UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10−Q

(Mark One)

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended: September 30, 2014

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File No. 000-30183

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS

LIMITED

(Exact Name of Registrant as Specified in Its

Charter)

| NEW YORK | 13-3874771 |

| (State or other jurisdiction of | (I.R.S. Empl. Ident. No.) |

| incorporation or organization) |

8/F East Area

Century Golden Resources Business

Center

69 Banjing Road

Haidian District

Beijing, People’s Republic of China, 100089

(Address of Principal Executive Offices)

+86-10-884-52568

(Registrant’s

Telephone Number, Including Area Code)

Check whether the issuer (1) filed all reports required to be

filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or

for such shorter period that the registrant was required to file such reports),

and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such

shorter period that the registrant was required to submit and post such files).

Yes [X] No [ ]

Indicate by check mark whether the registrant is a larger accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one)

Large accelerated filer [ ] Accelerated filer [ ] Non-accelerated filer [ ] Smaller reporting company [X]

Indicate by check mark whether the registrant is a shell

company (as defined in Rule 12b-2 of the Exchange Act).

Yes [

] No [X]

The numbers of shares outstanding of each of the issuer’s classes of common equity, as of November 12, 2014 are as follows:

| Class of Securities | Shares Outstanding |

| Common Stock, $0.01 par value | 77,655,862 |

TABLE OF CONTENTS

Part I – FINANCIAL INFORMATION

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

CONSOLIDATED FINANCIAL STATEMENTS

September 30, 2014

2

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

| September 30, | December 31, | |||||

| ASSETS | 2014 | 2013 | ||||

| Current assets | ||||||

| Cash and cash equivalents | $ | 10,237 | $ | 20,715 | ||

| Inventories | 397,348 | 400,924 | ||||

| Account receivalbes | 22,508 | 21,073 | ||||

| Other receivables | 8,004 | 10,160 | ||||

| Deposits and prepayments | 27,019 | 15,869 | ||||

| Total current assets | 465,116 | 468,741 | ||||

| Investment | 11,096 | 11,198 | ||||

| Property, plant and equipment (net) | 345,306 | 377,455 | ||||

| $ | 821,518 | $ | 857,394 | |||

| LIABILITIES AND EQUITY | ||||||

| Current liabilities | ||||||

| Accounts payable | $ | 5,626 | $ | 5,706 | ||

| Accrued liabilities | 166,408 | 167,514 | ||||

| Due to directors | 654,763 | 435,110 | ||||

| Due to related parties | 395,444 | 344,536 | ||||

| Other payables | 365,645 | 310,061 | ||||

| Total current liabilities | 1,587,886 | 1,262,927 | ||||

| Equity | ||||||

| Common

stock: par value $.01; 200,000,000 shares

authorized; 77,655,862 shares issued and outstanding |

776,558 | 776,558 | ||||

| Additional paid-in capital | 28,877,540 | 28,877,540 | ||||

| Deficit accumulated during the development stage | (30,641,628 | ) | (30,286,940 | ) | ||

| Accumulated other comprehensive income | 175,106 | 158,216 | ||||

| Total China Longyi stockholders' equity | (812,424 | ) | (474,626 | ) | ||

| Noncontrolling interest | 46,056 | 69,093 | ||||

| Total Equity | (766,368 | ) | (405,533 | ) | ||

| $ | 821,518 | $ | 857,394 |

See notes to consolidated financial statements

3

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(A

DEVELOPMENT STAGE COMPANY)

CONSOLIDATED STATEMENTS OF OPERATIONS AND

COMPREHENSIVE LOSS (UNAUDITED)

| Nine months ended | Three months ended | Period from Jun 4,1997 | |||||||||||||

| September 30, | September 30, | (inception) to | |||||||||||||

| 2014 | 2013 | 2014 | 2013 | September 30, 2014 | |||||||||||

| Revenues | |||||||||||||||

| Sales | $ | - | $ | 11,095 | $ | - | $ | 680 | $ | 1,027,204 | |||||

| Cost of sales | - | 7,409 | - | 406 | $ | 1,040,259 | |||||||||

| Gross margin | - | 3,686 | - | 274 | $ | (13,055 | ) | ||||||||

| Operating expenses | |||||||||||||||

| General and administrative expenses | 367,795 | 366,165 | 105,066 | 99,751 | $ | 19,571,638 | |||||||||

| Goodwill impairment loss | - | - | - | - | $ | 5,408,584 | |||||||||

| Write-off inventory and bus licenses | - | - | - | - | $ | 3,322,712 | |||||||||

| Research and development costs | - | - | - | $ | 8,880,206 | ||||||||||

| 367,795 | 366,165 | 105,066 | 99,751 | $ | 37,183,140 | ||||||||||

| Loss from operations | (367,795 | ) | (362,479 | ) | (105,066 | ) | (99,477 | ) | $ | (37,196,195 | ) | ||||

| Other income (expense) | |||||||||||||||

| Interest income | 16 | 23 | 9 | (8 | ) | $ | 325,703 | ||||||||

| Other income (expense) | 5,202 | - | 1,730 | - | $ | 1,253,413 | |||||||||

| Transaction exchange gain | (15,900 | ) | 21,404 | (14,988 | ) | 1,738 | $ | 1,073,983 | |||||||

| Gain on asset disposal | - | - | - | - | $ | 1,172 | |||||||||

| Gain on debt settlement | - | - | - | - | $ | 156,018 | |||||||||

| Gain on disposal subsidiary | - | - | - | - | $ | 4,093,455 | |||||||||

| Interest expense | - | - | - | $ | (712,302 | ) | |||||||||

| (10,682 | ) | 21,427 | (13,249 | ) | 1,730 | $ | 6,191,442 | ||||||||

| Loss before income tax expense and noncontrolling interest | (378,477 | ) | (341,052 | ) | (118,315 | ) | (97,747 | ) | $ | (31,004,753 | ) | ||||

| Income tax expense | - | - | - | - | $ | - | |||||||||

| Net loss | (378,477 | ) | (341,052 | ) | (118,315 | ) | (97,747 | ) | $ | (31,004,753 | ) | ||||

| Less: Net loss attributable to noncontrolling interest | 23,789 | 28,912 | 8,151 | (9,563 | ) | $ | 363,125 | ||||||||

| Net loss attributable to China Longyi | $ | (354,688 | ) | $ | (312,140 | ) | $ | (110,164 | ) | $ | (107,310 | ) | $ | (30,641,628 | ) |

| Basic and diluted loss per share | $ | (0.00 | ) | $ | (0.00 | ) | $ | (0.00 | ) | $ | (0.00 | ) | |||

| Weighted average number of shares outstanding-basic and diluted | 77,655,862 | 77,655,862 | 77,655,862 | 77,655,862 | |||||||||||

| Comprehensive loss | |||||||||||||||

| Net loss | $ | (378,477 | ) | $ | (341,052 | ) | $ | (118,315 | ) | $ | (97,747 | ) | $ | (31,004,753 | ) |

| Foreign currency translation adjustment | 17,642 | (18,465 | ) | 26,938 | (1,791 | ) | |||||||||

| Comprehensive loss | (360,835 | ) | (359,517 | ) | (91,377 | ) | (99,538 | ) | |||||||

| Comprehensive loss attributable to noncontrolling interest | (23,037 | ) | (29,903 | ) | (8,151 | ) | (9,760 | ) | |||||||

| Comprehensive loss attributable to China Longyi | $ | (337,798 | ) | $ | (329,614 | ) | $ | (83,226 | ) | $ | (89,778 | ) | |||

