000103544312/31/2020false12/31falsetruefalsefalse2020FYtruefalse00010354432020-01-012020-12-31iso4217:USD00010354432020-06-30xbrli:shares00010354432021-01-15xbrli:pure0001035443srt:NorthAmericaMember2020-12-310001035443srt:NorthAmericaMember2020-01-012020-12-3100010354432020-12-3100010354432019-12-310001035443are:IncomefromrentalsMember2020-01-012020-12-310001035443are:IncomefromrentalsMember2019-01-012019-12-310001035443are:IncomefromrentalsMember2018-01-012018-12-310001035443us-gaap:ProductAndServiceOtherMember2020-01-012020-12-310001035443us-gaap:ProductAndServiceOtherMember2019-01-012019-12-310001035443us-gaap:ProductAndServiceOtherMember2018-01-012018-12-3100010354432019-01-012019-12-3100010354432018-01-012018-12-31iso4217:USDxbrli:shares0001035443us-gaap:SeriesDPreferredStockMemberus-gaap:PreferredStockMember2017-12-310001035443us-gaap:CommonStockMember2017-12-310001035443us-gaap:AdditionalPaidInCapitalMember2017-12-310001035443us-gaap:RetainedEarningsMember2017-12-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2017-12-310001035443us-gaap:NoncontrollingInterestMember2017-12-3100010354432017-12-310001035443are:RedeemableNoncontrollingInterestsMember2017-12-310001035443us-gaap:RetainedEarningsMember2018-01-012018-12-310001035443us-gaap:NoncontrollingInterestMember2018-01-012018-12-310001035443are:RedeemableNoncontrollingInterestsMember2018-01-012018-12-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-01-012018-12-310001035443us-gaap:AdditionalPaidInCapitalMember2018-01-012018-12-310001035443us-gaap:CommonStockMember2018-01-012018-12-310001035443us-gaap:SeriesDPreferredStockMemberus-gaap:PreferredStockMember2018-01-012018-12-310001035443us-gaap:SeriesDPreferredStockMemberus-gaap:AdditionalPaidInCapitalMember2018-01-012018-12-310001035443us-gaap:SeriesDPreferredStockMemberus-gaap:RetainedEarningsMember2018-01-012018-12-310001035443us-gaap:SeriesDPreferredStockMember2018-01-012018-12-3100010354432019-01-012019-09-300001035443us-gaap:SeriesDPreferredStockMemberus-gaap:PreferredStockMember2018-12-310001035443us-gaap:CommonStockMember2018-12-310001035443us-gaap:AdditionalPaidInCapitalMember2018-12-310001035443us-gaap:RetainedEarningsMember2018-12-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-12-310001035443us-gaap:NoncontrollingInterestMember2018-12-3100010354432018-12-310001035443are:RedeemableNoncontrollingInterestsMember2018-12-310001035443us-gaap:RetainedEarningsMember2019-01-012019-12-310001035443us-gaap:NoncontrollingInterestMember2019-01-012019-12-310001035443are:RedeemableNoncontrollingInterestsMember2019-01-012019-12-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310001035443us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310001035443us-gaap:CommonStockMember2019-01-012019-12-310001035443us-gaap:SeriesDPreferredStockMemberus-gaap:PreferredStockMember2019-01-012019-12-310001035443us-gaap:SeriesDPreferredStockMemberus-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310001035443us-gaap:SeriesDPreferredStockMemberus-gaap:RetainedEarningsMember2019-01-012019-12-310001035443us-gaap:SeriesDPreferredStockMember2019-01-012019-12-310001035443us-gaap:CommonStockMember2019-12-310001035443us-gaap:RetainedEarningsMember2019-01-0100010354432019-01-010001035443us-gaap:SeriesDPreferredStockMemberus-gaap:PreferredStockMember2019-12-310001035443us-gaap:AdditionalPaidInCapitalMember2019-12-310001035443us-gaap:RetainedEarningsMember2019-12-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310001035443us-gaap:NoncontrollingInterestMember2019-12-310001035443are:RedeemableNoncontrollingInterestsMember2019-12-310001035443us-gaap:RetainedEarningsMember2020-01-012020-12-310001035443us-gaap:NoncontrollingInterestMember2020-01-012020-12-310001035443are:RedeemableNoncontrollingInterestsMember2020-01-012020-12-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310001035443us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001035443us-gaap:CommonStockMember2020-01-012020-12-310001035443us-gaap:RetainedEarningsMember2020-01-0100010354432020-01-010001035443us-gaap:CommonStockMember2020-12-310001035443us-gaap:AdditionalPaidInCapitalMember2020-12-310001035443us-gaap:RetainedEarningsMember2020-12-310001035443us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001035443us-gaap:NoncontrollingInterestMember2020-12-310001035443are:RedeemableNoncontrollingInterestsMember2020-12-310001035443us-gaap:BuildingAndBuildingImprovementsMembersrt:MaximumMember2020-01-012020-12-310001035443us-gaap:LandImprovementsMembersrt:MaximumMember2020-01-012020-12-31are:property0001035443country:CA2020-12-310001035443country:CN2020-12-310001035443are:IncomefromrentalsMemberus-gaap:AccountingStandardsUpdate201409Member2020-01-012020-12-310001035443are:IncomefromrentalsMemberus-gaap:AccountingStandardsUpdate201409Member2019-01-012019-12-310001035443are:RevenuessubjecttootheraccountingguidanceMember2020-01-012020-12-3100010354432019-01-012019-01-010001035443us-gaap:AccountsPayableAndAccruedLiabilitiesMember2019-01-0100010354432020-01-012020-03-3100010354432020-10-012020-12-3100010354432020-07-012020-09-3000010354432020-04-012020-06-300001035443us-gaap:AccountingStandardsUpdate201409Member2020-12-310001035443srt:NorthAmericaMember2019-12-310001035443srt:AsiaMember2020-12-310001035443srt:AsiaMember2019-12-310001035443are:GreaterBostonMember2020-12-31utr:sqft0001035443are:GreaterBostonMemberare:FuturedevelopmentprojectsMember2020-12-310001035443are:GreaterBostonMemberare:ActiveRedevelopmentMember2020-12-310001035443are:GreaterBostonMemberare:OperatingwithfuturedevelopmentandredevelopmentMember2020-12-310001035443are:OperatingpropertiesMemberare:GreaterBostonMember2020-12-310001035443are:GreaterBostonMember2020-01-012020-12-310001035443are:SanFranciscoMember2020-12-310001035443are:SanFranciscoMemberare:FuturedevelopmentprojectsMember2020-12-310001035443are:SanFranciscoMemberare:ActiveRedevelopmentMember2020-12-310001035443are:SanFranciscoMemberare:OperatingwithfuturedevelopmentandredevelopmentMember2020-12-310001035443are:SanFranciscoMemberare:OperatingpropertiesMember2020-12-310001035443are:SanFranciscoMember2020-01-012020-12-310001035443are:SanDiegoMember2020-12-310001035443are:SanDiegoMemberare:FuturedevelopmentprojectsMember2020-12-310001035443are:SanDiegoMemberare:ActiveRedevelopmentMember2020-12-310001035443are:SanDiegoMemberare:OperatingwithfuturedevelopmentandredevelopmentMember2020-12-310001035443are:OperatingpropertiesMemberare:SanDiegoMember2020-12-310001035443are:SanDiegoMember2020-01-012020-12-310001035443are:SeattleMember2020-12-310001035443are:SeattleMemberare:FuturedevelopmentprojectsMember2020-12-310001035443are:SeattleMemberare:ActiveRedevelopmentMember2020-12-310001035443are:SeattleMemberare:OperatingwithfuturedevelopmentandredevelopmentMember2020-12-310001035443are:OperatingpropertiesMemberare:SeattleMember2020-12-310001035443are:SeattleMember2020-01-012020-12-310001035443stpr:MD2020-12-310001035443stpr:MDare:FuturedevelopmentprojectsMember2020-12-310001035443stpr:MDare:ActiveRedevelopmentMember2020-12-310001035443stpr:MDare:OperatingwithfuturedevelopmentandredevelopmentMember2020-12-310001035443stpr:MDare:OperatingpropertiesMember2020-12-310001035443stpr:MD2020-01-012020-12-310001035443are:ResearchTriangleMember2020-12-310001035443are:ResearchTriangleMemberare:FuturedevelopmentprojectsMember2020-12-310001035443are:ResearchTriangleMemberare:ActiveRedevelopmentMember2020-12-310001035443are:ResearchTriangleMemberare:OperatingwithfuturedevelopmentandredevelopmentMember2020-12-310001035443are:ResearchTriangleMemberare:OperatingpropertiesMember2020-12-310001035443are:ResearchTriangleMember2020-01-012020-12-310001035443are:OthermarketsMember2020-12-310001035443are:OthermarketsMemberare:FuturedevelopmentprojectsMember2020-12-310001035443are:OthermarketsMemberare:ActiveRedevelopmentMember2020-12-310001035443are:OthermarketsMemberare:OperatingwithfuturedevelopmentandredevelopmentMember2020-12-310001035443are:OperatingpropertiesMemberare:OthermarketsMember2020-12-310001035443are:OthermarketsMember2020-01-012020-12-310001035443srt:NorthAmericaMemberare:FuturedevelopmentprojectsMember2020-12-310001035443srt:NorthAmericaMemberare:ActiveRedevelopmentMember2020-12-310001035443srt:NorthAmericaMemberare:OperatingwithfuturedevelopmentandredevelopmentMember2020-12-310001035443srt:NorthAmericaMemberare:OperatingpropertiesMember2020-12-310001035443are:BXPGateway601611651GatewayBoulevardMember2020-01-012020-03-310001035443us-gaap:LeasesAcquiredInPlaceMember2020-01-012020-12-310001035443are:AboveandBelowMarketLeasesMember2020-01-012020-12-310001035443us-gaap:SubsequentEventMemberare:A401ParkDriveAnd201BrooklineAvenueMember2021-02-010001035443us-gaap:SubsequentEventMemberare:A401ParkDriveAnd201BrooklineAvenueMember2021-01-012021-02-010001035443us-gaap:SubsequentEventMemberare:A401ParkDriveMember2021-02-010001035443are:A201BrooklineAvenueMemberus-gaap:SubsequentEventMember2021-02-010001035443us-gaap:SubsequentEventMemberare:A401ParkDriveAnd201BrooklineAvenueMemberare:FuturedevelopmentprojectsMember2021-02-010001035443are:AdditionalEntitlementRightsForDevelopmentMemberus-gaap:SubsequentEventMemberare:A401ParkDriveAnd201BrooklineAvenueMember2021-02-010001035443are:AdditionalEntitlementRightsForDevelopmentMemberus-gaap:SubsequentEventMemberare:A401ParkDriveAnd201BrooklineAvenueMember2021-01-012021-02-010001035443us-gaap:SubsequentEventMember2021-02-010001035443are:January2021AcquisitionsMemberus-gaap:SubsequentEventMember2021-01-012021-02-010001035443are:January2021AcquisitionsMemberus-gaap:SubsequentEventMember2021-02-010001035443are:AboveandBelowMarketLeasesMember2020-12-310001035443are:AboveandBelowMarketLeasesMember2019-12-310001035443are:AboveandBelowMarketLeasesMember2019-01-012019-12-310001035443are:AboveandBelowMarketLeasesMember2018-01-012018-12-310001035443us-gaap:LeasesAcquiredInPlaceMember2020-12-310001035443us-gaap:LeasesAcquiredInPlaceMember2019-12-310001035443us-gaap:LeasesAcquiredInPlaceMember2019-01-012019-12-310001035443us-gaap:LeasesAcquiredInPlaceMember2018-01-012018-12-310001035443are:A510TownsendStreetAnd505BrannanStreetMember2020-11-012020-11-300001035443are:A510TownsendStreetAnd505BrannanStreetMember2020-12-310001035443are:A510TownsendStreetAnd505BrannanStreetMember2020-10-012020-12-3100010354432020-01-012020-06-300001035443are:PendingacquisitionMember2020-01-012020-06-300001035443are:A260TownsendStreetMember2020-10-012020-12-310001035443are:A220And2402ndAvenueSouthMember2020-10-012020-12-310001035443are:A945MarketStreetMember2020-07-012020-09-300001035443are:A225BinneyStreetMember2020-12-310001035443are:A75125BinneyStreetMember2020-12-310001035443are:A57CoolidgeAvenueMember2020-12-310001035443are:A409499IllinoisStreetMember2020-12-310001035443are:A1500OwensStreetMember2020-12-310001035443are:InitialownershipinterestMemberare:AlexandriaTechnologyCenterGatewayMember2020-12-310001035443are:A500ForbesBoulevardMember2020-12-310001035443are:A1029010300CampusPointDriveand4110CampusPointCourtMember2020-12-310001035443are:A5200IlluminaWayMember2020-12-310001035443are:A9625TowneCentreDriveMember2020-12-310001035443are:SDTechbyAlexandriaMember2020-12-310001035443are:TheEastlakeLifeScienceCampusByAlexandriaMember2020-12-310001035443us-gaap:EquityMethodInvesteeMemberare:A1655and1715ThirdStreetMember2020-12-310001035443us-gaap:EquityMethodInvesteeMemberare:MenloGatewayMember2020-12-310001035443us-gaap:EquityMethodInvesteeMemberare:A704QuinceOrchardRoadMember2020-12-310001035443are:A57CoolidgeAvenueMember2020-09-300001035443are:A57CoolidgeAvenueMember2020-07-012020-09-300001035443are:InitialownershipinterestMemberare:AlexandriaTechnologyCenterGatewayMember2020-09-300001035443are:AlexandriaTechnologyCenterGatewayMember2020-03-310001035443are:BXPGateway601611651GatewayBoulevardMember2020-03-310001035443are:BXPGateway601611651GatewayBoulevardMemberare:FuturedevelopmentprojectsMember2020-03-310001035443are:BXPGateway681701751GatewayBoulevardMember2020-03-310001035443are:BXPGateway681701751GatewayBoulevardMemberare:FuturedevelopmentprojectsMember2020-03-310001035443are:BXPGateway681701751GatewayBoulevardMember2020-01-012020-03-310001035443are:AlexandriaTechnologyCenterGatewayMemberus-gaap:AdditionalPaidInCapitalMember2020-01-012020-03-310001035443us-gaap:EquityMethodInvesteeMemberare:A14011413ResearchBoulevardMember2020-12-310001035443us-gaap:EquityMethodInvesteeMemberare:A14011413ResearchBoulevardMember2019-12-310001035443us-gaap:EquityMethodInvesteeMemberare:A14011413ResearchBoulevardMember2020-01-012020-03-310001035443are:A9808and9868ScrantonRoadMember2020-04-300001035443are:A9808and9868ScrantonRoadMember2020-04-202020-04-200001035443us-gaap:NoncontrollingInterestMemberare:TheEastlakeLifeScienceCampusByAlexandriaMember2020-11-300001035443are:TheEastlakeLifeScienceCampusByAlexandriaMember2020-11-300001035443are:TheEastlakeLifeScienceCampusByAlexandriaMember2020-10-012020-12-310001035443us-gaap:AdditionalPaidInCapitalMemberare:TheEastlakeLifeScienceCampusByAlexandriaMember2020-10-012020-12-310001035443us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2020-12-310001035443us-gaap:VariableInterestEntityPrimaryBeneficiaryMember2019-12-310001035443us-gaap:EquityMethodInvesteeMemberare:MenloGatewayMember2019-12-310001035443us-gaap:EquityMethodInvesteeMemberare:A704QuinceOrchardRoadMember2019-12-310001035443us-gaap:EquityMethodInvesteeMemberare:A1655and1715ThirdStreetMember2019-12-310001035443are:OtherunconsolidatedrealestatejointventuresMemberus-gaap:EquityMethodInvesteeMember2020-12-310001035443are:OtherunconsolidatedrealestatejointventuresMemberus-gaap:EquityMethodInvesteeMember2019-12-310001035443are:Secureddebtmaturingon31623Memberus-gaap:EquityMethodInvesteeMemberare:A704QuinceOrchardRoadMember2020-01-012020-12-310001035443are:Secureddebtmaturingon31623Memberus-gaap:EquityMethodInvesteeMemberus-gaap:LondonInterbankOfferedRateLIBORMemberare:A704QuinceOrchardRoadMember2020-01-012020-12-310001035443are:Secureddebtmaturingon31623Memberus-gaap:EquityMethodInvesteeMemberare:A704QuinceOrchardRoadMember2020-12-310001035443us-gaap:EquityMethodInvesteeMemberare:A1655and1715ThirdStreetMemberare:Secureddebtmaturingon31025Member2020-01-012020-12-310001035443us-gaap:EquityMethodInvesteeMemberare:A1655and1715ThirdStreetMemberare:Secureddebtmaturingon31025Member2020-12-310001035443us-gaap:EquityMethodInvesteeMemberare:MenloGatewayMemberare:Secureddebtmaturingon5135Member2020-01-012020-12-310001035443us-gaap:EquityMethodInvesteeMemberare:MenloGatewayMemberare:Secureddebtmaturingon5135Member2020-12-310001035443are:Secureddebtmaturingon81035Memberus-gaap:EquityMethodInvesteeMemberare:MenloGatewayMember2020-01-012020-12-310001035443are:Secureddebtmaturingon81035Memberus-gaap:EquityMethodInvesteeMemberare:MenloGatewayMember2020-12-310001035443us-gaap:EquityMethodInvesteeMember2020-12-310001035443srt:MinimumMember2020-01-012020-12-310001035443srt:MaximumMember2020-01-012020-12-3100010354432017-10-012017-10-010001035443are:LandparcelssubjecttoleaseagreementthatcontainsapurchaseoptionMember2020-01-012020-12-3100010354432020-03-310001035443are:A88BluxomeStreetMember2020-12-310001035443are:A88BluxomeStreetMember2020-01-012020-12-310001035443us-gaap:AccountsPayableAndAccruedLiabilitiesMember2020-12-310001035443are:GroundandOperatingLeasesMember2020-12-310001035443are:FundsheldintrustunderthetermsofcertainsecurednotespayableMember2020-12-310001035443are:FundsheldintrustunderthetermsofcertainsecurednotespayableMember2019-12-310001035443are:FundsheldinescrowrelatedtoconstructionprojectsandinvestingactivitiesMember2020-12-310001035443are:FundsheldinescrowrelatedtoconstructionprojectsandinvestingactivitiesMember2019-12-310001035443are:OtherrestrictedcashMember2020-12-310001035443are:OtherrestrictedcashMember2019-12-310001035443are:InvestmentsinpubliclytradedcompaniesMember2020-12-310001035443are:LimitedpartnershipsMember2020-12-310001035443are:EntitieswithobservablepricechangeMemberare:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMember2020-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMember2020-12-310001035443are:InvestmentsinpubliclytradedcompaniesMember2019-12-310001035443are:LimitedpartnershipsMember2019-12-310001035443are:EntitieswithobservablepricechangeMemberare:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMember2019-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMember2019-12-310001035443are:EntitieswithobservablepricechangeMemberare:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMember2020-01-012020-12-310001035443are:EntitieswithobservablepricechangeMemberare:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMember2019-01-012019-12-310001035443are:EntitieswithobservablepricechangeMemberare:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMember2018-01-012018-12-310001035443are:TotalInvestmentsHeldMember2020-01-012020-12-310001035443are:TotalInvestmentsHeldMember2019-01-012019-12-310001035443are:TotalInvestmentsHeldMember2018-01-012018-12-310001035443are:LimitedpartnershipsMember2020-01-012020-12-310001035443us-gaap:FairValueMeasurementsRecurringMemberare:InvestmentsinpubliclytradedcompaniesMember2020-12-310001035443us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberare:InvestmentsinpubliclytradedcompaniesMember2020-12-310001035443us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberare:InvestmentsinpubliclytradedcompaniesMember2020-12-310001035443us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberare:InvestmentsinpubliclytradedcompaniesMember2020-12-310001035443us-gaap:FairValueMeasurementsRecurringMemberare:InvestmentsinpubliclytradedcompaniesMember2019-12-310001035443us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberare:InvestmentsinpubliclytradedcompaniesMember2019-12-310001035443us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMemberare:InvestmentsinpubliclytradedcompaniesMember2019-12-310001035443us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberare:InvestmentsinpubliclytradedcompaniesMember2019-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310001035443us-gaap:FairValueInputsLevel1Memberare:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310001035443us-gaap:FairValueInputsLevel2Memberare:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMember2020-12-310001035443are:InvestmentsinprivatelyheldentitiesthatdonotreportNAVMemberare:EntitieswithoutobservablepricechangesMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:FairValueInputsLevel3Member2020-12-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMember2020-12-310001035443us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMember2020-12-310001035443us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:FairValueInputsLevel3Memberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:CommercialPaperMemberus-gaap:CarryingReportedAmountFairValueDisclosureMember2020-12-310001035443us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:CommercialPaperMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:CommercialPaperMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:FairValueInputsLevel3Memberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:CommercialPaperMemberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMember2019-12-310001035443us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2019-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2019-12-310001035443us-gaap:CarryingReportedAmountFairValueDisclosureMemberare:A22BillionUnsecuredSeniorLineOfCreditMember2019-12-310001035443us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsNonrecurringMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2019-12-310001035443us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsNonrecurringMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2019-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:FairValueInputsLevel3Memberus-gaap:EstimateOfFairValueFairValueDisclosureMember2019-12-310001035443us-gaap:FairValueMeasurementsNonrecurringMemberare:A22BillionUnsecuredSeniorLineOfCreditMemberus-gaap:EstimateOfFairValueFairValueDisclosureMember2019-12-310001035443are:SecuredNotesPayableMaturingFebruary62024Member2020-12-310001035443are:SecuredNotesPayableMaturingFebruary62024Member2020-01-012020-12-310001035443are:SecuredNotesPayableMaturingon7126Member2020-12-310001035443are:SecuredNotesPayableMaturingon7126Member2020-01-012020-12-310001035443are:SecuredNotesPayableMaturingJuly12036Member2020-12-310001035443are:SecuredNotesPayableMaturingJuly12036Member2020-01-012020-12-310001035443us-gaap:SecuredDebtMember2020-12-310001035443us-gaap:CommercialPaperMember2020-12-310001035443us-gaap:LondonInterbankOfferedRateLIBORMemberus-gaap:LineOfCreditMember2020-01-012020-12-310001035443us-gaap:LineOfCreditMember2020-01-012020-12-310001035443us-gaap:LineOfCreditMember2020-12-310001035443are:A4.00UnsecuredSeniorNotePayableMember2020-12-310001035443are:A4.00UnsecuredSeniorNotePayableMember2020-01-012020-12-310001035443are:A3.45unsecuredseniornotespayableduein2025Member2020-12-310001035443are:A3.45unsecuredseniornotespayableduein2025Member2020-01-012020-12-310001035443are:A4.30UnsecuredSeniorNotesPayableMember2020-12-310001035443are:A4.30UnsecuredSeniorNotesPayableMember2020-01-012020-12-310001035443are:A3.80UnsecuredSeniorNotesPayableMember2020-12-310001035443are:A3.80UnsecuredSeniorNotesPayableMember2020-01-012020-12-310001035443are:A3.95UnsecuredSeniorNotesPayableMember2020-12-310001035443are:A3.95UnsecuredSeniorNotesPayableMember2020-01-012020-12-310001035443are:A3.95UnsecuredSeniorNotesPayableDuein2028Member2020-12-310001035443are:A3.95UnsecuredSeniorNotesPayableDuein2028Member2020-01-012020-12-310001035443are:UnsecuredSeniorNotesDueinJuly2029Member2020-12-310001035443are:UnsecuredSeniorNotesDueinJuly2029Member2020-01-012020-12-310001035443are:A2.75UnsecuredSeniorNotesPayableDue2029Member2020-12-310001035443are:A2.75UnsecuredSeniorNotesPayableDue2029Member2020-01-012020-12-310001035443are:A4.70UnsecuredSeniorNotesPayableMember2020-12-310001035443are:A4.70UnsecuredSeniorNotesPayableMember2020-01-012020-12-310001035443are:A4.90UnsecuredSeniorNotesPayableMember2020-12-310001035443are:A4.90UnsecuredSeniorNotesPayableMember2020-01-012020-12-310001035443are:A3.375UnsecuredSeniorNotesPayableMember2020-12-310001035443are:A3.375UnsecuredSeniorNotesPayableMember2020-01-012020-12-310001035443are:A1875UnsecuredSeniorNotesPayableMember2020-12-310001035443are:A1875UnsecuredSeniorNotesPayableMember2020-01-012020-12-310001035443are:A4.85UnsecuredSeniorNotePayableMember2020-12-310001035443are:A4.85UnsecuredSeniorNotePayableMember2020-01-012020-12-310001035443are:A4.00UnsecuredSeniorNotesPayablesDue2050Member2020-12-310001035443are:A4.00UnsecuredSeniorNotesPayablesDue2050Member2020-01-012020-12-310001035443us-gaap:UnsecuredDebtMember2020-12-310001035443us-gaap:SecuredDebtMember2020-01-012020-12-310001035443us-gaap:SeniorNotesMember2020-12-310001035443us-gaap:SeniorNotesMember2020-01-012020-12-310001035443us-gaap:CommercialPaperMembersrt:MaximumMember2020-01-012020-12-310001035443us-gaap:CommercialPaperMember2020-01-012020-12-310001035443us-gaap:CommercialPaperMember2020-10-012020-12-310001035443are:A30BillionUnsecuredSeniorLineOfCreditMember2020-10-012020-12-310001035443us-gaap:LondonInterbankOfferedRateLIBORMemberus-gaap:LineOfCreditMember2020-12-310001035443us-gaap:LineOfCreditMember2020-10-060001035443us-gaap:LondonInterbankOfferedRateLIBORMemberus-gaap:LineOfCreditMember2020-10-012020-12-310001035443are:A750millionunsecuredseniorlineofcreditMember2020-06-300001035443are:A750millionunsecuredseniorlineofcreditMember2020-04-012020-06-300001035443are:A750millionunsecuredseniorlineofcreditMemberus-gaap:LondonInterbankOfferedRateLIBORMember2020-04-012020-06-300001035443are:A750millionunsecuredseniorlineofcreditMember2020-07-012020-09-300001035443us-gaap:CommercialPaperMember2019-09-300001035443are:A4.90UnsecuredSeniorNotesPayableMember2020-01-012020-03-310001035443are:A1875UnsecuredSeniorNotesPayableMember2020-07-012020-09-300001035443are:A390UnsecuredSeniorNotesPayableMember2020-09-300001035443are:A390UnsecuredSeniorNotesPayableMember2020-07-012020-09-300001035443are:TotalunsecuredseniornotesissuedsinceJan.12019Member2019-01-012020-12-310001035443are:TotalunsecuredseniornotesissuedsinceJan.12019Member2020-12-310001035443are:TotalunsecuredseniornotesissuedsinceJan.12019Member2020-01-012020-12-310001035443are:SecuredNotesPayableMaturingMarch102023Member2020-10-012020-12-310001035443are:SecuredNotesPayableMaturingMarch102023Member2020-12-310001035443are:SecuredDebtMaturingonJanuary2023Member2020-10-012020-12-310001035443are:SecuredDebtMaturingonJanuary2023Member2020-12-310001035443us-gaap:AccountsPayableAndAccruedLiabilitiesMember2019-12-310001035443us-gaap:SeriesDPreferredStockMember2019-10-012019-10-290001035443us-gaap:SeriesDPreferredStockMember2019-12-310001035443us-gaap:SeriesDPreferredStockMember2020-12-31are:Leaseare:Tenant0001035443are:SingleTenantMemberare:LesseeConcentrationMember2020-01-012020-12-310001035443are:SingleTenantMemberare:LesseeConcentrationMember2020-12-310001035443are:ThreeLargestTenantsMemberare:LesseeConcentrationMemberare:AnnualizedBaseRentMember2020-01-012020-12-310001035443are:FirstLargestTenantMemberare:LesseeConcentrationMemberare:AnnualizedBaseRentMember2020-01-012020-12-310001035443are:SecondLargestTenantMemberare:LesseeConcentrationMemberare:AnnualizedBaseRentMember2020-01-012020-12-310001035443are:ThirdLargestTenantMemberare:LesseeConcentrationMemberare:AnnualizedBaseRentMember2020-01-012020-12-310001035443are:ATMCommonStockOfferingProgramEstablishedFebruary2020Memberare:ForwardEquitySalesAgreementsEnteredInJanuaryAndJuly2020Member2020-01-012020-12-310001035443are:ForwardEquitySalesAgreementsEnteredinJanuary2020Member2020-01-062020-01-060001035443are:ForwardEquitySalesAgreementsEnteredInJuly2020Member2020-07-082020-07-080001035443are:ForwardEquitySalesAgreementsEnteredinJanuary2020Member2020-01-060001035443are:ForwardEquitySalesAgreementsEnteredInJuly2020Member2020-07-080001035443are:ForwardEquitySalesAgreementsEnteredInJanuaryAndJuly2020Member2020-12-310001035443are:ForwardEquitySalesAgreementsEnteredInJanuaryAndJuly2020Member2020-01-012020-12-310001035443are:ATMCommonStockOfferingProgramEstablishedFebruary2020Member2020-02-100001035443are:ForwardEquitySalesAgreementsUnderATMProgramMember2020-10-012020-12-310001035443are:ForwardEquitySalesAgreementsUnderATMProgramMember2020-12-310001035443are:ForwardEquitySalesAgreementsUnderATMProgramMember2020-01-012020-12-310001035443are:ATMCommonStockOfferingProgramEstablishedFebruary2020Member2020-12-310001035443us-gaap:AccumulatedTranslationAdjustmentMember2019-12-310001035443us-gaap:AccumulatedTranslationAdjustmentMember2020-01-012020-12-310001035443us-gaap:AccumulatedTranslationAdjustmentMember2020-12-310001035443are:StockAwardMember2017-12-310001035443are:StockAwardMember2018-01-012018-12-310001035443are:StockAwardMember2018-12-310001035443are:StockAwardMember2019-01-012019-12-310001035443are:StockAwardMember2019-12-310001035443are:StockAwardMember2020-01-012020-12-310001035443are:StockAwardMember2020-12-310001035443are:AlexandriaTechnologyCenterGatewayMemberus-gaap:NoncontrollingInterestMember2020-12-310001035443us-gaap:NoncontrollingInterestMemberare:A9808and9868ScrantonRoadMember2020-12-310001035443us-gaap:NoncontrollingInterestMemberare:TheEastlakeLifeScienceCampusByAlexandriaMember2020-12-310001035443are:FourPropertiesHeldForSaleMember2020-01-012020-12-3100010354432019-01-012019-03-3100010354432019-04-012019-06-3000010354432019-07-012019-09-3000010354432019-10-012019-12-310001035443us-gaap:SubsequentEventMember2021-01-012021-02-010001035443us-gaap:SubsequentEventMemberare:ForwardEquitySalesAgreementsEnteredInJanuary2021Member2021-01-052021-01-050001035443us-gaap:SubsequentEventMemberare:ForwardEquitySalesAgreementsEnteredInJanuary2021Member2021-01-050001035443are:AlexandriaCenterAtKendallSquareInEastCambridgeMassachusettsMember2020-12-310001035443are:TechnologySquareMember2020-12-310001035443are:TheArsenalontheCharlesMember2020-12-310001035443are:OneKendallSquareMember2020-12-310001035443are:A480500ArsenalStreetMember2020-12-310001035443are:A640MemorialDriveMember2020-12-310001035443are:Number780And790MemorialDriveMember2020-12-310001035443are:A167SidneyStreetand99ErieStreetMember2020-12-310001035443are:Number79And96CharlestownNavyYardMember2020-12-310001035443are:A380And420EStreetMember2020-12-310001035443are:A5NeccoStreetMember2020-12-310001035443are:A10NeccoStreetMember2020-12-310001035443are:A15NeccoStreetMember2020-12-310001035443are:A99AStreetMember2020-12-310001035443are:ReservoirWoodsMember2020-12-310001035443are:A275GroveStreetMember2020-12-310001035443are:OneUplandRoadAnd100TechDriveMember2020-12-310001035443are:AlexandriaParkat128Member2020-12-310001035443are:A225266and275SecondAvenueMember2020-12-310001035443are:Number19PresidentialWayMember2020-12-310001035443are:Number100BeaverStreetMember2020-12-310001035443are:A285BearHillRoadMember2020-12-310001035443are:A111and130ForbesBoulevardMember2020-12-310001035443are:Number20WalkupDriveMember2020-12-310001035443are:AlexandriaCenterForScienceAndTechnologyMissionBayMember2020-12-310001035443are:A260TownsendStreetMember2020-12-310001035443are:AlexandriaTechnologyCenterGatewayMember2020-12-310001035443are:A213249259269279EastGrandAvenueMember2020-12-310001035443are:A201HaskinsWayMember2020-12-310001035443are:Number400And450EastJamieCourtMember2020-12-310001035443are:Number500ForbesBoulevardMember2020-12-310001035443are:Number7000ShorelineCourtMember2020-12-310001035443are:Number341And343OysterPointBlvdMember2020-12-310001035443are:A849863MittenRoad866MalcolmRoadMember2020-12-310001035443are:AlexandriaCenterForLifeScienceSanCarlosMember2020-12-310001035443are:A3825and3875FabianWayMember2020-12-310001035443are:A825and835IndustrialRoadMember2020-12-310001035443are:AlexandriaPARCMember2020-12-310001035443are:A333034123450And3460HillviewMember2020-12-310001035443are:Number2425GarciaAveAnd2400And2450BayshorePkyMember2020-12-310001035443are:ShorewayScienceCenterMember2020-12-310001035443are:A1450PageMillRoadMember2020-12-310001035443are:Number3350WestBayshoreRoadMember2020-12-310001035443are:Number2625And2627And2631HanoverStreetMember2020-12-310001035443are:AlexandriaCenterforLifeScienceMember2020-12-310001035443are:A219East42ndStreetMember2020-12-310001035443are:A475030thStreetMember2020-12-310001035443are:AlexandriaLifeScienceFactoryatLongIslandCityMember2020-12-310001035443are:ARESpectrumMember2020-12-310001035443are:TorreyRidgeScienceCenterMember2020-12-310001035443are:ARESunriseMember2020-12-310001035443are:ARENautilusMember2020-12-310001035443are:A1111911255And11355NorthTorreyPinesRoadMember2020-12-310001035443are:A3545CrayCourtMember2020-12-310001035443are:AlexandriaPointMember2020-12-310001035443are:Number5200IlluminaWayMainMember2020-12-310001035443are:UniversityDistrictMember2020-12-310001035443are:A6420And6450SequenceDriveMember2020-12-310001035443are:A99659995SummersRidgeRoadMember2020-12-310001035443are:AREPortolaMember2020-12-310001035443are:A58105820NancyRidgeDriveMember2020-12-310001035443are:Number7330CarrollRoadMember2020-12-310001035443are:A9877WaplesStreetMember2020-12-310001035443are:Number5871OberlinDriveMember2020-12-310001035443are:A39113931398540254031And4045SorrentoValleyBoulevardMember2020-12-310001035443are:A110251103511045110551106511075RoselleStreetMember2020-12-310001035443are:Number13112EveningCreekDriveMember2020-12-310001035443are:TownsgatebyAlexandriaMember2020-12-310001035443are:A400DexterAvenueNorthMember2020-12-310001035443are:A23015thAvenueMember2020-12-310001035443are:Number219TerryAvenueMember2020-12-310001035443are:A601DexterAvenueNorthMember2020-12-310001035443are:A701DexterAvenueNorthMember2020-12-310001035443are:A8304thAvenueSouthMember2020-12-310001035443are:Number3000And3018WesternAvenueMember2020-12-310001035443are:Number410WHarrisonAnd410ElliottAvenueWestMember2020-12-310001035443are:A10104thAvenueSouthMember2020-12-310001035443are:A9800980499009920And9950MedicalCenterDriveMember2020-12-310001035443are:A9704970897129714MedicalCenterDriveMember2020-12-310001035443are:Number1330PiccardDriveMember2020-12-310001035443are:A9605MedicalCenterDriveMember2020-12-310001035443are:Number1500And1550EastGudeDriveMember2020-12-310001035443are:A14920and15010BroschartRoadMember2020-12-310001035443are:Number1405ResearchBoulevardMember2020-12-310001035443are:Number5ResearchPlaceMember2020-12-310001035443are:Number5ResearchCourtMember2020-12-310001035443are:A9920BelwardCampusDriveMember2020-12-310001035443are:Number12301ParklawnDriveMember2020-12-310001035443are:A14200ShadyGroveRoadMember2020-12-310001035443are:AlexandriaTechnologyCenterGaithersburgIMember2020-12-310001035443are:AlexandriaTechnologyCenterGaithersburgIIMember2020-12-310001035443are:Number401ProfessionalDriveMember2020-12-310001035443are:Number950WindRiverLaneMember2020-12-310001035443are:Number620ProfessionalDriveMember2020-12-310001035443are:Number8000And9000And10000VirginiaManorRoadMember2020-12-310001035443are:Number14225NewbrookDriveMember2020-12-310001035443are:AlexandriaCenterForLifeScienceDurhamMember2020-12-310001035443are:AlexandriaCenterForAgTechMember2020-12-310001035443are:AlexandriaCenterForAdvancedTechnologiesMember2020-12-310001035443are:AlexandriaTechnologyCenterAlstonMember2020-12-310001035443are:Number108And110And112And114AlexanderRoadMember2020-12-310001035443are:AlexandriaInnovationCenterResearchTriangleParkMember2020-12-310001035443are:Number7TriangleDriveMember2020-12-310001035443are:Number2525StateHighway54Member2020-12-310001035443are:A407DavisDriveMember2020-12-310001035443are:Number601KeystoneParkDriveMember2020-12-310001035443are:A6040GeorgeWattsHillDriveMember2020-12-310001035443are:Number5TriangleDriveMember2020-12-310001035443are:Number6101QuadrangleDriveMember2020-12-310001035443country:CA2020-12-310001035443are:VariousMember2020-12-310001035443are:ChinaPropertiesMember2020-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

