UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

For the quarterly period ended June 30, 2021

OR

For the transition period from to .

Commission File No. 000-26770

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip code) | ||||||||||

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| x | Accelerated Filer | o | |||||||||

| Non-accelerated filer | o | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

The number of shares outstanding of the Registrant's Common Stock, $0.01 par value, was 74,484,166 as of July 31, 2021.

NOVAVAX, INC.

TABLE OF CONTENTS

| Page No. | ||||||||

i

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

NOVAVAX, INC.

CONSOLIDATED BALANCE SHEETS

(in thousands, except share and per share information)

| June 30, 2021 | December 31, 2020 | ||||||||||

| (unaudited) | |||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Marketable securities | |||||||||||

| Restricted cash | |||||||||||

| Accounts receivable | |||||||||||

| Unbilled services | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Total current assets | |||||||||||

| Restricted cash | |||||||||||

| Property and equipment, net | |||||||||||

| Intangible assets, net | |||||||||||

| Goodwill | |||||||||||

| Other non-current assets | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Deferred revenue | |||||||||||

| Current portion of finance lease liabilities | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Convertible notes payable | |||||||||||

| Non-current finance lease liabilities | |||||||||||

| Other non-current liabilities | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies | |||||||||||

Preferred stock, $ | |||||||||||

| Stockholders' equity: | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

Treasury stock, | ( | ( | |||||||||

| Accumulated other comprehensive income | |||||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

The accompanying notes are an integral part of these financial statements.

1

NOVAVAX, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share information)

(unaudited)

| For the Three Months Ended June 30, | For the Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Revenue: | |||||||||||||||||||||||

| Government contracts | $ | $ | $ | $ | |||||||||||||||||||

| Grant and other | |||||||||||||||||||||||

| Royalties | |||||||||||||||||||||||

| Total revenue | |||||||||||||||||||||||

| Expenses: | |||||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| General and administrative | |||||||||||||||||||||||

| Total expenses | |||||||||||||||||||||||

| Loss from operations | ( | ( | ( | ( | |||||||||||||||||||

| Other income (expense): | |||||||||||||||||||||||

| Investment income | |||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | |||||||||||||||||||

| Other income (expense) | ( | ||||||||||||||||||||||

| Net loss before income tax expense | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Income tax expense | |||||||||||||||||||||||

| Net loss | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Basic and diluted net loss per share | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Basic and diluted weighted average number of common shares outstanding | |||||||||||||||||||||||

CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(in thousands)

(unaudited)

| For the Three Months Ended June 30, | For the Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Net loss | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Other comprehensive income (loss): | |||||||||||||||||||||||

| Net unrealized losses on marketable securities available-for-sale, net of reclassifications | ( | ||||||||||||||||||||||

| Foreign currency translation adjustment | ( | ( | |||||||||||||||||||||

| Other comprehensive loss | ( | ( | |||||||||||||||||||||

| Comprehensive loss | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

The accompanying notes are an integral part of these financial statements.

2

NOVAVAX, INC.

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY (DEFICIT)

Three Months Ended June 30, 2021 and 2020

(in thousands, except share information)

(unaudited)

| Common Stock | Additional Paid-in Capital | Accumulated Deficit | Treasury Stock | Other Comprehensive Income (Loss) | Stockholders' Equity (Deficit) | ||||||||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2021 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||||

| Non-cash stock-based compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Stock issued under incentive programs | — | ( | — | ||||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Balance at June 30, 2021 | $ | $ | $ | ( | $ | ( | $ | $ | |||||||||||||||||||||||||||||||||

| Balance at March 31, 2020 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

| Preferred stock beneficial conversion feature | — | — | ( | — | — | ||||||||||||||||||||||||||||||||||||

| Non-cash stock-based compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Stock issued under incentive programs | — | — | — | ||||||||||||||||||||||||||||||||||||||

Issuance of common stock, net of issuance costs of $ | — | — | |||||||||||||||||||||||||||||||||||||||

| Unrealized loss on marketable securities | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Balance at June 30, 2020 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of these financial statements.

3

NOVAVAX, INC.

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY (DEFICIT)

Six Months Ended June 30, 2021 and 2020

(in thousands, except share information)

(unaudited)

| Common Stock | Additional Paid-in Capital | Accumulated Deficit | Treasury Stock | Other Comprehensive Income (Loss) | Stockholders' Equity (Deficit) | ||||||||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2020 | $ | $ | $ | ( | $ | ( | $ | $ | |||||||||||||||||||||||||||||||||

| Non-cash stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Stock issued under incentive programs | — | ( | — | ||||||||||||||||||||||||||||||||||||||

Issuance of common stock, net of issuance costs of $ | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Unrealized loss on marketable securities | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Balance at June 30, 2021 | $ | $ | $ | ( | $ | ( | $ | $ | |||||||||||||||||||||||||||||||||

| Balance at December 31, 2019 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||||||||||||||||||

| Preferred stock beneficial conversion feature | — | — | ( | — | |||||||||||||||||||||||||||||||||||||

| Non-cash stock-based compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Stock issued under incentive programs | — | ( | — | ||||||||||||||||||||||||||||||||||||||

Issuance of common stock, net of issuance costs of $ | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Unrealized loss on marketable securities | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Balance at June 30, 2020 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of these financial statements.

4

NOVAVAX, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

(unaudited)

| Six Months Ended June 30, | |||||||||||

| 2021 | 2020 | ||||||||||

| Operating Activities: | |||||||||||

| Net loss | $ | ( | $ | ( | |||||||

| Reconciliation of net loss to net cash used in operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Non-cash stock-based compensation | |||||||||||

| Right-of-use assets written off | |||||||||||

| Other | ( | ||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Receivables, prepaid expenses and other assets | ( | ||||||||||

| Accounts payable and accrued expenses | |||||||||||

| Deferred revenue | |||||||||||

| Net cash provided by operating activities | |||||||||||

| Investing Activities: | |||||||||||

| Capital expenditures | ( | ( | |||||||||

| Acquisition of Novavax CZ, net of cash required | ( | ||||||||||

| Purchases of marketable securities | ( | ( | |||||||||

| Proceeds from maturities and sale of marketable securities | |||||||||||

| Net cash provided by (used in) investing activities | ( | ||||||||||

| Financing Activities: | |||||||||||

| Net proceeds from sale of preferred stock | |||||||||||

| Net proceeds from sales of common stock | |||||||||||

| Net proceeds from the exercise of stock-based awards | |||||||||||

| Finance lease payments | ( | ||||||||||

| Net cash provided by financing activities | |||||||||||

| Effect of exchange rate on cash, cash equivalents and restricted cash | ( | ||||||||||

| Net increase in cash, cash equivalents and restricted cash | |||||||||||

| Cash, cash equivalents and restricted cash at beginning of period | |||||||||||

| Cash, cash equivalents and restricted cash at end of period | $ | $ | |||||||||

| Supplemental disclosure of non-cash activities: | |||||||||||

| Right-of-use assets from new lease agreements | $ | $ | |||||||||

| Capital expenditures included in accounts payable and accrued expenses | $ | $ | |||||||||

| Supplemental disclosure of cash flow information: | |||||||||||

| Cash interest payments | $ | $ | |||||||||

| Cash paid for income taxes | $ | $ | |||||||||

The accompanying notes are an integral part of these financial statements.

5

NOVAVAX, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2021

(unaudited)

Note 1 – Organization

Note 2 – Summary of Significant Accounting Policies

Basis of Presentation

The accompanying unaudited consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“U.S. GAAP”) for interim financial information and the instructions to Form 10-Q and Article 10 of Regulation S-X. The consolidated balance sheet as of June 30, 2021, the consolidated statements of operations and the consolidated statements of comprehensive loss for the three and six months ended June 30, 2021 and 2020, the consolidated statements of changes in stockholders’ equity (deficit) for the three and six months ended June 30, 2021 and 2020 and the consolidated statements of cash flows for the six months ended June 30, 2021 and 2020 are unaudited, but include all adjustments (consisting of normal recurring adjustments) that the Company considers necessary for a fair presentation of the financial position, operating results, comprehensive loss, changes in stockholders’ equity (deficit) and cash flows, respectively, for the periods presented. Although the Company believes that the disclosures in these unaudited consolidated financial statements are adequate to make the information presented not misleading, certain information and footnote information normally included in consolidated financial statements prepared in accordance with U.S. GAAP have been condensed or omitted as permitted under the rules and regulations of the United States Securities and Exchange Commission (“SEC”).