See notes to consolidated financial statements

4

CHINALONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| Nine months ended September 30, | Period from Jun 4, 1997 | ||||||||

| 2014 | 2013 | (inception) to 09.30, 2014 | |||||||

| Cash flows from operating activities: | |||||||||

| Net loss | $ | (378,477 | ) | $ | (341,052 | ) | $ | (31,004,753 | ) |

| Adjustments to reconcile net loss to net cash used in operations: | |||||||||

| Depreciation and amortization | 28,777 | 28,583 | 1,315,591 | ||||||

| Loss on sales of property and equipment | - | 9,873 | |||||||

| Impairment loss for fixed assets | - | - | 1,052,950 | ||||||

| Write-off goodwill and inventory | - | - | 7,101,506 | ||||||

| Stock issued for services and debt | - | - | 1,869,100 | ||||||

| (Gain) loss on disposition in subsidiary | - | - | (3,882,796 | ) | |||||

| Research and development expenses recorded in organization | - | - | 8,612,730 | ||||||

| Reorganization expenses recorded in organization | - | - | 455,830 | ||||||

| Changes in operating assets and liabilities: | |||||||||

| Accounts receivalbes | (1,628 | ) | 165,669 | (19,226 | ) | ||||

| Other receivables | 2,080 | (92 | ) | 5,325,578 | |||||

| Due from related parties | - | (4,350 | ) | 31,486 | |||||

| Interest receivable | - | - | 17,667 | ||||||

| Deposits and prepayment | (11,309 | ) | 35 | 682,914 | |||||

| Inventory | (47 | ) | 3,936 | (822,364 | ) | ||||

| Other payables | 57,995 | 87,850 | (212,223 | ) | |||||

| Due to related parties | 53,362 | 36,597 | 107,938 | ||||||

| Accounts payable and accrued liabilities | (28 | ) | 611 | (3,320,211 | ) | ||||

| Net cash used in operations | (249,275 | ) | (22,213 | ) | (12,678,410 | ) | |||

| Cash flows from investing activities: | |||||||||

| Reorganization - net of cash acquired | - | - | (320,579 | ) | |||||

| Purchase of subsidiaries | - | - | (1,690,474 | ) | |||||

| Redemption of short term investment | - | - | 665,092 | ||||||

| Purchase of investment | - | - | - | ||||||

| Purchases of intangible assets | - | - | (833,357 | ) | |||||

| Purchases of property and equipment | - | (1,512 | ) | (521,239 | ) | ||||

| Purchases of construction in progress | - | - | (169,081 | ) | |||||

| Sales of property and equipment | - | - | 701,100 | ||||||

| Deposit on subsidiary | - | - | (10,922 | ) | |||||

| Net cash provided by (used in) investing activities | - | (1,512 | ) | (2,179,460 | ) | ||||

| Cash flows from financing activities: | |||||||||

| Addition of short term loans | - | - | 1,612 | ||||||

| Collecttion from shareholders | - | - | 503,171 | ||||||

| Payments to stockholders | - | - | (1,634,763 | ) | |||||

| Proceeds from issuance of stock | - | - | 13,149,845 | ||||||

| Proceeds from convertible promissory note | - | - | 3,128,225 | ||||||

| Dividends paid | - | - | (1,000,000 | ) | |||||

| Proceeds to notes payable | - | - | 649,492 | ||||||

| Payments on notes payable | - | - | (612,582 | ) | |||||

| Proceeds (repayments) loans from directors | 222,970 | 45,036 | 531,616 | ||||||

| Net cash provided by financing activities | 222,970 | 45,036 | 14,716,616 | ||||||

| Effect of foreign exchange rate fluctuation | 15,827 | (21,191 | ) | 151,491 | |||||

| Increase(decrease) in cash and cash equivalents | (10,478 | ) | 120 | 10,237 | |||||

| Cash and cash equivalents, beginning of period | 20,715 | 11,916 | - | ||||||

| Cash and cash equivalents, end of period | $ | 10,237 | $ | 12,036 | $ | 10,237 | |||

| Supplemental disclosures of cash flow information: | |||||||||

| Cash paid for interest | $ | - | $ | - | $ | - | |||

| Cash paid for income taxes | $ | - | $ | - | $ | - | |||

See notes to consolidated financial statements

5

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

The accompanying unaudited interim consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“US GAAP”) for financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by US GAAP for annual financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. The consolidated financial statements of China Longyi Group International Holdings Limited (the “Company” or “China Longyi”) include the accounts of China Longyi and its wholly-owned and majority-owned subsidiaries. All material intercompany accounts and transactions have been eliminated in consolidation.

| 1. |

BUSINESS DESCRIPTION AND ORGANIZATION |

|

BUSINESS | |

|

Overview of Our Business | |

|

We are a holding company that only operates through our indirect Chinese subsidiaries Beijing SOD and Chongqing SOD. Through our Chinese subsidiaries, we develop, manufacture and market our SOD products in China. SOD is a naturally occurring enzyme which may act as a potent antioxidant defense in cells that are exposed to oxygen. Certain research has shown that under certain biological conditions, SOD revitalizes cells and reduces the rate of cell destruction. It neutralizes the most common free radical—superoxide radical—by converting it into hydrogen peroxide and water. Because superoxide is harmful to human cells, and certain forms of SOD exist naturally in most humans, many studies show that SOD is valuable in protecting human cells from the harmful effects of superoxide. SOD is thought to be more powerful than antioxidant vitamins as it activates the body's productions of its own antioxidants. As a result, SOD is referred to as the “enzyme of life.” Commercially, SOD has a wide range of applications and is widely applied in foods, drinks, skin care productions, pharmaceuticals, to combat ailments ranging from sunburn to rheumatoid arthritis. | |

|

History and Corporate Structure | |

|

We are a New York corporation that was incorporated on February 29, 1996, as United Network Technologies, Inc. and we changed our name to Panagra International Corporation on October 2, 1998. From our inception until 2001, we were relatively inactive with limited operations. On August 2, 2001 we changed our name to Minghua Group International Holdings Limited and at that time we also increased the authorized common shares of our common stock from 40,000,000 shares to 200,000,000 shares. On October 16, 2007, we effectuated a 1-for-20 reverse stock split of all our issued and outstanding shares of common stock, or the Reverse Split, and changed our name to China Longyi Group International Holdings Limited. | |

|

Reverse Acquisition | |

|

In June 2001 we formed Minghua Acquisition Corp., a Delaware corporation, and acquired all the equity interests of Minghua Group International Holding (Hong Kong) Limited, or Minghua Hong Kong, a Hong Kong limited company formed on June 4, 1997, for a purchase price of $1,000,000 in cash and 28,000,000 (pre Reverse Split) shares of our common stock. The shares received by the Minghua Hong Kong shareholders equaled 70% of our issued and outstanding shares of common stock, resulting in a change of control to the Minghua Hong Kong shareholders. |

