Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08257

STATE STREET INSTITUTIONAL FUNDS

(formerly known as GE Institutional Funds)

(Exact name of registrant as specified in charter)

1600 Summer Street

Stamford, Connecticut 06905

(Address of principal executive offices)(Zip code)

SSGA Funds Management, Inc.

1600 Summer Street

Stamford, Connecticut 06905

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: 800-242-0134

Date of fiscal year end: 09/30

Date of reporting period: 09/30/16

Table of Contents

Item 1. Reports to Stockholders

Table of Contents

Annual Report

September 30, 2016

GE Institutional Funds

Table of Contents

GE Institutional Funds

Annual Report

September 30, 2016

| Page | ||||

| Notes to Performance | 1 | |||

| Manager Reviews and Schedules of Investments | ||||

| 3 | ||||

| 11 | ||||

| 24 | ||||

| 31 | ||||

| 38 | ||||

| 50 | ||||

| 58 | ||||

| 84 | ||||

| Financial Statements | ||||

| 102 | ||||

| 112 | ||||

| 114 | ||||

| 116 | ||||

| 120 | ||||

| Report of Independent Registered Public Accounting Firm | 136 | |||

| Tax Information | 137 | |||

| Advisory and Administration Agreement Approval | 138 | |||

| Sub-Advisory Agreement Approval | 141 | |||

| Special Meeting of Shareholders — Voting Results | 143 | |||

| Additional Information | 151 | |||

| Investment Team | 155 | |||

This report has been prepared for shareholders and may be distributed to others only if accompanied with a current prospectus and/or summary prospectus.

Table of Contents

GE Institutional Funds

Notes to Performance — September 30, 2016 (Unaudited)

The information provided on the following performance pages relates to the GE Institutional Funds (the “Trust”) and each of its series portfolios (each, a Fund and collectively, the “Funds”).

Total returns take into account changes in share price and assume reinvestment of dividends and capital gains distributions, if any. Total returns shown are net of Fund expenses.

The performance data quoted represents past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate. Accordingly, your shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Periods less than one year are not annualized. Please call toll-free (800) 242-0134 or visit the Funds’ website at http://www.geam.com for the most recent month-end performance data.

An investment in a Fund is not a deposit of any bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (“FDIC”) or any other government agency. An investment in a Fund is subject to risk, including possible loss of principal invested.

The S&P 500® Composite Price Index of stocks (“S&P 500 Index”) is an unmanaged market capitalization-weighted index of stocks of 500 large U.S. companies, which is widely used as a measure of large-cap U.S. stock market performance.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes companies in the Russell 1000® Index with higher price-to-book ratios and higher forecasted growth values. It is a subset of the Russell 3000® Index and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership.

The Russell 2000® Index is a market capitalization-weighted index consisting of 2,000 of the smallest U.S.-domiciled publicly traded common stocks that are included in the Russell 3000® Index. The Russell 3000® Index is comprised of the 3,000 largest U.S.-domiciled companies.

The Morgan Stanley Capital International Europe, Australasia, and Far East Index (“MSCI® EAFE® Index”) is a market capitalization-weighted index of equity securities of companies domiciled in various countries. The MSCI® EAFE® Index is designed to represent the performance of developed stock markets outside the U.S. and Canada and excludes certain market segments unavailable to U.S. based investors.

The Morgan Stanley Capital International All Country World Index Ex-U.S. (“MSCI® ACWI Ex-U.S. Index”) is a market capitalization-weighted index designed to provide a broad measure of stock performance throughout the world, with the exception of U.S.-based companies. The MSCI® ACWI Ex-U.S. Index includes both developed and emerging markets.

The Barclays U.S. Aggregate Bond Index is an unmanaged market value-weighted index of taxable investment grade debt issues, including government, corporate, asset-backed and mortgage-backed securities, with maturities of one year or more. The Barclays U.S. Aggregate Bond Index is designed to represent performance of the U.S. investment-grade fixed rate bond market.

The results shown for the foregoing indices assume the reinvestment of net dividends or interest and do not reflect fees, expenses, or taxes. As such, index returns do not reflect the actual cost of investing in the instruments that comprise an index.

The peer universe of the underlying open end funds used for the peer group average annual total return calculation is based on a blend of Morningstar peer categories, as shown. Morningstar is an independent mutual fund rating service. A Fund’s performance may be compared to or ranked within a universe of mutual funds with investment objectives and policies similar but not necessarily identical to that of the Fund.

©2016 Morningstar, Inc. All Rights Reserved. The Morningstar information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damage or losses relating from any use of this information. Past performance does not guarantee future results.

The S&P 500 Index Fund is not sponsored, endorsed, sold or promoted by S&P Global Ratings (“S&P”), and S&P makes no representation or warranty, express or implied, to the investors of the Fund or any member of the public regarding the advisability of investing in the securities generally or in this Fund particularly or the ability of the S&P 500 Index Fund to track general stock market performance.

Russell Investment Group owns the Russell Index data, including all applicable trademarks and copyrights, used by SSGA Funds Management, Inc. (“SSGA FM”) in these materials. Any unauthorized use or redistribution of such Russell Index data is strictly prohibited. Russell Investment Group is not responsible for the configuration of this material or for any inaccuracy in SSGA FM’s presentation thereof.

| Notes to Performance | 1 |

Table of Contents

GE Institutional Funds

Notes to Performance, continued — September 30, 2016 (Unaudited)

The views, expressed in this document, reflect our judgment as of the publication date and are subject to change at any time without notice.

State Street Global Markets, LLC, member of FINRA & SIPC is the principal underwriter and distributor of the GE Institutional Funds and a wholly owned subsidiary of State Street Corporation. References to State Street may include State Street Corporation and its affiliates. The Funds pay State Street Bank and Trust Company for its services as custodian and Fund Accounting agent, and pay SSGA Funds Management, Inc. for investment advisory and administrative services.

| 2 | Notes to Performance |

Table of Contents

Portfolio Management Discussion and Analysis — September 30, 2016 (Unaudited)

| Q. | How did the GE Institutional U.S. Equity Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended September 30, 2016? |

| A. | For the twelve-month period ended September 30, 2016, the GE Institutional U.S. Equity Fund returned 13.29% for the Investment Class shares and 12.96% for the Service Class shares. The Fund’s benchmark, the S&P 500 Index returned 15.43% and the Fund’s Morningstar peer group of 1,576 US Large Blend funds returned an average of 11.76% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |

| A. | It was a volatile year for U.S. stocks. However, the market climbed a wall of worry and turned in solid double-digit gains in the last 12 months. Markets rebounded from serial concerns ranging from China’s currency devaluation at the beginning of the period, to global slowdown and recession fears in early 2016, to Britain’s astonishing referendum vote to leave the European Union in late June. Despite these uncertainties, U.S. stocks ended the year near all-time highs. |

| Plunging worldwide interest rates motivated equity investors to reach for yield, causing defensive telecomm, utilities and staples to outperform (and become richly valued, in our view). Commodity prices were stronger this year helping the materials and energy sectors to outperform. Also strong were the cyclical industrials and information technology sectors. Rallies in semiconductors, internet and software companies underpinned strength in technology stocks. |

| Only three sectors underperformed the S&P 500 broad market return: financials, consumer discretionary and health care. Careful stock selection was warranted in financials, as persistent low rates pressured interest-rate sensitive banks and insurance companies. Consumer discretionary — last year’s top-performing sector — took a breather as investors fretted growth. Health care stocks fell under pressure, caught in a stream of negative election year rhetoric around drug pricing. |

| Q. | What were the drivers behind Fund performance? |

| A. | The Fund outperformed the average Morningstar US Large Blend manager, yet failed to keep pace with the S&P 500 Index in a volatile and challenging investment environment. The Fund’s performance in the second half of the year was driven by a momentum reversal away from defensive yield sectors, favoring more cyclical sectors of the market. Given an outlook for continued slow economic growth, the Fund was underweight the defensive telecommunications, utilities and consumer staples sectors during the year — hurting annual relative performance but helping in recent months. In fact, portfolio positioning was the key negative performance driver in an environment that was largely macro-driven this year. |

