UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________

FORM 10-K

_____________________

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number 1-12981

_____________________

(Exact name of registrant as specified in its charter)

_____________________

(State or other jurisdiction of

incorporation or organization)

(Address of principal executive offices)

(I.R.S. Employer

Identification No.)

(Zip Code)

Registrant’s telephone number, including area code: (610 ) 647-2121

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Trading symbol(s)

Name of each exchange on which registered

Securities registered pursuant to Section 12(g) of the Act: None

_____________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

☒ | Accelerated filer | ☐ | ||||||||||||

Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting stock held by non-affiliates of the registrant was approximately $37.3 billion as of June 30, 2023, the last business day of the registrant’s most recently completed second fiscal quarter.

The number of shares of the registrant’s Common Stock outstanding as of January 31, 2024 was 231,012,685 .

Documents Incorporated by Reference

AMETEK, Inc.

2023 Form 10-K Annual Report

Table of Contents

| Page | ||||||||

1

PART I

Item 1. Business

General Development of Business

AMETEK, Inc. (“AMETEK” or the “Company”) is incorporated in Delaware. Its predecessor was originally incorporated in Delaware in 1930 under the name American Machine and Metals, Inc. AMETEK is a leading global manufacturer of electronic instruments and electromechanical devices with operations in North America, Europe, Asia and South America. AMETEK maintains its principal executive offices at 1100 Cassatt Road, Berwyn, Pennsylvania, 19312. Listed on the New York Stock Exchange (symbol: AME), the common stock of AMETEK is a component of the Standard and Poor’s 500 and the Russell 1000 Indices.

Products and Services

AMETEK’s products are marketed and sold worldwide through two operating groups: Electronic Instruments (“EIG”) and Electromechanical (“EMG”). Electronic Instruments is a leader in the design and manufacture of advanced instruments for the process, power and industrial, and aerospace markets. Electromechanical is a differentiated supplier of precision motion control solutions, thermal management systems, specialty metals and electrical interconnects. Its end markets include aerospace and defense, medical, automation and other industrial markets.

Competitive Strengths

Management believes AMETEK has significant competitive advantages that help strengthen and sustain its market positions. Those advantages include:

Significant Market Share. AMETEK maintains significant market share in a number of targeted niche markets through its ability to produce and deliver high-quality, differentiated products at competitive prices. EIG has significant market positions in niche segments of the process, power and industrial, and aerospace markets. EMG holds significant positions in niche segments of the aerospace and defense, automation and medical markets.

Technological and Development Capabilities. AMETEK believes it has certain technological advantages over its competitors that allow it to maintain its leading market positions. Historically, the Company has demonstrated an ability to develop innovative new products and solutions that support customer needs. AMETEK has consistently added to its investment in research, development and engineering, and improved its new product development efforts with the adoption of Design for Six Sigma and Value Analysis/Value Engineering methodologies. These have improved the pace and quality of product innovation and resulted in the introduction of a steady stream of new products across all of AMETEK’s businesses and aligned with attractive secular growth markets.

Efficient and Flexible Manufacturing Operations. Through its Operational Excellence initiatives, AMETEK has established a lean and flexible manufacturing platform for its businesses. In its effort to achieve best-cost manufacturing, AMETEK had operating facilities, as of December 31, 2023, in China, Czechia, Malaysia, Mexico, and Serbia. These facilities offer proximity to customers and provide opportunities for increasing international sales. Acquisitions also have allowed AMETEK to achieve operating synergies by consolidating operations, product lines and distribution channels, benefiting both of AMETEK’s operating groups.

Experienced Management Team. Another component of AMETEK’s success is the strength of its management team and that team’s commitment to improving Company performance. AMETEK senior management has extensive industry experience and an average of approximately 25 years of AMETEK service. The management team is focused on delivering strong, consistent and profitable growth, growing

2

shareholder value, and creating a sustainable future for all stakeholders. Individual performance is tied to financial results through Company-established stock ownership guidelines and equity incentive programs.

Business Strategy

AMETEK is committed to achieving earnings growth through the successful implementation of the AMETEK Growth Model. The goal of that model is double-digit annual percentage growth in sales and earnings per share over the business cycle, strong cash flow generation, and a superior return on total capital. Other financial initiatives have been or may be undertaken, including public and private debt or equity issuance, bank debt refinancing, local financing in certain foreign countries and share repurchases.

AMETEK’s Growth Model integrates the four growth strategies of Operational Excellence, Strategic Acquisitions, Global and Market Expansion, and New Product Development with a focus on cash generation and capital deployment.

Operational Excellence. Operational Excellence is AMETEK’s cornerstone strategy for accelerating growth, improving profit margins and strengthening its competitive position across its businesses. Operational Excellence focuses on initiatives to drive increased organic sales growth, improvements in operating efficiencies and sustainable practices. It emphasizes team building and a participative management culture. AMETEK’s Operational Excellence strategies include lean manufacturing, global sourcing, Design for Six Sigma, Value Engineering/Value Analysis, growth kaizens, and digitalization. Each plays an important role in improving efficiency, enhancing the pace and quality of innovation and driving profitable sales growth. Operational Excellence initiatives have yielded lower operating and administrative costs, shortened manufacturing cycle times, resulted in higher cash flow from operations and increased customer satisfaction. They also have played a key role in achieving synergies from newly acquired companies.

Strategic Acquisitions. Acquisitions are a key to achieving the goals of the AMETEK Growth Model. Since the beginning of 2019 through December 31, 2023, AMETEK has completed 15 acquisitions with annualized sales totaling approximately $1.6 billion. AMETEK targets companies that offer a compelling strategic, technical and cultural fit. It seeks to acquire businesses in adjacent markets with complementary products and technologies. It also looks for businesses that provide attractive growth opportunities aligned with strong secular growth themes, often in new and emerging markets. Through these and prior acquisitions, AMETEK’s management team has developed considerable skill in identifying, acquiring and integrating new businesses. As it has executed its acquisition strategy, AMETEK’s mix of businesses has shifted toward those that are more highly differentiated and, therefore, offer better opportunities for growth and profitability.

Global & Market Expansion. AMETEK has historically experienced growth outside the United States, reflecting an expanding international customer base, investments in its global infrastructure and the attractive growth potential of its businesses in overseas markets. While Europe remains its largest overseas market, AMETEK has pursued growth opportunities worldwide, especially in key emerging markets. It has grown sales in Latin America and Asia by strategically building, acquiring and expanding manufacturing facilities. AMETEK also has expanded its sales, service, and engineering capabilities globally. Recently acquired businesses have further added to AMETEK’s international presence.

New Product Development. New products are essential to AMETEK’s long-term growth. As a result, AMETEK has maintained a consistent investment in new product development and engineering. AMETEK's businesses help solve our customers' most complex challenges with differentiated technology solutions. In 2023, AMETEK added to its highly differentiated product portfolio with a range of new products across many of its businesses.

AMETEK focuses on cash generation and capital deployment. AMETEK generates strong cash flow given its asset-light business model and strong operational execution. This cash flow supports AMETEK’s capital deployment strategy with its primary focus on strategic, value-enhancing acquisitions. AMETEK is also committed to paying a consistently increasing cash dividend.