6

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

| 1. |

BUSINESS DESCRIPTION AND ORGANIZATION(Continued) |

|

At that time, the sole asset of Minghua Hong Kong was an 85% equity interest in the Shenzhen Minghua Environmental Protection Vehicle Co., Ltd., or Minghua EPV, a PRC corporation. The remaining 15% equity minority interest in China Minghua EPV was owned by a related party, Asia Key Group Limited, through its wholly-owned subsidiary Minghua Real Estate (Shenzhen) Ltd., formerly known as Minghua Investment Co., Ltd., or Minghua Real Estate. On January 29, 2004, the Company acquired this 15% minority interest held by Minghua Real Estate, in a related party transaction by paying $990,638 in cash and issuing 28,210,000 (prereverse split) shares of our common stock. Through Minghua EPV, our business became the development and commercialization of mass transit, hybrid electric vehicles, primarily buses. | |

|

Acquisition of the Bus Installation Company | |

|

On March 13, 2003, our indirect subsidiary, Ming Hua Environmental Protection Science and Technology Limited, a Hong Kong limited company, or Minghua Science, acquired an 89.8% equity interest in the Guangzhou City View Bus Installation Company, or the Bus Installation Company, through its acquisition of Good View Bus Manufacturing (Holdings) Company Limited, a Hong Kong limited company and Eagle Bus Development Limited, a Hong Kong limited company, which own 23.8% and 66% of the Bus Installation Company, respectively. The Bus Installation Company manufactured motor coaches for domestic sale in China and for export under the “Eagle” brand name. We sold 6 standard diesel buses in 2005 and 5 standard diesel buses in 2004, however, once we sold off the inventory of diesel buses and parts that we acquired along with our acquisition of the Bus Installation Company, we no longer sold or manufactured diesel buses. | |

|

Acquisition of Beijing Cardinal | |

|

On June 16, 2004, Minghua Hong Kong formed a wholly owned subsidiary in the PRC, named Beijing China Cardinal Real Estate Consulting Co., Ltd., or Beijing Cardinal. We intended to use Beijing Cardinal as a vehicle to make future real estate investments in the PRC. However, at December 31, 2006, Beijing Cardinal had not begun significant operations. | |

|

Sale of Environmental Vehicle Business | |

|

Through Minghua Hong Kong, we had been focused on the development and commercialization of mass transit, hybrid electric vehicles, primarily buses. However, although prototype hybrid vehicles and a limited number of other vehicles have been produced, we have not been able to successfully commercialize these vehicles. As a result, on September 28, 2006, we disposed of our entire interests in Minghua Hong Kong and Minghua Science to Messrs. Han Lian Zhong and Niu Rui Cheng for 1 HK$, in exchange for their assumption of Minghua Hong Kong and Minghua Science’s debt. However, we retained our interests in China Cardinal, which were transferred to our subsidiary, Euromax International Investments Limited, or Euromax, and in the Guangzhou City View Bus Installation Company, which was transferred to our subsidiary, Top Team Holdings Limited (BVI), or Top Team. |

7

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

| 1. |

BUSINESS DESCRIPTION AND ORGANIZATION(Continued) |

|

Qiang Long Investment | |

|

On January 29, 2004, we entered into a subscription agreement with Qiang Long Real Estate Development Co., Ltd., or Qiang Long, a PRC company, pursuant to which, as amended and supplemented from time to time, Qiang Long was obligated to purchase 140,000,000 (pre reverse split) shares of our common stock, par value $0.01 at an aggregate purchase price of US$29,400,000, or $0.21 per share. An amount equaling US$653,795 was paid to us as a performance bond and an additional US$632,911 was paid to us in 2006 in exchange for 3,013,862 (pre reverse split) shares. The balance of US$28,113,294 was to be paid in full by June 30, 2007, for the remaining 136,986,138 (pre reverse split) shares. On June 29, 2007, we consummated our obligations under the contract, pursuant to a letter agreement between the Company and Qiang Long. Pursuant to the letter agreement, we acknowledged our receipt of the final payment in cash from Qiang Long as fulfillment of Qiang Long’s investment obligation, and agreed to issue 50,000,000 (pre reverse split) shares to Qiang Long on or before July 23, 2007, and the remaining 86,986,138 (pre reverse split) shares within fifteen (15) business days following the effective date of an amendment to our Certificate of Incorporation to effect a one-for-twenty reverse split of our outstanding common stock, which will be equal to 4,349,307 shares post-reverse split. Accordingly, on August 2, 2007, 50,000,000 shares were issued to Qiang Long. | |

|

As a result of the closing of the investment transaction with Qiang Long, our Chairman, Mr. Changde Li, now beneficially owns and controls 155,000,000 (pre reverse split) shares (7,750,000 shares post-reverse split) or 54.0% of the Company’s issued and outstanding common stock, 15,000,000 (pre reverse split) of which he holds indirectly through Qiang Long, 136,986,137 (pre reverse split) of which he holds indirectly through Qiang Long’s affiliate, Jolly Concept Management Limited, a BVI company, and 3,013,863 (pre reverse split) of which he holds through Qiang Long’s affiliate, Chinese Dragon Heritage Investment Management Limited, a PRC company. | |

|

Acquisition of Top Time | |

|

From the time when we sold the 6 standard diesel buses in the first quarter of 2005 until November 12, 2007 when we completed the acquisition transaction with Daykeen Group Limited, or Daykeen, discussed herein, we had limited operations and did not engage in active business operations other than our search for, and evaluation of, potential business opportunities for acquisition or participation. | |

|

On November 12, 2007, we completed an acquisition transaction with Top Time International Limited, a Hong Kong Company, or Top Time, whereby we paid Daykeen, Top Time’s sole shareholder, a total consideration of $54.9 million (RMB 407 million, based on an exchange ratio of $1=RMB 7.414) in exchange for 100% ownership of Top Time, consisting of $30 million in cash and $24.9 million in shares of our common stock issuable within 90 days of the closing. $30 million of cash was paid to Daykeen by three transactions, Beijing Cardinal, De Qiu Hong, and Mr. Chen Zhiping paid $29 million, $0.4 million, and $0.6 million on behalf of the Company, respectively. As a result, the Company offset the same amounts of balance of the three parties’ current accounts. The equity portion of the purchase price amounts to a total of 62,250,000 (post reverse split) shares of our common stock (based upon $0.02/share, the average of the closing price of the Company’s common stock on the OTCBB for the 365 calendar days prior to May 31, 2007, which was adjusted for our stock split which occurred on October 16, 2007 and resulted an effective purchase price of $0.40 per share). Top Time thereby became our wholly owned subsidiary and Daykeen will become our controlling stockholder upon our issuance to Daykeen of the equity portion of the purchase price in accordance with the Share Purchase Agreement. |

