Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 0-20853

ANSYS, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 04-3219960 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

| 275 Technology Drive, Canonsburg, PA | 15317 | |

| (Address of principal executive offices) | (Zip Code) |

724-746-3304

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Common Stock, $.01 par value per share | The NASDAQ Stock Market, LLC | |

| (Title of each class) | (Name of exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by a check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by a check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by a check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by a check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in PART III of this Form 10-K, or any amendment to this Form 10-K. ¨

Indicate by a check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company (as defined in Exchange Act Rule 12b-2). (Check one):

| Large accelerated filer x |

Accelerated filer ¨ | |

| Non-accelerated filer ¨ |

Smaller reporting company ¨ |

Indicate by a check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes ¨ No x

The aggregate market value of the voting stock held by non-affiliates of the Registrant, based upon the closing sale price of the Common Stock on June 30, 2011 as reported on the NASDAQ Global Select Market, was approximately $4,186,000,000. Shares of Common Stock held by each officer and director and by each person who owns 5% or more of the outstanding Common Stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of the Registrant’s Common Stock, par value $.01 per share, outstanding as of February 16, 2012 was 92,780,708 shares.

Documents Incorporated By Reference:

Portions of the Proxy Statement for the Registrant’s 2012 Annual Meeting of Stockholders are incorporated by reference into Part III.

Table of Contents

ANNUAL REPORT ON FORM 10-K FOR FISCAL YEAR 2011

Table of Contents

| PART I |

| |||||

| Item 1. |

3 | |||||

| Item 1A. |

10 | |||||

| Item 1B. |

18 | |||||

| Item 2. |

18 | |||||

| Item 3. |

19 | |||||

| Item 4. |

19 | |||||

| PART II |

| |||||

| Item 5. |

20 | |||||

| Item 6. |

23 | |||||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

24 | ||||

| Item 7A. |

51 | |||||

| Item 8. |

53 | |||||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

54 | ||||

| Item 9A. |

54 | |||||

| Item 9B. |

55 | |||||

| PART III |

| |||||

| Item 10. |

56 | |||||

| Item 11. |

56 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

56 | ||||

| Item 13. |

Certain Relationships and Related Transactions and Director Independence |

56 | ||||

| Item 14. |

56 | |||||

| PART IV |

| |||||

| Item 15. |

57 | |||||

| 88 | ||||||

Table of Contents

Important Factors Regarding Future Results

Information provided by ANSYS, Inc. (hereafter the “Company” or “ANSYS”), in this Annual Report on Form 10-K, may contain forward-looking statements concerning such matters as projected financial performance, market and industry segment growth, product development and commercialization, acquisitions or other aspects of future operations. Such statements, made pursuant to the safe harbor established by the securities laws, are based on the assumptions and expectations of the Company’s management at the time such statements are made. The Company cautions investors that its performance (and, therefore, any forward-looking statement) is subject to risks and uncertainties. Various important factors including, but not limited to, those discussed in Item 1A “Risk Factors,” may cause the Company’s future results to differ materially from those projected in any forward-looking statement. All information presented is as of December 31, 2011, unless otherwise indicated.

PART I

| ITEM 1: | BUSINESS |

ANSYS develops and globally markets engineering simulation software and services widely used by engineers, designers, researchers and students across a broad spectrum of industries and academia, including aerospace, automotive, manufacturing, electronics, biomedical, energy and defense. Headquartered south of Pittsburgh, Pennsylvania, the Company and its subsidiaries employ approximately 2,100 people as of December 31, 2011 and focus on the development of open and flexible solutions that enable users to analyze designs directly on the desktop, providing a common platform for fast, efficient and cost-conscious product development, from design concept to final-stage testing and validation. The Company distributes its ANSYS suite of simulation technologies through a global network of independent resellers and distributors (collectively, channel partners) and direct sales offices in strategic, global locations. It is the Company’s intention to continue to maintain this hybrid sales and distribution model.

On August 1, 2011, the Company completed its acquisition of Apache Design, Inc., a leading simulation software provider for advanced, low-power solutions in the electronics industry. Under the terms of the merger agreement, ANSYS acquired 100% of the outstanding shares of Apache for a purchase price of $314.0 million, which included $31.9 million in acquired cash and short-term investments on Apache’s balance sheet, $3.2 million in ANSYS replacement stock option awards issued to holders of partially-vested Apache stock options and $9.5 million in contingent consideration that is based on the retention of a key member of Apache’s management. The Company funded the transaction entirely with existing cash balances. The complementary combination is expected to accelerate development and delivery of new and innovative products to the marketplace while lowering design and engineering costs for customers.

The Company’s product portfolio consists of the following:

ANSYS WorkbenchTM

ANSYS Workbench is the framework upon which the Company’s suite of advanced engineering simulation technologies is built. The innovative project schematic view ties together the entire simulation process, guiding the user through complex multiphysics analyses with drag-and-drop simplicity. With bi-directional computer-aided design (“CAD”) connectivity, powerful highly-automated meshing, a project-level update mechanism, pervasive parameter management and integrated optimization tools, the ANSYS Workbench platform delivers unprecedented productivity, enabling Simulation Driven Product DevelopmentTM.

Multiphysics

The Company’s multiphysics product suite allows engineers and designers to create virtual prototypes of their designs operating under real-world multiphysics conditions. As the range of need for simulation expands,

3

Table of Contents

companies must be able to accurately predict how complex products will behave in real-world environments, where multiple types of coupled physics interact. ANSYS multiphysics software enables engineers and scientists to simulate the interactions between structural mechanics, heat transfer, fluid flow and electromagnetics all within a single, unified engineering simulation environment.

Structural Mechanics

The Company’s structural mechanics product suite offers simulation tools for product design and optimization that increase productivity, minimize physical prototyping and help to deliver better and innovative products in less time. These tools tackle real-world analysis problems by making product development less costly and more reliable. In addition, these tools have capabilities that cover a broad range of analysis types, elements, contacts, materials, equation solvers and coupled physics capabilities all targeted toward understanding and solving complex design problems.

Fluid Dynamics

The Company’s fluid dynamics product suite offers modeling of fluid flow and other related physical phenomena. Fluid flow analysis capabilities provide all the tools needed to design and optimize new fluids equipment and to troubleshoot already existing installations. The fluid dynamics product suite contains general-purpose computational fluid dynamics software and specialized products to address specific industry applications.

Explicit Dynamics

The Company’s explicit dynamics product suite simulates events involving short-duration, large-strain, large-deformation, fracture, complete material failure or structural problems with complex interactions. This product suite is ideal for simulating physical events that occur in a short period of time and may result in material damage or failure. Such events are often difficult or expensive to study experimentally.

Electromagnetics

The Company’s electromagnetics product suite provides field simulation software for designing high-performance electronic and electromechanical products. The software streamlines the design process and predicts performance - all prior to building a prototype - of mobile communication and internet-access devices, broadband networking components and systems, integrated circuits (“IC”) and printed circuit boards (“PCB”), as well as electromechanical systems such as automotive components and power electronics equipment.