Commission file number 1-12993

ALEXANDRIA REAL ESTATE EQUITIES, INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Maryland | | 95-4502084 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

26 North Euclid Avenue, Pasadena, California 91101

(Address of principal executive offices) (Zip code)

(626) 578-0777

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.01 par value per share | ARE | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes o No x

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | x | | Smaller reporting company | o |

| Accelerated filer | o | | Emerging growth company | o |

| Non-accelerated filer | o | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the shares of Common Stock held by non-affiliates of registrant was approximately $20.2 billion based on the closing price for such shares on the New York Stock Exchange on June 30, 2020.

As of January 15, 2021, 136,692,746 shares of common stock were outstanding.

Documents Incorporated by Reference

Part III of this annual report on Form 10-K incorporates certain information by reference from the registrant’s definitive proxy statement to be filed within 120 days of the end of the fiscal year covered by this annual report on Form 10-K in connection with the registrant’s annual meeting of stockholders to be held on or about May 18, 2021.

INDEX TO FORM 10-K

ALEXANDRIA REAL ESTATE EQUITIES, INC.

| | | | | | | | |

| PART I | Page |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART II | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART III | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART IV | |

| | |

GLOSSARY

The following abbreviations or acronyms that may be used in this document shall have the adjacent meanings set forth below:

| | | | | |

| |

| |

| |

| ASU | Accounting Standards Update |

| ATM | At the Market |

| BBA | British Bankers’ Association |

| CIP | Construction in Progress |

| |

| EPS | Earnings per Share |

| FASB | Financial Accounting Standards Board |

| |

| |

| FDA | U.S. Food and Drug Administration |

| FDIC | Federal Deposit Insurance Corporation |

| FFO | Funds From Operations |

| GAAP | U.S. Generally Accepted Accounting Principles |

| HVAC | Heating, Ventilation, and Air Conditioning |

| IASB | International Accounting Standards Board |

| IFRS | International Financial Reporting Standards |

| IRS | Internal Revenue Service |

| JV | Joint Venture |

LEED® | Leadership in Energy and Environmental Design |

| LIBOR | London Interbank Offered Rate |

| Nareit | National Association of Real Estate Investment Trusts |

| NAV | Net Asset Value |

| |

| |

| |

| NYSE | New York Stock Exchange |

| REIT | Real Estate Investment Trust |

| RSF | Rentable Square Feet/Foot |

| SEC | Securities and Exchange Commission |

| SF | Square Feet/Foot |

| SoDo | South of Downtown submarket of Seattle |

| SoMa | South of Market submarket of San Francisco |

| |

| U.S. | United States |

| VIE | Variable Interest Entity |

PART I

Forward-looking statements

Certain information and statements included in this annual report on Form 10-K, including, without limitation, statements containing the words “forecast,” “guidance,” “goals,” “projects,” “estimates,” “anticipates,” “believes,” “expects,” “intends,” “may,” “plans,” “seeks,” “should,” or “will,” or the negative of these words or similar words, constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements involve inherent risks and uncertainties regarding events, conditions, and financial trends that may affect our future plans of operations, business strategy, results of operations, and financial position. A number of important factors could cause actual results to differ materially from those included within or contemplated by the forward-looking statements, including, but not limited to, the description of risks and uncertainties in “Item 1A. Risk factors” in this annual report on Form 10-K. Additional information regarding risk factors that may affect us is included in “Item 7. Management’s discussion and analysis of financial condition and results of operations” in this annual report on Form 10-K. Readers of our annual report on Form 10-K should also read our SEC and other publicly filed documents for further discussion regarding such factors.

As used in this annual report on Form 10-K, references to the “Company,” “Alexandria,” “we,” “us,” and “our” refer to Alexandria Real Estate Equities, Inc. and its consolidated subsidiaries. The following discussion should be read in conjunction with our consolidated financial statements and notes thereto under “Item 15. Exhibits and Financial Statement Schedules” in this annual report on Form 10-K.

ITEM 1. BUSINESS

Overview

We are a Maryland corporation formed in October 1994 that has elected to be taxed as a REIT for federal income tax purposes. We are an S&P 500® urban office REIT and the first, longest-tenured, and pioneering owner, operator, and developer uniquely focused on collaborative life science, technology, and agtech campuses in AAA innovation cluster locations. We consider AAA locations to be highly desirable for tenancy by life science, technology, and agtech entities because of their close proximity to concentrations of specialized skills, knowledge, institutions, and related businesses. Such locations are generally characterized by high barriers to entry for new landlords, high barriers to exit for tenants, and a limited supply of available space. Founded in 1994, Alexandria pioneered this niche and has since established a significant market presence in key locations, including Greater Boston, San Francisco, New York City, San Diego, Seattle, Maryland, and Research Triangle.

