UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 3, 2018

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-12107

ABERCROMBIE & FITCH CO.

(Exact name of registrant as specified in its charter)

Delaware | 31-1469076 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

6301 Fitch Path, New Albany, Ohio | 43054 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (614) 283-6500

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Class A Common Stock, $0.01 Par Value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | x | Accelerated filer | ¨ |

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Emerging growth company | ¨ | ||

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes x No

Aggregate market value of the Registrant’s Class A Common Stock (the only outstanding common equity of the Registrant) held by non-affiliates of the Registrant (for this purpose, executive officers and directors of the Registrant are considered affiliates) as of July 28, 2017: $662,946,023.

Number of shares outstanding of the Registrant’s common stock as of March 28, 2018: 68,032,248 shares of Class A Common Stock.

DOCUMENT INCORPORATED BY REFERENCE:

Portions of the Registrant’s definitive proxy statement for the Annual Meeting of Stockholders, to be held on June 14, 2018, are incorporated by reference into Part III of this Annual Report on Form 10-K.

ABERCROMBIE & FITCH CO.

TABLE OF CONTENTS

ITEM 1. | ||

ITEM 1A. | ||

ITEM 1B. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

ITEM 5. | ||

ITEM 6. | ||

ITEM 7. | ||

ITEM 7A. | ||

ITEM 8. | ||

ITEM 9. | ||

ITEM 9A. | ||

ITEM 9B. | ||

ITEM 10. | ||

ITEM 11. | ||

ITEM 12. | ||

ITEM 13. | ||

ITEM 14. | ||

ITEM 15. | ||

ITEM 16. | ||

PART I

ITEM 1. | BUSINESS |

GENERAL.

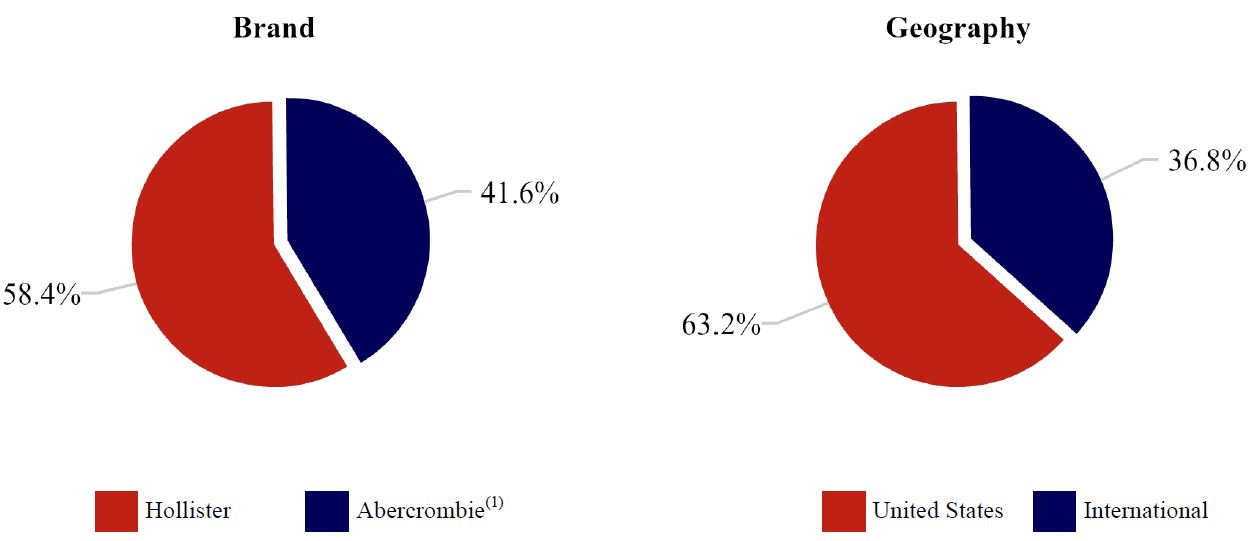

Abercrombie & Fitch Co. (“A&F”), a company incorporated in Delaware in 1996, through its subsidiaries (collectively, A&F and its subsidiaries are referred to as the “Company” and “we”), is a global, multi-brand specialty retailer, which primarily sells its products through its wholly-owned store and direct-to-consumer channels, as well as through various third-party wholesale, franchise and licensing arrangements. The Company offers a broad assortment of apparel, personal care products and accessories for men, women and kids under the Hollister, Abercrombie & Fitch and abercrombie kids brands. The brands share a commitment to offering products of enduring quality and exceptional comfort that allows customers around the world to express their own individuality and style. The Company has operations in North America, Europe, Asia and the Middle East. For the fifty-three week period ended February 3, 2018, 63.2% of the Company’s net sales were attributable to the United States (“U.S.”).

The Company’s fiscal year ends on the Saturday closest to January 31, typically resulting in a fifty-two week year, but occasionally giving rise to an additional week, resulting in a fifty-three week year, as was the case for the year ended February 3, 2018. Fiscal years are designated in the consolidated financial statements and notes, as well as the remainder of this Annual Report on Form 10-K, by the calendar year in which the fiscal year commenced. All references herein to the Company’s fiscal years are as follows:

Fiscal year | Year ended | Number of weeks | ||

Fiscal 2015 | January 30, 2016 | 52 | ||

Fiscal 2016 | January 28, 2017 | 52 | ||

Fiscal 2017 | February 3, 2018 | 53 | ||

Fiscal 2018 | February 2, 2019 | 52 | ||

A&F makes available free of charge on its website, corporate.abercrombie.com, under “Investors, Financials, SEC Filings,” its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or Section 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as well as A&F’s definitive proxy materials filed pursuant to Section 14 of the Exchange Act, as soon as reasonably practicable after A&F electronically files such material with, or furnishes it to, the Securities and Exchange Commission (“SEC”). The SEC maintains a website that contains electronic filings by A&F and other issuers at www.sec.gov. In addition, the public may read and copy any materials A&F files with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

The Company has included certain of its website addresses throughout this filing as textual references only. The information contained within these websites is not incorporated into this Annual Report on Form 10-K.

BRANDS.

Hollister. The quintessential apparel brand of the global teen consumer, Hollister celebrates the liberating spirit of the endless summer inside everyone. Inspired by California’s laidback attitude, Hollister’s clothes are designed to be lived in and made your own, for wherever life takes you. Hollister provides an engaging, welcoming and unique shopping experience around the globe. Hollister also carries intimates brand, Gilly Hicks, “the brand to start and end your day with.” Gilly Hicks product is designed to be effortless and comfortable to align with customers’ on-the-go, busy lifestyle.

Abercrombie & Fitch. Abercrombie & Fitch is a specialty retailer of high-quality apparel and accessories for men and women. For 125 years, the iconic brand has outfitted innovators, explorers and entrepreneurs. Today, it reflects an updated attitude of the 21 to 24-year old customer, while remaining true to its heritage of creating expertly crafted products with an effortless, American style.

abercrombie kids. abercrombie kids creates smart and creative apparel of enduring quality that celebrates the wide-eyed wonder of children from 5 to 14 years. Its products are made for play — tough enough to stand up to everyday adventures.

3

SEASONAL BUSINESS.

The retail industry has two principal selling seasons: the Spring season, which includes the first and second fiscal quarters (“Spring”); and the Fall season, which includes the third and fourth fiscal quarters (“Fall”). As is common in the retail industry, the Company experiences its greatest sales activity during the Fall season due to Back-to-School and Back-to-Fall in August for Hollister and Abercrombie, respectively, and the holiday sales periods in November and December.

COMPETITION.

The Company operates in a rapidly evolving and highly competitive retail business environment. Competitors include individual and chain specialty apparel retailers, local, regional, national and international department stores, discount stores and online businesses. Additionally, the Company competes for consumers’ discretionary spending with businesses in other product and experiential categories, such as technology, restaurants, travel and media content. The Company competes primarily on the basis of quality, fashion, brand experience and selection.

