UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________________

FORM 10-Q

_____________________________________

| Quarterly Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | ||||||||

For the quarterly period ended September 30, 2020

OR

| Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | ||||||||

Commission File Number: 1-11859

____________________________

(Exact name of Registrant as specified in its charter)

____________________________

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | ||||||||||||||||||||||

(Address of principal executive offices, including zip code)

(617 ) 374-9600

(Registrant’s telephone number, including area code)

____________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

x | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

There were 80,697,696 shares of the Registrant’s common stock, $0.01 par value per share, outstanding on October 19, 2020.

PEGASYSTEMS INC.

QUARTERLY REPORT ON FORM 10-Q

TABLE OF CONTENTS

Page | |||||

| PART I - FINANCIAL INFORMATION | |||||

| Item 1. Financial Statements | |||||

Unaudited Condensed Consolidated Balance Sheets as of September 30, 2020 and December 31, 2019 | |||||

Unaudited Condensed Consolidated Statements of Operations for the three and nine months ended September 30, 2020 and 2019 | |||||

Unaudited Condensed Consolidated Statements of Comprehensive (Loss) for the three and nine months ended September 30, 2020 and 2019 | |||||

Unaudited Condensed Consolidated Statements of Stockholders’ Equity for the nine months ended September 30, 2020 and 2019 | |||||

Unaudited Condensed Consolidated Statements of Cash Flows for the nine months ended September 30, 2020 and 2019 | |||||

| Notes to Unaudited Condensed Consolidated Financial Statements | |||||

| Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations | |||||

| Item 3. Quantitative and Qualitative Disclosures About Market Risk | |||||

| Item 4. Controls and Procedures | |||||

| PART II - OTHER INFORMATION | |||||

| Item 1A. Risk Factors | |||||

| Item 2. Unregistered Sales of Equity Securities and Use of Proceeds | |||||

| Item 6. Exhibits | |||||

| Signature | |||||

2

PART I - FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

PEGASYSTEMS INC.

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands)

| September 30, 2020 | December 31, 2019 | ||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Marketable securities | |||||||||||

| Total cash, cash equivalents, and marketable securities | |||||||||||

| Accounts receivable | |||||||||||

| Unbilled receivables | |||||||||||

| Other current assets | |||||||||||

| Total current assets | |||||||||||

Unbilled receivables | |||||||||||

| Goodwill | |||||||||||

| Other long-term assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and stockholders’ equity | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Accrued compensation and related expenses | |||||||||||

| Deferred revenue | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Convertible senior notes, net | |||||||||||

| Operating lease liabilities | |||||||||||

| Other long-term liabilities | |||||||||||

| Total liabilities | |||||||||||

| Stockholders’ equity: | |||||||||||

Preferred stock, | |||||||||||

Common stock, September 30, 2020 and December 31, 2019, respectively | |||||||||||

| Additional paid-in capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive (loss) | ( | ( | |||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

See notes to unaudited condensed consolidated financial statements.

3

PEGASYSTEMS INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share amounts)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Revenue | |||||||||||||||||||||||

| Software license | $ | $ | $ | $ | |||||||||||||||||||

| Maintenance | |||||||||||||||||||||||

| Pega Cloud | |||||||||||||||||||||||

| Consulting | |||||||||||||||||||||||

| Total revenue | |||||||||||||||||||||||

| Cost of revenue | |||||||||||||||||||||||

| Software license | |||||||||||||||||||||||

| Maintenance | |||||||||||||||||||||||

| Pega Cloud | |||||||||||||||||||||||

| Consulting | |||||||||||||||||||||||

| Total cost of revenue | |||||||||||||||||||||||

| Gross profit | |||||||||||||||||||||||

| Operating expenses | |||||||||||||||||||||||

| Selling and marketing | |||||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| General and administrative | |||||||||||||||||||||||

| Total operating expenses | |||||||||||||||||||||||

| (Loss) from operations | ( | ( | ( | ( | |||||||||||||||||||

| Foreign currency transaction gain (loss) | ( | ( | |||||||||||||||||||||

| Interest income | |||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | |||||||||||||||||||

| Gain on capped call transactions | |||||||||||||||||||||||

| Other income, net | |||||||||||||||||||||||

| (Loss) before (benefit from) income taxes | ( | ( | ( | ( | |||||||||||||||||||

| (Benefit from) income taxes | ( | ( | ( | ( | |||||||||||||||||||

| Net (loss) | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| (Loss) per share | |||||||||||||||||||||||

| Basic | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Diluted | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Weighted-average number of common shares outstanding | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Diluted | |||||||||||||||||||||||

See notes to unaudited condensed consolidated financial statements.

4

PEGASYSTEMS INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS)

(in thousands)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Net (loss) | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Other comprehensive (loss) income, net of tax | |||||||||||||||||||||||

| Unrealized (loss) gain on available-for-sale securities | ( | ( | ( | ||||||||||||||||||||

| Foreign currency translation adjustments | ( | ( | |||||||||||||||||||||

| Total other comprehensive (loss) income, net of tax | $ | ( | $ | ( | $ | $ | ( | ||||||||||||||||

| Comprehensive (loss) | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

See notes to unaudited condensed consolidated financial statements.

5

| PEGASYSTEMS INC. UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY (in thousands, except per share amounts) | |||||||||||||||||||||||||||||||||||

Common Stock | Additional Paid-In Capital | Retained Earnings | Accumulated Other Comprehensive (Loss) | Total Stockholders’ Equity | |||||||||||||||||||||||||||||||

| Number of Shares | Amount | ||||||||||||||||||||||||||||||||||

| December 31, 2018 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| Repurchase of common stock | ( | ( | ( | — | — | ( | |||||||||||||||||||||||||||||

| Issuance of common stock for share-based compensation plans | ( | — | — | ( | |||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

Cash dividends declared ($ | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | |||||||||||||||||||||||||||||||

| Net (loss) | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| March 31, 2019 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| Repurchase of common stock | ( | ( | ( | — | — | ( | |||||||||||||||||||||||||||||

| Issuance of common stock for share-based compensation plans | ( | — | — | ( | |||||||||||||||||||||||||||||||

| Issuance of common stock under the employee stock purchase plan | — | — | — | ||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

Cash dividends declared ($ | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Other comprehensive (loss) | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Net (loss) | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| June 30, 2019 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| Repurchase of common stock | ( | ( | ( | — | — | ( | |||||||||||||||||||||||||||||

| Issuance of common stock for share-based compensation plans | ( | — | — | ( | |||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

Cash dividends declared ($ | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Other comprehensive (loss) | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Net (loss) | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| September 30, 2019 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| See notes to unaudited condensed consolidated financial statements. | |||||||||||||||||||||||||||||||||||

6

| PEGASYSTEMS INC. UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY (in thousands, except per share amounts) | |||||||||||||||||||||||||||||||||||

Common Stock | Additional Paid-In Capital | Retained Earnings | Accumulated Other Comprehensive (Loss) | Total Stockholders’ Equity | |||||||||||||||||||||||||||||||

| Number of Shares | Amount | ||||||||||||||||||||||||||||||||||

| December 31, 2019 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| Equity component of convertible senior notes, net | — | — | — | — | |||||||||||||||||||||||||||||||

| Repurchase of common stock | ( | ( | ( | — | — | ( | |||||||||||||||||||||||||||||

| Issuance of common stock for share-based compensation plans | ( | — | — | ( | |||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

Cash dividends declared ($ | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Other comprehensive (loss) | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Net (loss) | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| March 31, 2020 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| Repurchase of common stock | ( | ( | — | — | ( | ||||||||||||||||||||||||||||||

| Issuance of common stock for share-based compensation plans | ( | — | — | ( | |||||||||||||||||||||||||||||||

| Issuance of common stock under the employee stock purchase plan | — | — | — | ||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

Cash dividends declared ($ | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | |||||||||||||||||||||||||||||||

| Net (loss) | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| June 30, 2020 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

| Repurchase of common stock | ( | ( | ( | — | — | ( | |||||||||||||||||||||||||||||

| Issuance of common stock for share-based compensation plans | ( | — | — | ( | |||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

Cash dividends declared ($ | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Other comprehensive (loss) | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Net (loss) | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| September 30, 2020 | $ | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||

See notes to unaudited condensed consolidated financial statements.

