| UNITED STATES SECURITIES AND EXCHANGE COMMISSION | ||

| Washington, D.C. 20549 | ||

FORM N-CSR | ||

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES | ||

| Investment Company Act file number: | (811-07513) |

| Exact name of registrant as specified in charter: | Putnam Funds Trust |

| Address of principal executive offices: | One Post Office Square, Boston, Massachusetts 02109 |

| Name and address of agent for service: | Robert T. Burns, Vice President One Post Office Square Boston, Massachusetts 02109 |

| Copy to: | Bryan Chegwidden, Esq. Ropes & Gray LLP 1211 Avenue of the Americas New York, New York 10036 |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| Date of fiscal year end: | October 31, 2015 |

| Date of reporting period: | November 1, 2014 – April 30, 2015 |

Item 1. Report to Stockholders: |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |||

Putnam

Absolute Return

700 Fund®

Semiannual report

4 | 30 | 15

|

Message from the Trustees |

1 |

|

About the fund |

2 |

|

Performance snapshot |

4 |

|

Interview with your fund’s portfolio manager |

5 |

|

Your fund’s performance |

11 |

|

Your fund’s expenses |

13 |

|

Terms and definitions |

15 |

|

Other information for shareholders |

16 |

|

Financial statements |

17 |

Consider these risks before investing: Allocation of assets among asset classes may hurt performance. Stock and bond prices may fall or fail to rise over time for several reasons, including general financial market conditions, factors related to a specific issuer or industry and, with respect to bond prices, changing market perceptions of the risk of default and changes in government intervention. These factors may also lead to increased volatility and reduced liquidity in the bond markets. The fund’s active trading strategy may lose money or not earn a return sufficient to cover associated trading and other costs. Use of leverage through derivatives adds risk by increasing investment exposure. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Unlike bonds, funds that invest in bonds have fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk and the risk that they may increase in value less when interest rates decline and decline in value more when interest rates rise. International investing involves currency, economic, and political risks. Emerging-market securities have illiquidity and volatility risks. Risks associated with derivatives include increased investment exposure (which may be considered leverage) and, in the case of over-the-counter instruments, the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. The fund may not achieve its goal, and it is not intended to be a complete investment program. The fund’s efforts to produce lower-volatility returns may not be successful and may make it more difficult at times for the fund to achieve its targeted return. Under certain market conditions, the fund may accept greater-than-typical volatility to seek its targeted return. Commodities have market, political, regulatory, and natural conditions risks. Investments in small and/or midsize companies may experience greater price fluctuations. Growth stocks may be more susceptible to earnings disappointments, and value stocks may fail to rebound. You can lose money by investing in the fund.

Message from the Trustees

Dear Fellow Shareholder:

With the midway point of 2015 at hand, we note the sixth anniversary of the beginning of the U.S. economic expansion as dated by the National Bureau of Economic Research, which tracks the ups and downs of U.S. business cycles. It has also been six years since the beginning of the current bull market in U.S. stocks.

Both the expansion and the bull market are longer than average, and both appear to owe their longevity, to some degree, to the extraordinary policy measures undertaken by the Federal Reserve. Recently, however, the Fed has been preparing markets for a shift toward tighter monetary policy. Short-term interest rates could increase for the first time since 2006.

While higher interest rates can be a reflection of solid economic conditions, they can also pose a risk to fixed-income investments, and can have a less direct impact on stocks. International markets, which have performed well in early 2015, would also feel the effects of higher rates in the world’s largest economy. In the following pages, your fund’s portfolio manager provides a market outlook in addition to an update on your fund’s performance.

With the possibility that markets could begin to move in different directions, it might be a prudent time to consult your financial advisor to determine whether any adjustments or additions to your portfolio are warranted.

As the owner of a Putnam fund, you have put your investment in the hands of professional managers who pursue a consistent strategy and have experience in navigating changing market conditions. They, and we, share a deep conviction that an active approach based on fundamental research can play a valuable role in your portfolio.

As always, thank you for investing with Putnam.

Respectfully yours,

Robert L. Reynolds

President and Chief Executive Officer

Putnam Investments

Jameson A. Baxter

Chair, Board of Trustees

June 11, 2015

Performance

snapshot

Annualized total return (%) comparison as of 4/30/15

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 5.75%; had they, returns would have been lower. See pages 3, 5 and 11–13 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

The fund seeks to earn a positive total return that exceeds the return on U.S. Treasury bills by 700 basis points (or 7.00%) on an annualized basis over a reasonable period of time (generally at least three years or more) regardless of market conditions. No information for the target return is provided for periods of less than one year.

The fund is not expected to outperform during periods of market rallies.

*Returns for the six-month period are not annualized, but cumulative.

4 Absolute Return 700 Fund

Interview with your fund’s portfolio manager

|

|

|

Robert J. Kea, CFA |

Bob, what was the investment environment like during the six-month reporting period ended April 30, 2015?

U.S. stocks were choppy, but still managed to gain more than 4%, as measured by the S&P 500 Index. Investors grappled with several issues. U.S. gross domestic product [GDP] fell to an anemic 0.2% annualized growth rate in 2015’s first quarter. Also, the strong U.S. dollar was a drag on corporate earnings, and the possibility of higher interest rates weighed on the market. Mid-cap stocks outpaced large- and small-cap shares, and growth stocks outperformed value-oriented equities by a considerable margin.

Overseas, the January launch of a larger-than-expected bond-buying program by the European Central Bank bolstered sentiment toward stocks in that region. Surprisingly, Japan outpaced many European markets in U.S.-dollar terms because the yen did not weaken as much versus the dollar as the euro did. Similar to Europe, Japan benefited from accommodative monetary policy, along with improving domestic and global economic conditions.

In fixed income, the period was marked by episodes of interest-rate volatility, but rates generally moved lower, allowing the broad Barclays U.S. Aggregate Bond Index to gain about 2%.

Pulled down in part by the weak U.S. GDP reading, the U.S. dollar declined in April,

Broad market index and fund performance

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 4/30/15. See pages 3, 4 and 11–13 for additional fund performance information. Index descriptions can be found on page 16.

Absolute Return 700 Fund 5

interrupting its steady march higher since last summer. Even though market participants largely attributed the slowdown to the dampening effects of harsh winter weather on consumer spending, attention turned toward the Federal Reserve’s interest-rate policy. A largely consensus opinion emerged that the Fed may wait longer to begin increasing interest rates, creating a possible headwind to dollar strength.

Crude oil prices, after bottoming at just over $47 per barrel in mid-March, rose and