Operating in a highly competitive industry environment can cause the Company to engage in greater promotional activity, resulting in pressure on average unit retail and gross profit. Refer to “ITEM 1A. RISK FACTORS,” for further discussion of the potential impacts competition may have on the Company.

STRATEGIC INITIATIVES.

The Company is focused on putting the customer at the center of everything it does and engaging with them wherever, whenever and however they choose to shop, through its three strategic pillars:

• | inspiring customers; |

• | innovating relentlessly; and |

• | developing leaders. |

Through the continued execution of the Company's brand playbooks, the Company is aligning product, brand voice and experience around the customer and is building and enhancing capabilities to react to a rapidly evolving retail landscape.

FINANCIAL INFORMATION ABOUT SEGMENTS.

The Company determines its segments on the same basis that it uses to allocate resources and assess performance. The Company’s two operating segments as of February 3, 2018 are brand-based: Hollister and Abercrombie, the latter of which includes the Company’s Abercrombie & Fitch and abercrombie kids brands. Both of the Company’s operating segments sell a similar group of products — apparel, personal care products and accessories for men, women and kids. These operating segments have similar economic characteristics, classes of consumers, products, production and distribution methods, operate in the same regulatory environments, and have been aggregated into one reportable segment. Refer to “ITEM 6. SELECTED FINANCIAL DATA,” “RESULTS OF OPERATIONS” in “ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS” and Note 17, “SEGMENT REPORTING,” of the Notes to Consolidated Financial Statements included in “ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA,” of this Annual Report on Form 10-K for for further discussion and information of the Company’s operating segments and reportable segment as well as information about the geographic areas in which the Company operates.

4

The following charts illustrate the Company’s net sales by brand and geography for Fiscal 2017:

(1) | Includes Abercrombie & Fitch and abercrombie kids brands. |

CHANNELS OF OPERATIONS.

Stores. The Company continues to evaluate and manage its store fleet through its ongoing channel optimization program to address shifts in customer preferences. Actions taken to optimize store productivity include remodeling, relocating, downsizing and store closings. At the end of Fiscal 2017, the Company operated 868 stores. The following table details the number of retail stores operated by the Company as of February 3, 2018:

Hollister (1) | Abercrombie (2) | Total | ||||

United States | 394 | 285 | 679 | |||

International | 144 | 45 | 189 | |||

Total | 538 | 330 | 868 | |||

(1) | Excludes five international franchise stores as of February 3, 2018. |

(2) | Includes Abercrombie & Fitch and abercrombie kids brands. Excludes four international franchise stores as of February 3, 2018. |

Omnichannel and direct-to-consumer operations. As customers increasingly shop across multiple channels, the Company has developed, and continues to expand, its omnichannel capabilities. These capabilities include purchase-online-pickup-in-store, reserve-in-store, order-in-store, ship-from-store, and online and in-store returns. The Company continues to invest in these and other omnichannel initiatives in order to create a more seamless shopping experience for its customers.

The Company operates 20 desktop and mobile websites for its brands globally, which are available in several languages and accept multiple currencies, that ship to more than 120 countries. Total net sales through direct-to-consumer operations, including shipping and handling revenue, were $973.9 million for Fiscal 2017, representing approximately 28% of total net sales. Mobile engagement continues to grow, with more than two-thirds of direct-to-consumer traffic was generated from mobile devices in Fiscal 2017. To improve the overall mobile experience, the Company continues to develop and expand its mobile capabilities, including streamlined mobile checkout and ease of navigation.

Wholesale, franchise and licensing operations. The Company continues to expand its international brand reach and create brand awareness through various wholesale, franchise and licensing arrangements. Total net sales from wholesale, franchise and licensing operations were $60.3 million for Fiscal 2017, representing approximately 2% of total net sales. As of February 3, 2018, the Company’s franchisees operated nine international franchise stores across the brands, located in Mexico, Qatar and Saudi Arabia.

5

CUSTOMER ENGAGEMENT.

The Company engages with its customers through in-store and online interactions, loyalty programs, social media platforms, mobile applications, online surveys and customer reviews, and continues to evolve in response to the feedback it receives through these channels. The Hollister and Abercrombie customer relationship management programs provide a platform with which the Company can develop direct relationships with its customers and harness insights. Both brands have a strong global following on key social media platforms, and the Company also partners with key influencers, such as celebrities, bloggers and stylists, to share its products and communicate its brands’ identities. The Company aims to be at the forefront of customer engagement and continues to explore new methods to connect with its customers.

Store experience. The Company’s stores continue to play an essential role in creating brand awareness and have been imagined with the best customer experience in mind with a focus on inspiring customers and serving as physical gateways to the brands. The stores are tailored to reflect the personality of each brand, with unique furniture, fixtures, music and scent adding to a rich brand experience, that is focused on the customer. These stores also serve as local hubs for online engagement as the Company continues to implement its omnichannel capabilities to create a seamless shopping experience. In Fiscal 2017, the Abercrombie and abercrombie kids brands launched new store prototypes which are both open and inviting, and have accommodating features such as innovative fitting rooms and omni-channel capabilities. Through the enhanced store environment, the Company has seen improved store engagement and greater overall productivity on a smaller footprint.

Loyalty programs. The Company offers the Club Cali® and A&F Club® loyalty programs for Hollister and Abercrombie customers, respectively. Under these programs, customers accumulate points based on purchase activity and earn rewards by reaching certain point thresholds, which can be redeemed for merchandise discounts. The loyalty programs continue to provide timely customer insights, while driving a higher average level of customer spend. In addition, the Company uses its loyalty programs as a tool to stay close to the customer by engaging with some of its most valuable customers through special offers, members-only items and access to unique members-only experiences, including early looks at collections.

MERCHANDISE VENDORS.

Global sourcing strategy. The Company depends on its network of third-party vendors to supply compelling, on-trend and high-quality product assortments to its customers. The Company partners with vendors that respect local laws and share its dedication to employing leading practices in human rights, labor rights, environmental responsibility and workplace safety. Maintaining close relationships with vendors allows the Company to be responsive and adaptable to customer feedback. During Fiscal 2017, the Company sourced merchandise through approximately 150 vendors located throughout the world, primarily in Asia and Central America, and did not source more than 10% of its merchandise from any single factory or supplier. The Company’s global sourcing strategy includes relationships with vendors in 18 countries, including the U.S. The Company’s global sourcing of merchandise is generally negotiated and settled in U.S. Dollars.

Quality assurance. High quality standards are an integral part of the Company’s identity, and all product sources, including independent manufacturers and suppliers, must achieve and maintain these standards. The Company has established supplier product quality standards to ensure the high quality of fabrics and other materials used in the Company’s products. Both home office and field employees participate in monitoring suppliers’ compliance with the Company’s product quality standards. Before production begins, all factories, including subcontractors of the factories, undergo a quality assurance assessment to ensure they meet Company standards. All factories are contractually required to adhere to the Company’s Vendor Code of Conduct, go through social audits, which include on-site walk-throughs to appraise the physical working conditions and health and safety practices, and review payroll and age documentation. Social audits of the factories are performed at least every two years after the initial audit.

