UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended | |||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 1-12297

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices) | (Zip Code) | ||||

(248 ) 648-2500

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated filer o | Non-accelerated filer o | Smaller reporting company | |||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

The aggregate market value of the voting common stock held by non-affiliates as of June 28, 2024 (the last trading day of the registrant's second fiscal quarter), was $2,759,410,642 . As of February 11, 2025, there were 66,749,222 shares of voting common stock outstanding.

Documents Incorporated by Reference

Certain portions, as expressly described in this report, of the registrant's proxy statement for the 2025 Annual Meeting of the Stockholders to be held May 14, 2025, are incorporated by reference into Part III, Items 10-14.

TABLE OF CONTENTS

| Item | Page | |||||||

PART I

Item 1. Business

We are a diversified international transportation services company and one of the world's premier automotive and commercial truck retailers. We operate dealerships in the United States, the United Kingdom, Canada, Germany, Italy, Japan, and Australia, and we are one of the largest retailers of commercial trucks in North America for Freightliner. We also distribute and retail commercial vehicles, diesel and gas engines, power systems, and related parts and services principally in Australia and New Zealand. We employ over 28,900 people worldwide. Additionally, we own 28.9% of Penske Transportation Solutions, a business that employs over 44,500 people worldwide, manages one of the largest, most comprehensive and modern trucking fleets in North America with over 435,000 trucks, tractors, and trailers under lease, rental, and/or maintenance contracts, and provides innovative transportation, supply chain, and technology solutions to its customers.

Business Overview

In 2024, our business generated $30.5 billion in total revenue, which is comprised of approximately $26.2 billion from retail automotive dealerships, $3.5 billion from retail commercial truck dealerships, and $777.9 million from commercial vehicle distribution and other operations. We generated $5.0 billion in gross profit, which is comprised of $4.3 billion from retail automotive dealerships, $584.5 million from retail commercial truck dealerships, and $178.2 million from commercial vehicle distribution and other operations.

Retail Automotive. We are one of the largest global automotive retailers as measured by the $26.2 billion in total retail automotive dealership revenue we generated in 2024. We are diversified geographically with 56% of our total retail automotive dealership revenues in 2024 generated in the U.S. and Puerto Rico and 44% generated outside of the U.S. We offer over 40 vehicle brands with 72% of our retail automotive franchised dealership revenue in 2024 generated from premium brands, such as Audi, BMW, Land Rover, Mercedes-Benz, and Porsche. As of December 31, 2024, we operated 353 retail automotive franchised dealerships, of which 148 are located in the U.S. and 205 are located outside of the U.S., principally in the U.K. As of December 31, 2024, we also operated 16 used vehicle dealerships, with six dealerships in the U.S. operating under the brand name CarShop, nine dealerships in the U.K. operating under the brand name Sytner Select, and one dealership in Australia operating under the brand name Penske Select. We retailed and wholesaled, including agency units, more than 594,000 vehicles in 2024.

In addition to selling new and used vehicles, we generate higher-margin revenue at each of our dealerships through maintenance and repair services, the sale and placement of third-party finance and insurance products, third-party extended service and maintenance contracts, replacement and aftermarket automotive products, and at certain of our locations, collision repair services. We operate our franchised dealerships under franchise agreements with a number of automotive manufacturers and distributors that are subject to certain rights and restrictions typical of the industry. Some of our dealerships in the U.K. and Europe operate under an agency model where we receive a fee for facilitating the sale by the manufacturer of a new vehicle but do not hold the vehicle in inventory. Vehicles sold under this agency model are counted as new agency units sold instead of new retail units sold by us, and only the fee we receive from the manufacturer, not the price of the vehicle, is reported as new revenue with no corresponding cost of sale.

We believe our diversified retail automotive income streams help to mitigate the historical cyclicality found in some elements of the automotive sector. Revenues from higher margin service and parts sales include warranty work, customer-paid work, rapid repair, collision repair services, and wholesale parts sales. Service and parts sales are typically less cyclical than retail vehicle sales and generate the largest part of our retail automotive gross profit.

1

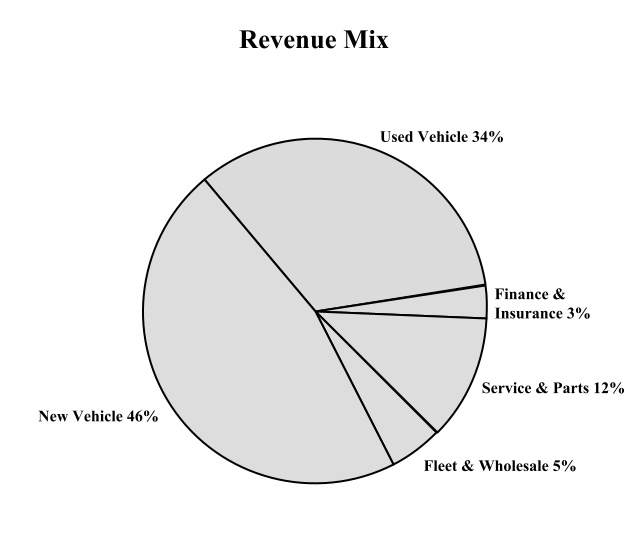

The following graphics show the percentage of our total retail automotive dealership revenues by product type and their respective contribution to our retail automotive gross profit:

Retail Commercial Truck Dealership. We operate Premier Truck Group ("PTG"), a heavy- and medium-duty truck dealership group offering primarily Freightliner and Western Star trucks (both Daimler brands), with locations across 10 U.S. states and the Canadian provinces of Ontario and Manitoba. As of December 31, 2024, PTG operated 45 locations selling new and/or used trucks, performing service and parts operations, or offering collision repair services. We retailed and wholesaled 20,947 new and used trucks in 2024. These businesses represented 11.6% of our total revenues and 11.7% of our total gross profit in 2024.

While our retail commercial truck business benefits from diversified income streams similar to those of the retail automotive sector, there are several key differences. As exhibited in the following charts, a greater part of our gross profit is derived from the sale of service and parts in the retail truck business given the large volume of parts business, in many cases, to fleet customers. In addition, the commercial truck business has a historically lower selling, general, and administrative expense as a percentage of gross profit as compared to retail automotive as approximately 65% of PTG's gross profit is attributable to higher margin service and parts compared to retail automotive which is approximately 42%. The following graphics show the percentage of our total retail commercial truck dealership revenues by product type and their respective contribution to our retail commercial truck gross profit:

Penske Australia. Penske Australia is the exclusive importer and distributor of Western Star heavy-duty trucks (a Daimler brand), MAN heavy- and medium-duty trucks and buses (a VW Group brand), and Dennis Eagle refuse collection

2

vehicles, together with associated parts, across Australia, New Zealand, and portions of the Pacific. In most of these same markets, we are also a leading distributor of diesel and gas engines and power systems, principally representing MTU (a Rolls-Royce solution), Detroit Diesel, Allison Transmission, and Bergen Engines. Penske Australia offers products across the on- and off-highway markets, including in the trucking, mining, power generation, energy solutions, defense, marine, rail, and construction sectors and supports full parts and aftersales service through a network of branches, field service locations, and dealers across the region. These businesses represented 2.5% of our total revenues and 3.5% of our total gross profit in 2024.