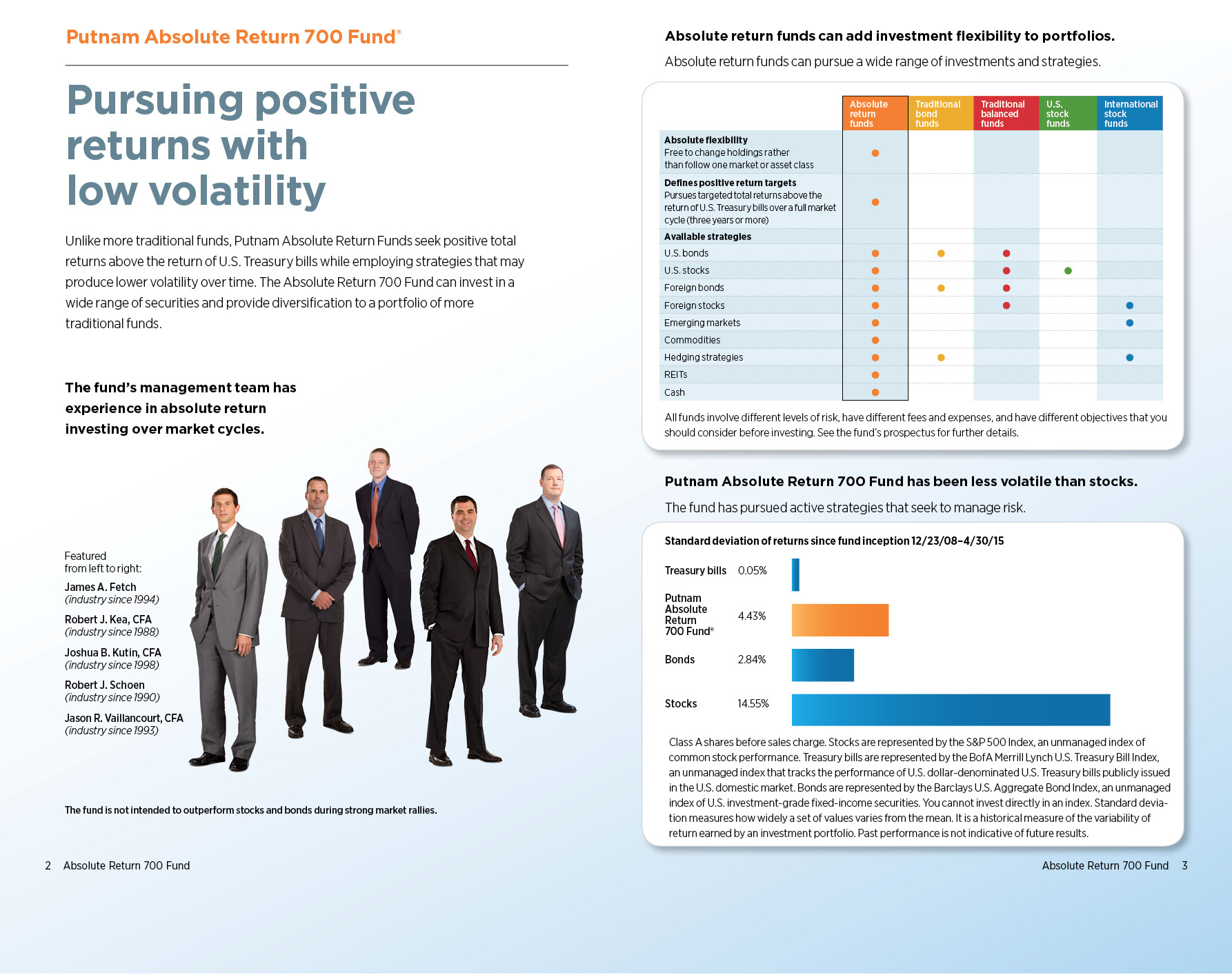

Portfolio composition

Allocations are shown as a percentage of the fund’s net assets as of 4/30/15. Cash and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, and the use of different classifications of securities for presentation purposes. Allocations may not total 100% because the table includes the notional value of derivatives (the economic value for purposes of calculating periodic payment obligations), in addition to the market value of securities. Holdings and allocations may vary over time.

Negative weights may result from timing differences between trade and settlement dates of securities, such as TBAs, or from the use of derivatives.

6 Absolute Return 700 Fund

“In our view, the macroeconomic

backdrop in the United States remains

generally supportive for taking equity

risk.”

Bob Kea

ended the period at $59.63 on the New York Mercantile Exchange. Signs that U.S. oil production may be peaking and global energy demand may be rising, coupled with a weaker U.S. dollar, buoyed the commodity’s price.

Would you please summarize the fund’s overall investment strategy?

Absolute Return 700 Fund seeks to earn a positive total return that exceeds the return of U.S. Treasury bills by 7% on an annualized basis over a full market cycle [generally at least three years] regardless of market conditions. We seek to do this by utilizing both directional and non-directional strategies. Directional strategies look to capitalize on opportunities in global markets based on our assessment of broad market trends. The trends may involve either positive or negative market movements. Non-directional strategies seek to add value regardless of global market trends. We shift the composition of the portfolio’s risk between directional and non-directional strategies based on our active views of the relative potential of these approaches. In addition, the portfolio’s total risk and expected return can be increased or

Top 10 holdings

This table shows the fund’s top 10 individual holdings and the percentage of the fund’s net assets that each represented as of 4/30/15. Short-term holdings, TBA commitments, and derivatives, if any, are excluded. Holdings may vary over time.

Absolute Return 700 Fund 7

decreased based on our outlook and current market conditions. We use a variety of tools to implement our investment process as we seek to manage various global risks.

How did directional strategies influence the fund’s performance during the six-month reporting period?

As a whole, our directional strategies added value, led by our equity allocation. The fund’s U.S. low-volatility strategy, which emphasizes stocks that have been less volatile than the overall market, benefited from a generally favorable backdrop for domestic equities.

The fund’s exposure to interest-rate risk also contributed, aided by a significant decline in rates during the period’s first half. For example, the yield on the benchmark 10-year U.S. Treasury fell from 2.36% at the start of the period to 1.64% at the beginning of February, its low for the period. Rates moved higher during the remainder of the period, but not enough to offset the solid contribution from our interest-rate strategy.

Commodities declined substantially during the period. As a result, our short position in the asset class, which was designed to benefit from downward movement in certain commodities indexes, also worked in the fund’s favor.

How did non-directional strategies perform during the period?

A variety of non-directional strategies performed well and provided a further boost to the fund’s return. Regional equity long/short trades were additive, and quantitative, equity-selection alpha strategies — one of which was focused in the United States and another in developed international markets — also aided the fund’s performance. Elsewhere, our global fixed-income alpha strategy was also productive, led by positions in securitized market sectors — such as collateralized mortgage obligations — mortgage credit, and

Portfolio composition comparison

This chart shows how the fund’s top weightings have changed over the past six months. Allocations are shown as a percentage of the fund’s net assets. Cash and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Current period summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, and the use of different classifications of securities for presentation purposes. Holdings and allocations may vary over time.

Data in the chart reflect a new calculation methodology put into effect within the past six months.

8 Absolute Return 700 Fund

prepayment-sensitive areas. Active currency positioning was another contributor, driven by long U.S.-dollar exposure coupled with tactical short positions in other major global currencies.

Which strategies didn’t work as well?

A long/short U.S. equity strategy that incorporates fundamental research from Putnam’s equity analysts was the only notable detractor, and partially offset the positive overall contribution from our stock-selection strategies.

How did you use derivatives during the period?

We used a variety of derivatives to reduce volatility and, in some cases, to enhance returns. We used futures to efficiently gain exposure to certain markets and to manage market risk. We also employed options to hedge against changes in the values of certain equities held by the fund. Lastly, we utilized total return swaps to help manage exposure to specific securities or baskets of securities.

What is your outlook for the coming months, and how are you positioning the fund?

Although first-quarter GDP growth was disappointing, we continue to have an overall optimistic view of the U.S. economic recovery. As noted above, we think the first-quarter slowdown was largely the result of weaker-than-expected consumer spending despite lower oil and gas prices, along with harsh winter weather in many parts of the country. In our view, the macroeconomic backdrop in the United States remains generally supportive for taking equity risk.

We continue to believe that the Fed is likely to begin raising its target for short-term interest rates sometime in 2015. However, with inflation stubbornly below the central bank’s 2% target at the end of the reporting period, we think the first increase won’t occur until the Fed sees enough consistent data to persuade it that the U.S. recovery is accelerating.

ABOUT DERIVATIVES

Derivatives are an increasingly common type of investment instrument, the performance of which is derived from an underlying security, index, currency, or other area of the capital markets. Derivatives employed by the fund’s managers generally serve one of two main purposes: to implement a strategy that may be difficult or more expensive to invest in through traditional securities, or to hedge unwanted risk associated with a particular position.

For example, the fund’s managers might use currency forward contracts to capitalize on an anticipated change in exchange rates between two currencies. This approach would require a significantly smaller outlay of capital than purchasing traditional bonds denominated in the underlying currencies. In another example, the managers may identify a bond that they believe is undervalued relative to its risk of default, but may seek to reduce the interest-rate risk of that bond by using interest-rate swaps, a derivative through which two parties “swap” payments based on the movement of certain rates. In other examples, the managers may use options and futures contracts to hedge against a variety of risks by establishing a combination of long and short exposures to specific equity markets or sectors.

