Jones Lang LaSalle Incorporated0001037976December 319,946,917,18149,885,103FY202110-KFALSETRUEDecember 31, 2021TRUEFALSE——0.8631327115230P3YP5Y———0.7—0.73.2—3.20.7—0.77.6—7.600010379762021-01-012021-12-3100010379762021-06-30iso4217:USD00010379762022-02-22xbrli:shares00010379762021-12-3100010379762020-12-310001037976jll:Longtermseniornotes4.4dueNovember2022Member2021-12-310001037976jll:Longtermseniornotes4.4dueNovember2022Member2020-12-310001037976us-gaap:LineOfCreditMember2021-12-310001037976us-gaap:LineOfCreditMember2020-12-310001037976us-gaap:SeniorNotesMember2021-12-310001037976us-gaap:SeniorNotesMember2020-12-31iso4217:USDxbrli:shares00010379762020-01-012020-12-3100010379762019-01-012019-12-310001037976us-gaap:CommonStockMember2018-12-310001037976us-gaap:AdditionalPaidInCapitalMember2018-12-310001037976us-gaap:RetainedEarningsMember2018-12-310001037976jll:SharesHeldInTrustMember2018-12-310001037976us-gaap:TreasuryStockMember2018-12-310001037976us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-12-310001037976us-gaap:NoncontrollingInterestMember2018-12-3100010379762018-12-310001037976us-gaap:RetainedEarningsMember2019-01-012019-12-310001037976us-gaap:NoncontrollingInterestMember2019-01-012019-12-310001037976us-gaap:CommonStockMember2019-01-012019-12-310001037976us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310001037976us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001037976jll:SharesHeldInTrustMember2019-01-012019-12-310001037976us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310001037976us-gaap:CommonStockMember2019-12-310001037976us-gaap:AdditionalPaidInCapitalMember2019-12-310001037976us-gaap:RetainedEarningsMember2019-12-310001037976jll:SharesHeldInTrustMember2019-12-310001037976us-gaap:TreasuryStockMember2019-12-310001037976us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310001037976us-gaap:NoncontrollingInterestMember2019-12-3100010379762019-12-310001037976us-gaap:RetainedEarningsMember2020-01-012020-12-310001037976us-gaap:NoncontrollingInterestMember2020-01-012020-12-310001037976us-gaap:CommonStockMember2020-01-012020-12-310001037976us-gaap:TreasuryStockMember2020-01-012020-12-310001037976jll:SharesHeldInTrustMember2020-01-012020-12-310001037976us-gaap:AccountingStandardsUpdate201613Memberus-gaap:RetainedEarningsMember2020-01-012020-12-310001037976us-gaap:AccountingStandardsUpdate201613Member2020-01-012020-12-310001037976us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310001037976us-gaap:CommonStockMember2020-12-310001037976us-gaap:AdditionalPaidInCapitalMember2020-12-310001037976us-gaap:RetainedEarningsMember2020-12-310001037976jll:SharesHeldInTrustMember2020-12-310001037976us-gaap:TreasuryStockMember2020-12-310001037976us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001037976us-gaap:NoncontrollingInterestMember2020-12-310001037976us-gaap:RetainedEarningsMember2021-01-012021-12-310001037976us-gaap:NoncontrollingInterestMember2021-01-012021-12-310001037976us-gaap:CommonStockMember2021-01-012021-12-310001037976us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001037976us-gaap:TreasuryStockMember2021-01-012021-12-310001037976jll:SharesHeldInTrustMember2021-01-012021-12-310001037976us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001037976us-gaap:CommonStockMember2021-12-310001037976us-gaap:AdditionalPaidInCapitalMember2021-12-310001037976us-gaap:RetainedEarningsMember2021-12-310001037976jll:SharesHeldInTrustMember2021-12-310001037976us-gaap:TreasuryStockMember2021-12-310001037976us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001037976us-gaap:NoncontrollingInterestMember2021-12-31jll:employeeutr:sqft0001037976jll:RealEstateServicesLeasingMember2021-01-012021-12-310001037976jll:RealEstateServicesLeasingMember2020-01-012020-12-310001037976jll:RealEstateServicesLeasingMember2019-01-012019-12-310001037976jll:RealEstateServicesCapitalMarketsAndHotelsMember2021-01-012021-12-310001037976jll:RealEstateServicesCapitalMarketsAndHotelsMember2020-01-012020-12-310001037976jll:RealEstateServicesCapitalMarketsAndHotelsMember2019-01-012019-12-310001037976jll:RealEstateServicesPropertyAndFacilitiesManagementMember2021-01-012021-12-310001037976jll:RealEstateServicesPropertyAndFacilitiesManagementMember2020-01-012020-12-310001037976jll:RealEstateServicesPropertyAndFacilitiesManagementMember2019-01-012019-12-310001037976jll:RealEstateServicesProjectAndDevelopmentServicesMember2021-01-012021-12-310001037976jll:RealEstateServicesProjectAndDevelopmentServicesMember2020-01-012020-12-310001037976jll:RealEstateServicesProjectAndDevelopmentServicesMember2019-01-012019-12-310001037976jll:RealEstateServicesAdvisoryConsultingAndOtherMember2021-01-012021-12-310001037976jll:RealEstateServicesAdvisoryConsultingAndOtherMember2020-01-012020-12-310001037976jll:RealEstateServicesAdvisoryConsultingAndOtherMember2019-01-012019-12-310001037976jll:LasalleInvestmentManagementMember2021-01-012021-12-310001037976jll:LasalleInvestmentManagementMember2020-01-012020-12-310001037976jll:LasalleInvestmentManagementMember2019-01-012019-12-3100010379762017-12-31xbrli:pure0001037976jll:OutofScopeofTopic606RevenueMember2021-01-012021-12-310001037976jll:OutofScopeofTopic606RevenueMember2020-01-012020-12-310001037976jll:OutofScopeofTopic606RevenueMember2019-01-012019-12-310001037976jll:AllowanceForDoubtfulAccountsCurrent.Member2020-12-310001037976jll:ASCTopic326OpeningBalanceAdjustmentMemberjll:AllowanceForDoubtfulAccountsCurrent.Member2020-12-310001037976jll:AllowanceForDoubtfulAccountsCurrent.Member2018-12-310001037976jll:AllowanceForDoubtfulAccountsCurrent.Member2021-01-012021-12-310001037976jll:AllowanceForDoubtfulAccountsCurrent.Member2020-01-012020-12-310001037976jll:AllowanceForDoubtfulAccountsCurrent.Member2019-01-012019-12-310001037976jll:AllowanceForDoubtfulAccountsCurrent.Member2021-12-310001037976jll:AllowanceForDoubtfulAccountsCurrent.Member2019-12-310001037976us-gaap:FurnitureAndFixturesMember2021-12-310001037976us-gaap:FurnitureAndFixturesMember2020-12-310001037976jll:ComputerEquipmentAndSoftwareMember2021-12-310001037976jll:ComputerEquipmentAndSoftwareMember2020-12-310001037976us-gaap:LeaseholdImprovementsMember2021-12-310001037976us-gaap:LeaseholdImprovementsMember2020-12-310001037976us-gaap:AutomobilesMember2021-12-310001037976us-gaap:AutomobilesMember2020-12-310001037976jll:JLLSparkGlobalVentureFundsDomain2021-12-310001037976jll:JLLSparkGlobalVentureFundsDomain2020-12-310001037976us-gaap:StockCompensationPlanMember2021-01-012021-12-31utr:Y0001037976srt:MinimumMemberus-gaap:FurnitureAndFixturesMember2021-01-012021-12-310001037976srt:MaximumMemberus-gaap:FurnitureAndFixturesMember2021-01-012021-12-310001037976jll:ComputerEquipmentAndSoftwareMembersrt:MinimumMember2021-01-012021-12-310001037976srt:MaximumMemberjll:ComputerEquipmentAndSoftwareMember2021-01-012021-12-310001037976srt:MinimumMemberus-gaap:LeaseholdImprovementsMember2021-01-012021-12-310001037976srt:MaximumMemberus-gaap:LeaseholdImprovementsMember2021-01-012021-12-310001037976us-gaap:AutomobilesMembersrt:MinimumMember2021-01-012021-12-310001037976srt:MaximumMemberus-gaap:AutomobilesMember2021-01-012021-12-310001037976srt:AmericasMemberjll:LeasingMember2021-01-012021-12-310001037976srt:AmericasMemberjll:LeasingMember2020-01-012020-12-310001037976srt:AmericasMemberjll:LeasingMember2019-01-012019-12-310001037976srt:AmericasMemberjll:CapitalMarketsMember2021-01-012021-12-310001037976srt:AmericasMemberjll:CapitalMarketsMember2020-01-012020-12-310001037976srt:AmericasMemberjll:CapitalMarketsMember2019-01-012019-12-310001037976jll:PropertyFacilityManagementMembersrt:AmericasMember2021-01-012021-12-310001037976jll:PropertyFacilityManagementMembersrt:AmericasMember2020-01-012020-12-310001037976jll:PropertyFacilityManagementMembersrt:AmericasMember2019-01-012019-12-310001037976jll:ProjectDevelopmentServicesMembersrt:AmericasMember2021-01-012021-12-310001037976jll:ProjectDevelopmentServicesMembersrt:AmericasMember2020-01-012020-12-310001037976jll:ProjectDevelopmentServicesMembersrt:AmericasMember2019-01-012019-12-310001037976jll:AdvisoryConsultingandOtherMembersrt:AmericasMember2021-01-012021-12-310001037976jll:AdvisoryConsultingandOtherMembersrt:AmericasMember2020-01-012020-12-310001037976jll:AdvisoryConsultingandOtherMembersrt:AmericasMember2019-01-012019-12-310001037976srt:AmericasMember2021-01-012021-12-310001037976srt:AmericasMember2020-01-012020-12-310001037976srt:AmericasMember2019-01-012019-12-310001037976us-gaap:EMEAMemberjll:LeasingMember2021-01-012021-12-310001037976us-gaap:EMEAMemberjll:LeasingMember2020-01-012020-12-310001037976us-gaap:EMEAMemberjll:LeasingMember2019-01-012019-12-310001037976us-gaap:EMEAMemberjll:CapitalMarketsMember2021-01-012021-12-310001037976us-gaap:EMEAMemberjll:CapitalMarketsMember2020-01-012020-12-310001037976us-gaap:EMEAMemberjll:CapitalMarketsMember2019-01-012019-12-310001037976us-gaap:EMEAMemberjll:PropertyFacilityManagementMember2021-01-012021-12-310001037976us-gaap:EMEAMemberjll:PropertyFacilityManagementMember2020-01-012020-12-310001037976us-gaap:EMEAMemberjll:PropertyFacilityManagementMember2019-01-012019-12-310001037976jll:ProjectDevelopmentServicesMemberus-gaap:EMEAMember2021-01-012021-12-310001037976jll:ProjectDevelopmentServicesMemberus-gaap:EMEAMember2020-01-012020-12-310001037