UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_______________________________________

FORM 10-K

FOR ANNUAL AND TRANSITION REPORTS

PURSUANT TO SECTIONS 13 OR

15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

(Mark One)

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 0-21044

_______________________________________

UNIVERSAL ELECTRONICS INC.

(Exact Name of Registrant as Specified in its Charter)

Delaware | 33-0204817 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

201 E. Sandpointe Avenue, 8th Floor Santa Ana, California | 92707 | |

(Address of Principal Executive Offices) | (Zip Code) | |

Registrant's telephone number, including area code: (714) 918-9500

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, par value $.01 per share | The NASDAQ Stock Market LLC | |

(Title of Class) | (Name of each exchange on which registered) | |

Securities registered pursuant to Section 12(g) of the Act:

None

_______________________________________

Indicate by check mark if whether the registrant is a well-known seasoned issuer (as defined in Rule 405 of the Securities Act). Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, any Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ¨ | Accelerated filer | ý |

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant on June 30, 2016, the last business day of the registrant's most recently completed second fiscal quarter was $566,737,072 based upon the closing sale price as reported on the NASDAQ Stock Market for that date.

On March 6, 2017, 14,390,071 shares of Common Stock, par value $.01 per share, of the registrant were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the registrant's notice of annual meeting of shareowners and proxy statement to be filed pursuant to Regulation 14A within 120 days after registrant's fiscal year end of December 31, 2016 are incorporated by reference into Part III of this Form 10-K. The Proxy Statement will be filed with the Securities and Exchange Commission no later than May 1, 2017.

Except as otherwise stated, the information contained in this Form 10-K is as of December 31, 2016.

UNIVERSAL ELECTRONICS INC.

Annual Report on Form 10-K

For the Fiscal Year Ended December 31, 2016

Table of Contents

Item Number | Page Number |

PART I | |

PART II | |

PART III | |

PART IV | |

PART I

ITEM 1. BUSINESS

Business of Universal Electronics Inc.

Universal Electronics Inc. ("UEI") was incorporated under the laws of Delaware in 1986 and began operations in 1987. The principal executive offices are located at 201 E. Sandpointe Avenue, 8th Floor, Santa Ana, California 92707. As used herein, the terms "we", "us" and "our" refer to UEI and its subsidiaries unless the context indicates to the contrary.

Additional information regarding UEI may be obtained at www.uei.com. Our website address is not intended to function as a hyperlink and the information available at our website address is not incorporated by reference into this Annual Report on Form 10-K. We make our periodic and current reports, together with amendments to these reports, available on our website, free of charge, as soon as reasonably practicable after such material is electronically filed with, or furnished to, the U.S. Securities and Exchange Commission ("SEC"). The SEC maintains a website at www.sec.gov that contains the reports, proxy and other information that we file electronically with the SEC.

Business Segment

Overview

Universal Electronics Inc. develops control and sensor technology solutions and manufactures a broad line of pre-programmed and universal remote control products, audio-video ("AV") accessories, and intelligent wireless security and automation components dedicated to redefining the home entertainment and security experience. Our offerings include the following:

• | easy-to-use, pre-programmed universal infrared ("IR") and radio frequency ("RF") remote controls that are sold primarily to subscription broadcasting providers (cable, satellite and Internet Protocol television ("IPTV")), original equipment manufacturers ("OEMs"), retailers, and private label customers; |

• | integrated circuits, on which our software and universal device control database is embedded, sold primarily to OEMs, subscription broadcasting providers, and private label customers; |

• | software, firmware and technology solutions that can enable devices such as TVs, set-top boxes, stereos, smart phones, tablets, gaming controllers and other consumer electronic devices to wirelessly connect and interact with home networks and interactive services to control and deliver digital entertainment and information; |

• | intellectual property which we license primarily to OEMs, software development companies, private label customers, and subscription broadcasting providers; |

• | proprietary and standards-based RF sensors designed for residential security, safety and automation applications; and |

• | AV accessories sold, directly and indirectly, to consumers. |

Our business is comprised of one reportable segment.

Principal Products and Markets

Our principal markets are the subscription broadcast, consumer and mobile electronics and residential security markets where our customers include subscription broadcasters, OEMs, international retailers, private label brands, pro-security dealers and companies in the computing industry.

We provide subscription broadcasting providers, both domestically and internationally, with our universal remote control devices and integrated circuits, on which our software and device code database library is embedded. We also sell integrated circuits, on which our software and IR device control code database is embedded, and license our IR device control database to OEMs that manufacture televisions, digital audio and video players, streamer boxes, cable converters, satellite receivers, set-top boxes, room air conditioning equipment, game consoles, and wireless mobile phones and tablets.

We continue to place significant emphasis on expanding our sales and marketing efforts to subscription broadcasters and OEMs in Asia, Latin America and Europe. Owning and operating our own factories in the People's Republic of China ("PRC") has enhanced our ability to compete in the OEM and subscription broadcasting markets. In addition, we have subsidiaries in Brazil and Mexico, which have allowed us to increase our reach and better compete in the Central and Latin American subscription broadcast market. We plan to continue to add new sales and administrative personnel to support anticipated sales growth in international markets over the next few years.

We continue to pursue further penetration of the more traditional OEM consumer electronics markets as well as newer product categories in the mobile electronics markets such as smart phones, tablets and other mobile smart devices. Customers in these

3

markets integrate our products and technology into their products to simplify and expand the universal control capabilities of home entertainment ecosystems. Growth in these markets has been driven by the increasing complexity of home entertainment, emerging digital technology, multimedia and interactive internet applications, and the increasing proliferation of connected smart devices offered by OEMs.

In 2015, we acquired Ecolink Intelligent Technology, Inc. ("Ecolink"), a leading developer of smart home technology. Ecolink provides a wide range of intelligent wireless security and automation components dedicated to redefining the home security experience. Ecolink has over 20 years of wireless engineering expertise in the home security and automation market and holds more than 25 related pending and issued patents. UEI’s current subscription broadcasting customers are adding home security and automation to their list of service offerings. Our acquisition of Ecolink, a premise equipment supplier to this market, enables us to broaden our design expertise and product portfolio to add home security and automation sensors to our capabilities.

For the years ended December 31, 2016 and 2015, our sales to Comcast Corporation accounted for 22.9% and 21.5% of our net sales, respectively. For the years ended December 31, 2016, 2015, and 2014, our sales to DIRECTV and its sub-contractors collectively accounted for 10.5%, 12.4%, and 10.4% of our net sales, respectively.

Our One For All® brand name remote controls and accessories sold within the international retail markets accounted for 7.2%, 8.1%, and 9.2% of our total net sales for the years ended December 31, 2016, 2015, and 2014, respectively.

Financial information relating to our international operations for the years ended December 31, 2016, 2015, and 2014 is included in "ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA - Notes to Consolidated Financial Statements - Note 15".

Intellectual Property and Technology

We hold a number of patents in the United States and abroad related to our products and technology, and have filed domestic and foreign applications for other patents that are pending. At the end of 2016, we had over 400 issued and pending United States patents related to remote control, home security, safety and automation as well as hundreds of foreign counterpart patents and applications in various territories around the world.