Like any other investment, derivatives may not appreciate in value and may lose money. Derivatives may amplify traditional investment risks through the creation of leverage and may be less liquid than traditional securities. And because derivatives typically represent contractual agreements between two financial institutions, derivatives entail “counterparty risk,” which is the risk that the other party is unable or unwilling to pay. Putnam monitors the counterparty risks we assume. For example, Putnam often enters into collateral agreements that require the counterparties to post collateral on a regular basis to cover their obligations to the fund. Counterparty risk for exchange-traded futures and centrally cleared swaps is mitigated by the daily exchange of margin and other safeguards against default through their respective clearinghouses.

Absolute Return 700 Fund 9

In terms of portfolio positioning, with the U.S. bull market now in its sixth year, and interest rates and yield premiums for credit-sensitive bonds low, we see fewer opportunities to make a meaningful impact on performance via shifts in directional strategies. As a result, we believe there is greater potential to add value through non-directional strategies and have increased the fund’s emphasis on those strategies accordingly. For example, we believe our quantitatively driven, equity selection alpha strategies offer the most attractive potential and, at period-end, most of the fund’s non-directional risk was focused in this area. We also think divergent central bank policies between the United States and the United Kingdom on the one hand and continental Europe on the other, offer the potential for attractive regional fixed-income trades.

Thanks for your time and for bringing us up to date, Bob.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager Robert J. Kea is Co-Head of Global Asset Allocation at Putnam. He holds an M.B.A. from the Bentley University Graduate School of Business and a B.A. from the University of Massachusetts, Amherst. He joined Putnam in 1989 and has been in the investment industry since 1988.

In addition to Bob, your fund’s portfolio managers are James A. Fetch; Joshua B. Kutin, CFA; Robert J. Schoen; and Jason R. Vaillancourt, CFA.

IN THE NEWS

There seems to be momentum in the U.S. equities market, which is now in its third-longest bull run since 1928. Inflation, as measured by the Consumer Price Index, was –0.1% before seasonal adjustment for the 12 months ended March 31, 2015, according to the Bureau of Labor Statistics. Low inflation and a resilient U.S. economy generally provide a supportive environment for equities. However, investors appear to be more cautious than celebratory. Uncertainties include the timing of the Federal Reserve’s decision to implement the first hike in short-term interest rates since 2006 and whether the strong dollar could continue to worsen the trade balance, which could in turn reduce gross domestic product. In March, exports grew by less than 1%, according to the Bureau of Economic Analysis, compared with a 7.7% jump in imports in the same month. For now, the S&P 500 Index continues to hover around the 2100 mark. Investors should keep in mind that equities tend to perform well when short-term rates are rising from low levels. The reason is, in part, because rising rates typically signal an improving economy.

10 Absolute Return 700 Fund

|

Your fund’s performance |

|

This section shows your fund’s performance, price, and distribution information for periods ended April 30, 2015, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance information as of the most recent calendar quarter-end and expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R, R5, R6, and Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund. |

Fund performance Total return for periods ended 4/30/15

|

Class A |

Class B |

Class C |

Class M |

Class R |

Class R5 |

Class R6 |

Class Y |

|||||

|

(inception dates) |

(12/23/08) |

(12/23/08) |

(12/23/08) |

(12/23/08) |

(12/23/08) |

(7/2/12) |

(7/2/12) |

(12/23/08) |

||||

|

Before sales charge |

After sales charge |

Before CDSC |

After CDSC |

Before CDSC |

After CDSC |

Before sales charge |

After sales charge |

Net |

Net |

Net |

Net |

|

|

Life of fund |

46.57% |

38.14% |

39.69% |

39.69% |

39.82% |

39.82% |

41.58% |

36.62% |

43.90% |

48.81% |

49.11% |

48.67% |

|

Annual average |

6.20 |

5.22 |

5.40 |

5.40 |

5.42 |

5.42 |

5.63 |

5.03 |

5.90 |

6.46 |

6.49 |

6.44 |

|

5 years |

26.08 |

18.83 |

21.55 |

19.55 |

21.49 |

21.49 |

22.85 |

18.55 |

24.47 |

27.76 |

28.02 |

27.65 |

|

Annual average |

4.74 |

3.51 |

3.98 |

3.64 |

3.97 |

3.97 |

4.20 |

3.46 |

4.47 |

5.02 |

5.06 |

5.00 |

|

3 years |

14.94 |

8.33 |

12.48 |

9.48 |

12.44 |

12.44 |

13.29 |

9.32 |

14.21 |

15.97 |

16.20 |

15.86 |

|

Annual average |

4.75 |

2.70 |

4.00 |

3.06 |

3.99 |

3.99 |

4.25 |

3.02 |

4.53 |

5.06 |

5.13 |

5.03 |

|

1 year |

6.12 |

0.02 |

5.38 |

0.39 |

5.36 |

4.36 |

5.58 |

1.88 |

5.86 |

6.42 |

6.47 |

6.33 |

|

6 months |

3.95 |

–2.02 |

3.60 |

–1.30 |

3.58 |

2.60 |

3.72 |

0.09 |

3.93 |

4.08 |

4.22 |

4.08 |

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 5.75% and 3.50% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R, R5, R6, and Y shares have no initial sales charge or CDSC. Performance for class R5 and R6 shares prior to their inception is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R5 and R6 shares; had it, returns would have been higher.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Absolute Return 700 Fund 11

Comparative index returns For periods ended 4/30/15

|

BofA Merrill Lynch U.S. Treasury Bill Index |

Barclays U.S. |

S&P 500 Index |

|

|

Life of fund |

0.96% |

33.68% |

176.97% |

|

Annual average |

0.15 |

4.68 |

17.40 |

|

5 years |

0.60 |

22.38 |

95.31 |

|

Annual average |

0.12 |

4.12 |

14.33 |

|

3 years |

0.29 |

8.01 |

59.05 |

|

Annual average |

0.10 |

2.60 |

16.73 |

|

1 year |

0.07 |

4.46 |

12.98 |

|

6 months |

0.04 |

2.06 |

4.40 |

Index results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

Fund price and distribution information For the six-month period ended 4/30/15

|

Distributions |

Class A |

Class B |

Class C |

Class M |

Class R |

Class R5 |

Class R6 |

Class Y |

||

|

Number |

1 |

1 |

1 |

1 |

1 |

1 |

1 |

1 |

||

|

Income |

$0.186 |

$0.095 |

$0.102 |

$0.132 |

$0.158 |

$0.224 |

$0.230 |

$0.222 |

||

|

Capital gains |

||||||||||

|

Long-term gains |

0.571 |

0.571 |

0.571 |

0.571 |

0.571 |

0.571 |

0.571 |

0.571 |

||

|

Short-term gains |

— |

— |

— |

— |

— |

— |

— |

— |

||

|

Total |

$0.757 |

$0.666 |

$0.673 |

$0.703 |

$0.729 |

$0.795 |

$0.801 |

$0.793 |

||

|

Share value |

Before |

After |

Net asset |

Net asset |

Before |

After |

Net asset |

Net asset |

Net asset |

Net asset |

|

10/31/14 |

$12.71 |

$13.49 |

$12.44 |

$12.44 |

$12.52 |

$12.97 |

$12.57 |

$12.78 |

$12.77 |

$12.74 |

|

4/30/15 |

12.44 |

13.20 |

12.21 |

12.20 |

12.27 |

12.72 |

12.32 |

12.49 |

12.49 |

12.45 |

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (5.75% for class A shares and 3.50% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

