Table of Contents

As filed with Securities and Exchange Commission on June 24, 2011

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number: 001-14714

(Exact name of Registrant as specified in its charter)

Yanzhou Coal Mining Company Limited

(Translation of Registrant’s name into English)

People’s Republic of China

(Jurisdiction of incorporation or organization)

298 Fushan South Road

Zoucheng, Shandong Province

People’s Republic of China

(Address of principal executive offices)

Zhang Baocai

298 South Fushan Road

Zoucheng, Shandong Province

People’s Republic of China (273500)

Tel: (86)537 5382319

Fax: (86)537 5383311

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class |

Name of each exchange on which registered | |

| American Depositary Shares | New York Stock Exchange | |

| Class H Ordinary Shares | New York Stock Exchange* | |

| * | Not for trading in the United States, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

2,960,000,000 Domestic Shares, par value RMB1.00 per share

1,958,400,000 H Shares, par value RMB1.00 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this Chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files.) Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ¨ | International Financial Reporting Standards as issued by the International Accounting Standards Board x |

Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Table of Contents

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report includes statements of our expectations, intentions, plans and beliefs that constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and are intended to come within the safe harbor protection provided by those sections. The statements relate to future events or our financial performance, including, but not limited to, projections and estimates concerning the timing and success of specific projects and acquisitions. We use words such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “will” and the negatives of such terms or other similar expressions to identify forward-looking statements.

Without limiting the foregoing, all statements relating to our future operating results and anticipated capital expenditures, borrowings and sources of funding are forward-looking statements and speak only as of the date of this annual report. These statements are based on numerous assumptions that we believe are reasonable, but are subject to a wide range of risks, uncertainties and contingencies, which may cause actual results to differ materially from those discussed in these statements. Among the factors that could cause actual results to differ materially are:

| • | price volatility for our coal and other products; |

| • | demand for coal in the PRC and overseas markets; |

| • | difficulty in managing our rapid growth, business diversification, geographic expansion and integrating our acquisitions; |

| • | changes in legislation, regulations and policies; |

| • | the recovery of the methanol industry and methanol prices; |

| • | our ability to reduce costs and compete effectively; |

| • | our need for, and ability to obtain, capital to finance our future expansion plans and capital expenditures; |

| • | expected increases in production capacity and utilization of new facilities; |

| • | intensity of competition; |

| • | uncertainties in estimating our proven and probable coal reserves and our ability to replace and develop coal reserves; |

| • | effects of land reclamation and other liabilities; |

| • | geologic, equipment and operational risks related to mining; |

| • | changes in economic strength and political stability of countries in which we have operations or serve customers; |

| • | our ability to realize the anticipated benefits of our acquisition of equity interests or assets of coal mines; |

| • | obtaining governmental permits and approvals for our operations; |

| • | proximity of our coal resources to end-markets and cost of transportation; |

| • | availability, timing of delivery and cost of key supplies; |

| • | impacts of natural disasters, epidemics and safety accidents; and |

| • | other factors, including, but not limited to, those discussed in the section headed Risk Factors, set forth in Part D of Item 3 of this annual report. |

All of the forward-looking statements made in this annual report are qualified by this cautionary statement. We cannot assure you that the actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected effect on us, our business or our operations. We caution you not to place undue reliance on any such forward-looking statements. Unless we are required to do so under U.S. federal securities laws or other applicable laws, we do not intend to update or revise any forward-looking statements.

DEFINITIONS AND SUPPLEMENTAL INFORMATION

As used in this annual report, references to “Yanzhou Coal,” “we,” “our,” “our Company,” “the Group” or “us” refer to Yanzhou Coal Mining Company Limited and its subsidiaries, which have been consolidated into its accounts for the purpose of the consolidated financial statements, unless the context indicates otherwise. References to “the Company” refer to Yanzhou Coal as a stand-alone statutory entity.

“A Shares” refers to domestic shares in the ordinary share capital of the Company, with nominal value of RMB1.00 each, which are listed on the Shanghai Stock Exchange.

“Articles of Association” refers to our Articles of Association, as amended from time to time.

1

Table of Contents

“Austar Company” refers to Austar Coal Mine Pty Limited, a wholly owned subsidiary of Yancoal Australia Limited incorporated in Australia, which mainly engages in the mining, processing and sale of coal in Australia.

“CASs” refers to Accounting Standard for Business Enterprises (2006) and the relevant regulations and explanations issued by the Ministry of Finance of the PRC.

“CBRC” refers to China Banking Regulatory Committee.

“Directors” as used herein refer to our directors as discussed in Item 6 herein.

“Felix” refers to Felix Resources Limited, a wholly owned subsidiary of Yancoal Australia Limited incorporated in Australia, which mainly engages in the exploration, mining and sale of coal in Australia.

“Grant Thornton” refers to a registered firm of certified public accountants in the People’s Republic of China and is the principal auditor for the purpose of reporting to the United States Securities and Exchange Commission and other relevant U.S. regulatory bodies.

“Grant Thornton Hong Kong” refers to a firm of certified public accountants in Hong Kong Special Administrative Region which was a former member firm of Grant Thornton International Ltd and has since changed its name to JBPB & Co as of December 10, 2010. (original official name in Hong Kong: Grant Thornton)

“Grant Thornton Jingdu Tianhua” refers to a firm of certified public accountants in Hong Kong Special Administrative Region, which has been a member firm of Grant Thornton International Ltd since November 2010. This firm is the auditor for the purpose of the Hong Kong H Share listing only.

“H Shares” refers to overseas listed foreign invested shares in the ordinary share capital of the Company, with nominal value of RMB1.00 each, which are listed on the Hong Kong Stock Exchange.

“Haosheng Company” refers to Inner Mongolia Haosheng Coal Mining Company Limited, a 61% owned subsidiary of the Company, which engages in applying for project development and mining rights for Shilawusu Coal Field in the Inner Mongolia Autonomous Region.

“Heze Nenghua” refers to Yanmei Heze Nenghua Company Limited, a 98.33% owned subsidiary of the Company that manages our exploration for coal resources at the Juye Mine in Heze City, Shandong Province.

“Hong Kong Stock Exchange” refers to The Stock Exchange of Hong Kong Limited.

“Hua Ju Energy” refers to Shangdong Hua Ju Energy Co., Limited, a 95.14% owned subsidiary of the Company that engages in the generation of electric power from coal gangue and coal slurry, which are by-products of our coal mining process.

“IFRS” refers to International Financial Reporting Standards as issued by the International Accounting Standard Board.

“JBPB” refers to JBPB & Co., a firm of certified public accountants in Hong Kong Special Administrative Region formerly known as Grant Thornton in Hong Kong.

“NDRC” refers to the National Development and Reform Commission of the PRC.

“NYSE” refers to New York Stock Exchange.

“Ordos Neng Hua” refers to Yanzhou Coal Ordos Neng Hua Company Limited, a wholly owned subsidiary of the Company that mainly engages in the construction of a 600,000-tonne methanol project in Ordos City and the development of coal resources in the Inner Mongolia Autonomous Region.

“PBOC” refers to the People’s Bank of China.

“PRC” refers to the People’s Republic of China.

“Promoter Shares” refers to the domestic legal person shares held by Yankuang Group.

“Shanxi Nenghua” refers to Yanzhou Coal Shanxi Nenghua Company Limited, a wholly owned subsidiary of the Company that manages our investment projects in Shanxi Province.

“Shares” refers collectively to our (i) domestic invested shares listed on the Shanghai Stock Exchange, par value RMB1.00 each (the “Domestic Shares” or “A Shares”), (ii) foreign-invested shares issued and traded in HK dollars and listed on the Hong Kong Stock Exchange, par value RMB1.00 each (the “H Shares”) and (iii) American Depositary Shares (the “ADSs”), each of which represents ten H Shares.

“Tianhao Chemicals” refers to Shanxi Tianhao Chemicals Company Limited, a 99.89% owned subsidiary of Shanxi Nenghua that mainly engages in the operation of a 100,000 tonne methanol project in Shanxi Province.

