UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

| |

| For the fiscal year ended |

| OR |

| |

| For the transition period from __________ to __________ |

Commission File Number

PETMED EXPRESS, INC.

(Exact name of registrant as specified in its charter)

| | | |

| (State or other jurisdiction of | (IRS Employer | |

| incorporation or organization) | Identification No.) | |

| | ||

| (Address of principal executive offices) (Zip Code) | ||

| Registrant’s telephone number, including area code: ( | ||

| Securities registered pursuant to Section 12(b) of the Act: | ||

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Common Stock, PETS $.001 Par value per share

| The (NASDAQ Global Select Market) | |

| Securities registered under Section 12(g) of the Act: | ||

| NONE | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | ||

| Non-accelerated filer | ☐ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

The aggregate market value of the registrant’s Common Stock held by non-affiliates of the registrant as of September 30, 2021, the last business day of the registrant’s most recently completed second fiscal quarter, was $

The number of shares of the registrant’s Common Stock outstanding as of May 24, 2022, was

DOCUMENTS INCORPORATED BY REFERENCE

Information to be set forth in our Proxy Statement relating to our 2022 Annual Meeting of Stockholders to be held on July 28, 2022, is incorporated by reference in Items 10, 11, 12, 13, and 14 of Part III of this report.

PETMED EXPRESS, INC.

2022 Annual Report on Form 10-K

TABLE OF CONTENTS

Page

| PART I | 1 | |

| Item 1. | Business | 1 |

| Item 1A. | Risk Factors | 7 |

| Item 1B. | Unresolved Staff Comments | 14 |

| Item 2 | Properties | 14 |

| Item 3. | Legal Proceedings | 14 |

| Item 4. | Mine Safety Disclosures | 14 |

| PART II | 15 | |

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 15 |

| Item 6. | [Reserved] | 17 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 18 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 27 |

| Item 8. | Financial Statements and Supplementary Data | 28 |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 48 |

| Item 9A. | Controls and Procedures | 48 |

| Item 9B. | Other Information | 48 |

| Item 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | 48 |

| PART III | 49 | |

| Item 10. | Directors, Executive Officers, and Corporate Governance | 49 |

| Item 11. | Executive Compensation | 49 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 49 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 49 |

| Item 14. | Principal Accountant Fees and Services | 49 |

| PART IV | 50 | |

| Item 15. | Exhibit and Financial Statement Schedules | 50 |

| Item 16. | Form 10-K Summary | 51 |

| SIGNATURES | 52 | |

PART I

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

Certain information in this Annual Report on Form 10-K includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (“Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (“Exchange Act”). You can identify these forward-looking statements by the words "believes," "intends," "expects," "may," "will," "should," "plan," "projects," "contemplates," "intends," "budgets," "predicts," "estimates," "anticipates," or similar expressions. These statements are based on our beliefs, as well as assumptions we have used based upon information currently available to us. Because these statements reflect our current views concerning future events, these statements involve risks, uncertainties, and assumptions. Actual future results may differ significantly from the results discussed in the forward-looking statements. Factors that might cause such differences include, but are not limited to, those discussed in Part I, Item 1A of this Annual Report on Form 10-K under the heading “Risk Factors.” A reader, whether investing in our common stock or not, should not place undue reliance on these forward-looking statements, which apply only as of the date of this Annual Report on Form 10-K. The Company assumes no obligation to revise or update any forward-looking statements for any reason, except as required by law.

When used in this Annual Report on Form 10-K, "PetMed Express," "1-800-PetMeds," “PetMeds,” "PetMed," “PetMeds.com,” "PetMed Express.com," "the Company," "we," "our," and "us" refers collectively to PetMed Express, Inc. and its wholly owned subsidiaries.

ITEM 1. BUSINESS

General

PetMed Express, Inc. and subsidiaries, d/b/a PetMeds®, is a leading nationwide pet pharmacy. The Company markets prescription and non-prescription pet medications, and other health products and supplies for dogs, cats, and horses direct to the consumer. The Company offers consumers an attractive alternative for obtaining pet medications in terms of convenience, price, speed of delivery, and valued customer service.

The Company markets its products through national advertising campaigns, which aim to increase the recognition of the “PetMeds” brand name, increase traffic on its website at www.petmeds.com, acquire new customers, and maximize repeat purchases. Virtually all of the Company’s sales are to residents in the United States. Our fiscal year end is March 31, our executive offices are currently located at 420 South Congress Avenue, Delray Beach, Florida 33445, and our telephone number is (561) 526-4444.

Our Products

We offer a broad selection of products for dogs, cats, and horses. Our current product line contains approximately 3,000 SKUs of the most popular pet medications, health products, and supplies. These products include a majority of the well-known brands of pet medications. Generally, our prices are competitive with the prices for medications charged by veterinarians, online retailers and other retailers. We also offer additional pet supplies on our website for sale, which are drop shipped to our customers by third parties. These pet supplies include: food, beds, crates, stairs, and other popular pet supplies. We research new products, and regularly select new products or the latest generation of existing products to become part of our product selection. In addition, we also refine our current products to respond to changing consumer-purchasing habits. Our website is designed to give us the flexibility to change featured products or promotions. Our product line provides customers with a wide variety of selections across the most popular health categories for dogs, cats, and horses. Our current products include:

Non-Prescription Medications (OTC) and supplies: Flea and tick control products, bone and joint care products, vitamins, treats, nutritional supplements, hygiene products, and supplies.

Prescription Medications (Rx): Heartworm and flea and tick preventatives, arthritis, dermatitis, thyroid, diabetes, pain medications, heart/blood pressure, and other specialty medications, as well as generic substitutes.

Sales

We offer our products through two main sales channels: (1) the Internet through our website and mobile app, and (2) the telephone contact center through our toll-free number. We have designed our website and mobile application to provide a convenient, cost-effective, and informative shopping experience that encourages consumers to purchase products important for a pet’s health and quality of life. We believe that these channels allow us to increase the visibility of our brand name and provide our customers with increased shopping flexibility and excellent service.

Internet

We seek to combine our product selection and pet health information with the shopping ease of the Internet to deliver a convenient and personalized shopping experience. Our website offers health and nutritional product selections for dogs, cats, and horses, and relevant editorial and easily obtainable or retrievable resource information. Customers can search our website for products and access resources on a variety of information on dogs, cats, and horses. Customers can shop at our website by category, product line, individual product, or symptom. We attracted approximately 28 million visits to our website (including our mobile app) during fiscal 2022, approximately 8.5% of those visits resulted in an order, and our website generated approximately 84% of our total sales for the same time period. On our website pet owners have access to health information covering pets’ behavior and illnesses, and natural and pharmaceutical remedies specifically for a pet’s problem. The pet education content on our main website is periodically updated with the latest research for pet owners. As part of our multichannel strategy, we also offer mobile versions of our website (www.petmeds.com) and an application for mobile phones, tablets, and other devices. Our website and mobile application features include: AutoShip & Save subscription (“AutoShip”); “ask-the-vet”; live web chat; easy refill medication reminders; local veterinarian finder; and express checkout to provide our customers with fast, easy, and helpful service from their mobile devices.