System Simulation

The Company delivers the unique ability to perform complete simulation studies as a “system” for some of the most modern and complex product designs. This is accomplished through a complete set of physics solutions that are integrated into a multiphysics capabilities set. A collaborative simulation environment provides modeling scalability specifically for evaluating entire systems, including 3-D high-fidelity models, multibody dynamics, circuit reduced-order models, and any combination of these. These technologies provide a complete view into predicted product performance, which creates greater design confidence for engineers.

Simulation Process and Data Management

ANSYS Engineering Knowledge ManagerTM (“ANSYS EKM”) is a comprehensive solution for simulation-based process and data management challenges. ANSYS EKM provides solutions and benefits to all levels of a company, enabling an organization to address the critical issues associated with simulation data, including backup and archival, traceability and audit trail, process automation, collaboration and capture of engineering expertise, and intellectual property protection.

4

Table of Contents

Academic

The Company’s academic product suite provides a highly scalable portfolio of academic products based on several usage tiers: associate, research and teaching. Each tier includes various noncommercial products that bundle a broad range of physics and advanced coupled field solver capabilities. The academic product suite provides entry-level tools intended for class demonstrations and hands-on instruction. It provides flexible terms of use and more complex analysis suitable for doctoral and post-doctoral research projects. The Company also provides a low-cost, problem-size-limited product suitable for student use at home.

High-Performance Computing

The Company’s high-performance computing (“HPC”) product suite enables enhanced insight into product performance and improves the productivity of the design process. The HPC product suite delivers cross-physics parallel processing capabilities for the full spectrum of the Company’s simulation software by supporting structural, fluids, thermal and electromagnetic simulations in a single HPC solution. This product suite decreases the turnaround time for individual simulations, allowing users to consider multiple design ideas and make the right design decisions early in the design cycle.

Geometry Interfaces

The Company offers comprehensive geometry handling solutions for engineering simulation in an integrated environment with direct interfaces to all major CAD systems, support of additional readers and translators, and an integrated geometry modeler exclusively focused on analysis.

Meshing

Creating a mesh that transforms a physical model into a mathematical model is a critical and foundational step in almost every engineering simulation study. Accurate meshing is especially challenging today with increasing product design complexity and heightened expectations of product performance. The Company’s meshing technology provides a means to balance these requirements, obtaining the right mesh for each simulation in the most automated way possible. The technology is built on the strengths of world-class leading algorithms; these are integrated in a single environment to produce the most robust and reliable meshing available.

Apache Design Low-Power Electronic Solutions

The Company’s suite of Apache software delivers power analysis and optimization platforms along with comprehensive and integrated methodologies that provide capabilities for managing the power budget, power delivery integrity, and power-induced noise in an electronic design, from initial prototyping to system sign-off. These solutions deliver accuracy with correlation to silicon measurement; the capacity to handle an entire electronic system including IC, package, and PCB; efficiency for ease-of-debug and fast turnaround time; and comprehensiveness to facilitate cross-domain communications and electronic ecosystem enablement.

PRODUCT DEVELOPMENT

The Company makes significant investments in research and development and emphasizes accelerated new integrated product releases. The Company’s product development strategy centers on ongoing development and innovation of new technologies to increase productivity and to provide engineering simulation solutions that customers can integrate into enterprise-wide product lifecycle management systems. The Company’s product development efforts focus on extensions of the full product line with new functional modules, further integration with CAD, electronic CAD (“ECAD”), product lifecycle management (“PLM”) products and the development of new products. The Company’s products run on the most widely used engineering computing platforms and operating systems, including Windows, Linux and most UNIX workstations.

5

Table of Contents

During 2011, the Company completed the following major product development activities and releases:

| • | The release of version 14.0 of ANSYS® software, which includes new, advanced features that make it easier, faster and less costly for organizations to bring new products to market. The software automates many user-intensive operations, which helps product developers minimize time spent setting up problems. The release also allows engineers to simulate product complexities such as state changes, nonlinear phenomena and multiphysics interactions as they exist in the real world, from a single component to entire systems. The release capitalizes on modern hardware advancements to deliver complex simulation calculations faster than other alternatives on the market today. |

| • | The release of Apache’s RTL Power Model (RPMTM), which is designed to optimize a wide range of power-sensitive applications, such as ultra-low-power electronics. RPM bridges the power gap from register-transfer-language (“RTL”) design to physical implementation. The new technology accurately predicts IC power behavior at the RTL level with consideration for how the design is physically implemented. As a result, the technology helps to enable chip power delivery network and IC package design decisions early in the design process, as well as to ensure chip power integrity sign-off. |

The Company’s total research and development expenses were $108.5 million, $89.0 million and $79.9 million in 2011, 2010 and 2009, respectively, or 15.7%, 15.3% and 15.4% of total revenue, respectively. As of December 31, 2011, the Company’s product development staff consisted of approximately 730 full-time employees, most of whom hold advanced degrees and have industry experience in engineering, mathematics, computer science or related disciplines. The Company has traditionally invested significant resources in research and development activities and intends to continue to make investments in this area, particularly as it relates to expanding the capabilities of its flagship products and other products within its broad portfolio of simulation software, evolution of its ANSYS® WorkbenchTM platform, HPC capabilities and ongoing integration.

PRODUCT QUALITY

The Company’s employees generally perform product development tasks according to predefined quality plans, procedures and work instructions. Certain technical support tasks are also subject to a quality process. These plans define for each project the methods to be used, the responsibilities of project participants and the quality objectives to be met. The majority of software products are developed under a quality system that is certified to the ISO 9001:2008 standard. The Company establishes quality plans for its products and services, and subjects product designs to multiple levels of testing and verification in accordance with processes established under the Company’s quality system.

SALES AND MARKETING

The Company distributes and supports its products through a global network of independent channel partners, as well as through its own direct sales offices. This network provides the Company with a cost-effective, highly specialized channel of distribution and technical support. It also enables the Company to draw on business and technical expertise from a global network, provides relative stability to the Company’s operations to offset geography-specific economic trends and provides the Company with an opportunity to take advantage of new geographic markets. Approximately 26% in 2011, 27% in 2010 and 26% in 2009 of the Company’s total revenue was derived through the indirect sales channel.

The channel partners sell ANSYS products to new customers, expand installations within the existing customer base, offer training and consulting services, and provide the first line of ANSYS technical support. The Company’s channel partner certification process helps to ensure that each channel partner has the ongoing capability to adequately represent the Company’s expanding product lines and to provide an acceptable level of training, consultation and customer support.

6

Table of Contents

The Company also has a direct sales management organization in place to develop an enterprise-wide, focused sales approach and to implement a worldwide major account strategy. The sales management organization also functions as a focal point for requests to ANSYS from the channel partners and provides additional support in strategic locations through the presence of direct sales offices. A Vice President of Worldwide Sales and Support heads the Company’s sales management organization.

During 2011, the Company continued to invest in its existing domestic and international strategic sales offices. In total, the Company’s direct sales offices employ approximately 1,050 full-time employees who are responsible for the sales, technical support, engineering consulting services, marketing initiatives and administrative activities designed to support the Company’s overall revenue growth and expansion strategies.