Alexandria develops dynamic urban cluster campuses and vibrant ecosystems that enable and inspire the world’s most brilliant minds and innovative companies to create life-changing scientific and technological breakthroughs. We believe in the utmost professionalism, humility, and teamwork. Alexandria manages its properties through fully integrated regional teams with real estate, life science, technology, and agtech expertise. Our tenants include multinational pharmaceutical companies; public and private biotechnology companies; life science product, service, and medical device companies; digital health, technology, and agtech companies; academic and medical research institutions; U.S. government research agencies; non-profit organizations; and venture capital firms. Alexandria has a longstanding and proven track record of developing Class A properties clustered in urban life science, technology, and agtech campuses that provide its innovative tenants with highly dynamic and collaborative environments that enhance their ability to successfully recruit and retain world-class talent and inspire productivity, efficiency, creativity, and success. Alexandria also provides strategic risk capital to transformative life science, technology, and agtech companies through its venture capital arm. We believe our unique business model and diligent underwriting ensure a high-quality and diverse tenant base that should result in higher occupancy levels, longer lease terms, higher rental income, higher returns, and greater long-term asset value.

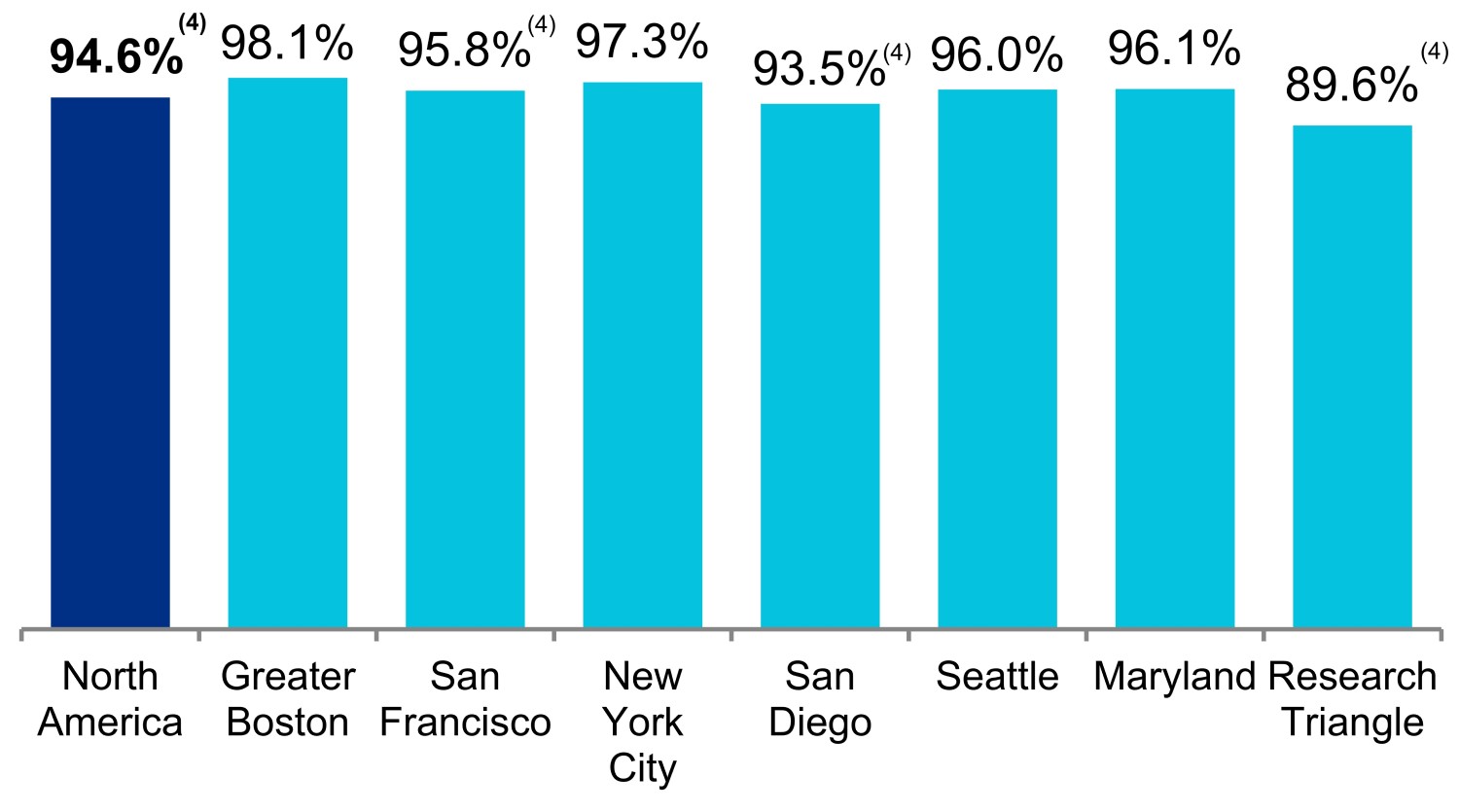

As of December 31, 2020, Alexandria’s total market capitalization was $31.9 billion. For the definition of “Total market capitalization,” refer to the “Non-GAAP measures and definitions” section under Item 7 in this annual report on Form 10-K. Our asset base in North America consisted of 49.7 million SF, which includes 31.9 million RSF of operating properties and 3.3 million RSF of Class A properties undergoing construction, 7.1 million RSF of near-term and intermediate-term development and redevelopment projects, and 7.4 million SF of future development projects as of December 31, 2020. These operating properties and development projects include 40 properties that are held by consolidated real estate joint ventures and six properties that are held by unconsolidated real estate joint ventures. The occupancy percentage of our operating properties in North America was 94.6% as of December 31, 2020. Our 10-year average occupancy rate of operating properties as of December 31, 2020, was 96%. Investment-grade or publicly traded large cap tenants represented 55% of our annual rental revenue in effect as of December 31, 2020. Additional information regarding our consolidated and unconsolidated real estate joint ventures is included in “Item 7. Management’s discussion and analysis of financial condition and results of operations” in this annual report on Form 10-K. Additional information regarding risk factors that may affect us is included in “Item 1A. Risk factors” and “Item 7. Management’s discussion and analysis of financial condition and results of operations” in this annual report on Form 10-K.

Business objective and strategies

Our primary business objective is to maximize long-term asset value and shareholder returns based on a multifaceted platform of internal and external growth. A key element of our strategy is our unique focus on Class A properties clustered in urban campuses located in AAA innovation cluster locations. These key urban campus locations are characterized by high barriers to entry for new landlords, high barriers to exit for tenants, and a limited supply of available space. They represent highly desirable locations for tenancy by life science, technology, and agtech entities because of their close proximity to concentrations of specialized skills, knowledge, institutions, and related businesses. Our strategy also includes drawing upon our deep and broad real estate, life science, technology, and agtech relationships in order to identify and attract new and leading tenants and to source additional value-creation real estate.

Our tenant base is broad and diverse within the life science, technology, and agtech industries and reflects our focus on regional, national, and international tenants with substantial financial and operational resources. For a more detailed description of our properties and tenants, refer to “Item 2. Properties” in this annual report on Form 10-K. We have an experienced Board of Directors and are led by an executive and senior management team with extensive experience in the real estate, life science, technology, and agtech industries.

Acquisitions

We seek to identify and acquire high-quality properties in our target cluster markets. Critical evaluation of prospective property acquisitions is an essential component of our acquisition strategy. When evaluating acquisition opportunities, we assess a full range of matters relating to the prospective property or properties, including:

•Proximity to centers of innovation and technological advances;

•Location of the property and our strategy in the relevant market;

•Quality of existing and prospective tenants;

•Condition and capacity of the building infrastructure;

•Physical condition of the structure and common area improvements;

•Quality and generic characteristics of the improvements;

•Opportunities available for leasing vacant space and for re-tenanting or renewing occupied space;

•Availability of and/or ability to add appropriate tenant amenities;

•Availability of land for future ground-up development of new space;

•Opportunities to generate higher rent through redevelopment of existing space;

•The property’s unlevered yields; and

•Our ability to increase the property’s long-term financial returns.

Development, pre-construction, and redevelopment

A key component of our business model is our value-creation development projects. Our development strategy is primarily to pursue selective projects with significant pre-leasing for which we expect to achieve appropriate investment returns and generally match a source of funds for this use. Our value-creation development projects focus on high-quality, generic, and reusable office/laboratory or tech office space to meet the real estate requirements of our diverse group of tenants.

We seek to meet growing demand from our stakeholders and continuously improve the efficiency of our buildings. We have committed to significant building goals to promote wellness and productivity for our buildings’ occupants, including targeting a minimum of LEED® Gold certification on all new ground-up construction projects.

Pre-construction activities include entitlements, permitting, design, site work, and other activities preceding commencement of construction of aboveground building improvements, which are focused on reducing the time required to deliver projects to prospective tenants. These critical activities add significant value to our future ground-up development and are required for the vertical construction of buildings. We normally do not commence vertical construction of new projects prior to achieving significant pre-leasing.

Another key component of our business model is our value-creation redevelopment of existing office, warehouse, or shell space, or newly acquired properties, into high-quality, generic, and reusable office/laboratory space that can be leased at higher rental rates. Our redevelopment strategy generally includes significant pre-leasing of projects prior to the commencement of redevelopment.

Non-real estate investments

We also hold equity investments in publicly traded companies, limited partnerships, and privately held entities primarily involved in the life science, technology, and agtech industries. We invest primarily in highly innovative entities whose focus on the development of therapies and products that advance health and transform patients’ lives is aligned with Alexandria’s purpose of making a positive and meaningful impact on the health, safety, and well-being of the global community. Our status as a REIT limits our ability to make such non-real estate investments. Therefore, we conduct, and will continue to conduct, our non-real estate investment activities in a manner that complies with REIT requirements.

