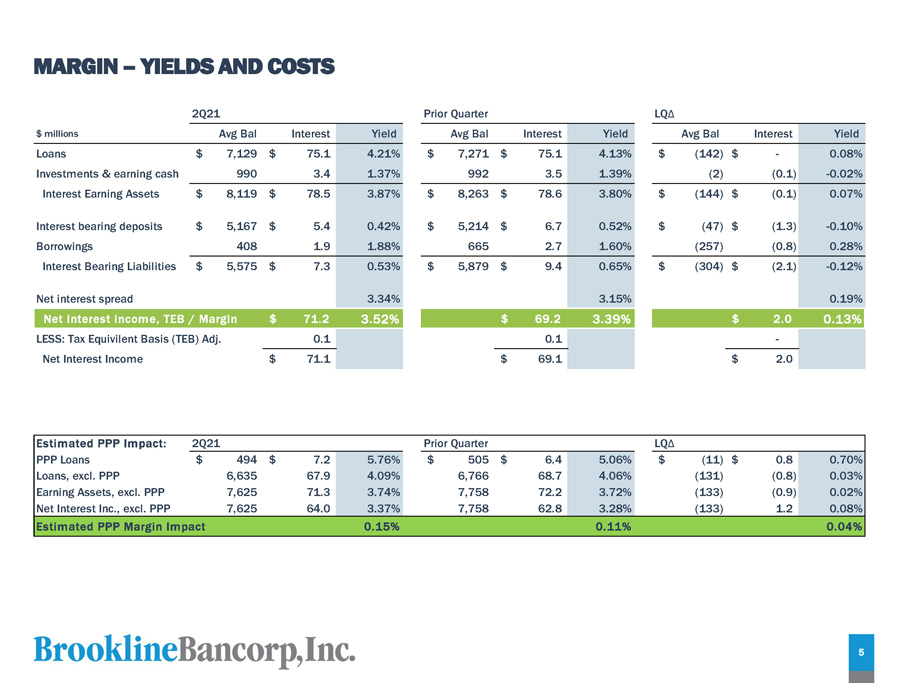

M A R G I N – Y I E L D S AN D C O S T S Estimated PPP Impact: 2Q21 Prior Quarter LQ Δ PPP Loans $ 494 $ 7.2 5.76% $ 505 $ 6.4 5.06% $ (11) $ 0.8 0.70% Loans, excl. PPP 6,635 67.9 4.09% 6,766 68.7 4.06% (131) (0.8) 0.03% Earning Assets, excl. PPP 7,625 71.3 3.74% 7,758 72.2 3.72% (133) (0.9) 0.02% Net Interest Inc., excl. PPP 7,625 64.0 3.37% 7,758 62.8 3.28% (133) 1.2 0.08% Estimated PPP Margin Impact 0.15% 0.11% 0.04% 2Q21 Prior Quarter L Q Δ $ milli o n s Avg Bal Interest Yield Avg Bal Interest Yield Avg Bal Interest Yield Loans $ 7,129 $ 75.1 4.21% $ 7,271 $ 75.1 4.13% $ (142) $ - 0.08% Investments & earning cash 990 3.4 1.37% 992 3.5 1.39% (2) (0.1) - 0.02% Interest Earning Assets $ 8,119 $ 78.5 3.87% $ 8,263 $ 78.6 3.80% $ (144) $ (0.1) 0.07% Interest bearing deposits $ 5,167 $ 5.4 0.42% $ 5,214 $ 6.7 0.52% $ (47) $ (1.3) - 0.10% Borrowings 408 1.9 1.88% 665 2.7 1.60% (257) (0.8) 0.28% Interest Bearing Liabilities $ 5,575 $ 7.3 0.53% $ 5,879 $ 9.4 0.65% $ (304) $ (2.1) - 0.12% Net interest spread 3.34% 3.15% 0.19% Net interest income, TEB / Margin $ 71.2 3.52% $ 69.2 3.39% $ 2.0 0.13% LESS: Tax Equivilent Basis (TEB) Adj. 0.1 0.1 - Net Interest Income $ 71.1 $ 69.1 $ 2.0 5