The Company’s products are utilized by organizations ranging in size from small consulting firms to the world’s largest industrial companies. No single customer accounted for more than 5% of the Company’s revenue in 2011, 2010 or 2009.

Information with respect to foreign and domestic revenue may be found in Note 17 to the consolidated financial statements in Part IV, Item 15 of this Annual Report on Form 10-K and in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 of this Annual Report on Form 10-K.

STRATEGIC ALLIANCES AND MARKETING RELATIONSHIPS

The Company has established and continues to pursue strategic alliances with advanced technology suppliers, and marketing relationships with hardware vendors, specialized application developers, and CAD, ECAD and PLM providers. The Company believes that these relationships facilitate accelerated incorporation of advanced technology into the Company’s products, provide access to new customers, expand the Company’s sales channels, develop specialized product applications and provide direct integration with leading CAD, electronic design automation (“EDA”), product data management and PLM systems.

The Company has technical and marketing relationships with leading CAD vendors, such as Autodesk, Dassault Systèmes, Parametric Technology Corporation and Siemens Product Lifecycle Management Software Inc., to provide direct links between products. These links facilitate the transfer of electronic data models between the CAD systems and ANSYS products. In addition, the Company has an agreement with Dassault Systèmes under which ANSYS fluid flow modeling technology is embedded in the CATIA V5 product lifecycle management environment. This fully integrated product, FLUENT for CATIA V5, enables model building, computation, post-processing and data management within the analysis infrastructure of CATIA V5.

Similarly, the Company maintains marketing and software development relationships with leading EDA software companies, including Cadence, Synopsys and Mentor Graphics. These relationships support transfer of data between electronics design and layout packages and the ANSYS electronics simulation portfolio.

The Company has established relationships with leading suppliers of computer hardware, including Intel, AMD, Microsoft, NVIDIA, Hewlett-Packard, IBM, Dell, Cray, QLogic, Mellanox, Platform Computing and other leading regional resellers and system integrators. These relationships provide the Company with joint marketing opportunities, such as advertising, public relations, editorial coverage and customer events. In addition, these alliances provide the Company with early access and technical collaboration on new and emerging computing technologies, ensuring that the Company’s software products are certified to run effectively on the most current hardware platforms. Key 2011 milestones included software tuning for the latest Intel processors, resulting in significant performance boosts, and extension of support for computations using General-Purpose Graphical Processing Units.

7

Table of Contents

The Company’s Enhanced Solution Partner Program actively encourages specialized developers of software solutions to use the Company’s technology as a development platform for their applications and provides customers with enhanced functionality related to their use of the Company’s software. With over 100 active enhanced solution partnerships, spanning a wide range of technologies, including electronics, mechanical simulation, fluid simulation, acoustics, turbomachinery and CAD, this partner ecosystem extends the depth and breadth of the Company’s technology offerings. During 2011, the Company extended its ecosystem of Workbench integrated partner solutions, working with FE-Design, Safe Technology, EVEN AG, RBF Morph, VCollab, and e-XStream.

The Company has a software license agreement with Livermore Software Technology Corporation (“LSTC”) whereby LSTC has provided LS-DYNA software for explicit dynamics solutions used in applications such as crash test simulations in automotive and other industries. Under this arrangement, LSTC assists in the integration of the LS-DYNA software with the Company’s pre- and post-processing capabilities and provides updates and problem resolution in return for royalties from sales of the ANSYS/LS-DYNA combined product.

The Company also has a software license agreement with HBM that provides the advanced fatigue capabilities of nCode DesignLifeTM, a leading durability software from HBM. ANSYS® nCode DesignLife technology leverages the open architecture of the ANSYS platform and enables mechanical engineers to more easily address complex product life and durability issues, all before a prototype is ever built. During 2011, customer events and “ask the expert” sessions were conducted with focus on the Workbench-integrated nCode DesignLife offering.

COMPETITION

The Company believes that the principal factors affecting sales of its software include ease of use, breadth and depth of functionality, flexibility, quality, ease of integration with other software systems, file compatibility across computer platforms, range of supported computer platforms, performance, price and total cost of ownership, customer service and support, company reputation and financial viability, and effectiveness of sales and marketing efforts.

The Company continues to experience competition across all markets for its products and services. Some of the Company’s current and possible future competitors have greater financial, technical, marketing and other resources than the Company, and some have well established relationships with current and potential customers of the Company. The Company’s current and possible future competitors also include firms that have or may in the future elect to compete by means of open source licensing. These competitive pressures may result in decreased sales volumes, price reductions and/or increased operating costs, and could result in lower revenues, margins and net income.

PROPRIETARY RIGHTS AND LICENSES

The Company regards its software as proprietary and relies on a combination of trade secret, copyright, patent and trademark laws; license agreements; nondisclosure and other contractual provisions; and technical measures to protect its proprietary rights in its products. The Company distributes its software products under software license agreements that grant customers nonexclusive licenses, which are typically nontransferable, for the use of the Company’s products. License agreements for the Company’s products are directly between the Company and end users. Use of the licensed software product is restricted to specified sites unless the customer obtains a multi-site license for its use of the software product. Software security measures are also employed to prevent unauthorized use of the Company’s software products and the licensed software is subject to terms and conditions prohibiting unauthorized reproduction. Customers may purchase a perpetual license of the technology with the right to annually purchase ongoing maintenance, technical support and upgrades, or may lease the product on a fixed-term basis for a fee that includes the license, maintenance, technical support and upgrades.

8

Table of Contents

The Company licenses its software products utilizing a combination of web-based and hard copy license terms and forms. For certain software products, the Company primarily relies on “click-wrapped” licenses. The enforceability of these types of agreements under the laws of some jurisdictions is uncertain.

The Company also seeks to protect the source code of its software as a trade secret and as unpublished copyrighted work. The Company has obtained federal trademark registration protection for ANSYS and other marks in the U.S. and in foreign countries. Additionally, the Company was awarded numerous patents by the U.S. Patent and Trademark Office, and has a number of patent applications pending. The Company does not always choose to seek patent protection for its intellectual property, as the process of obtaining patent protection is expensive and time consuming. As a result, the Company relies on the protection of its source code as a trade secret.

Employees of the Company have signed agreements under which they have agreed not to disclose trade secrets or confidential information and, where legally permitted, that restrict engagement in or connection with any business that is competitive with the Company anywhere in the world while employed by the Company (and, in some cases, for specified periods thereafter), and that any products or technology created by them during their term of employment are the property of the Company. In addition, the Company requires all channel partners to enter into agreements not to disclose the Company’s trade secrets and other proprietary information.

Despite these precautions, there can be no assurance that misappropriation of the Company’s technology and proprietary information will not occur. Further, there can be no assurance that copyright, trademark, patent and trade secret protection will be available for the Company’s products in certain jurisdictions, or that restrictions on the ability of employees and channel partners to engage in activities competitive with the Company will be enforceable. Costly and time-consuming litigation could be necessary in the future to enforce the Company’s rights to its trade secrets and proprietary information or to enforce its patent rights, and it is possible that in the future the Company’s competitors may be able to obtain our trade secrets or to independently develop unpatented technology similar to ours.

