Exhibit 10.1

CERTAIN INFORMATION IDENTIFIED WITH [***] HAS BEEN EXCLUDED FROM THIS EXHIBIT BECAUSE IT IS BOTH (i) NOT MATERIAL AND (ii) WOULD BE COMPETITIVELY HARMFUL IF PUBLICLY DISCLOSED.

CEPI

Outbreak Response Funding Agreement (Step 2)

Agreement Summary

AWARDEE INFORMATION | |

Name: | Novavax, Inc. (“Awardee”) |

Mailing Address: | 21 Firstfield Road, Gaithersburg, MD 20878 |

Project Lead: | [***], Director, Global Program Management |

Management Contact: | [***], SVP, Commercial Strategy |

Bank Account Details: | [***] |

CEPI INFORMATION | |

Mailing Address: | Coalition for Epidemic Preparedness Innovations, PO Box 123 Torshov, N-0412 Oslo, Norway |

Project Lead: | [***], Vaccine Development Project Leader |

Management Contact: | [***], Director of Vaccine Research & Development |

AGREEMENT INFORMATION | |

Project Name | Novavax Outbreak Response To Novel Coronavirus (COVID-19) |

CEPI Programme Name | Outbreak Response To Novel Coronavirus (COVID-19) |

Effective Date | Date of last signature below |

Expiry Date | As described in Clause 19.1 of the Terms and Conditions in Annex A. |

This Agreement includes and incorporates by reference: | The agreement (referred to as the “Agreement”) means this Agreement Summary together with the following: - Terms and Conditions (Annex A) - Team Charter (Annex B) - iPDP for Work Package(s) amended and restated (Annex C) - Budget for Work Package(s) amended and restated (Annex D) |

THIS AGREEMENT is between Awardee and the Coalition for Epidemic Preparedness Innovations (“CEPI”) and is effective as of the date of the last signature, below (the “Effective Date”). Each party to this Agreement may be referred to individually as a “Party” and together as the “Parties.” This Agreement sets out the terms and conditions governing the performance of the Project, funding of the Project and how the results of the Project shall be used to further CEPI’s mission. As a condition of this funding award, the Parties enter into this Agreement by having their authorized representatives sign below.

Signed for and on behalf of:

COALITION FOR EPIDEMIC PREPAREDNESS INNOVATIONS

Signature: | /s/ Richard Hatchett | |

| | |

Name: | Richard Hatchett | |

| | |

Title: | Chief Executive Officer | |

| | |

Date: | 2020-05-11 | |

| | |

NOVAVAX, INC. | | |

| | |

Signature: | /s/ John A. Herrmann III | |

| | |

Name: | John A. Herrmann III | |

| | |

Title: | SVP, General Counsel & Corporate Secretary | |

| | |

Date: | 2020-05-11 | |

-2-

Annex A: Terms and Conditions

{The Terms and Conditions follow this cover page.}

-3-

ANNEX A: Outbreak Response Award Terms and Conditions

1. | Definitions: |

1.1.“Affiliate” means any business entity controlled by, controlling or under common control with, a Party.

1.2.“Agreement Summary” means the signature page that identifies the Parties and to which this Annex A is attached.

1.3.“Awardee Background IP” has the meaning described in Clause 5.1.

1.4.“Background IP” has the meaning described in Clause 5.1.

1.5.“Budget” means the schedule of funds to be paid by CEPI for the Project activities in the Work Packages identified in Annex D, as may be amended from time to time.

1.6.“Commercial Benefits” has the meaning described in Clause 15.1.

1.7.“Cost of Goods” (or “COGs”) means [***] in conformity with relevant U.S. GAAP or IFRS accounting principles.

1.8.“Enabling Rights” means rights to Intellectual Property and Project Results that could be asserted by Awardee to block CEPI from exercising its rights under Clause 13 of this Agreement. For purposes of this Agreement, Enabling Rights also includes the contractual rights under contracts executed for the Project that control the use of such items, for example, in material transfer agreements.

1.9.“Equitable Access Plan” has the meaning described in Clause 14.11.

1.10.“Field” means the public health vaccine response to the Outbreak and to other coronaviruses against which a Project Vaccine may be at least partially cross-protective.

1.11.“Financial Report” has the meaning described in Clause 3.7.

1.12.“Integrated Product Development Plan” (or “iPDP”) means one or more Work Packages that collectively include the various activities, deliverables, milestones, phases, risks and timelines associated with the Project. The initial iPDP is set forth as Annex C.

1.13.“Intellectual Property” (or “IP”) means the intangible property rights claiming or covering the discoveries, inventions and materials as well as the works of authorship made by Awardee under the Project, such as copyrights, patents and trademarks.

1.14.“Joint Monitoring and Advisory Group” or “JMAG” has the meaning described in Clause 2.3.

1.15.“LMICs” means “Low and Middle Income Countries” as defined by the Organisation for Economic Co-operation and Development as may be updated from time-to-time.

-4-

1.16.“Outbreak” means the COVID-19 outbreak caused by the SARS-CoV-2 virus or any strain, mutations and related recurrences of such virus.

1.17.“Project” means Awardee’s activities under this Agreement, as are described in the Team Charter, Work Package(s) and Budget.

1.18.“Project Continuity Plan” has the meaning described in Clause 13 “Project Data” has the meaning described in Clause 9.1.

1.19.“Project Expansion” means the inclusion of additional Project activities to be undertaken by Awardee through an additional Work Package(s) as may be related to expanding activities or accelerating the timeline for research and development, clinical trials, manufacturing, production of product stockpiles, and the like.

1.20.“Project Materials” has the meaning described in Clause 9.2.

1.21.“Project Results” means all of the tangible results that are made or developed by Awardee under the Project, including the Project Vaccine, and directly related to such Product Vaccine, assays necessary for Project Vaccine production, whether in whole or in components, protocols used in Project Vaccine clinical or non-clinical evaluation, Project Data, and Project Materials.

1.22.“Project Vaccine” means Awardee’s lead vaccine candidate against SARS-CoV-2, as described in the iPDP in any form or dosage of pharmaceutical composition or preparation.

1.23.“Public Health License” means a grant by Awardee to CEPI of all relevant rights under Project Results, Enabling Rights and Background IP for use in the Field by CEPI as described in Clause 13.

1.24.“Ready Reserve of Clinical Trial Material” has the meaning described in Clause 12.1.

1.25.“Stage Gate” means a mutually agreed “go/no go” decision point to continue a given Work Package or to commence activities in another Work Package.

1.26.“Step 1 Agreement” means the agreement between the Parties covering the [***] of the Project effective March 8, 2020.

1.27.“Subawardees” has the meaning described in Clause 2.6.

1.28.“Sub-Grant Awardees” has the meaning described in Clause 2.6.

1.29.“Team Charter” has the meaning described in Clause 2.1.

1.30.“Technical Report(s)” has the meaning described in Clause 2.4.

1.31.“Third Party Background IP” has the meaning described in Clause 5.1.

1.32.“Third Party Code” has the meaning described in Clause 11.2.

-5-

1.33.“Trusted Collaborator” has the meaning described in Clause 13.2.

1.34.“Trusted Manufacturer” has the meaning described in Clause 13.2.

1.35.“Work Package(s)” means a discrete set of activities in an iPDP as identified in Annex C. Additional Work Package(s) may be agreed to by the Parties after the Effective Date, which, upon execution by both Parties, shall be annexed to and become a part of this Agreement.

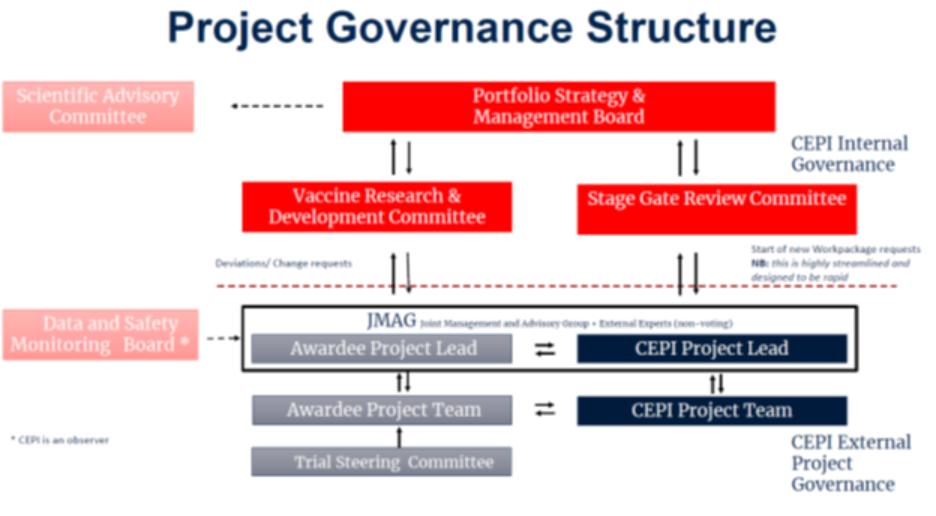

2. | Project Management and Organization: |

2.1.Team Charter. The Project shall be managed by the Parties as described in the Team Charter in Annex B.

