As filed with the Securities and Exchange Commission on October 6, 2017

Registration No. 333-220208

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

PRE-EFFECTIVE AMENDMENT NO. 2

POST-EFFECTIVE AMENDMENT NO.

(Check appropriate box or boxes)

FRONTIER FUNDS, INC.

(Exact Name of Registrant as Specified in Charter)

400 Skokie Blvd., Suite 500

Northbrook, Illinois 60062

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (847) 509-9860

William D. Forsyth III

400 Skokie Blvd., Suite 500

Northbrook, Illinois 60062

(Name and Address of Agent for Service)

Copies to:

Ellen R. Drought

Godfrey & Kahn, S.C.

833 East Michigan St., Suite 1800

Milwaukee, Wisconsin 53202

Approximate Date of Proposed Public Offering: As soon as practicable after the Registration Statement becomes effective under the Securities Act of 1933, as amended.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

No filing fee is required because of reliance on Section 24(f) of the Investment Company Act of 1940, as amended.

|

Title of Securities Being Registered |

Institutional Class shares of common stock, par value $0.01 per share, of the Frontier Phocas Small Cap Value Fund |

FRONTIER FUNDS, INC.

FRONTIER NETOLS SMALL CAP VALUE FUND

400 Skokie Blvd., Suite 500

Northbrook, Illinois 60062

(847) 509-9860 or toll-free at (888) 825-2100

www.frontiermutualfunds.com

October 9, 2017

Dear Shareholder,

We wish to provide you with some important information concerning your investment. After careful consideration, the Board of Directors of Frontier Funds, Inc. (the "Company") has unanimously approved the reorganization of Frontier Netols Small Cap Value Fund, a series of the Company (the "Acquired Fund"), with and into Frontier Phocas Small Cap Value Fund (the "Acquiring Fund" and together with the Acquired Fund, the "Funds"), also a series of the Company (the "Reorganization"). The Reorganization is subject to approval by shareholders of the Acquired Fund at a special meeting to be held on November 14, 2017.

If shareholders of the Acquired Fund approve the Reorganization, your shares would be exchanged for shares of the Acquiring Fund equal in value to the shares of the Acquired Fund that you currently hold. Frontegra Asset Management, Inc. (the "Adviser") serves as the investment adviser and Phocas Financial Corporation serves as the investment subadviser to both Funds. In addition, both Funds have substantially similar investment objectives, investment strategies and risks. Both Funds also have the same management fee rate and are subject to a similar fee waiver agreement.

In approving the Reorganization, the Board of Directors considered, among other things, the similarities between the Funds' investment objectives, strategies, policies, restrictions and risks; the fact that the Acquiring Fund's expense ratios are the same or lower than the Acquired Fund's; each Fund's prospects for future growth; the relative performance of the Acquiring Fund; the Adviser's agreement to pay all non-trading costs and expenses of the Reorganization; and the expected tax-free nature of the Reorganization to shareholders. Accordingly, the Board recommends you vote FOR the proposed reorganization.

Your vote is important no matter how many shares you own. Voting your shares early will help prevent costly follow-up mail and telephone solicitation. The Proxy Statement/Prospectus provides greater detail about the proposal. The Board recommends that you read the enclosed materials carefully and vote FOR the proposal.

You may choose one of the following options: (i) to authorize a proxy to vote your shares (which is commonly known as proxy voting), or (ii) to vote in person at the Meeting:

• Mail: Complete and return the enclosed proxy card(s).

• Internet: Access the website shown on your proxy card(s) and follow the online instructions.

• Telephone (automated service): Call the toll-free number shown on your proxy card(s) and follow the recorded instructions.

• In person: Attend the Meeting on November 14, 2017.

Thank you for your response and for your continued investment in the Frontier Funds.

Sincerely,

/s/ William D. Forsyth III

William D. Forsyth III

President of Frontier Funds, Inc.

FRONTIER FUNDS, INC.

FRONTIER NETOLS SMALL CAP VALUE FUND

400 Skokie Blvd., Suite 500

Northbrook, Illinois 60062

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To be held on November 14, 2017

Notice is hereby given that a special meeting (the "Meeting") of shareholders of the Frontier Netols Small Cap Value Fund, a series of Frontier Funds, Inc. (the "Company'), will be held on Tuesday, November 14, 2017, at 1:30 p.m., local time, at 400 Skokie Blvd., Suite 500, Northbrook, Illinois 60062 for the purpose of considering the following proposal, as well as any other business that may properly come before the Meeting or any adjournments or postponements thereof.

1. To approve an Agreement and Plan of Reorganization pursuant to which the Frontier Netols Small Cap Value Fund (the "Acquired Fund") will be reorganized with and into the Frontier Phocas Small Cap Value Fund, and the transactions it contemplates.

The Board of Directors of the Company recommends that shareholders vote FOR the proposal. Only shareholders of record of the Acquired Fund at the close of business on September 25, 2017, the record date for the Meeting, are entitled to notice of and to vote at the Meeting and at any adjournments or postponements thereof.

By Order of the Board of Directors,

/s/ William D. Forsyth III

William D. Forsyth III

Secretary of Frontier Funds, Inc.

Northbrook, Illinois

October 9, 2017

IMPORTANT — WE NEED YOUR PROXY VOTE IMMEDIATELY

A shareholder may think that his or her vote is not important, but it is vital for the Frontier Netols Small Cap Value Fund's continued operation. We urge you to sign and date the enclosed proxy card and return it in the enclosed addressed envelope which requires no postage if mailed in the United States (or to take advantage of the telephonic or internet voting procedures described on the proxy card). Your prompt return of the enclosed proxy card (or your authorization of a proxy by other available means) may save the necessity of further solicitations. If you wish to attend the Meeting and vote your shares in person at that time, you will still be able to do so. You may revoke your proxy at any time before it is exercised at the Meeting by submitting to the Secretary of the Frontier Netols Small Cap Value Fund a written notice of revocation or a subsequently signed proxy card or by attending the Meeting and voting in person.

PROXY STATEMENT/PROSPECTUS

Dated October 9, 2017

FOR THE REORGANIZATION OF

FRONTIER NETOLS SMALL CAP VALUE FUND

into

FRONTIER PHOCAS SMALL CAP VALUE FUND

Each a series of Frontier Funds, Inc.

400 Skokie Blvd., Suite 500

Northbrook, Illinois 60062

(888) 825-2100

www.frontiermutualfunds.com

This Proxy Statement/Prospectus contains the information you should know before voting on the proposed reorganization. Please read it carefully and retain it for future reference.

This Proxy Statement/Prospectus is being sent to you in connection with the solicitation of proxies by the Board of Directors (the "Board") of Frontier Funds, Inc. (the "Company") for use at the special meeting (the "Meeting") of shareholders of the Frontier Netols Small Cap Value Fund (the "Acquired Fund") to be held on Tuesday, November 14, 2017, at 1:30 p.m., local time, at 400 Skokie Blvd., Suite 500, Northbrook, Illinois 60062, and any adjournments or postponements thereof. At the Meeting, shareholders of the Acquired Fund will consider an Agreement and Plan of Reorganization (the "Reorganization Agreement"), which provides for the reorganization of the Acquired Fund into the Frontier Phocas Small Cap Value Fund (the "Acquiring Fund"). The Acquired Fund and the Acquiring Fund are each a series of the Company, an open-end investment management company organized as a Maryland corporation.

Under the Reorganization Agreement, as of the closing date of the reorganization, shareholders of the Acquired Fund will receive shares of the Frontier Phocas Small Cap Value Fund (the "Acquiring Fund" and together with the Acquired Fund, the "Funds"), also a series of the Company, equivalent in aggregate net asset value to the aggregate net asset value of their shares of the Acquired Fund, as follows:

As of the date hereof, the Service Class shares of the Acquired Fund had not commenced operations; therefore, there are no Service Class shares outstanding. Accordingly, information regarding the Service Class shares of the Acquired Fund is omitted from this Proxy Statement/Prospectus.

