UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________

FORM 10-K

______________________________

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED December 31, 2019

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File No. 000-24575

_____________________________

STABILIS ENERGY, INC.

(Exact name of registrant as specified in its charter)

_____________________________

Florida | 59-3410234 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

10375 Richmond Avenue, Suite 700, Houston, TX 77042

(Address of principal executive offices, including zip code)

(832) 456-6500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading symbol | Name of each exchange on which registered |

Common Stock, $.001 par value per share | SLNG | The OTCQX Best Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (S. 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

Non-accelerated filer | ☐ | Smaller reporting company | ☒ | |||

Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $4,427,550 based on the closing sale price on June 30, 2019 as reported by the NASDAQ Stock Market.

As of February 29, 2020, there were 16,835,318 outstanding shares of our common stock, par value $.001 per share.

STABILIS ENERGY, INC. AND SUBSIDIARIES

ANNUAL REPORT ON FORM 10-K

For the Fiscal Year Ended December 31, 2019

TABLE OF CONTENTS

Page | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | Mine Safety Disclosures | |

Item 5. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

Item 16. | ||

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This document includes statements that constitute forward-looking statements within the meaning of the federal securities laws. These statements are subject to risks and uncertainties. These statements may relate to, but are not limited to, information or assumptions about us, our capital and other expenditures, dividends, financing plans, capital structure, cash flow, our recent business combination, pending legal and regulatory proceedings and claims, including environmental matters, future economic performance, operating income, cost savings, and management’s plans, strategies, goals and objectives for future operations and growth. These forward-looking statements generally are accompanied by words such as “intend,” “anticipate,” “believe,” “estimate,” “expect,” “should,” “seek,” “project,” “plan” or similar expressions. Any statement that is not a historical fact is a forward-looking statement. It should be understood that these forward-looking statements are necessarily estimates reflecting the best judgment of senior management, not guarantees of future performance. They are subject to a number of assumptions, risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements. When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements described in Part I. “Item 1A. Risk Factors” in this document.

Forward-looking statements represent intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors. Many of those factors are outside of our control and could cause actual results to differ materially from the results expressed or implied by those forward-looking statements. In addition to the risk factors and other cautionary statements described in Part I. “Item 1A. Risk Factors” in this document, the factors include:

• | our ability to execute our business strategy; |

• | our limited operating history; |

• | our ability to obtain additional financing to effect our strategy; |

• | loss of one or more of our customers; |

• | cyclical or other changes in the demand for and price of LNG and natural gas; |

• | operational, regulatory, environmental, political, legal and economic risks pertaining to the construction and operation of our facilities; |

• | the effects of current and future worldwide economic conditions and demand for oil and natural gas and power system equipment and services; |

• | hurricanes or other natural or man-made disasters; |

• | public health crises, such as the coronavirus outbreak beginning in early 2020, which could impact economic conditions; |

• | dependence on contractors for successful completions of our energy related infrastructure; |

• | reliance on third party engineers; |

• | competition from third parties in our business; |

• | failure of LNG to be a competitive source of energy in the markets in which we operate, and seek to operate; |

• | increased labor costs, and the unavailability of skilled workers or our failure to attract and retain qualified personnel; |

• | major health and safety incidents relating to our business; |

• | failure to obtain and maintain approvals and permits from governmental and regulatory agencies including with respect to our planned operational expansion in Mexico; |

• | changes to health and safety, environmental and similar laws and governmental regulations that are adverse to our operations; |

• | volatility of the market price of our common stock; |

• | our ability to integrate successfully acquisitions in the expected timeframe; and |

• | future benefits to be derived from our investments in technologies, joint ventures and acquired companies; |

Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in the forward-looking statements contained herein. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws. All forward-looking statements included in this document are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue.

In this Annual Report on Form 10-K, we may rely on and refer to information from market research reports, analyst reports and other publicly available information. Although we believe that this information is reliable, we cannot guarantee the accuracy and completeness of this information, and we have not independently verified it.

3

PART I

ITEM 1. BUSINESS

OVERVIEW

Our Company

Stabilis Energy, Inc. and its subsidiaries (the “Company”, “Stabilis”, “our”, “us” or “we”) are a vertically integrated provider of distributed liquefied natural gas (“LNG”) production, distribution and fueling services to multiple end markets in North America. We have safely delivered over 200 million gallons of LNG through more than 20,000 truck deliveries during our 15-year operating history, which we believe makes us one of the largest and most experienced small-scale LNG providers in North America. We provide LNG to customers in diverse end markets, including the industrial, energy, mining, utility, pipeline, commercial, and high horsepower transportation markets. Our customers use LNG as an alternative to traditional fuel sources, such as distillate fuel oil and propane, to lower fuel costs and reduce harmful environmental emissions. Our customers also use LNG as a “virtual pipeline” solution when natural gas pipelines are not available or are curtailed.

We also provide electrical and instrumentation construction, installation and service to the oil and gas, marine, and industrial markets in Brazil and build electrical systems for sale in China through our 40% interest in our Chinese joint venture, BOMAY Electric Industries, Inc.

Our Industry

LNG can be used to deliver natural gas to locations where pipeline service is not available, has been interrupted, or needs to be supplemented. LNG can also be used to replace a variety of alternative fuels, including distillate fuel oil (including diesel fuel and other fuel oils) and propane, among others. We believe that these alternative fuel markets are large and provide significant opportunities for LNG substitution.

According to the Shell LNG Outlook 2020, the global LNG market is projected to grow by nearly 100% over the next 20 years due to the declining cost of natural gas and growing environmental concerns that are driving the use of cleaner fuels. We believe that similar macro trends are driving increased demand for small-scale LNG in North America. According to ADI Analytics, an independent energy market research and advisory firm, the North American small-scale LNG market was 499 million gallons in 2018 and is projected to grow by 271% to 1.9 billion gallons by 2030 (a 11.5% compound annual growth rate) due to the increased adoption of LNG across multiple end markets.

RECENT DEVELOPMENTS

On July 26, 2019 (the “Effective Date”), the Share Exchange with American Electric and its subsidiaries was completed. In the Share Exchange, American Electric acquired directly 100% of the outstanding limited liability company membership interests of Stabilis Energy, LLC (“Stabilis LLC”) from LNG Investment Company, LLC ("LNG Investment") and 20% of the outstanding limited liability membership interests of PEG Partners, LLC ("PEG") from AEGIS NG LLC ("AEGIS"). AEGIS owned a 20% noncontrolling interest of PEG. The remaining 80% of the outstanding limited liability company interests of PEG were owned directly by Stabilis LLC. As a result, Stabilis became a direct 100% owned subsidiary of American Electric and PEG became an indirectly-owned 100% subsidiary of American Electric. Under the Share Exchange Agreement, American Electric issued 13,178,750 post-split shares of common stock to acquire Stabilis LLC, which represented approximately 90% of the total amount of common stock of American Electric which was issued and outstanding as of July 26, 2019. The proposed transaction was approved by the shareholders of American Electric at a Special Meeting of Stockholders. The Share Exchange resulted in a change of control of American Electric to control by Casey Crenshaw by virtue of his beneficial ownership of 88.4% of the common stock of American Electric to be outstanding as of July 26, 2019.