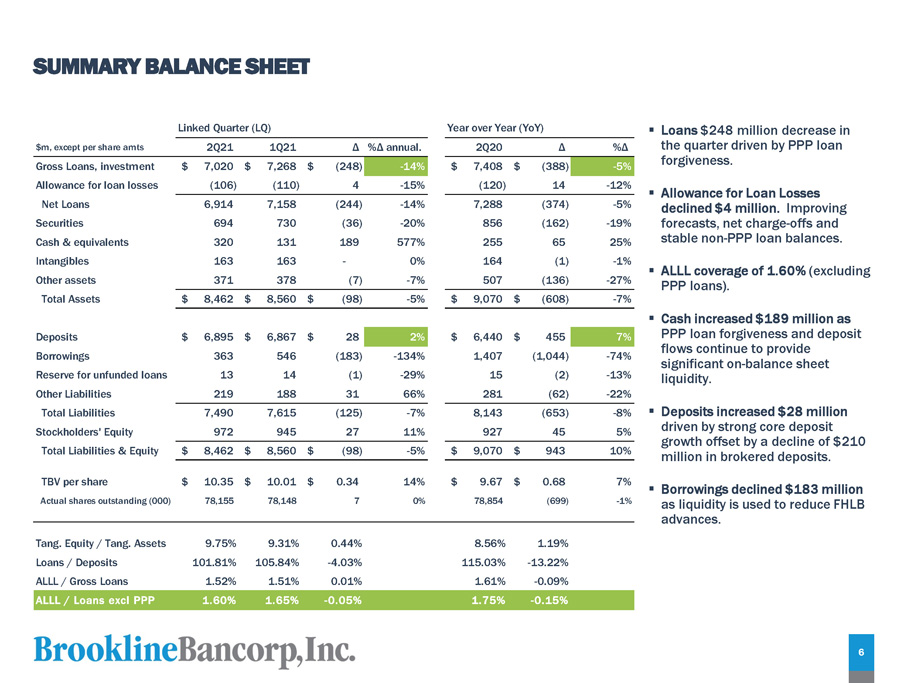

S U MM A R Y B ALAN C E SH EE T ▪ Loans $248 million decrease in the quarter driven by PPP loan forgiveness. ▪ Allowance for Loan Losses declined $4 million. Improving forecasts, net charge - offs and stable non - PPP loan balances. ▪ ALLL coverage of 1.60% (excluding PPP loans). ▪ Cash increased $189 million as PPP loan forgiveness and deposit flows continue to provide significant on - balance sheet liquidity. driven by strong core deposit growth offset by a decline of $210 million in brokered deposits. ▪ Borrowings declined $183 million as liquidity is used to reduce FHLB Deposits $ 6,895 $ 6,867 $ 28 2% $ 6,440 $ 455 7% Borrowings 363 546 (183) - 134% 1,407 (1,044) - 74% Reserve for unfunded loans 13 14 (1) - 29% 15 (2) - 13% Other Liabilities 219 188 31 66% 281 (62) - 22% Total Liabilities 7,490 7,615 (125) - 7% 8,143 (653) - 8% ▪ Deposits increased $28 million advances. Tang. Equity / Tang. Assets 9.75% 9.31% 0.44% 8.56% 1.19% Loans / Deposits 101.81% 105.84% - 4.03% 115.03% - 13.22% ALLL / Gross Loans 1.52% 1.51% 0.01% 1.61% - 0.09% ALLL / Loans excl PPP 1.60% 1.65% - 0.05% 1.75% - 0.15% $m, except per share amts Linked Quarter (LQ) 2 Q 2 1 1 Q 21 Δ %Δ annual. 2 Q 20 Δ %Δ Gross Loans, investment $ 7,020 $ 7,268 $ (248) - 14% $ 7,408 Allowance for loan losses (106) (110) Net Loans 6,914 7,158 Securities 694 730 Cash & equivalents 320 131 Intangibles 163 163 Other assets 371 378 Total Assets $ 8,462 $ 8,560 Stockholders' Equity 972 945 27 11% 927 45 5% Total Liabilities & Equity $ 8,462 $ 8,560 $ (98) - 5% $ 9,070 $ 943 10% TBV per share $ 10.35 $ 10.01 $ 0.34 14% $ 9.67 $ 0.68 7% Actual shares outstanding (000) 78,155 78,148 7 0% 78,854 (699) - 1% Year over Year (YoY) 6

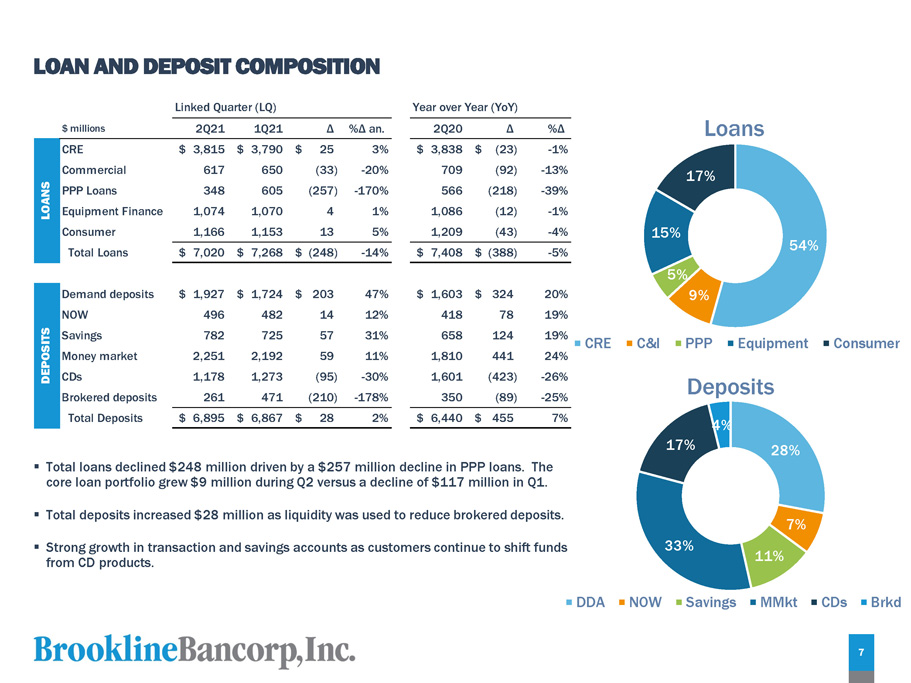

L O A N AN D D EP O SI T C O M P O SI T I O N 54% 5% 9% 15% 17% L oans Demand deposits $ 1,927 $ 1,724 $ 203 47% $ 1,603 $ 324 20% NOW 496 482 14 12% 418 78 19% IT S Savings 782 725 57 31% 658 124 19% P O S Money market 2,251 2,192 59 11% 1,810 441 24% D E CDs 1,178 1,273 (95) - 30% 1,601 (423) - 26% Brokered deposits 261 471 (210) - 178% 350 (89) - 25% Total Deposits $ 6,895 $ 6,867 $ 28 2% $ 6,440 $ 455 7% Co ns u m e r 28% 7% 11% 33% 17% CRE C&I PPP Equipment Deposits 4% D D A N O W Sa v i n g s MMk t C D s B rkd $ milli o n s 2Q21 1Q21 Δ %Δ an. 2 Q 2 0 Δ %Δ $ 3,815 617 348 1,074 1,166 $ 3,790 650 605 1,070 1,153 $ 2 5 3% (33) - 20% (257) - 170% 4 1% 13 5% CRE Co mm e r c i a l PPP Loans Equipment Finance Consumer Total Loans $ 3,838 709 566 1,086 1,209 $ ( 23 ) - 1% (92) - 13% (218) - 39% (12) - 1% (43) - 4% $ 7,020 $ 7,268 $ (248) - 14% $ 7,408 $ (388) - 5% Linked Quarter (LQ) Year over Year (YoY) LOANS ▪ Total loans declined $248 million driven by a $257 million decline in PPP loans. The core loan portfolio grew $9 million during Q2 versus a decline of $117 million in Q1. 7 ▪ Total deposits increased $28 million as liquidity was used to reduce brokered deposits. ▪ Strong growth in transaction and savings accounts as customers continue to shift funds from CD products.