In July 2021 we launched the new AutoShip program on our website. AutoShip is a new convenient way for our loyal customer base to have future pet medication orders delivered directly to them without the need to place an order each time. Currently, approximately 37% of our sales were generated via our AutoShip program in the month of March. The Company has set a goal of generating approximately 50% of its sales via the AutoShip program in FY 2023.

Telephone Contact Center

Our customer care representatives receive and process inbound and outbound customer calls, facilitate our live web chat, and process customer e-mails. Our telephone system is equipped with certain features including pop-up screens and call blending capabilities that give us the ability to efficiently utilize our customer care representatives’ time, providing excellent customer care, service, and support. Our customer care representatives receive a base salary and are rewarded with commissions for sales, and bonuses and other awards for achieving certain quality goals.

Our Customers

Approximately 2.0 million customers have purchased from us within the last two years. We attracted approximately 263,000 and 443,000 new customers in fiscal 2022 and 2021, respectively. Our customers are located throughout the United States, with approximately 50% of customers residing in California, Florida, Texas, New York, Pennsylvania, North Carolina, Georgia, and Virginia. Our primary focus has been on retail customers and the average purchase was approximately $93 and $89 for fiscal 2022 and fiscal 2021, respectively.

Marketing

The goal of our marketing strategy is to build brand recognition, increase customer traffic, add new customers, build strong customer loyalty, maximize reorders, and develop incremental revenue opportunities. We have an integrated marketing campaign that includes digital marketing, television advertising, and direct mail/print and e-mail.

Digital Marketing

We advertise and market our products primarily online. We make our brand available to Internet consumers by purchasing targeted keywords and achieving prominent placement on the top search engines and search engine networks. We utilize Internet display and video advertisements, social media, and comparison shopping, and we are also members of an affiliate program with merchant clients and affiliate websites.

Television Advertising

Our television advertising is designed to build brand equity, create brand awareness, and generate initial purchases of products via the telephone and the Internet. Our television commercials typically focus on our ability to rapidly deliver to customers the same medications offered by veterinarians. We believe that television advertising is particularly effective and instrumental in building brand awareness. Our most current television commercial, airing nationally, speaks to pet owners about the savings and convenience of purchasing the same exact pet medications from PetMeds.

Direct Mail/Print and E-mail

We use direct mail/print and e-mail to acquire new customers and to remind our existing customers to reorder.

Operations

Order Processing

Our website allows customers to easily browse and purchase all of our products online. Our website is designed to be fast, secure, and easy to use with order and shipping confirmations, and with online order tracking capabilities. We provide our customers with toll-free telephone access to our customer care representatives. Our call center generally operates from 7:00 AM to 11:00 PM, Monday through Thursday, 7:00 AM to 9:00 PM on Friday, 9:00 AM to 6:00 PM on Saturday, and 9:00 AM to 5:00 PM on Sunday, Eastern Time. The process of customers purchasing products from PetMeds consists of a few simple steps. A customer first places an order online or by calling our toll-free telephone number. The following information is needed to process prescription orders: pet information, prescription information, and the veterinarian’s name and phone number. This information is entered into our order process system. Then our pharmacists and pharmacy technicians verify all prescriptions. The order process system checks for the verification for prescription medication orders and a valid payment method for all orders. Verified orders are then sent to our fulfillment center, where items are picked, and then shipped via the United States Postal Service and United Parcel Service. Our customers enjoy the convenience of rapid home delivery, with the majority of all orders being shipped within 24 hours of ordering.

Customer Care and Support

We believe that a high level of customer care and support is critical in retaining and expanding our customer base. Customer care representatives participate in ongoing training programs under the supervision of our training managers. These training sessions include a variety of topics such as product knowledge, computer usage, customer service tips, and the relationship between our Company and veterinarians. Our customer care representatives respond to customers’ e-mails, calls, and live web chats that are related to products, order status, prices, and shipping. We believe our customer care representatives are a valuable source of feedback regarding customer satisfaction.

Warehousing and Shipping

We inventory our products and fill most customer orders from our corporate headquarters in Delray Beach, Florida. We have an in-house fulfillment and distribution operation, which is used to manage the entire supply chain, beginning with the placement of the order, continuing through order processing, and then fulfilling and shipping of the product to the customer. We offer a variety of shipping options, including next day delivery. We ship to anywhere in the United States served by the United States Postal Service or United Parcel Service. Priority orders are expedited in our fulfillment process. Our goal is to ship the products the same day that the order is received. For prescription medications, our goal is to ship the product immediately after the prescription has been authorized by the customer’s veterinarian. We currently offer free shipping to all customers whose order value is $49 or more.

Purchasing and Supply of Products

We purchase our products from a variety of sources, including certain manufacturers, domestic distributors, and wholesalers. There were five suppliers from whom we purchased approximately 80% of all products in fiscal 2022. We believe having strong relationships with product manufacturers and distributors will ensure the availability of an adequate volume of products ordered by our customers. Part of our growth strategy included developing direct relationships with all of the leading pharmaceutical manufacturers of the more popular prescription and non-prescription medications. We now have direct relationships with all these major manufacturers.

Technology

We utilize integrated technologies in our call centers, e-commerce, order entry, and inventory control/fulfillment operations. Our systems are custom configured by us to optimize our computer telephone integration and mail-order processing. The systems are designed to maintain a large database of specialized information and process a large volume of orders efficiently and effectively. Our systems provide our customer care representatives, and our customers on our website, including on our mobile application, with real time product availability information and updated customer information to enhance our customer care.

We also have an integrated direct connection for processing credit cards to ensure that a valid credit card number and authorization have been received at the same time our customer care representatives are on the telephone with the customer or when a customer submits an order on our website. Our information systems provide our customer care representatives with records of all prior contact with a customer, including the customer’s address, telephone number, e-mail address, prescription information, order history, payment history, and notes.

Competition

The pet medications market is competitive and highly fragmented. Our competitors consist of veterinarians, and online and traditional retailers. We believe that the following are the principal competitive factors in our market:

| ● |

Product selection and availability, including the availability of prescription and non-prescription medications; |

| ● |

Brand recognition; |

| ● |

Reliability and speed of delivery; |

| ● |

Personalized service and convenience; |

| ● |

Price; and |

| ● |

Website and mobile application usability and content. |

We compete with veterinarians, and online and traditional retailers for the sale of prescription and non-prescription pet medications and other health products. Many pet owners may prefer the convenience of purchasing their pet medications or other health products at the time of a veterinarian visit. In order to effectively compete with veterinarians, we must continue to educate pet owners about the service, convenience, and savings offered by our Company.

According to the American Pet Products Association, pet spending in the United States increased 19.3% to $123.6 billion in 2021. Veterinary care and Rx medications represented $34.3 billion, or 28% of the total spending on pets in the United States. The pet medication market, which included prescription and nonprescription medication, is estimated to be approximately $10.0 billion, with veterinarians having the majority of the prescription market share. The dog and cat population is approximately 184 million, with approximately 70% of all households having a pet.