Our patents have remaining lives ranging from one to 18 years. We have also obtained copyright registration and claim copyright protection for certain proprietary software and libraries of IR codes. Additionally, the names of many of our products are registered, or are being registered, as trademarks in the United States Patent and Trademark Office and in most of the other countries in which such products are sold. These registrations are valid for terms ranging up to 20 years and may be renewed as long as the trademarks continue to be used and are deemed by management to be important to our operations. While we follow the practice of obtaining patent, copyright and trademark registrations on new developments whenever advisable, in certain cases we have elected common law trade secret protection in lieu of obtaining such other protection.

A key factor in creating products and software for control of entertainment devices is the device control code database. Since our beginning in 1986, we have compiled an extensive device control code database library that covers nearly one million individual device functions and approximately 7,900 individual consumer electronic equipment brand names, including virtually all IR controlled set-top boxes, televisions, audio components, DVD players, Blu-Ray players, CD players, other remote controlled home entertainment devices and home automation control modules, and wired Consumer Electronics Control ("CEC") and wireless Internet Protocol ("IP") control protocols commonly found on many of the latest HDMI and internet connected devices. Our proprietary software automatically detects, identifies and enables the appropriate control commands for any given home entertainment, automation and air conditioning device in the home. Our library is continuously updated with device control codes used in newly introduced AV and Internet of Things ("IoT") devices. These control codes are captured directly from the remote control devices or the manufacturer's written specifications to ensure the accuracy and integrity of the database. Our proprietary software and know-how permit us to offer a device control code database that is more robust and efficient than similarly priced products of our competitors.

Our goal is to provide universal control solutions that require minimal or no user set-up and deliver consistent and intuitive one-touch control of all connected content sources and devices. QuickSet® is a software application that is currently embedded in millions of devices worldwide. QuickSet may be embedded in an AV device, set-top box, or other host device, or delivered as a Cloud-based service to enable universal remote setup and control. QuickSet enables universal remote control set-up using automated and guided on-screen instructions and a wireless two-way communication link between the remote and the QuickSet enabled device. The two-way connection allows device control code data and configuration settings to be sent to the remote control from the device and greatly simplifies the universal remote control set-up process and can enable other time saving features. QuickSet utilizes data transmitted over HDMI or IP networks to automatically detect various attributes of the connected device and downloads the appropriate control codes and functions into the remote control without the need for the user to enter any additional information. The user does not need to know the brand or model number to set up the device in the remote. Any compatible new device that is

4

connected is recognized. Consumers can quickly and easily set up their remotes to control multiple devices. Recently added features in QuickSet address common consumer challenges in universal device control, such as mode confusion and input switching. With QuickSet consumers switch easily between activities and reliably view their chosen content source with a single touch. QuickSet handles the device-specific control requirements. Licensees of QuickSet include service providers such as Comcast, DIRECTV and Echostar Technologies; smart TV manufacturers such as Sony and Samsung; leading game console manufacturer Microsoft on their Xbox One game system; and mobile and tablet device manufacturers Samsung, LG, OPPO, Huawei and LeTV on some of their mobile handset platforms.

Smart devices are becoming a more prevalent part of the home entertainment experience, and UEI offers several solutions to enable entertainment device control with a smart phone, tablet or smart TV. In its smart device control solutions, UEI offers all of the elements needed for device control from the IR microcontroller to the device control database to the user interface for the touchscreen. Nevo® is a UEI-designed and developed universal control suite of applications designed for Android and iOS tablets and smart phones that UEI has released and that is currently available for download at Google Play and the Apple App Store.

Methods of Distribution

Our distribution methods for our remote control devices are dependent on the sales channel. We distribute remote control devices, sensors and AV accessories directly to subscription broadcasters and OEMs, both domestically and internationally. We currently also distribute home security sensors to pro-security installers in the United States through a network of dealers. Outside of North America, we sell our wireless control devices and AV accessories under the One For All® and private label brand names to retailers through our international subsidiaries. We utilize third-party distributors for the retail channel in countries where we do not have subsidiaries.

We have developed a broad portfolio of patented technologies and the industry's leading database of device control codes. We ship integrated circuits, on which our software and control code database are embedded, directly to manufacturers for inclusion in their products. In addition, we license our software and technology to manufacturers. Licenses are delivered upon the transfer of a product master or on a per unit basis when the software or technology is used in a customer device.

We provide domestic and international consumer support to our various universal remote control marketers, including manufacturers, cable and satellite providers, retail distributors, and audio and video OEMs through our live and automated call centers. We also make available a web-based support resource, www.urcsupport.com, designed specifically for subscription broadcasters. This solution offers videos and online tools to help users easily set up their universal remote, and as a result reduce call volume at customer support centers. Additionally, the UEI Technical Support Services call center provides customer interaction management services from technical service and support to customer retention. Services include pre-repair calls, post-install surveys, and inbound calls for cable customers to provide greater bottom-line efficiencies.

5

Our 23 international subsidiaries are the following:

• | C.G. Development Ltd., established in Hong Kong; |

• | CG Mexico Remote Controls, S. de R.L. de C.V., established in Mexico; |

• | Enson Assets Ltd., established in the British Virgin Islands; |

• | Gemstar Polyfirst Ltd., established in Hong Kong; |

• | Gemstar Technology (China) Co. Ltd., established in the PRC; |

• | Gemstar Technology (Qinzhou) Co. Ltd., established in the PRC; |

• | Gemstar Technology (Yangzhou) Co. Ltd., established in the PRC; |

• | Guangzhou Universal Electronics Service Co., Ltd., established in the PRC; |

• | One For All Argentina S.R.L., established in Argentina; |

• | One For All France S.A.S., established in France; |

• | One For All GmbH, established in Germany; |

• | One for All Iberia S.L., established in Spain; |

• | One For All UK Ltd., established in the United Kingdom; |

• | UE Japan Ltd., established in Japan; |

• | UE Singapore Pte. Ltd., established in Singapore; |

• | UEI Cayman Inc., established in the Cayman Islands; |

• | UEI do Brasil Controles Remotos Ltda., established in Brazil; |

• | UEI Electronics Pte. Ltd., established in India; |

• | UEI Hong Kong Pte. Ltd., established in Hong Kong; |

• | Universal Electronics B.V., established in the Netherlands; |

• | Universal Electronics Italia S.R.L., established in Italy; |

• | Universal Electronics Trading Co., Ltd., established in the PRC; and |

• | Universal Electronics Yangzhou Co. Ltd., established in the PRC; |

Raw Materials and Dependence on Suppliers

We utilize our own manufacturing plants and third-party manufacturers and suppliers primarily located within the PRC to produce our remote control and sensor products. In 2016, Texas Instruments provided 11.7% of our total inventory purchases. In 2015, no single supplier provided more than 10% of our total inventory purchases. In 2014, Maxim Integrated Products International Limited provided 10.7% of our total inventory purchases.

Even though we operate three factories in the PRC and assembly plants in Brazil and Mexico, we continue to evaluate additional contract manufacturers and sources of supply. During 2016, we utilized multiple contract manufacturers and maintained duplicate tooling for certain of our products. Where possible we utilize standard parts and components, which are available from multiple sources.

