AWARD NOTICE

UNDER THE ANSYS, INC.

FIFTH AMENDED AND RESTATED LONG-TERM INCENTIVE PLAN

UNDER THE ANSYS, INC.

FIFTH AMENDED AND RESTATED LONG-TERM INCENTIVE PLAN

Name of Participant:

Target Award:

Grant Date of Target Award:

Performance Measurement Period: January 1, 2020 to December 31, 2022

Pursuant to the ANSYS, Inc. Fifth Amended and Restated Long-Term Incentive Plan (the “Plan”), ANSYS, Inc. (the “Company”) has selected the Participant named above to be awarded the Target Award specified above, subject to the terms and conditions of the Plan and this Award Notice. Capitalized terms used but not defined in this Award Notice shall have the meaning given such terms in the Plan. A copy of the Plan is attached hereto as Exhibit A.

1.Acceptance of Award. The total number of Restricted Stock Units that may be credited to the Participant (if any) shall be determined by the Company’s performance during the Performance Measurement Period specified above and as set forth in Section 4(b) of the Plan. The Measurement Period Target for the Performance Measurement Period shall be equal to the Target Award. The actual number of Restricted Stock Units that may be credited could be up to 200% of such Target Award and could also be lower than the Target Award and could be zero.

2. Termination of Employment. Subject to Section 3 below, if at any time prior to the conclusion of the Performance Measurement Period, the Participant’s employment with the Company terminates for any reason, the Participant shall automatically forfeit the right to receive any portion of the Award.

Notwithstanding the foregoing, if the Participant’s employment with the Company is terminated on account of the Participant’s death or Disability (as defined below), any Restricted Stock Units that are not vested will remain eligible to vest in accordance with their terms based upon achievement of the applicable performance condition and subject to the Company’s certification of the performance metric attainment but on a prorated basis based upon the number of months that the Participant provided services as a Participant to the Company prior to the Participant’s death or Disability during the applicable performance period. For purposes hereof, “Disability” shall mean the Participant’s termination of employment with the Company: (i) after becoming eligible to receive benefits under the Company’s then current long-term disability plan that is applicable to the Participant; (ii) where the Participant is not eligible under a Company long-term disability plan, after being officially declared permanently disabled under the mandatorily applicable health or welfare regulations of the applicable jurisdiction; or, (iii) in the absence of such a determination under said regulations, after being officially declared permanently disabled by a physician appointed by the Company in its sole discretion.

3. Change in Control. Upon a Change in Control, the Award shall be treated as specified in Section 6 of the Plan.

4. Issuance of Shares.

(a) Each Restricted Stock Unit relates to one share of the Company’s Stock. Shares of Stock (if any) shall be issued and delivered to the Participant in accordance with the terms of this Award Notice and of the Plan upon compliance to the satisfaction of the Committee with all requirements under applicable laws or regulations in connection with such issuance and with the requirements hereof and of the Plan. The determination of the Committee as to such compliance shall be final and binding on the Participant.

(b) Until such time as shares of Stock are issued to the Participant pursuant to the terms hereof and of the Plan, the Participant shall have no rights as a stockholder with respect to any shares of Stock underlying the Restricted Stock Units, including but not limited to any voting rights.

5. Non-Competition and Non-Solicitation. As additional consideration for the grant of this Award to the Participant, the Participant hereby agrees that he or she shall not, at any time during his or her employment with the Company, and for a period of one year immediately after the termination of such employment (no matter if terminated by the Participant or the Company and no matter what the reason for that termination),] engage for any reason, directly or indirectly, whether as owner, part-owner, shareholder, member, partner, director, officer, trustee, employee, agent or consultant, or in any other capacity, on behalf of himself or herself or any firm, corporation or other business organization other than the Company and its subsidiaries, in any one or more of the following activities:

(a) the development, marketing, solicitation, or selling of any product or service that is competitive with the products or services of the Company, or products or services that the Company has under development or that are subject to active planning at any time during Participant’s employment;

(b) the use of any of the Company’s confidential or proprietary information, copyrights, patents or trade secrets which was acquired by the Participant as an employee of the Company and its subsidiaries; or

(c) any activity for the purpose of inducing, encouraging, or arranging for the employment or engagement by anyone other than the Company and its subsidiaries of any employee, officer, director, agent, consultant, or sales representative of the Company and its subsidiaries or attempt to engage any of them in a manner which would deprive the Company and its subsidiaries of their services or place them in a conflict of interest with the Company and its subsidiaries.

The Participant acknowledges and agrees that the activities set forth in (a)-(c) (above) are adverse to the Company’s interests, and that it would be inequitable for Participant to benefit from this Award should Participant engage in any such activities during or within one year after termination of his or her employment with the Company. The Participant may be released from his or her obligations as stated above only if the Committee (or its duly appointed agent) determines in its sole discretion that such action is in the best interests of the Company and its subsidiaries. The one year post-employment non-compete provision set forth in this Agreement does not apply to residents of California.

6. Claw-Back of Award Proceeds. The Committee shall have the authority to unilaterally terminate this Award and/or cause some or all of the proceeds relating to this Award that have been received by the Participant to become immediately due and payable by the Participant to the Company upon the occurrence of any of the following events:

(a) the Participant’s violation of Section 5 of this Agreement (entitled Non-Competition and Non-Solicitation);

(b) the material restatement of the Company’s financial statements due to misconduct by the Participant;

(c) the material restatement of the Company’s financial statements that results in the Participant receiving more compensation under the Award than the Participant would have received absent the incorrect financial statements.

The determination of whether any of the foregoing events has occurred and the extent of the application of this Section to the Participant and this Award shall be determined by the Committee in its sole discretion.

7. Incorporation of Plan. Notwithstanding anything herein to the contrary, this Award Notice shall be subject to and governed by all the terms and conditions of the Plan, including the powers of the Committee set forth in Section 3 of the Plan.

8. Transferability. This Award is personal to the Participant, is non-assignable and is not transferable by Participant in any manner, by operation of law or otherwise, other than by will or the laws of descent and distribution. The Stock to be issued upon the settlement of this Award to the Participant shall be issued, during the Participant’s lifetime, only to the Participant, and thereafter, only to the Participant’s beneficiary. The Participant may designate a beneficiary by providing written notice of the name of such beneficiary to the Company, and may revoke or change such designation at any time by filing written notice of revocation or change with the Company.

9. No Contract for Continuing Services. Neither the Plan nor this Award Notice shall be construed as creating any contract for continued services between the Company or any of its subsidiaries and the Participant and nothing herein contained shall give the Participant the right to be retained as an employee or consultant of the Company or any of its subsidiaries.

10. Integration. This Agreement constitutes the entire agreement between the parties with respect to this Award and supersedes all prior agreements and discussions between the parties concerning such subject matter.