| In the last 12 months, financials weighed on returns, due to underperformance in rate-sensitive insurance companies, banks and asset managers. We reduced financials exposure during the period to reflect the Federal Reserve’s pushed-out path to interest rate normalization. Underweighting the most defensive staples companies hurt, despite relative strength in one of our high-quality beverage company holdings. The Fund also failed to capture all of the upside in the commodity sectors, given an underweight in materials and underperformance among some of the Fund’s oil exploration and production holdings in energy. Finally, one of the Fund’s health care holdings was involved in a large M&A transaction that did not materialize, negatively impacting returns. We maintained conviction in this holding’s prospects as a standalone specialty pharma company. In general, we find health care’s growth rates and valuations attractive, and believe the uncertainty overhang should begin to resolve post November 2016’s presidential election. |

| On the other hand, strong stock selection in consumer discretionary and information technology (“IT”) sectors bolstered returns. Among consumer cyclicals, several of the Fund’s U.S. media holdings demonstrated strong results, seemingly immune to economic growth fears. In addition, a new position in a home furnishings company demonstrated accretion from a recent merger, and a Macao-based casino company rebounded along with the Chinese gaming market. In IT, our communications equipment, semiconductor and IT services holdings outperformed. Finally, the Fund benefited from strong stock selection in Real Estate Investment Trusts (“REITs”), a classic yield sector (our REIT holdings generally offer stable earnings growth and aren’t held solely for dividend income). |

| The Fund does not invest in derivatives securities as part of its strategy, but may hold futures contracts or ETFs to equitize cash flows in advance of investment. The effect of derivatives on performance was de minimis for the year. |

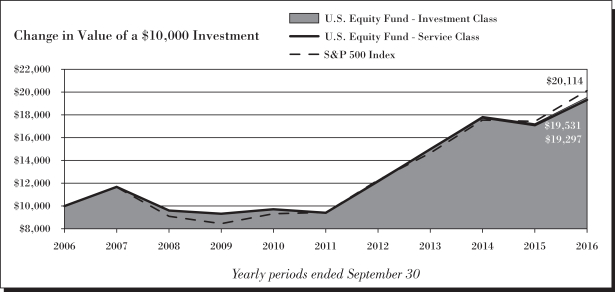

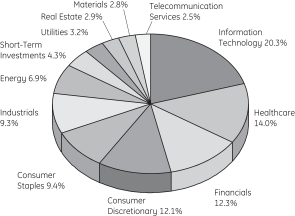

| U.S. Equity Fund | 3 |

Table of Contents

U.S. Equity Fund

Portfolio Management Discussion and Analysis, continued — September 30, 2016 (Unaudited)

| Q. | Were there any significant changes in the Fund during the period? |

| A. | There were no changes during the period in the portfolio management team or their approach to investing. Health care and financials remained key sector overweights, but we reduced our financials exposure somewhat as the Federal Reserve’s path of rate increases remained opaque. Modest positioning changes moderated the Fund’s cyclical tilt as we reach later innings of the business cycle. As such, the Fund also reduced its IT and materials exposures, and increased its consumer staples exposure, although still underweight at year-end. We are comfortable with our moderate pro-cyclical positioning as we think this business cycle may even reach extra innings due to the slow growth of this recovery. |

| 4 | U.S. Equity Fund |

Table of Contents

U.S. Equity Fund

Performance Summary — September 30, 2016 (Unaudited)

| U.S. Equity Fund | 5 |

Table of Contents

U.S. Equity Fund

Performance Summary, continued — September 30, 2016 (Unaudited)

| (a) | Fair Value basis is inclusive of short-term investment in State Street Institutional U.S. Government Money Market Fund Class G Shares. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| 6 | U.S. Equity Fund |

Table of Contents

U.S. Equity Fund

Understanding Your Fund’s Expenses — September 30, 2016 (Unaudited)

| U.S. Equity Fund | 7 |

Table of Contents

U.S. Equity Fund

Schedule of Investments — September 30, 2016

See accompanying notes to financial statements.

| 8 | U.S. Equity Fund |

Table of Contents

U.S. Equity Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| U.S. Equity Fund | 9 |

Table of Contents

U.S. Equity Fund

Schedule of Investments, continued — September 30, 2016

Other Information:

The Fund had the following long futures contracts open at September 30, 2016:

| Description | Expiration date |

Number of Contracts |

Current Notional Value |

Unrealized Depreciation |

||||||||||||

| S&P 500 Emini Index Futures |

December 2016 | 115 | $ | 12,422,300 | $ | (904 | ) | |||||||||

|

|

|

|||||||||||||||

Affiliate Table

| Number of Shares Held at 9/30/15 |

Value At 9/30/15 |

Shares Purchased |

Shares Sold |

Number of Shares Held at 9/30/16 |

Value at 9/30/16 |

Dividend/ Interest Income |

Realized Gain (Loss) |

|||||||||||||||||||||||||

| Financial Select Sector SPDR Fund |

72,629 | $ | 1,645,773 | 7,141 | 79,770 | — | $ | — | $ | 21,277 | $ | 560,910 | ||||||||||||||||||||

| Industrial Select Sector SPDR Fund |

131,838 | 6,577,398 | 39,270 | 171,108 | — | — | 130,507 | 2,393,943 | ||||||||||||||||||||||||

| State Street Institutional U.S. Government Money Market Fund - Class G Shares |

17,993,117 | 17,993,117 | 137,929,254 | 147,563,953 | 8,358,418 | 8,358,418 | 35,779 | — | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| $ | 8,358,418 | $ | 187,563 | $ | 2,954,853 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

See accompanying notes to financial statements.

| 10 | U.S. Equity Fund |

Table of Contents

Portfolio Management Discussion and Analysis — September 30, 2016 (Unaudited)

| Q. | How did the GE Institutional S&P 500 Index Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended September 30, 2016? |

| A. | For the twelve-month period ended September 30, 2016, the GE Institutional S&P 500 Index Fund returned 15.21% for the Investment Class shares and 14.90% for the Service Class shares. The Fund’s benchmark, the S&P 500 Index returned 15.43% and the Fund’s Morningstar peer group of 1,576 U.S. Large Blend funds returned an average of 11.76% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |

| A. | Overcoming the uncertainty prevailing at the end of 2015 and beginning of 2016 markets gained momentum and finished a 12-month period strongly with double-digit positive return. In contrast to August of 2015, when global equity markets witnessed their most volatile month since 2011, fast forward one year later and markets demonstrated an air of complacency in August 2016. In fact, the S&P 500 Index did not experience a daily price move of greater than 1%, up or down, between July 8th and September 8th. Using 30 day realized volatility as a measure, it was chronicled by the Wall Street Journal on August 23rd that the 30 preceding trading days had been the least volatile for the S&P 500 in over two decades. It was perhaps no coincidence that the relative stability markets exhibited in August occurred during a month in which the central banking calendar was relatively light. Attention around the Federal Reserve (“Fed”) in August focused on whether or not U.S. monetary policy would be tightened at some point in 2016, and by the end of the month a tightening as soon as September seemed a real possibility. Strong economic data including a second month of better than expected payroll gains paired with ever more confident pronouncements from Fed officials that the time for tightening could be gradually high nudged expectations for more imminent Fed action higher through August. |

| Q. | What were the drivers behind Fund performance? |

| A. | Information Technology, Industrials and Consumer Staples were the strongest contributing sectors to S&P 500 performance. Real Estate, Financials, and Utilities were to weakest contributors to the performance. Amazon, Microsoft and Facebook were the strongest contributors to the Fund’s performance. Wells Fargo, Gilead and Allergan were the weakest contributors to the performance. |

| S&P 500 Index Fund | 11 |

Table of Contents

S&P 500 Index Fund

Performance Summary — September 30, 2016 (Unaudited)

| 12 | S&P 500 Index Fund |

Table of Contents

S&P 500 Index Fund

Performance Summary, continued — September 30, 2016 (Unaudited)

| (a) | Fair Value basis is inclusive of short-term investment in State Street Institutional U.S. Government Money Market Fund Class G Shares. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| S&P 500 Index Fund | 13 |