6

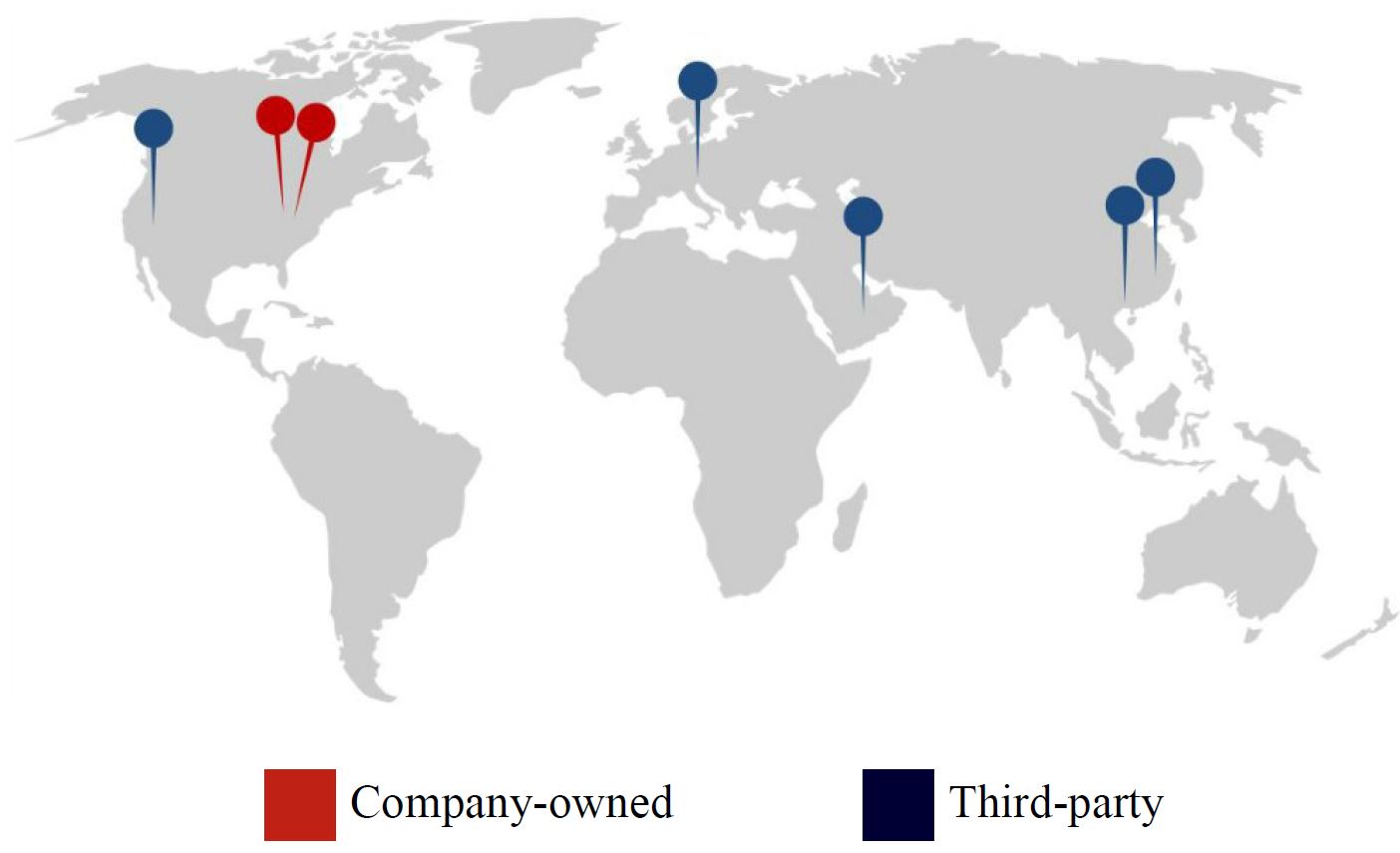

DISTRIBUTION OF MERCHANDISE INVENTORY.

The Company’s distribution network is built to deliver inventory to its stores and fulfill direct-to-consumer orders with speed and efficiency. Merchandise is shipped to the Company’s distribution centers (“DCs”), where it is received and inspected before being shipped to stores or direct-to-consumer customers. The Company primarily uses one contract carrier to ship merchandise and related materials to its North American stores and direct-to-consumer customers, and several contract carriers for its European and Asian stores and direct-to-consumer customers.

The Company relies on DCs to manage the receipt, storage, sorting, packing and distribution of its merchandise. The Company’s DCs by geography as of February 3, 2018 were as follows:

Additional information pertaining to the Company’s DCs is as follows:

Location | Company-owned or third-party | Areas of service | ||

New Albany, Ohio | Company-owned | Stores and direct-to-consumer operations in North America | ||

New Albany, Ohio | Company-owned | Direct-to-consumer operations in North America | ||

Reno, Nevada | Third-party | Stores and direct-to-consumer operations in North America | ||

Bergen op Zoom, Netherlands | Third-party | Stores and direct-to-consumer operations in Europe | ||

Shanghai, China | Third-party | Stores and direct-to-consumer operations in China | ||

Hong Kong | Third-party | Stores and direct-to-consumer operations in Asia | ||

Dubai, United Arab Emirates | Third-party | Stores in the Middle East | ||

INFORMATION SYSTEMS.

The Company’s management information systems consist of a full range of retail, merchandising, human resource and financial systems. The systems include applications related to point-of-sale, direct-to-consumer, inventory management, supply chain, planning, sourcing, merchandising, payroll, scheduling and financial reporting. The Company continues to invest in technology to upgrade its core systems to create efficiencies, including the support of its direct-to-consumer operations, omnichannel capabilities, customer relationship management tools and loyalty programs.

TRADEMARKS.

The trademarks Abercrombie & Fitch®, abercrombie®, Hollister®, Gilly Hicks® and the “Moose” and “Seagull” logos are registered with the U.S. Patent and Trademark Office and registered, or the Company has applications for registration pending, with the registries of countries where stores are located or likely to be located in the future. In addition, these trademarks are either registered, or the Company has applications for registration pending, with the registries of many of the foreign countries in which the manufacturers of the Company’s products are located. The Company has also registered, or has applied to register, certain other trademarks in the U.S. and around the world. The Company believes its products are identified by its trademarks and, therefore, its trademarks are of significant value. Each registered trademark has a duration of 10 to 20 years, depending on the date it was registered, and the country in which it is registered, and is subject to an indefinite number of renewals for a like period upon continued use and appropriate application. The Company intends to continue using its core trademarks and to timely renew each of its registered trademarks that remain in use.

7

ASSOCIATE RELATIONS.

As of March 28, 2018, the Company employed approximately 38,000 associates, of whom approximately 31,000 were part-time associates, which equates to approximately 4,000 full-time equivalents. On average, the Company employed approximately 14,000 full-time equivalents during Fiscal 2017.

ENVIRONMENTAL MATTERS.

The Company has committed to advancing environmental initiatives in its internal practices, by increasing education and awareness throughout its partnership base, and through communities in which they make and sell products. Compliance with domestic and international regulations related to environmental matters has not had, nor is it expected to have, any material effect on the Company’s capital expenditures, earnings or competitive position based on information and circumstances known to the Company at this time.

OTHER INFORMATION.

Additional information about the Company’s business, including its results of operations for the last three fiscal years and gross square footage of stores, is set forth under “ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS” of this Annual Report on Form 10-K.

EXECUTIVE OFFICERS OF THE REGISTRANT.

Set forth below is certain information regarding the executive officers of A&F as of March 28, 2018:

Stacia Andersen, 47, has been Brand President of Abercrombie & Fitch and abercrombie kids since June 2016. Prior to joining A&F, Ms. Andersen served in various positions with Target Corporation (“Target”), a general merchandise retailer selling products through Target stores and digital channels, from 1993 until December 2015. Most recently, Ms. Andersen served as Senior Vice President Merchandising, Apparel, Accessories and Baby of Target, from May 2014 to December 2015, and as Senior Vice President Merchandising, Home and Seasonal of Target, from October 2009 to May 2014. Prior to serving as a Senior Vice President Merchandising at Target, Ms. Andersen served as President, Target Sourcing Services/Associated Merchandising Corporation, from February 2006 to October 2009, and before that, in various sourcing and merchandising positions.

Robert E. Bostrom, 65, has been Senior Vice President, General Counsel and Corporate Secretary of A&F since January 2014. Since August 2014, Mr. Bostrom has been a member of the Board of Directors of NeuLion, Inc. From December 2012 to December 2013, Mr. Bostrom was Co-Chairman of the Financial Regulatory and Compliance Practice of Greenberg Traurig LLP, an international law firm. From August 2011 to November 2012, Mr. Bostrom was Co-Head of the Global Financial Institutions and Funds Sector of Dentons US LLP (formerly, SNR Denton), an international law firm. From February 2006 to August 2011, Mr. Bostrom was Executive Vice President, General Counsel and Corporate Secretary of the Federal Home Loan Mortgage Corporation (also known as Freddie Mac). Prior to his time with Freddie Mac, Mr. Bostrom was the Managing Partner of the New York office of Winston & Strawn LLP, a Member of that firm’s Executive Committee and Head of its Financial Institutions Practice.