11. Mandatory Arbitration. The Participant and the Company agree that any dispute or claim arising out of or in any way related to (i) the Participant’s employment with the Company, and/or (ii) this Agreement or any breach hereof, this Award, the Plan and/or any actions taken under the Plan, to the fullest extent permitted by law, shall be submitted to and resolved by confidential, binding arbitration by a single, neutral arbitrator. The arbitration shall be held in the county where the Company has an office at which the Participant provides services (for remote Participants, the nearest county where the Company has an office) or any other locale to which the parties jointly agree. The arbitration shall be administered by and under the auspices of JAMS in accordance with the then-current Employment Arbitration Rules & Procedures of JAMS (which are available at www.jamsadr.com/rules-employment). Arbitrator selection and discovery shall be conducted pursuant to the JAMS Rules. The arbitrator shall issue a written award setting forth the essential findings and conclusions on which the award is based, which shall be final and binding and judgment thereon may be entered in any court of competent jurisdiction. Other than an amount equal to the fee for filing such an action in the local state court, which amount the Participant shall pay toward the costs of the arbitration, the Company shall bear the administrative, filing and forum costs of the arbitration, including the JAMS administrative fees and the arbitrator’s fees. Except as otherwise provided by law or in the arbitrator’s ruling, each party shall otherwise bear its own respective attorneys’ fees and costs of the arbitration. The Participant and the Company agree that each may bring claims against the other only in an individual capacity, and not as a plaintiff, claimant or class member in any purported class action, collective action or other representative proceeding, or otherwise seeking to represent the interests of any other person. This agreement to arbitrate shall survive any separation of the Participant’s employment. Notwithstanding the foregoing, nothing herein or otherwise shall preclude the Company from pursuing a court action for the purpose of obtaining a temporary restraining order or other injunctive relief to enforce any restrictive covenants the Participant has with or for the benefit of the Company.

12. General Release of Claims by the Participant.

(a) As a condition of and in consideration for the promises made by the Company herein, including without limitation to provide the Award hereunder, the Participant hereby knowingly and voluntarily releases and discharges to the fullest extent permitted by law the Company and its past, present and future parents, subsidiaries, affiliates, and related entities, any and all of its or their past, present or future directors, shareholders, officers, executives, employees, and/or agents, and/or its and their respective predecessors, successors, and assigns (individually and collectively, the “Company Releasees”), from and with respect to any and all claims and causes of action whatsoever, in law or in equity, known or unknown, which the Participant ever had, has or may have against the Company and/or any or all of the other Company Releasees for, upon, or by reason of any matter whatsoever up to the date on which the Participant accepts this Agreement (individually and collectively, “Claims”). The parties intend the foregoing to be a general release of any and all Claims to the fullest extent permissible by law. Notwithstanding the foregoing, nothing herein is a release by the Participant of (A) any rights or Claims with respect to accrued and vested benefits and/or previously awarded equity interests, subject in each instance to the terms and conditions of any applicable plan, grant, and/or agreement pertaining to such benefits, awards or interests and applicable law, (B) any rights or Claims arising under or to enforce this Agreement, or (C) any rights or Claims that, under applicable law, cannot lawfully be released by private agreement or otherwise.

(b) FOR CALIFORNIA RESIDENTS ONLY: In granting the foregoing release, the Participant acknowledges that he/she has been advised to consult with legal counsel and is familiar with the provision of California Civil Code Section 1542, a statute that otherwise prohibits the release of unknown claims, which provides as follows:

“A GENERAL RELEASE DOES NOT EXTEND TO CLAIMS WHICH THE CREDITOR DOES NOT KNOW OR SUSPECT TO EXIST IN HIS FAVOR AT THE TIME OF EXECUTING THE RELEASE, WHICH IF KNOWN BY HIM MUST HAVE MATERIALLY AFFECTED HIS SETTLEMENT WITH THE DEBTOR.”

Being aware of said Code section, the Participant hereby expressly waives any rights the Participant may have thereunder, as well as under any other state or federal statutes or common law principles of similar effect.

(c) Nothing contained in this Agreement (including the foregoing general release) limits the Participant’s ability to file a charge or complaint with any federal, state or local governmental agency, commission or regulatory entity (a “Government Agency”). If the Participant files any charge or complaint with any Government Agency, if any Government Agency pursues any charge or claim on the Participant’s behalf, or if any other third party pursues any claim or charge on the Participant’s behalf, the Participant waives any right to monetary or other individualized relief (either individually, or as part of any collective or class action); provided, however, that nothing in this Agreement limits any right the Participant may have to receive a whistleblower award or bounty for information provided to the Securities and Exchange Commission. The Participant represents that he/she is not aware of any unlawful conduct or violations of any federal, state or local law, rule or regulation by the Company and/or any other Company Releasees or any basis to bring a charge or complaint to any Government Agency.

13. Notices. Notices hereunder shall be mailed or delivered to the Company at its principal place of business and shall be mailed or delivered to the Participant at the address on file with the Company or, in either case, at such other address as one party may subsequently furnish to the other party in writing.

14. Severability. If any provision(s) hereof shall be determined to be illegal or unenforceable, such determination shall in no manner affect the legality or enforceability of any other provision hereof.

15. Counterparts. For the convenience of the parties and to facilitate execution, this document may be executed in two or more counterparts, each of which shall be deemed an original, but all of which shall constitute one and the same document.

16. Time to Review and Accept; Right to Revoke; Effective Date. The Participant is advised by the Company to consult with an attorney in connection with this Agreement. The Participant understands that as part of his/her agreement to release Claims against the Company and the other Company Releasees, the Participant is releasing Claims for age discrimination under the federal Age Discrimination in Employment Act (the “ADEA”). ACCORDINGLY, THE PARTICIPANT HAS THE RIGHT, AND ACKNOWLEDGES THAT HE/SHE HAS BEEN GIVEN THE OPPORTUNITY, TO REVIEW AND CONSIDER THIS AGREEMENT FOR A PERIOD OF TWENTY-ONE (21) DAYS FROM THE PARTICIPANT’S RECEIPT OF THIS AGREEMENT BEFORE SIGNING IT (THE “REVIEW PERIOD”). To accept this Agreement and the Award granted hereunder, the Participant must ccept the agreement online via his/her E*TRADE employee stock plan account at any time before the end of the Review Period. If the Participant accepts this Agreement before the end of the Review Period, the Participant acknowledges that such decision was voluntary and that he/she had the opportunity to consider this Agreement for the full Review Period. For the period of seven (7) days from the date when the Participant accepts this Agreement, the Participant has the right to revoke this Agreement by written notice via email to human-resources@ansys.com and addressing stock administration, provided such notice is delivered so that it is received at or before the expiration of the 7-day revocation period. This Agreement shall not become effective or enforceable during the revocation period. If timely accepted and not revoked by the Participant prior to the end of the revocation period, this Agreement shall become effective on the first business day following the expiration of the revocation period (the “Effective Date”). If not timely accepted or if (after timely acceptance) the Participant revokes prior to the expiration of the revocation period, this Agreement shall not become effective and the Participant will not be entitled to or receive the Award granted hereunder and/or such Award shall be rescinded.