2.2.iPDP and Work Packages. The Project shall be described in an iPDP in Annex C and organized into one or more Work Packages, having an associated Budget attached in Annex D. The Parties may agree to multiple Work Packages as of the Effective Date, some of which shall be pursued in parallel, others of which shall commence upon the occurrence of Stage Gates and others being optional and exercisable in CEPI’s discretion. A Work Package may include one or more Stage Gates. Additional Work Packages may be added as additional annexes to this Agreement as agreed in writing by the Parties pursuant to Section 21.6. Work Packages may also be modified or extended with mutual written consent pursuant to Section 21.6.

2.3.Joint Monitoring and Advisory Group. The Team Charter establishes a joint monitoring and advisement group (“JMAG”) that shall meet and interact regularly on a [***] basis to advance the Project. The JMAG shall undertake to provide coordinated efforts by CEPI and Awardee to: (i) facilitate communications between the Parties; (ii) review the progress of the Project; (iii) discuss substantial proposed changes in the scope or conduct of applicable clinical and animal studies; (iv) discuss clinical trial protocols, publications and regulatory submissions; (v) coordinate the sharing of any Project Results identified in a Work Package as intended for use by other CEPI awardees; (vi) review and update the Project Continuity Plan; (vii) review and update the Equitable Access Plan; and (viii) discuss plans, as appropriate, for the development of manufacturing and its scale-up and scale-out.

2.4.Technical Reports and Access to Project Results. Awardee shall disclose Project Results informally to CEPI’s Project Lead, at meetings of the JMAG and through regular written reports of progress made under the iPDP using a template provided by CEPI (“Technical Reports”), within [***] of a Project’s [***]. Awardee also shall make Project Results available to CEPI as described in the iPDP or otherwise as may reasonably be requested.

2.5.Stage Gates. When Awardee believes that a Stage Gate in a Work Package will be achieved, Awardee shall notify the JMAG, [***] provide relevant information and request a meeting of CEPI’s committee authorized to assess completion of Stage Gates (“Stage Gate Review Committee”). Awardee’s Project Manager shall coordinate with CEPI’s Project Manager to schedule the Stage Gate Review Committee meeting to be held no more than [***] after the request. CEPI shall notify Awardee of the Stage Gate Review Committee’s decision no more than [***] after its meeting. If the Stage Gate Review Committee agrees that a Stage Gate has been successfully achieved, the JMAG shall [***] authorize Awardee to continue previously agreed Work Package activities. When a Stage Gate has not been achieved to the reasonable

-6-

satisfaction of the Stage Gate Review Committee, the JMAG shall [***] discuss in good faith how to address this and whether amendments to the relevant Work Package would address the issue or increase the probability of a successful outcome to the Project.

2.6.Affiliates and Subawardees. Awardee’s activities may be undertaken by Affiliates and contracted third parties (collectively, “Subawardees”) that are identified in a Work Package or reasonably approved by JMAG. Awardee shall be responsible for the acts and omissions of all of its Subawardees. Awardee shall ensure that: (i) Subawardees engaged as procurements pursuant to Clause 14 of the Third Party Code agree to the terms of the Third Party Code applicable to their activities; and (ii) Subawardees engaged as sub-grant awardees pursuant to Clause 15 of the Third Party Code (“Sub-Grant Awardees”) agree to be subject to the Third Party Code and to all of the obligations applicable to Awardee under this Agreement, including obligations for the auditing, inspections, record keeping, use of funds and all other compliance obligations as are applicable to Awardee under this Agreement.

2.7.Services Provided by Other CEPI Funding Recipients. Awardee acknowledges that a particular Work Package may require a further contract to be negotiated directly between Awardee and another recipient of CEPI funding, through which certain Services are provided directly to Awardee.

2.8.[***] Awardee shall use [***] to achieve the objectives and timelines of each Work Package and to meet each Stage Gate in a Work Package within the agreed timeframe, it being understood that neither Party can assure a positive technical outcome for any Work Package.

3. | Use of Funds; Procurement; Project Records: |

3.1.Use and Management of Funds. The Budget sets for the funding for each Work Package. Awardee shall use funding from CEPI only in accordance with a Work Package unless otherwise agreed by CEPI in advance. Awardee shall manage CEPI funds with financial controls and practices consistent with U.S. GAAP and further in compliance with CEPI’s policies and procedures as described in Clause 11.2 of this Agreement, which include CEPI’s Third Party Code, Cost Guidance and related procurement policies.

3.2.Procurement. All procurement by Awardee and Sub-Grant Awardees shall be conducted under the best practice regime for procurement activities within the territory where that procurement is taking place and also in compliance with Clause 11.2 of this Agreement.

3.3.Payments. Payments under this Agreement shall be made in U.S. dollars ($) to Awardee’s bank account identified on the Agreement Summary. CEPI shall make payments [***] identified in the Budget and shall make adjustments to the initial payment hereunder to accommodate any funds carried forward from the Step 1 Agreement. Awardee shall be entitled to submit a payment request form to CEPI upon execution of this Agreement and thereafter [***]. Tranches of funding for each payment request under this Agreement shall be paid by CEPI [***] after receipt of all of the following: (i) payment request by Awardee; (ii) any [***] Technical Report due at the time of the payment request; and (iii) any [***] Financial Report due at the time of the payment request, each to be submitted using templates provided by CEPI. Payments may be adjusted to reflect any [***] as well as any [***] as noted in the Financial Report.

-7-

3.4.Delayed Payments. CEPI may delay or condition a payment if:

(a)Awardee has not achieved a material milestone in accordance with the iPDP by the agreed time, unless such delay has been approved by the JMAG in accordance with the Team Charter or otherwise by CEPI;

(b)CEPI has been notified by Awardee that it or any Subawardees are no longer in compliance with the representations and warranties in Clause 16 at the time the payment tranche is requested; or

(c)Awardee has not reasonably completed the payment request form or submitted reasonably satisfactory [***] Technical Reports and Financial Reports.

3.5.Hold on Payment During a Material Breach. CEPI is not obliged to pay any tranches of funding for any Work Package for so long as Awardee is in breach of a material obligation under this Agreement.

3.6.Retained Final Payment. CEPI shall retain [***] identified in the Budget and release it within [***] days after accepting Awardee’s final Technical Report and Financial Report. Within [***] of CEPI’s receipt of the both the Technical Report and Financial Report, CEPI shall notify Awardee of CEPI’s acceptance or rejection of such report(s).

3.7.Financial Reports. Awardee shall provide reports of its expenditures under the Budget with supporting documentation and using a template provided by CEPI (“Financial Reports”) within [***] of a Project’s [***], such other date(s) as may be identified in the Budget. Awardee shall submit a final Financial Report within [***] after the completion of any Work Package.

3.8.Project Records. Awardee shall keep accurate records of its Project activities and expenditures under each Work Package and retain them for [***] after termination of this Agreement.

3.9.Access to Financial Records. During the term and for a period of [***] after expiration or termination of this Agreement, CEPI, or its designee (which shall be a internationally recognized certified public accounting firm, not engaged on a contingent basis), and at CEPI’s reasonable cost, shall have on-site access to inspect Awardee’s Project-related financial records once annually upon at least [***] advance notice. Such inspections shall be conducted during normal operating hours in a manner to minimize disruption to Awardee’s business. For clarity, access to such records also shall be provided to records related to Cost of Goods as described in Clause 14.

3.10.Project Financial Audits. During the term and for a period of [***] after expiration or termination of this Agreement, if requested by CEPI, and at CEPI’s reasonable cost, [***] notice, Awardee’s external auditors shall conduct a Project audit in accordance with ISA800 and/or ISA805 and like standards and provide CEPI with audited statements. Such requests shall not occur more frequently than [***] and will be conducted during normal operating hours in a manner to minimize disruption to Awardee’s business.