976jll:ProjectDevelopmentServicesMemberus-gaap:EMEAMember2019-01-012019-12-310001037976us-gaap:EMEAMemberjll:AdvisoryConsultingandOtherMember2021-01-012021-12-310001037976us-gaap:EMEAMemberjll:AdvisoryConsultingandOtherMember2020-01-012020-12-310001037976us-gaap:EMEAMemberjll:AdvisoryConsultingandOtherMember2019-01-012019-12-310001037976us-gaap:EMEAMember2021-01-012021-12-310001037976us-gaap:EMEAMember2020-01-012020-12-310001037976us-gaap:EMEAMember2019-01-012019-12-310001037976jll:LeasingMembersrt:AsiaPacificMember2021-01-012021-12-310001037976jll:LeasingMembersrt:AsiaPacificMember2020-01-012020-12-310001037976jll:LeasingMembersrt:AsiaPacificMember2019-01-012019-12-310001037976jll:CapitalMarketsMembersrt:AsiaPacificMember2021-01-012021-12-310001037976jll:CapitalMarketsMembersrt:AsiaPacificMember2020-01-012020-12-310001037976jll:CapitalMarketsMembersrt:AsiaPacificMember2019-01-012019-12-310001037976jll:PropertyFacilityManagementMembersrt:AsiaPacificMember2021-01-012021-12-310001037976jll:PropertyFacilityManagementMembersrt:AsiaPacificMember2020-01-012020-12-310001037976jll:PropertyFacilityManagementMembersrt:AsiaPacificMember2019-01-012019-12-310001037976jll:ProjectDevelopmentServicesMembersrt:AsiaPacificMember2021-01-012021-12-310001037976jll:ProjectDevelopmentServicesMembersrt:AsiaPacificMember2020-01-012020-12-310001037976jll:ProjectDevelopmentServicesMembersrt:AsiaPacificMember2019-01-012019-12-310001037976jll:AdvisoryConsultingandOtherMembersrt:AsiaPacificMember2021-01-012021-12-310001037976jll:AdvisoryConsultingandOtherMembersrt:AsiaPacificMember2020-01-012020-12-310001037976jll:AdvisoryConsultingandOtherMembersrt:AsiaPacificMember2019-01-012019-12-310001037976srt:AsiaPacificMember2021-01-012021-12-310001037976srt:AsiaPacificMember2020-01-012020-12-310001037976srt:AsiaPacificMember2019-01-012019-12-310001037976jll:LasalleInvestmentManagementMemberjll:AdvisoryFeesMember2021-01-012021-12-310001037976jll:LasalleInvestmentManagementMemberjll:AdvisoryFeesMember2020-01-012020-12-310001037976jll:LasalleInvestmentManagementMemberjll:AdvisoryFeesMember2019-01-012019-12-310001037976jll:TransactionFeesOtherMemberjll:LasalleInvestmentManagementMember2021-01-012021-12-310001037976jll:TransactionFeesOtherMemberjll:LasalleInvestmentManagementMember2020-01-012020-12-310001037976jll:TransactionFeesOtherMemberjll:LasalleInvestmentManagementMember2019-01-012019-12-310001037976jll:IncentiveFeesMemberjll:LasalleInvestmentManagementMember2021-01-012021-12-310001037976jll:IncentiveFeesMemberjll:LasalleInvestmentManagementMember2020-01-012020-12-310001037976jll:IncentiveFeesMemberjll:LasalleInvestmentManagementMember2019-01-012019-12-310001037976jll:LasalleInvestmentManagementMember2021-01-012021-12-310001037976jll:LasalleInvestmentManagementMember2020-01-012020-12-310001037976jll:LasalleInvestmentManagementMember2019-01-012019-12-310001037976currency:USD2021-01-012021-12-310001037976currency:USD2020-01-012020-12-310001037976currency:USD2019-01-012019-12-310001037976currency:GBP2021-01-012021-12-310001037976currency:GBP2020-01-012020-12-310001037976currency:GBP2019-01-012019-12-310001037976currency:EUR2021-01-012021-12-310001037976currency:EUR2020-01-012020-12-310001037976currency:EUR2019-01-012019-12-310001037976currency:AUD2021-01-012021-12-310001037976currency:AUD2020-01-012020-12-310001037976currency:AUD2019-01-012019-12-310001037976currency:HKD2021-01-012021-12-310001037976currency:HKD2020-01-012020-12-310001037976currency:HKD2019-01-012019-12-310001037976currency:CNY2021-01-012021-12-310001037976currency:CNY2020-01-012020-12-310001037976currency:CNY2019-01-012019-12-310001037976currency:CAD2021-01-012021-12-310001037976currency:CAD2020-01-012020-12-310001037976currency:CAD2019-01-012019-12-310001037976currency:INR2021-01-012021-12-310001037976currency:INR2020-01-012020-12-310001037976currency:INR2019-01-012019-12-310001037976currency:SGD2021-01-012021-12-310001037976currency:SGD2020-01-012020-12-310001037976currency:SGD2019-01-012019-12-310001037976currency:JPY2021-01-012021-12-310001037976currency:JPY2020-01-012020-12-310001037976currency:JPY2019-01-012019-12-310001037976jll:OtherCurrenciesMember2021-01-012021-12-310001037976jll:OtherCurrenciesMember2020-01-012020-12-310001037976jll:OtherCurrenciesMember2019-01-012019-12-31jll:acquisition0001037976jll:OtherAcquisitionsMember2021-01-012021-12-310001037976jll:OtherAcquisitionsDomain2021-01-012021-12-310001037976us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001037976us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2020-12-310001037976srt:AmericasMember2019-12-310001037976us-gaap:EMEAMember2019-12-310001037976srt:AsiaPacificMember2019-12-310001037976jll:InvestmentManagementMember2019-12-310001037976jll:InvestmentManagementMember2020-01-012020-12-310001037976srt:AmericasMember2020-12-310001037976us-gaap:EMEAMember2020-12-310001037976srt:AsiaPacificMember2020-12-310001037976jll:InvestmentManagementMember2020-12-310001037976jll:InvestmentManagementMember2021-01-012021-12-310001037976srt:AmericasMember2021-12-310001037976us-gaap:EMEAMember2021-12-310001037976srt:AsiaPacificMember2021-12-310001037976jll:InvestmentManagementMember2021-12-310001037976srt:AmericasMemberjll:MortgageservicingrightsMember2019-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AmericasMember2019-12-310001037976us-gaap:OtherIntangibleAssetsMemberus-gaap:EMEAMember2019-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AsiaPacificMember2019-12-310001037976srt:AmericasMemberjll:MortgageservicingrightsMember2020-01-012020-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AmericasMember2020-01-012020-12-310001037976us-gaap:OtherIntangibleAssetsMemberus-gaap:EMEAMember2020-01-012020-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AsiaPacificMember2020-01-012020-12-310001037976srt:AmericasMemberjll:MortgageservicingrightsMember2020-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AmericasMember2020-12-310001037976us-gaap:OtherIntangibleAssetsMemberus-gaap:EMEAMember2020-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AsiaPacificMember2020-12-310001037976srt:AmericasMemberjll:MortgageservicingrightsMember2021-01-012021-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AmericasMember2021-01-012021-12-310001037976us-gaap:OtherIntangibleAssetsMemberus-gaap:EMEAMember2021-01-012021-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AsiaPacificMember2021-01-012021-12-310001037976srt:AmericasMemberjll:MortgageservicingrightsMember2021-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AmericasMember2021-12-310001037976us-gaap:OtherIntangibleAssetsMemberus-gaap:EMEAMember2021-12-310001037976us-gaap:OtherIntangibleAssetsMembersrt:AsiaPacificMember2021-12-310001037976jll:MortgageservicingrightsMember2021-01-012021-12-310001037976us-gaap:OtherIntangibleAssetsMember2021-01-012021-12-310001037976jll:MortgageservicingrightsMember2021-12-310001037976us-gaap:OtherIntangibleAssetsMember2021-12-310001037976jll:LasalleInvestmentCompanyIiMember2021-12-310001037976jll:LasalleInvestmentCompanyIiMember2020-12-310001037976jll:JLLTechnologiesMember2021-12-310001037976jll:JLLTechnologiesMember2020-12-310001037976jll:OtherInvestmentsAndAdvanceToAffiliatesSubsidiariesAssociatesAndJointVenturesMember2021-12-310001037976jll:OtherInvestmentsAndAdvanceToAffiliatesSubsidiariesAssociatesAndJointVenturesMember2020-12-31jll:investment0001037976jll:LasalleInvestmentManagementMember2021-12-310001037976jll:ConsolidatedVariableInterestEntitiesMember2021-12-310001037976jll:ConsolidatedVariableInterestEntitiesMember2020-12-310001037976jll:ConsolidatedVariableInterestEntitiesMember2021-01-012021-12-310001037976jll:ConsolidatedVariableInterestEntitiesMember2020-01-012020-12-310001037976jll:ConsolidatedVariableInterestEntitiesMember2019-01-012019-12-310001037976us-gaap:StockCompensationPlanMember2021-12-310001037976jll:JonesLangLasalleSavingsRelatedShareOptionPlanMemberus-gaap:EmployeeStockOptionMember2021-01-012021-12-310001037976jll:UKSaveAsYouEarnSayePlanMemberus-gaap:EmployeeStockOptionMember2021-12-310001037976us-gaap:RestrictedStockUnitsRSUMemberus-gaap:StockCompensationPlanMember2021-01-012021-12-310001037976us-gaap:RestrictedStockUnitsRSUMemberus-gaap:StockCompensationPlanMember2020-01-012020-12-310001037976us-gaap:RestrictedStockUnitsRSUMemberus-gaap:StockCompensationPlanMember2019-01-012019-12-310001037976us-gaap:StockCompensationPlanMemberus-gaap:PerformanceSharesMember2021-01-012021-12-310001037976us-gaap:StockCompensationPlanMemberus-gaap:PerformanceSharesMember2020-01-012020-12-310001037976us-gaap:StockCompensationPlanMemberus-gaap:PerformanceSharesMember2019-01-012019-12-310001037976jll:UKSaveAsYouEarnSayePlanMemberus-gaap:EmployeeStockOptionMember2021-01-012021-12-310001037976jll:UKSaveAsYouEarnSayePlanMemberus-gaap:EmployeeStockOptionMember2020-01-012020-12-310001037976jll:UKSaveAsYouEarnSayePlanMemberus-gaap:EmployeeStockOptionMember2019-01-012019-12-310001037976us-gaap:RestrictedStockUnitsRSUMember2018-12-310001037976us-gaap:PerformanceSharesMember2018-12-310001037976us-gaap:StockCompensationPlanMember2018-12-310001037976us-gaap:StockCompensationPlanMember2018-01-012018-12-310001037976us-gaap:RestrictedStockUnitsRSUMember2019-01-012019-12-310001037976us-gaap:PerformanceSharesMember2019-01-012019