UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the fiscal year ended December 31, 2019 |

or

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the transition period from to |

Commission file number 0-21513

DXP Enterprises, Inc.

(Exact name of registrant as specified in its charter)

Texas | 76-0509661 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

5301 Hollister, Houston, Texas | 77040 | (713) 996-4700 | ||

(Address of principal executive offices) | (Zip Code) | (Registrant’s telephone number, including area code) | ||

Title of Each Class | Trading Symbol | Name of Exchange on which Registered | ||

Common Stock par value $0.01 | DXPE | NASDAQ Global Select Market | ||

Securities registered pursuant to Section 12(b) of the Act:

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☒ |

Non-accelerated filer ☐ | Smaller reporting company ☐ |

Emerging growth company ☐ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

Aggregate market value of the registrant's Common Stock held by non-affiliates of registrant as of June 28, 2019 was $605.1 million based on the closing sale price as reported on the NASDAQ Stock Market System.

Number of shares of registrant's Common Stock outstanding as of February 28, 2020: 17,647,751.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for our 2020 annual meeting of shareholders are incorporated by reference into Part III hereof.

The 2020 proxy statement will be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

TABLE OF CONTENTS

DESCRIPTION

Item | Page | |

PART I | ||

1. | ||

1A. | ||

1B. | ||

2. | ||

3. | ||

4. | ||

PART II | ||

5. | ||

6. | ||

7. | ||

7A. | ||

8. | ||

9. | ||

9A. | ||

9B. | ||

PART III | ||

10. | ||

11. | ||

12. | ||

13. | ||

14. | ||

PART IV | ||

15. | ||

16. | ||

2

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Report”) contains statements that constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, as amended. Such statements can be identified by the use of forward-looking terminology such as “believes”, “expects”, “may”, “might”, “estimates”, “will”, “should”, “could”, “plans”, or “anticipates”, or the negative thereof, other variations thereon, or comparable terminology, or by discussions of strategy. Any such forward-looking statements are not guarantees of future performance and may involve significant risks and uncertainties, and actual results may vary materially from those discussed in the forward-looking statements as a result of various factors. These factors include the effectiveness of management’s strategies and decisions, our ability to implement our internal growth and acquisition growth strategies, general economic and business conditions specific to our primary customers, changes in customer preferences and attitudes, changes in government regulations, our ability to effectively integrate businesses we may acquire, our success in remediating our internal control weaknesses, new or modified statutory or regulatory requirements, increased shipping and third-party transportation costs, risks associated with operating in foreign countries, availability of materials and labor, inability to obtain or delay in obtaining government or third-party approvals and permits, non-performance by third parties of their contractual obligations, unforeseen hazards such as weather conditions, pandemics, acts or war or terrorist acts and the governmental or military response thereto, cyber-attacks adversely affecting our operations, other geological, operating and economic considerations and declining prices and market conditions, including reduced oil and gas prices and supply or demand for maintenance, repair and operating products, equipment and service, and our ability to obtain financing on favorable terms or amend our credit facilities as needed and our ability to service the debt. This Report identifies other factors that could cause such differences. We cannot assure that these are all of the factors that could cause actual results to vary materially from the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in "Risk Factors", and elsewhere in this Report. We assume no obligation and do not intend to update these forward-looking statements. Unless the context otherwise requires, references in this Report to the "Company", "DXP", “we” or “our” shall mean DXP Enterprises, Inc., a Texas corporation, together with its subsidiaries.

3

PART I

ITEM 1. Business

Company Overview

DXP was incorporated in Texas in 1996 to be the successor to SEPCO Industries, Inc., founded in 1908. Since our predecessor company was founded, we have primarily been engaged in the business of distributing maintenance, repair and operating ("MRO") products, equipment and service to energy and industrial customers. The Company is organized into three business segments: Service Centers ("SC"), Supply Chain Services ("SCS") and Innovative Pumping Solutions ("IPS"). Sales, operating income, and other financial information for 2019, 2018 and 2017, and identifiable assets at the close of such years for our business segments are presented in Note 19 – Segment and Geographical Reporting to the Consolidated Financial Statements in Item 8. Financial Statements and Supplementary Data.

Our total sales have increased from $125 million in 1996 to $1.3 billion in 2019 through a combination of internal growth and business acquisitions. At December 31, 2019, we operated from 155 locations which included 35 states in the U.S., nine provinces in Canada and one location in Dubai serving customers engaged in a variety of industrial end markets. We have grown sales and profitability by adding additional products, services, and locations and becoming customer driven experts in maintenance, repair and operating solutions.

Our principal executive office is located at 5301 Hollister Houston, Texas 77040, and our telephone number is (713) 996-4700. Our website address on the internet is www.dxpe.com and emails may be sent to info@dxpe.com. The reference to our website address does not constitute incorporation by reference of the information contained on the website and such information should not be considered part of this report.

Industry Overview

The industrial distribution market is highly fragmented. Based on 2018 sales as reported by Industrial Distribution magazine, we were the 16 th largest distributor of MRO products in the United States. Most industrial customers currently purchase their industrial supplies through numerous local distribution and supply companies. These distributors generally provide the customer with repair and maintenance services, technical support and application expertise with respect to one product category. Products typically are purchased by the distributor for resale directly from the manufacturer and warehoused at distribution facilities of the distributor until sold to the customer. The customer also typically will purchase an amount of product inventory for its near term anticipated needs and store those products at its industrial site until the products are used.

We believe that the distribution system for industrial products, as described in the preceding paragraph, creates inefficiencies at both the customer and the distributor levels through excess inventory requirements and duplicative cost structures. To compete more effectively, our customers and other users of MRO products are seeking ways to enhance efficiencies and lower MRO product and procurement costs. In response to this customer desire, three primary trends have emerged in the industrial supply industry:

• | Industry Consolidation. Industrial customers have reduced the number of supplier relationships they maintain to lower total purchasing costs, improve inventory management, assure consistently high levels of customer service and enhance purchasing power. This focus on fewer suppliers has led to consolidation within the fragmented industrial distribution industry. |

• | Customized Integrated Service. As industrial customers focus on their core manufacturing or other production competencies, they increasingly demand customized integration services, consisting of value-added traditional distribution, supply chain services, modular equipment and repair and maintenance services. |

• | Single Source, First-Tier Distribution. As industrial customers continue to address cost containment, there is a trend toward reducing the number of suppliers and eliminating multiple tiers of distribution. Therefore, to lower overall costs to the customer, some MRO product distributors are expanding their product coverage to eliminate second-tier distributors and become a “one stop source”. |

We believe we have increased our competitive advantage through our traditional fabrication of integrated system pump packages and integrated supply programs, which are designed to address our customers’ specific product and procurement needs. We offer our customers various options for the integration of their supply needs, ranging from serving as a single source of supply for all our specific lines of products and product categories to offering a fully integrated supply package in which we assume procurement and management functions, which can include ownership of inventory, at the customer's location. Our approach to integrated

4

supply allows us to design a program that best fits the needs of the customer. Customers purchasing large quantities of product are able to outsource all or most of those needs to us. For customers with smaller supply needs, we are able to combine our traditional distribution capabilities with our broad product categories and advanced ordering systems to allow the customer to engage in one-stop sourcing without the commitment required under an integrated supply contract.

