Exhibit 99.1

MOUNTAIN PROVINCE DIAMONDS INC.

Annual Information Form

For the

Year Ended December 31, 2017

March 26, 2018

MOUNTAIN PROVINCE DIAMONDS INC.

TABLE OF CONTENTS

| CORPORATE STRUCTURE | 2 |

| NAME, ADDRESS AND INCORPORATION | 2 |

| INTERCORPORATE RELATIONSHIPS | 3 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 3 |

| THREE YEAR HISTORY | 4 |

| DESCRIPTION OF THE BUSINESS | 6 |

| GENERAL | 6 |

| Principal Markets and Distribution | 6 |

| Competitive Conditions | 6 |

| Employees | 7 |

| Specialized Skills and Knowledge | 7 |

| Environmental Protection | 7 |

| MINERAL PROPERTIES (The Gahcho Kué Diamond Mine) | 8 |

| Technical Report | 8 |

| Property Location, Access and Infrastructure | 8 |

| Overall Site Plan | 9 |

| History | 9 |

| Mineral Tenure and Royalties | 9 |

| Permits and Agreements | 10 |

| Mineral Reserve and Mineral Resource Estimates | 10 |

| Mining Method | 12 |

| Recovery Methods | 12 |

| Underground Mining | 12 |

| Capital and Operating Costs | 13 |

| Capital Cost Estimate | 13 |

| Operating Cost Estimate | 13 |

| Other Relevant Data and Information | 14 |

| Social and Environmental Policies | 14 |

| Aboriginal Issues and Local Resources at the GK Diamond Mine | 14 |

| Environmental Requirements for the GK Diamond Mine | 14 |

| RISKS FACTORS | 15 |

| DIVIDENDS | 20 |

| DESCRIPTION OF CAPITAL STRUCTURE | 20 |

| MARKET FOR SECURITIES | 22 |

| DIRECTORS AND OFFICERS | 22 |

| AUDIT COMMITTEE | 26 |

| LEGAL PROCEEDINGS | 27 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 27 |

| TRANSFER AGENT AND REGISTRAR | 27 |

| INTERESTS OF EXPERTS | 27 |

| MATERIAL CONTRACTS | 28 |

| ADDITIONAL INFORMATION | 28 |

| APPENDIX 1: AUDIT COMMITTEE CHARTER | 28 |

| APPENDIX 2: GLOSSARY OF TERMS USED FREQUENTLY IN THIS DOCUMENT | 32 |

Currency

Unless otherwise specified, all dollar references are to Canadian dollars. On March 26, 2018, one Canadian dollar was worth approximately $0.776 in United States currency, based on the noon exchange rate of the Bank of Canada.

Caution Regarding Forward-Looking Information

This Annual Information Form (“AIF”) contains certain “forward-looking statements” and “forward-looking information” under applicable Canadian and United States securities laws concerning the business, operations and financial performance and condition of Mountain Province Diamonds Inc. Forward-looking statements and forward-looking information include, but are not limited to, statements with respect to estimated production and mine life of the project of Mountain Province; the realization of mineral reserve estimates; the timing and amount of estimated future production; costs of production; the future price of diamonds; the estimation of mineral reserves and resources; the ability to manage debt; capital expenditures; the ability to obtain permits for operations; liquidity; tax rates; and currency exchange rate fluctuations. Except for statements of historical fact relating to Mountain Province, certain information contained herein constitutes forward-looking statements. Forward-looking statements are frequently characterized by words such as “anticipates,” “may,” “can,” “plans,” “believes,” “estimates,” “expects,” “projects,” “targets,” “intends,” “likely,” “will,” “should,” “to be”, “potential” and other similar words, or statements that certain events or conditions “may”, “should” or “will” occur. Forward-looking statements are based on the opinions and estimates of management at the date the statements are made, and are based on a number of assumptions and subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. Many of these assumptions are based on factors and events that are not within the control of Mountain Province and there is no assurance they will prove to be correct.

Factors that could cause actual results to vary materially from results anticipated by such forward-looking statements include variations in ore grade or recovery rates, changes in market conditions, changes in project parameters, mine sequencing; production rates; cash flow; risks relating to the availability and timeliness of permitting and governmental approvals; supply of, and demand for, diamonds; fluctuating commodity prices and currency exchange rates, the possibility of project cost overruns or unanticipated costs and expenses, labour disputes and other risks of the mining industry, failure of plant, equipment or processes to operate as anticipated.

These factors are discussed in greater detail in this AIF and in Mountain Province's most recent MD&A filed on SEDAR, which also provide additional general assumptions in connection with these statements. Mountain Province cautions that the foregoing list of important factors is not exhaustive. Investors and others who base themselves on forward-looking statements should carefully consider the above factors as well as the uncertainties they represent and the risk they entail. Mountain Province believes that the expectations reflected in those forward-looking statements are reasonable, but no assurance can be given that these expectations will prove to be correct and such forward-looking statements included in this AIF should not be unduly relied upon. These statements speak only as of the date of this AIF.

| 1 |

Although Mountain Province has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Mountain Province undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements. Statements concerning mineral reserve and resource estimates may also be deemed to constitute forward-looking statements to the extent they involve estimates of the mineralization that will be encountered as the property is developed.

Further, Mountain Province may make changes to its business plans that could affect its results. The principal assets of Mountain Province are administered pursuant to a joint venture under which Mountain Province is not the operator. Mountain Province is exposed to actions taken or omissions made by the operator within its prerogative and/or determinations made by the joint venture under its terms. Such actions or omissions may impact the future performance of Mountain Province. Under its current note and revolving credit facilities Mountain Province is subject to certain limitations on its ability to pay dividends on common stock. The declaration of dividends is at the discretion of Mountain Province’s Board of Directors, subject to the limitations under the Company’s debt facilities, and will depend on Mountain Province’s financial results, cash requirements, future prospects, and other factors deemed relevant by the Board.

CORPORATE STRUCTURE

Name, Address and Incorporation

Mountain Province Diamonds Inc., formerly Mountain Province Mining Inc., was formed on November 1, 1997 by the amalgamation of Mountain Province Mining Inc. ("Old MPV") and 444965 B.C. Ltd. ("444965"). The Company changed its name from Mountain Province Mining Inc. to Mountain Province Diamonds Inc. effective October 16, 2000. It commenced trading under its new name on the Toronto Stock Exchange (the “TSX”) on October 25, 2000.

Pursuant to an arrangement agreement (the "Arrangement Agreement") with Glenmore Highlands Inc. (“Glenmore”) dated May 10, 2000, Glenmore was amalgamated with a wholly owned subsidiary of the Company to form a new wholly-owned subsidiary ("Mountain Glen") of the Company. Glenmore had two wholly-owned subsidiaries, Baltic Minerals BV, incorporated in the Netherlands, and Baltic Minerals Finland OY, incorporated in Finland. Pursuant to the Arrangement Agreement, these companies became wholly-owned subsidiaries of the Company.

Pursuant to an Assignment and Assumption Agreement dated March 25, 2004 between the Company and Mountain Glen, Mountain Glen distributed its property and assets in specie to the Company. Mountain Glen was voluntarily dissolved on August 4, 2004. Baltic Minerals BV and its subsidiary Baltic Minerals Finland OY were voluntarily dissolved in 2006.

On September 20, 2005, the Company continued incorporation under the Business Corporations Act (Ontario).

On October 1, 2014, Camphor Ventures Inc. (formerly Sierra Madre Resources Inc.) and the Company were amalgamated under the name “Mountain Province Diamonds Inc.”

On October 2, 2014, 2435386 Ontario Inc. was incorporated as a wholly owned subsidiary of the Company. At the request of the project debt facility lenders, the participating interest of the Company in the Gahcho Kué Project was transferred to 2435386 Ontario Inc. in exchange for common shares of 2435386 Ontario Inc.

| 2 |

On October 3, 2014, 2435572 Ontario Inc. was incorporated as a wholly owned subsidiary of the Company.

On October 3, 2014, the Company transferred the shares of 2435386 Ontario Inc. to 2435572 Ontario Inc. in exchange for common shares of 2435572 Ontario Inc.

