UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year ended | ||||||||

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Transition period from to . | ||||||||

Commission file No. 001-15891

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices) | (Zip Code) | |||||||

(713 ) 537-3000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Exchange on Which Registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Accelerated filer | ☐ | ||||||||||||||||||||||

| Non-accelerated filer ☐ | Smaller reporting company | ||||||||||||||||||||||

| Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C 7262(b)) by the registered public accounting firm that prepared or issued its audit report ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

As of the last business day of the most recently completed second fiscal quarter, the aggregate market value of the common stock of the registrant held by non-affiliates was approximately $6,266,747,422 based on the closing sale price of $37.39 as reported on the New York Stock Exchange.

Indicate the number of shares outstanding of each of the registrant's classes of common stock as of the latest practicable date.

| Class | Outstanding at February 1, 2024 | |||||||

| Common Stock, par value $0.01 per share | ||||||||

Documents Incorporated by Reference:

Portions of the Registrant's definitive Proxy Statement relating to its 2024 Annual Meeting of Stockholders

1

TABLE OF CONTENTS

2

Glossary of Terms

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below:

| ACE | Affordable Clean Energy | |||||||

| Acquisition | The acquisition of Vivint Smart Home, Inc. by NRG completed on March 10, 2023 | |||||||

| Adjusted EBITDA | Adjusted earnings before interest, taxes, depreciation and amortization | |||||||

| AESO | Alberta Electric System Operator | |||||||

| ARO | Asset Retirement Obligation | |||||||

| ASC | The FASB Accounting Standards Codification, which the FASB established as the source of authoritative GAAP | |||||||

| ASR | Accelerated Share Repurchases | |||||||

| ASU | Accounting Standards Updates – updates to the ASC | |||||||

| AUC | Alberta Utilities Commission | |||||||

| BTU | British Thermal Unit | |||||||

| Business | NRG Business, which serves business customers | |||||||

| CAA | Clean Air Act | |||||||

| CAISO | California Independent System Operator | |||||||

| CAMT | 15% Corporate Alternative Minimum Tax enacted by the IRA on August 16, 2022 | |||||||

| CDD | Cooling Degree Day | |||||||

| CFTC | U.S. Commodity Futures Trading Commission | |||||||

CO2 | Carbon Dioxide | |||||||

CO2e | Carbon Dioxide Equivalents | |||||||

| Company | NRG Energy, Inc. | |||||||

| Convertible Senior Notes | As of December 31, 2023, consists of NRG’s $575 million unsecured 2.75% Convertible Senior Notes due 2048 | |||||||

| Cottonwood | Cottonwood Generating Station, a 1,166 MW natural gas-fueled plant | |||||||

| CPP | Clean Power Plan | |||||||

| CPUC | California Public Utilities Commission | |||||||

| CWA | Clean Water Act | |||||||

| D.C. Circuit | U.S. Court of Appeals for the District of Columbia Circuit | |||||||

| DSI | Dry Sorbent Injection | |||||||

| DSU | Deferred Stock Unit | |||||||

| Dth | Dekatherms | |||||||

| Dual fuel customers | Customer that have both electricity and natural gas service with the Company | |||||||

| Economic gross margin | Sum of retail revenue, energy revenue, capacity revenue and other revenue, less cost of fuels, purchased energy and other cost of sales | |||||||

| EGU | Electric Generating Unit | |||||||

| EPA | U.S. Environmental Protection Agency | |||||||

| EPC | Engineering, Procurement and Construction | |||||||

| ERCOT | Electric Reliability Council of Texas, the Independent System Operator and the regional reliability coordinator of the various electricity systems within Texas | |||||||

| ESP | Electrostatic Precipitator | |||||||

| ESPP | NRG Energy, Inc. Amended and Restated Employee Stock Purchase Plan | |||||||

| Exchange Act | The Securities Exchange Act of 1934, as amended | |||||||

| FASB | Financial Accounting Standards Board | |||||||

| FERC | Federal Energy Regulatory Commission | |||||||

| FGD | Flue gas desulfurization | |||||||

| FPA | Federal Power Act | |||||||

3

| FTRs | Financial Transmission Rights | |||||||

| GAAP | Generally accepted accounting principles in the United States | |||||||

| GHG | Greenhouse Gas | |||||||

| Green Mountain Energy | Green Mountain Energy Company | |||||||

| GW | Gigawatts | |||||||

| GWh | Gigawatt Hours | |||||||

| HDD | Heating Degree Day | |||||||

| Heat Rate | A measure of thermal efficiency computed by dividing the total BTU content of the fuel burned by the resulting kWhs generated. Heat rates can be expressed as either gross or net heat rates, depending whether the electricity output measured is gross or net generation and is generally expressed as BTU per net kWh | |||||||

| Home | NRG Home, which serves residential customers | |||||||

| ICE | Intercontinental Exchange | |||||||

| IoT | Internet of Things | |||||||

| IRA | Inflation Reduction Act | |||||||

| ISO | Independent System Operator, also referred to as RTOs | |||||||

| ISO-NE | ISO New England Inc. | |||||||

| Ivanpah | Ivanpah Solar Electric Generation Station, a 391 MW solar thermal power plant located in California's Mojave Desert in which NRG owns 54.5% interest | |||||||

| kWh | Kilowatt-hours | |||||||

| LaGen | Louisiana Generating LLC | |||||||

| LIBOR | London Inter-Bank Offered Rate | |||||||

| LSEs | Load Serving Entities | |||||||

| LTIPs | Collectively, the NRG LTIP and the Vivint LTIP | |||||||

| MDth | Thousand Dekatherms | |||||||

| Midwest Generation | Midwest Generation, LLC | |||||||

| MISO | Midcontinent Independent System Operator, Inc. | |||||||

| MMBtu | Million British Thermal Units | |||||||

| MMDth | Million Dekatherms | |||||||

| MW | Megawatts | |||||||

| MWh | Saleable megawatt hour net of internal/parasitic load megawatt-hour | |||||||

| NAAQS | National Ambient Air Quality Standards | |||||||

| NEPOOL | New England Power Pool | |||||||

| NERC | North American Electric Reliability Corporation | |||||||

| NERC-CIP | North American Electric Reliability Corporation Critical Infrastructure Protection | |||||||

| Net Capacity Factor | The net amount of electricity that a generating unit produces over a period of time divided by the net amount of electricity it could have produced if it had run at full power over that time period. The net amount of electricity produced is the total amount of electricity generated minus the amount of electricity used during generation | |||||||

| Net Exposure | Counterparty credit exposure to NRG, net of collateral | |||||||

| Net Generation | The net amount of electricity produced, expressed in kWhs or MWhs, that is the total amount of electricity generated (gross) minus the amount of electricity used during generation | |||||||

| NIST | National Institute of Standards and Technology | |||||||

| Nodal | Nodal Exchange is a derivatives exchange | |||||||

| NOL | Net Operating Loss | |||||||

NOx | Nitrogen Oxides | |||||||

| NPNS | Normal Purchase Normal Sale | |||||||

| NRC | U.S. Nuclear Regulatory Commission | |||||||

| NRG | NRG Energy, Inc. | |||||||

4

| NRG LTIP | NRG Energy, Inc. Amended and Restated Long-Term Incentive Plan | |||||||

| Nuclear Decommissioning Trust Fund | NRG's nuclear decommissioning trust fund assets, which were for the Company's portion of the decommissioning of the STP, units 1 & 2 through the sale of STP on November 1, 2023 | |||||||

| NYISO | New York Independent System Operator | |||||||

| NYMEX | New York Mercantile Exchange | |||||||

| OCI/OCL | Other Comprehensive Income/(Loss) | |||||||

| ORDC | Operating Reserve Demand Curve | |||||||

| ORDPA | Online Reliability Deployment Price Adder | |||||||

| PCI DSS | Payment Card Industry Data Security Standard | |||||||

| Peaking | Units expected to satisfy demand requirements during the periods of greatest or peak load on the system | |||||||

| Petra Nova | Petra Nova Parish Holdings, LLC | |||||||

| PJM | PJM Interconnection, LLC | |||||||

| PM2.5 | Particulate Matter that has a diameter of less than 2.5 micrometers | |||||||