-8-

4. | Changing Project Scope, Timelines or Funding as Outbreak Develops: |

4.1.Changing Project Scope. The Parties acknowledge the possibility that, as the Outbreak develops in ways not foreseen in the initial Work Package(s), a Project Expansion may become essential. For example, the extent or severity of the Outbreak may increase, the Project Vaccine may be prioritized by public health authorities for clinical studies and/or manufacture or advances in vaccine technology may permit acceleration of the Project. Alternatively, it may become necessary for CEPI to limit Project scope or defer certain activities. For example, the WHO may determine that the Outbreak is no longer a Public Health Emergency of International Concern (“PHEIC”), third party products may be prioritized for development or deployment by an international decision-making process, CEPI may need to focus its resources on other product in its portfolio, or the Project Vaccine may not appear to meet Outbreak response needs.

4.2.Implementing Changes in Project Scope or Timing. At the request of either Party, and as a matter of urgency, the Parties shall discuss in good faith: (i) whether a Project Expansion may be undertaken at CEPI’s cost through modification of an existing Work Package, approval of an additional Work Package or utilization of the Project Continuity Plan in Clause 13; or (ii) how best to limit Project scope or defer certain activities in a Work Package. For clarity, during the Outbreak, CEPI reserves the right to terminate a Work Package if this is necessary in its sole discretion, provided CEPI pays Awardee all costs incurred or obligated to date and including any non-cancellable costs under such Work Package, and also provided that, if requested by CEPI, Awardee shall reasonably demonstrate the incurred, obligated or non-cancellable nature of such costs.

4.3.Participation By Other Funders. Other funders may offer to fund certain parts of a Work Package or a Project Expansion. Additional funding mechanisms may become available to either Party. The Parties shall, in good faith, facilitate such participation and appropriate revisions to relevant Work Packages and the Budget, as well as managing any potentially conflicting commitments.

5. | Ownership of Project Results; Intellectual Property: |

5.1.Background IP. Awardee shall retain ownership of its intellectual property existing as of the Effective Date, or developed or acquired independently of the Project during the term of this Agreement (“Awardee Background IP”) and licenses to third party intellectual property secured prior to the Effective Date [***] (“Third Party Background IP” which, along with Awardee Background IP, shall be referred to as “Background IP”), and nothing in this Agreement shall be deemed to assign any ownership in, or grant a license to, CEPI with respect to such Background IP; except for the limited license rights otherwise expressly provided herein for the Public Health License.

5.2.Ownership of Project Results. Awardee shall own the rights to Project Results.

5.3.Ownership of Intellectual Property. Awardee shall own all Intellectual Property. Upon request [***] Awardee shall update CEPI regarding the status of Intellectual Property rights sought and obtained. Awardee shall have the right, but not the obligation, to seek IP protection at its own cost.

-9-

5.4.Third Party IP. The Parties shall notify each other [***] regarding any third party IP they become aware of that might impact Awardee’s ability to perform its obligations under this Agreement and activities contemplated under the Project Continuity Plan and Equitable Access Plan. The Parties shall cooperate in good faith to resolve any such matters.

6. | Clinical Studies: |

6.1.Clinical Trials. If any Work Package includes research involving human subjects, such activities must comply with applicable laws and regulations, including requirements related to use of clinical data outside of the country in which a given clinical trial is conducted. Clinical trials also shall comply with CEPI’s policies and procedures in Clause 11.2, which include CEPI’s Clinical Trials Policy.

6.2.Clinical Trial Protocols. Awardee shall be responsible for clinical trial protocol development and shall consult reasonably in advance with CEPI and/or CEPI’s designee regarding clinical trial protocols before they are finalized or submitted to institutional review boards, ethics committees or regulatory authorities.

6.3.Clinical Data. The data arising in the conduct of a clinical trial shall be collected in a way that ensures that each subject, prior to enrolment and in accordance with all applicable laws and regulations, including all applicable data protection and privacy requirements, provides informed consent to allow:

(a)direct access to her or his medical records;

(b)the processing of data relating to her or him and to the movement of that data to other countries, including countries outside of the European Economic Area;

(c)the transfer of such data to Awardee;

(d)the transfer of anonymised data to CEPI and/or CEPI’s designee;

(e)the collection and use of clinical trial data (duly anonymised and, at CEPI’s request, blinded) for the purposes of this Agreement;

(f)the collection and use of biological samples and the use of data (duly anonymised and, at CEPI’s request, blinded) derived from such samples by CEPI or its designated Assessors for the purposes of this Agreement; and

(g)the use of such data for the purpose of obtaining approval from applicable regulatory agencies.

6.4.Sponsorship and Management of Clinical Trials. Awardee shall be the sponsor of any clinical trial (unless CEPI and Awardee otherwise agree in writing), and shall be responsible for obtaining and maintaining all regulatory approvals (including ethical committee approvals) necessary or reasonably useful for the conduct of the clinical trial. In addition, Awardee shall establish an internal Trial Steering Committee (TSC) and a Safety Monitoring Committee or Data Safety Monitoring Board, as applicable (either, a DSMB). Awardee shall, consistent with

-10-

DSMB charter documents, permit a CEPI representative or designee to: (i) attend meetings of DSMB for the clinical trial as an observer (either in person or by electronic means); and (ii) receive all papers that a member of the DSMB would be entitled to receive. The foregoing obligation shall not apply to the extent CEPI’s attendance at a meeting or receipt of papers would jeopardize the integrity/blinded nature of an ongoing clinical trial; during an ongoing clinical trial, Awardee will provide CEPI open session DSMB documents, DSMB recommendation forms and other “open” documents and after a clinical trial is unblinded, CEPI may receive papers that a member of DSMB would be entitled to receive.

6.5.Safety Notifications. Awardee shall notify the JMAG in writing [***] following any single safety event of concern or a series of safety events considered by the DSMB as relevant in relation to the Project Vaccine and at least within [***] after such event or series of events becomes known to Awardee.

6.6.Registration of Clinical Trials: Awardee shall publish details of any clinical trial in a publicly accessible clinical trial register, where patient privacy is upheld, as required under law and, as applicable, prior to the commencement of patient recruitment for such clinical trial.

6.7.Priority for Clinical Trials. Awardee acknowledges that the pool of subjects available in areas of Outbreak to participate in a clinical trial to test products may be limited. Accordingly, if WHO, CEPI or a regulatory authority in the area where the clinical trial is to be conducted determines that a product other than a Project Vaccine has substantially greater potential and should be prioritized instead for a particular clinical trial, Awardee shall abide by such determination and shall not proceed with a clinical trial of such Project Vaccine unless required to do so by a relevant regulatory authority and Awardee shall be reimbursed for its costs, including non-cancellable costs, incurred resulting from such determination to not proceed.

6.8.Potential WHO Clinical Trials. Awardee shall not unreasonably decline a request to participate in a Phase IIb or III clinical trial as requested by WHO and/or CEPI to compare the Project Vaccine with other COVID-19 vaccine candidates, under a Project Expansion.

7. | Regulatory Activities: |

7.1.Regulatory Activities. Awardee shall pursue the regulatory activities described in the iPDP and associated Work Package(s).

7.2.Meetings with Regulatory Authorities. Awardee shall invite a CEPI or its designee to observe all material interactions between Awardee and regulatory authorities relating to a Project Vaccine. At CEPI’s reasonable request, Awardee shall request a meeting with regulatory authorities to deal with any significant unresolved issues.

7.3.Regulatory Filings. Awardee shall consult regularly with CEPI regarding regulatory strategy for a Project Vaccine and shall provide advance copies of all regulatory submissions for review and comment by CEPI no later than [***] prior to their contemplated submission to a regulatory authority. If a final version is not available by [***] prior to submission, then a mature draft version can be submitted to CEPI for review at that time. Additionally, Awardee shall put copies of the following on a confidential electronic archiving service designated CEPI:

-11-

(a)all submissions to regulatory authorities and regulatory filings in respect of a Project Vaccine together with all data included or referenced therein (other than ministerial submissions that do not involve safety or efficacy issues); and

(b)material documents and information exchanged between any regulatory authority and the Awardee relating to a Project Vaccine.

7.4.Product Development Standards. To the extent applicable to the Project, Awardee shall comply with Good Laboratory Practices, Good Clinical Practices, and Good Manufacturing Practices.

7.5.Other Access and Cross References. Awardee shall provide access to other regulatory files and records in good faith and as appropriate to achieve the objectives of this Agreement. For clarity, this may include permission to cross reference master files related to the platform on which the Project Vaccine is produced.