The unaudited consolidated financial statements include the accounts of Novavax, Inc. and its wholly owned subsidiaries, including Novavax AB and Novavax CZ. All intercompany accounts and transactions have been eliminated in consolidation.

The accompanying unaudited consolidated financial statements are presented in U.S. dollars. The functional currency of Novavax AB, which is located in Sweden, is the local currency (Swedish Krona), and the functional currency of Novavax CZ, which is located in the Czech Republic, is the local currency (Czech Koruna). The translation of assets and liabilities of these subsidiaries to U.S. dollars is made at the exchange rate in effect at the consolidated balance sheet date, while equity accounts are translated at historical rates. The translation of the statement of operations data is made at the average exchange rate in effect for the period. The translation of operating cash flow data is made at the average exchange rate in effect for the period, and investing and financing cash flow data is translated at the exchange rate in effect at the date of the underlying transaction. Translation gains and losses are recognized as a component of accumulated other comprehensive income in the accompanying unaudited consolidated balance sheets. Accumulated other comprehensive income included a foreign currency translation balance of $4.2 million and $7.0 million as of June 30, 2021 and December 31, 2020, respectively.

The accompanying unaudited consolidated financial statements should be read in conjunction with the financial statements and notes thereto included in the Company's Annual Report on Form 10-K for the year ended December 31, 2020. Results for this or any interim period are not necessarily indicative of results for any future interim period or for the entire year. The Company operates in one business segment.

6

Use of Estimates

The preparation of the consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ materially from those estimates.

Cash and Cash Equivalents

Cash and cash equivalents consist of highly liquid investments with maturities of three months or less from the date of purchase. Cash and cash equivalents consist of the following at (in thousands):

| June 30, 2021 | December 31, 2020 | ||||||||||

| Cash | $ | $ | |||||||||

| Money market funds | |||||||||||

| Government-backed securities | |||||||||||

| Treasury securities | |||||||||||

| Corporate debt securities | |||||||||||

| Agency securities | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

Marketable Securities

The Company invests in marketable securities that generally consist of debt securities with maturities greater than three months from the date of purchase that include commercial paper, government-backed securities, treasury securities, corporate notes and agency securities. Classification of marketable securities between current and non-current is dependent upon the maturity date at the balance sheet date taking into consideration the Company's ability and intent to hold the investment to maturity.

Interest and dividend income are recorded when earned and included in investment income in the consolidated statements of operations. Premiums and discounts, if any, on marketable securities are amortized or accreted to maturity and included in investment income in the consolidated statements of operations. The specific identification method is used in computing realized gains and losses on the sale of the Company's securities.

Restricted Cash

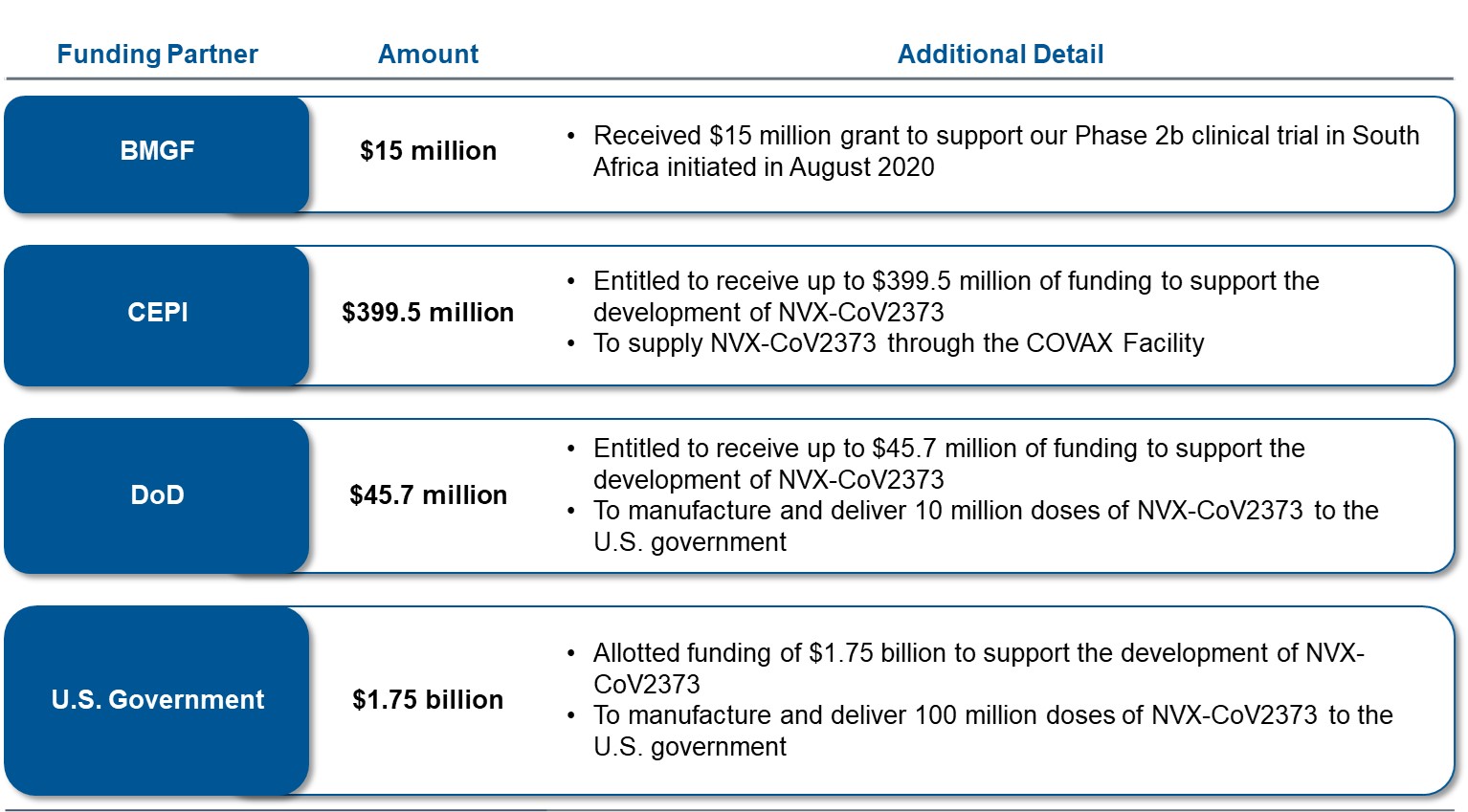

The Company’s current and non-current restricted cash includes payments received under the Coalition for Epidemic Preparedness Innovations (“CEPI”) funding agreements, payments received under the Bill & Melinda Gates Foundation (“BMGF”) grant agreements and cash collateral accounts under letters of credit that serve as security deposits for certain facility leases. The Company will utilize the CEPI and BMGF funds as it incurs expenses for services performed under these agreements.

7

As of June 30, 2021, the restricted cash balances (both current and non-current) consisted of $1.2 million for payments received from BMGF, $45.2 million of payments under the CEPI funding agreements and $1.5 million of security deposits. As of December 31, 2020, the restricted cash balances (both current and non-current) consisted of $1.5 million for payments received from BMGF, $92.4 million of payments under the CEPI funding agreements and $1.5 million of security deposits.