7

PEGASYSTEMS INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

| Nine Months Ended September 30, | |||||||||||

| 2020 | 2019 | ||||||||||

| Operating activities | |||||||||||

| Net (loss) | $ | ( | $ | ( | |||||||

| Adjustments to reconcile net (loss) to cash (used in) operating activities | |||||||||||

| Stock-based compensation | |||||||||||

| (Gain) on capped call transactions | ( | ||||||||||

| Deferred income taxes | ( | ( | |||||||||

| Amortization of deferred commissions | |||||||||||

| Lease expense | |||||||||||

| Amortization of debt discount and issuance costs | |||||||||||

| Amortization of intangible assets and depreciation | |||||||||||

| Amortization of investments | |||||||||||

| Foreign currency transaction (gain) loss | ( | ||||||||||

| Other non-cash | ( | ( | |||||||||

| Change in operating assets and liabilities, net | ( | ||||||||||

| Cash (used in) operating activities | ( | ( | |||||||||

| Investing activities | |||||||||||

| Purchases of investments | ( | ( | |||||||||

| Proceeds from maturities and called investments | |||||||||||

| Sales of investments | |||||||||||

| Payments for acquisitions, net of cash acquired | ( | ||||||||||

| Investment in property and equipment | ( | ( | |||||||||

| Cash (used in) provided by investing activities | ( | ||||||||||

| Financing activities | |||||||||||

| Proceeds from issuance of convertible senior notes | |||||||||||

| Purchase of capped calls related to convertible senior notes | ( | ||||||||||

| Payment of debt issuance costs | ( | ||||||||||

| Dividend payments to shareholders | ( | ( | |||||||||

| Common stock repurchases | ( | ( | |||||||||

| Cash provided by (used in) financing activities | ( | ||||||||||

| Effect of exchange rate changes on cash and cash equivalents | ( | ||||||||||

| Net increase (decrease) in cash and cash equivalents | ( | ||||||||||

| Cash and cash equivalents, beginning of period | |||||||||||

| Cash and cash equivalents, end of period | $ | $ | |||||||||

See notes to unaudited condensed consolidated financial statements.

8

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. BASIS OF PRESENTATION

Pegasystems Inc. (together with its subsidiaries, “the Company”) has prepared the accompanying unaudited condensed consolidated financial statements pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (“SEC”) regarding interim financial reporting. Accordingly, they do not include all the information required by accounting principles generally accepted in the United States of America (“U.S.”) for complete financial statements and should be read in conjunction with the Company’s audited financial statements included in the Annual Report on Form 10-K for the year ended December 31, 2019.

In the opinion of management, the Company has prepared the accompanying unaudited condensed consolidated financial statements on the same basis as its audited financial statements, and these financial statements include all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation of the results of the interim periods presented.

All intercompany transactions and balances have been eliminated in consolidation. The operating results for the interim periods presented are not necessarily indicative of the results expected for the full year 2020.

2. NEW ACCOUNTING PRONOUNCEMENTS

Convertible debt

In August 2020, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2020-06, “Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity” (ASU 2020-06), which simplifies the accounting for certain financial instruments with characteristics of liabilities and equity, including convertible instruments and contracts in an entity’s own equity. The standard eliminates the liability and equity separation model for convertible instruments with a cash conversion feature. As a result, after adoption, entities will no longer separately present in equity an embedded conversion feature for such debt. Additionally, the embedded conversion feature will no longer be amortized into income as interest expense over the instrument’s life. Instead, entities will account for a convertible debt instrument wholly as debt unless (1) a convertible instrument contains features that require bifurcation as a derivative under ASC Topic 815, Derivatives and Hedging, or (2) a convertible debt instrument was issued at a substantial premium. Additionally, the standard requires applying the if-converted method to calculate convertible instruments’ impact on diluted earnings per share (“EPS”). The standard is effective for fiscal years beginning after December 15, 2021, with early adoption permitted for fiscal years beginning after December 15, 2020. It can be adopted on either a full retrospective or modified retrospective basis. The Company is currently evaluating the effect this ASU will have on its consolidated financial statements and related disclosures. The Company expects to early adopt the new standard on January 1, 2021.

Financial instruments

In June 2016, the FASB issued ASU No. 2016-13, “Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments,” which requires measurement and recognition of expected credit losses for financial assets measured at amortized cost, including accounts receivable, upon initial recognition of that financial asset using a forward-looking expected loss model, rather than an incurred loss model. Credit losses relating to available-for-sale debt securities should be recorded through an allowance for credit losses when the fair value is below the asset’s amortized cost, removing the concept of “other-than-temporary” impairments. The Company adopted this standard effective January 1, 2020. The adoption of this standard did not have a material effect on the Company’s financial position or results of operations.

3. MARKETABLE SECURITIES

| September 30, 2020 | |||||||||||||||||||||||

| (in thousands) | Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | |||||||||||||||||||

| Government debt | $ | $ | $ | ( | $ | ||||||||||||||||||

| Corporate debt | ( | ||||||||||||||||||||||

| $ | $ | $ | ( | $ | |||||||||||||||||||

As of September 30, 2020, maturities of marketable securities ranged from October 2020 to September 2023, with a weighted-average remaining maturity of approximately 1.3 years.

As of December 31, 2019, the Company did not hold any marketable securities.

9

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

4. RECEIVABLES, CONTRACT ASSETS, AND DEFERRED REVENUE

Receivables

(in thousands) | September 30, 2020 | December 31, 2019 | |||||||||

| Accounts receivable | $ | $ | |||||||||

| Unbilled receivables | |||||||||||

| Long-term unbilled receivables | |||||||||||

| $ | $ | ||||||||||

Unbilled receivables are client committed amounts for which revenue recognition precedes billing, and billing is solely subject to the passage of time.

Unbilled receivables are expected to be billed in the future as follows:

(Dollars in thousands) | September 30, 2020 | |||||||

| 1 year or less | $ | % | ||||||

| 1-2 years | % | |||||||

| 2-5 years | % | |||||||

| $ | % | |||||||

Unbilled receivables based upon contract effective date:

(Dollars in thousands) | September 30, 2020 | |||||||

| 2020 | $ | % | ||||||

| 2019 | % | |||||||

| 2018 | % | |||||||

| 2017 | % | |||||||

| 2016 and prior | % | |||||||

| $ | % | |||||||

Major clients

Clients accounting for 10% or more of the Company’s receivables:

| September 30, 2020 | December 31, 2019 | ||||||||||

| Client A | % | * | |||||||||

* Client accounted for less than 10% of total receivables.

Contract assets and deferred revenue

(in thousands) | September 30, 2020 | December 31, 2019 | |||||||||

Contract assets (1) | $ | $ | |||||||||

Long-term contract assets (2) | |||||||||||

| Deferred revenue | |||||||||||

Long-term deferred revenue (3) | |||||||||||

| $ | $ | ||||||||||

(1) Included in other current assets. (2) Included in other long-term assets. (3) Included in other long-term liabilities.

Contract assets are client committed amounts for which revenue recognized exceeds the amount billed to the client and the right to payment is subject to conditions other than the passage of time, such as the completion of a related performance obligation. Deferred revenue consists of billings and payments received in advance of revenue recognition. Contract assets and deferred revenue are netted at the contract level for each reporting period.

The change in deferred revenue in the nine months ended September 30, 2020 was primarily due to new billings in advance of revenue recognition, and $170.5 million of revenue recognized during the period that was included in deferred revenue at December 31, 2019.

5. DEFERRED COMMISSIONS

(in thousands) | September 30, 2020 | December 31, 2019 | |||||||||

Deferred commissions (1) | $ | $ | |||||||||

(1) Included in other long-term assets.