We continually seek additional sources to reduce our dependence on our integrated circuit suppliers. To further manage our integrated circuit supplier dependence, we include flash microcontroller technology in most of our products. Flash microcontrollers can have shorter lead times than standard microcontrollers and may be reprogrammed, if necessary. This allows us flexibility during any unforeseen shipping delays and has the added benefit of potentially reducing excess and obsolete inventory exposure. This diversification lessens our dependence on any one supplier and allows us to negotiate more favorable terms.

Seasonality

Historically, our business has been influenced by the retail sales cycle, with increased sales in the second half of the year. We expect this pattern to be repeated during 2017.

See "ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA — Notes to Consolidated Financial Statements — Note 23" for further details regarding our quarterly results.

Competition

Our principal competitors in the subscription broadcasting market are Remote Solutions, Omni Remotes (formerly Philips Home Control Singapore PTE, Ltd.), SMK, and Universal Remote Control. In the international retail and private label markets for wireless

6

controls we compete with Logitech, Omni Remotes, Ruwido and Sony, as well as various manufacturers of wireless controls in Asia. Our primary competitors in the OEM market are the original equipment manufacturers themselves and wireless control manufacturers in Asia. In home security, safety and automation, we offer universal sub-gigahertz products that are compatible with the top security panel manufacturers, such as Honeywell, GE, Tyco/DSC and 2GIG. We compete in our markets on the basis of product quality, features, price, intellectual property and customer support. We believe that we will need to continue to introduce new and innovative products and software solutions to remain competitive and to recruit and retain competent personnel to successfully accomplish our future objectives.

Engineering, Research and Development

During 2016, our engineering efforts focused on the following:

• | broadening our product portfolio; |

• | launching new embedded software solutions designed to simplify set-up and control features; |

• | modifying existing products and technologies to improve features and lower costs; |

• | formulating measures to protect our proprietary technology and general know-how; |

• | improving our control solutions software; |

• | updating our library of device codes to include codes for new features and devices introduced worldwide; and |

• | creating innovative products that address consumer challenges in home entertainment control and security sensing. |

During 2016, our advanced engineering efforts focused on further developing our existing products, services and technologies. We released software updates to our embedded QuickSet application, and continued development initiatives around emerging RF technologies, such as RF4CE, Bluetooth, and Bluetooth Smart. Additionally, we released several new advanced remote control products that incorporate voice search capabilities in our subscription broadcast and OEM channels.

Our personnel are involved with various industry organizations and bodies, which are in the process of setting standards for IR, RF, power line, telephone and cable communications and networking in the home. Because of the nature of research and development activities, there can be no assurance that any of our research and development projects will be successfully completed or ultimately achieve commercial success.

Our expenditures on engineering, research and development were:

(In millions): | 2016 | 2015 | 2014 | |||||||||

Research and development | $ | 19.9 | $ | 18.1 | $ | 17.0 | ||||||

Engineering (1) | 10.5 | 9.5 | 9.8 | |||||||||

Total engineering, research and development | $ | 30.4 | $ | 27.6 | $ | 26.8 | ||||||

(1) | Engineering costs are included in selling, general and administrative expenses. |

Environmental Matters

Many of our products are subject to various federal, state, local and international laws governing chemical substances in products, including laws regulating the manufacture and distribution of chemical substances and laws restricting the presence of certain substances in electronics products. We may incur substantial costs, including cleanup costs, fines and civil or criminal sanctions, third-party damages or personal injury claims, if we were to violate or become liable under environmental laws or if our products become non-compliant with environmental laws. We also face increasing complexity in our product design and procurement operations as we adjust to new and future requirements relating to the materials composition of our products.

We may also face significant costs and liabilities in connection with product take-back legislation. The European Union's Waste Electrical and Electronic Equipment Directive ("WEEE") makes producers of electrical goods financially responsible for specified collection, recycling, treatment and disposal of past and future covered products. Our European subsidiaries are WEEE compliant. Similar legislation has been or may be enacted in other jurisdictions, including in the United States, Canada, Mexico, the PRC and Japan.

7

We believe that we have materially complied with all currently existing international and domestic federal, state and local statutes and regulations regarding environmental standards and occupational safety and health matters to which we are subject. During the years ended December 31, 2016, 2015 and 2014, the amounts incurred in complying with federal, state and local statutes and regulations pertaining to environmental standards and occupational safety and health laws and regulations did not materially affect our earnings or financial condition. However, future events, such as changes in existing laws and regulations or enforcement policies, may give rise to additional compliance costs that may have a material adverse effect upon our capital expenditures, earnings or financial condition.

Employees

At December 31, 2016, we employed 3,103 employees, of which 512 worked in engineering and research and development, 106 in sales and marketing, 71 in consumer service and support, 2,096 in operations and warehousing and 318 in executive and administrative functions. In addition, our factories in the PRC and our Asian operations employed an additional 6,921 staff contracted through agency agreements.

Labor unions represent approximately 13.8% of our 3,103 employees. Some unionized workers, employed in Manaus, Brazil, are represented under contract with the Sindicato dos Trabalhadores nas Industrias Metalugicas, Mecanicas e de Materiais Eletricos de Manaus. Other unionized workers, employed in Monterrey, Mexico, are represented under contract with the Sindicato Industrial de Trabajadores de Nuevo León adherido a la Federación Nacional de Sindicatos Independientes. Our business units are subject to various laws and regulations relating to their relationships with their employees. These laws and regulations are specific to the location of each business unit. We believe that our relationships with employees and their representative organizations are good.

International Operations

Financial information relating to our international operations for the years ended December 31, 2016, 2015 and 2014 is incorporated by reference to "ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA — Notes to Consolidated Financial Statements — Note 15".

Executive Officers of the Registrant(1)

The following table sets forth certain information concerning our executive officers on March 9, 2017:

Name | Age | Position | ||

Paul D. Arling | 54 | Chairman of the Board and Chief Executive Officer | ||

David Chong | 55 | Executive Vice President, Asia | ||

Louis S. Hughes | 52 | Chief Operating Officer | ||

Richard A. Firehammer, Jr. | 59 | Senior Vice President, General Counsel and Secretary | ||

Bryan M. Hackworth | 47 | Senior Vice President and Chief Financial Officer | ||

Menno V. Koopmans | 41 | Executive Vice President, Managing Director, Europe | ||

(1) | Included pursuant to Instruction 3 to Item 401(b) of Regulation S-K. |

Paul D. Arling is our Chairman and Chief Executive Officer. He joined us in May 1996 as Chief Financial Officer and was named to our Board of Directors in August 1996. He was appointed President and Chief Operating Officer in September 1998, was promoted to Chief Executive Officer in October 2000 and appointed as Chairman in July 2001. At the 2016 Annual Meeting of Stockholders, Mr. Arling was re-elected as our Chairman to serve until the 2017 Annual Meeting of Stockholders. From 1993 through May 1996, he served in various capacities at LESCO, Inc. (a manufacturer and distributor of professional turf care products). Prior to LESCO, he worked for Imperial Wall coverings (a manufacturer and distributor of wall covering products) as Director of Planning, and The Michael Allen Company (a strategic management consulting company) where he was employed as a management consultant.