Penske Transportation Solutions. We hold a 28.9% ownership interest in Penske Truck Leasing Co., L.P. ("PTL"). PTL is owned 41.1% by Penske Corporation, 28.9% by us, and 30.0% by Mitsui & Co., Ltd. ("Mitsui"). We account for our investment in PTL under the equity method, and we therefore record our share of PTL's earnings on our statements of income under the caption "Equity in earnings of affiliates," which also includes the results of our other equity method investments. Penske Transportation Solutions ("PTS") is the universal brand name for PTS' various businesses, which articulates the breadth of its services. Its business was founded over 50 years ago, and today it is a leading provider of transportation and supply chain services. PTS is capable of meeting customers' needs across the supply chain with a broad product offering that includes full-service truck leasing, truck rental, and contract maintenance along with logistics services, such as dedicated contract carriage, distribution center management, freight management, and dry van truckload carrier services. We recorded $198.0 million and $289.5 million in equity earnings from this investment in 2024 and 2023, respectively, and during 2024 and 2023, we received $98.4 million and $168.8 million, respectively, of pro rata cash distributions relating to this investment.

Outlook

Retail Automotive. During 2024, U.S. industry new light vehicle sales increased 2.5%, to 16.0 million units, including a 3.0% increase in retail sales, partially offset by a 2.5% decrease in fleet sales, as compared to 2023. U.K. new vehicle registrations increased 2.6% to 2.0 million registrations, including an 11.8% increase in fleet sales, partially offset by an 8.7% decrease in retail sales, as compared to 2023. New vehicle sales are being positively impacted by continued strong consumer demand in the U.S. and manufacturer incentives. Government incentives on electric vehicles ("EVs") also impact vehicle sales. Our new vehicle days' supply is 49 as of December 31, 2024, compared to 39 as of December 31, 2023, including vehicles which are unable to be sold due to open recalls. Our used vehicle days' supply is 47 as of December 31, 2024, compared to 48 as of December 31, 2023, and is being impacted by a lower supply of 1-4 year old used vehicles as a result of the lower number of new vehicles sold in recent years and fewer lease returns in the U.S. As a reference, our new and used days' supply was 71 and 52, respectively, as of December 31, 2019 (pre-COVID). According to the National Automobile Dealers Association, sales for the U.S. light vehicle market are expected to grow to 16.2 million units in 2025 compared to a 16.0 million market in 2024.

As the supply of new vehicles has improved, we have experienced, and may continue to experience, reduced new and used vehicle gross profit. The regulatory authorities in our markets have adopted emissions limits on new vehicles which are designed to incent adoption of electric or other zero-emissions vehicles. We believe there is a direct correlation between the availability of government incentives for EVs and EV sale levels. New vehicle sales levels could be impacted by changes to these regulatory mandates as well as vehicle affordability challenges, inflation, interest rates, or a reduction in consumer spending resulting in decreased demand. The unavailability of 1-4 year old quality, low-mileage used vehicles for sale may adversely impact our used vehicle operations.

Representatives of the U.K. government have proposed a ban on the sale of internal combustion engines in new cars and new vans that may take effect as early as 2030 while also providing government incentives on certain EVs to entice consumers to transition from internal combustion vehicles to EVs. In part due to these incentives, U.K. new registrations of EVs, excluding hybrid, represented 19.6% of the overall market during 2024, as compared to 16.5% during 2023, and represented 24.3% of our U.K. new unit sales, as compared to 22.4% during 2023. U.K. new registrations of hybrid vehicles represented 21.9% of the overall market during 2024, as compared to 20.0% during 2023, and represented 13.2% of our U.K. new unit sales, as compared to 11.9% during 2023. In the U.S., sales of EVs increased 7.3% to 1.3 million units as compared to 2023. EV sales (excluding hybrid) represented 8.1% of the overall U.S. market during 2024, as compared to 7.7% during 2023. In the U.S., sales of hybrid vehicles were 1.9 million units in 2024 as compared to 1.2 million units in 2023. EV sales may increase or decrease in our markets as a result of government policy, manufacturer incentives, and consumer acceptance of vehicle range or vehicle charging infrastructure. During 2024, 4.2% of new vehicle sales in the U.S., and 2.6% of the new vehicle sales in the U.K., were sold by vehicle manufacturers directly to consumers outside of the retail automotive franchised system, principally consisting of one manufacturer. We expect continued strong demand for our service and parts operations driven by increases in demand in light of increasing vehicle sales in recent years, recall campaigns, increased miles driven, and vehicle complexity.

3

Retail Commercial Truck Dealership. During 2024, North American sales of Class 6-8 medium- and heavy-duty trucks, the vehicles sold by our PTG business, decreased 3.0% from last year to 473,159 units, primarily due to increased deliveries in 2023 as a result of deliveries expected in 2022 being delayed into 2023 due to supply constraints as well as continued lower freight rates in the U.S. The Class 6-7 medium-duty truck market increased 0.5% from last year to 157,260 units, and Class 8 heavy-duty trucks, the largest North American market, decreased 4.7% from last year to 315,899 units. We expect replacement demand to continue in 2025, although a continued weak freight market may impact unit sales and service and parts demand. As of December 31, 2024, the Class 6-8 medium- and heavy-duty truck backlog is 213,366 units according to data published by ACT Research compared to 278,616 as of December 31, 2023. See Item 1. Business, "Retail Commercial Truck Dealership Operations."

Commercial Vehicle Distribution and Other. During 2024, the Australian heavy-duty truck market reported sales of 17,153 units, representing a decrease of 2.4% from last year, while the New Zealand market reported sales of 3,439 units, representing a decrease of 13.7% from the same period last year. Our power system operations continue to grow through sales in the off-highway segments such as energy solutions, which provide power systems for large data centers, mining, and military applications.

Penske Transportation Solutions. A majority of PTS' revenue is generated by multi-year contracts for full-service leasing, contract maintenance, and logistics services. PTS also rents additional trucks to commercial customers in response to demand for freight as well as consumer customers. With a managed fleet of over 435,000 vehicles at December 31, 2024, PTS regularly sells trucks in order to maintain a low fleet age as well as in response to changes in demand for truck leasing and records a gain or loss on those sales. PTS is currently experiencing positive revenue growth in its business despite adverse global economic freight conditions. This growth is being driven by its full-service leasing, contract maintenance and logistics businesses, partially offset by lower revenues in its commercial and consumer rental product lines. The weaker freight environment and higher interest rates have directly impacted demand for its transactional products as well as used vehicle pricing. PTS has decreased, and expects to continue to decrease, the size of its consumer and commercial rental fleets in connection with this lower demand, aimed at improving the utilization rate of the fleet. PTS further anticipates that these market conditions will continue through 2025, and possibly longer, before improving. Additionally, increased market interest rates compared to prior years have resulted in meaningful increases to its interest expense, both in its variable rate indebtedness and as it refinances existing fixed rate indebtedness, while lower average selling prices for used trucks has resulted in a meaningful decrease in gain on sale from remarketing activities.

As described in Item 1A. Risk Factors, there are a number of factors that could cause actual results to differ materially from our expectations. For a detailed discussion of our financial and operating results, see Part II, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

Diversification

Our business benefits from a diversified revenue and gross profit mix, including multiple revenue and gross profit streams in our traditional vehicle and commercial truck dealerships (new vehicles, used vehicles, finance and insurance, and service and parts operations) across many geographies, our commercial vehicle distribution and power systems operations, and returns relating to our joint venture investments, which we believe helps to mitigate the cyclicality that has historically impacted some elements of the automotive sector. Furthermore, PTG provides diversification both by business line and by its business being represented across the U.S. and in Canada. Finally, our ownership interest in PTS provides us with additional diversification as well as equity earnings, cash dividends, and significant cash savings on taxes.