17. Knowing and Voluntary Agreement. By accepting this Agreement, the Participant acknowledges and represents that the Participant (a) has carefully read this Agreement in its entirety; (b) is hereby advised by the Company in writing to consult with an attorney of the Participant’s choice before accepting this Agreement; (c) has been afforded and has had a full and reasonable opportunity and period of time of at least 21 days to consider the terms and conditions of this Agreement; (d) fully understands the meaning and significance, and consequences, of all of the terms and conditions of this Agreement (including without limitation the general release given by the Participant in this Agreement); and (e) is accepting this Agreement knowingly, voluntarily and of the Participant’s own free will and with the intent to be fully bound hereby.

ANSYS, Inc.

ANSYS, Inc.By:

Name: Ajei S. Gopal

Title: President and CEO

The foregoing Award is hereby accepted and the terms and conditions of this Agreement are hereby agreed to by the Participant. Electronic acceptance of this Award pursuant to the Company’s instructions to the Participant (including through an online acceptance process) is acceptable and the Participant agrees that documentation from E*TRADE showing online acceptance is valid evidence of acceptance.

Dated:

Participant’s signature

Participant’s name and address:

Exhibit A

ANSYS, INC.

FIFTH AMENDED AND RESTATED LONG-TERM INCENTIVE PLAN

FIFTH AMENDED AND RESTATED LONG-TERM INCENTIVE PLAN

1.Purpose

This Fifth Amended and Restated Long-Term Incentive Plan (the “Plan”) is intended to provide an incentive for superior work and to motivate executives and employees of ANSYS, Inc. (the “Company”) toward even higher achievement and business results, to tie their goals and interests to those of the Company and its stockholders and to enable the Company to attract and retain highly qualified executives and employees. The Plan is for the benefit of Participants (as defined below). Awards made under this Plan constitute Restricted Stock Unit Awards under Section 11 of the Company’s Fifth Amended and Restated 1996 Stock Option and Grant Plan (the “1996 Option Plan”) and shall be granted under, and subject to, the terms of the 1996 Option Plan.

2.Definitions

For purposes of this Plan:

(a) | “Award” means a grant to a Participant hereunder. From and after a Change in Control, any references to an Award shall mean the fixed number of Restricted Stock Units eligible to be earned by a Participant, as determined by the Committee pursuant to Section 6 hereof. |

(b) | “Award Notice” means a notice or agreement provided to a Participant that sets forth the terms, conditions and limitations of the Participant’s participation in this Plan, including, without limitation, the Participant’s Target Award. |

(c) | “Board” means the Board of Directors of the Company. |

(d) | “Cause” means, and shall be limited to a determination by the Company that the Participant’s employment shall be terminated as a result of any one or more of the following events: |

(i) any material breach by the Participant of any agreement between the Participant and the Company; or

(ii) the conviction of, indictment for or plea of nolo contendere by the Participant to a felony or a crime involving moral turpitude; or

(iii) any material misconduct or willful and deliberate non-performance (other than by reason of disability) by the Participant of the Participant’s duties to the Company; or

(iv) willful failure to cooperate with a bona fide internal investigation or an investigation by regulatory or law enforcement authorities, after being instructed by the Company to cooperate, or the willful destruction or failure to preserve documents or other materials known to be relevant to such investigation or the willful inducement of others to fail to cooperate or to produce documents or other materials in connection with such investigation.

(e) | “Change in Control” means any of the following: |

(i) any “person,” as such term is used in Sections 13(d) and 14(d) of the Securities Exchange Act of 1934, as amended (the “Act”) (other than the Company, any of its subsidiaries, or any trustee, fiduciary or other person or entity holding securities under any employee benefit plan or trust of the Company or any of its subsidiaries), together with all “affiliates” and “associates” (as such terms are defined in Rule 12b-2 under the Act) of such person, shall become the “beneficial owner” (as such term is defined in Rule 13d-3 under the Act), directly or indirectly, of securities of the Company representing 50 percent or more of the combined voting power of the Company’s then outstanding securities having the right to vote in an election of the Board (“Voting Securities”) (in such case other than as a result of an acquisition of securities directly from the Company); or

(ii) the consummation of (A) any consolidation or merger of the Company where the stockholders of the Company, immediately prior to the consolidation or merger, would not, immediately after the consolidation or merger, beneficially own (as such term is defined in Rule 13d-3 under the Act), directly or indirectly, shares representing in the aggregate more than 50 percent of the voting shares of the Company issuing cash or securities in the consolidation or merger (or of its ultimate parent corporation, if any), or (B) any sale or other transfer (in one transaction or a series of transactions contemplated or arranged by any party as a single plan) of all or substantially all of the assets of the Company.

Notwithstanding the foregoing, a “Change in Control” shall not be deemed to have occurred for purposes of the foregoing clause (i) solely as the result of an acquisition of securities by the Company which, by reducing the number of shares of Voting Securities outstanding, increases the proportionate number of Voting Securities beneficially owned by any person to 50 percent or more of the combined voting power of all of the then outstanding Voting Securities; provided, however, that if any person referred to in this sentence shall thereafter become the beneficial owner of any additional shares of Voting Securities (other than pursuant to a stock split, stock dividend, or similar transaction or as a result of an acquisition of securities directly from the Company) and immediately thereafter beneficially owns 50 percent or more of the combined voting power of all of the then outstanding Voting Securities, then a “Change in Control” shall be deemed to have occurred for purposes of the foregoing clause (i).

(f) | “Change in Control Date” means with respect to each Change in Control Performance Measurement Period, the last day of the month immediately preceding the effective date of the Change in Control. |

(g) | “Change in Control Performance Measurement Period” means the Performance Measurement Period that is shortened by the Committee such that such period shall be deemed to have concluded as of the Change in Control Date. |

(h) | “Change in Control Terminating Event” means during the 18-month period following the occurrence of a Change in Control, any of the following events: (i) termination by the Company of the Participant’s employment for any reason other than for Cause, death or disability; or (ii) the termination by the Participant of his or her employment with the Company for Good Reason. Notwithstanding the foregoing, a Change in Control Terminating Event shall not be deemed to have occurred herein solely as a result of the Participant being an employee of any direct or indirect successor to the business or assets of the Company. |

(i) | “Closing Index Value” means the Performance Measurement Index Value as of the last day of the Performance Measurement Period. |

(j) | “Closing Stock Price” means the Stock Price as of the last day of the Performance Measurement Period. |

(k) | “Code” means Internal Revenue Code of 1986, as amended. |

(l) | “Committee” means the Compensation Committee of the Board. |

(m) | “Effective Date” means as of January 1, 2019. |

(n) | “Good Reason” means that the Participant has complied with the “Good Reason Process” (hereinafter defined) following the occurrence of any of the following events: |

(i) a material diminution in the Participant’s responsibilities, authority or duties; or

(ii) a material reduction in the Participant’s Base Salary and Target Bonus except for across-the-board salary reductions similarly affecting all or substantially all management employees; or

(iii) a material change in the geographic location at which the Participant is principally employed.