The names of the Company's subsidiaries, their dates of incorporation and the jurisdictions in which they were incorporated as at the date of filing of this Annual Report, are as follows:

| Name of Subsidiary | Date of Incorporation | Jurisdiction of Incorporation | ||

| 2435386 Ontario Inc. | October 2, 2014 | Ontario Canada | ||

| 2435572 Ontario Inc. | October 3, 2014 | Ontario Canada |

The Company's registered, records, administrative, and executive office is at 161 Bay Street, Suite 1410, PO Box 216, Toronto, Ontario, Canada M5J 2S1, the telephone number is (416) 361-3562, and the fax number is (416) 603-8565.

The Company is a reporting issuer in every province of Canada other than Quebec, and the common shares of the Company are listed and posted for trading on the TSX and NASDAQ under the symbol “MPVD”.

Intercorporate Relationships

As at March 26, 2018, Mountain Province’s corporate structure was as follows:

GENERAL DEVELOPMENT OF THE BUSINESS

Mountain Province Diamonds Inc. is focused on the mining and marketing of rough diamonds to the global market. The Company supplies rough diamonds to the global market from its 49% ownership interest in the Gahcho Kué diamond mine (the “GK Diamond Mine”. The GK Diamond Mine is located in Canada’s Northwest Territories.

The Company acquired its interest in the mineral claims and properties that were developed into the GK Diamond Mine in August 1992. The GK Diamond Mine was built and is operated by a joint venture (the “Gahcho Kué Joint Venture”) in which the Company has an undivided 49% interest. The other joint venture participant, De Beers Canada Inc. (“De Beers”), has an undivided 51% interest.

| 3 |

Three Year History

Fiscal 2015

On April 2, 2015, the Company through its subsidiary, 2435572 Ontario Inc. entered into a Loan Facility of US$370 million with a syndicate of lenders led by Scotiabank, Natixis S.A. and Nedbank Ltd. and including ING Capital LLC, Export Development Canada and the Bank of Montreal. On April 29, 2015, Société Générale joined the lender syndicate. The term of the Loan Facility was seven years and the interest rate was U.S. dollar LIBOR plus 5.5 percent. The Loan Facility agreement can be viewed at www.SEDAR.com filed on March 28, 2016 under ‘Material contracts – Credit agreements’.

The Loan Facility was used to fund the Company’s share of the construction costs of the GK Diamond Mine, associated fees, operating costs, working capital during the build-up to commercial production, as defined below, general and administrative costs, interest costs and the repayment of $10 million of sunk costs, which became payable to De Beers upon achieving and maintaining 30 days running at 70% of designed production capacity, which is approximately 5,833.1 tonnes of ore processed per day. This was achieved on March 1, 2017 and De Beers was paid at the end of March, 2017. At September 30, 2017, the Company had drawn US$357 million against Loan Facility. The remaining US$13 million was not drawn.

On April 8, 2015, the Company deposited $93,345,000 into a restricted cost overrun account in 2435572 Ontario Inc. These funds were in addition to, and as partial security for repayment of, the Loan Facility.

On April 7, 2015, the Company entered into U.S. dollar interest rate swaps to manage interest rate risk associated with the U.S. dollar variable rate Loan Facility and entered into foreign currency forward strip contracts to mitigate the risk that a devaluation of the U.S. dollar against the Canadian dollar would reduce the Canadian dollar equivalent to the U.S. dollar Loan Facility and the Company would not have sufficient Canadian dollar funds to develop the GK Diamond Mine. On July 10, 2015, the Company entered into additional foreign currency forward strip contracts from August 4, 2015 to February 1, 2017.

Fiscal 2016

During 2016, the construction of the GK Diamond Mine was substantially completed and during June 2016 the Company announced that the GK Diamond Mine had achieved mechanical completion of the primary crusher and that commissioning of the process plant was progressing well. On August 3, 2016, the Company announced that commissioning of the Gahcho Kué diamond plant had been completed ahead of schedule, that ramp up to commercial production had commenced and that the GK Diamond Mine remained on track to achieve commercial production on schedule during the first quarter of 2017. On March 2, 2017, the Company announced that it had declared commercial production on March 1, 2017.

During 2016, the Company through its subsidiary 2435386 Ontario Inc. signed agreements with Diamond Manufacturing Management and Consultancy Ltd. (“DMMC”), a company incorporated in Mauritius, Worldwide Diamond Manufacturers Pvt Ltd. (“WDM”), a company incorporated in India, and with Bonas-Couzyn (Antwerp) N.V. (“Bonas”), a Company incorporated in Belgium to provide consultancy, cleaning and sorting services and marketing of the diamonds respectively.

DMMC is a diamond consulting company and has technical experts who are assisting in overseeing the sorting and pricing of the rough diamonds before they are sent to WDM to be cleaned and sorted into saleable parcels. On completion of the cleaning and sorting the rough diamonds are sent to Bonas based in Antwerp where they are presented to purchasers selected by Bonas and 2435386 Ontario Inc. for sale by open tender.

| 4 |

Fiscal Year 2017

On March 1, 2017, De Beers as Operator of the GK Diamond Mine determined that over a 30-day period, approximately 70% of the designed production capacity among other criteria had been achieved, and commercial production was declared for financial reporting purposes. During 2017 the GK Diamond Mine recovered approximately 5.9 million carats of diamonds on a 100% basis and the Company received its 49% share or approximately 2.9 million carats. During 2017, the Company sold approximately 2.7 million carats of diamonds, including pre-commercial production sales. The Company conducted ten sales during 2017.

Under the Gahcho Kué Joint Venture Agreement (see Mineral Properties – History on page 8), commercial production for sunk cost repayment purposes is based on the first day after 30 days (excluding maintenance days) of achieving and maintaining 70% of designed production capacity. For royalty purposes for the Government of the Northwest Territories, commercial production is based on the first day after 90 days of achieving 60% of designed production capacity.

In December 2017, the Company through its subsidiary 2435386 Ontario Inc. renewed agreements with DMMC, WDM and Bonas for 12 months to December 31, 2018.

On December 11, 2017, Mountain Province closed a private offering of U.S.$330,000,000 senior secured second lien notes due December 15, 2022 (the "Notes"). The Notes accrue interest at a coupon rate of 8.0% per year, payable semi-annually in arrears. Pursuant to an indenture, dated December 11, 2017, between Mountain Province, the guarantors and Computershare Trust Company, N.A. (the "Mountain Province Indenture"), the Notes are initially guaranteed on a senior secured basis by all of Mountain Province's existing subsidiaries and thereafter by all of Mountain Province's restricted subsidiaries (as such term is defined in the Mountain Province Indenture). The Notes and the guarantees are secured on a second-priority basis by substantially all of the assets of Mountain Province and the guarantors, including diamonds in inventory, equity interests in the guarantors and the assignment and pledge of Mountain Province's participation interests and rights in the Gahcho Kué Joint Venture, subject to certain customary exceptions.

Mountain Province used the net proceeds from the offering of the Notes, together with cash on its balance sheet, to fully repay and terminate its U.S.$370 million project loan facility (of which U.S.$357 million was outstanding as of September 30, 2017), to fully repay amounts owing to De Beers for historic sunk costs related to the development of the mine (of which approximately C$48.5 million of costs and accumulated interest was outstanding as of September 30, 2017), and to pay related fees and expenses of the offering of the Notes and the entry into the Revolving Credit Agreement. The Notes agreement can be viewed at www.SEDAR.com filed on December 21, 2017 under ‘Material documents’.

Concurrently with the closing of the Notes offering, Mountain Province entered into an undrawn U.S.$50 million first lien revolving credit facility agreement, dated December 11, 2017, among 2435572 as borrower, Mountain Province and 2435386 as guarantors, Scotiabank as administrative agent, and Scotiabank and Nedbank Limited, London Branch as lenders (the "Revolving Credit Agreement"). The liens securing the Notes are junior to liens securing the Revolving Credit Agreement.

The Revolving Credit Agreement contains customary covenants for such facility and financial maintenance covenants, including total leverage ratio and interest coverage ratio. The Revolving Credit Agreement also restricts Mountain Province's ability to make certain payments and distributions, including dividend payments, except where no default or event of default has occurred or would result and certain threshold tests of financial health are met.

| 5 |

Fiscal Year 2018

During 2018, the GK Diamond Mine expects to recover approximately 6.5 million carats of diamonds on a 100% basis and the Company expects to receive its 49% share or approximately 3.2 million carats. The Company expects to conduct ten sales during 2018.