Joanne C. Crevoiserat, 54, has been Executive Vice President and Chief Operating Officer of A&F since February 2017 and served as Executive Vice President and Chief Financial Officer of A&F from May 2014 to October 2017. In addition, Ms. Crevoiserat served as Interim Principal Executive Officer of A&F from June 2016 to February 2017 and was a member of the Office of the Chairman of A&F from October 2015 to February 2017. Prior to joining A&F, Ms. Crevoiserat served in a number of senior management roles at Kohl’s Inc., which operates family-oriented department stores and a website featuring apparel, footwear, accessories, soft home products and housewares. From June 2012 to April 2014, Ms. Crevoiserat was the Executive Vice President of Finance of Kohl’s and from November 2008 to June 2012, she served as the Executive Vice President of Merchandise Planning and Allocation of Kohl’s. Prior to her time with Kohl’s, Ms. Crevoiserat held senior finance positions with Wal-Mart Stores and May Department Stores, including Chief Financial Officer of the Filene’s, Foley’s and Famous-Barr brands.

Fran Horowitz, 54, has been Chief Executive Officer and a director of A&F since February 2017. In addition, Ms. Horowitz has been Principal Executive Officer of A&F since February 2017. Prior thereto, she had served as President & Chief Merchandising Officer for all brands of A&F since December 2015 and was a member of the Office of the Chairman of A&F from December 2014 to February 2017. Ms. Horowitz held the position of Brand President of Hollister from October 2014 to December 2015. Before joining Hollister, from October 2013 to October 2014, Ms. Horowitz served as the President of Ann Taylor Loft, a division of Ann Inc., the parent company of three specialty retail fashion brands in North America. Prior to her time with Ann Taylor Loft, from February 2005 to October 2012, she held various roles at Express, Inc., a specialty apparel and accessories retailer of women’s and men’s merchandise, including Executive Vice President of Women’s Merchandising and Design from May 2010 to November

8

2012. Before her time with Express, Inc., Ms. Horowitz spent 13 years at Bloomingdale’s in various women’s merchandising roles, including Vice President Divisional Merchandise Manager. Since March 2017, Ms. Horowitz has served on the Board of Directors of SeriousFun Children’s Network, Inc., a Connecticut non-profit corporation.

Scott Lipesky, 43, has been Senior Vice President and Chief Financial Officer of A&F, as well as Principal Financial Officer and Principal Accounting Officer of A&F, since October 2017. Prior to joining A&F, Mr. Lipesky served as Chief Financial Officer of American Signature, Inc., a privately-held home furnishings company, from October 2016 to October 2017. Prior to his time with American Signature, Inc., Mr. Lipesky served in various finance positions with A&F from November 2007 to October 2016, including as Chief Financial Officer, Hollister Brand, from September 2014 to October 2016, Vice President, Merchandise Finance from March 2013 to September 2014, Vice President, Financial Planning and Analysis from November 2012 to March 2013 and Senior Director, Financial Planning and Analysis from November 2010 to November 2012.

Kristin Scott, 50, has been Brand President of Hollister since August 2016. Before joining Hollister, Ms. Scott served in various positions with Victoria’s Secret, a specialty retailer of women’s intimate and other apparel which sells products at Victoria’s Secret stores and online, from December 2007 until April 2016. Most recently, Ms. Scott served as Executive Vice President, GMM Merchandising from March 2013 to April 2016, Senior Vice President, GMM Merchandising from March 2009 to March 2013 and Senior Vice President, GMM Merchandising - Stores from December 2007 to March 2009. Prior to her time with Victoria’s Secret, Ms. Scott served in merchandising positions at the Vice President level with Gap Outlet, Marshall Fields and Target.

The Board of Directors of A&F dissolved the Office of the Chairman, effective February 1, 2017 with the appointment of Fran Horowitz as Chief Executive Officer of A&F. The Office of the Chairman was formed in December 2014 to allow for effective management of the Company during a transition in leadership. The executive officers serve at the pleasure of the Board of Directors of A&F.

9

ITEM 1A. | RISK FACTORS |

FORWARD-LOOKING STATEMENTS AND RISK FACTORS.

We caution that any forward-looking statements (as such term is defined in the Private Securities Litigation Reform Act of 1995) contained in this Annual Report on Form 10-K or made by us, our management or our spokespeople involve risks and uncertainties and are subject to change based on various factors, many of which may be beyond our control. Words such as “estimate,” “project,” “plan,” “believe,” “expect,” “anticipate,” “intend” and similar expressions may identify forward-looking statements. Except as may be required by applicable law, we undertake no obligation to publicly update or revise any forward-looking statements.

Forward-looking statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict. The following factors, categorized by the primary nature of the associated risk, could affect our financial performance and cause actual results to differ materially from those expressed or implied in any of the forward-looking statements.

Macroeconomic and industry risks include:

• | Changes in global economic and financial conditions, and the resulting impact on consumer confidence and consumer spending, as well as other changes in consumer discretionary spending habits, could have a material adverse effect on our business, results of operations and liquidity; |

• | Failure to anticipate customer demand and changing fashion trends and to manage our inventory commensurately could adversely impact our sales levels and profitability; |

• | Our market share may be negatively impacted by increasing competition and pricing pressures from companies with brands or merchandise competitive with ours; |

• | Fluctuations in foreign currency exchange rates could adversely impact our financial condition and results of operations; |

• | Our ability to attract customers to our stores depends, in part, on the success of the shopping malls or area attractions that our stores are located in or around; and, |

• | The impact of war, acts of terrorism or civil unrest could have a material adverse effect on our operating results and financial condition. |

Strategic risks include:

• | The expansion of our direct-to-consumer sales channels and omnichannel initiatives are significant components of our growth strategy, and the failure to successfully develop our position across all channels could have an adverse impact on our results of operations; |

• | Our international growth strategy and ability to conduct business in international markets may be adversely affected by legal, regulatory, political and economic risks; and, |

• | Failure to successfully implement our strategic plans could have a negative impact on our growth and profitability. |

Operational risks include:

• | Failure to protect our reputation could have a material adverse effect on our brands; |

• | Our business could suffer if our information technology systems are disrupted or cease to operate effectively; |

• | We may be exposed to risks and costs associated with cyber-attacks, credit card fraud and identity theft that would cause us to incur unexpected expenses and reputation loss; |

• | Our reliance on DCs makes us susceptible to disruptions or adverse conditions affecting our supply chain; |

• | Changes in cost, availability and quality of raw materials, labor, transportation, and trade relations could cause manufacturing delays and increase our costs; |

• | We depend upon independent third parties for the manufacture and delivery of all our merchandise, and a disruption of the manufacture or delivery of our merchandise could result in lost sales and could increase our costs; |

• | We rely on the experience and skills of our senior executive officers and associates, the loss of whom could have a material adverse effect on our business; and, |

• | Extreme weather conditions, including natural disasters, pandemic disease and other unexpected events, could negatively impact our facilities, systems and stores, as well as the facilities and systems of our vendors and manufacturers, which could result in an interruption to our business and adversely affect our operating results. |

10

Legal, tax, regulatory and compliance risks include:

• | Fluctuations in our tax obligations and effective tax rate may result in volatility in our results of operations; |

• | Our litigation exposure could have a material adverse effect on our financial condition and results of operations; |

• | Failure to adequately protect our trademarks could have a negative impact on our brand image and limit our ability to penetrate new markets; |

• | Changes in the regulatory or compliance landscape and compliance with changing regulations for accounting, corporate governance and public disclosure could adversely affect our business, results of operations and reported financial results; and, |

• | Our Asset-Based Revolving Credit Agreement and our Term Loan Agreement include restrictive covenants that limit our flexibility in operating our business. |

The factors listed above are not our only risks. Additional risks may arise and current evaluations of risks may change, which could lead to material, adverse effects on our business, operating results and financial condition. The following sets forth a description of the preceding risk factors that we believe may be relevant to an understanding of our business. These risk factors could cause actual results to differ materially from those expressed or implied in any of our forward-looking statements.