Table of Contents

S&P 500 Index Fund

Understanding Your Fund’s Expenses — September 30, 2016 (Unaudited)

| 14 | S&P 500 Index Fund |

Table of Contents

S&P 500 Index Fund

Schedule of Investments — September 30, 2016

See accompanying notes to financial statements.

| S&P 500 Index Fund | 15 |

Table of Contents

S&P 500 Index Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 16 | S&P 500 Index Fund |

Table of Contents

S&P 500 Index Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| S&P 500 Index Fund | 17 |

Table of Contents

S&P 500 Index Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 18 | S&P 500 Index Fund |

Table of Contents

S&P 500 Index Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| S&P 500 Index Fund | 19 |

Table of Contents

S&P 500 Index Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 20 | S&P 500 Index Fund |

Table of Contents

S&P 500 Index Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| S&P 500 Index Fund | 21 |

Table of Contents

S&P 500 Index Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 22 | S&P 500 Index Fund |

Table of Contents

S&P 500 Index Fund

Schedule of Investments, continued — September 30, 2016

Other Information:

The Fund had the following long futures contracts open at September 30, 2016:

| Description | Expiration date |

Number of Contracts |

Current Notional Value |

Unrealized Appreciation |

||||||||||||

| S&P 500 Emini Index Futures |

December 2016 | 7 | $ | 756,140 | $ | 4,441 | ||||||||||

|

|

|

|||||||||||||||

Affiliate Table

| Number of Shares Held at 9/30/15 |

Value At 9/30/15 |

Shares Purchased |

Shares Sold |

Number of Shares Held at 9/30/16 |

Value at 9/30/16 |

Dividend/ Interest Income |

Realized Gain (Loss) |

|||||||||||||||||||||||

| General Electric Co.* |

15,333 | $ | 386,698 | 1,497 | 9,438 | 7,392 | $ | 218,951 | $ | 8,882 | $ | 99,102 | ||||||||||||||||||

| State Street Corp. |

637 | 42,813 | 29 | 364 | 302 | 21,028 | 562 | 7,711 | ||||||||||||||||||||||

| State Street Institutional U.S. Government Money Market Fund - Class G Shares |

1,221,898 | 1,221,898 | 6,017,076 | 6,537,519 | 701,455 | 701,455 | 1,406 | — | ||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| $ | 941,434 | $ | 10,850 | $ | 106,813 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| * | Non-affiliated investment as of September 30, 2016. |

See accompanying notes to financial statements.

| S&P 500 Index Fund | 23 |

Table of Contents

U.S. Large-Cap Core Equity Fund

Portfolio Management Discussion and Analysis — September 30, 2016 (Unaudited)

| Q. | How did the GE Institutional U.S. Large-Cap Core Equity Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended September 30, 2016? |

| A. | For the twelve-month period ended September 30, 2016, the GE Institutional U.S. Large-Cap Core Equity Fund returned 11.67% for the Investment Class shares and 11.58% for the Service Class shares. The Fund’s benchmark, the S&P 500 Index returned 15.43% and the Fund’s Morningstar peer group of 1,576 U.S. Large Blend funds returned an average of 11.76% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |

| A. | It was a volatile year for U.S. stocks. However, the market climbed a wall of worry and turned in solid double-digit gains in the last 12 months. Markets rebounded from serial concerns ranging from China’s currency devaluation at the beginning of the period, to global slowdown and recession fears in early 2016, to Britain’s astonishing referendum vote to leave the European Union in late June. Despite these uncertainties, U.S. stocks ended the year near all-time highs. |

| Plunging worldwide interest rates motivated equity investors to reach for yield, causing defensive telecomm, utilities and staples to outperform (and become richly valued, in our view). Commodity prices were stronger this year helping the materials and energy sectors to outperform. Also strong were the cyclical industrials and information technology sectors. Rallies in semiconductors, internet and software companies underpinned strength in technology stocks. |

| Only three sectors underperformed the S&P 500 broad market return: financials, consumer discretionary and health care. Sector performance in financials was dampened by poor performance of rate-sensitive banks and life insurance companies. Consumer discretionary — last year’s top-performing sector — took a breather as investors fretted a slowdown in consumer spending and disruption of traditional media. Health care stocks were pressured by negative election year rhetoric around drug pricing. |

| Q. | What were the drivers behind Fund performance? |

| A. | The Fund performed approximately in-line with Morningstar’s average U.S. Large Blend manager in a challenging investment environment, underperforming the S&P 500 Index. Given our relative value approach, the portfolio was underweight defensive sectors that rallied (e.g., telecommunications, utilities and consumer staples). Financials weighed on returns, led by rate-sensitive insurance companies and banks, and asset managers that lagged. We reduced financials exposure during the period to reflect the Federal Reserve’s pushed-out path to interest rate normalization. Within consumer discretionary and information technology, not owning expensive growth-oriented Internet companies hurt relative performance. The Fund also failed to capture all of the upside in the commodity sectors, given an underweight in materials and underperformance among some of the Fund’s oil exploration and production holdings in energy. |

| Strong stock selection in health care offered a bright spot, helping performance. The Fund emphasized health care device companies that seemed to stay out of the cross hairs of negative drug pricing rhetoric. The Fund’s pharmaceutical holdings outperformed, not only in the reach for dividend yield but due to strong pipelines and fundamentals in many cases. Finally, the Fund benefited from strong stock selection in REITs, another yield sector. |

| The Fund does not invest in derivatives securities as part of its strategy, but may hold futures contracts or ETFs to equitize cash flows in advance of investment. The effect of derivatives on performance was de minimis for the year. |

| Q. | Were there any significant changes in the Fund during the period? |

| A. | There were no changes during the period in the portfolio management team or the team’s approach to investing. Health care has remained a key sector overweight. However, the Fund significantly reduced its industrials exposure during the year, taking profits as the global growth outlook faded on the margin. We initiated an overweight in utilities. The Fund also increased its exposure to energy and materials, reflecting our outlook for better fundamentals and commodity prices. Finally, the Fund increased its underweights in consumer staples and telecommunications, reflecting the lack of relative value in those sectors. |

| 24 | U.S. Large-Cap Core Equity Fund |

Table of Contents

U.S. Large-Cap Core Equity Fund

Performance Summary — September 30, 2016 (Unaudited)

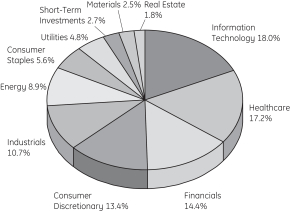

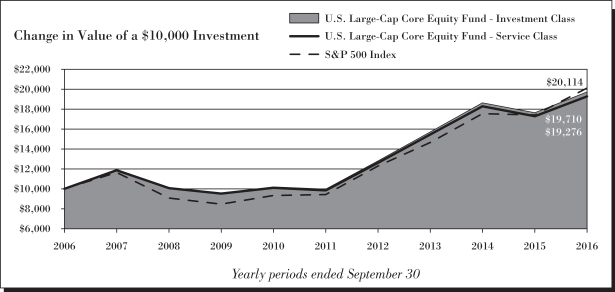

| U.S. Large-Cap Core Equity Fund | 25 |

Table of Contents

U.S. Large-Cap Core Equity Fund

Performance Summary, continued — September 30, 2016 (Unaudited)

| (a) | Fair Value basis is inclusive of short-term investment in State Street Institutional U.S. Government Money Market Fund Class G Shares. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| 26 | U.S. Large-Cap Core Equity Fund |

Table of Contents

U.S. Large-Cap Core Equity Fund

Understanding Your Fund’s Expenses — September 30, 2016 (Unaudited)

| U.S. Large-Cap Core Equity Fund | 27 |

Table of Contents

U.S. Large-Cap Core Equity Fund

Schedule of Investments — September 30, 2016

See accompanying notes to financial statements.

| 28 | U.S. Large-Cap Core Equity Fund |

Table of Contents

U.S. Large-Cap Core Equity Fund

Schedule of Investments, continued — September 30, 2016

Other Information:

The Fund had the following long futures contracts open at September 30, 2016:

| Description | Expiration date |

Number of Contracts |

Current Notional Value |

Unrealized Appreciation |

||||||||||||

| S&P 500 Emini Index Futures |

December 2016 | 2 | $ | 216,040 | $ | 854 | ||||||||||

|

|

|

|||||||||||||||

See accompanying notes to financial statements.

| U.S. Large-Cap Core Equity Fund | 29 |

Table of Contents

U.S. Large-Cap Core Equity Fund

Schedule of Investments, continued — September 30, 2016

Affiliate Table

| Number of Shares Held at 9/30/15 |

Value At 9/30/15 |

Shares Purchased |

Shares Sold |

Number of Shares Held at 9/30/16 |

Value at 9/30/16 |

Dividend/ Interest Income |

Realized Gain (Loss) |

|||||||||||||||||||||||||

| Financial Select Sector SPDR Fund |

7,859 | $ | 178,085 | 1,188 | 9,047 | — | $ | — | $ | 2,283 | $ | 82,314 | ||||||||||||||||||||

| Industrial Select Sector SPDR Fund |

14,295 | 713,178 | 5,057 | 19,352 | — | — | 13,753 | 253,911 | ||||||||||||||||||||||||

| State Street Institutional U.S. Government Money Market Fund - Class G Shares |

326,019 | 326,019 | 23,327,445 | 22,224,885 | 1,428,579 | 1,428,579 | 4,192 | — | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| $ | 1,428,579 | $ | 20,228 | $ | 336,225 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

See accompanying notes to financial statements.

| 30 | U.S. Large-Cap Core Equity Fund |

Table of Contents

Portfolio Management Discussion and Analysis — September 30, 2016 (Unaudited)

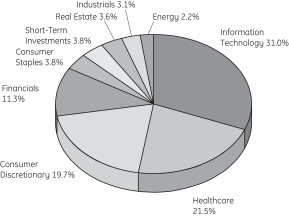

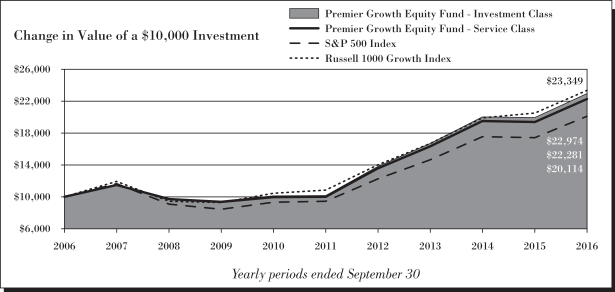

| Q. | How did the GE Institutional Premier Growth Equity Fund perform compared to its benchmarks and Morningstar peer group for the twelve-month period ended September 30, 2016? |

| A. | For the twelve-month period ended September 30, 2016, the GE Institutional Premier Growth Equity Fund returned 15.25% for the Investment Class shares and 14.99% for the Service Class shares. The Fund’s benchmarks, the S&P 500 Index and the Russell 1000 Growth Index returned 15.43% and 13.76%, respectively, and the Fund’s Morningstar peer group of 1,677 US Large Growth funds returned an average of 10.50% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |

| A. | It was a volatile year for U.S. stocks. However, the market climbed a wall of worry and turned in solid double-digit gains in the last 12 months. Markets rebounded from serial concerns ranging from China’s currency devaluation at the beginning of the period, to global slowdown and recession fears in early 2016, to Britain’s astonishing referendum vote to leave the European Union in late June. Despite these uncertainties, U.S. stocks ended the year near all-time highs. |

| Plunging worldwide interest rates motivated equity investors to reach for yield, causing defensive telecomm, utilities and staples to outperform (and become richly valued, in our view). Commodity prices were stronger this year helping the materials and energy sectors to outperform. Also strong were the cyclical industrials and information technology sectors. Rallies in semiconductors, internet and software companies underpinned strength in technology stocks. |

| Only three sectors underperformed the S&P 500 broad market return: financials, consumer discretionary and health care. Careful stock selection was warranted in financials, as persistent low rates pressured interest-rate sensitive banks and insurance companies. Consumer discretionary — last year’s top-performing sector — took a breather as investors fretted growth. Health care stocks fell under pressure, caught in a stream of negative election year rhetoric around drug pricing. As yield sectors led and commodity oriented sectors recovered, the large cap value style of investing outperformed large cap growth. |

| Q. | What were the drivers behind Fund performance? |

| A. | The Fund outperformed the Russell 1000 Growth Benchmark due to broad-based stock selection strength across the entire portfolio. Due to growth style headwinds, it slightly lagged the S&P 500 Index, net of fees. Consumer discretionary stock selection was a key positive performance driver, even as momentum reversed for the consumer cyclicals. The leading Internet retailer defied gravity as it took share from traditional retailers and asserted its leadership position in cloud computing services. In addition, a Macao-based casino company rebounded along with the Chinese gaming market and we eliminated the positon on strength. Several of the Fund’s U.S. media holdings demonstrated strong results, seemingly immune to economic growth fears. |

| Within financials, we avoided banks and insurance companies most leveraged to margin pressure from the low rate environment. Instead we held certain capital markets companies and diversified financials which discounted the potential for future rate increases early. On the other side of the financials barbell, the Fund’s sole Real Estate Investment Trust (“REIT”) holding also contributed to returns as the outlook for a Fed Funds rate increase got pushed out. In the information technology (“IT”) sector, the Fund benefited from strength among its communications equipment, internet and services holdings. |

| The Fund’s health care holdings trimmed relative performance as rhetoric around drug pricing intensified. One of our health care names was involved in a large M&A transaction that did not materialize, negatively impacting returns. We maintain conviction in this company’s ability to grow well on its own. We find health care’s superior growth rates and attractive valuations compelling, and believe the uncertainty overhang should begin to resolve post November 2016’s presidential election. |

| The Fund’s underweight positioning in defensive yield sectors modestly trimmed relative performance amid the year’s uncertainties. We do not see the combination of steady, visible double-digit earnings growth among the staples, telecomm and utilities sectors. Trading at rich multiples, these slower-growth areas of the market are unattractive at this point in the cycle. |

| The Fund does not invest in derivatives securities as part of its strategy, buy may hold futures contracts or ETFs to equitize cash flows in advance of investment. The effect of derivatives on performance was de minimis for the year. |

| Premier Growth Equity Fund | 31 |

Table of Contents

Premier Growth Equity Fund

Portfolio Management Discussion and Analysis, continued — September 30, 2016 (Unaudited)

| Q. | Were there any significant changes in the Fund during the period? |

| A. | There were no changes during the period in the portfolio management team or its approach to investing. Turnover remained relatively low in keeping with our long-term investment horizon, but did result in some changes in positioning. Among sectors, IT was the largest absolute weighting as the sector where we find many of the innovative, growth companies at reasonable valuations that we favor. We have modestly trimmed our exposure to IT in the past year. We also modestly reduced our financials exposure, and increased our overweight in health care. We eliminated our sole materials holding, increasing the Fund’s underweight in this commodity oriented sector. Consumer staples has been a consistent sector underweight, but that underweight was reduced somewhat over the last year due to outperformance in our sole holding, a beverage company. |

| 32 | Premier Growth Equity Fund |

Table of Contents

Premier Growth Equity Fund

Performance Summary — September 30, 2016 (Unaudited)

| Premier Growth Equity Fund | 33 |

Table of Contents

Premier Growth Equity Fund

Performance Summary, continued — September 30, 2016 (Unaudited)

| (a) | Fair Value basis is inclusive of short-term investment in State Street Institutional U.S. Government Money Market Fund Class G Shares. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| 34 | Premier Growth Equity Fund |

Table of Contents

Premier Growth Equity Fund

Understanding Your Fund’s Expenses — September 30, 2016 (Unaudited)

| Premier Growth Equity Fund | 35 |

Table of Contents

Premier Growth Equity Fund

Schedule of Investments — September 30, 2016

See accompanying notes to financial statements.