8

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

| 1. |

BUSINESS DESCRIPTION AND ORGANIZATION(Continued) |

|

Top Time was incorporated in Hong Kong in December 2006 and currently has two subsidiaries: Beijing SOD and Chongqing SOD. Beijing SOD was incorporated in China in March 2005 and is 90% owned by Top Time and 10% owned by Ms. Ran Wang. | |

|

For accounting purposes, the acquisition of Top Time was treated as a reorganization of entities under common control. When we refer in this report to business and financial information for periods prior to the consummation of the acquisition, we are referring to the business and financial information of Top Time on a consolidated basis unless the context suggests otherwise. | |

|

Sale of Top Team Subsidiaries | |

|

Through acquisition of Top Time, our business became the development, manufacture and sale of SOD products. As a result, on November 28, 2007, we disposed of five subsidiaries held by Top Team Holdings Limited (BVI): Euromax International Investments Limited, Beijing China Cardinal Real Estate Consulting Co., Ltd, Eagle Bus Development Limited (HK), Good View Bus Manufacturing Company Limited (HK), and Guangzhou City View Bus Installation Company Limited (PRC), to Mr. Zhiping Cheng, for an aggregate sale price of RMB5,000,000 (approximately $715,000). | |

|

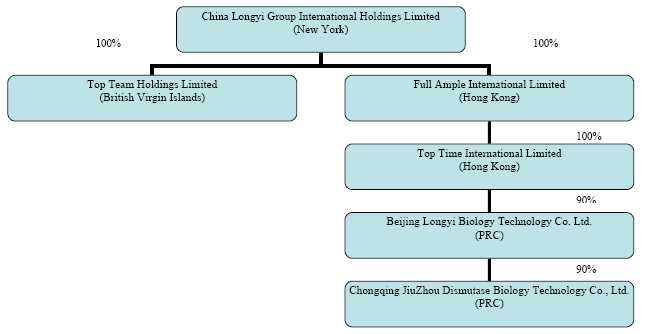

The following chart reflects our organizational structure as of the date of this report. |

According to all reasonably circumstances facing the company, the management prepared the financial report on the development stage company basis.

9

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

| 1. |

BUSINESS DESCRIPTION AND ORGANIZATION (Continued) |

|

CAPITAL RESOURCES AND BUSINESS RISKS | |

|

The Company remains in the development stage and only operates through indirect Chinese subsidiaries Beijing SOD and Chongqing SOD. Through Chinese subsidiaries, we develop, manufacture and market our SOD products in China. SOD is a naturally occurring enzyme which may act as a potent antioxidant defense in cells that are exposed to oxygen. All of the company’s future business operations are subject to all of the risks inherent in the establishment of a new business enterprise. The Company has no proven revenue stream from the sales of its products. Additional capital resources through current and future offerings of securities will be needed in order to accomplish the Company's present marketing, development and manufacturing plans. The manufacturing facility and other operations in China, as well as the business financial conditions and results of operations are, to a significant degree, subject to economic, political and social events in China. | |

|

The Company had incurred losses since inception and had working capital deficiency of $1,122,770 as at September 30, 2014 (December 31, 2013: deficiency of $794,186). There exits substantial doubt about the Company’s ability to continue as a going concern, which contemplated the realization of assets and the payment of liabilities in the ordinary course of business. To alleviate the situation, management obtained $28,113,294 in funding through the issuance of additional stock to one of the Company’s shareholders on July 27, 2007. On November 12, 2007, the Company completed an acquisition transaction with Top Time whereby it paid Daykeen, Top Time’s sole shareholder, a total consideration of $54.9 million, in exchange for 100% ownership of Top Time, consisting of $30 million in cash and $24.9 million in shares of our common stock issuable within 90 days of the closing. The equity portion of the purchase price amounts to a total of 62,250,000 post reverse split shares of the Company’s common stock. | |

|

On July 27, 2007, the Company instructed the prior Transfer Agent to issue the 2,500,000 post reverse split shares of common stock deliverable to Qiang Long in the name of Jolly Concept Management Limited, in accordance with Qiang Long’s instructions. On December 14, 2007, the Company instructed present Transfer Agent to issue the replacement certificate showing the new name of the company and the correct number of shares, post reverse-split, and the remaining 4,349,307 shares of common stock issuable to Qiang Long, to Jolly Concept Management Limited and to Zhang, Lifang. The Company also agreed to issue 1,131,026 shares of common stock post-reverse-split to Luck Pond Enterprises Limited or its designee, for its services as finder in connection with the Qiang Long investment. On December 14, 2007, the Company instructed present Transfer Agent to issue the total amount of 62,250,000 shares of the Company’s common stock, post-reverse-split, issuable to Daykeen, to Daykeen Investment Limited. | |

|

As of September 30, 2014 the Company has accumulated deficit from recurring net loss of $30,641,628 and cash and cash equivalent of $10,237. The application of the going concern basis of presentation assumes that the Company will continue in operation for the foreseeable future and be able to realize its assets and discharge its liabilities and commitments in the normal course of business. There is, primarily as a result of the conditions described above, substantial doubt as to the appropriateness of the use of the going concern assumption. The accompanying financial statements have been prepared on a going concern basis notwithstanding these conditions. | |

|

The ability of the Company to continue as a going concern is dependent on its ability to generate sufficient positive cash flows from future operations and the continued funding from the Company’s major shareholders. If the going concern basis were not appropriate for these financial statements, then adjustments would be necessary to the carrying values of assets and liabilities, the reported revenues and expenses, and the balance sheet classifications used. |

10

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

| 1. |

BUSINESS DESCRIPTION AND ORGANIZATION (Continued) |

|

RESTRICTIONS ON TRANSFER OF ASSET OUT OF CHINA | |

|

Dividend payments by the Company’s operating subsidiaries are limited by certain statutory regulations in China. No dividends may be paid by these subsidiaries without first receiving prior approval from the State Administration of Foreign Exchange. Dividend payments are restricted to 85% of profits, after tax. Repayments of loans or advances from subsidiaries to China Longyi, unless certain conditions are met, will be restricted by the Chinese government. | |

|

CONTROL BY PRINCIPAL STOCKHOLDERS | |

|

The directors, executive officers, affiliates and related parties own, beneficially and in the aggregate, the majority of the voting power of the outstanding shares of the common stock of the Company. Accordingly, if they voted their shares uniformly, directors, executive officers and affiliates would have the ability to control the approval of most corporate actions, including increasing the authorized capital stock of China Longyi and the dissolution, merger or sale of the Company's assets. | |

| 2. |

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

|

PRINCIPLES OF CONSOLIDATION AND BASIS OF PRESENTATION | |

|

The consolidated financial statements for all periods presented include the financial statements of China Longyi Group International Holdings Limited, and its subsidiaries Top Team Holdings Limited, Full Ample Group Limited (Daykeen Group, BVI), Top Time International Limited (HK), Beijing SOD, and Chongqing SOD. The consolidated financial statements have been prepared in accordance with US GAAP. All significant intercompany accounts and transactions have been eliminated. | |

|

The Company has determined the People’s Republic of China Chinese Yuan Renminbi (“RMB”) to be its functional currency. The accompanying consolidated financial statements are presented in United States (US) dollars. The consolidated financial statements are translated into US dollars from RMB at year-end exchange rates for assets and liabilities, and weighted average exchange rates for revenues and expenses. Capital accounts are translated at their historical exchange rates when the capital transactions occurred. | |

|

RMB is not freely convertible into the currency of other nations. All such exchange transactions must take place through authorized institutions. There is no guarantee the RMB amounts could have been, or could be, converted into US dollars at rates used in translation. | |

|

NONCONTROLLING INTEREST IN SUBSIDIARIES | |

|

The Company owns 90% of the equity interests in Beijing SOD, and the remaining 10% is owned by Miss Ran Wang. Therefore, the Company records noncontrolling interest expense to allocate 10% of the loss of the Beijing SOD to Miss Ran Wang, its noncontrolling shareholder. | |

|

The Company owns 81% of the equity interest in Chongqing SOD of which 9% is owned by Miss Ran Wang, and the remaining 10% by Mr. Guoqing Tan. Therefore, the Company records noncontrolling interest charge in the statement of operations to allocate 19% of the results of operations of Chongqing SOD to its noncontrolling shareholders. |