8. | Animal Studies: |

8.1.Animal Studies. If any Work Package includes research involving animals, such activities must comply with applicable laws and regulations, and with CEPI’s policies and procedures in Clause 11.2, which include CEPI’s Use of Animals Policy.

8.2.Approvals. Awardee shall obtain and maintain all regulatory approvals (including ethical committee approvals) necessary or reasonably useful for the conduct of research involving animals.

9. | Dissemination of Project Results; Publication: |

9.1.Dissemination of Project Data. Awardee shall disseminate pre-clinical and clinical trial data (including any negative results, animal model deaths and any toxicology study issues) produced under the Project (collectively, “Project Data”), as described in the iPDP and this Agreement or as otherwise agreed by the JMAG.

9.2.Dissemination of Project Materials. Awardee shall disseminate biological samples, Project Vaccines, and other tangible materials produced under the Project (collectively, “Project Materials”) as described in the iPDP and this Agreement or as otherwise agreed by the JMAG. If Awardee develops animal models under the Project, they shall also be considered Project Materials and disseminated as described in the iPDP and this Agreement or as otherwise agreed by the JMAG.

9.3.Dissemination of Project Results to the Broader Outbreak Community. As described in the iPDP and elsewhere in this Agreement, or as otherwise agreed by the JMAG, and subject to the payment by CEPI of actual costs and reasonable protection for Awardee’s rights under this Agreement, Awardee shall disseminate Project Results (excluding any chemistry, manufacturing and controls (“CMC”) data, or any information that would violate relevant privacy laws, or any information that Awardee can reasonably demonstrate to CEPI is sensitive and should not be so disseminated) with the broader Outbreak research community, such as disease-specific assays

-12-

and standards, animal models, correlates of protection or risk, or diagnostics and epidemic preparedness mechanisms.

9.4.Dissemination of Project Data to Countries Hosting Clinical Studies. Subject to reasonable protection for Awardee’s rights under this Agreement, Awardee shall, to the extent it has the legal right to do so, make all Project Data (excluding any chemistry, manufacturing and controls (CMC) data), such as results of disease-specific assays, animal models, correlates of protection or risk, or diagnostics and epidemic preparedness mechanisms arising from such clinical trial available to that country’s Ministry of Health or equivalent.

9.5.Publication of Project Data for the Outbreak Research Community. Project Data shall be shared rapidly with the broader community, consistent with Awardee’s requirements as a public company, in accordance with (i) WHO’s 2016 Guidance for Managing Ethical Issues in Infectious Disease Outbreaks; (ii) WHO’s 2016 Guidance on Good Participatory Practices in Trials of Interventions Against Emerging Pathogens; (iii) and Wellcome Trust’s Statement on Sharing Research Data and Findings Relevant to the Coronavirus (COVID-19) Outbreak to which CEPI is a signatory.

9.6.Clinical Trial Data. CEPI’s Clinical Trials Policy requires that clinical data and results (including negative results) must be disclosed publicly in as close to real time as possible. Accordingly, such data must be shared through an easily discoverable existing public route (website or system) that includes a metadata description, where patient privacy is upheld, and the system follows a request-for-information approach (where requests are fulfilled subject to an independent review and approval step). Clinical trial data shall be submitted for publication within twelve (12) months after each final study report or report submitted to CEPI. During the same time period, Awardee shall make the results available to the relevant country’s Ministry of Health or equivalent. The clinical trial ID or registry identifier code/number shall be included in all publications of clinical trials.

9.7.Open Access. CEPI requires “Open Access” for Project Data. This means that a copy of the final manuscript of all research publications, journal articles, scholarly monologues and book chapters published under this Clause 9 must be deposited into PubMed Central (or Europe PubMed Central) or otherwise made freely available upon acceptance for publication or immediately after the publisher’s official date of final publication. Moreover, all peer-reviewed published research that is funded, in whole or in part, by CEPI shall be published in accordance with the principles of Plan S (“Accelerating the transition to full and immediate Open Access to scientific publications”), a UK and European data sharing initiative for research funded by public grants.

9.8.Statement of Support in Publications. All such publications shall include a statement that the work was “supported, in whole or in part, by funding from CEPI” (or words to the same effect) and shall credit, where appropriate, the country in which any clinical trials were performed.

10. | Independent Assessors: |

10.1.Independent Assessors. As described in a Work Package or as otherwise reasonably required by CEPI, CEPI may engage one or more independent third-party laboratories or

-13-

collaborators (“Assessors”), in confidence and at CEPI’s expense, to evaluate Project Results, including the Project Vaccine, in order to provide CEPI with directly comparable evaluations of similar materials produced under CEPI’s portfolio of awarded projects. The results of the testing, analysis, meta-analysis or other assessments shall be subject to the confidentiality obligations under this Agreement. CEPI shall provide to the Awardee access to the results of such analysis or assessment relevant to Awardee’s activities under the Project, including information regarding the methodology of the overall analysis or assessment and rationale for conclusions reached under such analysis or assessment sufficient to give context to such results, as well as reasonable access to discuss the same with any such Assessors. For clarity, one of CEPI’s assessors is the Task Force for Global Health and its SPEAC team of vaccine safety experts.

10.2.Awardee Cooperation. Awardee shall provide reasonable assistance to CEPI and any designated Assessor, including:

(a)ensuring that any samples to be transferred or exported by or on behalf of Awardee from a clinical trial site or sample storage site are transferred and/or exported pursuant to the terms and conditions of a suitable to-be-agreed-upon material transfer agreement to be entered into between Awardee and the Assessor in addition to any other applicable laws and regulations.

(b)cooperate in regard to data analysis, to the extent relevant under a given Work Package, by CEPI’s Assessor by:

(i)providing data or other information generated under this Agreement to CEPI’s designated Assessor as CEPI shall request, including data regarding CMC, formulation or the results of any of its pre-clinical or clinical trials (duly anonymized and, upon CEPI’s request, blinded) and other documents and information such as study protocols, case report forms needed to develop standardized approaches and tools for safety data management;

(ii)providing CEPI’s designated Assessor with other data (duly anonymised and, upon CEPI’s request, blinded) as CEPI may reasonably request in order to conduct comparative assessments; and

(iii)providing CEPI’s designated Assessor with clinical trial data (duly de- identified and, at CEPI’s request, blinded) for the purposes of signal detection or meta-analyses of safety data (including across product candidates).

11. | Compliance: |

11.1.Compliance with Applicable Laws. Awardee shall comply with the laws and regulations that are applicable to the activities performed under the Project.

11.2.Compliance with CEPI’s Policies and Procedures. Awardee shall comply with those CEPI policies and procedures communicated to Awardee as they apply to the activities performed under the Project and the use of CEPI funds. As of the Effective Date of this Agreement, these policies and procedures consist of the Third Party Code and Cost Guidance. For clarity, the Third Party Code is a periodically updated, consolidated statement of CEPI’s

-14-

mission and vision, which further describes and incorporates various CEPI policies, procedures and requirements applicable to recipients of CEPI funds. The Third Party Code also describes requirements for procurements and sub-grants. For avoidance of doubt, Awardee shall be considered to have satisfied the Procurement Requirements of Article 14 of the Third Party Code in regard to those procurements/activities in the Budget or a Work Package for which Awardee has specifically identified a Subawardee. The Cost Guidance describes CEPI’s principles regarding eligible direct and indirect costs, non-eligible costs, and valuing in-kind contributions. CEPI shall advise Awardee from time-to-time of material changes to such policies and procedures.

11.3.Compliance Audit. Upon at least [***] notice, CEPI, or an auditor appointed by CEPI (which shall be an internationally recognized certified public accounting firm, not engaged on a contingent basis) shall be entitled to audit no more than [***] and at CEPI’s reasonable cost, Awardee’s performance of its compliance obligations under this Agreement. Such audits will be conducted during normal operating hours in a manner to minimize disruption to Awardee’s business.

12. | Ready Reserve of Clinical Trial Material: |

12.1.Ready Reserve. Unless already addressed by a Work Package, CEPI may request that Awardee undertake the manufacturing and maintenance of a Ready Reserve of Clinical Trial Material through an additional Work Package or Project Expansion, which may include doses from consistency batches. For purposes of this Agreement, a “Ready Reserve of Clinical Trial Material” means a quantity of doses for potential use in a clinical trial of the Project Vaccine, which has not yet received a marketing approval. Such Ready Reserve of Clinical Trial Material may be used for further clinical trials, to advance product development and for emergency use subject to the necessary regulatory approvals or consents, in each case in emergency situations based on national or international guidance (such as by the WHO) or in such other manner as CEPI may reasonably determine. An additional Work Package covering such activities shall be negotiated [***] and in good faith by the Parties.