10

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| (in thousands) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||

Amortization of deferred commissions (1) | $ | $ | $ | $ | |||||||||||||||||||

6. DEBT

Convertible senior notes and capped calls

Convertible senior notes

In February 2020, the Company issued Convertible Senior Notes (the "Notes") with an aggregate principal amount of $600 million, due March 1, 2025, in a private placement. The proceeds from the Notes were used or are anticipated to be used for the Capped Call Transactions (described below), working capital, and other general corporate purposes. There are no required principal payments prior to the maturity of the Notes. The Notes accrue interest at an annual rate of 0.75 %, payable semi-annually in arrears on March 1 and September 1, beginning on September 1, 2020.

Proceeds from the Notes and Capped Call Transactions:

| (in thousands) | Amount | |||||||

| Principal | $ | |||||||

| Less: issuance costs | ( | |||||||

| Less: Capped Call Transactions | ( | |||||||

| $ | ||||||||

Conversion rights

The conversion rate is 7.4045 shares of common stock per $1,000 principal amount of the Notes, representing an initial conversion price of approximately $135.05 per share of common stock. The Company will settle conversions by paying or delivering, as applicable, cash, shares of its common stock, or a combination of cash and shares of its common stock, at the Company’s election, based on the applicable conversion rate. The conversion rate will be adjusted upon the occurrence of certain events, including spin-offs, tender offers, exchange offers, and certain stockholder distributions.

Beginning on September 1, 2024, noteholders may convert their Notes at any time at their election. Before September 1, 2024, noteholders may convert their Notes in the following circumstances:

•During any calendar quarter commencing after the calendar quarter ending on June 30, 2020 (and only during such calendar quarter), if the last reported sale price per share of the Company’s common stock exceeds one hundred and thirty percent (130 %) of the conversion price for each of at least twenty (20 ) trading days (whether or not consecutive) during the thirty (30 ) consecutive trading days ending on, and including, the last trading day of the immediately preceding calendar quarter.

•During the five consecutive business days immediately after any five consecutive trading day period (the “Measurement Period”), if the trading price per $1,000 principal amount of Notes for each trading day of the Measurement Period was less than 98 % of the product of the last reported sale price per share of common stock on such trading day and the conversion rate on such trading day.

•Upon the occurrence of certain corporate events or distributions, or if the Company calls all or any Notes for redemption, then the noteholder of any Note may convert such Note at any time before the close of business on the business day immediately before the related redemption date (or if the Company fails to pay the redemption price due on such redemption date in full, at any time until the Company pays such redemption price in full).

As of September 30, 2020, no Notes were eligible for conversion at the noteholders’ election.

Repurchase rights

On or after March 1, 2023 and on or before the 40th scheduled trading day immediately before the maturity date, the Company may redeem for cash all or part of the Notes, at a repurchase price equal to 100 % of the principal amount, plus accrued and unpaid interest, if the last reported sale price of the Company’s common stock exceeded 130 % of the conversion price then in effect for at least 20 trading days (whether or not consecutive) during any 30 consecutive trading day period ending on, and including, the trading day immediately preceding the date on which the Company provides a redemption notice.

If certain corporate events that constitute a “Fundamental Change” (as described below) occur at any time, each noteholder will have the right, at such noteholder’s option, to require the Company to repurchase for cash all of such noteholder’s Notes, or any portion of the principal thereof that is equal to $1,000 or an integral multiple of $1,000, at a repurchase price equal to 100 % of the principal amount thereof, plus accrued and unpaid interest. A fundamental change relates to events such as mergers, changes in control of the Company, liquidation/dissolution of the Company, or the delisting of the Company’s common stock.

11

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Impact of the Notes

In accounting for the transaction, the Notes have been separated into liability and equity components.

•The initial carrying amount of the liability component was calculated by measuring a similar debt instrument’s fair value that does not have an associated conversion feature. The excess of the Notes’ principal amount over the initial carrying amount of the liability component, the debt discount, is amortized as interest expense over the Notes’ contractual term.

•The equity component was recorded as an increase to additional paid-in capital and is not remeasured as long as it continues to meet the conditions for equity classification.

The Company incurred issuance costs of $14.5 million related to the Notes, allocated between the Notes’ liability and equity components proportionate to the initial carrying amount of the liability and equity components.

•Issuance costs attributable to the liability component are recorded as an offset to the Notes’ principal balance. They are amortized as interest expense using the effective interest method over the contractual term of the Notes.

•Issuance costs attributable to the equity component are recorded as an offset to the equity component in additional paid-in capital and are not amortized.

Net carrying amount of the liability component:

| (in thousands) | September 30, 2020 | ||||

| Principal | $ | ||||

| Unamortized debt discount | ( | ||||

| Unamortized issuance costs | ( | ||||

| $ | |||||

Net carrying amount of the equity component, included in additional paid-in capital:

| (in thousands) | September 30, 2020 | ||||

Conversion options (1) | $ | ||||

(1) Net of issuance costs and taxes.

Interest expense related to the Notes:

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| (in thousands) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||

Contractual interest expense ( | $ | $ | $ | $ | |||||||||||||||||||

Amortization of debt discount (1) | |||||||||||||||||||||||

Amortization of issuance costs (1) | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

(1) Amortized based upon an effective interest rate of 4.31

Future payments of principal and contractual interest:

| September 30, 2020 | |||||||||||||||||

| (in thousands) | Principal | Interest | Total | ||||||||||||||

| 2020 | $ | $ | $ | ||||||||||||||

| 2021 | |||||||||||||||||

| 2022 | |||||||||||||||||

| 2023 | |||||||||||||||||

| 2024 | |||||||||||||||||

| 2025 | |||||||||||||||||

| $ | $ | $ | |||||||||||||||

Capped call transactions

In February 2020, the Company entered into privately negotiated capped call transactions (“Capped Call Transactions”) with certain financial institutions. The Capped Call Transactions cover approximately 4.4 million shares (representing the number of shares for which the Notes are initially convertible) of the Company’s common stock. They are generally expected to reduce potential dilution to the common stock upon any conversion of Notes and/or offset any potential cash payments the Company is required to make in excess of the principal amount of converted Notes, as the case may be, with such reduction and/or offset subject to a cap. The cap price of the Capped Call Transactions is $196.44 , subject to adjustment upon the occurrence of specified extraordinary events affecting the Company, including merger events and tender offers.

12

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

The Capped Call Transactions are accounted for as derivative instruments. The Capped Call Transactions do not qualify for the Company’s own equity scope exception in ASC 815 since, in some cases of early settlement, the settlement value of the Capped Call Transactions, calculated in accordance with the governing documents, may not represent a fair value measurement. The Capped Call Transactions are classified as “other long term assets” and remeasured to fair value at the end of each reporting period, resulting in a non-operating gain or loss.

Change in value of Capped Call Transactions:

| (in thousands) | Nine Months Ended September 30, 2020 | ||||

| Value at issuance | $ | ||||

| Fair value adjustment | |||||

| Balance as of September 30, | $ | ||||

Credit facility

In November 2019, and as amended in February 2020, July 2020, and October 2020, the Company entered into a five-year $100 million senior secured revolving credit agreement (the “Credit Facility”) with PNC Bank, National Association (“PNC”). The Company may use borrowings to finance working capital needs and for general corporate purposes. Subject to specific conditions, the Credit Facility allows the Company to increase the aggregate commitment to $200 million. The commitments expire on November 4, 2024, and any outstanding loans will be payable on such date. The Credit Facility, as amended, contains customary covenants, including, but not limited to, those relating to additional indebtedness, liens, asset divestitures, and affiliate transactions.

The Company is also required to comply with financial covenants, including:

•Beginning with the fiscal quarter ended on September 30, 2020 and ending with the fiscal quarter ended December 31, 2021 at least $200 million in cash and investments held by Pegasystems Inc.

•Beginning with the quarter ended on March 31, 2022 a maximum net consolidated leverage ratio of 3.5 to 1.0 (with a step-up in the event of certain acquisitions) and a minimum consolidated interest coverage ratio of 3.5 to 1.0.