Immediately following the Effective Date, the Company declared a reverse stock split of its outstanding common stock at a ratio of one-for-eight, American Electric changed its name to Stabilis Energy, Inc., and our common stock began trading under the ticker symbol “SLNG”. Our common stock traded under the symbol “SLNG” on the Nasdaq Stock Market from July 29, 2019 to October 2, 2019. On October 3, 2019 the Company’s common shares commenced trading on the OTCQX Best Market under the same symbol. Unless otherwise noted, any share or per share amounts in the accompanying consolidated financial statements and related notes give retroactive effect to the reverse stock split.

Because the former owners of Stabilis LLC owned 88.4% of the voting stock of the combined company immediately following the Effective Date, and certain other factors including that directors designated by LNG Investment constitute a majority of the post-closing board of directors, Stabilis LLC is treated as the acquiror of American Electric in the Share Exchange for accounting purposes. As a result, the Share Exchange is treated by American Electric as a reverse acquisition under the purchase method of accounting in

4

accordance with United States generally accepted accounting principles (“US GAAP”). For further information regarding this transaction, see Note 2—Acquisitions in the Notes to Consolidated Financial Statements.

On August 20, 2019, we expanded our presence in Mexico, acquiring a subsidiary that specializes in virtual LNG distribution systems, providing LNG to customers who use it as a fuel in mobile high horsepower applications and to customers who do not have natural gas pipeline access. The acquisition expands the Company's presence in the distributed LNG and compressed natural gas (“CNG”) markets in Mexico. We also established a joint venture to pursue investments in distributed natural gas production and distribution assets in Mexico.

OUR BUSINESS

Summary

Stabilis provides our customers with safe, reliable and cost effective LNG fueling solutions. We provide multiple products and services to our customers, including:

LNG Production and Sales—Stabilis builds and operates cryogenic natural gas processing facilities, called “liquefiers”, that convert natural gas into LNG through a multiple stage cooling process. We currently own and operate a liquefier that is designed to produce up to 100,000 LNG gallons (379 cubic meters) per day. We also purchase LNG from third-party production sources which allows us to support customers in markets where we do not own liquefiers. We define “small-scale” LNG production to include liquefiers that produce less than 1,000,000 LNG gallons per day (3,788 cubic meters per day).

Transportation and Logistics Services—Stabilis offers our customers a “virtual natural gas pipeline” by providing them with turnkey LNG transportation and logistics services in North America. We deliver LNG to our customers’ work sites from both our own production facility and our network of 25 third-party production sources located throughout North America. We own a fleet of LNG fueled trucks and cryogenic trailers to transport and deliver LNG. We also outsource similar equipment and transportation services from qualified third-party providers as required to support our customer base. We define “small-scale” LNG distribution to include distribution by trailer or tank container (up to 15,000 LNG gallons) or marine vessels that carry less than 8,000,000 LNG gallons (approximately 30,000 cubic meters).

Cryogenic Equipment Rental—Stabilis owns and operates a rental fleet of approximately 150 mobile LNG storage and vaporization assets, including: transportation trailers, electric and gas-fired vaporizers, ambient vaporizers, storage tanks, and mobile vehicle fuelers. We also own several stationary storage and regasification assets. We believe this is one of the largest fleets of small-scale LNG equipment in North America. Our fleet consists primarily of trailer-mounted mobile assets, making delivery to and between customer locations more efficient. We deploy these assets on job sites to provide our customers with the equipment required to transport, store, and consume LNG in their fueling operations.

Engineering and Field Support Services—Stabilis has experience in the safe, cost effective, and reliable use of LNG in multiple customer applications. We have also developed many processes and procedures that we believe improve our customers’ use of LNG in their operations. Our engineers help our customers design and integrate LNG into their fueling operations and our field service technicians help our customers mobilize, commission and reliably operate on the job site.

Stabilis generates revenue by selling and delivering LNG, which in many instances involves us providing engineering and field support services, to our customers. We also generate revenue by renting cryogenic equipment to our customers. We sell each product and service separately or as a bundle depending on the customer’s needs. LNG pricing depends on market pricing for natural gas and competing fuel sources (such as diesel, fuel oil, and propane among others), as well as the customer’s purchased volume, contract duration and credit profile.

Stabilis’ customers use natural gas in their operations for multiple reasons, including lower fuel cost, more stable fuel costs, reduced environmental emissions, and improved operating performance. We serve customers in a variety of end markets, including industrial, energy, mining, commercial, utilities and pipelines, and high horsepower transportation. We believe that LNG consumption will continue to increase in these end markets in the future.

Stabilis believes that our extensive operating experience positions us to be a leader in the North American small-scale LNG market. We operate an LNG liquefier and have executed approximately 200 turnkey LNG supply and distribution projects for our customers. We plan to leverage this experience to grow our business by investing in new LNG production and distribution assets throughout North America. We will also seek to consolidate the market by acquiring existing LNG production and distribution assets to create greater operating scale and efficiencies.

5

Power Delivery Solutions—We also provide electrical and instrumentation construction, installation and service to the oil and gas, marine, and industrial markets in Brazil and build electrical systems for sale in China through our 40% interest in our Chinese joint venture, BOMAY Electric Industries, Inc.

Market for Small-Scale LNG in North America

LNG can be used to deliver natural gas to locations where pipeline service is not available, has been interrupted, or needs to be supplemented. LNG can also be used to replace a variety of alternative fuels, including distillate fuel oil (including diesel fuel and other fuel oils) and propane, among others. We believe that these alternative fuel markets are large and provide significant opportunities for LNG substitution. U.S. Energy Information Administration (“EIA”) data for the U.S. market size for these alternative fuels in 2018 was as follows:

ADI Estimated LNG Market Size (LNG Gallons) | ||||||||||||||||

EIA Reported Gallons (Billions) | Cubic Meters (Millions) | LNG Gallon Equivalent (Billions) | 2018 (Billions) | % 2018 Combined | 2030 (Billions) | % 2018 Combined | ||||||||||

Distillate Fuel Oil | 63.4 | 408.0 | 107.7 | |||||||||||||

Propane | 13.1 | 54.7 | 14.4 | |||||||||||||

Combined | 76.5 | 462.7 | 122.1 | 0.5 | 0.4% | 1.9 | 1.6% | |||||||||

Note: Assumes 1.7 LNG gallons per distillate fuel oil gallon, 1.1 LNG gallons per propane gallon, and 264 LNG gallons per cubic meter

Source: U.S. Energy Information Administration and ADI Analytics

According to ADI Analytics ("ADI"), the North American small-scale LNG market was 499 million gallons in 2018 and is projected to be 1.9 billion gallons by 2030. This implies that LNG comprised approximately 0.4% of the combined U.S. distillate and propane markets in 2018 and will comprise approximately 1.6% of the current combined market size by 2030. We believe that LNG is a suitable substitute for most diesel and propane applications and that the LNG market share growth projected in the table above should be achievable based on current market trends.

We believe that the following factors could drive significant LNG market growth in North America over the next decade:

Less Expensive than Alternative Fuels. Technological advances in natural gas production have unlocked significant new reserves in North America. We believe that these proven, abundant and growing reserves of natural gas have the potential to produce among the highest volumes of natural gas in the world. This abundant supply of natural gas has supported relatively low natural gas prices in North America. The cost of natural gas in the United States and Canada currently is less than the cost of crude oil on an energy equivalent basis. In addition, because the price of the natural gas commodity makes up a smaller portion of the total cost of LNG relative to the commodity portion of competing fuels, the price of LNG is less sensitive to variations in the underlying commodity cost. These factors have made LNG cheaper than competing fuel sources at most times over the past ten years, and we believe that LNG will maintain this cost advantage into the foreseeable future.