If you need additional copies of this Proxy Statement/Prospectus or the proxy card, please contact the Company at 1-888-825-2100 or in writing at Frontier Funds, Inc., 400 Skokie Blvd., Suite 500, Northbrook, Illinois 60062. Additional copies of the Proxy Statement/Prospectus will be delivered to you promptly upon request. To obtain directions to attend the Meeting, please call 1-888-825-2100. For a free copy of the Funds' Semi-Annual and Annual Reports to Shareholders for the Fiscal Periods ended December 31, 2016 and June 30, 2017, respectively, please contact the Company at the telephone number and address listed above, or visit the Funds' website at http://frontiermutualfunds.com/.

A copy of the form of the Reorganization Agreement is attached to this Proxy Statement/Prospectus as Appendix A.

This Proxy Statement/Prospectus sets forth the basic information you should know before voting on the proposal and investing in the Acquiring Fund. You should read it and keep it for future reference. It is both a Proxy Statement for the Meeting and a Prospectus for the Acquiring Fund.

The following documents have been filed with the Securities and Exchange Commission (the "SEC") and are incorporated by reference herein:

• The Statement of Additional Information relating to transactions described herein, dated October 9, 2017 (the "Reorganization SAI");

• The Prospectus for the Acquired Fund, dated October 31, 2016, as supplemented to date (the "Acquired Fund Prospectus");

• The Prospectus for the Acquiring Fund, dated October 31, 2016, as supplemented to date (the "Acquiring Fund Prospectus" and together with the Acquired Fund Prospectus, the "Fund Prospectus"); and

• The Statement of Additional Information of the Company, dated October 31, 2016, as supplemented to date, but only with respect to the information about the Funds (the "Fund SAI").

In addition, the Acquiring Fund Prospectus accompanies this Proxy Statement/Prospectus.

This Proxy Statement/Prospectus and the accompanying materials were first mailed to shareholders of the Acquired Fund on or about October 9, 2017. Additional copies of these materials and other information about the Company, the Acquired Fund, and the Acquiring Fund are available upon request and without charge by writing to the address below, by visiting the Company's website at http://frontiermutualfunds.com/, or by calling the telephone number listed as follows:

Frontier Funds, Inc.

c/o U.S. Bancorp Fund Services, LLC

P.O. Box 701

Milwaukee, Wisconsin 53201-0701

(847) 509-9860 or toll-free at (888) 825-2100

www.frontiermutualfunds.com

Important Notice Regarding the Availability of Proxy Materials for the Shareholder Meeting to be held on November 14, 2017: The Notice of Meeting and Proxy Statement/Prospectus are available at www.proxyonline.com/docs/frontiernetols.pdf.

The SEC has not approved or disapproved the Acquiring Fund shares to be issued in the Reorganization nor has it passed on the accuracy or adequacy of this Proxy Statement/Prospectus. Any representation to the contrary is a criminal offense.

Mutual fund shares are not deposits or obligations of, or guaranteed or endorsed by, any bank, and are not insured by the Federal Deposit Insurance Corporation. Mutual fund shares involve investment risk, including the possible loss of principal.

No person has been authorized to give any information or to make any representations other than those contained in this Proxy Statement/Prospectus and in the materials expressly incorporated herein by reference and, if given or made, such other information or representations must not be relied upon as having been authorized by the Funds.

Table of Contents

|

Page |

|||||||

|

PROPOSAL 1 APPROVAL OF THE REORGANIZATION AGREEMENT |

1 |

||||||

|

SUMMARY |

1 |

||||||

|

INFORMATION ABOUT THE REORGANIZATION |

14 |

||||||

| VOTING INFORMATION |

19 |

||||||

| ADDITIONAL INFORMATION ABOUT THE FUNDS |

19 |

||||||

| AVAILABLE INFORMATION |

24 |

||||||

| LEGAL MATTERS |

24 |

||||||

| EXPERTS |

24 |

||||||

|

Appendix A — Form of Agreement and Plan of Reorganization |

A-1 |

||||||

|

Appendix B — Financial Highlights |

B-1 |

||||||

PROPOSAL 1

APPROVAL OF THE REORGANIZATION AGREEMENT

SUMMARY

This Proxy Statement/Prospectus is related to the reorganization of the Frontier Netols Small Cap Value Fund (the "Acquired Fund") with and into the Frontier Phocas Small Cap Value Fund (the "Acquiring Fund"), each a series of Frontier Funds, Inc. (the "Company"), which involves (1) the transfer of all of the assets and liabilities of the Acquired Fund to the Acquiring Fund; (2) the issuance of Institutional Class shares of common stock by the Acquiring Fund (the "Acquiring Fund Shares") to the Acquired Fund equal in value to the aggregate net asset value of the Institutional Class and Class Y shares of the Acquired Fund (the "Acquired Fund Shares") as of the time at which the Acquired Fund and the Acquiring Fund calculate their net asset values (the "Valuation Time") on the closing date of the reorganization; (3) the opening of accounts by the Acquiring Fund for the Acquired Fund shareholders and the crediting of Acquired Fund shareholders, in exchange for their Acquired Fund Shares, with that number of full and fractional Acquiring Fund Shares that are equivalent in aggregate net asset value to the aggregate net asset value of the shareholders' Acquired Fund Shares as of the Valuation Time; and (4) the dissolution and termination of the Acquired Fund (collectively referred to as the "Reorganization"). The Reorganization will be effected pursuant to the terms and conditions of an Agreement and Plan of Reorganization (the "Reorganization Agreement"), and is expected to close on or about November 17, 2017 (the "Closing Date"). The Acquired Fund and the Acquiring Fund are collectively referred to as the "Funds."

The following is a summary of more complete information appearing later in this Proxy Statement/Prospectus. You should read carefully the entire Proxy Statement/Prospectus, including the Reorganization Agreement, which is attached as Appendix A, because it contains details that are not in the summary.

The primary purpose of the Reorganization is to streamline the Company's small cap value portfolio offerings that have the same advisory and subadvisory relationships. The former subadviser of the Acquired Fund recently notified Frontegra Asset Management, Inc., the investment adviser to each Fund (the "Adviser"), that it wished to resign as subadviser due to the pending retirement of its lead portfolio manager. In order to avoid disruption to the Acquired Fund and its shareholders and to ensure orderly transition of the Fund's portfolio management, the Board of Directors of the Company (the "Board") determined to terminate the subadvisory agreement and approved an interim subadvisory agreement with Phocas Financial Corporation ("Phocas"), the subadviser to the Acquiring Fund, which was managed in a substantially similar small cap value strategy as the Acquired Fund. Thereafter, following careful consideration, the Board determined that reorganizing the Acquired Fund into the Acquiring Fund is in the best interests of shareholders of the Funds and that the interests of the existing shareholders of the Funds will not be diluted as a result of the proposed Reorganization. The Reorganization is expected to be a tax-free reorganization for federal income tax purposes under Section 368(a) of the Internal Revenue Code of 1986, as amended (the "Code"). For information on the tax consequences of the Reorganization, see the sections entitled "Summary — Federal Income Tax Consequences of the Reorganization" and "Information About the Reorganization — Federal Income Tax Consequences" in this Proxy Statement/Prospectus.

Comparison of the Acquired Fund to the Acquiring Fund. The following table presents a side-by-side comparison of the Acquired Fund to the Acquiring Fund.

|

Frontier Netols Small Cap Value Fund (Acquired Fund) |

Frontier Phocas Small Cap Value Fund Institutional Class (Acquiring Fund and Acquiring Class) |

||||||||||

|

Form of Organization |

A diversified series of the Company, an open-end investment management company organized as a Maryland corporation. |

Same. |

|||||||||

|

Net Assets as of June 30, 2017 |

Institutional Class — $44,237,651 Class Y — $93,796 |

Institutional Class — $34,505,978 |

|||||||||

1

|

Frontier Netols Small Cap Value Fund (Acquired Fund) |

Frontier Phocas Small Cap Value Fund Institutional Class (Acquiring Fund and Acquiring Class) |

||||||||||

|

Investment Adviser and Portfolio Managers |

Investment Adviser: Frontegra Asset Management, Inc. Sub-Adviser: Phocas Financial Corporation. Phocas became the subadviser to the Acquired Fund effective July 1, 2017 pursuant to an interim subadvisory agreement approved by the Board of Directors of the Company. Phocas replaced Netols Asset Management, Inc. as subadviser to the Acquired Fund following notice that Netols wished to resign as subadviser to the Acquired Fund. Portfolio Managers: William Schaff and Steve Block co-manage the Acquired Fund, and have done so since Phocas became the Fund's subadviser on July 1, 2017. |