The following table provides a reconciliation of cash, cash equivalents and restricted cash reported in the consolidated balance sheets that sum to the total of the same such amounts shown in the statement of cash flows (in thousands):

| June 30, 2021 | December 31, 2020 | ||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash current | |||||||||||

| Restricted cash non-current | |||||||||||

| Cash, cash equivalents and restricted cash | $ | $ | |||||||||

Income Taxes

The Company accounts for income taxes in accordance with ASC Topic 740, Income Taxes. Under the liability method, deferred income taxes are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis and operating loss carryforwards.

The Company has historically generated significant federal, state and foreign tax net operating losses, which may be subject to limitation in future periods. Management has fully reserved the related deferred tax assets with a valuation allowance in the current reporting period as more likely than not the related benefit will not be realized. The Company is currently subject to examination in all open tax years.

During the three and six months ended June 30, 2021, the Company recognized $3.5 million and $6.6 million, respectively, of income tax expense related to foreign withholding tax on royalties.

Net Loss per Share

Net loss per share is computed using the weighted average number of shares of common stock outstanding. As of June 30, 2021 and 2020, the Company had outstanding stock options, stock appreciation rights (“SARs”) and unvested restricted stock units (“RSUs”) totaling 6,092,983 and 7,797,651 , respectively.

As of June 30, 2021, the Company’s Notes (see Note 7) would have been convertible into approximately 2,385,800 shares of the Company’s common stock assuming a common stock price of $136.20 or higher. These shares, after giving effect to the add back of interest expense and unamortized debt issuance costs on the Notes and any shares due to the Company upon settlement of its capped call transactions, are excluded from the computation, as their effect is antidilutive.

8

Recent Accounting Pronouncements

Not Yet Adopted

In August 2020, the Financial Accounting Standards Board ("FASB") issued ASU No. 2020-06, Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity (“ASU 2020-06”), which will simplify the accounting for certain financial instruments with characteristics of liabilities and equity, including certain convertible instruments and contracts in an entity’s own equity. Specifically, the new standard will remove the separation models required for convertible debt with cash conversion features and convertible instruments with beneficial conversion features. It will also remove certain settlement conditions that are currently required for equity contracts to qualify for the derivative scope exception and will simplify the diluted earnings per share calculation for convertible instruments. ASU 2020-06 will be effective January 1, 2022 for the Company and may be applied using a full or modified retrospective approach. Management has evaluated the impact of adopting ASU 2020-06 and has determined that it will not have a material impact on the Company’s consolidated financial statements.

Note 3 – Fair Value Measurements

The following table represents the Company's fair value hierarchy for its financial assets and liabilities (in thousands):

| Fair Value at June 30, 2021 | Fair Value at December 31, 2020 | ||||||||||||||||||||||||||||||||||

| Assets | Level 1 | Level 2 | Level 3 | Level 1 | Level 2 | Level 3 | |||||||||||||||||||||||||||||

| Money market funds(1) | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Government-backed securities(1) | |||||||||||||||||||||||||||||||||||

| Treasury securities(2) | |||||||||||||||||||||||||||||||||||

| Corporate debt securities(3) | |||||||||||||||||||||||||||||||||||

| Agency securities(4) | |||||||||||||||||||||||||||||||||||

| Total cash equivalents and marketable securities | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Liabilities | |||||||||||||||||||||||||||||||||||

| Convertible notes payable | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

(1)Classified as cash and cash equivalents as of June 30, 2021 and December 31, 2020, respectively, on the consolidated balance sheets.

(2)Includes $199,990 and $44,052 classified as cash and cash equivalents as of June 30, 2021 and December 31, 2020, respectively, on the consolidated balance sheets.

(3)Includes $1,386,056 and $246,668 classified as cash and cash equivalents as of June 30, 2021 and December 31, 2020, respectively, on the consolidated balance sheets.

(4)Includes $110,993 classified as cash and cash equivalents as of June 30, 2021 on the consolidated balance sheets.

Fixed-income investments categorized as Level 2 are valued at the custodian bank by a third-party pricing vendor's valuation models that use verifiable observable market data, e.g., interest rates and yield curves observable at commonly quoted intervals and credit spreads, bids provided by brokers or dealers or quoted prices of securities with similar characteristics. Pricing of the Company's Notes (see Note 7) has been estimated using other observable inputs, including the price of the Company's common stock, implied volatility, interest rates and credit spreads among others.

During the six months ended June 30, 2021 and 2020, the Company did not have any transfers between levels.

9

Note 4 – Marketable Securities

Marketable securities classified as available-for-sale as of June 30, 2021 and December 31, 2020 were comprised of (in thousands):

| June 30, 2021 | December 31, 2020 | ||||||||||||||||||||||||||||||||||||||||||||||

| Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | ||||||||||||||||||||||||||||||||||||||||

| Treasury securities | $ | $ | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

| Corporate debt securities | ( | ||||||||||||||||||||||||||||||||||||||||||||||

| Agency securities | |||||||||||||||||||||||||||||||||||||||||||||||

| Total marketable securities | $ | $ | $ | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

The primary objective of the Company's investment policy is the preservation of capital; thus, the Company's investment policy limits investments to certain types of instruments with high-grade credit ratings, places restrictions on maturities and concentrations in certain industries and requires the Company to maintain a certain level of liquidity. As of June 30, 2021, all of the Company's investments were in securities classified as cash and cash equivalents.

Note 5 – Goodwill and Other Intangible Assets

Goodwill

The change in the carrying amounts of goodwill for the six months ended June 30, 2021 was as follows (in thousands):

| Amount | |||||

| Balance at December 31, 2020 | $ | ||||

| Currency translation adjustments | ( | ||||

| Balance at June 30, 2021 | $ | ||||

Identifiable Intangible Assets

Purchased intangible assets consisted of the following as of June 30, 2021 and December 31, 2020 (in thousands):

| June 30, 2021 | December 31, 2020 | ||||||||||||||||||||||||||||||||||

| Gross Carrying Amount | Accumulated Amortization | Intangible Assets, Net | Gross Carrying Amount | Accumulated Amortization | Intangible Assets, Net | ||||||||||||||||||||||||||||||

| Finite-lived intangible assets: | |||||||||||||||||||||||||||||||||||

| Proprietary adjuvant technology | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||

| Collaboration agreements | ( | ( | |||||||||||||||||||||||||||||||||

| Total identifiable intangible assets | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||

Amortization expense for the six months ended June 30, 2021 and 2020 was $0.2 million and $0.3 million, respectively.

Estimated amortization expense for existing intangible assets for the remainder of 2021 and for each of the five succeeding years ending December 31 will be as follows (in thousands):

| Year | Amount | |||||||

| 2021 (remainder) | $ | |||||||

| 2022 | ||||||||

| 2023 | ||||||||

| 2024 | ||||||||

| 2025 | ||||||||

| 2026 | ||||||||

10

Note 6 - Leases

During the second quarter of 2021, the Company evaluated the impact of changes in facts and circumstances on its Contract Manufacturing Organizations and Contract Development and Manufacturing Organizations agreements that had previously been determined to represent embedded lease arrangements. The Company concluded that the impact resulted in the modification of existing leases and, in accordance with its policy, the Company remeasured and reallocated the remaining consideration in the contracts and reassessed the lease classification as of the effective date of the modification. As a result, the Company recognized a Right-Of-Use ("ROU") asset and a corresponding long-term operating lease liability of $11.4 million on the remeasurement of one of its long-term supply agreements using an incremental borrowing rate of 6.5 %. The Company expensed the ROU asset since it relates to research and development activities for the development of NVX-CoV2373 for which the Company does not have an alternative future use. Modifications to leases with a lease term of 12 months or less at the commencement date did not result in a change in lease classification and, in accordance with the Company's election to apply the practical expedient in ASC Topic 842, Leases (“ASC 842”), it did not recognize a ROU asset or lease liability but instead, lease payments are recognized as an expense on a straight-line basis over the modified lease term and variable lease payments that do not depend on an index or rate, are recognized as an expense in the period in which the variable lease costs are incurred based on performance or usage in accordance with contractual agreements.