11

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

| 2. |

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) |

|

USE OF ESTIMATES | |

|

The preparation of financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. | |

|

SIGNIFICANT ESTIMATES | |

|

Several areas require significant management estimates relating to uncertainties for which it is reasonably possible that there will be a material change in the near term. The more significant areas requiring the use of management estimates related to determination of net realizable value of inventory, allowance for doubtful accounts, property and equipment, accrued liabilities, and the useful lives for depreciation. | |

|

REVENUE RECOGNITION | |

|

Revenues are recognized as earned when the following four criteria are met: (1) a customer issues a purchase order or otherwise agrees to purchase products; (2) products are delivered to the customer; (3) pricing is fixed or determined in accordance with the purchase order or agreement; and (4) collectability is reasonably assured. | |

|

PROPERTY AND EQUIPMENT | |

|

Impairment of long-lived assets is recognized when events or changes in circumstances indicate that the carrying amount of the asset, or related groups of assets, may not be recoverable. Under the provisions of SFAS No. 144, “Accounting for the Impairment of Long-Lived Assets and for Long-Lived Assets to Be Disposed Of”, the Company recognizes an “impairment charge” when the expected net undiscounted future cash flows from an asset's use and eventual disposition are less than the asset's carrying value and the asset's carrying value exceeds its fair value. Measurement of fair value for an asset or group of assets may be based on appraisal, market values of similar assets or estimated discounted future cash flows resulting from the use and ultimate disposition of the asset or assets. | |

|

Expenditures for maintenance, repairs and betterments, which do not materially extend the normal useful life of an asset, are charged to operations as incurred. Upon sale or other disposition of assets, the cost and related accumulated depreciation are removed from the accounts and any resulting gain or income (loss) is reflected in income. | |

|

Depreciation and amortization are provided for financial reporting purposes primarily on the straight-line method over the estimated useful lives of the respective assets as follows: |

| Estimated | |

| Useful Life | |

| Transportation equipment | 5 years |

| Office, computer software and equipment | 5 years |

| Furniture and fixtures | 5 years |

| Production equipment | 10 years |

| Building and improvements | 20 years |

12

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

| 2. |

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) |

|

CASH AND CASH EQUIVALENTS | |

|

The Company invests idle cash primarily in money market accounts, certificates of deposits and short-term commercial paper. Money market funds and all highly liquid debt instruments with an original maturity of three months or less are considered cash equivalents. | |

|

INTANGIBLE ASSETS | |

|

The Company adopted the provisions of ASC Topic 350 (formerly SFAS No. 142, Goodwill and Other Intangible Assets), according to which goodwill and indefinite lived intangible assets are not amortized, but are reviewed annually for impairment, or more frequently, if indications of possible impairment exist. The Company has performed the requisite annual transitional impairment tests on intangible assets and made the impairment adjustments as necessary. All goodwill and indefinite lived intangible assets had been written down to zero in the prior years. | |

|

INCOME TAXES | |

|

Income tax expense is based on reported income before income taxes. Deferred income taxes reflect the effect of temporary differences between assets and liabilities that are recognized for financial reporting purposes and the amounts that are recognized for income tax purposes. In accordance with ASC Topic 740 (formerly SFAS No. 109, “Accounting for income taxes”) these deferred taxes are measured by applying currently enacted tax laws. | |

|

The Company did not provide any current or deferred income tax provision or benefit for any period presented to date because it has experienced operating losses since inception. The benefit of any tax income (loss) carry forwards is fully offset by a valuation allowance, as there is a more than fifty percent chance that the Company will not realize those benefits. | |

|

There are net operating loss carry forwards allowed under the Hong Kong and China Governments’ tax system. | |

|

RESEARCH AND DEVELOPMENT COSTS | |

|

Company sponsored research and development costs, related to both present and future products, are charged to operations when incurred and are included in operating expenses. Expenditures for research and development for the nine months period ended September 30, 2014 and 2013 were both $0 and a cumulative amount of $8,880,206 for the period from June 4, 1997 (inception) to September 30, 2014. | |

|

SHIPPING AND HANDLING | |

|

Costs relating to shipping and handling are part of general and administrative expenses in the consolidated statements of operations and comprehensive loss. Insignificant amount of shipping and handling costs incurred during the nine months ended September 30, 2014 and 2013. |

13

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

| 2. |

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) |

|

EARNING (LOSS) PER SHARE | |

|

Basic earning (loss) per common share ("LPS") is calculated by dividing net income (loss) by the weighted average number of common shares outstanding during the period. Diluted earning (loss) per common share is calculated by adjusting the weighted average outstanding shares, assuming conversion of all potentially dilutive stock options. | |

|

There were no stock options and potentially dilutive securities outstanding at September 30, 2014. | |

|

EQUITY BASED COMPENSATION | |

|

The Company accounts for employee stock options in accordance with ASC Topic 718, (formerly SFAS 123(R), “Share-Based Payment.”) which requires that share-based payment transactions be measured based on the grant-date fair value of the equity instrument issued and recognized as compensation expense over the requisite service period, or vesting period. The Company had no such compensation expense for the nine months ended September 30, 2014 and 2013. | |

|

COMPARATIVE FIGURES | |

|

Certain comparative figures have been reclassified in order to conform with the presentation adopted in the current period. | |

|

COMPREHENSIVE INCOME (LOSS) | |

|

The accompanying financial statements are presented in U.S. dollars. The functional currency is the RMB. The financial statements are translated into U.S. dollars from RMB at year-end exchange rates for assets and liabilities, and weighted average exchange rates for revenues and expenses. Capital accounts are translated at their historical exchange rates when the capital transactions occurred. Currency translation adjustments are presented as other comprehensive income. | |

|

RMB is not freely convertible into the currency of other nations. All such exchange transactions must take place through authorized institutions. There is no guarantee the RMB amounts could have been, or could be, converted into US dollars at rates used in translation. | |

| 3. |

LONG TERM INVESTMENT |

|

On January 5, 2010, the Company invested in Cangshan Duoha Vegetable Food Company (“Duoha”) with 50,000 shares of the Company’s common stock worth $10,000 as $0.2 per share to acquire 20% equity interest in of Duoha. According to the investment agreement, although we own 20% equity of Duoha, we do not have significant influence over Duoha’s operating and financing policies. Therefore, the management of the Company implemented the cost method to account above investment. |

14

CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED

(A

DEVELOPMENT STAGE COMPANY)

Notes to condensed consolidated financial

statements (Unaudited)

September 30, 2014

| 4. |

INCOME TAXES |

|

Net operating loss carry forwards are allowed under the Hong Kong and Chinese governments’ tax systems. In China, the previous five years’ net operating losses are allowed to be carried forward to offset future taxable income. In Hong Kong, net operating losses can be carried forward indefinitely to offset future taxable income. No deferred tax asset has been recognized due to the uncertainty of the Company having future taxable profits. | |

| 5. |

COMMITMENTS AND CONTINGENCIES |

|

From time to time, the Company has disputes that arise in the ordinary course of its business. Currently, according to management, there are no material legal proceedings to which the Company is a party to or to which any of their property is subject that will have a material adverse effect on the Company’s financial condition. | |

| 6. |

SUBSEQUENT EVENTS |

|

Management has considered all events occurring through November 14, 2014, the date the financial statements have been issued, and has determined that there are no such events that are material to the financial statement. |

15

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read in conjunction with our financial statements and the notes thereto.