7. FAIR VALUE MEASUREMENTS

Assets and liabilities measured at fair value on a recurring basis

The Company records its cash equivalents, Capped Call Transactions, and venture investments at fair value on a recurring basis. Fair value is an exit price, representing the amount that would be received from the sale of an asset or paid to transfer a liability in an orderly transaction between market participants based on assumptions that market participants would use in pricing an asset or liability.

As a basis for classifying the fair value measurements, a three-tier fair value hierarchy, which classifies the fair value measurements based on the inputs used in measuring fair value, was established as follows:

•Level 1 - observable inputs such as quoted prices in active markets for identical assets or liabilities;

•Level 2 - significant other inputs that are observable either directly or indirectly; and

•Level 3 - significant unobservable inputs on which there is little or no market data, which require the Company to develop its own assumptions. This hierarchy requires the Company to use observable market data, when available, and minimize unobservable inputs when determining fair value.

The fair value of the Capped Call Transactions at the end of each reporting period is determined using a Black-Scholes option-pricing model. The valuation models use various market-based inputs, including stock price, remaining contractual term, expected volatility, risk-free interest rate, and expected dividend yield, as applicable. The Company applies judgment in its determination of expected volatility. The Company considers both historical and implied volatility levels of the underlying equity security and, to a lesser extent, historical peer group volatility levels. The Company’s venture investments are recorded at fair value based on valuation methods using the observable transaction price and other unobservable inputs, including the volatility, rights, and obligations of the securities the Company holds.

The Company’s assets and liabilities measured at fair value on a recurring basis:

| September 30, 2020 | December 31, 2019 | ||||||||||||||||||||||||||||||||||||||||||||||

| (in thousands) | Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | Total | |||||||||||||||||||||||||||||||||||||||

Cash equivalents (1) | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

| Marketable securities | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

Capped Call Transactions (2) (3) | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

Venture investments (2) (4) | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||

(1) Investments in money market funds. (2) Included in other long-term assets. (3) See "6. Debt" for additional information. (4) Investments in privately-held companies.

13

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

Change in venture investments:

| (in thousands) | Nine Months Ended September 30, 2020 | ||||

| December 31, 2019 | $ | ||||

| New investments | |||||

| Sales of investments | ( | ||||

| Fair value adjustment | |||||

| September 30, 2020 | $ | ||||

The carrying value of certain other financial instruments, including receivables and accounts payable, approximates fair value due to the relatively short maturity of these items.

Fair value of the Notes

The fair value of the Company’s Notes was recorded at $515.9 million upon issuance, which reflected the principal amount of the Notes less the fair value of the conversion feature. The fair value of the debt component was determined based on a discounted cash flow model. The discount rate used reflected both the time value of money and credit risk inherent in the Notes. The carrying value of the Notes will be accreted, over the remaining term to maturity, to their principal value of $600 million.

The Notes’ fair value (inclusive of the conversion feature, which is embedded in the Notes) was $680 million as of September 30, 2020. The fair value was determined based on the Notes’ quoted price in an over-the-counter market on the last trading day of the reporting period and classified within Level 2 in the fair value hierarchy. See "6. Debt" for additional information.

8. REVENUE

Geographic revenue

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||||||||||||||

(Dollars in thousands) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||||||||||||||

| U.S. | $ | % | $ | % | $ | % | $ | % | |||||||||||||||||||||||||||

| Other Americas | % | % | % | % | |||||||||||||||||||||||||||||||

| United Kingdom (“U.K.”) | % | % | % | % | |||||||||||||||||||||||||||||||

| Europe (excluding U.K.), Middle East, and Africa | % | % | % | % | |||||||||||||||||||||||||||||||

| Asia-Pacific | % | % | % | % | |||||||||||||||||||||||||||||||

| $ | % | $ | % | $ | % | $ | % | ||||||||||||||||||||||||||||

Revenue streams

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

(in thousands) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||

| Perpetual license | $ | $ | $ | $ | |||||||||||||||||||

| Term license | |||||||||||||||||||||||

| Revenue recognized at a point in time | |||||||||||||||||||||||

| Maintenance | |||||||||||||||||||||||

| Pega Cloud | |||||||||||||||||||||||

| Consulting | |||||||||||||||||||||||

| Revenue recognized over time | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

14

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

| (in thousands) | Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||

| Pega Cloud | $ | $ | $ | $ | |||||||||||||||||||

| Maintenance | |||||||||||||||||||||||

| Term license | |||||||||||||||||||||||

Subscription (1) | |||||||||||||||||||||||

| Perpetual license | |||||||||||||||||||||||

| Consulting | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

(1) Reflects client arrangements subject to renewal (Pega Cloud, maintenance, and term license).

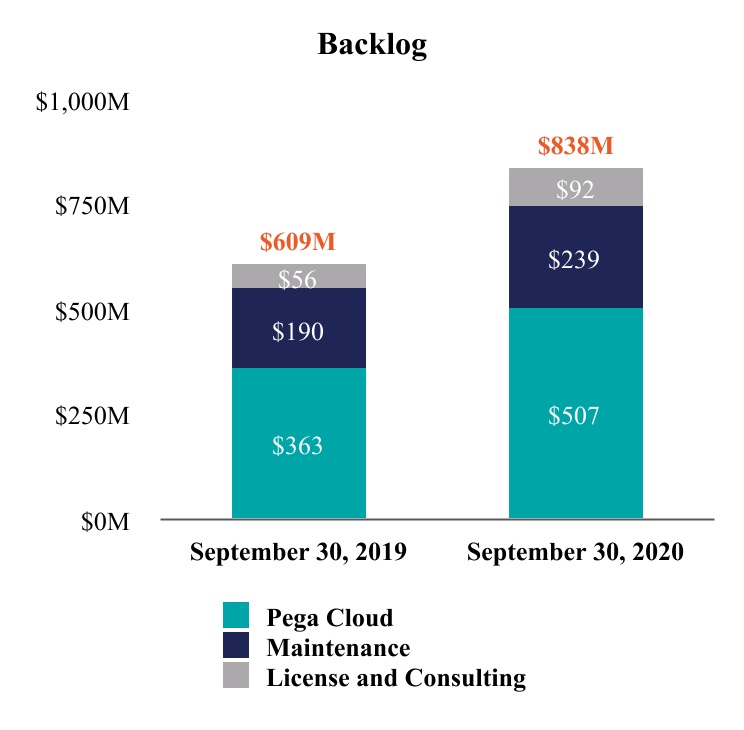

Remaining performance obligations ("Backlog")

Expected future revenue on existing contracts:

| September 30, 2020 | ||||||||||||||||||||||||||||||||||||||

(Dollars in thousands) | Perpetual license | Term license | Maintenance | Pega Cloud | Consulting | Total | ||||||||||||||||||||||||||||||||

| 1 year or less | $ | $ | $ | $ | $ | $ | % | |||||||||||||||||||||||||||||||

| 1-2 years | % | |||||||||||||||||||||||||||||||||||||

| 2-3 years | % | |||||||||||||||||||||||||||||||||||||

| Greater than 3 years | % | |||||||||||||||||||||||||||||||||||||

| $ | $ | $ | $ | $ | $ | % | ||||||||||||||||||||||||||||||||

| September 30, 2019 | ||||||||||||||||||||||||||||||||||||||

(Dollars in thousands) | Perpetual license | Term license | Maintenance | Pega Cloud | Consulting | Total | ||||||||||||||||||||||||||||||||

| 1 year or less | $ | $ | $ | $ | $ | $ | % | |||||||||||||||||||||||||||||||

| 1-2 years | % | |||||||||||||||||||||||||||||||||||||

| 2-3 years | % | |||||||||||||||||||||||||||||||||||||

| Greater than 3 years | % | |||||||||||||||||||||||||||||||||||||

| $ | $ | $ | $ | $ | $ | % | ||||||||||||||||||||||||||||||||

9. STOCK-BASED COMPENSATION

Expense

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| (in thousands) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||

Cost of revenue | $ | $ | $ | $ | |||||||||||||||||||

Selling and marketing | |||||||||||||||||||||||

Research and development | |||||||||||||||||||||||

General and administrative | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

Income tax benefit | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

As of September 30, 2020, the Company had $115.0 million of unrecognized stock-based compensation expense, net of estimated forfeitures, which is expected to be recognized over a weighted-average period of 2.2 years.