During the three and six months ended June 30, 2021, the Company recognized a short-term lease expense of $86.6 million and $214.2 million, respectively, related to its embedded leases, including a new lease that commenced during the first quarter of 2021. The Company did no

During the three and six months ended June 30, 2021, the Company recognized $1.8 million and $4.0 of interest expenses, respectively, on its finance lease liabilities. The Company did no

Note 7 – Long-Term Debt

Convertible Notes

The Company incurred approximately $10.0 million of debt issuance costs during the first quarter of 2016 relating to the issuance of $325 million aggregate principal amount of convertible senior unsecured notes that will mature on February 1, 2023 (the “Notes”), which were recorded as a reduction to the Notes on the consolidated balance sheet. The $10.0 million of debt issuance costs is being amortized and recognized as additional interest expense over the seven year contractual term of the Notes on a straight-line basis, which approximates the effective interest rate method.

Total convertible notes payable consisted of the following at (in thousands):

| June 30, 2021 | December 31, 2020 | ||||||||||

| Principal amount of Notes | $ | $ | |||||||||

| Unamortized debt issuance costs | ( | ( | |||||||||

| Total convertible notes payable | $ | $ | |||||||||

The interest expense incurred in connection with the Notes consisted of the following (in thousands):

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

Coupon interest at | $ | $ | $ | $ | |||||||||||||||||||

| Amortization of debt issuance costs | |||||||||||||||||||||||

| Total interest expense on Notes | $ | $ | $ | $ | |||||||||||||||||||

11

Note 8 – Stockholders' Equity

Note 9 – Stock-Based Compensation

Equity Plans

The 2015 Stock Incentive Plan, as amended (“2015 Plan”), was approved at the Company's annual meeting of stockholders in June 2015. Under the 2015 Plan, equity awards may be granted to officers, directors, employees and consultants of and advisors to the Company and any present or future subsidiary.

The 2015 Plan authorizes the issuance of up to 12.4 million shares of common stock under equity awards granted under the 2015 Plan, including an increase of 1.5 million shares approved for issuance under the 2015 Plan at the Company's 2021 annual meeting of stockholders. All such shares authorized for issuance under the 2015 Plan have been reserved. The 2015 Plan will expire on March 4, 2025.

The Amended and Restated 2005 Stock Incentive Plan (“2005 Plan”) expired in February 2015 and no new awards may be made under such plan, although awards will continue to be outstanding in accordance with their terms.

The 2015 Plan permits and the 2005 Plan permitted the grant of stock options (including incentive stock options), restricted stock, stock appreciation rights and restricted stock units. In addition, under the 2015 Plan, unrestricted stock, stock units and performance awards may be granted. Stock options and stock appreciation rights generally have a maximum term of ten years and may be or were granted with an exercise price that is no less than 100 % of the fair market value of the Company's common stock at the time of grant. Grants of stock options are generally subject to vesting over periods ranging from to four years .

Stock Options and Stock Appreciation Rights

The following is a summary of stock options and SARs activity under the 2015 Plan and 2005 Plan for the six months ended June 30, 2021:

| 2015 Plan | 2005 Plan | ||||||||||||||||||||||

| Stock Options and SARs | Weighted-Average Exercise Price | Stock Options | Weighted-Average Exercise Price | ||||||||||||||||||||

| Outstanding at January 1, 2021 | $ | $ | |||||||||||||||||||||

| Granted | $ | $ | |||||||||||||||||||||

| Exercised | ( | $ | ( | $ | |||||||||||||||||||

| Canceled | ( | $ | $ | ||||||||||||||||||||

| Outstanding at June 30, 2021 | $ | $ | |||||||||||||||||||||

| Shares exercisable at June 30, 2021 | $ | $ | |||||||||||||||||||||

| Shares available for grant at June 30, 2021 | |||||||||||||||||||||||

12

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Weighted average Black-Scholes fair value of stock options granted | $ | $ | $ | $ | |||||||||||||||||||

| Risk-free interest rate | |||||||||||||||||||||||

| Dividend yield | |||||||||||||||||||||||

| Volatility | |||||||||||||||||||||||

| Expected term (in years) | |||||||||||||||||||||||

The total aggregate intrinsic value and weighted-average remaining contractual term of stock options and SARs outstanding under the 2015 Plan and 2005 Plan as of June 30, 2021 was approximately $865 million and 8.1 years, respectively. The total aggregate intrinsic value and weighted-average remaining contractual term of stock options and SARs exercisable under the 2015 Plan and 2005 Plan as of June 30, 2021 was approximately $121 million and 5.5 years, respectively. The aggregate intrinsic value represents the total intrinsic value (the difference between the Company's closing stock price on the last trading day of the period and the exercise price, multiplied by the number of in-the-money stock options and SARs) that would have been received by the holders had all stock option and SAR holders exercised their stock options and stock appreciation rights on June 30, 2021. This amount is subject to change based on changes to the closing price of the Company's common stock. The aggregate intrinsic value of stock options and vesting of restricted stock awards for the six months ended June 30, 2021 and 2020 was approximately $115 million and $8 million, respectively.

Employee Stock Purchase Plan

The Employee Stock Purchase Plan, as amended (the “ESPP”), was approved at the Company's annual meeting of stockholders in June 2013. The ESPP currently authorizes an aggregate of 600,000 shares of common stock to be purchased. The ESPP allows employees to purchase shares of common stock of the Company at each purchase date through payroll deductions of up to a maximum of 15 % of their compensation, at 85 % of the lesser of the market price of the shares at the time of purchase or the market price on the beginning date of an option period (or, if later, the date during the option period when the employee was first eligible to participate). As of June 30, 2021, there were 212,876 shares available for issuance under the ESPP.

The ESPP is considered compensatory for financial reporting purposes. As such, the fair value of ESPP shares was estimated at the date of grant using the Black-Scholes option-pricing model with the following assumptions:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Range of Black-Scholes fair values of ESPP shares granted | $ | $ | $ | $ | |||||||||||||||||||

| Risk-free interest rate | |||||||||||||||||||||||

| Dividend yield | |||||||||||||||||||||||

| Volatility | |||||||||||||||||||||||

| Expected term (in years) | |||||||||||||||||||||||

13

Restricted Stock Units

The following is a summary of restricted stock units activity for the six months ended June 30, 2021:

| Number of Shares | Per Share Weighted- Average Fair Value | ||||||||||

| Outstanding and Unvested at January 1, 2020 | $ | ||||||||||

| Restricted stock units granted | $ | ||||||||||

| Restricted stock units vested | ( | $ | |||||||||

| Restricted stock units forfeited | ( | $ | |||||||||

| Outstanding and Unvested at June 30, 2021 | $ | ||||||||||

The Company recorded all stock-based compensation expense in the consolidated statements of operations as follows (in thousands):

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Research and development | $ | $ | $ | $ | |||||||||||||||||||

| General and administrative | |||||||||||||||||||||||

| Total stock-based compensation expense | $ | $ | $ | $ | |||||||||||||||||||

As of June 30, 2021, there was approximately $230 million of total unrecognized compensation expense related to unvested stock options, SARs, restricted stock units and the ESPP. The increase in unrecognized compensation expense is primarily due to the significant increase in the Company's common stock price starting in 2020. This unrecognized non-cash compensation expense is expected to be recognized over a weighted-average period of one year , and will be allocated between research and development and general and administrative expenses accordingly. This estimate does not include the impact of other possible stock-based awards that may be made during future periods and awards that require approval by the stockholders.

Note 10 –Contingencies

Note 11 – Revenue

14

consisted of funding under U.S. government contracts and the Company's funding arrangement with CEPI to advance the clinical development and manufacturing of NVX-CoV2373.