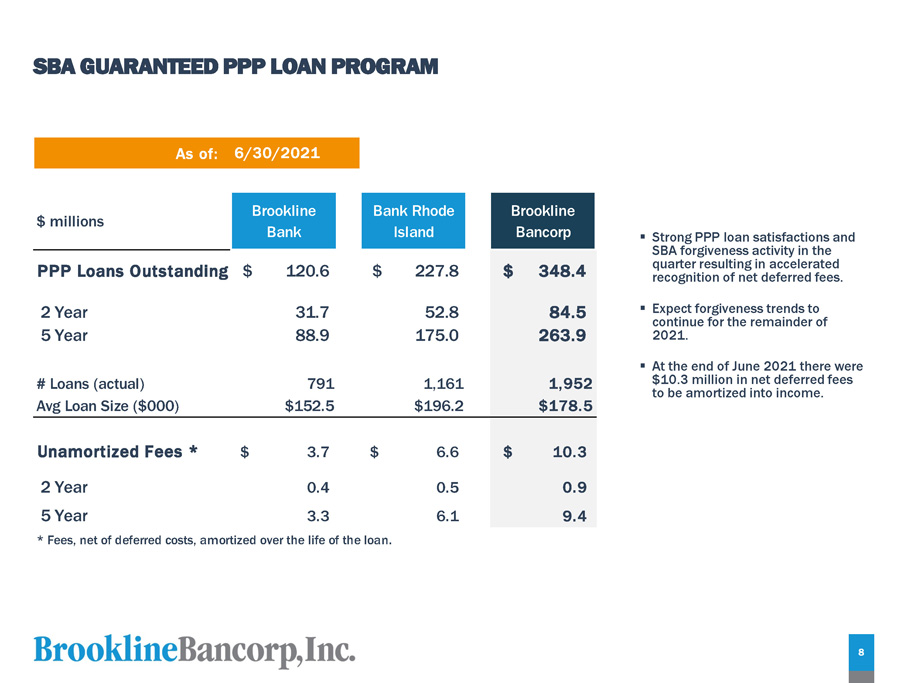

S B A G U A R A N TEE D PP P L O A N P R OG RA M ▪ Strong PPP loan satisfactions and SBA forgiveness activity in the quarter resulting in accelerated recognition of net deferred fees. ▪ Expect forgiveness trends to continue for the remainder of 2021. ▪ At the end of June 2021 there were $10.3 million in net deferred fees to be amortized into income. As of: 6/30/2021 * Fees, net of deferred costs, amortized over the life of the loan. $ millions B r oo k li n e Bank Bank Rhode Island B r oo k li n e Bancorp PPP Loans Outstanding $ 120.6 $ 227.8 $ 348.4 2 Year 31.7 52.8 84.5 5 Year 88.9 175.0 263.9 # Loans (actual) 791 1,161 1,952 Avg Loan Size ($000) $152.5 $196.2 $178.5 Unamortized Fees * $ 3.7 $ 6.6 $ 10.3 2 Year 0.4 0.5 0.9 5 Year 3.3 6.1 9.4 8

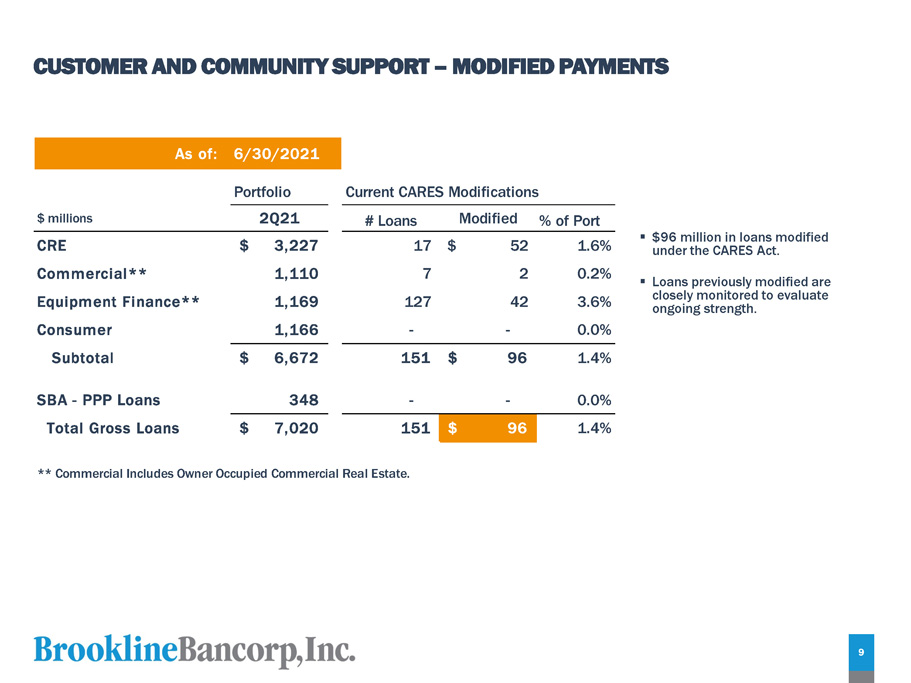

CUSTOMER AND COMMUNITY SUPPORT – MODIFIED PAYMENTS As of: 6/30/2021 Portfolio Current CARES Modifications $ millions 2Q21 # Loans Modified % of Port CRE $ 3,227 17 $ 52 1.6% Commercial** 1,110 7 2 0.2% Equipment Finance** 1,169 127 42 3.6% Consumer 1,166 - - 0.0% Subtotal $ 6,672 151 $ 96 1.4% - 0 . 0% 9 6 1 . 4% SBA - PPP Loans 348 - T o t a l Gr o s s L o an s $ 7 , 02 0 15 1 $ ** Commercial Includes Owner Occupied Commercial Real Estate. ▪ $ 96 million in loans modified under the CARES Act . ▪ Loans previously modified are closely monitored to evaluate ongoing strength . 9

