UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(X) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the Fiscal Year Ended September 30, 2011

OR

( ) TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the transition period from N/A to N/A

Commission File Number: 000-28745

Cloud Medical Doctor Software Corporation

(Name of small business issuer as specified in its charter)

(Formerly National Scientific Corporation)

| Texas | 86-0837077 | |

| State of Incorporation | IRS Employer Identification No. |

1291 Galleria Drive, Suite 200

Henderson, NV 89014

(Address of principal executive offices)

(Former Address 8361 East Evans Road, Suite 106, Scottsdale, AZ 85260-3617)

(702) 818-9011

(Issuer’s telephone number)

(Former telephone number (480) 948-8324)

Securities registered under Section 12(b) of the Exchange Act:

None

Securities registered under Section 12(g) of the Exchange Act:

Common Stock, $0.001 par value per share

(Title of Class)

Common Stock, $.001 Par Value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[ ] Yes [x] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

[x] Yes [ ] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ ] No [x]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [ ] No [x]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,”“accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non–Accelerated filer | [ ] | Small reporting company | [x] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b–2 of the Exchange Act). Yes [ ] No [x]

Aggregate market value of the voting stock held by non-affiliates: $5,087,389 as based on the closing price of the stock on September 26, 2013. The voting stock held by non-affiliates on that date consisted of 169,579,649 shares of common stock.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. As of September 25, 2013, there were 214,634,216 shares of common stock, par value $0.01, issued and outstanding 4,000,000 shares of preferred stock, par value $0.10.

Documents Incorporated by Reference: None

THE COMPANY PREVIOUSLY HAD INSUFFICIENT WORKING CAPITAL TO PAY FOR THE PROFESSIONAL SERVICES REQUIRED TO PREPARE, AUDIT, AND FILE THE QUARTERLY AND ANNUAL REPORTS REQUIRED BY THE SECURITIES ACT OF 1934. AS A RESULT, THE AUDITORS WHO AUDITED THE SEPTEMBER 30, 2007 FINANCIAL STATEMENTS AND REVIEWED THE QUARTERLY REPORTS THROUGH JUNE 30, 2008 RESIGNED EFFECTIVE DECEMBER 13, 2011.

IN FEBRUARY 2010 THE BOARD OF DIRECTORS VOTED TO DISCONTINUE THE MOBILE DVR AND LOCATION PRODUCTS LINE OF BUSINESS REPORTED IN THESE FINANCIAL STATEMENTS DUE TO THE CUMULATIVE EFFECTS OF SEVERELY DECLINING REVENUES RESULTING FROM THE 2008 RECESSION. SINCE THIS DECISION WAS MADE SUBSEQUENT TO THE YEARS ENDED SEPTEMBER 30, 2008 AND 2009, THE QUARTERLY AND YEAR END STATEMENTS FOR THOSE YEARS ARE BEING REPORTED ON A GOING CONCERN BASIS RATHER THAN AS DISCONTINUED OPERATIONS. THEY WILL, HOWEVER, BE REPORTED AS DISCONTINUED OPERATIONS COMMENCING WITH THE FISCAL 2010 FILINGS.

NEW MANAGEMENT HAS SUBSEQUENTLY INFUSED SUFFICIENT WORKING CAPITAL TO BRING THE 1934 ACT FILINGS CURRENT. ADDITIONALLY, A NEW LINE OF BUSINESS HAS ALSO COMMENCED WHICH WILL BE REPORTED ON IN THE FISCAL 2011 AND 2012 FILINGS.

ACCORDINGLY, THIS FILING IS BEING SUBMITTED ONLY TO COMPLY WITH SEC RULES AND REGULATIONS AND SHOULD NOT BE RELIED UPON FOR YOUR INVESTMENT DECISIONS. THE OPERATIONS REPORTED ON IN THIS DOCUMENT HAVE BEEN DISCONTINUED AS OF FEBRUARY 4, 2010. NEW MANAGEMENT ENCOURAGES THE READERS OF THIS DOCUMENT TO SUSPEND ANY INVESTMENT DECISIONS PERTAINING TO THIS STOCK UNTIL THE FILINGS ARE BROUGHT CURRENT.

Cloud Medical Doctor Software Corporation

FORM 10-K ANNUAL REPORT

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2011 and 2010

| PART I | ||||

| ITEM 1. | BUSINESS | 2 | ||

| ITEM 1A. | RISK FACTORS | 7 | ||

| ITEM 1B. | UNRESOLVED STAFF COMMENTS | 12 | ||

| ITEM 2. | PROPERTIES | 12 | ||

| ITEM 3. | LEGAL PROCEEDINGS | 12 | ||

| ITEM 4. | REMOVED AND RESERVED | 13 | ||

| PART II | ||||

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 14 | ||

| ITEM 6. | SELECTED FINANCIAL DATA | 17 | ||

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 17 | ||

| ITEM 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 19 | ||

| ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | F-1 | ||

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 20 | ||

| ITEM 9A. | CONTROLS AND PROCEDURES | 21 | ||

| ITEM 9B. | OTHER INFORMATION | 22 | ||

| PART III | ||||

| ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS, AND CORPORATE GOVERNANCE | 23 | ||

| ITEM 11. | EXECUTIVE COMPENSATION | 25 | ||

| ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 29 | ||

| ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 31 | ||

| ITEM 14. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 32 | ||

| PART IV | ||||

| ITEM 15. | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 33 | ||

| SIGNATURES | 34 | |||

CERTIFICATIONS

Exhibit 31.1 – Management certification

Exhibit 31.2 – Management certification

Exhibit 32.1 – Sarbanes-Oxley Act

Exhibit 32.2 – Sarbanes-Oxley Act

Special Note Regarding Forward-Looking Statements

Some of our statements under "Business," "Properties," "Legal Proceedings," "Management's Discussion and Analysis of Financial Condition and Results of Operations,"" the Notes to Financial Statements and elsewhere in this report constitute "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements are subject to certain events, risks and uncertainties that may be outside our control. Some of these forward-looking statements include statements of:

| · | management's plans, objectives and budgets for its future operations and future economic performance; | |

| · | capital budget and future capital requirements; | |

| · | meeting future capital needs; | |

| · | realization of any deferred tax assets; | |

| · | the level of future expenditures; | |

| · | impact of recent accounting pronouncements; | |

| · | the outcome of regulatory and litigation matters; | |

| · | the assumptions described in this report underlying such forward-looking statements; and | |

| · | Actual results and developments may materially differ from those expressed in or implied by such statements due to a number of factors, including: |

| o | those described in the context of such forward-looking statements; | |

| o | future service costs; | |

| o | changes in our incentive plans; | |

| o | the markets of our domestic operations; | |

| o | the impact of competitive products and pricing; | |

| o | the political, social and economic climate in which we conduct operations; and | |

| o | the risk factors described in other documents and reports filed with the Securities and Exchange Commission. |

In some cases, forward-looking statements are identified by terminology such as "may," "will," "should," "could," "would," "expects," "plans," "intends," "anticipates," "believes," "estimates," "approximates," "predicts," "potential" or "continue" or the negative of such terms and other comparable terminology.

Although we believe that the expectations reflected in these forward-looking statements are reasonable, it cannot guarantee future results, levels of activity, performance or achievements. Moreover, neither we nor anyone else assumes responsibility for the accuracy and completeness of such statements and is under no duty to update any of the forward-looking statements after the date of this report.

PART I

ITEM 1. BUSINESS.

General

The financial statements presented in this report of Cloud Medical Doctor Software Corporation, a Texas corporation. When the terms “Cloud, the Company,” “we,” “us” or “our” are used in this document, those terms refer to Cloud Medical Doctor Software Corporation.

Our Company

The Company was incorporated in Texas on June 22, 1953 as American Mortgage Company. On May 16, 1996, the Company changed its name to National Scientific Corporation. On April 3, 2012, the Company changed its name to Cloud Medical Doctor Software Corporation. During 1996, the Company acquired the operations of Eden Systems, Inc. (Eden) as a wholly owned subsidiary. Eden was engaged in water treatment and the retailing of cleaning products. Eden’s operations were sold on October 1, 1997. From September 30, 1997 through the year ended September 30, 2001, we aimed our efforts in the research and development of semiconductor proprietary technology and processes and in raising capital to fund its operations and research.

