UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

20549

FORM 10-Q

(Mark One)

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2018

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF 1934

For the transition period from _____________ to _____________

Commission file number: 000-31203

NET 1 UEPS TECHNOLOGIES, INC.

(Exact name of registrant as specified in its charter)

| Florida | 98-0171860 |

| (State or other jurisdiction | (IRS Employer |

| of incorporation or organization) | Identification No.) |

President Place, 4th Floor, Cnr. Jan

Smuts Avenue and Bolton Road

Rosebank, Johannesburg 2196, South

Africa

(Address of principal executive offices, including zip code)

Registrant’s telephone number, including area code: 27-11-343-2000

Not Applicable

(Former Name, Former Address

and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant (1) has filed all

reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days.

YES

[X] NO [ ]

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-T (§232.405 of this chapter) during the preceding 12 months (or for such

shorter period that the registrant was required to submit and post such files).

YES [X] NO [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act (check one):

| [ ] | Large accelerated filer | [X] | Accelerated filer |

| [ ] | Non-accelerated filer | [ ] | Smaller reporting company |

| (do not check if a smaller reporting company) | |||

| [ ] | Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell

company (as defined in Rule 12b-2 of the Exchange Act).

YES [ ] NO [X ]

As of May 6, 2018 (the latest practicable date), 56,862,187 shares of the registrant’s common stock, par value $0.001 per share, net of treasury shares, were outstanding.

Form 10-Q

NET 1 UEPS TECHNOLOGIES, INC.

Table of Contents

1

Part I. Financial Information

Item 1. Financial Statements

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed

Consolidated Balance Sheets

| Unaudited | (A) | |||||

| March 31, | June 30, | |||||

| 2018 | 2017 | |||||

| (In thousands, except share data) | ||||||

| ASSETS | ||||||

| CURRENT ASSETS | ||||||

| Cash and cash equivalents | $ | 87,172 | $ | 258,457 | ||

| Pre-funded social welfare grants receivable (Note 2) | 4,643 | 2,322 | ||||

| Accounts receivable, net of allowances of – March: $966; June: $1,255 | 120,664 | 111,429 | ||||

| Finance loans receivable, net of allowances of – March: $17,622; June: $7,469 | 76,916 | 80,177 | ||||

| Inventory (Note 3) | 11,808 | 8,020 | ||||

| Deferred income taxes (Note 1) | - | 5,330 | ||||

| Total current assets before settlement assets | 301,203 | 465,735 | ||||

| Settlement assets (Note 4) | 394,138 | 640,455 | ||||

| Total current assets | 695,341 | 1,106,190 | ||||

| PROPERTY, PLANT AND EQUIPMENT, net of accumulated depreciation of – March: $145,163; June: $120,212 | 31,592 | 39,411 | ||||

| EQUITY-ACCOUNTED INVESTMENTS (Note 6) | 185,023 | 27,862 | ||||

| GOODWILL (Note 7) | 182,534 | 188,833 | ||||

| INTANGIBLE ASSETS, net (Note 7) | 31,428 | 38,764 | ||||

| DEFERRED INCOME TAXES (Note 1) | 3,363 | - | ||||

| OTHER LONG-TERM ASSETS, including reinsurance assets (Note 6 and Note 8) | 271,185 | 49,696 | ||||

| TOTAL ASSETS | 1,400,466 | 1,450,756 | ||||

| LIABILITIES | ||||||

| CURRENT LIABILITIES | ||||||

| Short-term credit facilities (Note 9) | 3,400 | 16,579 | ||||

| Accounts payable | 16,995 | 15,136 | ||||

| Other payables | 43,001 | 34,799 | ||||

| Current portion of long-term borrowings (Note 10) | 56,446 | 8,738 | ||||

| Income taxes payable | 14,502 | 5,607 | ||||

| Total current liabilities before settlement obligations | 134,344 | 80,859 | ||||

| Settlement obligations (Note 4) | 394,138 | 640,455 | ||||

| Total current liabilities | 528,482 | 721,314 | ||||

| DEFERRED INCOME TAXES (Note 1) | 17,789 | 11,139 | ||||

| LONG-TERM BORROWINGS (Note 10) | 19,008 | 7,501 | ||||

| OTHER LONG-TERM LIABILITIES, including insurance policy liabilities (Note 8) | 2,901 | 2,795 | ||||

| TOTAL LIABILITIES | 568,180 | 742,749 | ||||

| COMMITMENTS AND CONTINGENCIES (Note 18) | ||||||

| REDEEMABLE COMMON STOCK (Note 1) | 107,672 | 107,672 | ||||

| EQUITY | ||||||

| COMMON STOCK (Note

11) Authorized: 200,000,000 with $0.001 par value; Issued and outstanding shares, net of treasury - March: 56,855,187; June: 56,369,737 |

80 | 80 | ||||

| PREFERRED

STOCK Authorized shares: 50,000,000 with $0.001 par value; Issued and outstanding shares, net of treasury: March: -; June: - |

- | - | ||||

| ADDITIONAL PAID-IN-CAPITAL | 275,536 | 273,733 | ||||

| TREASURY SHARES, AT COST: March: 24,891,292; June: 24,891,292 | (286,951 | ) | (286,951 | ) | ||

| ACCUMULATED OTHER COMPREHENSIVE LOSS (Note 12) | (73,481 | ) | (162,569 | ) | ||

| RETAINED EARNINGS | 805,390 | 773,276 | ||||

| TOTAL NET1 EQUITY | 720,574 | 597,569 | ||||

| NON-CONTROLLING INTEREST | 4,040 | 2,766 | ||||

| TOTAL EQUITY (Note 1) | 724,614 | 600,335 | ||||

| TOTAL LIABILITIES, REDEEMABLE COMMON STOCK AND SHAREHOLDERS’ EQUITY | $ | 1,400,466 | $ | 1,450,756 | ||

(A) – Derived from audited financial statements

See Notes to Unaudited Condensed Consolidated Financial Statements

2

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed

Consolidated Statements of Operations

| Three months ended | Nine months ended | |||||||||||

| March 31, | March 31, | |||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||

| (In thousands, except per share data) | (In thousands, except per share data) | |||||||||||

| REVENUE | $ | 162,721 | $ | 147,944 | $ | 463,695 | $ | 455,010 | ||||

| EXPENSE | ||||||||||||

| Cost of goods sold, IT processing, servicing and support | 77,860 | 70,912 | 226,506 | 219,210 | ||||||||

| Selling, general and administration | 48,091 | 42,195 | 141,417 | 122,366 | ||||||||

| Depreciation and amortization | 9,341 | 10,290 | 27,030 | 31,117 | ||||||||

| Impairment loss (note 7) | 19,865 | - | 19,865 | - | ||||||||

| OPERATING INCOME | 7,564 | 24,547 | 48,877 | 82,317 | ||||||||

| INTEREST INCOME | 5,154 | 5,124 | 14,903 | 14,489 | ||||||||

| INTEREST EXPENSE | 2,426 | 467 | 6,872 | 1,773 | ||||||||

| INCOME BEFORE INCOME TAX EXPENSE | 10,292 | 29,204 | 56,908 | 95,033 | ||||||||

| INCOME TAX EXPENSE (Note 17) | 10,941 | 10,233 | 31,280 | 32,320 | ||||||||

| NET (LOSS) INCOME BEFORE EARNINGS FROM EQUITY-ACCOUNTED INVESTMENTS | (649 | ) | 18,971 | 25,628 | 62,713 | |||||||

| EARNINGS FROM EQUITY-ACCOUNTED INVESTMENTS | 3,960 | 45 | 7,389 | 778 | ||||||||

| NET INCOME | 3,311 | 19,016 | 33,017 | 63,491 | ||||||||

| LESS NET INCOME ATTRIBUTABLE TO NON- CONTROLLING INTEREST | 302 | 624 | 903 | 1,826 | ||||||||

| NET INCOME ATTRIBUTABLE TO NET1 | $ | 3,009 | $ | 18,392 | $ | 32,114 | $ | 61,665 | ||||

| Net income per share, in U.S. dollars (Note 14) | ||||||||||||

| Basic earnings attributable to Net1 shareholders | $ | 0.05 | $ | 0.34 | $ | 0.57 | $ | 1.16 | ||||

| Diluted earnings attributable to Net1 shareholders | $ | 0.05 | $ | 0.34 | $ | 0.56 | $ | 1.16 | ||||

See Notes to Unaudited Condensed Consolidated Financial Statements

3

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed

Consolidated Statements of Comprehensive Income

| Three months ended | Nine months ended | |||||||||||

| March 31, | March 31, | |||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||

| (In thousands) | (In thousands) | |||||||||||

| Net income | $ | 3,311 | $ | 19,016 | $ | 33,017 | $ | 63,491 | ||||

| Other comprehensive income (loss) | ||||||||||||

| Movement in foreign currency translation reserve | 20,683 | 24,158 | 60,320 | 25,694 | ||||||||

| Net unrealized income on asset available for sale, net of tax | 29,366 | - | 29,366 | - | ||||||||

| Movement

in foreign currency translation reserve related to equity-accounted investments |