We believe that the following are the main competitive strengths that differentiate PetMeds from the competition:

| ● |

Pure Play Channel leader, in an estimated $10.0 billion industry; |

| ● |

“1-800-PetMeds” brand name with 25 years of experience, consumers know us as the trusted pet medication experts; |

| ● |

Licensed pharmacy to conduct business in 50 states, and a Pharmacy Verified website (a website verification program by the National Association of Boards of Pharmacy®, which identifies online pharmacies and pharmacy-related websites as safe and legitimate); and |

| ● |

Exceptional customer care and support. |

Intellectual Property

We conduct our business under the trade name “PetMeds” and use a family of trade names all containing the term “PetMeds” or “PetMed” in some form. We believe the “1-800-PetMeds” trade name, which is also our toll-free telephone number, and the “PetMeds” family of trademarks, have added significant value and are important factors in the marketing of our products. We have also obtained the right to use and control the Internet addresses www.1800petmeds.com, www.1888petmeds.com, www.petmedexpress.com, www.petmed.com, and www.petmeds.com.

We also obtained the right to use and control the Internet addresses www.petmeds.pharmacy, www.petmed.pharmacy, and www.1800petmeds.pharmacy, through a National Association of Boards of Pharmacy® initiative to ensure high standards for online pharmacies. We do not expect to lose the ability to use the Internet addresses; however, there can be no assurance in this regard and the loss of these addresses may have a material adverse effect on our financial position and results of operations. We are the exclusive owners of United States Trademark Registrations for “America’s Largest Pet Pharmacy®,” “America’s Most Trusted Pet Pharmacy®,” “Trusted Pet Medication Experts®,” “PetMed Express and Design®,”1-800-PetMeds and Design®,” 1-800-PetMeds®,” and “PetMeds®,” among numerous others.

Government Regulation

Dispensing prescription medications is governed at the state level by Boards of Pharmacy, or similar regulatory agencies, of each state where prescription medications are dispensed. We are subject to regulation by the State of Florida and are licensed as a community pharmacy by the Florida Board of Pharmacy. Our current license is valid until February 28, 2023, and prior to that date a renewal application will be submitted to the Board of Pharmacy. During fiscal 2015 we obtained a federal registration, and state registrations/permits as required, to dispense Schedule IV controlled substances, and we also updated our federal registration and state registrations/permits as required to include the ability to dispense Schedule V controlled substances.

Our pharmacy practice is also licensed and/or regulated by 49 other state pharmacy boards, the District of Columbia Board of Pharmacy, and the United States Drug Enforcement Administration, and with respect to our products, by other regulatory authorities including, but not necessarily limited to, the United States Food and Drug Administration (“FDA”) and the United States Environmental Protection Agency. As a licensed pharmacy in the State of Florida, we are subject to the Florida Pharmacy Act and regulations promulgated thereunder. To the extent that we are unable to maintain our license as a community pharmacy with the Florida Board of Pharmacy, or if we do not maintain the licenses granted by other state pharmacy boards, or if we become subject to actions by the FDA, or other enforcement regulators, our distribution of prescription medications to pet owners could cease, which could have a material adverse effect on our financial condition and results of operations.

We rely on legal and operational compliance programs, as well as outside counsel, to guide our business in complying with applicable laws and regulations in the areas in which we do business. In addition, regulatory regime changes may add cost and complexity to our compliance efforts. Based on information currently available, we believe that our compliance in general with federal and state regulations will not have a material effect on our earnings or financial condition. However, it is difficult to predict with certainty the potential impact of future compliance efforts and thus, future costs associated with such matters may exceed current reserves. As of March 31, 2022 we have no reserves related to federal and state regulations.

Human Capital Resources

We strive to create a high-performance culture that embraces diversity, inclusion, diverse perspectives and experiences, to ensure that employees have opportunities to develop the skills they need to grow and excel in their fields. Human capital management is a priority for our executives and Board of Directors, and we are committed to identifying and developing the talent necessary for our long-term success. We have a talent and succession planning process and have established programs to support the development of our talent pipeline for critical roles in our organization. We conduct an annual review with human resources and the departmental leadership teams, focusing on high performing and high potential talent, diverse talent and succession for our critical roles.

We also recognize that it is important to develop our future leaders. We provide a variety of resources to help our employees build and develop their skills, including online development resources as well as individual development opportunities and projects for key talent. Additionally, we have leadership development resources for our future leaders as they continue to develop their skills.

We also foster a strong corporate culture that promotes high standards of ethics and compliance for our business, including policies that set forth principles to guide employee, officer, director, and vendor conduct, such as our Code of Business Conduct and Ethics. We also maintain a whistleblower policy and anonymous hotline for the confidential reporting of any suspected policy violations or unethical business conduct on the part of our employees, officers, directors, or vendors.

We currently have 212 full time employees, including: 126 in customer care and marketing; 23 in fulfillment and purchasing; 46 in our pharmacy; 4 in information technology; 7 in accounting/human resources; and 6 in management. None of our employees are represented by a labor union or governed by any collective bargaining agreements. We consider relations with our employees to be in good standing. The majority of our employees work at our headquarters and distribution center located in Delray Beach, Florida. As a result of the COVID-19 pandemic many of our personnel are currently working remotely, and in the long term, we expect some personnel to transition into working remotely on a regular basis.

In response to the COVID-19 pandemic, we implemented significant changes that we determined were in the best interest of our employees as well as the communities in which we operate. These measures include allowing most employees to work from home and implementing additional safety measures for employees continuing critical on-site work. We believe in supporting our employees’ health and well-being. Our goal is to help employees make informed decisions about their health by providing the tools and resources necessary to achieve a healthier lifestyle. We offer our employees a wide array of benefits such as life and health (medical, dental, and vision) insurance, paid time off and retirement benefits, as well as emotional well-being services through our health insurance program.

We offer competitive compensation to attract and retain the best people, and we help care for our people so they can focus on our mission. Our employees' total compensation package includes market-competitive salary, bonuses or sales commissions, and equity. We generally offer annual equity grants to certain full-time employees, primarily management. Having compensation tied to annual equity grants helps ensure that our employees will be committed to the Company’s long-term success. We have conducted an annual pay equity analysis and continue to be committed to pay equity.

Available Information

Our website address is www.petmeds.com. The information on our website is not, and shall not be deemed to be, a part of or incorporated into this Annual Report on Form 10-K or any other filings we make with the Securities and Exchange Commission ("SEC"). We file annual, quarterly, and current reports, proxy statements, and other information with the SEC. Our SEC filings, including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to the Exchange Act are available free of charge over the Internet on our website or at the SEC's web site at www.sec.gov. Our SEC filings will be available through our website as soon as reasonably practicable after we have electronically filed or furnished them to the SEC.

ITEM 1A. RISK FACTORS

Our operations and financial results are subject to various risks and uncertainties, including those described below, that could materially and adversely affect our business, financial condition, operating results and the trading price of our common stock. Because of the following factors, as well as other factors affecting the Company’s results of operations and financial condition, past financial performance should not be considered to be a reliable indicator of future performance, and investors should not use historical trends to anticipate results or trends in future periods. This discussion of risk factors contains forward-looking statements. This section should be read in conjunction with Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and accompanying notes in Part II, Item 8, “Financial Statements and Supplementary Data” of this Annual Report on Form 10-K.