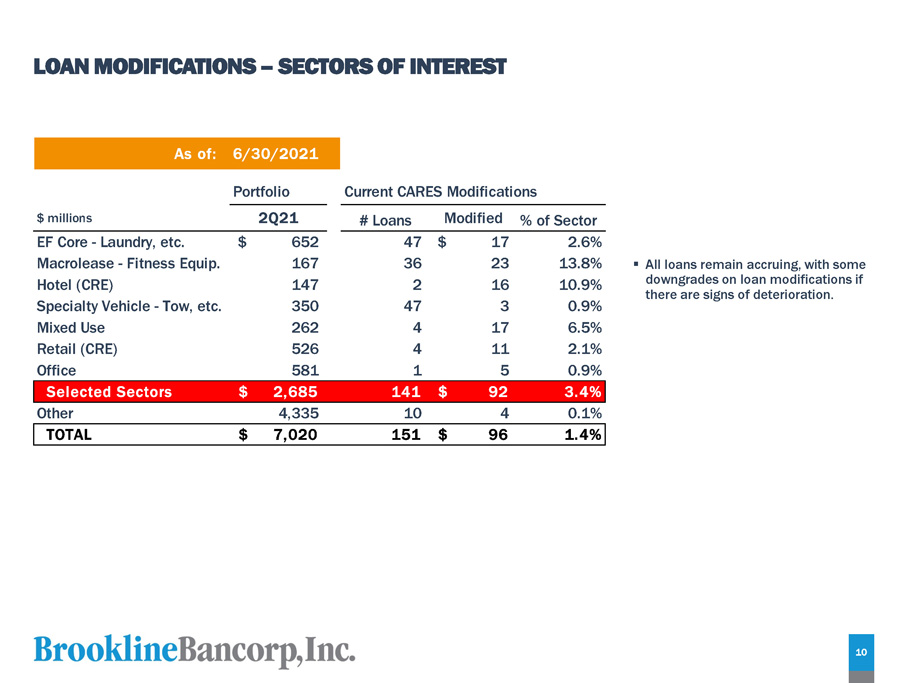

LOAN MODIFICATIONS – SECTORS OF INTEREST $ millions 2Q21 # Loans Modified % of Sector EF Core - Laundry, etc. $ 652 47 $ 17 2.6% Macrolease - Fitness Equip. 167 36 23 13.8% Hotel (CRE) 147 2 16 10.9% Specialty Vehicle - Tow, etc. 350 47 3 0.9% Mixed Use 262 4 17 6.5% Retail (CRE) 526 4 11 2.1% Office 581 1 5 0.9% Selected Sectors $ 2,685 141 $ 92 3.4% Other 4,335 10 4 0.1% TOTAL $ 7,020 151 $ 96 1.4% As of: 6/30/2021 Portfolio Current CARES Modifications ▪ All loans remain accruing, with some downgrades on loan modifications if there are signs of deterioration . 10

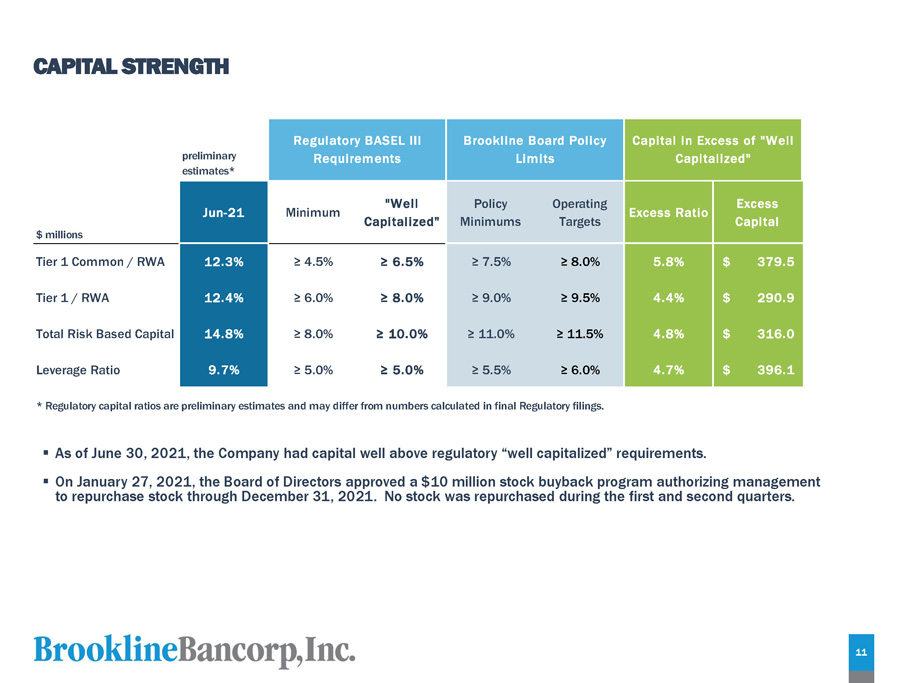

C A P I T A L S T RE N GTH 11 * Regulatory capital ratios are preliminary estimates and may differ from numbers calculated in final Regulatory filings. ▪ As of June 30, 2021, the Company had capital well above regulatory “well capitalized” requirements. ▪ On January 27, 2021, the Board of Directors approved a $10 million stock buyback program authorizing management to repurchase stock through December 31, 2021. No stock was repurchased during the first and second quarters. p r e limi na r y e s t im a t e s * Regulatory BASEL III Requirements Brookline Board Policy Limits Capital in Excess of "Well Capitalized" $ milli o n s Jun - 21 Minimum "Well C ap i t a li ze d " Policy M i n i m u m s Op e r a t i n g Targets Excess Ratio E x c e ss C ap i t al Tier 1 Common / RWA 12.3% ≥ 4.5% ≥ 6.5% ≥ 7.5% ≥ 8.0% 5.8% $ 379.5 Tier 1 / RWA 12.4% ≥ 6.0% ≥ 8.0% ≥ 9.0% ≥ 9.5% 4.4% $ 290.9 Total Risk Based Capital 14.8% ≥ 8.0% ≥ 10.0% ≥ 11.0% ≥ 11.5% 4.8% $ 316.0 Leverage Ratio 9.7% ≥ 5.0% ≥ 5.0% ≥ 5.5% ≥ 6.0% 4.7% $ 396.1