-12-310001037976us-gaap:StockCompensationPlanMember2019-01-012019-12-310001037976us-gaap:RestrictedStockUnitsRSUMember2019-12-310001037976us-gaap:PerformanceSharesMember2019-12-310001037976us-gaap:StockCompensationPlanMember2019-12-310001037976us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310001037976us-gaap:PerformanceSharesMember2020-01-012020-12-310001037976us-gaap:StockCompensationPlanMember2020-01-012020-12-310001037976us-gaap:RestrictedStockUnitsRSUMember2020-12-310001037976us-gaap:PerformanceSharesMember2020-12-310001037976us-gaap:StockCompensationPlanMember2020-12-310001037976us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001037976us-gaap:PerformanceSharesMember2021-01-012021-12-310001037976us-gaap:RestrictedStockUnitsRSUMember2021-12-310001037976us-gaap:PerformanceSharesMember2021-12-310001037976us-gaap:StockCompensationPlanMemberjll:HFFAcquisitionMember2021-12-310001037976jll:HFFAcquisitionMember2019-01-012019-12-310001037976jll:JonesLangLasalleSavingsRelatedShareOptionPlanMemberus-gaap:EmployeeStockOptionMemberjll:VestingPeriodOneMember2021-01-012021-12-310001037976jll:JonesLangLasalleSavingsRelatedShareOptionPlanMemberus-gaap:EmployeeStockOptionMemberjll:VestingPeriodTwoMember2021-01-012021-12-310001037976jll:UnitedStatesRetirementPlansOfUsEntityDefinedContributionMember2021-01-012021-12-310001037976jll:UnitedStatesRetirementPlansOfUsEntityDefinedContributionMember2020-01-012020-12-310001037976jll:UnitedStatesRetirementPlansOfUsEntityDefinedContributionMember2019-01-012019-12-310001037976jll:ForeignRetirementPlansDefinedContributionMember2021-01-012021-12-310001037976jll:ForeignRetirementPlansDefinedContributionMember2020-01-012020-12-310001037976jll:ForeignRetirementPlansDefinedContributionMember2019-01-012019-12-31jll:plan0001037976us-gaap:ForeignPlanMember2021-12-310001037976us-gaap:ForeignPlanMember2020-12-310001037976us-gaap:ForeignPlanMember2021-12-310001037976us-gaap:ForeignPlanMember2020-12-31jll:country0001037976country:HK2021-01-012021-12-310001037976country:SG2021-01-012021-12-310001037976country:SA2021-01-012021-12-310001037976us-gaap:DomesticCountryMember2021-12-310001037976us-gaap:StateAndLocalJurisdictionMember2021-12-310001037976us-gaap:ForeignCountryMember2021-12-310001037976jll:DeferredTaxAssetsOperatingLossCarryforwardsUtilizedOrExpiredMember2021-01-012021-12-310001037976jll:DeferredTaxAssetsOperatingLossCarryforwardsEstablishedOrContinuedMember2021-01-012021-12-31jll:statejll:city0001037976jll:ConclusionOfExaminationByTaxAuthoritiesMember2021-12-310001037976us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueMeasuredAtNetAssetValuePerShareMember2021-12-310001037976us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueMeasuredAtNetAssetValuePerShareMember2020-12-310001037976us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001037976us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001037976us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2020-12-310001037976us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2020-12-310001037976us-gaap:ForeignExchangeContractMember2021-12-310001037976us-gaap:ForeignExchangeContractMember2020-12-310001037976us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:InvestmentsMember2021-01-012021-12-310001037976us-gaap:FairValueInputsLevel3Memberus-gaap:DerivativeMemberus-gaap:FairValueMeasurementsRecurringMember2021-01-012021-12-310001037976us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberjll:EarnoutLiabilitiesMember2021-01-012021-12-310001037976us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2019-12-310001037976us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:InvestmentsMember2020-01-012020-12-310001037976us-gaap:FairValueInputsLevel3Memberus-gaap:DerivativeMemberus-gaap:FairValueMeasurementsRecurringMember2020-01-012020-12-310001037976us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberjll:EarnoutLiabilitiesMember2020-01-012020-12-3100010379762020-03-3100010379762021-03-310001037976jll:Longtermseniornotes4.4dueNovember2022Member2021-12-310001037976jll:Longtermseniornotes4.4dueNovember2022Member2020-12-310001037976jll:LongtermseniornotesEuronotes1.96dueJune2027Member2021-12-31iso4217:EUR0001037976jll:LongtermseniornotesEuronotes1.96dueJune2027Member2020-12-310001037976jll:LongtermseniornotesEuronotes2.21dueJune2029Member2021-12-310001037976jll:LongtermseniornotesEuronotes2.21dueJune2029Member2020-12-310001037976us-gaap:LineOfCreditMember2021-01-012021-12-310001037976us-gaap:LineOfCreditMember2020-01-012020-12-310001037976jll:AgreementExpiresSeptember192022ExtensionMember2021-01-012021-12-310001037976jll:AgreementExpiresSeptember192022ExtensionMember2021-12-310001037976jll:AgreementExpiresSeptember192022ExtensionMember2020-12-310001037976jll:AgreementExpiresSeptember162022ExtensionMember2021-01-012021-12-310001037976jll:AgreementExpiresSeptember162022ExtensionMember2021-12-310001037976jll:AgreementExpiresSeptember162022ExtensionMember2020-12-310001037976jll:AgreementExpiresAugust272022ExtensionMember2021-01-012021-12-310001037976jll:AgreementExpiresAugust272022ExtensionMember2021-12-310001037976jll:AgreementExpiresAugust272022ExtensionMember2020-12-310001037976jll:AgreementExpiresJuly302022ExtensionMember2021-01-012021-12-310001037976jll:AgreementExpiresJuly302022ExtensionMember2021-12-310001037976jll:AgreementExpiresJuly302022ExtensionMember2020-12-310001037976jll:FannieMaeASAPprogramMember2021-01-012021-12-310001037976jll:FannieMaeASAPprogramMember2021-12-310001037976jll:FannieMaeASAPprogramMember2020-12-310001037976jll:PNCAgreementHFFExtensionMemberMember2021-01-012021-12-310001037976jll:PNCAgreementHFFExtensionMemberMember2021-12-310001037976jll:PNCAgreementHFFExtensionMemberMember2020-12-310001037976jll:LineofCreditGrossMember2021-12-310001037976jll:LineofCreditGrossMember2020-12-310001037976us-gaap:WarehouseAgreementBorrowingsMember2021-12-310001037976us-gaap:WarehouseAgreementBorrowingsMember2020-12-310001037976us-gaap:EquityMethodInvesteeMember2021-01-012021-12-310001037976us-gaap:EquityMethodInvesteeMember2020-01-012020-12-310001037976us-gaap:EquityMethodInvesteeMember2019-01-012019-12-310001037976us-gaap:EquityMethodInvesteeMember2021-12-310001037976us-gaap:EquityMethodInvesteeMember2020-12-310001037976jll:LoansRelatedToCoInvestmentsMemberjll:EmployeesMember2021-12-310001037976jll:LoansRelatedToCoInvestmentsMemberjll:EmployeesMember2020-12-310001037976jll:TravelRelocationAndOtherMiscellaneousAdvancesMemberjll:EmployeesMember2021-12-310001037976jll:TravelRelocationAndOtherMiscellaneousAdvancesMemberjll:EmployeesMember2020-12-310001037976jll:EmployeesMember2021-12-310001037976jll:EmployeesMember2020-12-310001037976us-gaap:InsuranceClaimsMember2018-12-310001037976us-gaap:InsuranceClaimsMember2019-01-012019-12-310001037976us-gaap:InsuranceClaimsMember2019-12-310001037976us-gaap:InsuranceClaimsMember2020-01-012020-12-310001037976us-gaap:InsuranceClaimsMember2020-12-310001037976us-gaap:InsuranceClaimsMember2021-01-012021-12-310001037976us-gaap:InsuranceClaimsMember2021-12-310001037976us-gaap:EmployeeSeveranceMember2021-01-012021-12-310001037976us-gaap:EmployeeSeveranceMember2020-01-012020-12-310001037976us-gaap:EmployeeSeveranceMember2019-01-012019-12-310001037976jll:ContractTerminationAndOtherChargesMember2021-01-012021-12-310001037976jll:ContractTerminationAndOtherChargesMember2020-01-012020-12-310001037976jll:ContractTerminationAndOtherChargesMember2019-01-012019-12-310001037976jll:HFFAcquisitionMember2021-01-012021-12-310001037976jll:HFFAcquisitionMember2020-01-012020-12-310001037976us-gaap:EmployeeSeveranceMember2018-12-310001037976us-gaap:ContractTerminationMember2018-12-310001037976us-gaap:OtherRestructuringMember2018-12-310001037976us-gaap:ContractTerminationMember2019-01-012019-12-310001037976us-gaap:OtherRestructuringMember2019-01-012019-12-310001037976us-gaap:EmployeeSeveranceMember2019-12-310001037976us-gaap:ContractTerminationMember2019-12-310001037976us-gaap:OtherRestructuringMember2019-12-310001037976us-gaap:ContractTerminationMember2020-01-012020-12-310001037976us-gaap:OtherRestructuringMember2020-01-012020-12-310001037976us-gaap:EmployeeSeveranceMember2020-12-310001037976us-gaap:ContractTerminationMember2020-12-310001037976us-gaap:OtherRestructuringMember2020-12-310001037976us-gaap:ContractTerminationMember2021-01-012021-12-310001037976us-gaap:OtherRestructuringMember2021-01-012021-12-310001037976us-gaap:EmployeeSeveranceMember2021-12-310001037976us-gaap:ContractTerminationMember2021-12-310001037976us-gaap:OtherRestructuringMember2021-12-310001037976us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2019-12-310001037976us-gaap:AccumulatedTranslationAdjustmentMember2019-12-310001037976us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-01-012020-12-310001037976us-gaap:AccumulatedTranslationAdjustmentMember2020-01-012020-12-310001037976us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-12-310001037976us-gaap:AccumulatedTranslationAdjustmentMember2020-12-310001037976us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-01-012021-12-310001037976us-gaap:AccumulatedTranslationAdjustmentMember2021-01-012021-12-310001037976us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-12-310001037976us-gaap:AccumulatedTranslationAdjustmentMember2021-12-31