David Chong is our Executive Vice President, Asia. He is responsible for general management of our Asia region and Global Operations. Mr. Chong joined us in January 2009 as Senior Vice President of Global OEM. Prior to joining us, Mr. Chong served as Senior Vice President at Philips Consumer Electronics Division and as the Chief Marketing Officer of the business group Philips Display (Philips TV and Computer Monitor business). At Philips Display, he led the re-engineering of the Product Creation, Marketing and Sales Organization to compete successfully in the LCD TV space. Prior to this, he also served as Vice President and General Manager of the Audio Video Business in Asia, Vice President and Global Business Line Manager for Audio and various senior management positions at Philips' CE Division. Mr. Chong started at Philips Research Lab in 1984 as a research

8

scientist working in the area of VLSI design methodologies. He also served as Managing Director for Asia at InVue Security Product before joining us at the present position. Mr. Chong had his senior education in The United Kingdom, holding a B.S. in Electrical and Electronics Engineering with High Honors from University of Nottingham.

Louis S. Hughes is our Executive Vice President, Americas. He joined us in 2004 as General Manager of Simple Devices as part of our acquisition of Simples Devices, Inc. in that same year. From 2008 to 2011, he was our Vice President Corporate Development. From 2011 to 2014, he was our Senior Vice President - Americas and was promoted to his current position in 2015. Prior to joining us, Mr. Hughes co-founded SimpleDevices, Inc. (a company that pioneered local area network digital media distribution to a wide variety of consumer electronics devices) and Supplybase (a company that provided enterprise wide, web-based supply chain management systems and information). He also held various positions with General Electric Company over a ten-year period.

Richard A. Firehammer, Jr., Esq. is our Senior Vice President, General Counsel and Secretary. He joined us in October 1993 as General Counsel. He became our Secretary in February 1994. He was our Vice President from May 1997 until August 1998, and served as counsel to us from September 1998 until February 1999 at which time he was promoted to his current position. From November 1992 to September 1993, he was associated with the Chicago, Illinois law firm, Shefsky & Froelich, Ltd. From 1987 to 1992, he was with the law firm Vedder, Price, Kaufman & Kammholz in Chicago, Illinois.

Bryan M. Hackworth is our Senior Vice President and Chief Financial Officer. He was promoted to Chief Financial Officer in August 2006. Mr. Hackworth joined us in June 2004 as Corporate Controller and subsequently assumed the role of Chief Accounting Officer in May 2006. Before joining us in 2004, he spent five years at Mars, Inc., a privately held international manufacturer and distributor of consumer products and served in several financial and strategic roles (Controller — Ice Cream Division; Strategic Planning Manager for the WHISKAS ® Brand) and various other financial management positions. Prior to joining Mars, Inc., Mr. Hackworth spent six years at Deloitte & Touche LLP as an auditor, specializing in the manufacturing and retail industries.

Menno V. Koopmans is our Senior Vice President and Managing Director, Europe. From 2014 to the end of 2016, he was our Senior Vice President for subscription broadcasting business in Europe and India where he led the customer transition into smart remote controls. From 2005 until 2013, he was the head of our worldwide consumer business and its One For All® brand. Prior to joining us, Mr. Koopmans worked at Mars, Sony Europe and Royal Philips Electronics in different product, marketing and sales management roles in both fast-moving consumer goods and durable consumer goods categories. Mr. Koopmans received his Masters in Science of Business Administration from Erasmus University in Rotterdam, The Netherlands.

ITEM 1A. RISK FACTORS

Forward-Looking Statements

We make forward-looking statements in Management's Discussion and Analysis of Financial Condition and Results of Operations and elsewhere in this report based on the beliefs and assumptions of our management and on information currently available to us. Forward-looking statements include information about our possible or assumed future results of operations, which follow under the headings "Business", "Liquidity and Capital Resources", and other statements throughout this report preceded by, followed by or that include the words "believes", "expects", "anticipates", "intends", "plans", "estimates" or similar expressions.

Any number of risks and uncertainties could cause actual results to differ materially from those we express in our forward-looking statements, including the risks and uncertainties we describe below and other factors we describe from time to time in our periodic filings with the U.S. Securities and Exchange Commission (the "SEC"). We therefore caution you not to rely unduly on any forward-looking statement. The forward-looking statements in this report speak only as of the date of this report, and we undertake no obligation to update or revise any forward-looking statement, whether as a result of new information, future developments, or otherwise.

Risks and Uncertainties

We are subject to various risks that could have a negative effect on us or on our financial condition. You should understand that these risks could cause results to differ materially from those we express in forward-looking statements contained in this report or in other Company communications. Because there is no way to determine in advance whether, or to what extent, any present uncertainty will ultimately impact our business, you should give equal weight to each of the following:

9

Risks Related to Doing Business in the PRC

We manufacture a majority of our products in our factories in the PRC. Additionally, many of our contract manufacturers are located in the PRC. Doing business in the PRC carries a number of risks including the following:

Changes in the policies of the PRC government may have a significant impact upon the business we may be able to conduct in the PRC and the profitability of such business.

Our business operations may be adversely affected by the current and future political environment in the PRC. The government of the PRC has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy, through regulation and state ownership. Our ability to operate in the PRC may be adversely affected by changes in Chinese laws and regulations, including those relating to taxation, labor and social insurance, import and export tariffs, raw materials, environmental regulations, land use rights, property and other matters.

The PRC laws and regulations governing our current business operations are sometimes vague and uncertain. Any changes in such PRC laws and regulations may harm our business.

There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations, including but not limited to the laws and regulations governing our business, or the enforcement and performance of our arrangements with customers in the event of the imposition of statutory liens, death, bankruptcy and criminal proceedings. We cannot predict what effect the interpretation of existing or new PRC laws or regulations may have on our business. If the relevant authorities find that we are in violation of PRC laws or regulations, they would have broad discretion in dealing with such a violation, including, without limitation:

• | levying fines; |

• | revoking our business and other licenses; |

• | requiring that we restructure our ownership or operations; and |

• | requiring that we discontinue any portion or all of our business. |

The fluctuation of the Chinese Yuan Renminbi may harm your investment.

Under Chinese monetary policy, the Chinese Yuan Renminbi is permitted to fluctuate within a managed band against a basket of certain foreign currencies and has resulted in a 16.9% appreciation of the Chinese Yuan Renminbi against the U.S. Dollar through December 31, 2016. While the international reaction to the Chinese Yuan Renminbi revaluation has been positive, there remains international pressure on the PRC government to adopt an even more flexible currency policy, which may result in a further and more significant appreciation of the Chinese Yuan Renminbi against the U.S. Dollar, which could lead to higher manufacturing costs for our products.

The PRC's legal and judicial system may not adequately protect our business and operations and the rights of foreign investors.

The PRC legal and judicial system may negatively impact foreign investors, with enforcement of existing laws inconsistent. In addition, the promulgation of new laws, changes to existing laws and the pre-emption of local regulations by national laws may adversely affect foreign investors.