We are also diversified geographically as established by the following table, which shows our consolidated revenue and gross profit by country as a percentage of our total revenue and total gross profit:

| Country | % of Total 2024 Revenue | % of Total 2024 Gross Profit | ||||||||||||

| United States | 58 | % | 61 | % | ||||||||||

| United Kingdom | 31 | % | 27 | % | ||||||||||

| Germany/Italy | 5 | % | 5 | % | ||||||||||

| Japan | 1 | % | 1 | % | ||||||||||

| Canada | 2 | % | 2 | % | ||||||||||

| Australia/New Zealand | 3 | % | 4 | % | ||||||||||

4

We are also diversified within our automotive retail operations by brand. We represent over 40 brands in our markets and our automotive dealership revenue mix consists of 72% related to premium brands, 21% related to volume non-U.S. brands, 2% related to brands of U.S. based manufacturers, and 5% related to our used vehicle dealerships as further detailed in the chart below:

Corporate Responsibility

As a leading international, diversified transportation services company, we recognize it is our responsibility to ensure that we contribute to a healthy environment, economic opportunity, and social equity in the communities where we operate around the world. We recognize we are accountable to key stakeholders and the communities in which we do business. We are committed to responsible business practices, continuous improvement of our operations, and strengthening relationships with our stakeholders. We focus our efforts where we can have the most positive impact on our business and society and are driven by our core values that ensures we enrich our communities, manage our environmental impact, protect the health and safety of our team members and customers, and promote opportunities for our personnel – all while creating value for our stakeholders. The most important investments we make are in our people. Everything we aspire to be as a company builds on our ability to come together as one team.

5

Retail Automotive Dealership Operations

Retail Automotive Franchises. We routinely acquire and dispose of retail automotive franchises. The following table exhibits our retail automotive franchises by location and manufacturer as of December 31, 2024:

| Location | Franchises | Franchises | U.S. | Non-U.S. | Total | |||||||||||||||||||||||||||

| Arizona | 24 | BMW/MINI | 26 | 66 | 92 | |||||||||||||||||||||||||||

| Arkansas | 4 | Toyota/Lexus | 23 | — | 23 | |||||||||||||||||||||||||||

| California | 30 | Mercedes-Benz/Sprinter/smart | 18 | 29 | 47 | |||||||||||||||||||||||||||

| Connecticut | 8 | Audi/Volkswagen/Bentley | 17 | 35 | 52 | |||||||||||||||||||||||||||

| Florida | 3 | Chrysler/Jeep/Dodge/Ram | 4 | — | 4 | |||||||||||||||||||||||||||

| Georgia | 4 | Honda/Acura | 19 | — | 19 | |||||||||||||||||||||||||||

| Indiana | 4 | Ferrari/Maserati | 2 | 12 | 14 | |||||||||||||||||||||||||||

| Maryland | 1 | Porsche | 10 | 15 | 25 | |||||||||||||||||||||||||||

| Massachusetts | 5 | Jaguar/Land Rover | 7 | 19 | 26 | |||||||||||||||||||||||||||

| Michigan | 2 | Lamborghini | 1 | 5 | 6 | |||||||||||||||||||||||||||

| Minnesota | 2 | Nissan/Infiniti | 3 | — | 3 | |||||||||||||||||||||||||||

| New Jersey | 18 | Cadillac/Chevrolet | 4 | — | 4 | |||||||||||||||||||||||||||

| North Carolina | 4 | Others | 14 | 24 | 38 | |||||||||||||||||||||||||||

| Ohio | 7 | Total | 148 | 205 | 353 | |||||||||||||||||||||||||||

| Puerto Rico | 4 | |||||||||||||||||||||||||||||||

| Rhode Island | 8 | |||||||||||||||||||||||||||||||

| Tennessee | 1 | |||||||||||||||||||||||||||||||

| Texas | 11 | |||||||||||||||||||||||||||||||

| Virginia | 7 | |||||||||||||||||||||||||||||||

| Wisconsin | 1 | |||||||||||||||||||||||||||||||

| Total U.S. | 148 | |||||||||||||||||||||||||||||||

| U.K. | 141 | |||||||||||||||||||||||||||||||

| Germany | 23 | |||||||||||||||||||||||||||||||

| Italy | 26 | |||||||||||||||||||||||||||||||

| Japan | 12 | |||||||||||||||||||||||||||||||

| Australia | 3 | |||||||||||||||||||||||||||||||

| Total Non-U.S. | 205 | |||||||||||||||||||||||||||||||

| Total Worldwide | 353 | |||||||||||||||||||||||||||||||

Retail Automotive Used Vehicle Dealerships. The following table exhibits our used vehicle dealerships we operated by geographic location as of December 31, 2024:

| Location | Number of Dealerships | |||||||

| U.S. (CarShop) | ||||||||

| Pennsylvania | 5 | |||||||

| New Jersey | 1 | |||||||

| Total U.S. | 6 | |||||||

| U.K. (Sytner Select) | 9 | |||||||

| Australia (Penske Select) | 1 | |||||||

| Total | 16 | |||||||

New Vehicle Retail Sales. In 2024, we retailed, including agency units, more than 244,990 new vehicles which generated 46.1% of our retail automotive dealership revenue and 27.0% of our retail automotive dealership gross profit. We strive to maintain outstanding relationships with the automotive manufacturers based in part on our long-term presence

6

in the retail automotive market, our commitment to providing premium facilities, our commitment to drive customer satisfaction, the reputation of our management team, and the consistent sales volume at our dealerships. Our dealerships finance the purchase of most new vehicles from the manufacturers through floor plan financing provided primarily by various manufacturers' captive finance companies.

Used Vehicle Retail Sales. In 2024, we retailed 246,608 used vehicles, which generated 33.5% of our retail automotive dealership revenue and 10.7% of our retail automotive dealership gross profit. We acquire used vehicles from various sources, including trade-ins from consumers in connection with their purchase of a new or used vehicle from us, purchases of used vehicles directly from consumers, lease expirations, public auctions, and auctions open only to authorized new vehicle dealers. To improve customer confidence in our used vehicle inventory, we provide vehicle history reports for all used vehicles, and virtually all of our franchised new vehicle dealerships participate in manufacturer certification processes for used vehicles. If certification is obtained, the used vehicle owner is typically provided benefits and warranties similar to those offered to new vehicle owners by the applicable manufacturer.

Vehicle Finance and Insurance Sales. Finance and insurance sales represented 3.1% of our retail automotive dealership revenue and 19.1% of our retail automotive dealership gross profit in 2024. At our customers' option, our dealerships can arrange third-party financing or leasing in connection with vehicle purchases. We typically receive a flat fee or a portion of the cost of the financing or leasing paid by the customer for each transaction. While these services are generally non-recourse to us, we are subject to chargebacks in certain circumstances, such as default under a financing arrangement or pre-payment. These chargebacks vary by finance product but typically are limited to the fee we receive.

We also offer our customers various vehicle warranty and extended protection products, including extended service contracts, maintenance programs, and voluntary vehicle protection products. The extended service contracts and other products that our dealerships currently offer to customers are underwritten by independent third parties, including the vehicle manufacturers' captive finance companies. Similar to finance transactions, we are subject to chargebacks relating to fees earned in connection with the sale of certain protection products. We also offer for sale other aftermarket products, including security systems and protective coatings.

We offer finance and insurance products using a "menu" process, which is designed to ensure that we offer our customers a complete range of finance, insurance, protection, and other aftermarket products in a transparent manner. We utilize docuPAD® at our U.S. dealerships, an interactive electronic interface designed to improve document processing and menu presentation of finance and insurance options during the purchase or lease transaction.