3

Attracting, retaining, and developing talent is critical to the success and sustainability of the AMETEK Growth Model as our employees are responsible for successfully driving these strategies.

2023 Overview

Operating Performance

In 2023, the Company posted record sales, operating income, operating margins, net income, diluted earnings per share, orders, backlog, and operating cash flow. The Company achieved these results from organic sales growth, contributions from recent acquisitions, as well as the Company's Operational Excellence initiatives. See "Results of Operations" in Part II, Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations for further details.

In 2023, the Company achieved record sales of $6,597.0 million, an increase of 7.3% from 2022 due to a 4% organic sales increase and a 3% increase from acquisitions. Diluted earnings per share for 2023 were a record $5.67, an increase of $0.66 or 13.2%, compared with $5.01 per diluted share in 2022.

Recent Acquisitions

AMETEK spent $2,237.9 million in cash, net of cash acquired, to purchase four businesses:

In March 2023, AMETEK acquired Bison Gear & Engineering Corp. ("Bison"), a designer and manufacturer of custom motion control solutions.

In August 2023, AMETEK acquired United Electronic Industries ("UEI"), a designer and manufacturer of high-performance test, measurement, simulation and control solutions.

In October 2023, AMETEK acquired Amplifier Research Corp. ("Amplifier Research"), a leading provider of amplifiers and electromagnetic compatibility testing equipment.

In December 2023, AMETEK acquired Paragon Medical ("Paragon"), a leading provider of highly engineered medical components and instruments.

Description of Business

Described below are the products and markets of each reportable segment:

EIG

EIG is a leader in the design and manufacture of advanced analytical, test and measurement instruments for the process, aerospace, medical, research, power and industrial markets. Its growth is based on the strategies outlined in the AMETEK Growth Model. In many instances, EIG's products differ from or are technologically superior to its competitors’ products. EIG has achieved competitive advantage through continued investment in research, development and engineering to develop market-leading products and solutions that serve niche markets. EIG has also has expanded its sales and service capabilities globally to serve its customers.

EIG is a leader in many of the specialized markets it serves. Products supplied to these markets include process control instruments for the life sciences, pharmaceutical, semiconductor, automation, power, food and beverage, oil and gas, and petrochemical industries. It provides a growing range of instruments to the research and laboratory equipment, ultra-precision manufacturing, optics, medical, and test and measurement markets. It is a leader in power quality monitoring and metering, uninterruptible power systems, programmable power equipment, electromagnetic compatibility test equipment, sensors for gas turbines, dashboard instruments for heavy trucks, and instrumentation and controls for the food and beverage industries. EIG supplies the aerospace industry with aircraft

4

and engine sensors, monitoring systems, embedded computing systems, power supplies, fuel and fluid measurement systems, and data acquisition systems.

In 2023, 48% of EIG’s net sales were to customers outside the United States. At December 31, 2023, EIG employed approximately 11,800 people, of whom approximately 800 were covered by collective bargaining agreements. At December 31, 2023, EIG had operating facilities in the United States, the United Kingdom, Germany, Canada, China, Denmark, Finland, France, Switzerland, Argentina, Austria, Serbia, and Mexico. EIG also shares operating facilities with EMG in China and Mexico.

Process and Analytical Instrumentation Markets and Products

Process and analytical instrumentation sales represented 71% of EIG’s 2023 net sales. These businesses include process analyzers, emission monitors and spectrometers; elemental and surface analysis instruments; level, pressure and temperature sensors and transmitters; radiation measurement devices; level measurement devices; precision manufacturing systems; materials- and force-testing instruments; contact and non-contact metrology products; and clinical and educational communication solutions. Among the industries it serves are power generation; pharmaceutical manufacturing; medical and healthcare; research and development; water and waste treatment; renewable energy production, semiconductor manufacturing; natural gas distribution; emissions monitoring, and oil, gas, and petrochemical refining. Its instruments are used for precision measurement in a number of applications, including radiation detection, trace element and materials analysis, nanotechnology research, ultraprecise manufacturing, advanced optical metrology, and test and measurement.

Acquired in September 2022, Navitar is a designer and manufacturer of customized, fully integrated optical imaging systems, components, and software. Navitar's market leading optical components and solutions complement the Company's existing optics portfolio.

Aerospace and Power Instrumentation Markets and Products

Aerospace and Power Instrumentation sales represented 29% of EIG’s 2023 net sales. These businesses produce a wide array of instrumentation, systems and sensors for applications in the aerospace, power and industrial markets.

These businesses produce power monitoring and metering instruments, uninterruptible power supply systems and programmable power supplies used in a wide range of industrial settings. It is a leader in the design and manufacture of power measurement, quality monitoring and event recorders for use in power generation, transmission and distribution. These businesses provide uninterruptible power supply systems, multifunction electric meters, and highly specialized communications equipment for smart grid applications and renewable energy applications. It also offers precision power supplies and power conditioning products, and electrical immunity and EMC test equipment, sensors for electric vehicle testing, gas turbines, dashboard instruments for heavy trucks and other vehicles, and instrumentation and controls for the food and beverage industries.

AMETEK’s aerospace products are designed to customer specifications and manufactured to stringent operational and reliability requirements. These products include airborne data systems, turbine engine temperature measurement products, vibration-monitoring systems, cockpit instruments and displays, fuel and fluid measurement products, embedded computing systems, and sensors and switches. AMETEK serves all segments of the commercial and military aerospace market, including commercial airliners, business jets, regional aircraft and helicopters.

AMETEK operates in highly specialized aerospace market segments in which it has proven technological or manufacturing advantages versus its competition. Among its more significant competitive advantages is its 70-year-plus reputation as an established aerospace supplier. AMETEK has long-standing relationships with the world’s leading commercial and military aircraft, jet engine and original equipment manufacturers and aerospace system integrators. AMETEK also is a leading provider of spare part sales, repairs and overhaul services to commercial aerospace.

5

Acquired in October 2023, Amplifier Research is a leading provider of amplifiers and electromagnetic compatibility testing equipment. Amplifier Research's diverse product portfolio complements the Company's existing capabilities in the electromagnetic compatibility testing market.

Acquired in August 2023, UEI is a designer and manufacturer of high-performance test, measurement, simulation and control solutions. UEI's innovative solutions complement the Company's existing testing and data acquisition expertise.

Acquired in October 2022, RTDS is a leading provider of real-time power simulation systems used by utilities, and research and education institutions in the development and testing of the electric power grid and renewable energy applications. RTDS's solutions complement the Company's existing power instruments businesses.

Customers

EIG is not dependent on any single customer such that the loss of that customer would have a material adverse effect on EIG’s operations. Approximately 6% of EIG’s 2023 net sales were made to its five largest customers. No single customer comprises more than 2% of net sales.

EMG

EMG is a leader in the design and manufacture of highly engineered medical components and devices, automation solutions, thermal management systems, specialty metals and electrical interconnects. EMG is a leader in many of the niche markets in which it competes. Products supplied to these markets include single-use and consumable surgical instruments, implantable components, and drug delivery systems used across a wide range of medical applications, advanced precision motion control solutions, which are used in a wide range of automation applications across the medical, semiconductor, aerospace, defense, and food and beverage industries, as well as highly engineered electrical connectors and electronics packaging used in aerospace and defense, medical, and industrial applications.