Investment Adviser: Same. Sub-Adviser: Phocas is also the subadviser to the Acquiring Fund, and has served in this capacity since 2010. Portfolio Managers: The same portfolio managers who manage the Acquired Fund's portfolio manage the Acquiring Fund's portfolio, and have done so since inception. |

|||||||||

|

Annual Operating Expenses as a Percentage of Average Net Assets (Please see Summary Fee Table on page 11 for more complete information) |

Actual Fees For the Year Ended June 30, 2017: Total Operating Expenses Institutional Class 1.25% Class Y* 1.25% Fee Waiver and Expense Reimbursement Institutional Class (0.30)% Class Y (0.30)% Net Operating Expenses** Institutional Class 0.95% Class Y 0.95% *Class Y shares of the Acquired Fund are subject to an annual distribution fee of up to 0.25% and an annual shareholder servicing fee of up to 0.15%, but such fees were not accrued in fiscal 2017. **The Adviser has agreed to waive its management fee and/or reimburse the Acquired Fund's operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, acquired fund fees and expenses ("AFFE") and extraordinary expenses) do not exceed 0.95% and 1.35% of the Fund's average daily net assets attributable to Institutional Class and Class Y shares, respectively. The Adviser is entitled to recoup the fees waived and/or expenses reimbursed within a three-year period from the time the expenses were incurred to the extent of the expense limitation described above is in place at the time of recoupment. The expense cap agreement will continue in effect until October 31, 2019, with successive renewal terms of one year unless terminated by the Adviser or the Company prior to any such renewal. The current expense cap agreement can be terminated only by, or with the consent of, the Board of Directors of the Company. The expense cap agreement between the Adviser and the Acquired Fund was effective July l, 2017, which had the effect of reducing the net expense ratio of each class offered by the Funds by 0.15%. The expense information in this table has been restated to reflect current fees and to reflect the fact that Class Y Shares did not accrue 12b-1 or shareholder servicing fees in fiscal 2017. |

Pro Forma Fees (assuming the Reorganization occurred on the first day of the 12-month period ended June 30, 2017): Total Operating Expenses Institutional Class 1.17% Fee Waiver and Expense Reimbursement Institutional Class (0.22)% Net Operating Expenses* Institutional Class 0.95% *The Adviser has entered into the same fee waiver agreement for the Acquiring Fund as the Adviser has with the Acquired Fund, with the same fee cap for Institutional Class shares (0.95%), but with a lower fee cap for the Acquiring Fund's Institutional Class shares than the Acquired Fund's Class Y shares (0.95% versus 1.35%). The expense cap agreement between the Adviser and the Acquiring Fund was effective July l, 2017, which had the effect of reducing the net expense ratio of each class offered by the Funds by 0.15%. The expense information in this table has been restated to reflect current fees. |

|||||||||

2

|

Frontier Netols Small Cap Value Fund (Acquired Fund) |

Frontier Phocas Small Cap Value Fund Institutional Class (Acquiring Fund and Acquiring Class) |

||||||||||

|

Investment Objective |

The Acquired Fund's investment objective is capital appreciation. This investment objective is fundamental and may not be changed without shareholder approval. |

The Acquiring Fund's investment objective is substantially the same as the Acquired Fund's: long-term total investment return though capital appreciation. Like the Acquired Fund's investment objective, this investment objective is fundamental and may not be changed without shareholder approval. |

|||||||||

|

Principal Investment Strategies |

Under normal market conditions, the Acquired Fund invests at least 80% of its net assets in domestic common stocks and other equity securities (including convertible preferred stocks and warrants) of small-capitalization companies, consistent with companies within the Russell 2000® Value Index. For purposes of the 80% policy, net assets include any borrowings for investment purposes. The Acquired Fund pursues its investment objective by investing in a diversified portfolio of small-capitalization securities selling at discounts to their fair value as assessed by the investment and research team of Phocas. Phocas will typically invest in 80 to 120 companies with initial weightings between 0.50% to 1.50% of the Acquired Fund's total assets in order to have broad industry representation and reduce individual security risk within the Acquired Fund. |

Same. |

|||||||||

|

Investment Process |

Initial Screening. The selection process for the Acquired Fund focuses on U.S. small-cap value stocks. Phocas conducts an initial screening of marketable U.S. equity universe for liquidity and market capitalization. The initial screening eliminates the large and mid-cap U.S. equity universe, and also the micro-cap U.S. equity universe. Phocas establishes valuation screens for each major industry segment of the Russell 2000® Value Index. Traditional valuation metrics such as price/book, price/sales, cash flow metrics and other factors are used either individually or in combination. Depending upon the industry segment, adjustments are made for balance sheet risk relative to peer group. The initial screens are intended to result in identifying the most reasonably priced companies within the U.S. small-cap universe. |

Same. |

|||||||||

3

|

Frontier Netols Small Cap Value Fund (Acquired Fund) |

Frontier Phocas Small Cap Value Fund Institutional Class (Acquiring Fund and Acquiring Class) |

||||||||||

|

Research. Phocas' research team then focuses on specific company qualitative analysis, income statement and balance sheet review, as well as any other major factors that might impact share price. Portfolio Management. The Acquired Fund will have exposure to most of the major industry segments of the Russell 2000® Value Index that equal or exceed 5% of the total index. The portfolio will invest in every major sector with no less than 50% exposure to the benchmark industry weight, or more than 200% of the benchmark weight, with a maximum of 50% in any one sector regardless of the 200% limit; provided, however, the Acquired Fund will not invest more than 25% of its assets in any one industry. |

|||||||||||

|

Temporary Investment Strategies |

The Acquired Fund may invest up to 100% of its total assets in cash, money market mutual funds and short-term fixed income securities as a temporary defensive position during adverse market, economic or political conditions or in other limited circumstances, such as in the case of unusually large cash inflows or redemptions. When so invested, the Acquired Fund may not achieve its investment objective. |

Same. |

|||||||||

|

Fundamental and Non-Fundamental Investment Policies and Restrictions |

In general, the Acquired Fund has adopted fundamental policies that, subject to certain exceptions, restrict the Acquired Fund with respect to the following activities: 1. purchasing securities of any issuer if, as a result, (i) more than 5% of the Acquired Fund's assets would be invested in the securities of that issuer, or (ii) the Acquired Fund would hold more than 10% of the outstanding voting securities of that issuer; 2. borrowing money; 3. issuing senior securities; 4. underwriting securities of other issuers; 5. purchasing or selling commodities; 6. lending any security or making any other loan; 7. concentrating its investments in any particular industry or group of industries; 8. purchasing or selling real estate; and 9. changing its investment objective. |

Same. |

|||||||||

4

|

Frontier Netols Small Cap Value Fund (Acquired Fund) |

Frontier Phocas Small Cap Value Fund Institutional Class (Acquiring Fund and Acquiring Class) |

||||||||||

|

Notwithstanding any other fundamental investment policy or restriction, the Acquired Fund may invest all of its assets in the securities of a single open-end management investment company with substantially the same investment objective, policies and restrictions as the Acquired Fund In addition, the Acquired Fund has adopted non-fundamental policies that, subject to certain exceptions, restrict the Acquired Fund with respect to the following activities: 1. selling securities short; 2. buying securities on margin; 3. investing in illiquid and restricted securities; 4. investing in other investment companies in compliance with the Investment Company Act of 1940, as amended (the "1940 Act"); 5. investing all of its assets in the securities of a single open-end management investment company with substantially the same investment objective, policies and restrictions as the Acquired Fund; 6. investing in futures or options on futures; 7. borrowing money, except from banks or through reverse repurchase agreements; 8. making loans other than loans of portfolio securities; and 9. making any change in its investment policy of investing a minimum percentage of its net assets in investments suggested by the Fund's name without first providing shareholders of the Acquired Fund at least 60 days' notice. The Acquired Fund may not change its fundamental investment policies and restrictions without first obtaining shareholder approval. However, non-fundamental investment policies and restrictions may be changed by the Board without obtaining the approval of shareholders. |