Beginning in calendar 2002, we focused our efforts on the development, acquisition, enhancement and marketing of location device technologies. Our revenue is derived from sales of electronic devices, recognized as the product is delivered.

In February 4, 2010 the prior Board members Mr. Michael Grollman and Mr. Greg Szabo, decided to discontinue and wind down the operation of the Company's Mobile DVR and Location Products business and operate these remaining Company assets in a Limited Liability Company named NSC Labs, LLC controlled and owned by Mr. Grollman. Mr. Grollman and NSC Labs, LLC was to pay the Company 2% of revenues and $100,000. However, Mr. Grollman nor NSC Labs, LLC never paid consideration for this transaction.

In November 19, 2010, the prior management was terminated and new management began working on operations related to the Company’s medical billing software. In fiscal 2011, the year of termination of prior management, new management has deemed that the above transaction transferring prior operations to NSC Labs, LLC was transacted in full and final settlement of the liabilities to former management including those captioned as “disputed accrued expenses – related party” on the Balance Sheet. Since the transaction was related to former management who had the ability to affect the terms and outcomes of the liabilities, the transaction has been subsequently recorded as an increase to additional paid in capital.

Our Current Business of the Company – Cloud Doctor Medical Software

In 2011 Cloud-MD Software Solutions introduced the Cloud-MD Office, a “Cloud Based”, 5010 and ICD-10 compliant, fully integrated and interoperable suite of medical software and services, designed by experienced healthcare analysts and programmers for healthcare providers, that produces “Actionable Information” to help Independent Physician Practices, New Care Delivery Models (ACO), Healthcare Systems and Billing Services optimize a wide range of business processes resulting in Increased Profits, Higher Quality, Greater Efficiency, Noticeable Cost Reductions and Better Patient Care. Current software product offerings include Practice Management, Electronic Medical Records, Revenue Management, Patient Financial Solutions, Medical and Pharmaceutical Supply Management, Claims Management and PHI Exchange.

Cloud-MD Billing Services provides: Management of Medical Claims from posting physician charges into our medical billing software to posting of payments; Continuous Insurance Claim Follow Up to track and research all rejected or denied medical claims; Comprehensive Reporting including monthly financial Statements sent to our clients so they can see how their practice is doing and a variety of detailed reports give our clients the important information and tools used to assist in the increased production which leads to more profit; Patient Account Inquiries & Support to assist patients with their billing and insurance questions.

Cloud-MD Medical and Pharmaceutical Supply Management Software Services provides: a ground breaking cloud-based Medical Supply Inventory Management System, specifically designed for small and medium Medical Practices, DME’s, Home Health, Long-term Care, and Surgery Centers that offers:

Centralized management control over your medical supply and drug inventory

Real time utilization and financial inventory summary

Low price notifications

Par level/reorder tracking

RX expiration tracking

Auto supply re-ordering

Based on a barcode scanning system, designed to reduce workloads by automating inventory control processes, the Cloud-MD® Inventory Management System requires no installation, on-site software or special hardware. The Cloud-MD® application suite is fully delivered via the Internet and requires no special computing environment at the end-user facility.

Cloud-MD Healthcare Systems Consulting Services specializes in the implementation of sustainable, comprehensive solutions that increase financial and operational performance in healthcare businesses. By partnering with clients, we deliver solutions across the healthcare enterprise that improve quality, increase revenue, reduce operational expenses and attract physicians, patients and employees. We bring resources, in-depth knowledge, and significantly deeper experience than most in the field.

Cloud-MD Acquisition Services provides medical supply acquisition services that are fully integrated with Cloud-MD Office’s Medical and Pharmaceutical Inventory Management software and offers a full range of medical, surgical, and laboratory supply products and equipment for medical offices and surgery centers. Cloud-MD Acquisition Services easy-to-use and seamless process makes supply purchasing quicker and more cost efficient.

Item 1. Description of Business

Discontinued Operations of the Business up through February 4, 2010

Mobile DVR and Location Products

Most of our customers require monitoring and or tracking of a person or object, and reporting this information back to a central location.

Our current MDVR technology has not been awarded any patents as of the date of this report and has been awarded trademark protection on one other. We use a combination of confidentiality agreements, copyright and other trade secret management techniques to protect our trade secrets.

Location Products

Overview of This Technology

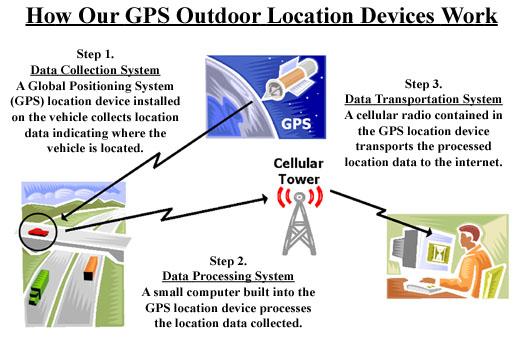

We have developed a group of mobile products with the capability to record high quality digital video, determine location and identify individuals and concatenate this information into a homogeneous information stream that can be easily displayed on a remote computer. We use a technology called Global Positioning System or GPS to determine location. These products report the location information as well as other desired information back to the user through a radio network. The products typically contain a small computer to provide the overall control and data processing capacity for the device. The products can be thought of as having three distinct pieces or systems. These are the data collection system, the data control & processing system, and the data transport system. This design concept is the basis for our Mobile DVR products. The diagram below shows in a general way how the system works with our products:

Data Collection System

This system can be thought of as the “eyes and ears” of the product. It is comprised of two systems. One determines location of the product, while the other system records specific events that the customer may be interested in, such as a door opening on a school bus or the speed of the bus at a certain location. The location system determines the position of the product using a technology developed by the U.S. Government called the Global Positioning System, or GPS, as it is commonly known. The U.S. Government developed the system which consists of approximately 24 satellites that orbit the earth rapidly. It is a worldwide navigation support system that allows users of GPS receivers to determine their precise geographic locations to within a few meters in most cases. The network of satellites and their ground control and monitoring stations are maintained and operated by the United States Department of Defense, which maintains an ongoing satellite replenishment program to ensure continuous global system coverage. Access to the system for all users is currently provided free of charge by the U.S. Government.

GPS works by ranging and triangulating the product’s position from a group of satellites. Of the 24 GPS satellites in orbit, a minimum of four is needed to reliably determine the product’s three-dimensional position. A GPS receiver measures distance by calculating the amount of time it takes a navigation and time reference radio signal from the satellite to make a one-way trip to the GPS receiver.

GPS receivers typically are very compact; and it is not necessary to have a large dish antenna to receive GPS signals. Typical information that can be obtained from these GPS signals are latitude, longitude, elevation, speed, direction, date, and time.

The second part of this Data Collection System is customer specific. Many customers have additional types of data that they want to know or want collected relevant to a location. An example of this is, every time a child enters or leaves a school bus or the time and location that the bus stops. This data input system can therefore be customized to meet the exact needs of a customer.

Another kind of data collection technology we use in some of our products is called RFID, which stands for Radio Frequency Identification. RFID devices are small radios that could be used to track information about people or objects. RFID provides a low-cost solution for certain kinds of tracking activities, especially short-range activities, typically less than a hundred feet. RFID devices are primarily used to determine if the object is close to a given location.

Another kind of data collection technology we use in some of our products is called MDVR, which stands for mobile digital video recorder. MDVR devices use a small digital camera that takes up to 30 pictures per second and then stores these images electronically. When these individual pictures are ‘played back’, you see a movie of the recorded event. Schools are particularly interested in this type of technology in conjunction with GPS to monitor what is happening on their buses.

