Exhibit 1

|

||||

| TSX: CCO | website: cameco.com | |||

| NYSE: CCJ | currency: Cdn (unless noted) |

2121 – 11th Street West, Saskatoon, Saskatchewan, S7M 1J3 Canada

Tel: 306-956-6200 Fax: 306-956-6201

Cameco announces 2022 results; strong market fundamentals captured in record long-term contracting of 80 million pounds uranium and 17 million kgU of conversion services; disciplined return to tier-one run rate with exposure to improving prices

Saskatoon, Saskatchewan, Canada, February 9, 2023 .. . . . . . . . . . .. . . . . .

Cameco (TSX: CCO; NYSE: CCJ) today reported its consolidated financial and operating results for the fourth quarter and year ended December 31, 2022 in accordance with International Financial Reporting Standards (IFRS).

“Demand for nuclear power, supported by growth across the near, medium and long term, is driving the best fundamentals we have ever seen for the nuclear fuel market. The growing structural gap has led to supply uncertainty, which was amplified in 2022. As a proven, reliable, independent, commercial supplier of nuclear fuels, Cameco is positioned to benefit from these fundamentals. Our 2022 results, and our guidance for 2023, reflect the transformative year that we have had and the opportunity that remains ahead of us. In 2022, we were successful in contracting 80 million pounds of uranium and 17 million kgU of conversion services, with a record number of contracts signed in a market that has strengthened and is in durable growth mode. Our contracting also allows us to sustainably operate our assets, including tier-one assets that are expected to generate full-cycle value for Cameco. And, in 2022, with the resumption of production at McArthur River and Key Lake, we began the return to a tier-one run rate, which we expect will significantly improve our financial results,” said Tim Gitzel, Cameco’s president and CEO.

“The geopolitical events that impacted 2022 accelerated security of supply concerns and coupled with the ongoing focus on the climate crisis, created what we believe are transformative tailwinds for the nuclear power industry from both a demand and supply perspective. In early-January, unrest in Kazakhstan raised concerns about the security of the more than 40% of global uranium supply that originates from Kazakhstan. However, it was the Russian invasion of Ukraine in late-February that was the most transformative event for our industry. We believe it has set in motion a geopolitical realignment in energy markets that is highlighting the crucial role for nuclear power not just in providing clean energy, but also in providing secure and affordable energy. And, with the global nuclear industry reliant on Russian supplies for approximately 14% of uranium concentrates, 27% of conversion and 39% of enrichment, it is highlighting the security of supply risk associated with the growing primary supply gap and shrinking secondary supplies, and increasing the focus on origin of supply.

“We continue to believe that Cameco remains the best way to invest in the recovery of the uranium market. With nuclear energy clearly back in durable growth mode, Cameco is also back in durable growth mode. Growth that will be sought in the same manner as we approach all aspects of our business; strategic, deliberate, disciplined, and with a focus on generating full-cycle value.

“We have had success capturing the improving market fundamentals with a record number of contracts signed. Our contracting focus has been on obtaining market-related pricing mechanisms, while also providing adequate downside protection. We continue to be strategically patient in our discussions to maximize value in our contract portfolio and to maintain exposure to higher prices with unencumbered future productive capacity.

- 1 -

“With the improvements in the market, the new long-term contracts we have put in place and our pipeline of contracting discussions, we are moving to the next phase of our supply discipline. Our plan will now be for McArthur River/Key Lake to produce 18 million pounds per year (100% basis) starting in 2024 and we will continue to operate Cigar Lake at its licensed capacity of 18 million pounds per year (100% basis) in 2024. At Inkai, production will continue to follow the 20% reduction planned by Kazatomprom (KAP) until the end of 2023. With annual licensed capacity of 25 million pounds at McArthur River/Key Lake, we continue to have the ability to expand production from our existing assets. If we took advantage of all of the tier-one expansion opportunities available to us, our annual share of tier-one supply could be about 32 million pounds. However, any decision to expand production will be dependent on further improvements in the uranium market and our ability to secure the appropriate long-term contract homes for our unencumbered, in-ground inventory, demonstrating that we continue to responsibly manage our supply in accordance with our customers’ needs.