The Company recorded revenue as follows (in thousands):

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Government contracts | |||||||||||||||||||||||

| OWS | $ | $ | $ | $ | |||||||||||||||||||

| DoD | |||||||||||||||||||||||

| Grants and other | |||||||||||||||||||||||

| CEPI | |||||||||||||||||||||||

BMGF | |||||||||||||||||||||||

| Other | |||||||||||||||||||||||

| Royalties | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

Government Contracts and Grants

The Company’s U.S. government contracts comprise an agreement with Advanced Technology International (“ATI”), the Consortium Management Firm acting on behalf of the Medical CBRN Defense Consortium in connection with the partnership formerly known as Operation Warp Speed (“OWS”) and a contract with the U.S. Department of Defense (the “DoD”). As of June 30, 2021, the Company's OWS agreement was fully funded up to $1.75 billion to support certain activities related to the development of NVX-CoV2373 and the manufacture and delivery of 100 million doses of the vaccine candidate to the U.S. government. The U.S. government has recently instructed the Company to prioritize alignment with the U.S. Food and Drug Administration on the Company's analytic methods before conducting additional U.S. manufacturing and further indicated that the U.S. government will not fund additional U.S. manufacturing until such agreement has been made. The U.S. government also instructed the Company to proceed with work under the OWS Agreement related to all other activities, including ongoing clinical trials and nonclinical studies, regulatory interactions, analytics/assays and characterization of manufactured vaccine and project management. The Company’s revenue from CEPI comprises grant and forgivable loan funding. The latter is repayable if the proceeds from the sales of NVX-CoV2373 to one or more third parties cover the Company’s costs of manufacturing the vaccine, not including manufacturing costs funded by CEPI.

Collaboration and License Agreements

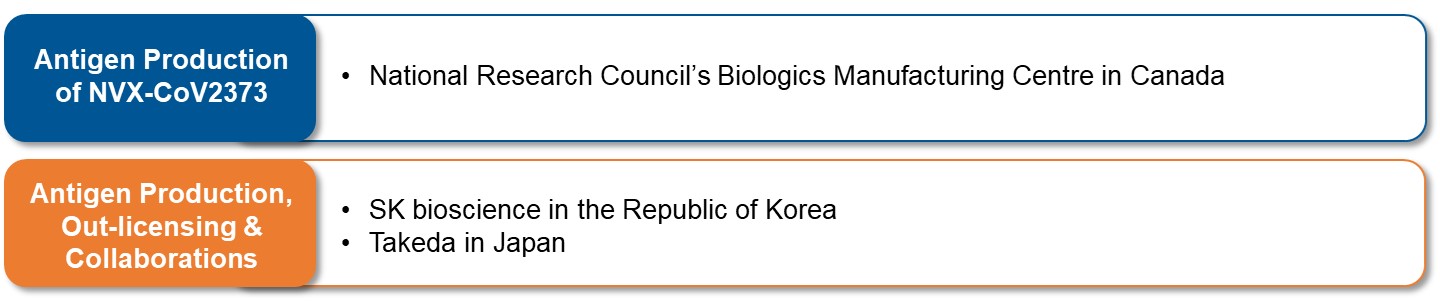

In February 2021, the Company finalized an expanded collaboration and license agreement with SK bioscience to manufacture and commercialize NVX-CoV2373 for sale to the government of Korea. Concurrently, SK bioscience finalized an advance purchase agreement with the Korean government to supply 40 million doses of NVX-CoV2373 to the Republic of Korea beginning in 2021. The agreement is in addition to the Company's existing manufacturing arrangement with SK bioscience entered into in August 2020. Under the collaboration agreement, SK bioscience was granted an exclusive license to develop, manufacture and commercialize NVX-CoV2373 in the Republic of Korea. SK bioscience expanded its capacity to manufacture the antigen component of NVX-CoV2373 for use in the final drug product globally, including product distributed by the COVAX Facility. SK bioscience will also purchase a certain quantity of NVX-CoV2373 directly from the Company, subject to approval by relevant regulatory authority, and sufficient doses of Matrix-M™ adjuvant to manufacture the remainder of the 40 million doses of NVX-CoV2373 it expects to sell to the Korean government. SK bioscience will pay the Company a tiered royalty in the low to middle double-digit range on the sale of NVX-CoV2373. The Company recognized royalties of $23.5

In February 2021, the Company finalized a collaboration agreement previously announced in August 2020, with Takeda Pharmaceutical Company Limited (“Takeda”) for the exclusive development, manufacturing and commercialization of NVX-CoV2373 in Japan. Under the agreement, the Company will transfer technology and supply the Matrix-M™ adjuvant to Takeda, which will manufacture the antigen component of NVX-CoV2373. Takeda will receive funding from the Government

15

of Japan’s Ministry of Health, Labour and Welfare to support the technology transfer, establishment of infrastructure and scale-up of manufacturing. The Company will be entitled to receive royalties based on the achievement of certain development and commercial milestones, as well as on a portion of net profits from the sale of the vaccine.

Vaccine Supply Agreements

During the six months ended June 30, 2021, the Company entered into various Advanced Purchase Agreements ("APAs"), including an agreement with Her Majesty the Queen in Right of Canada as represented by the Minister of Public Works and Government Services to supply 52 million doses of NVX-CoV2373. The Company will submit an application for regulatory approval in Canada following its first submission for regulatory approval in another priority market and the Canada authority will provide reasonable assistance to the Company with obtaining such regulatory approval. As part of the agreement, Canada will have the option to purchase up to an additional 24 million doses of NVX-CoV2373. In February 2021, the Company reached a MOU with the Canadian government to produce NVX-CoV2373 in Canada. The Company plans to produce NVX-CoV2373 at the National Research Council’s Biologics Manufacturing Centre in Montreal once both the vaccine candidate and the facility receive Health Canada approvals.

In May 2021, the Company finalized an APA with Gavi, the Vaccine Alliance ("Gavi") building upon its MOU previously announced in February 2021. Under the terms of the agreement, 1.1 billion doses of NVX-CoV2373 are to be made available to countries participating in the COVAX Facility, which was established to allocate and distribute vaccines equitably to participating countries and economies. The Company expects to manufacture and distribute 350 million doses of NVX-CoV2373 to countries participating under the COVAX Facility. Under a separate purchase agreement with Gavi, Serum Institute of India Private Limited ("SIIPL") is expected to manufacture and deliver the balance of the 1.1 billion doses of NVX-CoV2373 for low- and middle-income countries participating in the COVAX Facility. The Company expects to deliver doses with antigen and adjuvant manufactured at facilities directly funded under the Company's funding agreement with CEPI. The Company expects to supply significant doses that Gavi would allocate to low-, middle- and high-income countries, subject to certain limitations, utilizing a tiered pricing schedule and Gavi may prioritize such doses to low- and middle- income countries, at lower prices. Additionally, the Company may provide additional doses of NVX-CoV2373, to the extent available from CEPI funded manufacturing facilities, in the event that SIIPL cannot materially deliver expected vaccine doses to the COVAX Facility. Together with SIIPL, the Company expects to initiate delivery of doses following receipt of appropriate regulatory authorizations. Under the agreement, the Company received an upfront payment from Gavi of $350 million during the second quarter of 2021 and expects to receive an additional payment of $350 million if the Company secures emergency use listing for NVX-CoV2373 by the World Health Organization ("WHO").

During the six months ended June 30, 2021, changes in the Company's accounts receivables, unbilled services and deferred revenue balances were as follows (in thousands):

| December 31, 2020 | Additions | Deductions | June 30, 2021 | |||||||||||||||||||||||

| Accounts receivable | $ | $ | $ | ( | $ | |||||||||||||||||||||

| Unbilled services | ( | |||||||||||||||||||||||||

| Deferred revenue | ( | |||||||||||||||||||||||||

As of June 30, 2021, the deferred revenue of $1.2 billion primarily comprised of approximately $1.1 billion related to upfront payments under APAs.

Note 12 – Subsequent Events

In August 2021, the Company announced that it finalized the terms of an APA with the European Commission, which the parties expect to execute during the third quarter of 2021, for the purchase of up to 100 million initial doses of NVX-CoV2373, with the option of the European Commission to purchase an additional 100 million doses through 2023.