Data Control & Processing System

This system can be thought of as the “brains” of the product. A technical term for this system is an embedded system, meaning one that lives deep inside the overall product. An embedded system is a small special-purpose computer system built into a larger device. The reason we use an embedded system in our products is to keep cost to us low, so our products stay more competitive in price. Simple embedded systems can cost us as little as a few dollars each and use very little power compared to the desktop computers that many people are familiar with, which usually cost much more. On our embedded systems there is typically no disk drive, operating system, keyboard, or screen. Our embedded systems instead communicate with other computers by radio. These other computers typically have a keyboard and screens, and they are used to display our information.

The programs that we run on these systems are custom designed and built by our software engineers. These programs are called firmware. The firmware controls how the data is collected, what data should be collected and what events should be monitored and reported, what should be ignored, and how, when and what data should be sent back to the user. As mentioned above, the system is relatively easy to customize, and the firmware is also easy to customize as it has been written in a modular fashion that allows changes to one section to be implemented without the need to completely re-write the program. This also helps us keep costs down.

Data Transport System

This system can be thought of as the “mouth” of the product. It communicates to the outside world where it is and what has happened. There are many different types of technology that can be used to transport this data back to the user, generally using some kind of wireless technology based on radios. We currently use cellular radios, satellite radios, Wi-Fi radios, and other special purpose radios.

We use a cellular radio based on GSM cellular technology. GSM, or Global System for Mobile Communications, is a second-generation digital mobile telephone standard. GSM was initially developed as pan-European collaboration, intended to enable mobile roaming between member countries.

The cellular radios typically operate in “real time.” When an event occurs, the data is immediately transported back to a user at a remote location.

While cellular coverage and reception is good in urban areas, it is less effective in rural areas and is non-existent in most wilderness areas. Sometimes our products are used in areas where there is poor or no cellular coverage. To overcome this we sometimes use a special radio that communicates with satellites orbiting the earth. This form of communication has the advantage that our products can be used in very remote areas almost anywhere in the world. The major downside is that these radios are large and expensive and the airtime usage costs can be high. Another problem associated with this technology is that, like GPS, these satellite radios work best when there is a clear line of site to the satellites; as such they may not work well indoors, or under dense foliage or in deep valleys. The satellite radios typically operate in “real time.” When an event occurs, the data is immediately transported back to the user. Some of our customers do not want to have the expense of a real time cellular or satellite connection, nor are they interested in having the data in real time. For this we use either a special purpose radio or a Wi-Fi radio.

The Wi-Fi radio operates in a very similar manner to cordless phones found in many households. These phones typically consist of a base station and handset. Our system is very similar; it consists of a base station unit that receives data from the mobile unit that would be on the asset or vehicle being tracked. The base station is typically attached to a personal computer that takes the raw data from the radio and re-formats it into information that can be displayed by other computers on the Internet. Wi-Fi stands for “Wireless Fidelity” and is a technology in very common use to wirelessly connect personal computers to other computer networks, including the Internet.

Our special purpose radios work in a very similar manner to the Wi-Fi radio, except that they can sometimes transmit data over longer distances.

Wi-Fi radios operate in an unlicensed part of the radio spectrum and as such do not have any special government licensing fees associated with them. Because they operate in a license-free spectrum, the Federal Communications Commission (FCC) imposes some restrictions on the use of these radios. One major restriction is that the radio signal range is limited to about 300 feet.

Since most of the time our product operates well beyond 300 feet from the base station, all the collected data is stored within the device for later transmission when the product comes back into that range again. When the vehicle or asset comes back into base-station range, the mobile units automatically download their information. We call this mode of operation “near time.” These “near time” products do not incur any special airtime usage charges. As such, they can be significantly cheaper to operate than the cellular or satellite equivalents.

Once the data is transmitted back to the user they can either display the information on our software or on some other computer application.

Personnel

As of the date of this report, we have twenty full time employees.

WHERE YOU CAN FIND MORE INFORMATION

You are advised to read this Form 10-K in conjunction with other reports and documents that we file from time to time with the SEC. In particular, please read our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K that we file from time to time. You may obtain copies of these reports directly from us or from the SEC at the SEC’s Public Reference Room at 100 F. Street, N.E. Washington, D.C. 20549, and you may obtain information about obtaining access to the Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains information for electronic filers at its website http://www.sec.gov.

In an effort to keep our stockholders and the public informed about our business, we may make “forward-looking statements.” Forward-looking statements usually relate to future events and anticipated revenues, earnings, cash flows or other aspects of our operations or operating results. As indicated previously, forward-looking statements are often identified by words, “will”, “may”, “should”, “continue”, “anticipate”, “believe”, “expect”, “plan”, “forecast”, “project”, “estimate”, “intend” and words of similar nature. Forward-looking statements generally include statements containing:

| • | projections about accounting and finances; | |

| • | plans and objectives for the future; | |

| • | projections or estimates about assumptions relating to our performance; or | |

| • | our opinions, views or beliefs about the effects of current or future events, circumstances or performance. |

You should view those statements with caution. Those statements are not guarantees of future performance, circumstances or events. They are based on facts and circumstances known to us as of the date the statements are made. All phases of our business are subject to uncertainties, risks and other influences, many of which we do not control. Any of these factors either alone or taken together, could have a material adverse effect on us and could change whether any forward-looking statement ultimately turns out to be true. Additionally, we assume no obligation to update any forward-looking statement as a result of future events, circumstances or developments.

Outlined below are some of the risks that we believe could affect our business and financial statements for 2011 and beyond. An investment in our common stock involves a high degree of risk. You should carefully consider the following information about these risks, together with the other information contained in this Annual Report on Form 10-K, before investing in our common stock. If any of the events anticipated by the risks described below occur, our results of operations and financial condition could be adversely affected which could result in a decline in the market price of our common stock, causing you to lose all or part of your investment.

The Report Of Our Independent Registered Public Accounting Firm Contains Explanatory Language That Substantial Doubt Exists About Our Ability To Continue As A Going Concern

The independent auditor’s report on our financial statements contains explanatory language that substantial doubt exists about our ability to continue as a going concern. We have a net loss for the year ended September 30, 2011of $356,629, an accumulated deficit at September 30, 2011 of $26,229,970, cash flows used in of $220,628 and need additional cash flows to maintain our operations. We depend on the continued contributions of our executive officers to finance our operations and need to obtain additional funding sources to explore potential strategic relationships and to provide capital and other resources for the further development and marketing of our products and business. If we are unable to obtain sufficient financing in the near term or achieve profitability, then we would, in all likelihood, experience severe liquidity problems and may have to curtail or cease our operations altogether. If we curtail our operations or cease our operations, we may be placed into bankruptcy or undergo liquidation, the result of which will adversely affect the value of our common shares.

Because We Are Quoted On The OTCBB “OTC Markets “formerly known as “Pinks Sheets” Instead Of An Exchange Or National Quotation System, Our Investors May Have A Tougher Time Selling Their Stock Or Experience Negative Volatility On The Market Price Of Our Stock.

Our common stock is traded on the OTCBB “OTC Markets”. The OTCBB “OTC Markets” is often highly illiquid, in part because it does not have a national quotation system by which potential investors can follow the market price of shares except through information received and generated by a limited number of broker-dealers that make markets in particular stocks. There is a greater chance of volatility for securities that trade on the OTCBB “OTC Markets” as compared to a national exchange or quotation system. This volatility may be caused by a variety of factors, including the lack of readily available price quotations, the absence of consistent administrative supervision of bid and ask quotations, lower trading volume, and market conditions. Investors in our common stock may experience high fluctuations in the market price and volume of the trading market for our securities. These fluctuations, when they occur, have a negative effect on the market price for our securities. Accordingly, our stockholders may not be able to realize a fair price from their shares when they determine to sell them or may have to hold them for a substantial period of time until the market for our common stock improves.

We depend significantly upon the continued involvement of our present management.

The Company’s success depends significantly upon the involvement of our present management, who is in charge of our strategic planning and operations. We may need to attract and retain additional talented individuals in order to carry out our business objectives. The competition for individuals with expertise in this industry could be intense and there are no assurances that these individuals will be available to us.