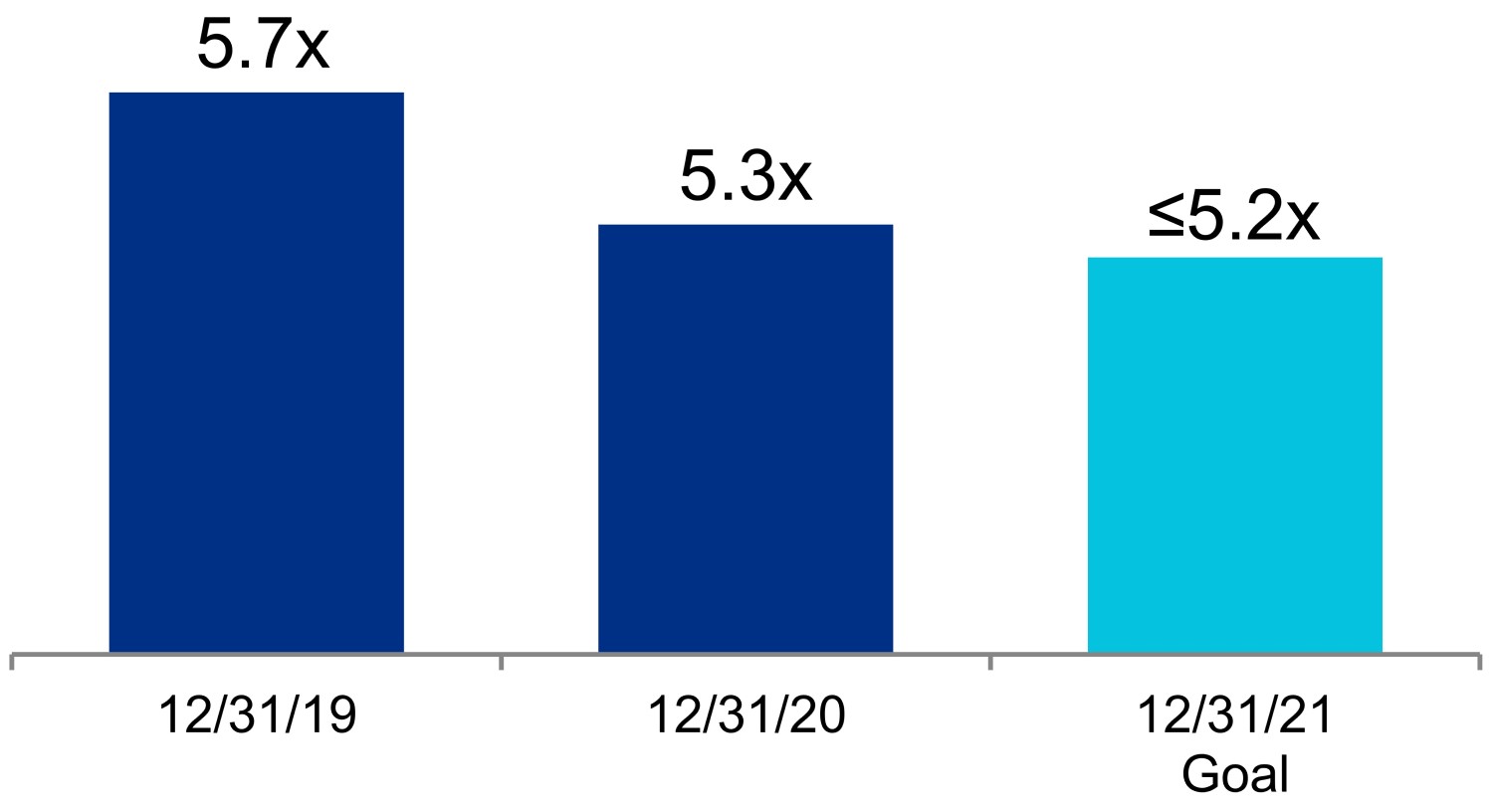

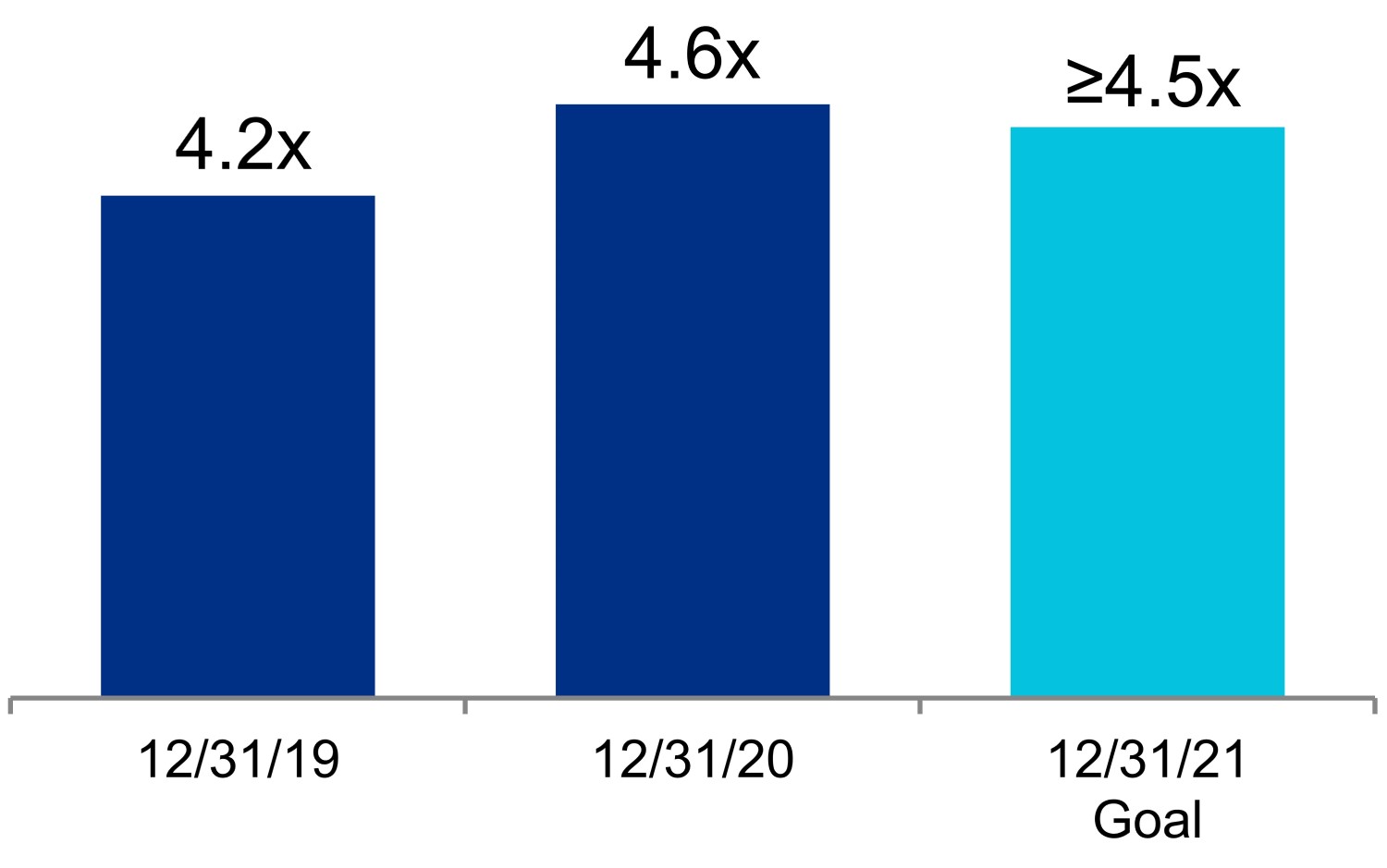

Balance sheet and financial strategy

We seek to maximize balance sheet liquidity and flexibility, cash flows, and cash available for distribution to our stockholders through the ownership, operation, management, and selective acquisition, development, and redevelopment of office/laboratory and tech office space, as well as the management of our balance sheet. In particular, we seek to maximize balance sheet liquidity and flexibility, cash flows, and cash available for distribution to our stockholders by:

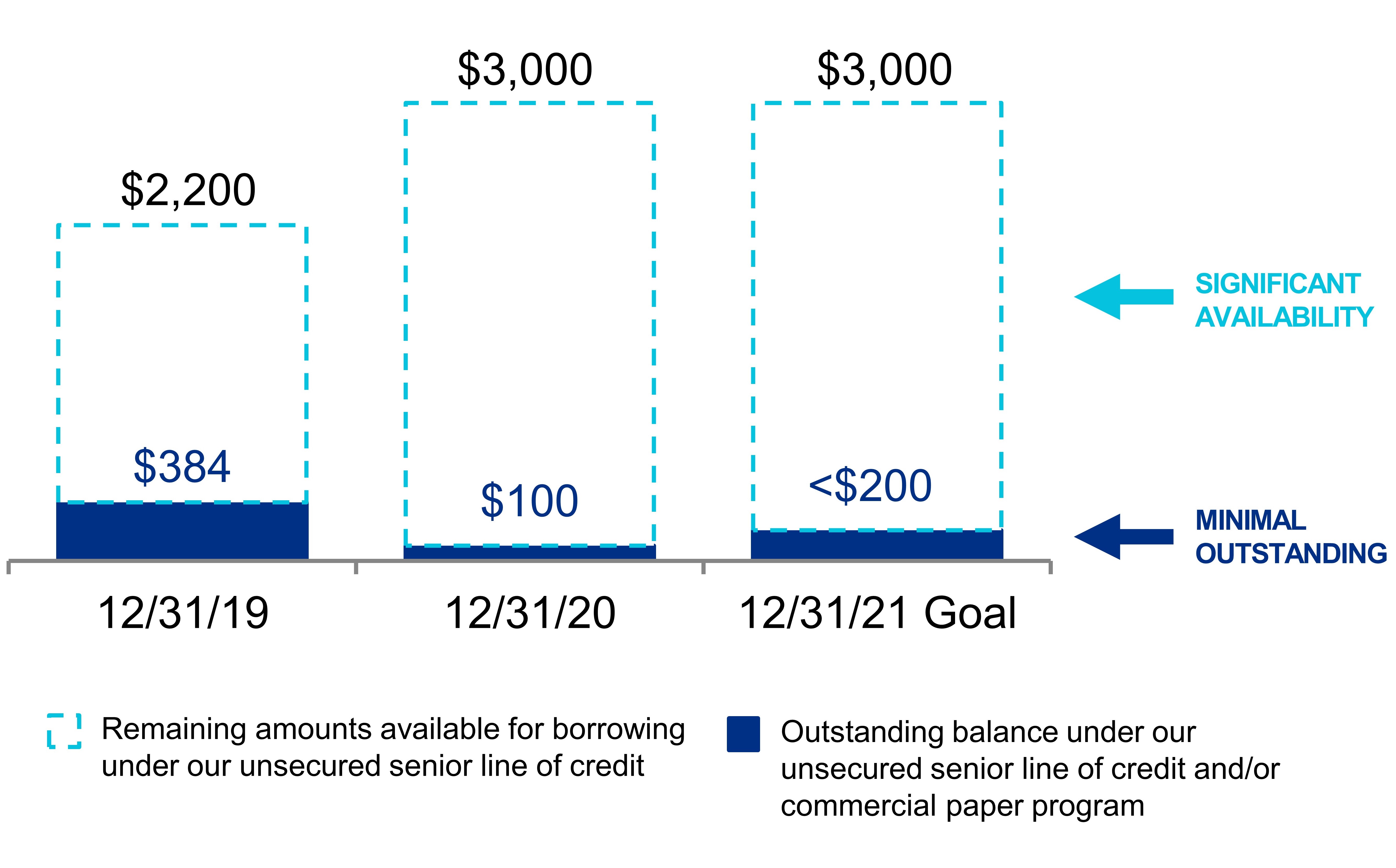

•Maintaining access to diverse sources of capital, including operating cash flows after dividends, incremental debt, asset sales, and other capital such as the sale of equity or joint venture capital;