- | - | (227 | ) | - | |||||||

| Total other comprehensive income, net of taxes | 50,049 | 24,158 | 89,459 | 25,694 | ||||||||

| Comprehensive income | 53,360 | 43,174 | 122,476 | 89,185 | ||||||||

| Less comprehensive income attributable to non- controlling interest | (473 | ) | (649 | ) | (1,274 | ) | (2,330 | ) | ||||

| Comprehensive income attributable to Net1 | $ | 52,887 | $ | 42,525 | $ | 121,202 | $ | 86,855 | ||||

See Notes to Unaudited Condensed Consolidated Financial Statements

4

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed Consolidated

Statement of Changes in Equity for the nine

months ended March 31, 2018 (dollar amounts in

thousands)

| Net 1 UEPS Technologies, Inc. Shareholders | ||||||||||||||||||||||||||||||||||||

| Number | Accumulated | |||||||||||||||||||||||||||||||||||

| Number | of | Number of | Additional | Other | Total | Non- | Redeemable | |||||||||||||||||||||||||||||

| of | Treasury | Treasury | Shares, Net | Paid-In | Retained | Comprehensive | Net1 | Controlling | Common Stock | |||||||||||||||||||||||||||

| Shares | Amount | Shares | Shares | of Treasury | Capital | Earnings | (Loss) Income | Equity | Interest | Total | (Note 1) | |||||||||||||||||||||||||

| Balance – July 1, 2017 | 81,261,029 | $ | 80 | (24,891,292 | ) | $ | (286,951 | ) | 56,369,737 | $ | 273,733 | $ | 773,276 | $ | (162,569 | ) | $ | 597,569 | $ | 2,766 | $ | 600,335 | $ | 107,672 | ||||||||||||

| Restricted stock granted (Note 13) | 611,411 | 611,411 | - | - | ||||||||||||||||||||||||||||||||

| Stock-based compensation charge (Note 13) | 2,052 | 2,052 | 2,052 | |||||||||||||||||||||||||||||||||

| Reversal of stock compensation charge (Note 13) | (125,961 | ) | (125,961 | ) | (42 | ) | (42 | ) | (42 | ) | ||||||||||||||||||||||||||

| Reversal of stock based- compensation charge related to equity-accounted investment | (207 | ) | (207 | ) | (207 | ) | ||||||||||||||||||||||||||||||

| Net income | 32,114 | 32,114 | 903 | 33,017 | ||||||||||||||||||||||||||||||||

| Other comprehensive income (Note 12) | 89,088 | 89,088 | 371 | 89,459 | ||||||||||||||||||||||||||||||||

| Balance – March 31, 2018 | 81,746,479 | $ | 80 | (24,891,292 | ) | $ | (286,951 | ) | 56,855,187 | $ | 275,536 | $ | 805,390 | $ | (73,481 | ) | $ | 720,574 | $ | 4,040 | $ | 724,614 | $ | 107,672 | ||||||||||||

See Notes to Unaudited Condensed Consolidated Financial Statements

5

NET 1 UEPS TECHNOLOGIES, INC.

Unaudited Condensed

Consolidated Statements of Cash Flows

| Three months ended | Nine months ended | |||||||||||

| March 31, | March 31, | |||||||||||

| 2018 | 2017 | 2018 | 2017 | |||||||||

| (In thousands) | (In thousands) | |||||||||||

| Cash flows from operating activities | ||||||||||||

| Net income | $ | 3,311 | $ | 19,016 | $ | 33,017 | $ | 63,491 | ||||

| Depreciation and amortization | 9,341 | 10,290 | 27,030 | 31,117 | ||||||||

| Earnings from equity-accounted investments | (3,960 | ) | (45 | ) | (7,389 | ) | (778 | ) | ||||

| Interest on Cedar Cellular note (Note 6) | (587 | ) | - | (769 | ) | - | ||||||

| Fair value adjustments | (110 | ) | (50 | ) | (209 | ) | (61 | ) | ||||

| Interest payable | (17 | ) | 75 | (264 | ) | 84 | ||||||

| Facility fee amortized | 120 | 27 | 467 | 94 | ||||||||

| (Profit) Loss on disposal of property, plant and equipment | (50 | ) | (98 | ) | 71 | (571 | ) | |||||

| Profit on disposal of business | - | - | (463 | ) | - | |||||||

| Stock-based compensation charge (reversal), net (Note 13) | 575 | 621 | 2,010 | (68 | ) | |||||||

| Dividends received from equity accounted investments | 1,946 | - | 4,111 | 370 | ||||||||

| Impairment loss (Note 7) | 19,865 | - | 19,865 | - | ||||||||

| Decrease (Increase) in accounts receivable, pre-funded social welfare grants receivable and finance loans receivable | 42,558 | (16,612 | ) | 9,422 | (2,261 | ) | ||||||

| Decrease (Increase) in inventory | 1,072 | 3,893 | (2,776 | ) | 308 | |||||||

| Increase (Decrease) in accounts payable and other payables | 2,827 | (1,486 | ) | 5,775 | (4,386 | ) | ||||||

| Decrease in taxes payable | 9,007 | 6,678 | 8,091 | 5,819 | ||||||||

| Decrease in deferred taxes | (653 | ) | (506 | ) | (225 | ) | (1,752 | ) | ||||

| Net cash provided by operating activities | 85,245 | 21,803 | 97,764 | 91,406 | ||||||||

| Cash flows from investing activities | ||||||||||||

| Capital expenditures | (4,225 | ) | (1,949 | ) | (7,801 | ) | (8,498 | ) | ||||

| Proceeds from disposal of property, plant and equipment | 160 | 330 | 575 | 1,344 | ||||||||

| Investment in Cell C (Note 6) | - | - | (151,003 | ) | - | |||||||

| Investment in equity of equity-accounted investments (Note 6) | (18,597 | ) | - | (132,335 | ) | - | ||||||

| Loans to equity-accounted investments (Note 6) | (10,635 | ) | (2,000 | ) | (10,635 | ) | (12,044 | ) | ||||

| Acquisition of held to maturity investment (Note 6) | - | - | (9,000 | ) | - | |||||||

| Investment in MobiKwik | - | - | - | (15,347 | ) | |||||||

| Acquisitions, net of cash acquired | - | - | - | (4,651 | ) | |||||||

| Other investing activities | - | - | (154 | ) | - | |||||||

| Net change in settlement assets (Note 4) | 43,222 | (165,945 | ) | 280,390 | 54,827 | |||||||

| Net cash provided by (used in) investing activities | 9,925 | (169,564 | ) | (29,963 | ) | 15,631 | ||||||

| Cash flows from financing activities | ||||||||||||

| Long-term borrowings utilized (Note 10) | 17,726 | 274 | 113,157 | 521 | ||||||||

| Repayment of long-term borrowings (Note 10) | (15,826 | ) | - | (60,967 | ) | (28,493 | ) | |||||

| Repayment of bank overdraft (Note 9) | (42,650 | ) | - | (56,993 | ) | - | ||||||

| Proceeds from bank overdraft (Note 9) | 9,802 | - | 42,372 | - | ||||||||

| Guarantee fee paid (Note 10) | (202 | ) | - | (754 | ) | (1,145 | ) | |||||

| Proceeds from issue of common stock | - | 45,629 | - | 45,629 | ||||||||

| Acquisition of treasury stock (Note 11) | - | - | - | (32,081 | ) | |||||||

| Dividends paid to non-controlling interest | - | - | - | (613 | ) | |||||||

| Net change in settlement obligations (Note 4) | (43,222 | ) | 165,955 | (280,390 | ) | (54,817 | ) | |||||

| Net cash (used in) provided by financing activities | (74,372 | ) | 211,858 | (243,575 | ) | (70,999 | ) | |||||

| Effect of exchange rate changes on cash | 1,478 | 4,719 | 4,489 | 8,025 | ||||||||

| Net increase (decrease) in cash, cash equivalents and restricted cash | 22,276 | 68,816 | (171,285 | ) | 44,063 | |||||||

| Cash, cash equivalents and restricted cash – beginning of period | 64,896 | 198,891 | 258,457 | 223,644 | ||||||||

| Cash, cash equivalents and restricted cash – end of period (1) | $ | 87,172 | $ | 267,707 | $ | 87,172 | $ | 267,707 | ||||

See Notes to Unaudited Condensed Consolidated Financial Statements

(1) Cash, cash equivalents and restricted cash as of March 31, 2017, includes restricted cash of approximately $44.7 million related to the guarantee issued by FirstRand Bank Limited (acting through its Rand Merchant Bank division). This cash was placed into an escrow account and was considered restricted as to use and therefore was classified as restricted cash. The restriction lapsed upon expiry of the guarantee.

6

NET 1 UEPS TECHNOLOGIES, INC.