12.2.Management of Ready Reserve. The Parties agree that CEPI may delegate the management of the Ready Reserve of Clinical Trial Material to WHO or other CEPI designee.

13. | Project Continuity: |

13.1.Awardee Contingency Plan. [***] Awardee shall create and maintain a contingency plan, reasonably approved by CEPI, to address the possible impacts of the COVID-19 pandemic on its own organization as relates to the Project, as described in the iPDP.

13.2.Project Continuity Plan. Because of the exigent nature of the Outbreak, the iPDP shall include a Project Continuity Plan that, at a minimum, shall address the following items:

(a)responsibilities and level of access on the part of other collaborators, Subawardees and consortium members, if any, to Project Results and Enabling Rights;

-15-

(b)management of key Project Materials through participants in the Project and other entities such as the BioEscrow® deposit service of the American Type Culture Collection;

(c)identification of a proposed third party, for example, a Subawardee, under contract to Awardee that is capable of performing the activities in agreed Work Packages, Additional Work Packages or a Project Expansion (“Trusted Collaborator”), in the event that Awardee is unable to continue its activities under this Agreement or declines CEPI’s request to undertake additional Work Packages or a Project Expansion; and

(d)at least a preliminary identification of one or more geographically dispersed manufacturing sites, under contract with Awardee, to produce Project Vaccine for use in the Field (“Trusted Manufacturer”). Awardee shall make a final designation of one or more Trusted Manufacturers, in consultation with CEPI, and prior to the start of a Phase II clinical trial.

13.3.Alternative Designations by CEPI. If Awardee does not designate a Trusted Collaborator and/or Trusted Manufacturer, or they notify Awardee that they are no longer available, then CEPI may propose a Trusted Collaborator or Trusted Manufacturer to Awardee. Neither Party may unreasonably decline to accept the designation of a proposed Trusted Collaborator under Clause 13.2 or this Clause 13.3. Once designated and under contract to pursue Project activities, a Trusted Collaborator and Trusted Manufacturer shall be a Subawardee for the purposes of this Agreement.

13.4.Public Health License. Subject to the terms of this Agreement, Awardee hereby grants a worldwide and royalty free Public Health License to CEPI, on the condition that CEPI may only exercise the rights granted under the Public Health License in the event that:

(a)CEPI is not in material breach of its obligations under this Agreement;

(b)the Project Vaccine has achieved licensure with at least one regulatory body (including but not limited to emergency licensure); and

(c)one or more of the triggers set out in Clause 13.5 has occurred.

CEPI shall be entitled to sublicense Project Results, Enabling IP and Background IP included in the Public Health License in accordance with this Clause 13. Each sublicense shall be in writing and CEPI shall require that each sublicensee complies with the terms of the Public Health License, and if receiving a sublicense to Third Party Background IP, also complies with the terms of the Third Party Background IP license agreement. If a license to Third Party Background IP does not permit further sublicensing by CEPI, Awardee agrees to directly grant CEPI’s designee a sublicense consistent with the Public Health License, provided such third party designee agrees to comply with the terms of the Third Party Background IP license agreement, including, without limitation, any payment of sublicense fees attributable to such sublicense grant. CEPI will remain responsible and liable for the performance of sublicenses under such sublicensed rights to the same extent as if such activities were conducted by CEPI.

-16-

13.5.Public Health License Triggers. Consistent with Clause 13.4, CEPI’s right to exercise the Public Health License shall be satisfied when:

(a)Awardee declines to participate in an Additional Work Package or Project Expansion as requested by CEPI, either directly or indirectly through a Subawardee;

(b)CEPI and Awardee agree, in good faith, that Awardee shall not be able to perform the activities under an agreed Work Package, either directly or indirectly through a Sub awardee;

(c)Awardee is in material breach of this Agreement or the Equitable Access Plan and has not cured such breach within [***] days of notification of such breach by CEPI unless otherwise mutually agreed; or

(d)the Agreement is terminated by CEPI pursuant to Clause 19.2(a)-(b) (default or insolvency) or 19.3(c) - (e) (unavailability to perform Project activities, failure to satisfy payment criteria or fraud).

13.6.Agreement between CEPI and the Trusted Collaborator or Trusted Manufacturer. In the event that the Public Health License is exercised, CEPI may request assignment of the relevant Trusted Collaborator or Trusted Manufacturer contracts from Awardee or, at CEPI’s option, endeavour to reach agreement directly with the Trusted Collaborator and/or Trusted Manufacturer, as the case may be, to perform such activities as CEPI may deem necessary. At CEPI’s request, Awardee shall use [***] to facilitate the conclusion of a direct contractual relationship between the Trusted Collaborator or Trusted Manufacturer, as the case may be, and CEPI. If those negotiations do not result in an agreement in [***], then CEPI may grant rights under its Public Health License to a third party unilaterally designated by CEPI as a Trusted Collaborator or Trusted Manufacturer, without approval from Awardee.

13.7.Effects of Exercise of the Public Health License. Upon exercise of the Public Health License and written notice to Awardee, Awardee [***] shall:

(a)provide CEPI with an updated list of Enabling Rights and applicable Background IP, along with an invoice for any payments due under any license agreement for Third Party Background IP attributable to the grant of the Public Health License to CEPI or a sublicensee;

(b)provide CEPI with a good faith schedule of key technology transfer activities and estimated costs for the technology transfer in Clause 13.6;

(c)[***] transfer to the Trusted Collaborator and/or Trusted Manufacturer, as the case may be, and at CEPI’s reasonable cost, all Project Results, Project Materials described in Clause 13.2(b), all guidance, information, materials and assistance reasonably required to accomplish the Project activities identified by CEPI; and

(d)shall be deemed to have covenanted not to sue CEPI or designee for the exercise of the Public Health License.

-17-

14. | Equitable Access: |

14.1.Commitment to Equitable Access. CEPI is committed to achieving equitable access to the results of all CEPI-supported programmes pursuant to the “Equitable Access Policy” referenced in CEPI’s Third Party Code. Equitable Access means that a Project Vaccine is available first to populations at risk when and where they are needed at affordable prices. For clarity, it is CEPI’s intention that the price of a Project Vaccine shall be commercially sustainable to the manufacturer.

14.2.Project Vaccine Registration. Awardee shall cooperate with CEPI, and at CEPI’s cost, take such actions as are mutually agreed to register Project Vaccines in countries identified as priorities. If Awardee is not the license holder for purposes of registration in a given country, then Awardee shall be responsible for ensuring that its Subawardee facilitate such registrations as requested by CEPI. Awardee shall utilize WHO pre-qualification or similar registrations systems to the extent available.

14.3.Global Allocation. It is the Parties’ expectation that a global allocation and purchasing entity (the “Global Allocation Body”) shall be constituted within six (6) months after the Effective Date of this Agreement to purchase, allocate, and direct the distribution of COVID-19 vaccines including Project Vaccine. Awardee, will negotiate, in good faith a separate agreement or purchase order to supply Project Vaccine as may be required by the Global Allocation Body in such agreement or purchase order to the Global Allocation Body during the Pandemic Period and after the Pandemic Period for LMICs. For the purposes of this paragraph “Pandemic Period” means the period of time between the date that WHO declared COVID-19 to be a PHEIC (that is, 30 January 2020) and the date that WHO declares the PHEIC to have ended including any period of a COVID-19 pandemic re-emergence as declared by the WHO.

14.4.Pandemic Period Production and Supply. During the Pandemic Period, Awardee shall:

(a)produce Project Vaccine as described in the Work Package(s), if not greater;

(b)provide the JMAG with a regularly updated [***] statement of its actual capacity and a forecast of its planned capacity for manufacturing of Project Vaccine;

(c)provide the JMAG with [***] advance written notice of each manufacturing run for the Project Vaccine;

(d)supply up to [***] of the quantity of the Project Vaccine produced for purchase by the Global Allocation Body pursuant to Clause 14.3 during the Pandemic Period. For clarity, Awardee may not allocate or obligate Project Vaccine doses to other third parties during the Pandemic Period that conflicts with its obligations under this Clause 14; and

(e)discuss in good faith with JMAG how to achieve its requirements for doses of Project Vaccine, including any potential increase in Awardee’s manufacturing capacity.