“Thanks to our deliberate actions and conservative financial management we have been and continue to be resilient. The strength of our balance sheet allowed us to take advantage of two opportunities in 2022 that we believe will add significant long-term value for Cameco. We acquired a greater share in the Cigar Lake mine, increasing our ownership to 54.5%. We are pleased to increase our share in the Cigar Lake operation, which is a proven, permitted and fully licensed tier-one mine in a safe and stable jurisdiction that we operate with the tremendous participation and support of our neighbouring Indigenous partner communities. And, we entered a strategic partnership with Brookfield Renewable Partners and its institutional partners (Brookfield Renewable) to jointly acquire 100% of Westinghouse Electric Company (Westinghouse), a global provider of mission-critical and specialized technologies, products and services across most phases of the nuclear power sector. The acquisition is expected to close in the second half of 2023 and is subject to customary closing conditions and certain regulatory approvals. Once the transaction closes, Brookfield Renewable, will beneficially own a 51% interest in Westinghouse and we will beneficially own 49%. We believe bringing together our expertise in the nuclear industry with Brookfield Renewable’s expertise in clean energy positions nuclear power at the heart of the clean energy transition and creates a powerful platform for strategic growth across the nuclear sector.

“With the renewed recognition of the role nuclear power must play, we are optimistic about Cameco’s role in supporting the transition to a net-zero carbon economy. Through our innovative decarbonization actions across efficiency, electrification, waste to value, carbon economy, and fuel switching themes – we expect to achieve a 30% absolute reduction from our total Scope 1 and 2 emissions level by 2030 from our 2015 baseline as our first major milestone on the journey to achieve our ambition of being net zero. We believe our largest contribution to the transition to a net-zero carbon economy comes from the nuclear fuels that we supply to support the generation of nuclear power – 100% carbon-free electricity.

“We have tier-one assets that are licensed, permitted, long-lived, and proven reliable, and that have expansion capacity. These tier-one assets are backed up by idle tier-two assets and what we think is the best exploration portfolio that leverages existing infrastructure. We also provide our customers with access to conversion, as well as fuel fabrication and reactor components for heavy water CANDU reactors. With the pending joint acquisition of Westinghouse, we are excited about being able to extend the base of our reach in the nuclear fuel cycle with assets that, like ours, are strategic, proven, licensed, permitted, and located in geopolitically important jurisdictions. Assets that we expect will be able to participate in the growing demand profile for nuclear energy from their existing footprint. And, we are exploring opportunities in the nuclear fuel cycle and in innovative, non-traditional commercial uses of nuclear power in Canada and around the world.

“We believe we have the right strategy to achieve our vision of ‘energizing a clean-air world’ and we will do so in a manner that reflects our values. Embedded in all our decisions is a commitment to addressing the environmental, social and governance risks and opportunities that we believe will make our business sustainable over the long term.”

Summary of Q4 and 2022 results and developments:

| • | Record contracting secures long-term revenues and cash flows: In our uranium segment, in 2022, we added 80 million pounds to our portfolio of long-term uranium contracts, with a record number of contracts signed. Of the 80 million pounds, about 58 million pounds have been finalized under contracts and the remaining 22 million pounds have been accepted with key commercial terms, such as pricing mechanism, volume and tenor having been agreed to, but still awaiting contract finalization. We also have a large and growing pipeline of uranium business under discussion. In addition, with strong demand in the UF6 conversion market, we were successful in adding long-term contracts that we expect will underpin that operation for years to come. We finalized contracts for almost 12 million kgU of UF6 conversion in 2022 and have another almost 5 million kgU that have been accepted and are awaiting contract finalization. |