On January 29, 2018, Mountain Province and Kennady jointly announced that they had entered into a definitive arrangement agreement dated January 28, 2018 (the “Kennady Arrangement Agreement”), whereby, subject to the terms and conditions of the Kennady Arrangement Agreement, Mountain Province will acquire all of the issued and outstanding common shares of Kennady Diamonds Inc. (“Kennady”) by way of a statutory plan of arrangement (the “Kennady Arrangement”) under the Business Corporations Act (Ontario). Under the terms of the Kennady Arrangement, shareholders of Kennady will be entitled to receive, in exchange for each common share of Kennady held at the effective time of the Kennady Arrangement, 0.975 of a common share of Mountain Province. The Kennady Arrangement constitutes a "related party transaction" for purposes of Multilateral Instrument 61-101, because (i) Kennady is a "related party" of the Company by virtue of Mr. Dermot Fachtna Desmond, together with Bottin (International) Investments Ltd., a corporation controlled by him, being a "control person" (as defined in section 1(1) of the Securities Act (Ontario)) of both the Company and Kennady, and (ii) the Arrangement will result in the Company acquiring Kennady through an arrangement.

The Kennady Arrangement Agreement can be viewed at www.sedar.com, filed on February 7, 2018 under 'Material documents'. The Kennady Arrangement is anticipated to become effective on or about April 13, 2018, subject to obtaining the required approvals from the shareholders of both Mountain Province and Kennady, the final order from the Ontario Superior Court of Justice (Commercial List) and the satisfaction or waiver of all other closing conditions.

Concurrently with the signing of the Kennady Arrangement Agreement, the Company entered into voting and support agreements (the "Kennady Voting and Support Agreements") with certain Kennady shareholders, namely Mr. Desmond, Bottin (International) Investments Ltd., and all of the directors and officers of Kennady, pursuant to which, and subject to the terms of which, they have agreed, among other things, to vote their common shares of Kennady in favour of the Kennady Arrangement resolution. On March 16, 2018, the Company announced it had signed a non-binding memorandum of understanding (“MoU”) with De Beers. The MoU contemplates a framework under which properties owned by Kennady into the Gahcho Kué joint venture, in the event that the Company’s proposed acquisition of Kennady is approved. The Company and De Beers will now work towards a definitive agreement based on the MoU.

DESCRIPTION OF THE BUSINESS

General

The Company is focused on the mining and marketing of rough diamonds to the global market. The Company’s participation in the mining sector of the diamond industry is through its ownership interest in 2435386 Ontario Inc., which is a 49% participant in the Gahcho Kué Joint Venture which owns and operates the GK Diamond Mine in the Northwest Territories.

Principal Markets and Distribution

The Company markets its 49% share of production from the GK Diamond Mine by sorting and valuing diamonds that are then sold into the international diamond market in Antwerp, Belgium.

Competitive Conditions

The Global Diamond Industry Report 2017 published by Bain & Company Inc. (the “Bain Report”), reported a return to normal trading conditions across the diamond industry through 2016 into mid-year 2017.

According to the Bain Report, rough diamond producers reported increased sales in 2016 due to sell down of inventories, with the top five producers’ aggregate operating profit increasing approximately 3%.

In late 2016, the rough diamond market faced disruption from the Indian government’s demonetization of large-denomination currency notes, which halted much of the cash-driven manufacturing industry in Indian cutting centres. Rough diamond producers posted a small decline in H1 2017 revenues, due in part to lower price assortments making up an increasing share of sales. By mid 2017 the effects of demonetization had largely dissipated, with Indian polished centres returning to operational capacity and India’s jewellery retail sector reporting strengthening demand.

| 6 |

Midstream players saw a brief return to profitability in 2016 as rough prices declined faster than polished, however this trend was reversed in the first half of 2017 renewing pressure on manufacturing margins. Polished manufacturers are focused on operational improvement initiatives and new technology investments in order to reduce cycle times, optimise polishing yields and secure financing.

The Bain Report states that global retail sales of diamond jewellery remained stable in US dollar terms in 2016. The medium-term outlook is also stable with major retail chains in key markets reporting flat or increasing revenues amid healthy macroeconomic fundamentals. Retailers are diversifying their sales platforms as consumers move increasingly to online sales.

Three persistent and urgent challenges are being addressed by the diamond industry. In the face of increased competition from other luxury goods and experiences, rough diamond producers have invested U.S.$150 million in promotional spend with the aim of increasing consumer demand for natural diamonds. The industry continues its efforts to protect the natural diamond supply chain from the threat of contamination by laboratory grown diamonds. Efforts focus on synthetic stone detection, disclosure and differentiation, with technologies developing rapidly in recent years. The third challenge faced by the industry is the overall profitability of the midstream sector. While key players in this segment operate effective, profitable business models, the majority of the segment must address operating inefficiencies and sustainable access to finance.

Employees

As at March 26, 2018, the Company had 7 employees and retained 2 part-time consultants.

Persons employed at the GK Diamond Mine are employees of De Beers, the operator of the GK Diamond Mine.

Specialized Skills and Knowledge

The Company’s success at marketing diamonds is dependent on the services of key executives and skilled employees, and the continuance of key relationships with certain third parties, such as diamantaires for the marketing of rough diamonds. The Company competes for these skilled employees with other diamond producers.

De Beers, as operator of the GK Diamond Mine, is responsible for ensuring that it has the mining engineers and skilled miners required to mine the diamonds and process the diamond production from the GK Diamond Mine. De Beers competes for these skilled employees with other mines in the Northwest Territories and elsewhere in Canada. The Company is not responsible for the hiring or retention of these skilled employees.

Environmental Protection

The Gahcho Kué Diamond Mine are subject to environmental requirements and conditions of operation contained in several statutes and administered by Canadian federal and Northwest Territorial authorities. These requirements and conditions may change from time to time, and a breach of legislation may result in the imposition of fines or penalties. Environmental legislation continues to evolve in a manner such that standards, enforcement, fines and penalties for non-compliance are becoming stricter. Environmental assessments of proposed projects carry a heightened degree of responsibility for companies, directors, officers and employees. The cost of compliance with changes in government regulations has the potential to reduce the profitability of future operations.

Northwest Territories’ requirements are administered by the various territorial government departments and Workers’ Safety and Compensation Commission-Prevention Services. Laws and regulations that might impact the Gahcho Kué Diamond Mine include those that protect heritage resources, wildlife and the environment and those that regulate workplace safety, mine safety, training in the handling of dangerous materials, road transportation, air quality, and the use of hazardous substances and pesticides.

| 7 |

Mineral Properties

The Gahcho Kué Diamond Mine

The Company has no other mineral properties other than its 49% undivided interest in the GK Diamond Mine.

Technical Report

The Company has published an updated technical report in respect of the GK Diamond Mine titled “Gahcho Kué Mine NI-43-101 Technical Report” and dated March 16th, 2018 (with information effective as of December 31st, 2017) (the “2017 Technical Report”) as prepared and completed by JDS Energy and Mining Inc. (“JDS”), filed by the Company on SEDAR on March 26, 2018 and concurrently on EDGAR under Form 6K. The following summary is derived from the 2017 Technical Report.

Property Location, Access and Infrastructure

The GK Diamond Mine is located in the Northwest Territories (“NWT”) of Canada, in the District of Mackenzie, 300 km east-northeast of Yellowknife and 80 km east-southeast of the Snap Lake Mine (owned by De Beers and currently on care and maintenance). The site lies on the edge of the continuous permafrost zone in an area known as the barren lands. The surface is characterised as heath/tundra, with occasional knolls, bedrock outcrops, and localised surface depressions interspersed with lakes. A thin discontinuous cover of organic and mineral soil overlies primarily bedrock, which, occurs typically within a few metres of surface. Some small stands of stunted spruce are found in the area. There are myriad lakes in the area. Kennady Lake, under which the kimberlite pipes lie, is a local headwater lake with a minimal catchment area.

A winter road connects Yellowknife to the Snap Lake, Ekati, and Diavik mines during February and March each year (Figure 1-1). The road is operated under a Licence of Occupation by the winter road joint venture partners who operate the Ekati, Diavik, and Snap Lake mines (Snap Lake ceased operations in December 2015). The GK Diamond Mine became a winter road joint venture partner in 2013. The road passes within 70 km of the GK Diamond Mine, at Mackay Lake. A 120 km winter road spur has been established from Mackay Lake to the project site, and was open in 1999, 2001, 2002, 2006, 2013, 2014, 2015, 2016 and 2017. The 120 km winter road spur will be constructed each year to support the mining operation.