| 36 | Premier Growth Equity Fund |

Table of Contents

Premier Growth Equity Fund

Schedule of Investments, continued — September 30, 2016

Other Information:

The Fund had the following long futures contracts open at September 30, 2016:

| Description | Expiration date |

Number of Contracts |

Current Notional Value |

Unrealized Appreciation |

||||||||||||

| S&P 500 Emini Index Futures |

December 2016 | 30 | $ | 3,240,600 | $ | 22,586 | ||||||||||

|

|

|

|||||||||||||||

Affiliate Table

| Number of Shares Held at 9/30/15 |

Value At 9/30/15 |

Shares Purchased |

Shares Sold |

Number of Shares Held at 9/30/16 |

Value at 9/30/16 |

Dividend/ Interest Income |

Realized Gain (Loss) |

|||||||||||||||||||||||||

| State Street Institutional U.S. Government Money Market Fund - Class G Shares |

4,317,388 | $ | 4,317,388 | 93,824,923 | 85,297,584 | 12,844,727 | $ | 12,844,727 | $ | 19,746 | $ | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| $ | 12,844,727 | $ | 19,746 | $ | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

See accompanying notes to financial statements.

| Premier Growth Equity Fund | 37 |

Table of Contents

Portfolio Management Discussion and Analysis — September 30, 2016 (Unaudited)

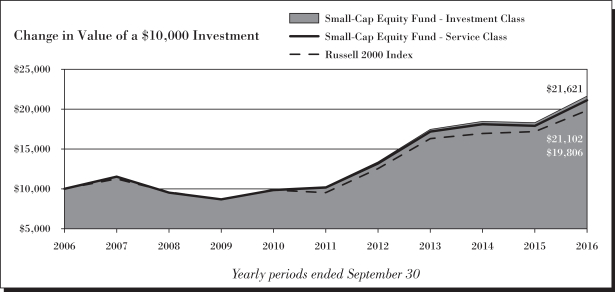

| Q. | How did the GE Institutional Small-Cap Equity Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended September 30, 2016? |

| A. | For the twelve-month period ended September 30, 2016, the GE Institutional Small-Cap Equity Fund returned 18.24% for the Investment Class shares and 17.96% for the Service Class shares. The Fund’s benchmark, the Russell 2000 Index returned 15.47% and the Fund’s Morningstar peer group of 857 US Small Blend funds returned an average of 13.08% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |

| A. | A strong rally in U.S. small cap equities helped propel the Fund throughout the 12 month period. Value and quality were rewarded earlier on in the year in a substantial way, which helped drive the returns of the Fund above the index especially in the industrials, healthcare, and technology sectors where the portfolio managers’ price discipline and preference for strong balance sheets led to excess returns. |

| Q. | What were the drivers behind Fund performance? |

| A. | Performance was driven largely by security selection. While each manager has their own unique style of investing, most of those were rewarded over the period. The Fund remained significantly underweight financials, which ended up being a mild additive as one of the more volatile components of the index (mortgage REITS) were not held in the portfolio. While approximately 1% of the Fund’s assets were invested in derivatives to equitize cash, they replicate the index performance and did not materially add or detract from performance. |

| Q. | Were there any significant changes in the Fund during the period? |

| A. | While, managers were rebalanced up and down towards the strategic weights in the fund, no significant changes were made to the overall Fund. |

| 38 | Small-Cap Equity Fund |

Table of Contents

Small-Cap Equity Fund

Performance Summary — September 30, 2016 (Unaudited)

| Small-Cap Equity Fund | 39 |

Table of Contents

Small-Cap Equity Fund

Performance Summary, continued — September 30, 2016 (Unaudited)

| (a) | Fair Value basis is inclusive of short-term investment in State Street Institutional U.S. Government Money Market Fund Class G Shares. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| 40 | Small-Cap Equity Fund |

Table of Contents

Small-Cap Equity Fund

Understanding Your Fund’s Expenses — September 30, 2016 (Unaudited)

| Small-Cap Equity Fund | 41 |

Table of Contents

Small-Cap Equity Fund

Schedule of Investments — September 30, 2016

See accompanying notes to financial statements.

| 42 | Small-Cap Equity Fund |

Table of Contents

Small-Cap Equity Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Small-Cap Equity Fund | 43 |

Table of Contents

Small-Cap Equity Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 44 | Small-Cap Equity Fund |

Table of Contents

Small-Cap Equity Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Small-Cap Equity Fund | 45 |

Table of Contents

Small-Cap Equity Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 46 | Small-Cap Equity Fund |

Table of Contents

Small-Cap Equity Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Small-Cap Equity Fund | 47 |

Table of Contents

Small-Cap Equity Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 48 | Small-Cap Equity Fund |

Table of Contents

Small-Cap Equity Fund

Schedule of Investments, continued — September 30, 2016

Other Information:

The Fund had the following long futures contracts open at September 30, 2016:

| Description | Expiration date |

Number of Contracts |

Current Notional Value |

Unrealized Appreciation |

||||||||||||

| Russell 2000 Mini Index Futures |

December 2016 | 209 | $ | 26,089,470 | $ | 128,327 | ||||||||||

|

|

|

|||||||||||||||

Affiliate Table

| Number of Shares Held at 9/30/15 |

Value At 9/30/15 |

Shares Purchased |

Shares Sold |

Number of Shares Held at 9/30/16 |

Value at 9/30/16 |

Dividend/ Interest Income |

Realized Gain (Loss) |

|||||||||||||||||||||||||

| State Street Institutional U.S. Government Money Market Fund - Class G Shares |

68,607,689 | $ | 68,607,689 | 335,101,289 | 335,420,772 | 68,288,206 | $ | 68,288,206 | $ | 157,078 | $ | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| $ | 68,288,206 | $ | 157,078 | $ | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

See accompanying notes to financial statements.

| Small-Cap Equity Fund | 49 |

Table of Contents

Portfolio Management Discussion and Analysis — September 30, 2016 (Unaudited)

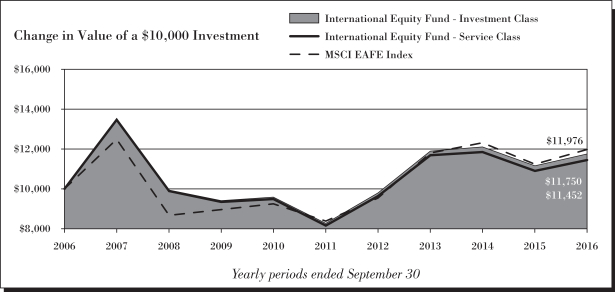

| Q. | How did the GE Institutional International Equity Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended September 30, 2016? |

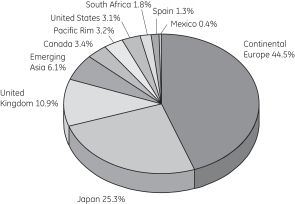

| A. | For the twelve-month period ended September 30, 2016, the GE Institutional International Equity Fund returned 5.32% for the Investment Class shares and 5.01% for the Service Class shares. The Fund’s benchmark, the MSCI® EAFE® Index returned 6.52% and the Fund’s Morningstar peer group of 879 Foreign Large Blend funds returned an average of 6.71% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |

| A. | The one-year period that ended September 30, 2016 began on a positive note with the market recovering from the late summer 2015 swoon that was brought about by fears of currency devaluation and an economic crash in China. As the situation stabilized and it appeared that China was not on the verge of collapse, the market surged last October. The good mood was not to last, however, and by late December, fear had returned to the market driven again by China worries as well as expectations of slower global growth. 2016 opened with one of the worst starts ever for equity markets. But in keeping with recent patterns, the weakness did not last. By the end of the quarter, the market had recovered most of what it had lost and was looking forward to its next source of turbulence: the U.K.’s coming referendum on European Union membership. By late June, when the Brexit vote took place, the market had enjoyed a few months of relative strength and most observers were expecting a close but nevertheless sensible vote to remain in the EU. The shock when the vote went the other way resulted in yet another swift market fall, followed, again, by a surprisingly quick recovery. By September of 2016, the MSCI® EAFE® Index was hitting its highs of the year, leading many to wonder if the market was being too complacent. |