14.5.Post-Pandemic Period Production and Supply. After the Pandemic Period, Awardee shall continue to produce and supply Project Vaccine for purchase as required by the Global Allocation Body pursuant to Clause 14.3.

-18-

14.6.Pricing Objectives. The Parties acknowledge that the price of the Project Vaccine is critical to achieving Equitable Access during the Pandemic Period. Accordingly, Awardee agrees that its pricing shall be reasonable to achieve Equitable Access for populations in need of a Project Vaccine as well as an appropriate return on investment for vaccine manufacturers that make on-going supply commercially sustainable. The Parties acknowledge that the availability of pandemic insurance as described in Clause 17.7 shall be a relevant cost factor in Equitable Access. For clarity, the purchase of Project Vaccine by the Global Allocation Body or by any other purchasing agent(s) designated by CEPI shall be considered to have satisfied the pricing requirements for Equitable Access.

14.7.Costs and Sales. Consistent with the commitments in Clauses 14.4 to 14.6, Awardee shall:

(a)provide written [***] updates to the JMAG regarding its COGs for Project Vaccines and discuss relevant product development decisions that could affect COGs; and

(b)sell the Project Vaccine doses to the Global Allocation Body during and after the Pandemic Period pursuant to Clause 14.3.

14.8.Information about Production, Supply, Pricing and Sales. Upon written request by CEPI, Awardee shall provide reasonable information about its COGs, production, supply, pricing and sales of Project Vaccine sufficient to evaluate whether such activities meet the Equitable Access Policy.

14.9.Audit of Cost of Goods. No more than [***] and at CEPI’s reasonable cost, CEPI shall have the right to review or to designate an external auditor (which shall be an internationally recognized certified public accounting firm, not engaged on a contingent basis) to review Awardee’s financial records relevant to the information provided in Clause 14.8. Such audits will be conducted during normal operating hours in a manner to minimize disruption to Awardee’s business. In event that the audit concludes that the COGs and production, allocation, supply or pricing of Project Vaccine doses are not substantially in accordance with the achievement of Equitable Access as described in Clause 14.1, then Awardee shall: [***]. The provisions of this Clause 14.9 shall apply to any Sub-Grant Awardees and Trusted Collaborators.

14.10.Manufacturing in Multiple Countries. Awardee shall use [***] to establish operational manufacturing facilities in one or more geographically dispersed manufacturing sites as described in the Work Packages.

14.11.Equitable Access Plan. The foregoing commitments regarding Equitable Access shall constitute the “Equitable Access Plan.” This Equitable Access Plan shall be reviewed by JMAG no less than annually and shall take into account changes in COGs over time, production yield and volume and production economics. The Equitable Access Plan shall be regularly updated during the term of this Agreement.

14.12.Alternative to the Global Allocation Body. In the event that a Global Allocation Body is not constituted as expected by the Parties in Clause 14.3, then CEPI or its designated purchasing agent(s) shall have the rights attributed in this Clause 14 to the Global Allocation Body.

-19-

14.13.Loan Facility. CEPI shall fund certain of Awardee’s manufacturing related expenses, that may include reservation fees to secure future production capacity for the Project, certain acquisition fees to secure materials for the Project, and the like, each a “Loan Facility Payment,” as described in the iPDP and Budget, which Awardee may, in its sole discretion, elect to draw upon. CEPI, as lender, shall provide funds to Awardee, as borrower, as follows:

(a)CEPI hereby makes available to Awardee a term loan facility in an amount up to USD $142,500,000.00 (“Loan Amount”), which Loan Amount may be increased by mutual written agreement pursuant to Awardee’s request and CEPI’s acceptance of a loan request as described in subsection (d) below.

(b)Awardee shall apply the full amount of each tranche borrowed by it (each, a “Loan”) under this Clause 14.13 towards each such Loan Facility Payment.

(c)Awardee will request any Loan from CEPI hereunder generally no less than [***] prior to the proposed date of such Loan. For clarity, the advance of a Loan by CEPI for activities under any Work Package shall not be deemed as agreement by CEPI that any required Stage Gates have been achieved.

(d)Loans shall be requested by Awardee on a loan request form provided by CEPI which shall require that Awardee:

(i)affirms that, as of the date of such request, Awardee is not in default or insolvent pursuant to Clause 19.2;

(ii)affirms that the representations and warranties made by Awardee in Clauses 16.1 and 16.2 remain true and correct;

(iii)sets out the amount of the requested Loan, with a supporting third-party agreement or invoice and other documentation reasonably requested by CEPI;

(iv)sets forth any reimbursement to CEPI for or credit offsets against any [***] of a prior Loan amount that was not applied to a Loan Facility Payment; and

(v)sets out a triggering event for repayment (“Repayment Trigger”) for each Loan Facility Payment. For clarity, the nominal Repayment Trigger is the date that Awardee receives an advance purchase commitment or other purchase of Project Vaccine pursuant to Clauses 14.3 to 14.5. The Repayment Trigger may be adjusted by mutual written agreement. In general it is understood that Awardee will undertake to repay each Loan (if such Loan has not otherwise been Discharged) at the time it receives payment for one or more purchases of the Project Vaccine related to such Loan, provided such payment covers Awardee’s actual COGs, not including the amount of the associated Loan, as further described in Clause 14.14.

Awardee’s failure to meet these requirements shall be grounds for CEPI to deny the advancement of any requested Loan, until such requirements are met.

-20-

14.14.Repayment and Discharge. Unless Discharged, each Loan shall be repaid on the date determined by its Repayment Trigger and when repaid by Awardee, will be acknowledged by CEPI as cancelled. Failure by Awardee to repay the Loans to CEPI as described in this Clause 14.14, shall be a material breach of this Agreement and CEPI shall be entitled to specific performance of this obligation. Generally, Awardee shall be released from repaying a Loan (“Discharged”) and such Loan shall be deemed a grant made by CEPI to Awardee when (i) Awardee demonstrates on or before the date determined by its Repayment Trigger of such Loan that Awardee was unable to utilize such reserved capacity or materials, as the case may be, or (ii) Awardee demonstrates that it was unable to secure one or more advanced purchase commitments or other purchases of the associated Project Vaccine and further demonstrates, to CEPI’s reasonable satisfaction, that there is no likely prospect for sale of such Project Vaccine or that Novavax is disposing of such Project Vaccine.

Repayment of Loans shall be made as follows:

(a)If (i) CEPI and Awardee agree to fully utilize reserved capacity from a Loan and (ii) Awardee obtains one or more advance purchase commitments or other purchases of the Project Vaccine produced pursuant to such reserved capacity, any such purchase proceeds that Awardee receives that are in excess of Awardee’s corresponding actual COGs, not including the amount of the associated Loan, shall be used to repay the Loan up to the full amount;

(b)If (i) CEPI and Awardee agree to partially utilize reserved capacity from a Loan and (ii) Awardee obtains one or more advance purchase commitments or other purchases of the Project Vaccine produced pursuant to such reserved capacity, in the interest of assuring Equitable Access to Project Vaccine, a pro-rated portion of the Loan related to the unused reserved capacity will be Discharged and any such purchase proceeds that Awardee receives that are in excess of Awardee’s corresponding actual COGs, not including the amount of the associated Loan, shall be used to repay the remaining portion of the Loan;

(c)If CEPI and Awardee agree not to utilize any reserved capacity from a Loan (whether or not CEPI utilizes the reserved capacity pursuant to Clause 14.16(a)), the entire amount of the Loan shall be Discharged;

(d)If against CEPI’s agreement, Awardee utilizes all or a portion of the reserved capacity from a Loan, Awardee shall repay the Loan in the full amount in [***] after Awardee starts utilizing the reserved capacity;

(e)For a Loan related to the purchase of materials, if Awardee obtains one or more advance purchase commitments or other purchases of the Project Vaccine produced using such material, any such purchase proceeds that Awardee receives that are in excess of Awardee’s corresponding actual COGs, not including the amount of the associated Loan, shall be used to repay the Loan up to the full amount; and

(f)Notwithstanding the previous, the Parties recognize that a variety of external factors, may impact repayment of a Loan and therefore agree to timely meet as requested

-21-

by one Party and discuss a good faith adjustment to the repayment scenarios described herein.

14.15.Interest on Loans. No interest shall accrue or be payable on any Loan made under the Loan Facility.

14.16.Other Use of Reserved Capacity.