- 2 -

| • | Contract acceptance with Energoatom: As announced on February 8, we have reached agreement on commercial terms for a major supply contract to provide sufficient volumes of natural uranium hexafluoride (UF6) (consisting of uranium and conversion services) to SE NNEGC Energoatom (Energoatom) to meet Ukraine’s full nuclear fuel needs through 2035. Key commercial terms, such as pricing mechanism, volume and tenor, have been agreed to, but the contract is subject to finalization, which is anticipated in the first quarter of 2023. The agreement will contain a required degree of flexibility, given present circumstances in Ukraine. The volumes are not included in our total 2022 contracted volumes, and represent potential total requirements of 25.7 million kgU as UF6 (the equivalent of 67.3 million pounds of uranium) that were accepted in 2023. This brings our total contracting from the start of 2022 to over 147 million pounds of uranium (58 million pounds finalized and 89 million pounds accepted and awaiting contract finalization) and almost 43 million kgU in conversion services (12 million kgU finalized and almost 31 million kgU accepted and awaiting contract finalization). |

| • | 2023 guidance provided, returning to tier-one run rate: Our outlook for 2023 is beginning to reflect the transition of our cost structure back to a tier-one run rate, as we plan our production to satisfy the growing long-term commitments under our contract portfolio. With the improvements in the market, the new long-term contracts we have put in place, and a pipeline of contracting discussions, our plan will now be for McArthur River/Key Lake to produce 18 million pounds (100% basis) starting in 2024 and to continue to operate Cigar Lake at its licensed capacity of 18 million pounds per year (100% basis) in 2024. At Inkai, production will continue to follow the 20% reduction planned by KAP until the end of 2023. With annual licensed capacity of 25 million pounds (100% basis) at McArthur River/Key Lake, we continue to have the ability to expand production from our existing assets, however some additional investment would be required. Any decision to expand production will be dependent on further improvements in the uranium market and our ability to secure the appropriate long-term contract homes for our unencumbered, in-ground inventory, demonstrating that we continue to responsibly manage our supply in accordance with our customers’ needs. In addition to our plans to expand uranium production, at our Port Hope conversion facility we are working on increasing UF6 production to 12,000 tonnes by 2024 to satisfy our book of long-term business for conversion services and customer demand at a time when conversion prices are at historic highs. As a result of these plans, we expect to see continued improvement in our financial performance. See Outlook for 2023 in our 2022 annual MD&A for more information. |

| • | Increased ownership at Cigar Lake: In May 2022, we announced the acquisition of a greater share in the Cigar Lake mine for $107 million, increasing our ownership to 54.5% (from 50%). Cigar Lake is a proven, permitted and fully licensed tier-one mine in a safe and stable jurisdiction that we operate with the tremendous participation and support of our neighbouring Indigenous partner communities. |

| • | Proposed acquisition of Westinghouse: In October 2022, we announced we had entered into a strategic partnership with Brookfield Renewable to jointly acquire 100% of Westinghouse, a global provider of mission-critical and specialized technologies, products and services across most phases of the nuclear power sector. Concurrently with the execution of the acquisition agreement, we secured commitments that provide for a $1 billion (US) bridge loan facility and $600 million (US) in term loans. Following the announcement, we undertook a $650 million (US) bought deal offering of common shares, with an underwriter option to purchase additional shares. The offering closed on October 17, 2022, providing us with gross proceeds of approximately $747.6 million (US) including the underwriters’ exercise in full of the option to purchase additional shares. The acquisition is expected to close in the second half of 2023 and is subject to customary closing conditions and certain regulatory approvals. Once the transaction closes, Brookfield Renewable will beneficially own a 51% interest in Westinghouse and we will beneficially own 49%. We believe bringing together our expertise in the nuclear industry with Brookfield Renewable’s expertise in clean energy positions nuclear power at the heart of the clean energy transition and creates a powerful platform for strategic growth across the nuclear sector. See Proposed acquisition of Westinghouse in our 2022 annual MD&A and our October 18, 2022 material change report (available on www.sedar.com and www.sec.gov) for more information. |

| • | Fourth quarter net loss of $15 million; adjusted net earnings of $36 million: Fourth quarter results are driven by normal quarterly variations in contract deliveries and the continued execution of our strategy. Adjusted net earnings is a non-IFRS measure, see page 5. |