The GK Diamond Mine is typical of many northern Canadian mining operations that lack local and regional infrastructure such as permanent road access, navigable shipping routes and ports, and external utilities. Therefore, the Gahcho Kué site requires extensive infrastructure to sustain operations, including power generation, sewage and water treatment, personnel accommodation for 478 people, storage facilities for materials delivered on the limited annual winter ice road, and a 1600-meter-long gravel airstrip that can be accessed in both summer and winter months with small and large aircrafts during the day and at night to provide year-round cargo, food and passenger aircraft access.

| 8 |

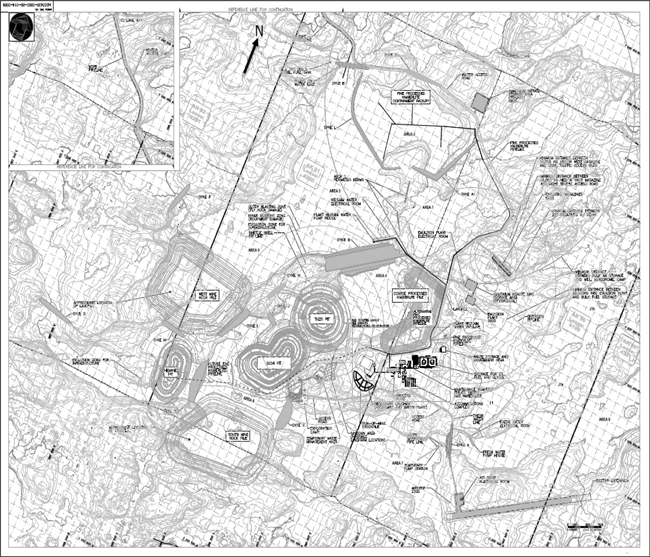

Overall Site Plan

History

In August 1992, the Company acquired a 100% interest in the mineral properties upon which the GK Diamond Mine is situated. During 2002, the Company entered into the Gahcho Kué Joint Venture Agreement with De Beers and Camphor Ventures Inc. This agreement provided that De Beers could have earned up to a 55% interest in the project by funding and completing a positive definitive feasibility study.

The agreement also provided that De Beers could have earned up to a 60% interest in the project by funding development and construction of a commercial-scale mine. This Gahcho Kué Joint Venture Agreement was amended and restated in July 2009, pursuant to which the De Beers ownership interest was established at 51% of the GK Diamond Mine and the Company’s at 49%.

Mineral Tenure and Royalties

A royalty is payable to the government of the Northwest Territories (the “NWT Royalty”). The NWT Royalty is equal to the lesser of either (i) 13% of the output value of the mine, or (ii) an amount calculated based on a sliding scale of royalty rates dependent upon the value of output of the mine, that can range from 0% to 14%.

| 9 |

Permits and Agreements

Exploration programs to date were conducted under the permits obtained from the appropriate authority, including:

• Indian and Northern Affairs Canada – Type A Land Use Permit

• Indian and Northern Affairs Canada – Type B Water Licence

• Workers’ Compensation Board, Mine Health and Safety – Drilling Authorization

• Indian and Northern Affairs Canada – Quarry Permit

• Indian and Northern Affairs Canada – Registration of Fuel Storage Tanks

• Prince of Wales Northern Heritage Centre – Archaeology.

On August 12, 2014, De Beers and the Company announced that the Mackenzie Valley Land and Water Board had issued the Gahcho Kué Type A Land Use Permit and sent the Type A Water License for final approval to the Minister of Environment and Natural Resources (of the Government of the Northwest Territories.

On September 25, 2014, De Beers and the Company announced that the Gahcho Kué Project had received approval of the Type A Water License by the Minister of Environment and Natural Resources of the Government of the Northwest Territories.

Mineral Reserve and Mineral Resources Estimates

Summarized from the 2017 Technical Report (depleted for production up to December 31, 2017):

Table 1.1 Mineral Reserves Summary (as of December 31, 2017) (Presented on a 100% basis)

| Pipe | Classification | Tonnes (Mt) | Carats (Mct) | Grade (cpt) | ||||||||||

| 5034 | Probable | 9.7 | 18.4 | 1.91 | ||||||||||

| Hearne | Probable | 5.5 | 10.9 | 1.99 | ||||||||||

| Tuzo | Probable | 15.7 | 19.1 | 1.22 | ||||||||||

| In-Situ Total | Probable | 30.9 | 48.4 | 1.57 | ||||||||||

| Stockpile | Probable | 0.6 | 1.0 | 1.61 | ||||||||||

| Total | Probable | 31.5 | 49.4 | 1.57 | ||||||||||

Notes:

| (1) | Mineral Reserves are reported at a bottom cut-off of 1.0 mm |

| (2) | Mineral Reserves have been depleted to account for mining and processing activity prior to Dec 31 2017. |

| (3) | Q4 2017 depletion is based on forecasted values and may differ slightly from actual depletion. |

| (4) | Mineral Reserves are based upon the updated resource model (2017) and therefore reflect any changes to the estimation of Tonnes, Grade and Contained Carats within that resource. Details on resource changes are summarized in Section 14. |

| (5) | Prices used to determine optimal pit shells have been escalated by factors varying by pit, which are indicative of the respective pits timing and duration. |

| 10 |

Table 1.2 Mineral Resources Summary (as of December 31, 2017) (Presented on a 100% basis)

| Resource | Classification | Tonnes (Mt) | Carats (Mct) | Grade (cpt) | ||||||||||

| 5034 | Indicated | 0.9 | 1.5 | 1.61 | ||||||||||

| Inferred | 0.8 | 1.3 | 1.63 | |||||||||||

| Hearne | Indicated | 0.2 | 0.3 | 1.68 | ||||||||||

| Inferred | 1.2 | 2.1 | 1.75 | |||||||||||

| Tuzo | Indicated | 0.8 | 0.9 | 1.14 | ||||||||||

| Inferred | 10.8 | 14.6 | 1.35 | |||||||||||

| Summary (In-Situ) | Indicated | 1.8 | 2.6 | 1.42 | ||||||||||

| Inferred | 12.8 | 18.0 | 1.40 | |||||||||||

| Stockpiles | Indicated | 0.0 | 0.0 | 0.0 | ||||||||||

| Inferred | 0.0 | 0.0 | 1.15 | (3) | ||||||||||

Notes:

| (1) | Mineral Resources are reported at a bottom cut-off of 1.0 mm. Incidental diamonds are not incorporated in grade calculations. |

| (2) | Mineral Resources are not mineral reserves and do not have demonstrated economic viability. |

| (3) | Volume, tonnes and carats are rounded to the nearest 100,000. 12,300t of inferred resources stockpiled @ 1.15cpt (14,250cts total). |

| (4) | Tuzo volume and tonnes exclude 0.6 Mt of a granite raft and CRX_BX. |

| (5) | Resources are exclusive of indicated tonnages converted to probable reserves. |

| (6) | Resources have been depleted of any material that was processed prior to and including Dec 31 2017. Q4 depletion is based on forecasted values and may differ slightly from actual values. |

Table 1.1 and 1.2 were reviewed by JDS and complies with CIM definitions and standards for an operating mine and with the standards of National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”). The economic viability presented in Section 22 of the “2017 Technical Report” confirms that the probable reserve estimates meet and comply with CIM definitions and standards. At the time of this report, the mine is economically viable using current diamond prices and prevailing long-term price estimates

Cautionary Note to United States Investors Concerning Disclosure of Mineral Reserves and Resources:

The Company is organized under the laws of Canada. The mineral reserves and resources described herein are estimates, and have been prepared in compliance with NI 43-101. The definitions of proven and probable reserves used in NI 43-101 differ from the definitions in the United States Securities and Exchange Commission (“SEC”) Industry Guide 7. In addition, the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7, and normally are not permitted to be used in reports and registration statements filed with the SEC. Accordingly, information contained in this AIF containing descriptions of the GK Diamond Mine’s mineral deposits may not be comparable to similar information made public by US companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder. United States investors are cautioned not to assume that all or any part of Measured or Indicated Mineral Resources will ever be converted into Mineral Reserves. United States investors are also cautioned not to assume that all or any part of an Inferred Mineral Resource exists or is economically or legally mineable.