The software development industry is characterized by rapid technological change. Therefore, the Company believes that factors such as the technological and creative skills of its personnel, new product developments, frequent product enhancements, name recognition and reliable product maintenance are also important to establishing and maintaining technology leadership in addition to the various legal protections of its technology that may be available.

The Company does not believe that any of its products infringe upon the proprietary rights of third parties. There can be no assurance, however, that third parties will not claim such infringement by the Company or its licensors or licensees with respect to current or future products. The Company expects that software suppliers will increasingly be subject to the risk of such claims as the number of products and suppliers continues to expand and the functionality of products continues to increase. Any such claims, with or without merit, could be time consuming, result in costly litigation, cause product shipment delays or require the Company to enter into royalty or licensing agreements. Such royalty or licensing agreements, if required, may not be available on terms acceptable to the Company.

SEASONAL VARIATIONS

The Company’s business has experienced seasonality, including quarterly reductions in software sales resulting from the slowdown during the summer months, particularly in Europe, as well as from the seasonal purchasing and budgeting patterns of the Company’s global customers. The Company’s revenue is typically highest in the fourth quarter.

9

Table of Contents

BACKLOG

As a result of the timing of the Company’s invoicing with respect to its acceptance of an order and execution of a software license agreement, the Company has historically had an insignificant order backlog. Due to the August 1, 2011 acquisition of Apache, which has different billing arrangements with customers than those historically used by the Company, there is a backlog of $56.3 million of orders received but not invoiced as of December 31, 2011.

EMPLOYEES

As of December 31, 2011, the Company and its subsidiaries had approximately 2,100 full-time employees. At that date, there were also contract personnel and co-op students providing ongoing development services and technical support. The Company believes that its relationship with its employees is good.

AVAILABLE INFORMATION

The Company’s website is www.ansys.com. The Company makes available on its website, free of charge, Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, reports filed pursuant to Section 16 and amendments to those reports as soon as reasonably practicable after such materials are electronically filed or furnished to the Securities and Exchange Commission. In addition, the Company has posted the charters for its Audit Committee, Compensation Committee, Nominating and Corporate Governance Committee, and Strategy Committee, as well as the Company’s Code of Business Conduct and Ethics, Standard Business Practices and Corporate Governance Guidelines on its website. Information posted on the Company’s website is not incorporated by reference in this Annual Report on Form 10-K.

| ITEM 1A: | RISK FACTORS |

Information provided by the Company or its spokespersons, including information contained in this Annual Report on Form 10-K, may from time to time contain forward-looking statements concerning projected financial performance, market and industry sector growth, product development and commercialization or other aspects of future operations. Such statements will be based on the assumptions and expectations of the Company’s management at the time such statements are made. The Company cautions investors that its performance (and, therefore, any forward-looking statement) is subject to risks and uncertainties. Various important factors including, but not limited to, the following may cause the Company’s future results to differ materially from those projected in any forward-looking statement.

Volatility in the Global Economy and Disruption in Financial Markets. The financial markets in certain geographies continue to experience disruption, including, among other things, volatility in securities prices, diminished liquidity and credit availability, rating downgrades of certain investments and declining valuations of others. While currently these conditions have not impaired the Company’s ability to access credit markets and finance operations, there can be no assurance that there will not be continued instability in, or renewed deterioration of financial markets and confidence in major economies. The Company is impacted by these economic developments, both domestically and globally, in that the current tightening of credit in certain financial markets adversely affects the ability of its customers and suppliers to obtain financing for significant purchases and operations, and could result in a decrease in orders for the Company’s products and services. These economic conditions may negatively impact the Company as some of its customers defer purchasing decisions, thereby lengthening the Company’s sales cycles. In addition, certain of the Company’s customers’ budgets may be constrained and they may be unable to purchase the Company’s products at the same level. The Company’s customers’ ability to pay for the Company’s products and services may also be impaired, which may lead to an increase in the Company’s allowance for doubtful accounts and write-offs of accounts receivable. The Company is unable to predict the likely duration and severity of the current economic conditions. Should these economic conditions result in the Company not meeting its revenue growth objectives, the Company’s operating results, cash flows and financial condition could be adversely affected.

10

Table of Contents

Decline in Customers’ Business. The Company’s sales are based significantly on end user demand for products in key industrial sectors. Many of these sectors periodically experience economic declines, which may be exacerbated by other economic factors, including the recent global economic disruptions. These factors may adversely affect the Company’s business by extending sales cycles and reducing revenue. These economic factors may cause the Company’s customers to reduce the size of their workforce or cut back on operations and may lead to a reduction in license renewals or ongoing maintenance contracts with the Company. The Company’s customers may also request discounts or extended payment terms on new products or seek to extend payment terms on existing contracts, all of which may cause fluctuations in the Company’s future operating results. The Company may not be able to adjust its operating expenses to offset such fluctuations because a substantial portion of the Company’s operating expenses is related to personnel, facilities and marketing programs. The level of personnel and related expenses may not be able to be adjusted quickly and is based, in significant part, on the Company’s expectation for future revenue.

Risks Associated with International Activities. A majority of the Company’s business comes from outside the United States and the Company has customers that supply a wide spectrum of goods and services in virtually all of the world’s major economic regions. As the Company continues to expand its sales presence in international regions, the portion of its revenue, expenses, cash, accounts receivable and payment obligations denominated in foreign currencies continues to increase. The Company’s revenues and operating results are adversely affected when the U.S. Dollar strengthens relative to other currencies and are positively affected when the U.S. Dollar weakens. As a result, changes in currency exchange rates will affect the Company’s financial position, results of operations and cash flows. In the event that there are economic declines in countries in which the Company conducts transactions, the resulting changes in currency exchange rates may affect the Company’s financial position, results of operations and cash flows. The Company is most impacted by movements in and among the British Pound, Euro, Japanese Yen, Canadian Dollar, Indian Rupee, Swedish Krona, Chinese Renminbi, Korean Won, Taiwan Dollar and the U.S. Dollar. The Company seeks to reduce these risks primarily through its normal operating and treasury activities, but there can be no assurance that it will be successful in reducing these risks.

Additional risks inherent in the Company’s international business activities include imposition of government controls; export license requirements; restrictions on the export of critical technology, products and services; political and economic instability; trade restrictions; changes in tariffs and taxes; difficulties in staffing and managing international operations; longer accounts receivable payment cycles; and the burdens of complying with a wide variety of foreign laws and regulations. Effective patent, copyright, trademark and trade secret protection may not be available in every foreign country in which the Company sells its products and services. The Company’s business, financial position, results of operations and cash flows could be materially, adversely affected by any of these risks.