- 3 -

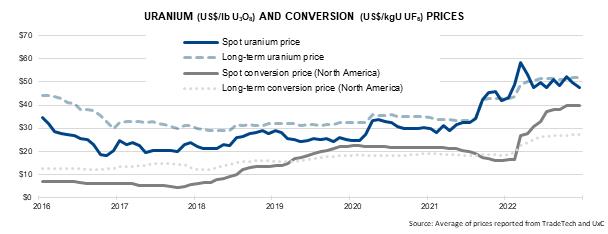

| • | Annual net earnings of $89 million; adjusted net earnings of $135 million: Annual results are beginning to reflect the transition of our cost structure back to a tier-one run rate as contemplated by the continued execution of our strategy. Our results also reflect the improvement in average realized prices as uranium prices and conversion prices continue to increase catalyzed by geopolitical uncertainty and security of supply concerns. In our uranium segment we delivered over 25 million pounds. Production for 2022 was 10.4 million pounds in our uranium segment as Cigar Lake met its annual production target of 18 million pounds (100% basis) and McArthur River/Key Lake restarted operations producing 1.1 million pounds (100% basis). In our fuel services segment, we produced 13.0 million kgU, which included an annual UF6 production record. In addition, we generated $305 million in cash from operations, with higher sales volumes in our uranium segment and higher average realized prices in both our uranium and fuel services segments compared to 2021. Adjusted net earnings is a non-IFRS measure, see page 5. |

| • | Strong balance sheet: As of December 31, 2022, we had $2.3 billion in cash and cash equivalents and short-term investments and $997 million in long-term debt. Net proceeds from the announced share issuance were received in October 2022 and the US dollar cash and cash equivalents and short-term investments are included on our balance sheet. The final financing for the Westinghouse acquisition is not required until close of the acquisition and will be determined based on market conditions and the expected run rate of our business at that time. We expect a permanent financing mix of capital sources, including cash, debt and equity, designed to preserve our balance sheet and ratings strength, while maintaining healthy liquidity. In addition, we have a $1 billion undrawn credit facility. |

| • | Received dividends from JV Inkai: In 2022, we received dividend payments from JV Inkai totaling $93 million (US). JV Inkai distributes excess cash, net of working capital requirements, to the partners as dividends. See Uranium – Tier-one operations – Inkai in our 2022 annual MD&A. |

Consolidated financial results

| THREE MONTHS ENDED | YEAR ENDED | |||||||||||||||

| CONSOLIDATED HIGHLIGHTS | DECEMBER 31 | DECEMBER 31 | ||||||||||||||

| ($ MILLIONS EXCEPT WHERE INDICATED) |

2022 | 2021 | 2022 | 2021 | ||||||||||||

| Revenue |

524 | 465 | 1,868 | 1,475 | ||||||||||||

| Gross profit |

65 | 56 | 233 | 2 | ||||||||||||

| Net earnings (loss) attributable to equity holders |

(15 | ) | 11 | 89 | (103 | ) | ||||||||||

| $ per common share (basic) |

(0.04 | ) | 0.03 | 0.22 | (0.26 | ) | ||||||||||

| $ per common share (diluted) |

(0.04 | ) | 0.03 | 0.22 | (0.26 | ) | ||||||||||

| Adjusted net earnings (loss) (non-IFRS, see page 5) |

36 | 23 | 135 | (98 | ) | |||||||||||

| $ per common share (adjusted and diluted) |

0.09 | 0.06 | 0.33 | (0.25 | ) | |||||||||||

| Cash provided by operations |

77 | 59 | 305 | 458 | ||||||||||||

The 2022 annual financial statements have been audited; however, the 2021 fourth quarter and 2022 fourth quarter financial information presented is unaudited. You can find a copy of our 2022 annual MD&A and our 2022 audited financial statements on our website at cameco.com.

NET EARNINGS

The following table shows what contributed to the change in net earnings and adjusted net earnings (non-IFRS measure, see page 5) in the three months and year ended December 31, 2022, compared to the same period in 2021.