EMG supplies high-purity powdered metals, strip and foil, specialty clad metals and metal matrix composites. EMG's heat exchangers provide electronic cooling and environmental control for the aerospace and defense and semiconductor industries. EMG's motors are widely used in commercial appliances, food and beverage machines, hydraulic pumps and industrial blowers. Additionally, EMG operates a global network of aviation maintenance, repair and overhaul (“MRO”) facilities.

EMG designs and manufactures products that, in many instances, are significantly different from or technologically superior to competitors’ products. It has achieved competitive advantage through continued investment in research, development and engineering, efficiency improvements from operational excellence, acquisition synergies and improved supply chain management.

In 2023, 45% of EMG’s net sales were to customers outside the United States. At December 31, 2023, EMG employed approximately 10,000 people, of whom approximately 2,100 were covered by collective bargaining agreements. At December 31, 2023, EMG had operating facilities in the United States, the United Kingdom, China, Germany, France, Italy, Poland, Mexico, Serbia, Czechia, Malaysia, and Taiwan.

Automation and Engineered Solutions Markets and Products

Automation and Engineered Solution sales represented 70% of EMG’s 2023 net sales. These businesses produce precision motion control solutions, brushless motors, blowers and pumps, heat exchangers and other electromechanical systems. These products are used in a wide variety of high-precision automation applications, including semiconductor equipment, and laboratory and medical equipment.

6

AMETEK is a leader in highly engineered single-use and consumable surgical instruments, implantable components and drug delivery systems. Its electrical connectors and electronics packaging are designed specifically for harsh environments and highly customized applications, and are used to protect sensitive devices and mission-critical electronics. In addition, AMETEK is an innovator and market leader in specialized metal powder, strip, wire and bonded products used in medical, aerospace and defense, telecommunications, automotive and general industrial applications.

Acquired in March 2023, Bison is a designer and manufacturer of custom motion control solutions. Bison's engineering expertise and broad product portfolio complement the Company's existing motion control and automation solutions business.

Acquired in December 2023, Paragon is a leading provider of highly engineered medical components and instruments. Paragon's product portfolio includes single-use and consumable surgical instruments and implantable components sold to a diverse blue-chip customer base of leading medical device manufacturers. Paragon expands the Company's presence in the MedTech space and provides access to new market segments with strong growth rates.

Aerospace Markets and Products

Aerospace sales represented 30% of EMG’s 2023 net sales. These businesses produce motor-blower systems and heat exchangers used in thermal management and other applications on a variety of military and commercial aircraft and military ground vehicles. In addition, these businesses provide the commercial and military aerospace industry with third-party MRO services on a global basis with facilities in the United States, Europe and Asia.

Customers

EMG is not dependent on any single customer such that the loss of that customer would have a material adverse effect on EMG’s operations. Approximately 8% of EMG’s 2023 net sales were made to its five largest customers. No single customer comprises greater than 2% of net sales.

Marketing

AMETEK’s marketing efforts generally are organized and carried out at the business level. EIG makes use of specialized distributors and sales representatives to market its products along with a direct sales force for its technically sophisticated products. Within aerospace, the specialized customer base of aircraft and jet engine manufacturers is served primarily by direct sales engineers. Given the technical nature of its many products, as well as its significant market share, EMG conducts much of its domestic and international marketing activities through a direct sales force and makes some use of sales representatives and distributors, both in the United States and in other countries.

Competition

In general, AMETEK’s markets are highly competitive with competition based on technology, performance, quality, service and price.

In EIG’s markets, AMETEK believes it ranks as a leader in certain analytical measurement and control instruments, and power and industrial markets. It also is a major instrument and sensor supplier to commercial aviation. In process and analytical instruments, numerous companies compete in each market on the basis of product quality, performance and innovation. In power and industrial and in aerospace, AMETEK competes with a number of companies depending on the specific market segment.

EMG’s businesses compete with a number of companies in each of its markets. Competition is generally based on product innovation, performance and price. There also is competition from alternative materials and processes.

7

Availability of Raw Materials

AMETEK’s reportable segments obtain raw materials and supplies from a variety of sources and generally from more than one supplier. For EMG, however, certain items, including various base metals and certain steel components, are available from only a limited number of suppliers. AMETEK believes its sources and supplies of raw materials are adequate for its needs.

Environmental and Other Governmental Regulation

AMETEK's operations and properties are subject to laws and regulations relating to environmental protection, including those governing air emissions, water discharges, waste management, and workplace safety. The Company uses, generates and disposes of hazardous substances and waste in its operations and could be subject to material liabilities relating to the investigation and clean-up of contaminated properties and related claims. The Company is required to conform our operations and properties to these laws and adapt to regulatory requirements in all countries as these requirements change. The Company has a robust Environmental Health and Safety program responsible for supporting its environmental monitoring and compliance efforts. In connection with acquisitions, the Company will assess potential material environmental liabilities, and determine regulatory and fiduciary obligations during the course of the due diligence process. In addition, new laws and regulations, the discovery of previously unknown contamination or the imposition of new requirements could increase costs or subject AMETEK to new or increased liabilities.

Information with respect to environmental matters is set forth in Note 13 to the Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K.

Patents, Licenses and Trademarks

AMETEK owns numerous unexpired U.S. and foreign patents, including counterparts of its more important U.S. patents, in the major industrial countries of the world. It is a licensor or licensee under patent agreements of various types, and its products are marketed under various registered and unregistered U.S. and foreign trademarks and trade names. AMETEK, however, does not consider any single patent or trademark, or any group of them, essential either to its business as a whole or to either one of its reportable segments. The annual royalties received or paid under license agreements are not significant to either of its reportable segments or to AMETEK’s overall operations.

Sustainability and Human Capital Management

Sustainability

AMETEK is committed to providing a consistent and excellent return to our stakeholders, all while maintaining a strong commitment to environmental stewardship, social responsibility, inclusion, and sound corporate governance. We believe that effectively prioritizing and managing our sustainability initiatives will help create long-term value and a better future for our stakeholders.

Our Sustainability Report highlights our sustainability initiatives and is available on our website at https://www.ametek.com/who-we-are/sustainability.

Key elements in the Company’s approach to sustainability include the following:

Core Values. Our core values — Ethics and Integrity, Respect for the Individual, Inclusion, Teamwork, and Social Responsibility — remain the most critical components of our sustainability efforts. Sustainability is an integral aspect of the core values that guide the way we do business.

Upholding Sound Governance. Our commitment to transparency, accountability, and ethical and responsible decision-making is demonstrated through our core values, corporate governance structure, compliance measures, and focus on sustainability oversight. Together, AMETEK’s governance structure underpins our distributed

8

operating structure and provides our colleagues with the foundation to advance sustainability initiatives across their businesses.

Protecting Our Environment. Our ongoing commitment to serve as environmental stewards and protect the environment for future generations is reflected in our proactive approach to environmental management and sustainability. From emissions reduction initiatives to optimizing resource consumption, we emphasize environmental protection in every facet of our operations. We are firmly committed to reducing our carbon footprint and have made outstanding progress toward our stated greenhouse gas emissions reduction target.