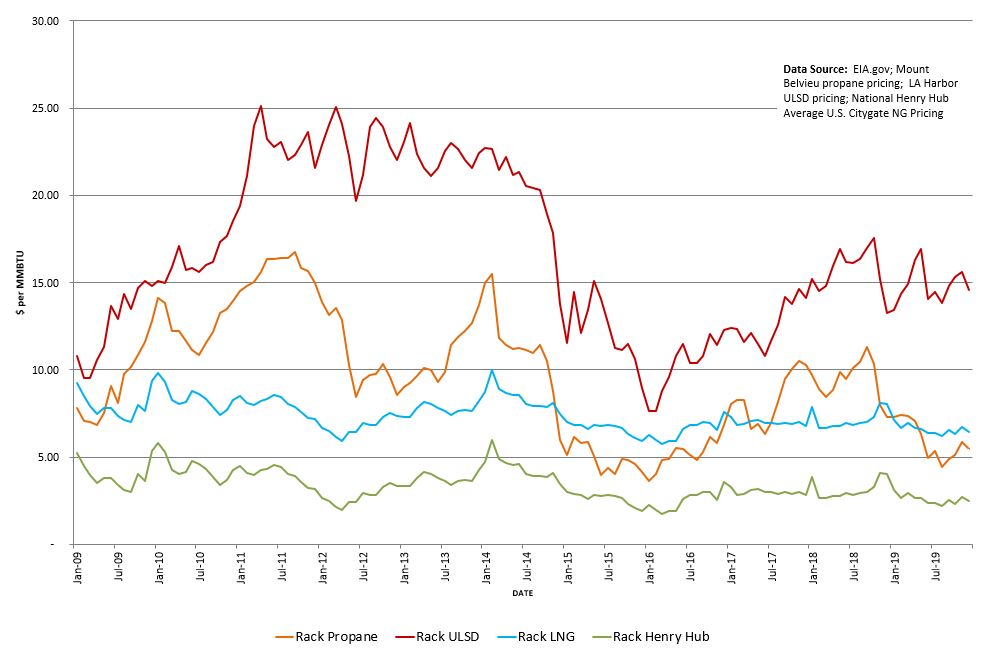

6

The following chart sets forth the wholesale price of Propane, Ultra-Low No. 2 Diesel, Indicative Liquefied Natural Gas and Natural Gas (Henry Hub).

ULSD, Propane & LNG pricing-2009 to Current

Lower Emissions than Alternative Fossil Fuels. Natural gas contains less carbon than most other fossil fuels and, as a result, produces fewer carbon dioxide emissions when burned. The National Energy Technology Laboratory indicates that new natural gas power plants emit between 50% and 60% less carbon dioxide compared with emissions from a typical coal plant. The Argonne National Laboratory indicates that natural gas vehicles produce between 13% and 21% fewer greenhouse gas emissions than comparable gasoline and diesel fueled vehicles. Additional studies indicate that natural gas also produces lower particulate matter and sulphur emissions than other fossil fuels. We believe the relative environmental benefits of natural gas as a fuel could become increasingly important if, as we expect, air quality regulations become increasingly stringent, new regulations mandating low carbon fuels are enacted, and our customers expand their corporate sustainability mandates to lower greenhouse gas emissions and increase fuel diversity.

Better Safety than Alternative Fuels. The physical characteristics of LNG make it a safer fuel when compared to diesel and propane because it boils and dissipates rapidly into the air when spilled instead of pooling on or near the ground. If released, LNG is also less combustible than diesel and propane because it ignites at relatively high temperatures and within a narrow flammability range when mixed with air. In addition, LNG fuel tanks and systems used in natural gas applications are subjected to a number of federal and state required safety tests, such as fire, environmental hazard, burst pressure and crash testing that ensure their safety.

Established LNG Production and Distribution Technology. ADI reports that small-scale LNG production and distribution technologies have been proven and are now widely available from multiple vendors. Small-scale liquefiers are available in modular formats from several vendors and many of them have established track records of reliable and safe operating performance. LNG transport trailers, storage vessels, and vaporization equipment are also available from multiple vendors, and most of this equipment also comes with an established operating track record. We believe that the availability of proven small-scale LNG production and distribution technologies reduces the technology risk in growing the industry, but it also places a premium on the owner’s or operator’s construction and operating capabilities.

7

Increasing Growth in Renewable Energy Production: Energy production from renewable energy sources, in particular wind and solar, is growing rapidly across the world as many governments and businesses seek to reduce their carbon emissions. The International Renewable Energy Agency (“IRENA”) reports that global power capacity based on renewable energy increased 7.9% in 2018 with solar and wind accounting for 84% of the growth. IRENA projects similar growth trends for the renewable energy production over the next several years. However, wind and solar are intermittent energy sources that require back-up energy sources that can come into service quickly and reliably. We believe that natural gas driven turbines are preferred viable back-up power source as they meet these operating requirements and use relatively clean natural gas fuel. We believe that natural gas power generation could support the growth of wind and solar energy production and that LNG could be a preferred source of natural gas fuel for off-pipeline applications.

Our Products, Services and Other Business Activities

Stabilis’ principal products, services and business activities are described below. Financial information about the revenue we receive from these activities is discussed in this report in Management’s Discussion and Analysis of Financial Condition and Results of Operations.

LNG Production. Stabilis owns and operates an LNG liquefier near George West, Texas, which we refer to as the “George West Liquefier”, that has the capacity to produce 36.5 million LNG gallons (129,395 cubic meters) per year or 100,000 LNG gallons (379 cubic meters) per day. This plant includes a dual truck trailer loading system and a 270,000 LNG gallon (1,023 cubic meters) storage tank system. The George West Liquefier was 98.6% dispatchable in 2019 with the only shutdowns coming for routine scheduled maintenance. We intend to build or acquire additional liquefiers throughout North America over the next several years as we seek to optimize our North American LNG supply network.

Stabilis believes that our new liquefiers will be able to produce LNG at costs that make it a competitive fuel source for our customers. Based on our operating experience at the George West Liquefier, our direct costs to liquefy gas range from $0.15 - $0.20 per LNG gallon ($1.82 - $2.42 per MMBtu) when the plant is operating in excess of 50% capacity. This includes plant operating costs, such as electricity and labor, but does not include the cost of the natural gas feedstock. This liquefaction cost could vary by time and plant location if input costs change. Our direct cost to deliver LNG via truck transportation is approximately $0.05 - $0.10 per gallon per every 100 miles traveled. These costs of liquefaction and transportation exclude corporate expenses such as sales and marketing, administration, and financing, among others. We believe that this cost of production and distribution will allow our LNG to be competitive with alternative fuel sources in most commodity market environments.

Stabilis owns a second liquefier that has a production capacity of 9.1 million LNG gallons (34,470 cubic meters) per year or 25,000 LNG gallons (95 cubic meters) per day. This liquefier is in storage awaiting deployment and we are actively exploring sites where it could be located. We are also in the process of evaluating other opportunities to develop liquefiers throughout North America, including several locations in Mexico.