12 Absolute Return 700 Fund

Fund performance as of most recent calendar quarter Total return for periods ended 3/31/15

|

Class A |

Class B |

Class C |

Class M |

Class R |

Class R5 |

Class R6 |

Class Y |

|||||

|

(inception dates) |

(12/23/08) |

(12/23/08) |

(12/23/08) |

(12/23/08) |

(12/23/08) |

(7/2/12) |

(7/2/12) |

(12/23/08) |

||||

|

Before sales charge |

After sales charge |

Before CDSC |

After CDSC |

Before CDSC |

After CDSC |

Before sales charge |

After sales charge |

Net |

Net |

Net |

Net |

|

|

Life of fund |

47.28% |

38.81% |

40.38% |

40.38% |

40.51% |

40.51% |

42.38% |

37.40% |

44.60% |

49.52% |

49.70% |

49.39% |

|

Annual average |

6.37 |

5.37 |

5.56 |

5.56 |

5.57 |

5.57 |

5.80 |

5.20 |

6.06 |

6.62 |

6.65 |

6.61 |

|

5 years |

27.25 |

19.93 |

22.58 |

20.58 |

22.63 |

22.63 |

24.10 |

19.76 |

25.73 |

29.06 |

29.21 |

28.94 |

|

Annual average |

4.94 |

3.70 |

4.16 |

3.81 |

4.16 |

4.16 |

4.41 |

3.67 |

4.69 |

5.23 |

5.26 |

5.21 |

|

3 years |

16.60 |

9.90 |

14.02 |

11.02 |

13.99 |

13.99 |

14.93 |

10.91 |

15.77 |

17.64 |

17.78 |

17.53 |

|

Annual average |

5.25 |

3.20 |

4.47 |

3.55 |

4.46 |

4.46 |

4.75 |

3.51 |

5.00 |

5.56 |

5.61 |

5.53 |

|

1 year |

6.72 |

0.59 |

5.90 |

0.90 |

5.88 |

4.88 |

6.26 |

2.55 |

6.46 |

7.10 |

7.07 |

7.02 |

|

6 months |

4.62 |

–1.40 |

4.28 |

–0.66 |

4.26 |

3.27 |

4.48 |

0.82 |

4.60 |

4.83 |

4.80 |

4.83 |

See the discussion following the fund performance table on page 11 for information about the calculation of fund performance.

|

Your fund’s expenses |

|

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative. |

Expense ratios

|

Class A |

Class B |

Class C |

Class M |

Class R |

Class R5 |

Class R6 |

Class Y |

|

|

Total annual operating expenses for the fiscal year ended 10/31/14 |

1.24% |

1.99% |

1.99% |

1.74% |

1.49% |

0.99% |

0.92% |

0.99% |

|

Annualized expense ratio for the six-month period ended 4/30/15* |

1.27% |

2.02% |

2.02% |

1.77% |

1.52% |

1.01% |

0.94% |

1.02% |

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report.

Expenses are shown as a percentage of average net assets.

*Includes a decrease of 0.04% from annualizing the performance fee adjustment for the six months ended 4/30/15.

Absolute Return 700 Fund 13

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from November 1, 2014, to April 30, 2015. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

|

Class A |

Class B |

Class C |

Class M |

Class R |

Class R5 |

Class R6 |

Class Y |

|

|

Expenses paid per $1,000*† |

$6.42 |

$10.20 |

$10.20 |

$8.94 |

$7.69 |

$5.11 |

$4.76 |

$5.16 |

|

Ending value (after expenses) |

$1,039.50 |

$1,036.00 |

$1,035.80 |

$1,037.20 |

$1,039.30 |

$1,040.80 |

$1,042.20 |

$1,040.80 |

*Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 4/30/15. The expense ratio may differ for each share class.

†Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

|

Estimate the expenses you paid |

|

To estimate the ongoing expenses you paid for the six months ended April 30, 2015, use the following calculation method. To find the value of your investment on November 1, 2014, call Putnam at 1-800-225-1581. |

|

|

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

|

Class A |

Class B |

Class C |

Class M |

Class R |

Class R5 |

Class R6 |

Class Y |

|

|

Expenses paid per $1,000*† |

$6.36 |

$10.09 |

$10.09 |

$8.85 |

$7.60 |

$5.06 |

$4.71 |

$5.11 |

|

Ending value (after expenses) |

$1,018.50 |

$1,014.78 |

$1,014.78 |

$1,016.02 |

$1,017.26 |

$1,019.79 |

$1,020.13 |

$1,019.74 |

*Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 4/30/15. The expense ratio may differ for each share class.

†Expenses are calculated by multiplying the expense ratio by the average account value for the six-month period; then multiplying the result by the number of days in the six-month period; and then dividing that result by the number of days in the year.

14 Absolute Return 700 Fund

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 5.75% maximum sales charge for class A shares and 3.50% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge and may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class R shares are not subject to an initial sales charge or CDSC and are available only to employer-sponsored retirement plans.

Class R5 and R6 shares are not subject to an initial sales charge or CDSC and carry no 12b-1 fee. They are only available to employer-sponsored retirement plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Fixed-income terms

Current rate is the annual rate of return earned from dividends or interest of an investment. Current rate is expressed as a percentage of the price of a security, fund share, or principal investment.

Mortgage-backed security (MBS), also known as a mortgage “pass-through,” is a type of asset-backed security that is secured by a mortgage or collection of mortgages. The following are types of MBSs:

•Agency “pass-through” has its principal and interest backed by a U.S. government agency, such as the Federal National Mortgage Association (Fannie Mae), Government National Mortgage Association (Ginnie Mae), and Federal Home Loan Mortgage Corporation (Freddie Mac).

•Collateralized mortgage obligation (CMO) represents claims to specific cash flows from pools of home mortgages. The streams of principal and interest payments on the mortgages are distributed to the different classes of CMO interests in “tranches.” Each tranche may have different principal balances, coupon rates, prepayment risks, and maturity dates. A CMO is highly sensitive to changes in interest rates and any resulting change in the rate at which homeowners sell their properties, refinance, or otherwise prepay loans. CMOs are subject to prepayment, market, and liquidity risks.

•Interest-only (IO) security is a type of CMO in which the underlying asset is the interest portion of mortgage, Treasury, or bond payments.

•Non-agency residential mortgage-backed security (RMBS) is an MBS not backed by Fannie Mae, Ginnie Mae, or Freddie Mac. One type of RMBS is an Alt-A mortgage-backed security.

Absolute Return 700 Fund 15

•Commercial mortgage-backed security (CMBS) is secured by the loan on a commercial property.

Yield curve is a graph that plots the yields of bonds with equal credit quality against their differing maturity dates, ranging from shortest to longest. It is used as a benchmark for other debt, such as mortgage or bank lending rates.

Comparative indexes

Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA (Bank of America) Merrill Lynch U.S. Treasury Bill Index is an unmanaged index that tracks the performance of U.S. dollar-denominated U.S. Treasury bills publicly issued in the U.S. domestic market. Qualifying securities must have a remaining term of at least one month to final maturity and a minimum amount outstanding of $1 billion.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2014, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Form N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of April 30, 2015, Putnam employees had approximately $498,000,000 and the Trustees had approximately $142,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

16 Absolute Return 700 Fund

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

Absolute Return 700 Fund 17

The fund’s portfolio 4/30/15 (Unaudited)