Notes to the Unaudited Condensed Consolidated Financial

Statements

for the three and nine months ended March 31, 2018 and

2017

(All amounts in tables stated in thousands or thousands of U.S.

dollars, unless otherwise stated)

| 1. |

Basis of Presentation and Summary of Significant Accounting Policies |

Unaudited Interim Financial Information

The accompanying unaudited condensed consolidated financial statements include all majority-owned subsidiaries over which the Company exercises control and have been prepared in accordance with U.S. generally accepted accounting principles (“GAAP”) and the rules and regulations of the United States Securities and Exchange Commission for Quarterly Reports on Form 10-Q and include all of the information and disclosures required for interim financial reporting. The results of operations for the three and nine months ended March 31, 2018 and 2017, are not necessarily indicative of the results for the full year. The Company believes that the disclosures are adequate to make the information presented not misleading.

These financial statements should be read in conjunction with the financial statements, accounting policies and financial notes thereto included in the Company’s Annual Report on Form 10-K for the fiscal year ended June 30, 2017. In the opinion of management, the accompanying unaudited condensed consolidated financial statements reflect all adjustments (consisting only of normal recurring adjustments), which are necessary for a fair representation of financial results for the interim periods presented. During the three months ended December 31, 2017, the Company reclassified redeemable common stock out of total equity because redeemable common stock is required to be presented outside of permanent equity. The Company has restated these amounts in its unaudited condensed consolidated balance sheet as at June 30, 2017 and unaudited condensed consolidated statement of changes in equity for the nine months ended March 31, 2018. The reclassification resulted in a decrease in total equity by approximately $107.7 million and an increase in redeemable common stock, presented outside of permanent equity, of approximately $107.7 million. This reclassification had no impact on the Company’s previously reported consolidated income, comprehensive income or cash flows.

References to the “Company” refer to Net1 and its consolidated subsidiaries, collectively, unless the context otherwise requires. References to “Net1” are references solely to Net 1 UEPS Technologies, Inc.

Recent accounting pronouncements adopted

In August 2014, the FASB issued guidance regarding Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern. This guidance requires an entity to perform interim and annual assessments of its ability to continue as a going concern within one year of the date that its financial statements are issued. An entity must provide certain disclosures if conditions or events raise substantial doubt about the entity’s ability to continue as a going concern. The guidance is effective for the Company beginning July 1, 2017. The adoption of this guidance did not have a material impact on the Company’s financial statements disclosures.

In July 2015, the FASB issued guidance regarding Simplifying the Measurement of Inventory. This guidance requires entities to measure most inventory “at the lower of cost and net realizable value,” thereby simplifying the current guidance under which an entity must measure inventory at the lower of cost or market (market in this context is defined as one of three different measures). The guidance will not apply to inventories that are measured by using either the last-in, first-out (“LIFO”) method or the retail inventory method (“RIM”). The guidance is effective for the Company beginning July 1, 2017. The adoption of this guidance did not have a material impact on the Company’s financial statements.

In November 2015, the FASB issued guidance regarding Balance Sheet Classification of Deferred Taxes. This guidance requires that deferred tax liabilities and assets are to be classified as non-current in a classified statement of financial position. The current requirement that deferred tax liabilities and assets of a tax-paying component of an entity be offset and presented as a single amount is not affected by the amendments in this update. This guidance is effective for the Company beginning July 1, 2017, and has been applied on a prospective basis. The adoption of this guidance has resulted in the reclassification of current deferred tax assets and liabilities as non-current deferred tax assets and liabilities in the unaudited condensed consolidated balance sheet as of March 31, 2018. Prior period current deferred tax assets have not been reclassified as non-current in the unaudited condensed consolidated balance sheet as of June 30, 2017.

In March 2016, the FASB issued guidance regarding Improvements to Employee Share-Based Payment Accounting. The guidance simplifies several aspects of the accounting for employee share-based payment transactions for both public and nonpublic entities, including the accounting for income taxes, forfeitures, and statutory tax withholding requirements, as well as classification in the statement of cash flows. This guidance is effective for the Company beginning July 1, 2017. The adoption of this guidance did not have a material impact on the Company’s financial statements. The Company has elected to continue to estimate the number of forfeitures when an award is made.

7

| 1. |

Basis of Presentation and Summary of Significant Accounting Policies (continued) |

Recent accounting pronouncements not yet adopted as of March 31, 2018

In May 2014, the FASB issued guidance regarding Revenue from Contracts with Customers. This guidance requires an entity to recognize revenue when a customer obtains control of promised goods or services in an amount that reflects the consideration which the entity expects to receive in exchange for those goods or services. In addition, the standard requires disclosure of the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The guidance was originally set to be effective for the Company beginning July 1, 2017, however in August 2015, the FASB issued guidance regarding Revenue from Contracts with Customers, Deferral of the Effective Date. This guidance defers the required implementation date specified in Revenue from Contracts with Customers to December 2017. Public companies may elect to adopt the standard along the original timeline.

The guidance is effective for the Company beginning July 1, 2018. The Company expects that this guidance may have a material impact on its financial statements and is currently evaluating the impact of this guidance on its financial statements on adoption.

In January 2016, the FASB issued guidance regarding Recognition and Measurement of Financial Assets and Financial Liabilities. The guidance primarily affects the accounting for equity investments, financial liabilities under the fair value option and the presentation and disclosure requirements for financial instruments. The guidance requires changes in the fair value of the Company’s equity investments, with certain exceptions, to be recognized through net income rather than other comprehensive income. In addition, the guidance clarifies the valuation allowance assessment when recognizing deferred tax assets resulting from unrealized losses on available-for-sale debt securities. This guidance is effective for the Company beginning July 1, 2018, and early adoption is not permitted, with certain exceptions. The amendments are required to be applied by means of a cumulative-effect adjustment on the balance sheet as of the beginning of the fiscal year of adoption. The Company is currently assessing the impact of this guidance on its financial statements disclosure.

In February 2016, the FASB issued guidance regarding Leases. The guidance increases transparency and comparability among organizations by requiring the recognition of lease assets and lease liabilities on the balance sheet. The amendments to current lease guidance include the recognition of assets and liabilities by lessees for those leases currently classified as operating leases. The guidance also requires disclosures to meet the objective of enabling users of financial statements to assess the amount, timing, and uncertainty of cash flows arising from leases. This guidance is effective for the Company beginning July 1, 2019. Early adoption is permitted. The Company expects that this guidance may have a material impact on its financial statements and is currently evaluating the impact of this guidance on its financial statements on adoption.

In June 2016, the FASB issued guidance regarding Measurement of Credit Losses on Financial Instruments. The guidance replaces the incurred loss impairment methodology in current GAAP with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. For trade and other receivables, loans, and other financial instruments, an entity is required to use a forward-looking expected loss model rather than the incurred loss model for recognizing credit losses, which reflects losses that are probable. Credit losses relating to available-for-sale debt securities will also be recorded through an allowance for credit losses rather than as a reduction in the amortized cost basis of the securities. This guidance is effective for the Company beginning July 1, 2020. Early adoption is permitted beginning July 1, 2019. The Company is currently assessing the impact of this guidance on its financial statements disclosure.

In June 2016, the FASB issued guidance regarding Classification of Certain Cash Receipts and Cash Payments. The guidance is intended to reduce diversity in practice and explains how certain cash receipts and payments are presented and classified in the statement of cash flows, including beneficial interests in securitization, which would impact the presentation of the deferred purchase price from sales of receivables. This guidance is effective for the Company beginning July 1, 2018, and must be applied retrospectively. Early adoption is permitted. The Company is currently assessing the impact of this guidance on its financial statements disclosure.

In January 2017, the FASB issued guidance regarding Clarifying the Definition of a Business. This guidance provides a more robust framework to use in determining when a set of assets and activities is a business. Because the current definition of a business is interpreted broadly and can be difficult to apply, stakeholders indicated that analyzing transactions is inefficient and costly and that the definition does not permit the use of reasonable judgment. The amendments provide more consistency in applying the guidance, reduce the costs of application, and make the definition of a business more operable. The guidance is effective for the Company beginning July 1, 2018. Early adoption is permitted. The Company is currently assessing the impact of this guidance on its financial statements disclosure.

In January 2017, the FASB issued guidance regarding Simplifying the Test for Goodwill Impairment. This guidance removes the requirement for an entity to calculate the implied fair value of goodwill (as part of step 2 of the current goodwill impairment test) in measuring a goodwill impairment loss. The guidance is effective for the Company beginning July 1, 2020. Early adoption is permitted for interim or annual goodwill impairment tests performed on testing dates after January 1, 2017. The Company is currently assessing the impact of this guidance.