LNG Sales. Stabilis supplies our customers with LNG produced at our own liquefaction facility as well as LNG produced at third-party facilities. We make the determination of LNG supply sources based on the cost of LNG, the transportation cost to deliver to regional customer locations, and the reliability of the supply source. Our network of 25 third-party LNG production facilities located throughout North America includes: 1) utility owned peak shaving plants, 2) natural gas/helium processing facilities, and 3) other merchant LNG production facilities similar to our George West Liquefier. We have contracts with these production sources that allow us to purchase LNG for our customers as required and without firm or long-term volume commitments. We believe that our third-party supply network is the largest and most complete in North America allowing us access to approximately 500 million LNG gallons (1.9 million cubic meters) of capacity annually on an as required basis. Occasionally the LNG we obtain from third parties may be purchased under take-or-pay contracts that require us to purchase minimum volumes. In situations where firm take or pay contracts are required, we try to support them with back-to-back customer purchase agreements. Currently we have one take-or-pay LNG supply contract that is matched to contracted customer demand. In 2019, we purchased approximately 40% of our LNG from third-party suppliers and we produced the remainder at the George West Liquefier.

Stabilis sells LNG on a bulk or wholesale basis to our customers. We sell LNG through supply contracts that are priced on a regional commodity index-plus basis, such that LNG sales under these contracts increase or decrease as a result of changes in the commodity cost of natural gas. We sell LNG to our customers based on the same commodity index we buy natural gas to reduce our exposure to commodity prices changes. We sell LNG fuel at prices we set based on prevailing market conditions. Our pricing methodology depends on our cost of natural gas and LNG production, the customer’s commercial requirements, the price of competing

8

energy sources, volumes required, contract duration, and the customer’s credit profile. Although we have long-term commercial relationships with many of our customers, our customer contracts are generally short-term in nature.

Transportation and Logistics Services. Stabilis offers its customers a “virtual natural gas pipeline” by providing them with turnkey transportation and logistics services for delivery from the LNG production source to the LNG consumption site. Our logistics and scheduling team offers 24-hour support to our customers. We utilize customized telemetry and fuel dispatch software systems to optimize our LNG deliveries. Customers can call our logistics team and have LNG delivered quickly and efficiently to almost any location in North America. We deliver LNG to our customers’ sites with our fleet of 42 tanker trailers, where it is stored and then vaporized on demand to fuel our customers consuming equipment which includes engines, turbines, generators, furnaces, dryers, boilers, kilns, pipelines, and other high horsepower applications.

Stabilis owns a fleet of LNG fueled trucks that are used to make deliveries to our customers near the George West Liquefier. We also have contracts with multiple national and regional trucking companies to deliver LNG to our customers. These carriers are certified to transport hazardous materials and the drivers are trained on safe LNG operating and delivery procedures. We believe that our established relationships with these carriers gives us a unique ability to reliably and safely deliver LNG to almost any location in North America on short notice.

Cryogenic Equipment Rental. Stabilis believes that we own the largest rental fleet of mobile LNG storage, transportation and vaporization equipment in North America. Our asset base includes 151 pieces of equipment, including: transportation trailers, electric and gas-fired vaporizers, ambient vaporizers, storage tanks, and mobile vehicle fuelers. We use these assets to provide customers with the necessary equipment to transport, store, and consume LNG in their operations.

Stabilis rents our cryogenic and related equipment to customers based on day rates that vary by the cost and availability of our equipment, and align with our customers’ contract terms. Our equipment is designed specifically for use in small-scale LNG applications and includes the safety and operational features that our customers and our regulators require. We believe that our current fleet of equipment can support significant growth in volumes in our business. We continually evaluate adding additional equipment as required by our customers to optimize their operations.

Mobile Asset Base

Asset Type | Qty | Description | |||

Mobile Storage and Vaporization Units | 92 | Located on customer sites for storage and delivery of LNG fuel | |||

Transport Trailers | 42 | Deliver LNG from production sources to customer sites | |||

Mobile Truck Fuelers | 8 | Mobile fueling station used to fill heavy duty trucks | |||

Other Cryogenic Assets | 9 | Includes hose reels, pump skids, generators, and other | |||

Total | 151 | ||||

Engineering and Field Service Support Services. Stabilis believes it has significant experience in the safe, cost efficient and reliable use of LNG in multiple customer applications. Our engineering team provides our customers with safe and effective LNG fueling plans. Our engineering services are usually included in our efforts to sell and commission customer projects, however sometimes we bill customers for them on an hourly or fixed project basis. Our staff of approximately 14 trained field service technicians help our customers use LNG safely and efficiently on their job sites. We generally bill our customers for field service technicians on a day rate basis but sometimes this cost is included in bundled pricing.

Power Delivery Solutions—As a result of the business combination with American Electric, we provide power delivery services and products for the oil and gas, marine vessel, power generation and broad industrial market segments in Brazil, and build electrical systems for sale in China through our 40% interest in BOMAY.

Our Customers

Stabilis serves customers in a variety of end markets, including industrial, energy, utilities and pipelines, mining, commercial, and transportation within the United States, Mexico and Canada. We believe these customer markets are well suited to use LNG because they consume relatively high volumes of fuel, operate in mobile, temporary or off-pipeline locations, have limited access to alternative fuel sources, and/or are facing increasingly stringent emissions or other environmental requirements. We currently serve approximately 74 customers. For the year ended December 31, 2019, Noble Energy, Inc. accounted for more than 10% of our revenues. For the year ended December 31, 2018, Noble Energy, Inc. and Blue Roads Solutions, LLC each accounted for more than 10% of our revenues. During such periods, no other purchaser accounted for 10% or more of our revenue. We believe that the loss

9

of any of these purchasers would not result in a material adverse effect on our financial condition or results of operations because LNG is a fungible product with well-established markets and numerous purchasers.

Industrial. Industrial applications for LNG include sand and aggregate producers, asphalt plants, greenhouses, food processers, paper mills, agricultural dryers, and general manufacturing facilities. Remote sand producers and mobile asphalt plants that use LNG to produce heat for their processing and drying operation are among our largest customers. LNG often replaces propane, fuel oil, or diesel fuel in these applications. These customers often cannot justify the cost of new pipeline infrastructure and using LNG requires minimal up-front costs, regulatory approvals, and lead time requirements. We believe LNG is optimal for these applications because it is cost-effective with stable pricing, offers consistent supply without curtailments, provides an energy density that minimizes storage requirements, and has a clean and consistent burn that makes heating operations more predictable. Based on our experience, sand production facilities can consume 10,000 to 20,000 LNG gallons per day, and asphalt plants can use 5,000 to 10,000 LNG gallons per day.

Energy. Energy producers use high horsepower engines to power their drilling and pressure pumping operations. LNG displaces some of the total diesel fuel consumption in these applications using dual-fuel engine technology. We believe that energy producers can use LNG to reduce fuel costs and to meet environmental emissions requirements. Based on our experience, dual-fuel drill rigs can consume 1,000 to 5,000 LNG gallons per day and dual-fuel pressure pumping spreads can consume 10,000 to 20,000 LNG gallons per day. Recently, energy producers began using the field gas being produced in their operations to fuel the turbine engines that power their pressure pumping spreads. While turbines can burn field gas, they often require significant amounts of LNG for primary or back-up fuel supply because field gas often varies widely in volume, composition, and pressure. Based on our experience, turbine driven pressure pumping operations can consume 30,000 to 60,000 LNG gallons per day when using LNG as the primary fuel.