For purposes of this Section 2(n)(i), a change in the reporting relationship, or a change in a title will not, by itself, be sufficient to constitute a material diminution of responsibilities, authority or duty.

(o) | “Good Reason Process” means: |

(i) the Participant reasonably determines in good faith that a “Good Reason” condition has occurred;

(ii) the Participant notifies the Company in writing of the occurrence of the Good Reason condition within 60 days of the first occurrence of such condition;

(iii) the Participant cooperates in good faith with the Company’s efforts, for a period not less than 30 days following such notice (the “Cure Period”), to remedy the condition;

(iv) notwithstanding such efforts, the Good Reason condition continues to exist following the Cure Period; and

(v) the Participant terminates his or her employment within 30 days after the end of the Cure Period.

If the Company cures the Good Reason condition during the Cure Period, Good Reason shall be deemed not to have occurred.

(p) | “Initial Index Value” means, the Performance Measurement Index Value as of January 1 of the first calendar year in any Performance Measurement Period. |

(q) | “Initial Stock Price” means the Stock Price as of January 1 of the first calendar year in any Performance Measurement Period. |

(r) | “Participant” means an executive or employee of the Company selected by the Committee to participate in the Plan. |

(s) | “Performance Measurement Index” means the NASDAQ Composite Index (^IXIC), or, in the event such index is discontinued or its methodology significantly changed, a comparable index selected by the Committee in good faith. |

(t) | “Performance Measurement Index Value” means, with respect to any date, the average value of the Performance Measurement Index for the ten consecutive trading days immediately preceding such date. |

(u) | “Performance Measurement Period” means a three-year period commencing on January 1 and ending on the third December 31 thereafter. There shall be overlapping Performance Measurement Periods. The first Performance Measurement Period under the Plan will commence on January 1, 2019 and subsequent Performance Measurement Periods will commence on each January 1 thereafter while the Plan is effective. |

(v) | “Performance Multiplier” means the percentage between 0% and 200% by which the applicable portion of the Target Award is multiplied to determine the number of credited Restricted Stock Units for the Performance Measurement Period. |

(w) | “Restricted Stock Units” means the stock units of the Company to be settled in shares of Stock. |

(x) | “Stock” means the Company’s common stock, par value $0.01 per share. |

(y) | “Stock Price” means, as of a particular date, the average closing price of one share of Stock for the ten consecutive trading days ending on, and including, such date; provided however, that in the event of a Change in Control of the Company, the Stock Price shall equal the fair market value, as determined by the Committee in its discretion, of the total consideration paid or payable in the transaction resulting in the Change in Control for one share of Stock. |

(z) | “Target Award” means the target number of Restricted Stock Units that comprise a Participant’s Award for each Performance Measurement Period, as set forth in the Participant’s Award Notice. |

(aa) | “Total Shareholder Return” means, with respect to a Performance Measurement Period, the total percentage return per share, achieved by the Stock assuming contemporaneous reinvestment in the Stock of all dividends and other distributions (excluding dividends and distributions paid in the form of additional shares of Stock) at the closing price of one share of Stock on the date such dividend or other distribution was paid, based on the Initial Stock Price, and the Closing Stock Price for the last day of the applicable Performance Measurement Period. |

3.Administration

(a) The Plan shall be administered by the Committee. The Committee shall have the discretionary authority to make all determinations (including, without limitation, the interpretation and construction of the Plan and the determination of relevant facts) regarding the entitlement to any Award hereunder and the amount of any Award to be paid under the Plan (including the number of shares of Stock issuable to any Participant), provided such determinations are made in good faith and are consistent with the purpose and intent of the Plan. In particular, but without limitation and subject to the foregoing, the Committee shall have the authority:

(i) to select Participants under the Plan;

(ii) to determine the number and length of each Performance Measurement Period;

(iii) to determine the Target Award and any formula or criteria for the determination of the Target Award for each Participant;

(iv) to determine the terms and conditions, not inconsistent with the terms of this Plan, which shall govern Award Notices and all other written instruments evidencing an Award hereunder, including the waiver or modification of any such conditions;

(v) to adopt, alter and repeal such administrative rules, guidelines and practices governing the Plan as it shall from time to time deem advisable; and

(vi) to interpret the terms and provisions of the Plan and any Award granted under the Plan (and any Award Notices or other agreements relating thereto) and to otherwise supervise the administration of the Plan.

(b) Notwithstanding anything herein to the contrary, the Committee may, in its discretion, make appropriate adjustments to any Award, any Target Award, any Initial Stock Price, any Closing Stock Price or the Total Shareholder Return for any period in connection with or as a result of any of the following events which occur or have occurred after the Effective Date: reorganization, recapitalization, reclassification, stock dividend, stock split, reverse stock split or other similar change in the Company’s capital stock, if the outstanding shares of Stock are increased or decreased or are exchanged for a different number or kind of shares or other securities of the Company, or additional shares or new or different shares or other securities of the Company or other non-cash assets are distributed with respect to such shares of Stock or other securities.

(c) Subject to the terms hereof, all decisions made by the Committee pursuant to the Plan shall be final, conclusive and binding on all persons, including the Company and the Participants. No member of the Board or the Committee, nor any officer or employee of the Company acting on behalf of the Board or the Committee shall be personally liable for any action, determination or interpretation taken or made in good faith with respect to the Plan, and all members of the Board or Committee and each and any officer or employee of the Company acting on their behalf shall, to the extent permitted by law, be fully indemnified and protected by the Company in respect of any such action, determination or interpretation.