Stock Market and Stock Price Volatility. Market prices for securities of software companies have generally been volatile. In particular, the market price of the Company’s common stock has been, and may continue to be, subject to significant fluctuations as a result of factors affecting the Company, the software industry or the securities markets in general. Such factors include, but are not limited to, declines in trading price that may be triggered by the Company’s failure to meet the expectations of securities analysts and investors. Moreover, the trading price could be subject to additional fluctuations in response to quarter-to-quarter variations in the Company’s operating results, material announcements made by the Company or its competitors, conditions in the financial markets or the software industry generally or other events and factors, many of which are beyond the Company’s control.

Rapidly Changing Technology; New Products; Risk of Product Defects. The Company operates in an industry generally characterized by rapidly changing technology and frequent new product introductions, which can render existing products obsolete or unmarketable. A major factor in the Company’s future success will be its ability to anticipate technological changes and to develop and introduce, in a timely manner, enhancements to its existing products, products acquired in acquisitions and new products to meet those changes. If the Company is

11

Table of Contents

unable to introduce new products and to respond quickly to industry changes, its business, financial position, results of operations and cash flows could be materially, adversely affected.

The introduction and marketing of new or enhanced products require the Company to manage the transition from existing products in order to minimize disruption in customer purchasing patterns. There can be no assurance that the Company will be successful in developing and marketing, on a timely basis, new products or product enhancements, that its new products will adequately address the changing needs of the marketplace or that it will successfully manage the transition from existing products. Software products as complex as those offered by the Company may contain undetected errors or failures when first introduced, or as new versions are released, and the likelihood of errors is increased as a result of the Company’s commitment to the frequency of its product releases. There can be no assurance that errors will not be found in any new or enhanced products after commencement of commercial shipments. Certain of these products require a higher level of sales and support expertise. The ability of the Company’s sales channel, particularly the indirect channel, to obtain this expertise and to sell the new product offerings effectively could have an adverse impact on the Company’s sales in future periods. Any of these problems may result in the loss of or delay in customer acceptance, diversion of development resources, damage to the Company’s reputation, or increased service and warranty costs, any of which could have a material, adverse effect on the Company’s business, financial position, results of operations and cash flows.

Competition. The Company continues to experience competition across all markets for its products and services. Some of the Company’s current and possible future competitors have greater financial, technical, marketing and other resources than the Company, and some have well established relationships with current and potential customers of the Company. The Company’s current and possible future competitors also include firms that have or may in the future elect to compete by means of open source licensing. These competitive pressures may result in decreased sales volumes, price reductions and/or increased operating costs, and could result in lower revenues, margins and net income.

Changes in the Company’s Pricing Models. The intense competition the Company faces in the sales of its products and services, and general economic and business conditions, can put pressure on the Company to adjust its prices. If the Company’s competitors offer deep discounts on certain products or services, or develop products that the marketplace considers more valuable, the Company may need to lower prices or offer other favorable terms in order to compete successfully. Any such changes may reduce operating margins and could adversely affect operating results. The Company’s software license updates and product support fees are generally priced as a percentage of its net new software license fees. The Company’s competitors may offer lower percentage pricing on product updates and support, that could put pressure on the Company to further discount its new license prices.

Any broad-based change to the Company’s prices and pricing policies could cause new software license and service revenues to decline or be delayed as its sales force implements and its customers adjust to the new pricing policies. Some of the Company’s competitors may bundle software products for promotional purposes or as a long-term pricing strategy or provide guarantees of prices and product implementations. These practices could, over time, significantly constrain the prices that the Company can charge for certain of its products. If the Company does not adapt its pricing models to reflect changes in customer use of its products or changes in customer demand, the Company’s new software license revenues could decrease. Additionally, increased distribution of applications through application service providers, including software-as-a-service providers, may reduce the average price for the Company’s products or adversely affect other sales of the Company’s products, reducing new software license revenues unless the Company can offset price reductions with volume increases. The increase in open source software distribution may also cause the Company to adjust its pricing models.

Dependence on Senior Management and Key Technical Personnel. The Company’s success depends upon the continued services of the Company’s senior executives, key technical employees and other employees. Each of the Company’s executive officers, key technical personnel and other employees could terminate his or her

12

Table of Contents

relationship with the Company at any time. The loss of any of the Company’s senior executives might significantly delay or prevent the achievement of the Company’s business objectives and could materially harm the Company’s business and customer relationships. In addition, because of the highly technical nature of the Company’s products, the loss of any significant number of existing engineering and development personnel could have a material, adverse effect on the Company’s business and operating results.

Dependence on Proprietary Technology. The Company’s success is highly dependent upon its proprietary technology. The Company generally relies on contracts and the laws of copyright, patents, trademarks and trade secrets to protect its technology. The Company maintains a trade secrets program, enters into confidentiality agreements with its employees and channel partners, and limits access to and distribution of its software, documentation and other proprietary information. There can be no assurance that the steps taken by the Company to protect its proprietary technology will be adequate to prevent misappropriation of its technology by third parties, or that third parties will not be able to develop similar technology independently. Costly and time-consuming litigation could be necessary to enforce and determine the scope of our trade secret rights and related confidentiality and nondisclosure provisions. Although the Company is not aware that any of its technology infringes upon the rights of third parties, there can be no assurance that other parties will not assert technology infringement claims against the Company or that, if asserted, such claims will not prevail.

Dependence on Channel Partners. The Company continues to distribute a meaningful portion of its products through its global network of independent, regional channel partners. The channel partners sell the Company’s software products to new and existing customers, expand installations within the existing customer base, offer consulting services and provide the first line of technical support. Consequently, in certain geographies, the Company is highly dependent upon the efforts of the channel partners. Difficulties in ongoing relationships with channel partners, such as failure to meet performance criteria or to promote the Company’s products as aggressively as the Company expects, and differences in the handling of customer relationships, could adversely affect the Company’s performance. Additionally, the loss of any major channel partner for any reason, including a channel partner’s decision to sell competing products rather than the Company’s products, could have a material, adverse effect on the Company. Moreover, the Company’s future success will depend substantially on the ability and willingness of its channel partners to continue to dedicate the resources necessary to promote the Company’s portfolio of products and to support a larger installed base of the Company’s products. If the channel partners are unable or unwilling to do so, the Company may be unable to sustain revenue growth.

During times of significant fluctuations in world currencies, certain channel partners may have solvency issues to the extent that effective hedge transactions are not employed or there is not sufficient working capital. In particular, if the U.S. Dollar strengthens relative to other currencies, certain channel partners who pay the Company in U.S. Dollars may have trouble paying the Company on time or may have trouble distributing the Company’s products due to the impact of the currency exchange fluctuation on such channel partner’s cash flows. This may impact the Company’s ability to distribute its products into certain regions and markets, and may have an adverse effect on the Company’s results of operations and cash flows.

Reliance on Perpetual Licenses. Although the Company has historically maintained stable recurring revenue from the sale of software lease licenses and software maintenance subscriptions, it also has relied on sales of perpetual licenses that involve payment of a single, up-front fee and that are more typical in the computer software industry. While revenue generated from software lease licenses and software maintenance subscriptions currently represents a portion of the Company’s revenue, to the extent that perpetual license revenue continues to represent a significant percentage of total revenue, the Company’s revenue in any period will depend increasingly on sales completed during that period.