2

Table of Contents

“Tianchi Energy” refers to Shanxi Heshun Tianchi Energy Company Limited, an 81.31% owned subsidiary of Shanxi Nenghua that mainly engages in the operation of Tianchi Coal Mine.

“Tonne” means metric tonne, which is equivalent to 1,000 kilograms or approximately 2,205 pounds.

“Twelfth Five-Year Plan” refers to the Twelfth Five-Year Plan (2011 to 2015) for National Economic and Social Development in the PRC.

“Yancoal Australia” refers to Yancoal Australia Limited, a wholly owned subsidiary of the Company that manages our investment projects in Australia.

“Yankuang Group” or “Controlling Shareholder” refers to Yankuang Group Corporation Limited (formerly known as Yanzhou Mining (Group) Corporation Limited).

“Yulin Nenghua” refers to Yanzhou Coal Yulin Nenghua Company Limited, a wholly owned subsidiary of the Company that mainly engages in the operation of a 600,000-tonne methanol project in Shaanxi Province.

“Yushuwan Coal Mine Company” refers to Shaanxi Yushuwan Coal Mine Company Limited, a joint venture among the Company, Chia Tai Energy & Chemicals Company Limited and Yushen Coal Company Limited, of which we will hold a 41% equity interest. As of the date of this annual report, the establishment of Yushuwan Coal Mine Company is still pending regulatory approval.

For purpose of this annual report, “Eastern China” refers collectively to Shandong Province, Jiangsu Province, Anhui Province, Zhejiang Province, Fujian Province, Jiangxi Province and Shanghai Municipality; “Southern China” refers to Guangdong Province and Hunan Province and Guangxi Autonomous Region; and “Northern China” refers to Beijing Municipality, Tianjin Municipality, Hebei Province, Shanxi Province and the Inner Mongolia Autonomous Region.

Certain mining terms used in this annual report are defined in the “Glossary of Mining Terms”, which was included as Appendix B to our registration statement on Form F-l that we filed with the U.S. Securities and Exchange Commission. A copy of the “Glossary of Mining Terms” may be obtained upon written request to the Company.

Unless otherwise specified, references in this annual report to “U.S. dollars”, “USD” or “US$” are to United States dollars, references to “HK dollars”, “HKD” or “HK$” are to Hong Kong dollars, references to “A$” are to Australian dollars and references to “RMB” are to Renminbi, the lawful currency of the PRC. Our financial statements are denominated in RMB and, except as otherwise stated, all monetary amounts in this annual report are presented in RMB.

Solely for your convenience, certain items in this annual report contain translations of Renminbi amounts into U.S. dollars, which have been made at the rate of RMB6.6000 to US$1.00, the certified exchange rate as set forth in the H.10 statistical release of the Federal Reserve Board for December 30, 2010. No representation is made that the Renminbi amounts could have been or could be converted into U.S. dollars at that rate, or at all.

In this annual report, where information has been presented in thousands or millions of units, amounts may have been rounded up or down. Accordingly, the amounts identified as total amounts in tables may not be equal to the apparent sum of the amounts listed therein.

PART I

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

3

Table of Contents

| ITEM 3. | KEY INFORMATION |

| A. | Selected Financial Data |

Historical Financial Data

The following table sets forth selected financial data as of and for the years ended December 31, 2006, 2007, 2008, 2009 and 2010. The selected income statement and cash flow data for the years ended December 31, 2008, 2009 and 2010 and the selected balance sheet data as of December 31, 2009 and 2010 have been derived from our audited consolidated financial statements included elsewhere in this annual report and should be read in conjunction with those financial statements and the accompanying notes. Unless otherwise indicated, the financial statements have been prepared and presented in accordance with IFRS, as issued by the International Accounting Standards Board. Our selected income statement and cash flow data for the years ended December 31, 2006 and 2007 and our selected balance sheet data as of December 31, 2006, 2007 and 2008 have been derived from our audited consolidated financial statements for those periods and dates, which are not included in this annual report.

| As of and for the Year Ended December 31, | ||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | 2010 | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | US$ | |||||||||||||||||||

| (in millions except per Share and per ADS data) | ||||||||||||||||||||||||

| INCOME STATEMENT DATA |

||||||||||||||||||||||||

| Total revenue(1) |

13,224.3 | 15,403.7 | 25,287.4 | 20,677.1 | 33,944.3 | 5,143.1 | ||||||||||||||||||

| Gross sales of coal |

13,058.8 | 15,193.0 | 24,933.3 | 19,947.8 | 32,590.9 | 4,938.0 | ||||||||||||||||||

| Railway transportation services income |

165.5 | 210.7 | 255.7 | 267.3 | 513.3 | 77.8 | ||||||||||||||||||

| Gross sales of electricity power |

— | — | 59.8 | 187.5 | 185.5 | 28.1 | ||||||||||||||||||

| Gross sales of methanol |

— | — | 38.6 | 258.9 | 629.3 | 95.3 | ||||||||||||||||||

| Gross sales of heat supply |

— | — | — | 15.6 | 25.2 | 3.8 | ||||||||||||||||||

| Transportation costs of coal |

(936.6 | ) | (549.8 | ) | (508.7 | ) | (403.3 | ) | (1,160.5 | ) | (175.8 | ) | ||||||||||||

| Cost of sales and service provided(1) |

(6,470.4 | ) | (7,625.2 | ) | (12,201.1 | ) | (10,590.0 | ) | (16,801.3 | ) | (2,545.7 | ) | ||||||||||||

| Cost of electricity power |

— | — | (88.3 | ) | (190.8 | ) | (195.5 | ) | (29.6 | ) | ||||||||||||||

| Cost of methanol |

— | — | (37.8 | ) | (352.9 | ) | (716.8 | ) | (108.6 | ) | ||||||||||||||

| Cost of heat supply |

— | — | — | (9.7 | ) | (12.5 | ) | (1.9 | ) | |||||||||||||||

| Gross profit |

5,817.3 | 7,228.7 | 12,451.5 | 9,130.4 | 15,057.6 | 2,281.5 | ||||||||||||||||||

| Selling, general and administrative expenses |

(2,230.1 | ) | (2,854.7 | ) | (3,832.0 | ) | (3,820.2 | ) | (5,093.9 | ) | (771.8 | ) | ||||||||||||

| Share of income (loss) of an associate |

— | (2.4 | ) | (67.4 | ) | 109.8 | 8.9 | 1.3 | ||||||||||||||||

| Other income |

165.8 | 198.9 | 351.5 | 311.0 | 3,108.1 | 470.9 | ||||||||||||||||||

| Interest expense |

(26.3 | ) | (27.2 | ) | (38.4 | ) | (45.1 | ) | (603.3 | ) | (91.4 | ) | ||||||||||||

| Profit before income taxes |

3,726.7 | 4,543.3 | 8,865.2 | 5,685.8 | 12,477.3 | 1,890.5 | ||||||||||||||||||

| Income taxes |

(1,354.7 | ) | (1,315.5 | ) | (2,385.6 | ) | (1,553.3 | ) | (3,171.0 | ) | (480.5 | ) | ||||||||||||

| Profit for the year |

2,372.0 | 3,227.8 | 6,479.6 | 4,132.5 | 9,306.3 | 1,410.0 | ||||||||||||||||||

| Profit attributable to our equity holders |

2,373.0 | 3,230.5 | 6,488.9 | 4,117.3 | 9,281.4 | 1,406.3 | ||||||||||||||||||

| Earnings per Share |

0.48 | 0.66 | 1.32 | 0.84 | 1.89 | 0.3 | ||||||||||||||||||

| Earnings per ADS |

4.82 | 6.56 | 13.19 | 8.37 | 18.87 | 2.9 | ||||||||||||||||||

| Operating income per Share before income tax |

0.76 | 0.92 | 1.80 | 1.16 | 2.54 | 0.4 | ||||||||||||||||||

| Profit from continuing operation per ADS before income tax |

7.58 | 9.24 | 18.02 | 11.56 | 25.37 | 3.8 | ||||||||||||||||||

| CASH FLOW DATA |

||||||||||||||||||||||||

| Net cash from operating activities |

3,767.2 | 4,558.6 | 7,095.5 | 6,520.1 | 5,399.8 | 818.2 | ||||||||||||||||||

| Net cash from (used in) investing activities |

(3,625.5 | ) | (3,790.9 | ) | (2,091.5 | ) | (24,842.9 | ) | (5,884.4 | ) | (891.6 | ) | ||||||||||||