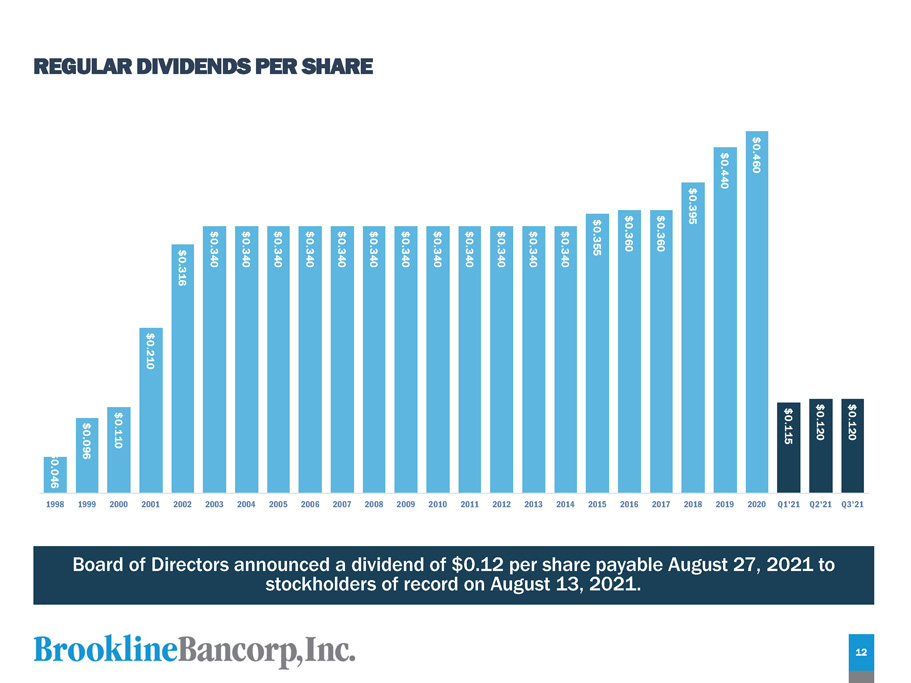

RE G U LA R D I V I D E N D S PE R SH A RE Board of Directors announced a dividend of $0.12 per share payable August 27, 2021 to stockholders of record on August 13, 2021. $0 . 0 4 6 12 $0 . 0 9 6 $0 . 1 1 0 $0 . 2 1 0 $0 . 3 1 6 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 4 0 $0 . 3 5 5 $0 . 3 6 0 $0 . 3 6 0 $0 . 3 9 5 $0 . 4 4 0 $0 . 4 6 0 $0 . 1 1 5 $0 . 1 2 0 $0 . 1 2 0 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Q1'21 Q2'21 Q3'21

QUESTIONS Paul A. Perrault, Chairman and Chief Executive Officer Carl M. Carlson, Chief Financial Officer M. Robert Rose, Chief Credit Officer 13 13

APPENDIX 13 14

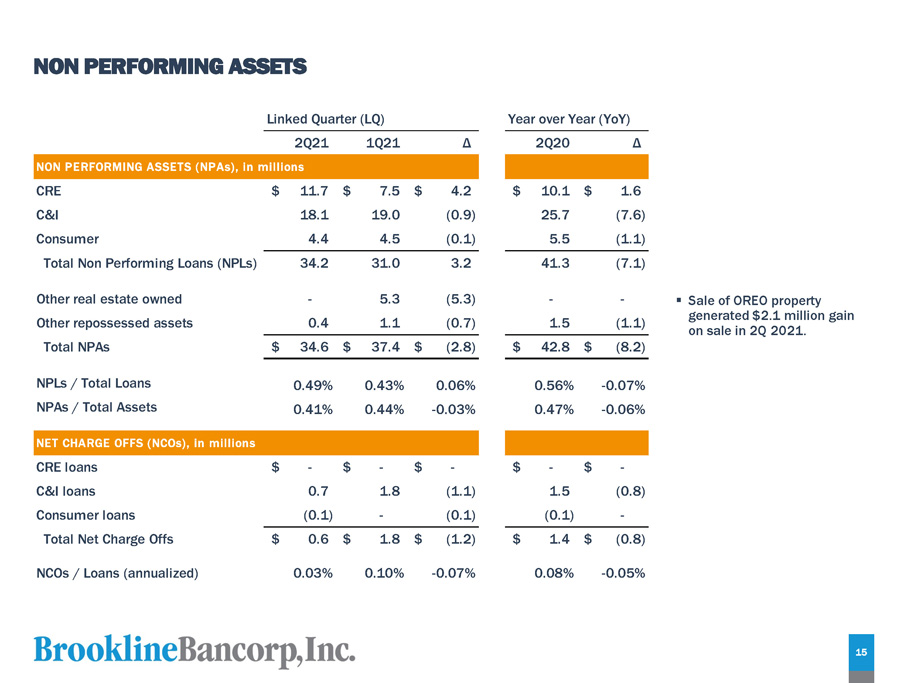

NO N PER F O R M IN G A SS E T S NON PERFORMING ASSETS (NPAs), in millions CRE $ 11.7 $ 7.5 $ 4.2 $ 10.1 $ 1.6 C&I 18.1 19.0 (0.9) 25.7 (7.6) Consumer 4.4 4.5 (0.1) 5.5 (1.1) Total Non Performing Loans (NPLs) 34.2 31.0 3.2 41.3 (7.1) Other real estate owned - 5.3 (5.3) - - ▪ Other repossessed assets 0.4 1.1 (0.7) 1.5 (1.1) Total NPAs $ 34.6 $ 37.4 $ (2.8) $ 42.8 $ (8.2) NPLs / Total Loans 0.49% 0.43% 0.06% 0.56% - 0.07% NPAs / Total Assets 0.41% 0.44% - 0.03% 0.47% - 0.06% NET CHARGE OFFS (NCOs), in millions CRE loans $ - $ - $ - $ - $ - C&I loans 0.7 1.8 (1.1) 1.5 (0.8) Consumer loans (0.1) - (0.1) (0.1) - Total Net Charge Offs $ 0.6 $ 1.8 $ (1.2) $ 1.4 $ (0.8) NCOs / Loans (annualized) 0.03% 0.10% - 0.07% 0.08% - 0.05% Linked Quarter (LQ) 2 Q 2 1 1 Q 21 Year over Year (YoY) Δ 2 Q 20 Δ Sale of OREO property generated $2.1 million gain on sale in 2Q 2021. 15