Risks Associated with Acquisitions. Historically, the Company has consummated acquisitions in order to support the Company’s long-term strategic direction, accelerate innovation, provide increased capabilities to its existing products, supply new products and services, expand its customer base and enhance its distribution channels. In the future, the Company may not be able to identify suitable acquisition candidates or, if suitable

13

Table of Contents

candidates are identified, the Company may not be able to complete the business combination on commercially acceptable terms. The process of exploring and pursuing acquisition opportunities may result in devotion of significant management and financial resources.

Even if the Company is able to consummate acquisitions that it believes will be successful, such transactions present many risks. Significant risks to such acquisitions include, among others: failing to achieve anticipated synergies and revenue increases; difficulty incorporating and integrating the acquired technologies or products with the Company’s existing product lines; difficulty in coordinating, establishing or expanding sales, distribution and marketing functions, as necessary; disruption of the Company’s ongoing business and diversion of management’s attention to transition or integration issues; unanticipated and unknown liabilities; the loss of key employees, customers, partners and channel partners of the Company or of the acquired company; and difficulties implementing and maintaining sufficient controls, policies and procedures over the systems, products and processes of the acquired company. If the Company does not achieve the anticipated benefits of its acquisitions as rapidly or to the extent anticipated by the Company’s management and financial or industry analysts, or if others do not perceive the same benefits of the acquisition as the Company, there could be a material, adverse effect on the Company’s stock price, business, financial position, results of operations or cash flows.

In addition, for companies acquired, limited experience will exist for several quarters following the acquisition relating to how the acquired company’s sales pipelines will convert into sales or revenues and the conversion rate post-acquisition may be quite different than the historical conversion rate. Because a substantial portion of the Company’s sales are completed in the latter part of a quarter, and its cost structure is largely fixed in the short term, revenue shortfalls may have a negative impact on the Company’s profitability. A delay in a small number of large, new software license transactions could cause the Company’s quarterly software license revenues to fall significantly short of its predictions.

Risks Associated with the Apache Acquisition. On August 1, 2011, the Company completed its acquisition of Apache Design, Inc., a leading simulation software provider for advanced, low-power solutions in the electronics industry. Under the terms of the merger agreement, ANSYS acquired 100% of the outstanding shares of Apache for a purchase price of $314.0 million, which included $31.9 million in acquired cash and short-term investments on Apache’s balance sheet, $3.2 million in ANSYS replacement stock option awards issued to holders of partially-vested Apache stock options and $9.5 million in contingent consideration that is based on the retention of a key member of Apache’s management. While the acquisition of Apache is expected to accelerate development and delivery of new and innovative products to the marketplace while lowering design and engineering costs for customers, the Company will need to meet significant challenges to realize the expected benefits and synergies of the acquisition. These challenges include:

| • | Integrating the management teams, strategies, cultures and operations of the two companies. |

| • | Retaining and assimilating the key personnel of each company. |

| • | Integrating sales and business development operations. |

| • | Retaining existing customers of each company. |

| • | Developing new products and services that utilize the technologies and resources of both companies. |

| • | Creating uniform standards, controls, procedures, policies and information systems. |

| • | Realizing the anticipated cost savings in the combined company. |

| • | Combining the businesses of the Company and Apache in a manner that does not materially disrupt Apache’s existing customer relationships nor otherwise result in decreased revenues and that allows the Company to capitalize on Apache’s growth opportunities. |

14

Table of Contents

The accomplishment of these post-acquisition objectives will involve considerable risks, including:

| • | The loss of key employees that are critical to the successful integration and future operations of the companies. |

| • | The potential disruption of each company’s ongoing business and distraction of their respective management teams. |

| • | The difficulty of incorporating acquired technology and rights into the Company’s products and services. |

| • | Unanticipated expenses related to technology integration. |

| • | Potential disruptions in each company’s operations, loss of existing customers, loss of key information, expertise or know-how, and unanticipated additional recruitment and training costs. |

| • | Possible inconsistencies in standards, controls, procedures and policies that could adversely affect the Company’s ability to maintain relationships with customers and employees or to achieve the anticipated benefits of the acquisition. |

| • | Potential unknown liabilities associated with the acquisition. |

The market price of the Company’s common stock may decline as a result of the acquisition for a number of reasons, including:

| • | The integration of Apache by the Company may be unsuccessful. |

| • | The Company may not achieve the perceived benefits of the acquisition as rapidly as, or to the extent, anticipated by financial or industry analysts. |

| • | The effect of the acquisition on the Company’s financial results may not be consistent with the expectations of financial or industry analysts. |

If the Company does not succeed in addressing these challenges or any other problems encountered in connection with the acquisition, its operating results and financial condition could be adversely affected.

The Company continues to believe that the acquisition of Apache will be accretive to non-GAAP earnings within the first year following the acquisition. The Company’s ability to realize this goal will depend on meeting many of the challenges outlined above. In the event that Apache is not accretive within the first year following the acquisition, or to the extent anticipated by the Company’s management and financial or industry analysts, it may have an adverse effect on the Company’s business, financial position and reputation.

Disruption of Operations or Infrastructure Failures. A significant portion of the Company’s software development personnel, source code and computer equipment is located at operating facilities in the United States, Canada, India, Japan and throughout Europe. The occurrence of a natural disaster or other unforeseen catastrophe at any of these facilities could cause interruptions in the Company’s operations, services and product development activities. Additionally, if the Company experiences problems that impair its business infrastructure, such as a computer virus, telephone system failure or an intentional disruption of its information technology systems by a third party, these interruptions could have a material, adverse effect on the Company’s business, financial position, results of operations, cash flows and the ability to meet financial reporting timelines. Further, because the Company’s sales are not generally linear during any quarterly period, the potential adverse effects resulting from any of the events described above or any other disruption of the Company’s business could be accentuated if it occurs close to the end of a fiscal quarter.

Sales Forecasts. The Company makes many operational and strategic decisions based upon short- and long-term sales forecasts. The Company’s sales personnel continually monitor the status of all proposals, including the estimated closing date and the value of the sale, in order to forecast quarterly sales. These forecasts are subject to

15

Table of Contents

significant estimation and are impacted by many external factors, including global economic conditions and the performance of the Company’s customers. A variation in actual sales activity from that forecasted could cause the Company to plan or to budget incorrectly and, therefore, could adversely affect the Company’s business, financial position, results of operations and cash flows. The Company’s management team forecasts macroeconomic trends and developments, and integrates them through long-range planning into budgets, research and development strategies and a wide variety of general management duties. Global economic conditions, and the effect those conditions and other disruptions in global markets have on the Company’s customers, may have a significant impact on the accuracy of the Company’s sales forecasts. These conditions may increase the likelihood or the magnitude of variations between actual sales activity and the Company’s sales forecasts and, as a result, the Company’s performance may be hindered because of a failure to properly match corporate strategy with economic conditions. This, in turn, may adversely affect the Company’s business, financial position, results of operations and cash flows.