|

COMMON STOCKS (43.5%)* |

Shares |

Value |

|

|

Basic materials (2.5%) |

|||

|

Airgas, Inc. |

9,000 |

$911,520 |

|

|

Anhui Conch Cement Co., Ltd. (China) |

765,000 |

3,107,685 |

|

|

Axalta Coating Systems, Ltd. † |

9,700 |

297,596 |

|

|

Bemis Co., Inc. |

17,200 |

774,000 |

|

|

Braskem SA (Brazil) |

627,800 |

2,625,427 |

|

|

China Lesso Group Holdings, Ltd. (China) |

2,432,000 |

1,792,261 |

|

|

China Singyes Solar Technologies Holdings, Ltd. (China) |

1,454,000 |

2,388,907 |

|

|

Huabao International Holdings, Ltd. (China) |

3,174,000 |

3,565,133 |

|

|

International Flavors & Fragrances, Inc. |

10,571 |

1,213,022 |

|

|

Koza Altin Isletmeleri AS (Turkey) |

105,674 |

1,101,680 |

|

|

Newmont Mining Corp. |

76,400 |

2,023,836 |

|

|

Royal Gold, Inc. |

11,700 |

755,001 |

|

|

Sappi, Ltd. (South Africa) † |

324,821 |

1,331,544 |

|

|

SBA Communications Corp. Class A † |

21,900 |

2,536,458 |

|

|

Sherwin-Williams Co. (The) |

13,700 |

3,808,600 |

|

|

Sibanye Gold, Ltd. (South Africa) |

1,294,642 |

3,055,742 |

|

|

31,288,412 |

|||

|

Capital goods (2.2%) |

|||

|

Avery Dennison Corp. |

15,800 |

878,322 |

|

|

Ball Corp. |

22,700 |

1,666,407 |

|

|

China Railway Group, Ltd. (China) |

1,943,000 |

2,727,079 |

|

|

General Dynamics Corp. |

42,300 |

5,808,636 |

|

|

Lockheed Martin Corp. |

29,300 |

5,467,380 |

|

|

Raytheon Co. |

40,800 |

4,243,200 |

|

|

Rockwell Collins, Inc. |

22,500 |

2,189,925 |

|

|

Stericycle, Inc. † |

8,700 |

1,160,841 |

|

|

TransDigm Group, Inc. |

8,300 |

1,760,679 |

|

|

Waste Management, Inc. |

41,300 |

2,045,589 |

|

|

27,948,058 |

|||

|

Communication services (1.2%) |

|||

|

America Movil SAB de CV ADR Class L (Mexico) |

84,300 |

1,761,027 |

|

|

China Mobile, Ltd. (China) |

280,000 |

4,003,611 |

|

|

SK Telecom Co., Ltd. (South Korea) |

10,609 |

2,838,144 |

|

|

Verizon Communications, Inc. |

113,017 |

5,700,577 |

|

|

14,303,359 |

|||

|

Conglomerates (1.5%) |

|||

|

Danaher Corp. |

64,692 |

5,296,981 |

|

|

Marubeni Corp. (Japan) |

757,900 |

4,702,094 |

|

|

Mitsubishi Corp. (Japan) |

273,000 |

5,902,005 |

|

|

Mitsui & Co., Ltd. (Japan) |

218,900 |

3,065,136 |

|

|

18,966,216 |

|||

|

Consumer cyclicals (4.4%) |

|||

|

ANTA Sports Products, Ltd. (China) |

481,000 |

1,059,053 |

|

|

Automatic Data Processing, Inc. |

45,900 |

3,880,386 |

|

|

AutoZone, Inc. † |

5,546 |

3,730,572 |

|

|

Clorox Co. (The) |

11,300 |

1,198,930 |

|

|

Discovery Communications, Inc. Class C † |

39,000 |

1,178,970 |

|

|

Dollar General Corp. |

52,200 |

3,795,462 |

18 Absolute Return 700 Fund

|

COMMON STOCKS (43.5%)* cont. |

Shares |

Value |

|

|

Consumer cyclicals cont. |

|||

|

Dollar Tree, Inc. † |

35,063 |

$2,679,164 |

|

|

FactSet Research Systems, Inc. |

5,400 |

849,906 |

|

|

FF Group (Greece) |

73,194 |

2,209,867 |

|

|

Harley-Davidson, Inc. |

35,900 |

2,017,939 |

|

|

Interpublic Group of Cos., Inc. (The) |

69,600 |

1,450,464 |

|

|

Kohl’s Corp. |

11,300 |

809,645 |

|

|

Lear Corp. |

2,900 |

321,987 |

|

|

LF Corp. (South Korea) |

21,640 |

709,675 |

|

|

Madison Square Garden Co. (The) Class A † |

10,600 |

851,180 |

|

|

Naspers, Ltd. Class N (South Africa) |

3,198 |

501,818 |

|

|

NIKE, Inc. Class B |

2,700 |

266,868 |

|

|

Omnicom Group, Inc. |

32,672 |

2,475,231 |

|

|

OPAP SA (Greece) |

165,081 |

1,466,944 |

|

|

Ralph Lauren Corp. |

9,800 |

1,307,418 |

|

|

Scripps Networks Interactive Class A |

17,995 |

1,257,131 |

|

|

Target Corp. |

80,000 |

6,306,400 |

|

|

Tata Motors, Ltd. ADR (India) |

67,100 |

2,763,849 |

|

|

Tongaat Hulett, Ltd. (South Africa) |

64,997 |

723,699 |

|

|

Vantiv, Inc. Class A † |

21,900 |

856,290 |

|

|

VF Corp. |

43,100 |

3,121,733 |

|

|

Wal-Mart Stores, Inc. |

24,700 |

1,927,835 |

|

|

Walt Disney Co. (The) |

54,000 |

5,870,880 |

|

|

55,589,296 |

|||

|

Consumer staples (4.2%) |

|||

|

Altria Group, Inc. |

129,631 |

6,488,032 |

|

|

Amorepacific Group (South Korea) F |

22,930 |

3,486,558 |

|

|

Bunge, Ltd. |

21,300 |

1,839,681 |

|

|

Chipotle Mexican Grill, Inc. † |

700 |

434,938 |

|

|

Church & Dwight Co., Inc. |

13,100 |

1,063,327 |

|

|

Colgate-Palmolive Co. |

68,100 |

4,581,768 |

|

|

Costco Wholesale Corp. |

44,800 |

6,408,640 |

|

|

Daesang Corp. (South Korea) |

66,275 |

2,862,360 |

|

|

Dr. Pepper Snapple Group, Inc. |

30,700 |

2,289,606 |

|

|

Gruma SAB de CV Class B (Mexico) |

204,301 |

2,461,147 |

|

|

Indofood Sukses Makmur Tbk PT (Indonesia) |

3,439,900 |

1,783,287 |

|

|

JBS SA (Brazil) |

251,651 |

1,297,949 |

|

|

McDonald’s Corp. |

72,168 |

6,967,820 |

|

|

Philip Morris International, Inc. |

28,000 |

2,337,160 |

|

|

Pinnacle Foods, Inc. |

8,900 |

360,895 |

|

|

Reynolds American, Inc. |

40,500 |

2,968,650 |

|

|

Sao Martinho SA (Brazil) |

137,501 |

1,749,254 |

|

|

Sumitomo Corp. (Japan) |

262,700 |

3,104,702 |

|

|

Tupperware Brands Corp. |

8,500 |

568,310 |

|

|

53,054,084 |

|||

|

Energy (2.3%) |

|||

|

Bangchak Petroleum PCL (The) (Thailand) |

1,630,100 |

1,755,454 |

|

|

Exxon Mobil Corp. |

133,431 |

11,657,866 |

|

|

HollyFrontier Corp. |

33,100 |

1,283,618 |

|

|

Lukoil OAO ADR (Russia) |

30,723 |

1,566,455 |

Absolute Return 700 Fund 19

|

COMMON STOCKS (43.5%)* cont. |

Shares |

Value |

|

|

Energy cont. |

|||

|

National Oilwell Varco, Inc. |

62,500 |

$3,400,625 |

|

|

Spectra Energy Corp. |

112,666 |

4,196,809 |

|

|

Tambang Batubara Bukit Asam Persero Tbk PT (Indonesia) |

2,009,000 |

1,444,730 |

|

|

Thai Oil PCL (Thailand) |

894,700 |

1,587,743 |

|

|

Tupras Turkiye Petrol Rafinerileri AS (Turkey) † |

79,346 |

1,928,686 |

|

|

28,821,986 |

|||

|

Financials (9.0%) |

|||

|

Alexandria Real Estate Equities, Inc. R |

8,400 |

775,992 |

|

|

American Campus Communities, Inc. R |

17,900 |

718,506 |

|

|

American Capital Agency Corp. R |

60,500 |

1,248,418 |

|

|

Axis Capital Holdings, Ltd. |

14,900 |

775,694 |

|

|

Banco Bradesco SA ADR (Brazil) |

394,321 |

4,215,291 |

|

|

Banco do Brasil SA (Brazil) |

341,701 |

3,018,995 |

|

|

Bank Negara Indonesia Persero Tbk PT (Indonesia) |

5,476,500 |

2,709,868 |

|

|

BB&T Corp. |

96,400 |

3,691,156 |

|

|

Berkshire Hathaway, Inc. Class B † |

58,134 |

8,209,102 |

|

|

Brixmor Property Group, Inc. R |

9,200 |

215,740 |

|

|