Same. Same. |

||||||||||

|

Management and Other Fees |

Management Fees: The Acquired Fund pays the Adviser, on a monthly basis, an annual management fee based on a percentage of the average daily net assets ("ADNA") of the Fund of 1.00%. In addition, for its services to the Acquired Fund, the Adviser (not the Acquired Fund) pays Phocas a subadvisory fee at the annual rate of 0.60% of the Acquired Fund's ADNA. | Management Fees. The Acquiring Fund's management fee rate is the same as that of the Acquired Fund. In addition, for its services to the Acquiring Fund, the Adviser (not the Acquiring Fund) pays Phocas a subadvisory fee at an annual rate of 0.25% of the Acquiring Fund's ADNA of $75 million or less and 50% of the net fee received by the Adviser from the Fund if the Acquiring Fund's net assets exceed $75 million. | |||||||||

5

|

Frontier Netols Small Cap Value Fund (Acquired Fund) |

Frontier Phocas Small Cap Value Fund Institutional Class (Acquiring Fund and Acquiring Class) |

||||||||||

|

Distribution (Rule 12b-1) Fees: The Class Y shares of the Acquired Fund pay a Rule 12b-1 distribution fee at the annual rate of up to 0.25% of the Acquired Fund's ADNA. This fee is paid to the Acquired Fund's distributor, which in turn, uses the fee to pay financial intermediaries who perform activities intended to result in the sale of the Class Y shares. Following the Reorganization, the Acquired Fund's Class Y shares will be exchanged for Institutional Class shares of the Acquiring Fund and the Rule 12b-1 distribution fee will no longer be paid. Other Fees: In addition to the Rule 12b-1 fees, Class Y shares of the Acquired Fund pay a shareholder servicing fee to the Fund's distributor for payments to financial intermediaries for non-distribution services, including, but not limited to, establishing and maintaining shareholder accounts, mailing prospectuses and account statements and other fund documents to shareholders, processing shareholder transactions and providing recordkeeping, sub-accounting and administrative services for Class Y shareholders at the annual rate of up to 0.15% of the Class Y shares' ADNA. The Institutional Class shares of the Acquired Fund may pay a financial intermediary for performing sub-transfer agent and other administrative services to clients that hold such shares through an omnibus account in an amount that is intended to compensate the intermediary for its provision of services of the type that are provided by the Fund's transfer agent. The Acquired Fund also pays a fee to U.S. Bancorp Fund Services, LLC ("USBFS") for transfer agency and custodial services. |

Distribution (Rule 12b-1) Fees: None. Other Fees: The Institutional Class shares of the Acquiring Fund may pay a financial intermediary for performing sub-transfer agent and other administrative services to clients that hold such shares through an omnibus account in an amount that is intended to compensate the intermediary for its provision of services of the type that are provided by the Fund's transfer agent. The Acquiring Fund also pays a fee to USBFS for transfer agency and custodial services. |

||||||||||

|

Buying Shares |

You may buy shares directly through the Acquired Fund's transfer agent or other financial intermediaries. |

Same. |

|||||||||

|

Exchange Privilege |

You may exchange all or a portion of your investment in the Acquired Fund between classes or from one series of the Company to another series free of charge, subject to limitations under the Company's market timing policy to ensure that the exchanges do not disadvantage the Acquired Fund or its shareholders. |

Same. |

|||||||||

6

|

Frontier Netols Small Cap Value Fund (Acquired Fund) |

Frontier Phocas Small Cap Value Fund Institutional Class (Acquiring Fund and Acquiring Class) |

||||||||||

|

Redeeming Shares |

Shares of the Acquired Fund will be redeemed at the net asset value ("NAV") per share calculated after the Fund receives your transaction request in proper form. |

Same. |

|||||||||

Comparison of Principal Risks of Investing in the Funds. Because each Fund has the same portfolio managers, substantially similar investment objectives and identical investment strategies, the investment risks associated with an investment in the Acquired Fund are substantially the same as those associated with an investment in the Acquiring Fund. A discussion of the principal risks of investing in the Acquired Fund is set forth below, which risks also apply to an investment in the Acquiring Fund except as otherwise noted. This discussion is qualified in its entirety by the more extensive discussion of risk factors set forth in the Fund Prospectus. As with all mutual funds, there is the risk that you could lose all or a portion of your investment in the Funds.

Market Risks. An investment in the Fund is subject to market risk, which may cause the value of the Fund's investments to decline. If the value of the Fund's investments goes down, the share price of the Fund will go down, and you may lose money. U.S. and international markets have experienced extreme volatility, reduced liquidity, credit downgrades, increased likelihood of default and valuation difficulties in recent years.

Equity Securities Risks. Common stocks and other equity securities held by the Fund will fluctuate in value based on the earnings of the company and on general industry and market conditions, leading to fluctuations in the Fund's share price.

Foreign Securities Risks. Investments in securities of foreign companies involve additional risks, including less liquidity, currency-rate fluctuations, political and economic instability, differences in financial reporting standards and securities market regulation, and imposition of foreign withholding taxes.

Stock Selection Risks. The stocks selected for the Fund may decline in value or not increase in value when the stock market in general is rising.

Small Capitalization Company Risks. Securities of companies with small market capitalizations are often more volatile, less liquid and more susceptible to market pressures than larger companies.

Management Risks. The Fund is subject to management risk as an actively-managed investment portfolio and depends on the decisions of the portfolio managers to produce the desired results.

Value Investing Risks. The Fund invests primarily in value-style stocks, stocks whose prices Phocas believes are undervalued in relation to fundamental measures. Value stocks may never increase in price or pay dividends as anticipated by Phocas, or may decline even further if the market fails to recognize the company's value, if the factors that Phocas believes will increase the price do not occur or if a stock judged to be undervalued is actually appropriately priced.

Sector Risks. Although Phocas selects stocks based on their individual merits, some economic sectors will represent a larger portion of the Fund's overall investment portfolio than other sectors. Potential negative market or economic developments affecting one of the larger sectors could have a greater impact on the Fund than on a fund with fewer holdings in that sector. Given the current composition of the Russell 2000® Value Index, the Fund may invest a relatively large percentage of its assets in the financial sector and, therefore, the Fund's performance may be adversely affected by volatility in financial and credit markets. Financial services companies are subject to extensive government regulation, interest rate risk, credit losses and price competition, among other factors.

Cybersecurity Risks. Despite the various protections utilized by the Fund and its service providers, systems, networks, or devices utilized by the Fund potentially can be breached. The Fund and its shareholders could be negatively impacted as a result of a cybersecurity breach.

High Portfolio Turnover Risk (Acquired Fund only). Because Phocas only recently began subadvising the Fund on July 1, 2017, during the initial period of Phocas' management, the Fund may experience

7

a high portfolio turnover rate (over 100%). High portfolio turnover is likely to lead to increased Fund expenses, such as brokerage commissions and other transaction costs. Additionally, a high portfolio turnover rate may result in higher short-term capital gains taxable to shareholders and in lower investment returns. Following the Reorganization, this risk factor is not expected to be applicable.

Other Consequences of the Reorganization.

Management Fee and Structure. The Adviser serves as the investment adviser to both the Acquired Fund and the Acquiring Fund, and for these services, the Adviser receives a management fee from both Funds at the same annual rate. Each Fund pays the Adviser an annual rate of 1.00% of each Fund's ADNA.

In addition, for its subadvisory services to the Acquired Fund, the Adviser (not the Acquired Fund) pays Phocas a fee at the annual rate of 0.60% of the Acquired Fund's ADNA. For its subadvisory services to the Acquiring Fund, the Adviser (not the Acquiring Fund), pays Phocas a fee at the annual rate of 0.25% of the Acquiring Fund's ADNA of $75 million or less and 50% of the net fee received by the Adviser from the Fund if the Acquiring Fund's net assets exceed $75 million. After the Reorganization, the Adviser will continue to serve as the investment adviser, and Phocas will continue to serve as subadviser, to the Acquiring Fund.

Expense Limitations. Currently, both Funds are party to a fee waiver agreement with the Adviser pursuant to which the Adviser has agreed to waive its management fee and/or reimburse the Funds' operating expenses to the extent necessary to ensure that the Fund's total operating expenses (excluding taxes, interest, brokerage commissions, AFFE and extraordinary expenses) do not exceed the following limits:

• Acquired Fund: Institutional Class shares — 0.95% of ADNA; and Class Y shares — 1.35% of ADNA.