Risks Associated with Significant Sales to Existing Customers. A significant portion of the Company’s sales include follow-on sales to existing customers that invest in the Company’s broad suite of engineering simulation software and services. If a significant number of current customers were to become dissatisfied with the Company’s products and services, or choose to license or utilize competitive offerings, the Company’s follow-on sales, and recurring lease and maintenance revenues, could be materially, adversely impacted, resulting in reduced revenue, operating margins, net income and cash flows.

Renewal Rates for Annual Lease and Maintenance Contracts. A substantial portion of the Company’s license and maintenance revenue is derived from annual lease and maintenance contracts. These contracts are generally renewed on an annual basis and typically have a high rate of customer renewal. In addition to the recurring revenue base associated with these contracts, a majority of customers purchasing new perpetual licenses also purchase related annual maintenance contracts. If the rate of renewal for these contracts is adversely affected by economic or other factors, the Company’s license and maintenance growth will be adversely affected over the term that the revenue for those contracts would have otherwise been recognized. As a result, the Company’s business, financial position, results of operations and cash flows may also be adversely impacted during those periods.

Income Tax Estimates. The Company makes significant estimates in determining its worldwide income tax provision. These estimates involve complex tax regulations in a number of jurisdictions across the Company’s global operations and are subject to many transactions and calculations in which the ultimate tax outcome is uncertain. The final outcome of tax matters could be different than the estimates reflected in the historical income tax provision and related accruals. Such differences could have a material impact on income tax expense and net income in the periods in which such determinations are made.

The amount of income tax paid by the Company is subject to ongoing audits by federal, state and foreign tax authorities. These audits can often result in additional assessments, including interest and penalties. The Company’s estimate for liabilities associated with uncertain tax positions is highly judgmental and actual future outcomes may result in favorable or unfavorable adjustments to the Company’s estimated tax liabilities, including estimates for uncertain tax positions, in the period the assessments are made or resolved, audits are closed or when statutes of limitations on potential assessments expire. As a result, the Company’s effective tax rate may fluctuate significantly on a quarterly or annual basis.

The Company allocates a portion of its purchase price to goodwill and intangible assets. Impairment charges associated with goodwill are generally not tax deductible and will result in an increased effective income tax rate in the period the impairment is recorded. The Company has recorded significant deferred tax liabilities related to acquired intangible assets that are not deductible for tax purposes. These deferred tax liabilities are based on future statutory tax rates in the locations in which the intangible assets are recorded. Any future changes in statutory tax rates would be recorded as an adjustment to the deferred tax liabilities in the period the change is announced, and could have a material impact on the Company’s effective tax rate during that period.

16

Table of Contents

Periodic Reorganization of Sales Force. The Company relies heavily on its direct sales force. From time to time, the Company reorganizes and makes adjustments to its sales force in response to such factors as management changes, performance issues, market opportunities and other considerations. These changes may result in a temporary lack of sales production and may adversely impact revenue in future quarters. There can be no assurance that the Company will not restructure its sales force in future periods or that the transition issues associated with such a restructuring will not occur.

Regulatory Compliance. Like all other public companies, the Company is subject to the rules and regulations of the Securities and Exchange Commission (“SEC”), including those that require the Company to report on and receive an attestation from its independent registered public accounting firm regarding the Company’s internal control over financial reporting. Compliance with these requirements causes the Company to incur additional expenses and causes management to divert time from the day-to-day operations of the Company. While the Company anticipates being able to fully comply with these requirements, if it is not able to comply with the Sarbanes-Oxley reporting or attestation requirements relating to internal control over financial reporting, the Company may be subject to sanctions by the SEC or NASDAQ. Such sanctions could divert the attention of the Company’s management from implementing its business plan and could have an adverse effect on the Company’s business and results of operations.

As the Company’s stock is listed on the NASDAQ Global Select Market, the Company is subject to the ongoing financial and corporate governance requirements of NASDAQ. While the Company anticipates being able to fully comply with these requirements, if it is not able to comply, the Company’s name may be published on NASDAQ’s daily Non-Compliant Companies list until NASDAQ determines that it has regained compliance or the Company no longer trades on NASDAQ. If the Company were unable to return to compliance with the governance requirements of NASDAQ, the Company may be delisted from the NASDAQ Global Select Market, which could have an adverse effect on the market value of the Company’s equity securities and the ability to raise additional capital.

Governmental Revenue Sources. The Company’s sales to the United States government must comply with the regulations set forth in the Federal Acquisition Regulations. Failure to comply with these regulations could result in penalties being assessed against the Company or an order preventing the Company from making future sales to the United States government. Further, the Company’s international activities must comply with the export control laws of the United States, the Foreign Corrupt Practices Act and a variety of other laws and regulations of the United States and other countries in which the Company operates. Failure to comply with any of these laws and regulations could adversely affect the Company’s business, financial position, results of operations and cash flows.

In certain circumstances, the United States government, state and local governments and their respective agencies, and certain foreign governments may have the right to terminate contractual arrangements at any time, without cause. The United States, European Union and certain other government contracts, as well as the Company’s state and local level contracts, are subject to the approval of appropriations or funding authorizations. Certain of these contracts permit the imposition of various civil and criminal penalties and administrative sanctions, including, but not limited to, termination of contracts, refund of a portion of fees received, forfeiture of profits, suspension of payments, fines and suspensions or debarment from future government business, any of which could have an adverse effect on the Company’s results of operations and cash flows.

Contingencies. The Company is subject to various investigations, claims and legal proceedings that arise in the ordinary course of business, including alleged infringement of intellectual property rights, commercial disputes, labor and employment matters, tax audits and other matters. Each of these matters is subject to various uncertainties, and it is possible that an unfavorable resolution of one or more of these matters could materially affect the Company’s results of operations, cash flows or financial position.

17

Table of Contents

Changes in Existing Financial Accounting Standards. Changes in existing accounting rules or practices, new accounting pronouncements, or varying interpretations of current accounting pronouncements could have a significant, adverse effect on the Company’s results of operations or the manner in which the Company conducts its business.

Changes in Tax Law. The Company’s operations are subject to income and transaction taxes in the United States and in multiple foreign jurisdictions. A change in the tax law in the jurisdictions in which the Company does business, including an increase in tax rates or an adverse change in the treatment of an item of income or expense, could result in a material increase in tax expense. Currently, a substantial portion of the Company’s revenue is generated from customers located outside the United States, and a substantial portion of assets are located outside the United States. United States income taxes and foreign withholding taxes have not been provided on undistributed earnings for non-United States subsidiaries to the extent such earnings are considered to be indefinitely reinvested in the operations of those subsidiaries. Changes in existing taxation rules or practices, new taxation rules, or varying interpretations of current taxation practices could have a material, adverse effect on the Company’s results of operations or the manner in which the Company conducts its business.

The Company has significant operations in India. Recently, there have been court rulings concerning certain Indian tax laws that have been inconsistent with tax positions taken by the Company and inconsistent with the advice provided to the Company by its tax advisors. The impact of changes in tax law interpretation has been included in the Company’s results of operations during the period of the resolution of the applicable court case. Other court cases are pending in India that could have a material impact on the Company’s financial position, results of operations or cash flows if the ultimate outcome of those cases is similarly inconsistent with tax positions taken by the Company.