Regulatory Risks

We may inadvertently fail to comply with various state or federal regulations covering the dispensing of prescription pet medications which may subject us to reprimands, sanctions, probations, fines, suspensions, or the loss of one or more of our pharmacy licenses.

The sale and delivery of prescription pet medications is generally governed by state laws and state regulations, and with respect to controlled substances, also by federal law. Since our pharmacy is located in the State of Florida, the Company is governed by the laws and regulations of the State of Florida. Each prescription pet medication sale we make is likely also to be covered by the laws of the state where the customer is located. The laws and regulations relating to the sale and delivery of prescription pet medications vary from state to state, but generally require that prescription pet medications be dispensed with the authorization from a prescribing veterinarian. Our current license is valid until February 28, 2023, and there is no guarantee that we will be able to renew it. To the extent that we are unable to maintain our license as a community pharmacy with the Florida Board of Pharmacy, or if we do not maintain the licenses granted by other state boards, or if we become subject to actions by the FDA, or other enforcement regulators, our dispensing of prescription medications to pet owners could cease, which could have a material adverse effect on our operations.

The Company is a party to routine litigation and administrative complaints incidental to its business. Management does not believe that the resolution of any or all of such routine litigation and administrative complaints is likely to have a material adverse effect on the Company’s financial condition or results of operations. While we make every effort to fully comply with all applicable state rules, laws, and regulations, from time to time we have been the subject of administrative complaints regarding the authorization of prescriptions prior to shipment. We cannot assure you that we will not be the subject of administrative complaints in the future. We cannot guarantee you that we will not be subject to reprimands, sanctions, probations, or fines, or that one or more of our pharmacy licenses will not be suspended or revoked. If we were unable to maintain our license as a community pharmacy in the State of Florida, or if we are not granted licensure in a state that begins to require licensure, or if one or more of the licenses granted by other state boards should be suspended or revoked, our ability to continue to sell prescription medications and to continue our business as it is presently conducted could be in jeopardy.

Business Risks

Our failure to properly manage our inventory may result in excessive inventory carrying costs, or inadequate supply of products, which could materially adversely affect our financial condition and results of operations.

Our current product line contains approximately 3,000 SKUs. A significant portion of our sales is attributable to products representing approximately 100 SKUs, including the most popular flea and tick, and heartworm preventative brands. We need to properly manage our inventory to provide an adequate supply of these products and avoid excessive inventory of the products representing the balance of the SKUs. We generally place orders for products with our suppliers based upon our internal estimates of the amounts of inventory we will need to fill future orders. These estimates may be significantly different from the actual orders we receive.

In the event that subsequent orders fall short of original estimates, we may be left with excess inventory. Significant excess inventory could result in price discounts, increased inventory carrying costs, and obsolescence. Similarly, if we fail to have an adequate supply of some SKUs, we may lose sales opportunities. We cannot guarantee that we will maintain appropriate inventory levels. Any failure on our part to maintain appropriate inventory levels may have a material adverse effect on our financial condition and results of operations.

Resistance from veterinarians to authorize prescriptions, or attempts/efforts on their part to discourage pet owners from purchasing from us could cause our sales to decrease and could materially adversely affect our financial condition and results of operations.

Since we began our operations, some veterinarians have resisted providing our customers with a copy of their pet’s prescription or authorizing the prescription to our pharmacy staff, thereby effectively preventing us from filling such prescriptions under state law. We have also been informed by customers and consumers that veterinarians have tried to discourage pet owners from purchasing from internet mail-order pharmacies.

Although veterinarians in some states are required by law to provide a pet owner with a prescription if medically appropriate, if the number of veterinarians who refuse to authorize prescriptions should increase, or if veterinarians are successful in discouraging pet owners from purchasing from internet mail-order pharmacies, our sales could decrease, and our financial condition and results of operations may be materially adversely affected.

Significant portions of our sales are made to residents of eight states. If we should lose our pharmacy license in one or more of these states, our financial condition and results of operations would be materially adversely affected.

While we ship pet medications to customers in all 50 states, approximately 50% of our sales for the fiscal year ended March 31, 2022, were made to customers located in the states of California, Florida, Texas, New York, Pennsylvania, North Carolina, Georgia, and Virginia. If for any reason our license to operate a pharmacy in one or more of those states should be suspended or revoked, or if it is not renewed, our ability to sell prescription medications to residents of those states would cease and our financial condition and results of operations in future periods would be materially adversely affected.

We now have direct buying relationships with all the major pet medication manufacturers; the contractual relationship depends on our compliance with their minimum advertised pricing policies (MAPP).

During fiscal 2020, the Company established direct purchasing relationships with all the major pet medication manufacturers. These relationships entitle the Company to buy directly from the manufacturer under the terms and conditions of a purchasing agreement which dictates purchase pricing of inventory and criteria to obtain additional discounts and rebates. The terms of these agreements also require the Company to comply with the manufacturers’ MAPP. Each advertisement and/or promotion of a product below the MAPP price, should they occur, would be a violation of the policy. This policy applies to all advertisements of products in all media including, without limitation, flyers, posters, coupons, mailers, inserts, newspapers, magazines, on-line catalogs, mail order catalogs, public signage and all Internet or similar electronic media, television, radio and public signage, including websites, email newsletters, forums, and auction sites.

At the discretion of the manufacturers, non-compliance with the MAPP can result in one or more of the following actions: (1) forfeiture of future rebates or discounts from the manufacturer, (2) suspension of future purchases from the manufacturer, (3) or termination of current or future business relationship. The Company has and will continue to make every attempt to abide by the manufacturers MAPP. However, no assurances can be made that the Company will not violate MAPP inadvertently. A reduction or discontinuance of these rebates or discounts would increase our costs and could reduce our profitability. If any of these major pet medication manufacturers were to terminate our purchasing relationship it could materially adversely affect our business. If the manufacturers are not able to enforce their MAPP industry-wide, then our profit margins and results of operations may also be impacted negatively.

The loss of any of our key suppliers would negatively impact our business.

We have direct purchasing relationships with all of the major pet medication manufacturers, the majority of which we purchase significant quantities of pet medication products, with the majority from these major manufacturers. We do maintain annual purchasing contracts with these major manufacturers. While we believe that our supplier relationships are good, a supplier could discontinue selling to us at any time. The loss of any of our key suppliers of pet medications offered by us would have a negative impact on our business, financial condition, and results of operations.

Shipping is a critical part of our business and any changes in, or disruptions to, our shipping arrangements could adversely affect our business, financial condition, and results of operations.