8

| 1. |

Basis of Presentation and Summary of Significant Accounting Policies (continued) |

Recent accounting pronouncements not yet adopted as of March 31, 2018 (continued)

In May 2017, the FASB issued guidance regarding Compensation—Stock Compensation (Topic 718): Scope of Modification Accounting. The guidance amends the scope of modification accounting for share-based payment arrangements and provides guidance on the types of changes to the terms or conditions of share-based payment awards to which an entity would be required to apply modification accounting under Accounting Standards Codification 718. Specifically, an entity would not apply modification accounting if the fair value, vesting conditions, and classification of the awards are the same immediately before and after the modification. The guidance is effective for the Company beginning July 1, 2018. Early adoption is permitted. The Company is currently assessing the impact of this guidance on its financial statements disclosure.

| 2. |

Pre-funded social welfare grants receivable |

Pre-funded social welfare grants receivable represents primarily amounts pre-funded by the Company to certain merchants participating in the merchant acquiring system. The April 2018 payment service commenced on April 3, 2018, but the Company pre-funded certain merchants participating in the merchant acquiring systems on March 31, 2018. The July 2017 payment service commenced on July 1, 2017, but the Company pre-funded certain merchants participating in the merchant acquiring systems on the last day of June 2017.

| 3. |

Inventory |

The Company’s inventory comprised the following category as of March 31, 2018 and June 30, 2017.

| March 31, | June 30, | ||||||

| 2018 | 2017 | ||||||

| Finished goods | $ | 11,808 | $ | 8,020 | |||

| $ | 11,808 | $ | 8,020 |

| 4. |

Settlement assets and settlement obligations |

Settlement assets comprise (1) cash received from the South African government that the Company holds pending disbursement to recipient cardholders of social welfare grants and (2) cash received from customers on whose behalf the Company processes payroll payments that the Company will disburse to customer employees, payroll-related payees and other payees designated by the customer.

Settlement obligations comprise (1) amounts that the Company is obligated to disburse to recipient cardholders of social welfare grants, and (2) amounts that the Company is obligated to pay to customer employees, payroll-related payees and other payees designated by the customer.

The balances at each reporting date may vary widely depending on the timing of the receipts and payments of these assets and obligations.

| 5. |

Fair value of financial instruments |

Fair value of financial instruments

Initial recognition and measurement

Financial instruments are recognized when the Company becomes a party to the transaction. Initial measurements are at cost, which includes transaction costs.

Risk management

The Company manages its exposure to currency exchange, translation, interest rate, customer concentration, credit and equity price and liquidity risks as discussed below.

Currency exchange risk

The Company is subject to currency exchange risk because it purchases inventories that it is required to settle in other currencies, primarily the euro and U.S. dollar. The Company has used forward contracts in order to limit its exposure in these transactions to fluctuations in exchange rates between the South African rand, on the one hand, and the U.S. dollar and the euro, on the other hand.

9

| 5. |

Fair value of financial instruments (continued) |

Fair value of financial instruments (continued)

Risk management (continued)

Translation risk

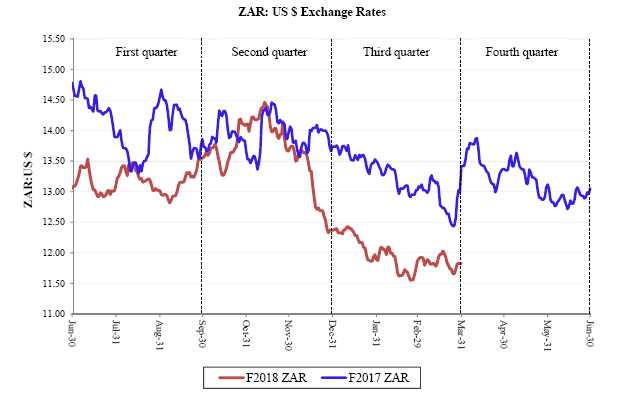

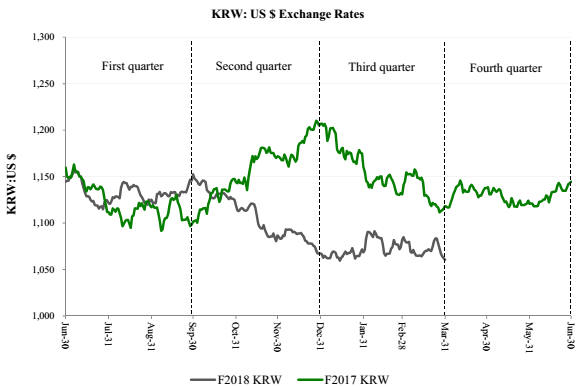

Translation risk relates to the risk that the Company’s results of operations will vary significantly as the U.S. dollar is its reporting currency, but it earns most of its revenues and incurs most of its expenses in ZAR. The U.S. dollar to ZAR exchange rate has fluctuated significantly over the past three years. As exchange rates are outside the Company’s control, there can be no assurance that future fluctuations will not adversely affect the Company’s results of operations and financial condition.

Interest rate risk

As a result of its normal borrowing and lending activities, the Company’s operating results are exposed to fluctuations in interest rates, which it manages primarily through regular financing activities. The Company generally maintains limited investments in cash equivalents and held to maturity investments and has occasionally invested in marketable securities.

Credit risk

Credit risk relates to the risk of loss that the Company would incur as a result of non-performance by counterparties. The Company maintains credit risk policies with regard to its counterparties to minimize overall credit risk. These policies include an evaluation of a potential counterparty’s financial condition, credit rating, and other credit criteria and risk mitigation tools as the Company’s management deems appropriate.

With respect to credit risk on financial instruments, the Company maintains a policy of entering into such transactions only with South African and European financial institutions that have a credit rating of “BB+” (or its equivalent) or better, as determined by credit rating agencies such as Standard & Poor’s, Moody’s and Fitch Ratings.

Microlending credit risk

The Company is exposed to credit risk in its microlending activities, which provide unsecured short-term loans to qualifying customers. The Company manages this risk by performing an affordability test for each prospective customer and assigning a “creditworthiness score”, which takes into account a variety of factors such as other debts and total expenditures on normal household and lifestyle expenses.

Equity price and liquidity risk

Equity price risk relates to the risk of loss that the Company would incur as a result of the volatility in the exchange-traded price of equity securities that it holds and the risk that it may not be able to liquidate these securities. The market price of these securities may fluctuate for a variety of reasons and, consequently, the amount that the Company may obtain in a subsequent sale of these securities may significantly differ from the reported market value.

Liquidity risk relates to the risk of loss that the Company would incur as a result of the lack of liquidity on the exchange on which these securities are listed. The Company may not be able to sell some or all of these securities at one time, or over an extended period of time without influencing the exchange traded price, or at all.

Financial instruments

The following section describes the valuation methodologies the Company uses to measure its significant financial assets and liabilities at fair value.

In general, and where applicable, the Company uses quoted prices in active markets for identical assets or liabilities to determine fair value. This pricing methodology would apply to Level 1 investments. If quoted prices in active markets for identical assets or liabilities are not available to determine fair value, then the Company uses quoted prices for similar assets and liabilities or inputs other than the quoted prices that are observable either directly or indirectly. These investments would be included in Level 2 investments. In circumstances in which inputs are generally unobservable, values typically reflect management’s estimates of assumptions that market participants would use in pricing the asset or liability. The fair values are therefore determined using model-based techniques that include option pricing models, discounted cash flow models, and similar techniques. Investments valued using such techniques are included in Level 3 investments.

10

| 5. |

Fair value of financial instruments (continued) |

Financial instruments (continued)

Asset measured at fair value using significant unobservable inputs – investment in Cell C

The Company's Level 3 asset represents an investment of 75,000,000 class “A” shares in Cell C (Pty) Limited (“Cell C”), a leading mobile telecoms provider in South Africa (refer to Note 6). The Company has designated such shares as available for sale investments. Cell C shares are not listed on an exchange and there is no readily determinable market value for the shares. The Company has developed an adjusted EV/EBITDA multiple valuation model in order to determine the fair value of the Cell C shares. The primary inputs to the valuation model are Cell C’s adjusted EBITDA for the 12 months ended December 31, 2017, of ZAR 3.7 billion ($309.0 million, translated at exchange rates applicable as of March 31, 2018), an EBITDA multiple of 7.20, Cell C’s net external debt of ZAR 8.2 billion ($691.6 million, translated at exchange rates applicable as of March 31, 2018) and a marketability discount of 10% as Cell C is not yet listed. The EBITDA multiple was determined based on an analysis of Cell C’s peer group, which comprises the primary mobile operators (Vodacom and MTN) in the South African marketplace. The fair value of Cell C utilizing the adjusted EV/EBITDA valuation model developed by the Company is sensitive to the following inputs: (i) the Company’s determination of adjusted EBITDA (ii) the EBITDA multiple used and (iii) the marketability discount used. Utilization of different inputs, or changes to these inputs, may result in significant higher or lower fair value measurement.

The fair value of the Cell C shares as of March 31, 2018, represented approximately 15% of the Company’s total assets, including these shares. The Company expects to hold these shares for an extended period of time and it is not concerned with short-term equity price volatility with respect to these shares provided that the underlying business, economic and management characteristics of the company remain sound.