• Acquiring Fund: Institutional Class shares — 0.95% of ADNA.

The Adviser is entitled to recoup the fees waived and/or expenses reimbursed within a three-year period from the time the expenses were incurred to the extent of the expense limitations described above and in place at the time of recoupment. The expense cap agreement will continue in effect until October 31, 2019, with successive renewal terms of one year unless terminated by the Adviser or the Company prior to any such renewal. The current expense cap agreement can be terminated only by, or with the consent of, the Board of Directors of the Company.

Share Classes. In connection with the Reorganization, shareholders of the Acquired Fund will receive Institutional Class shares of the Acquiring Fund. Institutional Class shares of the Acquired Fund will be exchanged for Institutional Class shares of the Acquiring Fund and Class Y shares of the Acquired Fund will be exchanged for Institutional Class shares of the Acquiring Fund. Because of the fee waiver agreement described above, if the Reorganization is consummated, shareholders of the Acquired Fund's Institutional Class shares will see no change in overall fund expenses (total annual net operating expenses will remain limited to 0.95% of average net assets), while shareholders of the Acquired Fund's Class Y shares will experience lower net expenses (total annual net operating expenses will be subject to a limit of 0.95% of average net assets rather than the current 1.35% of average net assets).

Information Regarding Purchases, Exchanges and Redemption of Shares. The following describes the procedures for buying, exchanging, and redeeming Fund shares. Because both Funds are separate portfolios of the same fund family and both Funds offer Institutional Class and Service Class shares, the procedures described below are applicable to both Funds.

Buying Shares. You may purchase or redeem shares of the Funds on any business day by written request to Frontier Funds, Inc., c/o U.S. Bancorp Fund Services, LLC, P.O. Box 701, Milwaukee, Wisconsin 53201-0701, by wire or through a financial intermediary. The Funds' minimum initial and subsequent investment amounts are shown below, which may be modified for purchases made

8

through certain financial intermediaries. The Funds may reduce or waive the minimums in its sole discretion.

|

Minimum Initial Investment |

Minimum Subsequent Investments |

||||||||||

|

Institutional Class |

$ |

100,000 |

$ |

1,000 |

|||||||

|

Class Y* |

$ |

1,000 |

$ |

50 |

|||||||

* Only the Acquired Fund offers Class Y shares, which will be exchanged for Institutional Class shares of the Acquiring Fund in connection with the Reorganization.

Exchange Privilege. You may exchange all or a portion of your investment in the Acquired Fund between classes or from one Frontier Fund to another Frontier Fund free of charge, subject to limitations under the Market Timing Policy to ensure that the exchanges do not disadvantage the Acquired Fund or its shareholders.

Redeeming Shares. Shares of the Acquired Fund will be redeemed at the NAV per share calculated after the Fund receives your transaction request in proper form.

Past Performance. The bar charts and tables below show the historical performance of the Funds' shares and provide some indication of the risks of investing in the Funds. The bar charts show how the Funds' total returns before taxes have varied from year to year, while the tables compare the Funds' average annual total returns to the returns of a broad measure of market performance and an index of funds with similar investment objectives. Please keep in mind that past performance, before and after taxes, does not represent how the Funds will perform in the future. Investors may obtain updated performance information for the Funds at www.frontiermutualfunds.com. The Acquiring Fund will be the survivor of the Reorganization for performance reporting purposes.

FRONTIER NETOLS SMALL CAP VALUE FUND

(Acquired Fund)

Calendar Year Total Returns for Institutional Class Shares

|

The Fund's return from January 1, 2017, through June 30, 2017, was 1.26%. |

|||

Best and Worst Quarterly Performance (during the periods shown above)

| Best Quarter Return |

Worst Quarter Return |

||||||

| 19.58% (2nd quarter, 2009) |

(25.16)% (3rd quarter, 2011) |

||||||

9

Average Annual Total Returns

(For the periods ended December 31, 2016)

|

One Year |

Five Year |

Ten Year or Since Inception (if less)(1) |

|||||||||||||

|

Institutional Class |

|||||||||||||||

|

Return Before Taxes |

19.62 |

% |

13.14 |

% |

7.25 |

% |

|||||||||

|

Return After Taxes on Distributions |

17.78 |

% |

8.98 |

% |

5.23 |

% |

|||||||||

|

Return After Taxes on Distributions and Sale of Fund Shares |

12.67 |

% |

10.08 |

% |

5.66 |

% |

|||||||||

|

Russell 2000 Value Index (reflects no deductions for fees, expense or taxes) |

31.74 |

% |

15.07 |

% |

6.26 |

% |

|||||||||

|

Class Y |

|||||||||||||||

|

Return Before Taxes |

19.42 |

% |

12.83 |

% |

6.53 |

% |

|||||||||

|

Russell 2000 Value Index (reflects no deductions for fees, expense or taxes) |

31.74 |

% |

15.07 |

% |

7.57 |

% |

|||||||||

(1) The Institutional Class and Class Y commenced operations on December 16, 2005, and November 1, 2007, respectively.

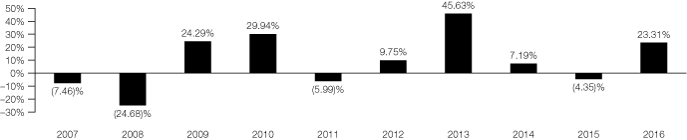

FRONTIER PHOCAS SMALL CAP VALUE FUND

(Acquiring Fund)

Calendar Year Total Returns for Institutional Class Shares(1)(2)

(1) The Acquiring Fund is the successor to the Phocas Small Cap Value Fund (the "Predecessor Fund") pursuant to a reorganization that was completed on October 8, 2010. Prior to this date, the Acquiring Fund had no investment operations. Accordingly, the performance and financial information for the periods prior to October 8, 2010, is historical information for the Predecessor Fund.

(2) Returns for calendar years 2007-2009 and for the period from January 1, 2010, to October 7, 2010, reflect the performance of the Predecessor Fund. Returns for the period from October 8, 2010, to October 31, 2012, reflect the performance of the Class L shares of the Fund. Effective November 1, 2012, the Class L shares were redesignated as Institutional Class shares.

|

The Fund's return from January 1, 2017, through June 30, 2017, was (0.40)%. |

|||

Best and Worst Quarterly Performance (during the periods shown above)

| Best Quarter Return |

Worst Quarter Return |

||||||

| 22.69% (3rd quarter, 2009) |

(20.11)% (3rd quarter, 2011) |

||||||

10

Average Annual Total Returns(1)

(For periods ended December 31, 2016)

|

One Year |

Five Year |

Ten Year |

|||||||||||||

|

Institutional Class |

|||||||||||||||

|

Return Before Taxes |

23.31 |

% |

15.11 |

% |

7.90 |

% |

|||||||||

|

Return After Taxes on Distributions |

23.19 |

% |

14.32 |

% |

7.48 |

% |

|||||||||

|

Return After Taxes on Distributions and Sale of Fund Shares |

13.29 |

% |

12.01 |

% |

6.35 |

% |

|||||||||

|

Russell 2000® Value Index (reflects no deductions for fees, expenses or taxes) |

31.74 |

% |

15.07 |

% |

6.26 |

% |

|||||||||

(1) Fund returns for the period from September 29, 2006 to October 7, 2010, reflect the performance of the Predecessor Fund. Fund returns for the period from October 8, 2010, to October 31, 2012, reflect the performance of the Class L shares of the Fund. Effective November 1, 2012, the Class L shares were redesignated as Institutional Class shares.

After-tax returns are shown only for Institutional Class shares for the Funds and after-tax returns for other share classes will vary. After-tax returns for the Funds were calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor's tax situation and may differ from those shown, and after-tax returns are not relevant to investors who hold shares of the Funds through tax-deferred arrangements, such as a 401(k) plan or individual retirement account. In certain cases, the figure representing "Return After Taxes on Distributions and Sale of Fund Shares" may be higher than other return figures for the same period. A higher after-tax return results when a capital loss occurs upon redemption and provides an assumed tax deduction that benefits the investor.