Service and Parts Sales. Service and parts sales represented 11.7% of our retail automotive dealership revenue and 41.7% of our retail automotive dealership gross profit in 2024. We generate service and parts revenue in connection with providing a wide range of services such as vehicle maintenance, cosmetic repair, manufacturer recalls, warranty, out-of-warranty, rapid repair, and collision repair services. We also recondition used vehicles that we intend to sell in our dealerships. We look to generate higher revenue by driving higher levels of customer satisfaction, marketing, and the use of technology such as videos which allow our technicians to interact directly with the customer, obtain digital approvals, and increase efficiency. Additionally, our AI-driven service scheduling and reception system at certain of our dealerships enhances the customer experience by providing instant support, reducing wait times, and offering 24/7 assistance, enabling seamless service even outside regular hours. By accurately interpreting customer needs and automating appointment bookings, the system streamlines operations, allowing staff to focus on more complex tasks while providing customers with access to human support when necessary. We also believe our service and parts revenues benefit from the increasingly complex technology built into vehicles today. We believe this offers an advantage to our automotive dealerships as the complexity makes it increasingly difficult for independent repair shops and do-it-yourself enthusiasts to maintain and repair today’s vehicles, including the components and systems used in battery and hybrid EVs. We also offer rapid repair services, such as paintless dent repair, tire sales, and windshield replacement at most of our facilities in order to offer our customers the convenience of one-stop shopping for all of their automotive requirements.

We also operate 36 automotive collision repair centers, each of which is operated as an integral part of our dealership operations. The collision centers are staffed with factory-certified technicians with broad capabilities, extending to complete vehicle reconstruction and mechanical engine repairs. Our collision centers also carry an extensive inventory of parts for the new and used vehicles they repair.

Fleet and Wholesale Sales. Fleet and wholesale sales represented 5.6% of our retail automotive dealership revenue and 1.5% of our retail automotive dealership gross profit in 2024. Fleet activities represent the sale of new units to customers that are deemed to not be retail customers, such as cities, municipalities, or rental car companies and are generally sold at

7

contracted amounts. Wholesale activities relate to the sale of used vehicles generally to other dealers and occur at auction. In the U.K., we offer used vehicles to wholesalers and other dealers via a proprietary online auction.

Retail Commercial Truck Dealership Operations

Premier Truck Group (“PTG”) is a heavy- and medium-duty truck dealership group offering primarily Freightliner and Western Star trucks (both Daimler brands) with 45 locations across 10 U.S. states and the Canadian provinces of Ontario and Manitoba. PTG dealerships provide a similar suite of services as our automotive dealerships, offering new trucks and a large selection of used trucks for sale, a full range of parts, maintenance and repair services, collision centers, and finance and insurance options by facilitating truck and trailer financing and leasing, extended maintenance plans, voluntary vehicle protection products, and other programs.

The maintenance and repair of commercial trucks is an essential service and a key area of differentiation for our business. We offer “Elite Support” certified locations to help maximize vehicle uptime. Elite Support certified locations provide an express assessment whereby we communicate a primary diagnosis, check parts availability, and provide an estimate of cost and repair time within a few hours of service write-up. As part of this service, many of our locations offer a comfortable environment for customers with amenities such as customer lounges, lockers, showers, and laundry facilities. We also offer roadside remote service for certain repairs and provide 24/7 technician support for breakdown/emergency service in select locations.

The collision centers at PTG are full-service, heavy-duty paint and collision repair facilities with certified professionals that can handle everything from light cosmetic issues to complete vehicle reconstruction, including mechanical engine repairs. PTG also carries an extensive inventory of parts for the new and used trucks they sell and service. The service and parts business of our PTG commercial truck dealerships represents approximately 65% of our retail commercial truck dealership gross profit.

A significant portion of our new commercial vehicle sales are to customers with large fleets of commercial vehicles. Because of the size and geographic scope of our dealership locations, our strong relationships with our fleet customers and our ability to manage large quantities of used commercial vehicle trade-ins, we are able to successfully market and sell to large fleet customers. We believe that we have a competitive advantage over many dealerships because we can absorb multi-unit trade-ins often associated with fleet sales and effectively disperse the used commercial vehicles for resale throughout our dealership network. We believe that the broad range of products and services we offer to purchasers of commercial vehicles at the time of purchase and post-purchase results in a high level of customer loyalty.

Backlog is a key industry metric for commercial vehicle retailers. Backlog is the number of new commercial vehicles ordered by customers, however, such orders are subject to cancellation. In the event of order cancellation, retailers generally have no contractual right to require the customer to purchase the vehicle. The delivery time for a customer ordered commercial vehicle varies depending on the truck specifications and demand for the model ordered. We sell the majority of our new heavy-duty commercial vehicles by customer special order and we sell the majority of our medium duty commercial vehicles out of inventory. As of December 31, 2024, the Class 6-8 medium- and heavy-duty truck backlog is 213,366 units according to data published by ACT Research compared to 278,616 at December 31, 2023.

Fixed Absorption Ratio. We believe the fixed absorption ratio is useful to investors as it improves the transparency of our disclosures and provides a meaningful metric evidencing the impact of our commercial truck businesses' parts and service operations on PTG's overall operating profitability. Our fixed absorption ratio is calculated by dividing PTG's gross profit from our parts and service departments by PTG's total overhead expenses, except for the variable selling expenses of the new and used commercial vehicle departments, advertising expense, and carrying costs of new and used commercial vehicle inventory. Our commercial truck dealerships achieved a 125.0% fixed absorption ratio for 2024, compared to a 129.2% fixed absorption ratio for 2023.

Commercial Vehicle Distribution and Other Operations

Penske Australia. Penske Australia is the exclusive importer and distributor of Western Star heavy-duty trucks (a Daimler brand), MAN heavy- and medium-duty trucks and buses (a VW Group brand), and Dennis Eagle refuse collection vehicles, together with associated parts, across Australia, New Zealand, and portions of the Pacific. In most of these same markets, we are also a leading distributor of diesel and gas engines and power systems, principally representing MTU (a Rolls-Royce solution), Detroit Diesel, Allison Transmission, and Bergen Engines. Penske Australia offers products across the on- and off-highway markets, including in the trucking, mining, power generation, energy solutions, defense, marine, rail, and construction sectors and supports full parts and aftersales service through a network of branches, field service locations, and dealers across the region.

8

Penske Australia distributes commercial vehicles and parts for Western Star, MAN, and Dennis Eagle to a network which comprises on average of more than 70 dealership locations across Australia, New Zealand, and portions of the Pacific. Of these dealership locations, 12 are company-owned retail commercial vehicle and/or service and parts dealerships in Australia and three are company-owned retail commercial vehicle dealerships in New Zealand.

Western Star trucks are manufactured by Daimler Trucks North America in Portland, Oregon. These technologically advanced, custom-built vehicles are ordered by customers to meet their particular needs for line haul, long distance road train, mining, logging, and other heavy-duty applications. We are also the exclusive importer of MAN trucks and buses. MAN Truck and Bus, a VW Group company, is a leading producer of medium- and heavy-duty trucks as well as city and coach buses. These cab-forward, fuel efficient vehicles are principally produced in several sites in Germany and are ordered by customers for line haul, local distribution, mining, and other off-road applications. Dennis Eagle refuse collection vehicles are manufactured by Ros Roca in Warwick, England. These brands represented 4.1% of heavy-duty truck units sold in Australia and 2.0% in New Zealand during 2024.