| For the one-year period, the MSCI® EAFE® Index was up 6.5% in U.S. dollar terms. Earnings growth during this period was not strong causing the market P/E to rise from a slightly elevated 18.5 at the beginning of the year to an expensive 24.8 at the end. At this valuation, the question for investors is whether the market is being overly optimistic or is it correctly pricing in healthier future earnings growth. There are some signs of earnings improvement, with, for example, Europe recently seeing the first upgrades in over a year, but this trend will need to be sustained to justify current valuations. |

| Regionally, the Pacific Basin had the strongest return, up 20.0%, followed by Japan, +12.1%. Lagging on currency weakness was the U.K., up only 1.5% in U.S. dollars. |

| Commodity prices were stronger this year helping the materials and energy sectors to outperform. Also strong were the cyclical sectors of information technology (“IT”) and industrials. The weakest sectors were financials, where the profitability of banks came under increasing pressure due to persistent low interest rates, and healthcare. |

| Q. | What were the drivers behind Fund performance? |

| A. | The Fund underperformed its MSCI® EAFE® Index during the one-year period ended September 30, 2016. The biggest factor in this underperformance was the portfolio’s bank holdings. These included Japanese banks that were impacted by the Bank of Japan’s moves into negative interest rates, as well as European banks which were hit by economic weakness, low interest rates, and Brexit. As of September 30, 2016, we continued to hold most of these names based on their attractive valuations and potential upside from higher rates and improving economic growth. The Fund’s bank holdings as a group are relatively well-capitalized, have cut costs, have improving profitability, and are very cheap on a price to book basis. In the latest quarter, some of what we have been waiting for began to be seen as interest rates moved higher and economic growth expectations improved. This resulted in the banks industry generally and the Fund’s holdings even more so outperforming the market. |

| Another headwind experienced by the Fund during this period, was the outperformance of the defensive growth sector, consumer staples. Consumer staples names have surged this year with the popularity of low volatility and high yield factors. We consider many of these names to be overvalued relative to the growth that we expect them to deliver and have therefore mostly avoided them in the Fund. While this hurt the relative performance of the Fund over the past twelve months, we expect that over time the over-valuation in the sector is likely to correct. We saw some signs of this happening in the third quarter, when consumer staples was one of the worst performing sectors. |

| On the other side of the ledger, the Fund was helped by its holdings in and allocation to the information technology sector. IT is a place where we find many of the innovative, growing companies at reasonable valuations that we favor. Having an overweight to this sector helped relative performance, as IT in general outperformed the market, but it was the portfolio’s specific IT holdings that really added value, up more than 30% as a group. |

| 50 | International Equity Fund |

Table of Contents

International Equity Fund

Portfolio Management Discussion and Analysis, continued — September 30, 2016 (Unaudited)

| Derivatives did not have any material impact on Fund performance. |

| Q. | Were there any significant changes in the Fund during the period? |

| A. | There were no changes during the period in the portfolio management team or their approach to investing. Turnover remained relatively low in keeping with our long-term investment horizon, but did result in some changes in positioning. Regionally, the Fund’s weight in emerging market countries increased as a result of both outperformance and trading. The Fund’s overweight in Japan decreased somewhat but remained positive, a benefit to the Fund as that market is on pace for a fourth year in a row of outperformance versus the MSCI® EAFE® Index (measured in U.S. dollars). The Fund’s underweight in the Pacific region outside of Japan and in the U.K. both became larger over the past year. |

| Among sectors, IT was the largest overweight and that overweight has grown over the last year. Financials has gone from a small overweight to a moderate underweight, due in large part to recent reductions in Japanese banks. Consumer staples has been a consistent underweight, but that underweight was reduced somewhat over the last year. |

| International Equity Fund | 51 |

Table of Contents

International Equity Fund

Performance Summary — September 30, 2016 (Unaudited)

| 52 | International Equity Fund |

Table of Contents

International Equity Fund

Performance Summary, continued — September 30, 2016 (Unaudited)

| (a) | Fair Value basis is inclusive of short-term investment in State Street Institutional U.S. Government Money Market Fund Class G Shares. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| International Equity Fund | 53 |

Table of Contents

International Equity Fund

Understanding Your Fund’s Expenses — September 30, 2016 (Unaudited)

| 54 | International Equity Fund |

Table of Contents

International Equity Fund

Schedule of Investments — September 30, 2016

See accompanying notes to financial statements.

| International Equity Fund | 55 |

Table of Contents

International Equity Fund

Schedule of Investments, continued — September 30, 2016

Other Information:

The Fund had the following long futures contracts open at September 30, 2016:

| Description | Expiration date |

Number of Contracts |

Current Notional Value |

Unrealized Appreciation |

||||||||||||

| MSCI EAFE Mini Index Futures |

December 2016 | 16 | $ | 1,365,360 | $ | 17,674 | ||||||||||

|

|

|

|||||||||||||||

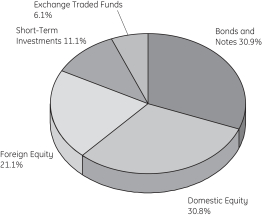

The Fund was invested in the following sectors at September 30, 2016 (unaudited):

See accompanying notes to financial statements.

| 56 | International Equity Fund |

Table of Contents

International Equity Fund

Schedule of Investments, continued — September 30, 2016

| Affiliate Table

|

||||||||||||||||||||||||||||||||

| Number of Shares Held at 9/30/15 |

Value At 9/30/15 |

Shares Purchased |

Shares Sold |

Number of Shares Held at 9/30/16 |

Value at 9/30/16 |

Dividend/ Interest Income |

Realized Gain (Loss) |

|||||||||||||||||||||||||

| State Street Institutional U.S. Government Money Market Fund - Class G Shares |

37,712,664 | $ | 37,712,664 | 285,263,981 | 283,948,962 | 39,027,683 | $ | 39,027,683 | $ | 67,198 | $ | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| $ | 39,027,683 | $ | 67,198 | $ | — | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

See accompanying notes to financial statements.

| International Equity Fund | 57 |

Table of Contents

Portfolio Management Discussion and Analysis — September 30, 2016 (Unaudited)

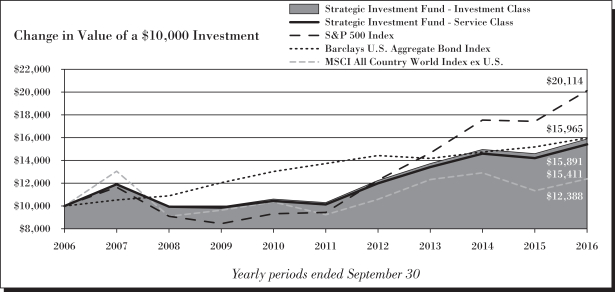

| Q. | How did the GE Institutional Strategic Investment Fund perform compared to its benchmarks and Morningstar peer group for the twelve-month period ended September 30, 2016? |

| A. | For the twelve-month period ended September 30, 2016, the GE Institutional Strategic Investment Fund returned 8.83% for the Investment Class shares and 8.53% for the Service Class shares. The Fund’s broad based benchmarks, the S&P 500 Index, the MSCI All Country World ex-US Index and the Barclays Capital U.S. Aggregate Bond Index returned 15.43%, 9.26% and 5.19%, respectively and the Fund’s Morningstar peer group of 951 U.S. Moderate Allocation funds returned an average of 9.02% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |

| A. | Over the last year, gains across markets have been strong. Continued economic expansion has supported risk appetite in equity and in credit fixed income markets. Meanwhile, accommodative monetary policy against a backdrop of modest growth and inflation have helped keep interest rates low and, therefore, returns in government bonds robust. |

| Q. | What were the drivers behind Fund performance |

| A. | In general an overweight allocation to equities was a positive contributor to performance as was a preference for U.S. equities relative to international equities. An underweight allocation to fixed income, offset by an overweight position in cash, acted as a drag on performance relative to our benchmark allocation given strong returns in bond markets. A small allocation to high yield bonds was beneficial to returns. |