We currently rely on third-party national, regional, and local logistics providers to deliver the products we offer on our website. If we are not able to negotiate acceptable pricing and other terms with these providers, or if these providers experience performance problems or other difficulties in processing our orders or delivering our products to customers, it could negatively impact our results of operations and our customers’ experience. In addition, our ability to receive inbound inventory efficiently and ship merchandise to customers may be negatively affected by factors beyond our and these providers’ control, including inclement weather, fire, flood, power loss, earthquakes, acts of war or terrorism or other events, such as labor shortages and disputes, financial difficulties, volatility in the prices of fuel, gasoline and commodities such as paper and packing supplies, system failures and other disruptions to the operations of the shipping companies on which we rely. We are also subject to risks of damage or loss during delivery by our shipping vendors. Further, due to the continuing spread of COVID-19 and its variant strains and related work and travel restrictions, there may be disruptions and delays in national, regional and local shipping, which may negatively impact our customers’ experience and our operations and financial results. The spread of COVID-19, and any future similar outbreak, may disrupt our suppliers and logistics providers and other third- party delivery agents, as their workers may be prohibited or otherwise unable to report to work and transporting products within regions may be limited due to factory closures, port closures and increased border controls and closures, among other things. If the products ordered by our customers are not delivered in a timely fashion or are damaged or lost during the delivery process, our customers could become dissatisfied and cease buying products through our website and mobile applications, which would adversely affect our business, financial condition, and results of operations.

The content of our website could expose us to various kinds of liability, which, if prosecuted successfully, could negatively impact our business.

Because we post product and pet health information and other content on our website, we face potential liability for negligence, copyright infringement, patent infringement, trademark infringement, defamation, and/or other claims based on the nature and content of the materials we post. Various claims have been brought, and sometimes successfully prosecuted, against Internet content distributors. We could be exposed to liability with respect to the unauthorized duplication of content or unauthorized use of other parties’ proprietary technology. Although we maintain general liability insurance, our insurance may not cover potential claims of this type or may not be adequate to indemnify us for all liability that may be imposed. Any imposition of liability that is not covered by insurance, or is in excess of insurance coverage, could materially adversely affect our financial condition and results of operations.

We may not be able to protect our intellectual property rights, and/or we may be found to infringe on the proprietary rights of others.

We rely on a combination of trademarks, trade secrets, copyright laws, and contractual restrictions to protect our intellectual property rights. These afford only limited protection. Despite our efforts to protect our proprietary rights, unauthorized parties may attempt to copy our non-prescription private label or generic equivalents, when and if developed, as well as aspects of our sales formats, or to obtain and use information that we regard as proprietary, including the technology used to operate our website and our content, and our trademarks. Litigation or proceedings before the United States Patent and Trademark Office or other bodies may be necessary in the future to enforce our intellectual property rights, to protect our trade secrets and domain names, or to determine the validity and scope of the proprietary rights of others. Any litigation or adverse proceeding could result in substantial costs and diversion of resources and could seriously harm our business and operating results. Third parties may also claim infringement by us with respect to past, current, or future technologies. We expect that participants in our market will be increasingly involved in infringement claims as the number of services and competitors in our industry segment grows. Any claim, whether meritorious or not, could be time-consuming, result in costly litigation, cause service upgrade delays, or require us to enter into royalty or licensing agreements. These royalty or licensing agreements might not be available on terms acceptable to us or at all.

If we are unable to protect our Internet addresses or to prevent others from using Internet addresses that are confusingly similar, our business may be adversely impacted.

Our Internet addresses, www.1800petmeds.com, www.1888petmeds.com, www.petmedexpress.com, www.petmed.com, www.petmeds.com, www.petmeds.pharmacy, www.petmed.pharmacy, and www.1800petmeds.pharmacy, are critical to our brand recognition and our overall success. If we are unable to protect these Internet addresses, our competitors could capitalize on our brand recognition. There may be similar Internet addresses used by competitors. Governmental agencies and their designees generally regulate the acquisition and maintenance of Internet addresses. The regulation of Internet addresses in the United States and in foreign countries has changed and may undergo further change in the near future. Furthermore, the relationship between regulations governing Internet addresses and laws protecting trademarks and similar proprietary rights is unclear. Therefore, we may not be able to protect our own Internet addresses or prevent third parties from acquiring Internet addresses that are confusingly similar to, infringe upon, or otherwise decrease the value of our Internet addresses.

Since all of our operations are housed in a single location, we are more susceptible to a business interruption in the event of damage to, or disruptions in, our facility.

Our headquarters and distribution center are currently located in one location in South Florida, and most of our shipments of products to our customers are made from this sole distribution center. Because we consolidate our operations in one location, we are more susceptible to power and equipment failures, and business interruptions in the event of fires, floods, and other natural disasters than if we had additional locations. Furthermore, because we are located in South Florida, which is a hurricane-sensitive area, we are particularly susceptible to the risk of damage to, or total destruction of, our headquarters and distribution center and surrounding transportation infrastructure caused by a hurricane. We cannot assure you that we are adequately insured to cover the amount of any losses relating to any of these potential events, including business interruptions resulting from damage to or destruction of our headquarters and distribution center, or power and equipment failures relating to our call center or websites, or interruptions or disruptions to major transportation infrastructure, or other events that do not occur on our premises. The occurrence of one or more of these events could adversely impact our ability to generate revenues in future periods.

A failure of our information systems and customer-facing technology systems or any security breach or unauthorized disclosure of confidential information, or other cyber-attacks on our systems, could result in litigation and regulatory risk, harm our reputation and have a material adverse effect on our business.

Our business is dependent upon the efficient operation of our information systems. In particular, we rely on our information systems to effectively manage our business model strategy, with tools to track and manage sales, inventory, marketing, customer service efforts, the preparation of our consolidated financial and operating data, credit card information, and customer information. The failure of our information systems to perform as designed or the failure to maintain and enhance or protect the integrity of these systems could disrupt our business operations, adversely impact sales and the results of operations, expose us to customer or third-party claims, or result in adverse publicity.

Through our information technology, we are able to provide an improved overall shopping and interconnected retail experience that empowers our customers to shop and interact with us from computers, tablets, smartphones and other mobile devices. We use our website and our mobile application both as sales channels for our products and also as methods of providing product and other relevant information to our customers to drive online sales. Our online programs, communities and knowledge center allow us to inform, assist and interact with our customers. We also continually seek to enhance all of our online properties to provide an attractive user-friendly interface for our customers. Disruptions, failures or other performance issues with these customer-facing technology systems could impair the benefits that they provide to our online business and negatively affect our relationship with our customers.

Additionally, we collect, process, and retain sensitive and confidential customer information in the normal course of our business. Despite the security measures we have in place and any additional measures we may implement in the future, our facilities and systems, and those of our third-party service providers, could be vulnerable to security breaches, computer viruses, lost or misplaced data, programming errors, human errors, acts of vandalism, or other events. Any security breach or event resulting in the misappropriation, loss, or other unauthorized disclosure of confidential information, whether by us directly or our third-party service providers, could damage our reputation, expose us to the risks of litigation and liability, disrupt our business, or otherwise affect our results of operations.

Our operating results are difficult to predict and may fluctuate, and a portion of our sales are seasonal.