Utilities and Pipelines. North America has an expansive network of pipelines that, based on age and increasingly more stringent regulations, require routine testing and maintenance. During such events LNG fueling solutions can provide flow assurance to address natural gas supply interruptions during pipeline hydrostatic testing, repairs, gas distribution system curtailments, or unplanned outages. Such solutions can also provide a bridge for large industrial or utility customers before permanent pipelines are installed. LNG is becoming more predominant in regions where natural gas demand is growing and utilities and pipelines are required to continue to meet critical peak gas demand. LNG can provide an economic solution to support these supply requirements during peak weather conditions, gas curtailments and/or pipeline repairs. LNG usage in utility and pipeline applications varies significantly by project type.

Mining. Mines, including those producing metals, rare earth materials, and coal, are often located in remote locations that are off the electrical grid and do not have natural gas pipeline access. Mines use LNG to fuel electrical generators and to produce heat for their processing activities. Several mines have also tested using LNG as a fuel for their mine trucks and other high horsepower engine equipment. In addition to fuel cost benefits, LNG can help reduce emissions at mines that are often located in environmentally sensitive areas. Based on our experience, power generation and heating applications at mines can consume 10,000 to 100,000 LNG gallons per day.

Commercial. Commercial locations, including offices, calls centers, data centers, campuses, often need fuel for primary or back-up power generation. LNG often replaces propane or diesel fuel in these applications. LNG usage in commercial applications varies significantly by location size and purpose.

Transportation. LNG is being used to fuel high horsepower engines in multiple transportation applications, including over-the-road trucking, mine haul trucks, locomotives, and marine engines due to reduced emissions and cost savings benefits. Extensive LNG fueling networks exist currently in the United States, the European Union, and China. Regulatory requirements are accelerating the adoption of LNG as a transportation fuel in other markets, particularly in the marine sector. The International Maritime Organization (“IMO”) has imposed a global sulphur cap of 0.5% on ships trading outside of established emission control areas starting in January 2020, a level that could be difficult to achieve using common marine fuels, such as heavy fuel oil, but could be achieved using LNG. Large marine vessels can take several hundred thousand gallons of LNG in a single fuel bunkering event. LNG is also being tested as a fuel for rail locomotives and mining trucks, and is also a commonly used rocket propellant. LNG usage in transportation application varies by the horsepower requirements of the application.

Mexico. The volume of U.S. produced natural gas going to Mexico has been increasing significantly over the last several years as pipelines have been built to deliver natural gas to major Mexican cities and utility sites. However, a large portion of Mexico does not have access to these pipelines and is not expected to have access soon so LNG can be used to provide energy to these areas. We believe we are currently one of the largest small-scale LNG exporters to Mexico with multiple truckloads crossing the border from

10

our George West Liquefier daily. Primary end markets for LNG in Mexico include the industrial, mining, and commercial sectors. We believe that the demand for LNG will continue to grow as the population and economy grow.

We actively deliver LNG through virtual distribution systems, providing LNG to customers who use it as a fuel in mobile high horsepower applications and to customers who do not have natural gas pipeline access.

Brazil. We offer a range of electrical and instrumentation construction and installation services to our customers. These services include new construction as well as electrical and instrumentation turnarounds, maintenance and renovation projects.

China. Through our 40% interest in BOMAY, we provide power and control systems for the land drilling market in China.

Growth Strategy

Stabilis’ primary business objective is to provide superior returns to our shareholders by becoming the leading vertically integrated small-scale LNG provider in the Americas. We intend to accomplish this objective by implementing the following growth strategies:

Expand our LNG production business throughout North America. Stabilis believes that the customers and markets we serve could benefit from localized LNG supply sourcing. To this end, we believe that expanding our LNG liquefaction footprint throughout North America will enhance our competitive position by lowering our delivered cost and by creating a comprehensive and reliable supply network for our customers. We intend to leverage our liquefier development, construction, and operations experience to develop new liquefiers in markets that require LNG supply. We plan to both build new liquefiers and acquire existing liquefiers based on whichever offers the best service to our customers and returns to our investors.

In addition to growth in our existing domestic markets, Stabilis plans to focus on opening liquefiers in Mexico and Canada. We believe that both countries are attractive development opportunities given their lack of natural gas pipeline infrastructure in certain regions and focus on reducing environmentally harmful emissions. Both markets are also home to large fuel consumers such as mines, manufacturing and process facilities, and remote commercial and residential communities. Currently we are pursuing partnerships and acquisition opportunities that we believe will give us the capabilities required to grow rapidly.

Expand our LNG distribution business throughout North America. Stabilis believes that expanding our LNG distribution capabilities throughout North America will enhance our competitive position by creating a comprehensive and reliable supply network for our customers, lowering our delivered LNG costs, and expanding our ability to service new industries and geographies. We currently provide LNG distribution and field service support throughout the United States and parts of Mexico and Canada. We plan to expand our distribution capabilities by adding equipment to our fleet, including the high-flow, high pressure vaporization equipment required by pipelines and turbine powered pressure pumping spreads. In addition, we plan to explore opportunities that expand our geographic reach and industry expertise, including acquisitions of companies that already service our targeted customers. Finally, we plan to explore opportunities to expand into the compressed natural gas (“CNG”) market to become a comprehensive mobile natural gas solution provider for our customers.

Consistent with our strategy to expand of our LNG production business, Stabilis will focus the expansion of our LNG distribution business on the United States, Mexico and Canada. We believe that supporting our liquefiers with our distribution capabilities optimizes our asset base and our ability to service our customers. We also plan to expand our third-party LNG supply network in these markets so we can provide our customers with comprehensive and reliable service.

Use our LNG production and distribution expertise to expand into Latin and South America. Stabilis believes there is a significant opportunity to leverage our expertise in LNG production and distribution to expand our business into power generation opportunities in Latin and South America. Our business development team is identifying utilities and industrial energy consumers that may view LNG as a compelling alternative to traditional distillate fuels. We believe it will be compelling for them to enter into long-term contracts that support the development of the infrastructure required to deliver LNG directly to their power generation and other assets. We are currently developing partnerships and customer relationships in various regions of Latin and South America. We expect that these markets will require some combination of LNG production or sourcing, local logistics, distribution services and field support, paired with Stabilis-owned power generation assets in some instances.

Maintain financial strength and flexibility. Stabilis will seek to maintain a conservative balance sheet which we believe will allow us to better react to market opportunities. We believe that maintaining adequate balance sheet flexibility, along with positive cash flows from operations, will provide us with sufficient liquidity to execute on our business strategies.