| Net cash from (used in) financing activities |

(1,291.5 | ) | (1,018.7 | ) | (921.7 | ) | 18,503.7 | 1,360.5 | 206.1 | |||||||||||||||

| BALANCE SHEET DATA |

||||||||||||||||||||||||

| Total current assets |

9,871.9 | 9,908.2 | 14,994.4 | 20,000.9 | 24,281.4 | 3,679.0 | ||||||||||||||||||

| Total current liabilities |

3,828.0 | 4,099.5 | 5,297.0 | 10,410.4 | 10,133.9 | 1,535.4 | ||||||||||||||||||

| Net current assets |

6,043.9 | 5,808.7 | 9,697.4 | 9,590.5 | 14,147.5 | 2,143.6 | ||||||||||||||||||

| Property, plant and equipment |

12,139.9 | 13,524.6 | 14,149.4 | 18,877.1 | 19,874.6 | 3,011.3 | ||||||||||||||||||

| Total assets |

23,458.7 | 26,187.4 | 32,338.6 | 62,432.6 | 72,755.9 | 11,023.6 | ||||||||||||||||||

| Long-term bank borrowing |

330.0 | 258.0 | 176.0 | 20,911.7 | 22,400.8 | 3,394.1 | ||||||||||||||||||

| Equity attributable to our equity holders |

18,931.8 | 21,417.5 | 26,755.1 | 29,151.8 | 37,331.9 | 5,656.3 | ||||||||||||||||||

| DIVIDEND DECLARED PER SHARE |

||||||||||||||||||||||||

| A and H Shares |

0.22 | 0.20 | 0.17 | 0.40 | 0.59 | 0.09 | ||||||||||||||||||

| ADSs |

2.20 | 2.00 | 1.70 | 4.00 | 5.9 | 0.9 | ||||||||||||||||||

| (1) | In this annual report, business taxes and surcharges have been reclassified as corresponding costs of each category of revenue to provide a more appropriate presentation. The same adjustments have been made to the corresponding prior year. The reclassification has no impact on the overall results of the Group. The attention of Shareholders and potential investors is drawn to such adjustments. For details, please see Note 2 of the consolidated financial statements attached to this annual report. |

Number of Shares Outstanding

The following table sets forth the number of our A Shares, H Shares and ADSs outstanding as of the dates indicated.

| As of December 31, | ||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | ||||||||||||||||

| A Shares |

2,960,000,000 | 2,960,000,000 | 2,960,000,000 | 2,960,000,000 | 2,960,000,000 | |||||||||||||||

| H Shares |

1,958,400,000 | 1,958,400,000 | 1,958,400,000 | 1,958,400,000 | 1,958,400,000 | |||||||||||||||

|

ADSs |

5,461,179 | 3,338,368 | 18,919,105 | 19,403,533 | 19,744,158 | |||||||||||||||

4

Table of Contents

Exchange Rate Information

The following table sets forth information concerning exchange rates between the Renminbi and the U.S. dollar for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we use in this annual report or will use in the preparation of our periodic reports or any other information to be provided to you. The source of these rates is the Federal Reserve H.10 Statistical Release.

| Period |

Period End | Average(1) | High | Low | ||||||||||||

| (expressed in RMB per US$) | ||||||||||||||||

| 2005 |

8.0702 | 8.1826 | 8.2765 | 8.0702 | ||||||||||||

| 2006 |

7.8041 | 7.9579 | 8.0702 | 7.8041 | ||||||||||||

| 2007 |

7.2946 | 7.5806 | 7.8127 | 7.2946 | ||||||||||||

| 2008 |

6.8225 | 6.9193 | 7.2946 | 6.7800 | ||||||||||||

| 2009 |

6.8259 | 6.8295 | 6.8470 | 6.8176 | ||||||||||||

| 2010 |

6.6000 | 6.7603 | 6.8330 | 6.6000 | ||||||||||||

| October |

6.6707 | 6.6678 | 6.6912 | 6.6397 | ||||||||||||

| November |

6.6670 | 6.6538 | 6.6892 | 6.6330 | ||||||||||||

| December |

6.6000 | 6.6497 | 6.6745 | 6.6000 | ||||||||||||

| 2011 |

||||||||||||||||

| January |

6.6017 | 6.5964 | 6.6364 | 6.5809 | ||||||||||||

| February |

6.5713 | 6.5761 | 6.5965 | 6.5520 | ||||||||||||

| March |

6.5483 | 6.5645 | 6.5743 | 6.5483 | ||||||||||||

| April |

6.4900 | 6.5224 | 6.5477 | 6.4900 | ||||||||||||

| May |

6.4786 | 6.4957 | 6.5073 | 6.4786 | ||||||||||||

| June (through June 17, 2011) |

6.4700 | 6.4785 | 6.4830 | 6.4700 | ||||||||||||

| (1) | Determined by averaging the rates on the last business day of each month during the respective period, except for monthly averages, which are determined by averaging the rates on each business day of the month. |

On June 17, 2011, the noon buying rate was US$1.00 = RMB6.4700.

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Our business, financial condition and results of operations are subject to various changing business, competitive, economic, political and social conditions in China and worldwide. In addition to the factors discussed elsewhere in this annual report, the following are some of the important factors that could cause our actual results to differ materially from those projected in any forward-looking statements.

Our business and profitability are affected by global economic conditions.

The coal industry depends on general economic conditions, including the strength of global and local economies. In 2008 and 2009, the economies of the United States, Europe and certain countries in Asia experienced a severe and prolonged recession and China experienced a slowdown in overall economic growth, which led to a reduction in economic activity. In 2010, the average selling price of coal in the PRC experienced fluctuations due to global and local economic conditions. In spite of certain policies and initiatives implemented by the PRC government to alternately stimulate, and then moderate economic conditions, we cannot assure you that another recession would not occur or that a decline in overall economic conditions would not recur in the future. In the event of such a recession or decline in economic conditions, whether globally, locally in the PRC or in our major markets, our business and profitability may be adversely affected. We cannot assure you that the PRC government will not implement tightening policies to manage the growth of the economy or to control an overheated economy in the future, which may in turn affect coal prices. In the event that this occurs, our business and profitability may be materially and adversely affected.

5

Table of Contents

Our business and results of operations depend on the volatile domestic and international coal markets.

As we derive a substantial portion of our revenue from sales of coal, our business and operating results depend upon supply and demand for coal in the domestic and international coal markets. The prices of coal have been historically volatile and fluctuate in response to general economic conditions, supply and demand and the level of global inventories. From the fourth quarter of 2008 through early 2009, the demand for coal decreased significantly as a result of the global financial crisis. Since 2009, demand for coal in China and worldwide, along with coal prices, has substantially recovered. The average selling price of our coal products was RMB663.9, RMB529.2 and RMB663.5 per tonne in 2008, 2009 and 2010, respectively. However, we cannot assure you that demand for and prices of coal will not decline again, the occurrence of which may adversely affect our results of operations.

Global coal demand correlates strongly with the global economy and the performance of coal-consuming industries, including the power generation, chemical, metallurgy and construction materials industries. In addition, the availability and prices of alternative energy sources to coal, as well as international shipping costs, also affect coal demand. Coal supply, on the other hand, is primarily affected by the geographical location of coal reserves, transportation capacity, the level of domestic and international coal supplies and the type, quality and price of coal from other producers. Developments in the international coal market may adversely affect our overseas sales, which we expect to increase following the expansion of our Australian operations. A significant increase in global coal supply or reduction in demand for coal from key consuming industries may decrease coal prices, which in turn may reduce our profitability and adversely affect our business and results of operations.

Our business is dependent on short-term sales contracts and letters of intent.