(a)If, as described in Clause 14.14(c), CEPI and Awardee agree not to utilize any reserved capacity from a Loan and the period of time for such reserved capacity is available, then CEPI shall have the right, but not an obligation, to use the reserved capacity for production of a designated third party product at its own cost but with the benefit of any unused credit recognized from the Loan Facility Payment, as provided by the underlying agreement with the entity with which such manufacturing capacity has been reserved.

(b)Awardee shall ensure that any contract with a relevant manufacturer to reserve and utilize reserved capacity secured by one or more Loan Facility Payment shall provide CEPI with the rights contemplated in the immediately preceding subsection (a); and shall provide copies of such contracts to CEPI in confidence. For clarity, Awardee shall have [***] after the Effective Date of this Agreement in which to secure such rights under any relevant third party contract already signed as of the Effective Date.

15. | Commercial Benefits: |

15.1.Commercial Benefits. CEPI is required by its own funders to obtain a share of any awardee’s Commercial Benefits as a contribution to support CEPI’s programme activities. As used in this Agreement, “Commercial Benefits” means any economically quantifiable benefits that arise from the commercial exploitation of the Project Results (including the Project Vaccine) other than in preparation for or in response to the Outbreak. Examples of Commercial Benefits include the sales of a Project Vaccine for market, commercial licensing of Project IP, receipt of government-granted incentives such as Priority Review Vouchers and revenue from the commercialization of combination, derivative or follow-on products (including antibody products, assays and vaccines) or application of production technology resulting in whole or part from CEPI funding.

15.2.Sharing of Commercial Benefits. Notwithstanding Clause 15.1, In consideration for the Awardee accepting and complying with the provisions of Clause 13, CEPI agrees to forgo any share of potential Commercial Benefits.

16. | Representations and Warranties: |

16.1.Awardee Warranties. Awardee warrants that the following statements are true and correct to its reasonable knowledge and belief as they relate to the Project as of the Effective Date:

(a)it has the full power and authority to enter into and assume its obligations under this Agreement;

-22-

(b)this Agreement has been duly executed and is legal binding and enforceable in accordance with its terms:

(c)it is in material compliance with all statutes, regulations, directives and requirements of any governmental entity;

(d)it does not infringe, misappropriate or violate the intellectual property, privacy or publicity rights of any third party;

(e)it is not under any obligation, contractual or otherwise, to any person or third party in respect of the Enabling Rights that conflicts with or is inconsistent in any material respect with the terms of this Agreement or that would impede the complete fulfillment of its obligations under this Agreement;

(f)it has disclosed in writing to CEPI any actual or contemplated commitments or obligations to third parties for Project Vaccine doses;

(g)it has identified Enabling Rights in writing to CEPI;

(h)neither Awardee nor agreed Subawardees, if any, nor any officer or employee of the foregoing has been debarred or is subject to debarment by a regulatory authority or funding agency anywhere in the world; and

(i)all financial and other information submitted to CEPI in relation to this Agreement is true, complete and accurate in all material respects.

16.2.Awardee Representation. During the Term of this Agreement, Awardee shall:

(a)notify CEPI [***] in the event that any of the foregoing warranties are no longer true and correct, and shall so notify CEPI at least at the time that Awardee requests any disbursement of Project funds;

(b)provide written updates to the JMAG regarding Enabling Rights acquired or created during the course of the Project;

(c)notify CEPI before accepting third-party funds related to the Project (not including public financings by Awardee via at-the-market offerings or other follow-on offerings of equity or debt);

(d)make no encumbrances over, dispose of, or otherwise deal with the Project Results, Intellectual Property and Enabling Rights in any way that would be reasonably deemed inconsistent with this Agreement, including the Public Health License, or that would impede the complete fulfillment of its obligations under this Agreement without the express written permission of CEPI; and

(e)notify CEPI promptly if it becomes aware that any actions are likely or have already been taken by the government of any country in which Awardee shall conduct Project activities that may adversely affect Awardee’s commitments in this Agreement, including

-23-

Equitable Access. For clarity, such government actions may relate, for example, to the exercise of eminent domain or sovereign rights over Project Vaccine doses.

16.3.Additional Awardee Representation. In the event that the Public Health License becomes exercisable, then continuing after the expiration or termination of this Agreement, Awardee shall make no encumbrances over, dispose of, or otherwise deal with the Project Results, Intellectual Property and Enabling Rights, in any way that may be inconsistent with the objectives of this Agreement, including the Public Health License, without the express written permission of CEPI

16.4.CEPI Warranties. CEPI warrants that the following statements are true and correct to its reasonable knowledge and belief, as relate to the Project:

(a)it has the full power and authority to enter into and assume its obligations under this Agreement;

(b)it is in material compliance with all statutes, regulations, directives and requirements of any governmental entity; and

(c)it has not granted rights to any third party in respect of Project Results (other than in accordance with the terms of this Agreement).

16.5.No Other Warranties. EXCEPT AS EXPRESSLY SET FORTH IN THIS AGREEMENT, NO PARTY MAKES, AND EACH PARTY EXPRESSLY DISCLAIMS, ANY AND ALL WARRANTIES OF ANY KIND, EXPRESS OR IMPLIED, INCLUDING THE WARRANTIES OF DESIGN, MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE, VALIDITY OF PATENTS, NON-INFRINGEMENT OF THE INTELLECTUAL PROPERTY RIGHTS OF THIRD PARTIES, OR ARISING FROM A COURSE OF DEALING, USAGE OR TRADE PRACTICES.

17. | Insurance, Liability and Indemnification; Liability: |

17.1.Insurance. Awardee shall maintain insurance sufficient to cover the activities, risks, and potential omissions relevant to the Project, including clinical trial liability insurance cover, in accordance with generally accepted industry standards and as required by law. In the event that the Public Health License becomes exercisable and CEPI exercises such rights, CEPI shall maintain comparable insurance protection. Awardee shall provide CEPI with a certificate confirming such insurance upon request.

17.2.Indemnification for Third Party Claims. Awardee shall indemnify and defend CEPI, its Affiliates, officers, directors, third party contractors and employees from and against any and all claims, damages, and liabilities asserted by third parties (including claims for negligence) which arise directly or indirectly from: (i) Awardee’s, or its Affiliate’s or Subawardee’s activities under this Agreement, (ii) the research, development, manufacture, promotion or use of any Project Vaccine, Project Results or Enabling Rights (including for clarity, the use of any Project Results in development activities and clinical studies) conducted by Awardee, or its Affiliates or Subawardees, or (iii) any claim that the use of Awardee’s Intellectual Property Rights infringe the intellectual property rights of any third party, except to the extent such claim, damage or liability is caused by CEPI’s negligence or intentional misconduct. In the event that the Public

-24-

Health License becomes exercisable and CEPI exercises such rights, the obligations of this Clause 17.2 shall apply to CEPI mutatis mutandis.

17.3.Conduct of Responses to Third Party Claims. Each Party shall use all reasonable endeavours to inform the other Party [***] of any circumstances that are likely to give rise to a third party claim which may be covered by Clause 17.2 together with copies of all relevant papers and official documents. The indemnified party shall not take any material action in respect of any third party claim which is covered by Clause 17.2 without the consent of the indemnifying party, including settlement of any such third party claim, provided such consent is not unreasonably conditioned, withheld or delayed. The indemnifying party assumes control of defence of the claim and shall keep the indemnified party fully informed of the progress of all relevant third party claims which are covered by Clause 17.2 and shall fully consult with the indemnified party on the nature of any defence to be advanced in advance. The indemnified party may have its counsel participate in (but not control) the defence of a claim at the indemnified party’s own expense.

17.4.Exclusions. Except in the event of a breach of a Party’s confidentiality obligations under Clause 18 or CEPI’s breach of the scope of the Publice Health License, neither Party shall be liable to the other Party for any [***] arising out of any breach of or failure to perform any of the provisions of this Agreement.

17.5.Liability Cap. [***]

17.6.Exclusions from Liability Cap. Notwithstanding the foregoing, nothing in this Agreement shall limit the liability of either Party in respect of: [***]

17.7.Pandemic Insurance. The Parties acknowledge that, as of the Effective Date, the WHO is considering an insurance mechanism that would provide insurance cover for the suppliers of investigational products for use in the case of a PHEIC declared by WHO. The Parties agree that, if and when this mechanism is established, they shall discuss in good faith the impact of such arrangements on the Parties’ obligations under this Agreement and how it would apply to the supply of Project Vaccines.