We also distribute diesel gas engines and power systems to over 100 dealer locations that are strategically located throughout Australia, New Zealand, and portions of the Pacific. Most of the dealers represent the Detroit Diesel brand, with the majority aligned to Western Star and/or Freightliner truck manufacturers. The remaining dealers represent the MTU and Allison Transmission brands. The “off-highway” business principally includes the sale and servicing of power systems directly to customers in the commercial, defense, mining, maritime, power generation, and energy solutions sectors from 20 facilities we operate across Australia and New Zealand. We also utilize mobile remote field service units to travel directly to customer premises.

Penske Transportation Solutions

We hold a 28.9% ownership interest in Penske Truck Leasing Co., L.P. (“PTL”). Penske Transportation Solutions (“PTS”) is the universal brand name for PTL's various business lines through which it is capable of meeting customers' needs across the supply chain with a broad product offering that includes full-service truck leasing, truck rental, and contract maintenance along with logistics services, such as dedicated contract carriage, distribution center management, freight management, and dry van truckload carrier services. PTS has a highly diversified customer base ranging from multi-national corporations across industries, such as food and beverage, transportation, manufacturing, automotive, retail, and healthcare, with whom they have long-term contracts to individual consumers who rent a single truck on a daily basis.

PTS manages one of the largest, most comprehensive and modern trucking fleets in North America, with approximately 435,000 trucks, tractors and trailers under lease, rental and/or maintenance contracts as of December 31, 2024, through their network of locations throughout North America. Furthermore, PTS has consistently been among the largest purchasers of commercial trucks in North America and had an average full-service leasing Class 8 tractor fleet age of approximately 3.4 years as of December 31, 2024, which is substantially lower than the overall Class 8 tractor fleet age in the United States.

Full-service truck leasing, truck rental, and contract maintenance. Full-service truck leasing, truck rental, and contract maintenance of commercial trucks, tractors, and trailers constitutes PTS' largest business. PTS manages a fleet of over 435,000 trucks, tractors, and trailers, consisting of over 282,900 vehicles owned by PTS and leased to customers under full-service lease or rental agreements and over 152,300 customer-owned and -operated vehicles for which they provided contract maintenance services. Lease terms under its full-service leases generally range from four to seven years for tractors and trucks and six to twelve years for trailers. Its commercial and consumer rental fleet as of December 31, 2024, consisted of approximately 94,800 vehicles for use by its full-service truck leasing, small business, and consumer customers for periods generally ranging from less than a day to 12 months. Most of its leased vehicles are configured according to customer specifications, including custom painting and lettering, while its rental trucks bear Penske branding.

Commercial customers often outsource to PTS to reduce the complexity, cost, and total capital associated with vehicle ownership. Under a full-service lease, PTS provides and fully maintains the vehicle, which is generally configured for the customer. The services provided under full-service lease and contract maintenance agreements generally include preventive and regular maintenance, advanced diagnostics, emergency road service, fleet services, safety programs, and fuel services through PTS' network of company-operated facilities and a nationwide network of independent truck stops. In addition, PTS makes available to its full-service leasing and contract maintenance customers additional vehicles on a rental basis. PTS' commercial rental operations offer short-term availability of tractors, trucks, and trailers typically to accommodate seasonal, emergency, and other temporary needs. A significant portion of these rentals are to existing full-service leasing and contract maintenance customers who are seeking flexibility in their fleet management. PTS has established a network of approximately 930 locations to provide full-service truck leasing, truck rental, and contract maintenance services to

9

customers. This network enables PTS to meet multi-location customer requirements. PTS' commercial rental business generated 19% of its revenue for 2024 and its full-service lease and contract maintenance business generated 50% of its revenue in 2024.

For consumer customers, PTS provides short-term rental of light- and medium-duty vehicles on a one-way and local basis, typically to transport household goods. Customers typically include local small businesses and individuals seeking a do-it-yourself solution to their moving needs. PTS' consumer fleet generally consists of late model vehicles ranging in size from small vans to 26-foot trucks, and its consumer rentals are conducted through approximately 1,910 independent rental agents and approximately 410 of its company-operated leasing and rental facilities. PTS' consumer business generated 3% of its revenue for 2024.

Logistics. PTS' logistics business offers an extensive variety of services, including dedicated contract carriage, distribution center management, freight management, lead logistics provider, and dry van truckload carrier services. PTS coordinates services for its customers across the supply chain, including inbound material flow, handling and packaging, inventory management, distribution and technologies, and sourcing of third-party carriers. These services are available individually or on a combined basis and often involve its associates performing services at the customer's location. By offering a scalable series of services to its customers, PTS can manage the customer's entire supply chain or any stand-alone service. PTS also utilizes specialized software that enables real-time fleet visibility and provides reporting metrics, giving customers detailed information on fuel economy and other critical supply chain costs. PTS' international logistics business has approximately 520 locations in North America, South America, and Europe. PTS' logistics business generated 28% of its revenue for 2024.

Industry Information

Retail Automotive. Approximately 56% of our retail automotive dealership revenues are generated in the U.S. and Puerto Rico, which in 2024 was one of the world's largest automotive retail markets as measured by units sold. In 2024, sales of new cars and light trucks were approximately 16.0 million units, an increase of 2.5% from 2023, and were generated at approximately 16,900 franchised new-car dealerships. According to data from the National Automobile Dealers Association, dealership revenue is generally derived as follows: 54% from new vehicle sales, 33% from used vehicle sales (in each case including related finance and insurance revenues), and 13% from service and parts sales.

In the U.S., the franchised automotive dealer industry is one of the largest retail businesses by revenue in a market of approximately $1.2 trillion. Although significant consolidation has already taken place, the industry remains highly fragmented with approximately 90% of the U.S. industry's market share remaining in the hands of smaller regional and independent dealers. Our other markets are similarly fragmented. We believe that further consolidation in these markets is probable due to the significant capital requirements of maintaining manufacturer facility standards and the limited number of viable alternative exit strategies for dealership owners.

Our international automotive retail dealerships operate in the U.K., the European Union, Japan, and Australia. In the U.K., new vehicle registrations in 2024 totaled 1.95 million, which increased 2.6% from 1.90 million new vehicle registrations in 2023. Our European Union markets consist of Germany, Italy, and Spain, which represented the first, third, and fourth largest automotive retail markets, respectively, in the European Union in 2024 and accounted for approximately 51% of the total vehicle sales in the European Union markets. Unit sales of automobiles in the European Union were approximately 10.6 million in 2024, a 0.8% increase compared to 2023. In Germany, Italy, and Spain, new car sales were approximately 2.8 million, 1.6 million, and 1.0 million units, respectively, in 2024, new car sales in Japan were approximately 4.4 million in 2024, and new car sales in Australia were approximately 1.2 million in 2024.

As of December 31, 2024, we also operated 16 used vehicle dealerships. Used vehicle sales are even more fragmented than new vehicle sales and are generated by new car dealerships, used vehicle dealerships, individual small lot sellers, as well as individual to individual sales. In 2024, used vehicle sales were approximately 36.8 million units in the U.S. according to data from Cox Automotive, compared to 35.9 million in the prior year, and approximately 7.6 million units in the U.K. according to data from the Society of Motor Manufacturers and Traders, compared to 7.2 million in the prior year.