In August 2021, the Company filed regulatory submissions in partnership with SIIPL for emergency use authorization in multiple markets. Regulatory submissions were filed with the Drugs Controller General of India, as well as regulatory agencies in Indonesia and the Philippines. In addition to these filings, the Company expects to file a submission to the WHO for emergency use listing in August of 2021.

16

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Any statements in the discussion below and elsewhere in this Quarterly Report about expectations, beliefs, plans, objectives, assumptions or future events or performance of Novavax, Inc. (“Novavax,” together with its wholly owned subsidiaries Novavax AB and Novavax CZ, the “Company,” “we” or “us”) are not historical facts and are forward-looking statements. Such forward-looking statements include, without limitation, statements about our capabilities, goals, expectations regarding future revenue and expense levels and capital raising activities; our operating plans and prospects; potential market sizes and demand for our product candidates; the efficacy, safety and intended utilization of our product candidates; the development of our clinical-stage product candidates and our recombinant vaccine and adjuvant technologies; the development of our preclinical product candidates; the conduct, timing and potential results from clinical trials and other preclinical studies; plans for and potential timing of regulatory filings; our expectation of manufacturing capacity, timing, production and delivery for NVX-CoV2373; our expectations with respect to the anticipated ongoing development and potential commercialization or licensure of NVX-CoV2373 and NanoFlu™; the expected timing and content of regulatory actions; funding from the U.S. government partnership formerly known as Operation Warp Speed (“OWS”), the U.S. Department of Defense (“DoD”) and the Coalition for Epidemic Preparedness Innovations (“CEPI”), and payments from the Bill & Melinda Gates Foundation (“BMGF”); funding under our advance purchase agreements and supply agreements; our available cash resources and usage and the availability of financing generally; plans regarding partnering activities and business development initiatives; and other matters referenced herein. Generally, forward-looking statements can be identified through the use of words or phrases such as “believe,” “may,” “could,” “will,” “would,” “possible,” “can,” “estimate,” “continue,” “ongoing,” “consider,” “anticipate,” “intend,” “seek,” “plan,” “project,” “expect,” “should,” “would,” “aim,” or “assume,” the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words.

Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs and expectations about the future of our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Forward-looking statements involve estimates, assumptions, risks and uncertainties that could cause actual results or outcomes to differ materially from those expressed or implied in any forward-looking statements, and, therefore, you should not place considerable reliance on any such forward-looking statements. Such risks and uncertainties include, without limitation, challenges satisfying, alone or together with partners, various safety, efficacy, and product characterization requirements, including those related to process qualification and assay validation, necessary to satisfy each applicable regulatory authority, like the U.S. Food and Drug Administration (“FDA”), World Health Organization (“WHO”), UK Medicines and Healthcare Products Regulatory Agency (“MHRA”), the European Medicines Agency (“EMA”), the Republic of Korea’s Ministry of Food and Drug Safety (“MFDS”), or Japan’s Ministry of Health, Labour and Welfare (“MHLW”); difficulty obtaining scarce raw materials; resource, including human capital and manufacturing capacity, constraints on our ability to pursue these regulatory pathways, alone or with partners, in multiple jurisdictions simultaneously, leading to staggering of regulatory filings and potential regulatory actions; challenges meeting contractual requirements under agreements with multiple commercial, governmental, and other entities; and other risks and uncertainties identified in Part II, Item 1A “Risk Factors” of this Quarterly Report and in Part I, Item 1A “Risk Factors” of our Annual Report on Form 10-K, which may be detailed and modified or updated in other documents filed with the United States Securities and Exchange Commission (“SEC”) from time to time, and are available at www.sec.gov and at www.novavax.com. You are encouraged to read these filings as they are made.

We cannot guarantee future results, events, level of activity, performance or achievement. Any or all of our forward-looking statements in this Quarterly Report may turn out to be inaccurate or materially different from actual results. Further, any forward-looking statement speaks only as of the date when it is made, and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by law. New factors emerge from time to time, and it is not possible for us to predict which factors will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

Overview

Novavax, Inc., together with our wholly-owned subsidiaries, Novavax AB and Novavax CZ, is a biotechnology company promoting improved global health through the discovery, development and commercialization of innovative vaccines to prevent serious infectious diseases and address urgent, global health needs. Our vaccine candidates, including both our coronavirus vaccine candidate (“NVX-CoV2373”) and our seasonal quadrivalent influenza vaccine candidate (“NanoFlu™”), are genetically engineered, three-dimensional nanostructures of recombinant proteins critical to disease pathogenesis. We believe that our protein-subunit-based candidates elicit differentiated immune responses that may be more efficacious than naturally occurring immunity or other vaccine approaches. Additionally, our Matrix-M™ adjuvant has been shown to enhance functional immune responses and has been well-tolerated in multiple clinical trials. To date, we have formulated many of the vaccine candidates in our pipeline with our Matrix-M™ adjuvant, including NVX-CoV2373 and NanoFlu™.

17

Near-term Clinical Development Pipeline

Our development pipeline encompasses vaccine candidates addressing therapeutic areas including coronavirus, seasonal influenza, respiratory syncytial virus (“RSV”) and other emerging infectious diseases. At the forefront of our pipeline is NVX-CoV2373. We have advanced NVX-CoV2373 through two Phase 3 clinical trials, which have demonstrated high efficacy against the original COVID-19 strain and commonly circulating variants of COVID-19 with a favorable safety profile. We have also advanced our NanoFlu™ vaccine program through a Phase 3 clinical trial, which demonstrated positive top-line results and achieved statistical significance in key secondary endpoints. We continue to evaluate the viability of certain combination vaccines, including combinations of our NanoFlu™, NVX-CoV2373 and respiratory syncytial virus fusion (F) protein nanoparticle vaccine candidate (“RSV F Vaccine”).

We remain focused on bringing our NVX-CoV2373 vaccine candidate to market following global regulatory approvals. Through ongoing crossover and booster studies in our clinical trials, as well as the development of our COVID-19 variant strain vaccine candidates, we continue to collect data to characterize and optimize vaccine performance. We expect to leverage these clinical insights to advance our booster strategy given the evolving COVID-19 pandemic.

In addition to our COVID-19 clinical development, NanoFlu™ continues to be a priority for our team, especially as it relates to development of our NanoFlu™ / NVX-CoV2373 combination vaccine candidate (“qNIV/CoV2373”).

Although NVX-CoV2373 and NanoFlu™ are our near-term priorities, we remain optimistic that the additional programs in our pipeline, including our vaccine candidates for RSV and other emerging infectious diseases, present viable opportunities for future development.

The pipeline chart below summarizes the clinical and preclinical development programs that we are focusing on in the near-term.

(1)Supported by funding from OWS, DoD, CEPI and BMGF

18

(2)Ongoing PREVENT-19, a Phase 3 clinical trial in the U.S. and Mexico; Ongoing PREVENT-19 pediatric expansion in the U.S.; Ongoing Phase 3 clinical trial in the UK; Ongoing Phase 2b clinical trial in South Africa

(3)Reflects malaria vaccine candidate (“R21”) created by the University of Oxford and formulated with Matrix-M™

adjuvant; Ongoing Phase 3 clinical trial in Africa; R21 is licensed to Serum Institute of India Private Limited ("SIIPL"); Novavax will have commercial rights to sell and distribute R21 in certain countries, primarily in travelers' and military vaccine markets

(4)Reflects malaria transmission blocking vaccine candidate (“R0.6C”) manufactured by Statens Serum Institut; Ongoing Phase 1 clinical trial in the Netherlands to evaluate R0.6C, Matrix-M™ adjuvant and common aluminum hydroxide adjuvant

Matrix-M™ Adjuvant

Our proprietary Matrix-M™ adjuvant has demonstrated potent and well-tolerated efficacy by stimulating the entry of antigen presenting cells (“APCs”) into the injection site and enhancing antigen presentation in local lymph nodes, which in turn activates T-cell, B-cell, and APC populations, thereby boosting immune response. Our Matrix-M™ adjuvant has been shown to increase neutralizing antibodies and induces long-lasting memory B cells, which enhances B-cell immunity and recruits and increases the frequency of CD4+ and CD8+ T cells to enhance T-cell immunity in preclinical models. The potent immune-stimulating mechanism of action enables a lower dose of antigen required to achieve the desired immune response, ultimately contributing to increased supply and manufacturing capacity. These immune-boosting and dose-sparing capabilities contribute to the adjuvant’s highly unique profile. Our Matrix-M™ adjuvant is being evaluated in combination with several other vaccine antigens produced by other manufacturers.