In 2008, 2009 and 2010, the majority of our sales income (the invoiced amount of coal sold net of returns and discounts) of coal was derived from short-term sales contracts or letters of intent. These sales contracts and letters of intent generally specify the quantity and delivery schedule of purchases for a term generally not exceeding one year. If we experience a weak coal pricing environment that results in a decline in coal prices at the time of actual sale, our revenue and profitability would be reduced.

Historically, our customers have performed a significant majority of their purchase obligations under the sales contracts and letters of intent with us. However, a significant increase in the proportion of unperformed sales contracts and letters of intent or unrealized sales could have a material adverse impact on our results of operations if we are not able to locate alternative purchasers at the similar level of profitability. Furthermore, any changes in the cost or availability of labor, raw materials or transportation or volatility in foreign exchange rates during the period between the formation and performance of these sales contracts and letters of intent may adversely affect our ability to perform our contractual obligations or our profitability.

Our products may be subject to governmental price control measures, which may adversely affect our profitability.

Although the PRC government has implemented measures to overhaul historical price and supply controls and continues to support the development of a market-orientated PRC coal market, it may intervene in the domestic coal market from time to time through the use of macroeconomic measures to stabilize the market and achieve national social and economic goals. For example, the State Council of China and the NDRC published announcements in November and December 2010, respectively, imposing price caps on coal sold pursuant to key thermal coal supply agreements imposed with reference to the coal prices of the agreements entered into by the relevant enterprises in 2010. Such price caps were reemphasized by the NDRC in announcements issued in April 2011. These price-intervention measures may limit the degree of control we have over certain aspects of our business and may have a negative impact on our operations, pricing and profitability.

We rely on the PRC national railway system to deliver our products.

We rely on the PRC national railway system, as well as our railway network, to deliver coal to customers. We generated approximately 33.6%, 32.1% and 22.7% of our sales income (the invoiced amount of coal sold net of returns and discounts) of coal products sold and transported on the PRC state-owned railway system (exclusive of coal transported on our own railway network) in 2008, 2009 and 2010, respectively. Although the PRC government has taken steps to upgrade and expand the national railway system, its current capacity is not sufficient to meet the entire domestic coal transportation requirement. Even though our domestic customers are mainly located in Eastern China, where the railway system is relatively more developed than other regions of China, our ability to deliver coal is still restricted by the transportation capacity. In addition to railway transportation, we use major coal shipping ports along the coast of China to deliver coal to customers located along the coastal regions of China. However, we cannot assure you that we will be able to continue securing sufficient railway and port capacity to deliver our coal or that we will not experience any material delivery delays or substantial increases in transportation costs as a result of insufficient railway capacity. For details about our sales income of coal, please refer to “Item 5. Operating and Financial Review and Prospects — Coal Business”.

6

Table of Contents

The coal reserve data in this annual report are only estimates, which may differ materially from actual results.

Our coal reserve data are only estimates, which may differ materially from actual reserves. Our reserve estimates may change substantially if new information becomes available. There are inherent uncertainties in estimating reserves, which require the consideration of a number of factors, assumptions and variables, many of which may be beyond our control and cannot be ascertained despite due investigation. Our actual results of operations may differ materially from our long-term business and operational plans, which are based on our coal reserve estimates. We cannot assure you that we will not adjust our coal reserve estimates downward in the future, and in such event, our long-term production and the useful life of our mines may be materially and adversely affected.

Competition in the PRC and the international coal industry is intensifying, and we may not be able to maintain our competitiveness.

We face competition in all aspects of our business, including pricing, production capacity, coal quality and specifications, transportation capacity, cost structure and brand recognition. Our coal business competes in the domestic and international markets with other large domestic and international coal producers. Ongoing consolidation in the PRC coal industry has increased the level of competition in China. Our competitors may have higher production capacities, stronger brand names and more financial, marketing, distribution and other resources than we do.

We may not be able to maintain our competitiveness if changes or developments in the market weaken our existing competitive advantages. We cannot assure you that efforts taken by our competitors to improve the quality of their coal will not erode the quality advantage we have over them. Continual improvements in China’s transportation infrastructure, particularly the national railway transportation network, may diminish our proximity advantage of being located in Eastern China, the region with the highest coal demand in the PRC. Our principal competitors are located predominately in Shanxi Province, Shaanxi Province and the Inner Mongolia Autonomous Region, where there have been occasional rail capacity shortages and the costs of transporting coal to Eastern China are more significant. However, the PRC government has constructed and plans to continue constructing additional railways to transport coal from northern and northwestern China to Eastern China. The completion of these railway projects may increase the supply of coal to customers in Eastern China, increasing the effective supply of coal, which may have a material adverse impact on our results of operations.

Our results of operations depend on our ability to continue acquiring or developing suitable coal reserves.

The recoverable coal reserves in our existing mines decline as we produce coal. Due to the limitation on our ability to significantly increase our production capacity at existing mines, such as Jining II Coal Mine, Jining III Coal Mine and Tianchi Coal Mine, the increase in our coal production depends on the coal reserves we developed recently or will develop in the future, as well as our newly acquired coal resources.

We acquired the mining rights of Zhaolou Coal Mine through Heze Nenghua in May 2008, and commenced production at Zhaolou Coal Mine in December 2009. On December 23, 2009, we completed the acquisition of the entire equity interest in Felix, which had an equity interest in three operational mines and three exploratory mines. In December 2009, we established Ordos Neng Hua to manage our investments in the Inner Mongolia Autonomous Region, including a coal mining project. In 2010, Ordos Neng Hua acquired a 100% equity interest in a 600,000 tonnes methanol project. We acquired the entire assets of Anyuan Coal Mine in December 2010, which has commenced production in early 2011. We also obtained a 61% equity interest in Haosheng Company as of the date of this annual report. We are also in the process of establishing an associate company for a coal mining project in Yushuwan, Shaanxi Province. For more information about the development and acquisition of our coal resources, please refer to “Item 4. Information on the Company — History and Development of Our Company” in this annual report.

The acquisition of new mines by PRC coal companies, either within China or overseas, and the procurement of related licenses and permits are subject to PRC government approval. Delays in securing or failure to secure relevant PRC government approvals, licenses or permits, as well as any adverse change in government policies may hinder our expansion plans, which may materially and adversely affect our profitability and growth prospects. In connection with overseas acquisitions and expansion, we may encounter challenges due to our unfamiliarity with local laws and regulations, suffer foreign exchange losses on overseas investments or face political or regulatory obstacles to acquisitions. We cannot assure you that our overseas expansion plans and investments will be successful.

We cannot assure you that we will be able to continue to identify suitable acquisition targets or acquire these targets on competitive terms and in a timely manner. We may not be able to successfully develop new coal mines or expand our existing ones in accordance with our development plans, or at all. Failure to successfully acquire suitable targets on competitive terms, develop new coal mines or expand our existing coal mines could have an adverse effect on our competitiveness and growth prospects.

7

Table of Contents

Our operations may be affected by uncertain mining conditions.

Our operations are subject to certain risks inherent in underground mining, which may affect the safety of our workforce or cost of producing coal, including, without limitation, roof collapses, deterioration in the quality or variations in the thickness of coal seams, minewater discharge, explosions from methane gas or coal dust, ground falls and other mining hazards. Additionally, we are exposed to operational risks associated with industrial or engineering activities, such as maintenance problems or equipment failures. Although we conduct geological assessments on mining conditions and adapt our mining plans to the mining conditions at each mine, we cannot assure you that adverse mining conditions would not endanger our workforce, increase our production costs, reduce our coal output or temporarily suspend our operations. The occurrence of any of the foregoing events or conditions would have a material adverse impact on our business and results of operations.

We may suffer losses resulting from mining safety incidents.

Our coal mines and operating facilities may be damaged by water, gas, fire or cave-ins due to unstable geological structures. Like other coal mining companies, we have experienced accidents that have resulted in property damage and personal injuries. Although we have implemented safety measures at our mining sites, trained our employees on occupational safety and maintain liability insurance for personal injuries as well as limited property damage for certain of our operations, we cannot assure you that safety incidents will not occur. Any significant accident, business disruption or safety incident could result in substantial uninsured costs and the diversion of our resources, which could materially and adversely affect our business operations and financial condition.