Natural Disaster in Japan. The Company has significant operations in Japan. During the first quarter of 2011, Japan experienced a catastrophic earthquake and tsunami. While the Company’s operating facilities in Japan were unharmed, this natural disaster has had an economic impact on the Company’s customers in Japan and on customers in other geographic regions who may rely on production or suppliers in Japan. As a result, the predictability of the timing and amounts of the Company’s sales to customers in Japan or that are otherwise affected by the Japan natural disaster has become less reliable than it was prior to the earthquake and tsunami. These circumstances could cause the Company’s business, financial position, results of operations and cash flows to be adversely impacted.

| ITEM 1B: | UNRESOLVED STAFF COMMENTS |

The Company has received no written comments regarding our periodic or current reports from the staff of the SEC that were issued 180 days or more preceding the end of our fiscal year 2011 and that remain unresolved.

| ITEM 2: | PROPERTIES |

The Company’s executive offices and those related to certain domestic product development, marketing, production and administration are located in a 107,000 square foot office facility in Canonsburg, Pennsylvania. In May 2004, the Company entered into the first amendment to its existing lease agreement on this facility, effective January 1, 2004. The lease was extended from its original period to a period through 2014, with an option to extend through 2019. Total required minimum payments under the operating lease will be $1.4 million per annum from January 1, 2012 through December 31, 2014.

As part of the acquisition of Apache on August 1, 2011, the Company acquired certain leased office property, including executive offices, which comprise a 52,000 square foot office facility in San Jose, California. In March 2011, Apache entered into the second amendment to its existing lease agreement, effective March 14, 2011. The lease term was extended to October 31, 2015. Total required minimum payments under the operating lease will be $910,000 in 2012, $980,000 in 2013, $1.3 million in 2014 and $1.1 million in 2015.

18

Table of Contents

The Company also leases certain office property, including executive offices, which comprise a 28,000 square foot office facility in Pittsburgh, Pennsylvania. In August 2009, the Company extended the executive office space lease agreement for a period of approximately three years and ten months, commencing February 15, 2011 and expiring December 31, 2014. Total required minimum payments under the operating lease will be $570,000 per annum from January 1, 2012 through December 31, 2014.

The Company owns certain office property, including executive offices, which comprise a 94,000 square foot office facility in Lebanon, New Hampshire. In addition, the Company owns a 40,000 square foot facility in Pune, India, which supports worldwide product development, marketing and sales activities.

The Company and its subsidiaries also lease office space in various locations throughout the world. The Company owns substantially all equipment used in its facilities. Management believes that, in most geographic locations, its facilities allow for sufficient space to support not only its present needs, but also allow for expansion and growth as the business may require in the foreseeable future. In other geographic locations, the Company expects that it will be required to expand capacity beyond that which it currently owns or leases.

In the opinion of management, the Company’s properties and its equipment are in good operating condition and are adequate for the Company’s current needs. The Company does not anticipate difficulty in renewing existing leases as they expire or in finding alternative facilities.

| ITEM 3: | LEGAL PROCEEDINGS |

The Company is subject to various investigations, claims and legal proceedings that arise in the ordinary course of business, including alleged infringement of intellectual property rights, commercial disputes, labor and employment matters, tax audits and other matters. In the opinion of the Company, the resolution of pending matters is not expected to have a material, adverse effect on the Company’s consolidated results of operations, cash flows or financial position. However, each of these matters is subject to various uncertainties and it is possible that an unfavorable resolution of one or more of these proceedings could in the future materially affect the Company’s results of operations, cash flows or financial position.

| ITEM 4: | MINE SAFETY DISCLOSURES |

Not applicable.

19

Table of Contents

PART II

| ITEM 5: | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

The Company’s common stock trades on the NASDAQ Global Select Market tier of the NASDAQ Stock Market under the symbol: “ANSS.” The following table sets forth the low and high sale price of the Company’s common stock in each of the Company’s last eight fiscal quarters.

| Fiscal Quarter Ended 2011 | Fiscal Quarter Ended 2010 | |||||||||||||||

| Low Sale Price |

High Sale Price |

Low Sale Price |

High Sale Price |

|||||||||||||

| December 31 |

$ | 45.96 | $ | 62.30 | $ | 40.63 | $ | 53.64 | ||||||||

| September 30 |

$ | 45.72 | $ | 57.15 | $ | 38.69 | $ | 46.66 | ||||||||

| June 30 |

$ | 51.22 | $ | 57.50 | $ | 40.49 | $ | 46.88 | ||||||||

| March 31 |

$ | 49.71 | $ | 56.86 | $ | 40.24 | $ | 46.49 | ||||||||

On February 10, 2012, there were 239 stockholders of record and approximately 56,242 beneficial holders of the Company’s common stock.

The Company has not paid cash dividends on its common stock as it has retained earnings for use in its business. The Company reviews its policy with respect to the payment of dividends from time to time; however, there can be no assurance that any dividends will be paid in the future.

20

Table of Contents

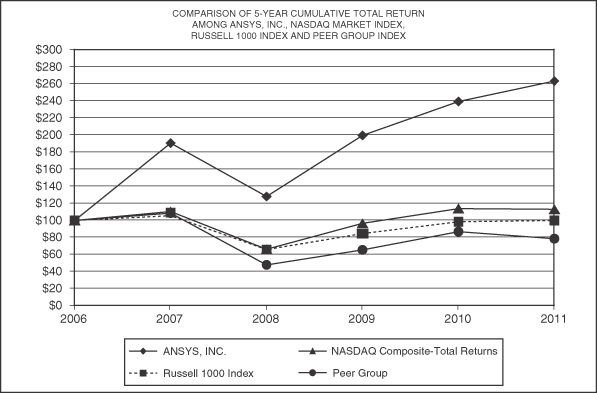

Performance Graph

Set forth below is a line graph comparing the yearly percentage change in the cumulative total stockholder return on the Company’s common stock, based on the market price of the Company’s common stock, with the total return of companies included within the Russell 1000 Index, the NASDAQ Composite Stock Market Index and a peer group of four companies (Autodesk, Inc., Parametric Technology Corporation, Cadence Design Systems, Inc. and Synopsys, Inc.) selected by the Company, for the period commencing January 1, 2007 and ending December 31, 2011. The calculation of total cumulative returns assumes a $100 investment in the Company’s common stock, the Russell 1000 Index, the NASDAQ Composite Stock Market Index and the Peer Group Index on January 1, 2007, and the reinvestment of all dividends, and accounts for all stock splits. The historical information set forth below is not necessarily indicative of future performance.

ASSUMES $100 INVESTED ON JAN. 1, 2007

ASSUMES DIVIDENDS REINVESTED

FIVE FISCAL YEARS ENDING DEC. 31, 2011

21

Table of Contents

Equity Compensation Plan Information as of December 31, 2011