| PPA | Power Purchase Agreement | |||||||

| PUCT | Public Utility Commission of Texas | |||||||

| RCRA | Resource Conservation and Recovery Act of 1976 | |||||||

| Receivables Facility | NRG Receivables LLC, a bankruptcy remote, special purpose, wholly-owned indirect subsidiary of the Company's $1.4 billion accounts receivables securitization facility due 2024, which was last amended on October 6, 2023 | |||||||

| Receivables Securitization Facilities | Collectively, the Receivables Facility and the Repurchase Facility | |||||||

| RECs | Renewable Energy Certificates | |||||||

| Renewable PPA | A third-party PPA entered into directly with a renewable generation facility for the offtake of the RECs or other similar environmental attributes generated by such facility, coupled with the associated power generated by that facility | |||||||

| Renewables | Consists of the following projects in which NRG has an ownership interest: Ivanpah and solar generating stations located at various NFL Stadiums | |||||||

| Renewables Platform | The renewable operating and development platform sold to Global Infrastructure Partners with NRG's interest in NRG Yield | |||||||

| REP | Retail electric provider | |||||||

| Repurchase Facility | NRG's $150 million uncommitted repurchase facility related to the Receivables Facility due 2024, which was last amended on October 6, 2023 | |||||||

| Revolving Credit Facility | The Company's $4.3 billion revolving credit facility due 2028, which was last modified on March 13, 2023 | |||||||

| RGGI | Regional Greenhouse Gas Initiative | |||||||

| RMR | Reliability Must-Run | |||||||

| RPS | Renewable Portfolio Standards | |||||||

| RPSU | Relative Performance Stock Unit | |||||||

| RSU | Restricted Stock Unit | |||||||

| RTO | Regional Transmission Organization | |||||||

| SCR | Selective Catalytic Reduction Control System | |||||||

| SEC | U.S. Securities and Exchange Commission | |||||||

| Securities Act | The Securities Act of 1933, as amended | |||||||

| Senior Notes | As of December 31, 2023, NRG's $4.0 billion outstanding unsecured senior notes consisting of $375 million of the 6.625% senior notes due 2027, $821 million of 5.75% senior notes due 2028, $733 million of the 5.25% senior notes due 2029, $500 million of the 3.375% senior notes due 2029, $1.0 billion of the 3.625% senior notes due 2031 and $480 million of the 3.875% senior notes due 2032 | |||||||

5

| Senior Secured First Lien Notes | As of December 31, 2023, NRG’s $3.2 billion outstanding Senior Secured First Lien Notes consists of $600 million of the 3.75% Senior Secured First Lien Notes due 2024, $500 million of the 2.0% Senior Secured First Lien Notes due 2025, $900 million of the 2.45% Senior Secured First Lien Notes due 2027, $500 million of the 4.45% Senior Secured First Lien Notes due 2029 and $740 million of the 7.000% Senior Secured First Lien Notes due 2033 | |||||||

| Series A Preferred Stock | As of December 31, 2023, NRG's Series A Preferred Stock consists of 650,000 outstanding shares of the 10.25% Series A Fixed-Rate Reset Cumulative Redeemable Perpetual Preferred Stock, with a $1,000 liquidation preference per share | |||||||

| Services | NRG Services, which primarily includes the services businesses acquired in the Direct Energy acquisition and the Goal Zero business | |||||||

SO2 | Sulfur Dioxide | |||||||

| SOFR | Secured overnight financing rate | |||||||

| South Central Portfolio | NRG's South Central Portfolio, which owned and operated a portfolio of generation assets consisting of Bayou Cove, Big Cajun-I, Big Cajun-II, Cottonwood and Sterlington, was sold on February 4, 2019. NRG is leasing back the Cottonwood facility through May 2025 | |||||||

| S&P | Standard & Poor's | |||||||

| STP | South Texas Project — nuclear generating facility located near Bay City, Texas in which NRG owned a 44% interest. NRG closed on the sale of its interest in STP on November 1, 2023 | |||||||

| STPNOC | South Texas Project Nuclear Operating Company | |||||||

| Tax Act | The Tax Cuts and Jobs Act of 2017 | |||||||

| TDSP | Transmission/distribution service provider | |||||||

| Texas Genco | Texas Genco LLC | |||||||

| TSR | Total Shareholder Return | |||||||

| TWh | Terawatt Hours | |||||||

| U.S. | United States of America | |||||||

| VaR | Value at Risk | |||||||

| VIE | Variable Interest Entity | |||||||

| Vivint LTIP | Vivint Smart Home, Inc. Long-Term Incentive Plan assumed by NRG pursuant to merger between NRG and Vivint | |||||||

| Winter Storm Elliott | A major winter storm that had impacts across the majority of the United States and parts of Canada occurring in December 2022 | |||||||

| Winter Storm Uri | A major winter and ice storm that had widespread impacts across North America occurring in February 2021 | |||||||

6

PART I

Item 1 — Business

General

NRG Energy, Inc., or NRG or the Company, sits at the intersection of energy and home services. NRG is a leading energy and home services company fueled by market-leading brands, proprietary technologies and complementary sales channels. Across the U.S. and Canada, NRG delivers innovative, sustainable solutions, predominately under brand names such as NRG, Reliant, Direct Energy, Green Mountain Energy and Vivint, while also advocating for competitive energy markets and customer choice. The Company has a customer base that includes approximately 8 million residential consumers in addition to commercial, industrial, and wholesale customers, supported by approximately 13 GW of generation as of December 31, 2023.

NRG sold 152 TWhs of electricity and 1,892 MMDth of natural gas in 2023, making it one of the largest competitive energy retailers in the U.S. As of the end of 2023, NRG had recurring electricity and/or natural gas sales in 25 U.S. states, the District of Columbia, and 8 provinces in Canada, as well as Vivint served customers in all 50 U.S. states. NRG's retail brands, collectively, have the largest share of competitively served residential electric customers in Texas and nationwide.

The following chart represents NRG's sales volumes for the year ended December 31, 2023:

Strategy

NRG's strategy is to maximize stakeholder value by being a leader in the emerging convergence of energy and smart automation in the home and business. Through a diversified supply strategy, the Company sells reliable electricity and natural gas to its customers in the markets it serves, while also providing innovative home solutions to customers. NRG's unique combination of assets and capabilities enables the Company to develop and sell highly differentiated offerings that bring together every day essential services like powering and securing the home through a seamless and integrated experience. This strategy is intended to enable the Company to optimize its unique integrated platform to delight customers, generate recurring cash flow, significantly strengthen earnings and cost competitiveness, and lower risk and volatility. Sustainability is a philosophy that underpins and facilitates value creation across NRG's business for its stakeholders. It is an integral piece of NRG's strategy and ties directly to business success, reduced risks and enhanced reputation.

To effectuate the Company’s strategy, NRG is focused on: (i) serving the energy needs of end-use residential, commercial and industrial, and wholesale counterparties in competitive markets and optimizing on additional revenue opportunities through its multiple brands and channels; (ii) offering a variety of energy products and services, including renewable energy solutions and smart home products and services that are differentiated by innovative features, premium service, integrated platforms, sustainability and loyalty/affinity programs; (iii) excellence in operating performance of its assets; (iv) achieving the optimal mix of supply to serve its customer load requirements through a diversified supply strategy; and (v) engaging in disciplined and transparent capital allocation.

7

The following transactions were completed during 2023 in furtherance of the Company’s strategy: (i) the March 10, 2023 acquisition of Vivint Smart Home, a leading smart home platform company; (ii) portfolio optimization, including the sale of the Company’s 44% equity interest in STP for $1.7 billion; and (iii) disciplined capital allocation through the execution of $1.2 billion in share repurchases and $1.4 billion in debt reduction.

Business Overview

The Company’s core businesses are the sale of electricity and natural gas to residential, commercial and industrial and wholesale customers, supported by the Company's wholesale electric generation, as well as the sale of smart home products and services. NRG manages its electricity and natural gas operations based on the combined results of the retail and wholesale generation businesses with a geographical focus. Vivint Smart Home operations are reported within the Vivint Smart Home segment.

The Company's business is segmented as follows:

•Texas, which includes all activity related to customer, plant and market operations in Texas, other than Cottonwood;

•East, which includes all activity related to customer, plant and market operations in the East;

•West/Services/Other, which primarily includes the following assets and activities: (i) all activity related to customer, plant and market operations in the West and Canada, (ii) the Services businesses, (iii) activity related to the Cottonwood facility and other investments;

•Vivint Smart Home; and

•Corporate activities.

