Development activities mainly concerned: (i) the Berkine North area (Eni’s interest 49%) with the drilling and hook-up of an additional gas production well and three additional oil production wells as well as workover activities; (ii) production optimization at the Zea field in the Block 403 a/d and the BRN/BRW field in the Block 403 as well as the Block 405b and the Block 404; and (iii) maintenance activity at the Block 208.

In March 2022 exploration activity yielded positive results with the HDLE oil and associated gas discovery in the Zemlet el Arbi concession (Eni’s interest 49%), in the Berkine North area.

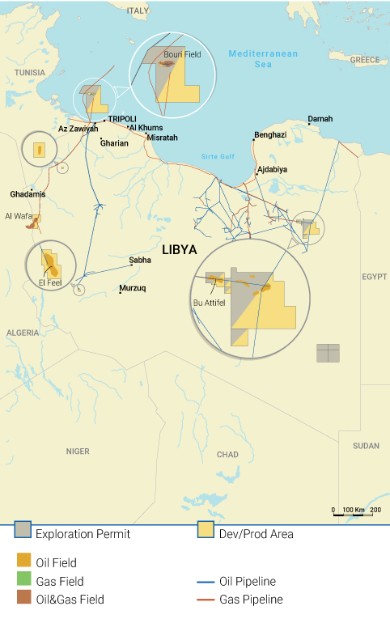

Libya. Currently, Libya represents approximately 10% of the Group’s total production. The social and political instability of the Country dates back to the revolution of 2011 that brought a change of regime and a civil war, triggering an uninterrupted period of lack of well-established institutions and recurrent events of internal conflict, clashes, disorders and other forms of civil turmoil and unrest between the two conflicting factions. In the year of the revolution, Eni’s operations in Libya were materially affected by a full-scale war, which forced the Company to shut down its development and extractive activities for almost all of 2011, with a significant negative impact on the Group’s results of operation and cash flow. In subsequent years Eni has experienced frequent disruptions to its operations, albeit on a smaller scale than in 2011, due to security threats to its installations and personnel. The situation begun to improve in September 2020, thanks to a peace agreement between the conflicting factions which enabled full resumption of operations at all Libyan oilfields, revoking force majeure declared at the start of 2020. Currently, notwithstanding temporary shutdowns, producing activities in Libya are proceeding in a stable manner, even though the institutional framework remains uncertain. Going forward, management believes that Libya’s geopolitical situation will continue to represent a source of risk and uncertainty to Eni’s operations in the Country and to the Group results of operations and cash flow. For further information on this matter, see “Item 3 – Risk factors – Political considerations”.

The rights of Eni to produce at its assets in Libya will expire in 2038 for Contract Area C, in 2042 for Contract Area E, in 2043 for Contract Area A, B and D production.

Tunisia. Development activities concerned the drilling and start-up of an additional production well in the MLD concession.

66