Availability of adequate workforce levels

Presently, the vast majority of workers at our PRC factories are obtained from third-party employment agencies. As the labor laws, social insurance and wage levels continue to mature and grow and the workers become more sophisticated, our costs to employ these and other workers in the PRC may grow beyond that anticipated by management. In addition, as the PRC market continues to open up and grow, with the advent of more companies opening plants and businesses in the PRC, we may experience an increase in competition for the same workers, resulting in either an inability to attract and retain an adequate number of qualified workers or an increase in our employment costs to obtain and retain these workers.

Expansion in the PRC

As our global business grows, we may decide to expand in China to meet demand. This would be dependent on our ability to locate suitable facilities to support this expansion, to obtain the necessary permits and funding, to attract and retain adequate levels of qualified workers, and to enter into a long-term land lease that is common in the PRC.

Sale of Guangzhou factory

On September 26, 2016, we entered into an agreement to sell our Guangzhou manufacturing facility. The sale is expected to close in 2018. In anticipation of a successful closing of the sale, we have been transitioning manufacturing activities from this factory to our other three China factories. However, if we are unable to successfully complete this transition as anticipated or are unable to obtain necessary personnel at our other factories, this could have a material adverse effect on our results of operations and

10

financial condition. Additionally, if the sale does not close, we may incur unexpected costs associated with an unutilized factory, we may incur additional costs to sell the factory to another buyer, and we may be forced to sell the factory at a less favorable price.

Risks and Uncertainties Associated with Our Expansion Into and Our Operations Outside of the United States May Adversely Affect Our Results of Operations, Cash Flow, Liquidity or Financial Condition

Net external sales of our consolidated foreign subsidiaries totaled approximately 41.0%, 43.5% and 55.2% of our total consolidated net sales in 2016, 2015 and 2014, respectively. We expect that the international share of our total revenues will continue to make up a significant part of our current business and future strategic plans. Additionally, we operate factories in the PRC, Brazil and Mexico, as well as an engineering center in India. As a result, we are increasingly exposed to the challenges and risks of doing business outside the United States, which could reduce our revenues or profits, increase our costs, result in significant liabilities or sanctions, or otherwise disrupt our business. These challenges include: (1) compliance with complex and changing laws, regulations and policies of governments that may impact our operations, such as foreign ownership restrictions, import and export controls, tariffs, and trade restrictions; (2) compliance with U.S. and foreign laws that affect the activities of companies abroad, such as anti-corruption laws, competition laws, currency regulations, and laws affecting dealings with certain nations; (3) limitations on our ability to repatriate non-U.S. earnings in a tax effective manner; (4) the difficulties involved in managing an organization doing business in many different countries; (5) uncertainties as to the enforceability of contract and intellectual property rights under local laws; (6) rapid changes in government policy, political or civil unrest in the Middle East and elsewhere, acts of terrorism, or the threat of international boycotts or U.S. anti-boycott legislation; and (7) currency exchange rate fluctuations.

We are also exposed to risks relating to U.S. policy with respect to companies doing business in foreign jurisdictions, particularly in light of the new U.S. presidential administration. Legislation or other changes in the U.S. tax laws could increase our U.S. income tax liability and adversely affect our after-tax profitability. For example, U.S. lawmakers are considering several U.S. corporate tax reform proposals, including, among others, proposals which could reduce or eliminate U.S. income tax deferrals on unrepatriated foreign earnings and eliminate tax incentives in exchange for a lower U.S. statutory tax rate. In addition, the new U.S. presidential administration has introduced greater uncertainty with respect to future tax, trade regulations and trade agreements. Changes in tax policy, trade regulations or trade agreements, such as the disallowance of tax deductions on imported merchandise or the imposition of new tariffs on imported products, could have a material adverse effect on our business and results of operations.

Failure by Our International Operations to Comply With Anti-Corruption Laws or Trade Sanctions Could Increase Our Costs, Reduce Our Profits, Limit Our Growth, Harm Our Reputation, or Subject us to Broader Liability

We are subject to restrictions imposed by the U.S. Foreign Corrupt Practices Act and anti-corruption laws and regulations of other countries applicable to our operations. Anti-corruption laws and regulations generally prohibit companies and their intermediaries from making improper payments to government officials or other persons in order to receive or retain business. The compliance programs, internal controls and policies we maintain and enforce to promote compliance with applicable anti-bribery and anti-corruption laws may not prevent our associates, contractors or agents from acting in ways prohibited by these laws and regulations. We are also subject to trade sanctions administered by the Office of Foreign Assets Control and the U.S. Department of Commerce. Our compliance programs and internal controls also may not prevent conduct that is prohibited under these rules. The United States may impose additional sanctions at any time against any country in which or with whom we do business. Depending on the nature of the sanctions imposed, our operations in the relevant country could be restricted or otherwise adversely affected. Any violations of anti-corruption laws and regulations or trade sanctions could result in significant civil and criminal penalties, reduce our profits, disrupt our business or damage our reputation. In addition, an imposition of further restrictions in these areas could increase our cost of operations, reduce our profits or cause us to forgo development opportunities that would otherwise support growth.

Fluctuations in Foreign Currency Exchange Rates May Adversely Affect Our Results of Operations, Cash Flow, Liquidity or Financial Condition.

Because of our international operations, we are exposed to risk associated with interest rates and value changes in foreign currencies, which may adversely affect our business. Historically, our reported net sales, earnings, cash flow and financial condition have been subjected to fluctuations in foreign exchange rates. Our primary exchange rate exposure is in the Argentinian Peso, Brazilian Real, British Pound, Chinese Yuan Renminbi, Euro, Hong Kong Dollar, Indian Rupee, Japanese Yen and Mexican Peso. While we actively manage the exposure of our foreign currency risk as part of our overall financial risk management policy, we believe we may experience losses from foreign currency exchange rate fluctuations, and such losses may adversely affect our sales, earnings, cash flow, liquidity or financial condition.

11

Risks Relating to Natural or Man-made Disasters, Contagious Disease, Terrorist Activity, and War May Adversely Affect Our Business, Financial Condition and Results of Operations

Our ability, including manufacturing or distribution capabilities, and that of our suppliers, business partners and contract manufacturers, to make, move and sell products is critical to our success. So called “Acts of God,” such as hurricanes, earthquakes, tsunamis, and other natural disasters, as well as the potential spread of contagious diseases such as MERS (Middle East Respiratory Syndrome), Zika virus, and Ebola in locations where we or they own or operate significant operations could cause a disruption in our or our third party’s production and distribution capabilities or a decline in demand for our products and services. In addition, actual or threatened war, terrorist activity, political unrest, or civil strife, such as recent events in Ukraine and Russia, the Middle East, and other geopolitical uncertainty could have a similar effect. Any one or more of these events may reduce our ability to produce or sell our products which may adversely affect our business, financial condition and results of operations, as well as require additional resources to restore our supply chain.