In Texas, the Company’s generation supply is fully integrated with its retail load. This integrated model provides the advantage of being able to supply a portion of the Company’s retail customers with electricity from the Company’s assets, which reduces the need to sell electricity to, and buy electricity from, other institutions and intermediaries, resulting in more stable earnings and cash flows, lower transaction costs and less credit exposure. The integrated model also results in a reduction in actual and contingent collateral through offsetting transactions, thereby reducing transactions with third parties.

The integrated model consists of three core functions in each geographic segment above: Customer Operations, Market Operations and Plant Operations.

Customer Operations

Customer Operations is responsible for growing and retaining the customer base and delivering an outstanding customer experience. This includes acquisition and retention of all of NRG’s residential, small commercial, commercial and industrial, and government customers. NRG employs a multi-brand strategy that leverages a wide array of sales and partnership channels, direct face-to-face sales channels, call centers, websites, and brokers. Go-to-market activities include market strategy planning and development, product innovation, offer design, campaign execution, marketing and creative services, and selling. Customer portfolio maintenance and retention activities include fulfillment, billing, payment processing, collections, customer service, issue resolution, and contract renewals. NRG provides energy and related services at either fixed, indexed or month-to-month prices. Home customers typically contract for terms ranging from one month to five years, while Business contracts are often between one year and five years in length. Throughout all Customer Operations activities, the customer experience is kept at the forefront to inform decision-making and optimize retention, while creating supporters and advocates for NRG’s brands in the market. Customer Operations comprises three end-use customer facing teams: NRG Home, which serves residential customers, NRG Business, which serves business customers, and NRG Services, which primarily includes the Services businesses.

Product Offerings

NRG sells a variety of products to residential and small commercial customers, including retail electricity and energy management, natural gas, line and surge protection products, HVAC installation, repair and maintenance, home protection products, carbon offsets, back-up power stations, portable power, portable solar and portable lighting. Home and Services customers make purchase decisions based on a variety of factors, including price, incentive, customer service, brand, innovative offers/features and referrals from friends and family. Through its broad range of service offerings and value propositions, NRG seeks to attract, retain, and increase the value of its customer relationships. NRG's brands are recognized for exemplary customer service, innovative smart energy and technology product offerings, and environmentally-friendly solutions.

The Company provides power and natural gas to the business-to-business markets in North America, as well as retail services, including demand response, commodity sales, energy efficiency and energy management solutions to Business customers. The Company is an integrated provider of supply and distributed energy resources and focuses on distributed products and services as businesses seek greater reliability, cleaner power and other benefits that they cannot obtain from the grid. These solutions include system power, distributed generation, renewable and low-carbon products, carbon management

8

and specialty services, backup generation, storage and distributed solar, demand response, and energy efficiency and advisory services.

Market Operations

Market Operations has two primary objectives: to supply energy to customers in the most cost-efficient manner and to maximize the value of the Company's assets in satisfying its customer load requirements. These objectives are intended to reduce supply costs and maximize earnings with predictable cash flows.

Power and natural gas are the two main commercial groups within Market Operations.

Power

The power commercial group is responsible for end-use electricity supply including power plant optimization and certain fuel supply. To meet the market operations objectives, NRG enters into supply, power and gas hedging agreements via a wide range of products and contracts, including (i) physical and financial commodity instruments, (ii) fuel supply and transportation contracts, (iii) PPAs and Renewable PPAs and (iv) capacity and other contracted revenue or supply sources, as further discussed below.

In addition, because changes in power prices in the markets where NRG operates are generally correlated to changes in natural gas prices, NRG uses hedging strategies that may include power and natural gas forward purchases and sales contracts to manage commodity price risk.

Physical and Financial Commodity Instruments

NRG trades power, natural gas, environmental, weather and other physical and financial commodity related products, including forwards, futures, options and swaps. NRG enters into these instruments primarily to manage price and delivery risk, optimize physical and contractual assets in the portfolio, manage working capital requirements, reduce the carbon exposure in its business and to comply with laws and regulations.

Fuel Supply and Transportation Contracts

NRG's fuel requirements consist of various forms of fossil fuel. The prices of fossil fuels can be volatile. The Company obtains its fossil fuels from multiple suppliers and through multiple transporters. Although availability is generally not an issue, localized shortages, transportation availability, delays arising from extreme weather conditions and supplier financial stability issues can and do occur. The preceding factors related to the sources and availability of raw materials are fairly uniform across the Company's business and fuel products used. NRG's primary fuel requirements consist of the following:

Natural Gas — NRG operates a fleet of mid-merit and peaking natural gas plants. Fuel needs are managed by the natural gas commercial group, generally on a spot basis, as the Company does not believe it is prudent to forward purchase natural gas for these types of units as the dispatch is highly unpredictable. Natural gas storage and transportation contracts are utilized to reduce daily volatility.

Coal —NRG actively manages its coal requirements based on forecasted generation, market volatility and its inventory on site. The Company believes it is adequately hedged, using forward coal supply agreements, for its domestic coal consumption for 2024. As of December 31, 2023, NRG had purchased forward contracts to provide fuel for the Company's expected requirements for 2024. For the domestic fleet, NRG purchased approximately 13 million tons of coal in 2023, almost all of which was Powder River Basin coal. For fuel transport, NRG has entered into various rail transportation and rail car lease agreements with varying tenures, which will provide for the Company's transportation requirements of Powder River Basin coal for the next two years.

Renewable PPAs

The Company's strategy is to procure mid to long-term renewable generation through power purchase agreements. As of December 31, 2023, NRG has entered into Renewable PPAs totaling approximately 1.9 GW with third-party project developers and other counterparties, of which approximately 1.1 GW are operational. The average tenure of these agreements is eleven years. The Company expects to continue evaluating and executing similar agreements that support the needs of the business. The total GW entered into through Renewable PPAs may be impacted by contract terminations when they occur.

Capacity and Other Contracted Revenue or Supply Sources

NRG's revenues and/or cash flows, primarily in the East and West, benefit from capacity/demand payments and other contracted revenue sources, originating from market clearing capacity prices, tolling arrangements and other long-term contractual arrangements.

9

Natural Gas

The natural gas commercial group is responsible for costing, logistics and supply for all of NRG's residential, commercial and industrial, and wholesale customers. NRG has contractual rights to natural gas transportation and storage assets across its footprint that allow for optimal supply economics in support of its various businesses. NRG's diversified load coupled with this asset portfolio enables the Company to deliver supply economically while providing incremental optimization activities when market conditions allow. The scale of the natural gas operation extends from the wellhead (through its producer services business) to end use customers (through NRG's various sales channels). This scale, coupled with the Company's associated assets, gas system platform and people, create significant value across North America.

Plant Operations

The Company owns and leases a diversified wholesale generation portfolio with approximately 13 GW of fossil fuel, and renewable generation capacity at 19 plants as of December 31, 2023. The Company's wholesale generation assets are diversified by fuel-type and dispatch level, which helps mitigate the risks associated with fuel price volatility and market demand cycles. NRG continually evaluates its generation portfolio to focus on asset optimization opportunities and the locational value of its generation assets in each of the markets where the Company participates, as well as opportunities for the development of new generation.

The following table summarizes NRG's generation portfolio as of December 31, 2023:

(In MW)(a) | ||||||||||||||||||||||||||

| Type | Texas | East | West/Services/Other(b) | Total | ||||||||||||||||||||||

| Natural gas | 4,353 | 80 | 1,279 | 5,712 | ||||||||||||||||||||||

| Coal | 4,174 | 1,948 | 605 | 6,727 | ||||||||||||||||||||||

| Oil | — | 455 | — | 455 | ||||||||||||||||||||||

| Utility Scale Solar | — | — | 216 | 216 | ||||||||||||||||||||||

| Battery Storage | 2 | — | — | 2 | ||||||||||||||||||||||

| Total generation capacity | 8,529 | 2,483 | 2,100 | 13,112 | ||||||||||||||||||||||

(a)Utility Scale Solar is described in MW on an alternating current basis. MW figures provided represent nominal summer net MW capacity of power generated as adjusted for the Company's owned interest

(b)Includes proportionate share of equity owned investments

Plant Operations is responsible for operating the Company's generation facilities at the highest standards of safety and regulatory compliance, and includes (i) operations and maintenance, (ii) asset management, and (iii) development, engineering and construction.