Coronavirus

NVX-CoV2373 Clinical Development

We have evaluated NVX-CoV2373 in various preclinical and clinical trials, including two Phase 3 trials, one Phase 2b trial, and one Phase 1/2 trial. Through our clinical development program to date, we confirmed the use of a 5-microgram dose of NVX-CoV2373 with Matrix-M™ adjuvant for late-stage development. We have also collected data that indicates a reassuring safety profile and high levels of efficacy for NVX-CoV2373 against original COVID-19 strain and commonly circulating variants. A summary and status of our clinical development of NVX-CoV2373 follows:

PREVENT-19 Pediatric Expansion

In June 2021, we completed enrollment of the pediatric expansion of our PREVENT-19 Phase 3 trial in the U.S. that was initiated in April 2021. The pediatric expansion is a placebo-controlled study to evaluate efficacy, safety, and immunogenicity of NVX-CoV2373 in 2,248 adolescent participants aged 12 to 17 across up to 75 sites in the U.S. Participants will randomly receive either the vaccine candidate or placebo in two doses, administered 21 days apart. Two-thirds of participants will receive intramuscular injections of the vaccine and one-third will receive placebo. All primary doses have been administered and a blinded crossover is planned to take place in August 2021 to ensure that all trial participants receive active vaccine before the start of the 2021-2022 school year. Participants will be monitored for safety for up to two years following the final administered dose.

PREVENT-19 Phase 3 U.S. and Mexico

In June 2021, we announced results from the final analysis of our PREVENT-19 Phase 3 trial in the U.S. and Mexico initiated in December 2020. The final analysis was conducted on events accrued prior to participants receiving crossover vaccine. In the final analysis, NVX-CoV2373 achieved its primary efficacy endpoint with an overall efficacy of 90.4% despite over half the illness cases being caused by Variants of Interest ("VoI") and Variants of Concern ("VoC"). Additionally, NVX-CoV2373 demonstrated 100% protection against moderate and severe disease, including those caused by variants.

PREVENT-19 was a randomized, placebo-controlled, observer-blinded trial to evaluate the efficacy, safety, and immunogenicity of NVX-CoV2373 in 29,960 participants aged 18 years or older across 119 sites in the U.S. and Mexico. Enrollment for PREVENT-19 emphasized recruiting high-risk groups most impacted by COVID-19. The participant trial population was composed of the following: 22% Latin American, 12% African American, 7% Native American, 4% Asian American, 37% with underlying medical co-morbidities and 13% older adults aged 65 years and older. The trial design was harmonized to align with other Phase 3 trials conducted under the auspices of OWS, including the use of a single external, independent Data and Safety Monitoring Board to evaluate safety. The trial’s primary endpoint was the first occurrence of PCR-confirmed, symptomatic (mild, moderate or severe) COVID-19 with onset at least seven days after the second study

19

vaccination in participants who had not been previously infected with SARS-CoV-2. Two-thirds of the participants were assigned to randomly receive two intramuscular injections of NVX-CoV2373 comprising 5 micrograms of antigen with 50 micrograms of Matrix-M™ adjuvant, administered 21 days apart, while one-third of the trial participants received placebo. The primary efficacy analysis was event-driven, based on the number of participants with symptomatic mild, moderate, or severe COVID-19 disease.

Efficacy endpoints were accrued from January 25, 2021, through April 30, 2021, at a time when the Alpha (B.1.1.7) variant strain became the predominant strain in the U.S. Other strains, including VoI and VoC, were also on the rise during the PREVENT-19 endpoint accrual window. PREVENT-19 met a key secondary endpoint, demonstrating 100% efficacy against variants not considered VoC/VoI. NVX-CoV2373 also demonstrated 92.6% efficacy against VoC/VoI, achieving a key exploratory endpoint of the study. Among high-risk populations (participants over age 65, under age 65 with certain comorbidities, or having life circumstances with frequent COVID-19 exposure), NVX-CoV2373 demonstrated 91.0% efficacy. Preliminary safety data showed NVX-CoV2373 to be generally well-tolerated, with serious and severe adverse events low in number and balanced between vaccine and placebo groups. Participants will be followed for 24 months following the second injection. PREVENT-19 was conducted with support and funding from OWS.

Phase 3 United Kingdom (“UK”)

In June 2021, the final analysis of our Phase 3 UK trial was published in the New England Journal of Medicine. The publication of the final analysis highlights the robust safety and efficacy data for NVX-CoV2373. The final analysis confirmed 89.7% overall efficacy, with over 60% of the cases caused by the Alpha (B.1.1.7) variant strain. The analysis also confirmed 96.4% efficacy against non-Alpha (non-B.1.1.7) variant strains, which represents strains most similar to the original COVID-19 virus. The final analysis also demonstrated that initial vaccine side effects were mostly mild and transient, and that no imbalance was seen in more serious adverse events compared with the placebo arm. The final analysis builds upon the interim analysis conducted in January 2021 and updated analysis announced in March 2021. The trial was a randomized, observer-blinded, placebo-controlled study that enrolled 15,203 adults aged 18 to 84. Half of the trial participants received two intramuscular injections of NVX-CoV2373 comprising 5 micrograms of antigen with 50 micrograms of Matrix-M™ adjuvant, administered 21 days apart, while the other half of the trial participants received placebo. The trial was conducted in partnership with the UK government Vaccines Taskforce and led by researchers at St George’s, University of London and St George’s Hospital, London.

Phase 3 UK Co-Administration Sub-Study

In June 2021, we announced data from the co-administration sub-study of NVX-CoV2373 and an approved influenza vaccine, conducted as part of our Phase 3 UK trial. In this study, 431 participants enrolled in our Phase 3 UK trial received an approved seasonal influenza vaccine (Seqirus, adjuvanted, trivalent seasonal influenza vaccine or a cell-based quadrivalent seasonal influenza vaccine). Approximately half of the participants in the study were also co-vaccinated with NVX-CoV2373, while the remainder received placebo. Results demonstrated a robust immune response and a favorable safety and reactogenicity profile. Immunogenicity of the influenza vaccine was preserved with concomitant administration, while a modest decrease in the immunogenicity of NVX-CoV2373 was found. There was an adequate number of participants aged 18 to 64 to confirm an efficacy trend of 87.5% against COVID-19. The majority of local and systemic reactogenicity events were absent or mild, with small increases in pain and tenderness at the injection site and muscle aches being elevated amongst participants who were co-vaccinated with NVX-CoV2373 and influenza vaccine. Rates of severe adverse events ("SAEs") were low in all groups, and there were no additional early safety concerns associated with co-administration. Rates of unsolicited adverse events (“AEs”), medically attended AEs, and SAEs were low and balanced between the groups. Data from this study have been submitted for peer review and are available ahead of publication via the preprint server on medRxiv. The co-administration sub-study represents the first study of a SARS-CoV-2 vaccine candidate and an approved influenza vaccine, and was led by researchers at St George’s, University of London and St George’s Hospital, London.

Phase 2b South Africa

In May 2021, results from the initial primary analysis of our Phase 2b South Africa trial were published in the New England Journal of Medicine. The publication of the initial primary analysis, which was previously announced in January 2021, highlights NVX-CoV2373’s cross-protection against the Beta (B.1.351) variant strain prevalent in South Africa during the study.