Business Segments

The Company is organized into three business segments: Service Centers (“SC”), Supply Chain Services (“SCS”) and Innovative Pumping Solutions (“IPS”). Our segments provide management with a comprehensive financial view of our key businesses. The segments enable the alignment of strategies and objectives and provide a framework for timely and rational allocation of resources within our businesses. In addition to the three business segments, our consolidated financial results include "Corporate and other expenses" which includes costs related to our centralized support functions, consisting, of accounting and finance, information technology, human resources, legal, inventory management & procurement and other support services and removes inter-company transactions. The following table sets forth DXP’s sales by business segments as of December 31, 2019. See Results of Operations under Item 7. Management Discussion and Analysis of Financial Condition and Results of Operations for further information on our segments’ financial results.

Segment | 2019 Sales (in millions) | % of Sales | End-Markets | Locations | Employees | |||||

SC | 762.3 | 60.2% | Oil & Gas, Food & Beverage, General Industrial, Chemical & Petrochemical, Transportation, Aerospace | 141 service centers, 4 distribution centers | 1,586 | |||||

IPS | 303.7 | 24.0% | Oil & Gas Food & Beverage, Mining & Transportation | 10 fabrication facilities | 498 | |||||

SCS | 201.3 | 15.9% | Oil & Gas Mining Utilities | 89 customers facilities' | 406 | |||||

Service Centers

The Service Centers are engaged in providing MRO products, equipment and integrated services, including technical expertise and logistics capabilities, to energy and industrial customers with the ability to provide same day delivery. We offer our customers a single source of supply on an efficient and competitive basis by being a first-tier distributor that can purchase products directly from manufacturers. As a first-tier distributor, we are able to reduce our customers' costs and improve efficiencies in the supply chain. We offer a wide range of industrial MRO products, equipment and integrated services through a continuum of customized and efficient MRO solutions. We also provide services such as field safety supervision, in-house and field repair and predictive maintenance.

A majority of our Service Center segment sales are derived from customer purchase orders for products. Sales are directly solicited from customers by our sales force. DXP Service Centers are stocked and staffed with knowledgeable sales associates and backed by a centralized customer service team of experienced industry professionals. At December 31, 2019, our Service Centers’ products and services were distributed from 141 service centers and 4 distribution centers. DXP Service Centers provide a wide range of MRO products in the rotating equipment, bearing, power transmission, hose, fluid power, metal working, industrial supply and safety product and service categories. We currently serve as a first-tier distributor of more than 1,000,000 items of which more than 60,000 are stock keeping units (SKUs) for use primarily by customers engaged in the oil and gas, food and beverage, petrochemical, transportation and other general industrial industries. Other industries served by our Service Centers include mining, construction, chemical, municipal, agriculture and pulp and paper.

The Service Centers segment’s long-lived assets are located in the United States, Canada and Dubai. Approximately 10.1% of the Service Centers segment’s revenues were in Canada and the remainder was virtually all in the U.S. Our foreign operations are subject to certain unique risks, which are more fully disclosed in Item 1A “Risk Factors,” “Risks Associated with Conducting Business in Foreign Countries”.

At December 31, 2019, the Service Centers segment had approximately 1,586 employees, all of whom were full-time.

5

Innovative Pumping Solutions

DXP’s Innovative Pumping Solutions® (IPS) segment provides integrated, custom pump skid packages, pump remanufacturing and manufactures branded private label pumps to meet the capital equipment needs of our global customer base. Our IPS segment provides a single source for engineering, systems design and fabrication for unique customer specifications.

Our sales of integrated pump packages, remanufactured pumps or branded private label pumps are generally derived from customer purchase orders containing the customers’ unique specifications. Sales are directly solicited from customers by our dedicated sales force.

DXP’s engineering staff can design a complete custom pump package to meet our customers’ project specifications. Drafting programs such as Solidworks® and AutoCAD® allow our engineering team to verify the design and layout of packages with our customers prior to the start of fabrication. Finite Elemental Analysis programs such as Cosmos Professional® are used to design the package to meet all normal and future loads and forces. This process helps maximize the pump packages’ life and minimizes any impact to the environment.

With over 100 years of fabrication experience, DXP has acquired the technical expertise to ensure that our pumps and pump packages are built to meet the highest standards. DXP utilizes manufacturer authorized equipment and manufacturer certified personnel. Pump packages require MRO products and original equipment manufacturers’ (OEM) equipment such as pumps, motors, valves, and consumable products, such as welding supplies. DXP leverages its MRO product inventories and breadth of authorized products to lower the total cost and maintain the quality of our pump packages.

DXP’s fabrication facilities provide convenient technical support and pump repair services. The facilities contain state of the art equipment to provide the technical expertise our customers require including, but not limited to, the following:

• | Structural welding |

• | Pipe welding |

• | Custom skid assembly |

• | Custom coatings |

• | Hydrostatic pressure testing |

• | Mechanical string testing |

Examples of our innovative pump packages include, but are not limited to:

• | Diesel and electric driven firewater packages |

• | Pipeline booster packages |

• | Potable water packages |

• | Pigging pump packages |

• | Lease Automatic Custody Transfer (LACT) charge units |

• | Chemical injection pump packages wash down units |

• | Seawater lift pump packages |

• | Jockey pump packages |

• | Condensate pump packages |

• | Cooling water packages |

• | Seawater/produced water injection packages |

• | Variety of packages to meet customer required industry specifications such as API, ANSI and NFPA |

At December 31, 2019, the Innovative Pumping Solutions segment operated out of 10 facilities, eight of which are located in the United States and two in Canada.

Approximately 3.3% of the IPS segment’s long-lived assets are located in Canada and the remainder are located in the U.S. Approximately 6.2% of the IPS segment’s 2019 revenues were recognized in Canada and 93.8% were in the U.S.

At December 31, 2019, the IPS segment had approximately 498 employees, all of whom were full-time.

Total backlog, representing firm orders for the IPS segment products that have been received and entered into our production systems, was $101.1 million and $124.2 million at December 31, 2019 and 2018, respectively.

6

Supply Chain Services

DXP’s Supply Chain Services (SCS) segment manages all or part of its customers’ supply chains, including procurement and inventory management. The SCS segment enters into long-term contracts with its customers that can be canceled on little or no notice under certain circumstances. The SCS segment provides fully outsourced MRO solutions for sourcing MRO products including, but not limited to, the following: inventory optimization and management; store room management; transaction consolidation and control; vendor oversight and procurement cost optimization; productivity improvement services; and customized reporting. Our mission is to help our customers become more competitive by reducing their indirect material costs and order cycle time by increasing productivity and by creating enterprise-wide inventory and procurement visibility and control.

DXP has developed assessment tools and master plan templates aimed at taking cost out of supply chain processes, streamlining operations and boosting productivity. This multi-faceted approach allows us to manage the entire MRO products channel for maximum efficiency and optimal control, which ultimately provides our customers with a low-cost solution.

DXP takes a consultative approach to determine the strengths and opportunities for improvement within a customer’s MRO products supply chain. This assessment determines if and how we can best streamline operations, drive value within the procurement process, and increase control in storeroom management.