•Maintaining significant liquidity through borrowing capacity under our unsecured senior line of credit and commercial paper program, marketable securities, issuances of forward equity contracts from time to time, and cash, cash equivalents, and restricted cash;

•Continuing to improve our credit profile;

•Minimizing the amount of near-term debt maturities in a single year;

•Maintaining commitment to long-term capital to fund growth;

•Maintaining low to modest leverage;

•Minimizing variable interest rate risk;

•Generating high-quality, strong, and increasing operating cash flows;

•Selectively selling real estate assets, including land parcels and non-core/“core-like” operating assets, and reinvesting the proceeds into our highly leased value-creation development and redevelopment projects;

•Allocating capital to Class A properties located in collaborative life science, technology, and agtech campuses in AAA urban innovation clusters;

•Maintaining geographic diversity in urban intellectual centers of innovation;

•Selectively acquiring high-quality office/laboratory and tech office space in our target urban innovation cluster submarkets at prices that enable us to realize attractive returns;

•Selectively developing properties in our target urban innovation cluster submarkets;

•Selectively redeveloping existing office, warehouse, or shell space, or newly acquired properties, into high-quality, generic, and reusable office/laboratory space that can be leased at higher rental rates in our target urban innovation cluster submarkets;

•Renewing existing tenant space at higher rental rates to the extent possible;

•Minimizing tenant improvement costs;

•Improving investment returns through the leasing of vacant space and the replacing of existing tenants with new tenants at higher rental rates;

•Executing leases with high-quality tenants and proactively monitoring tenant health;

•Maintaining solid occupancy while attaining high rental rates;

•Realizing contractual rental rate escalations; and

•Implementing effective cost control measures, including negotiating pass-through provisions in tenant leases for operating expenses and certain capital expenditures.

Competition

In general, other office/laboratory and tech office properties are located in close proximity to our properties. The amount of rentable space available in any market could have a material effect on our ability to rent space and on the rental rates we can attain for our properties. In addition, we compete for investment opportunities with other REITs, insurance companies, pension and investment funds, private equity entities, partnerships, developers, investment companies, owners/occupants, and foreign investors. Many of these entities have substantially greater financial resources than we do and may be able to invest more than we can or accept more risk than we are willing to accept. These entities may be less sensitive to risks with respect to the creditworthiness of a tenant or the overall expected returns from real estate investments. In addition, as a result of their financial resources, our competitors may offer more free rent concessions, lower rental rates, or higher tenant improvement allowances in order to attract tenants. These leasing incentives could hinder our ability to maintain or raise rents and attract or retain tenants. Competition may also reduce the number of suitable investment opportunities available to us or may increase the bargaining power of property owners seeking to sell. Competition in acquiring existing properties and land, both from institutional capital sources and from other REITs, has been very strong over the past several years; however, we believe we have differentiated ourselves from our competitors. As the first and only publicly traded urban office REIT to focus primarily on the office/laboratory real estate niche, we provide world-class collaborative life science, technology, and agtech campuses in AAA innovation cluster locations and maintain and cultivate many of the most important and strategic relationships in the life science, technology, and agtech industries.

Financial information about our reportable segment

Refer to Note 2 – “Summary of significant accounting policies” to our consolidated financial statements under Item 15 in this annual report on Form 10-K for information about our one reportable segment.

Regulation

General

Properties in our markets are subject to various laws, ordinances, and regulations, including regulations relating to common areas. We believe we have the necessary permits and approvals to operate each of our properties.

Americans with Disabilities Act

Our properties must comply with Title III of the Americans with Disabilities Act of 1990 (“ADA”) to the extent that such properties are “public accommodations” as defined by the ADA. The ADA may require removal of structural barriers to permit access by persons with disabilities in certain public areas of our properties where such removal is readily achievable. We believe that our properties are in substantial compliance with the ADA and that we will not be required to incur substantial capital expenditures to address the requirements of the ADA. However, noncompliance with the ADA could result in the imposition of fines or an award of damages to private litigants. The obligation to make readily achievable accommodations is an ongoing one, and we will continue to assess our properties and make alterations as appropriate in this respect.

Environmental matters

Under various environmental protection laws, a current or previous owner or operator of real estate may be liable for contamination resulting from the presence or discharge of hazardous or toxic substances at that property and may be required to investigate and remediate contamination located on or emanating from that property. Such laws often impose liability without regard to whether the owner or operator knew of, or was responsible for, the presence of the contaminants, and the liability may be joint and several. Previous owners may have used some of our properties for industrial and other purposes, so those properties may contain some level of environmental contamination. The presence of contamination or the failure to remediate contamination at our properties may expose us to third-party liability or may materially adversely affect our ability to sell, lease, or develop the real estate or to borrow using the real estate as collateral.

Some of our properties may have asbestos-containing building materials. Environmental laws require that asbestos-containing building materials be properly managed and maintained and may impose fines and penalties on building owners or operators for failure to comply with these requirements. These laws may also allow third parties to seek recovery from owners or operators for personal injury associated with exposure to asbestos-containing building materials.

In addition, some of our tenants handle hazardous substances and wastes as part of their routine operations at our properties. Environmental laws and regulations subject our tenants, and potentially us, to liability resulting from such activities. Environmental liabilities could also affect a tenant’s ability to make rental payments to us. We require our tenants to comply with these environmental laws and regulations and to indemnify us against any related liabilities.

Independent environmental consultants have conducted Phase I or similar environmental site assessments on the properties in our portfolio. Site assessments are intended to discover and evaluate information regarding the environmental condition of the surveyed property and surrounding properties and do not generally include soil samplings, subsurface investigations, or an asbestos survey. To date, these assessments have not revealed any material environmental liability that we believe would have a material adverse effect on our business, assets, or results of operations. Nevertheless, it is possible that the assessments on our properties have not revealed all environmental conditions, liabilities, or compliance concerns that may have arisen after the review was completed or may arise in the future; and future laws, ordinances, or regulations may also impose additional material environmental liabilities.

Insurance

With respect to our properties, we carry commercial general liability, all-risk property, and business interruption insurance, including loss of rental income coverage. We select policy specifications and insured limits that we believe to be appropriate given the relative risk of loss and the cost of the coverage. In addition, we have obtained earthquake insurance for certain properties located in the vicinity of known active earthquake zones in an amount and with deductibles we believe are commercially reasonable. We also carry environmental insurance and title insurance policies on our properties. We generally obtain title insurance policies when we acquire the property, with each policy covering an amount equal to the initial purchase price of each property. Accordingly, any of our title insurance policies may be in an amount less than the current value of the related property. Additional information regarding risk factors that may affect us is included in “Item 1A. Risk factors” in this annual report on Form 10-K.

Available information

Copies of our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, including any amendments to the foregoing reports, are available, free of charge, through our corporate website at www.are.com as soon as is reasonably practicable after such material is electronically filed with, or furnished to, the SEC. The current charters of our Board of Directors’ Audit, Compensation, and Nominating & Governance Committees, along with our corporate governance guidelines and Business Integrity Policy and Procedures for Reporting Non-Compliance (the “Business Integrity Policy”), are also available on our corporate website. Additionally, any amendments to, and waivers of, our Business Integrity Policy that apply to our Co-Chief Executive Officers or our Chief Financial Officer will be available free of charge on our corporate website in accordance with applicable SEC and NYSE requirements. Written requests should be sent to Alexandria Real Estate Equities, Inc., 26 North Euclid Avenue, Pasadena, California 91101, Attention: Investor Relations. The public may also download these materials from the SEC’s website at www.sec.gov.

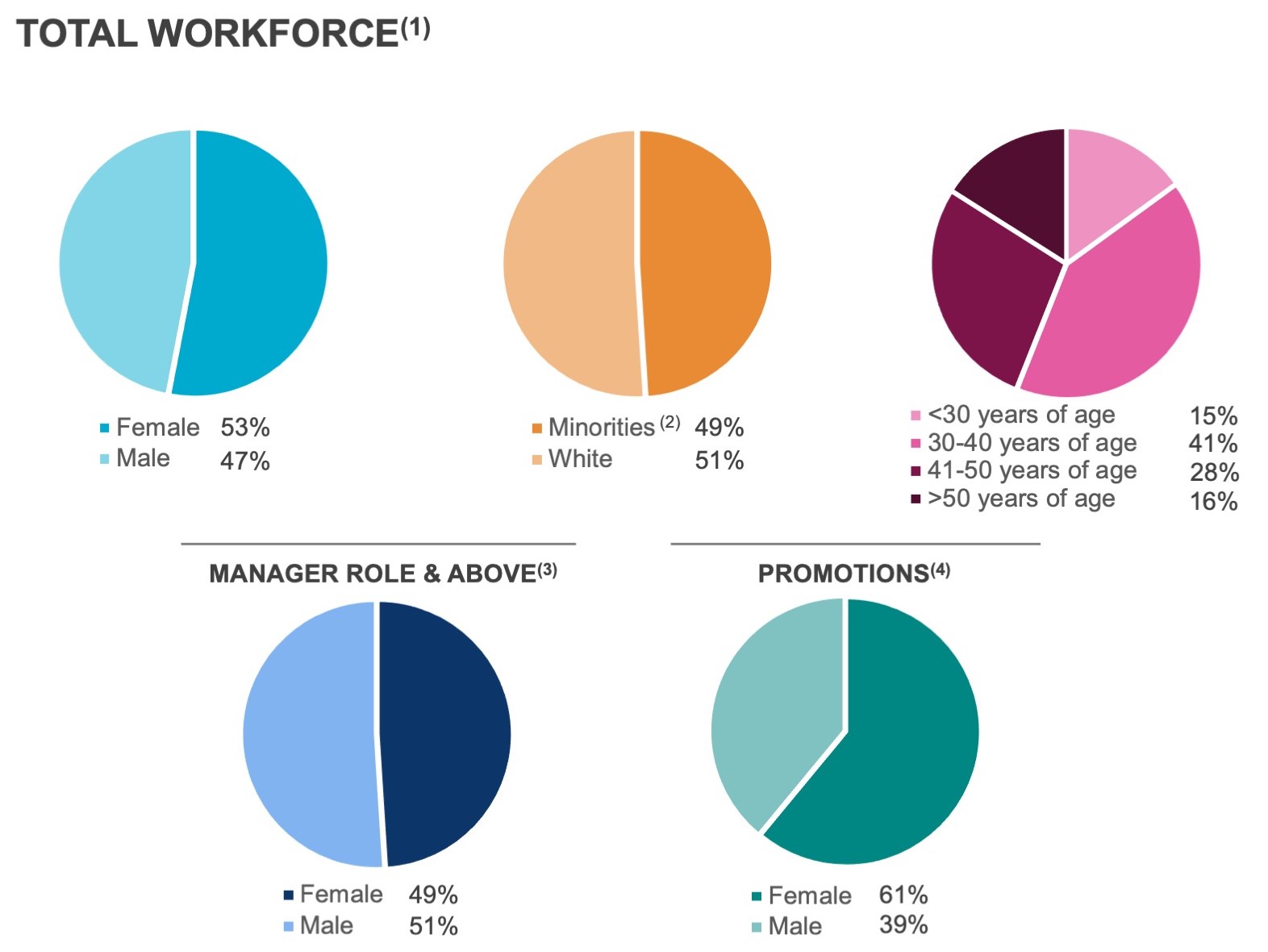

Human Capital

As of December 31, 2020, we had 470 employees. We believe that we have good relations with our employees. We have adopted a Business Integrity Policy that applies to all of our employees, and its receipt and review by each employee is documented and verified annually. In order to promote an exceptional corporate culture, Alexandria continuously monitors employee satisfaction, seeks employee feedback, and seeks opportunities to enhance our offerings. We participate in annual performance reviews with our employees and conduct formal employee surveys, and our talent management team holds annual meetings with employees. The positive employee experience is evidenced by our low voluntary and total turnover rates (averaging 4.1% and 8.1%, respectively, over the last five years, from 2016 to 2020), which are well below the reported median voluntary and total turnover rates of 10% and 18.0%, respectively, in the Nareit 2020 Compensation & Benefits Survey (data for 2019).