Capital One Financial Corp. |

74,800 |

6,047,580 |

|

|

China Cinda Asset Management Co., Ltd. (China) † |

4,907,000 |

2,920,580 |

|

|

China Construction Bank Corp. (China) |

1,020,000 |

992,657 |

|

|

China Merchants Bank Co., Ltd. (China) |

1,229,000 |

3,715,596 |

|

|

Chongqing Rural Commercial Bank Co., Ltd. (China) |

3,782,000 |

3,383,333 |

|

|

Chubb Corp. (The) |

10,600 |

1,042,510 |

|

|

Cullen/Frost Bankers, Inc. |

8,700 |

634,578 |

|

|

Everest Re Group, Ltd. |

6,086 |

1,088,846 |

|

|

Gentera SAB de CV (Mexico) † |

409,301 |

700,576 |

|

|

HCP, Inc. R |

62,700 |

2,526,183 |

|

|

Health Care REIT, Inc. R |

30,200 |

2,175,004 |

|

|

Industrial & Commercial Bank of China, Ltd. (China) |

830,000 |

721,057 |

|

|

Itau Unibanco Holding SA ADR (Preference) (Brazil) |

369,552 |

4,737,657 |

|

|

King’s Town Bank Co., Ltd. (Taiwan) |

1,282,000 |

1,315,156 |

|

|

Liberty Holdings, Ltd. (South Africa) |

206,971 |

2,880,934 |

|

|

MMI Holdings, Ltd. (South Africa) |

1,025,711 |

2,918,161 |

|

|

NASDAQ OMX Group, Inc. (The) |

4,800 |

233,424 |

|

|

Nedbank Group, Ltd. (South Africa) |

143,663 |

3,096,227 |

|

|

Northern Trust Corp. |

24,500 |

1,792,175 |

|

|

PartnerRe, Ltd. |

7,507 |

960,896 |

|

|

PNC Financial Services Group, Inc. |

55,500 |

5,091,015 |

|

|

Porto Seguro SA (Brazil) |

158,951 |

1,988,371 |

|

|

Public Storage R |

12,339 |

2,318,621 |

|

|

Quality Houses PCL (Thailand) |

26,265,516 |

2,469,986 |

|

|

RenaissanceRe Holdings, Ltd. |

6,754 |

692,217 |

|

|

RMB Holdings, Ltd. (South Africa) |

127,570 |

768,011 |

|

|

Spirit Realty Capital, Inc. R |

67,300 |

759,817 |

|

|

Starwood Property Trust, Inc. R |

37,600 |

902,776 |

|

|

Supalai PCL (Thailand) |

1,368,500 |

830,275 |

|

|

Synchrony Financial † |

22,000 |

685,300 |

|

|

Taishin Financial Holding Co., Ltd. (Taiwan) |

5,788,000 |

2,650,096 |

20 Absolute Return 700 Fund

|

COMMON STOCKS (43.5%)* cont. |

Shares |

Value |

|

|

Financials cont. |

|||

|

Taubman Centers, Inc. R |

9,100 |

$655,291 |

|

|

Travelers Cos., Inc. (The) |

44,700 |

4,519,617 |

|

|

Turkiye Is Bankasi Class C (Turkey) |

267,681 |

602,200 |

|

|

Turkiye Sinai Kalkinma Bankasi AS (Turkey) |

823,051 |

621,903 |

|

|

Visa, Inc. Class A |

101,700 |

6,717,285 |

|

|

Wells Fargo & Co. |

179,680 |

9,900,368 |

|

|

XL Group PLC |

46,500 |

1,724,220 |

|

|

113,359,261 |

|||

|

Health care (4.4%) |

|||

|

Abbott Laboratories |

113,500 |

5,268,670 |

|

|

AmerisourceBergen Corp. |

38,300 |

4,377,690 |

|

|

C.R. Bard, Inc. |

11,073 |

1,844,540 |

|

|

Cardinal Health, Inc. |

17,928 |

1,512,048 |

|

|

DaVita HealthCare Partners, Inc. † |

28,500 |

2,311,350 |

|

|

Edwards Lifesciences Corp. † |

17,900 |

2,267,035 |

|

|

Eli Lilly & Co. |

89,315 |

6,419,069 |

|

|

Johnson & Johnson |

98,985 |

9,819,312 |

|

|

Mednax, Inc. † |

13,700 |

969,686 |

|

|

Merck & Co., Inc. |

133,427 |

7,946,912 |

|

|

Netcare, Ltd. (South Africa) |

827,944 |

2,893,001 |

|

|

Pfizer, Inc. |

256,900 |

8,716,617 |

|

|

54,345,930 |

|||

|

Technology (8.0%) |

|||

|

Accenture PLC Class A |

63,800 |

5,911,070 |

|

|

Analog Devices, Inc. |

31,900 |

1,972,696 |

|

|

Apple, Inc. |

55,705 |

6,971,481 |

|

|

AU Optronics Corp. (Taiwan) |

6,380,000 |

3,217,301 |

|

|

Broadcom Corp. Class A |

90,200 |

3,987,291 |

|

|

Cisco Systems, Inc. |

277,800 |

8,008,974 |

|

|

Computer Sciences Corp. |

24,200 |

1,559,690 |

|

|

eBay, Inc. † |

118,700 |

6,915,462 |

|

|

EMC Corp. |

233,000 |

6,270,030 |

|

|

Fidelity National Information Services, Inc. |

21,700 |

1,356,033 |

|

|

Fiserv, Inc. † |

26,900 |

2,087,440 |

|

|

Gentex Corp. |

49,700 |

862,295 |

|

|

Innolux Corp. (Taiwan) |

6,235,000 |

3,223,286 |

|

|

Intuit, Inc. |

38,400 |

3,852,672 |

|

|

King Yuan Electronics Co., Ltd. (Taiwan) |

2,831,000 |

2,578,477 |

|

|

L-3 Communications Holdings, Inc. |

15,000 |

1,723,650 |

|

|

Linear Technology Corp. |

18,900 |

871,857 |

|

|

Maxim Integrated Products, Inc. |

48,100 |

1,579,123 |

|

|

Microsoft Corp. |

12,923 |

628,575 |

|

|

Motorola Solutions, Inc. |

5,600 |

334,600 |

|

|

NCSoft Corp. (South Korea) |

17,378 |

3,310,793 |

|

|

NetApp, Inc. |

53,300 |

1,932,125 |

|

|

NetEase, Inc. ADR (China) |

24,000 |

3,076,560 |

|

|

Paychex, Inc. |

55,400 |

2,680,806 |

|

|

Samsung Electronics Co., Ltd. (South Korea) |

7,991 |

10,480,312 |

|

|

SK Hynix, Inc. (South Korea) |

100,859 |

4,311,971 |

Absolute Return 700 Fund 21

|

COMMON STOCKS (43.5%)* cont. |

Shares |

Value |

|

|

Technology cont. |

|||

|

Taiwan Semiconductor Manufacturing Co., Ltd. ADR (Taiwan) |

319,500 |

$7,808,580 |

|

|

Tencent Holdings, Ltd. (China) |

112,800 |

2,329,596 |

|

|

99,842,746 |

|||

|

Transportation (1.7%) |

|||

|

AirAsia Bhd (Malaysia) |

3,589,900 |

2,286,145 |

|

|

CH Robinson Worldwide, Inc. |

25,200 |

1,622,628 |

|

|

China Eastern Airlines Corp., Ltd. (China) † |

940,000 |

721,410 |

|

|

Expeditors International of Washington, Inc. |

8,900 |

407,887 |

|

|

Korea Line Corp. (South Korea) † |

108,028 |

2,330,868 |

|

|

OHL Mexico SAB de CV (Mexico) † |

935,354 |

1,889,974 |

|

|

Turk Hava Yollari Anonim Ortakligi (Turkey) † |

707,925 |

2,352,124 |

|

|

United Parcel Service, Inc. Class B |

64,099 |

6,443,872 |

|

|

Yangzijiang Shipbuilding Holdings, Ltd. (China) |

2,807,900 |

3,102,396 |

|

|

21,157,304 |

|||

|

Utilities and power (2.1%) |

|||

|

Alliant Energy Corp. |

7,700 |

465,619 |

|

|

American Electric Power Co., Inc. |

56,200 |

3,196,094 |

|

|

American Water Works Co., Inc. |

16,400 |

894,128 |

|

|

Huadian Power International Corp., Ltd. (China) |

3,026,000 |

3,347,758 |

|

|

Huaneng Power International, Inc. (China) |

2,168,000 |

3,073,922 |

|

|

Kinder Morgan, Inc. |

151,900 |

6,524,105 |

|

|

Pinnacle West Capital Corp. |

18,700 |

1,144,440 |

|

|

Southern Co. (The) |

111,700 |

4,948,310 |

|

|

Tauron Polska Energia SA (Poland) |

1,778,065 |

2,381,838 |

|

|

Tenaga Nasional Bhd (Malaysia) |

128,100 |

515,619 |

|

|

26,491,833 |

|||

|

Total common stocks (cost $491,917,387) |

|

||

|

U.S. GOVERNMENT AND AGENCY |

Principal |

Value |

|

|

U.S. Government Agency Mortgage Obligations (23.7%) |

|||

|

Federal Home Loan Mortgage Corporation Pass-Through Certificates 4 1/2s, May 1, 2044 |