Special Note Regarding Forward-Looking Statements

This Quarterly Report on Form 10-Q, including the following “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” contains “forward-looking statements” relating to the business of China Longyi Group International Holdings Limited and its subsidiary companies. The forward-looking statements include, among others, statements concerning our expected financial performance and strategic and operational plans, as well as all assumptions, expectations, predictions, intentions or beliefs about future events. These statements are based on assumptions and are subject to known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. Risks and uncertainties include risks related to new and existing products; any projections of sales, earnings, revenue, margins or other financial items; any statements of the plans, strategies and objectives of management for future operations; any statements regarding future economic conditions or performance; uncertainties related to conducting business in China; any statements of belief or intention; and any of the factors mentioned in the “Risk Factors” section of the Company’s annual report on Form 10-K filed on March 31, 2014. Given these uncertainties, you should not place undue reliance on these forward-looking statements. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

Use of Certain Defined Terms

Except as otherwise indicated by the context, references in this report to:

- “Beijing SOD” are references to Beijing Longyi Biology Technology Co. Ltd., our indirect, 90% owned subsidiary, a PRC company;

- “China” and “PRC” are references to the People’s Republic of China;

- “China Longyi,” “we,” “us,” “our,” or the “Company” are references to the combined business of China Longyi Group International Holdings Limited (formerly known as Minghua Group International Holdings Limited) and/or its consolidated subsidiaries, as the case may be;

- “Chongqing SOD” are references to Chongqing JiuZhou Dismutase Biology Technology Co., Ltd., our indirect, majority-owned subsidiary, a PRC company;

- “Exchange Act” mean the Securities Exchange Act of 1934, as amended;

- “RMB” refer to Renminbi, the legal currency of China;

- “Securities Act” mean the Securities Act of 1933, as amended;

- “Top Time” are references to Top Time International Limited, our indirect wholly-owned subsidiary, a Hong Kong company; and

- “U.S. dollar,” “$” and “US$” are to the legal currency of the United States.

Overview of our Business

We are a holding company that only operates through our indirect Chinese subsidiaries Beijing SOD and Chongqing SOD. Through our Chinese subsidiaries, we develop, manufacture and market our SOD products in China. SOD is a naturally occurring enzyme which may act as a potent antioxidant defense in cells that are exposed to oxygen. Certain research has shown that under certain biological conditions, SOD revitalizes cells and reduces the rate of cell destruction. It neutralizes the most common free radical—superoxide radical—by converting it into hydrogen peroxide and water. Because superoxide is harmful to human cells, and certain forms of SOD exist naturally in most humans, many studies show that SOD is valuable in protecting human cells from the harmful effects of superoxide. SOD is thought to be more powerful than antioxidant vitamins as it activates the body's productions of its own antioxidants. As a result, SOD is referred to as the “enzyme of life.” Commercially, SOD has a wide range of applications and is widely applied in foods, drinks, skin care productions, pharmaceuticals, to combat ailments ranging from sunburn to rheumatoid arthritis.

16

Third Quarter of 2014 Financial Performance Highlights

The following are some financial highlights for the three months ended September 30, 2014:

| • |

Revenue: Revenue decreased $680, to $0 for the three months ended September 30, 2014, from $680 for the same period in 2013. | |

| • |

Expense from operations: Expense from operations increased $5,315, or 5.33%, to $105,066 for the three months ended September 30, 2014, from $99,751 for the same period in 2013. | |

| • |

Net loss: Net loss increased $20,568, or 21%, to $(118,315) for the three months ended September 30, 2014, from $(97,747) for the same period in 2013. | |

| • |

Fully diluted net income per share: Fully diluted net loss per share was $0 for the three months ended September 30, 2014, as compared to $0 for the same period in 2013. |

Provision for Income Taxes

| • |

United States: China Longyi Group International Holding Limited is subject to United States tax at a tax rate of 34%. No provision for income taxes in the United States has been made as China Longyi Group International Holding Limited had no income subject to United States taxation in the third quarter of 2014. | |

| • |

British Virgin Islands: Our wholly owned subsidiary Top Team Holdings Limited was incorporated in the British Virgin Islands, or the BVI, and, under the current laws of the BVI, is not subject to income taxes. | |

| • |

China: Before the implementation of the enterprise income tax, or EIT, Foreign Invested Enterprises or FIEs, established in the PRC were generally subject to an EIT rate of 33.0%, which includes a 30.0% state income tax and a 3.0% local income tax. On March 16, 2007, the National People’s Congress of China passed the new Corporate Income Tax Law, or EIT Law, and on November 28, 2007, the State Council of China passed the Implementing Rules for the EIT Law, or Implementing Rules, which took effect on January 1, 2008. The EIT Law and Implementing Rules impose a unified EIT of 25.0% on all domestic- invested enterprises and FIEs, unless they qualify under certain limited exceptions. Therefore, nearly all FIEs are subject to the new tax rate alongside other domestic businesses rather than benefiting from the old tax laws applicable to FIEs, and its associated preferential tax treatments, beginning January 1, 2008. | |

|

Despite these pending changes, the EIT Law gives the FIEs established before March 16, 2007, or Old FIEs, such as our subsidiaries Beijing SOD and Chongqing SOD, a five-year grandfather period during which they can continue to enjoy their existing preferential tax treatments. During this five-year grandfather period, the Old FIEs which enjoyed tax rates lower than 25% under the original EIT Law shall gradually increase their EIT rate by 2% per year until the tax rate reaches 25%. In addition, the Old FIEs that are eligible for the “two-year exemption and three-year half reduction” or “five-year exemption and five-year half-reduction” under the original EIT Law, are allowed to remain to enjoy their preference until these holidays expire. The discontinuation of any such special or preferential tax treatment or other incentives would have an adverse effect on any organization’s business, fiscal condition and current operations in China. | ||

|

In addition to the changes to the current tax structure, under the EIT Law, an enterprise established outside of China with “de facto management bodies” within China is considered a resident enterprise and will normally be subject to a EIT of 25.0% on its global income. The Implementing Rules define the term “de facto management bodies” as “an establishment that exercises, in substance, overall management and control over the production, business, personnel, accounting, etc., of a Chinese enterprise.” If the PRC tax authorities subsequently determine that we should be classified as a resident enterprise, then our consolidated global income will be subject to PRC income tax of 25.0% . |

17

We incurred no income taxes in either the three months ended September 30, 2014 or the three months ended September 30, 2013.