Operations & Maintenance

NRG operates and maintains its generation portfolio, as well as approximately 6,500 MW of additional coal, natural gas and wind generation capacity at 15 plants operated on behalf of third parties, as of December 31, 2023, using prudent industry practices for the safe, reliable and economic generation of electricity in compliance with all local, state and federal requirements. The Company follows a consistent set of operating requirements, including a solid base of training, required adherence to specific safety and environmental limits, procedure and checklist usage, and the implementation of continuous process improvement through incident investigations.

NRG uses best-in-class maintenance practices for preventive, predictive, and corrective maintenance planning. The Company’s strategic planning process evaluates equipment condition, performance, and obsolescence to support the development of a comprehensive work scope and schedule for long-term performance.

Asset Management

NRG manages all aspects of its generation portfolio to optimize the lifecycle value of the assets, consistent with the Company’s goals. The Company evaluates capital projects required for continued operation and strategic enhancement of the assets, provides quality assurance on capital outlays, and assesses the impact of rules, regulations, and laws on business profitability. In addition, the Company manages its long-term contracts, PPAs, and real estate holdings and provides third-party asset management services.

Development, Engineering & Construction

NRG develops, engineers and executes major plant modifications, “new build” generation and energy storage projects that enhance the value of its generation portfolio and provide options to meet generation growth needs in the retail markets it serves, in accordance with the Company’s strategic goals. These projects have included gas-fired generation development and

10

construction, coal to gas conversions, grid scale energy storage development, grid scale renewable construction, and asset demolition, remediation and reclamation work.

Vivint Smart Home

In March 2023, NRG completed the acquisition of Vivint Smart Home, which is a leading smart home platform that provides subscribers with technology, products and services to create a smarter, greener, safer home. A smart home has multiple devices integrated into a single expandable platform that incorporates artificial intelligence and machine-learning in its operating system allowing customers to interact with and manage their home from anywhere via the Vivint app on their smart device. Vivint Smart Home enables a customized solution for the home using integrated smart cameras (indoor, outdoor and doorbell), locks, lights, thermostats, garage door control and a host of other safety and security sensors.

Vivint Smart Home provides a fully integrated solution for consumers, including hardware, software, sales, installation by trained and experienced in-home service professionals, customer service, technical support and professional monitoring. This seamless integration of high-quality products and services resulted in an average subscriber lifetime of approximately nine years as of December 31, 2023. The Company believes its ability to offer related or adjacent products and services that leverage the existing smart home platform, as well as energy services, can extend the average subscriber lifetime and increase the lifetime value of subscribers. Vivint Smart Home's cloud-based home platform currently manages more than 30 million in-home devices as of December 31, 2023. The average subscriber on Vivint Smart Home's cloud-based home platform engages with the smart home app approximately 16 times per day and has approximately 15 devices in its home.

Through the addition of Vivint Smart Home, NRG identified opportunities to improve gross margin, customer retention and customer lifetime value.

Operational Statistics

The following statistics represent the Company's retail load and customer count:

| Year ended December 31, | |||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||

Sales volumes - Electricity (in GWh) | |||||||||||||||||

| Home - Texas | 40,032 | 43,155 | 42,397 | ||||||||||||||

| Home - East | 12,838 | 13,269 | 14,108 | ||||||||||||||

| Home - West/Services/Other | 2,243 | 2,250 | 2,252 | ||||||||||||||

| Business - Texas | 40,250 | 38,447 | 34,367 | ||||||||||||||

| Business - East | 46,438 | 47,724 | 53,204 | ||||||||||||||

| Business - West/Services/Other | 10,393 | 10,231 | 10,625 | ||||||||||||||

| Total Load | 152,194 | 155,076 | 156,953 | ||||||||||||||

Sales volumes - Natural gas (in MDth) | |||||||||||||||||

| Home - East | 49,990 | 53,051 | 50,417 | ||||||||||||||

| Home - West/Services/Other | 75,150 | 92,035 | 97,272 | ||||||||||||||

| Business - East | 1,587,052 | 1,618,946 | 1,620,036 | ||||||||||||||

| Business - West/Services/Other | 179,888 | 154,074 | 109,021 | ||||||||||||||

| Total Load | 1,892,080 | 1,918,106 | 1,876,746 | ||||||||||||||

11

| Year ended December 31, | |||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||

Customer count - Electricity customers(a)(b) (in thousands) | |||||||||||||||||

| Home - Texas | |||||||||||||||||

| Average retail | 2,878 | 2,961 | 3,040 | ||||||||||||||

| Ending retail | 2,928 | 2,859 | 3,010 | ||||||||||||||

Home - East | |||||||||||||||||

| Average retail | 1,466 | 1,408 | 1,484 | ||||||||||||||

| Ending retail | 1,752 | 1,381 | 1,402 | ||||||||||||||

| Home - West/Services/Other | |||||||||||||||||

Average retail(c) | 393 | 383 | 525 | ||||||||||||||

Ending retail(c) | 404 | 390 | 512 | ||||||||||||||

Customer count - Natural gas customers(b) (in thousands) | |||||||||||||||||

Home - East | |||||||||||||||||

| Average retail | 390 | 375 | 360 | ||||||||||||||

| Ending retail | 385 | 380 | 364 | ||||||||||||||

| Home - West/Services/Other | |||||||||||||||||

| Average retail | 381 | 416 | 452 | ||||||||||||||

| Ending retail | 358 | 396 | 434 | ||||||||||||||

Total Customer count (in thousands) | |||||||||||||||||

| Average retail - Home - Electricity and Natural gas | 5,508 | 5,543 | 5,861 | ||||||||||||||

Average - Vivint Smart Home(d) | 2,008 | — | — | ||||||||||||||

| Ending retail - Home - Electricity and Natural gas | 5,827 | 5,406 | 5,722 | ||||||||||||||

Ending - Vivint Smart Home(d) | 2,043 | — | — | ||||||||||||||

| Total Ending retail and Vivint Smart Home | 7,870 | 5,406 | 5,722 | ||||||||||||||

(a) Includes Services customers | |||||||||||||||||

| (b) Dual fuel customers are included within electricity customer counts only | |||||||||||||||||

| (c) Includes 135 thousand whole home warranty customers as of December 31, 2021. The whole home warranty business was sold in January 2022 | |||||||||||||||||

| (d) Vivint Smart Home subscribers includes customers that also purchase other NRG products | |||||||||||||||||

The following are industry statistics for the Company's fossil and nuclear plants, as defined by the NERC:

Annual Equivalent Availability Factor, or EAF — Measures the percentage of maximum generation available over time as the fraction of net maximum generation that could be provided over a defined period of time after all types of outages and deratings, including seasonal deratings, are taken into account.

Net Heat Rate — The net heat rate represents the total amount of fuel in BTU required to generate one net kWh provided.

Net Capacity Factor — The net amount of electricity that a generating unit produces over a period of time divided by the net amount of electricity it could have produced if it had run at full power over that time period. The net amount of electricity produced is the total amount of electricity generated minus the amount of electricity used during generation by the station.

12

The tables below present these performance metrics for the Company's generation portfolio, including leased facilities, for the years ended December 31, 2023 and 2022:

| Year Ended December 31, 2023 | |||||||||||||||||||||||||||||

Fossil and Nuclear Plants (a) | |||||||||||||||||||||||||||||

| Net Owned Capacity (MW) | Net Generation (In thousands of MWh) (a) | Annual Equivalent Availability Factor | Average Net Heat Rate BTU/kWh | Net Capacity Factor | |||||||||||||||||||||||||

| Texas | 8,529 | 30,776 | 74.2 | % | 11,175 | 35.4 | % | ||||||||||||||||||||||

| East | 2,483 | 2,016 | 85.5 | % | 13,007 | 6.6 | % | ||||||||||||||||||||||

| West/Services/Other | 1,169 | 5,903 | 73.5 | % | 7,449 | 56.8 | % | ||||||||||||||||||||||

(a)Excludes equity method investments

| Year Ended December 31, 2022 | |||||||||||||||||||||||||||||

Fossil and Nuclear Plants (a) | |||||||||||||||||||||||||||||

| Net Owned Capacity (MW) | Net Generation (In thousands of MWh) (a) | Annual Equivalent Availability Factor | Average Net Heat Rate BTU/kWh | Net Capacity Factor | |||||||||||||||||||||||||

| Texas | 10,027 | 37,275 | 69.5 | % | 10,733 | 41.8 | % | ||||||||||||||||||||||

| East | 4,285 | 7,282 | 78.1 | % | 11,959 | 17.3 | % | ||||||||||||||||||||||

| West/Services/Other | 1,172 | 6,676 | 84.5 | % | 7,442 | 64.9 | % | ||||||||||||||||||||||