The Funds' Fees and Expenses. The following table shows the current fees and expenses for the Acquired Fund compared to those of the Acquiring Fund (based on the fiscal year ended June 30, 2017) and the pro forma fees and expenses of the Acquiring Fund assuming the Reorganization had occurred on the first day of the twelve-month year ended June 30, 2017.

As discussed above, Institutional Class shares of the Acquired Fund will be exchanged for Institutional Class shares of the Acquiring Fund and Class Y shares of the Acquired Fund will be exchanged for Institutional Class shares of the Acquiring Fund in the Reorganization.

Summary Fee Table

|

Frontier Netols Small Cap Value Fund (Acquired Fund) |

Frontier Phocas Small Cap Value Fund (Acquiring Fund) |

Frontier Phocas Small Cap Value Fund Pro Forma (Acquiring Fund) |

|||||||||||||||||

|

Shareholder Transaction Fees (fees paid directly from your investment)(1) |

Institutional |

Class Y |

Institutional |

Institutional |

|||||||||||||||

|

Redemption Fee (as a percentage of the amount redeemed) |

None |

None |

None |

None |

|||||||||||||||

|

Service Fee (for shares redeemed by wire) |

$ |

15.00 |

$ |

15.00 |

$ |

15.00 |

$ |

15.00 |

|||||||||||

|

Annual Fund Operating Expenses (expenses you pay each year as a percentage of the value of your investment)(2) |

|||||||||||||||||||

|

Management Fees |

1.00 |

% |

1.00 |

% |

1.00 |

% |

1.00 |

% |

|||||||||||

|

Distribution (12b-1) Fees |

None |

None(3) |

None |

None |

|||||||||||||||

|

Other Expenses |

|||||||||||||||||||

|

Shareholder Servicing Fee |

None |

None(3) |

None |

None |

|||||||||||||||

|

Additional Other Expenses |

0.25 |

% |

0.25 |

% |

0.45 |

% |

0.17 |

% |

|||||||||||

|

Total Other Expenses |

0.25 |

% |

0.25 |

% |

0.45 |

% |

0.17 |

% |

|||||||||||

|

Total Annual Fund Operating Expenses |

1.25 |

% |

1.25 |

% |

1.45 |

% |

1.17 |

% |

|||||||||||

|

Less: Fee Waiver(4) |

(0.30 |

)% |

(0.30 |

)% |

(0.50 |

)% |

(0.22 |

)% |

|||||||||||

|

Total Annual Fund Operating Expenses After Fee Waiver(4) |

0.95 |

% |

0.95 |

%(4) |

0.95 |

% |

0.95 |

% |

|||||||||||

(1) The Funds charge a service fee of $25.00 for checks that do not clear.

(2) Stated as a percentage of ADNA.

11

(3) Class Y shares are subject to an annual distribution fee of up to 0.25%, and a shareholder servicing fee of up to 0.15%, of the Fund's ADNA attributable to Class Y shares. No such fees were accrued in the fiscal year ended June 30, 2017 and such fees are not currently being accrued. However, if shareholders do not approve the Reorganization and the Acquired Fund continues to exist, Class Y shares may incur such fees again in the future.

(4) Pursuant to expense cap agreements between the Adviser and the Funds, the Adviser has agreed to waive its management fee and/or reimburse Fund operating expenses to the extent necessary to ensure that total operating expenses (excluding taxes, interest, brokerage commissions, AFFE and extraordinary expenses) do not exceed the following levels: (i) for the Acquired Fund, 0.95% and 1.35% of the Fund's ADNA attributable to Institutional Class and Class Y shares, respectively; and (ii) for the Acquiring Fund, 0.95% of the Fund's ADNA attributable to Institutional Class shares. The Adviser is entitled to recoup the fees waived and/or expenses reimbursed within a three-year period from the time the expenses were incurred to the extent of the expense limitation described above and in place at the time of recoupment. The expense cap agreements will continue in effect until October 31, 2019, with successive renewal terms of one year unless terminated by the Adviser or the Company prior to any such renewal. The current expense cap agreement can be terminated only by, or with the consent of, the Board of Directors of the Company. The expense cap agreements between the Adviser and the Funds were effective July l, 2017, which had the effect of reducing the net expense ratio of each class offered by the Funds by 0.15%. The expense information in this table has been restated to reflect current fees and to reflect the fact that Class Y Shares did not accrue 12b-1 or shareholder servicing fees in fiscal 2017.

Examples

The Examples below are intended to help you compare the cost of investing in the Acquired Fund with the cost of investing in the Acquiring Fund, assuming the Reorganization has been completed. The Examples assume that you invest $10,000 in the specified Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Examples also assume that your investment has a 5% return each year, and that each Fund's total operating expenses remain the same. The Examples reflect the Adviser's agreement to waive and reimburse expenses as noted in the expense table above. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

Institutional Class and Class Y

|

Fund |

Year 1 |

Year 3 |

Year 5 |

Year 10 |

|||||||||||||||

|

Frontier Netols Small Cap Value Fund — Institutional Class (Acquired Fund) |

$ |

97 |

$ |

336 |

$ |

627 |

$ |

1,457 |

|||||||||||

|

Frontier Phocas Small Cap Value Fund — Institutional Class (Acquiring Fund) |

$ |

97 |

$ |

358 |

$ |

694 |

$ |

1,647 |

|||||||||||

|

Frontier Netols Small Cap Value Fund — Class Y (Acquired Fund) |

$ |

97 |

$ |

336 |

$ |

627 |

$ |

1,457 |

|||||||||||

|

Frontier Phocas Small Cap Value Fund Pro Forma — Institutional Class (Acquiring Fund) |

$ |

97 |

$ |

327 |

$ |

600 |

$ |

1,380 |

|||||||||||

These examples are for comparison purposes only and are not a representation of the Funds' actual expenses and returns, either past or future. Actual expenses may be greater or less than those shown above.

Portfolio Turnover. The Acquired Fund and Acquired Fund pay transaction costs, such as commissions, when each Fund buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when such Fund's shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Funds' performance. During its most recent fiscal year, the Acquired Fund had a portfolio turnover rate of approximately 23% of the average value of its portfolio and the Acquiring Fund had a portfolio turnover rate of approximately 53% of the average value of its portfolio.

Federal Income Tax Consequences of the Reorganization. As a condition to the Reorganization, the Company expects to receive, upon the closing of the Reorganization, an opinion of counsel to the effect that the Reorganization will qualify as a tax-free reorganization for federal income tax purposes within the meaning of Section 368(a) of the Code. Accordingly, while there can be no guarantee that the Internal Revenue Service ("IRS") will adopt a similar position, neither the Funds nor their shareholders will recognize any gain or loss

12

for federal income tax purposes as a result of the Reorganization. In addition, the aggregate tax basis and the holding period of the Acquiring Fund Shares received by each shareholder of the Acquired Fund in the Reorganization will be the same as the aggregate tax basis and holding period of the Acquired Fund Shares given up by such shareholder in the Reorganization; provided that, with respect to the holding period for the Acquiring Fund Shares received, the Acquired Fund Shares given up must have been held as capital assets by the shareholder. As discussed below, following the appointment of Phocas as subadviser on July 1, 2017, the Acquired Fund experienced a much higher portfolio turnover rate.

If any assets would be sold by the Acquired Fund in connection with the Reorganization, the actual tax effect of sales of Acquired Fund assets depends on the difference between the price at which such portfolio assets are sold and the tax basis in such assets of the Acquired Fund. Any capital gains recognized in these sales on a net basis, after reduction by any available capital losses, will be distributed to shareholders as net capital gain distributions (to the extent of net realized long-term capital gains over net realized short-term capital losses) or net investment income distributions (to the extent of net realized short-term capital gains over net realized long-term capital losses) during or with respect to the taxable year of sale that ends on the Closing Date, and such distributions will be taxable to the Acquired Fund's shareholders. Phocas disposed of most of the Acquired Fund's portfolio holdings upon being appointed subadviser to the Acquired Fund effective July 1, 2017. The sale of these positions generated taxable gains, which will be distributed to shareholders of the Acquired Fund prior to the Closing Date.

See "Information About the Reorganization — Federal Income Tax Consequences," below for additional tax information.