4.Determination and Payment of Awards

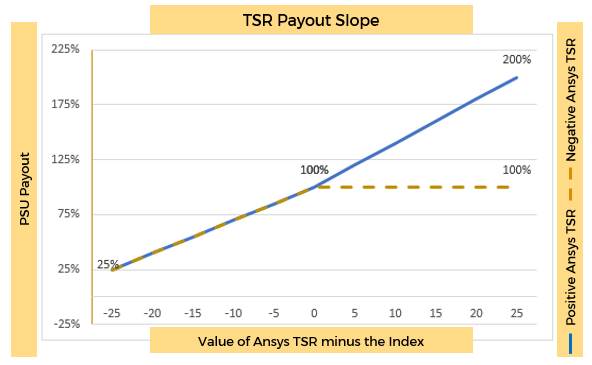

(a) Measurement Period Target. Each Participant’s Award Notice shall specify such Participant’s Target Award, and the portion of which shall be eligible to be credited for the Performance Measurement Period (the “Measurement Period Target”). The Target Award shall be expressed as a number of Restricted Stock Units. The percentage of the Measurement Period Target that is eligible to be credited shall be determined by reference to the Company’s performance for the Performance Measurement Period as measured by the Total Shareholder Return relative to the percentage appreciation of the Performance Measurement Index for such calendar year or years. The percentage appreciation of the Performance Measurement Index shall be established by comparing the Initial Index Value to the Closing Index Value.

(b) Performance Multiplier: If Total Shareholder Return for a Performance Measurement Period is less than the Performance Measurement Index, the Performance Multiplier shall be 100% minus A, where A is (the amount by which the Performance Measurement Index exceeds Total Shareholder Return) times three; provided however that the Performance Multiplier shall be zero if A results in a number greater than 75. If Total Shareholder Return for a Performance Measurement Period, is equal to the Performance Measurement Index, the Performance Multiplier shall be 100%. If Total Shareholder Return for a Performance Measurement Period is greater than the Performance Measurement Index, the Performance Multiplier is 100% plus B, where B is (the amount by which Total Shareholder Return exceeds the Performance Measurement Index) times four.

In no event will any portion of a Participant’s Target Award be credited for a Performance Measurement Period in which the Performance Multiplier calculates to a number of less than 25% (i.e., in such event the Performance Multiplier shall be 0% for such Performance Measurement Period).

Notwithstanding the foregoing, in no event shall the Performance Multiplier be less than 0% or exceed 200%, regardless of a Total Shareholder Return that would result in a Performance Multiplier of less than 0% or in excess of 200%.

Notwithstanding the foregoing, if the Total Shareholder Return in a Performance Measurement Period is a negative percentage, then a maximum of 100% of the Measurement Period Target may be credited for such period, even if the Total Shareholder Return relative to the median percentage appreciation (depreciation) of the Performance Measurement Index would result in a greater Performance Multiplier.

(c) Committee Determination. The Committee, at its first meeting following the conclusion of a Performance Measurement Period, shall determine the actual number of Restricted Stock Units that will be deemed to have been credited as of the final day of such Performance Measurement Period. The number of Restricted Stock Units credited for such period shall equal the Measurement Period Target multiplied by the Performance Multiplier, subject to the terms and conditions hereof.

(d) Vesting and Settlement. Subject to Section 5, as soon as practicable (but in no event later than 74 days) following the conclusion of the Performance Measurement Period, the Restricted Stock Units that were credited, if any, for the Performance Measurement Period will be vested and settled in an equal number of shares of Stock.

5.Termination of Employment. Unless otherwise provided in any Award Notice or as provided in Section 6 below, if at any time prior to the conclusion of a Performance Measurement Period, a Participant’s employment with the Company terminates for any reason, such Participant shall automatically forfeit the right to receive any Award credited as of the date of termination of employment.

6.Change in Control. Unless otherwise provided in any Award Notice, upon a Change in Control of the Company, the following shall occur:

(a) With respect to each Change In Control Performance Measurement Period, the Committee, in accordance with Section 4, shall determine the actual number of Restricted Stock Units that are eligible to be credited based on the Total Shareholder Return for the Change in Control Performance Measurement Period relative to the median percentage appreciation of the Performance Measurement Index for such Change in Control Performance Measurement Period and such Award shall not be deemed fully vested until the conclusion of the Performance Measurement Period, subject to the continued employment of the Participant through such date. For example, if a Change in Control occurs during the eleventh month of the Performance Measurement Period, the Committee shall determine the number of Restricted Stock Units that are eligible to be credited with respect to the applicable Change in Control Performance Measurement Period based on performance for such period, but the Award shall not be deemed vested and will not be settled until the end of the full 36 month Performance Measurement Period. For the avoidance of doubt, since the Plan contemplates overlapping Performance Measurement Periods, there may be up to three different Change In Control Performance Measurement Periods.

(b) In the event that subsequent to a Change in Control, a Participant’s employment with the Company terminates for any reason other than a Change in Control Terminating Event, such Participant shall automatically forfeit the right to receive all outstanding Awards that have been credited as of the date of termination of employment.

(c) In the event a Change in Control Terminating Event occurs with respect to a Participant, all outstanding Awards held by such Participant shall immediately vest and become payable.

(d) If as a result of a Change in Control, no Stock remains outstanding and the surviving corporation (or its ultimate parent) does not agree to convert the Awards into a number of restricted stock units of equivalent value of the surviving corporation (or its ultimate parent), then the Awards shall be converted to a dollar value based on the Stock Price.

7.Miscellaneous

(a) | Amendment and Termination. The Company reserves the right to amend or terminate the Plan at any time in its discretion without the consent of any Participants, but no such amendment shall adversely affect the rights of the Participants with regard to outstanding Awards. In the event the Plan is terminated, the Company shall determine the Awards payable to Participants based on the Total Shareholder Return relative to the Performance Measurement Index for each Performance Measurement Period ending on the date of Plan termination. The Awards for each Performance Measurement Period shall be further prorated to reflect the shortened Performance Measurement Period. |

(b) | No Contract for Continuing Services. This Plan shall not be construed as creating any contract for continued services between the Company or any of its subsidiaries and any Participant and nothing herein contained shall give any Participant the right to be retained as an employee or consultant of the Company or any of its subsidiaries. |

(c) | No Transfers. A Participant’s rights in an interest under the Plan may not be assigned or transferred. |

(d) | Unfunded Plan. The Plan shall be unfunded and shall not create (or be construed to create) a trust or separate fund. Likewise, the Plan shall not establish any fiduciary relationship between the Company or any of subsidiaries or affiliates and any Participant. To the extent that any Participant holds any rights by virtue of an Award under the Plan, such right shall be no greater than the right of an unsecured general creditor of the Company or any of its subsidiaries. |

(e) | Governing Law. The Plan and each Award Notice awarded under the Plan shall be construed in accordance with and governed the laws of the State of Delaware, without regard to principles of conflict of laws of such state. |

(f) | Tax Withholding. Any issuance of shares of Stock to a Participant shall be subject to tax withholding. The minimum tax withholding obligation shall be satisfied through a net issuance of shares. The Company shall withhold from shares of Stock to be issued to the Participant a number of shares of Stock with an aggregate fair market value that would satisfy the minimum withholding amount due. |

(g) | Construction. Wherever appropriate, the use of the masculine gender shall be extended to include the feminine and/or neuter or vice versa; and the singular form of words shall be extended to include the plural; and the plural shall be restricted to mean the singular. |

(h) | Headings. The Section headings and Section numbers are included solely for ease of reference. If there is any conflict between such headings or numbers and the text of this Plan, the text shall control. |

(i) | Effect on Other Plans. Nothing in this Plan shall be construed to limit the rights of Participants under the Company’s or its subsidiaries’ benefit plans, programs or policies. |

(j) | Effective Date. The Plan shall be effective as of the Effective Date. |

8.Section 409A.