Inferred resources are not considered to have sufficient geological confidence to be converted into any reserve classification regardless of economic merit.

| 11 |

Mining Method

Open Pit Mining

The Gahcho Kué Diamond Mine employs conventional open pit mining methods. Waste and ore are blasted and loaded out using a fleet of diesel powered trucks, shovels, drills and ancillary equipment. Waste rock will be stored in two surface mine rock piles as well as in two of the excavated pits at later stages of the mine life. Kimberlite ore is hauled to a run-of-mine storage pad where the ore is stockpiled and loaded into the primary crusher via a front end loader. Kimberlite processing creates two additional waste streams of coarse and fine processed kimberlite. Coarse processed kimberlite (“CPK”) is loaded into haul trucks and stacked in a pile North of the plant, while the fine processed kimberlite (“FPK”) is deposited via slurry into a settlement pond known as Area 2. Non-acid generating (“NAG”) and potentially-acid generating (“PAG”) waste rock is differentiated using an on-site sampling system of blast hole cuttings. PAG rock is encapsulated within the surface mine rock piles and below the restored final lake elevation of Kennady Lake during period of pit backfill.

The mine design and consequent mine plan considers conventional truck / shovel mining utilizing 29 m3 bucket diesel hydraulic front shovels, a 17 m3 front-end loader and 218 tonne class haulage trucks will be employed to mine the kimberlite and waste quantities. This large fleet will be augmented by 12 m3 bucket front-end loaders, scaling excavators and 100 tonne haul trucks. Production drill and blast activities will be supported by a fleet of rotary blast hole drills drilling 251mm holes. Pre-shear drilling will be supported with a pair of down the hole percussion drills drilling 171mm holes.

The three open pits are mined in a sequence which maximizes the value of the contained ore. The pre-strip sequence for the pits is 5034, Hearne and finally Tuzo, with production from all three pits overlapping at times. All three kimberlite deposits exist under Kennady Lake, and required substantial dewatering efforts prior to mining. Dewatering of the southern portion of Kennady Lake (Area 8, 7 and 6) was completed in 2015 along with construction of the primary dewatering infrastructure exposing the 5034 and Hearne deposits. Completion of the remaining dewatering dike network and substantial dewatering of Area 4 is planned for 2018 and 2019, which will expose the Tuzo mining area.

The Hearne pit will be used as a storage facility for processed kimberlite as well as waste mine rock upon depletion in 2022, and 5034 will be used as a waste rock storage facility for Tuzo mining operations from 2024 to the end of the mine life.

Recovery Methods

In the process plant, the ore is treated via crushing, screening, dense media separation and x-ray sorting, to produce a diamond rich concentrate that is sent to Yellowknife for final cleaning and Northwest Territories Government valuation. The processing plant targets the recovery of liberated diamonds in the 1 to 28 mm size range. The processing plant is designed for efficient diamond recovery over the mine’s twelve-year life.

Underground Mining

Underground mining is not currently part of the mine plan.

| 12 |

Capital and Operating Costs

Capital Cost Estimate

Table below is a summary of capital cost expenditures forecasted for the fiscal year 2018:

2018 Capital Cost Forecast Summary in Canadian dollars and on 100% basis

| Stay In Business Capital | (000’ C$) | C$/tonne of ore | C$/carat | |||||||||

| Mining | 41,067 | 13.18 | 6.06 | |||||||||

| Treatment | 4,517 | 1.45 | 0.67 | |||||||||

| Other Infrastructure | 9,045 | 2.90 | 1.33 | |||||||||

| SIB Total | 54,629 | 17.54 | 8.06 | |||||||||

| Capitalized Waste | 63,732 | 20.46 | 9.40 | |||||||||

| Total Capital Expenditure | 118,361 | 38.00 | 17.45 | |||||||||

Operating Cost Estimate

Operating cost estimate inputs were originally provided by De Beers and are based on a detailed Life of Mine Plan study combined with historical production from operating experience at the Gahcho Kué Diamond Mine in 2017, the Snap Lake Mine in the NWT and the Victor Mine in Northern Ontario.

The following table is a summary of the operating costs forecasted for the Gahcho Kué Diamond Mine in 2018. The figures of the table below are on 100% basis for the mine.

2018 Operating Cost Forecast Summary in Canadian dollars and on 100% basis

| Description | (000’ C$) | C$/tonne of ore | C$/carat | |||||||||

| Mining Costs | 77,648 | 24.93 | 11.45 | |||||||||

| Treatment Costs | 28,570 | 9.17 | 4.21 | |||||||||

| Support Services | ||||||||||||

| BU Management | 3,949 | 1.27 | 0.58 | |||||||||

| Aboriginal Affairs | 1,487 | 0.48 | 0.22 | |||||||||

| Eng. & Site Services | 55,712 | 17.89 | 8.21 | |||||||||

| Supply Chain | 28,077 | 9.01 | 4.14 | |||||||||

| Environmental Management | 7,833 | 2.51 | 1.15 | |||||||||

| Finance | 7,596 | 2.44 | 1.12 | |||||||||

| MRM | 3,720 | 1.19 | 0.55 | |||||||||

| Human Resources | 3,426 | 1.10 | 0.51 | |||||||||

| Protective Services | 3,274 | 1.05 | 0.48 | |||||||||

| Diamond Liaison and Selling | 4,012 | 1.29 | 0.59 | |||||||||

| Safety, Health & Risk | 2,717 | 0.87 | 0.40 | |||||||||

| Other Services | 1,037 | 0.33 | 0.15 | |||||||||

| Total Support Services | 122,842 | 39.44 | 18.11 | |||||||||

| Indirect Costs | ||||||||||||

| First Nation Compensation | 7,085 | 2.27 | 1.04 | |||||||||

| Retrenchment costs | - | - | - | |||||||||

| Total Indirect Costs | 7,085 | 2.27 | 1.04 | |||||||||

| Total Production Costs (net of capitalized stripping) | 236,145 | 75.82 | 34.82 | |||||||||

| 13 |

Other Relevant Data and Information

A full-time environmental staff is responsible for monitoring, directing and reporting environmental matters. The GK Diamond Mine has at all times since inception been in compliance with all permits and there are no outstanding liabilities or charges known at this time.

Ore produced from the mine is brought to the ore processing plant on site which has operated continuously since the beginning and kept pace with demands.

The processing plant uses no chemicals or reagents. Gravity-based methods rely on the relatively heavier weight of diamonds to separate them. The process involves crushing, screening, separation in dense media (ferro-silicon) and x-ray sorting. The recovered diamonds are separated and packaged by size, weighed, secured in a vault to await transport, packed into a special container and flown discreetly to the high-security sorting facility in the city of Yellowknife.

In Yellowknife, the diamonds are cleaned, sorted and split into the Company’s 49% share and De Beer’s 51% share. The cleaning and sorting facility’s quality management earned ISO 9001 certification.

The Company’s share of the diamonds is transported from Yellowknife to WDM in India where the rough diamonds are cleaned and sorted into saleable packages before being sent to Bonas in Antwerp where the diamonds are sold into international markets.

Social and Environmental Policies

Aboriginal Issues and Local Resources at the GK Diamond Mine

The Gahcho Kué Diamond Mine employs approximately 360 full time employees (excluding long term contractors), 45% of whom reside in the north. Approximately 20% of the total are Aboriginal.

Ni Hadi Xa (“NHX”), the Aboriginal led environmental monitoring agreement for the Gahcho Kué Mine, is in its third year of operations. The group is comprised of 5 Aboriginal parties (LKDFN, DKFN, NWTMN, NSMA, and TG) and De Beers. There are 4 employees including an on-site Environmental Monitor, a Technical Coordinator, a Traditional Knowledge Administrator, and a Traditional Knowledge Monitor. 75% of NHX employees are Aboriginal and 100% are Northern residents. In 2016, NHX constructed a Traditional Knowledge cabin on the northern end of Fletcher Lake, approximately 30 km north of the mine. The cabin serves as the base for the full-time Traditional Knowledge monitors to observe the effects of the mine on the environment. In 2017, NHX launched the Family Culture Program, which involves community members from each of the 5 Aboriginal parties travelling to the cabin during the ice-free season to practice traditional methods of watching over the land. All observations collected will be shared with De Beers in an effort to ensure traditional knowledge is incorporated into mine planning and operations.