(a)Excludes equity method investments

The generation performance by region for the three years ended December 31, 2023, 2022 and 2021 is shown below:

| Net Generation | |||||||||||||||||

| (In thousands of MWh) | 2023 | 2022 | 2021 | ||||||||||||||

| Texas | |||||||||||||||||

| Coal | 15,576 | 18,860 | 18,876 | ||||||||||||||

| Gas | 7,333 | 8,763 | 8,846 | ||||||||||||||

Nuclear (a) | 7,867 | 9,652 | 9,198 | ||||||||||||||

| Total Texas | 30,776 | 37,275 | 36,920 | ||||||||||||||

| East | |||||||||||||||||

| Coal | 1,328 | 6,738 | 5,774 | ||||||||||||||

| Oil | 3 | 7 | 201 | ||||||||||||||

| Gas | 685 | 537 | 1,519 | ||||||||||||||

Total East (b) | 2,016 | 7,282 | 7,494 | ||||||||||||||

| West/Services/Other | |||||||||||||||||

| Gas | 5,899 | 6,669 | 7,941 | ||||||||||||||

| Renewables | 4 | 7 | 8 | ||||||||||||||

Total West/Services/Other (c) | 5,903 | 6,676 | 7,949 | ||||||||||||||

| Total generation performance | 38,695 | 51,233 | 52,363 | ||||||||||||||

(a)Reflects the Company's undivided interest in total MWh generated by STP. The Company sold its interest in STP on November 1, 2023

(b)Includes gas generation of 855 thousand MWh and oil generation of 199 thousand MWh for the year ended December 31, 2021, that was sold to Generation Bridge on December 1, 2021

(c)Includes gas generation of 2,445 thousand MWh for the year ended December 31, 2021, that was sold to Generation Bridge on December 1, 2021

13

Competition

While there has been consolidation in the competitive retail energy space over the past few years, there is still considerable competition for customers. In Texas, there is healthy competition in deregulated areas and customers can choose providers based on the most appealing offers. Outside of Texas, electricity retailers compete with the incumbent utilities, in addition to other retail electric providers, which can inhibit competition depending on the market rules of the state. There is a high degree of fragmentation, with both large and small competitors offering a range of value propositions, including value, rewards, and sustainability-based offerings.

Wholesale generation is highly fragmented and diverse in terms of industry structure by region. As such, there is wide variation in terms of the capabilities, resources, nature and identities of the Company’s competitors depending on the market. Competitors include regulated utilities, municipalities, cooperatives, other independent power producers, and power marketers or trading companies, including those owned by financial institutions.

The smart home market is an expanding global opportunity and is in the early stages of broad consumer adoption. It is highly competitive and fragmented. Major competitors range from large-cap technology companies seeking to expand their core market opportunity who predominantly offer do-it-yourself ("DIY") devices that put a large burden on homeowners to self-install and support many devices, to security-based providers, as well as industrial and telecommunications companies that offer connected home experiences. Vivint Smart Home provides the full smart home experience, with an end-to-end solution that includes a wide range of unique capabilities and use cases. Currently, the vast majority of competitors do not offer comprehensive smart home solutions and accompanying services.

Seasonality and Price Volatility

The sale of power and natural gas to retail customers are seasonal businesses with the demand for power generally peaking during the summer, and the demand for natural gas generally peaking during the winter. As a result, net working capital requirements for the Company's retail operations generally increase during summer and winter months along with the higher revenues, and then decline during off-peak months. Weather may impact operating results and extreme weather conditions could have a material impact. The rates charged to retail customers may be impacted by fluctuations in total power prices and market dynamics, such as the price of natural gas, transmission constraints, competitor actions, and changes in market heat rates.

Annual and quarterly operating results of the Company's generation portfolio can be significantly affected by weather and energy commodity price volatility. Significant other events, such as the demand for natural gas, interruptions in fuel supply infrastructure and relative levels of hydroelectric capacity can increase seasonal fuel and power price volatility. The preceding factors related to seasonality and price volatility are fairly uniform across the regions in which the Company operates.

Market Framework

NRG sells electricity, natural gas and related products and services, and smart home products and services to customers throughout the U.S. and Canada. In most of the states and regions that have introduced retail consumer choice, NRG competitively offers electricity, natural gas, portable power and other value-enhancing services to customers. Each retail consumer choice state or province establishes its own retail competition laws and regulations, and the specific operational, licensing, and compliance requirements vary by state or province. Regulated terms and conditions of default service, as well as any movement to replace default service with competitive services, as is done in ERCOT, can affect customer participation in retail competition. In Canada, NRG sells energy and related services to residential and commercial customers in the province of Alberta pursuant both to a regulated rate service governed by provincial regulations as well as a competitive service with rates set by market forces. Sales of energy to commercial customers take place in other provinces as well. The attractiveness of NRG's retail offerings may be impacted by the rules, regulations, market structure and communication requirements from public utility commissions in each state and province.

NRG's fleet of power plants which it owns, operates or manages are located in organized energy markets, known as RTOs or ISOs. Each organized market administers day-ahead and real-time centralized bid-based energy and ancillary services markets pursuant to tariffs approved by FERC, or in the case of ERCOT, market rules approved by the PUCT. These tariffs and rules dictate how the energy markets operate, how market participants make bilateral sales with one another and how entities with market-based rates are compensated. Established prices reflect the value of energy at the specific location and time it is delivered, which is known as the Locational Marginal Price. Each market is subject to market mitigation measures designed to limit the exercise of locational market power. These market structures facilitate NRG's sale of power and capacity products at market-based rates.

Other than ERCOT and AESO, each of the ISO regions also operates a capacity or resource adequacy market that provides an opportunity for generating and demand response resources to earn revenues to offset their fixed costs that are not recovered in the energy and ancillary services markets. The ISOs are also responsible for transmission planning and operations.

14

Texas

NRG's business in Texas is subject to standards and regulations adopted by the PUCT and ERCOT1, including the requirement for retailers to be certified by the PUCT in order to contract with end-users to sell electricity. The ERCOT market is one of the nation's largest and, historically, fastest growing power markets. ERCOT is an energy-only market. The majority of the retail load in the ERCOT market region is served by competitive retail suppliers, except certain areas that have not opted into competitive consumer choice and are served by municipal utilities and electric cooperatives.

East

While most of the states in the East region of the U.S. have introduced some level of retail consumer choice for electricity and/or natural gas, the incumbent utilities currently provide default service in most of the states and as a result typically serve the majority of residential customers. NRG’s retail activities in the East are subject to standards and regulations adopted by the ISOs, state public utility commissions and legislators, including the requirement for retailers to be certified in each state in order to contract with end-users to sell electricity.

Power plants owned, operated or managed by NRG and NRG's demand response assets located in the East region of the U.S. are within the control areas of PJM, NYISO and MISO. Each of the market regions in the East region provides for robust competition in the day-ahead and real-time energy and ancillary services markets. Additionally, the assets in the East region receive a significant portion of their revenues from capacity markets. PJM uses a forward capacity auction, while NYISO uses a month-ahead capacity auction. MISO has an annual auction. Capacity market prices are sensitive to design parameters, as well as additions of new capacity. PJM operates a pay-for-performance model where capacity payments are modified based on real-time generator performance. In such markets, NRG’s actual capacity revenues will be the combination of cleared auction prices times the quantity of MW cleared, plus the net of any over-performance "bonus payments" and any under-performance charges. Additionally, bidding rules allow for the incorporation of a risk premium into generator bids.

West

In the West region of the U.S., NRG owns equity interests, operates or manages power plants located entirely within the CAISO footprint. The CAISO operates day-ahead and real-time locational markets for energy and ancillary services, while managing congestion primarily through nodal prices. The CAISO system facilitates NRG's sale of power, ancillary services and capacity products at market-based rates, either within the CAISO's centralized energy and ancillary service markets or bilaterally. The CPUC also determines capacity requirements for LSEs and for specified local areas utilizing inputs from the CAISO. Both the CAISO and CPUC rules require LSEs to contract with sufficient generation resources in order to maintain minimum levels of generation within defined local areas. Additionally, the CAISO has independent authority to contract with needed resources under certain circumstances, typically either when LSEs have failed to procure sufficient resources, or system conditions change unexpectedly.