(a) | All payments and benefits described in this Plan are intended to constitute a short term deferral for purposes of Section 409A of the Internal Revenue Code of 1986, as amended. To the extent that any payment or benefit described in this Plan constitutes “non-qualified deferred compensation” under Section 409A of the Code, and to the extent that such payment or benefit is payable upon the Participant’s termination of employment, then such payments or benefits shall be payable only upon the Participant’s “separation from service.” The determination of whether and when a separation from service has occurred shall be made in accordance with the presumptions set forth in Treasury Regulation Section 1.409A‑1(h). |

(b) | The parties intend that this Plan will be administered in accordance with Section 409A of the Code. To the extent that any provision of this Plan is ambiguous as to its compliance with Section 409A of the Code, the provision shall be read in such a manner so that all payments hereunder comply with Section 409A of the Code. The parties agree that this Plan may be amended, as reasonably requested by either party, and as may be necessary to fully comply with Section 409A of the Code and all related rules and regulations in order to preserve the payments and benefits provided hereunder without additional cost to either party. |

(c) | The Company makes no representation or warranty and shall have no liability to the Participant or any other person if any provisions of this Plan are determined to constitute deferred compensation subject to Section 409A of the Code but do not satisfy an exemption from, or the conditions of, such Section. |

INTERNATIONAL APPENDIX

Additional Terms and Conditions

Terms and Conditions

This International Appendix includes additional terms and conditions that govern the award granted to you under the Plan for your country. Certain capitalized terms used but not defined in this International Appendix have the meanings set forth in the Plan and the Agreement that relate to your award. By acceptance of the award you agree to be bound by the terms and conditions contained in the paragraphs below in addition to the terms of the Plan and the Agreement and the terms of any other document that may apply to you and your award.

Notifications

This International Appendix also includes information regarding issues of which you should be aware with respect to participation in the Plan. The information is based on the securities, exchange control, and other laws in effect in the respective countries as of the date set forth above. Such laws are often complex and change frequently. As a result, it is strongly recommended that you not rely on the information in this International Appendix as the only source of information relating to the consequences of your participation in the Plan because the information may be out of date at the time you vest in your award or sell shares acquired under the Plan.

The information contained herein is general in nature and may not apply to your particular situation, and the Company is not in a position to assure you of a particular result. In addition, please note that the requirements may differ for residents and non-residents. Accordingly, you are advised to seek appropriate professional advice as to how the relevant laws in your country may apply to your situation.

Finally, if you are a citizen or resident of a country other than the one in which you are currently working, transferred employment to another country after the award was granted to you, or are considered a resident of another country for local law purposes, the information contained herein may not apply.

Provisions Applicable to all International Awards

Data Privacy. The Participant explicitly and unambiguously consents to the collection, use and transfer, in electronic or other form, of the Participant’s personal data by and among, as applicable, the Company, its subsidiaries and affiliates, for the exclusive purpose of implementing, administering and managing the Participant’s participation in the Plan. The Participant hereby understands that the Company, its subsidiaries and affiliates hold (but only process or transfer to the extent required or permitted by local law) certain personal information about the Participant, including, but not limited to, the Participant’s name, home address and telephone number, date of birth, social insurance number or other identification number, salary, nationality, job title, any Shares or directorships held in the Company, details of all Restricted Stock Units or any other entitlement to Shares awarded, canceled, exercised, vested, unvested or outstanding in the Participant’s favor, for the purpose of implementing, administering and managing the Plan (“Data”). The Participant hereby understands that Data may be transferred to any third parties assisting in the implementation, administration and management of the Plan, that these recipients may be located in the Participant’s country or elsewhere (including countries outside of the European Economic Area such as the United States of America), and that the recipient’s country may have different data privacy laws and protections than the Participant’s country. The Participant hereby understands that the Participant may request a list with the names and addresses of any potential recipients of the Data by contacting the Participant’s local human resources representative. The Participant authorizes the recipients to receive, possess, use, retain and transfer the Data, in electronic or other form, for the purposes of implementing, administering and managing the Participant’s participation in the Plan, including any requisite transfer of such Data as may be required to a broker or other third party with whom the Participant may elect to deposit any Shares acquired upon exercise. The Participant hereby understands that Data will be held only as long as is necessary to implement, administer and manage the Participant’s participation in the Plan and in accordance with local law. The Participant hereby understands that the Participant may, at any time, view Data, request additional information about the storage and processing of Data, require any necessary amendments to Data or refuse or withdraw the consents herein, in any case without cost, by contacting in writing the Participant’s local human resources representative. The Participant hereby understands, however, that refusing or withdrawing the Participant’s consent may affect the Participant’s ability to participate in the Plan. For more information on the consequences of the Participant’s refusal to consent or withdrawal of consent, the Participant hereby understands that the Participant may contact the Participant’s local human resources representative.

Nature of Grant. In accepting the grant of Restricted Stock Units, the Participant acknowledges that:

(a) the Plan is established voluntarily by the Company, is discretionary in nature and may be modified, amended, suspended or terminated by the Company at any time, unless otherwise provided in the Plan and this Agreement;

(b) the grant of Restricted Stock Units is voluntary and occasional and does not create any contractual or other right to receive future grants of Restricted Stock Units, or benefits in lieu of Restricted Stock Units, even if Restricted Stock Units have been granted repeatedly in the past;

(c) all decisions with respect to future Restricted Stock Units, if any, will be at the sole discretion of the Company;

(d) the Participant’s participation in the Plan will not create a right to further employment with the Participant’s employer (the “Employer”) and shall not interfere with the ability of the Employer to terminate the Participant’s employment relationship;

(e) the Participant is voluntarily participating in the Plan;

(f) the Restricted Stock Units are an extraordinary item that does not constitute compensation of any kind for services of any kind rendered to the Company or the Employer, and which is outside the scope of the Participant’s employment contract, if any;

(g) the Restricted Stock Units are not part of normal or expected compensation or salary for any purposes, including, but not limited to, calculating any severance, resignation, termination, redundancy, end of service payments, bonuses, long-service awards, pension or retirement benefits or similar payments and in no event should be considered as compensation for, or relating in any way to, past services for the Company or the Employer;