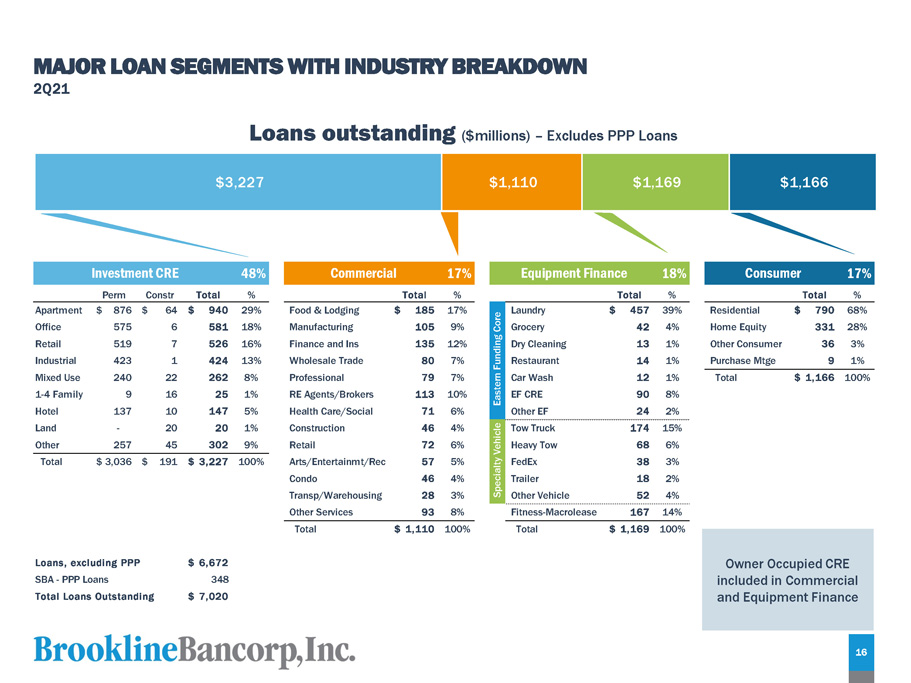

M A J O R L O A N S E G M E N T S WI T H I ND U S T R Y BRE A K D O W N 2Q21 $3,227 $1,110 $1,169 $1,166 Loans outstanding ($millions) – Excludes PPP Loans Investment CRE 48% Commercial 17% Equipment Finance 18% Consumer 17% P e r m Co n s t r T o t a l % T o t a l % T o t a l % T o t a l % Food & Lodging Manufacturing Finance and Ins W h o l e s a l e T ra d e Professional RE Agents/Brokers Health Care/Social Construction Retail Ar t s / E n t e r t a i n m t /R ec Condo Transp/Warehousing Other Services $ 18 5 17% 105 9% 135 12% 80 7% 79 7% 113 10% 71 6% 46 4% 72 6% 57 5% 46 4% 28 3% 93 8% Residential Home Equity Ot h er Co n s u m er Purchase Mtge $ 79 0 68% 331 28% 36 3% 9 1% Total $ 1,166 100% - Apar t m e n t Office Retail Industrial Mixed Use 1 - 4 F a m il y Hotel Land Ot h er 257 $ 87 6 $ 6 4 $ 94 0 29% 575 6 581 18% 519 7 526 16% 423 1 424 13% 240 22 262 8% 9 16 25 1% 137 10 147 5% 20 20 1% 45 302 9% Total $ 3,036 $ 191 $ 3,227 100% Fitness - Macrolease 16 7 14% Eastern Funding Core Laundry $ 457 39% Grocery 42 4% Dry Cleaning 13 1% Restaurant 14 1% Car Wash 12 1% EF CRE 90 8% Other EF 24 2% Specialty Vehicle Tow Truck 174 15% Heavy Tow 68 6% FedEx 38 3% Trailer 18 2% Other Vehicle 52 4% Total $ 1,110 100% Total $ 1,169 100% Loans, excluding PPP SBA - PPP Loans Total Loans Outstanding $ 6,672 348 $ 7,020 Owner Occupied CRE included in Commercial and Equipment Finance 16

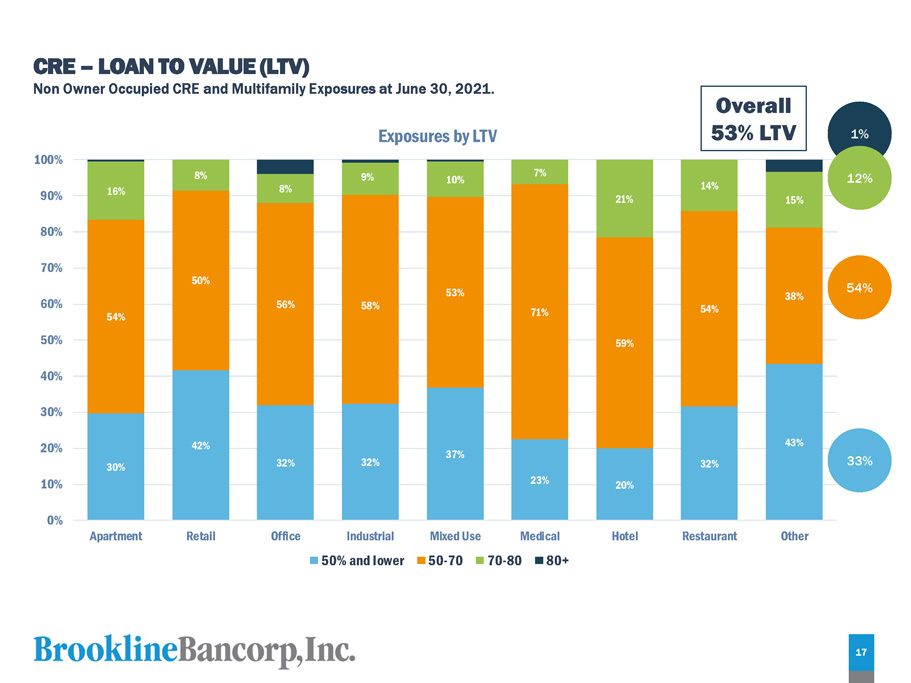

C R E – L O A N T O V A L U E ( L T V) Non Owner Occupied CRE and Multifamily Exposures at June 30, 2021. 30% 42% 32% 32% 37% 23% 20% 32% 43% 54% 50% 56% 58% 53% 7 1 % 59% 54% 38% 16% 8% 8% 9% 10% 7% 21% 14% 15% 0% 1 0 % 2 0 % 3 0 % 4 0 % 5 0 % 6 0 % 7 0 % 8 0 % 9 0 % 1 0 0% A p a rt m e nt R e t a i l O f f i c e Medical H o t e l R e s t au r a n t O t h e r Exposures by LTV Industrial 50% and lower M i x e d U s e 50 - 70 70 - 8 0 80+ 33% 54% 1% 12% 17 Overall 53% LTV