Canada

In Canada, NRG sells to residential and commercial retail customers in Alberta, within the AESO footprint, under both regulated rates approved by the AUC as well as through competitive service. The Company's regulated rates are approved through periodic rate applications that establish rates for power and gas sales as well as for recovery of other costs associated with operating the regulated business. In addition, the Company sells energy to commercial customers in other provinces. All sales and operations are subject to applicable federal and provincial laws and regulations.

Vivint Smart Home

Vivint Smart Home operates in states that regulate in some manner the sale, installation, servicing, monitoring or maintenance of smart home and electronic security systems. Vivint Smart Home and Vivint Smart Home sales representatives are typically required to obtain and maintain licenses, certifications or similar permits from governmental entities as a condition to engaging in the smart home and security service business. Vivint Smart Home is subject to federal and state laws related to consumer financing which may include rules related to fees and charges, disclosures and regulation of the party extending consumer credit.

1 The Cottonwood facility is located in Deweyville, Texas, but operates in the MISO market

15

Energy Regulatory Matters

As participants in wholesale and retail energy markets and owners and operators of power plants, certain NRG entities are subject to regulation by various federal, state and provincial agencies. These include the CFTC, FERC, and the PUCT, as well as other public utility commissions in certain states where NRG's generation or distributed generation assets are located. In addition, NRG is subject to the market rules, procedures and protocols of the various ISO and RTO markets in which it participates. These power markets are subject to ongoing legislative and regulatory changes that may impact NRG's wholesale and retail operations. NRG must also comply with the mandatory reliability requirements imposed by NERC and the regional reliability entities in the regions where NRG operates.

NRG's operations within the ERCOT footprint are not subject to rate regulation by FERC, as they are deemed to operate solely within the ERCOT market and not in interstate commerce. These operations are subject to regulation by the PUCT.

Regional Regulatory Developments

NRG is affected by rule/tariff changes that occur in the ISO regions. For further discussion on regulatory developments see Item 15 — Note 24, Regulatory Matters, to the Consolidated Financial Statements.

Texas

Public Utility Commission of Texas’s Actions with Respect to Wholesale Pricing and Market Design — The PUCT continues to analyze and implement multiple options for promoting increased reliability in the wholesale electric market, including the adoption of a reliability standard for resource adequacy and market-based mechanisms to achieve this standard. During the 88th Regular Session, the Texas Legislature authorized deployment of the Performance Credit Mechanism ("PCM"), which will measure real-time contribution to system reliability and provide compensation for resources to be available, subject to certain "guardrails" such as an annual net cost cap, as part of its adoption of the PUCT Sunset Bill (House Bill 1500). The Texas Legislature also directed the PUCT to implement additional market design changes such as the creation of a new ancillary service called Dispatchable Reliability Reserve Service ("DRRS") to further increase ERCOT's capability to manage net load variability and firming requirements for new generation resources which penalize poor performance during periods of low grid reserves. The PUCT directed ERCOT to implement DRRS as a standalone product which will delay implementation until late 2025 or 2026. Additionally, through Senate Bill 2627, the Texas Legislature created the Texas Energy Fund, which received voter approval in November 2023, and will provide grants and low-interest loans to incentivize the development of more dispatchable generation and smaller backup generation in ERCOT. The PUCT has initiated a rulemaking proceeding to establish the process by which the Texas Energy fund loan proceeds will be distributed. A final rule creating the general structure of the loan program is expected to be adopted in March 2024.

Operating Reserve Demand Curve ("ORDC") — On August 3, 2023, the PUCT approved implementation of an enhancement to the ORDC as a bridge solution that was recommended by the ERCOT Technical Advisory Committee and the ERCOT board of directors. The ORDC enhancement will install price floors of $10 and $20 at reserve levels of 7,000 MW and 6,500 MW or below, respectively. ERCOT completed implementation on November 1, 2023.

Ruling on Pricing during Winter Storm Uri — On March 17, 2023, the Third Court of Appeals issued a ruling in Luminant Energy Co. v. PUCT, which is an appeal relating to the validity of two orders issued by the PUCT on February 15 and 16, 2021, respectively, governing scarcity pricing in the ERCOT wholesale electricity market during Winter Storm Uri. The Third Court found that the PUCT exceeded its statutory authority by ordering the market price of energy to be set at the high system wide offer cap due to scarcity conditions as a result of firm load shed occurring in ERCOT. The Third Court reversed the PUCT's orders and remanded the case. On March 23, 2023, the PUCT filed a petition for review to the Supreme Court of Texas seeking reversal of the Third Court's decision, which was granted on September 29, 2023. The Court received briefing on the merits and oral arguments occurred on January 30, 2024. The outcome of this appeal could potentially require a retroactive repricing of the ERCOT market prices during the subject time period.

Voluntary Mitigation Plan ("VMP") Changes — On March 13, 2023, the PUCT Staff determined that a portion of NRG's VMP should be terminated due to the increase in procurement of ancillary services by ERCOT, specifically non-spin reserve services, following Winter Storm Uri. As such, PUCT Staff terminated part of the VMP for NRG which provides protection from wholesale market power abuse accusations related to offers for ancillary services. NRG agreed with these changes to the VMP. At the March 23, 2023 open meeting, the PUCT approved the amended VMP. On February 23, 2024, NRG filed a notice of intent with the PUCT to terminate its existing VMP as of March 1, 2024.

ERCOT Request for Proposals for Winter Capacity — On October 2, 2023, ERCOT issued a Request for Proposals for Capacity ("RFP") for Winter 2023-2024. Proposals were due in early November to provide capacity for the December 1, 2023 to February 29, 2024 period. The RFP requirements were limited to demand response resources that have not participated in ERCOT or price responsive products. Ultimately, ERCOT cancelled the procurement due to lack of participation by qualified participants.

16

Lubbock, Texas Transition to Competition — The customers of Lubbock Power and Light ("LP&L"), a municipally owned utility, will enter the Texas retail competitive market in March 2024. Starting in January 2024, LP&L customers can shop for a REP. Customers who do not select a REP by February 15, 2024 will be assigned to one of three default REPs, one of which is Reliant. LP&L customers will start transitioning to their chosen REP or a default REP on March 4, 2024.

PJM

Revisions to PJM Local Deliverability Area Reliability Requirement — The Base Residual Auction for the 2024/2025 delivery year commenced on December 7, 2022 and closed on December 13, 2022. On December 19, 2022, PJM announced that it would delay the publication of the auction results. On December 23, 2022, PJM made a filing at FERC to revise the definition of Locational Deliverability Area Reliability Requirement in the Tariff. This would allow PJM to exclude certain resources from the calculation of the Local Deliverability Area Reliability Requirement. On February 21, 2023, FERC accepted PJM's filing. Multiple parties, including NRG, filed for rehearing. Rehearing was denied by operation of law, and multiple parties, including the Company, filed appeals to the Third Circuit Court of Appeals. The price of the auction cleared significantly lower as a result of the PJM Tariff change.

Capacity Performance Penalties and Bonuses from Winter Storm Elliott — PJM experienced approximately 23 hours of Capacity Performance events from December 23-24, 2022 across PJM's entire footprint. The Company is subject to penalty and bonus payments related to the events. On April 3, 2023, FERC approved PJM's request to allow Winter Storm Elliott penalty payments to be spread over 9 months (with interest) and allow future penalties to have a 9 month window to be satisfied without interest. Multiple generators filed various complaints against PJM at FERC alleging that PJM violated its Tariff in, among other things, the manner in which it operated the system during Winter Storm Elliott and the resulting assessment of capacity performance penalties. On June 5, 2023, FERC issued an order setting the various complaints for settlement. A settlement in principle was filed with FERC on September 29, 2023 and was approved on December 19, 2023.

PJM Base Residual Auction Revisions and Delay — On April 11, 2023, PJM filed, and FERC subsequently approved, to delay the Base Residual Auctions for the 2025/2026 to 2028/2029 delivery years. On October 13, 2023, PJM made two filings proposing to develop market reforms to improve the operation of the capacity market through changes to the Market Seller Offer Cap rules, changes to PJM's resource adequacy risk modeling and capacity accreditation processes, and changes to capacity performance enhancements. On January 30, 2024, FERC accepted certain reforms to PJM's resource adequacy risk modeling and accreditation processes; on February 6, 2024, FERC rejected PJM's proposed changes to certain Market Seller Offer Cap rules and capacity performance enhancements. The approved changes will be in effect for the 2025/2026 Base Residual Auction scheduled to occur in July 2024, and will impact both demand and supply characteristics.