Grants

The Company granted the following stock-based compensation awards:

| Nine Months Ended September 30, 2020 | |||||||||||

| (in thousands) | Shares | Total Fair Value | |||||||||

RSUs | $ | ||||||||||

Non-qualified stock options | $ | ||||||||||

| Common stock | $ | ||||||||||

15

PEGASYSTEMS INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (continued)

10. INCOME TAXES

Effective income tax rate

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| (Dollars in thousands) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||

| (Benefit from) income taxes | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Effective income tax rate | % | % | |||||||||||||||||||||

11. (LOSS) PER SHARE

Basic (loss) per share is calculated using the weighted-average number of common shares outstanding during the period. Diluted (loss) per share is calculated using the weighted-average number of common shares outstanding during the period, plus the dilutive effect of outstanding stock options, RSUs, and the conversion spread of the Company’s convertible senior notes.

Calculation of the basic and diluted earnings per share:

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| (in thousands, except per share amounts) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||

| Net (loss) | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Weighted-average common shares outstanding | |||||||||||||||||||||||

| (Loss) per share, basic | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Net (loss) | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

Weighted-average common shares outstanding, assuming dilution (1) (2) | |||||||||||||||||||||||

| (Loss) per share, diluted | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

Outstanding anti-dilutive stock options and RSUs (3) | |||||||||||||||||||||||

(1) The Company expects to settle the principal amount of the Notes in cash. As a result, only the amount by which the conversion value exceeds the aggregated principal amount of the Notes is included in the diluted earnings per share computation under the treasury stock method. The conversion spread has a dilutive impact on diluted net income per share when the average market price of the Company’s common stock for a given period exceeds the initial conversion price of $135.05 per share for the Notes. In connection with the Notes’ issuance, the Company entered into Capped Call Transactions, which were not included in calculating the number of diluted shares outstanding, as their effect would have been anti-dilutive.

(2) In periods of loss, all dilutive securities are excluded as their inclusion would be anti-dilutive.

(3) Certain outstanding stock options and RSUs were excluded from the computation of diluted earnings per share because they were anti-dilutive in the period presented. These awards may be dilutive in the future.

16

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains or incorporates forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995.

Words such as expects, anticipates, intends, plans, believes, will, could, should, estimates, may, targets, strategies, intends to, projects, forecasts, guidance, likely, and usually, or variations of such words and other similar expressions identify forward-looking statements, which are based on current expectations and assumptions.

These forward-looking statements deal with future events, and are subject to various risks and uncertainties that are difficult to predict, including, but not limited to, statements about our future financial performance and business plans, the adequacy of our liquidity and capital resources, the continued payment of quarterly dividends, the timing of revenue recognition, management of our transition to a more subscription-based business model, variation in demand for our products and services, including among clients in the public sector, the impact of actual or threatened public health emergencies, such as the Coronavirus (COVID-19), reliance on third-party service providers, compliance with our debt obligations and debt covenants, the potential impact of our convertible senior notes and related Capped Call Transactions, reliance on key personnel, the continued uncertainties in the global economy, foreign currency exchange rates, the potential legal and financial liabilities and reputation damage due to cyber-attacks, security breaches and security flaws, our ability to protect our intellectual property rights and costs associated with defending such rights, maintenance of our client retention rate, and management of our growth. These risks and others that may cause actual results to differ materially from those expressed in such forward-looking statements are described further in Part I of our Annual Report on Form 10-K for the year ended December 31, 2019, and other filings we make with the U.S. Securities and Exchange Commission (“SEC”).

Except as required by applicable law, we do not undertake and expressly disclaim any obligation to publicly update or revise these forward-looking statements whether as the result of new information, future events, or otherwise.

BUSINESS OVERVIEW

We develop, market, license, host, and support enterprise software applications that help organizations transform how they engage with their customers and process work across their enterprise. We also license our low-code Pega Platform™ for rapid application development to clients that wish to build and extend their business applications. Our cloud-architected portfolio of customer engagement and digital process automation applications leverages artificial intelligence (“AI”), case management, and robotic automation technology, built on our unified low-code Pega Platform, empowering businesses to quickly design, extend, and scale their enterprise applications to meet strategic business needs.

Our target clients are Global 3000 organizations and government agencies that require applications to differentiate themselves in the markets they serve. Our applications achieve and facilitate differentiation by increasing business agility, driving growth, improving productivity, attracting and retaining customers, and reducing risk. We deliver applications tailored to our clients’ specific industry needs.

Cloud Transition

We are in the process of transitioning our business to primarily sell software through subscription arrangements, particularly Pega Cloud (“Cloud Transition”). Until we substantially complete our Cloud Transition, which we expect to occur in early 2023, we expect to continue to experience lower revenue growth and lower operating cash flow growth or negative cash flow. The actual mix of perpetual license, term license, and Pega Cloud in a given period can fluctuate based on client preferences.

Additional information on the transition’s impact can be found below and in the “Risk Factors” section of our Annual Report on Form 10-K for the year ended December 31, 2019.

COVID-19

As of September 30, 2020, COVID-19 has not had a material impact on our results of operations or financial condition.

The ultimate impact of COVID-19 on our operational and financial performance will depend on future developments, including the duration and spread of the outbreak, impact on our clients and our sales cycles, and impact on our partners, vendors, or employees, all of which are uncertain and unpredictable. Our shift towards subscription-based revenue streams, the industry mix of our clients, our product mix, the fact that many of our clients are well-known and of large size, and the critical nature of our products to our clients may reduce or delay the impact of COVID-19 on our business. However, it is not possible to estimate the ultimate impact that COVID-19 will have on our business. See “Coronavirus (“COVID-19”)” under Item 1A. Risk Factors for additional information.

17

Performance metrics

We utilize several performance metrics to analyze and assess our overall performance, make operating decisions, and forecast and plan for future periods, including:

Annual contract value (“ACV”) | Increased 21% since September 30, 2019

•ACV represents the annualized value of our active contracts as of the measurement date. The contract's total value is divided by its duration in years to calculate ACV for term license and Pega Cloud contracts. Maintenance revenue for the quarter then ended is multiplied by four to calculate ACV for maintenance. Client Cloud ACV is composed of maintenance ACV and ACV from term license contracts. We believe the presentation of ACV on a constant currency basis enhances the understanding of our results, as it provides visibility into the impact of changes in foreign currency exchange rates, which are outside of our control. All periods shown reflect foreign currency exchange rates as of September 30, 2020.

Remaining performance obligations (“Backlog”) | Increased 38% since September 30, 2019

•Backlog represents contracted revenue that has not yet been recognized and includes deferred revenue and non-cancellable amounts expected to be invoiced and recognized as revenue in future periods.

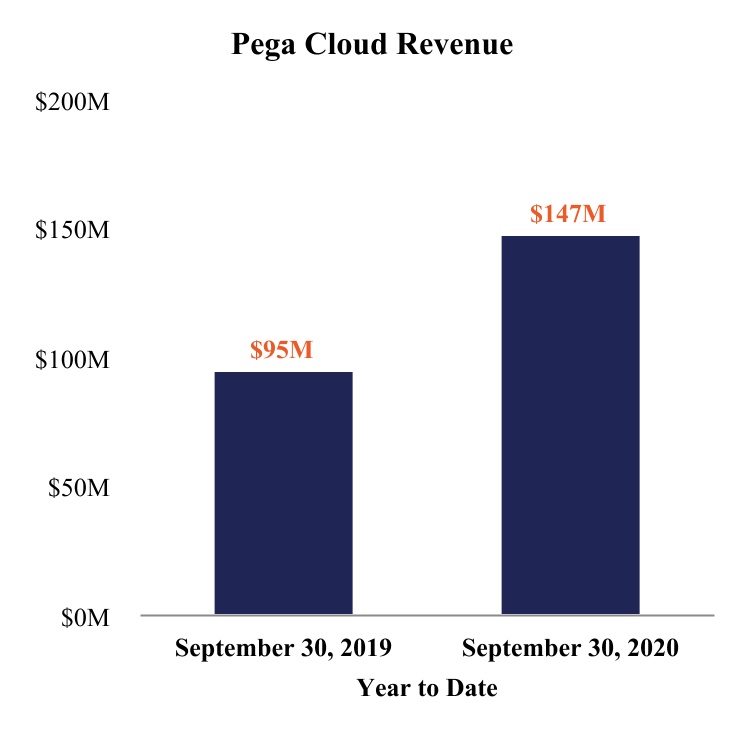

Year to date Pega Cloud revenue | Increased 55% since September 30, 2019

•Pega Cloud revenue is revenue as reported under U.S. GAAP for cloud contracts.