MACROECONOMIC AND INDUSTRY RISKS.

Changes in global economic and financial conditions, and the resulting impact on consumer confidence and consumer spending, as well as other changes in consumer discretionary spending habits, could have a material adverse effect on our business, results of operations and liquidity.

Our business depends on consumer demand for our merchandise. Consumer purchases of discretionary items, including our merchandise, can be adversely impacted by recessionary periods and other periods where disposable income is adversely affected. Our performance is subject to factors that affect worldwide economic conditions including unemployment, consumer credit availability, consumer debt levels, reductions in net worth based on declines in the financial, residential real estate and mortgage markets, sales and personal income tax rates, fuel and energy prices, interest rates, consumer confidence in future economic and political conditions, consumer perceptions of personal well-being and security, the value of the U.S. Dollar versus foreign currencies and other macroeconomic factors. Additionally, changes in consumer preferences and discretionary spending habits may negatively impact the specialty apparel retail market. Global economic uncertainty and changing consumer preferences and discretionary spending habits could have a material adverse effect on our results of operations, liquidity and capital resources if reduced consumer demand for our merchandise should occur. It could also impact our ability to fund growth and/or result in our becoming reliant on external financing, the availability and cost of which may be uncertain.

The economic conditions and factors described above could adversely affect the profitability of our business, as well as adversely affect the pace of opening new stores, or their productivity once opened. Finally, the economic environment may exacerbate some of the risks noted below, including consumer demand, strain on available resources, our international growth strategy, availability of real estate, interruption of the flow of merchandise from key vendors and manufacturers, and foreign currency exchange rate fluctuations.

Failure to anticipate customer demand and changing fashion trends and to manage our inventory commensurately could adversely impact our sales levels and profitability.

Our success largely depends on our ability to anticipate and gauge the fashion preferences of our customers and provide merchandise that satisfies constantly shifting demands in a timely manner. Because we enter into agreements for the manufacture and purchase of merchandise well in advance of the applicable selling season, we are vulnerable to changes in consumer preferences and demand, pricing shifts, and the sub-optimal selection and timing of merchandise purchases. Moreover, there can be no assurance that we will continue to anticipate consumer demands and accurately plan inventory successfully in the future. Changing consumer preferences and fashion trends, whether we are able to anticipate, identify and respond to them or not, could adversely impact our sales. Inventory levels for certain merchandise styles no longer considered to be “on trend” may increase, leading to higher markdowns to sell through excess inventory and therefore, lower than planned margins. A distressed economic and retail environment, in which many of our competitors continue to engage in aggressive promotional activities increases the importance of reacting appropriately to changing consumer preferences and fashion trends. Conversely, if we underestimate consumer demand for our merchandise, or if our manufacturers fail to supply quality products in a timely manner, we may experience inventory shortages, which may negatively impact customer relationships, diminish brand loyalty and result in lost sales. In addition, we could be at a competitive disadvantage if we are unable to leverage data analytics to retrieve timely, customer insights to appropriately respond to customer demands. Any of these events could significantly harm our operating results and financial condition.

11

Our market share may be negatively impacted by increasing competition and pricing pressures from companies with brands or merchandise competitive with ours.

The sale of apparel and personal care products through stores and direct-to-consumer channels is a highly competitive business with numerous participants, including individual and chain specialty apparel retailers, local, regional, national and international department stores, discount stores and online businesses. Proliferation of the direct-to-consumer channel within the last few years has encouraged the entry of many new competitors and an increase in competition from established companies. We face a variety of competitive challenges, including:

• | anticipating and quickly responding to changing consumer demands or preferences better than our competitors, including being able to adapt to new, emerging technologies that alter customer experience expectations; |

• | maintaining favorable brand recognition and effective marketing of our products to consumers in several diverse demographic markets; |

• | sourcing merchandise efficiently; |

• | developing innovative, high-quality merchandise in styles that appeal to our consumers and in ways that favorably distinguish us from our competitors; and, |

• | countering the aggressive pricing and promotional activities of many of our competitors without diminishing the aspirational nature of our brands and brand equity. |

In light of the competitive challenges we face, we may not be able to compete successfully in the future. Further, increases in competition could reduce our sales and harm our operating results and business.

Fluctuations in foreign currency exchange rates could adversely impact our financial condition and results of operations.

The functional currency of our foreign subsidiaries is generally the local currency in which each entity operates, while our consolidated financial statements are presented in U.S. Dollars. Therefore, we must translate revenues, expenses, assets and liabilities from functional currencies into U.S. Dollars at exchange rates in effect during, or at the end of the reporting period. In addition, our international subsidiaries transact in currencies other than their functional currency, including intercompany transactions, which results in foreign currency transaction gains or losses. Furthermore, we purchase substantially all of our inventory in U.S. Dollars. As a result, our sales and gross profit rate from international operations will be negatively impacted during periods of a strengthened U.S. dollar relative to the functional currencies of our foreign subsidiaries. Additionally, tourism spending may be affected by changes in foreign currency exchange rates, and as a result, sales in our flagship stores and other stores with higher tourism traffic have, at times, been adversely impacted, and may continue to be adversely impacted, by fluctuations in foreign currency exchange rates. Certain events, such as the June 2016 decision by the United Kingdom to leave the European Union and the November 2016 U.S. elections, have increased global economic and political uncertainty and caused volatility in foreign currency exchange rates. Our business and results of operations may be impacted by these developments. For Fiscal 2017, 63.2%, 23.2% and 13.5% of the Company’s net sales were attributable to the U.S., Europe and other geographic areas, respectively.

Our ability to attract customers to our stores depends, in part, on the success of the shopping malls or area attractions that our stores are located in or around.

In order to generate customer traffic, we locate many of our stores in prominent locations within successful shopping malls or street locations. Our stores benefit from the ability of the malls’ “anchor” tenants, generally large department stores and other area attractions, to generate consumer traffic in the vicinity of our stores. We cannot control the loss of an anchor or other significant tenant in a shopping mall in which we have a store; the development of new shopping malls in the U.S. or around the world, the availability or cost of appropriate locations, competition with other retailers for prominent locations or the success of individual shopping malls. All of these factors may impact our ability to meet our productivity targets for our domestic stores and our growth objectives for our international stores and could have a material adverse effect on our financial condition or results of operations. In addition, some malls that were in prominent locations when we opened our stores may cease to be viewed as prominent. If this trend continues or if the popularity of mall shopping continues to decline generally among our customers, our sales may decline, which would impact our gross profits and net income.

Part of our future growth is dependent on our ability to operate stores in desirable locations with capital investment and lease costs providing the opportunity to earn a reasonable return. We cannot be sure as to when or whether such desirable locations will become available at reasonable costs.

12

The impact of war, acts of terrorism or civil unrest could have a material adverse effect on our operating results and financial condition.

The continued threat of terrorism and the associated heightened security measures and military actions in response to acts of terrorism have disrupted commerce. Further acts of terrorism, future conflicts or civil unrest may disrupt commerce and undermine consumer confidence and consumer spending by causing domestic and/or tourist traffic in malls and the Company’s flagship and other stores to decline, which could negatively impact our sales revenue. Furthermore, war or an act of terrorism, or the threat thereof, or any other unforeseen interruption of commerce, could negatively impact our business by interfering with our ability to obtain merchandise from foreign manufacturers. With a substantial portion of our merchandise being imported from foreign countries, failure to obtain merchandise from our foreign manufacturers or substitute other manufacturers, at similar costs and in a timely manner, could adversely affect our operating results and financial condition.

STRATEGIC RISKS.

The expansion of our direct-to-consumer sales channels and omnichannel initiatives are significant components of our growth strategy, and the failure to successfully develop our position across all channels could have an adverse impact on our results of operations.