Investing in Our People. Our people are the most essential resource in driving AMETEK’s long-term success and in achieving our sustainability ambitions. AMETEK is committed to developing an inclusive culture to help power innovation, growth, and greater opportunities for all employees. Through strategic investments in talent acquisition, learning and development, and employee well-being, we foster a culture of empowerment, innovation, and inclusivity, driving our collective success and sustainable growth. We are continually expanding our employee development, engagement, and training initiatives to provide meaningful opportunities for personal and professional development.

Driving Sustainable Product Solutions. AMETEK is committed to advancing a low-carbon economy. Our growing portfolio of clean technology and sustainability-related solutions includes a wide range of products and solutions that have a positive, global environmental impact across a broad set of diverse end markets, supporting customers in achieving their sustainability goals and creating a more sustainable future. Through collaborative partnerships with our customers, we develop solutions which help reduce carbon emissions, promote renewable energy adoption, improve efficiency and productivity, and improve healthcare outcomes.

Partnering with Our Communities. We cultivate strong and lasting relationships with the communities in which we operate, actively contributing to their social and economic prosperity. Our charitable arm, the AMETEK Foundation, provides wide-ranging support to non-profit and educational organizations. Through employee volunteerism, financial support, and contributions from the AMETEK Foundation, we partner to strengthen the work of non-profit charities around the world.

Human Capital Management

As a global organization, we have seen firsthand that the innovation needed to solve our customers’ biggest challenges can only come from employees that are fully engaged and committed, and who have diverse perspectives and backgrounds. Our Board regularly receives updates and presentations on key topics, including sustainability, compliance, inclusion, and employee development and succession.

Our executive management team reviews the key talent across our company and assesses the adequacy of talent to meet business challenges and future growth needs. We have an active Inclusion Council, which drives initiatives focused on mentorship, education and career guidance.

We have created a leadership development program for employees on track to become P&L leaders in the company. This focused and intensive program involves both internal and external training on leadership effectiveness as well as specific job-related skills. In addition, participants receive hands-on experience in key AMETEK business system processes such as growth kaizens and acquisition due diligence. We have a long-standing commitment to responsible corporate conduct. Each employee is provided with annual performance goals which are reviewed in a performance review with their manager. Employee feedback is actively encouraged through an open-door policy for all managers, regular town hall/all hands meetings, executive presentations with Q&A sessions, a regular CEO podcast for all employees, and a hotline that can be used to report complaints.

Giving back to our community is an important part of our culture. Established in 1960, the AMETEK Foundation is the charitable giving arm of AMETEK. The Foundation’s mission is to empower AMETEK colleagues making a positive impact in their local communities, with a focus on health and welfare, civic and social service programs, and education.

9

As of December 31, 2023, we have approximately 21,500 employees. Our compensation programs are designed to provide competitive salaries and benefit programs to attract, retain and motivate a world-class workforce. Selected employees participate in short- and long-term incentive programs that align employee and shareholder interests and promote long-term retention. Additionally, we strive to protect health and safety in every aspect of our enterprise – from the way we design, manufacture and deliver our products to the way our customers use them. We continue to drive towards our goal of zero lost-time work incidents. In 2023, we achieved a lost-time incident rate that was significantly below the industry average. We continue to enhance our safety initiatives as each facility is tasked with identifying opportunities for additional safety measures. Businesses with zero incidents share best practices and ensure ongoing training to maintain their safety excellence. In addition to our EHS facility audits, our facilities include safety committees, continual training, documented self-audits, and behavior-based safety observations and feedback.

Our U.S. Federal Employment Information Report (EEO-1) for 2022 is available at www.ametek.com.

Available Information

AMETEK’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports filed or furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934 are made available free of charge on the Company’s website at www.ametek.com in the “Investors – Reporting” section as soon as reasonably practicable after such material is electronically filed with, or furnished to, the U.S. Securities and Exchange Commission. All reports filed with the Securities Exchange Commission can also be viewed on their website at www.sec.gov. AMETEK has posted in the “Investors – Governance” section of its website its corporate governance guidelines, Board committee charters, codes of ethics, and social and environmental policies. Those documents also are available free of charge in published form to any stockholder who requests them by writing to the Investor Relations Department at AMETEK, Inc., 1100 Cassatt Road, Berwyn, Pennsylvania, 19312.

Item 1A. Risk Factors

You should consider carefully the following risk factors and all other information contained in this Annual Report on Form 10-K and the documents we incorporate by reference in this Annual Report on Form 10-K. Any of the following risks could materially and adversely affect our business, financial condition, results of operations and cash flows.

Risks Related to Our Operations

Our growth could suffer if the markets into which we sell our products and services decline, do not grow as anticipated, experience cyclicality, or a general downturn in the economy could adversely affect our business.

A number of the industries in which we operate are cyclical in nature and therefore are affected by factors beyond our control. A downturn in the U.S. or global economy, and, in particular, in the aerospace and defense, oil and gas, process instrumentation or power markets could have an adverse effect on our business, financial condition and results of operations.

Our growth depends in part on the growth of the markets which we serve. Visibility into the future performance of certain of our markets is limited (particularly for markets into which we sell through distribution). Our quarterly sales and profits depend substantially on the volume and timing of orders received during the fiscal quarter, which are difficult to forecast. Any decline or lower than expected growth in our served markets could diminish demand for our products and services, which would adversely affect our financial statements. A number of our businesses operate in industries that may experience periodic, cyclical downturns. In addition, in certain of our businesses, demand depends on customers’ capital spending budgets, as well as government funding policies. Matters of public policy and government budget dynamics, as well as product and economic cycles, can affect the spending decisions of these customers. Demand for our products and services is also sensitive to changes in

10

customer order patterns, which may be affected by announced price changes, changes in incentive programs, new product introductions and customer inventory levels. Any of these factors could adversely affect our growth and results of operations in any given period.

We may not properly execute, or realize anticipated cost savings or benefits from, our Operational Excellence initiatives.

Our success is partly dependent upon properly executing and realizing cost savings or other benefits from our ongoing production and procurement initiatives. These initiatives are primarily designed to make the Company more efficient, which is necessary in the Company’s highly competitive industries. These initiatives are often complex, and a failure to implement them properly may, in addition to not meeting projected cost savings or benefits, adversely affect our business and operations.

Foreign and domestic economic, political, legal, compliance and business factors could negatively affect our international sales and operations.

International sales for 2023 and 2022 represented 47.4% and 48.7% of our consolidated net sales, respectively. As a result of our growth strategy, we anticipate that the percentage of sales outside the United States will increase in the future. As of December 31, 2023, we have manufacturing operations in 20 countries outside the United States, with significant operations in Canada, China, France, Germany, Mexico, Serbia, Poland and the United Kingdom. A disruption of our ability to obtain a supply of goods from these countries or a change in the cost to purchase, manufacture, or distribute these products could have an adverse effect on our sales and operations. International sales and operations are subject to the customary risks of operating in an international environment, including:

•Imposition of trade or foreign exchange restrictions, including in the United States;

•Overlap of different tax structures, including the development of a global minimum tax;

•Unexpected changes in regulatory requirements, including in the United States;

•Trade protection measures, such as the imposition of or increase in tariffs and other trade barriers, including in the United States;

•The difficulty and/or costs of designing and implementing an effective control environment across diverse regions and employee bases;

•Restrictions on currency repatriation;

•General economic conditions;

•Unstable political situations and social unrest, both internationally and in the United States;

•Increasing trade tensions between the United States and certain countries, including China;

•Nationalization of assets; and

•Compliance with a wide variety of international and U.S. laws and regulatory requirements.