Environmental Requirements for the GK Diamond Mine

The GK Diamond Mine is subject to environmental requirements and conditions of operation contained in several statutes and administered by Canadian federal and Northwest Territorial authorities. In addition to federal and territorial requirements, the GK Diamond Mine must also comply with the Environmental Agreements. These requirements and conditions may change from time to time, and a breach of legislation may result in the imposition of fines or other penalties. Environmental legislation continues to evolve in a manner such that standards, enforcement, fines and other penalties for non-compliance are becoming stricter. Environmental assessments of proposed projects carry a heightened degree of responsibility for companies, directors, officers and employees. The cost of compliance with changes in government regulations has the potential to reduce the profitability of future operations. To the best of the Company’s knowledge, the GK Diamond Mine is in compliance with environmental laws and regulations currently in effect in the Northwest Territories applicable to its operations.

| 14 |

Federal requirements are administered by Environment Canada, Fisheries and Oceans, the Department of Indian Affairs and Northern Development, Natural Resources Canada and Transport Canada. Environmental laws and regulations that have a potential impact on the GK Diamond Mine include those that protect air quality, water quality, archeological sites, migratory birds, animals and fish. Other important laws and regulations applicable to the GK Diamond Mine are those that regulate mine development, land use, water use and waste disposal, release of contaminants, water spills, spill responses, transportation of dangerous goods, explosives use and the maintenance of navigable channels. As a result of Devolution, responsibility for the administration and management of public lands, water, mineral and other natural resources in the Northwest Territories transferred from the Government of Canada to the Government of Northwest Territories (“GNWT”) effective as of April 1, 2014. The GNWT became responsible for the management of onshore lands, the issuance of rights and interests with respect to onshore minerals, and collection of royalties in the Northwest Territories. The Government of Canada will retain responsibility for the remediation of existing contaminated waste sites, the administration of offshore lands and the negotiation of Aboriginal Rights agreements.

Northwest Territories’ requirements are administered by the various territorial government departments and Workers’ Safety and Compensation Commission-Prevention Services as well as by co-management Boards charged with regulating land and water use in designated areas. Laws and regulations that might impact the GK Diamond Mine include those that protect heritage resources, wildlife and the environment and those that regulate workplace safety, mine safety, training in the handling of dangerous materials, road transportation, air quality, and the use of hazardous substances and pesticides. De Beers holds a number of permits and licenses to address each of these areas and regularly reports on compliance obligations to the respective government departments or regulator. The primary environmental permits were issued on August 11, 2014 (Land Use Permit) and September 24, 2014 (Water License), respectively by the Mackenzie Valley Land and Water Board allowing for the construction and operation of the Gahcho Kué Diamond Mine.

The Environmental Agreement relating to the GK Diamond Mine requires that security be provided to cover estimated reclamation and remediation costs. During 2014, the Company reached an agreement with De Beers, the Operator of the Joint Venture whereby the Company was required to post its proportionate share of the security deposit used to secure the reclamation obligations for the GK Diamond Mine. Currently, De Beers, on behalf of the Joint Venture has provided letters of credit in the amount of $47,794,132 (100%) to the GNWT as security for the reclamation obligations for the GK Diamond Mine. The Company pays De Beers a fee of 3% on its proportionate share of reclamation obligation.

Requirements in the Environmental Agreement are monitored by the Environmental Monitoring Advisory Board (“EMAB”), which was established as part of the agreement. EMAB includes board members from each of the signatories to the Environmental Agreement and operates at arm’s length and independent of the parties to the Environmental Agreement as a public watchdog of the regulatory process and implementation of the Environmental Agreement.

Risk Factors

The Company is subject to a number of risks and uncertainties as a result of its operations. Readers should give careful consideration to the following risks, each of which could have a material adverse effect on the Company’s business prospects or financial condition.

| 15 |

Nature of Mining

The Company’s mining operation is subject to risks inherent in the mining industry, including variations in grade and other geological differences, unexpected problems associated with required water retention dikes, water quality, surface and underground conditions, processing problems, equipment performance, accidents, labour disputes, risks relating to the physical security of the diamonds, force majeure risks and natural disasters.

The Company’s mineral properties, because of their remote northern location and access only by winter road or by air, are subject to special climate and transportation risks. These risks include the inability to operate or to operate efficiently during periods of extreme cold, the unavailability of materials and equipment, and increased transportation costs due to the late opening and/or early closure of the winter road. Such factors can add to the cost of mine development, production and operation and/or impair production and mining activities, thereby affecting the Company’s profitability.

Joint Ventures

The Company’s participation in the mining sector of the diamond industry is through its ownership interest in the GK Diamond Mine group of mineral claims. The GK Diamond Mine is a joint arrangement between De Beers (51%) and the Company (49%).

The Company’s joint venture interest in the GK Diamond Mine is subject to the risks normally associated with the conduct of joint ventures, including: (i) disagreement with a joint venture partner about how to develop, operate or finance operations; (ii) that a joint venture partner may not comply with the underlying agreements governing the joint ventures and may fail to meet its obligations thereunder to the Company or to third parties; (iii) that a joint venture partner may at any time have economic or business interests or goals that are, or become, inconsistent with the Company’s interests or goals; (iv) the possibility that a joint venture partner may become insolvent; and (v) the possibility of litigation with a joint venture partner.

Diamond Prices and Demand for Diamonds

The profitability of the Company is dependent upon the Company’s mineral properties and the worldwide demand for and price of diamonds. Diamond prices fluctuate and are affected by numerous factors beyond the control of the Company, including worldwide economic trends, worldwide levels of diamond discovery and production, and the level of demand for, and discretionary spending on, luxury goods such as diamonds. Low or negative growth in the worldwide economy, renewed or additional credit market disruptions, natural disasters or the occurrence of terrorist attacks or similar activities creating disruptions in economic growth could result in decreased demand for luxury goods such as diamonds, thereby negatively affecting the price of diamonds. Similarly, a substantial increase in the worldwide level of diamond production or the release of stocks held back during recent periods of lower demand could also negatively affect the price of diamonds. In each case, such developments could have a material adverse effect on the Company’s results of operations.

Cash Flow and Liquidity

The Company’s liquidity requirements fluctuate from quarter to quarter and year to year depending on, among other factors, the seasonality of production at the GK Diamond Mine, the seasonality of mine operating expenses, exploration expenses, capital expenditure programs, the number of rough diamond sales events conducted during the quarter, and the volume, size and quality distribution of rough diamonds delivered from the Company’s mineral properties and sold by the Company in each quarter.

| 16 |

The Company’s principal working capital needs include investments in inventory, prepaid expenses and other current assets, and accounts payable and income taxes payable and interest and loan repayments.

There can be no assurance that the Company will be able to meet each or all of its liquidity requirements. A failure by the Company to meet its liquidity requirements could result in the Company failing to meet its joint venture commitments, or in the Company being in default of a contractual obligation, each of which could have a material adverse effect on the Company’s business prospects or financial condition.

Event of Default

The Company’s secured notes payable and revolving credit facility are subject to various terms and conditions. If any of the terms and conditions are not met, it could result in an event of default which could affect the Company’s ability to continue as a going concern.

Credit Rating

The Company’s debt currently has a non-investment grade rating, and any rating assigned could be lowered or withdrawn entirely by a rating agency, if, in that rating agency’s judgment, future circumstances relating to the basis of the rating, such as adverse changes, so warrant. Any future lowering of the Company’s ratings likely would make it more difficult or more expensive for it to obtain additional debt financing.

Economic Environment

The Company’s financial results are tied to the global economic conditions and their impact on levels of consumer confidence and consumer spending. The global markets have experienced the impact of a significant United States and international economic downturn since autumn 2008. A return to a recession or a weak recovery, due to recent disruptions in financial markets in the United States, the Eurozone with Brexit or elsewhere, budget policy issues in the United States, political upheavals in the Middle East and Ukraine, economic sanctions against Russia, and demonetization/taxation changes in India could cause the Company to experience revenue declines due to deteriorated consumer confidence and spending, and a decrease in the availability of credit, which could have a material adverse effect on the Company’s business prospects or financial condition. The credit facilities essential to the diamond polishing industry are partially underwritten by European banks that are currently under stress. The withdrawal or reduction of such facilities could also have a material adverse effect on the Company’s business prospects or financial condition. The Company monitors economic developments in the markets in which it operates and uses this information in its continuous strategic and operational planning in an effort to adjust its business in response to changing economic conditions.