United States

Securities and Exchange Commission

Washington, D.C. 20549

Form 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Act of 1934

| | | | | | | | | | | |

| For the fiscal year ended | December 31, 2021 | Commission File Number | 1-13145 |

Jones Lang LaSalle Incorporated

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Maryland | 36-4150422 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 200 East Randolph Drive | Chicago, | IL | | | 60601 | |

| (Address of principal executive offices) | | (Zip Code) | |

| Registrant's telephone number, including area code: | | (312) | 782-5800 | | | | |

| | | | | | | | | | | | | | |

| |

| | |

| | |

| |

| | | | | | | | | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act: |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common Stock, par value $0.01 | | JLL | | The New York Stock Exchange |

| Securities registered pursuant to Section 12(g) of the Act: None |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such period that the registrant was required to submit such files). Yes x No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth corporation (as defined in Rule 12b-2 of the Exchange Act).

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | x | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

The aggregate market value of the voting stock (common stock) held by non-affiliates of the registrant as of the close of business on June 30, 2021 was $9,946,917,181.

The number of shares outstanding of the registrant's common stock (par value $0.01) as of the close of business on February 22, 2022 was 49,885,103.

Portions of the Registrant's Proxy Statement for its 2022 Annual Meeting of Shareholders are incorporated by reference in Part III of this report.

JONES LANG LASALLE INCORPORATED

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| | | | | | | | |

| | Page |

| | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | |

| Item 15. | | |

| Item 16. | | |

| | |

| | |

| | |

| | |

PART I

ITEM 1. BUSINESS

COMPANY OVERVIEW

Jones Lang LaSalle Incorporated, incorporated in 1997, is a Maryland corporation. References to “JLL,” “the Company,” “we,” “us” and “our” refer to Jones Lang LaSalle Incorporated and include all of its consolidated subsidiaries, unless otherwise indicated or the context requires otherwise. Our common stock is listed on The New York Stock Exchange ("NYSE") under the symbol “JLL.”

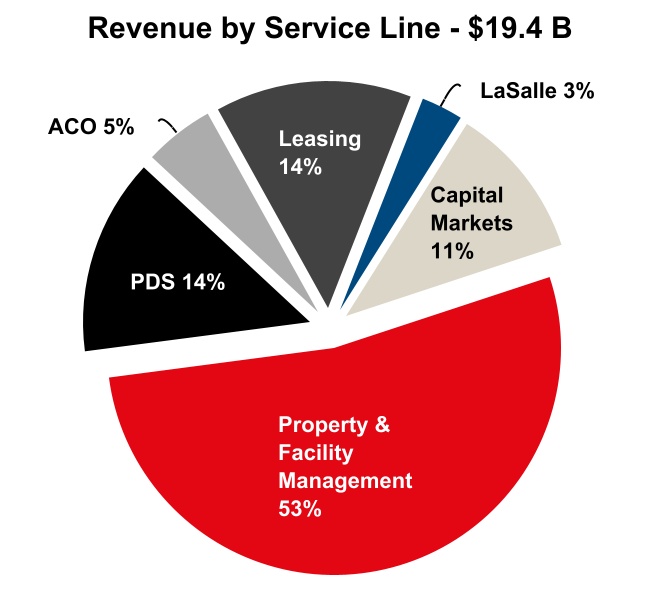

JLL is a leading professional services firm that specializes in real estate and investment management. We shape the future of real estate for a better world by using the most advanced technology to create rewarding opportunities, amazing spaces and sustainable real estate solutions for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $19.4 billion, operations in over 80 countries and a global workforce of over 98,000 as of December 31, 2021. We provide services for a broad range of clients who represent a wide variety of industries and are based in markets throughout the world. Our clients vary greatly in size and include for-profit and not-for-profit entities, public-private partnerships and governmental ("public sector") entities. Through LaSalle Investment Management, we invest for clients on a global basis in both private assets and publicly traded real estate securities.

Our global platform and diverse service and product offerings position us to take advantage of the opportunities in a consolidating industry and to successfully navigate the dynamic and challenging markets in which we compete worldwide.

We use JLL as our principal trading name. Jones Lang LaSalle Incorporated remains our legal name. JLL is a registered trademark in the countries in which we do business, as is our logo. In addition, LaSalle Investment Management, which uses LaSalle as its principal trading name, is a wholly-owned subsidiary of Jones Lang LaSalle Incorporated. LaSalle is also a registered trademark in the countries in which we conduct business, as is our logo.

Through December 31, 2021, we delivered an array of services across four business segments, managing our Real Estate Services (“RES”) offerings across three geographic segments (i) the Americas, (ii) Europe, Middle East and Africa ("EMEA"), and (iii) Asia Pacific, and managing our investment management business globally as (iv) LaSalle. In our Americas, EMEA and Asia Pacific segments, we provided a full range of leasing, capital markets, integrated property and facility management, project management, advisory, consulting, valuations and technology solutions services locally, regionally and globally. LaSalle is one of the world's largest and most diversified real estate investment management companies with $76.6 billion assets under management as of December 31, 2021.

Effective January 1, 2022, our Real Estate Services operations were reorganized into four global business segments focused on product offerings versus geographical alignment. The new RES segments are: (i) Markets Advisory, (ii) Capital Markets, (iii) Work Dynamics, and (iv) JLL Technologies ("JLLT"). Effective with financial reporting in 2022, prior period results will be restated to conform with our new organizational structure. We will continue to manage our investment management business globally as LaSalle, a distinct segment.

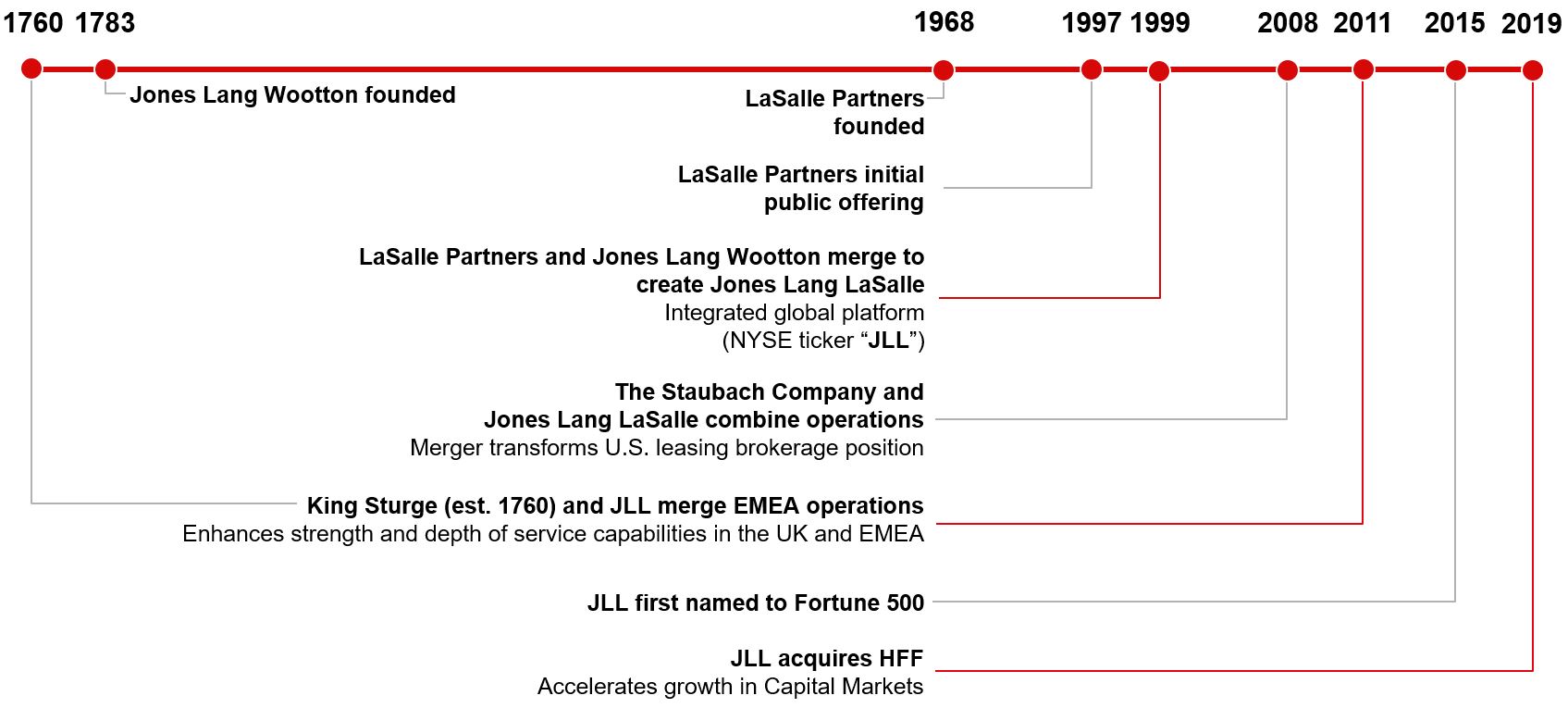

OUR HISTORY

We began to establish our network of services across the globe through the 1999 merger of the Jones Lang Wootton companies ("JLW", founded in England in 1783) with LaSalle Partners Incorporated ("LaSalle Partners", founded in the United States in 1968 and incorporated in 1997). We have grown our business by expanding our client base and the range of our services and products, both organically and through a series of mergers and acquisitions. Our extensive global platform and in-depth knowledge of local real estate markets enable us to serve as a single-source provider of solutions for the full spectrum of our clients' real estate needs. These mergers and acquisitions have given us additional share and scale in key geographical markets, expanded our capabilities in certain service offerings and further broadened the global platform we make available to our clients.