We have an exceptional track record of identifying highly qualified candidates for promotion from within the Company. Alexandria’s executive and senior management team, represented by our senior vice presidents and above, consists of 47 individuals, averaging 24 years of real estate experience, including 12 years with Alexandria. Our executive management team alone averages 17 years of experience with Alexandria. Alexandria’s executive and senior management team has unique experience and expertise in creating, owning, and operating highly dynamic and collaborative campuses in key urban life science, technology, and agtech cluster locations. Alexandria’s highly experienced management team also includes regional market directors with leading reputations and longstanding relationships within the life science, technology, and agtech communities in their respective urban innovation clusters. We believe that our expertise, experience, reputation, and key relationships in the real estate, life science, technology, and agtech industries provide Alexandria with significant competitive advantages in attracting new business opportunities.

At Alexandria, people come first. At the outset of the COVID-19 pandemic, we moved swiftly to support our employees’ medical, mental, emotional, physical, and financial health. Our commitment to our people has always been our primary focus, and we continue to devote extraordinary efforts to hire, develop, and retain a healthy and diverse workforce.

Supporting our employees through COVID-19 and beyond

In response to COVID-19-related state and local government orders to stay at home, Alexandria immediately issued a $1,000 emergency bonus to each of our non-officer employees, connected employees to LiveHealth Online support, and shared comprehensive resources and tools to help our team members cope with stress, anxiety, isolation, and loss and also balance work and child care obligations. To further support our employees in prioritizing their health and well-being, the Company temporarily enhanced our existing wellness benefit. This enrichment included reimbursement of fitness and mindfulness applications, online classes, and exercise equipment to help our employees reach their individual wellness goals and stay physically and mentally strong. Additionally, Alexandria has been able to leverage our world-class network to curate a series of internal webinars featuring leading experts on COVID-19 to keep our employees informed and address some of their questions or pressing concerns.

Providing exceptional benefits to support our employees’ well-being, medical and financial health

We provide a comprehensive benefits package intended to meet and exceed the needs of our employees and their families. Our highly competitive offering helps our employees stay healthy, balance their work and personal lives, and meet their financial and retirement goals. We pay 100% of the health insurance premiums for our employees and their families and provide an employee assistance program to help them address a wide range of issues. In addition, Alexandria’s Operation CARE program provides the following services to our employees:

•Alexandria Access. Alexandria’s unparalleled network in the life science community affords us access to deep medical expertise. Alexandria Access makes this expertise available to our employees and their immediate family members who are experiencing an illness or injury and would benefit from specialized expertise.

•Matching Gifts. Alexandria matches each employee’s financial contributions to, or funds raised for, eligible nonprofit organizations on a dollar-for-dollar basis, up to $2,500 per person each calendar year, to double the impact of their charitable gifts.

•Volunteer Time Off. Each Alexandria employee receives 16 hours (two days) per calendar year of paid volunteer time off to use at the eligible non-profit(s) of their choice.

•Volunteer Rewards. When an Alexandria employee volunteers more than 25 hours in any one quarter at an eligible nonprofit(s), Alexandria donates a total of $2,500 to the eligible non-profit(s) of their choice.

Investing in professional development and training

We understand that to attract and retain the best talent, we must provide opportunities for our people to grow and develop. Therefore, we invest in training and development programs to enhance our employees’ engagement, effectiveness, and well-being.

In-person and virtual training topics include project management, business writing, leadership, change management, interviewing, presentations, productivity, conversations crucial to business results, effective one-on-ones, goal setting, delegation,

flexibility, self-direction, and feedback. Our annual mentoring program allows employees to partner with senior leaders throughout the organization and receive career guidance. To customize training and development, we conduct needs assessments and design training programs for specific functional teams as well as offer a highly customized coaching program for high-potential executives, leaders, and teams. We provide access to expert panels and cutting-edge information via webinars in order to share information and support our team. We also provide on-demand learning resources such as LinkedIn Learning for employees to take classes that range from creating effective PowerPoint presentations to understanding how the brain reacts to stress.

To continuously monitor and improve employee performance and engagement, we issue satisfaction surveys and conduct annual performance reviews. Our talent management team additionally conducts formal surveys and holds regular feedback meetings with our employees.

Building a diverse and inclusive workforce

We work every day to create an open and respectful environment where everyone can actively contribute, have equal access to opportunities and resources, be themselves, and realize their potential.

Our Corporate Governance Guidelines highlight the Board of Directors’ focus on diversity, which explicitly states the board’s commitment to considering qualified women and minority director candidates, as well its policy of requesting an initial list of diverse candidates of any search firm it retains. As an Equal Opportunity Employer, we emphasize inclusion through hiring and compensation practices and consider a pool of diverse candidates for open positions and internal advancement opportunities. To address issues related to pay discrimination, we do not ask potential candidates about their current or previous compensation during the hiring process, and we incorporate equal and fair pay reviews into every employment compensation decision. To reinforce our corporate culture of respect, diversity, and inclusion, each of our employees completes anti-harassment training annually.

(1)As of December 31, 2020.

(2)Minorities are defined to include individuals of Asian, Black/African American, Hispanic/Latino, Native American or Pacific Islander, or multiracial background. We determine race and gender based on our employees' self-identification or other information compiled to meet requirements of the U.S. government.

(3)Managers and above include individuals who lead others and/or oversee projects.

(4)Represents a five-year average from 2016 to 2020.

Overview

The following risk factors may adversely affect our overall business, financial condition, results of operations, and cash flows; our ability to make distributions to our stockholders; our access to capital; or the market price of our common stock, as further described in each risk factor below. In addition to the information set forth in this annual report on Form 10-K, one should carefully review and consider the information contained in our other reports and periodic filings that we make with the SEC. Those risk factors could materially affect our overall business, financial condition, results of operations, and cash flows; our ability to make distributions to our stockholders; our access to capital; or the market price of our common stock. The risks that we describe in our public filings are not the only risks that we face. Additional risks and uncertainties not presently known to us, or that we currently consider immaterial, also may materially adversely affect our business, financial condition, and results of operations. Additional information regarding forward-looking statements is included in the beginning of “Part I” in this annual report on Form 10-K.

Risk factors summary

An investment in our securities involves various risks. Such risks, including those set forth in the summary of material risks in this Item 1A, should be carefully considered before purchasing our securities.

Risks related to operating factors

•We may be unable to identify and complete acquisitions, investments, or development or redevelopment projects or to successfully and profitably operate properties.

•We could default on our ground leases or be unable to renew or re-lease our land or space on favorable terms or at all. Our tenants may also be unable to pay us rent.

•The cost of maintaining and improving the quality of our properties may be higher than anticipated, and we may be unable to pass any increased operating costs through to our tenants, which can result in reduced cash flows and profitability.

•We could be held liable for environmental damages resulting from our tenants’ use of hazardous materials, or from harmful mold, poor air quality, or other defects from our properties, or we could face increased costs in complying with other environmental laws.

•The loss of services of any of our senior officers or key employees and increased competition for skilled personnel could adversely affect us and/or increase our labor costs.

•We rely on a limited number of vendors to provide utilities and other services at our properties, and disruption in such services may have an adverse effect on our operations and financial condition.

•Our insurance may not adequately cover all of our potential losses, or we may incur costs due to the financial condition of our insurance carriers.

•We may change business policies without stockholder approval.

•Failure to maintain effective internal control over financial reporting could have a material adverse effect on our business.

•If we failed to qualify as a REIT, we would be taxed at corporate rates and would not be able to take certain deductions when computing our taxable income.

•We may not be able to raise sufficient capital to fund our operations due to adverse changes in our credit ratings, our inability to refinance our existing debt or issue new debt, or our inability to sell existing properties quickly.

•We may invest or spend the net proceeds from our equity or debt offerings in ways with which our investors may not agree and in ways that may not earn a profit.

•Our debt service obligations may restrict our ability to engage in some business activities or cause other adverse effects on our business.

•We face risks and liabilities associated with our investments (including those in connection with short-term liquid investments) and the companies in which we invest (including properties owned through partnerships, limited liability companies, and joint ventures, as well as through our non-real estate venture investment portfolio), which expose us to risks similar to those of our tenant base and additional risks inherent in venture capital investing. We may be limited in our ability to diversify our investments.

Risks related to market and industry factors

•There are limits on ownership of our stock under which a stockholder may lose beneficial ownership of its shares, as well as certain provisions of our charter and bylaws that may delay or prevent transactions that otherwise may be desirable to our stockholders.

•Possible future sales of shares of our common stock could adversely affect its market price.

•We are dependent on the health of the life science, technology, and agtech industries, and changes within these industries, increased competition, or the inability of our tenants and non-real estate equity investments within these industries to obtain funding for research, development, and other operations may adversely impact their ability to make rental payments to us or adversely impact their value.

•Market disruption and volatility, poor economic conditions in the capital markets and global economy, including in connection with the COVID-19 pandemic, and high unemployment levels could adversely affect the value of the companies in which we hold equity investments or the ability of tenants and the companies in which we invest to raise additional capital or access capital from venture capital investors or financial institutions on favorable terms.

Risks related to government and global factors

•Actions, policy, or key leadership changes in government agencies, or changes to laws or regulations, including those related to tax, accounting, debt, derivatives, government spending, or funding (including those related to the FDA, the National Institutes of Health (the “NIH”), the SEC, and other agencies), and drug and healthcare pricing, costs, and programs could have a significant negative impact on the overall economy, our tenants, and our business.