Synthetic Diamonds

Synthetic diamonds are diamonds that are produced by artificial processes (e.g., laboratory grown), as opposed to natural diamonds, which are created by geological processes. An increase in the acceptance of synthetic gem-quality diamonds could negatively affect the market prices for natural stones. Although significant questions remain as to the ability of producers to produce synthetic diamonds economically within a full range of sizes and natural diamond colours, and as to consumer acceptance of synthetic diamonds, synthetic diamonds are becoming a larger factor in the market. Should synthetic diamonds be offered in significant quantities or consumers begin to readily embrace synthetic diamonds on a large scale, demand and prices for natural diamonds may be negatively affected. Additionally, the presence of undisclosed synthetic diamonds in jewelry would erode consumer confidence in the natural product and negatively impact demand.

| 17 |

Currency Risk

Currency fluctuations may affect the Company’s financial performance. Diamonds are sold throughout the world based principally on the US dollar price, and the Company reports its financial results in Canadian dollars. A majority of the costs and expenses of the GK Diamond Mine are incurred in Canadian dollars. From time to time, the Company may use derivative financial instruments to manage its foreign currency exposure.

Licences and Permits

The Company’s mining operations require licences and permits from the Canadian and Northwest Territories governments, and the process for obtaining, amending and renewing such licences and permits often takes an extended period of time and is subject to numerous delays and uncertainties. Such licences and permits are subject to change in various circumstances. Failure to comply with applicable laws and regulations may result in injunctions, fines, criminal liability, suspensions or revocation of permits and licences, and other penalties. There can be no assurance that De Beers, as the operator of the GK Diamond Mine, will be at all times in compliance with all such laws and regulations and with their applicable licences and permits, or that De Beers will be able to obtain on a timely basis or maintain in the future all necessary licences and permits.

Regulatory and Environmental Risks

The operations of the GK Diamond Mine are subject to various laws and regulations governing the protection of the environment, exploration, development, production, taxes, labour standards, occupational health, waste disposal, mine safety and other matters. New laws and regulations, amendments to existing laws and regulations, or more stringent implementation or changes in enforcement policies under existing laws and regulations could have a material adverse effect on the Company by increasing costs and/or causing a reduction in levels of production from the GK Diamond Mine.

Mining is subject to potential risks and liabilities associated with pollution of the environment and the disposal of waste products occurring as a result of mining operations. To the extent that the GK Diamond Mine is subject to uninsured environmental liabilities, the payment of such liabilities could have a material adverse effect on the GK Diamond Mine.

Climate Change

The Canadian government has established a number of policy measures in response to concerns relating to climate change. While the impact of these measures cannot be quantified at this time, the likely effect will be to increase costs for fossil fuels, electricity and transportation; restrict industrial emission levels; impose added costs for emissions in excess of permitted levels; and increase costs for monitoring and reporting. Compliance with these initiatives could have a material adverse effect on the Company’s results of operations.

| 18 |

Resource and Reserve Estimates

The Company’s figures for mineral resources and ore reserves are estimates and no assurance can be given that the anticipated carats will be recovered. The estimation of reserves is a subjective process. Forecasts are based on engineering data, projected future rates of production and the timing of future expenditures, all of which are subject to numerous uncertainties and various interpretations. Estimates made at a given time may change significantly in the future when new information becomes available. The Company expects that its estimates of reserves will change to reflect updated information as well as to reflect depletion due to production. Reserve estimates may be revised upward or downward based on the results of current and future drilling, testing or production levels, and on changes in mine design. In addition, market fluctuations in the price of diamonds or increases in the costs to recover diamonds from the Company’s mineral properties may render the mining of ore reserves uneconomical. Any material changes in the quantity of mineral reserves or resources or the related grades may affect the economic viability of the Company’s mining operations and could have a material adverse effect on the Company’s business, financial condition, results of operations or prospects.

Mineral resources that are not mineral reserves do not have demonstrated economic viability. Due to the uncertainty that may attach to inferred mineral resources, there is no assurance that mineral resources will be upgraded to proven and probable ore reserves. Inferred mineral resources are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves.

Dependent on the GK Diamond Mine for future operating revenue

The Company’s only economic interest is its indirect 100% equity ownership interest in 2435386 Ontario Inc., which is a 49% participant in the Gahcho Kué Joint Venture, which owns and operates the GK Diamond Mine. As a result, the Company is solely dependent upon its interest in the GK Diamond Mine for its revenue and profits. In addition, production and operating costs are difficult to predict and may render further production at the GK Diamond Mine financially unfeasible. If commercial production and operation of the GK Diamond Mine becomes financially unfeasible, for engineering, technical, economic, political, legal or other reasons, the Company's business and financial position will be materially and adversely affected. In addition, the book value of the Company's interest in the GK Diamond Mine is subject to certain accounting assumptions. If such assumptions prove to be incorrect, then the book value of the Company's interest in the GK Diamond Mine could be impaired, which could have a material adverse effect on the Company.

No assurance that the Company will be able to extend the mine life beyond 2028

The Company is currently exploring options to potentially extend the mine life beyond 2028 through resource conversion and deep mining of the Tuzo kimberlite. Additional exploration and resource delineation is required to assess the viability of these prospects at Tuzo. A transition to underground mining generally increases per unit costs and can limit the annual volumes that can be economically extracted from such orebodies. There is no assurance that the Company will be able to extend the mine life beyond 2028 through resource conversion or deep mining.

Volatility of diamond prices

The Company’s profitability will be dependent upon its mineral properties and the worldwide demand for and price of diamonds. Diamond prices fluctuate and are affected by numerous factors beyond the Company’s control, including worldwide economic trends, worldwide levels of diamond discovery and production, and the level of demand for, and discretionary spending on, luxury goods such as diamonds. Low or negative growth in the worldwide economy, renewed or additional credit market disruptions, natural disasters or the occurrence of terrorist attacks or similar activities creating disruptions in economic growth could result in decreased demand for luxury goods such as diamonds, thereby negatively affecting the price of diamonds. Similarly, a substantial increase in the worldwide level of diamond production or the release of stocks held back during recent periods of lower demand could also negatively affect the price of diamonds. In each case, such developments could have a material adverse effect on the Company’s results of operations. In addition, prices for the higher value and lower value market segments can move independently of one another, depending on relative demand. For example, strengthening prices in one market segment can offset weakening prices in another, or synchronize with strengthening prices in another, which increases the unpredictability of diamond prices.

Insurance

The Company’s business is subject to a number of risks and hazards, including adverse environmental conditions, industrial accidents, labour disputes, unusual or unexpected geological conditions, risks relating to the physical security of diamonds held as inventory or in transit, changes in the regulatory environment, and natural phenomena such as inclement weather conditions. Such occurrences could result in damage to the GK Diamond Mine, personal injury or death, environmental damage to the GK Diamond Mine, delays in mining, monetary losses and possible legal liability. Although insurance is maintained to protect against certain risks in connection with the GK Diamond Mine, the insurance in place will not cover all potential risks. It may not be possible to maintain insurance to cover insurable risks at economically feasible premiums.

Fuel Costs

The expected fuel needs for the GK Diamond Mine are purchased in February and March each year and transported to the mine site by way of the winter road. These costs will increase if transportation by air freight is required due to a shortened “winter road season” or unexpected high fuel usage.

The cost of the fuel purchased is based on the then prevailing price and expensed into operating costs on a usage basis. The GK Diamond Mine currently has no hedges for future anticipated fuel consumption.

Reliance on Skilled Employees

Production at the GK Diamond Mine is dependent upon the efforts of certain skilled employees. The loss of these employees or the inability to attract and retain additional skilled employees may adversely affect the level of diamond production.

The Company’s success in marketing its 49% share of the rough diamonds is dependent on the services of key executives and skilled employees, as well as the continuance of key relationships with certain third parties, such as diamantaires. The loss of these persons or the Company’s inability to attract and retain additional skilled employees or to establish and maintain relationships with required third parties may adversely affect its business and future operations in marketing diamonds.

| 19 |

DIVIDENDS

The Company did not declare or pay dividends in fiscal 2017 or 2016. The Company has declared a corporate strategy of returning value to the shareholders by distributing available cash flow in a prudent manner in the form of dividends, with a goal of initiating a dividend policy during the 2018 fiscal year. The specifics of the policy are expected to be established over the course of the year as rough diamond price trends are confirmed, and in conjunction with determining the allocation of capital to the callable component of the Company’s senior notes. The future payment of dividends or distributions is not certain, however, and will be dependent upon the financial condition of the Company and other factors the Board of Directors of the Company may consider appropriate under the circumstances. The Mountain Province indenture governing Notes and the Revolving Credit Agreement, contain customary terms which restrict, subject to exceptions and qualifications, ability of the Company and its subsidiaries to make certain dividend payments, distributions, redemptions, repurchases, investments and other restricted payments.