For information on recent acquisitions, refer to Note 4, Business Combinations, Goodwill and Other Intangible Assets, of the Notes to the Consolidated Financial Statements, included in Item 8.

A timeline of notable milestones in our history is illustrated below.

OUR SERVICES AND BUSINESS SEGMENTS

We are driven to shape the future of real estate for a better world. We do this by addressing the needs of real estate owners, occupiers and investors, leveraging our deep real estate expertise and experience to provide clients with a full range of services on a local, regional and global scale.

We offer our real estate services locally, regionally and globally to real estate owners, occupiers, investors and developers for a variety of property types, including (ordered alphabetically):

| | | | | | | | |

| • Critical Environments and Data Centers | • Hotels and Hospitality Facilities | • Office (including Flex Space) |

| • Cultural Facilities | • Industrial and Warehouse | • Residential (Individual and Multifamily) |

| • Educational Facilities | • Infrastructure Projects | • Retail and Shopping Malls |

| • Government Facilities | • Logistics (Sort & Fulfillment) | • Sports Facilities |

| • Healthcare and Laboratory Facilities | • Military Housing | • Transportation Centers |

We develop and activate technology to make real estate work for the long-term benefit of our people, clients and communities. Across our service lines, we offer and will continue to develop and invest in unique technology products and services that help us and our clients transform the way they acquire, operate, manage, and experience commercial real estate. Refer to the Technology portion of our Strategic Framework section below for additional information about our technology agenda.

We believe our market reach and depth of service offerings strengthen the long-term value of the enterprise in a number of ways, including: (i) reducing the potential impact of episodic volatility or disruption in any specific region; (ii) enhancing the expertise of our people through knowledge sharing across the globe to facilitate opportunities to engage clients across our service offerings; and (iii) allowing us to identify and quickly react to emerging trends, risks and opportunities.

The following reflects our revenue and fee revenue by service line for the year ended December 31, 2021:

To calculate fee revenue, we deduct directly reimbursed expenses from revenue and then exclude (i) net non-cash mortgage servicing rights and mortgage banking derivative activity and (ii) gross contract costs associated with client-dedicated labor, and third-party vendors and subcontractors. Refer to Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations for additional discussion of fee revenue, a non-GAAP measure, and reconciliation from the most comparable U.S. GAAP measure, Revenue.

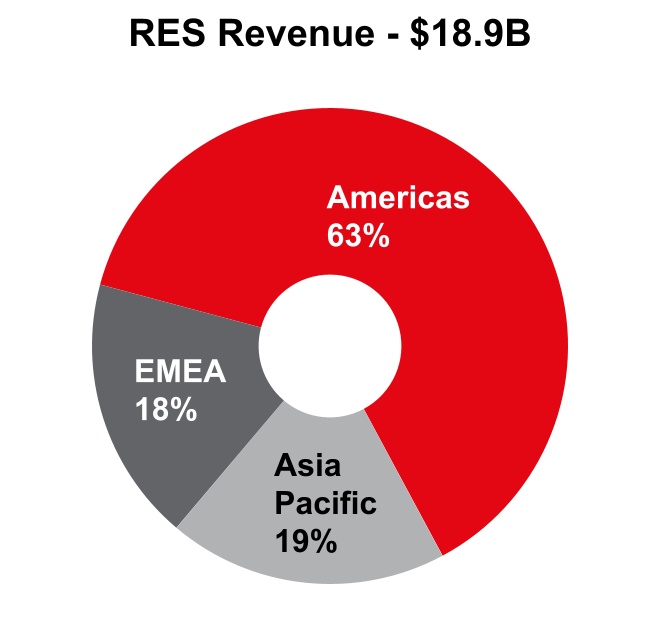

Real Estate Services: Americas, EMEA, and Asia Pacific

For the year ended December 31, 2021, our RES revenue and fee revenue was:

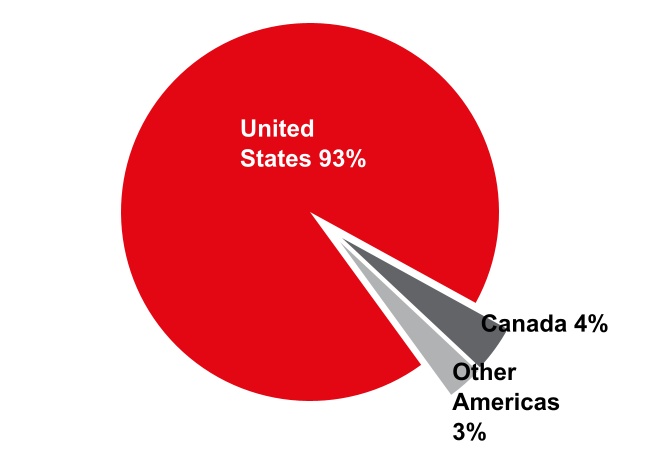

In the Americas, our RES revenue and fee revenue for 2021 was earned geographically as follows:

| | | | | |

Americas Revenue by Country - $11.9B | Americas Fee Revenue by Country - $4.9B |

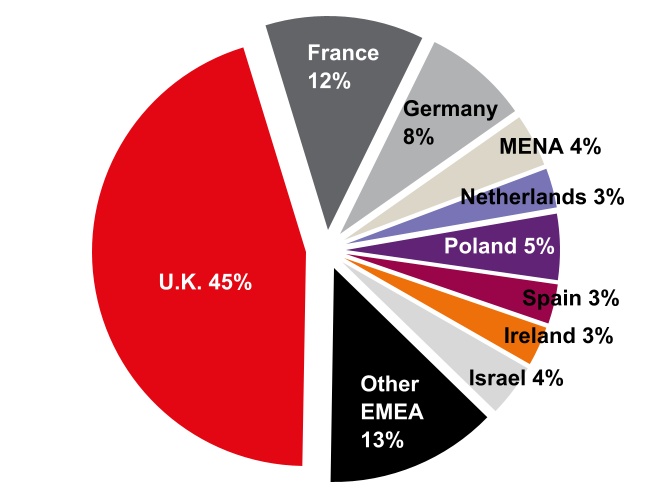

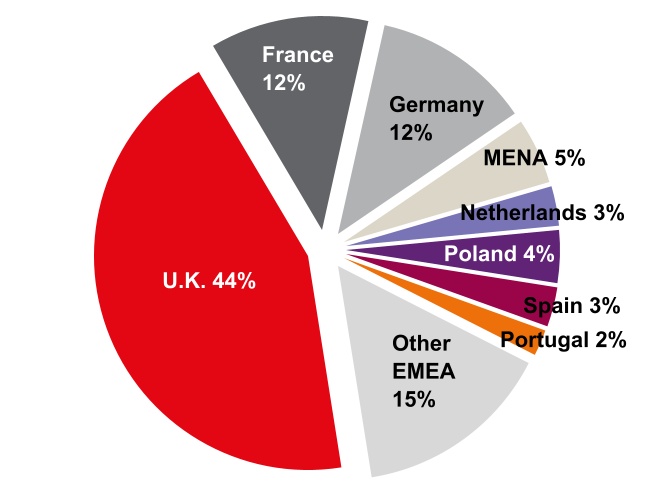

In EMEA, our RES revenue and fee revenue for 2021 was earned geographically as follows:

| | | | | |

EMEA Revenue by Country - $3.5B | EMEA Fee Revenue by Country - $1.6B |

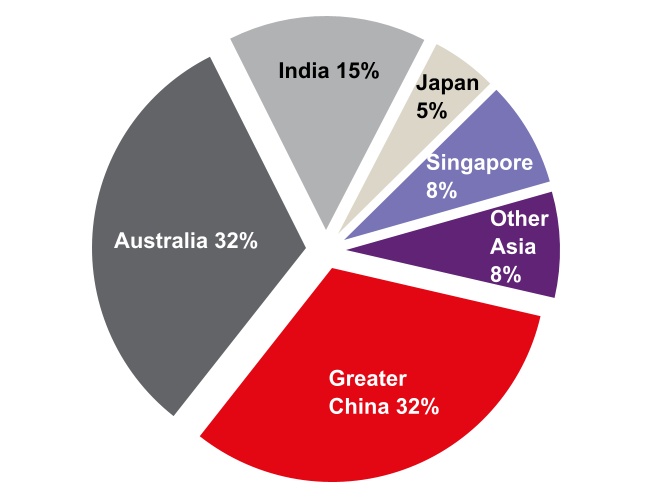

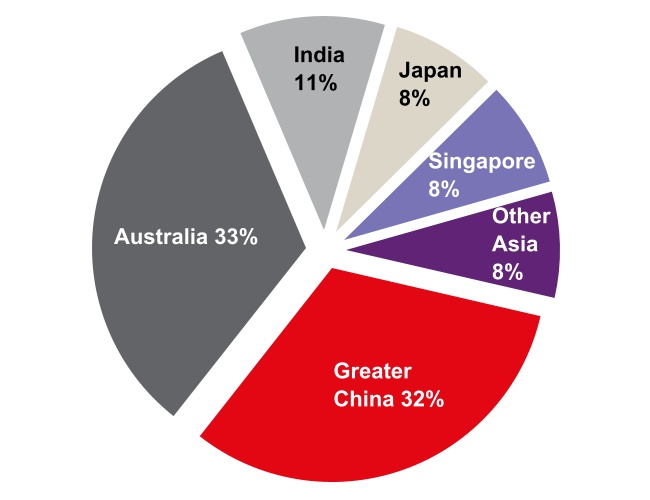

In Asia Pacific, our RES revenue and fee revenue for 2021 was earned geographically as follows:

| | | | | |

Asia Pacific Revenue by Country - $3.5B | Asia Pacific Fee Revenue by Country - $1.1B |

Our five RES service lines, and the services we provide within them, include:

1. Leasing

Agency Leasing executes leasing programs, including marketing, on behalf of property owners (including investors, developers, property-owning companies and public entities) to secure tenants and negotiate leases with terms that reflect our clients' best interests. In 2021, we completed approximately 15,200 agency leasing transactions representing 298 million square feet of space.