* * * * * * * * * * * * *

The preceding is only a summary of certain information contained in this Proxy Statement/Prospectus relating to the Reorganization. This summary is qualified by reference to the more complete information contained elsewhere in this Proxy Statement/Prospectus, the Reorganization SAI, the Fund Prospectus, the Fund SAI and the Reorganization Agreement. Shareholders should read this entire Proxy Statement/Prospectus carefully.

13

INFORMATION ABOUT THE REORGANIZATION

Reasons for the Reorganization. The primary purpose of the Reorganization is to streamline the Company's small cap value portfolio offerings that have the same advisory and subadvisory relationships. The former subadviser of the Acquired Fund recently notified the Adviser that it wished to resign as subadviser due to the pending retirement of its lead portfolio manager. In order to avoid disruption to the Acquired Fund and its shareholders and to ensure orderly transition of the Fund's portfolio management, the Board determined to terminate that subadvisory agreement and approved an interim subadvisory agreement with Phocas. Given that Phocas is the subadviser to two small cap value Funds offered by the Company and in light of the similarities between the investment objective, investment strategies, and risks of the Acquired Fund and the Acquiring Fund, the Adviser recommended the Reorganization, and the Board unanimously approved the Reorganization of the Acquired Fund into the Acquiring Fund. In considering the Adviser's recommendation, the Board considered a number of factors, which are discussed in more detail below, including potential alternatives to the Reorganization. Pursuant to the Reorganization Agreement, the Adviser has agreed to bear all expenses incurred in connection with the Reorganization; provided, however, that the costs of restructuring the Funds' portfolios (if any), including, but not limited to brokerage commissions and other transactions costs, will be borne by the Fund directly incurring them.

The Reorganization is subject to approval by shareholders of the Acquired Fund. If the Acquired Fund does not obtain shareholder approval of the Reorganization, the Board would then consider other alternatives, which may include liquidating the Acquired Fund.

Reorganization Agreement. The Reorganization Agreement sets forth the terms by which the Acquired Fund will be reorganized into the Acquiring Fund. The form of the Reorganization Agreement is attached as Appendix A, and the description of the Reorganization Agreement contained herein is qualified in its entirety by the attached Reorganization Agreement. The following sections summarize the material terms of the Reorganization Agreement and material federal income tax consequences of the Reorganization.

The Reorganization. The Reorganization Agreement provides that upon the transfer of all of the assets and liabilities of the Acquired Fund to the Acquiring Fund, the Acquiring Fund will issue to the Acquired Fund the number of full and fractional Acquiring Fund shares equal in value to the Acquired Fund shares outstanding as of the last daily determination of the Acquired Fund's net asset value as of the close of regular trading on the New York Stock Exchange on the closing date of the Reorganization (the "Valuation Date"). The Acquired Fund will distribute the shares received in the exchange to the shareholders of the Acquired Fund in complete liquidation of the Acquired Fund, on a pro rata basis, and in redemption of its shares. The Acquired Fund will then be terminated as a series of the Company.

Upon completion of the Reorganization, each shareholder of the Acquired Fund will own that number of full and fractional shares of the Acquiring Fund having an aggregate net asset value equal to the aggregate net asset value of such shareholder's shares held in the Acquired Fund as of the Valuation Date. Such shares will be held in an account with the Acquiring Fund identical in all material respects to the account currently maintained by the Acquired Fund for such shareholder.

Until the closing, shareholders of the Acquired Fund will continue to be able to redeem their shares at the net asset value next determined after receipt by the Acquired Fund's transfer agent of a redemption request in proper form. Redemption and purchase requests received by the transfer agent after the closing will be treated as requests received for the redemption or purchase of shares of the Acquiring Fund received by the shareholder in connection with the Reorganization. After the Reorganization, all of the issued and outstanding shares of the Acquired Fund will be canceled on the books of the fund and the transfer agent's books of the Acquired Fund will be permanently closed.

The Reorganization is subject to a number of conditions, including, without limitation, approval by shareholders of the Acquired Fund, the receipt of a legal opinion from counsel to the Funds with respect to certain tax issues, as more fully described in "Federal Income Tax Consequences" below, and the parties' performance in all material respects of their respective agreements and undertakings in the Reorganization Agreement. Assuming satisfaction of the conditions in the Reorganization Agreement, the effective time of the Reorganization will be at 3:00 p.m. Central Time on November 17, 2017, or such other date as is agreed to by the parties.

Federal Income Tax Consequences. Subject to the assumptions and limitations discussed below, the following discussion describes the expected material U.S. federal income tax consequences of the

14

Reorganization to shareholders of the Acquired Fund. This discussion is based on the Code, applicable Treasury regulations, and federal administrative interpretations and court decisions in effect as of the date of this Proxy Statement/Prospectus, all of which may change, possibly with retroactive effect. Any such changes could alter the tax consequences described in this summary.

This discussion of material U.S. federal income tax consequences of the Reorganization does not address all aspects of U.S. federal income taxation that may be important to a holder of Acquired Fund Shares in light of that shareholder's particular circumstances or to a shareholder subject to special rules. In addition, this discussion does not address any other state, local, or foreign income tax or non-income tax consequences of the Reorganization or of any transactions other than the Reorganization. Note: Acquired Fund shareholders are urged to consult their own tax advisers to determine the particular U.S. federal income tax or other tax consequences to them of the Reorganization and the other transactions contemplated herein.

Contingent upon receiving satisfactory representations from the Funds and the absence of material changes in circumstances prior to the Reorganization, the law firm of Godfrey & Kahn, S.C. anticipates rendering an opinion to the Funds substantially to the effect that, based on certain facts, assumptions, and representations made by the Funds, on the basis of existing provisions of the Code, current administrative rules, and court decisions, for federal income tax purposes:

a. the Reorganization will constitute a "reorganization" within the meaning of Section 368(a) of the Code, and the Acquiring Fund and the Acquired Fund will each be "a party to a reorganization" within the meaning of Section 368(b) of the Code;

b. no gain or loss will be recognized by the Acquired Fund upon the transfer of all of its assets to the Acquiring Fund in exchange solely for the Acquiring Fund Shares and the assumption by the Acquiring Fund of the Acquired Fund's liabilities, or upon the distribution of the Acquiring Fund Shares to the Acquired Fund's shareholders in exchange for their shares of the Acquired Fund in complete liquidation of the Acquired Fund, except for any gain or loss that will be recognized (1) on assets in which gain or loss recognition is required by the Code even if the transaction otherwise constitutes a nontaxable transaction, (2) on "Section 1256 contracts" as defined in Section 1256(b) of the Code, (3) on stock in a "passive foreign investment company" as defined in Section 1297(a) of the Code, (4) as a result of the closing of the tax year of the Acquired Fund, or (5) upon termination of a position;

c. no gain or loss will be recognized by the Acquiring Fund upon the receipt of the assets of the Acquired Fund solely in exchange for Acquiring Fund Shares and the assumption by the Acquiring Fund of the liabilities of the Acquired Fund;

d. no gain or loss will be recognized by the Acquired Fund shareholders upon the exchange of their shares of the Acquired Fund for the Acquiring Fund Shares in the Reorganization (including fractional shares to which they may be entitled);

e. the aggregate tax basis of the Acquiring Fund Shares received by each current shareholder of the Acquired Fund pursuant to the Reorganization will be the same as the aggregate tax basis of the shares of the Acquired Fund exchanged therefor;

f. the holding period of the Acquiring Fund Shares received by the Acquired Fund's shareholders (including fractional shares to which they may be entitled) will include the holding period of the Acquired Fund Shares surrendered in exchange therefor, provided that the Acquired Fund Shares were held as a capital asset at time of the exchange;

g. the aggregate tax basis of the assets of the Acquired Fund acquired by the Acquiring Fund will be the same as the basis of such assets to the Acquired Fund immediately prior to the transfer thereof; and

h. the holding period of the assets of the Acquired Fund received by the Acquiring Fund, other than any asset with respect to which gain or loss is required to be recognized as described in (b), above, will include the holding period of those assets in the hands of the Acquired Fund immediately prior to the Reorganization.

If the Funds or the Company are unable to provide satisfactory representations to Godfrey & Kahn, S.C., or if a change in facts or circumstances occurs prior to the Reorganization that adversely affects the tax treatment of the Reorganization, Godfrey & Kahn, S.C. may render a tax opinion with a lower level of certainty than that described above or may be unable to render a tax opinion.