18

CRITICAL ACCOUNTING POLICIES

Management’s Discussion and Analysis of Financial Condition and Results of Operations is based upon our unaudited condensed consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States (“U.S.”) and the rules and regulations of the SEC for interim financial reporting. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues, expenses, and the related disclosure of contingent assets and liabilities. We base our estimates and judgments on historical experience, knowledge of current conditions, and expectations of what could occur in the future given the available information.

For more information regarding our critical accounting policies, we encourage you to read the discussion in the following locations in our Annual Report on Form 10-K for the year ended December 31, 2019:

•“Critical Accounting Estimates and Significant Judgments” in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations”; and

•Note 2. “Significant Accounting Policies” in Item 8. “Financial Statements and Supplementary Data.”

There have been no significant changes to our critical accounting policies as disclosed in our Annual Report on Form 10-K for the year ended December 31, 2019 other than those listed below.

Capped Call Transactions

In February 2020, we entered into privately negotiated capped call transactions (“Capped Call Transactions”) with certain financial institutions. The Capped Call Transactions cover approximately 4.4 million shares (representing the number of shares for which the Notes are initially convertible) of our common stock and are generally expected to reduce potential dilution of our common stock upon any conversion of the Notes. The fair value of the Capped Call Transactions at the end of each reporting period is determined using a Black-Scholes option-pricing model. The valuation models use various market-based inputs, including stock price, remaining contractual term, expected volatility, risk-free interest rate, and expected dividend yield, as applicable. Management applies judgment in its determination of expected volatility. We consider both historical and implied volatility levels of the underlying equity security and, to a lesser extent, historical peer group volatility levels.

The Capped Call Transactions are classified as “other long-term assets” and remeasured to fair value at the end of each reporting period, resulting in a non-operating gain or loss.

See "6. Debt" and “7. Fair Value Measurements” in Item 1 of this Quarterly Report for additional information.

19

RESULTS OF OPERATIONS

Revenue

Our Pega Cloud revenue is derived from our hosted Pega Platform and software applications. Our license revenue is derived from sales of our applications and the Pega Platform.

Cloud Transition

We are in the process of transitioning our business to primarily sell software through subscription arrangements, particularly Pega Cloud. As revenue from Pega Cloud arrangements is generally recognized over the contract term while revenue from perpetual and term licenses is generally recognized when the license rights become effective, the shift has and is expected to continue to result in slower revenue growth during the transition.

| (Dollars in thousands) | Three Months Ended September 30, | Change | Nine Months Ended September 30, | Change | |||||||||||||||||||||||||||||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Pega Cloud | $ | 54,776 | 24 | % | $ | 35,153 | 16 | % | $ | 19,623 | 56 | % | $ | 147,080 | 20 | % | $ | 94,610 | 15 | % | $ | 52,470 | 55 | % | |||||||||||||||||||||||||||||

| Maintenance | 74,670 | 33 | % | 70,371 | 32 | % | 4,299 | 6 | % | 220,587 | 31 | % | 207,406 | 33 | % | 13,181 | 6 | % | |||||||||||||||||||||||||||||||||||

| Term license | 35,932 | 16 | % | 48,989 | 23 | % | (13,057) | (27) | % | 170,455 | 24 | % | 122,257 | 19 | % | 48,198 | 39 | % | |||||||||||||||||||||||||||||||||||

Subscription (1) | $ | 165,378 | 73 | % | $ | 154,513 | 71 | % | 10,865 | 7 | % | $ | 538,122 | 75 | % | $ | 424,273 | 67 | % | 113,849 | 27 | % | |||||||||||||||||||||||||||||||

| Perpetual license | 3,852 | 2 | % | 9,016 | 4 | % | (5,164) | (57) | % | 16,568 | 2 | % | 43,286 | 7 | % | (26,718) | (62) | % | |||||||||||||||||||||||||||||||||||

| Consulting | 56,721 | 25 | % | 53,174 | 25 | % | 3,547 | 7 | % | 164,227 | 23 | % | 167,282 | 26 | % | (3,055) | (2) | % | |||||||||||||||||||||||||||||||||||

| $ | 225,951 | 100 | % | $ | 216,703 | 100 | % | $ | 9,248 | 4 | % | $ | 718,917 | 100 | % | $ | 634,841 | 100 | % | $ | 84,076 | 13 | % | ||||||||||||||||||||||||||||||

(1) Reflects client arrangements subject to renewal (Pega Cloud, maintenance, and term license).

The changes in total revenue in the three and nine months ended September 30, 2020 generally reflect our Cloud Transition. Other factors impacting our revenue included:

•Term license revenue was higher in the three months ended September 30, 2019 primarily due to a greater number of large deals than in the three months ended September 30, 2020.

•An increasing portion of our term license contracts include multi-year committed maintenance periods instead of annually renewable maintenance. Under such arrangements, a greater portion of the total contract value is recorded as maintenance revenue, which is recognized over the contract term, rather than as term revenue, as the license rights become effective which is usually shortly after contract execution. In the three and nine months ended September 30, 2020 multi-year committed maintenance contributed $2.9 million and $7.7 million to maintenance revenue growth. In the nine months ended September 30, 2020 multi-year committed maintenance reduced term revenue growth by $10.2 million.

•Maintenance renewal rates remained over 90% in the nine months ended September 30, 2020.

•The decrease in consulting revenue in the nine months ended September 30, 2020 was primarily due to lower billable travel expenses as a result of COVID-19. The increase in consulting revenue in the three months ended September 30, 2020 was primarily due to increased billable hours which more than offset the impact of reduced billable travel expenses due to COVID-19.

Gross profit

| Three Months Ended September 30, | Change | Nine Months Ended September 30, | Change | ||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in thousands) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Software license | $ | 39,093 | 98 | % | $ | 57,329 | 99 | % | $ | (18,236) | (32) | % | $ | 184,669 | 99 | % | $ | 162,561 | 98 | % | $ | 22,108 | 14 | % | |||||||||||||||||||||||||||||

| Maintenance | 69,192 | 93 | % | 63,683 | 90 | % | 5,509 | 9 | % | 203,942 | 92 | % | 188,091 | 91 | % | 15,851 | 8 | % | |||||||||||||||||||||||||||||||||||

| Pega Cloud | 35,059 | 64 | % | 17,329 | 49 | % | 17,730 | 102 | % | 90,842 | 62 | % | 46,841 | 50 | % | 44,001 | 94 | % | |||||||||||||||||||||||||||||||||||

| Consulting | 4,808 | 8 | % | (2,536) | (5) | % | 7,344 | * | 5,446 | 3 | % | 4,933 | 3 | % | 513 | 10 | % | ||||||||||||||||||||||||||||||||||||

| $ | 148,152 | 66 | % | $ | 135,805 | 63 | % | $ | 12,347 | 9 | % | $ | 484,899 | 67 | % | $ | 402,426 | 63 | % | $ | 82,473 | 20 | % | ||||||||||||||||||||||||||||||

* not meaningful

•The changes in gross profit in the three and nine months ended September 30, 2020 were primarily due to our Cloud Transition, revenue growth, and cost efficiency gains as Pega Cloud grows and scales.