11

Competition

The market for natural gas is highly competitive. Stabilis believes the biggest competition for LNG in these applications are distillate fuels and propane as they power the majority of engines and generators in our target markets. We also compete with other fuel sources including pipeline natural gas and CNG. We believe we have multiple competitors in the market for natural gas fuel, including, but not limited to:

• | Producers and distributors of LNG, including Clean Energy Fuels Corp., Applied LNG, New Fortress Energy LLC, Kinetrex Energy, Pivotal LNG Inc., numerous utilities located across the country which produces LNG for peak shaving purposes, and numerous local providers of cryogenic distribution and field services; and |

• | Producers and distributors of CNG, including NG Advantage LLC, Xpress Natural Gas LLC, Compass Natural Gas Partners LP and Certarus Ltd. |

Stabilis competes with other natural gas companies, as well as other fossil fuel sources, based on a variety of factors, including, among others, cost, supply, availability, quality, cleanliness and safety of the fuel. Location is often a primary competitive factor as transportation costs limit the distance LNG can be hauled at competitive prices. We believe we compare favorably with many of our competitors on the basis of these factors; however, some of our competitors have longer operating histories and market based experience, larger customer bases, more expansive brand recognition, deeper market penetration and substantially greater financial, marketing and other resources than our business. As a result, they may be able to respond more quickly to changes in customer preferences, legal requirements or other industry or regulatory trends, devote greater resources to the development, promotion and sale of their products, adopt more aggressive pricing policies, dedicate more effort to infrastructure and systems development in support of their business or product development activities and exert more influence on the regulatory landscape that impacts the natural gas fuel market. Additionally, utilities and their affiliates typically have unique competitive advantages, including a lower cost of capital, substantial and predictable cash flows, long-standing customer relationships, greater brand awareness, and large sales and marketing organizations.

Stabilis does not believe that we compete with mid-scale and world-scale LNG liquefiers that produce more than 1,000,000 LNG-gallons (18,939 cubic meters) per day. These large LNG production facilities, such as those operated by Cheniere Energy and Freeport LNG, typically are designed and permitted to fill large marine vessels that deliver cargos of 21,120,000 LNG-gallons (80,000 cubic meters) or more to large import terminals in foreign markets. We do not believe that any of them currently have or plan to have truck loading facilities that would be required to supply LNG to small-scale LNG customers. We also do not believe that any mid-scale or large-scale liquefiers currently have plans to install LNG loading capabilities for vessels smaller than 7,920,000 LNG-gallons (30,000 cubic meters).

Competitive Strengths

Stabilis believes that we are well positioned to execute our business strategies based on the following competitive strengths:

LNG is an economically and environmentally attractive product. Stabilis believes that the combination of cost benefits and environmental benefits makes LNG a compelling fuel source for many energy consumers. We believe that LNG can be delivered to customers at prices that are lower and more stable than what they would pay for distillate fuels or propane. In addition, several of our customers have reported that LNG as a fuel decreases their operating costs by reducing equipment maintenance requirements and providing more consistent burn characteristics. We also believe that many of our customers use LNG because it can significantly reduce harmful carbon dioxide, nitrogen oxide, sulphur, particulate matter, and other emissions as compared to oil-based fuels.

Demonstrated ability to execute LNG projects safely and cost effectively. Stabilis has produced and delivered over 200 million gallons of LNG to our customers throughout our 15-year operating history. Our experience includes building and operating LNG production facilities, delivering LNG from third-party sources to our customers, and designing and executing a wide-variety of turnkey LNG fueling solutions for our customers using our cryogenic equipment fleet supported by our field service team. We have experience serving customers in multiple end markets including industrial, energy, utilities and pipelines, mining, commercial, and transportation. We also have experience exporting LNG to Mexico and Canada. Finally, we believe our team is among the most experienced in the small-scale LNG industry. We believe that we can leverage this proven LNG execution experience to grow our business in existing markets and expand our business into new markets.

Comprehensive provider of “virtual natural gas pipeline” solutions throughout North America. Stabilis offers our customers a comprehensive off-pipeline natural gas solution by providing the supply infrastructure, transportation and logistics, and field service support necessary to deliver LNG to them in a program that is tailored to their consumption needs. We believe we own one of the largest fleets of cryogenic transportation, storage, and vaporization equipment in North America. We can provide our customers LNG and related services for a wide variety of applications almost anywhere in United States, and we plan to expand our geographic

12

coverage in Mexico and Canada. We believe that our ability to be a “one stop shop” for all of our customers’ off-pipeline natural gas requirements throughout North America is unique among LNG providers.

Ability to leverage existing LNG production and delivery capabilities into new markets. Stabilis believes that our experience producing and distributing LNG can be leveraged to grow into new geographic and service end markets. Since our founding we have expanded our service area across the United States, northeastern Mexico, and western Canada. We have also expanded our industry coverage to include multiple new end markets and customers. We accomplished this expansion into new markets by leveraging our LNG production and distribution expertise, in combination with our cryogenic engineering and project development capabilities, to meet new customer needs.

Sales and Marketing

Stabilis markets our products and services primarily through our direct sales force, which includes sales representatives covering all of our major geographic and customer markets, as well as attendance at trade shows and participation in industry conferences and events. Our technical, sales and marketing teams also work closely with federal, state and local government agencies to provide education about the value of natural gas as a fuel and to keep abreast of proposed and newly adopted regulations that affect our industry.

Seasonality

A portion of Stabilis’ operating revenues and profits relate to providing backup gas for the local distribution infrastructure in the United States and Mexico to support utilities during times of peak heating demand from November through March. Revenues are generally lower from April to October during the months when heating demand is seasonally lower.

Government Regulation and Environmental Matters

Stabilis is subject to a variety of federal, international, state, provincial and local laws and regulations relating to the environment, health and safety, labor and employment, building codes and construction, zoning and land use, public reporting and taxation, among others. Any changes to existing laws or regulations, the adoption of new laws or regulations, or failure by us to comply with applicable laws or regulations could result in significant additional expense to us or our customers or a variety of administrative, civil and criminal enforcement measures, any of which could have a material adverse effect on our business, reputation, financial condition and results of operations. Regulations that significantly affect our operating activities are described below. Compliance with these regulations has not had a material effect on our capital expenditures, earnings or competitive position to date, but new laws or regulations or amendments to existing laws or regulations to make them more stringent could have such an effect in the future. We cannot estimate the costs that may be required for us to comply with potential new laws or changes to existing laws, and these unknown costs are not contemplated by our existing customer agreements or our budgets and cost estimates. We believe that we are in compliance with all environmental and other governmental regulations. Our compliance has, to date, had no material effect on our capital expenditures, earnings, or competitive position.

Construction and Operation of LNG Liquefaction Plants. To build and operate LNG liquefaction plants, Stabilis must apply for facility permits or licenses that address many factors, including storm water and wastewater discharges, waste handling, and air emissions related to production activities and equipment operation. The construction of LNG plants must also be approved by local planning boards and fire departments.

Transportation of LNG. Federal and state safety standards require that LNG is moved by qualified drivers in cryogenic containers designed for LNG transportation. Drivers are subject to US Department of Transportation (“USDOT”) regulations, such as FMCSA, Hazardous Materials Regulations, and state certification requirements, such as certifications by the Alternative Energy Division of the Railroad Commission of Texas. Cryogenic containers have to undergo annual USDOT visual inspections and periodic pressure tests. Motor vehicles equipped with an LNG container or other motor vehicles used principally for transporting LNG in portable containers in Texas have to be registered with the Railroad Commission of Texas.

Transfer of LNG. Federal safety standards require each transfer of LNG to be conducted in accordance with specific written safety procedures. These procedures must require that qualified personnel be in attendance during all LNG transfer operations, and these procedures must be implemented, and copies of the procedures must be available/displayed, at each LNG transfer location.

Storage and Vaporization of LNG at Customer Sites. To install and operate both temporary and permanent storage and vaporization equipment, Stabilis may apply for permits or licenses that address many factors, including waste handling and air

13

emissions related to onsite storage and equipment operation or consult with customers so they may apply for needed permits. The operation and siting of storage and vaporization of LNG may also require approval by local planning boards and fire departments.