- 4 -

| THREE MONTHS ENDED | YEAR ENDED | |||||||||||||||||

| CHANGES IN EARNINGS | DECEMBER 31 | DECEMBER 31 | ||||||||||||||||

| ($ MILLIONS) |

IFRS | ADJUSTED | IFRS | ADJUSTED | ||||||||||||||

| Net earnings (losses) - 2021 |

11 | 23 | (103 | ) | (98 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| Change in gross profit by segment |

||||||||||||||||||

| (we calculate gross profit by deducting from revenue the cost of products and services sold, and depreciation and amortization (D&A), net of hedging benefits) |

| |||||||||||||||||

| Uranium |

Impact from sales volume changes |

1 | 1 | (6 | ) | (6 | ) | |||||||||||

| Higher realized prices ($US) |

29 | 29 | 328 | 328 | ||||||||||||||

| Foreign exchange impact on realized prices |

25 | 25 | 44 | 44 | ||||||||||||||

| Higher costs |

(41 | ) | (41 | ) | (137 | ) | (137 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| change – uranium |

14 | 14 | 229 | 229 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| Fuel services |

Impact from sales volume changes |

(10 | ) | (10 | ) | (21 | ) | (21 | ) | |||||||||

| Higher realized prices ($Cdn) |

4 | 4 | 33 | 33 | ||||||||||||||

| Lower (higher) costs |

1 | 1 | (13 | ) | (13 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| change – fuel services |

(5 | ) | (5 | ) | (1 | ) | (1 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| Other changes |

||||||||||||||||||

| Lower (higher) administration expenditures |

8 | 8 | (44 | ) | (44 | ) | ||||||||||||

| Higher exploration expenditures |

— | — | (3 | ) | (3 | ) | ||||||||||||

| Change in reclamation provisions |

(78 | ) | — | (31 | ) | 3 | ||||||||||||

| Change in gains or losses on derivatives |

12 | (12 | ) | (86 | ) | (23 | ) | |||||||||||

| Change in foreign exchange gains or losses |

6 | 6 | 74 | 74 | ||||||||||||||

| Change in earnings from equity-accounted investments |

(19 | ) | (19 | ) | 26 | 26 | ||||||||||||

| Canadian Emergency Wage Subsidy |

— | — | (21 | ) | (21 | ) | ||||||||||||

| Bargain purchase gain on CLJV ownership interest increase |

— | — | 23 | — | ||||||||||||||

| Higher finance income |

21 | 21 | 30 | 30 | ||||||||||||||

| Change in income tax recovery or expense |

13 | (2 | ) | 3 | (30 | ) | ||||||||||||

| Other |

2 | 2 | (7 | ) | (7 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

| Net earnings (losses) - 2022 |

(15 | ) | 36 | 89 | 135 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

Non-IFRS measures

ADJUSTED NET EARNINGS

Adjusted net earnings (ANE) is a measure that does not have a standardized meaning or a consistent basis of calculation under IFRS (non-IFRS financial measure). We use this measure as a more meaningful way to compare our financial performance from period to period. Adjusted net earnings is our net earnings attributable to equity holders, adjusted to better reflect the underlying financial performance for the reporting period. We believe that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate our performance. Adjusted net earnings is one of the targets that we measure to form the basis for a portion of annual employee and executive compensation (see Measuring our results in our 2022 annual MD&A).

In calculating ANE we adjust for derivatives. We do not use hedge accounting under IFRS and, therefore, we are required to report gains and losses on all hedging activity, both for contracts that close in the period and those that remain outstanding at the end of the period. For the contracts that remain outstanding, we must treat them as though they were settled at the end of the reporting period (mark-to-market). However, we do not believe the gains and losses that we are required to report under IFRS appropriately reflect the intent of our hedging activities, so we make adjustments in calculating our ANE to better reflect the impact of our hedging program in the applicable reporting period. See Foreign exchange in our 2022 annual MD&A for more information.