Our Common Stock Is Subject To Penny Stock Regulation

Our shares are subject to the provisions of Section 15(g) and Rule 15g-9 of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), commonly referred to as the "penny stock" rule. Section 15(g) sets forth certain requirements for transactions in penny stocks and Rule 15g-9(d)(1) incorporates the definition of penny stock as that used in Rule 3a51-1 of the Exchange Act. The Commission generally defines penny stock to be any equity security that has a market price less than $5.00 per share, subject to certain exceptions. Rule 3a51-1 provides that any equity security is considered to be penny stock unless that security is: registered and traded on a national securities exchange meeting specified criteria set by the Commission; authorized for quotation on the NASDAQ Stock Market; issued by a registered investment company; excluded from the definition on the basis of price (at least $5.00 per share) or the registrant's net tangible assets; or exempted from the definition by the Commission. Since our shares are deemed to be "penny stock", trading in the shares will be subject to additional sales practice requirements on broker/dealers who sell penny stock to persons other than established customers and accredited investors.

Compliance with changing regulation of corporate governance and public disclosure will result in additional expenses and pose challenges for our management.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including the Dodd-Frank Wall Street Reform and Consumer Protection Act and the rules and regulations promulgated there under, the Sarbanes-Oxley Act and SEC regulations, have created uncertainty for public companies and significantly increased the costs and risks associated with accessing the U.S. public markets. Our management team will need to devote significant time and financial resources to comply with both existing and evolving standards for public companies, which will lead to increased general and administrative expenses and a diversion of management time and attention from revenue generating activities to compliance activities.

We rely heavily on international third parties to manufacture subsystems of our available on acceptable terms, if at all. If such financing is not available on satisfactory terms, we may be unable to continue, products.

We currently rely on international third-party contractors to manufacture key sub assemblies to satisfy the needs of such customers. Reliance on one or more international third-party manufacturers exposes us to the risk that delivery schedules cannot be met, and that we cannot fulfill orders for some of our products in a timely way at the right price in U.S. dollars. This risk includes the concern that:

| • | Third-party manufacturers might be unable to manufacture our products in the volume and of the quality required to meet customers’ needs; | |

| • | Our existing and future contract manufacturers may not perform as agreed or may not remain in the contract manufacturing business for the time required to supply our customers; | |

| • | If any third-party manufacturer makes improvements in the manufacturing process for our products, we may not own, or may have to share, the intellectual property rights to the innovation. |

Each of these conditions could delay the shipments to our customers, approvals required by regulatory authorities, and the commercialization of some of our customers’ products. These risks could also result in higher costs to the customer or could deprive us of potential product revenues.

Risks Relating To Our Industry

There are substantial inherent risks in attempting to commercialize new technological applications, and, as a result, we may not be able to successfully develop products or technology for commercial use.

Our company conducts ongoing development on our medical billing software. Our product development team is working on developing technology and products in various stages. Software development requires significant amounts of capital and takes an extremely long time to reach commercial viability, if at all. During the development of our software, we may experience technological barriers that we may be unable to overcome. Because of these uncertainties, it is possible that none of our product candidates will be successfully developed.

Risks Related to our Securities

The market price for our common stock may be volatile, and you may not be able to sell our stock at a favorable price or at all.

Many factors could cause the market price of our common stock to rise and fall, including:

| • | actual or anticipated variations in our quarterly results of operations; | |

| • | changes in market valuations of companies in our industry; | |

| • | changes in expectations of future financial performance; | |

| • | fluctuations in stock market prices and volumes; | |

| • | issuances of dilutive common stock or other securities in the future; | |

| • | the addition or departure of key personnel; | |

| • | announcements by us or our competitors of acquisitions, investments or strategic alliances; and | |

| • | it is possible that the proceeds from sales of our common stock may not equal or exceed the prices you paid for the shares after including the costs and fees of making the sales |

Substantial sales of our common stock, or the perception that such sales might occur, could depress the market price of our common stock.

We cannot predict whether future issuances of our common stock or resale in the open market will decrease the market price of our common stock. The consequence of any such issuances or resale of our common stock on our market price may be increased as a result of the fact that our common stock is thinly, or infrequently, traded. The exercise of any options, or the vesting of any restricted stock that we may grant to directors, executive officers and other employees in the future, the issuance of common stock in connection with acquisitions and other issuances of our common stock may decrease the market price of our common stock.

Holders of our common stock have a risk of potential dilution if we issue additional shares of common stock in the future.

Although our Board of Directors intends to utilize its reasonable business judgment to fulfill its fiduciary obligations to our then existing stockholders in connection with any future issuance of our common stock, the future issuance of additional shares of our common stock would cause immediate, and potentially substantial, dilution to the net tangible book value of those shares of common stock that are issued and outstanding immediately prior to such transaction. Any future decrease in the net tangible book value of our issued and outstanding shares could have a material adverse effect on the market value of our shares.

We do not intend to pay cash dividends to our stockholders, so you will not receive any return on your investment in our Company prior to selling your interest in the Company.

The Company has never paid any cash dividends to our stockholders. We currently intend to retain any future earnings for funding growth and, therefore, do not expect to pay any cash dividends in the foreseeable future. As a result, you will not receive any return on your investment prior to selling your shares in our Company and, for the other reasons discussed in this “Risk Factors” section, you may not receive any return on your investment even when you sell your shares in our Company.

Certain shares of our common stock are restricted from immediate resale. The lapse of those restrictions, coupled with the sale of the related shares in the market, or the market’s expectation of such sales, could result in an immediate and substantial decline in the market price of our common stock.

Most of our shares of common stock are restricted from immediate resale in the public market. The restricted shares are restricted in accordance with Rule 144, which states that if unregistered, restricted securities are to be sold, a minimum of one year must elapse between the later of the date of acquisition of the securities from the issuer or from an affiliate of the issuer, and any resale of those securities in reliance on Rule 144. The Rule 144 restrictive legend remains on the stock until the holder of the stock holds the stock for longer than six months (unless an affiliate) and meets the other requirements of Rule 144 to have the restriction removed. The sale or resale of those shares in the public market, or the market’s expectation of such sales, may result in an immediate and substantial decline in the market price of our shares. Such a decline will adversely affect our investors, and make it more difficult for us to raise additional funds through equity offerings in the future.

Our common stock is subject to restrictions on sales by broker-dealers and penny stock rules, which may be detrimental to investors.

Our common stock is subject to Rules 15g-1 through 15g-9 under the Exchange Act, which imposes certain sales practice requirements on broker-dealers who sell our common stock to persons other than established customers and “accredited investors” (as defined in Rule 501(a) of the Securities Act). For transactions covered by this rule, a broker-dealer must make a special suitability determination for the purchaser and have received the purchaser’s written consent to the transaction prior to the sale. This rule adversely affects the ability of broker-dealers to sell our common stock and purchasers of our common stock to sell their shares of our common stock.

Additionally, our common stock is subject to SEC regulations applicable to “penny stocks.” Penny stocks include any non-Nasdaq equity security that has a market price of less than $5.00 per share, subject to certain exceptions. The regulations require that prior to any non-exempt buy/sell transaction in a penny stock; a disclosure schedule proscribed by the SEC relating to the penny stock market must be delivered by a broker-dealer to the purchaser of such penny stock. This disclosure must include the amount of commissions payable to both the broker-dealer and the registered representative and current price quotations for our common stock. The regulations also require that monthly statements be sent to holders of a penny stock that disclose recent price information for the penny stock and information of the limited market for penny stocks. These requirements adversely affect the market liquidity of our common stock.

Our Articles of Incorporation allow us to sell preferred stock without shareholder approval.

Our Board of Directors has the authority to issue up to 4,000,000 shares of preferred stock and to determine the price, rights, preferences, privileges and restrictions, including voting rights, of those shares without any additional vote or action by our shareholders. The rights of the holders of the common stock will be subject to, and could be materially adversely affected by, the rights of the holders of any preferred stock that may be issued in the future. For example we could issue preferred stock that has superior rights to dividends or is convertible into shares of common stock. This might adversely affect the market price of the common stock.