Furthermore, fluctuations in foreign currency exchange rates, including changes in the relative value of currencies in the countries where we operate, subject us to exchange rate exposure and may adversely affect our financial statements. For example, increased strength in the U.S. dollar will increase the effective price of our

11

products sold overseas, which may adversely affect sales or require us to lower our prices. In addition, our consolidated financial statements are presented in U.S. dollars, and we must translate our assets, liabilities, sales and expenses into U.S. dollars for external reporting purposes. As a result, changes in the value of the U.S. dollar due to fluctuations in currency exchange rates or currency exchange controls may materially and negatively affect the value of these items in our consolidated financial statements, even if their value has not changed in their local currency.

Our international sales and operations may be adversely impacted by compliance with export laws.

We are required to comply with various import, export, export control and economic sanctions laws, which may affect our transactions with certain customers, business partners and other persons, including in certain cases dealings with or between our employees and subsidiaries. In certain circumstances, export control and economic sanctions regulations may prohibit the export of certain products, services and technologies and in other circumstances, we may be required to obtain an export license before exporting a controlled item. In addition, failure to comply with any of these regulations could result in civil and criminal, monetary and non-monetary penalties, disruptions to our business, limitations on our ability to import and export products and services and damage to our reputation.

Our reputation, ability to do business and financial statements may be impaired by improper conduct by any of our employees, agents or business partners.

We cannot provide assurance that our internal controls and compliance systems will always protect us from acts committed by employees, agents or business partners of ours (or of businesses we acquire or partner with) that would violate U.S. and/or non-U.S. laws, including the laws governing payments to government officials, bribery, fraud, kickbacks and false claims, pricing, sales and marketing practices, conflicts of interest, competition, export and import compliance, money laundering and data privacy. In particular, the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act and similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments to government officials for the purpose of obtaining or retaining business, and we operate in many parts of the world that have experienced governmental corruption to some degree. Any such improper actions or allegations of such acts could damage our reputation and subject us to civil or criminal investigations in the U.S. and in other jurisdictions and related shareholder lawsuits could lead to substantial civil and criminal, monetary and non-monetary penalties and could cause us to incur significant legal and investigatory fees. In addition, we rely on our suppliers to adhere to our supplier standards of conduct and violations of such standards of conduct could occur that could have a material effect on our financial statements.

Any inability to hire, train and retain a sufficient number of skilled officers and other employees could impede our ability to compete successfully.

If we cannot hire, train and retain a sufficient number of qualified employees, we may not be able to effectively integrate acquired businesses and realize anticipated results from those businesses, manage our expanding international operations and otherwise profitably grow our business. Even if we do hire and retain a sufficient number of employees, the expense necessary to attract and motivate these officers and employees may adversely affect our results of operations.

If we are unable to develop new products on a timely basis, it could adversely affect our business and prospects.

We believe that our future success depends, in part, on our ability to develop, on a timely basis, technologically advanced products that meet or exceed appropriate industry standards. Maintaining our existing technological advantages will require us to continue investing in research and development and sales and marketing. There can be no assurance that we will have sufficient resources to make such investments, that we will be able to make the technological advances necessary to maintain such competitive advantages or that we can recover major research and development expenses. We are not currently aware of any emerging standards or new products which could render our existing products obsolete, although there can be no assurance that this will not occur or that we will be able to develop and successfully market new products.

12

Our technology is important to our success and our failure to protect this technology could put us at a competitive disadvantage.

Many of our products rely on proprietary technology; therefore, we endeavor to protect our intellectual property rights through patents, copyrights, trade secrets, trademarks, confidentiality agreements and other contractual provisions. Despite our efforts to protect proprietary rights, unauthorized parties or competitors may copy or otherwise obtain and use our products or technology. In addition, our ability to protect and enforce our intellectual property rights may be limited in certain countries outside the U.S. Actions to enforce our rights may result in substantial costs and diversion of resources and we make no assurances that any such actions will be successful.

A disruption in, shortage of, or price increases for, supply of our components and raw materials may adversely impact our operations.

While we manufacture certain parts and components used in our products, we require substantial amounts of raw materials and purchase some parts and components, including semiconductor chips and other electronic components, from suppliers. The availability and prices for raw materials, parts and components may be subject to curtailment or change due to, among other things, suppliers' allocation to other purchasers, interruptions in production by suppliers, changes in exchange rates and prevailing price levels. In addition, our facilities, supply chains, distribution systems, and products may be impacted by natural or man-made disruptions, including armed conflict, damaging weather or other acts of nature, pandemics or other public health crises. A shutdown of, or inability to utilize, one or more of our facilities, our supply chain, or our distribution system could significantly disrupt our operations, delay production and shipments, damage our relationships and reputation with customers, suppliers, employees, stockholders and others, result in lost sales, result in the misappropriation or corruption of data, or result in legal exposure and large remediation or other expenses. Furthermore, certain items, including base metals and certain steel components, are available only from a limited number of suppliers and are subject to commodity market fluctuations. Shortages in raw materials or price increases therefore could affect the prices we charge, our operating costs and our competitive position, which could adversely affect our business, financial condition, results of operations and cash flows.

We are subject to numerous governmental regulations, which may be burdensome or lead to significant costs.

Our operations are subject to numerous federal, state, local and foreign governmental laws and regulations. In addition, existing laws and regulations may be revised or reinterpreted and new laws and regulations, including with respect to privacy legislation and climate change, may be adopted or become applicable to us or customers for our products. These laws continue to develop and may be inconsistent from jurisdiction to jurisdiction. Complying with emerging and changing international requirements may cause the Company to incur substantial costs or require the Company to change its business practices. We cannot predict the form any such new laws or regulations will take or the impact any of these laws and regulations will have on our business or operations.

13

We operate in highly competitive industries, which may adversely affect our results of operations or ability to expand our business.

Our markets are highly competitive. We compete, domestically and internationally, with individual producers, as well as with vertically integrated manufacturers, some of which have resources greater than we do. The principal elements of competition for our products are product technology, quality, service, distribution and price. Although we believe EIG is a market leader, competition is strong and could intensify in the markets served by EIG. In the aerospace markets served by EIG, a limited number of companies compete on the basis of product quality, performance and innovation. EMG’s competition in specialty metal products stems from alternative materials and processes. Our competitors may develop new or improve existing products that are superior to our products or may adapt more readily to new technologies or changing requirements of our customers. There can be no assurance that our business will not be adversely affected by increased competition in the markets in which it operates or that our products will be able to compete successfully with those of our competitors.

Our business and financial performance could be adversely impacted by a significant disruption in, or breach in security of, our information technology systems.