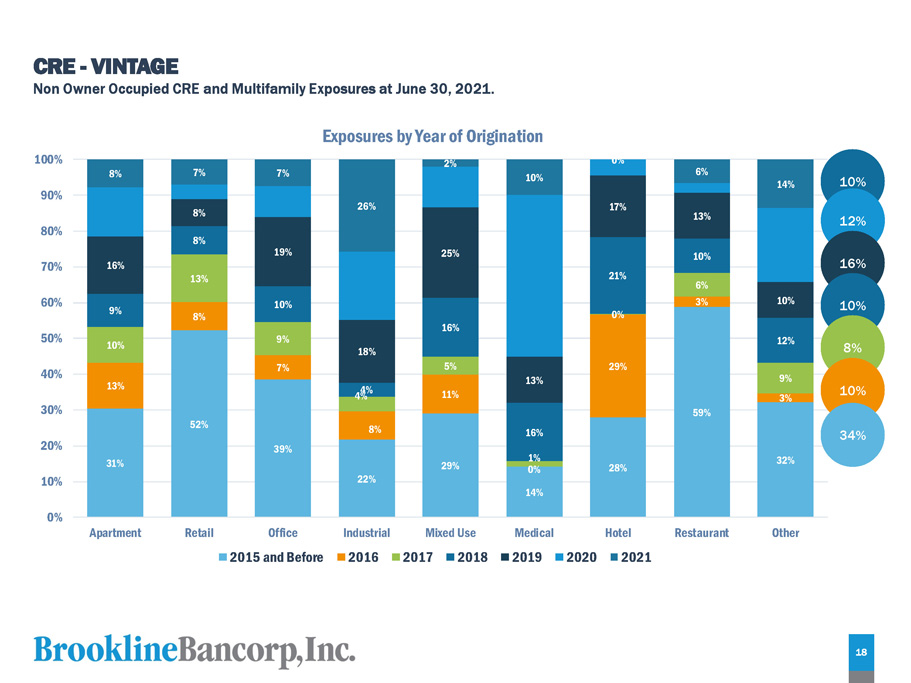

3 1 % 52% 39% 22% 29% 14% 28% 59% 32% 13% 8% 7% 8% 1 1 % 0% 29% 3% 10% 13% 9% 4% 5% 1% 0% 6% 9% 3% 9% 8% 10% 4% 16% 16% 2 1 % 10% 12% 16% 8% 19% 18% 25% 13% 1 7 % 13% 10% 8% 7% 7% 26% 2% 10% 0% 6% 14% 0% 1 0 % 2 0 % 3 0 % 4 0 % 5 0 % 6 0 % 7 0 % 8 0 % 9 0 % 1 0 0% Apartment R e t a i l Office 2015 and Before Restaurant O t h e r Exposures by Year of Origination Industrial Mixed Use Medical Hotel 201 6 201 7 201 8 201 9 202 0 2021 10 % C R E - V I N T A G E Non Owner Occupied CRE and Multifamily Exposures at June 30, 2021. 12 % 16 % 10 % 8 % 10 % 34 % 18

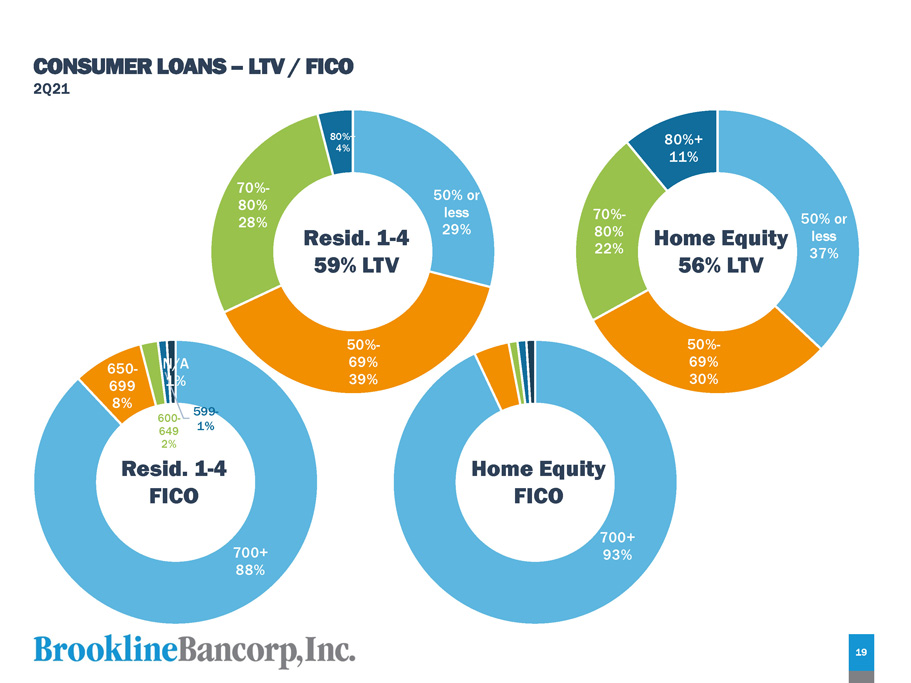

C ON S U M E R L O AN S – L T V / FIC O 2Q21 700+ 88% 19 650 - 699 8% 50% or less 29% 70 % - 80% 28% 80 %+ 4% 50% or less 37% 50% - 50% - N/A 69% 69% 1% 39% 30% 600 - 649 599 - 1% 2% 70 % - 80% 22% 80 % + 11% Resid. 1 - 4 59% LTV Resid. 1 - 4 FICO Home Equity FICO 700+ 93% Home Equity 56% LTV