Derivative transactions - Foreign exchange contracts

As part of the Company’s risk management strategy, the Company enters into derivative transactions to mitigate exposures to foreign currencies using foreign exchange contracts. These foreign exchange contracts are over-the-counter derivative transactions. Substantially all of the Company’s derivative exposures are with counterparties that have long-term credit ratings of “BB+” (or equivalent) or better. The Company uses quoted prices in active markets for similar assets and liabilities to determine fair value (Level 2). The Company has no derivatives that require fair value measurement under Level 1 or 3 of the fair value hierarchy. The Company had no outstanding foreign exchange contracts as of March 31, 2018 and June 30, 2017, respectively.

The following table presents the Company’s assets measured at fair value on a recurring basis as of March 31, 2018, according to the fair value hierarchy:

| Quoted price in | Significant | ||||||||||||

| active markets | other | Significant | |||||||||||

| for identical | observable | unobservable | |||||||||||

| assets | inputs | inputs | |||||||||||

| (Level 1) | (Level 2) | (Level 3) | Total | ||||||||||

| Assets | |||||||||||||

| Investment in Cell C | $ | - | $ | - | $ | 206,970 | $ | 206,970 | |||||

| Related to insurance business: | |||||||||||||

| Cash and cash equivalents (included in other long-term assets) | 701 | - | - | 701 | |||||||||

| Fixed maturity investments (included in cash and cash equivalents) | 9,230 | - | - | 9,230 | |||||||||

| Other | - | 40 | - | 40 | |||||||||

| Total assets at fair value | $ | 9,931 | $ | 40 | $ | 206,970 | $ | 216,941 |

11

| 5. |

Fair value of financial instruments (continued) |

Financial instruments (continued)

The following table presents the Company’s assets measured at fair value on a recurring basis as of June 30, 2017, according to the fair value hierarchy:

| Quoted Price | Significant | ||||||||||||

| in Active | Other | Significant | |||||||||||

| Markets for | Observable | Unobservable | |||||||||||

| Identical Assets | Inputs | Inputs | |||||||||||

| (Level 1) | (Level 2) | (Level 3) | Total | ||||||||||

| Assets | |||||||||||||

| Related to insurance business: | |||||||||||||

| Cash and cash equivalents (included in other long-term assets) | $ | 627 | $ | - | $ | - | $ | 627 | |||||

| Fixed maturity investments (included in cash and cash equivalents) | 5,160 | - | - | 5,160 | |||||||||

| Other | - | 37 | - | 37 | |||||||||

| Total assets at fair value | $ | 5,787 | $ | 37 | $ | - | $ | 5,824 |

There have been no transfers in or out of Level 3 during the three and nine months ended March 31, 2018 and 2017, respectively.

Assets and liabilities measured at fair value on a nonrecurring basis

The Company measures its assets at fair value on a nonrecurring basis when they are deemed to be other-than-temporarily impaired. The Company has no liabilities that are measured at fair value on a nonrecurring basis. The Company reviews the carrying values of its assets when events and circumstances warrant and considers all available evidence in evaluating when declines in fair value are other-than-temporary. The fair values of the Company’s assets are determined using the best information available, and may include quoted market prices, market comparables, and discounted cash flow projections. An impairment charge is recorded when the cost of the asset exceeds its fair value and the excess is determined to be other-than-temporary. The Company has not recorded any impairment charges during the reporting periods presented herein.

| 6. |

Equity-accounted investments and other long-term assets |

Equity-accounted investments

The Company’s ownership percentage in its equity-accounted investments as of March 31, 2018 and June 30, 2017, was as follows:

| March 31, | June 30, | ||||||

| 2018 | 2017 | ||||||

| DNI-4PL (Pty) Ltd (“DNI”) | 49% | - | |||||

| Bank Frick & Co AG (“Bank Frick”) | 35% | - | |||||

| Finbond Group Limited (“Finbond”) | 26% | 26% | |||||

| OneFi Limited (formerly KZ One) (“OneFi”) | 25% | 25% | |||||

| SmartSwitch Namibia (Pty) Ltd (“SmartSwitch Namibia”) | 50% | 50% | |||||

| Walletdoc Proprietary Limited (“Walletdoc”) | 20% | 20% |

On July 27, 2017, the Company subscribed for 44,999,999 ordinary A shares in DNI, representing a 45% voting and economic interest in DNI, for a subscription price of ZAR 945.0 million ($72.0 million) in cash. On March 9, 2018, the Company subscribed for an additional 4,000,000 ordinary A shares in DNI for a subscription price of ZAR 89.3 million ($7.5 million), in cash, which increased its voting and economic interest in DNI as of March 31, 2018, to 49%.

On March 9, 2018, the Company agreed to subscribe for an additional 6,000,000 ordinary A shares in DNI for an aggregate subscription price of ZAR 126.0 million ($10.7 million, translated at exchange rates applicable as of March 31, 2018), which will increase its voting and economic interest to 55% in DNI. The subscription is subject to certain conditions, including obtaining South African Competition Commission approval. On March 9, 2018, the Company provided DNI with an interest-free loan of ZAR 126.0 million ($10.6 million) which is repayable at the earlier of June 30, 2018, or within twenty days of the 6,000,000 ordinary A share subscription agreement (i) becoming unconditional, (ii) lapsing because the Competition Commission prohibits the subscription, or (iii) the agreement is cancelled for any reason. The loan is included in accounts receivable, net, as of March 31, 2018, on the Company’s unaudited condensed consolidated balance sheet. As described in Note 10, on March 9, 2018, the Company obtained financing to partially fund the acquisition of 4,000,000 ordinary A DNI shares and to provide the loan to DNI.

12

| 6. |

Equity-accounted investments and other long-term assets (continued) |

Equity-accounted investments (continued)

Under the terms of the July 27, 2017, agreement, the Company agreed to pay to DNI an additional amount of up to ZAR 360.0 million ($30.4 million), in cash, subject to the achievement of certain performance targets by DNI. In connection with the subscription agreements executed in March 2018, the Company agreed to increase the total additional amount from up to ZAR 360.0 million to up to ZAR 380.0 million ($32.1 million) following the purchase of the additional 4,000,000 shares and further agreed to increase the total additional amount from up to ZAR 380.0 million to up to ZAR 400.0 million ($33.8 million) if the Company subscribes for the additional 6,000,000 shares. Therefore the maximum additional amount that is payable is ZAR 400.0 million if all subscriptions are completed. The Company has not accrued for any of this contingent consideration as of March 31, 2018. Net1 SA pledged, among other things, its entire equity interest in DNI as security for the South African facilities described in Note 10. All amounts denominated in ZAR have been translated at exchange rates applicable as of March 31, 2018.

On October 2, 2017, the Company acquired a 30% interest in Bank Frick, a fully licensed bank based in Balzers, Liechtenstein, from the Kuno Frick Family Foundation (“Frick Foundation”) for approximately CHF 39.8 million ($40.9 million) in cash. On February 9, 2018, the Company purchased an additional 5% in Bank Frick from the Frick Foundation for CHF 10.4 million ($11.1 million) and the Frick Foundation contributed approximately CHF 3.8 million ($4.1 million) to Bank Frick to facilitate the development of Bank Frick’s Fintech and blockchain businesses. The Company has an option, exercisable until October 2, 2019, to acquire an additional 35% interest in Bank Frick.

Bank Frick provides a complete suite of banking services, with one of its key strategic pillars being the provision of payment services and funding of financial technology opportunities. Bank Frick holds acquiring licenses from both Visa and MasterCard and operates a branch in London. The Company and Bank Frick have jointly identified several funding opportunities, including for the Company’s card issuing and acquiring and transaction processing activities as well as new opportunities in blockchain and crypto-currencies. The investment in Bank Frick has the potential to provide the Company with a stable, long-term and strategic relationship with a fully-licensed bank.

As of March 31, 2018, the Company owned 205,483,967 shares in Finbond. Finbond is listed on the Johannesburg Stock Exchange and its closing price on March 29, 2018, the last trading day of the quarter, was R4.00 per share. The market value of the Company’s holding in Finbond on March 31, 2018 was ZAR 821.9 million ($69.5 million translated at exchange rates applicable as of March 31, 2018). On July 13, 2017, the Company acquired an additional 3.6 million shares in Finbond for approximately ZAR 11.2 million ($0.8 million). On July 17, 2017, the Company, pursuant to its election, received an additional 4,361,532 shares in Finbond as a capitalization share issue in lieu of a dividend.

On October 7, 2016, the Company provided a loan of ZAR 139.2 million ($10.0 million, translated at the foreign exchange rates applicable on the date of the loan) to Finbond in order to partially finance Finbond’s expansion strategy in the United States. Interest on the loan is payable quarterly in arrears and is based on the London Interbank Offered Rate (“LIBOR”) in effect from time to time plus a margin of 12.00% . The LIBOR rate was 2.31175% on March 29, 2018.