Decades of supply chain inventory management experience and comprehensive research, as well as a thorough understanding of our customers’ businesses and industries have allowed us to design standardized programs that are flexible enough to be fully adaptable to address our customers’ unique MRO products supply chain challenges. These standardized programs include:

• | SmartAgreement, a planned, pro-active MRO products procurement solution for MRO categories leveraging DXP’s local Service Centers. |

• | SmartBuy, DXP’s on-site or centralized MRO procurement solution. |

• | SmartSource SM, DXP’s on-site procurement and storeroom management by DXP personnel. |

• | SmartStore, DXP’s customized e-Catalog solution. |

• | SmartVend, DXP’s industrial dispensing solution, which allows for inventory-level optimization, user accountability and item usage reduction by an initial 20-40%. |

• | SmartServ, DXP’s integrated service pump solution. It provides a more efficient way to manage the entire life cycle of pumping systems and rotating equipment. |

DXP’s SmartSolutions programs listed above help customers to cut product costs, improve supply chain efficiencies and obtain expert technical support. DXP represents manufacturers of up to 90% of all the maintenance, repair and operating products of our customers. Unlike many other distributors who buy products from second-tier sources, DXP takes customers to the source of the products they need.

At December 31, 2019, the Supply Chain Services segment operated supply chain installations in 89 of our customers’ facilities.

All of the SCS segment’s long-lived assets are in the U.S. and the majority of the SCS segment’s 2019 revenues were recognized in the U.S.

At December 31, 2019, the Supply Chain Services segment had approximately 406 employees, all of whom were full-time.

Products

Most industrial customers currently purchase their MRO products through local or national distribution companies that are focused on single or unique product categories. As a first-tier distributor, our network of service and distribution centers stock more than 60,000 SKUs and provide customers with access to more than 1,000,000 items. Given our breadth of product and our industrial distribution customers’ focus around specific product categories, we have become customer driven experts in five key product categories. As such, our three business segments are supported by the following five key product categories: rotating equipment; bearings & power transmission; industrial supplies; metal working; and safety products & services. Each business segment tailors its inventory and leverages product experts to meet the needs of its local customers.

Key product categories that we offer include:

• | Rotating Equipment. Our rotating equipment products include a full line of centrifugal pumps for transfer and process service applications, such as petrochemicals, refining and crude oil production; rotary gear pumps for low- to- medium pressure service applications, such as pumping lubricating oils and other viscous liquids; plunger and piston pumps |

7

for high-pressure service applications such as disposal of produced water and crude oil pipeline service; and air-operated diaphragm pumps. We also provide a large variety of pump accessories.

• | Bearings & Power Transmission. Our bearing products include several types of mounted and un-mounted bearings for a variety of applications. The power transmission products we distribute include speed reducers, flexible-coupling drives, chain drives, sprockets, gears, conveyors, clutches, brakes and hoses. |

• | Industrial Supplies. We offer a broad range of industrial supplies, such as abrasives, tapes and adhesive products, coatings and lubricants, fasteners, hand tools, janitorial products, pneumatic tools, welding supplies and welding equipment. |

• | Metal Working. Our metal working products include a broad range of cutting tools, abrasives, coolants, gauges, industrial tools and machine shop supplies. |

• | Safety Products & Services. We sell a broad range of safety products including eye and face protection, first aid, hand protection, hazardous material handling, instrumentation and respiratory protection products. Additionally, we provide safety services including hydrogen sulfide (H2S) gas protection and safety, specialized and standby fire protection, safety supervision, training, monitoring, equipment rental and consulting. Our safety services include safety supervision, medic services, safety audits, instrument repair and calibration, training, monitoring, equipment rental and consulting. |

We acquire our products through numerous OEMs. We are authorized to distribute certain manufacturers' products only in specific geographic areas. All of our oral or written distribution authorizations are subject to cancellation by the manufacturer, some upon little or no notice. For the last three fiscal years, no manufacturer provided products that accounted for 10% or more of our revenues.

Over 90% of our business relates to sales of products. Service revenues are less than 10% of sales.

The Company has operations in the United States of America, Canada and Dubai. Information regarding financial data by geographic areas is set forth in Note 19 - Segment and Geographical Reporting of the Notes to Consolidated Financial Statements.

Recent Acquisitions

A key component of our growth strategy includes effecting acquisitions of businesses with complementary or desirable product lines, locations or customers. Since 2004, we have completed 37 acquisitions across our three business segments.

On January 31, 2020, the Company completed the acquisition of Turbo Machinery Repair (“Turbo”), a pump and industrial equipment repair, maintenance, machining and labor services company. The purchase of Turbo was funded with cash on hand.

On January 2, 2020, the Company completed the acquisition of Pumping Systems, Inc. (“PSI”), a distributor of pumps, systems and related services. The PSI acquisition was funded with cash on hand as well as issuing DXP's common stock.

On January 1, 2018, the Company completed the acquisition of Application Specialties, Inc. (“ASI”), a distributor of cutting tools, abrasives, coolants and machine shop supplies. DXP paid approximately $11.7 million for ASI at closing plus an additional earn-out provision for up to $4.6 million. The purchase was financed with $10.8 million of cash on hand as well as issuing $0.9 million of DXP’s common stock, and the potential earnout extends for a three period.

Competition

Our business is highly competitive. In the Service Centers segment we compete with a variety of industrial supply distributors, some of which may have greater financial and other resources than we do. Some of our competitors are small enterprises selling to customers in a limited geographic area. We also compete with catalog distributors, large warehouse stores and, to a lesser extent, manufacturers. While certain catalog distributors provide product offerings as broad as ours, these competitors do not offer the product application, technical expertise and after-the-sale services that we provide. In the Supply Chain Services segment we compete with larger distributors that provide integrated supply programs and outsourcing services, some of which might be able to supply their products in a more efficient and cost-effective manner than we can provide. In the Innovative Pumping Solutions segment we compete against a variety of manufacturers, distributors and fabricators, many of which may have greater financial and other resources than we do. We generally compete on expertise, responsiveness and price in all of our segments.

8

Insurance

We maintain liability and other insurance that we believe to be customary and generally consistent with industry practice. We retain a portion of the risk for medical claims, general liability, worker’s compensation and property losses. The various deductibles of our insurance policies generally do not exceed $250,000 per occurrence. There are also certain risks for which we do not maintain insurance. There can be no assurance that such insurance will be adequate for the risks involved, that coverage limits will not be exceeded or that such insurance will apply to all liabilities. The occurrence of an adverse claim in excess of the coverage limits that we maintain could have a material adverse effect on our financial condition and results of operations. Additionally, we are partially self-insured for our group health plan, worker’s compensation, auto liability and general liability insurance.

Government Regulation and Environmental Matters

We are subject to various laws and regulations relating to our business and operations, and various health and safety regulations including those established by the Occupational Safety and Health Administration and Canadian Occupational Health and Safety.

Certain of our operations are subject to federal, state and local laws and regulations as well as provincial regulations controlling the discharge of materials into or otherwise relating to the protection of the environment.

Although we believe that we have adequate procedures to comply with applicable discharge and other environmental laws, such laws and regulations could result in costs to remediate releases of regulated substances into the environment or costs to remediate sites to which we sent regulated substances for disposal. In some cases, these laws can impose strict liability for the entire cost of clean-up on any responsible party without regard to negligence or fault and impose liability on us for the conduct of others or conditions others have caused, or for our acts that complied with all applicable requirements when we performed them. New laws have been enacted and regulations are being adopted by various regulatory agencies on a continuing basis and the costs of compliance with these new laws can only be broadly appraised until their implementation becomes more defined.