Retail Commercial Truck Dealership. The retail heavy-duty truck market is affected by a number of factors, including general economic conditions, fuel prices, other methods of transportation, environmental and other government regulation, interest rate fluctuations, freight metrics, and customer business cycles. According to data published by ACT Research, in recent years, total U.S. retail sales of new Class 8 commercial vehicles have ranged from a low of approximately 97,000 in 2009 to a high of approximately 334,000 in 2019. Class 8 trucks are defined by the American Automobile Association as trucks with a minimum gross vehicle weight rating above 33,000 pounds. Typically, Class 8 trucks are assembled by manufacturers utilizing certain components that may be manufactured by other companies, including engines,

10

transmissions, axles, wheels and other components. As commercial vehicles and certain commercial vehicle components have become increasingly complex, the ability to provide service for commercial vehicles has become an increasingly competitive factor in the industry. The ability to provide such service requires a significant capital investment in diagnostic and other equipment, parts inventory and highly trained service personnel. The EPA and Department of Transportation regulatory guidelines for service processes, including collision center, paint work and waste disposal, require sophisticated equipment to ensure compliance with environmental and safety standards. In 2024, North American sales of Class 6-8 medium- and heavy-duty trucks, the principal vehicles sold by our PTG business, decreased 3.0% from last year to 473,159 units and were generated at approximately 3,800 new-truck dealerships. The Class 6-7 medium-duty truck market increased 0.5% from last year to 157,260 units, and Class 8 heavy-duty trucks, the largest North American market, decreased 4.7% from last year to 315,899 units. Our principal brands, Freightliner and Western Star, represent approximately 42.9% of the Class 8 heavy-duty truck market during 2024.

Commercial Vehicle Distribution and Other. Our commercial vehicle distribution and other business operates principally in Australia and New Zealand. In 2024, heavy-duty truck sales in Australia and New Zealand combined were 20,592 units, representing a decrease of 4.5% from 2023. The brands we sell represented 4.1% of the heavy-duty truck units sold in Australia and 2.0% in New Zealand during 2024.

Penske Transportation Solutions. PTS participates broadly in the global supply chain, estimated at $11.2 trillion annually, and particularly, in the U.S. supply chain, estimated at $2.3 trillion annually. Only 13.2% of the total U.S. supply chain function is outsourced to third parties, such as PTS. We estimate, based on R. L. Polk registration data, that there are approximately 9.6 million commercial trucks operating in the United States and Canada, of which up to 5.0 million could be potential opportunities for PTS' full-service leasing and contract maintenance offerings.

Business Description

Marketing Strategy

Our integrated marketing strategies empower each dealership to capitalize on local branding while being supported by corporate programs and web presence, allowing us to leverage scale. We align ourselves with the marketing implemented by our vehicle manufacturer partners for their respective brands and integrate those initiatives and resources across the brands we represent.

We are focused on executing a comprehensive data-driven digital strategy with emphasis on customization, personalization, and creating a connection with our customers. We endeavor to build and optimize our presence across all digital platforms and deliver a seamless, convenient, and transparent experience that gives customers the ability to purchase, sell, or schedule service for their vehicles on their terms.

To stay at the forefront of technological innovations, we leverage software and systems to support our customers regardless of how they want to engage with us, from fully online to in-person or anywhere in between. In addition, we have implemented AI-driven technologies at certain of our dealerships, including a voice assistant to answer and appoint inbound service calls and an engagement system to address customer lead inquiries and schedule sales and service appointments. These technologies are designed to improve our customer experience and allow customers to engage with us 24/7.

We monitor customer satisfaction data to gain insight into our business performance and enhance the areas of our business that drive customer referral and loyalty. Social media is a highly valued element of our marketing strategy that enables us to engage with customers, increase dealership awareness, improve customer satisfaction, and enhance repeat and referral business. Additionally, we leverage corporate social media efforts and partners to benefit our dealerships and create a strong sense of community. Online reputation management sites are proactively monitored to ensure we are offering superior customer experience.

Agreements with Vehicle and Equipment Manufacturers

We operate our new vehicle dealerships under separate agreements with the manufacturers or distributors of each brand of vehicle sold at that dealership. These agreements are typical throughout the industry and may contain provisions and standards governing almost every aspect of the dealership including ownership, management, personnel, training, maintenance of a minimum of working capital, net worth requirements, maintenance of minimum lines of credit, advertising and marketing activities, facilities, signs, products and services, maintenance of minimum amounts of insurance, achievement of minimum customer service standards, and monthly financial reporting. In addition, the General Manager and/or the owner of a dealership typically cannot be changed without the manufacturer's consent. In exchange for

11

complying with these provisions and standards, we are granted the non-exclusive right to sell the manufacturer's or distributor's brand of vehicles and related parts and warranty services at our dealerships. The agreements also grant us a non-exclusive license to use each manufacturer's trademarks, service marks, and designs in connection with our sales and service of its brand at our dealership.

Many of these agreements also grant the manufacturer or distributor a security interest in the vehicles and/or parts sold by them to the dealership as well as other dealership assets and permit them to terminate or not renew the agreement for a variety of causes, including failure to adequately operate the dealership, insolvency or bankruptcy, impairment of the dealer's reputation or financial standing, changes in the dealership's management, owners, or location without consent, sales of the dealership's assets without consent, failure to maintain adequate working capital or floor plan financing, changes in the dealership's financial or other condition, failure to submit required information to them on a timely basis, failure to have any permit or license necessary to operate the dealership, and material breaches of other provisions of the agreement. In the U.S., these termination rights are subject to state franchise laws that limit a manufacturer's right to terminate a franchise. In the U.K., we operate without such local franchise law protection (see “Regulation” below).

In the U.S., some of our franchise agreements, including those with BMW, Daimler Truck North America, Honda, Hyundai, and Toyota, expire after a specified period of time ranging from one to six years. Manufacturers have not historically terminated our franchise agreements, and our franchise agreements with fixed terms have typically been renewed. We currently expect the manufacturers to renew all of our U.S. franchise agreements as they expire. In the U.K., many of our agreements have two-year rolling terms. Our agreements with BMW, our largest U.K. manufacturer, expire in December 2025. Similar to the U.S., the manufacturers in the U.K. have not historically terminated our agreements, and our agreements with fixed terms have typically been renewed.

In addition, we are subject to certain framework agreements with manufacturers that allow us as a multi-point, public company to own and operate multiple franchises in exchange for us agreeing, among other things, to limit the total number of dealerships of that brand that we may own in a particular geographic area and in some cases, limit the total number of their vehicles that we may sell as a percentage of a particular manufacturer's overall sales. Manufacturers may also limit the ownership of stores in contiguous markets. Certain of our franchise agreements have similar limits. We have reached certain national and regional geographical limitations under the agreements from time to time. Where these limits are reached or we otherwise fail to satisfy certain performance or other conditions specified in the framework agreements, we cannot acquire additional franchises of those brands in the relevant market unless we can negotiate modifications or waivers to the agreements.

These agreements also typically restrict the acquisition of additional dealerships unless the Company’s dealerships of that brand individually and/or in the aggregate are meeting certain requirements. These framework agreements typically provide the manufacturer or distributor the right in some circumstances (including upon a merger, sale, change of control of the Company, or in some cases a material change in our business or capital structure) to acquire the dealerships from us at fair market value or other predetermined values, including upon the acquisition of 20% or more of our voting stock by a person, entity, group, or another manufacturer (subject to certain exceptions), an extraordinary corporate transaction (such as a merger, reorganization, or sale of a material amount of assets), or a change of control of our board of directors. See Item 1A. Risk Factors, "Vehicle manufacturers exercise significant control over us and our success is largely dependent on the success of our manufacturer partners."