•The increase in consulting gross profit in the three months ended September 30, 2020 was primarily due to an increase in consultant utilization. Consultant utilization is impacted by several factors, including the scope and timing of new implementation projects and our level of involvement in implementation projects compared to our consulting partners and enabled clients. To support our long-term strategy, we intend to grow and increasingly leverage our partners and enabled clients for future implementation projects, which may reduce the future growth rate.

20

Operating expenses

| (Dollars in thousands) | Three Months Ended September 30, | Change | Nine Months Ended September 30, | Change | |||||||||||||||||||||||||||||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| % of Revenue | % of Revenue | % of Revenue | % of Revenue | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Selling and marketing | $ | 132,053 | 58 | % | $ | 115,237 | 53 | % | $ | 16,816 | 15 | % | $ | 395,684 | 55 | % | $ | 341,064 | 54 | % | $ | 54,620 | 16 | % | |||||||||||||||||||||||||||||

| Research and development | $ | 60,024 | 27 | % | $ | 52,492 | 24 | % | $ | 7,532 | 14 | % | $ | 177,620 | 25 | % | $ | 152,802 | 24 | % | $ | 24,818 | 16 | % | |||||||||||||||||||||||||||||

| General and administrative | $ | 17,907 | 8 | % | $ | 14,843 | 7 | % | $ | 3,064 | 21 | % | $ | 49,192 | 7 | % | $ | 41,693 | 7 | % | $ | 7,499 | 18 | % | |||||||||||||||||||||||||||||

•The increases in selling and marketing in the three and nine months ended September 30, 2020 were primarily due to increases in compensation and benefits of $24.4 million and $76.0 million, attributable to increases in headcount and equity compensation. The increases in headcount reflect our efforts to increase our sales capacity to deepen relationships with existing clients and target new accounts. These increases were partially offset by decreases in travel and entertainment of $8.5 million and $17.4 million as a result of COVID-19.

•The increases in research and development in the three and nine months ended September 30, 2020 were primarily due to increases in compensation and benefits of $7.8 million and $23.6 million, attributable to increases in headcount and equity compensation.

•The increases in general and administrative in the three and nine months ended September 30, 2020 were primarily due to increases in compensation and benefits of $0.8 million and $3.0 million, attributed to increases in headcount and equity compensation, and increases in professional services fees of $1.5 million and $4.2 million.

Other income (expense), net

| (Dollars in thousands) | Three Months Ended September 30, | Change | Nine Months Ended September 30, | Change | |||||||||||||||||||||||||||||||||||||

| 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||||||||||||||||||||||

| Foreign currency transaction gain (loss) | $ | 4,236 | $ | (1,970) | $ | 6,206 | * | $ | 2,545 | $ | (3,577) | $ | 6,122 | * | |||||||||||||||||||||||||||

| Interest income | 243 | 598 | (355) | (59) | % | 1,092 | 1,865 | (773) | (41) | % | |||||||||||||||||||||||||||||||

| Interest expense | (5,956) | (42) | (5,914) | (14,081) | % | (13,791) | (42) | (13,749) | (32,736) | % | |||||||||||||||||||||||||||||||

| Gain on capped call transactions | 18,989 | — | 18,989 | * | 19,816 | — | 19,816 | * | |||||||||||||||||||||||||||||||||

| Other income, net | — | 323 | (323) | (100) | % | 1,374 | 378 | 996 | 263 | % | |||||||||||||||||||||||||||||||

| $ | 17,512 | $ | (1,091) | $ | 18,603 | * | $ | 11,036 | $ | (1,376) | $ | 12,412 | * | ||||||||||||||||||||||||||||

* not meaningful

•The changes in foreign currency transaction gain (loss) in the three and nine months ended September 30, 2020 were primarily due to the impact of fluctuations in foreign currency exchange rates associated with our foreign currency-denominated cash, accounts receivable, and intercompany receivables and payables held by our United Kingdom (“U.K.”) subsidiary.

•The decreases in interest income in the three and nine months ended September 30, 2020 were due to the decreases in market interest rates.

•The increases in interest expense in the three and nine months ended September 30, 2020 were due to our issuance of $600 million in aggregate principal amount of the Notes on February 24, 2020. See "6. Debt" in Item 1 of this Quarterly Report for additional information.

Interest expense related to the Notes:

| Three Months Ended September 30, | Change | Nine Months Ended September 30, | Change | ||||||||||||||||||||||||||||||||

| (in thousands) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||||||||||||||

Contractual interest expense (0.75% coupon) | $ | 1,125 | $ | — | $ | 1,125 | $ | 2,700 | $ | — | $ | 2,700 | |||||||||||||||||||||||

| Amortization of debt discount | 3,807 | — | 3,807 | 9,060 | — | 9,060 | |||||||||||||||||||||||||||||

| Amortization of issuance costs | 565 | — | 565 | 1,345 | — | 1,345 | |||||||||||||||||||||||||||||

| $ | 5,497 | $ | — | $ | 5,497 | $ | 13,105 | $ | — | $ | 13,105 | ||||||||||||||||||||||||

•The increases in the gain on capped call transactions in the three and nine months ended September 30, 2020 were due to fair value adjustments on the Capped Call Transactions entered into in connection with our issuance of the Notes. See "6. Debt" in Item 1 of this Quarterly Report for additional information.

•The increase in other income, net in the nine months ended September 30, 2020 was due to a gain from our venture investments portfolio.

21

(Benefit from) income taxes

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| (Dollars in thousands) | 2020 | 2019 | 2020 | 2019 | |||||||||||||||||||

| (Benefit from) income taxes | $ | (25,053) | $ | (17,520) | $ | (61,182) | $ | (43,158) | |||||||||||||||

Effective income tax rate | 48 | % | 32 | % | |||||||||||||||||||

The inclusion of excess tax benefits from stock-based compensation in the provision for income taxes has increased the variability of the effective tax rates in recent periods. This fluctuation may continue in future periods, depending on our future stock price in relation to the fair value of awards, the timing of the vestings of RSU awards, the exercise behavior of our stock option holders, and the total value of future grants of stock-based compensation awards.

During the nine months ended September 30, 2020, our effective income tax rate benefit increased primarily due to the excess tax benefits from stock-based compensation and a carryback claim benefit as a result of the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”).

LIQUIDITY AND CAPITAL RESOURCES

| Nine Months Ended September 30, | |||||||||||

| (in thousands) | 2020 | 2019 | |||||||||

| Cash provided by (used in): | |||||||||||

| Operating activities | $ | (26,257) | $ | (13,462) | |||||||

| Investing activities | (210,701) | 53,448 | |||||||||

| Financing activities | 449,630 | (61,941) | |||||||||

| Effect of exchange rates on cash and cash equivalents | 183 | (363) | |||||||||

| Net increase (decrease) in cash and cash equivalents | $ | 212,855 | $ | (22,318) | |||||||

(in thousands) | September 30, 2020 | December 31, 2019 | |||||||||

Held by U.S. entities | $ | 415,358 | $ | 23,437 | |||||||

Held by foreign entities | 52,670 | 44,926 | |||||||||

Total cash, cash equivalents, and marketable securities | $ | 468,028 | $ | 68,363 | |||||||

We believe that our current cash, cash flow from operations, and borrowing capacity will be sufficient to fund our operations and quarterly cash dividends for at least the next 12 months. Whether these resources are adequate to meet our liquidity needs beyond that period will depend on our growth, operating results, and the investments required to respond to the possible increased demand for our services. If we require additional capital resources to grow our business, we may seek to finance our operations from available funds or additional external financing.

If it became necessary to repatriate foreign funds, we may be required to pay U.S. and foreign taxes upon repatriation. Due to the complexity of income tax laws and regulations, and the Tax Reform Act’s effects, it is impracticable to estimate the amount of taxes we would have to pay.

Cash (used in) operating activities

We are in the process of transitioning our business to primarily sell software through subscription arrangements, particularly Pega Cloud. As cash from Pega Cloud and term arrangements is generally collected over the contract term while cash from perpetual licenses is generally collected when the license rights become effective, the shift has and is expected to continue to impact our cash collections. As client preferences continue to shift in favor of Pega Cloud arrangements, we could continue to experience slower operating cash flow growth, or negative cash flow, in the near term.