PJM Files to Make Changes to the Performance Assessment Interval Trigger — On May 30, 2023, PJM filed proposed tariff revisions at FERC that narrow the definition of Emergency Actions used to determine Performance Assessment Intervals ("PAIs"). On July 28, 2023, FERC accepted the tariff revisions, and PJM made its compliance filing on August 28, 2023. The new definition narrows the instances of when PAIs can occur and therefore decrease the instances of when capacity performance penalties are assessed.

Independent Market Monitor Market Seller Offer Cap Complaint — On March 18, 2021, finding that the calculation of the default Market Seller Offer Cap was unjust and unreasonable, FERC issued an Order, which permitted the PJM May 2021 capacity auction for the 2022/2023 delivery rule to continue under the existing rules and set a procedural schedule for parties to file briefs with possible solutions. On September 2, 2021, FERC issued an order in response to a complaint filed by the PJM Independent Market Monitor's proposal, which eliminated the Cost of New Entry-based Market Seller Offer Cap, implemented a limited default cap for certain asset classes based on going-forward costs and provided for unit specific cost review by the Independent Market Monitor for all other non-zero offers into the auctions. On October 4, 2021, as required by the Order, PJM submitted its compliance tariff and certain parties filed a motion for rehearing, which was denied by operation of law. On February 18, 2022, FERC addressed the arguments raised on rehearing and rejected the rehearing requests. Multiple parties filed appeals at the Court of Appeals for the D.C. Circuit, and on August 15, 2023, the Court denied the petitions for review. On January 12, 2024, the generator trade association filed a petition for review with the U.S. Supreme Court to overturn the August 15, 2023 judgment.

California

California Resource Planning Proceedings — As part of the Integrated Resource Procurement docket, the CPUC is requiring that all LSEs procure a pro rata share of 15.5 GW of new non-fossil resource adequacy ("RA") from 2023 to 2026. The new RA program rules adopted in 2023 are now in an implementation phase with a compliance process likely to be continually recalibrated through the first quarter of 2024. CPUC jurisdictional retail providers will be required to procure RA that meets their hourly load shape beginning in 2025. The result of these changes may create upward pressure on RA prices through 2024, and if LSEs cannot meet their RA obligations, penalties and restrictions on serving new customers may be issued. As relief to the tightness of the RA market, the CPUC adopted a final decision in December 2023 to extend PG&E's

17

Diablo Canyon nuclear facility. The decision would allow the RA and GHG-free attributes of this 2-GW facility to be allocated to all LSEs to provide some relief to all LSEs' RA positions.

Other Regulatory Matters

From time to time, NRG entities may be subject to examinations, investigations and/or enforcement actions by federal, state and provincial licensing agencies and may face the risk of penalties for violation of financial services, consumer protections and other applicable laws and regulations.

Environmental Regulatory Matters

NRG is subject to numerous environmental laws in the development, construction, ownership and operation of power plants. These laws generally require that governmental permits and approvals be obtained before construction and maintained during operation of power plants. Federal and state environmental laws have become more stringent over time. Future laws may require the addition of emissions controls or other environmental controls or impose restrictions on the Company's operations including unit retirements. Complying with environmental laws often involves specialized human resources and significant capital and operating expenses, as well as occasionally curtailing operations. NRG decides to invest capital for environmental controls based on the relative certainty of the requirements, an evaluation of compliance options and the expected economic returns on capital.

A number of regulations that affect the Company have been and continue to be revised by the EPA, including requirements regarding coal ash, NAAQS revisions and implementation, and effluent limitation guidelines. NRG will evaluate the impact of these regulations as they are revised but cannot fully predict the impact of each until anticipated revisions and legal challenges are finally resolved.

Air

The CAA and related regulations (as well as similar state and local requirements) have the potential to affect air emissions, operating practices and pollution control equipment required at power plants. Under the CAA, the EPA sets NAAQS for certain pollutants including SO2, ozone, and PM2.5. Many of the Company's facilities are located in or near areas that are classified by the EPA as not achieving certain NAAQS (non-attainment areas). The relevant NAAQS may become more stringent. On February 7, 2024, the EPA released a prepublication version of a final rule that when published in the Federal Register will increase the stringency of the PM2.5 NAAQS. The Company maintains a comprehensive compliance strategy to address continuing and new requirements. Complying with increasingly stringent air regulations could require the installation of additional emissions control equipment at some NRG facilities or retiring of units if installing such controls is not economic. Significant changes to air regulatory programs affecting the Company are described below.

CPP/ACE Rules — The attention in recent years on GHG emissions has resulted in federal and state regulations. In 2019, the EPA promulgated the ACE rule, which rescinded the CPP, which had sought to broadly regulate CO2 emissions from the power sector. On January 19, 2021, the D.C. Circuit vacated the ACE rule (but on February 22, 2021, at the EPA's request, stayed the issuance of the portion of the mandate that would vacate the repeal of the CPP). On June 30, 2022, the U.S. Supreme Court held that the "generation shifting" approach in the CPP exceeded the powers granted to the EPA by Congress. The Court did not address the related issues of whether the EPA may adopt only measures applied at each source. On May 23, 2023, the EPA proposed significantly revising the manner in which new and existing EGU's GHG emissions should be regulated including using hydrogen as a fuel, capturing and storing/sequestering CO2 and requiring new units to be more efficient. The EPA has stated that it intends to finalize these revisions in 2024. The Company expects that the final rule will be challenged in the courts and accordingly uncertain over the next several years.

Cross-State Air Pollution Rule ("CSAPR") — On March 15, 2023, the EPA signed and released a prepublication of a final rule that sought to significantly revise the CSAPR to address the good-neighbor obligations of the 2015 ozone NAAQS for 23 states after earlier having disapproved numerous state plans to address the issue. Several states, including Texas, challenged the EPA's disapproval of their state plans. On May 1, 2023, the United States Court of Appeals for the Fifth Circuit stayed the EPA's disapproval of Texas' and Louisiana's state plans, which disapprovals are a condition precedent to the EPA imposing its plan on Texas and Louisiana. Several other states are also similarly situated because of similar stays. Nonetheless, on June 5, 2023, the EPA published this rule in the Federal Register. On July 31, 2023, the EPA promulgated an interim final rule that addresses the various judicial orders that have stayed several State-Implementation-Plan disapprovals by limiting the effectiveness of certain requirements of the final rule promulgated on June 5, 2023 in Texas and five other states. The final rule decreases, over time, the ozone-season NOx allowances allocated to generators in the states not affected by the judicial stays beginning in 2023 by assuming that participants in this cap-and-trade program had or would optimize existing NOx controls and later install additional NOx controls. The Company cannot predict the outcome of the legal challenges to the: (i) various state disapprovals; (ii) the final rule promulgated on June 5, 2023; and (iii) the interim final rule promulgated on July 31, 2023 that seeks to address the judicial orders.

18

Regional Haze Proposal — On May 2023, the EPA proposed to withdraw the existing Texas Sulfur Dioxide Trading Program and replace it with unit-specific SO2 limits for 12 units in Texas to address requirements to improve visibility at National Parks and Wilderness areas. If finalized as proposed, the rule would result in more stringent SO2 limits for two of the Company's coal-fired units in Texas. The Company cannot predict the outcome of this proposal.

Greenhouse Gas Emissions — NRG emits CO2 (and small quantities of other GHGs) when generating electricity at a majority of its facilities. Nearly all of NRG's domestic GHG emissions are subject to federal (U.S. EPA) GHG reporting requirements.