We may be required to allocate additional funds for land subsidence.

Underground mining may cause the land above mining sites to subside. We may compensate inhabitants in areas surrounding our mining sites for their relocation expenses or for any property loss or damage as a result of our mining activities. PRC regulations require us to set aside provisions to cover the costs associated with land subsidence, restoration, rehabilitation and environmental protection. An estimated provision is deducted as an expense in our income statement based on the amount of coal actually extracted.

In 2010, approximately RMB693.7 million of our provisions for land subsidence, restoration, rehabilitation and environmental protection was expensed. The provision for land subsidence, restoration, rehabilitation and environmental costs is determined by our Directors based on estimations on various factors, including past occurrences of land subsidence. However, the provisions that we make are only estimates and may be adjusted to reflect the actual effects of our mining activities on the land above and surrounding our mining sites. Therefore, there can be no assurance that such estimates will be accurate or that our land subsidence, restoration, rehabilitation and environmental costs will not substantially increase in the future or that the PRC government will not impose new fees or change the basis of calculating compensation and reclamation costs in respect of land subsidence, the occurrence of any of which could increase our costs and have a material adverse effect on our results of operations.

PRC quotas for coal exports may adversely affect the level of our coal export sales.

Our export sales conducted from China (not including the sales by Yancoal Australia) accounted for approximately 0.9%, 0.3% and 0.03% of our sales income of coal in 2008, 2009 and 2010, respectively. The NDRC and the Ministry of Commerce set an annual export quota for domestic coal producers and allocate the quota among authorized coal exporters. Our export agents have historically received sufficient export quota to satisfy our export requirements. However, we are unable to predict what impact, if any, the national export quota may have on the level of our future export sales. If the national quota for coal exports is further reduced, our future export sales could be limited, which in turn could adversely affect our results of operations.

We do not have an export permit and cannot directly export our coal. All of our export sales must be made through intermediary export agents such as China National Coal Industry Import and Export Corporation, China National Minerals Import and Export Company Limited and Shanxi Coal Import and Export Group Company. The terms of our export sales are determined collectively by us, the export agents and our overseas customers. Although we have applied to the PRC central government for direct export rights with the assistance of the Shandong provincial government, we may not obtain such rights and may have to continue relying on export agents to export our coal from China.

8

Table of Contents

Our business operations may be adversely affected by present or future environmental regulations.

As a PRC coal producer, we are subject to extensive and increasingly stringent environmental protection laws and regulations. These laws and regulations:

| • | impose fees for the discharge of waste substances; |

| • | require provisions for land reclamation and rehabilitation; |

| • | impose fines and other penalties for serious environmental offenses; and |

| • | authorize the PRC government to close any facility that fails to comply with environmental regulations and suspend any coal operation that causes excessive environmental damage. |

Our coal mining operations produce waste water, gas emissions and solid waste materials. The PRC government has tightened its enforcement of applicable laws and regulations and adopted more stringent environmental standards. Similarly, our Australian operations are subject to Australia’s stringent environmental regulations. Our budgeted amount for environmental regulatory compliance may not be sufficient, and we may need to allocate additional funds for this purpose. If we fail to comply with current or future environmental laws and regulations, we may be required to pay penalties or fines or take corrective actions, any of which may have a material adverse effect on our business, results of operations and financial condition.

In March 2011, the NDRC promulgated the main targets of resources conservation and environment protection for 2011, which set the goals to decrease the amount of energy consumed per unit of GDP by 3.5% and to reduce the emission of certain major pollutants by 1.5% in 2011 compared with that in 2010. If efforts to increase energy efficiency, control greenhouse gas emissions and enhance environmental protection result in a decrease in coal consumption, our revenue may decrease and our business may be adversely affected.

We face pricing volatility and intense competition in our methanol operations.

We entered the PRC methanol market and commenced production of coal-based methanol at Tianhao Chemicals and Yulin Nenghua in September 2008 and August 2009, respectively. The methanol business is a cyclical and competitive commodity industry with dynamic supply and demand fundamentals. From 2006 to 2010, the domestic methanol industry suffered from significant overcapacity following a period of rapid expansion and increased investment, which were stimulated by speculation on the development of methanol downstream applications and the overheated coal chemical industry. Stagnation in market demand for methanol as a result of difficulty in promoting the utilization of methanol downstream products caused the over capacity issue to further deteriorate. We expect methanol prices in domestic market to remain sluggish due to the above mentioned conditions. In March 2011, the PRC benchmark methanol price increased to RMB2,670 per tonne from RMB2,590 per tonne in March 2010, representing a 3.1% increase.

We expect our methanol prices to be affected by a number of factors, including, without limitation:

| • | global and domestic methanol production; |

| • | global energy prices; |

| • | methanol plant utilization rates, capacity additions and shut downs; |

| • | global economic conditions; |

| • | our cost structure, product quality, availability of raw materials and utilization of our methanol plants; |

| • | compliance costs and environmental risks; and |

| • | foreign competition from low cost methanol producers which may have greater resources. |

As of the end of 2010, we had a total methanol production capacity of 700,000 tonnes. As with developing any new business, we may not optimize the utilization of our new facilities as planned. For example, Tianhao Chemicals has not been able to procure a steady supply of key raw material from its sole supplier of coke oven waste gas and has not been able to maintain steady operations as of the date of this annual report, which significantly curtailed its production in 2010.

If our projections for the domestic methanol market prove incorrect or if we are unable to otherwise compete effectively, we may not recover the capital and resources we have invested in our methanol operations and realize the intended benefits of our business expansion. In either event, our business and profitability will be adversely affected.

Our electric power business is heavily regulated, which may affect our results of operations.

We generated RMB185.5 million of revenue from electric power sales, which represented approximately 0.5% of our total revenue in 2010. The majority of electricity that we produced was for our internal use and we sold the remaining portion to external customers. To the extent that we do sell electricity, any decrease in the government-set grid power prices, the price at which power grid operators purchase electricity from power plants, including our power plants, may reduce our profitability and adversely affect our results of operations.

9

Table of Contents

The operation of coal-fired power plants is subject to increasingly stringent emission standards of the PRC government, in particular, the resources conservation and environmental protection standards for 2011 set forth by the NDRC, which stipulated the standards for air pollutant emissions for the power plants. As a result, our compliance costs will likely increase and the profitability of our electric power business may be reduced.

We are exposed to fluctuations in exchange rates and interest rates.

We mainly face risks relating to RMB fluctuations and risks stemming from exchange rate fluctuations between the Australian dollar and U.S. dollar. China has adopted a managed floating exchange rate system to allow the value of the Renminbi to fluctuate within a regulated band based on market supply and demand with reference to a basket of currencies. The primary effect of exchange rate fluctuations on us is due to our exports denominated in U.S. dollars and Australian dollars. As a result, exchange rate fluctuations can affect our export sales. In addition, exchange rate fluctuations can result in exchange losses on our foreign currency deposits and loans. As of December 31, 2010, the exchange rate for the Australian dollar against the U.S. dollar was 1.0163 (A$1.00 = US$1.0163), compared with A$1.00 = US$0.8985 as of December 31, 2009. Yancoal Australia recorded an exchange gain of RMB2,688.2 million during the reporting period. Exchange rate fluctuations can affect our cost of imported equipment and components.

To manage uncertainty in our revenue stream and capital expenditures caused by exchange rate fluctuations, we have entered into forward foreign exchange contracts to sell or purchase specified amounts of foreign currencies at stipulated exchange rates. We have also entered into interest rate swap contracts with banks to hedge a portion of our variable interest rate borrowings. As of December 31, 2010, the fair value of our derivative assets in respect of our foreign exchange contracts was RMB239.5 million, compared with the fair value of our derivative liabilities in respect of our forward contracts and interest rate swap contracts of approximately RMB166.2 million. See “Item 11. Quantitative and Qualitative Disclosures about Market Risks — Foreign Currency Exchange Rate Risk” for details on our hedging activities. We cannot assure you that our hedging arrangements will remain effective or that our results of operations will be not negatively affected by fluctuations in exchange rates or interest rates.