15

If any assets will be sold by the Acquired Fund in connection with the Reorganization, the actual tax effect of such sales depends on the difference between the price at which such portfolio assets are sold and the tax basis in such assets of the Acquired Fund. Any capital gains recognized in these sales on a net basis, after reduction by any available capital losses, will be distributed to shareholders as net capital gain distributions (to the extent of net realized long-term capital gains over net realized short-term capital losses) or net investment income distributions (to the extent of net realized short-term capital gains over net realized long-term capital losses) during or with respect to the year of sale that ends on the date of the Reorganization, and such distributions will be taxable to the Acquired Fund shareholders. Phocas disposed of most of the Acquired Fund's portfolio holdings upon being appointed subadviser to the Acquired Fund effective July 1, 2017. The sale of these positions generated taxable gains, which will be distributed to shareholders of the Acquired Fund prior to the Closing Date. The Reorganization will end the tax year of the Acquired Fund, and will therefore accelerate any required distributions to shareholders from the Acquired Fund for its short tax year ending on the date of the Reorganization. Those tax year-end distributions will be taxable to shareholders who are not tax-exempt and will include any undistributed capital gains resulting from portfolio turnover prior to the Reorganization.

The Reorganization will impact the use of the Acquired Fund's "pre-acquisition losses" (capital loss carryforwards, if any, generated in the Acquired Fund's short taxable year ending on the Closing Date and unrealized losses that exceed certain thresholds) generally in the following manner: (1) the pre-acquisition losses, subject to the limitations described herein, would benefit the shareholders of the combined Fund, rather than only the shareholders of the Acquired Fund; (2) the amount of the pre-acquisition losses that could be utilized in any taxable year will equal the product of long-term tax-exempt rate at such time, multiplied by the aggregate net asset value of the Acquired Fund at the time of the Reorganization (assuming the Acquired Fund is the smaller of the two Funds on the Closing Date), and this yearly limitation would be increased by any capital gains realized after the Reorganization on securities held by the Acquired Fund that had net unrealized appreciation above a certain threshold at the time of the Reorganization; (3) for five years following the date of the Reorganization and assuming certain thresholds are exceeded, subsequently recognized gains that are attributable to appreciation in the Acquiring Fund's portfolio at the time of the Reorganization cannot be utilized against any pre-acquisition losses of the Acquired Fund; and (4) the Acquired Fund's loss carryforwards, as limited under the previous two rules, are permitted to offset that portion of the gains of the Acquiring Fund for the taxable year of the Reorganization that is equal to the portion of the Acquiring Fund's taxable year that follows the date of the Reorganization (prorated according to the number of days).

The Reorganization will impact the use of the Acquiring Fund's pre-Reorganization losses, if any, generally in the following manner: (1) the shareholders of the combined Fund, subject to the limitations described herein, would benefit from the pre-acquisition losses rather than only the shareholders of the Acquiring Fund; and (2) for five years following the date of the Reorganization and assuming certain thresholds are exceeded, any gains recognized after the Reorganization that are attributable to appreciation in the Acquired Fund's portfolio at the time of the Reorganization would not be able to be offset by any pre-acquisition losses of the Acquiring Fund.

The ability of each Fund to use pre-acquisition losses (even in the absence of the Reorganization) also depends on factors other than loss limitations, such as the future realization of capital gains or losses.

As a result of the blending of tax attributes of the Acquired Fund and the Acquiring Fund (as affected by the rules discussed above), shareholders of a Fund may pay taxes sooner, or pay more taxes, than they would have had the Reorganization not occurred.

Shareholders of the Acquired Fund will receive a proportionate share of any taxable income and gains realized by the Acquiring Fund, including any gains realized in connection with portfolio assets sold by the Acquiring Fund in connection with the Reorganization, and not distributed to its shareholders prior to the Reorganization when such income and gains eventually are distributed by the Acquiring Fund. As a result, shareholders of the Acquired Fund may receive a greater amount of taxable distributions than they would have had the Reorganization not occurred. In addition, if the Acquiring Fund, following the Reorganization, has proportionately greater unrealized appreciation in its portfolio investments as a percentage of its net assets than the Acquired Fund, shareholders of the Acquired Fund, post-closing, may receive greater amounts of taxable gain as such portfolio investments are sold than they otherwise might have if the Reorganization had not occurred. At June 30, 2017, the Acquired Fund's unrealized appreciation in value of investments as a percentage of its net asset value was 36% compared to the Acquiring Fund of 24%. Accordingly, the Acquired

16

Fund shareholders, post-closing, will be exposed to slightly less unrealized appreciation in portfolio investments.

If the Reorganization is challenged by the IRS or the courts determine that the Reorganization does not qualify as a tax-free reorganization under the Code, and thus is taxable, the Acquired Fund would recognize gain or loss on the transfer of its assets to the Acquiring Fund and each Acquired Fund shareholder will recognize gain or loss with respect to each Acquired Fund share equal to the difference between that shareholder's adjusted tax basis in the share and the fair market value, as of the time of the Reorganization, of the Acquiring Fund Shares received in exchange therefor. In such event, a shareholder's aggregate adjusted tax basis in the shares of the Acquiring Fund received in the exchange would equal such fair market value, and the shareholder's holding period for the shares would not include the period during which such shareholder held Acquired Fund Shares. In addition, the Acquiring Fund would not be able to use any pre-acquisition losses of the Acquired Fund.

If any of the representations or covenants of the parties in connection with the tax opinion are inaccurate, the tax consequences of the transaction could differ materially from those summarized above. Furthermore, the description of the tax consequences set forth herein and the tax opinion to be issued as described hereunder will neither bind the IRS, nor preclude the IRS or the courts from adopting a contrary position. No assurance can be given that contrary positions will not successfully be asserted by the IRS or adopted by a court if the issues are litigated. No ruling has been or will be requested from the IRS in connection with this transaction. No assurance can be given that future legislative, judicial, or administrative changes, on either a prospective or retroactive basis, or future factual developments, would not adversely affect the accuracy of the conclusions stated herein or the ability of Godfrey & Kahn, S.C. to render an opinion as described above. Therefore, shareholders may find it advisable to consult their own tax adviser as to the specific tax consequences to them under the federal income tax laws, as well as any consequences under other applicable state or local or foreign tax laws given each shareholder's own particular tax circumstances.

Board Considerations. The Adviser recommended that the Board approve the Reorganization. The Adviser believes that its mutual fund offerings and the interest of each Fund's shareholders will be well served by consolidating the Funds and by Phocas managing the Fund's combined assets in accordance with the Acquiring Fund's investment objective and strategy, which are virtually identical to those of the Acquired Fund. In considering and approving the Reorganization at a meeting held on August 22, 2017, the Board discussed the future of the Acquired Fund and the advantages of reorganizing the Acquired Fund into the Acquiring Fund. Among other things, the Board also reviewed, with the assistance of outside legal counsel, the overall proposal for the Reorganization, the principal terms and conditions of the Reorganization Agreement, including that the Reorganization be consummated on a tax-free basis, and certain other materials provided prior to and during the meeting.

In considering the Reorganization, the Board took into account a number of additional factors. Some of the more prominent considerations are discussed further below. The Board considered the following matters, among others and in no order of priority:

• The Acquired Fund and the Acquiring Fund have substantially similar investment objectives and identical investment strategies, investment policies and restrictions;

• The Adviser, subadviser and portfolio managers are identical for the two Funds;

• The other service providers for the Acquired Fund and Acquiring Fund are the same;

• The Board will continue to oversee the Acquiring Fund;

• Both Funds have the same management fee;

• As a result of an expense limitation agreement that is currently in place for both Funds until at least October 31, 2019, shareholders of the Acquired Fund's Institutional Class shares will see no change in overall fund expenses (total annual net operating expenses will remain limited to 0.95% of average net assets), while shareholders of the Acquired Fund's Class Y shares will experience lower net expenses (total annual net operating expenses will be subject to a limit of 0.95% of average net assets rather than the current 1.35% of average net assets);

• Each Fund's prospects for future growth as a standalone fund versus the prospects for growth as a combined fund offering;

17

• The Reorganization is expected to be tax-free for federal income tax purposes for the Acquired Fund and its shareholders;