Tenant Representation establishes strategic alliances with occupier clients to help them evaluate and execute transactions to meet their occupancy requirements and ongoing real estate needs. We partner with clients to define space requirements, identify suitable alternatives, recommend appropriate occupancy solutions, and negotiate lease and ownership terms with landlords. Our involvement helps our clients reduce real estate costs, minimize occupancy risk, improve occupancy control and flexibility, and create more productive office environments. In 2021, we completed approximately 27,000 tenant representation transactions representing 722 million square feet of space.

Our agency leasing and tenant representation fees are typically based on a percentage of the value of the lease revenue commitment for executed leases, although in some cases they are based on a monetary amount per square foot leased.

2. Capital Markets serves our clients locally, regionally and globally by leveraging extensive knowledge of the commercial and residential real estate markets and our fully-integrated capital markets platform to provide a broad array of advisory services. Our services primarily include (ordered alphabetically):

| | | | | | | | |

| ● Corporate Capital Markets | | | | ● Investment sales and advisory |

| ● Debt advisory | | | | ● Loan sales |

● Equity advisory (funds and placement, M&A

and corporate advisory) | | | | ● Loan servicing |

In the U.S., we are an approved Freddie Mac, Fannie Mae and Housing and Urban Development/Ginnie Mae commercial multifamily lender and loan servicer. In addition, we are one of only 23 Fannie Mae Delegated Underwriting & Servicing ("DUS") lenders. M&A and corporate advisory include sourcing capital, both equity and debt, and other traditional investment banking services designed to assist investor and corporate clients in maximizing the value of their real estate. To meet client demands for selling and acquiring real estate assets internationally and investing outside of their home markets, our Capital Markets teams combine local market knowledge with our access to global capital sources to provide superior execution in raising capital for real estate transactions. By researching, developing and introducing innovative new financial products and strategies, Capital Markets is integral to the business development efforts of our other businesses.

Most of our revenues are in the form of fees, derived from the value of transactions we complete or securities we place. In certain circumstances, we receive retainer fees for portfolio advisory or consulting services. In addition, we also earn fees from commercial loan servicing activities.

For the year ended December 31, 2021, we provided capital markets services for approximately $315 billion of client transactions.

3. Property & Facility Management

Property Management provides on-site management services to real estate owners for office, industrial, retail, multifamily residential and specialty properties. We seek to leverage our market share and buying power to deliver superior service and value to our clients. Our extended delivery team includes our own personnel as well as third-party vendors and subcontractors, striving to maintain high levels of occupancy and tenant satisfaction while partnering with clients to reduce property operating costs. As of December 31, 2021, we provided on-site property management services for properties totaling approximately 3.9 billion square feet.

We typically provide property management services through an on-site general manager and staff. Our general managers are responsible for day-to-day property management activities, client satisfaction and financial results. We support them with regional supervisory teams and central resources in such areas as training, technical and environmental services, accounting, marketing, and human resources.

We are generally compensated based upon a percentage of cash collections we make on behalf of our clients or square footage managed; in some cases, management agreements provide for incentive compensation relating to operating expense reductions, gross revenue or occupancy objectives, or tenant satisfaction levels. Consistent with industry custom, management contract terms typically range from one to three years, although some contracts can be terminated at will at any time following a short notice period, usually 30 to 120 days, as is typical in the industry.

Integrated Facilities Management ("IFM") provides comprehensive facility management services to corporations and institutions that outsource the management of the real estate they occupy, typically those with large portfolios (usually over one million square feet) that offer significant opportunities to reduce costs, meet sustainability targets, improve service delivery and enhance end-user experience. Our IFM offering focuses on the work, worker and workplace to help clients achieve optimal financial and operational results from their facilities, while also enhancing the experience and productivity of the end-user. Our extended delivery team includes our own personnel as well as third-party vendors and subcontractors who can meet clients' needs by providing consistent service delivery worldwide and a single point of contact from their real estate service providers.

The scope of IFM solutions offered to clients generally fall within one of the following three categories:

•Full-service IFM outsourcing: Day-to-day operations management of client site locations, delivered through a globally integrated platform with standardized processes. Facilities under management cover all real estate asset classes, including corporate headquarters, distribution facilities, hospitals, research & development facilities, data centers and industrial complexes. As of December 31, 2021, IFM managed approximately 1.6 billion square feet of real estate for our clients.

•Technology-enabled IFM solutions: Technology is the backbone of our IFM offering. Facilities teams leverage advanced products to enhance the experience of end users as well as make faster and more informed decisions, manage compliance, and improve efficiency through automation, accountability, assets, and analytics. One example is Corrigo, which enables facilities managers to easily manage work orders, centralizing repair, maintenance, and analytics as well as automating tasks. We also provide technology-enabled predictive maintenance strategies and smart building technologies which can help extend the lifespan of costly equipment while preventing system failures.

•Mobile engineering services: We provide mobile engineering services to clients with large portfolios of sites or where we have multiple clients in proximity to each other. This model reduces clients' operating costs by offering a single point of contact for services, bundling on-site services, leveraging resources across multiple accounts, and reducing travel time between sites.

IFM contracts are typically structured to include reimbursement for costs of client-dedicated personnel and third-party vendors and subcontractors in addition to a base fee and performance-based fees. Performance-based fees result from achieving quantitative performance measures and/or target scores on recurring client satisfaction surveys. IFM agreements are typically three to seven years in duration, although most contracts can be terminated at will by the client upon a short notice period, usually 30 to 60 days, as is typical in the industry.

4. Project & Development Services provides consulting, design, management and build services to tenants of leased space, owners in self-occupied buildings and owners of real estate investments, leveraging technology to drive outstanding service delivery. We bring a "life cycle" perspective to our clients, from consulting and capital management through design, construction and occupancy. In addition, we provide these services to public-sector clients, particularly to military and government entities, as well as educational institutions, primarily in the U.S. and to a growing extent in other countries. Predominantly in Europe, we provide design, fit-out and refurbishment services under the Tétris brand.

Our Project & Development Services business is generally compensated on the basis of negotiated fees as well as reimbursement of costs when we are principal to a contract (or client). Individual projects are generally completed in less than one year, but client contracts may extend multiple years in duration and govern a number of discrete projects.

5. Advisory, Consulting and Other

Advisory and Consulting provides clients with specialized, value-added real estate consulting services in such areas as technology implementation and optimization, mergers and acquisitions advisory, asset management, occupier portfolio strategy, workplace solutions, location advisory, industry research, financial optimization strategies, organizational strategy and Six Sigma process solutions. Our professionals focus on translating global best practices into local real estate solutions, creating optimal financial and operational results for our clients across asset classes.

We typically negotiate compensation for Advisory and Consulting based on developed work plans that vary based on the scope and complexity of projects.

Valuation Advisory delivers customized solutions to enable clients to take the fastest, best informed decisions for their investment interests throughout the life cycle. The services include valuation, secured lending advisory, transaction support, data & analytics, development advisory, asset and infrastructure advisory, business valuation, property tax advisory, restructuring and complex litigation. We are a sector-based organization and have strong expertise in retail, alternatives & special use, infrastructure, public sector, office, residential, hotels & hospitality, agribusiness, healthcare, senior living, and industrial and logistics.

We usually negotiate compensation for Valuation Advisory services based on the scale and complexity of each assignment, and our fees typically relate in part to the value of the underlying assets.

Energy and Sustainability Services help occupiers and investors realize the positive impact of sustainability on their brand, workforce, financial statements and the environment. Like JLL, our clients are increasingly recognizing that there are both potential risks and opportunities associated with addressing the impacts of climate change, and are turning to partners like us for guidance and assistance. Our accredited energy and sustainability specialists worldwide assist clients with technologies and strategic solutions to deliver measurable improvements that yield clear environmental and societal benefits, as well as operational and cost efficiencies. This includes managing energy consumption and carbon footprint through sustainable construction and operations; providing green building assessments; leading green retrofits/upgrades; advising on occupier experience and engagement, advising on socio-economic impacts and site locations; and creating corporate social responsibility and sustainability reports. The breadth of our sustainability expertise positions us as the best choice to partner with clients, regardless of their focus, from leasing to capital markets transactions, and projects to facility management.

Refer to our latest Global Sustainability Report, available on our website, for metrics on documented energy savings, reduction in greenhouse gas emissions and the work of our sustainability teams.

We have a variety of compensation models for Energy and Sustainability Services including those based on shared savings as well as a fee for service, depending on the scale and complexity of the project.

Technology Services help organizations transform the way they acquire, operate, manage, and experience space. We offer multiple cloud-based software solutions that generate value for occupiers and investors by improving the quality of decision-making through improved data and analytics, delivering unique insights, and improving net operating income. For example, Building Engines serves as a comprehensive, easy-to-use system that unites all the technology and applications used to run buildings in one place, streamlining work orders, making maintenance more efficient, and simplifying interactions between building tenants, management and staff. Hank uses machine learning and AI to optimize building energy efficiency, air quality, maintenance costs, and tenant comfort, which ultimately delivers opportunities to reduce operating costs while accelerating the achievement of buildings’ sustainability goals. Corrigo enables facilities managers to easily manage work orders, centralizing repair, maintenance, and analytics as well as automating tasks. JLL Marketplace provides more transparency and efficiency to increase the flow of capital and improve quality of services delivered.

Work Dynamics

As a strategic partner of clients with a global footprint, Work Dynamics offers a single and cohesive team to clients in order to bring together services across our RES service lines, including partnering with other JLL professionals to help clients execute leasing and capital markets transactions. Our global delivery platform enables consistent outcomes on both a local and global scale, and places us in a small cohort of competitors who can deliver on clients’ multi-service, multi-geography needs.