$2,627,439 |

$2,931,145 |

|

|

Federal National Mortgage Association Pass-Through Certificates |

|||

|

5 1/2s, TBA, May 1, 2045 |

3,000,000 |

3,396,094 |

|

|

4 1/2s, with due dates from May 1, 2041 to February 1, 2044 |

2,117,267 |

2,321,467 |

|

|

4 1/2s, TBA, June 1, 2045 |

2,000,000 |

2,174,062 |

|

|

4 1/2s, TBA, May 1, 2045 |

9,000,000 |

9,794,531 |

|

|

4s, with due dates from May 1, 2044 to June 1, 2044 |

1,895,277 |

2,046,157 |

|

|

4s, TBA, June 1, 2045 |

6,000,000 |

6,404,063 |

|

|

4s, TBA, May 1, 2045 |

18,000,000 |

19,237,500 |

|

|

3 1/2s, June 1, 2042 |

777,335 |

817,963 |

|

|

3 1/2s, TBA, May 1, 2045 |

42,000,000 |

44,008,125 |

|

|

3s, with due dates from January 1, 2043 to February 1, 2043 ## |

2,575,767 |

2,629,263 |

|

|

3s, TBA, May 1, 2045 |

198,000,000 |

201,495,928 |

|

|

297,256,298 |

|||

|

Total U.S. government and agency mortgage obligations (cost $298,010,210) |

|

||

22 Absolute Return 700 Fund

|

MORTGAGE-BACKED SECURITIES (14.3%)* |

Principal |

Value |

||

|

Agency collateralized mortgage obligations (7.3%) |

||||

|

Federal Home Loan Mortgage Corporation |

||||

|

IFB Ser. 2990, Class LB, 16.482s, 2034 |

$382,255 |

$510,777 |

||

|

IFB Ser. 3232, Class KS, IO, 6.119s, 2036 |

645,552 |

92,395 |

||

|

IFB Ser. 4104, Class S, IO, 5.919s, 2042 |

839,469 |

175,835 |

||

|

IFB Ser. 3116, Class AS, IO, 5.919s, 2034 |

628,924 |

28,609 |

||

|

IFB Ser. 3852, Class NT, 5.819s, 2041 |

2,180,467 |

2,268,296 |

||

|

IFB Ser. 317, Class S3, IO, 5.799s, 2043 |

3,826,276 |

976,875 |

||

|

IFB Ser. 308, Class S1, IO, 5.769s, 2043 |

4,577,927 |

1,170,942 |

||

|

IFB Ser. 314, Class AS, IO, 5.709s, 2043 |

2,355,323 |

584,381 |

||

|

Ser. 3687, Class CI, IO, 5s, 2038 |

1,692,415 |

245,282 |

||

|

Ser. 4122, Class TI, IO, 4 1/2s, 2042 |

1,852,843 |

310,907 |

||

|

Ser. 4193, Class PI, IO, 4s, 2043 |

4,066,856 |

673,452 |

||

|

Ser. 4116, Class MI, IO, 4s, 2042 |

4,135,660 |

789,131 |

||

|

Ser. 4213, Class GI, IO, 4s, 2041 |

2,907,436 |

397,447 |

||

|

Ser. 3996, Class IK, IO, 4s, 2039 |

5,716,569 |

705,065 |

||

|

Ser. 4013, Class AI, IO, 4s, 2039 |

5,533,668 |

806,403 |

||

|

Ser. 4305, Class KI, IO, 4s, 2038 |

11,013,871 |

1,222,870 |

||

|

Ser. 304, Class C53, IO, 4s, 2032 |

2,883,113 |

470,236 |

||

|

Ser. 4369, Class IA, IO, 3 1/2s, 2044 |

1,983,058 |

337,352 |

||

|

Ser. 311, IO, 3 1/2s, 2043 |

2,637,812 |

520,085 |

||

|

Ser. 303, Class C18, IO, 3 1/2s, 2043 |

5,446,828 |

1,092,260 |

||

|

Ser. 303, Class C19, IO, 3 1/2s, 2043 |

3,661,657 |

725,050 |

||

|

Ser. 4150, IO, 3 1/2s, 2043 |

4,175,222 |

870,687 |

||

|

Ser. 304, Class C22, IO, 3 1/2s, 2042 |

3,552,697 |

805,331 |

||

|

Ser. 4141, Class IM, IO, 3 1/2s, 2042 |

4,002,989 |

731,235 |

||

|

Ser. 4141, Class IQ, IO, 3 1/2s, 2042 |

1,983,350 |

357,015 |

||

|

Ser. 4121, Class AI, IO, 3 1/2s, 2042 |

7,106,072 |

1,425,462 |

||

|

Ser. 4122, Class CI, IO, 3 1/2s, 2042 |

6,467,781 |

855,844 |

||

|

Ser. 4136, Class IW, IO, 3 1/2s, 2042 |

4,127,415 |

613,956 |

||

|

Ser. 4166, Class PI, IO, 3 1/2s, 2041 |

3,129,585 |

495,194 |

||

|

Ser. 4097, Class PI, IO, 3 1/2s, 2040 |

5,604,890 |

748,496 |

||

|

Ser. 304, IO, 3 1/2s, 2027 |

1,906,942 |

211,842 |

||

|

Ser. 304, Class C37, IO, 3 1/2s, 2027 |

1,415,373 |

154,318 |

||

|

Ser. 4150, Class DI, IO, 3s, 2043 |

3,574,102 |

585,259 |

||

|

Ser. 4158, Class TI, IO, 3s, 2042 |

7,228,404 |

891,118 |

||

|

Ser. 4165, Class TI, IO, 3s, 2042 |

8,134,100 |

964,704 |

||

|

Ser. 4134, Class PI, IO, 3s, 2042 |

9,598,385 |

1,230,129 |

||

|

Ser. 4183, Class MI, IO, 3s, 2042 |

2,720,036 |

331,300 |

||

|

Ser. 4206, Class IP, IO, 3s, 2041 |

5,675,642 |

688,455 |

||

|

Ser. 4179, Class EI, IO, 3s, 2030 |

6,552,482 |

733,092 |

||

|

Ser. 304, Class C45, IO, 3s, 2027 |

3,001,640 |

317,308 |

||

|

Ser. 3939, Class EI, IO, 3s, 2026 |

6,040,417 |

553,206 |

||

|

FRB Ser. T-8, Class A9, IO, 0.466s, 2028 |

189,869 |

2,611 |

||

|

FRB Ser. T-59, Class 1AX, IO, 0.271s, 2043 |

460,749 |

5,597 |

||

|

Ser. T-48, Class A2, IO, 0.212s, 2033 |

673,812 |

6,501 |

Absolute Return 700 Fund 23

|

MORTGAGE-BACKED SECURITIES (14.3%)* cont. |

Principal |

Value |

||

|

Agency collateralized mortgage obligations cont. |

||||

|

Federal National Mortgage Association |

||||

|

IFB Ser. 05-74, Class NK, 26.594s, 2035 |

$64,757 |

$104,398 |

||

|

IFB Ser. 05-122, Class SE, 22.466s, 2035 |

188,340 |

278,079 |

||

|

IFB Ser. 11-4, Class CS, 12.538s, 2040 |

1,073,739 |

1,308,986 |

||

|

IFB Ser. 13-81, Class QS, IO, 6.019s, 2041 |

2,748,849 |

417,374 |

||

|

IFB Ser. 12-153, Class SK, IO, 5.969s, 2043 |

2,325,108 |

555,492 |