Factors that may cause our operating results to fluctuate include:

| ● |

Our ability to obtain new customers at a reasonable cost, retain existing customers, or encourage reorders; |

| ● |

Our ability to increase the number of visitors to our website, or our ability to convert visitors to our website into customers; |

| ● |

The mix of medications and other pet products sold by us; |

| ● |

Our ability to manage inventory levels or obtain an adequate supply of products; |

| ● |

Our ability to adequately maintain, upgrade, and develop our website, the systems that we use to process customers’ orders and payments, or our computer network; |

| ● |

Increased competition within our market niche; |

| ● |

Price competition; |

| ● |

New products introduced to the market, including generics; |

| ● |

Increases in the cost of advertising; |

| ● |

The amount and timing of operating costs and capital expenditures relating to expansion of our product line or operations; |

| ● |

Disruption of our toll-free telephone service, technical difficulties, or systems and Internet outages or slowdowns; |

| ● |

The impact of COVID-19 on our business operations and generally on the economy, including the measures taken by governmental authorities to address it; and |

| ● |

Unfavorable general economic trends. |

Because our operating results are difficult to predict, we believe that quarter-to-quarter comparisons of our operating results are not a good indication of our future performance. The majority of our product sales are affected by the seasons, due to the seasonality of mainly flea, tick, and heartworm medications. For the quarters ended June 30, 2021, September 30, 2021, December 31, 2021, and March 31, 2022, Company sales were 29%, 25%, 22%, and 24%, respectively. In addition to the seasonality of our sales, our annual and quarterly operating results have fluctuated in the past and may fluctuate significantly in the future due to a variety of factors, including weather, many of which are out of our control. Any change in one or more of these factors could materially adversely affect our financial condition and results of operations in future periods.

Uncertainties in economic conditions and their impact on consumer spending patterns could adversely impact our business, financial condition, and results of operations.

Our results of operations are sensitive to changes in certain macro-economic conditions that impact consumer spending on pet products and services. Some of the factors that may affect consumer spending on pet products and services include consumer confidence, levels of unemployment, inflation, interest rates, tax rates and general uncertainty regarding the overall future economic environment. We may experience declines in sales or changes in the types of products sold during economic downturns. Any material decline in the amount of consumer spending or other adverse economic changes could reduce our sales, and a decrease in the sales of higher-margin products could reduce profitability and, in each case, harm our business, financial condition, and results of operations.

We may seek to grow our business through acquisitions of, or investments in, new or complementary businesses, facilities, technologies, offerings, or products, or through strategic alliances, and the failure to manage these acquisitions, investments, or other strategic alliances, or to integrate them with our existing business, could have a material adverse effect on us.

We recently entered into, and made an investment in, a strategic alliance, and we may in the future consider opportunities to acquire or make investments in new or complementary businesses, facilities, technologies, offerings, or products, or enter into other strategic alliances, which may enhance our capabilities, complement our current products and services or expand the breadth of our markets. Acquisitions, investments and other strategic alliances involve numerous risks, including:

| ● |

problems integrating the acquired business, facilities, technologies or products, including issues maintaining uniform standards, procedures, controls and policies; |

| ● |

unanticipated costs associated with acquisitions, investments or strategic alliances; |

| ● |

losses we may incur as a result of declines in the value of an investment or as a result of incorporating an investee’s financial performance into our financial results; |

| ● |

diversion of management’s attention from our existing business; |

| ● |

risks associated with entering new markets in which we may have limited or no experience; |

| ● |

the risks associated with businesses we acquire or invest in, which may differ from or be more significant than the risks our other businesses face; |

| ● |

potential unknown liabilities associated with a business we acquire or in which we invest; and |

| ● |

increased legal and accounting compliance costs. |

Our ability to successfully grow through strategic transactions depends upon our ability to identify, negotiate, complete and integrate suitable target businesses, facilities, technologies, products and services. These efforts could be expensive and time-consuming and may disrupt our ongoing business and prevent management from focusing on our operations. As a result of future strategic transactions, we might need to issue additional equity securities, spend our cash, or incur debt (which may only be available on unfavorable terms, if at all) or contingent liabilities, any of which could reduce our profitability and harm our business. If we are unable to identify suitable acquisitions, investments or strategic relationships, or if we are unable to integrate any acquired businesses, facilities, technologies, offerings and products effectively, our business, financial condition, and results of operations could be materially and adversely affected. Also, while we employ several different methodologies to assess potential business opportunities, the new businesses or investments may not meet or exceed our expectations or desired objectives.

Financial Risks

We are subject to payment-related risks that could increase our operating costs, expose us to fraud or theft, subject us to potential liability and potentially disrupt our business.

We accept payments using a variety of methods, including credit and debit cards, PayPal, and checks, and we may offer new payment options over time. Acceptance of these payment options subjects us to rules, regulations, contractual obligations and compliance requirements, including payment network rules and operating guidelines, data security standards and certification requirements, and rules governing electronic funds transfers. These requirements may change over time or be reinterpreted, making compliance more difficult or costly. For certain payment methods, including credit and debit cards, we pay interchange and other fees, which may increase over time and raise our operating costs.

We rely on third parties to provide payment processing services, including the processing of credit cards, debit cards, and other forms of electronic payment. If these companies become unable to provide these services to us, or if their systems are compromised, it could potentially disrupt our business. The payment methods that we offer also subject us to potential fraud and theft by criminals, who are becoming increasingly more sophisticated, seeking to obtain unauthorized access to or exploit weaknesses that may exist in the payment systems. If we fail to comply with applicable rules or requirements for the payment methods we accept, or if payment-related data is compromised due to a breach or misuse of data, we may be liable for costs incurred by payment card issuing banks and other third parties or subject to fines and higher transaction fees, or our ability to accept or facilitate certain types of payments may be impaired. As a result, our business and operating results could be adversely affected.

Industry Risks

We face significant competition from veterinarians and online and traditional retailers and may not be able to compete profitably with them.

We compete directly and indirectly with veterinarians for the sale of pet medications and other health products. Veterinarians hold a competitive advantage over us because many pet owners may find it more convenient or preferable to purchase these products directly from their veterinarians at the time of an office visit. We also compete directly and indirectly with both online and traditional retailers. Both online and traditional retailers may hold a competitive advantage over us because of longer operating histories, established brand names, greater resources, and/or an established customer base. Online retailers may have a competitive advantage over us because of established affiliate relationships to drive traffic to their website. Traditional retailers may hold a competitive advantage over us because pet owners may prefer to purchase these products from a store instead of online. In addition, we face growing competition from online and multichannel retailers, some of whom may have a lower cost structure than ours, as customers now routinely use computers, tablets, smartphones, and other mobile devices and mobile applications to shop online and compare prices and products in real time. In order to effectively compete in the future, we may be required to offer promotions and other incentives, which may result in lower operating margins and adversely affect the results of operations. We also face a significant challenge from our competitors forming alliances with each other, such as those between online and traditional retailers. These relationships may enable both their online and retail stores to negotiate better pricing and better terms from suppliers by aggregating the demand for products and negotiating volume discounts, which could be a competitive disadvantage to us.

Risks Related to COVID-19

The COVID-19 global pandemic and related government, private sector and individual consumer responsive actions may adversely affect our business operations, employee availability, financial performance, liquidity and cash flow for an unknown period of time.