The risks of accidental contamination or injury from the discharge of controlled or hazardous materials and chemicals cannot be eliminated completely. In the event of such a discharge, we could be held liable for any damages that result, and any such liability could have a material adverse effect on us.

We are not currently aware of any situation or condition that we believe is likely to have a material adverse effect on our results of operations or financial condition.

Employees

At December 31, 2019, DXP had 2,747 employees, all of whom were full-time.

Executive Officers

The following is a list of DXP’s executive officers, their age, positions, and a description of each officer’s business experience as of March 9, 2020. All of our executive officers hold office at the pleasure of DXP’s Board of Directors.

NAME | AGE | TITLE |

David R. Little | 68 | Chairman of the Board, President and Chief Executive Officer |

Kent Yee | 44 | Senior Vice President/Chief Financial Officer |

Gene Padgett | 49 | Senior Vice President/Chief Accounting Officer |

David C. Vinson | 69 | Senior Vice President/Innovative Pumping Solutions |

John J. Jeffery | 52 | Senior Vice President/Supply Chain Services |

Todd Hamlin | 48 | Senior Vice President/Service Centers |

Chris Gregory | 45 | Senior Vice President/Information Technology |

David R. Little. Mr. Little has served as Chairman of the Board, President and Chief Executive Officer of DXP since its organization in 1996 and also has held these positions with SEPCO Industries, Inc., predecessor to the Company (“SEPCO”), since he acquired a controlling interest in SEPCO in 1986. Mr. Little has been employed by SEPCO since 1975 in various capacities, including Staff Accountant, Controller, Vice President/Finance and President. Mr. Little gives our Board insight and in-depth knowledge of our industry and our specific operations and strategies. He also provides leadership skills and knowledge of our local community and business environment, which he has gained through his long career with DXP and its predecessor companies.

9

Kent Yee. Mr. Yee was appointed Senior Vice President/Chief Financial Officer in June 2017. Currently, Mr. Yee is responsible for acquisitions, finance, accounting and human resources of DXP. From March 2011 to June 2017, Mr. Yee served as Senior Vice President Corporate Development and led DXP's mergers and acquisitions, business integration and internal strategic project activities. During March 2011, Mr. Yee joined DXP from Stephens Inc.'s Industrial Distribution and Services team where he served in various positions and most recently as Vice President from August 2005 to February 2011. Prior to Stephens, Mr. Yee was a member of The Home Depot’s Strategic Business Development Group with a primary focus on acquisition activity for HD Supply. Mr. Yee was also an Associate in the Global Syndicated Finance Group at JPMorgan Chase. He has executed over 44 transactions including more than $1.5 billion in M&A and $3.4 billion in financing transactions primarily for change of control deals and numerous industrial and distribution acquisition and sale assignments. He holds a Bachelors of Arts in Urban Planning from Morehouse College and an MBA from Harvard University Graduate School of Business.

Gene Padgett. Mr. Padgett was appointed Senior Vice President/Chief Accounting Officer in May 2018. Prior to joining the Company, Mr. Padgett spent ten years with Spectra Energy in several positions with increasing responsibility including General Manager of U.S. and Canadian Tax, Director of U.S. Operations Accounting and General Manager Corporate Accounting. Prior to Spectra Energy, he spent seven years with Duke Energy in various roles covering Corporate Accounting, Accounting Research and Policy and working as a divisional controller. Mr. Padgett started his career at PricewaterhouseCoopers.

David C. Vinson. Mr. Vinson was elected Senior Vice President/Innovative Pumping Solutions in January 2006. He served as Senior Vice President/Operations of DXP from October 2000 to December 2005. From 1996 until October 2000, Mr. Vinson served as Vice President/Traffic, Logistics and Inventory. Mr. Vinson has served in various capacities with DXP since his employment in 1981.

John J. Jeffery. Mr. Jeffery serves as Senior Vice President of Supply Chain Services, Marketing and Information Technology. He oversees the strategic direction for the Supply Chain Services business unit while leveraging both Marketing and Information Technology to drive innovative business development initiatives for organizational growth and visibility. He began his career with T.L. Walker, which was later acquired by DXP in 1991. During his tenure with DXP, Mr. Jeffery has served in various significant capacities including branch, area, regional and national sales management as well as sales, marketing and Service Center vice president roles. He holds a Bachelor of Science in Industrial Distribution from Texas A&M University and is also a graduate of the Executive Business Program at Rice University.

Todd Hamlin. Mr. Hamlin was elected Senior Vice President of DXP Service Centers in June of 2010. Mr. Hamlin joined the Company in 1995. From February 2006 until June 2010 he served as Regional Vice President of the Gulf Coast Region. Prior to serving as Regional Vice President of the Gulf Coast Region he served in various capacities, including application engineer, product specialist and sales representative. From April 2005 through February 2006, Mr. Hamlin worked as a sales manager for the UPS Supply Chain Services division of United Parcel Service, Inc. He holds a Bachelor’s of Science in Industrial Distribution from Texas A&M University and a Master in Distribution from Texas A&M University. Mr. Hamlin serves on the Advisory Board for Texas A&M’s Master in Distribution degree program. In 2014, Mr. Hamlin was elected to the Bearing Specialists Association’s Board of Directors.

Chris Gregory. Mr. Gregory was elected Senior Vice President and Chief Information Officer in March of 2018. Mr. Gregory joined the Company in August 2006. From December 2014 until January 2018 he served as Vice President of IT Strategic Solutions. Prior to serving as Vice President of IT Strategic Solutions he served in various roles, including application developer, database manager as well as leading the business intelligence and application development departments. He holds a Bachelor of Business Administration and Computer Information Systems from the University of Houston and an MBA from The University of Texas at Austin, McCombs School of Business.

All officers of DXP hold office until the regular meeting of the board of directors following the Annual Meeting of Shareholders or until their respective successors are duly elected and qualified or their earlier resignation or removal.

10

Available Information

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as amended (the “Exchange Act”), are available free of charge through our Internet website (www.dxpe.com) as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission. The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with SEC at http://www.sec.gov. Additionally, we make the following available free of charge through our Internet website ir.dxpe.com:

• | DXP Code of Ethics for Senior Financial Officers; |

• | DXP Code of Conduct; |

• | Compensation Committee Charter; |

• | Nominating and Governance Committee Charter; and |

• | Audit Committee Charter |

ITEM 1A. Risk Factors

We are subject to various risks and uncertainties in the course of our business. Investing in DXP involves risk. In deciding whether to invest in DXP, you should carefully consider the risk factors below as well as those matters referenced in the foregoing pages under “Disclosure Regarding Forward-Looking Statements” and other information included and incorporated by reference into this Report and other reports and materials filed by us with the Securities and Exchange Commission. Any of these risk factors could have a significant or material adverse effect on our businesses, results of operations, financial condition or liquidity. They could also cause significant fluctuations and volatility in the trading price of our securities. Readers should not consider any descriptions of these factors to be a complete set of all potential risks that could affect DXP. Further, many of these risks are interrelated and could occur under similar business and economic conditions, and the occurrence of certain of them may in turn cause the emergence or exacerbate the effects of others. Such a combination could materially increase the severity of the impact of these risks on our results of operations, liquidity and financial condition.

Decreased capital expenditures in the energy industry can adversely impact our customers’ demand for our products and services.