The loan was initially set to mature at the earlier of Finbond concluding a rights offer or February 28, 2017, but the agreement was subsequently amended to extend the repayment date to on or before February 28, 2018, or such later date as may be mutually agreed by the parties in writing. The Company had the right to elect for the loan to be repaid in either Finbond ordinary shares, including through a rights offering, (in accordance with an agreed mechanism) or in cash. The Company is required to make a repayment election within 180 days after the repayment date otherwise the repayment election will automatically default to repayment in ordinary shares. Finbond undertook to perform all necessary steps reasonably required to effect the issuance of shares to settle the repayment of the loan if that option is elected by the Company.

In March 2018, the parties amended the agreement to extend the repayment date from February 28, 2018 to August 31, 2018, and to finalize certain matters related to the rights offering mechanism and determining the maximum number of shares that Finbond would issue to parties participating in a rights offering. On March 23, 2018, Finbond publicly announced that it had commenced a rights offering process and that the proceeds of the offering would be used to settle certain loans, including the loan due to the Company. The loan is included in equity accounted investments as of March 31, 2018, and accounts receivable, net, as of June 30, 2017, on the Company’s unaudited condensed consolidated balance sheet. The rights offering closed on April 20, 2018. The Company agreed to underwrite the Finbond rights offer up to an amount of 55,585,514 shares and from April 23, 2018, now owns 261,069,481 Finbond shares, representing approximately 27.6% of Finbond’s issued and outstanding ordinary shares after the rights offering.

The Company provided a credit facility of up to $10 million in the form of convertible debt to OneFi, of which $2 million was drawn as of March 31, 2018 and June 30, 2017. In April 2018, an additional $1.0 million was drawn under the credit facility.

13

| 6. |

Equity-accounted investments and other long-term assets (continued) |

Equity-accounted investments (continued)

Summarized below is the movement in equity-accounted investments during the nine months ended March 31, 2018:

| Bank | ||||||||||||||||

| DNI | Frick | Finbond | Other(1) | Total | ||||||||||||

| Investment in equity: | ||||||||||||||||

| Balance as of June 30, 2017 | $ | - | $ | - | $ | 18,961 | $ | 6,742 | $ | 25,703 | ||||||

| Acquisition of shares | 79,541 | 51,949 | 1,941 | - | 133,431 | |||||||||||

| Stock-based compensation | - | - | (207 | ) | - | (207 | ) | |||||||||

| Comprehensive income (loss): | 5,202 | 975 | 874 | 111 | 7,162 | |||||||||||

| Other comprehensive loss | - | - | (227 | ) | - | (227 | ) | |||||||||

| Equity accounted earnings (loss) | 5,202 | 975 | 1,101 | 111 | 7,389 | |||||||||||

| Share of net income (loss) | 6,868 | 1,234 | 1,931 | 111 | 10,144 | |||||||||||

| Amortization of acquired intangible assets | (2,315 | ) | (342 | ) | - | - | (2,657 | ) | ||||||||

| Deferred taxes on acquired intangible assets | 649 | 83 | - | - | 732 | |||||||||||

| Dilution resulting from corporate transactions | - | - | (830 | ) | - | (830 | ) | |||||||||

| Dividends received | (1,765 | ) | (1,946 | ) | (1,096 | ) | (400 | ) | (5,207 | ) | ||||||

| Foreign currency adjustment(2) | 7,917 | 639 | 2,127 | (489 | ) | 10,194 | ||||||||||

| Balance as of March 31, 2018 | $ | 90,895 | $ | 51,617 | $ | 22,600 | $ | 5,964 | $ | 171,076 | ||||||

| Investment in loans: | ||||||||||||||||

| Balance as of June 30, 2017 | $ | - | $ | - | $ | - | $ | 2,159 | $ | 2,159 | ||||||

| Transfer from accounts receivable, net | - | - | 11,772 | - | 11,772 | |||||||||||

| Foreign currency adjustment(2) | - | - | - | 16 | 16 | |||||||||||

| Balance as of March 31, 2018 | $ | - | $ | - | $ | 11,772 | $ | 2,175 | $ | 13,947 | ||||||

| Equity | Loans | Total | ||||||||||||||

| Carrying amount as of: | ||||||||||||||||

| June 30, 2017 | $ | 25,703 | $ | 2,159 | $ | 27,862 | ||||||||||

| March 31, 2018 | $ | 171,076 | $ | 13,947 | $ | 185,023 |

(1) Includes OneFi, SmartSwitch Namibia and Walletdoc;

(2) The foreign currency adjustment represents the effects of the fluctuations of the South African rand, Nigerian naira and Namibian dollar, against the U.S. dollar on the carrying value.

Other long-term assets

Summarized below is the breakdown of other long-term assets as of March 31, 2018, and June 30, 2017:

| March 31, | June 30, | ||||||

| 2018 | 2017 | ||||||

| Investment in 15% of Cell C (Pty) Limited (“Cell C”), at fair value | $ | 206,970 | $ | - | |||

| Investment in 12% of One MobiKwik Systems Private Limited (“MobiKwik”), at cost | 28,391 | 26,317 | |||||

| Total equity investments | 235,361 | 26,317 | |||||

| Investment in 7.625% of Cedar Cellular Investment 1 (RF) (Pty) Ltd 8.625% notes due in 2022 | 9,769 | - | |||||

| Total held to maturity investments | 9,769 | - | |||||

| Long-term portion of payments to agents in South Korea amortized over the contract period | 19,447 | 17,290 | |||||

| Policy holder assets under investment contracts (Note 8) | 701 | 627 | |||||

| Reinsurance assets under insurance contracts Note 8) | 224 | 191 | |||||

| Other long-term assets | 5,683 | 5,271 | |||||

| Total other long-term assets | $ | 271,185 | $ | 49,696 |

On August 2, 2017, the Company, through its subsidiary, Net1 Applied Technologies South Africa Proprietary Limited (“Net1 SA”), purchased 75,000,000 class “A” shares of Cell C for an aggregate purchase price of ZAR 2.0 billion ($151.0 million) in cash. The Company funded the transaction through a combination of cash and the facilities described in Note 14 to the Company’s audited consolidated financial statements included in its Annual Report on Form 10-K for the year ended June 30, 2017. Net1 SA has pledged, among other things, its entire equity interest in Cell C as security for the South African facilities described in Note 10 used to partially fund the acquisition of Cell C.

14

| 6. |

Equity-accounted investments and other long-term assets (continued) |

Other long-term assets (continued)

The Company has signed a subscription agreement with MobiKwik, which is India’s largest independent mobile payments network, with over 65 million users and two million merchants. Pursuant to the subscription agreement, the Company agreed to make an equity investment of up to $40.0 million in MobiKwik over a 24 month period. The Company made an initial $15.0 million investment in August 2016 and a further $10.6 million investment in June 2017, under this subscription agreement. As of June 30, 2017, the Company owned approximately 13.5% of MobiKwik. In August 2017, MobiKwik raised additional funding through the issuance of additional shares to a new shareholder at a 90% premium to the Company’s investments and the Company’s percentage ownership was diluted to 12.0%, which also represents the Company’s ownership as of March 31, 2018. In addition, through a technology agreement, the Company’s Virtual Card technology will be integrated across all MobiKwik wallets in order to provide ubiquity across all merchants in India, and as part of the Company’s continued strategic relationship, a number of our other products including our digital banking platform, are expected to be deployed by MobiKwik over the next year.

In December 2017, the Company purchased, for cash, $9.0 million of notes, with a face value of $20.5 million, issued by Cedar Cellular Investment 1 (RF) (Pty) Ltd (“Cedar Cellular”), a Cell C shareholder, representing 7.625% of the issuance. The investment in the notes was made in connection with the Cell C investment discussed above. The notes bear interest semi-annually at 8.625% per annum on the face value and interest is payable in cash or deferred, at Cedar Cellular’s election, for payment on the maturity date. The notes mature on August 2, 2022. The notes are secured by all of Cedar Cellular’s investment in Cell C (59,000,000 class “A” shares) and the fair value of the Cell C shares pledged exceeds the carrying value of the notes as of March 31, 2018. The notes are listed on The International Stock Exchange. The Company has elected to treat the investment in the notes as held to maturity securities.

Summarized below are the components of the Company’s available for sale and held to maturity investments as of March 31, 2018:

| Unrealized | Unrealized | ||||||||||||

| holding | holding | Carrying | |||||||||||

| Cost basis | gains | losses | value | ||||||||||

| Available for sale: | |||||||||||||

| Investment in Cell C | $ | 169,127 | $ | 37,843 | $ | - | $ | 206,970 | |||||

| Held to maturity: | |||||||||||||

| Investment in Cedar Cellular notes | 9,000 | 769 | - | 9,769 | |||||||||

| Total | $ | 178,127 | $ | 38,612 | $ | - | $ | 216,739 |

The Company had no available for sale or held to maturity investments as of June 30, 2017.