(h) in the event that the Participant is not an employee of the Company, the grant of Restricted Stock Units will not be interpreted to form an employment contract or relationship with the Company; and furthermore, the grant of Restricted Stock Units will not be interpreted to form an employment contract with the Employer or any subsidiary or affiliate of the Company;

(i) the future value of the underlying Shares is unknown and cannot be predicted with certainty;

(j) if the Participant vests in the Restricted Stock Units and obtains Shares, the value of those Shares may increase or decrease in value;

(k) in consideration of the grant of the Restricted Stock Units, no claim or entitlement to compensation or damages shall arise from termination of the Restricted Stock Units or diminution in value of the Restricted Stock Units or Shares acquired resulting from termination of the Participant’s employment by the Company or the Employer, and the Participant irrevocably releases the Company and the Employer from any such claim that may arise; if, notwithstanding the foregoing, any such claim is found by a court of competent jurisdiction to have arisen, then, by signing this Agreement, the Participant will be deemed irrevocably to have waived his or her entitlement to pursue such claim; and

(l) in the event of termination of the Participant’s employment, Participant’s right to receive the Restricted Stock Units and vest in the Restricted Stock Units under the Plan, if any, will terminate effective as of the date that the Participant is no longer actively employed.

Country-Specific Language

Below please find country-specific language that applies to you if you are a citizen or resident of one of the following countries: Belgium, Canada, China, France, Germany, Greece, India, Ireland, Italy, Japan, Poland, Singapore, South Korea, Spain, Sweden, Switzerland, Taiwan and United Kingdom.

BELGIUM

Notifications

Tax Reporting Information. Participants are required to report any bank accounts opened and maintained outside Belgium on their annual tax return.

CANADA

Terms and Conditions

Restricted Stock Units Settled in Shares Only. Notwithstanding anything to the contrary in the Plan and/or the Agreement, you understand that any Restricted Stock Units granted to you shall be paid in shares only and do not provide any right for you to receive a cash payment.

The following provision will apply to residents of Quebec:

Language Consent. The parties to the Agreement have expressly required that the Agreement and all documents and notices relating to the Agreement be drafted in English.

Les parties aux présentes ont expressément exigé que la présente convention et tous les documents et avis qui y sont afférents soient rédigés en anglais.

Notifications

Additional Restrictions on Resale. In addition to the restrictions on resale and transfer noted in Plan materials, securities purchased under the Plan may be subject to certain restrictions on resale imposed by Canadian provincial securities laws. Participants are encouraged to seek legal advice prior to any resale of such securities. In general, Participants resident in Canada may resell their securities in transactions carried out on exchanges outside of Canada.

Tax Reporting. The Tax Act and the regulations thereunder require a Canadian resident individual (among others) to file an information return disclosing prescribed information where, at any time in a tax year, the total cost amount of such individual’s “specified foreign property” (which includes shares) exceeds Cdn.$100,000. Participants should consult their own tax advisor regarding this reporting requirement.

CHINA

Due to Chinese legal requirements, Shares of ANSYS, Inc. acquired under any company equity plans must be maintained in the designated brokerage account until the Shares are sold through the designated brokerage account with the net sales proceeds being paid to you through your current or most recent PRC employer. As a condition of the grant of PSUs, to the extent that you hold any Shares on the date that is six (6) months after the date of your termination of active employment with ANSYS and its subsidiaries and affiliates, you authorize E*TRADE Financial Corporate Services, Inc. (or any successor broker designated by ANSYS) to sell such Shares on your behalf at that time or as soon as is administratively practical thereafter.

Under local law, Participant is required to repatriate to China the proceeds from your participation in any company equity Plans, including proceeds from the sale of Shares acquired through PSU lapses and any dividends or dividend equivalents paid to you through a special exchange control account established by ANSYS or one of its subsidiaries or affiliates in China. You hereby agree that any proceeds from your participation in the Plan may be transferred to such special account prior to being delivered to you through your current or most recent PRC employer. Further, if the proceeds from your participation in the Plan are converted to local currency, you acknowledge that the Company (including its subsidiaries and affiliates) are under no obligation to secure any currency conversion rate, and may face delays in converting the proceeds to local currency due to exchange control restrictions in China. You agree to bear the risk of any currency conversion rate fluctuation between the date that your proceeds are delivered to the special exchange control account and the date of conversion of the proceeds to local currency.

ANSYS reserves the right to impose such further restrictions or conditions as may be necessary to comply with changes in applicable local laws in China.

Please note that the above provisions will apply to all PSUs granted to you under a company equity plan.

If you are not a PRC national, the above provision will apply to you to the extent approved by SAFE or its local branch office in accordance with local laws.

FRANCE

Notifications

Exchange Control Information. If a Participant imports or exports cash (e.g., sale proceeds received under the Plan) with a value equal to or exceeding €10,000 and does not use a financial institution to do so, Participant must submit a report to the customs and excise authorities. If Participant maintains a foreign bank account, Participant is required to report such account to the French tax authorities when filing his/her annual tax return.

GERMANY

Notifications

Exchange Control Information. Cross-border payments in excess of €12,500 must be reported monthly to the German Federal Bank. If a Participant uses a German bank to transfer a cross-border payment in excess of €12,500 in connection with the sale of Shares acquired under the Plan, the bank will file the report for the Participant.

INDIA

Terms and Conditions

Repatriation of Proceeds. You understand that you must repatriate any proceeds from the sale of Shares acquired upon vesting of the Restricted Stock Units to India and convert the proceeds into local currency within 90 days of receipt. You will receive a foreign inward remittance certificate (“FIRC”) from the bank where you deposit the foreign currency. You should maintain the FIRC as evidence of the repatriation of funds in the event the Reserve Bank of India or your employer requests proof of repatriation.

Notifications

Tax Information. The amount subject to tax at vesting may partially be dependent upon a valuation of Shares from a Merchant Banker in India. The Company has no responsibility or obligation to obtain the most favorable valuation possible nor obtain valuations more frequently than required under Indian tax law.

IRELAND

Notifications

Director Notification Requirement. If you are a director or a shadow director or secretary of an Irish affiliate of Ansys, pursuant to Section 53 of the Irish Company Act of 1990, and you own more than a 1% interest in Ansys, you must notify the Irish affiliate of Ansys in writing within five business days of receiving or disposing of an interest in Ansys (e.g., stock options, RSUs, shares, etc.) or within five business days of the event giving rise to the notification requirement, or within five days of becoming a director, shadow director or secretary if such an interest exists at that time. This notification requirement also applies with respect to the interests of a spouse or minor child, whose interests will be attributed to the director, shadow director or secretary.

ITALY

Notifications

Exchange Control Information. By September 30th of each year, the Participants are required to report on their annual tax return (Form RW) any foreign investments (including proceeds from the sale of Shares acquired upon vesting) held outside of Italy if the investment may give rise to income in Italy. However, deposits and bank accounts held outside of Italy only need to be disclosed if the value of the assets exceeds €10,000 during any part of the tax year.