18. | Confidentiality: |

18.1.Confidential Information. Confidential Information means non-public information disclosed by one Party to the other. For avoidance of doubt, for so long as none of the exceptions in Section 18.2 apply, COGs, production, supply, pricing and sales of Project Vaccine shall be deemed Confidential Information of Awardee, provided however, that CEPI shall have the right to utilize and disclose such Confidential Information in a manner that anonymizes Awardee’s identity by aggregating it with similar information from other of CEPI’s awardees or third parties. Each Party undertakes that during the term of this Agreement and for [***] after, it shall keep confidential and not disclose the other Party’s Confidential Information to any person other than its employees, agents, consultants, contractors, professional advisers, Subawardees and regulatory authorities and, in the case of CEPI, its funders and Assessors, who have a need to know and agree to respect its confidentiality. Each Party shall take commercially reasonable

-25-

precautions to protect against unauthorized disclosure. For clarity, Project Results may be disclosed and utilized by the Parties as set out in this Agreement.

18.2.Confidentiality Limitations. Confidential Information shall not include:

(a)information already known to the receiving Party and which is not subject to prexisting obligations of confidentiality;

(b)information that is independently developed by the receiving Party;

(c)information that is or becomes part of the public domain other than by unauthorized disclosure by receiving Party;

(d)information properly obtained by the receiving Party from a source that, to the best knowledge of the receiving Party, is not bound by a confidentiality obligation to the disclosing Party; and

(e)information to the limited extent that is required to be disclosed by a competent legal authority; provided, that where it is free to do so, the receiving Party shall give notice of such disclosure to the disclosing Party as soon as reasonably practicable.

19. | Term and Termination: |

19.1.Term. This Agreement shall commence on the Effective Date identified in the Agreement Summary and shall continue in full force and effect until the activities set out in all active Work Packages, including any additional Work Packages, have been completed or until the Agreement otherwise is terminated pursuant to this Clause 19 (the “Term”).

19.2.Termination by Either Party for Default or Insolvency. Either Party (the “Terminating Party”) may terminate this Agreement by giving written notice of termination, effective immediately, if the other Party (the “Defaulting Party”):

(a)breaches a material obligation in this Agreement and either fails to cure that breach within a cure period of [***] after notice from the Terminating Party or longer time if agreed in writing or if prompt and reasonable steps to cure the breach are undertaken when the breach is not reasonably capable of cure with [***] and such diligent efforts are maintained until cure is achieved; or

(b)makes any arrangement with its creditors, resolves to or undergoes any insolvency proceeding anywhere in the world (except for the purpose of solvent amalgamation or reconstruction).

19.3.Other Termination by CEPI. CEPI shall be entitled to terminate this Agreement by providing written notice of termination to Awardee in the following circumstances:

(a)with [***] if CEPI notifies Awardee that there are material safety, regulatory or ethical issues with continuing the Project, as reasonably determined by CEPI;

-26-

(b)subject to Clause 4.2 upon [***] prior written notice, if CEPI determines that the Project must be limited in scope or terminated;

(c)CEPI reasonably determines that Awardee is unable, or shall become unable, to discharge its obligations under this Agreement, [***] and Awardee does not reasonably alleviate CEPI’s concerns within a cure period of [***] or such longer time as may be agreed by the Parties in writing; or

(d)Awardee does not satisfy the criteria in Clause 3.4 required for CEPI to pay funding tranches under a Work Package and fails to satisfy those criteria in full within a cure period of [***] or such longer time as may be agreed by the Parties in writing.

(e)Awardee has committed fraud or a Financial Irregularity. For purposes of this Agreement, “Financial Irregularity” refers to any and all kinds of corruption, including bribery, nepotism and illegal gratuities; misappropriation of cash, inventory and all other kinds of assets; and making fraudulent financial and non-financial statements to CEPI.

19.4.Payments After Certain Terminations by Awardee. If this Agreement is terminated by Awardee pursuant to Clause 19.2(a) - (b) (default or insolvency on the part of CEPI) or terminated by CEPI pursuant to Clause 19.3(a) - (b) (issues precluding continuation of the Project or limiting of Project Scope by CEPI), then CEPI shall reimburse Awardee for all reasonably incurred expenses through termination and any non-cancellable expenses relating to Project activities that were included in the iPDP and/or authorised by CEPI and that arise through termination and after the termination date, solely to the extent they are not otherwise covered by CEPI funding.

19.5.Effects of Termination by CEPI under Clause 19.2(a) - (b) or 19.3 (c) - (e). If this Agreement is terminated by CEPI pursuant to Clause 19.2(a) - (b) (default or insolvency on the part of Awardee) or 19.3 (c) - (e) (inability to proceed or financial issues with Awardee), then, CEPI shall reimburse Awardee for all reasonably incurred expenses through termination and any non-cancellable expenses relating to the Project activities that were included in in the iPDP and/or authorised by CEPI and that arise through termination and after the termination date]. Additionally, Awardee shall use all reasonable endeavours to, at CEPI’s expense:

(a)make all Project Data publicly available in such manner as CEPI may direct, except to the extent that to do so would result in the public disclosure of Enabling Rights that would not otherwise reasonably be publicly disclosed;

(b)ship to CEPI (or its designee) all Project Materials within [***] of CEPI requesting such Materials in writing;

(c)[***] transfer to CEPI (or its designee), any regulatory approvals and applications for regulatory approvals relating to the Project Vaccine;

(d)provide CEPI with an updated list of all sublicense, contract manufacturing agreements and other third party agreements and arrangement to which Awardee is a party that solely relate to the development of the Project Vaccine and still have work outstanding (the “Contracts”) within [***] of the Termination Date;

-27-

(e)as requested by CEPI, and to the extent it has the legal right to do so (i) assign the benefit (subject to the assumption of the burden) of one or more Contracts to CEPI (or its designee) and, where consent of a third party is required, seek to obtain such consent; (ii) novate one or more Contracts to CEPI (or its designee); or (iii) terminate one or more Contracts in accordance with its terms [***];

(f)as requested by CEPI, perform technology transfer, on an expedited basis, to a Trusted Collaborator or Trusted Manufacturer, as the case may be; and

(g)as requested by CEPI, provide written confirmation or ratification in the event that CEPI exercises the Public Health License.

19.6.Additional Effects of Termination. In all termination events:

(a)CEPI shall not be required to make any further payments to Awardee under this Agreement or any Work Package other than as specified in this Clause 19;

(b)Awardee shall return any CEPI funds within [***] from the date of termination that are unspent, if any, after deducting reimbursement to Awardee for all reasonably incurred expenses through termination and any non-cancellable expenses relating to the Project activities that were included in the iPDP and/or authorised by CEPI and that arise through termination and after the termination date;

(c)each Party shall return or destroy, as requested by the other Party, the Confidential Information of the other Party, except: (i) CEPI may retain the Project Results subject to the obligations of confidentiality set out in Clause 18, (ii) each Party may keep one (1) copy of such Confidential Information for monitoring compliance, and (iii) solely in the event that the Public Health License has been exercised, CEPI may retain such other Confidential Information reasonably required by CEPI to exercise and benefit from the Public Health License. Neither Party shall be required to delete copies of Confidential Information stored on automatic electronic backup systems;

(d)if there is an on-going clinical trial, unless agreed otherwise by the Parties in writing, Awardee shall ensure that no additional trial subjects are enrolled and the Parties shall work together to plan and implement a wind-down of the study in an orderly fashion, with due regard for patient safety and the rights of any participating subjects.

19.7.Repayment of Funds for Financial Irregularity. Where termination is due to any Financial Irregularity or fraudulent or illegal activity by Awardee, Awardee shall repay to CEPI the amount of funds related to such financial irregularity or fraudulent or illegal activity within [***] of the notice of termination.

19.8.Survival of Rights and Identified Clauses. Termination of this Agreement shall be without prejudice to the rights and duties of either Party accrued prior to termination. The following sections shall continue to be enforceable notwithstanding termination or expiration: Clauses 2.6, 3.6 - 3.10, 6.4 - 6.5, 9 -11, 13 - 15, 17, 18.1 and 19 - 20 as well as any other provision, which by its nature, is intended to survive termination.

-28-

20. | Resolving Differences: |

20.1.Resolution by the JMAG. Awardee and CEPI shall cooperate in good faith to resolve differences and disputes about the Project at the JMAG.

20.2.Escalation to Senior Management of the Parties. Any difference or dispute that cannot be resolved by the JMAG shall be submitted to the Parties’ respective Chief Executive Officers or designees for resolution. If the Parties remain unable to resolve such dispute within [***] or such additional time as mutually agreed, then the Parties irrevocably submit to arbitration for its resolution.