| The Fund does employ the use of derivatives at times. In our fixed income portfolios, U.S. Treasury and Long Bond futures are used for access to government bond exposure and to manage duration within the portfolio. As such, changes in interest rates can impact the value of these securities. Moreover, for parts of the past year, we have used S&P 500 equity futures as a means of tactically managing our overall exposure to equity markets. Given the tactical nature of these holdings, we preferred this more nimble approach to changing our allocation to the underlying funds. As equity markets moved slightly higher during much of the third quarter, these vehicles acted as a modest detractor to performance in the aggregate, though they dampened volatility during the Brexit-related volatility sell-off in late-Q2 and the very early part of Q3. |

| Q. | Were there any significant changes in the Fund during the period? |

| A. | No, there were no significant changes to the Fund. |

| 58 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Performance Summary — September 30, 2016 (Unaudited)

| Strategic Investment Fund | 59 |

Table of Contents

Strategic Investment Fund

Performance Summary, continued — September 30, 2016 (Unaudited)

| (a) | Fair Value basis is inclusive of short-term investment in State Street Institutional U.S. Government Money Market Fund Class G Shares. |

| (b) | The securities information regarding holdings, allocations and other characteristics is presented to illustrate examples of securities that the Fund has bought and the diversity of areas in which the Fund may invest as of a particular date. It may not be representative of the Fund’s current or future investments and should not be construed as a recommendation to purchase or sell a particular security. |

See Notes to Performance beginning on page 1 for further information, including an explanation of Morningstar peer categories.

Past performance does not predict future performance. The performance shown in the graphs and tables does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| 60 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Understanding Your Fund’s Expenses — September 30, 2016 (Unaudited)

| Strategic Investment Fund | 61 |

Table of Contents

Strategic Investment Fund

Schedule of Investments — September 30, 2016

See accompanying notes to financial statements.

| 62 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Strategic Investment Fund | 63 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 64 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Strategic Investment Fund | 65 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 66 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Strategic Investment Fund | 67 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 68 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Strategic Investment Fund | 69 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 70 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Strategic Investment Fund | 71 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 72 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Strategic Investment Fund | 73 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 74 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Strategic Investment Fund | 75 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 76 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| Strategic Investment Fund | 77 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

See accompanying notes to financial statements.

| 78 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

Other Information:

Centrally Cleared Credit Default Swaps - Buy Protection

| Reference Entity | Counterparty | Notional Amount (000s omitted) |

Contract annual Fixed Rate |

Termination Date |

Market Value |

Unamortized Upfront Payments Received |

Unrealized Depreciation |

|||||||||||||||||||

| Markit CDX North America High Yield Index |

CME Group Inc. | $ | 11,900 | 5.00% | 12/20/20 | $ | (697,024 | ) | $ | (246,505 | ) | $ | (450,519 | ) | ||||||||||||

| Markit CDX North America Investment Grade Index |

CME Group Inc. | $ | 6,127 | 1.00% | 06/20/21 | $ | (88,770 | ) | $ | (74,464 | ) | $ | (14,306 | ) | ||||||||||||

|

|

|

|||||||||||||||||||||||||

| $ | (464,825 | ) | ||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||

See accompanying notes to financial statements.

| Strategic Investment Fund | 79 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

The Fund had the following long futures contracts open at September 30, 2016:

| Description | Expiration date |

Number of Contracts |

Current Notional Value |

Unrealized Appreciation |

||||||||||||

| MSCI EAFE Mini Index Futures |

December 2016 | 27 | $ | 2,304,045 | $ | 37,972 | ||||||||||

| S&P 500 Emini Index Futures |

December 2016 | 38 | 4,104,760 | 17,092 | ||||||||||||

| S&P Mid 400 Emini Index Futures |

December 2016 | 104 | 16,115,840 | 71,017 | ||||||||||||

| 2 Yr. U.S. Treasury Notes Futures |

December 2016 | 71 | 15,511,281 | 3,597 | ||||||||||||

| 5 Yr. U.S. Treasury Notes Futures |

December 2016 | 17 | 2,065,766 | 3,687 | ||||||||||||

|

|

|

|||||||||||||||

| $ | 133,365 | |||||||||||||||

|

|

|

|||||||||||||||

The Fund had the following short futures contracts open at September 30, 2016:

| Description | Expiration date |

Number of Contracts |

Current Notional Value |

Unrealized Appreciation (Depreciation) |

||||||||||||

| S&P 500 Emini Index Futures |

December 2016 | 145 | $ | (15,662,900 | ) | $ | (61,935 | ) | ||||||||

| U.S. Long Bond Futures |

December 2016 | 15 | (2,522,344 | ) | 10,753 | |||||||||||

| 10 Yr. U.S. Treasury Notes Futures |

December 2016 | 104 | (13,637,000 | ) | 10,650 | |||||||||||

|

|

|

|||||||||||||||

| $ | (40,532 | ) | ||||||||||||||

|

|

|

|||||||||||||||

| $ | 92,833 | |||||||||||||||

|

|

|

|||||||||||||||

The Fund was invested in the following countries/territories at September 30, 2016 (unaudited):

See accompanying notes to financial statements.

| 80 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

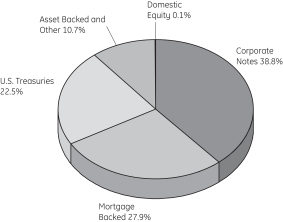

The Fund’s % share of investment in the various categories, based on Fair Value, is as follows at September 30, 2016 (unaudited):