Results of Operations

Three Months Ended September 30, 2014 Compared to Three Months ended September 30, 2013

The following table summarizes the results of our operations for the three months ended September 30, 2014 and 2013 and provides information regarding the dollar and percentage increase or (decrease) from the three months ended September 30, 2013 to the same period of 2014.

| Three Months Ended | ||||||||||||

| September 30, | Increase | % Increase | ||||||||||

| Item | 2014 | 2013 | (Decrease) | (% Decrease) | ||||||||

| Revenue | $ | 0 | $ | 680 | $ | (680 | ) | (100% | ) | |||

| Cost of Revenue | 0 | 406 | (406 | ) | (100% | ) | ||||||

| Gross Profit | 0 | 274 | (274 | ) | (100% | ) | ||||||

| Operating Expenses | 105,066 | 99,751 | 5,315 | 5.33% | ||||||||

| Other Income | (13,249 | ) | 1,730 | (14,979 | ) | (865.84% | ) | |||||

| Provision for Taxes | - | - | - | - | ||||||||

| Net loss attributable to China Longyi | $ | (110,164 | ) | $ | (107,310 | ) | $ | 2,854 | 2.66% | |||

Revenues. Our revenues were historically derived primarily from sales of our SOD products. Revenues decreased $680, to $0 for the three months ended September 30, 2014, from $680 for the same period in 2013 as we did not sell any SOD products and our operating subsidiary, Chongqing SOD, ceased production and was in the process of the relocation.

Cost of Revenues. Our cost of revenues is primarily comprised of the costs of our raw materials, labor and overhead. Our cost of revenues decreased $406, to $0 for the three months ended September 30, 2014, from $406 during the same period in 2013 as we did not have any sales in this period.

Gross Profit. Since we did not have any sales for the three months ended September 31, 2014, our gross profit decreased by $274, to $0 for the three months ended September 30, 2014 from $274 during the same period in 2013.

Operating Expenses. Our total operating expenses for the three months ended September 30, 2014 increased $5,315, or 5.33%, to $105,066, from $99,751 for the same period in 2013. This increase was mainly because of the increased fees for professional services.

Other Income (expense). Other income was $(13,249) during the three months ended September 30, 2014, a decrease of $14,979 from $1,730 during a same period in 2013. Such decrease mainly came from the transaction exchange gain.

Net Loss attributable to China Longyi. As a result of above facts, our net loss increased by $2,854, or 2.66%, to $(110,164) for the three months ended September 30, 2014, from $(107,310) for the same period in 2013.

18

Nine Months Ended September 30, 2014 Compared to Nine Months ended September 30, 2013

The following table summarizes the results of our operations for the nine months ended September 30, 2014 and 2013 and provides information regarding the dollar and percentage increase or (decrease) from the nine months ended September 30, 2013 to the same period of 2014.

| Nine Months Ended | ||||||||||||

| September 30, | Increase | % Increase | ||||||||||

| Item | 2014 | 2013 | (Decrease) | (% Decrease) | ||||||||

| Revenue | $ | 0 | $ | 11,095 | $ | (11,095 | ) | (100% | ) | |||

| Cost of Revenue | 0 | 7,409 | (7,409 | ) | (100% | ) | ||||||

| Gross Profit | 0 | 3,686 | (3,686 | ) | (100% | ) | ||||||

| Operating Expenses | 367,795 | 366,165 | 1,630 | 0.45% | ||||||||

| Other Income | (10,682 | ) | 21,427 | (32,109 | ) | (149.85% | ) | |||||

| Provision for Taxes | - | - | - | - | ||||||||

| Net loss attributable to China Longyi | $ | (354,688 | ) | $ | (312,140 | ) | $ | 42,548 | 13.63% | |||

Revenues. Revenues decreased $11,095, to $0 for the nine months ended September 30, 2014, from $11,095 for the same period in 2013 as we did not sell any SOD products and our operating subsidiary, Chongqing SOD, ceased production and was in the process of the relocation.

Cost of Revenues. Our cost of revenues decreased $7,409, to $0 for the nine months ended September 30, 2014, from $7,409 during the same period in 2013 as we did not have any sales in this period.

Gross Profit. Since we did not have any sales in current period, our gross profit decreased by $3,686, to $0 for the nine months ended September 30, 2014 from $3,686 during the same period in 2013.

Operating Expenses. Our total operating expenses for the nine months ended September 30, 2014 increased $1,630, or 0.45%, to $367,795, from $366,165 for the same period in 2013. This increase was mainly due to the increase in professional fees paid to third parties.

Other Income (expense). Other income was $(10,682) during the nine months ended September 30, 2014, a decrease of $32,109 from $21,427 during a same period in 2013. Such decrease mainly came from the reduction of transaction exchange gains.

Net Loss attributable to China Longyi. As a result of above facts, our net loss increased by $42,548, or 13.63%, to $(354,688) for the nine months ended September 30, 2014, from $(312,140) for the same period in 2013.

Liquidity and Capital Resources

We had $10,237 in cash and cash equivalents as of September 30, 2014. As of such date, we also had total current assets of $465,116 and total assets of $821,518. We had total current liabilities (consisting of accounts payable, accrued liabilities, due to directors and other payables) in the amount of $1,587,886. Our stockholders’ equity as of September 30, 2014 was $(766,368). Since inception, we have accumulated a net loss of $30,641,628.

The following table summarizes the statements of cash flows from the financial statements for the nine months ended September 30, 2014 compared to the nine months ended September 30, 2013:

19

| Nine Months Ended | ||||||

| September 30, | ||||||

| 2014 | 2013 | |||||

| Net Cash Provided By (Used In) Operating Activities | $ | (249,275 | ) | $ | (22,213 | ) |

| Net Cash Provided By (Used In) Investing Activities | 0 | (1,512 | ) | |||

| Net Cash Provided By (Used In) Financing Activities | 222,970 | 45,036 | ||||

| Effect of foreign exchange rate fluctuation | 15,827 | (21,191 | ) | |||

| Net increase (decrease) in Cash and Cash Equivalents | (10,478 | ) | 120 | |||

| Cash and Cash Equivalents - Beginning of Period | 20,715 | 11,916 | ||||

| Cash and Cash Equivalents – End of Period | 10,237 | 12,036 | ||||

Operating Activities

Net cash used in operating activities was $249,275 for the nine-month period ended September 30, 2014, which is an increase of $227,062 from $22,213 of net cash used in the operating activities for the same period of 2013. The increase of the cash used in operating activities was mainly attributed to the fact that there was a change of accounts receivables. Cash provided from accounts receivables was $165,669 for the nine months ended September 30, 2013, while the cash provided from accounts receivable was $(1,628) for the nine months ended September 30, 2014.

Investing Activities

Net cash used in investing activities for the nine-month period ended September 30, 2014 was $0, which is a decrease of approximately $1,512 from net cash used in investing activities of $1,512 for the same period of 2013.

Financing Activities

Net cash provided by financing activities for the nine-month period ended September 30, 2014 was $222,970 as compared to $45,036 provided by financing activities for the same period in 2013. We received $222,970 as the loan from one of our directors for the nine months ended September 30, 2014.

The Company did not have any bank loans as of September 30, 2014.