If we experience delays and/or defaults in customer payments, we could be unable to recover all expenditures.

Because of the nature of our contracts, at times we commit resources to projects prior to receiving payments from the customer in amounts sufficient to cover expenditures on projects as they are incurred. Delays in customer payments may require us to make a working capital investment. If a customer defaults in making their payments on a project in which we have devoted resources, it could have a material negative effect on our results of operations.

If we do not effectively manage our growth, our existing infrastructure may become strained, and we may be unable to increase revenue growth.

Our past growth that we have experienced, and in the future may experience, may provide challenges to our organization, requiring us to expand our personnel and our operations. Future growth may strain our infrastructure, operations and other managerial and operating resources. If our business resources become strained, our earnings may be adversely affected and we may be unable to increase revenue growth. Further, we may undertake contractual commitments that exceed our labor resources, which could also adversely affect our earnings and our ability to increase revenue growth.

SHOULD ONE OR MORE OF THE FOREGOING RISKS OR UNCERTAINTIES MATERIALIZE, OR SHOULD THE UNDERLYING ASSUMPTIONS PROVE INCORRECT, ACTUAL RESULTS MAY DIFFER SIGNIFICANTLY FROM THOSE ANTICIPATED, BELIEVED, ESTIMATED, EXPECTED, INTENDED OR PLANNED

ITEM 1B. UNRESOLVED STAFF COMMENTS

This Item is not applicable to us as we are not an accelerated filer, a large accelerated filer, or a well-seasoned issuer.

ITEM 2. PROPERTIES

During December 31, 2010 the Company uses the Chief Financial Officers office as the Corporation’s office at no cost to the Company.

Since January 2012, the Company uses the office at 1291 Galleria Drive, Suite 200, Henderson, NV 89014. The office is at no cost to the Company.

ITEM 3. LEGAL PROCEEDINGS

We are currently not involved in any litigation that we believe could have a material adverse effect on our financial condition or results of operations. There is no action, suit, proceeding, inquiry or investigation before or by any court, public board, government agency, self-regulatory organization or body pending or, to the knowledge of the executive officers of our company or any of our subsidiaries, threatened against or affecting our company, our common stock, any of our subsidiaries or of our company’s or our company’s subsidiaries’ officers or directors in their capacities as such, in which an adverse decision could have a material adverse effect.

On July 5, 2013 the Company filed a complaint for the collection of $150,000 of unpaid medical billing fees that were seriously delinquent. After many attempts by the Company to begin collections, the Defendants refused to pay the outstanding balances, however expected the Company to continue to bill for them. The Company’s complaint was filed against Krooss Medical Management Systems, LLC, William F. Krooss and Marie W. Krooss in the United States District Court, District of Nevada Case No. 2013-CV-01187-ABG-VCF.

On August 13, 2013 Krooss Medical Management Systems et al filed a Complaint in Chancery Court of Rankin County, Mississippi Case No. 13-1372 as a strategy to keep the collection matter in Mississippi Chancery Court.

Case No. 13-1372 was remanded to the United States District Court, Southern District of Mississippi Jackson Division Case No. 3:13CV507-HTW-LRA.

This litigation is a collection matter of unpaid fees by the Defendants and the Company vehemently denies the allegations filed in Mississippi Chancery Court related to this collection matter. The Company does not expect the cost to litigate this matter to adversely affect the Company’s operations.

ITEM 4. N/A

PART II

ITEM 5. MARKET FOR REGISTANT’S COMMON STOCK, RELATED STOCKHOLDER MATTERS AND ISSUERS PURCHASES OF EQUITY SECURITIES.

Cloud common stock is traded in the over-the-counter market, and quoted in the National Association of Securities Dealers Inter-dealer Quotation System (“Electronic Bulletin Board) and can be accessed on the Internet at OTCmarkets.com under the symbol “NSCT.”

At September 30, 2011, there were 180,526,879 shares of common stock of Cloud outstanding and there were in excess of 8,000 shareholders of record of the Company’s common stock.

The following table sets forth for the periods indicated the high and low bid quotations for Cloud’s common stock. These quotations represent inter-dealer quotations, without adjustment for retail markup, markdown or commission and may not represent actual transactions.

| Periods | High | Low | |||||

| Fiscal Year 2011 | |||||||

| First Quarter (October – December 2010) | $ | 0.01 | $ | 0.01 | |||

| Second Quarter (January – March 2011) | $ | 0.01 | $ | 0.01 | |||

| Third Quarter (April - June 2011) | $ | 0.01 | $ | 0.01 | |||

| Fourth Quarter (July – September 2011) | $ | 0.00 | $ | 0.00 | |||

|

Fiscal Year 2010 |

|||||||

| First Quarter (October – December 2009) | $ | 0.0008 | $ | 0.0008 | |||

| Second Quarter (January – March 2010) | $ | 0.0012 | $ | .0012 | |||

| Third Quarter (April - June 2010) | $ | 0.0008 | $ | 0.0008 | |||

| Fourth Quarter (July – September 2010) | $ | 0.0004 | $ | 0.0004 | |||

On September 25, 2013, the closing bid price of our common stock was $0.03

Dividends

We may never pay any dividends to our shareholders. We did not declare any dividends for the year ended September 30, 2011. Our Board of Directors does not intend to distribute dividends in the near future. The declaration, payment and amount of any future dividends will be made at the discretion of the Board of Directors, and will depend upon, among other things, the results of our operations, cash flows and financial condition, operating and capital requirements, and other factors as the Board of Directors considers relevant. There is no assurance that future dividends will be paid, and if dividends are paid, there is no assurance with respect to the amount of any such dividend.

Transfer Agent

Cloud’s Transfer Agent and Registrar for the common stock is Pacific Stock Transfer located in Las Vegas, Nevada.

Recent sales of Unregistered Securities

2013

In October, 2012 the Company issued 137,500 common shares for $46,000 and issued 10,000 common stock in conjunction with the sale of medical software.

In December 6, 2012 the Company issued 500,000 common shares for the acquisition of CipherSmith software, issued 200,000 common shares for the sale of medical software.

In January 22, 2013 the Company issued 200,000 common shares for the acquisition of CipherSmith software.

In March 21, 2013 the Company issued 270,000 common shares for software investment in the company in accordance with the Software Investment Agreements.

In March 21, 2013 the Company issued 500,000 to Krooss Family Trust LLP for the acquisition of Doctors Network of America in Flowood, Mississippi and all of the assets of that company. Also on April 17, 2013 the Company issued 167,000 for compensation for the salaries for the entire year of 2013 those shares were issued to Krooss Family Trust LLP in accordance with the Agreement. On April 17, 2013 the Company issued 378,500 to Krooss Family Trust LLP in accordance with the Agreement with total shares issued to William and Marie Krooss of 1,045,500 common shares.

April 17, 2013 the Company cancelled the 200,000 common shares issued to for the acquisition and reissued 220,004 common shares for the acquisition of CipherSmith software.

April 17, 2013 the Company issued 95,000 for the software investment in the Company in accordance with the Software Investment Agreements.

May 10, 2013 the Company issued 20,000 common shares for software investment in the company in accordance with the Software Investment Agreements.

June 26, 2013 the Company issued 25,000 common shares for software investment in the company in accordance with the Software Investment Agreements.

August 26, 2013 the Company issued 120,000 common shares to two Software Sales Personal located in California.

Fiscal Year Ended 2012

During the ten months ended July 31, 2012 the Company issued 30,000,000 common shares for there the reduction of debt from our CEO and reduced debt of the company by $3,325,949. The Company also issued 19,000 common shares for services rendered by professionals and recorded the expenses based upon the trading price of the common shares of $0.0102 and expensed $204 as consulting fees. The Company issued 706,333 common shares to third parties that have purchased our medical billing software at the trading price of the common stock of $0.0160 and recorded a revenue contra account of $10,401.

The Company issued 90,000 common shares for $18,000 in cash.