Import & Export of LNG. To import or export LNG from the United States to Mexico and Canada via truck, numerous authorizations are required. In support of our business in Canada, Stabilis maintains an import and export license from the United States Department of Energy (“DOE”) and from the National Energy Board of Canada (“NEB”). We maintain an Emergency Response Action Plan (“ERAP”) with Transport Canada. In support of our business in Mexico, we maintain an export license from the DOE and maintain import permits to bring the LNG into the country. Exporting LNG in large quantities would require additional permits and licenses from various regulatory agencies, including the DOE and the Federal Energy Regulatory Commission (“FERC”). We do not have these permits at this time but could file for such authorizations in the future.

Employees

As of December 31, 2019, Stabilis had 162 employees. We believe our relations with employees are satisfactory. None of our employees are currently subject to a collective bargaining agreement.

Intellectual Property

The intellectual property portfolio of Stabilis and its subsidiaries includes patents and trademarks. The Company has two pending patent applications in the United States, specifically a non-provisional patent application for the use of natural gas for well-enhancement and a non-provisional patent application for natural gas deliquification. The Company has four pending foreign patent applications (two in Canada and two in Mexico). Additionally, the Company owns or has exclusive license to five U.S. and one foreign (Mexico) patents. The last patent to expire in the U.S. will expire in January 2031, absent any adjustments or extensions. The Company has ten U.S. trademark registrations and one foreign trademark registration (Canada). The Company has no pending trademark applications.

Additional Information

The Company was originally incorporated on October 21, 1996 as American Access Technologies, Inc., a Florida corporation. On May 15, 2007, American Access Technologies, Inc. completed a business combination with M&I Electric Industries, Inc. (“M&I” or “M&I Electric”), a Texas corporation, and changed its name to American Electric Technologies, Inc. On August 12, 2018, all of the U.S. business operations of American Electric Technologies, Inc. based in the United States (“U.S.”) were sold to an affiliate of Myers Power Products, Inc. As a result, 100% of the company’s ongoing business was from international operations conducted through a Brazilian subsidiary, and an interest in a Chinese joint venture.

As previously discussed under Recent Developments, Stabilis completed the Share Exchange with American Electric and its subsidiaries on July 26, 2019. Immediately following the completion, the Company declared a reverse stock split of its outstanding common stock at a ratio of one-for-eight, American Electric changed its name to Stabilis Energy, Inc., and our common stock began trading under the ticker symbol “SLNG”.

Stabilis’ principal executive office is located at 10375 Richmond Ave., Suite 700, Houston, Texas 77042. Our telephone number is 832-456-6500 and our website address is www.stabilisenergy.com. We make our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, amendments to those reports and other information filed with or furnished to the SEC available, free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. The reference to Stabilis’ website is not intended to incorporate the information on the website into this report.

ITEM 1A. RISK FACTORS

Investing in shares of our common stock involves a high degree of risk. You should carefully consider the risks described below with all of the other information included in this report in evaluating an investment in our common stock. If any of the following risks were to occur, our business, financial condition, results of operations, and cash flows could be materially adversely affected. In that case, the trading price of our common stock could decline and you could lose all or part of your investment. Additional risks not presently known to us or that we currently deem immaterial may also impair our business operations.

Risks Related to Our Business

Our ability to implement our business strategy may be materially and adversely affected by many known and unknown factors.

14

Our business strategy relies upon our future ability to successfully market natural gas to end-users, develop and maintain cost-effective logistics in our supply chain and construct, develop and operate energy-related infrastructure in North America. Our business strategy assumes that we will be able to expand our operations further in North America, enter into long-term purchase and supply contracts with end-users, acquire and transport LNG at attractive prices, develop infrastructure, and other future projects, into efficient and profitable operations in a timely and cost-effective way, obtain approvals from all relevant federal, international, state and local authorities, as needed, for the construction and operation of these projects and other relevant approvals, and obtain long-term capital appreciation and liquidity with respect to such investments. Our strategy may also be affected by future governmental laws and regulations. It also assumes that we will be able to enter into strategic relationships with energy end-users, power utilities, LNG providers, shipping companies, infrastructure developers, financing counterparties and other partners. These assumptions are subject to significant economic, competitive, regulatory and operational uncertainties, contingencies and risks, many of which are beyond our control. Additionally, in furtherance of our business strategy, we may acquire operating businesses or other assets in the future. Any such acquisitions would be subject to significant risks and contingencies, including the risk of integration, and we may not be able to realize the benefits of any such acquisitions.

Our future ability to execute our business strategy is uncertain, and it can be expected that one or more of our assumptions will prove to be incorrect and that we will face unanticipated events and circumstances that may adversely affect our business. Any one or more of the following factors may have a material adverse effect on our ability to implement our proposed strategy and achieve our targets:

• | failure to develop cost-effective logistics solutions; |

• | failure to manage expanding operations in the projected time frame; |

• | inability to structure innovative and profitable energy-related transactions and to optimally price and manage position, performance and counterparty risks; |

• | inability to develop infrastructure and other future projects in a timely and cost-effective manner; |

• | inability to attract and retain personnel in a timely and cost-effective manner; |

• | failure of investments in technology and machinery, such as liquefaction technology or LNG tank truck technology, to perform as expected; |

• | increases in competition which could increase costs and undermine profits; |

• | inability to source LNG in sufficient quantities and/or at economically attractive prices; |

• | failure to anticipate and adapt to new trends in the energy sector in North America and elsewhere; |

• | increases in operating costs, including the need for capital improvements, insurance premiums, general taxes, real estate taxes and utilities, affecting our profit margins; |

• | inability to raise significant additional debt and equity capital in the future to implement our business strategy as well as to operate and expand our business; |

• | general economic, political and business conditions in North America and in the other geographic areas we now operate and intend to operate in the future; |

• | inflation, depreciation of the currencies of the countries in which we operate and fluctuations in interest rates; |

• | failure to win new bids or contracts; |

• | failure to obtain approvals from governmental regulators and relevant local authorities for the construction and operation of potential future projects and other relevant approvals; |

• | existing and future governmental laws and regulations; or |

• | inability, or failure, of any customer or contract counterparty to perform their contractual obligations to us (for further discussion of counterparty risk, see “—Risks Related to Our Business—Our current ability to generate cash is substantially dependent upon the performance by customers under short-term contracts that we have entered into or will enter into in the near future, and we could be materially and adversely affected if any customer fails to perform its contractual obligations for any reason, including nonpayment and nonperformance, or if we fail to enter into such contracts at all”). |

If we experience any of these failures, such failure may adversely affect our financial condition, results of operations and ability to execute our business strategy.

15

Investment in us is speculative.

Our strategy may not be successful, and if unsuccessful, we may be unable to modify it in a timely and successful manner. We cannot give you any assurance that we will be able to implement our strategy on a timely basis, if at all, or achieve our internal model or that our assumptions will be accurate. Accordingly, your investment in our company is speculative and subject to a high degree of risk, and you should understand that there is a possibility of the loss of your entire investment. Our limited history also means that we continue to develop and implement various policies and procedures including those related to data privacy and other matters.