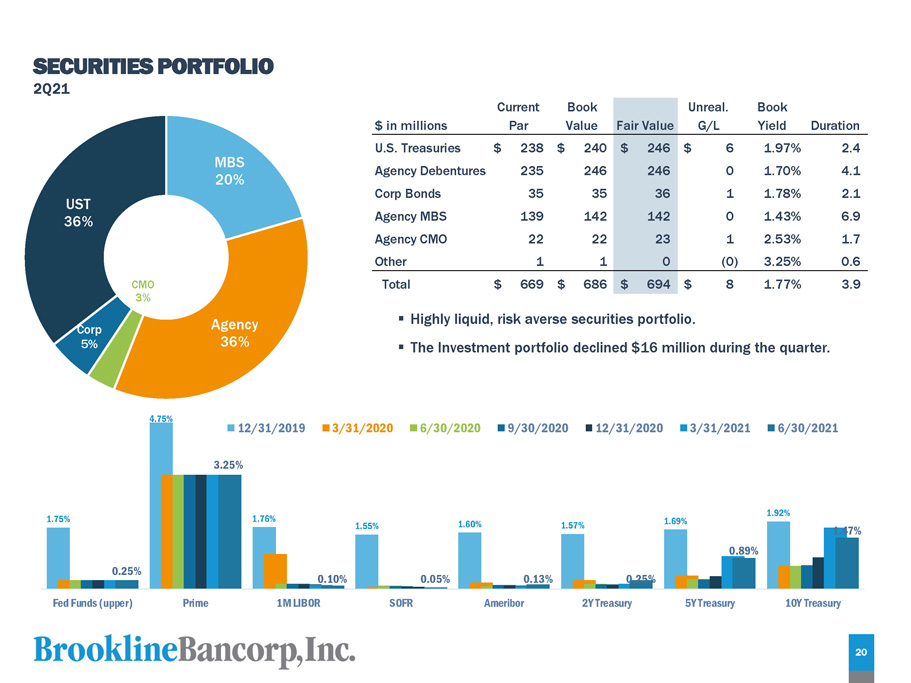

S E C UR I T I E S P O R T F OL I O 2Q21 ▪ Highly liquid, risk averse securities portfolio. ▪ The Investment portfolio declined $16 million during the quarter. 1.75 % 4.75 % 1.76 % 1.55 % 1.60 % 1.57 % 1.69 % 1.92 % 0 . 25 % 3 . 25 % 0 . 10 % 0 . 05 % 0 . 13 % 0 . 25 % 0 . 89 % 1 .4 7% F e d F u nd s ( up p e r ) P r i m e 1 M L I B OR S O F R Ameribor 2 Y T r e a s u r y 5 Y T r e a s u r y 10Y Treasury 12/31/2019 3/31/2020 6/30/2020 9/30/2020 12/31/2020 3/31/2021 6/30/2021 $ in millions Current Par Book Value Fair Value Unreal. G/L Book Yield Duration U.S. Treasuries $ 238 $ 240 $ 246 $ 6 1.97% 2.4 Agency Debentures 235 246 246 0 1.70% 4.1 Corp Bonds 35 35 36 1 1.78% 2.1 Agency MBS 139 142 142 0 1.43% 6.9 Agency CMO 22 22 23 1 2.53% 1.7 Other 1 1 0 (0) 3.25% 0.6 Total $ 669 $ 686 $ 694 $ 8 1.77% 3.9 M BS 20% 20 A g e n c y 36% C M O 3% C o r p 5% UST 36%

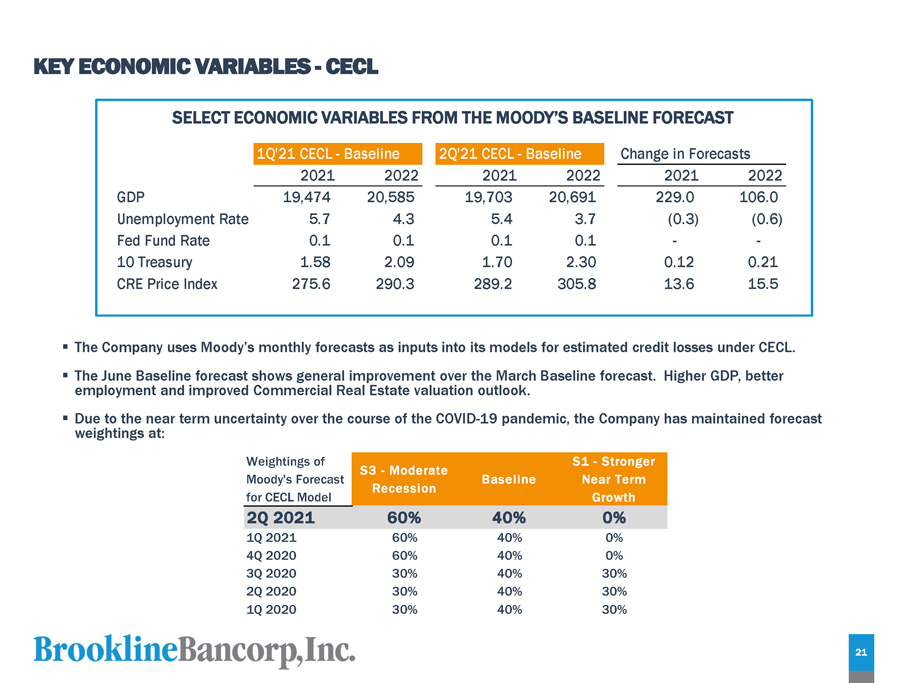

KE Y E C ONO MI C V A R I AB L E S - C E C L SE L ECT E C ONOMIC VARIABLES F 1 Q ' 2 1 C E C L - B a s e li n e ROM THE MOO 2 Q ' 2 1 C E C L - B D Y ’ S B A SE aseline LINE FORECAST Change in Forecasts 2021 2022 2021 2022 2021 2022 GDP 19,474 20,585 19,703 20,691 229.0 106.0 Unemployment Rate 5.7 4.3 5.4 3.7 (0.3) (0.6) Fed Fund Rate 0.1 0.1 0.1 0.1 - - 1 0 T r e a s ury 1.58 2.09 1.70 2.30 0.12 0.21 CRE Price Index 275.6 290.3 289.2 305.8 13.6 15.5 ▪ The Company uses Moody’s monthly forecasts as inputs into its models for estimated credit losses under CECL. ▪ The June Baseline forecast shows general improvement over the March Baseline forecast. Higher GDP, better employment and improved Commercial Real Estate valuation outlook. ▪ Due to the near term uncertainty over the course of the COVID - 19 pandemic, the Company has maintained forecast weightings at: 21 Weightings of Moody's Forecast for CECL Model S3 - Moderate Recession Baseline S1 - Stronger Near Term Growth 2Q 2021 60% 40% 0% 1Q 2021 60% 40% 0% 4Q 2020 60% 40% 0% 3Q 2020 30% 40% 30% 2Q 2020 30% 40% 30% 1Q 2020 30% 40% 30%