We also adjust for changes to our reclamation provisions that flow directly through earnings. Every quarter we are required to update the reclamation provisions for all operations based on new cash flow estimates, discount and inflation rates. This normally results in an adjustment to our asset retirement obligation in addition to the provision balance. When the assets of an operation have been written off due to an impairment, as is the case with our Rabbit Lake and US ISR operations, the adjustment is recorded directly to the statement of earnings as “other operating expense (income)”. See note 16 of our annual financial statements for more information. This amount has been excluded from our ANE measure.

- 5 -

Adjusted net earnings is a non-IFRS financial measure and should not be considered in isolation or as a substitute for financial information prepared according to accounting standards. Other companies may calculate this measure differently, so you may not be able to make a direct comparison to similar measures presented by other companies.

The following table reconciles adjusted net earnings with our net earnings for the three months and years ended December 31, 2022 and 2021.

| THREE MONTHS ENDED | YEAR ENDED | |||||||||||||||

| DECEMBER 31 | DECEMBER 31 | |||||||||||||||

| ($ MILLIONS) |

2022 | 2021 | 2022 | 2021 | ||||||||||||

| Net earnings (loss) attributable to equity holders |

(15 | ) | 11 | 89 | (103 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjustments |

||||||||||||||||

| Adjustments on derivatives |

(19 | ) | 5 | 76 | 13 | |||||||||||

| Adjustments on other operating expense (income) |

88 | 10 | 26 | (8 | ) | |||||||||||

| Adjustment to other income |

— | — | (23 | ) | — | |||||||||||

| Income taxes on adjustments |

(18 | ) | (3 | ) | (33 | ) | — | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted net earnings (loss) |

36 | 23 | 135 | (98 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Selected segmented highlights

| THREE MONTHS ENDED | YEAR ENDED | |||||||||||||||||||||||||||||

| DECEMBER 31 | DECEMBER 31 | |||||||||||||||||||||||||||||

| HIGHLIGHTS |

2022 | 2021 | CHANGE | 2022 | 2021 | CHANGE | ||||||||||||||||||||||||

| Uranium |

Production volume (million lbs) | 3.7 | 2.8 | 32 | % | 10.4 | 6.1 | 70 | % | |||||||||||||||||||||

| Sales volume (million lbs) | 6.9 | 6.5 | 6 | % | 25.6 | 24.3 | 5 | % | ||||||||||||||||||||||

| Average realized price1 | ($US/lb) | 43.05 | 39.65 | 9 | % | 44.73 | 34.53 | 30 | % | |||||||||||||||||||||

| ($Cdn/lb) | 57.87 | 49.94 | 16 | % | 57.85 | 43.34 | 33 | % | ||||||||||||||||||||||

| Revenue ($ millions) | 397 | 323 | 23 | % | 1,480 | 1,055 | 40 | % | ||||||||||||||||||||||

| Gross profit (loss) ($ millions) | 24 | 10 | >100 | % | 121 | (108 | ) | >100 | % | |||||||||||||||||||||

| Fuel services |

Production volume (million kgU) | 3.7 | 3.1 | 19 | % | 13.0 | 12.1 | 7 | % | |||||||||||||||||||||

| Sales volume (million kgU) | 3.8 | 4.9 | (22 | )% | 11.1 | 13.6 | (18 | )% | ||||||||||||||||||||||

| Average realized price 2 | ($Cdn/kgU) | 30.11 | 28.80 | 5 | % | 32.92 | 29.72 | 11 | % | |||||||||||||||||||||

| Revenue ($ millions) | 115 | 140 | (18 | )% | 365 | 404 | (10 | )% | ||||||||||||||||||||||

| Gross profit ($ millions) | 41 | 46 | (11 | )% | 117 | 118 | (1 | )% | ||||||||||||||||||||||

| 1 | Uranium average realized price is calculated as the revenue from sales of uranium concentrate, transportation and storage fees divided by the volume of uranium concentrates sold. |

| 2 | Fuel services average realized price is calculated as revenue from the sale of conversion and fabrication services, including fuel bundles and reactor components, transportation and storage fees divided by the volumes sold. |

Executive team update

Grant Isaac has been appointed executive vice-president and retains the chief financial officer (CFO) function. Isaac continues to report to the president and CEO. Prior to this role, Isaac was senior vice-president and CFO. Heidi Shockey has been appointed senior vice-president and deputy CFO and reports to Isaac. Prior to this, Shockey was Cameco’s vice president and controller. Both appointments are effective February 1, 2023.