Consumers are increasingly shopping online and via mobile devices, and we have made significant investments in capital spending and labor to develop these channels globally, invested in digital media to attract new customers and developed localized fulfillment, shipping and customer service operations. As omnichannel retailing continues to grow and evolve, our customers increasingly interact with our brands through a variety of media including smart phones and tablets, and expect seamless integration across all touchpoints. Our success depends on our ability to introduce innovative means of engaging our customers and our ability to respond to shifting consumer traffic patterns and direct-to-consumer buying trends. There is no assurance that we will be able to continue to successfully maintain or expand our direct-to-consumer sales channels and omnichannel initiatives and failure to adequately respond to these risks and uncertainties or to successfully maintain and expand our direct-to-consumer business may have an adverse impact on our results of operations.

In addition, direct-to-consumer operations are subject to numerous risks, including reliance on third-party computer hardware/software and service providers, data breaches, violations of state, federal or international laws, including those relating to online privacy, credit card fraud, telecommunication failures and electronic break-ins and similar disruptions, and disruption of Internet service. Changes in foreign governmental regulations may also negatively impact our ability to deliver product to our customers. Failure to successfully respond to these risks may adversely affect sales in our direct-to-consumer business as well as damage our reputation and brands.

Our international growth strategy and ability to conduct business in international markets may be adversely affected by legal, regulatory, political and economic risks.

International expansion is a significant component of our growth strategy and may require significant capital investment, which could strain our resources and adversely impact current store performance, while adding complexity to our current operations. We are subject to domestic laws, including the Foreign Corrupt Practices Act, in addition to the laws of the foreign countries in which we operate. If any of our overseas operations, or our associates or agents, violate such laws, we could become subject to sanctions or other penalties that could negatively affect our reputation, business and operating results.

Additionally, we may face operational issues that could have a material adverse effect on our reputation, business and results of operations if we fail to address certain factors including, but not limited to, the following:

• | address the different operational characteristics present in each country in which we operate, including employment and labor, transportation, logistics, real estate, lease provisions and local reporting or legal requirements; |

• | hire, train and retain qualified personnel; |

• | maintain good relations with individual associates and groups of associates; |

• | avoid work stoppages or other labor-related issues in our European stores where associates are represented by workers’ councils and unions; |

• | retain acceptance from foreign customers; |

• | manage inventory effectively to meet the needs of existing stores on a timely basis; and |

• | manage foreign currency exchange rate risks effectively. |

13

Failure to successfully implement our strategic plans could have a negative impact on our growth and profitability.

Our ability to execute our long-term strategies successfully and in a timely fashion is subject to various risks and uncertainties as described under this “Risk Factors” section. Specifically, these risks can be categorized into macroeconomic risk, strategic risk, operational risk and legal, tax, regulatory and compliance risk. Achieving the goals of our long-term strategy is also dependent on us executing the strategy successfully. Finally, it may take longer than anticipated to generate the expected benefits from our long-term strategy, the initiatives we implement in connection with our long-term strategy may not resonate with our customers and there can be no guarantee that these initiatives will result in improved operating results. In addition, failure to successfully implement our long-term strategy could have a negative impact on our growth and profitability.

OPERATIONAL RISKS.

Failure to protect our reputation could have a material adverse effect on our brands.

Our ability to maintain our reputation is critical to our brands. Our reputation could be jeopardized if we fail to maintain high standards for merchandise quality and integrity, if our third-party vendors fail to comply with our vendor code of conduct, if any third parties with which we have a business relationship fail to represent our brands in a manner consistent with our brand image and customer experience standards or as a result of a cyber-attack. In addition, the increasing use of social media platforms allows for rapid communication and any negative publicity related to the aforementioned concerns may reduce demand for our merchandise. Failure to comply with ethical, social, product, labor, health and safety, accounting or environmental standards, or related political considerations, could also jeopardize our reputation and potentially lead to various adverse consumer actions, including boycotts. Public perception about our products or our stores, whether justified or not, could impair our reputation, involve us in litigation, damage our brands and have a material adverse effect on our business. Damage to our reputation or loss of consumer confidence for any of these or other reasons could have a material adverse effect on our results of operations and financial condition, as well as require additional resources to rebuild our reputation.

Our business could suffer if our information technology systems are disrupted or cease to operate effectively.

We rely heavily on our information technology systems to operate our websites; record and process transactions; respond to customer inquiries; manage inventory; purchase, sell and ship merchandise on a timely basis; and maintain cost-efficient operations. Given the significant number of transactions that are completed annually, it is vital to maintain constant operation of our computer hardware and software systems and maintain cyber security. Despite efforts to prevent such an occurrence, our information technology systems may be vulnerable from time to time to damage or interruption from computer viruses, power outages, third-party intrusions, inadvertent or intentional breach by our employees and other technical malfunctions. If our systems are damaged, or fail to function properly, we may have to make monetary investments to repair or replace the systems, and we could endure delays in our operations.

While we regularly evaluate our information technology systems and requirements, we are aware of the inherent risks associated with replacing and modifying these systems, including inaccurate system information, system disruptions and user acceptance and understanding. Any material disruption or slowdown of our systems, including a disruption or slowdown caused by our failure to successfully upgrade our systems could cause information to be lost or delayed, including data related to customer orders. Such a loss or delay, especially if the disruption or slowdown occurred during our peak selling seasons, could have a material adverse effect on our results of operations.

14

We may be exposed to risks and costs associated with cyber-attacks, credit card fraud and identity theft that would cause us to incur unexpected expenses and reputation loss.

In the standard course of business, we process customer information, including payment information, through our stores and direct-to-consumer channels. Rapidly evolving technologies, payment capabilities offered and types of cyber-attacks may result in this information being compromised or breached. The retail industry in particular has been the target of many recent cyber-attacks, and as a result, there is heightened concern over the security of personal information transmitted over or accessible through the Internet, consumer identity theft and user privacy. We endeavor to protect consumer identity and payment information through the implementation of security technologies, processes and procedures, including training programs for employees to raise awareness about phishing, malware and other cyber risks and could experience increased costs associated with maintaining these protections as threats of cyber-attacks increase in sophistication and complexity. It is possible that an individual or group could defeat our security measures and access sensitive customer and associate information. Actual or anticipated cyber-attacks may cause us to incur increased costs, including costs to deploy additional personnel and protective technologies, train employees and engage third-party experts and consultants. Exposure of customer data through any means, including through third-party service providers and vendors, could materially harm the Company by, but not limited to, reputation loss, regulatory fines and penalties, legal liability and costs of litigation.

Our reliance on DCs makes us susceptible to disruptions or adverse conditions affecting our supply chain.

We rely on two Company-owned DCs and five third-party DCs to manage the receipt, storage, sorting, packing and distribution of our merchandise. The Company utilizes primarily one contract carrier to ship merchandise and related materials to its North American stores and direct-to-consumer customers, and several contract carriers for its European and Asian stores and direct-to-consumer customers. As a result, our operations are susceptible to local and regional factors, such as system failures, accidents, economic and weather conditions, natural disasters, demographic and population changes, as well as other unforeseen events and circumstances. If our distribution operations were disrupted, our ability to replace inventory in our stores and process direct-to-consumer and wholesale orders could be interrupted negatively impacting sales and could experience increased costs related to these disruptions. Refer to “ITEM 1. BUSINESS,” for a listing of the DCs we rely on.

Changes in cost, availability and quality of raw materials, labor, transportation, and trade relations could cause manufacturing delays and increase our costs.