We will continue to incur significant capital and operating expenditures while we develop infrastructure for our supply chain and other future projects. We will need to invest significant amounts of additional capital to implement our strategy. We could experience delays beyond the expected development period which could increase the level of operating losses and negative operating cash flows. Our future liquidity may also be affected by the timing of construction financing availability in relation to the incurrence of construction costs and other outflows and by the timing of receipt of cash flows under our customer contracts in relation to the incurrence of project and operating expenses. Our ability to generate any positive operating cash flow and achieve profitability in the future is dependent on, among other things, our ability to develop an efficient supply chain and successfully and timely complete necessary infrastructures and fulfill our gas delivery obligations under our customer contracts.

Our business is dependent upon obtaining substantial additional funding from various sources, which may not be available or may only be available on unfavorable terms.

Our net working capital may not be sufficient to fully execute our business plan in the future. Assuming the accuracy of our assumptions relating to our business strategy, we believe that our cash resources will only be sufficient to meet projected capital expenditures, financing obligations and operating requirements in the near term. In the future, we expect to pursue additional offerings of debt or equity securities to assist us in developing our operations. If we are unable to secure additional funding, or if it is only available on terms that we determine are not acceptable, we may be unable to fully execute our business plan, and our business, financial condition or results of operations may be adversely affected. Our ability to raise additional capital will depend on financial, economic and market conditions and other factors, many of which are beyond our control. We cannot assure you that such additional funding will be available on acceptable terms, or at all.

A variety of factors beyond our control could impact the availability or cost of capital, including domestic or international economic conditions, increases in key benchmark interest rates and/or credit spreads, the adoption of new or amended banking or capital market laws or regulations, the re-pricing of market risks and volatility in capital and financial markets, risks relating to the credit risk of our customers and the jurisdictions in which we operate, as well as general risks applicable to the energy sector. Our financing costs could increase or future borrowings or equity offerings may be unavailable to us or unsuccessful, which could cause us to be unable to pay or refinance our indebtedness or to fund our other liquidity needs. We may rely on borrowings under debt instruments to fund our capital expenditures. If any of the lenders under these potential debt instruments were unable to perform on its commitments, we may need to seek replacement financing, which may not be available as needed, or may be available in more limited amounts or on more expensive or otherwise unfavorable terms.

After our recent acquisitions, we may not be profitable for an indeterminate period of time.

We have a limited operating history and therefore have not achieved consistent profitability on an annual basis. We will need to make significant additional investments to develop, improve and operate our business. We also expect to make significant expenditures and investments in identifying, acquiring and/or developing other future projects. We also expect to incur significant expenses in connection with the launch and continued growth of our business, including costs for LNG purchases, truck transportation, shipping and logistics, personnel and technological improvements. We may need to raise significant additional debt and equity capital to achieve our goals.

We may not be able to achieve profitability, and if we do, we cannot assure you that we would be able to sustain such profitability in the future. Our failure to achieve or sustain profitability would have a material adverse effect on our business and the value of our common stock.

Because we are currently dependent upon a limited number of customers, the loss of a significant customer could adversely affect our operating results.

A limited number of customers currently represent a substantial majority of our income. Our operating results are currently contingent on our ability to maintain LNG services to these customers. At least in the short term, we expect that a substantial majority of our sales will continue to arise from a concentrated number of customers, such as power utilities, energy producers and industrial end-users. We may be unable to accomplish our business plan to diversify and expand our customer base by attracting a broad array of customers, which could negatively affect our business, results of operations and financial condition.

16

Our current ability to generate cash is substantially dependent upon the performance by customers under short-term contracts that we have entered into or will enter into in the near future, and we could be materially and adversely affected if any customer fails to perform its contractual obligations for any reason, including nonpayment and nonperformance, or if we fail to enter into such contracts at all.

Our current results of operations and liquidity are, and will continue to be in the near future, substantially dependent upon performance by a small number of customers, which have each entered into supply agreements and other similar contracts of variable durations. Our near term ability to generate cash is dependent on the small number of customers’ continued willingness and ability to perform their obligations under their respective contracts. If any of these customers fails to perform its obligations under their contracts, our operating results, cash flow and liquidity could be materially and adversely affected, even if we were ultimately successful in seeking damages from any of these customers for a breach of the contract.

Risks of nonpayment and nonperformance by customers are a consideration in our businesses, and our credit procedures and policies may be inadequate to sufficiently eliminate customer credit risk. As part of our business strategy, we intend to target customers who have not been traditional purchasers of natural gas, including customers in developing countries, and these customers may have greater credit risk than typical natural gas purchasers. Therefore, we may request pre-payments in advance for purchasing LNG or our services for certain customers that pose a greater customer credit risk than other companies in the industry. Further, adverse economic conditions in the energy industry increase the risk of nonpayment and nonperformance by customers, particularly customers that have sub-investment grade credit ratings or significant counterparty risks.

Our customer contracts are subject to termination under certain circumstances.

Our customer contracts contain various termination rights. For example, each of the long-term customer contracts we maintain contains various termination rights including, without limitation:

• | for no cause by giving notice as agreed in the contract; |

• | upon the occurrence of certain events of force majeure; |

• | if we fail to make available specified scheduled cargo quantities; |

• | upon the occurrence of certain uncured payment defaults; |

• | upon the occurrence of an insolvency event; |

• | upon the occurrence of certain uncured, material breaches; and |

• | if we fail to commence commercial operations within the agreed timeframes. |

We may not be able to replace these contracts on desirable terms, or at all, if they are terminated. Contracts that we enter into in the future may contain similar provisions. If any of these current or future contracts are terminated, such termination could have a material adverse effect on our business, contracts, financial condition, operating results, cash flows, liquidity and prospects.

Cyclical or other changes in the demand for and price of LNG and natural gas may adversely affect our business and the performance of our customers and could have a material adverse effect on our business, contracts, financial condition, operating results, cash flows, liquidity and prospects.

Our business and the development of energy-related infrastructure and projects generally is based on assumptions about the future availability and price of natural gas and LNG markets. Natural gas and LNG prices have at various times been and may become volatile due to one or more of the following factors:

• | additions to competitive regasification capacity in North America and other markets, which could divert LNG or natural gas from our business; |

• | insufficient or oversupply of natural gas liquefaction or export capacity worldwide; |

• | insufficient LNG tanker capacity; |

• | weather conditions and natural disasters; |

• | reduced demand and lower prices for natural gas; |

• | increased natural gas production deliverable by pipelines, which could suppress demand for LNG; |

• | decreased oil and natural gas exploration activities, which may decrease the production of natural gas, or decrease the demand for LNG used in the oil and gas exploration and production process; |

• | cost improvements that allow competitors to offer LNG regasification services at reduced prices; |

17

• | changes in supplies of, and prices for, alternative energy sources such as coal, oil, nuclear, hydroelectric, wind and solar energy, which may reduce the demand for natural gas; |

• | changes in regulatory, tax or other governmental policies regarding imported or exported LNG, natural gas or alternative energy sources, which may reduce the demand for imported or exported LNG and/or natural gas; |

• | political conditions in natural gas producing regions; |

• | imposition of tariffs by China or any other jurisdiction on imports of LNG from the United States; and |

• | cyclical trends in general business and economic conditions that cause changes in the demand for natural gas. |

Adverse trends or developments affecting any of these factors could result in decreases in the prices at which we are able to sell LNG and natural gas and related services or increases in the prices we have to pay for natural gas or LNG, which could materially and adversely affect the performance of our customers, and could have a material adverse effect on our business, contracts, financial condition, operating results, cash flows, liquidity and prospects.