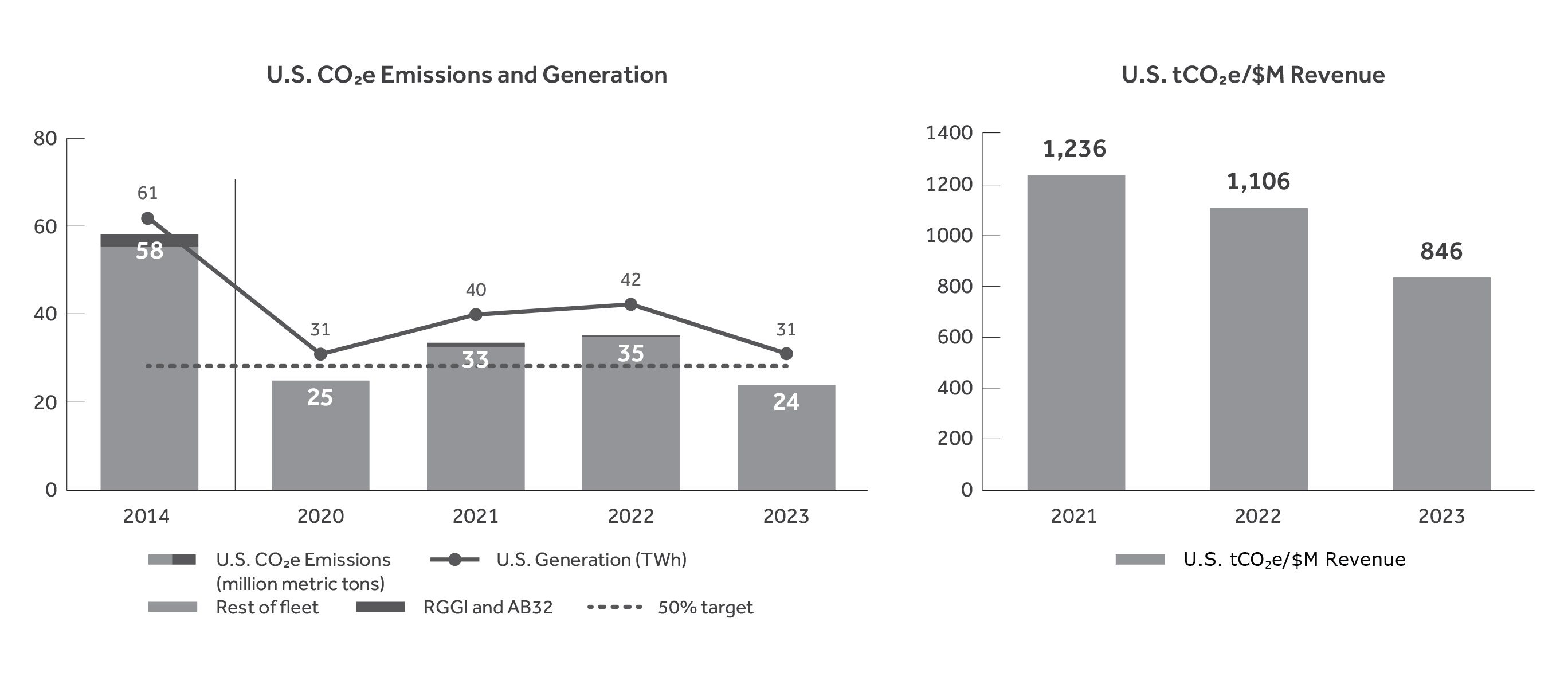

NRG's climate goals are to reduce greenhouse gas emissions by 50% by 2025, from its current 2014 base year, and to achieve net-zero emissions by 2050. Greenhouse gas emissions included in NRG's goals are directly controlled emissions, emissions from purchased electricity for NRG's consumption and emissions from employee business travel. In March 2021, the Science Based Targets initiative validated NRG's 2025 and 2050 goals as aligned with a 1.5 degree Celsius trajectory. This validation was based on NRG’s business in 2020, prior to its acquisition of Direct Energy and Vivint. Following the acquisitions, the magnitude of NRG’s indirect emissions changed, and the Company is currently in the process of analyzing these emissions.

From the current 2014 base year through 2023, the Company's directly controlled CO2e emissions decreased from 58 million metric tons to 24 million metric tons, representing a cumulative 58% reduction. The decrease is attributed to reductions in fleet-wide annual net generation and an overall market-driven shift away from coal as a primary fuel to natural gas. The achievement of NRG's 2025 emissions reduction targets could be impacted by volatility within the power markets, driven by market conditions and changes in regulatory policies.

As of December 31, 2023, less than 5% of the Company's consolidated revenues were derived from coal-fired operating assets.

The following charts reflect the Company’s domestic generation portfolio, including leased facilities and those accounted for through equity method investments, but excluding the battery storage and remaining renewables activity. Prior year information on U.S. CO2e emissions and U.S. generation was adjusted to remove divested assets.

Byproducts

In 2015, the EPA finalized a rule regulating byproducts of coal combustion (e.g., ash and gypsum) as solid wastes under the RCRA. On August 21, 2018, the D.C. Circuit found, among other things, that the EPA had not adequately regulated unlined ponds and legacy surface impoundments. On August 28, 2020, the EPA finalized "A Holistic Approach to Closure Part A: Deadline to Initiate Closure," which amended the April 2015 Rule to address the August 2018 D.C. Circuit decision and extend some of the deadlines. On November 12, 2020, the EPA finalized "A Holistic Approach to Closure Part B: Alternative Demonstration for Unlined Surface Impoundments," which further amended the April 2015 Rule to, among other things, provide procedures for requesting approval to operate existing ash impoundments with an alternate liner. On May 23, 2023, the EPA proposed establishing requirements for: (i) inactive (or legacy) surface impoundments at inactive facilities and (ii) all CCR management units (regardless of how or when the CCR was placed) at regulated facilities. NRG anticipates further rulemaking related to legacy surface impoundments and the Federal Permit Program.

19

Domestic Site Remediation Matters

Under certain federal, state and local environmental laws, a current or previous owner or operator of a facility, including an electric generating facility, may be required to investigate and remediate releases or threatened releases of hazardous or toxic substances or petroleum products. NRG may be responsible for property damage, personal injury and investigation and remediation costs incurred by a party in connection with hazardous material releases or threatened releases. These laws impose liability without regard to whether the owner knew of or caused the presence of the hazardous substances, and the courts have interpreted liability under such laws to be strict (without fault) and joint and several. Cleanup obligations can often be triggered during the closure or decommissioning of a facility, in addition to spills during its operations.

Jewett Mine Lignite Contract — The Company's Limestone facility historically burned lignite obtained from the Jewett mine. Active mining ceased as of December 31, 2016; however, the Company remains responsible for reclamation activities and is responsible for all reclamation costs. NRG has recorded an adequate ARO liability. The Railroad Commission of Texas has imposed a bond obligation of approximately $112 million for the reclamation of the Jewett mine, which NRG supports through surety bonds. The cost of the reclamation may exceed the value of the bonds. NRG may provide additional performance assurance if required by the Railroad Commission of Texas.

Water

The Company is required under the CWA to comply with intake and discharge requirements, requirements for technological controls and operating practices. As with air quality regulations, federal and state water regulations have become more stringent and imposed new requirements.

Effluent Limitations Guidelines — In 2015, the EPA revised the Effluent Limitations Guidelines ("ELG") for Steam Electric Generating Facilities, which imposed more stringent requirements (as individual permits were renewed) for wastewater streams from FGD, fly ash, bottom ash and flue gas mercury control. On September 18, 2017, the EPA promulgated a final rule that, among other things, postponed the compliance dates to preserve the status quo for FGD wastewater and bottom ash transport water by two years to November 2020 until the EPA amended the rule. On October 13, 2020, the EPA amended the 2015 ELG rule by: (i) altering the stringency of certain limits for FGD wastewater; (ii) relaxing the zero-discharge requirement for bottom ash transport water; and (iii) changing several deadlines. In October 2021, NRG informed its regulators that the Company intends to comply with the ELG by ceasing combustion of coal by the end of 2028 at its domestic coal units outside of Texas, and installing appropriate controls by the end of 2025 at its two plants that have coal-fired units in Texas. On March 29, 2023, the EPA proposed revisions to the ELG and sought comments, which the EPA is analyzing.

Regional Environmental Developments

Ash Regulation in Illinois — On July 30, 2019, Illinois enacted legislation that required the state to promulgate regulations regarding coal ash at surface impoundments. On April 15, 2021, the state promulgated the implementing regulation, which became effective on April 21, 2021. NRG has applied for initial operating permits and construction permits (for closure and retrofits) as required by the regulation and is waiting for permits to be issued by the Illinois EPA.

Houston Nonattainment for 2008 Ozone Standard — During the fourth quarter of 2022, the EPA changed the Houston area’s classification from Serious to Severe nonattainment for the 2008 Ozone Standard. Accordingly, Texas is required to develop a new control strategy and submit it to the EPA, which is expected by May 2024.

Customers