With respect to our commercial vehicle distribution and other operations in Australia and New Zealand, we are party to distributor agreements with each manufacturer of products we distribute pursuant to which we are the distributor of these products in those countries and nearby markets. The agreements govern all aspects of our distribution rights, including sales and service activities, service and warranty terms, use of intellectual property, promotion and advertising provisions, pricing and payment terms, and indemnification requirements. The agreement with Western Star expires in 2031, the agreement with MTU expires in 2029, and the agreement with Detroit Diesel expires in 2031. We also are party to shipping agreements with respect to importing those products. For each of our non-company-owned dealers, we have signed a franchise agreement with terms that set forth the dealer's obligations with respect to the sales and servicing of commercial vehicles and associated parts.

Competition

Dealerships. We believe that the principal factors consumers consider when determining where to purchase a vehicle are vehicle pricing (including manufacturer rebates and other special offers), marketing campaigns conducted by manufacturers, the ability of dealerships to offer a wide selection of the most popular vehicles, offering a multi-channel experience to customers so they may purchase a vehicle on site or remotely, the location of dealerships, and the quality of

12

the customer experience. Other factors include customer preference for particular brands of vehicles and warranties. We believe that our dealerships are competitive in all of these areas.

The automotive and truck retail industry is currently served by franchised or agency dealerships, automotive manufacturers that sell directly to consumers, independent used vehicle dealerships, and individual consumers who sell used vehicles in private transactions. For new vehicle sales, we compete primarily with other franchised dealers in each of our marketing areas and automotive manufacturers that sell directly to consumers, relying on our premium facilities, superior customer service, advertising and merchandising, management experience, sales expertise, reputation, and the location of our dealerships to attract and retain customers. Each of our markets may include a number of well-capitalized competitors, including in certain instances dealerships owned by manufacturers and national and regional retail chains. In our retail commercial truck dealership operations, we compete with other manufacturers and retailers of medium- and heavy-duty trucks, such as Ford, International Kenworth, Mack, Peterbilt, and Volvo. We also compete with dealers that sell the same brands of new vehicles that we sell and with dealers that sell other brands of new vehicles that we do not represent in a particular market. Our new vehicle dealership competitors have franchise agreements which give them access to new vehicles on the same terms as us. Automotive dealers also face competition in the sale of new vehicles from purchasing services, and electric vehicle manufacturers that sell directly to consumers. With respect to arranging financing for our customers' vehicle purchases, we compete with a broad range of financial institutions, such as banks and local credit unions.

For used vehicle sales, we compete in a highly fragmented market which sells approximately 36.8 million units in the U.S. and approximately 7.6 million units in the U.K. annually through other franchised dealers, independent used vehicle dealers, automobile rental agencies, purchasing services, private parties, online retailers, and used vehicle “superstores” for the procurement and resale of used vehicles.

We compete with other franchised dealers to perform warranty repairs and with other dealers, franchised and non-franchised service center chains, and independent garages for non-warranty repair and routine maintenance business. We compete with other dealers, franchised and independent aftermarket repair shops, and parts retailers in our parts operations. We believe that the principal factors consumers consider when determining where to purchase vehicle parts and service are price, the use of factory-approved replacement parts, facility location, the familiarity with a manufacturer's brands, and the quality of customer service. A number of regional or national chains offer selected parts and services at prices that may be lower than our prices.

We believe the majority of consumers are utilizing the Internet and other digital media in connection with the purchase of new and used vehicles. Accordingly, we face increased competition from online vehicle websites, including those developed by manufacturers and other dealership groups.

Commercial Vehicle Distribution and Other. With respect to our commercial vehicle distribution and other operations in Australia and New Zealand, we compete with manufacturers, distributors, and retailers of other vehicles and products in our markets.

PTS. As an alternative to using PTS' full-service truck leasing or contract maintenance services, we believe that most potential customers perform some or all of these services themselves. They may also purchase similar or alternative services from other third-party vendors. Its full-service truck leasing operations compete with companies providing similar services on a national, regional, and local level. Many regional and local competitors provide services on a national level through their participation in various cooperative programs. Competitive factors include price, maintenance, service, and geographic coverage. PTS competes with finance lessors, truck and trailer manufacturers, and independent dealers, each of which provides full-service lease products, finance leases, extended warranty maintenance, rental, and other transportation services. Its contract maintenance offering competes primarily with truck and trailer manufacturers and independent dealers who provide maintenance services.

PTS' commercial and consumer rental operations compete with several other nationwide vehicle rental systems, a large number of vehicle leasing, and rental companies with multiple branches operating on a regional basis and many similar companies operating primarily on a local basis. Because a significant portion of its consumer rentals are used for moving and relocation, PTS competes with local and national moving and storage companies as well as alternatives such as portable container-based transportation and storage. In its commercial and consumer rental operations, it competes primarily on the basis of equipment availability, geographic location, and customer service.

PTS' logistics business competes with other dedicated logistics providers, freight management businesses, freight brokers, warehouse providers, and truckload carriers on a national, regional, and local level as well as with the internal supply chain functions of prospective customers who rely on their own resources for logistics management. Competitive

13

factors include price, efficient logistical design offerings, equipment, maintenance, service, technology, geographic coverage, and driver and operations expertise. PTS seeks to combine its logistics services with its existing full-service truck leasing and truck rental business to create an integrated transportation solution for its customers.

Human Capital

We believe that our Human Capital is our greatest asset and is an integral component of our growth and value creation strategy. We understand that exceptional customer service can only be consistently delivered by attracting, motivating, training, and retaining the very best team members. We strive to provide a work environment that promotes opportunity and is free from any form of discrimination based on any protected status in accordance with all applicable federal, state, and local laws. With this in mind, we put our employees at the heart of everything that we do by developing their talent and enabling them to build long-term careers.

In recognition of our people-first philosophy, in 2024, 79 of our dealerships were named to the "Automotive News Best Dealerships To Work For", which ranks the top 150 dealerships in the United States, including nine of the top ten spots and 17 of the top 20 spots nationally in 2024's rankings with one of our dealerships claiming the number one spot, more than any other dealership group. Our dealerships were also recognized for their commitment to promoting inclusive workplaces, receiving accolades for being among the best in the following categories: Best Dealerships for Employees 30 or Younger; Best Dealerships for Diversity, Equity and Inclusion; Best Dealerships for Minority Leadership; Best Dealerships for Family Friendliness. PTG was also named as one of the 2024 "Top Companies for Women to Work in Transportation." Also, in January 2024, we were notified that Penske Automotive Group was named by Fortune as a "World's Most Admired Company".

As of December 31, 2024, we employed approximately 28,900 people, of which approximately 683 were covered by collective bargaining agreements with labor unions. We believe our relations with our employees, including those represented by collective bargaining agreements, are generally good. We believe our inclusive culture enhances our ability to attract and retain the most talented leadership and workforce, thereby enabling us to better serve and broaden our customer base.

We maintain a culture grounded in safety and endeavor to eliminate workplace incidents, risks, and hazards. We have partnered with environmental and safety consulting firms to assist in compliance with specific local and federal laws and regulations relating to environmental and safety issues and to promote best safety practices. Audits are regularly performed to ensure and maintain compliance.

We believe our employee turnover of approximately 20% is below the industry averages for our businesses. We seek to motivate our key managers and salespersons through, among other things, variable compensation programs tied principally to local profitability and customer satisfaction. We also annually survey our employees to gauge their satisfaction and address any resulting concerns.