| Industry | Domestic | Foreign | Total | |||||||||

| Exchange Traded Funds |

6.13% | 0.00% | 6.13% | |||||||||

| Diversified Banks |

2.11% | 2.04% | 4.15% | |||||||||

| Pharmaceuticals |

2.90% | 1.23% | 4.13% | |||||||||

| Healthcare Equipment |

0.82% | 1.39% | 2.21% | |||||||||

| Biotechnology |

1.71% | 0.43% | 2.14% | |||||||||

| Integrated Oil & Gas |

1.49% | 0.60% | 2.09% | |||||||||

| Cable & Satellite |

1.63% | 0.37% | 2.00% | |||||||||

| Internet Software & Services |

1.51% | 0.37% | 1.88% | |||||||||

| Technology Hardware, Storage & Peripherals |

1.53% | 0.29% | 1.82% | |||||||||

| Semiconductors |

0.90% | 0.87% | 1.77% | |||||||||

| Oil & Gas Exploration & Production |

0.94% | 0.32% | 1.26% | |||||||||

| Aerospace & Defense |

0.80% | 0.38% | 1.18% | |||||||||

| Communications Equipment |

0.73% | 0.30% | 1.03% | |||||||||

| Semiconductor Equipment |

0.58% | 0.41% | 0.99% | |||||||||

| Packaged Foods & Meats |

0.41% | 0.58% | 0.99% | |||||||||

| Movies & Entertainment |

0.76% | 0.20% | 0.96% | |||||||||

| Financial Exchanges & Data |

0.84% | 0.00% | 0.84% | |||||||||

| Industrial Machinery |

0.51% | 0.32% | 0.83% | |||||||||

| Data Processing & Outsourced Services |

0.72% | 0.01% | 0.73% | |||||||||

| Wireless Telecommunication Services |

0.00% | 0.72% | 0.72% | |||||||||

| Soft Drinks |

0.72% | 0.00% | 0.72% | |||||||||

| Systems Software |

0.71% | 0.00% | 0.71% | |||||||||

| Electrical Components & Equipment |

0.00% | 0.71% | 0.71% | |||||||||

| Internet & Direct Marketing Retail |

0.52% | 0.16% | 0.68% | |||||||||

| Electronic Equipment & Instruments |

0.00% | 0.66% | 0.66% | |||||||||

| Property & Casualty Insurance |

0.00% | 0.66% | 0.66% | |||||||||

| Auto Parts & Equipment |

0.00% | 0.65% | 0.65% | |||||||||

| Application Software |

0.35% | 0.30% | 0.65% | |||||||||

| Electric Utilities |

0.29% | 0.35% | 0.64% | |||||||||

| Specialized REITs |

0.62% | 0.00% | 0.62% | |||||||||

| Automobile Manufacturers |

0.10% | 0.50% | 0.60% | |||||||||

| Life & Health Insurance |

0.00% | 0.57% | 0.57% | |||||||||

| Multi-Line Insurance |

0.34% | 0.22% | 0.56% | |||||||||

| Asset Management & Custody Banks |

0.46% | 0.09% | 0.55% | |||||||||

| Diversified Real Estate Activities |

0.00% | 0.54% | 0.54% | |||||||||

| Multi-Utilities |

0.52% | 0.00% | 0.52% | |||||||||

| Consumer Finance |

0.52% | 0.00% | 0.52% | |||||||||

| Building Products |

0.00% | 0.50% | 0.50% | |||||||||

| Oil & Gas Equipment & Services |

0.34% | 0.14% | 0.48% | |||||||||

| Specialty Chemicals |

0.05% | 0.43% | 0.48% | |||||||||

| Housewares & Specialties |

0.44% | 0.00% | 0.44% | |||||||||

| Home Improvement Retail |

0.44% | 0.00% | 0.44% | |||||||||

| Personal Products |

0.00% | 0.43% | 0.43% | |||||||||

| Research & Consulting Services |

0.40% | 0.00% | 0.40% | |||||||||

| Trading Companies & Distributors |

0.39% | 0.00% | 0.39% | |||||||||

| Brewers |

0.00% | 0.39% | 0.39% | |||||||||

| Airlines |

0.38% | 0.00% | 0.38% | |||||||||

| Investment Banking & Brokerage |

0.37% | 0.00% | 0.37% | |||||||||

| Leisure Products |

0.00% | 0.31% | 0.31% | |||||||||

| Healthcare Services |

0.00% | 0.28% | 0.28% | |||||||||

| Security & Alarm Services |

0.00% | 0.27% | 0.27% | |||||||||

| Construction Materials |

0.00% | 0.26% | 0.26% | |||||||||

See accompanying notes to financial statements.

| Strategic Investment Fund | 81 |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

| Industry | Domestic | Foreign | Total | |||||||||

| Apparel, Accessories & Luxury Goods |

0.24% | 0.01% | 0.25% | |||||||||

| Construction Machinery & Heavy Trucks |

0.00% | 0.24% | 0.24% | |||||||||

| Electronic Components |

0.00% | 0.23% | 0.23% | |||||||||

| Advertising |

0.00% | 0.23% | 0.23% | |||||||||

| Home Building |

0.00% | 0.22% | 0.22% | |||||||||

| Industrial Gases |

0.08% | 0.13% | 0.21% | |||||||||

| Healthcare Supplies |

0.20% | 0.00% | 0.20% | |||||||||

| Industrial Conglomerates |

0.18% | 0.00% | 0.18% | |||||||||

| Household Products |

0.06% | 0.12% | 0.18% | |||||||||

| Hypermarkets & Super Centers |

0.17% | 0.01% | 0.18% | |||||||||

| General Merchandise Stores |

0.16% | 0.00% | 0.16% | |||||||||

| Gold |

0.14% | 0.01% | 0.15% | |||||||||

| Automotive Retail |

0.14% | 0.00% | 0.14% | |||||||||

| Diversified Metals & Mining |

0.00% | 0.13% | 0.13% | |||||||||

| Railroads |

0.00% | 0.13% | 0.13% | |||||||||

| Independent Power Producers & Energy Traders |

0.13% | 0.00% | 0.13% | |||||||||

| Air Freight & Logistics |

0.12% | 0.00% | 0.12% | |||||||||

| Hotels, Resorts & Cruise Lines |

0.12% | 0.00% | 0.12% | |||||||||

| Agricultural Products |

0.11% | 0.00% | 0.11% | |||||||||

| Human Resource & Employment Services |

0.00% | 0.10% | 0.10% | |||||||||

| Diversified Support Services |

0.00% | 0.06% | 0.06% | |||||||||

| Paper Packaging |

0.06% | 0.00% | 0.06% | |||||||||

| Drug Retail |

0.05% | 0.00% | 0.05% | |||||||||

| Thrifts & Mortgage Finance |

0.00% | 0.05% | 0.05% | |||||||||

| Department Stores |

0.00% | 0.03% | 0.03% | |||||||||

| IT Consulting & Other Services |

0.00% | 0.03% | 0.03% | |||||||||

| Food Retail |

0.00% | 0.02% | 0.02% | |||||||||

| Other Diversified Financial Services |

0.00% | 0.02% | 0.02% | |||||||||

| Highways & Railtracks |

0.00% | 0.01% | 0.01% | |||||||||

| Diversified REITs |

0.00% | 0.01% | 0.01% | |||||||||

| Construction & Engineering |

0.00% | 0.01% | 0.01% | |||||||||

| Household Appliances |

0.00% | 0.01% | 0.01% | |||||||||

| Real Estate Development |

0.00% | 0.01% | 0.01% | |||||||||

| Footwear |

0.00% | 0.01% | 0.01% | |||||||||

| Broadcasting |

0.00% | 0.00% | 0.00% | |||||||||

| Residential REITs |

0.00% | 0.00% | 0.00% | |||||||||

| Steel |

0.00% | 0.00% | 0.00% | |||||||||

|

|

|

|||||||||||

| 58.02% | ||||||||||||

|

|

|

|||||||||||

See accompanying notes to financial statements.

| 82 | Strategic Investment Fund |

Table of Contents

Strategic Investment Fund

Schedule of Investments, continued — September 30, 2016

Affiliate Table

| Number of Shares Held at 9/30/15 |

Value At 9/30/15 |

Shares Purchased |

Shares Sold | Number of Shares Held at 9/30/16 |

Value at 9/30/16 |

Dividend/ Interest Income |

Realized Gain (Loss) |

|||||||||||||||||||||||||

| Financial Select Sector SPDR Fund |

28,982 | $ | 656,732 | 3,846 | 32,828 | — | $ | — | $ | 8,380 | $ | 190,504 | ||||||||||||||||||||

| Industrial Select Sector SPDR Fund |

52,114 | 2,599,967 | 20,040 | 72,154 | — | — | 53,600 | 955,895 | ||||||||||||||||||||||||

| SPDR Barclays High Yield Bond ETF |

— | — | 632,267 | — | 632,267 | 23,216,844 | 395,283 | — | ||||||||||||||||||||||||

| State Street Institutional U.S. Government Money Market Fund - Class G Shares |

102,285,749 | 102,285,749 | 242,863,794 | 259,244,286 | 85,905,257 | 85,905,257 | 179,709 | — | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| $ | 109,122,101 | $ | 636,972 | $ | 1,146,399 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

See accompanying notes to financial statements.

| Strategic Investment Fund | 83 |

Table of Contents

Portfolio Management Discussion and Analysis — September 30, 2016 (Unaudited)

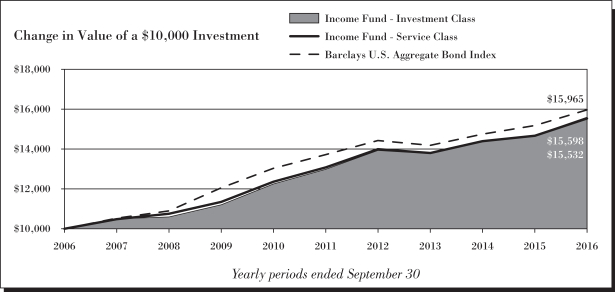

| Q. | How did the GE Institutional Income Fund perform compared to its benchmark and Morningstar peer group for the twelve-month period ended September 30, 2016? |

| A. | For the twelve-month period ended September 30, 2016, the GE Institutional Income Fund returned 6.18% for the Investment Class shares and 5.95% for the Service Class shares. The Fund’s benchmark, the Barclays Capital U.S. Aggregate Bond Index returned 5.19% and the Fund’s Morningstar peer group of 1,101 U.S. Intermediate-Term Bond funds returned an average of 5.29% over the same period. |

| Q. | What market conditions impacted the Fund’s performance? |