Changes in the cost, availability and quality of the fabrics or other raw materials used to manufacture our merchandise could have a material adverse effect on our cost of sales, or our ability to meet customer demand. The prices for such fabrics depend largely on the market prices for the raw materials used to produce them, particularly cotton, as well as the cost of compliance with sourcing laws. The price and availability of such raw materials may fluctuate significantly, depending on many factors, including crop yields and weather patterns. Such factors may be exacerbated by legislation and regulations associated with global climate change. In addition, the cost of labor at many of our third-party manufacturers has been increasing significantly, and as the middle class in developing countries continues to grow, it is unlikely such cost pressure will abate. The Company is also susceptible to fluctuations in the cost of transportation. We may not be able to pass all or a portion of higher raw materials prices or labor or transportation costs on to our customers, which could adversely affect our gross margin and results of our operations. Recently, there has been greater uncertainty with respect to trade policies, tariffs and government regulations affecting trade between the U.S. and other countries, such as the threat of additional tariffs on imported consumer goods from China. Major developments in trade policies, such as the imposition of unilateral tariffs on imported products, could have a material adverse effect on our business, results of operations and liquidity.

15

We depend upon independent third parties for the manufacture and delivery of all our merchandise, and a disruption of the manufacture or delivery of our merchandise could result in lost sales and could increase our costs.

We do not own or operate any manufacturing facilities. As a result, the continued success of our operations is tied to our timely receipt of quality merchandise from third-party manufacturers. We source the majority of our merchandise outside of the U.S. through arrangements with approximately 150 vendors which includes foreign manufacturers located throughout the world, primarily in Asia and Central America. Political, social or economic instability in Asia and Central America, or in other regions in which our manufacturers are located, could cause disruptions in trade, including exports to the U.S. A manufacturer’s inability to ship orders in a timely manner or meet our quality standards could cause delays in responding to consumer demands and negatively affect consumer confidence or negatively impact our competitive position, any of which could have a material adverse effect on our financial condition and results of operations.

Other events that could disrupt the timely delivery of our merchandise include new trade law provisions or regulations, reliance on a limited number of shipping carriers, significant labor disputes and significant delays in the delivery of cargo due to port security considerations. Furthermore, we are susceptible to increases in fuel costs which may increase the cost of distribution. If we are not able to pass this cost on to our customers, our financial condition and results of operations could be adversely affected.

We rely on the experience and skills of our senior executive officers and associates, the loss of whom could have a material adverse effect on our business.

Our ability to succeed may be adversely impacted if we are not able to attract, retain and develop talent and future leaders, including our senior executive officers and associates. Our senior executive officers closely supervise all aspects of our business including the design of our merchandise and the operation of our stores and have substantial experience and expertise in the retail business and have an integral role in the growth and success of our brands. If we were to lose the benefit of the involvement of multiple senior executives or other personnel, our business could be adversely affected. In addition, if unexpected turnover occurs at the associate level without adequate succession plans, the loss of the services of any of these individuals, or any resulting negative perceptions of our business, could damage our reputation and our business. Competition for such qualified talent is intense, and we cannot be sure we will be able to attract, retain and develop a sufficient number of qualified individuals in future periods.

Extreme weather conditions, including natural disasters, pandemic disease and other unexpected events, could negatively impact our facilities, systems and stores, as well as the facilities and systems of our vendors and manufacturers, which could result in an interruption to our business and adversely affect our operating results.

Our retail stores, corporate offices, distribution centers, infrastructure projects and direct-to-consumer operations, as well as the operations of our vendors and manufacturers, are vulnerable to damage from natural disasters, pandemic disease and other unexpected events. If any of these events result in damage to our facilities, systems or stores, or the facilities or systems of our vendors or manufacturers, we may experience interruptions in our business until the damage is repaired, resulting in the potential loss of customers and revenues. In addition, we may incur costs in repairing any damage which exceed our applicable insurance coverage.

In addition, historically, our operations have been seasonal, with a significant amount of net sales and operating income occurring in the fourth fiscal quarter. Severe weather conditions and changes in weather patterns can influence customer trends, consumer traffic and shopping habits. Unseasonable weather may diminish demand for our seasonal merchandise. In addition, severe weather can also decrease customer traffic in our stores and reduce sales and profitability. As a result of this seasonality, net sales and net income during any fiscal quarter cannot be used as an accurate indicator of our annual results. Any factors negatively affecting us during the third and fourth fiscal quarters of any year, including inclement weather, could have a material adverse effect on our financial condition and results of operations for the entire year.

16

LEGAL, TAX, REGULATORY AND COMPLIANCE RISKS.

Fluctuations in our tax obligations and effective tax rate may result in volatility in our results of operations.

We are subject to income taxes in many U.S. and foreign jurisdictions. In addition, our products are subject to import and excise duties and/or sales, consumption or value-added taxes (“VAT”) in many jurisdictions. We record tax expense based on our estimates of future payments, which include reserves for estimates of probable settlements of foreign and domestic tax audits. At any one time, many tax years are subject to audit by various taxing jurisdictions. The results of these audits and negotiations with taxing authorities may affect the ultimate settlement of these issues. As a result, we expect that throughout the year there could be ongoing variability in our quarterly tax rates as taxable events occur and exposures are evaluated. In addition, our effective tax rate in any given financial reporting period may be materially impacted by changes in the mix and level of earnings or losses by taxing jurisdictions or by changes to existing accounting rules or regulations. Fluctuations in duties could also have a material impact on our financial condition, results of operations or cash flows. In some international markets, we are required to hold and submit VAT to the appropriate local tax authorities. Failure to correctly calculate or submit the appropriate amounts could subject us to substantial fines and penalties that could have an adverse effect on our financial condition, results of operations or cash flows. In addition, tax law may be enacted in the future, domestically or abroad, that impacts our current or future tax structure and effective tax rate.

On December 22, 2017, the Tax Cuts and Jobs Act of 2017 (the “Act”) was enacted into law. The Act makes broad and significantly complex changes to the U.S. corporate income tax system. Given the complexities associated with the Act, the estimated financial impacts for fiscal 2017 are provisional and subject to further analysis, interpretation and clarification of the Act. In addition, the U.S. Treasury Department, the Internal Revenue Service and other standard-setting bodies could interpret or issue guidance on how provisions of the Act will be applied or otherwise administered that differs from our interpretations and could result in changes to our estimates. Changes to these estimates during Fiscal 2018 could have a material adverse effect on our business, results of operations and liquidity. Refer to Note 10, “INCOME TAXES,” for further discussion.

Our litigation exposure could have a material adverse effect on our financial condition and results of operations.

We, along with third parties we do business with, are involved, from time to time, in litigation arising in the ordinary course of business. Litigation matters may include, but are not limited to, contract disputes, employment-related actions, labor relations, commercial litigation, intellectual property rights and shareholder actions. Any litigation that we become a party to could be costly and time consuming and could divert our management and key personnel from our business operations. Our current litigation exposure could be impacted by litigation trends, discovery of damaging facts with respect to legal matters pending against us or determinations by judges, juries or other finders of fact that are not in accordance with management’s evaluation of existing claims. Should management’s evaluation prove incorrect, our exposure could greatly exceed expectations and have a material adverse effect on our financial condition, results of operations or cash flows.

Failure to adequately protect our trademarks could have a negative impact on our brand image and limit our ability to penetrate new markets.

We believe our core trademarks, Abercrombie & Fitch®, abercrombie®, Hollister®, Gilly Hicks® and the “Moose” and “Seagull” logos, are essential to the effective implementation of our strategy. We have obtained or applied for federal registration of these trademarks with the U.S. Patent and Trademark Office and the registries of countries where stores are located or likely to be located in the future. In addition, we own registrations and have pending applications for other trademarks in the U.S. and have applied for or obtained registrations from the registries in many foreign countries in which our stores or our manufacturers are located. There can be no assurance that we will obtain registrations that have been applied for or that the registrations we obtain will prevent the imitation of our products or infringement of our intellectual property rights by others. Although brand security initiatives are in place, we cannot guarantee that our efforts against the counterfeiting of our brands will be successful. If a third-party copies our products in a manner that projects lesser quality or carries a negative connotation, our brand image could be materially adversely affected.

