provision for credit losses on loans in the first quarter of fiscal 2024 ($545,000, which includes $9,000 for unfunded commitment reserves).

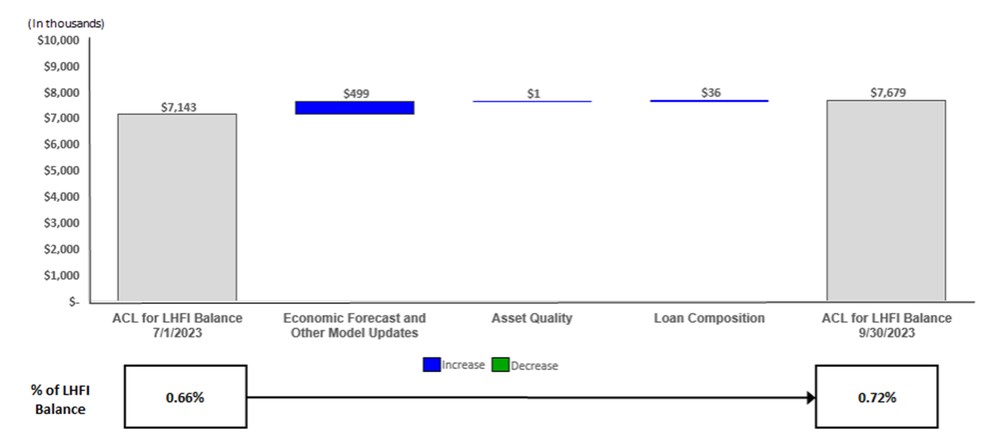

The following chart quantifies the factors contributing to the changes in the ACL on loans held for investment (“LHFI”) for the quarter ended September 30, 2023 subsequent to the CECL adoption on July 1, 2023:

Management considers, based on currently available information, the ACL sufficient to absorb estimated losses in loans held for investment. See “Asset Quality” below and Note 5 of the Notes to Unaudited Interim Condensed Consolidated Financial Statements in this Form 10-Q for additional discussion regarding the ACL on loans held for investment.

Non-Interest Income:

For the Quarters Ended September 30, 2023 and 2022. Non-interest income decreased $252,000, or 25 percent, to $751,000 in the first quarter of fiscal 2024 from $1.0 million in the same period last year, primarily due to a decrease in loan servicing and other fees, and, to a lesser extent, decreases in deposit account fees, card and processing fees, and other non-interest income.

Loan servicing and other fees decreased $129,000 or 119 percent to a net loss of $21,000 in the first quarter of fiscal 2024 from a net gain of $108,000 in the same quarter last year. The decrease was attributable primarily to lower loan prepayment fees resulting from fewer loan payoffs, particularly in multi-family loans. Total loan prepayment fees in the first quarter of fiscal 2024 were $19,000, down $140,000 or 88 percent from $159,000 in the same quarter last year. Total loan repayments were $23.0 million in the first quarter of fiscal 2024, down 27 percent from $31.7 million in the same quarter last year.

Non-Interest Expense:

For the Quarters Ended September 30, 2023 and 2022. Non-interest expenses decreased $85,000 or one percent to $6.9 million in the first quarter of fiscal 2024 from the same quarter last year. The decrease in the non-interest expense in the first quarter of fiscal 2024 was primarily due to lower professional expenses, attributable mainly to lower legal expenses.

Provision for Income Taxes:

The income tax provision reflects accruals for taxes at the applicable rates for federal income tax and California franchise tax based upon reported pre-tax income, adjusted for the effect of all permanent differences between income for tax and financial reporting purposes, such as non-deductible stock-based compensation, earnings from bank-owned life insurance

42