The outbreak of COVID-19 was declared a pandemic by the World Health Organization and continues to spread in the United States, Canada, and in many other countries globally. COVID-19 has had, and continues to have, a significant impact in the United States and around the world, prompting governments and businesses to take unprecedented measures in response. Such measures have included restrictions on travel and business operations, temporary closures of businesses, and quarantine and shelter-in-place orders. The COVID-19 pandemic has at times significantly curtailed economic activity in the United States and globally, and caused significant volatility and disruption in global financial markets. The continued adverse public health developments, the related government and private sector responsive actions, and the economic effects of the COVID-19 pandemic may adversely affect our business operations. It is impossible to predict the effect and ultimate impact of the COVID-19 pandemic, as the situation is continually evolving. The COVID-19 pandemic may disrupt the global supply chain and may cause disruptions to our operations if a significant number of employees are quarantined or if they are otherwise limited in their ability to work at our fulfillment center. Additional federal or state mandates could also impact our ability to take or fulfill our customers’ orders and operate our business. As an essential business, we have been open during our normal business hours without any material disruptions to our operations. We are dedicated to making every effort to ensure the health and safety of our employees. We have implemented working from home where possible and enhanced disinfection and social distancing within our workplace. Many of our personnel are working remotely and it is possible that this could have a negative impact on the execution of our business plans and operations. If a natural disaster, power outage, connectivity issue, or other event occurs that impacts our employees’ ability to work remotely, it may be difficult or, in certain cases, impossible, for us to continue our business for a substantial period of time. The increase in remote working may also result in consumer privacy, IT security and fraud concerns as well as operational inefficiencies.

The operations of our fulfillment center may be substantially disrupted by additional federal or state mandates ordering shutdowns or by the inability of our employees to travel to work due to COVID-19. The inability to ship from our fulfillment center due to a COVID-19 outbreak, disruptions to the operations of our fulfillment center, or increased costs in fulfillment center capacity may negatively impact our financial performance or slow our future growth.

The uncertainty around the duration of business disruptions and the extent of the spread of the virus and the emergence of new variants of the virus in the United States and to other areas of the world will likely continue to adversely impact the national and global economy and negatively impact consumer spending. Any of these outcomes could have a material adverse impact on our business, financial condition, operating results and ability to execute and capitalize on our strategies. The full extent of COVID-19’s impact on our operations and financial performance depends on future developments that are uncertain and unpredictable, including the duration and spread of the pandemic, its impact on capital and financial markets and any new information that may emerge concerning the severity and new variants of the virus, its spread to other regions as well as the actions taken to contain it, among others.

Securities Risks

Our stock price fluctuates from time to time and may fall below expectations of securities analysts and investors, and could subject us to litigation, which may result in you suffering a loss on your investment.

The market price of our common stock may fluctuate significantly in response to a number of factors, many of which are out of our control. These factors include: quarterly variations in operating results; changes in accounting treatments or principles; announcements by us or our competitors of new products and services offerings; significant contracts, acquisitions, or strategic relationships; additions or departures of key personnel; any future sales of our common stock or other securities; stock market price and volume fluctuations of publicly traded companies; and general political, economic, and market conditions. In some future quarter our operating results may fall below the expectations of securities analysts and investors, which could result in a decrease in the trading price of our common stock. In addition, if the Company fails to meet expectations related to future growth, profitability, dividends, or other market expectations, the price of the Company’s common stock may decline significantly, which could have a material adverse impact on investor confidence and employee retention. In the past, securities class action litigation has often been brought against a company following periods of volatility in the market price of its securities. We may be the target of similar litigation in the future. Securities litigation could result in substantial costs and divert management's attention and resources, which could seriously harm our business and operating results.

We may issue additional shares of preferred stock that could defer a change of control or dilute the interests of our common shareholders. Our charter documents could defer a takeover effort which could inhibit your ability to receive an acquisition premium for your shares.

Our charter permits our Board of Directors to issue up to 5.0 million shares of preferred stock without shareholder approval. Currently there are 2,500 shares of our Convertible Preferred Stock issued and outstanding. This leaves slightly less than 5.0 million shares of preferred stock available for issuance at the discretion of our Board of Directors. These shares, if issued, could contain dividend, liquidation, conversion, voting, or other rights which could adversely affect the rights of our common shareholders and which could also be utilized, under some circumstances, as a method of discouraging, delaying, or preventing a change in control. Provisions of our articles of incorporation, bylaws and Florida law could make it more difficult for a third party to acquire us, even if many of our shareholders believe it is in their best interest.

Our ability to pay regular dividends to our shareholders and the amounts of any such dividends are subject to the discretion of the Board and may be limited by our financial condition, or limitations under Florida law.

We have paid dividends to our shareholders since 2009 and it is currently anticipated that we will continue to pay regular quarterly dividends, any such determination to pay dividends and the amounts thereof will be at the discretion of the Board and will be dependent on then-existing conditions, including our financial condition, income, legal requirements, including limitations under Florida law, and other factors the Board deems relevant. The Board has previously decided, and may in the future decide, in its sole discretion, to change the amount or frequency of dividends or discontinue the payment of dividends entirely. For these reasons, shareholders will not be able to rely on dividends to receive a return on investment. Accordingly, realization of any gain on shares of our common stock may depend on the appreciation of the price of our common stock, which may not occur.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None

ITEM 2. PROPERTIES

We own our facilities, including our principal executive offices and distribution center, which are located at 420 South Congress Avenue, Delray Beach, Florida 33445 (the “Property”). The Property consists of approximately 634,000 square feet of land or 14.6 acres with two building complexes totaling approximately 185,000 square feet, with additional land for future use. The first building complex consists of approximately 125,000 square feet and the second building complex consists of approximately 60,000 square feet each consisting of both office and warehouse space. The Company occupies approximately 97,000 square feet of the first building for its principal offices and distribution center. As of March 31, 2022, 48% of the Property was leased to two tenants with a remaining weighted average lease term of 3.0 years. We believe that our facilities are sufficient for our current needs and are in good condition in all material respects.

ITEM 3. LEGAL PROCEEDINGS

The Company has settled complaints that had been filed with various states’ pharmacy boards in the past. There can be no assurances made other states will not attempt to take similar actions against the Company in the future. The Company initiates litigation to protect its trade or service marks. There can be no assurance that the Company will be successful in protecting its trade or service marks. Legal costs related to the above matters are expensed as incurred.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES ’

Price Range of Common Stock

Our common stock is traded on the NASDAQ Global Select Market (“NASDAQ”) under the symbol “PETS.” The prices set forth below reflect the high and low sale prices per share in each of the quarters of fiscal 2022 and 2021 as reported by the NASDAQ.

| Fiscal 2022: |

High |

Low |

||||||

| First Quarter |

$46.06 | $27.73 | ||||||

| Second Quarter |

$34.00 | $26.50 | ||||||

| Third Quarter |

$32.00 | $25.26 | ||||||

| Fourth Quarter |

$29.18 | $23.62 | ||||||

| Fiscal 2021: |

High |

Low |

||||||

| First Quarter |

$40.96 | $27.94 | ||||||

| Second Quarter |

$41.83 | $29.00 | ||||||

| Third Quarter |

$33.77 | $28.96 | ||||||

| Fourth Quarter |

$51.80 | $29.77 | ||||||

Holders

There were 105 holders of record of our common stock on May 24, 2022, and approximately 48,300 of our holders are “street name” or beneficial holders, whose shares are held by banks, brokers, or other financial institutions.