Dependence on Foreign Manufacturing

Although we own and operate factories in the PRC, Brazil and Mexico, third-party manufacturers located in Asia continue to manufacture a portion of our products. Our arrangements with these foreign manufacturers are subject to the risks of doing business abroad, such as tariffs, environmental and trade restrictions, intellectual property protection and enforcement, export license requirements, work stoppages, political and social instability, economic and labor conditions, foreign currency exchange rate fluctuations, changes in laws and policies (including fiscal policies), and other factors, which may have a material adverse effect on our business, results of operations and cash flows. We believe that the loss of any one or more of our manufacturers would not have a long-term material adverse effect on our business, results of operations and cash flows, because numerous other manufacturers are available to fulfill our requirements; however, the loss of any of our major manufacturers may adversely affect our business, operating results, financial condition and cash flows until alternative manufacturing arrangements are secured.

Dependence upon Key Suppliers

Most of the components used in our products are available from multiple sources. However, we purchase integrated circuits, used principally in our wireless control products, from a small number of key suppliers. To reduce our dependence on our integrated circuit suppliers we continually seek additional sources. We maintain inventories of our integrated circuits, which may be used in part to mitigate, but not eliminate, delays resulting from supply interruptions.

We have identified alternative sources of supply for our integrated circuit, component parts, and finished goods needs; however, there can be no assurance that we will be able to continue to obtain these inventory purchases on a timely basis. Any extended interruption, shortage or termination in the supply of any of the components used in our products, or a reduction in their quality or reliability, or a significant increase in prices of components, would have an adverse effect on our operating results, financial position and cash flows.

Patents, Trademarks, and Copyrights

The procedures by which we identify, document and file for patent, trademark, and copyright protection are based solely on engineering and management judgment, with no assurance that a specific filing will be issued, or if issued, will deliver any lasting value to us. Because of the rapid innovation of products and technologies that is characteristic of our industry, there can be no assurance that rights granted under any patent will provide competitive advantages to us or will be adequate to safeguard and maintain our proprietary rights. Moreover, the laws of certain countries in which our products are or may be manufactured or sold may not offer protection on such products and associated intellectual property to the same extent that the United States legal system may offer.

In our opinion, our intellectual property holdings as well as our engineering, production, and marketing skills and the experience of our personnel are of equal importance to our market position. We further believe that our business is not materially dependent upon any single patent, copyright, trademark, or trade secret.

Some of our products include or use technology and/or components of third parties. While it may be necessary in the future to seek or renew licenses relating to various aspects of such products, we believe that, based upon past experience and industry practice, such licenses may be obtained on commercially reasonable terms; however, there can be no guarantee that such licenses may be obtained on such terms or at all. Because of technological changes in the wireless and home control industry, current extensive patent coverage, and the rapid rate of issuance of new patents, it is possible certain components of our products and business methods may unknowingly infringe upon the patents of others.

12

Potential for Litigation

As is typical in our industry and for the nature and kind of business in which we are engaged, from time to time various claims, charges and litigation are asserted or commenced by third parties against us or by us against third parties, arising from or related to product liability, infringement of patent or other intellectual property rights, breach of warranty, contractual relations or employee relations. The amounts claimed may be substantial, but they may not bear any reasonable relationship to the merits of the claims or the extent of any real risk of court awards assessed against us or in our favor.

Technology Changes in Wireless Control

We currently derive substantial revenue from the sale of wireless remote controls based on IR and RF and other technologies. Other control technologies exist or may be developed that may compete with this technology. In addition, we develop and maintain our own database of IR and RF codes. There are competing IR and RF libraries offered by companies that we compete with in the marketplace. The advantage that we may have compared to our competitors is difficult to measure. In addition, if other wireless control technology gains acceptance and starts to be integrated into home electronics devices currently controlled through our remote controllers, demand for our products may decrease, resulting in decreased operating results, financial condition, and cash flows.

Our Technology Development Activities May Experience Delays.

We may experience technical, financial, resource or other difficulties or delays related to the further development of our technologies. Delays may have adverse financial effects and may allow competitors with comparable technology offerings to gain an advantage over us in the marketplace or in the standards setting arena. There can be no assurance that we will continue to have adequate staffing or that our development efforts will ultimately be successful. Moreover, certain of our technologies have not been fully tested in commercial use, and it is possible that they may not perform as expected. In such cases, our business, financial condition and operating results may be adversely affected, and our ability to secure new licensees and other business opportunities may be diminished.

Change in Competition and Pricing

Even with having our own factories located in the PRC, Brazil and Mexico, we will continue to rely on third-party manufacturers to build a portion of our universal wireless control products. Price is always an issue in winning and retaining business. If customers become increasingly price sensitive, new competition may arise from manufacturers who decide to go into direct competition with us or from current competitors who perform their own manufacturing. If such a trend develops, we may experience downward pressure on our pricing or lose sales, which may have a material adverse effect on our operating results, financial condition and cash flows.

Risks Related to Adverse Changes in General Business and Economic Conditions

Adverse changes in general business and economic conditions in the United States and worldwide may reduce the demand for some of our products and adversely affect our results of operations, cash flow, liquidity or financial condition. Higher inflation rates, interest rates, tax rates and unemployment rates, higher labor and health care costs, recessions, changing governmental policies, laws and regulations, increased tariffs, and other economic factors may adversely affect our results of operations, cash flow, liquidity or financial condition. Any such changes may impact our business in a number of ways, including:

Potential deferment of purchases and orders by customers and cyclical nature of portions of our business

Uncertainty about current and future global economic conditions may cause consumers, businesses and governments to defer purchases in response to tighter credit, decreased cash availability and declining consumer confidence. Accordingly, future demand for our products may differ materially from our current expectations.

In addition, portions of our business involve the sale of products to sectors of the economy that are cyclical in nature, particularly the retail sector. Our sales to these sectors are affected by the levels of discretionary consumer and business spending. During economic downturns, the levels of consumer and business discretionary spending in these sectors may decrease, and the recovery of these sectors may lag behind the recovery of the overall economy. This decrease in spending will likely reduce the demand for some of our products and may adversely affect our sales, earnings, cash flow or financial condition. Although many of our end markets have shown signs of stabilization and modest improvement from the recent global economic downturn, the recovery has been erratic. A worsening in these sectors may cause a reduction in the demand for some of our products and may adversely impact sales, earnings, cash flow and financial condition.

13

Customers' inability to obtain financing to make purchases from us and/or maintain their business

Some of our customers require substantial financing in order to fund their operations and make purchases from us. The inability of these customers to obtain sufficient credit to finance purchases of our products may adversely impact our financial results. In addition, an economic downturn could result in insolvencies for our customers, which may adversely impact our financial results.

Potential impact on trade receivables

Credit market conditions may slow our collection efforts as customers experience increased difficulty in obtaining requisite financing, leading to higher than normal accounts receivable balances and longer days sales outstanding. Continuation of these conditions may limit our ability to collect our accounts receivable, which may result in greater expense associated with collection efforts and increased bad debt expense.

Negative impact from increased financial pressures on third-party dealers, distributors and retailers

We make sales in certain regions of the world through third-party dealers, distributors and retailers. Although many of these third parties have significant operations and maintain access to available credit, others are smaller and more likely to be impacted by a significant decrease in available credit. If credit pressures or other financial difficulties result in insolvency for these third parties and we are unable to successfully transition our end customers to purchase products from other third parties or from us directly, it may adversely impact our financial results.