With respect to Shares received upon vesting of the Restricted Stock Units, the Participants must report (i) the value of the Shares at the beginning of the year or on the day the Participant acquired the Shares, whichever is later; and (ii) the value of the Shares when sold, or if the Participant still owns the Shares at the end of the year, the value of the Shares at the end of the year. The value to be reported is the fair market value of the Shares on the applicable dates mentioned above.

JAPAN

Notifications

Exchange Control Information. If you acquire Shares valued at more than ¥100,000,000 in a single transaction, you must file a Securities Acquisition Report with the Ministry of Finance through the Bank of Japan within 20 days of the acquisition of the Shares.

POLAND

Notifications

Exchange Control Information. While you are responsible for any exchange control filings, no advance foreign exchange permit is required for the acquisition, holding or disposal of Shares. However, if the value of your Shares exceeds the equivalent of PLN 7,000,000, you will have to notify the National Bank of Poland of such holdings on a quarterly basis. If such reporting obligation applies to you and your shareholding exceeds 10% of the Company’s total voting stock, you will also be required to notify the National Bank of Poland by the end of May of each subsequent year.

Exchange Control Information. If a Polish resident transfers funds in excess of €15,000 into Poland, the funds must be transferred via a Polish bank account or financial institution. Polish residents are required to retain the documents connected with a foreign exchange transaction for a period of five years, as measured from the end of the year in which such transaction occurred.

SINGAPORE

Notifications

Director Notification Requirement - If you are a director, associate director or shadow director of a Singapore affiliate of the Company, you are subject to certain notification requirements under the Singapore Companies Act. Among these requirements is an obligation to notify the Singaporean affiliate in writing when you receive an interest in shares (e.g., RSUs or Shares) in the Company or any related companies. In addition, you must notify the Singapore affiliate when you sell Shares or any related company (including when you sell Shares acquired through vesting of your RSU or pursuant to any other Award granted under the Plan). These notifications must be made within two business days of acquiring or disposing of any interest in shares of the Company or any related company. In addition, a notification must be made of your interests in shares of the Company or any related company within two business days of becoming a director.

Securities Law Information - The grant of the Awards is being made pursuant to the “Qualifying Person” exemption” under section 273(1)(f) of the Securities and Futures Act (Chapter 289, 2006 Ed.) (“SFA”). As a result, the grant is exempt from the prospectus and registration requirements under Singaporean law and is not made with a view to the underlying Shares being subsequently offered for sale to any other party. The Plan has not been, and will not be, lodged or registered as a prospectus with the Monetary Authority of Singapore.

SOUTH KOREA

Notifications

Exchange Control Information. If you receive US$500,000 or more from the sale of underlying Shares, Korean exchange control laws require you to repatriate the proceeds to South Korea within 18 months of sale.

SPAIN

Notifications

Exchange Control Information. All acquisitions of foreign shares by Spanish residents must comply with exchange control regulations in Spain. Because of foreign investment requirements, the acquisition of Shares upon vesting of the Restricted Stock Units must be declared for statistical purposes to the Spanish Direccion General de Politica Comercial y de Inversiones Extranjeras (the “DGPCIE”). If you acquire Shares through the use of a Spanish financial institution, that institution will automatically make the declaration to the DGPCIE for you. Otherwise, you must make the declaration by filing a form with the DGPCIE.

If you import the Shares acquired upon vesting of the Restricted Stock Units into Spain, you must declare the importation of the share certificates to the DGPCIE.

In addition, you must also file a declaration of the ownership of the Shares with the Directorate of Foreign Transactions each January while the shares are owned. These filings are made on standard forms furnished by the Directorate of Foreign Transactions.

When you receive any foreign currency payments (i.e., as a result of the sale of the Shares), you must inform the institution receiving the payment of the basis upon which such payment is made and provide certain specific information (e.g., name, address, and fiscal identification number; the name and corporate domicile of the company; the amount of the payment; the type of foreign currency received; the country of origin; and the reason for the payment).

Tax Reporting. If you hold assets (e.g., cash or shares in a bank or brokerage account) or rights outside Spain that exceed €50,000 per type of asset, you must file a Form 720 with the Spanish Tax Authorities by April 30th of each year.

SWITZERLAND

Notifications

Securities Law Information. The offer of the Restricted Stock Units is considered a private offering in Switzerland and is not subject to registration in Switzerland.

TAIWAN

Notifications

Exchange Control Information. Taiwan’s foreign exchange control regulations may have an impact on the grant and vesting of the Restricted Stock Units as well as the repatriation of capital gains realized from the holding or sale of the underlying Shares. Under current foreign exchange regulations, a Taiwanese resident can remit up to US $5 million (or an equivalent amount of other foreign currencies) per year into or out of Taiwan without prior approval from the Taiwan Central Bank.

If the transaction amount is TWD500,000 or more in a single transaction, you must submit a Foreign Exchange Transaction Form. If the transaction amount is US$500,000 or more in a single transaction, you must also provide supporting documentation to the satisfaction of the remitting bank.

UNITED KINGDOM

Terms and Conditions

(i) Purpose. This section is to modify those provisions of the Plan in order for awards made under the Plan, and communications concerning those awards, to be exempt from provisions of the United Kingdom Financial Services and Markets Act 2000 (the "FSMA").

(ii) Application. These provisions shall be used solely to grant awards to employees of the Company or any member of the same group as the Company resident and providing services in the United Kingdom. (The term "group" in relation to the Company shall bear the meaning given to such term in section 421 of the FSMA.)

(iii) Restricted Delivery of Awards. Payments of benefits under these provisions shall be made only in Shares or such other securities of the Company that may arise from such Shares under the adjustment provisions of the Plan. For the avoidance of doubt, and without limitation, no cash settlement of awards (including dividends or dividend equivalent payments in cash) shall be permissible.

(iv) Exercise of Restricted Stock Units/Vesting of Awards. The Administrator may specify, in its discretion, any other conditions of exercise and/or vesting of awards that will be specified in the award agreement.

(v) Restricted Transfer of Rights. The persons to whom rights under awards may be assigned or transferred, whether by will or the laws of descent and distribution or any transferability of awards shall be limited to a Participant's children and step-children under the age of eighteen, spouses and surviving spouses and civil partners and civil partners (within the meaning of the United Kingdom Civil Partnerships Act 2004) and surviving partners.

(vi) Tax. All awards will be subject to tax withholding and all references to "tax" shall be read and construed as including, without limitation, United Kingdom income tax and primary class 1 (employee's) national insurance contributions that the Participant's employer is liable to account for and, if so agreed between the Company and the Participant, secondary class 1 (employer's) national insurance contributions that the Participant's employer is liable to account for.

1