A significant portion of our revenue depends upon the level of capital and operating expenditures in the oil and natural gas industry, including capital expenditures in connection with the upstream, midstream, and downstream phases in the energy industry. Therefore, a significant decline in oil or natural gas prices could lead to a decrease in our customers’ capital and other expenditures and could adversely affect our revenues.

Demand for our products could decrease if the manufacturers of those products sell them directly to end users.

Typically, MRO products have been purchased through distributors and not directly from the manufacturers of those products. If customers were to purchase our products directly from manufacturers, or if manufacturers sought to increase their efforts to sell directly to end users, we could experience a significant decrease in sales and earnings.

Changes in our customer and product mix, or adverse changes to the cost of goods we sell, could cause our gross margin percentage to fluctuate or decrease, and we may not be able to maintain historical margins.

Changes in our customer mix have resulted from geographic expansion, daily selling activities within current geographic markets, and targeted selling activities to new customers. Changes in our product mix have resulted from marketing activities to existing customers and needs communicated to us from existing and prospective customers. There can be no assurance that we will be able to maintain our historical gross margins. In addition, we may also be subject to price increases from vendors that we may not be able to pass along to our customers.

Our manufacturers may cancel our oral or written distribution authorizations upon little or no notice, which could adversely impact our revenues and profits from distributing certain manufacturer’s products.

We are authorized to distribute certain manufacturers’ products in specific geographic areas and all of our oral or written distribution authorizations are subject to cancellation by the manufacturer, some upon little or no notice. If certain manufacturers cancel the distribution authorizations they granted to us, our distribution of their products could be disrupted and such occurrence could have a material adverse effect on our results of operations and financial conditions.

11

A deterioration in the oil and gas sector or other circumstances may negatively impact our business and results of operations and thus hinder our ability to comply with financial covenants under our credit facilities, including the Secured Leverage Ratio and Fixed Charge Coverage Ratio financial covenants.

A deterioration of the oil and gas sector or other circumstances that reduce our earnings may hinder our ability to comply with certain financial covenants under our credit facilities. Specifically, compliance with the Secured Leverage Ratio and Fixed Charge Coverage Ratio covenants depend on our ability to maintain net income and prevent losses. In the future we may not be able to comply with the covenants and, if we are not able to do so, our lenders may not be willing to waive such non-compliance or amend such covenants. If we are unable to comply with our financial covenants or obtain a waiver or amendment of those covenants or obtain alternative financing, our business and financial condition would be adversely affected.

We rely upon third-party transportation providers for our merchandise shipments and are subject to increased shipping costs as well as the potential inability of our third-party transportation providers to deliver products on a timely basis.

We rely upon independent third-party transportation providers for our merchandise shipments, including shipments to and from all of our service centers. Our utilization of these delivery services for shipments is subject to risks, including increases in fuel prices, labor availability, labor strikes and inclement weather, which may impact a shipping company’s ability to provide delivery services that adequately meet our shipping needs. If we change the shipping companies we use, we could face logistical difficulties that could adversely affect deliveries and we would incur costs and expend resources in connection with such change. In addition, we may not be able to obtain favorable terms as we have with our current third-party transportation providers.

Our business has substantial competition that could adversely affect our results.

Our business is highly competitive. We compete with a variety of industrial supply distributors, some of which may have greater financial and other resources than us. Although many of our traditional distribution competitors are small enterprises selling to customers in a limited geographic area, we also compete with larger distributors that provide integrated supply programs such as those offered through outsourcing services similar to those that are offered by our SCS segment. Some of these large distributors may be able to supply their products in a more timely and cost-efficient manner than us. Our competitors include catalog suppliers, large warehouse stores and, to a lesser extent, certain manufacturers. Competitive pressures could adversely affect DXP’s sales and profitability.

Adverse weather events or natural disasters could negatively disrupt our operations.

Certain areas in which we operate are susceptible to adverse weather conditions or natural disasters, such as hurricanes, tornadoes, floods and earthquakes. These events can disrupt our operations, result in damage to our properties and negatively affect the local economies in which we operate. Additionally, we may experience communication disruptions with our customers, vendors and employees.

We cannot predict whether or to what extent damage caused by these events will affect our operations or the economies in regions where we operate. These adverse events could result in disruption of our purchasing or distribution capabilities, interruption of our business that exceeds our insurance coverage, our inability to collect from customers and increased operating costs. Our business or results of operations may be adversely affected by these and other negative effects of these events.

Pandemic or other public health crisis could result in disruptions in supply chain, decreased customer demand, lower oil price and volatility in the stock market and the global economy, which could negatively impact our operations.

Pandemic or other public health crisis occurring at our or our vendors’ facilities could adversely impact or disrupt our operations, negatively affect the local economies where we operate and these types of events could negatively impact our customers’ spending in the impacted regions or depending upon the severity, globally, which could adversely impact our business, reputation, results of operations or financial conditions. For example, since December 2019, a strain of 2019 Novel Coronavirus (“COVID-19”) has surfaced from China and has spread into several regions globally, resulting in certain supply chain disruptions, volatilities in the stock market, lower oil prices, lockdown in international travels, which could adversely impact the global economy and potential decreased demand from our customers. At this point, the extent to which the COVID-19 virus may impact our operation results is uncertain.

The loss of or the failure to attract and retain key personnel could adversely impact our results of operations.

The loss of the services of any of the executive officers of the Company could have a material adverse effect on our financial condition and results of operations. In addition, our ability to grow successfully will be dependent upon our ability to attract and

12

retain qualified management and technical and operational personnel. The failure to attract and retain such persons could materially adversely affect our financial condition and results of operations.

The loss of any key supplier could adversely affect DXP’s sales and profitability.

We have distribution rights for certain product lines and depend on these distribution rights for a substantial portion of our business. Many of these distribution rights are pursuant to contracts that are subject to cancellation upon little or no prior notice. The termination or limitation by any key supplier of its relationship with the Company could result in a temporary disruption of our business and, in turn, could adversely affect our results of operations and financial condition.

We are subject to various government regulations, the cost of compliance of such regulations could increase our cost of conducting business and any violations of such regulations could materially adversely affect our financial condition or results of operations.

We are subject to laws and regulations in every jurisdiction where we operate. Compliance with laws and regulations increases our cost of doing business. We are subject to a variety of laws and regulations, including without limitation import and export requirements, the Foreign Corrupt Practices Act (the “FCPA”), tax laws (including U.S. taxes on our foreign subsidiaries), data privacy requirements, labor laws and anti-competition regulations. We are also subject to audits and inquiries in the ordinary course of business. Changes to the legal and regulatory environments could increase the cost of doing business, and such costs may increase in the future as a result of changes in these laws and regulations or in their interpretation. Our employees, contractors or agents may violate laws and regulations despite our attempts to implement policies and procedures to comply with such laws and regulations. Any such violations could individually or in the aggregate materially adversely affect our financial condition or results of operations.

We are subject to environmental, health and safety laws and regulations.

We are subject to federal, state, local, foreign and provincial environmental, health and safety laws and regulations. Fines and penalties may be imposed for non-compliance with applicable environmental, health and safety requirements and the failure to have or to comply with the terms and conditions of required permits. The failure by us to comply with applicable environmental, health and safety requirements could result in fines, penalties, enforcement actions, third party claims for property damage and personal injury, requirements to clean up property or to pay for the costs of cleanup, or regulatory or judicial orders requiring corrective measures.