Our substantial indebtedness could adversely affect our business, financial condition and results of operations.

As of December 31, 2010, we had approximately RMB23,015.8 million in bank borrowings, of which approximately RMB614.9 million is due within a year, approximately RMB22,356.8 million is due after one year but within five years and approximately RMB44.0 million is due after more than five years. This level of debt could have significant consequences on our operations, including:

| • | reducing the availability of our cash flow to fund working capital, capital expenditures, acquisitions and other general corporate purposes as a result of our debt servicing obligations; |

| • | limiting our flexibility in planning for, or reacting to, and increasing our vulnerability to, changes in our business, our industry and the general economy; and |

| • | potentially limiting our ability to obtain or increasing the cost of any additional financing. |

In addition, Yancoal Australia obtained a syndicated loan amounting to approximately US$3,040.0 million attributable to the Felix acquisition in December 2009, which is guaranteed by us and secured by a counter guarantee from Yankuang Group. Failure by us to satisfy our repayment obligations could result in an event of a default that, if not cured or waived, could have a material adverse effect on us.

If we are not able to generate sufficient cash flow to service our debt obligations, we may need to refinance or restructure our debt, sell assets, reduce or delay capital investments, or seek to raise additional capital. If we are unable to implement one or more of these alternatives, our results of operations and financial condition may be materially and adversely affected.

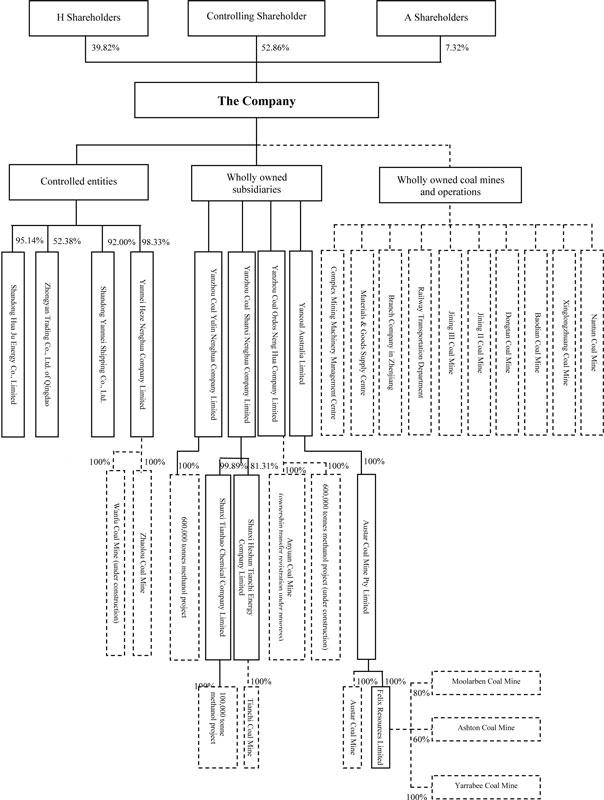

The operations of our Controlling Shareholder have a significant impact on us.

As of December 31, 2010, our Controlling Shareholder, the Yankuang Group, owned 52.86% of our outstanding shares and exerts significant influence over us. We may continue to enter into a number of connected transactions with the Yankuang Group. Pursuant to the regulations of the Hong Kong Stock Exchange and the Shanghai Stock Exchange on continuing connected transactions, we complete the necessary review and approval procedures before entering into continuing connected transactions. We have entered into five continuing connected transaction agreements with the Yankuang Group, namely the Materials Supply Agreement, Supply of Labor and Services Agreement, Pension Fund Management Agreement, Coal Products and Materials Supply Agreement and Electricity and Heat Energy Supply Agreement, each of which has a term from 2009 to 2011. In the fourth quarter of 2008, our shareholders approved the amendment and renewal of the five foregoing continuing connected agreements. On April 23, 2011, we also entered into the Finance Services Agreement with Yankuang Group Finance Company Limited, a joint venture established by the Yankuang Group, China Credit Trust Co., Ltd and us. Any material financial or operational developments experienced by the Yankuang Group that lead to the disruption of its operations or impairs its ability to perform its obligations under the agreements could materially affect our operations and future prospects.

As our Controlling Shareholder, the Yankuang Group has the ability to exercise control over the Company’s business and affairs, including, but not limited to, decisions with respect to:

| • | mergers or other business combinations; |

| • | the acquisition or disposition of assets; |

| • | the issuance of any additional shares or other equity securities; |

| • | the timing and amount of dividend payments; and |

| • | the management of our Company. |

10

Table of Contents

Our operations are affected by a number of risks relating to the PRC.

Because a significant majority of our assets and operations are located in China, we are subject to a number of risks relating to conducting business in China, including, but not limited to, the following:

| • | The central and local governments of the PRC have historically supported the development of the PRC coal industry and the continued operation of selected coal producers. A change in current policies that are favorable to us may adversely affect our ability to expand our business operations or increase our profitability. |

| • | Under current PRC regulatory requirements, we must obtain approval from relevant administrative authorities of the PRC government for any material capital expenditure project. Failure to obtain timely approvals for our projects may adversely affect our business plans and operating results. |

| • | China is still in the process of developing a comprehensive legal system. The enforcement of certain laws in China may still be subject to uncertainty. For instance, under current PRC tax laws, dividends payable to an non-PRC individual holders of shares outside the PRC are no longer exempted from PRC individual income tax and are subject to 20% individual income tax. However, this rate is still subject to adjustment in accordance with the applicable tax treaties or arrangement, pending on further confirmation from the relevant PRC authorities. Please refer to “Item 10. Additional Information — E. Taxation” for more details about this tax treatment. |

| • | The PRC government’s ongoing reform of the PRC economic system may increase the uncertainties in our business as a number of reforms are unprecedented or experimental and may be subject to refinement and adjustments. We may be directly affected by these reforms or indirectly affected by changes in political, economic and social factors that result from these reform measures. Our operating results may be adversely affected by changes in economic and social conditions in China and changes in the PRC government policies related, but not limited, to inflation control, economic stimulus policies, tax policies and rates, currency conversion restrictions and tariffs and other import restrictions. |

Our coal operations are extensively regulated by the PRC and Australian government and government regulations may limit our activities and adversely affect our business operations.

Our coal operations in China are subject to extensive regulation by the PRC government. National governmental authorities, such as the NDRC, the Ministry of Environmental Protection, the Ministry of Land and Resources, the State Administration of Coal Mine Safety and the State Bureau of Taxation, as well as corresponding provincial and local authorities and agencies, exercise extensive control over the mining and transportation (including rail and sea transport) of coal within China.

Our operations in Australia are subject to similar laws and regulations of general application governing mining and processing, land tenure and use, environmental requirements, including site specific environmental licenses, permits and statutory authorizations, workplace health and safety, trade and export, competition, access to infrastructure, foreign investment and taxation. These regulations may be implemented by various federal and state government departments and authorities including the Department of Resources, Energy and Tourism, the Department of Environment, Water, Heritage and the Arts and the National Native Title Tribunal.

Regulatory oversight from these authorities and agencies may affect the following, among others, aspects of our operations:

| • | the use and grant of mining rights; |

| • | rehabilitation of mining sites and surrounding areas; |

| • | mining recovery rates; |

| • | pricing of our transportation services for coal in China; |

| • | taxes, levies and fees on our business; |

| • | application of capital investments; |

| • | export quotas and procedures; |

| • | pension fund contributions; |

| • | preferential tax treatment; and |

| • | environmental and safety standards. |

As a result of the foregoing regulation, our ability to execute our business strategies or to carry out or expand our business operations may be restricted. We may experience substantial delays in obtaining regulatory approvals, permits and licenses for our business operations. Our business may also be adversely affected by future changes in PRC or Australian regulations and policies that affect the coal industry. The adoption of new legislation or regulations, or the new interpretation of existing legislation or regulations, may materially and adversely affect our operations, our cost structure or product demand. The occurrence of any of the foregoing may cause us to substantially change our existing operations or incur significant compliance costs. For example, the Australia federal government announced proposals to implement a 40% Resource Super Profits Tax generated from non-renewable resources by mining companies, which is currently scheduled to come into effect on July 1, 2012. The tax payable of coal producers will increase substantially should this tax proposal become effective. The newly elected prime minister of Australia, Julia Gillard, later announced certain modifications to the Resource Super Profits Tax proposal, including, without limitation, reducing the number of affected companies, decreasing the applicable tax rate and increasing the range of tax credit available to mining companies. Notwithstanding the substantial modifications, the new tax proposal will still increase the taxation obligation of coal producers. In addition, we are subject to various uncertainties in relation to the foregoing tax proposal which has not yet been approved by the Australian government, including, without limitation, the final arrangement and the time of implementation. We expect the implementation of the foregoing tax proposal will have a material adverse effect to the profitability of our operations in Australia.