||

|

IFB Ser. 13-124, Class SB, IO, 5.769s, 2043 |

2,075,580 |

527,889 |

||

|

IFB Ser. 13-92, Class SA, IO, 5.769s, 2043 |

1,352,832 |

345,013 |

||

|

IFB Ser. 13-98, Class SA, IO, 5.769s, 2043 |

2,956,120 |

778,642 |

||

|

IFB Ser. 13-103, Class SK, IO, 5.739s, 2043 |

1,317,977 |

344,510 |

||

|

IFB Ser. 13-128, Class CS, IO, 5.719s, 2043 |

3,490,855 |

864,336 |

||

|

IFB Ser. 13-101, Class SE, IO, 5.719s, 2043 |

4,186,413 |

1,086,416 |

||

|

IFB Ser. 13-102, Class SH, IO, 5.719s, 2043 |

1,984,762 |

498,949 |

||

|

Ser. 397, Class 2, IO, 5s, 2039 |

55,519 |

9,133 |

||

|

Ser. 10-13, Class EI, IO, 5s, 2038 |

50,029 |

342 |

||

|

Ser. 15-4, Class IO, IO, 4 1/2s, 2045 |

3,224,625 |

627,512 |

||

|

Ser. 12-75, Class AI, IO, 4 1/2s, 2027 |

2,175,021 |

265,527 |

||

|

Ser. 14-47, Class IP, IO, 4s, 2044 |

8,522,868 |

1,138,478 |

||

|

Ser. 418, Class C24, IO, 4s, 2043 |

4,989,404 |

964,631 |

||

|

Ser. 13-44, Class PI, IO, 4s, 2043 |

1,344,876 |

205,934 |

||

|

Ser. 12-124, Class UI, IO, 4s, 2042 |

5,165,780 |

978,399 |

||

|

Ser. 12-118, Class PI, IO, 4s, 2042 |

5,187,384 |

964,914 |

||

|

Ser. 13-11, Class IP, IO, 4s, 2042 |

5,296,946 |

954,880 |

||

|

Ser. 12-96, Class PI, IO, 4s, 2041 |

1,369,441 |

211,551 |

||

|

Ser. 12-40, Class MI, IO, 4s, 2041 |

3,132,945 |

506,677 |

||

|

Ser. 12-22, Class CI, IO, 4s, 2041 |

4,560,538 |

751,958 |

||

|

Ser. 12-62, Class MI, IO, 4s, 2041 |

4,574,066 |

694,748 |

||

|

Ser. 406, Class 2, IO, 4s, 2041 |

262,756 |

36,339 |

||

|

Ser. 406, Class 1, IO, 4s, 2041 |

144,847 |

23,827 |

||

|

Ser. 409, Class C16, IO, 4s, 2040 |

638,523 |

109,991 |

||

|

Ser. 14-95, Class TI, IO, 4s, 2039 |

6,621,469 |

937,600 |

||

|

Ser. 12-104, Class HI, IO, 4s, 2027 |

6,406,494 |

808,992 |

||

|

Ser. 15-10, Class AI, IO, 3 1/2s, 2043 |

2,379,625 |

348,663 |

||

|

Ser. 418, Class C15, IO, 3 1/2s, 2043 |

8,640,913 |

1,705,771 |

||

|

Ser. 417, Class C24, IO, 3 1/2s, 2042 |

3,078,030 |

668,887 |

||

|

Ser. 12-136, Class PI, IO, 3 1/2s, 2042 |

3,640,238 |

430,422 |

||

|

Ser. 14-10, IO, 3 1/2s, 2042 |

3,471,348 |

553,583 |

||

|

Ser. 12-101, Class PI, IO, 3 1/2s, 2040 |

3,577,391 |

412,759 |

||

|

Ser. 14-76, IO, 3 1/2s, 2039 |

6,735,005 |

950,749 |

||

|

Ser. 13-21, Class AI, IO, 3 1/2s, 2033 |

4,112,827 |

754,210 |

||

|

Ser. 417, Class C19, IO, 3 1/2s, 2033 |

3,461,362 |

513,978 |

||

|

Ser. 12-93, Class DI, IO, 3 1/2s, 2027 |

4,877,455 |

595,781 |

||

|

Ser. 78, Class KI, IO, 3 1/2s, 2027 |

1,876,205 |

259,249 |

||

|

Ser. 12-53, Class BI, IO, 3 1/2s, 2027 |

3,318,949 |

400,099 |

||

|

Ser. 12-151, Class PI, IO, 3s, 2043 |

3,183,697 |

407,195 |

||

|

Ser. 13-8, Class NI, IO, 3s, 2042 |

5,542,437 |

738,348 |

||

|

Ser. 6, Class BI, IO, 3s, 2042 |

6,936,161 |

685,986 |

||

|

Ser. 13-35, Class IP, IO, 3s, 2042 |

3,325,628 |

356,336 |

24 Absolute Return 700 Fund

|

MORTGAGE-BACKED SECURITIES (14.3%)* cont. |

Principal |

Value |

||

|

Agency collateralized mortgage obligations cont. |

||||

|

Federal National Mortgage Association |

||||

|

Ser. 13-23, Class PI, IO, 3s, 2041 |

$4,322,497 |

$392,050 |

||

|

Ser. 13-31, Class NI, IO, 3s, 2041 |

6,191,012 |

574,650 |

||

|

Ser. 13-7, Class EI, IO, 3s, 2040 |

4,687,253 |

751,273 |

||

|

Ser. 13-55, Class MI, IO, 3s, 2032 |

3,165,608 |

379,208 |

||

|

FRB Ser. 03-W10, Class 1, IO, 0.955s, 2043 |

244,445 |

5,567 |

||

|

Ser. 98-W5, Class X, IO, 0.871s, 2028 |

355,121 |

17,534 |

||

|

Ser. 98-W2, Class X, IO, 0.76s, 2028 |

1,206,682 |

63,351 |

||

|

Ser. 08-36, Class OV, PO, zero %, 2036 |

24,936 |

23,245 |

||

|

Federal National Mortgage Association Connecticut Avenue Securities FRB Ser. 15-C01, Class 2M2, 4.731s, 2025 |

253,000 |

261,653 |

||

|

Government National Mortgage Association |

||||

|

IFB Ser. 11-81, Class SB, IO, 6.523s, 2036 |

1,988,577 |

272,634 |

||

|

IFB Ser. 11-93, Class SA, IO, 6.479s, 2041 |

8,143,437 |

1,871,494 |

||

|

Ser. 09-79, Class IC, IO, 6s, 2039 |

2,884,886 |

574,006 |

||

|

IFB Ser. 13-129, Class SN, IO, 5.969s, 2043 |

1,176,526 |

202,657 |

||

|

IFB Ser. 13-129, Class CS, IO, 5.969s, 2042 |

3,053,833 |

440,576 |

||

|

IFB Ser. 14-90, Class HS, IO, 5.919s, 2044 |

2,365,765 |

575,756 |

||

|

IFB Ser. 12-77, Class MS, IO, 5.919s, 2042 |

2,301,929 |

604,233 |

||

|

IFB Ser. 13-99, Class VS, IO, 5.918s, 2043 |

1,331,297 |

278,401 |

||

|

IFB Ser. 12-34, Class SA, IO, 5.869s, 2042 |

2,973,208 |

666,742 |

||

|

IFB Ser. 11-70, Class SN, IO, 5.718s, 2041 |

1,504,883 |

256,116 |

||

|

IFB Ser. 11-70, Class SH, IO, 5.708s, 2041 |

1,812,942 |

313,675 |

||

|

Ser. 14-133, Class IP, IO, 5s, 2044 |

4,914,762 |

1,069,207 |

||

|