We rely on information technology systems, some of which are managed by third-parties, to process, transmit and store electronic information (including sensitive data such as confidential business information and personally identifiable data relating to employees, customers, other business partners and patients), and to monitor, manage, and support a variety of critical business processes and activities including receiving and fulfilling orders, billing, collecting and making payments, shipping products, providing services and support to customers and fulfilling contractual obligations. Despite our implementation of certain controls to protect our systems and sensitive, confidential or personal data or information, these systems, products, data and services may be damaged, compromised, disrupted or shut down due to attacks by computer hackers, computer viruses, ransomware, human error or malfeasance, power outages, hardware failures, telecommunication or utility failures, catastrophes or other unforeseen events. In any such circumstances our system redundancy and other disaster recovery planning may be ineffective or inadequate. Further, we also face information security risks due to our reliance on internet technology and use of hybrid work arrangements, which could strain our technology resources or create additional opportunity for cyber-attackers to exploit vulnerabilities.

Attacks may also target hardware, software and information installed, stored or transmitted in our products after such products have been purchased and incorporated into third-party products, facilities or infrastructure. Like most multinational corporations, our information technology systems have been subject to computer viruses, malicious codes, unauthorized access and other cyber-attacks and we expect the sophistication and frequency of such attacks to continue to increase. Any of the attacks, breaches or other disruptions or damage described above could interrupt our operations or the operations of our customers and partners, delay production and shipments, result in theft of intellectual property and trade secrets, damage customer and business partner relationships and our reputation or result in defective products or services, legal claims and proceedings, liability and penalties under privacy laws and increased costs for security and remediation, each of which could adversely affect our business, reputation and financial statements. Further, given the increasing sophistication of cyber-attacks and the complexity of techniques used, any of these attacks or breaches could potentially persist for an extended period before being detected. As a result, it could take a significant time before an investigation can be completed and new disclosure regulations could result in us being required to disclose information about a material cybersecurity incident before it has been mitigated or resolved, or even fully investigated. Although we maintain cyber risk insurance, damages and claims arising from such incidents may not be covered or may exceed the amount of any insurance available.

14

Risks Related to Our Acquisitions

Our growth strategy includes strategic acquisitions. We may not be able to consummate future acquisitions or successfully integrate recent and future acquisitions.

A portion of our growth has been attributed to acquisitions of strategic businesses. We plan to continue making strategic acquisitions to enhance our global market position and broaden our product offerings. Although we have been successful with our acquisition strategy in the past, our ability to successfully effectuate acquisitions will be dependent upon a number of factors, including:

•Our ability to identify acceptable acquisition candidates;

•The impact of increased competition for acquisitions, which may increase acquisition costs, affect our ability to consummate acquisitions on favorable terms, and result in us assuming a greater portion of the seller’s liabilities;

•Successfully integrating acquired businesses, including integrating the management, technological and operational processes, procedures and controls of the acquired businesses with those of our existing operations;

•Adequate financing for acquisitions being available on terms acceptable to us;

•Unexpected losses of key employees, customers and suppliers of acquired businesses;

•Mitigating assumed, contingent and unknown liabilities; and

•Challenges in managing the increased scope, geographic diversity and complexity of our operations.

The process of integrating acquired businesses into our existing operations may result in unforeseen operating difficulties and may require additional financial resources and attention from management that would otherwise be available for the ongoing development or expansion of our existing operations. Furthermore, even if successfully integrated, the acquired business may not achieve the results we expected or produce expected benefits in the time frame planned. Failure to continue with our acquisition strategy and the successful integration of acquired businesses could have an adverse effect on our business, financial condition, results of operations and cash flows.

The indemnification provisions of acquisition agreements by which we have acquired companies may not fully protect us and as a result we may face unexpected liabilities.

Certain of the acquisition agreements by which we have acquired companies require the former owners to indemnify us against certain liabilities related to the operation of the company before we acquired it. In most of these agreements, however, the liability of the former owners is limited, and certain former owners may be unable to meet their indemnification responsibilities. We may also obtain representation and warranty insurance to address certain potential risks and liabilities. We cannot assure you that these indemnification provisions and insurance policies will protect us fully or at all, and as a result we may face unexpected liabilities that adversely affect our financial statements.

Risks Related to Our Financial Condition

Certain environmental risks may cause us to be liable for costs associated with hazardous or toxic substance clean-up which may adversely affect our financial condition.

Our businesses, operations and facilities are subject to a number of federal, state, local and foreign environmental and occupational health and safety laws and regulations concerning, among other things, air

15

emissions, discharges to waters and the use, manufacturing, generation, handling, storage, transportation and disposal of hazardous substances and wastes. Environmental risks are inherent in many of our manufacturing operations. Certain laws provide that a current or previous owner or operator of property may be liable for the costs of investigating, removing and remediating hazardous materials at such property, regardless of whether the owner or operator knew of, or was responsible for, the presence of such hazardous materials. In addition, the Comprehensive Environmental Response, Compensation and Liability Act generally imposes joint and several liability for clean-up costs, without regard to fault, on parties contributing hazardous substances to sites designated for clean-up under the Act. We have been named a potentially responsible party at several sites, which are the subject of government-mandated clean-ups. As the result of our ownership and operation of facilities that use, manufacture, store, handle and dispose of various hazardous materials, we may incur substantial costs for investigation, removal, remediation and capital expenditures related to compliance with environmental laws. While it is not possible to precisely quantify the potential financial impact of pending environmental matters, based on our experience to date, we believe that the outcome of these matters is not likely to have a material adverse effect on our financial position or future results of operations. In addition, new laws and regulations, new classification of hazardous materials, stricter enforcement of existing laws and regulations, the discovery of previously unknown contamination or the imposition of new clean-up requirements could require us to incur costs or become the basis for new or increased liabilities that could have a material adverse effect on our business, financial condition and results of operations. There can be no assurance that future environmental liabilities will not occur or that environmental damages due to prior or present practices will not result in future liabilities.

We are subject to a variety of litigation and other legal and regulatory proceedings in the course of our business that could adversely affect our financial statements.

We are subject to a variety of litigation and other legal and regulatory proceedings incidental to our business (or the business operations of previously owned entities), including claims for damages arising out of the use of products or services and claims relating to intellectual property matters, employment matters, tax matters, commercial disputes, competition and sales and trading practices, environmental matters, personal injury, insurance coverage and acquisition-related matters, as well as regulatory investigations or enforcement. These lawsuits may include claims for compensatory damages, punitive and consequential damages and/or injunctive relief. The defense of these lawsuits may divert our management’s attention, we may incur significant expenses in defending these lawsuits, and we may be required to pay damage awards or settlements or become subject to equitable remedies that could adversely affect our operations and financial statements. Moreover, any insurance or indemnification rights that we may have may be insufficient or unavailable to protect us against such losses. In addition, developments in proceedings in any given period may require us to adjust the loss contingency estimates that we have recorded in our financial statements, record estimates for liabilities or assets previously not susceptible of reasonable estimates or pay cash settlements or judgments. Any of these developments could adversely affect our financial statements in any particular period. We cannot assure you that our liabilities in connection with litigation and other legal and regulatory proceedings will not exceed our estimates or adversely affect our financial statements and reputation. However, based on our experience, current information and applicable law, we do not believe that any amounts we may be required to pay in connection with litigation and other legal and regulatory proceedings in excess of our reserves will have a material effect on our financial statements.

Restrictions contained in our revolving credit facility and other debt agreements may limit our ability to incur additional indebtedness.