11

Table of Contents

| ITEM 4. | INFORMATION ON THE COMPANY |

| A. | History and Development of our Company |

Yanzhou Coal Mining Company Limited was established on September 25, 1997 as a joint stock company with limited liability under the Company Law of the PRC (the “Company Law”). The predecessor of our Company, Yanzhou Mining Bureau, was established in 1976. With the approval of the former State Economic and Trade Commission and the former Ministry of Coal Industry in 1996, the predecessor was incorporated under the name Yanzhou Mining (Group) Corporation Limited and subsequently renamed Yankuang Group Corporation Limited after undergoing a reorganization in 1999.

In 1999, the Minister of Foreign Trade and Economic Cooperation, the predecessor of the Ministry of Commerce, approved our conversion into a Sino-foreign joint stock company with limited liability under the Company Law and the Sino-Foreign Joint Venture Law of the PRC.

| Our contact information is: | ||||

| • Business address |

: | 298 South Fushan Road | ||

| Zoucheng, Shandong Province | ||||

| People’s Republic of China (273500) | ||||

| • Telephone number |

: | (86) 537 538 2319 | ||

| • Website |

: | http://www.yanzhoucoal.com.cn | ||

Establishment of Ordos Neng Hua and Acquisition of Coal Chemical Project

We established Ordos Neng Hua in the Inner Mongolia Autonomous Region in December, 2009. Ordos Neng Hua will act as our investment management platform for coal mining, coal chemicals and a coal power project in Inner Mongolia. As of the date of this annual report, the registered capital of Ordos Neng Hua was RMB3.1 billion.

Subsequently, the Company and Ordos Neng Hua successively completed the following related acquisitions: acquisition of 100% of the equity interests in a 600,000-tonne methanol project, the acquisition of a 61% equity interest in Haosheng Company, the acquisition of the entire assets of Anyuan Coal Mine and obtaining the mining rights of Zhuan Longwan coal mine field through public bidding. These acquisitions should assist us in acquiring coal resources in Ordos City, further participating in coal resources development in the Inner Mongolia Autonomous Region and enhancing the sustainable development ability and core competitiveness of the Company.

12

Table of Contents

Acquisition of 100% equity interest in the 600,000-tonne methanol project

Pursuant to approval granted at the general manager working meeting held on December 1, 2009, Ordos Neng Hua acquired 100% of the equity interests held by Kingboard Chemical Holdings Limited in Inner Mongolia Rongxin Chemicals Co., Ltd, Inner Mongolia Daxin Industrial Gas Co., Ltd and Inner Mongolia Yize Mining Investment Co., Ltd, for a consideration of RMB190 million out of its own resources. The relevant procedures for the share ownership transfer procedures were completed on April 16, 2010. The above companies are responsible for the establishment of the first phase of the 600,000-tonne methanol project.

Acquisition of Inner Mongolia Haosheng Coal Mining Company Limited

Currently, Haosheng Company is primarily responsible for the approval application for the mining project and the grant of the mining rights of Shilawusu Coal Mine field Project in the Inner Mongolia Dongsheng Coal Field.

Pursuant to approval granted at the fifteenth meeting of the fourth session of the Board held on August 20, 2010, we entered into the equity transfer agreement of Haosheng Company and its supplementary agreement on September 6, 2010 and October 19, 2010, respectively. Under such agreements, we acquired 51% of equity interests in Haosheng Company originally held by Shanghai Huayi (Group) Company (“Huayi”), Ordos Jinchengtai Chemical Co., Ltd (“Jinchengtai”) and Shandong Jiutai Chemical Industrial Technology Company Limited (“Jiutai Technology”) in Haosheng Company for a consideration of approximately RMB6,649 million. The Company and other shareholders of Haosheng Company are obligated to inject further capital on a pro-rata basis in order to increase the registered capital from RMB50 million to RMB150 million.

The initial payment of the consideration and capital increase in Haosheng Company in a total amount of approximately RMB2,045.8 million was paid by us on October 20, 2010 and the share ownership transfer procedures were completed on November 4, 2010. We are obligated to pay a second installment of approximately RMB2,659.6 million within 15 working days when any of the following requirements has been met: (i) Haosheng Company obtains the exploration rights license of Shilawusu Coal Mine field; (ii) the mining zone delineation of Shilawsu Coal Mine Zone or other applications related to mining rights have been approved by the Ministry of Land and Resources (the main body to have obtained the mining zone delineation or other mining rights must be Haosheng Company). The third installment of approximately RMB1,994.7 million shall be paid within 10 months after completion of the second payment.

As of March 31, 2011, we entered into an equity transfer agreement of Haosheng Company with Ordos City Jiutaimanlai Coal Mining Company Limited (“Jiutaimanlai”) and Jiutai Technology to acquire 10% of the equity interests in Haosheng Company held by Jiutaimanlai and Jiutai Technology for a consideration of approximately RMB1,313.8 million. We paid the initial payment of approximately RMB394.1 million (representing 30% of the total amount) on April 7, 2011. Currently, we are processing the share ownership transfer procedures. Upon completion of the transfer, we will hold 61% of the equity interests in Haosheng Company. We are obligated to pay the second and third installments upon the same conditions as the payment arrangements in our acquisition of 51% of the equity interests.

Acquisition of Anyuan Coal Mine

Pursuant to approval granted at the general manager working meeting held on November 12, 2010, Ordos Neng Hua entered into Anyuan Coal Mine Transfer Agreement and its supplementary agreement on November 20, 2010 and January 20, 2011, respectively, to acquire the total assets of Anyuan Coal Mine for a consideration of approximately RMB1,435 million. Pursuant to the transfer agreement, Ordos Neng Hua acquired the Anyuan Coal Mine on December 1, 2010, but still subject to relevant governmental approval. Since December 1, 2010, Ordos Neng Hua owns all the coal produced and earnings derived from Anyuan Coal Mine. As of the date of this annual report, approximately RMB1,290 million has been paid by Ordos Neng Hua, and the balance of the consideration is expected to be paid in July 2011.

Anyuan Coal Mine, located in Ejin Horo Banner of Ordos City, is an underground coal mine. Anyuan Coal Mine covers an area of 9.26 km2 and with coal reserves of 40.51 million tonnes and recoverable coal reserves of 20.47 million tonnes. Its designed annual production capacity is 600,000 tonnes of raw coal. The Department of Coal Industry of Inner Mongolia Autonomous Region has approved the increase in annual production capacity of the mine to 1.2 million tonnes. Currently, its expansion and acceptance inspection procedures are in progress.

13

Table of Contents

Bidding for Mining Rights of Zhuan Longwan Coal Mine Field

Pursuant to approval granted at the nineteenth meeting of the fourth session of the Board held on January 28, 2011, Ordos Neng Hua successfully bid for the mining rights of Zhuan Longwan coal mine field of Dongsheng Coal Field in Inner Mongolia Autonomous Region for a consideration of RMB7,800 million. Ordos Neng Hua paid the first installment of RMB3,120 million (representing 40% of the total consideration) on February 25, 2011. Ordos Neng Hua is obligated to pay the second installment of RMB2,340 million (representing 30% of the total consideration) in full by November 30, 2011 and the third installment of RMB2,340 million (representing 30% of the total consideration) in full by November 30, 2012.