The Company issued 200,000 common shares to Kroos Medical Management in accordance with the acquisition agreement and recorded it at the trading price of the common shares of $0.020 and recorded an investment in Kroos Medical Management of $4,000.

Fiscal Year Ended 2011

In September 30, 2011 the Company issued 15,000,000 common shares at the trading price of the common stock of $0.007. The Stock was issued for compensation to new management and recorded and expense of $105,000.

The Company issued 250,000 in common stock for $25,000 in cash.

Fiscal Year Ended 2010

No common stock was issued.

Common Stock

On April 11, 2011 the Company amended its articles of incorporation to increase the authorized shares to 650,000,000, at $0.01 par value and 180,526,879 are issued and outstanding as of September 30, 2011. The holders of our common stock are entitled to receive such dividends, if any, as may be declared by our board of directors from time to time out of legally available funds. The dividend rights of our common stock are junior to any preferential dividend rights of any outstanding shares of preferred stock. The holders of our common stock also are entitled to receive distributions upon our liquidation, dissolution or winding up of our assets that are legally available for distribution, after payment of all debt and other liabilities and distribution in full of preferential amounts, if any, to be distributed to holders of our preferred stock.

The holders of our common stock are not entitled to preemptive, subscription, redemption or conversion rights. The rights, preferences and privileges of holders of our common stock are subject to, and may be adversely affected by, the rights of any series of preferred stock that we may designate and issue in the future.

Preferred Stock

The Company has authorized 4,000,000 shares of preferred stock, at $.001 par value and 4,000,000 are issued and outstanding as of September 30, 2011. The Corporation established and designates the rights and preferences of a Series A Convertible Preferred Stock, and reserves 4,000,000 shares of preferred stock against its issuance, such rights, preferences and designations. Each share of the Preferred Stock shall have 150 votes on all matters presented to be voted by the holders of our common stock. All 4,000,000 shares of preferred stock that have been granted to our CEO & CFO on November 30, 2010 and issued on April 11, 2012 which was valued at the trading price of the common stock of $0.0095 and recorded as an expense of $38,000.

The issuance of preferred stock by our board of directors could adversely affect the rights of holders of the common stock by, among other things, establishing preferential dividends, liquidation rights or voting powers. See “Risk Factors” above.

Warrants and Options

All warrants issued have expired.

Stock Option Plan

Our board of directors adopted the 2000 Stock Option Plan effective January 1, 2001. Our stockholders formally approved the 2000 Stock Option Plan on February 14, 2001. The 2000 Stock Option plan terminates in accordance with the term on December 1, 2010. The Current Board of Directors has not approved nor extended the Stock Option Plan therefore it is terminated.

ITEM 6. SELECTED FINANCIAL DATA.

The following information has been summarized from financial information included elsewhere and should be read in conjunction with such financial statements and notes thereto.

Summary of Statements of Operations and Financial Position of NSCT

Years Ended September 30, 2011 and 2010

| September 30, | ||||||||

| Operating Data: | 2011 | 2010 | ||||||

| Revenue | — | $ | — | |||||

| Operating and Other Expenses | 340,417 | 21,964 | ||||||

| Discontinued operations | 16,212 | 35,121 | ||||||

| Net Loss | (356,629 | ) | $ | (57,085 | ) | |||

| September 30, | ||||||||

| Balance Sheet Data: | 2011 | 2010 | ||||||

| Current Assets | — | $ | — | |||||

| Total Assets | 11,016 | 2,597 | ||||||

| Current Liabilities | 1,200,106 | 1,788,741 | ||||||

| Non-Current Liabilities | — | — | ||||||

| Total Liabilities | 1,985,790 | 1,788,741 | ||||||

| Working Capital (Deficit) | (1,974,774 | ) | (1,788,741 | ) | ||||

| Shareholders’ Equity | (1,974,774 | ) | $ | (1,786,145 | ) | |||

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following is management’s discussion and analysis of certain significant factors that have affected our financial position and operating results during the periods included in the accompanying financial statements, as well as information relating to the plans of our current management. This report includes forward-looking statements. Undue reliance should not be placed on these forward-looking statements which speak only as of the date hereof. We undertake no obligation to update these forward-looking statements.

The following discussion and analysis should be read in conjunction with our financial statements and the related notes thereto and other financial information contained elsewhere in this Form 10-K.

Business

The Company was incorporated in Texas on June 22, 1953 as American Mortgage Company. On May 16, 1996, the Company changed its name to National Scientific Corporation. On April 3, 2012, the Company changed its name to Cloud Medical Doctor Software Corporation. During 1996, the Company acquired the operations of Eden Systems, Inc. (Eden) as a wholly owned subsidiary. Eden was engaged in water treatment and the retailing of cleaning products. Eden’s operations were sold on October 1, 1997. From September 30, 1997 through the year ended September 30, 2001, we aimed our efforts in the research and development of semiconductor proprietary technology and processes and in raising capital to fund its operations and research. Beginning in calendar 2002, we focused our efforts on the development, acquisition, enhancement and marketing of location device technologies. Our revenue was derived from sales of electronic devices, recognized as the product is delivered.

In February 4, 2010 the prior Board members Mr. Michael Grollman and Mr. Greg Szabo, voted to discontinue and wind down the operations of the Company's Mobile DVR and Location Products business and operate these remaining Company assets in a Limited Liability Company named NSC Labs, LLC, a company controlled and owned by Mr. Grollman. Mr. Grollman and NSC Labs, LLC entered into an agreement to pay the Company $100,000 plus 2% of revenues. Since as of this filing neither Mr. Grollman nor NSC Labs, LLC have paid the specified consideration for this transaction the transaction has not been recorded in the accounting records of the Company.

In November 19, 2010, the prior management was terminated and new management began working on operations related to the Company’s medical billing software. In fiscal 2011, the year of termination of prior management, new management has deemed that the above transaction transferring prior operations to NSC Labs, LLC was transacted in full and final settlement of the liabilities to former management including those captioned as “disputed accrued expenses – related party” on the Balance Sheet Since the transaction was related to former management who had the ability to affect the terms and outcomes of the liabilities, the transaction has been subsequently recorded as an increase to additional paid in capital.

Critical Accounting Policies

Use of Estimates and Assumptions

The preparation of financial statements in conformity with accounting principles generally accepted in the United States (“GAAP”) requires management to make estimates and assumptions that affect (i) the reported amounts of assets and liabilities, (ii) the disclosure of contingent assets and liabilities known to exist as of the date the financial statements are published, and (iii) the reported amount of net revenues and expenses recognized during the periods presented. Adjustments made with respect to the use of estimates often relate to improved information not previously available. Uncertainties with respect to such estimates and assumptions are inherent in the preparation of financial statements; accordingly, actual results could differ from these estimates.

These estimates and assumptions also affect the reported amounts of revenues, costs and expenses during the reporting period. Management evaluates these estimates and assumptions on a regular basis. Actual results could differ from those estimates.

Revenue Recognition

Revenue includes product sales and provision of services. The Company recognizes revenue from product sales and provision of services at the time evidence of an arrangement exists, fees are contractually fixed or determinable, collection is reasonably assured through historical collection results and regular credit evaluations, and there are no uncertainties regarding customer acceptance.

Cash and Cash Equivalents

The Company considers all highly liquid investments with an original maturity of three months or less to be cash equivalents. At September 30, 2011, cash and cash equivalents include cash on hand and cash in the bank and the FDIC insures these deposits up to $250,000.

Share-Based Compensation

The Company measures the cost of services received in exchange for an award of an equity instrument based on the grant-date fair value of the award. Compensation cost is recognized over the vesting or requisite service period. The Black-Scholes option-pricing model is used to estimate the fair value of options or warrants granted.

RESULTS OF OPERATIONS FROM DISCONTINUED MOBILE DVR AND LOCATION PRODUCTS BUSINESS

Fiscal Year Ended September 30, 2011, Compared to Fiscal Year Ended September 30, 2010

General and administrative expenses increased to $21,964 from $0 for the years ended September 30, 2011 and 2010, respectively. Our General and administrative expenses is related to the new medical billing company operations.