Contractual maturities of held to maturity investments

Summarized below are the contractual maturities of the Company’s held to maturity investment as of March 31, 2018:

| Cost | Estimated | ||||||

| basis | fair value | ||||||

| Due in one year or less | $ | - | $ | - | |||

| Due in one year through five years | 9,000 | 9,769 | |||||

| Due in five years through ten years | - | - | |||||

| Due after ten years | - | - | |||||

| Total | $ | 9,000 | $ | 9,769 |

| 7. |

Goodwill and intangible assets, net |

Goodwill

Summarized below is the movement in the carrying value of goodwill for the nine months ended March 31, 2018:

| Accumulated | Carrying | |||||||||

| Gross value | impairment | value | ||||||||

| Balance as of June 30, 2017 | $ | 188,833 | $ | - | $ | 188,833 | ||||

| Impairment of goodwill | - | (19,865 | ) | (19,865 | ) | |||||

| Foreign currency adjustment(1) | 13,566 | - | 13,566 | |||||||

| Balance as of March 31, 2018 | $ | 202,399 | $ | (19,865 | ) | $ | 182,534 |

(1) – Represents the effects of the fluctuations of the South African rand, euro and the Korean won, against the U.S. dollar on the carrying value.

15

| 7. |

Goodwill and intangible assets, net (continued) |

Goodwill (continued)

Goodwill has been allocated to the Company’s reportable segments as follows:

| South | Financial | ||||||||||||

| African | International | inclusion and | |||||||||||

| transaction | transaction | applied | Carrying | ||||||||||

| processing | processing | technologies | value | ||||||||||

| Balance as of June 30, 2017 | $ | 23,131 | $ | 140,570 | $ | 25,132 | $ | 188,833 | |||||

| Impairment of goodwill | - | (19,865 | ) | - | (19,865 | ) | |||||||

| Foreign currency adjustment(1) | 2,404 | 9,155 | 2,007 | 13,566 | |||||||||

| Balance as of March 31, 2018 | $ | 25,535 | $ | 129,860 | $ | 27,139 | $ | 182,534 |

(1) – Represents the effects of the fluctuations of the South African rand, euro and the Korean won, against the U.S. dollar on the carrying value.

Impairment loss

The Company assesses the carrying value of goodwill for impairment annually, or more frequently, whenever events occur and circumstances change indicating potential impairment. The Company performs its annual impairment test as at June 30 of each year. During the three and nine months ended March 31, 2018, the Company recognized an impairment loss of approximately $19.9 million related to goodwill allocated to the Masterpayment business within its international transaction processing operating segment as a result of changes to the operating model of Masterpayment. During the second quarter of fiscal 2018, the Company re-evaluated the operating performance and ongoing viability of Masterpayment’s working capital financing and supply chain solutions offering and determined to exit this portion of its business. While the Company believed that it could scale this offering in the medium to long-term by focusing on customers and industries outside Masterpayment’s initial target market, this standalone offering did not fit the Company’s strategy of providing payment solutions and working capital to small and medium-sized merchants. In order to focus on the Company’s stated international strategy, the Company decided to wind-down the traditional working capital finance book issued to non-payment solutions customers. During the third quarter of fiscal 2018, the Company evaluated Masterpayment’s business strategy and following the wind-down referred to above, it has determined that Masterpayment is unlikely to deliver the financial results or cash flows previously anticipated. The Company and two of Masterpayment’s senior managers have agreed, by mutual consent, that with effect from the end of March 2018, the managers terminated their employment with Masterpayment in order to dedicate themselves to new professional tasks.

In order to determine the amount of goodwill impairment, the estimated fair value of the Company’s Masterpayment business was allocated to the individual fair value of the assets and liabilities of Masterpayment as if it had been acquired in a business combination, which resulted in the implied fair value of the goodwill. The allocation of the fair value of Masterpayment required the Company to make a number of assumptions and estimates about the fair value of assets and liabilities where the fair values were not readily available or observable.

A further deterioration in the international transaction processing operating segment, or in any other of the Company’s businesses, may lead to additional impairments in future periods.

16

| 7. |

Goodwill and intangible assets, net (continued) |

Intangible assets, net

Carrying value and amortization of intangible assets

Summarized below is the carrying value and accumulated amortization of the intangible assets as of March 31, 2018 and June 30, 2017:

| As of March 31, 2018 | As of June 30, 2017 | ||||||||||||||||||

| Gross | Net | Gross | Net | ||||||||||||||||

| carrying | Accumulated | carrying | carrying | Accumulated | carrying | ||||||||||||||

| value | amortization | value | value | amortization | value | ||||||||||||||

| Finite-lived intangible assets: | |||||||||||||||||||

| Customer relationships | $ | 106,620 | $ | (78,746 | ) | $ | 27,874 | $ | 99,209 | $ | (65,595 | ) | $ | 33,614 | |||||

| Software and unpatented | |||||||||||||||||||

| technology | 35,265 | (34,242 | ) | 1,023 | 33,273 | (31,112 | ) | 2,161 | |||||||||||

| FTS patent | 3,240 | (3,240 | ) | - | 2,935 | (2,935 | ) | - | |||||||||||

| Exclusive licenses | 4,506 | (4,506 | ) | - | 4,506 | (4,506 | ) | - | |||||||||||

| Trademarks | 7,493 | (5,799 | ) | 1,694 | 6,972 | (4,759 | ) | 2,213 | |||||||||||

| Total finite-lived intangible assets | 157,124 | (126,533 | ) | 30,591 | 146,895 | (108,907 | ) | 37,988 | |||||||||||

| Indefinite-lived intangible assets: | |||||||||||||||||||

| Financial institution license | 837 | - | 837 | 776 | - | 776 | |||||||||||||

| Total indefinite-lived intangible assets | 837 | - | 837 | 776 | - | 776 | |||||||||||||

| Total intangible assets | $ | 157,961 | $ | (126,533 | ) | $ | 31,428 | $ | 147,671 | $ | (108,907 | ) | $ | 38,764 | |||||

Aggregate amortization expense on the finite-lived intangible assets for the three months ended March 31, 2018 and 2017, was approximately $3.0 million and $3.7 million, respectively. Aggregate amortization expense on the finite-lived intangible assets for the nine months ended March 31, 2018 and 2017, was approximately $8.8 million and $10.2 million, respectively.

Future estimated annual amortization expense for the next five fiscal years and thereafter, assuming exchange rates that prevailed on March 31, 2018, is presented in the table below. Actual amortization expense in future periods could differ from this estimate as a result of acquisitions, changes in useful lives, exchange rate fluctuations and other relevant factors.

| Fiscal 2018 | $ | 12,915 | ||

| Fiscal 2019 | 11,445 | |||

| Fiscal 2020 | 10,727 | |||

| Fiscal 2021 | 4,620 | |||

| Fiscal 2022 | 85 | |||

| Thereafter | 345 | |||

| Total future estimated annual amortization expense | $ | 40,137 |

| 8. |

Reinsurance assets and policyholder liabilities under insurance and investment contracts |

Reinsurance assets and policyholder liabilities under insurance contracts

Summarized below is the movement in reinsurance assets and policyholder liabilities under insurance contracts during the nine

| Reinsurance | Insurance | ||||||

| assets(1) | contracts(2) | ||||||

| Balance as of June 30, 2017 | $ | 191 | $ | (1,611 | ) | ||

| Increase in policyholder benefits under insurance contracts | 1,276 | (7,881 | ) | ||||

| Claims and policyholders’ benefits under insurance contracts . | (1,263 | ) | 7,691 | ||||

| Foreign currency adjustment(3) | 20 | (168 | ) | ||||

| Balance as of March 31, 2018 | $ | 224 | $ | (1,969 | ) |

(1) Included in other long-term

assets.

(2) Included in other long-term

liabilities.

(3) Represents the effects of the

fluctuations between the ZAR against the U.S. dollar.

17

| 8. |

Reinsurance assets and policyholder liabilities under insurance and investment contracts (continued) |

Reinsurance assets and policyholder liabilities under insurance contracts (continued)

The Company has agreements with reinsurance companies in order to limit its losses from certain insurance contracts, however, if the reinsurer is unable to meet its obligations, the Company retains the liability.

The Company determines its reserves for policy benefits under its life insurance products using a model which estimates claims incurred that have not been reported at the balance sheet date. This model includes best estimate assumptions of experience plus prescribed margins, as required in the markets in which these products are offered, namely South Africa. The best estimate assumptions include those assumptions related to mortality, morbidity and claim reporting delays, and the main assumptions used to calculate the reserve for policy benefits include (i) mortality and morbidity assumptions reflecting the company’s most recent experience and (ii) claim reporting delays reflecting Company specific and industry experience. The values of matured guaranteed endowments were increased by late payment interest (net of the asset management fee and allowance for tax on investment income).

Assets and policyholder liabilities under investment contracts

Summarized below is the movement in assets and policyholder liabilities under investment contracts during the nine months ended March 31, 2018:

| Investment | |||||||

| Assets(1) | contracts(2) | ||||||

| Balance as of June 30, 2017 | $ | 627 | $ | (627 | ) | ||

| Increase in policyholder benefits under investment contracts | 9 | (9 | ) | ||||

| Foreign currency adjustment(3) | 65 | (65 | ) | ||||

| Balance as of March 31, 2018 | $ | 701 | $ | (701 | ) |

(1) Included in other long-term

assets.