In the nine months ended September 30, 2020, COVID-19 did not have a material impact on our cash flows from operations. See “Coronavirus (“COVID-19”)” under Item 1A. Risk Factors for additional information.

The change in cash (used in) operating activities in the nine months ended September 30, 2020 was primarily due to our Cloud Transition and increased costs as we accelerated investments in our Pega Cloud offering and selling and marketing activities to support future growth.

22

Cash (used in) provided by investing activities

The change in cash (used in) provided by investing activities in the nine months ended September 30, 2020 was primarily driven by purchases of financial instruments and investments in property and equipment at several of our office locations.

Cash provided by (used in) financing activities

Convertible senior notes

In February 2020, we issued $600 million in aggregate principal amount of our convertible senior notes (“Notes”) due March 1, 2025, which provided proceeds as follows:

| (in thousands) | Amount | |||||||

| Principal | $ | 600,000 | ||||||

| Less: issuance costs | (14,527) | |||||||

| Less: Capped Call Transactions | (51,900) | |||||||

| $ | 533,573 | |||||||

A portion of the proceeds of the Notes was used to fund the Capped Call Transactions with the remainder to be used for working capital and other general corporate purposes. See "6. Debt" in Item 1 of this Quarterly Report for additional information.

Credit facility

In November 2019, and as amended in February 2020, July 2020, and October 2020, we entered into a five-year $100 million senior secured revolving credit agreement (the “Credit Facility”) with PNC Bank, National Association (“PNC”). As of September 30, 2020, we had no outstanding borrowings under the Credit Facility. See "6. Debt" in Item 1 of this Quarterly Report for additional information.

Stock repurchase program (1)

Changes in the remaining stock repurchase authority:

| (in thousands) | Nine Months Ended September 30, 2020 | ||||

| December 31, 2019 | $ | 45,484 | |||

Authorizations (2) | 20,516 | ||||

| Repurchases | (18,828) | ||||

| September 30, 2020 | $ | 47,172 | |||

(1) Purchases under this program have been made on the open market. (2) On June 15, 2020, we announced that our Board of Directors extended the current stock repurchase program’s expiration date to June 30, 2021 and increased the remaining stock repurchase authority to $60 million.

Common stock repurchases

| Nine Months Ended September 30, | |||||||||||||||||||||||

| 2020 | 2019 | ||||||||||||||||||||||

| (in thousands) | Shares | Amount | Shares | Amount | |||||||||||||||||||

| Tax withholdings for net settlement of equity awards | 599 | $ | 59,613 | 514 | $ | 34,871 | |||||||||||||||||

| Stock repurchase program | 204 | 18,828 | 321 | 20,286 | |||||||||||||||||||

| 803 | $ | 78,441 | 835 | $ | 55,157 | ||||||||||||||||||

During the nine months ended September 30, 2020 and 2019, instead of receiving cash from the equity holders, we withheld shares with a value of $49.5 million and $31.6 million, respectively, for the exercise price of options. These amounts have been excluded from the table above.

Dividends

| Nine Months Ended September 30, | |||||||||||

| (in thousands) | 2020 | 2019 | |||||||||

| Dividend payments to shareholders | $ | 7,206 | $ | 7,105 | |||||||

We currently intend to pay a quarterly cash dividend of $0.03 per share. However, the Board of Directors may terminate or modify the dividend program at any time without prior notice.

23

Contractual obligations

As of September 30, 2020, our contractual obligations were:

| Payments due by period | |||||||||||||||||||||||||||||||||||||||||

| (in thousands) | 2020 | 2021 | 2022-2023 | 2024-2025 | 2026 and thereafter | Other | Total | ||||||||||||||||||||||||||||||||||

Purchase obligations (1) | $ | 21,627 | $ | 56,689 | $ | 61,117 | $ | 173 | $ | — | $ | — | $ | 139,606 | |||||||||||||||||||||||||||

Investment commitments (2) | 300 | 500 | — | — | — | — | 800 | ||||||||||||||||||||||||||||||||||

Liability for uncertain tax positions (3) | — | — | — | — | — | 5,441 | 5,441 | ||||||||||||||||||||||||||||||||||

| Operating lease obligations | 5,490 | 22,887 | 43,888 | 13,187 | 9,959 | — | 95,411 | ||||||||||||||||||||||||||||||||||

| $ | 27,417 | $ | 80,076 | $ | 105,005 | $ | 13,360 | $ | 9,959 | $ | 5,441 | $ | 241,258 | ||||||||||||||||||||||||||||

(1) Represents the fixed or minimum amounts due under purchase obligations for hosting services and sales and marketing programs.

(2) Represents the maximum funding that would be expected under existing venture investment agreements. Our investment agreements generally allow us to withhold unpaid committed funds at our discretion.

(3) We are unable to reasonably estimate the timing of the cash outflow due to uncertainties in the timing of the effective settlement of tax positions.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Market risk represents the risk of loss that may affect us due to adverse changes in financial market prices and rates.

Foreign currency exposure

Translation risk

Our foreign operations’ operating expenses are primarily denominated in foreign currencies. However, our international sales are also primarily denominated in foreign currencies, which partially offsets our foreign currency exposure.

A hypothetical 10% strengthening in the U.S. dollar against other currencies would result in the following impact:

| Nine Months Ended September 30, | |||||||||||

| 2020 | 2019 | ||||||||||

| (Decrease) increase in revenue | (4) | % | (4) | % | |||||||

| (Decrease) increase in net (loss) | (13) | % | (6) | % | |||||||

Remeasurement risk

We experience fluctuations in transaction gains or losses from remeasurement of monetary assets and liabilities denominated in currencies other than the functional currency of the entities in which they are recorded.

We are primarily exposed to changes in foreign currency exchange rates associated with the Australian dollar, Euro, and U.S. dollar-denominated cash and cash equivalents, accounts receivable, unbilled receivables, and intercompany receivables and payables held by our U.K. subsidiary, a British pound functional entity.

A hypothetical 10% strengthening in the British pound exchange rate in comparison to the Australian dollar, Euro, and U.S. dollar would result in the following impact:

| Nine Months Ended September 30, | |||||||||||

| (in thousands) | 2020 | 2019 | |||||||||

| Foreign currency gain (loss) | $ | (6,326) | $ | 1,099 | |||||||

ITEM 4. CONTROLS AND PROCEDURES

(a) Evaluation of disclosure controls and procedures

Our management, with the participation of our Chief Executive Officer (“CEO”) and Chief Financial Officer (“CFO”), evaluated the effectiveness of our disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934, as amended (“Exchange Act”)) as of September 30, 2020. In designing and evaluating our disclosure controls and procedures, our management recognized that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving their objectives, and our management necessarily applied its judgment in evaluating the cost-benefit relationship of possible controls and procedures. Based on this evaluation, our CEO and CFO concluded that our disclosure controls and procedures were effective as of September 30, 2020.

24

(b) Changes in internal control over financial reporting

There have been no changes in our internal control over financial reporting (as defined in Rules 13a-15(f) and 15d-15(f) under the Exchange Act) during the quarter ended September 30, 2020 that have materially affected or are reasonably likely to materially affect our internal control over financial reporting.

COVID-19

In response to COVID-19, we have undertaken measures to protect our employees, partners, and clients, including encouraging employees to work remotely. These changes have compelled us to modify some of our control procedures. However, those changes have so far not been material.

25

PART II - OTHER INFORMATION

ITEM 1A. RISK FACTORS

We encourage you to carefully consider the risk factors identified below and in Item 1A. “Risk Factors” of our Annual Report on Form 10-K for the year ended December 31, 2019, filed with the Securities and Exchange Commission on February 12, 2020. These risk factors could materially affect our business, financial condition, and future results, and they could cause our actual business and financial results to differ materially from those contained in forward-looking statements made in this Quarterly Report on Form 10-Q or elsewhere by management.

Coronavirus (“COVID-19”)