“I am pleased to recognize Grant’s continued excellent contributions to Cameco with his appointment to executive vice-president. I am also pleased to welcome Heidi to the senior executive team, who brings extensive financial expertise to her role as deputy CFO,” said Gitzel. “They are part of an exceptionally strong and experienced management team.”

Management’s discussion and analysis (MD&A) and financial statements

The 2022 annual MD&A and consolidated financial statements provide a detailed explanation of our operating results for the three and twelve months ended December 31, 2022, as compared to the same periods last year, and our outlook for 2023. This news release should be read in conjunction with these documents, as well as our most recent annual information form, all of which are available on our website at cameco.com, on SEDAR at sedar.com, and on EDGAR at sec.gov/edgar.shtml.

- 6 -

Qualified persons

The technical and scientific information discussed in this document for our material properties McArthur River/Key Lake, Cigar Lake and Inkai was approved by the following individuals who are qualified persons for the purposes of NI 43-101:

MCARTHUR RIVER/KEY LAKE

| • | Greg Murdock, general manager, McArthur River, Cameco |

| • | Daley McIntyre, general manager, Key Lake, Cameco |

CIGAR LAKE

| • | Lloyd Rowson, general manager, Cigar Lake, Cameco |

INKAI

| • | Sergey Ivanov, deputy director general, technical services, Cameco Kazakhstan LLP |

Caution about forward-looking information

This news release includes statements and information about our expectations for the future, which we refer to as forward-looking information. Forward-looking information is based on our current views, which can change significantly, and actual results and events may be significantly different from what we currently expect.

Examples of forward-looking information in this news release include: our views regarding supply and demand for nuclear power and its growth across the near, medium and long term; our ability to benefit from market fundamentals and opportunities; the durability of growth in our uranium and conversion services contracting; our ability to operate our assets sustainably, and our expectations regarding the value they will generate for us; our expectations regarding the impact of a return to a tier-one run rate on our financial results; our views regarding the impact on the nuclear power industry of geopolitical events and ongoing focus on climate crisis; our belief that Cameco is the best way to invest in the recovery in the uranium market; the durability of our growth, and our ability to pursue growth and generate full-cycle value; our contract portfolio strategy and ability to maintain exposure to higher prices with unencumbered future productive capacity; our supply plans, including production levels at McArthur River/Key Lake, Cigar Lake and Inkai; our ability to expand production from our existing assets, and the production level we could achieve through our tier-one expansion opportunities; the factors we will consider in making decisions regarding expanding production; the anticipated timing for the finalization of the SE NNEGC Energoatom (Energoatom) supply contract and our expectation that Cameco will provide sufficient volumes of UF6 under it to meet Ukraine’s full nuclear fuel needs through 2035; our ability to continue to be resilient; our views regarding the future value of increasing our share in the Cigar Lake mine, and our strategic partnership with Brookfield Renewable to acquire 100% of Westinghouse; the expected timing of the closing of the Westinghouse acquisition; our optimism regarding our role in supporting a transition to a net-zero carbon economy, and expectations regarding our ability to achieve emissions level reductions within our expected timeframes; our expectation that the Westinghouse acquisition will permit us to extend our reach in the nuclear fuel cycle; our exploration of other expansion opportunities in the nuclear fuel cycle and in non-traditional commercial uses of nuclear power; our vision of energizing a clean-air world and belief in our strategy for doing so in a manner that reflects our values; our views regarding the long-term sustainability of our business; and the expected date for announcement of our 2023 first quarter results.