We recorded a loss from discontinued operations for the year ended September 30, 2011 of $16,212 of $35,121 for year ended September 30, 2009. The Company is currently engaged in the medical billing operations. Until October 1, 2009, the Company’s sole sources of revenues were from GPS operational device business. The Company discontinued its GPS operational device business in February 2010 (See “Note 3 - Discontinued Operations” to the accompanying Financial Statements). The Company’s GPS operational device business was its primary operations and only sources of revenues for the year ended September 30, 2009.

Liquidity and Capital Resources

The Company has material notes, one from our prior Chief Executive Officer for approximately $59,704, one convertible note with an investor relationship with Strategic Working Capital Fund, LP $175,000 net of discount and beneficial conversion feature of $0.00 with a total balance due of $175,000, and three notes with shareholders of $31,625. As of September 30, 2011 the Company was in default on all notes since the Company has not paid the required quarterly interest payments. In July 2010 our new CEO advanced $159,515.

Our cash (used in) provided by operating activities were ($220,628) and ($31,518) for the years ended September 30, 2011 and 2010, respectively. The decrease in cash flows used in operations was primarily attributable to the changes in operating assets and liabilities, primarily related to increases in amounts payable, in 2011 as compared to the 2010 period.

Cash provided by (used in) financing activities was $229,050 and $21,281 for the years ended September 30, 2011 and 2010, respectively. We received advances from our CEO of $159,515.

There is a strong possibility that we may not be able to satisfy our cash requirements over the next twelve months and may be required to raise additional cash from outside sources.

In the event that we are required to raise additional cash from outside source, we may issue equity securities or incur additional debt. There is no assurance that such funding, if required will be available to us or, if available, will be available upon terms favorable to us.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We do not hold any derivative instruments and do not engage in any hedging activities.

ITEM 8. FINANCIAL STATEMENTS

CLOUD MEDICAL DOCTOR SOFTWARE CORPORATION

| TABLE OF CONTENTS | Page | |

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRMS: | F-2 | |

| FINANCIAL STATEMENTS: | ||

| Balance Sheet at September 30, 2011 and 2010 | F-3 | |

| Statements of Operations for the year ended September 30, 2011 and 2010 | F-4 | |

| Statement of Stockholders’ (Deficit) for the year ended September 30, 2011 and 2010 | F-5 | |

| Statements of Cash Flows for the year ended September 30, 2011 and 2010 | F-6 | |

| NOTES TO FINANCIAL STATEMENTS | F-7 |

S.E.Clark & Company, P.C.

Registered Firm: Public Company Accounting Oversight Board

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors

Cloud Medical Doctor Software Corporation,

fka National Scientific Corporation

Phoenix, Arizona

We have audited the accompanying balance sheets of Cloud Medical Doctor Software Corporation, fka National Scientific Corporation (the “Company”), as of September 30, 2011 and 2010, and the related statements of operations, stockholders’ deficit and cash flows for the years then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Cloud Medical Doctor Software Corporation, fka National Scientific Corporation, as of September 30, 2011 and 2010 and the results of their operations and their cash flows for the years then ended, in conformity with accounting principles generally accepted in the United States of America.

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 3 to the financial statements, the Company has a net loss for the year ended September 30, 2011 of $356,629, an accumulated deficit at September 30, 2011 of $26,229,970, cash flows used by operating activities of $220,628, and needs additional cash flows to maintain its operations. Those conditions raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans in regard to those matters are also described in Note 3. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ S.E.Clark & Company, P.C.

Tucson, Arizona

September 30, 2013

| CLOUD MEDICAL DOCTOR SOFTWARE CORPORATION | ||||||||

| (Formerly National Scientific Corporation) | ||||||||

| BALANCE SHEETS | ||||||||

| September 30, | ||||||||

| 2011 | 2010 | |||||||

| ASSETS | ||||||||

| CURRENT ASSETS: | ||||||||

| Cash | $ | 11,016 | $ | — | ||||

| Net assets of discontinued operations | — | 2,597 | ||||||

| Total current assets | 11,016 | 2,597 | ||||||

| Proprietary technology | 1,200,106 | — | ||||||

| TOTAL ASSETS | $ | 1,211,122 | $ | 2,597 | ||||

| LIABILITIES AND STOCKHOLDERS' DEFICIT | ||||||||

| CURRENT LIABILITIES: | ||||||||

| Advances from officers | $ | 180,795 | $ | 21,281 | ||||

| Line of Credit | 44,535 | — | ||||||

| Net liabilities of discontinued operations | 1,760,459 | 1,767,460 | ||||||

| Total current liabilities | 1,985,790 | 1,788,741 | ||||||

| Note payable affiliate | 1,200,106 | — | ||||||

| TOTAL LIABILITIES | 3,185,896 | 1,788,741 | ||||||

| STOCKHOLDERS' DEFICIT: | ||||||||

| Preferred stock, $.10 par value, 4,000,000 shares authorized; none issued and outstanding as of September 30, 2011 and 2010 | 40,000 | — | ||||||

| Common stock, $.01 par value, 650,000,000 shares authorized; 180,526,879 and 165,276,913 issued and outstanding as of September 30, 2011 and 2010, respectively | 1,805,269 | 1,652,769 | ||||||

| Additional paid-in capital | 22,409,927 | 22,434,427 | ||||||

| Accumulated deficit | (26,229,970 | ) | (25,873,341 | ) | ||||

| Total stockholders' deficit | (1,974,774 | ) | (1,786,145 | ) | ||||

| TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIT | $ | 1,211,122 | $ | 2,597 | ||||

| The accompanying notes are an integral part of these financial statements. | ||||||||

| CLOUD MEDICAL DOCTOR SOFTWARE CORPORATION | ||||||||

| (Formerly National Scientific Corporation) | ||||||||

| STATEMENTS OF OPERATIONS | ||||||||

| Years Ended September 30, | ||||||||

| 2011 | 2010 | |||||||

| OPERATING EXPENSES: | ||||||||

| Total operating expenses | $ | 340,417 | $ | 21,964 | ||||

| OPERATING LOSS | (340,417 | ) | (21,964 | ) | ||||

| (LOSS) INCOME BEFORE TAXES AND DISCOUNTED OPERATIONS | $ | (340,417 | ) | (21,964 | ) | |||

| (LOSS) INCOME FROM CONTINUED OPERATIONS | (340,417 | ) | (21,964 | ) | ||||

| (LOSS) INCOME FROM DISCONTINUED OPERATIONS | (16,212 | ) | (35,121 | ) | ||||

| NET LOSS | $ | (356,629 | ) | $ | (57,085 | ) | ||

| NET LOSS PER COMMON SHARE: | ||||||||

| Basic | ||||||||

| Continuing operations | $ | (0.00 | ) | $ | (0.00 | ) | ||

| Discontinuing operations | $ | (0.00 | ) | $ | (0.00 | ) | ||

| NET (LOSS) INCOME PER COMMON SHARE | ||||||||

| Basic | $ | (0.00 | ) | $ | (0.00 | ) | ||

| WEIGHTED AVERAGE COMMON SHARES OUTSTANDING | ||||||||

| Basic | 180,526,879 | 165,276,879 | ||||||

| The accompanying notes are an integral part of these financial statements. | ||||||||

| CLOUD MEDICAL DOCTOR SOFTWARE CORPORATION | ||||||||||||||||||||||||||||

| (Formerly National Scientific Corporation) | ||||||||||||||||||||||||||||

| STATEMENTS OF STOCKHOLDERS' DEFICIT | ||||||||||||||||||||||||||||

| FOR THE YEARS ENDED SEPTEMBER 30, 2011 AND 2010 | ||||||||||||||||||||||||||||

| Preferred Stock | Common Stock | |||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Additional Paid-in Capital | Accumulated Deficit | Total | ||||||||||||||||||||||

| SEPTEMBER 30, 2008 | — | $ | — | 137,276,879 | $ | 1,372,770 | $ | 22,658,682 | $ | (25,491,084 | ) | $ | (1,459,633 | ) | ||||||||||||||