Negative impact from increased financial pressures on key suppliers

Our ability to meet customers' demands depends, in part, on our ability to obtain timely and adequate delivery of quality materials, parts and components from our suppliers. Certain of our components are available only from a single source or limited sources. If certain key suppliers were to become capacity constrained or insolvent as a result of an economic downturn, it may result in a reduction or interruption in supplies or a significant increase in the price of supplies and adversely impact our financial results. In addition, credit constraints at key suppliers may result in accelerated payment of accounts payable by us, impacting our cash flow.

Potential Fluctuations in Quarterly Results

We may from time to time increase our operating expenses to fund greater levels of research and development, sales and marketing activities, development of new distribution channels, improvements in our operational and financial systems and development of our customer support capabilities, and to support our efforts to comply with various government regulations. To the extent such expenses precede or are not subsequently followed by increased revenues, our business, operating results, financial condition and cash flows will be adversely affected.

In addition, we may experience significant fluctuations in future quarterly operating results that may be caused by many other factors, including demand for our products, introduction or enhancement of products by us and our competitors, the loss or acquisition of any significant customers, market acceptance of new products, price reductions by us or our competitors, mix of distribution channels through which our products are sold, product or supply constraints, level of product returns, mix of customers and products sold, component pricing, mix of international and domestic revenues, foreign currency exchange rate fluctuations and general economic conditions. In addition, as a strategic response to changes in the competitive environment, we may from time to time make certain pricing or marketing decisions or acquisitions that may have a material adverse effect on our business, results of operations or financial condition. As a result, we believe period-to-period comparisons of our results of operations are not necessarily meaningful and should not be relied upon as an indication of future performance.

Due to all of the foregoing factors, it is possible that in some future quarters our operating results will be below the expectations of public market analysts and investors. If this happens the price of our common stock may be materially adversely affected.

Our Ability to Generate Cash Depends on Many Factors Beyond Our Control. We Also Depend on the Business of Our Subsidiaries to Satisfy Our Cash Needs.

Our historical financial results have been, and we anticipate that our future financial results will be, subject to fluctuations. Our ability to generate cash is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control. We cannot assure you that our business will generate sufficient cash flow from our operations or that future borrowings will be available to us in an amount sufficient to enable us to make payments of our debt, fund our other liquidity needs and make planned capital expenditures.

A significant portion of our operations are conducted through our subsidiaries. As a result, our ability to generate sufficient cash flow for our needs is dependent to some extent on the earnings of our subsidiaries and the payment of those earnings to us in the form of dividends, loans or advances and through repayment of loans or advances from us. Our subsidiaries are separate and distinct legal entities. Our subsidiaries have no obligation to pay any amounts due on our debt or to provide us with funds to meet

14

our cash flow needs, whether in the form of dividends, distributions, loans or other payments. In addition, any payment of dividends, loans or advances by our subsidiaries may be subject to statutory or contractual restrictions. Payments to us by our subsidiaries will also be contingent upon our subsidiaries' earnings and business considerations. Our right to receive any assets of any of our subsidiaries upon their liquidation or reorganization will be effectively subordinated to the claims of that subsidiary's creditors, including trade creditors. In addition, even if we are a creditor of any of our subsidiaries, our rights as a creditor would be subordinate to any security interest in the assets of our subsidiaries and any indebtedness of our subsidiaries senior to that held by us. Further, changes in the laws of foreign jurisdictions in which we operate may adversely affect the ability of some of our foreign subsidiaries to repatriate funds to us.

In addition, we may fund a portion of our seasonal working capital needs and obtain funding for other general corporate purposes through short-term borrowings backed by our revolving credit facility and other financing facilities. If any of the banks in these credit and financing facilities are unable to perform on their commitments, which may adversely affect our ability to fund seasonal working capital needs and obtain funding for other general corporate purposes, our cash flow, liquidity or financial condition may be adversely impacted. Although we currently have available credit facilities to fund our current operating needs, we cannot be certain that we will be able to replace our existing credit facilities or refinance our existing or future debt when necessary. Our cost of borrowing and ability to access the capital markets are affected not only by market conditions, but also by our debt and credit ratings assigned by the major credit rating agencies. Downgrades in these ratings will increase our cost of borrowing and may have an adverse effect on our access to the capital markets, including our access to the commercial paper market. An inability to access the capital markets may have a material adverse effect on our results of operations, cash flow, liquidity or financial condition.

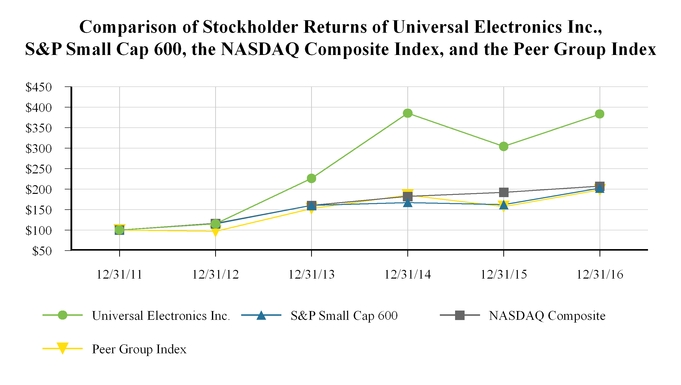

The Price of Our Common Stock is Volatile and May Decline Regardless of Our Operating Performance.

Historically, we have had large fluctuations in the price of our common stock, and such fluctuations may continue. From January 1, 2012 to March 6, 2017, the trading price of our common stock has ranged from a low of $11.40 per share to a high of $80.42 per share. The market price for our common stock is volatile and may fluctuate significantly in response to a number of factors, most of which we cannot control, including:

• | the public's response to press releases or other public announcements by us or third parties, including our filings with the SEC and announcements relating to product and technology development, relationships with new and existing customers, litigation and other legal proceedings in which we are involved and intellectual property impacting us or our business; |

• | announcements concerning strategic transactions, such as spin-offs, joint ventures and acquisitions or divestitures; |

• | the financial projections we may provide to the public, any changes in these projections or our failure to meet these projections; |

• | changes in financial estimates or ratings by any securities analysts who follow our common stock, our failure to meet these estimates or failure of those analysts to initiate or maintain coverage of our common stock; |

• | investor perceptions as to the likelihood of achievement of near-term goals; |

• | changes in market share of significant customers; |

• | changes in operating performance and stock market valuations of other technology or content providing companies generally; and |

• | market conditions or trends in our industry or the economy as a whole. |

In the past, stockholders have instituted securities class action litigation following periods of market volatility. If we were involved in securities litigation, we may incur substantial costs and our resources and the attention of management may be diverted from our business.

In addition, our executive officers periodically sell shares of our common stock which they own, often pursuant to trading plans established under Rule 10b5-1 of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Sales of shares by our executive officers may not be indicative of their respective opinions of our performance at the time of sale or of our potential future performance. Nonetheless, the market price of our stock may be affected by such sales of shares by our executive officers.

If Securities or Industry Analysts Fail to Continue Publishing Research About Our Business, Our Stock Price and Trading Volume May Decline.

The trading market for our common stock is influenced by the research and reports that industry or securities analysts publish about us or our business. If one or more of these analysts cease coverage of our company or fail to publish reports on us regularly, we may lose visibility in the financial markets, which in turn may cause our stock price or trading volume to decline.