A general slowdown in the economy could negatively impact DXP’s sales growth and profitability.

Economic and industry trends affect DXP’s business. Demand for our products is subject to economic trends affecting our customers and the industries in which they compete in particular. Many of these industries, such as the oil and gas industry, are subject to volatility while others, such as the petrochemical industry, are cyclical and materially affected by changes in the economy. As a result, demand for our products could be adversely impacted by changes in the markets of our customers. We traditionally do not enter into long-term contracts with our customers which increases the likelihood that economic downturns would affect our business.

Tax changes could affect our effective tax rate and profitability.

Future results could be adversely affected by changes in the effective tax rate as a result of changes in our overall profitability and changes in the mix of earnings and losses in countries with differing statutory tax rates, changes in tax legislation, the valuation of deferred tax assets and liabilities, the results of the examination of previously filed tax returns and continuing assessment of the Company's tax exposure.

Risks associated with conducting business in foreign countries.

We conduct a meaningful amount of business outside of the United States of America. We could be adversely affected by economic, legal, political and regulatory developments in countries that we conduct business in. We have meaningful operations in Canada in which the functional currency is denominated in Canadian dollars. We also have operations in Dubai, where the functional currency is dirham. As the value of currencies in foreign countries in which we have operations increases or decreases related to the U.S. dollar, the sales, expenses, profits, losses assets and liabilities of our foreign operations, as reported in our consolidated financial statements, increase or decrease, accordingly. Moreover, our international operations subject us to a variety of foreign laws and regulations, including without limitation, import and export requirements, the FCPA, U.S. and foreign tax laws, data privacy requirements, labor laws and anti-competition regulations. Our employees, contractors or agents may violate laws and

13

regulations despite our attempts to implement policies and procedures to comply with such laws and regulations. Any such violations could individually or in the aggregate materially adversely affect our financial condition or results of operations.

The trading price of our common stock may be volatile.

The market price of our common stock could be subject to wide fluctuations in response to, among other things, the risk factors described in this and other periodic reports, and other factors beyond our control, such as fluctuations in the valuation of companies perceived by investors to be comparable to us. Furthermore, the stock markets have experienced price and volume fluctuations that have affected and continue to affect the market prices of equity securities of many companies. These fluctuations often have been unrelated or disproportionate to the operating performance of those companies. These broad market and industry fluctuations, as well as general economic, political, and market conditions, such as recessions, interest rate changes or international currency fluctuations, may negatively affect the market price of our common stock. In the past, many companies that have experienced volatility in the market price of their stock have been subject to securities class action litigation. We may be the target of this type of litigation in the future. Securities litigation against us could result in substantial costs and divert our management's attention from other business concerns, which could adversely affect our business.

Our future results will be impacted by our ability to implement our internal growth strategy.

Our future results will depend in part on our success in implementing our internal growth strategy, which includes expanding our existing geographic areas, selling additional products to existing customers and adding new customers. Our ability to implement this strategy will depend on our success in selling more products and services to existing customers, acquiring new customers, hiring qualified sales persons, and marketing integrated forms of supply management such as those being pursued by us through our SmartSource SM program. We may not be successful in efforts to increase sales and product offerings to existing customers. Consolidation in our industry could heighten the impacts of competition on our business and results of operations discussed above. The fact that we do not traditionally enter into long-term contracts with our suppliers or customers may provide opportunities for our competitors.

We are subject to personal injury and product liability claims involving allegedly defective products.

A variety of products we distribute are used in potentially hazardous applications that can result in personal injury and product liability claims. A catastrophic occurrence at a location where the products we distribute are used may result in us being named as a defendant in lawsuits asserting potentially large claims and applicable law may render us liable for damages without regard to negligence or fault.

Risks associated with acquisition strategy.

Our future results will depend in part on our ability to successfully implement our acquisition strategy. We may not be able to consummate acquisitions at rates similar to the past, which could adversely impact our growth rate and stock price. This strategy includes taking advantage of a consolidation trend in the industry and effecting acquisitions of businesses with complementary or desirable product lines, strategic distribution locations, attractive customer bases or manufacturer relationships. Promising acquisitions are difficult to identify and complete for a number of reasons, including high valuations, competition among prospective buyers, the need for regulatory (including antitrust) approvals and the availability of affordable funding in the capital markets. In addition, competition for acquisitions in our business areas is significant and may result in higher purchase prices. Changes in accounting or regulatory requirements or instability in the credit markets could also adversely impact our ability to consummate acquisitions. In addition, acquisitions involve a number of special risks, including possible adverse effects on our operating results, diversion of management’s attention, failure to retain key personnel of the acquired business, difficulties in integrating operations, technologies, services and personnel of acquired companies, potential loss of customers of acquired companies, preserving business relationships of the acquired companies, risks associated with unanticipated events or liabilities, and expenses associated with obsolete inventory of an acquired business, some or all of which could have a material adverse effect on our business, financial condition and results of operations. Our ability to grow at or above our historic rates depends in part upon our ability to identify and successfully acquire and integrate companies and businesses at appropriate prices and realize anticipated cost savings.

Risks related to acquisition financing.

We may need to finance acquisitions by using shares of common stock for a portion or all of the consideration to be paid. In the event that the common stock does not maintain a sufficient market value, or potential acquisition candidates are otherwise unwilling to accept common stock as part of the consideration for the sale of their businesses, we may be required to use more of our cash resources, if available, to maintain our acquisition program. These cash resources may include borrowings under our existing credit agreements or equity or debt financings. Our current credit agreements with lenders contain certain restrictions that could adversely

14

affect our ability to implement and finance potential acquisitions. Such restrictions include provisions which limit our ability to merge or consolidate with, or acquire all or a substantial part of the properties or capital stock of, other entities without the prior written consent of the lenders. There can be no assurance that we will be able to obtain the lenders’ consent to any of our proposed acquisitions. If we do not have sufficient cash resources, our growth could be limited unless we are able to obtain additional capital through debt or equity financings.

Our failure to comply with financial covenants of our credit facilities may adversely affect our results of operations and our financial conditions.

Our credit facilities require the Company to comply with certain specified covenants, restrictions, financial ratios and other financial and operating tests. The Company’s ability to comply with any of the foregoing restrictions will depend on its future performance, which will be subject to prevailing economic conditions and other factors, including factors beyond the Company’s control. A failure to comply with any of these obligations could result in an event of default under the credit facilities, which could permit acceleration of the Company’s indebtedness under the credit facilities. The Company from time to time has been unable to comply with some of the financial covenants contained in previous credit facilities (relating to, among other things, the maintenance of prescribed financial ratios) and has, when necessary, obtained waivers or amendments to the covenants from its lenders. In the future the Company may not be able to comply with the covenants or, if is not able to do so, that its lenders will be willing to waive such non-compliance or amend such covenants.

We may not be able to refinance on favorable terms or may not refinance, extend or repay our debt, which could adversely affect our results of operations or may result in default of our debt.

We may not be able to refinance existing debt or the terms of any refinancing may not be as favorable as the terms of our existing debt. If principal payments due upon default or at maturity cannot be refinanced, extended or repaid with proceeds from other sources, such as new equity capital, our cash flow may not be sufficient to repay all maturing debt in years when significant payments come due. If such circumstance happens, our business, reputation, results of operations or financial condition could be adversely affected and our existing debt could be in default.