(2) Included in other long-term

liabilities.

(3) Represents the effects of the

fluctuations between the ZAR against the U.S. dollar.

The Company does not offer any investment products with guarantees related to capital or returns.

| 9. |

Short-term credit facilities |

Summarized below are the Company’s available short-term facilities and the amounts utilized as of March 31, 2018 and June 30, 2017, all amounts below were translated at the exchange rates applicable as of the date presented:

| March 31, 2018 | June 30, 2017 | ||||||||||||

| Available | Utilized | Available | Utilized | ||||||||||

| United States: | |||||||||||||

| Bank Frick(1) | $ | 10,000 | $ | 3,400 | $ | - | $ | - | |||||

| Europe: | |||||||||||||

| Bank Frick(1) | - | - | 66,579 | 16,579 | |||||||||

| South Africa: | |||||||||||||

| Nedbank Limited | 33,800 | 9,136 | 30,600 | 10,000 | |||||||||

| Overdraft facility(1) | 21,100 | - | 19,109 | - | |||||||||

| Indirect and derivative facilities (Note 18) | $ | 12,700 | $ | 9,136 | $ | 11,491 | $ | 10,000 | |||||

(1) Utilized amount included in short-term facilities on the unaudited condensed consolidated balance sheets.

United States

On January 29, 2018, the Company obtained a $10.0 million overdraft facility from Bank Frick. The interest rate on the facilities is 4.50% plus 3-month US Dollar LIBOR and interest is payable quarterly commencing on March 31, 2018. The 3-month US Dollar LIBOR rate was 2.31175% on March 29, 2018. The facility has no fixed term, however, it may be terminated by either party with six weeks written notice. The facility is secured by a pledge of the Company’s investment in Bank Frick. As of March 31, 2018, the Company had utilized approximately $3.4 million of this facility.

18

| 9. |

Short-term credit facilities (continued) |

Europe

The Company had obtained EUR 40.0 million and CHF 20 million revolving overdraft facilities from Bank Frick during the year ended June 30, 2017. The Company assigned all claims against amounts due from Masterpayment customers, which have been financed from the CHF 20 million facility, plus all secondary rights and preferential rights as collateral for this facility to Bank Frick. Masterpayment was required to open a primary business account with Bank Frick and this account was pledged to Bank Frick as collateral for the EUR 40 million facility. Net1 stood as guarantor for both of these facilities. The facilities were settled in full in January 2018 and were terminated in February 2018. As of June 30, 2017, the Company had utilized approximately CHF 15.9 million ($16.6 million) of the CHF 20 million facility and had not utilized any of the EUR 40 million facility. All amounts have been translated at exchange rates applicable as of June 30, 2017.

South Africa

The aggregate amount of the Company’s short-term South African credit facility with Nedbank Limited was ZAR 400 million ($33.8 million) and consists of (i) a primary amount of up to ZAR 200 million ($16.9 million, and (ii) a secondary amount of up to ZAR 200 million ($16.9 million). The primary amount comprises an overdraft facility of up to ZAR 50 million ($4.2 million) and indirect and derivative facilities of up to ZAR 150 million ($12.7 million), which include letters of guarantee, letters of credit and forward exchange contracts. All amounts denominated in ZAR and translated at exchange rates applicable as of March 31, 2018.

As of March 31, 2018, the interest rate on the overdraft facility was 8.85% . The Company has ceded its investment in Cash Paymaster Services Proprietary Limited (“CPS”), a South African subsidiary, as security for its repayment obligations under the facility. A commitment fee of 0.35% per annum is payable on the monthly unutilized amount of the overdraft portion of the short-term facility. The Company is required to comply with customary non-financial covenants, including, without limitation, covenants that restrict its ability to dispose of or encumber its assets, incur additional indebtedness or engage in certain business combinations.

As of each of March 31, 2018 and June 30, 2017, respectively, the Company had not utilized any of its overdraft facility. As of March 31, 2018, the Company had utilized approximately ZAR 108.0 million ($9.1 million, translated at exchange rates applicable as of March 31, 2018) of its ZAR 150 million indirect and derivative facilities to enable the bank to issue guarantees, including stand-by letters of credit, in order for the Company to honor its obligations to third parties requiring such guarantees (refer to Note 18). As of June 30, 2017, the Company had utilized approximately ZAR 130.5 million ($10.0 million, translated at exchange rates applicable as of June 30, 2017) of its ZAR 150 million indirect and derivative facilities.

| 10. |

Long-term borrowings |

South Africa

The Company’s South African long-term facility agreement is described in Note 14 to the Company’s audited consolidated financial statements included in its Annual Report on Form 10-K for the year ended June 30, 2017. As of March 31, 2018, $75.5 million was outstanding under the Company’s South African long-term facility agreement, and the carrying amount of the long-term borrowings approximated fair value. On March 8, 2018, the Company amended its South African long-term facility to include an additional term loan of up to ZAR 210.0 million (approximately $17.8 million translated at exchange rates applicable as of March 31, 2018). This loan matures on March 31, 2020. Interest on the ZAR 210 million term loan is payable on the last day of March, June, September and December of each year and on the final maturity date based on the Johannesburg Interbank Agreed Rate (“JIBAR”) in effect from time to time plus a margin of 2.75% . The JIBAR has been set at 6.867% for the period to June 29, 2018, in respect of the loans provided under the South African long-term facilities agreement.

On July 26, 2017, the Company utilized ZAR 1.25 billion (approximately $92.2 million) of its South African long-term facility to partially fund the acquisition of 15% of Cell C. On March 9, 2018, the Company utilized ZAR 84.0 million (approximately $7.1 million) of its new ZAR 210 million South African long-term facility to partially fund the acquisition of a further 4.0% in DNI and the balance of the facility to extend a ZAR 126.0 million (approximately $10.6 million) loan to DNI (refer to Note 6).

Principal repayments of the facilities are due in twelve quarterly installments commencing on September 29, 2017 and the Company has made scheduled repayments of ZAR 562.5 million ($44.4 million) during the nine months ended March 31, 2018. The next scheduled principal payment will be made on June 29, 2018. The amount to be paid will be either (i) ZAR 324.0 million ($27.4 million) if the Company is unable to proceed with its acquisition of a further 6% in DNI or (ii) ZAR 213.8 million ($18.1 million) if the Company concludes its investment, all amounts translated at exchange rates applicable as of March 31, 2018.

The Company paid a non-refundable origination fee of approximately ZAR 6.3 million ($0.6 million) in August 2017 and a non-refundable origination fee of ZAR 2.4 million ($0.2 million) in March 2018. Interest expense incurred during the three and nine months ended March 31, 2018, was $1.9 million and $5.5 million, respectively. During the three and nine months ended March 31, 2018, $0.1 million and $0.3 million, respectively, of prepaid facility fees were amortized.

19

| 10. |

Long-term borrowings (continued) |

South Korea

The South Korean senior secured loan facility is described in Note 14 to the Company’s audited consolidated financial statements included in its Annual Report on Form 10-K for the year ended June 30, 2017. On July 29, 2017, the Company utilized approximately KRW 0.3 billion ($0.3 million) of its Facility C revolving credit facility under the Company’s South Korean long-term facility agreement to pay interest due on the Company’s South Korean senior secured loan facility. On October 20, 2017, the Company made an unscheduled repayment of $16.6 million and settled the full outstanding balance, including interest, related to these borrowings.

Interest expense incurred during the three months ended March 31, 2017, was $0.3 million. Interest expense incurred during the nine months ended March 31, 2018 and 2017, was $0.4 million and $0.9 million, respectively. Prepaid facility fees amortized during the three months ended March 31, 2017, was $0.03 million. Prepaid facility fees amortized during the nine months ended March 31, 2018 and 2017, was $0.1 million and $0.09 million, respectively.

| 11. |

Capital structure |

The following table presents a reconciliation between the number of shares, net of treasury, presented in the unaudited condensed consolidated statement of changes in equity during the nine months ended March 31, 2018 and 2017, respectively, and the number of shares, net of treasury, excluding non-vested equity shares that have not vested during the nine months ended March 31, 2018 and 2017, respectively:

| March 31, | March 31, | ||||||

| 2018 | 2017 | ||||||

| Number of shares, net of treasury: | |||||||

| Statement of changes in equity | 56,855,187 | 57,590,085 | |||||

| Less: Non-vested equity shares that have not vested (Note 13) | (934,673 | ) | (904,356 | ) | |||

| Number of shares, net of treasury excluding non-vested equity shares that have not vested | 55,920,514 | 56,685,729 |

Common stock repurchases

Executed under share repurchase authorizations

The Company did not repurchase any of its shares during the three and nine months ended March 31, 2018, or during the three months ended March 31, 2017.