Rapid and complex change, including digitization, increasing regulation, globalization and evolving workforce demographics, have transformed the world of work. Organizations are realizing the potential for workplaces and real estate portfolios to help address broader business objectives, such as talent attraction, customer experience, employee well-being and productivity, financial performance and environmental sustainability (See Growth of Corporate Outsourcing in the Industry Trends section below). As clients buy with an increasingly global and/or multi-service mindset, they are looking to simplify and consolidate their supply chain with more integrated solutions. This puts Work Dynamics in a unique position to help clients bring together their real estate ecosystem, simplify decision making and maximize value of their real estate investments.

While each client is unique, they are consistent in looking for real estate to enable business transformation around three key value levers: (1) making informed, data-driven decisions and digital transformation, (2) achieving operational excellence through improved productivity and financial performance, and (3) attracting and retaining key talent through an enhanced user experience.

| | | | | |

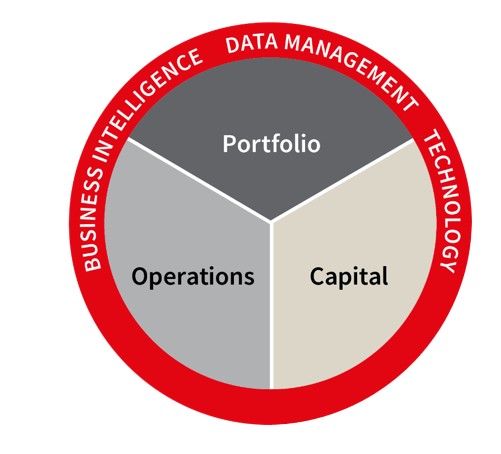

| Our offering addresses the entire life cycle, which we consider to include portfolio, capital and operations functions. |

Portfolio. Through the nexus of services our Work Dynamics business provides to clients, we gain deep knowledge and extensive data about their corporate real estate footprints, business strategies and organizational priorities. Combining this with the expertise we draw from JLL's integrated global platform, we advise clients on how to optimize their workplace strategies and occupancy planning efforts to improve utilization and ultimately enhance the productivity and well-being of those who use the space. More broadly, this advice may extend to our clients’ portfolio strategies, including location advisory, technology implementation and optimization, and options to add and integrate flexible space solutions. When evolution of strategies dictates change, our Work Dynamics business partners work with other professionals throughout our organization to help clients execute leasing, acquisition and disposition strategies. | |

Capital. Viewing workplaces as living environments that can help individuals, organizations and communities innovate and thrive, Work Dynamics advises clients about how and when to make critical capital decisions to maximize the human and financial returns on portfolio investments. Our design and build professionals work alongside clients to capture and advance their organization’s brand identity, purpose and sustainability commitments through the design of space they occupy, including owned, leased, static and flexible environments. We then manage, and in some cases are responsible for, the successful completion of the fit-out activities to achieve their vision. Helping our clients manage the costs they incur to realize their space and location objectives is essential to that strategy. When capital decisions involve a change in location, our relocation management professionals facilitate smooth transitions. |

Operations. IFM is our largest Work Dynamics service offering. Composed of integrated, digitally-enabled and flexible services that blend human, digital and experiential elements, this offering helps clients drive enhanced value from their facilities by improving operational performance and the experience of employees and other users of the space. Most frequently, new client relationships are formed through IFM business wins, which we accomplish through transitions from other service providers or conversions from insourced real estate management models. In addition to maximizing efficiency and quality of service delivery, our digitally-enabled platform also provides clients with opportunities to tailor the balance of services we provide versus what they self-perform. |

Business Intelligence, Data Management and Technology. Data and technology are core to all clients’ workplace and business transformation agendas. Our comprehensive data and technology platform underpins all of our offerings, helping clients make fast, informed decisions that enhance the performance of their workplaces, portfolios and people. Experts in our JLLT group guide clients’ selection, implementation and management of real estate-related software and applications. The Corrigo ecosystem opens new client segments by revolutionizing end-to-end facility repair and maintenance service delivery, and helping clients find the best service providers. |

LaSalle

Complementing our real estate services capabilities, our global real estate investment management business, LaSalle, is one of the world's largest managers of institutional and individual capital invested in real estate assets and securities. We seek to establish and maintain relationships of trust with sophisticated investors who value our global platform and extensive local market knowledge. Our three strategic priorities:

•Deliver superior risk-adjusted investment returns to our clients

•Develop and execute investment strategies that meet the specific investment objectives of our clients

•Deliver uniformly high levels of client service globally

LaSalle provides clients with a broad range of real estate investment products and services in private and public capital markets. We design these products and services to meet the differing strategic, asset allocation, risk/return and liquidity requirements of our clients. The range of investment solutions includes private and public equity investments in multiple real estate property types, including traditional sectors such as office, retail, industrial, and multifamily residential, as well as emerging or specialized sectors such as healthcare, life sciences, self-storage and data centers. We also have established commercial debt investment vehicles in Europe and North America that diversify our capital stack exposure. We act either through commingled investment funds or single client account relationships ("separate accounts"). We also offer global indirect investments, primarily in private equity funds, joint ventures and co-investments, as well as publicly traded real estate investment trusts ("REITs") and other real estate equities. Where consistent with client requirements and market terms and conditions, LaSalle retains JLL to provide services to assets in LaSalle funds in the ordinary course of business.

We believe LaSalle's success is the product of our strong investment performance, research capabilities, experienced investment professionals, innovative investment strategies, global presence and coordinated platform, local market knowledge and steadfast client focus.

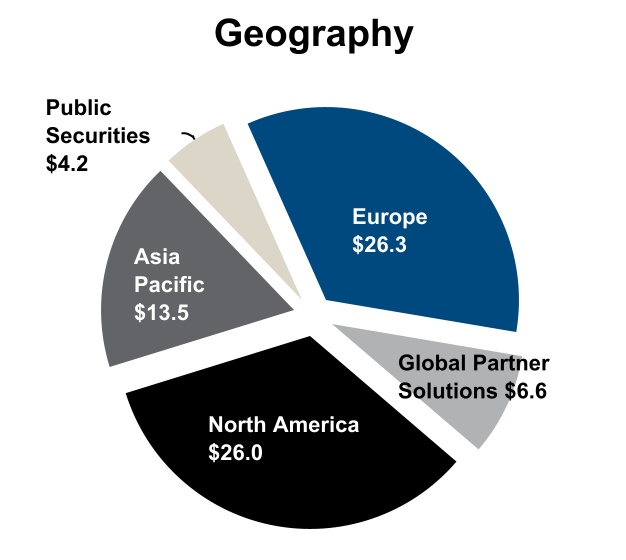

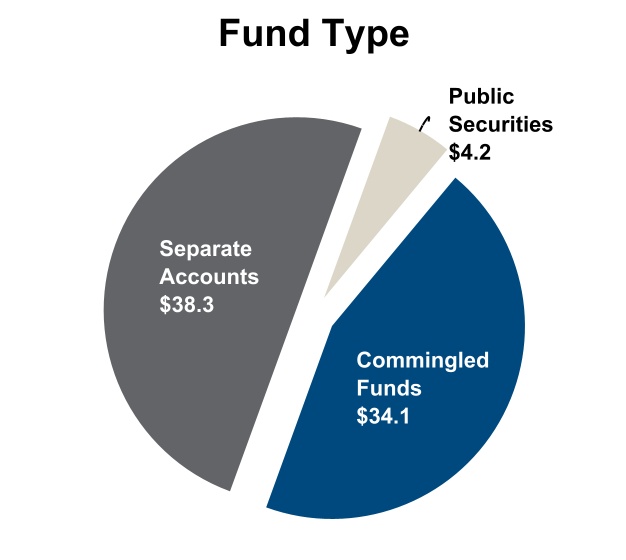

LaSalle launched its first institutional investment fund in 1979, making us one of the most experienced real estate focused investment managers in the industry. We have invested, on behalf of clients, in real estate assets in 28 countries around the globe, as well as in public real estate companies traded on all major stock exchanges. LaSalle's assets under management ("AUM") of $76.6 billion, as of December 31, 2021, by geographic distribution and fund type is detailed in the following graphics ($ in billions).

In serving our investment management clients, LaSalle is responsible for the acquisition, financing, leasing, management and divestiture of real estate investments across a broad range of real estate property types.

Some investors prefer to partner with investment managers who are willing to co-invest their own funds to more closely align the interests of the investor and the investment manager. We believe our ability to co-invest alongside our clients' funds will continue to be an important factor in maintaining and improving our competitive position. As of December 31, 2021, we had a total of $354.6 million of co-investments, alongside our clients, in real estate ventures included in total AUM.

LaSalle is generally compensated for investment management services for private equity investments based on capital committed, invested and managed (advisory fees), with additional fees (incentive fees) tied to investment performance above specific hurdles. In some cases, LaSalle also receives fees tied to acquisitions, financings and dispositions (transaction fees). Separate account advisory agreements generally have specific terms with "at will" termination provisions, and include fee arrangements linked to the market value of the AUM, plus incentive fees in some cases.

Our investment funds have various life spans, typically ranging between five and nine years, but in some cases are open ended. In 2021, our open-ended funds grew nearly 20% and represented approximately 30% AUM as of December 31, 2021.

ORGANIZATIONAL PURPOSE

JLL’s organizational purpose is to shape the future of real estate for a better world. Staying true to this purpose in all that we do enables us to fully align with the best interests and ambitions of our clients and all our stakeholders. It exemplifies our commitment to the highest standards of environmental, social and corporate governance ("ESG"), and to a more sustainable, diverse and inclusive future.

| | |

| We shape the future of real estate for a better world |

This core organizational purpose is fully aligned with, and supported by, our corporate values of teamwork, ethics and excellence. Ultimate responsibility for promoting awareness and ensuring adherence to our values and purpose across the enterprise is held by the JLL Global Executive Board ("GEB") and is endorsed by our Board of Directors. Our purpose guides our strategic growth vision and informs our response to the macro trends prevalent in the real estate industry. These trends and our strategic framework are summarized below.

INDUSTRY TRENDS

Informing our long-term growth strategy, we have identified five macro trends we see as major guiding influences on the continued growth and evolution of the real estate sector. Each of these trends has a multi-year lifespan, and while the COVID-19 pandemic (the "pandemic") has slowed some and accelerated others, we expect all five trends to maintain their long-term trajectory and relevance in the post-pandemic era. These macro trends are:

Rising investment allocations and globalization of capital flows to real estate

During the past decade, real estate has grown out of its previous 'alternative investment' classification to become a major defined asset class of its own, attracting a sustained long-term trend of rising investment allocations. While the initial impacts of the pandemic slowed all transactional markets during 2020, this trend strongly reasserted in 2021. As we move into the post-pandemic economy, pension companies and other institutional investors and capital sources continue to be drawn to real estate's attractive returns and distinctive investment characteristics.