Our existing revolving credit facility and other debt agreements (each a “Debt Facility” and collectively, “Debt Facilities”) contain restrictive covenants, including restrictions on our ability to incur indebtedness. These restrictions could limit our ability to effectuate future acquisitions, limit our ability to pay dividends, limit our ability to make capital expenditures or restrict our financial flexibility. Our Debt Facilities contain covenants requiring us to achieve certain financial and operating results and maintain compliance with specified financial ratios. Our ability to meet the financial covenants or requirements in our Debt Facilities may be affected by events beyond our control, and we may not be able to satisfy such covenants and requirements. A breach of these covenants or our inability to comply with the financial ratios, tests or other restrictions contained in a Debt Facility could result in an event of default under one or more of our other Debt Facilities. Upon the occurrence of an event of default under a Debt

16

Facility, and the expiration of any grace periods, the lenders could elect to declare all amounts outstanding under one or more of our other Debt Facilities, together with accrued interest, to be immediately due and payable. If this were to occur, our assets may not be sufficient to fully repay the amounts due under our Debt Facilities or our other indebtedness.

Our goodwill and other intangible assets represent a substantial proportion of our total assets and the impairment of such substantial goodwill and intangible assets could have a negative impact on our financial condition and results of operations.

Our total assets include substantial amounts of intangible assets, primarily goodwill. At December 31, 2023, goodwill and other intangible assets, net of accumulated amortization, totaled $10,612.9 million or 71% of our total assets. The goodwill results from our acquisitions, representing the excess of cost over the estimated fair value of the net tangible and other identifiable intangible assets we have acquired. If future operating performance at one or more of our reporting units were to fall significantly below current levels, we could record, under current applicable accounting rules, a non-cash charge to operating income for goodwill or other intangible asset impairment. Any determination requiring the impairment of a significant portion of goodwill or other intangible assets would negatively affect our financial condition and results of operations.

Item 1B. Unresolved Staff Comments

None.

Item 1C. Cybersecurity

AMETEK’s cybersecurity risk management practices are based on the widely recognized National Institute of Standards and Technology Framework for Improving Critical Infrastructure Cybersecurity (The NIST Cybersecurity Framework and the NIST 800-171 Revision 2 Standard). This guidance was developed with private sector input and provides a framework and toolkit for organizations to manage cybersecurity risk.

We utilize a broad team of in-house information technology and security personnel, as well as third-party consultants, services and software, to help manage our cybersecurity efforts and initiatives. We regularly assess our threat landscape and monitor our systems and other technical security controls. Additionally, we maintain information security policies and procedures, including a breach response plan and maintenance of backup and protective systems.

We regularly review our policies, practices, and plans with assistance from third-party experts and advisors. Our Chief Information Officer is responsible for corporate-wide data security. Our management team is actively engaged in regular reviews of cyber risks. Additionally, our full Board of Directors receives quarterly briefings on enterprise-wide cybersecurity risk management and our overall cybersecurity risk environment.

We have implemented two risk management groups, the Enterprise Risk Management Committee, and the Cybersecurity Steering Committee. These committees meet quarterly. They are responsible for the overall governance of our cyber management. The implementation of the Cyber polices and strategy is the responsibility of the Chief Information Officer and the Director of Cyber Security. The CIO reports to the Chief Administrative Officer and the Director of Cyber Security reports to the CIO. We also have a team of full-time cybersecurity specialists who hold various industry technology accreditations. The CIO has more than 35 years in Senior IT Leadership positions, and the Director of Cyber Security has more than 30 years IT experience overall, 15 of which are in leadership roles.

Operationally, we deploy multiple layers of cyber defenses including multiple tools and processes that identify security risks across our global networks, largely in real time. We also maintain good relationships with law enforcement agencies to remain informed on potential cyber risks.

17

Mandatory cybersecurity training is conducted eight times a year for all of AMETEK’s employees with email access. The training provides critical information on how employees can protect themselves and AMETEK against cybersecurity risks. AMETEK financial professionals receive additional training due to the nature of their roles.

Item 2. Properties

At December 31, 2023, the Company conducted business from office and operating facilities at owned and leased locations throughout the United States and select global markets. The Company leases a facility in Berwyn, Pennsylvania for its corporate headquarters.

The Company believes that all facilities have been adequately maintained, are in good operating condition, and are suitable for our current needs.

Item 3. Legal Proceedings

Please refer to Note 13 to the Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K for information regarding certain litigation matters.

The Company is subject to a variety of litigation and other legal and regulatory proceedings incidental to its business (or the business operations of previously owned entities), including claims for damages arising out of the use of the Company’s products or services and claims relating to intellectual property matters, employment matters, tax matters, commercial disputes, competition and sales and trading practices, environmental matters, personal injury, insurance coverage and acquisition-related matters, as well as regulatory investigations or enforcement. Based upon the Company’s experience, the Company does not believe that these proceedings and claims will have a material adverse effect on its results of operations, financial position or cash flows.

Item 4. Mine Safety Disclosures

Not Applicable.

18

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The principal market on which the Company’s common stock is traded is the New York Stock Exchange and it is traded under the symbol “AME.” On January 31, 2024, there were approximately 1,700 holders of record of the Company’s common stock.

Market price and dividend information with respect to the Company’s common stock is set forth below. Future dividend payments by the Company will be dependent on future earnings, financial requirements, contractual provisions of debt agreements and other relevant factors.

Under its share repurchase program, the Company repurchased approximately 55,800 shares of its common stock for $7.8 million in 2023 and approximately 2,673,000 shares of its common stock for $332.8 million in 2022.

The objective and rationale of the share repurchases is to enhance shareholder value through the opportunistic repurchases of the Company’s common stock. The Company takes a balanced approach when determining how to deploy capital, including strategic acquisitions, dividends, and share repurchases. The factors evaluated when considering how to deploy capital include: the Company’s share price, the Company’s cash balances, balance sheet flexibility, business prospects, the leverage of the Company, and other investment opportunities.

Issuer Purchases of Equity Securities

The following table reflects purchases of AMETEK, Inc. common stock by the Company during the three months ended December 31, 2023:

| Period | Total Number of Shares Purchased (1)(2) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plan (2) | Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plan | |||||||||||||||||||

| October 1, 2023 to October 31, 2023 | — | $ | — | — | $ | 817,325,034 | |||||||||||||||||

| November 1, 2023 to November 30, 2023 | 8,323 | 143.46 | 8,323 | 816,130,993 | |||||||||||||||||||

| December 1, 2023 to December 31, 2023 | — | — | — | 816,130,993 | |||||||||||||||||||

| Total | 8,323 | $ | 143.46 | 8,323 | |||||||||||||||||||

_____________________

(1)Represents shares surrendered to the Company to satisfy tax withholding obligations in connection with employees’ share-based compensation awards.

(2)Consists of the number of shares purchased pursuant to the Company’s Board of Directors $1 billion authorization for the repurchase of its common stock announced in May 2022, which replaces the previous $500 million authorization for repurchase of its common stock announced in February 2019. Such purchases may be effected from time to time in the open market or in private transactions, subject to market conditions and at management’s discretion.