| Options expired | — | 19,945 | 19,945 | |||||||||||||||||||||||||

| Common stock issued for back pay of officers | 28,000,000 | 280,000 | (244,200 | ) | — | 35,800 | ||||||||||||||||||||||

| Net loss | (325,172 | ) | (325,172 | ) | ||||||||||||||||||||||||

| SEPTEMBER 30, 2009 | — | $ | — | 165,276,879 | $ | 1,652,769 | $ | 22,434,427 | $ | (25,816,256 | ) | $ | (1,729,061 | ) | ||||||||||||||

| Net loss | (57,085 | ) | (57,085 | ) | ||||||||||||||||||||||||

| SEPTEMBER 30, 2010 | — | $ | — | 165,276,879 | $ | 1,652,769 | $ | 22,434,427 | $ | (25,873,341 | ) | $ | (1,786,146 | ) | ||||||||||||||

| Common stock issued for compensation | 15,000,000 | 150,000 | (45,000 | ) | 105,000 | |||||||||||||||||||||||

| Preferred stock issued for compensation | 4,000,000 | 40,000 | (2,000 | ) | 38,000 | |||||||||||||||||||||||

| Common stock issued for cash | 250,000 | 2,500 | 22,500 | 25,000 | ||||||||||||||||||||||||

| Net loss | (356,629 | ) | (356,629 | ) | ||||||||||||||||||||||||

| SEPTEMBER 30, 2011 | 4,000,000 | $ | 40,000 | 180,526,879 | $ | 1,805,269 | $ | 22,409,927 | $ | (26,229,970 | ) | $ | (1,974,775 | ) | ||||||||||||||

| THE LINE OF BUSINESS REPORTED ON THESE FINANCIAL STATEMENTS | ||||||||||||||||||||||||||||

| WAS DISCONTINUED IN FEBRUARY 2010. SEE NOTE 1 | ||||||||||||||||||||||||||||

| The accompanying notes are an integral part of these financial statements | ||||||||||||||||||||||||||||

| CLOUD MEDICAL DOCTOR SOFTWARE CORPORATION | ||||||||

| (Formerly National Scientific Corporation) | ||||||||

| STATEMENTS OF CASH FLOWS | ||||||||

| September 30, | ||||||||

| 2011 | 2010 | |||||||

| Net Loss | $ | (356,629 | ) | $ | (57,085 | ) | ||

| Adjustments to reconcile net loss to net cash | ||||||||

| (used in) operating activities: | ||||||||

| Discontinued operations | 16,212 | 35,121 | ||||||

| Changes in assets and liabilities: | ||||||||

| Stock issued for compensation | 143,000 | — | ||||||

| Net assets and liabilities from discontinued operations | (23,214 | ) | (9,554 | ) | ||||

| Net cash used in operating activities | (220,631 | ) | (31,518 | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Common stock issued for cash | 25,000 | — | ||||||

| Advances from affiliates | 159,515 | 36,000 | ||||||

| Line of credit | 44,535 | (14,719 | ) | |||||

| Net cash provided by financing activities | 229,050 | 21,281 | ||||||

| INCREASE IN CASH | 8,419 | (10,237 | ) | |||||

| CASH, BEGINNING OF PERIOD | 2,597 | 12,434 | ||||||

| CASH, END OF PERIOD | $ | 11,016 | $ | 2,197 | ||||

| SUPPLEMENTAL CASH FLOW INFORMATION: | ||||||||

| Interest paid | $ | — | $ | — | ||||

| Taxes paid | $ | — | $ | — | ||||

| Purchase of proprietary technology | $ | 1,200,106 | $ | — | ||||

| The accompanying notes are an integral part of these financial statements. | ||||||||

CLOUD MEDICAL DOCTOR SOFTWARE CORPORATION

NOTES TO FINANCIAL STATEMENTS

FOR THE YEARS ENDED SEPTEMBER 30, 2011 AND 2010

NOTE 1 - DESCRIPTION OF BUSINESS

THE COMPANY PREVIOUSLY HAD INSUFFICIENT WORKING CAPITAL TO PAY FOR THE PROFESSIONAL SERVICES REQUIRED TO PREPARE, AUDIT, AND FILE THE QUARTERLY AND ANNUAL REPORTS REQUIRED BY THE SECURITIES ACT OF 1934. AS A RESULT, THE AUDITORS WHO AUDITED THE SEPTEMBER 30, 2007 FINANCIAL STATEMENTS AND REVIEWED THE QUARTERLY REPORTS THROUGH JUNE 30, 2008 RESIGNED EFFECTIVE DECEMBER 13, 2011.

IN FEBRUARY 2010 THE BOARD OF DIRECTORS VOTED TO DISCONTINUE THE MOBILE DVR AND LOCATION PRODUCTS LINE OF BUSINESS REPORTED IN THESE FINANCIAL STATEMENTS DUE TO THE CUMULATIVE EFFECTS OF SEVERELY DECLINING REVENUES RESULTING FROM THE 2008 RECESSION. SINCE THIS DECISION WAS MADE SUBSEQUENT TO THE YEARS ENDED SEPTEMBER 30, 2008 AND 2009, THE QUARTERLY AND YEAR END STATEMENTS FOR THOSE YEARS ARE BEING REPORTED ON A GOING CONCERN BASIS RATHER THAN AS DISCONTINUED OPERATIONS. THEY WILL, HOWEVER, BE REPORTED AS DISCONTINUED OPERATIONS COMMENCING WITH THE FISCAL 2010 FILINGS.

NEW MANAGEMENT HAS SUBSEQUENTLY INFUSED SUFFICIENT WORKING CAPITAL TO BRING THE 1934 ACT FILINGS CURRENT. ADDITIONALLY, A NEW LINE OF BUSINESS HAS ALSO COMMENCED WHICH WILL BE REPORTED ON IN THE FISCAL 2011 AND 2012 FILINGS.

ACCORDINGLY, THESE FINANCIAL STATEMENTS ARE BEING SUBMITTED ONLY TO COMPLY WITH SEC RULES AND REGULATIONS AND SHOULD NOT BE RELIED UPON FOR YOUR INVESTMENT DECISIONS. THE OPERATIONS REPORTED ON IN THESE FINANCIAL STATEMENTS HAVE BEEN DISCONTINUED AS OF FEBRUARY 4, 2010. NEW MANAGEMENT ENCOURAGES THE READERS OF THESE FINANCIAL STATEMENTS TO SUSPEND ANY INVESTMENT DECISIONS PERTAINING TO THE STOCK OF THIS COMPANY UNTIL ALL REQUIRED 1934 ACT FILINGS ARE BROUGHT CURRENT.

The Company was incorporated in Texas on June 22, 1953 as American Mortgage Company. On May 16, 1996, the Company changed its name to National Scientific Corporation. On April 3, 2012, the Company changed its name to Cloud Medical Doctor Software Corporation. During 1996, the Company acquired the operations of Eden Systems, Inc. (Eden) as a wholly owned subsidiary. Eden was engaged in water treatment and the retailing of cleaning products. Eden’s operations were sold on October 1, 1997. From September 30, 1997 through the year ended September 30, 2001, we aimed our efforts in the research and development of semiconductor proprietary technology and processes and in raising capital to fund its operations and research. Beginning in calendar 2002, we focused our efforts on the development, acquisition, enhancement and marketing of location device technologies. Our revenue is derived from sales of electronic devices, recognized as the product is delivered.

In February 4, 2010 the prior Board members Mr. Michael Grollman and Mr. Greg Szabo, voted to discontinue and wind down the operations of the Company's Mobile DVR and Location Products business and operate the remaining Company assets in a Limited Liability Company named NSC Labs, LLC, a company controlled and owned by Mr. Grollman. Mr. Grollman and NSC Labs, LLC entered into an agreement to pay the Company $100,000 plus 2% of revenues. Since as of this filing neither Mr. Grollman nor NSC Labs, LLC have paid the specified consideration for this transaction the transaction has not been recorded in the accounting records of the Company