We expect that our directors will continue to provide cash as loans to the company. However, we may in the future require additional cash resources due to changed business conditions, implementation of our strategy to expand our production capacity or other investments or acquisitions we may decide to pursue. If our own financial resources are insufficient to satisfy our capital requirements, we may seek to sell additional equity or debt securities or obtain additional credit facilities. The sale of additional equity securities could result in dilution to our stockholders. The incurrence of indebtedness would result in increased debt service obligations and could require us to agree to operating and financial covenants that would restrict our operations. Financing may not be available in amounts or on terms acceptable to us, if at all. Any failure by us to raise additional funds on terms favorable to us, or at all, could limit our ability to expand our business operations and could harm our overall business prospects.

Critical Accounting Policies

Economic and Political Risks

The Company faces a

number of risks and challenges as a result of having primary operations and

marketing in the PRC. Changing political climates in the PRC could have a

significant effect on the Company’s business.

20

Foreign Currencies

The company has determined that RMB to be its functional currency. The accompanying consolidated financial statements are presented in U.S. dollars. The consolidation financial statements are translated into US dollars from RMB at quarter-end exchange rates for assets and liabilities, and weighted average exchange rates for revenues and expenses. Capital accounts are translated at their historical exchange rates when the capital transactions occurred.

| September 30, | December 31, | |||||||||||||||||

| 2014 | 2013 | 2013 | ||||||||||||||||

| RMB | HK$ | RMB | HK$ | RMB | HK$ | |||||||||||||

| Balance sheet items, except for equity accounts | 6.1525 | 7.7638 | 6.1480 | 7.7541 | 6.0969 | 7.7546 | ||||||||||||

| Items in the statements of income and comprehensive income, and the statements of cash flows | 6.1442 | 7.7541 | 6.2172 | 7.7577 | 6.1929 | 7.7532 | ||||||||||||

Use of Estimates

The preparation of financial

statements in conformity with accounting principles generally accepted in the

United States of America requires management to make estimates and assumptions

that affect the reported amounts of assets and liabilities and disclosure of

contingent assets and liabilities at the date of the financial statements and

reported amounts of revenues and expenses during the reporting period. Actual

results could differ from those estimates.

Significant Estimates

Several areas require

significant management estimates relating to uncertainties for which it is

reasonably possible that there will be a material change in the near term. The

more significant areas requiring the use of management estimates related to

determination of net realizable value of inventory, allowance for doubtful

accounts, property and equipment, accrued liabilities and, the useful lives for

depreciation.

Restrictions on Transfer of Assets Out of the PRC

Dividend payments by Beijing SOD are limited by certain statutory

regulations in the PRC. No dividends may be paid by Beijing SOD without first

receiving prior approval from the Foreign Currency Exchange Management Bureau.

Dividend payments are restricted to 85% of profits, after tax.

Revenue Recognition

The Company recognizes revenue

in accordance with Staff Accounting Bulletin No.104 “Revenue recognition” (“ASC

Topic 605”). Revenues are recognized as earned when the following four criteria

are met: (1) a customer issues purchase orders or otherwise agrees to purchase

products; (2) products are delivered to the customer; (3) pricing is fixed or

determined in accordance with the purchase order or agreement; and (4)

collectability is reasonably assured.

Inflation

Inflation does not materially affect our business or the results of our operations.

Seasonality

We may experience seasonal variations in our future revenues and our operating costs, however, we do not believe that these variations will be material.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that are material to investors.

21

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not Applicable.

ITEMS 4. CONTROLS AND PROCEDURES

Disclosure Controls and Procedures’

Our management, with the participation of our chief executive officer and chief financial officer, Ms. Jie Chen and Mr. Xinmin Pan, respectively, evaluated the effectiveness of our disclosure controls and procedures. The term “disclosure controls and procedures,” as defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act, means controls and other procedures of a company that are designed to ensure that information required to be disclosed by a company in the reports, such as this report, that it files or submits under the Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the SEC’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed by a company in the reports that it files or submits under the Exchange Act is accumulated and communicated to the company’s management, including its principal executive and principal financial officers, as appropriate to allow timely decisions regarding required disclosure. Management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving their objectives and management necessarily applies its judgment in evaluating the cost-benefit relationship of possible controls and procedures. Based on that evaluation, Ms. Jie Chen and Mr. Xinmin Pan concluded that as of September 30, 2014, our disclosure controls and procedures were effective at the reasonable assurance level.

Internal Controls Over Financial Reporting

During the quarter ended September 30, 2014, there were no changes in our internal control over financial reporting identified in connection with the evaluation performed that occurred during the fiscal quarter covered by this report that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

22

PART II – OTHER INFORMATION

ITEM 1. LEGAL PROCEEDINGS

From time to time, the Company has disputes that arise in the ordinary course of its business. Currently, there are no material legal proceedings to which the Company is a party to or to which any of its property is subject that will have a material adverse effect on the Company's financial condition.

ITEM 1A. RISK FACTORS

Not applicable.

ITEM 2. UNREGISTERED SHARES OF EQUITY SECURITIES AND USE OF PROCEEDS

We have not sold any equity securities during the fiscal quarter ended September 30, 2014 that were not previously disclosed in a current report on Form 8-K that was filed during that period.

ITEM 3. DEFAULTS UPON SENIOR SECURITIES

Not applicable.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

ITEM 5. OTHER INFORMATION

None.

ITEM 6. EXHIBITS

| Exhibit | |

| Number | Description |

| 31.1 | |

| 31.2 | |

| 32.1 | |

| 32.2 | |

| 101 |

The following financial information from The China Longyi Group International Holdings Limited's Quarterly Report on Form 10-Q for the quarter ended September 30, 2014, formatted in XBRL (Extensible Business Reporting Language): (i) Consolidated Balance Sheets at September 30, 2014 and December 31, 2013, (ii) Consolidated Statements of Operations and Comprehensive Loss for the three and nine months ended September 30, 2014 and 2013, (iii) Consolidated Statements of Cash Flows for the nine months ended September 30, 2014 and 2013, and (iv) the Notes to Consolidated Financial Statements. |

23

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| CHINA LONGYI GROUP INTERNATIONAL HOLDINGS LIMITED | |

| DATED: November 14, 2014 | |

| By: /s/ Jie Chen | |

| ------------------------------------- | |

| Jie Chen | |

| Chief Executive Officer | |

| (Principal Executive Officer) | |

| DATED: November 14, 2014 | By: /s/ Xinmin Pan |

| ------------------------------------- | |

| Xinmin Pan | |

| Chief Financial Officer | |

| (Principal Financial Officer and Accounting Officer) |

24

EXHIBIT INDEX

| Exhibit | |

| Number | Description |

| 31.1 | |

| 31.2 | |

| 32.1 | |

| 32.2 | |

| 101 | The following financial information from The China Longyi Group International Holdings Limited's Quarterly Report on Form 10-Q for the quarter ended September 30, 2014, formatted in XBRL (Extensible Business Reporting Language): (i) Consolidated Balance Sheets at September 30, 2014 and December 31, 2013, (ii) Consolidated Statements of Operations and Comprehensive Loss for the three and nine months ended September 30, 2014 and 2013, (iii) Consolidated Statements of Cash Flows for the nine months ended September 30, 2014 and 2013, and (iv) the Notes to Consolidated Financial Statements. |

25