Complementing this, we see long-term sustained strong transaction volumes and increasing capital flows across borders and between continents, creating new opportunities for advisors and investment managers equipped to source and facilitate these capital flows and execute cross-border transactions. Our real estate investment expertise, linking seamlessly across the world's major markets, is ideally placed to support our clients' investment ambitions.

Growth in corporate outsourcing

While corporate outsourcing of real estate services still represents a relatively small proportion of the total commercial-built real estate worldwide, the steady long-term trend towards outsourcing which began in the early 1990s, originally with U.S.-based corporations, is now a global trend. By focusing their own resources on core competencies and partnering with dedicated service providers like JLL to manage real estate strategy and activities, organizations are better positioned to advance their goals of financial and operational performance, talent attraction, customer experience, employee productivity and environmental sustainability.

In corporate boardrooms around the world, the pandemic has significantly enhanced the growing focus on reimagining workplaces and concepts for the future of work. These are areas in which JLL holds deep expertise and sector-leading specialist experience and resources. Across different industries we are positioned to provide highly adaptive and relevant solutions that promote organizational culture and prioritize health and well-being, flexible working models and technology enablement. In the post-pandemic era, we predict further growth in the strong and sustained trend for organizations to outsource real estate services while increasingly seeking strategic advice on reimagining their workspaces and workstyles to reinforce culture, attract talent and drive performance.

Urbanization

While the world of urban living and working was thrown into flux by the initial onset of the pandemic, we believe its foundations are deep and secure, and a dynamic future is already taking discernible shape. With the successful rollout of vaccination programs, the concentrations of culture, diversity, opportunity, facilities and creative expression in the world’s major cities will continue to attract strong inflows of ambitious and aspirational people. In the post-pandemic era, cities will again thrive, characterized by vibrant and reimagined office, cultural, retail and residential profiles.

Growth in major urban populations around the world will continue to be a prevalent trend, and with it comes increasing demand for all forms of real estate services and advice. JLL has a well-established global research series - the City Momentum Index - exploring this and associated trends in more depth, including related dynamics in the way the world’s 130 emerging and established markets are growing, adapting and evolving.

Fourth Industrial Revolution

The World Economic Forum defines the Fourth Industrial Revolution as the wave of change being driven through advances in technology, data and artificial intelligence. The real estate industry is affected in many ways, a few examples include: (1) the transition to flexible and hybrid office working models, (2) new data-driven understanding of how all forms of real estate can be more efficient, sustainable and productive, (3) the rise of experiential and online retail, (4) new asset management technologies, and (5) the growth of the logistics sector.

While there is currently no single technology disruptor positioned to dominate the real estate industry, there are thousands of start-ups, applications and concepts vying to transform the marketplace, collectively known as proptech. The challenge to innovate and maximize the current and future benefits of proptech is constant. At the heart of our Beyond strategy (discussed below), supported by major ongoing investments and innovations, we continue to accelerate progress toward our goal of becoming the widely-recognized leading user of technology and data in real estate.

Sustainability

Addressing and managing climate change and the finite nature of global resources are defining issues for our time. According to the International Energy Agency, real estate and the built environment account for nearly 40% of total global direct and indirect CO₂ emissions. At the same time, stakeholders are demanding greater focus on ESG from businesses and organizations in all areas of society. These and other factors, including heightened awareness of the importance of promoting health and well-being, coalesce into strong rising demand for sustainability services and advice across the real estate industry. JLL has identified meeting this demand as a major growth opportunity and priority, aligning with our purpose to shape the future of real estate for a better world.

Refer to our annual Global Sustainability Report for more detailed research, case studies and information, including JLL's commitment to net-zero carbon operations for our leased offices and updates on progress toward achieving our broader net-zero emissions target, which was certified to the new Net-Zero Standard by the Science Based Target initiative ("SBTi") in 2021.

STRATEGIC FRAMEWORK

Our GEB has set out the Beyond strategic vision and framework to deliver long-term sustainable and profitable global growth. This framework comprises broad strategic priorities grouped into five pillars – Clients, Brand, Technology, People and Values – which collectively support and drive our ambitious long-term growth trajectory.

Beyond: Our Strategic Vision for Long-Term Sustainable and Profitable Growth

Clients

We successfully completed a multi-year transformation program building fully integrated global organizational structures for all our business lines and functions. As a result, we are now even better positioned to provide seamless and highly consistent services to our clients across the world, as well as smoothly and rapidly deploy innovations, best practice and new technologies.

We continue to enhance our comprehensive service offering to create real value for our clients. Guided by our Beyond strategy, we are making significant ongoing investments in advanced client relationship management processes and tools, ensuring we can quickly assemble the best multidisciplinary teams and expertise tailored to meet each client’s requirements.

Brand

During the height of the pandemic and the subsequent economic recovery, JLL’s status as trusted adviser and partner to our clients has been readily apparent. Clients turned to us for solutions and insights to adapt their real estate strategies and operations to weather unprecedented challenges, and to plan ahead for the post-pandemic world. Our major research-led global focus on reimagining real estate ensured our brand and services were positioned in the vanguard of the industry’s response.

We continue to strengthen and expand awareness of our brand beyond the traditional real estate sector, with a focused goal in our Beyond strategic vision to reach more CEOs and other senior decision makers. Supporting this goal, we are an active strategic partner of the World Economic Forum, member of the World Green Building Council and a founding partner of Bloomberg Green. In November 2021, JLL actively supported the UN climate negotiations and participated in the events surrounding COP26 in Glasgow, UK. Further, in February 2022, Fortune magazine again named JLL as one of the World’s Most Admired Companies (refer to the Distinguishing Attributes and Competitive Differentiators section below for additional awards and recognition during the past year).

Technology

JLL is embracing technology to meet the needs of clients today and anticipate the opportunities of tomorrow. Leading this transformation is core to our growth strategy and reflected in our significant investments. JLLT is a global leader in proptech – expanding and refining our technology capabilities to deliver significant competitive advantage and value for our clients and our company. The group offers multiple cloud-based software solutions that generate value for occupiers and investors by improving the quality of decision-making leveraging data and analytics, delivering unique insights, and reduce operating costs. During 2021, we strengthened our tech capabilities and broadened our offerings by acquiring:

•Skyline, a leading artificial intelligence technology company which uses proprietary machine learning models to gain a competitive advantage in the origination and analysis of real estate opportunities for our producers

•Building Engines, a leading building operations platform

•Hank, a virtual engineering platform focused on sustainability.

Additionally, we continue to be committed to the Spark Global Venture funds, which incubate and drive proptech innovation as well as an increasing array of advanced market-leading technology products and data analytics tools. Visit our website at www.jll.com to see the full portfolio of technology offerings.

Within our own operations, the substantial platform technology investments we made in the early phases of our Beyond journey are benefiting all areas within our enterprise.

People

People are at the heart of our business. We are dedicated to helping our people achieve their ambitions by enabling them to explore new opportunities, build expertise, create long-term careers, and draw inspiration through working with talented colleagues and clients. We are committed to promoting and achieving true diversity and inclusion, as exemplified by the composition of our highly talented and experienced Board of Directors.

Global economic recovery during 2021 has further accelerated the war for talent, resulting in highly fluid and competitive recruitment markets. A successful enterprise-wide coordinated talent strategy is central to our Beyond vision and delivery. This strategy ensures JLL is positioned as an employer of choice for top talent, achieving and sustaining a diverse, inclusive and collaborative culture that strongly appeals to our people and our clients alike.

Values

All of our people are committed to the core values of teamwork, ethics and excellence. These values are the foundation of our organization. Clients, employees, business partners and potential recruits are strongly attracted to these values and to our commitments to strong ESG, including ambitious goals and regular transparent reporting.

In September 2020, we signed the World Green Building Council’s Net Zero Carbon Buildings Commitment, pledging to achieve net zero carbon emissions from JLL-occupied buildings by 2030. Building on this pledge, in October 2021, the SBTi certified our commitment to reach net zero greenhouse gas emissions across our value chain by 2040. This places JLL among a select group of global companies to be recognized for aligning its net zero commitments with climate science. Within this overall target, JLL has committed to:

1.A near-term target to reduce absolute scope 1, 2 and 3 emissions by 51% by 2030 from a 2018 base year

2.A long-term target to reduce absolute scope 1, 2 and 3 emissions by 95% by 2040 from a 2018 base year

We have earned repeated recognition from organizations such as the Ethisphere Institute, which has named JLL as one of the World’s Most Ethical Companies every year since 2008.

In addition, during the fourth quarter of 2021, JLL collaborated with the World Economic Forum in establishing 10 Green Building Principles to guide real estate investors and corporate occupiers on implementing and achieving their net zero targets across their portfolios.

Growth

Our Beyond priorities for Clients, Brand, Technology, People and Values combine to provide an integrated strategic vision and platform for growth. This vision is supported by our commitment to enhance productivity, optimize sustainable and profitable long-term growth, and create value for all of our stakeholders. It embraces our opportunity to play a leading role in understanding and guiding the future of work, workplaces and cities, while enabling clients and communities to deliver on their sustainability targets and ambitions. It recognizes and leverages the vital part continuing innovations in data and technology will play, ensuring JLL has the products and data-driven insights to lead this wave of change.

Our growth strategy and strategic vision places a central focus on diversity and inclusion, ensuring we attract and retain a truly diverse, inclusive and talented global workforce, committed to inspiring each other and delivering outstanding results for our clients.

All of which is infused through our closely integrated global platform and vibrant business culture, combining deep local market knowledge with seamless advice and services tailored to each client’s specific needs.

SUSTAINING OUR ENTERPRISE: A BUSINESS MODEL THAT COMBINES DIFFERENT CAPITAL TO CREATE STAKEHOLDER VALUE

As referenced above, the built environment is estimated to account for over one-third of global final energy consumption and nearly 40% of total direct and indirect CO2 emissions, meaning JLL can have a significant impact through the work we do with our clients as well as in our workplaces and communities. | | | | | |

| Our Global Sustainability Program | |