Regulation

We operate in a highly regulated industry and a number of regulations affect the marketing, selling, financing, servicing, and distribution of vehicles. Under the laws of the jurisdictions in which we currently operate, we typically must obtain a license in order to establish, operate, relocate a dealership, or operate a repair facility. These laws also regulate our business conduct, including our advertising, operating, financing, employment, distribution, and sales practices. Other laws and regulations include franchise laws and regulations, environmental laws and regulations (see “Environmental Matters” below), laws and regulations applicable to new and used motor vehicle dealers as well as customer and employee privacy, identity theft prevention, wage-hour, anti-discrimination, and other employment practices laws. With respect to online sales, many laws and regulations applicable to our business were adopted prior to the introduction of the Internet, certain digital technologies, and e-commerce, generally. As a result, we are tasked with maintaining compliance in an uncertain regulatory environment.

Our financing activities with customers are subject to truth-in-lending, consumer leasing, equal credit opportunity, and similar regulations as well as motor vehicle finance laws, installment finance laws, insurance laws, usury laws, and other installment sales laws. Some jurisdictions regulate finance fees that may be paid as a result of vehicle sales. In the U.K., the Financial Conduct Authority (the "FCA") regulates financial services firms and financial markets, including our activities in acting as broker for the financing of vehicle sales. The FCA has announced that it will investigate the historic use of discretionary commission arrangements ("DCAs") amid concerns that this practice may have been unfair to customers. The purpose of the investigation is to consider whether the historic use of DCAs caused customers to pay too much for their car loans and, if so, to consider potential remediation measures. The investigation is being undertaken after the Financial

14

Ombudsman Service (a public body, which resolves financial complaints) determined that DCAs, in two separate cases which do not involve us, had caused financial losses to customers. We await the outcome of the FCA’s investigation which is expected in May of 2025. Any regulatory or judicial outcome that ultimately results in the refund of historical commissions paid to us or that reduces the commissions paid to us could materially and adversely affect us. Further, on October 25, 2024, the U.K. Court of Appeal (the second highest court in the U.K.) issued a judgment requiring lenders to repay certain customers the commissions paid to dealers for vehicle finance agreements determining that there was a duty to the customers to disclose the amount of the commissions paid to those dealers. Although this judgment has been appealed by the relevant lenders to the U.K. Supreme Court (the highest court in the U.K.), our U.K. consumer lending partners have required that we now disclose to customers the commissions we receive from their vehicle financing. The ultimate resolution of these matters may impact our procedural processes and expose us to claims for repayment of historical commissions. See Item 1A. Risk Factors, "Other Regulatory Issues".

In the U.S., we benefit from the protection of numerous state franchise laws that generally provide that a manufacturer or distributor may not terminate or refuse to renew a franchise agreement unless it has first provided the dealer with written notice setting forth good cause and stating the grounds for termination or non-renewal. Some state franchise laws allow dealers to file protests or petitions or to attempt to comply with the manufacturer's criteria within the notice period to avoid termination or non-renewal. Our international locations generally do not have these laws, and as a result, our international operations operate without these types of protections. See Item 1. Business, "Agreements with Vehicle and Equipment Manufacturers."

Environmental Matters

We are subject to a wide range of environmental laws and regulations, including those governing discharges into the air and water, the operation and removal of aboveground and underground storage tanks, the use, handling, storage, and disposal of hazardous substances and other materials, and the investigation and remediation of environmental contamination. Our business involves the generation, use, handling, and contracting for recycling or disposal of hazardous or toxic substances or waste, including environmentally sensitive materials such as motor oil, filters, transmission fluid, antifreeze, refrigerant, batteries, solvents, lubricants, tires, and fuel. EVs pose additional risks regarding the use, maintenance, and disposal of electric batteries which may be subject to additional regulations. We have incurred, and will continue to incur, capital and operating expenditures and other costs in complying with such laws and regulations.

Our operations involving the management of hazardous and other environmentally sensitive materials are subject to numerous requirements. Our business also involves the operation of storage tanks containing such materials. Storage tanks are subject to periodic testing, containment, upgrading, and removal under applicable law. Furthermore, investigation or remediation may be necessary in the event of leaks or other discharges from current or former underground or aboveground storage tanks. In addition, water quality protection programs govern certain discharges from some of our operations. Similarly, certain air emissions from our operations, such as vehicle painting, may be subject to relevant laws. Various health and safety standards also apply to our operations.

We may have liability in connection with materials that are sent to third-party recycling, treatment, and/or disposal facilities under the U.S. Comprehensive Environmental Response, Compensation, and Liability Act and comparable statutes. These statutes impose liability for investigation and remediation of contamination without regard to fault or the legality of the conduct that contributed to the contamination. Responsible parties under these statutes may include the owner or operator of the site where the contamination occurred and companies that disposed or arranged for the disposal of the hazardous substances released at these sites.

We have a proactive strategy related to environmental, health, and safety compliance, which includes contracting with third parties to inspect our facilities periodically. We believe that we do not have any material environmental liabilities and that compliance with environmental laws and regulations will not, individually or in the aggregate, have a material effect on us. However, soil and groundwater contamination are known to exist at certain of our current or former properties. Further, environmental laws and regulations are complex and subject to change. In addition, in connection with our acquisitions, it is possible that we will assume or become subject to new or unforeseen environmental costs or liabilities, some of which may be material. Compliance with current, amended, new, or more stringent laws or regulations, stricter interpretations of existing laws, or the future discovery of environmental conditions could require additional expenditures by us, and such expenditures could be material.

Vehicle Emissions Regulation

Federal and state governments and regulators in our markets have increasingly placed restrictions and limitations on new vehicles in an effort to combat perceived negative environmental effects. In response to concerns that emissions of

15

carbon dioxide and certain other gases, referred to as "greenhouse gases" or "GHGs," may be contributing to warming of the Earth's atmosphere, climate change-related legislation and policy changes to restrict GHGs have been implemented at state and federal levels in a manner that impacts our business. The impact of the new U.S. presidential administration on U.S. federal policy in this area is uncertain. See Item 1A. Risk Factors, "Vehicle Emissions and Other Environmental Regulations".

Retail Automotive. Many jurisdictions in which we operate have placed restrictions on new vehicle GHG emissions. The U.S. Environmental Protection Agency ("EPA") has adopted standards that require vehicle manufacturers achieve progressively lower emissions for new vehicles in model years 2027 through 2032. The standards apply to all new light-duty and medium-duty vehicles, which includes passenger vehicles, light trucks and large pickups and vans. The standards require an industry-wide average target for light-duty vehicles of 85 grams of carbon dioxide per mile in model year 2032, a nearly 50% reduction from the 2026 standard. Medium-duty vehicles must achieve a final standard of 274 grams of carbon dioxide per mile by 2032, a 44% reduction from the 2026 standard. The EPA regulates motor vehicle emissions through performance-based standards that impose fleet-wide average emissions limits—individual vehicles with higher emissions are allowable if the fleet average achieves the EPA's emissions targets. The standards do not require the adoption of specific technologies. Automakers may decide which technologies will achieve the standards, such as advanced gasoline engines and transmissions, improvements to tailpipe controls, and electrification. Nonetheless, the EPA projects that the influence of these standards, in conjunction with other market developments like incentives available under the Inflation Reduction Act, will result in plug-in EVs accounting for 68% of new light-duty vehicles by model year 2032.

Moreover, the EPA has allowed the State of California Air Resource Board (“CARB”) to adopt its Advanced Clean Cars II program which requires that new vehicle sales by vehicle manufacturers to be 35% Zero Emissions Vehicles (ZEVs) for model year 2026 which increases to 100% ZEVs by model year 2035 (with certain allowances for hybrid gas/EVs). Certain states have also adopted California’s mandate, in whole or in part.