19

Securities Authorized for Issuance Under Equity Compensation Plan Information

The following table sets forth information as of December 31, 2023 regarding all of the Company’s existing compensation plans pursuant to which equity securities are authorized for issuance to employees and non-employee directors:

| Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights (a) | Weighted average exercise price of outstanding options, warrants and rights (b) | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) (c) | ||||||||||||||

| Equity compensation plans approved by security holders | 2,741,164 | $ | 101.20 | 5,526,792 | |||||||||||||

| Equity compensation plans not approved by security holders | — | — | — | ||||||||||||||

| Total | 2,741,164 | $ | 101.20 | 5,526,792 | |||||||||||||

20

Stock Performance Graph

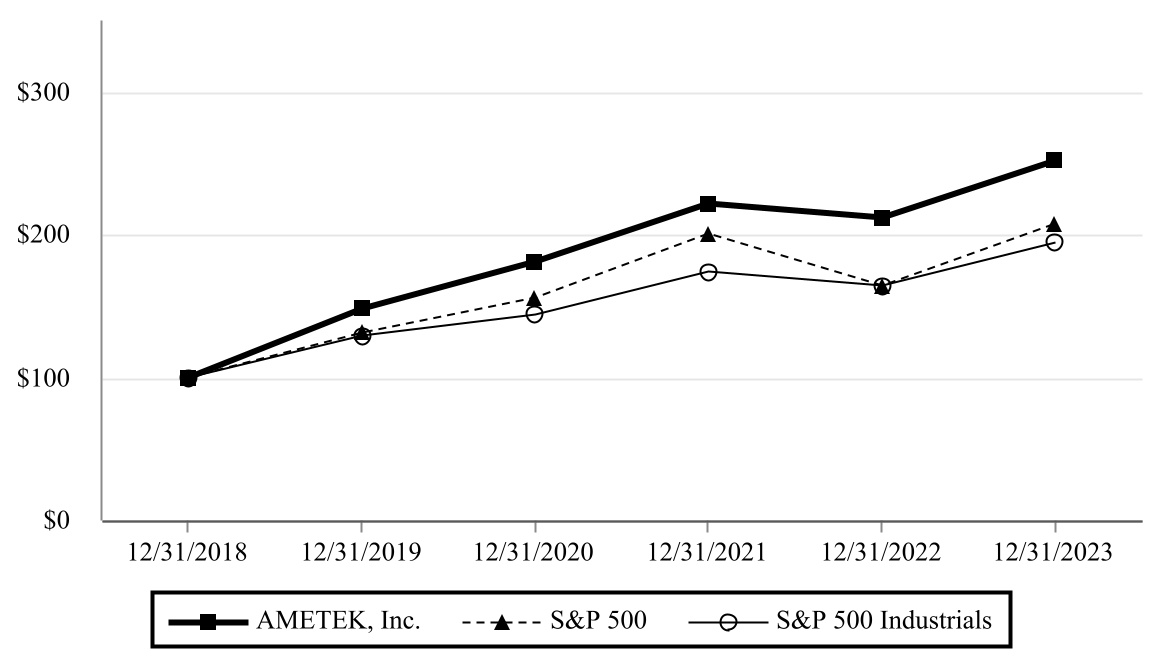

The following graph and accompanying table compare the cumulative total stockholder return for AMETEK over the last five years ended December 31, 2023 with total returns for the same period for the Standard and Poor’s (“S&P”) 500 Index and S&P 500 Industrials. AMETEK’s stock price is a component of both indices. The performance graph and table assume a $100 investment made on December 31, 2018 and reinvestment of all dividends. The stock performance shown on the graph below is based on historical data and is not necessarily indicative of future stock price performance.

COMPARISON OF FIVE-YEAR CUMULATIVE TOTAL RETURN | ||

| December 31, | |||||||||||||||||||||||||||||||||||

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | ||||||||||||||||||||||||||||||

| AMETEK, Inc. | $ | 100.00 | $ | 148.26 | $ | 181.23 | $ | 221.68 | $ | 212.10 | $ | 251.99 | |||||||||||||||||||||||

| S&P 500 Index | 100.00 | 131.49 | 155.68 | 200.37 | 164.08 | 207.21 | |||||||||||||||||||||||||||||

| S&P 500 Industrials | 100.00 | 129.37 | 143.68 | 174.02 | 164.49 | 194.31 | |||||||||||||||||||||||||||||

Item 6. Reserved

21

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

This report includes forward-looking statements based on the Company’s current assumptions, expectations and projections about future events. When used in this report, the words “believes,” “anticipates,” “may,” “expect,” “intend,” “estimate,” “project” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such words. In this report, the Company discloses important factors that could cause actual results to differ materially from management’s expectations. For more information on these and other factors, see “Forward-Looking Information” herein.

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations should be read in conjunction with “Item 1A. Risk Factors,” and the consolidated financial statements and related notes included elsewhere in this Annual Report on Form 10-K.

Business Overview

AMETEK’s operations are affected by global, regional and industry-specific economic factors. However, the Company’s strategic geographic and industry diversification, and its mix of products and services, have helped to mitigate the potential adverse impact of any unfavorable developments in any one industry or the economy of any single country on its consolidated operating results. In 2023, the Company posted record sales, operating income, operating margins, net income, diluted earnings per share, orders, backlog, and operating cash flow. Positive market trends, the Company's record backlog, contributions from recent acquisitions, and continued focus on and implementation of Operational Excellence initiatives had a positive impact on 2023 results. The Company also benefited from its strategic initiatives under AMETEK's four key strategies: Operational Excellence, Strategic Acquisitions, Global & Market Expansion and New Products.

Highlights in 2023 were:

•Net sales for 2023 were a record $6,597.0 million, an increase of $446.5 million or 7.3%, compared with net sales of $6,150.5 million in 2022. The increase in net sales for 2023 was due to a 4% organic sales increase and a 3% increase from acquisitions.

•Net income for 2023 was a record $1,313.2 million, an increase of $153.7 million or 13.3%, compared with $1,159.5 million in 2022.

•Diluted earnings per share for 2023 were a record $5.67, an increase of $0.66 or 13.2%, compared with $5.01 per diluted share in 2022.

•Cash provided by operating activities totaled a record $1,735.3 million in 2023, an increase of $585.9 million or 51.0%, compared with cash provided by operating activities of $1,149.4 million in 2022.

•The Company's backlog of unfilled orders at December 31, 2023 was a record $3,534.1 million.

•During 2023, the Company spent $2,237.9 million in cash, net of cash acquired, to purchase four businesses:

•In March 2023, AMETEK acquired Bison Gear & Engineering Corp. ("Bison"), a designer and manufacturer of custom motion control solutions.

•In August 2023, AMETEK acquired United Electronic Industries ("UEI"), a designer and manufacturer of high-performance test, measurement, simulation and control solutions.

•In October 2023, AMETEK acquired Amplifier Research Corp. ("Amplifier Research"), a leading provider of amplifiers and electromagnetic compatibility testing equipment.

22

•In December 2023, AMETEK acquired Paragon Medical ("Paragon"), a leading provider of highly engineered medical components and instruments.

•EBITDA (earnings before interest, income taxes, depreciation, and amortization) was a record $2,014.7 million in 2023, compared with $1,829.7 million in 2022.

•The Company continued its emphasis on investment in research, development and engineering, spending $351.7 million in 2023. Approximately 25% of sales in 2023 were from products introduced in the past three years.