Goodwill and intangible assets recorded as a result of our acquisitions could become impaired.

Goodwill represents the difference between the purchase price of acquired companies and the related fair values of net assets acquired. We test goodwill for impairment annually and whenever events or changes in circumstances indicate that impairment may have occurred. Goodwill and intangibles represent a significant amount of our total assets. As of December 31, 2019, our combined goodwill and intangible assets amounted to $246.6 million, net of accumulated amortization. To the extent we do not generate sufficient cash flows to recover the net amount of any investments in goodwill and other intangible assets recorded, the investment could be considered impaired and subject to write-off which would directly impact earnings. We expect to record additional goodwill and other intangible assets as a result of future business acquisitions. Future amortization of such other intangible assets or impairments, if any, of goodwill or intangible assets would adversely affect our results of operations in any given period.

15

Interruptions in the proper functioning of our information systems could disrupt operations and cause increases in costs and/or decreases in revenues.

The proper functioning of DXP’s information systems is critical to the successful operation of our business. Our information systems are vulnerable to natural disasters, power losses, telecommunication failures and other problems despite the protection of our information systems through physical and software safeguards and remote processing capabilities. If critical information systems fail or are otherwise unavailable, DXP’s ability to procure products to sell, process and ship customer orders, identify business opportunities, maintain proper levels of inventories, collect accounts receivable and pay accounts payable and expenses could be adversely affected.

Risks associated with insurance.

In the ordinary course of business we at times may become the subject of various claims, lawsuits or administrative proceedings seeking damages or other remedies concerning our commercial operations, the products we distribute, employees and other matters, including potential claims by individuals alleging exposure to hazardous materials as a result of the products we distribute or our operations. Some of these claims may relate to the activities of businesses that we have acquired, even though these activities may have occurred prior to acquisition. The products we distribute, and/or manufacture, are subject to inherent risks that could result in personal injury, property damage, pollution, death or loss of production.

We maintain insurance to cover potential losses, and we are subject to various deductibles and caps under our insurance. It is possible, however, that judgments could be rendered against us in cases in which we would be uninsured and beyond the amounts that we currently have reserved or anticipate incurring for such matters. Even a partially uninsured claim, if successful and of significant size, could have a material adverse effect on our business, results of operations and financial condition. Furthermore, we may not be able to continue to obtain insurance on commercially reasonable terms in the future, and we may incur losses from interruption of our business that exceed our insurance coverage. In cases where we maintain insurance coverage, our insurers may raise various objections and exceptions to coverage which could make uncertain the timing and amount of any possible insurance recovery.

Risks associated with cyber-security.

Through our sales channels and electronic communications with customers generally, we collect and maintain confidential information that customers provide to us in order to purchase products or services. We also acquire and retain information about suppliers and employees in the normal course of business. Computer hackers may attempt to penetrate our information systems or our vendors' information systems and, if successful, misappropriate confidential customer, supplier, employee or other business information. In addition, one of our employees, contractors or other third party may attempt to circumvent security measures in order to obtain such information or inadvertently cause a breach involving such information. Loss of information could expose us to claims from customers, suppliers, financial institutions, regulators, payment card associations, employees and other persons, any of which could have an adverse effect on our financial condition and results of operations. We may not be able to adequately insure against cyber risks.

The nature of our manufactured products carries the possibility of significant product liability and warranty claims, which could harm our business and future results

Customers use some of our products, in particular manufactured pumps and pump packages, in potentially harmful and high-risk applications that may in some instances can cause personal injury or loss of life and/or damage to property, equipment or the environment. In addition, our products are integral to the production process for some end-users, and a failure of our products could result in a business interruption of their operations. Although we maintain quality controls and procedures, our products may not be completely free from defects and/or malfunction or failure. We maintain various levels and types of insurance coverage that we believe are adequate and commensurate with normal industry practice for a company of our risk profile, relative size, and we further limit our liability by contract wherever possible. However, as described earlier, insurance may not be available or adequate to cover all potential liability. We could be named as a defendant in product liability or other lawsuits asserting potentially large claims if an accident occurs at a location where our equipment is installed or services have been or are being used.

ITEM 1B. Unresolved Staff Comments

None.

16

ITEM 2. Properties

We own seven of our facilities while the remainder of our facilities are leased. At December 31, 2019, we had approximately 155 facilities which contained 141 services centers, 4 distribution centers and 10 fabrication facilities.

At December 31, 2019, the Service Centers segment operated out of 141 service center facilities. Of these facilities, 112 were located in the U.S. in 35 states, 28 were located in nine Canadian provinces and one was located in Dubai. All of the distribution centers were located in the U.S., specifically in Texas, Montana and Nebraska. At December 31, 2019, the Innovative Pumping Solutions segment operated out of 10 fabrication facilities located in two states in the U.S. and two provinces in Canada. At December 31, 2019, the Supply Chain Services segment operated supply chain installations in 89 of our customers’ facilities in 26 U.S. states and one in Canada.

At December 31, 2019, our owned facilities ranged from 5,000 square feet to 45,000 square feet in size. We leased facilities for terms generally ranging from one to fifteen years. The leased facilities ranged from approximately 570 square feet to 105,000 square feet in size. The leases provide for periodic specified rental payments and certain leases are renewable at our option. We believe that our facilities are suitable and adequate for the needs of our existing business. We believe that if the leases for any of our facilities were not renewed, other suitable facilities could be leased with no material adverse effect on our business, financial condition or results of operations.

ITEM 3. Legal Proceedings

From time to time, the Company is a party to various legal proceedings arising in the ordinary course of business. While DXP is unable to predict the outcome of these lawsuits, it believes that the ultimate resolution will not have, either individually or in the aggregate, a material adverse effect on DXP’s business, consolidated financial position, cash flows, or results of operations.

ITEM 4. Mine Safety Disclosures

Not applicable.

17

PART II

ITEM 5. Market for the Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities

Our common stock trades on The NASDAQ Global Select Market under the stock ticker symbol "DXPE".

On February 28, 2020, we had approximately registered 367 holders of record for outstanding shares of our common stock. This number does not include shareholders for whom shares are held in “nominee” or “street name”. We do not anticipate paying cash dividends on our common stock in the foreseeable future. The payment of any future dividends will be at the discretion of our Board of Directors and will depend upon, among other things, future earnings, the success of our business activities, regulatory and capital requirements, lenders, and general financial and business conditions.

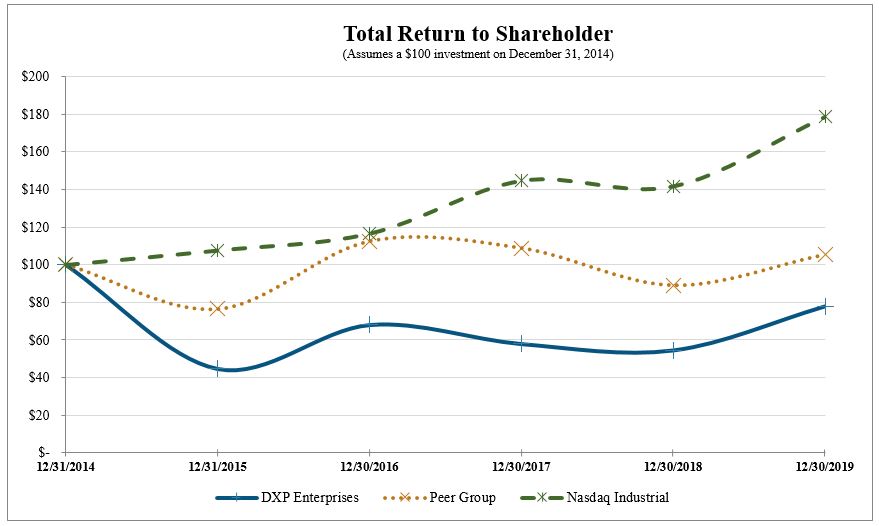

Stock Performance

The following performance graph compares the performance of DXP’s common stock to the NASDAQ Industrial Index and a customized peer group of three companies that includes: NOW Inc., MRC Global Inc. and Applied Industrial Technologies Inc. The graph assumes that the value of the investment in DXP’s common stock and in each index was $100 at December 31, 2014 and that all dividends were reinvested.