- 7 -

Material risks that could lead to different results include: unexpected changes in uranium supply, demand, long-term contracting, and prices; changes in consumer demand for nuclear power and uranium as a result of changing societal views and objectives regarding nuclear power, electrification and decarbonization; the risk that we may not continue with our supply discipline strategy; the risk that we may not be able to implement changes to future operating and production levels for Cigar Lake and McArthur River/Key Lake to the planned levels within the expected timeframes, or that the costs involved in doing so, or the costs associated with care and maintenance activities, exceed our expectations; the risk that production levels at Inkai may not be at expected levels; the risk that our revenues and cash flows may not improve to the extent expected; risks relating to the Energoatom supply contract, including the risk that it will not be finalized within the time or on the terms expected, our ability to supply UF6 under the contract, and that the continuation or outcome of the conflict between the Ukraine and Russia may prevent Cameco from realizing its expected benefits; the risk that we may not be able to meet sales commitments for any reason; the risk that we may not be able to continue to be resilient or continue to improve our financial performance; the risks to our business associated with potential production disruptions, including those related to global supply chain disruptions, global economic uncertainty and political volatility; the risk that we may not be able to implement our business objectives in a manner consistent with our environmental, social, governance and other values; the risk that the strategy we are pursuing may prove unsuccessful, or that we may not be able to execute it successfully; the risk that we may not be successful in pursuing innovation or implementing advanced technologies, or realizing the expected benefits of the Westinghouse acquisition; and the risk that we may be delayed in announcing our future financial results.

In presenting the forward-looking information, we have made material assumptions which may prove incorrect about: uranium demand, supply, consumption, long-term contracting, growth in the demand for and global public acceptance of nuclear energy, and prices; our production, purchases, sales, deliveries and costs; the market conditions and other factors upon which we have based our future plans and forecasts; the success of our plans and strategies, including planned operating and production changes; assumptions regarding the Energoatom supply contract, including that we will reach agreement on final terms within the time and on the terms expected, our ability to supply UF6 under the contract, and that we will not be prevented from realizing the expected benefits of the contract because of the continuation or outcome of the conflict between Ukraine and Russia; the absence of new and adverse government regulations, policies or decisions; that there will not be any significant unanticipated adverse consequences to our business resulting from production disruptions, including those relating to supply disruptions, and economic or political uncertainty and volatility; our ability to realize the expected benefits of the Westinghouse acquisition; and our ability to announce future financial results when expected.

Please also review the discussion in our 2022 annual MD&A and most recent annual information form for other material risks that could cause actual results to differ significantly from our current expectations, and other material assumptions we have made. Forward-looking information is designed to help you understand management’s current views of our near-term and longer-term prospects, and it may not be appropriate for other purposes. We will not necessarily update this information unless we are required to by securities laws.

Conference call

We invite you to join our fourth quarter conference call on Thursday, February 9, 2023 at 8:00 a.m. Eastern.

The call will be open to all investors and the media. To join the call, please dial (800) 319-4610 (Canada and US) or (604) 638-5340. An operator will put your call through. The slides and a live webcast of the conference call will be available from a link at cameco.com. See the link on our home page on the day of the call.

A recorded version of the proceedings will be available:

| • | on our website, cameco.com, shortly after the call |

| • | on post view until midnight, Eastern, March 9, 2023, by calling (800) 319-6413 (Canada and US) or (604) 638-9010 (Passcode 9717) |

2023 first quarter report release date

We plan to announce our 2023 first quarter results before markets open on April 28, 2023.

- 8 -

Profile

Cameco is one of the largest global providers of the uranium fuel needed to energize a clean-air world. Our competitive position is based on our controlling ownership of the world’s largest high-grade reserves and low-cost operations. Utilities around the world rely on our nuclear fuel products to generate safe, reliable, carbon-free nuclear power. Our shares trade on the Toronto and New York stock exchanges. Our head office is in Saskatoon, Saskatchewan.

As used in this news release, the terms we, us, our, the Company and Cameco mean Cameco Corporation and its subsidiaries unless otherwise indicated.

– End –

Investor inquiries:

Rachelle Girard

306-956-6403

rachelle_girard@cameco.com

Media inquiries:

Veronica Baker

306-385-5541

veronica_baker@cameco.com

- 9 -