Because we have not yet registered all of our trademarks in all categories, or in all foreign countries in which we source or offer our merchandise now, or may in the future, our international expansion and our merchandising of products using these marks could be limited. The pending applications for international registration of various trademarks could be challenged or rejected in those countries because third parties of whom we are not currently aware have already registered similar marks in those countries. Accordingly, it may be possible, in those foreign countries where the status of various applications is pending or unclear, for a third-party owner of the national trademark registration for a similar mark to prohibit the manufacture, sale or exportation of branded goods in or from that country. Failure to register our trademarks or purchase or license the right to use our trademarks or

17

logos in these jurisdictions could limit our ability to obtain supplies from, or manufacture in, less costly markets or penetrate new markets should our business plan include selling our merchandise in those non-U.S. jurisdictions.

Changes in the regulatory or compliance landscape and compliance with changing regulations for accounting, corporate governance and public disclosure could adversely affect our business, results of operations and reported financial results.

We are subject to numerous laws and regulations, including customs, truth-in-advertising, securities laws, consumer protection, general privacy, health information privacy, identity theft, online privacy, employee health and safety, international minimum wage laws, unsolicited commercial communication and zoning and occupancy laws and ordinances that regulate retailers generally and/or govern the importation, intellectual property, promotion and sale of merchandise and the operation of retail stores, direct-to-consumer operations and distribution centers. Laws and regulations at the local, state, federal and various international levels frequently change, and the ultimate cost of compliance cannot be precisely estimated. If these laws and regulations were to change, or were violated by our management, associates, suppliers, vendors or other parties with whom we do business, the costs of certain merchandise could increase, or we could experience delays in shipments of our merchandise, be subject to fines or penalties, temporary or permanent store closures, increased regulatory scrutiny or suffer reputational harm, which could reduce demand for our merchandise and adversely affect our business and results of operations. Any changes in regulations, the imposition of additional regulations, or the enactment of any new or more stringent legislation including the areas referenced above, could adversely affect our business and results of operations.

In addition, changing regulatory requirements for corporate governance and public disclosure, including SEC regulations and the Financial Accounting Standards Board’s Accounting Standards Codification (“ASC”) are creating additional complexities for public companies. For example, in July 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act (“the Dodd-Frank Act”), was enacted. There are significant corporate governance and executive compensation related provisions in the Dodd-Frank Act that have required the SEC to adopt additional rules and regulations in these areas.

Stockholder activism, the current political environment, financial reform legislation and the current high level of government intervention and regulatory reform may lead to substantial new regulations and disclosure obligations. In addition, the potential requirement to transition to, or converge with, international financial reporting standards in the future may create uncertainty and additional complexities. These changing regulatory requirements may lead to additional compliance costs, as well as the diversion of our management’s time and attention from strategic business activities and could have a significant effect on our reported results for the affected periods.

Our Asset-Based Revolving Credit Agreement and our Term Loan Agreement include restrictive covenants that limit our flexibility in operating our business.

Our Asset-Based Revolving Credit Agreement, as amended, expires on October 19, 2022 and our Term Loan Agreement, as amended, has a maturity date of August 7, 2021. Both our Asset-Based Revolving Credit Agreement and our Term Loan Agreement contain restrictive covenants that, subject to specified exemptions, restrict our ability to incur indebtedness, grant liens, make certain investments, pay dividends or distributions on our capital stock and engage in mergers. The inability to obtain credit on commercially reasonable terms in the future when these facilities expire could adversely impact our liquidity and results of operations. In addition, market conditions could potentially impact the size and terms of a replacement facility or facilities.

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

18

ITEM 2. | PROPERTIES |

The Company’s headquarters and support functions occupy 501 acres, consisting of the home office, distribution and shipping facilities centralized on a campus-like setting in New Albany, Ohio, all of which are owned by the Company. Additionally, the Company leases small facilities to house its human resources, finance, design and sourcing support centers in Hong Kong and New York City, New York, as well as offices in China, Denmark, France, Germany, South Korea, Spain, Switzerland and the United Kingdom. The Company’s home office, distribution and shipping facilities, design support centers and stores are currently suitable and adequate.

All of the retail stores operated by the Company, as of March 28, 2018, are located in leased facilities, primarily in shopping centers. The leases expire at various dates, between 2018 and 2031.

For store count and gross square footage by brand and geography as of February 3, 2018 and January 28, 2017, refer to “STORE ACTIVITY,” in “ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.” As of March 28, 2018, the Company’s 868 stores were located as follows:

United States: | ||||||||||

Alabama | 3 | Louisiana | 5 | Ohio | 22 | |||||

Arizona | 12 | Maine | 3 | Oklahoma | 4 | |||||

Arkansas | 3 | Maryland | 11 | Oregon | 6 | |||||

California | 105 | Massachusetts | 24 | Pennsylvania | 27 | |||||

Colorado | 5 | Michigan | 15 | Rhode Island | 2 | |||||

Connecticut | 15 | Minnesota | 9 | South Carolina | 8 | |||||

Delaware | 5 | Mississippi | 3 | Tennessee | 12 | |||||

District Of Columbia | 1 | Missouri | 4 | Texas | 65 | |||||

Florida | 67 | Montana | 1 | Utah | 5 | |||||

Georgia | 18 | Nebraska | 1 | Virginia | 20 | |||||

Hawaii | 7 | Nevada | 8 | Washington | 15 | |||||

Idaho | 2 | New Hampshire | 8 | West Virginia | 3 | |||||

Illinois | 26 | New Jersey | 35 | Wisconsin | 5 | |||||

Indiana | 10 | New Mexico | 3 | Puerto Rico | 2 | |||||

Iowa | 4 | New York | 42 | |||||||

Kansas | 4 | North Carolina | 15 | |||||||

Kentucky | 8 | North Dakota | 1 | |||||||

International: | ||||||||||

Austria | 6 | Hong Kong | 4 | Republic of Korea | 2 | |||||

Belgium | 3 | Ireland | 2 | Singapore | 1 | |||||

Canada | 18 | Italy | 11 | Spain | 12 | |||||

China | 28 | Japan | 11 | Sweden | 3 | |||||

Denmark | 1 | Kuwait | 2 | United Kingdom | 34 | |||||

France | 15 | Netherlands | 4 | United Arab Emirates | 6 | |||||

Germany | 25 | Poland | 1 | |||||||

Refer to “Distribution of Merchandise Inventory,” in “ITEM 1. BUSINESS,” for information regarding the DCs the Company relies on to manage the receipt, storage, sorting, packing and distribution of its merchandise.

19

ITEM 3. | LEGAL PROCEEDINGS |

The Company is a defendant in lawsuits and other adversary proceedings arising in the ordinary course of business. Legal costs incurred in connection with the resolution of claims and lawsuits are generally expensed as incurred, and the Company establishes estimated liabilities for the outcome of litigation where losses are deemed probable and reasonably estimable. The Company’s assessment of the current exposure could change in the event of the discovery of additional facts. As of February 3, 2018, the Company had accrued charges of approximately $18 million for certain legal contingencies, which are classified within other current liabilities on the Consolidated Balance Sheet included in “ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA,” of this Annual Report on Form 10-K. Actual liabilities may differ from the amounts recorded, and there can be no assurance that final resolution of these matters will not have a material adverse effect on the Company’s financial condition, results of operations or cash flows. There are certain claims and legal proceedings pending against the Company for which accruals have not been established.

ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

20

PART II

ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

A&F’s Class A Common Stock (“Common Stock”) is traded on the New York Stock Exchange under the symbol “ANF.” The table below sets forth the high and low sales prices of A&F’s Common Stock on the New York Stock Exchange for Fiscal 2017 and Fiscal 2016:

Sales Price | ||||||||

High | Low | |||||||

Fiscal 2017 | ||||||||

4th quarter | $ | 23.53 | $ | 11.62 | ||||

3rd quarter | $ | 14.82 | $ | 9.03 | ||||

2nd quarter | $ | 14.50 | $ | 8.81 | ||||

1st quarter | $ | 13.75 | $ | 10.50 | ||||

Fiscal 2016 | ||||||||

4th quarter | $ | 17.35 | $ | 11.29 | ||||

3rd quarter | $ | 23.29 | $ | 14.71 | ||||

2nd quarter | $ | 27.37 | $ | 16.49 | ||||

1st quarter | $ | 32.83 | $ | 23.45 | ||||