Pursuant to the Announcement in relation to Public Auction of the Mining Rights of Zhuan Longwan Coal Mine Field of Dongsheng Coal Field issued by the Department of Land and Resources of the Inner Mongolia Autonomous Region, the coal mining field of Zhuan Longwan coal mine covers an area of 43.50 km2 and with reserves of 548 million tonnes. Extra large mines with a designed production capacity of 5 million tonnes per year can be constructed in the coal mine field.

The Department of Land and Resources of the Inner Mongolia Autonomous Region was entrusted by the Ministry of Land and Resources of the PRC to conduct the auction. At present, Ordos Neng Hua is undertaking the application procedure for the mining rights of Zhuan Longwan coal mine zone. The bidding was approved at the 2010 annual general meeting of the Company held on May 20, 2011.

Acquisition of Ashton Coal Mine Joint Venture in Australia

Pursuant to approval granted at the seventeenth meeting of the fourth session of the Board held on December 30, 2010, White Mining (NSW) Pty Limited, a wholly-owned subsidiary of Yancoal Australia, started the process of acquiring 30% of the equity interests in the Ashton Coal Mine Joint Venture originally held by Austral-Asia Coal Holdings Pty Ltd, a wholly-owned subsidiary of Singapore IMC Group, for a consideration of US$250 million. Upon the completion of this acquisition in May 2011, our ownership in the Ashton Coal Mine Joint Venture increased from 60% to 90%.

Ashton Coal Mine, located in Hunter Valley, New South Wales, Australia, consists of an open-cut coal mine and an underground coal mine, with annual designed production capacity of 5.20 million tonnes of raw coal. According to an assessment based on the Australian JORC Code, the aggregate coal reserves of Ashton Coal Mine amounted to 96.50 million tonnes. The types of coal are semi-soft coking coal and premium thermal coal with characteristics of low ash and high calorific value.

Disposal of equity interests in Minerva Coal Mine Joint Venture in Australia

Pursuant to approval granted at the seventeenth meeting of the fourth session of the Board held on December 30, 2010, Felix, a wholly-owned subsidiary of Yancoal Australia, disposed its 51% equity interests in the Minerva Coal Mine Joint Venture to Sojitz Coal Resources Pty Ltd, a wholly-owned subsidiary of Sojitz Corporation in Australia, for a consideration of A$201 million. Upon completion of the disposal, we have no interest in the Minerva Mine Coal Joint Venture.

Minerva Coal Mine, located in Bowen Basin, Queensland, is an open-cut coal mine, with annual production capacity of 2.80 million tonnes of raw coal. According to an assessment based on the Australia JORC Code, the aggregate coal resources of Minerva Coal Mine amounted to 76 million tones, with reserves of 23.6 million tonnes. The type of coal is thermal coal.

Establishment of Yankuang Group Finance Company Limited

Pursuant to approval granted at the thirteenth meeting of the third session of the Board held on August 3, 2007, we established a joint venture company, Yankuang Group Finance Company Limited (“Yankuang Finance”) on September 13, 2010, jointly with Yankuang Group and China Credit Trust Co., Ltd. The registered capital of Yankuang Finance is RMB500.0 million, of which we have contributed cash of RMB125.0 million representing 25% of the equity interest. Yankuang Finance commenced operation on November 1, 2010, with its principal business including making the bill acceptance and discount for the members and accepting deposits from and lending funds to members.

At the fourteenth meeting of the fourth session of the Board held on April 23, 2010, we entered into the Financial Services Agreement with Yankuang Finance on January 7, 2011. Under the financial service agreement, Yankuang Finance agreed to provide deposit service, loan service and miscellaneous financial services to us with transaction caps for 2010 and 2011. Pursuant to the agreement, the fees charged by Yankuang Finance for the financial services to be provided to us shall be in accordance with the relevant benchmark rates determined by the PBOC or the CBRC (if any), which shall not exceed those charged by the major commercial banks in the PRC for the same kind of financial services provided to us. The agreement also provided risk control measures on funds for both parties to secure the safety of funds.

14

Table of Contents

Establishment of Shaanxi Future Energy Chemical Corp. Ltd

Pursuant to approval granted at the seventeenth meeting of the fourth session of the Board held on December 30, 2010, we established Shaanxi Future Energy Chemical Corp. Ltd (“Future Energy”) jointly with Yankuang Group and Shaanxi Yanchang Petroleum (Group) Corp. Ltd on February 25, 2011. The registered capital of Future Energy is RMB5,400 million, of which we will contribute RMB1,350 million in cash, representing an equity interest of 25%. The registered capital will be paid in full in three installments by August 2012. Future Energy will mainly engage in investment and participation in the coal liquefaction project in Shaanxi Province as well as the preparation for development of ancillary coal mines.

Increasing Investments in Ordos Neng Hua

Pursuant to approval granted at the eighteenth meeting of the fourth session of the Board held on January 17, 2011, we increased our capital investment in Ordos Neng Hua by RMB2,600 million with our own funds. On January 24, 2011, the registered capital of Ordos Neng Hua increased from RMB500 million to RMB3,100 million.

Increasing Investments in Yancoal Australia

Pursuant to approval granted at the seventeenth meeting of the fourth session of the Board held on December 30, 2010, we increased the capital investment in Yancoal Australia by A$909 million (approximately RMB5,900 million) with our own funds. Upon completion of the capital injection, our capital investment in Yancoal Australia increased from A$64 million to A$973 million. The capital increase has been approved by the Foreign Investment Review Board of Australia and the NDRC and the procedures for remitting the capital increase are currently in progress.

Capital Expenditures

Our principal source of cash in 2010 was cash generated from our operating activities and bank borrowings. Our capital expenditures in 2010 were primarily for operational capital expenditures, purchase of properties, machinery and equipment, payment of dividends, the acquisition of 51% equity interests in Haosheng Company, the acquisition of Anyuan Coal Mine and investment in Yankuang Finance.

The following table sets forth a summary of our capital expenditures in the periods indicated:

| Year Ended December 31, | ||||||||||||||||

| 2008 | 2009 | 2010 | 2010 | |||||||||||||

| RMB | RMB | RMB | US$ | |||||||||||||

| (in millions) | ||||||||||||||||

| Coal mining |

1,925.3 | 24,086.5 | 3,298.0 | 486.5 | ||||||||||||

| Coal railway transportation |

29.2 | 11.4 | 34.5 | 5.1 | ||||||||||||

| Electricity power and methanol |

925.1 | 1,220.0 | 452.8 | 66.8 | ||||||||||||

| Undistributed items |

— | — | — | — | ||||||||||||

| Corporate |

2.1 | 7.0 | — | — | ||||||||||||

| Total |

2,881.7 | 25,324.9 | 3,785.3 | 558.4 | ||||||||||||

Our planned capital expenditures for 2011 is approximately RMB5,103.1 million. For more information, see “Item 5. Operating and Financial Review and Prospects — B. Liquidity and Capital Resources — Capital Expenditures” in this annual report.

Potential Takeovers by Third Parties

There were no indications of any public takeover offers by third parties in respect of our common shares in 2010.

15

Table of Contents

| B. | Business Overview |

The Company is one of the primary coal producers in China with rapidly growing coal mining operations in Australia. We primarily engage in the mining, preparation and sale of coal as well as the railway transportation of coal. In recent years, we have expanded our operations to include the production of coal chemicals and generation of electricity and heat.

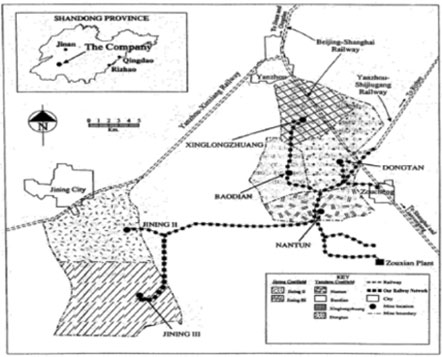

The Company directly owns and operates six coal mines: Nantun, Xinglongzhuang, Baodian, Dongtan, Jining II and Jining III (collectively, the “Six Coal Mines”), which produce a substantial majority of our total coal output. As of December 31, 2010, the Six Coal Mines had an estimated collective in-place proven and probable reserve base of approximately 1,797.3 million tonnes.