DESCRIPTION OF CAPITAL STRUCTURE

The authorized capital of the Company consists of an unlimited number of common shares. Holders of common shares are entitled to receive notice of, attend and vote at all meetings of the shareholders of the Company. Each common share carries the right to one vote in person or by proxy at all meetings of the shareholders of the Company. The holders of common shares are entitled to receive dividends as and when declared by the Board of Directors of the Company. Subject to the rights, privileges, restrictions and conditions attaching to any other class of shares of the Company, the holders of the common shares are entitled to receive the Company’s proportionate remaining share of the assets of the GK Diamond Mine and any other assets the Company may hold in the event of liquidation, dissolution or winding-up of the Company.

Ratings

The following table sets out the ratings of the Company’s corporate debt by the rating agencies indicated as of March 26, 2018:

| Standard & Poor’s | Moody’s Investors Services |

Fitch Ratings | ||||

| Corporate rating | B- | B3 | B | |||

| First lien senior secured revolving credit facility | - | - | BB/RR1 | |||

| Senior secured second lien notes payable | B- | B3/LGD4 | BB-/RR2 | |||

| Recovery rating | 3 | - | - | |||

| Outlook | Stable | Stable | Stable |

Standard & Poor’s Ratings Services (“S&P”) credit ratings for long-term debt are on a rating scale ranging from AAA to D, which represents the range from highest to lowest quality. The ratings from AA to CCC may be modified by the addition of a plus (+) or minus (–) sign to show relative standing within the major rating categories. S&P’s rating is a forward-looking opinion about credit risk and assesses the credit quality of the individual debt issue and the relative likelihood that the issuer may default. If S&P anticipates that a credit rating may change in the next six to 24 months, it may issue an updated ratings outlook indicating whether the possible change is likely to be “positive”, “negative”, “stable” or “developing”. However, a rating outlook does not mean that a rating change is inevitable.

| 20 |

The B- rating is ranked seventh out of S&P’s eleven major rating categories. According to the S&P rating system, debt securities rated B- are more vulnerable to adverse business, financial and economic conditions but currently the Company has the capacity to meet financial commitments. In addition, S&P uses a scale of 1+ to 6 for recovery ratings, which focuses solely, from high to low, on expected recovery in the event of a payment default of a specific debt issue. A “3” recovery rating ranks fourth out of S&P’s seven recovery rating categories and indicates S&P’s expectation of meaningful (50% - 70%) recovery in the event of default.

Moody’s Investors Service (“Moody’s”) credit ratings are on a rating scale that ranges from Aaa to C, which represents the range from highest to lowest quality of such securities rated. According to Moody’s, a rating of B is the sixth highest of nine major categories. Obligations rated in the B category are considered speculative and are subject to high credit risk. Moody’s applies numerical modifiers 1, 2, and 3 to each generic rating classification from Aa through Caa in its long-term rating scale. The modifier 1 indicates that the obligation ranks in the higher end of its generic rating category; the modifier 2 indicates a mid-range ranking; and the modifier 3 indicates a ranking in the lower end of that generic category. Moody’s also issues a rating outlook opinion regarding the likely rating direction over the medium term. Rating outlooks fall into four categories: positive, negative, stable, and developing. A stable outlook indicates a low likelihood of a rating change over the medium term. A negative, positive or developing outlook indicates a higher likelihood of a rating change over the medium term. A designation of “Under Review” indicates that a rating is under consideration for a change in the near term. A rating can be placed on review for upgrade, downgrade, or more rarely with direction uncertain.

In addition, Moody’s Loss Given Default (“LGD”) assessments are opinions about expected loss given default expressed as a percent of principal and accrued interest at the resolution of the default based on a scale of 1 to 6. A LGD4 ranks fourth out of Moody’s six LGD assessment categories and indicates a ≥50% and <70% difference between value received at default resolution and principal outstanding and accrued interest due at resolution of the default.

Fitch Ratings (“Fitch”) credit ratings are on a rating scale that ranges from AAA to C, which represents the range from highest to lowest quality of such securities rated. According to Fitch, a rating of BB is the fifth highest of nine major categories. Obligations rated in the BB category are more vulnerable to adverse business, financial and economic conditions but currently the Company has the capacity to meet financial commitments. In addition, Fitch uses a scale of RR1 to RR6 for recovery ratings, which focuses solely, from high to low, on expected recovery in the event of a payment default of a specific debt issue. A “RR1” recovery rating ranks first out of Fitch’s six recovery rating categories and indicates Fitch’s expectation of meaningful (91% - 100%) recovery in the event of default and a “RR2” recovery rating ranks second out of Fitch’s six recovery categories and indicates Fitch’s expectation of meaningful (71% - 90%) recovery in the event of default.

The Company understands that the rating agencies ratings are based on, among other things, information furnished to the above ratings agencies by the Company and information obtained by the ratings agencies from publicly available sources. The credit ratings are not recommendations to buy, sell or hold securities since such ratings do not comment as to market price or suitability for a particular investor. Credit ratings are intended to provide investors with an independent measure of the credit quality of an individual debt issue; an indication of the likelihood of repayment for an issue of securities; and an indication of the capacity and willingness of the issuer to meet its financial obligations in accordance with the terms of those securities. Credit ratings are not intended as guarantees of credit quality or exact measures of the probability of default. Credit ratings assigned to the Company’s corporate debt may not reflect the potential impact of all risks on the value of debt instruments, including risks related to market or other factors discussed in this Annual Information Form. See also “Risk Factors”.

| 21 |

MARKET FOR SECURITIES

The Company’s common shares have been listed for trading on the TSX (symbol MPVD) since October 25, 2000. The Company is a reporting issuer, or equivalent, in each of the provinces and territories of Canada. The Company’s common shares are also listed for trading on NASDAQ under the symbol MPVD.

Trading Price and Volume

The following table outlines the 52-week trading history, as well as monthly trading history during the period from January 2017 to December 2017 for Mountain Province Diamonds Inc. shares on the TSX for the Company’s fiscal year ended December 31, 2017:

| 52 – Week High: | CDN$6.89 |

| 52 – Week Low | CDN$3.41 |

| Average Daily Volume | 140,530 |

| Month | High (CDN$) | Low (CDN$) | Average Daily Volume | |||||||||

| January (2017) | 6.94 | 5.27 | 152,247 | |||||||||

| February | 6.40 | 5.15 | 369,675 | |||||||||

| March | 5.55 | 4.07 | 308,942 | |||||||||

| April | 4.84 | 3.89 | 200,716 | |||||||||

| May | 4.12 | 3.56 | 122,736 | |||||||||

| June | 4.39 | 3.63 | 58,530 | |||||||||

| July | 5.10 | 3.75 | 86,948 | |||||||||

| August | 4.99 | 4.07 | 68,213 | |||||||||

| September | 4.27 | 3.95 | 65,616 | |||||||||

| October | 4.10 | 3.53 | 44,559 | |||||||||

| November | 3.84 | 3.35 | 105,696 | |||||||||

| December (2017) | 3.55 | 3.28 | 115,338 | |||||||||

Prior Sales

| Date of Issuance | Number of Securities Issued | Type of Security | Price per Security ($) | Reason for Issuance | ||||||||

| June 30, 2017 | 10,000 | Mountain Province Shares | 3.91 | RSUs vested and issued | ||||||||

| July 19, 2017 | 50,000 | Mountain Province Shares | 4.77 | RSUs vested and issued | ||||||||

| August 15, 2017 | 3,000 | Mountain Province Shares | 4.96 | RSUs vested and issued | ||||||||

| August 31, 2017 | 8,333 | Mountain Province Shares | 4.46 | RSUs vested and issued | ||||||||

| December 21, 2017 | 8,335 | Mountain Province Shares | 3.48 | RSUs vested and issued | ||||||||