Dividends

During fiscal 2021 and 2022, our Board of Directors declared the following dividends:

| Declaration Date |

Per Share Dividend |

Record Date |

Total Amount (In thousands) |

Payment Date |

||||||

| May 4, 2020 |

$0.28 | May 15, 2020 |

$5,647 | May 22, 2020 |

||||||

| July 20, 2020 |

$0.28 | July 31, 2020 |

$5,647 | August 7, 2020 |

||||||

| October 26, 2020 |

$0.28 | November 9, 2020 |

$5,676 | November 20, 2020 |

||||||

| January 19, 2021 |

$0.28 | February 1, 2021 |

$5,676 | February 12, 2021 |

||||||

| May 3, 2021 |

$0.30 | May 14, 2021 |

$6,081 | May 21, 2021 |

||||||

| July 26, 2021 |

$0.30 | August 6, 2021 |

$6,102 | August 13, 2021 |

||||||

| October 25, 2021 |

$0.30 | November 8, 2021 |

$6,283 | November 19, 2021 |

||||||

| January 24, 2022 |

$0.30 | February 7, 2022 |

$6,294 | February 18, 2022 |

||||||

On May 3, 2021, the Company’s Board of Directors declared an increased quarterly dividend from $0.28 to $0.30 per share, on its common stock. The Company’s Board of Directors declared a quarterly dividend of $0.30 per share on May 9, 2022. The Board established a May 20, 2022 record date and a May 27, 2022 payment date. The Company intends to continue to pay regular quarterly dividends; however, the declaration and payment of future dividends is discretionary and will be subject to a determination by the Board of Directors each quarter following its review of the Company’s financial performance.

Issuer Purchases of Equity Securities

On November 8, 2006, the Company's Board of Directors approved a share repurchase plan of up to $20.0 million. On October 31, 2008, November 1, 2010, and August 1, 2011, the Company’s Board of Directors approved an increase under the share repurchase plan, each for an additional $20.0 million. The repurchase plan is intended to be implemented through purchases made from time to time in either the open market or through private transactions at the Company's discretion, subject to market conditions and other factors, in accordance with SEC requirements.

There can be no assurances as to the precise number of shares that will be repurchased under the share repurchase plan, and the Company may discontinue the share repurchase plan at any time subject to compliance with applicable regulatory requirements. Shares purchased pursuant to the share repurchase plan will either be cancelled or held in the Company's treasury. On January 25, 2019, the Company’s Board of Directors authorized an additional $30.0 million under the repurchase plan. During fiscal 2020 the Company purchased and retired approximately 613,000 shares of its common stock for approximately $11.5 million, averaging approximately $18.73 per share. As of March 31, 2022, the Company had approximately $28.7 million remaining under the Company’s share repurchase plan. Since the inception of the share repurchase plan up to March 31, 2022, approximately 6.2 million shares have been repurchased under the plan for approximately $81.3 million, averaging approximately $13.11 per share.

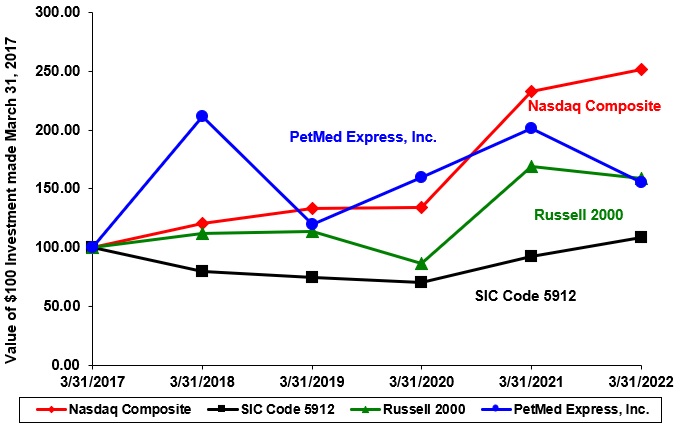

Performance Graph

Set forth below is a line graph comparing the five-year cumulative performance of our Common Stock with the Nasdaq Composite, the Russell 2000, and our SIC Code 5912 (pharmacy peer group) from March 31, 2017, to March 31, 2022. The graph assumes that $100 was invested on March 31, 2017, in each of our Common Stock, the Nasdaq Composite, the Russell 2000, and the SIC Code 5912 (pharmacy peer group). Because we have historically paid dividends on a quarterly basis, the graph assumes that dividends were reinvested. The performance graph and related information below shall not be deemed “filed” with the SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act or Exchange Act, each as amended, except to the extent that we specifically incorporate it by reference into such filing.

Performance graph data:

| Fiscal Year Ended March 31, |

||||||||||||||||||||||||

| 2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

|||||||||||||||||||

| PetMed Express, Inc. |

100.00 | 211.75 | 119.69 | 159.37 | 201.60 | 155.76 | ||||||||||||||||||

| Nasdaq Composite |

100.00 | 120.76 | 133.60 | 134.52 | 233.26 | 252.05 | ||||||||||||||||||

| SIC Code 5912 |

100.00 | 80.17 | 75.01 | 70.52 | 92.62 | 108.31 | ||||||||||||||||||

| Russell 2000 |

100.00 | 111.79 | 114.09 | 86.72 | 168.96 | 159.19 | ||||||||||||||||||

Securities Authorized for Issuance under Equity Compensation Plans

The following table sets forth securities authorized for issuance under equity compensation plans, including individual compensation arrangements, by us under our 2015 Outside Director Equity Compensation Restricted Stock Plan and 2016 Employee Equity Compensation Restricted Stock Plan as of March 31, 2022:

| EQUITY COMPENSATION PLAN INFORMATION |

|||||||||||

| (In thousands) |

| Number of securities |

Number of securities |

|||||||||||

| to be issued upon |

Weighted average |

remaining available |

||||||||||

| exercise of outstanding |

exercise price of |

for future issuance |

||||||||||

| options, warrants |

outstanding options, |

under equity |

||||||||||

| Plan category |

and rights |

warrants and rights |

compensation plans |

|||||||||

| 2015 Outside Director Equity Compensation Restricted Stock Plan |

65 | - | 488 | (1) | ||||||||

| 2016 Employee Equity Compensation Restricted Stock Plan |

706 | - | 107 | |||||||||

| Total |

771 | 595 | ||||||||||

| (1) |

The number of shares of common stock available for issuance under the 2015 Outside Director Equity Compensation Restricted Stock Plan automatically increase on the first trading day of January each calendar year during the term of the 2015 Outside Director Equity Compensation Restricted Stock Plan, by an amount equal to ten percent (10%) of the total number of shares of common stock authorized under the 2015 Outside Director Equity Compensation Restricted Stock Plan. |

ITEM 6. [RESERVED]

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Executive Summary

PetMed Express (the “Company”) was incorporated in the state of Florida in January 1996, and since 2004 its common stock has traded on the NASDAQ Global Select Market under the symbol “PETS.” The Company began selling pet medications and other pet health products in September 1996, and in March 2010, the Company started offering additional pet supplies on its website for sale, and these items are drop shipped to customers by third party vendors. Presently, the Company’s product line includes approximately 3,000 of the most popular pet medications, health products, and supplies for dogs, cats, and horses.