15

Future Sales of Our Equity May Depress the Market Price of Our Common Stock.

We have several institutional stockholders that own significant blocks of our common stock. If one or more of these stockholders were to sell large portions of their holdings in a relatively short time, for liquidity or other reasons, the prevailing market price of our common stock may be negatively affected. Additionally, in March 2016, we issued common stock purchase warrants to Comcast Corporation ("Comcast") to purchase up to 725,000 shares of our common stock at a price of $54.55 per share. The right to exercise the warrants is subject to vesting over three successive two-year periods (with the first two-year period commencing on January 1, 2016) based on the level of purchases of goods and services from us by Comcast and its affiliates, as defined in the warrants. To the extent that the warrants vest and Comcast exercises the warrants and sells any of the shares of common stock issuable upon exercise, or the perception that such sales may occur, could adversely affect the market price of our common stock.

Approved Stock Repurchase Programs May Not Result in a Positive Return of Capital to Stockholders.

Our board-approved stock repurchase programs may not return value to stockholders because the market price of the stock may decline significantly below the levels at which we repurchased shares of stock. Stock repurchase programs are intended to deliver stockholder value over the long term, but stock price fluctuations can reduce the effectiveness of such programs.

Dependence on Consumer Preference

We are susceptible to fluctuations in our business based upon consumer demand for our products. In addition, we cannot guarantee that increases in demand for our products associated with increases in the deployment of new technology will continue. We believe that our success depends on our ability to anticipate, gauge and respond to fluctuations in consumer preferences. However, it is impossible to predict with complete accuracy the occurrence and effect of fluctuations in consumer demand over a product's life cycle. Moreover, any growth in revenues that we achieve may be transitory and should not be relied upon as an indication of future performance.

Demand for Consumer Service and Support

We have continually provided domestic and international consumer service and support to our customers to add overall value and to help differentiate us from our competitors. We continually review our service and support group and are marketing our expertise in this area to other potential customers. There can be no assurance that we will be able to attract new customers in the future.

In addition, certain of our products have more features and are more complex than others and therefore require more end-user technical support. In some instances, we rely on distributors or dealers to provide the initial level of technical support to the end-users. We provide the second level of technical support for bug fixes and other issues at no additional charge. Therefore, as the mix of our products includes more of these complex product lines, support costs may increase, which may have an adverse effect on our business, operating results, financial condition and cash flows.

Dependence upon New Product Introduction

Our ability to remain competitive in the wireless control and AV accessory products market will depend considerably upon our ability to successfully identify new product opportunities, as well as develop and introduce these products and enhancements on a timely and cost effective basis. There can be no assurance that we will be successful at developing and marketing new products or enhancing our existing products, or that these new or enhanced products will achieve consumer acceptance and, if achieved, will sustain that acceptance. In addition, there can be no assurance that products developed by others will not render our products non-competitive or obsolete or that we will be able to obtain or maintain the rights to use proprietary technologies developed by others which are incorporated in our products. Any failure to anticipate or respond adequately to technological developments and customer requirements, or any significant delays in product development or introduction, may have a material adverse effect on our operating results, financial condition and cash flows.

In addition, the introduction of new products may require significant expenditures for research and development, tooling, manufacturing processes, inventory and marketing. In order to achieve high volume production of any new product, we may have to make substantial investments in inventory and expand our production capabilities.

Dependence on Major Customers

The economic strength and weakness of our worldwide customers affect our performance. We sell our wireless control products, AV accessory products, and proprietary technologies to subscription broadcasters, original equipment manufacturers, retailers and private label customers. We also supply our products to our wholly owned, non-U.S. subsidiaries and to independent foreign distributors, who in turn distribute our products worldwide, with Europe, Asia and Latin America currently representing our principal foreign markets.

16

During the years ended December 31, 2016 and 2015, we had sales in excess of 10% of our net sales to each of Comcast and DIRECTV and its sub-contractors. During the year ended December 31, 2014, we had sales to DIRECTV and its sub-contractors that totaled in excess of 10% of our net sales. The loss of any of these customers or of any other key customer, either in the United States or abroad or our inability to maintain order volume with these customers, may have an adverse effect on our operating results, financial condition and cash flows.

Outsourced Labor

We continue to use outside resources to assist us in the development of some of our products and technologies. While we believe that such outside services will continue to be available to us, if they cease to be available, the development of these products and technologies may be substantially delayed, which may have a material adverse effect on our operating results, financial condition and cash flows.

Disruptions Caused by Labor Disputes or Organized Labor Activities Could Materially Harm our Business and Reputation

Currently, approximately 400 of our Brazil and Mexico employees are represented by labor unions. Disputes with the current labor unions or new union organizing activities could lead to production slowdowns or stoppages and make it difficult or impossible for us to meet scheduled delivery times for product shipments to some of our customers, which could result in a loss of business and material damage to our reputation. In addition, union activity and compliance with international labor standards could result in higher labor costs, which could have a material adverse effect on our financial position and results of operations.

Competition

Competition within the wireless control industry is based primarily on product availability, price, speed of delivery, ability to tailor specific solutions to customer needs, quality, and depth of product lines. Our competition is fragmented across our products, and, accordingly, we do not compete with any one company across all product lines. We compete with a variety of entities, some of which have greater financial resources. Other competitors are smaller and may be able to offer more specialized products. Our ability to remain competitive in this industry depends in part on our ability to successfully identify new product opportunities, develop and introduce new products and enhancements on a timely and cost effective basis, as well as our ability to successfully identify and enter into strategic alliances with entities doing business within the industries we serve. Competition in any of these areas may reduce our sales and adversely affect our earnings or cash flow by resulting in decreased sales volumes, reduced prices and increased costs of manufacturing, distributing and selling our products. There can be no assurance that our product offerings will be, and/or will remain, competitive or that strategic alliances, if any, will achieve the type, extent, and amount of success or business that we expect them to achieve. The sales of our products and technology may not occur or grow in the manner we expect, and thus we may not recoup costs incurred in the research and development of these products as quickly as we expect, if at all.

The home security and automation industry is highly fragmented and subject to significant competition and pricing pressures. In particular, the monitored security industry providers have highly recognized brands which may drive increased awareness of their security/automation offerings rather than ours, have access to greater capital and resources than us, and may spend significantly more on advertising, marketing and promotional resources which could have a material adverse effect on our ability to drive awareness and demand for our products and services. In addition, cable and telecommunications companies have expanded into the monitored security industry and are bundling their existing offerings with monitored security services. We also face competition from Do-It-Yourself (DIY) companies that are increasingly provided products which enable customers to self-monitor and control their environments without third-party involvement. Further, DIY providers may also offer professional monitoring with the purchase of their systems and equipment or new IoT devices and services with automated features and capabilities that may be appealing to customers. Continued pricing pressure, improvements in technology and shifts in customer preferences towards self-monitoring or DIY could adversely impact our customer base and/or pricing structure and have a material adverse effect on our business, financial condition, results of operations and cash flows.

We are Exposed to Greater Risks of Liability for Omissions or System Failures