Investors are cautioned against drawing conclusions from the data contained in the graph below as past results are not necessarily indicative of future performance.

18

Equity Compensation Table

The following table provides information regarding shares covered by the Company’s equity compensation plans as of December 31, 2019:

Plan category | Number of Securities to be issued upon exercise of outstanding options | Weighted average exercise price of outstanding options | Non-vested restricted shares outstanding | Weighted average grant price | Number of securities remaining available for future issuance under equity compensation plans | |||||||||||

Equity compensation plans approved by shareholders | N/A | N/A | 144,250 | $ | 32.71 | 697,797 | (1) | |||||||||

Equity compensation plans not approved by shareholders | N/A | N/A | N/A | N/A | N/A | |||||||||||

Total | N/A | N/A | 144,250 | $ | 32.71 | 697,797 | (1) | |||||||||

(1)Represents shares of common stock authorized for issuance under the 2016 Omnibus Incentive Plan. | ||||||||||||||||

Unregistered Shares

DXP issued 30,305 unregistered shares of DXP’s common stock as part of the consideration for the January 1, 2018 acquisition of ASI. The unregistered shares were issued to the sellers of ASI.

We relied on Section 4(a)(2) of the Securities Exchange Act as a basis for exemption from registration. All issuances were as a result of private negotiation, and not pursuant to public solicitation. In addition, we believe the shares were issued to “accredited investors” as defined by Rule 501 of the Securities Act.

Repurchases of Common Stock

During 2019, 2018 and 2017 the Company withheld 7,760, 12,122 and 30,500 shares, respectively, to satisfy tax withholding obligations in connection with vesting of employee equity awards.

ITEM 6. Selected Financial Data

The selected historical consolidated financial data set forth below for each of the years in the five-year period ended December 31, 2019 has been derived from our audited Consolidated Financial Statements. This information should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the Consolidated Financial Statements and notes thereto included elsewhere in this Report.

19

Years Ended December 31 | ||||||||||||||||||

2019 | 2018 | 2017 | 2016 | 2015(1) | ||||||||||||||

(in thousands, except per share amounts) | ||||||||||||||||||

Consolidated Statements of Earnings Data: | ||||||||||||||||||

Sales | $ | 1,267,189 | $ | 1,216,197 | $ | 1,006,782 | $ | 962,092 | $ | 1,247,043 | ||||||||

Gross Profit | 347,224 | 332,208 | 271,581 | 264,802 | 351,986 | |||||||||||||

Operating income (loss) | 66,122 | 68,451 | 33,490 | 19,332 | (27,916 | ) | ||||||||||||

Net income (loss) | 35,775 | 35,521 | 16,529 | 7,151 | (39,070 | ) | ||||||||||||

Net loss attributable to non-controlling interest | (260 | ) | (111 | ) | (359 | ) | (551 | ) | (534 | ) | ||||||||

Net income (loss) attributable to DXP | $ | 36,035 | $ | 35,632 | $ | 16,888 | $ | 7,702 | $ | (38,536 | ) | |||||||

Earnings per share: | ||||||||||||||||||

Basic earnings (loss)(2) | $ | 2.04 | $ | 2.02 | $ | 0.97 | $ | 0.51 | $ | (2.68 | ) | |||||||

Diluted earnings (loss)(2) | $ | 1.96 | $ | 1.94 | $ | 0.93 | $ | 0.49 | $ | (2.68 | ) | |||||||

(1)The impairment expense in 2015, reduced operating income by $68.7 million, increased the net loss by $58.4 million, and

increased basic and diluted loss per share by $4.05.

(2) See Note 13 - Earnings per Share Data of the Notes to Consolidated Financial Statements for the calculation of basic and

diluted earnings per share.

Years Ended December 31 | |||||||||||||||||||

2019 | 2018 | 2017 | 2016 | 2015 | |||||||||||||||

(in thousands) | |||||||||||||||||||

Consolidated Balance Sheet Data: | |||||||||||||||||||

Cash(1) | $ | 54,327 | $ | 40,519 | $ | 25,579 | $ | 1,590 | $ | 1,693 | |||||||||

Net Working Capital (2) | 208,483 | 205,201 | 170,892 | 140,430 | 166,667 | ||||||||||||||

Total Assets | 788,220 | 699,962 | 639,083 | 602,052 | 674,984 | ||||||||||||||

Long-term Debt Obligations | 241,875 | 245,309 | 248,716 | 174,323 | 300,726 | ||||||||||||||

Total Shareholders’ Equity | $ | 344,948 | $ | 308,254 | $ | 268,546 | $ | 252,549 | $ | 198,870 | |||||||||

(1) Cash includes cash and cash equivalents plus restricted cash

(2) Net Working Capital equals current assets minus current liabilities excluding cash and short-term debt

ITEM 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis should be read in conjunction with the Consolidated Financial Statements and related notes contained within Item 8, Financial Statements and Supplementary Data and the other financial information found elsewhere in this Report. Management’s Discussion and Analysis uses forward-looking statements that involve certain risks and uncertainties as described previously in our Disclosure Regarding Forward-looking Statements and Item 1A. Risk Factors.

General Overview

DXP's products are marketed in the United States, Canada and Dubai to customers that are engaged in a variety of industries, many of which may be countercyclical to each other. Demand for our products generally is subject to changes in the United States and Canada, and global and macro-economic trends affecting our customers and the industries in which they compete in particular. Certain of these industries, such as the oil and gas industry, are subject to volatility driven by a variety of factors, while others, such as the petrochemical industry and the construction industry, are cyclical and materially affected by changes in the United States and global economy. As a result, we may experience changes in demand within particular markets, segments and product categories as changes occur in our customers' respective markets.

20

Operating Environment Overview* | ||||||||||||

2019 | 2018 | 2017 | ||||||||||

Active Drilling Rigs** | ||||||||||||

U.S | 944 | 1,032 | 875 | |||||||||

Canada | 135 | 191 | 207 | |||||||||

International | 1,098 | 988 | 948 | |||||||||

Worldwide | 2,177 | 2,211 | 2,030 | |||||||||

Gross Domestic Product (in billions) | $ | 21,429.0 | $ | 20,500.6 | $ | 19,485.4 | ||||||

West Texas Intermediate ** (per barrel) | $ | 56.98 | $ | 65.23 | $ | 50.80 | ||||||

Purchasing Managers Index | 47.2 | 54.3 | 59.3 | |||||||||

* The information contained in this table has been obtained from third party publicly available sources.

** Averages for the years indicated.