The Phase 2b South Africa trial was a randomized, observer-blinded, placebo-controlled study that enrolled 4,404 participants. Half of the trial participants received two intramuscular injections of NVX-CoV2373 comprising 5 micrograms of antigen with 50 micrograms of Matrix-M™ adjuvant, administered 21 days apart, while the other half of the trial participants received placebo.

20

In the complete analysis announced in March 2021, NVX-CoV2373 demonstrated 55.4% efficacy for the prevention of mild, moderate and severe COVID-19 disease in the 95% of the trial population that was HIV-negative. Overall efficacy, including both HIV-positive and HIV-negative participants, was 48.6% predominantly against the Beta (B.1.351) variant strain, with the complete analysis showing that NVX-CoV2373 achieved its primary efficacy endpoint in the overall trial population. During the efficacy analysis, the Beta (B.1.351) variant strain circulating in South Africa accounted for approximately 93% of sequenced cases in our Phase 2b trial. There were no cases of severe disease in the NVX-CoV2373 group, and all hospitalization and death occurred in the placebo group. This trial also showed that the vaccine is well-tolerated, with low levels of SAEs through day 35, balanced between vaccine and placebo groups.

While the interim analysis announced in January 2021 reported that prior infection with the original COVID-19 strain may not completely protect against subsequent infection by the variant predominantly circulating in South Africa, the complete analysis indicated that there may be a late protective effect of prior exposure with the original COVID-19 strain. In placebo recipients, at 90 days the illness rate was 8.0% in baseline seronegative participants, with a rate of 5.9% in baseline seropositive participants. CEPI funded the manufacturing of doses of NVX-CoV2373 for this Phase 2b clinical trial, which was also supported in part by a $15.0 million grant from BMGF.

NVX-CoV2373 Booster and Crossover Studies

Novavax-Led Crossover Studies

In April 2021, we initiated crossover arms in our Phase 3 UK, Phase 2b South Africa and PREVENT-19 Phase 3 trials. In June 2021, we completed crossover arms in our Phase 3 UK trial. As of August 2021, our Phase 2b South Africa and PREVENT-19 crossover arms are ongoing.

In our Phase 3 UK and PREVENT-19 trials, participants were offered the opportunity to receive an additional round of injections. Participants who elected to do so received an additional two-dose regimen of either vaccine for those who originally received placebo or placebo for those who originally received vaccine. In our Phase 2b South Africa trial, participants will receive either active vaccine for those who initially received placebo or a booster dose of active vaccine for those who initially received active vaccine. Throughout our crossover arms, participants in all of our trials will remain blinded to their courses of treatment to preserve the ability to assess clinical data in an unbiased manner.

Novavax-Led Booster Study

In August 2021, we announced data from our six-month booster study in the Phase 2 portion of our U.S. and Australia Phase 1/2 trial, which we initiated in March 2021. In this booster study, select participants in the 5 microgram dose cohort from the Phase 2 portion of the Phase 1/2 trial received a third 5 microgram dose (a booster dose) at six months to examine the functional immune response of our vaccine candidate. Results from this study showed that twenty-eight days following boosting, anti-spike IgG increased approximately 4.6-fold compared to the peak response seen after the second dose (Day 217 GMEU = 200,408 (95% CI: 159,796; 251,342)). This boosted value represents a 3.7 to 4.4-fold increase in anti-spike IgG values that were associated with protection in our PREVENT-19 and Phase 3 UK trials. Similarly, wild-type neutralization responses increased approximately 4.3-fold compared to the peak response seen after Dose 2 (IC50 neutralization titers = 6,231 (95% CI: 4,738; 8,195)). This boosted value represents a 4.6 to 5.5-fold increase over the neutralization response associated with protection in our PREVENT-19 and Phase 3 UK trials. The data showed that functional hACE-2 inhibitory antibodies were induced with primary vaccination against Alpha (B.1.1.7), Beta (B.1.351) and Delta and that these levels increased 6- to 10-fold following a single 6-month boost with prototype vaccine. Additionally, functional ACE-2 binding inhibition antibodies cross-reactive with the Delta (B.1.617.2) variant strain were more than 6-fold higher than the primary vaccination series. The administration of booster doses was generally well-tolerated. Local and systemic reactogenicity increased between dose one, dose two, and dose three, with 90% of symptoms rated as mild or moderate after the third dose.

Mix-and-Match COVID-19 Vaccine Booster Trial ("Cov-Boost")

In July 2021, enrollment was completed in Cov-Boost, a mix-and-match (vaccine interchangeability) COVID-19 vaccine booster trial, for which we announced our participation in May 2021. The trial, which was initiated in June 2021, enrolled 2,886 participants aged 30 years and older. NVX-CoV2373 is one of seven COVID-19 vaccines that is being studied to evaluate the potential for providing a booster dose from different manufacturers to individuals who have previously received two doses of an authorized vaccine. Of the 2,886 participants enrolled, 230 participants received a full dose of NVX-CoV2373, while 216 participants received a half volume dose of NVX-CoV2373. The trial assesses the safety and immune response against COVID-19 provided by the various vaccine schedules. The trial is led by the University Hospital Southampton NHS

21

Foundation Trust and other UK National Institute for Health Research sites. Cov-Boost is receiving support from the UK government Vaccines Taskforce and Department of Health and Social Care.

Comparing COVID-19 Vaccine Schedule Combinations - Stage 2 ("Com-COV2")

In May 2021, enrollment was completed in Com-COV2, a newly expanded investigator-initiated Phase 2 clinical trial, for which we announced our participation in April 2021. The trial enrolled 1,072 adults aged 50 years and older who received their first vaccination during the previous 8-12 weeks. NVX-CoV2373 is one of four COVID-19 vaccines that is being studied to evaluate the potential for combined regimens that mix vaccines from different manufacturers to achieve immune protection against COVID-19. Participants received one of four different vaccines as a second dose, 359 of whom were administered NVX-CoV2373. The trial compares the immune system responses from those who receive a heterologous regimen to those who receive a homologous regimen. Participants in this non-inferiority study are followed for reactogenicity (safety) and immune responses. The trial is conducted by the University of Oxford and supported by the UK government Vaccines Taskforce. The MHRA and Joint Committee on Vaccination and Immunisation formally assesses the safety and efficacy of any new vaccination regiment before it is made available to the public.

NVX-CoV2373 Clinical Development Conducted by Partners

Phase 2/3 India

In March 2021, SIIPL initiated a Phase 2/3 clinical trial of NVX-CoV2373 in India. The initial cohort was fully enrolled in April 2021 and the total study includes approximately 1,600 participants aged 18 to 65 years.

Phase 1/2 Japan

In March 2021, Takeda Pharmaceutical Company Limited (“Takeda”) completed enrollment of a Phase 1/2 clinical trial of NVX-CoV2373 in Japan. This placebo-controlled trial will evaluate the immunogenicity and safety of NVX-CoV2373 in 200 participants aged 20 years and older.

Variant Strain (Monovalent and/or Bivalent) Vaccine Development

Our nanoparticle vaccine technology is purpose-built to rapidly address evolving infectious disease threats. In January 2021, we initiated development of new constructs against the emerging strains of COVID-19, and in February 2021, we selected variant strain vaccines for preclinical evaluation. We are currently evaluating multiple variant strain vaccine candidates, including a recombinant spike protein antigen based on the Beta (B.1.351) virus lineage (“rS-B.1.351”).

COVID-19 Beta (B.1.351) Variant Strain Vaccine ("rS-B.1.351")

In June 2021, we announced data from three complementary non-clinical studies of our rS-B.1.351 variant strain vaccine. The studies compared rS-B.1.351 to NVX-CoV2373 as standalone, in combination, and as a heterologous prime boost vaccine. The data showed that rS-B.1.351 demonstrated strong immunogenicity and protection against the Alpha (B.1.1.7) variant strain, Beta (B.1.351) variant strain and the original COVID-19 virus in animal studies. The findings also showed a broad array of cellular and humoral responses in animal models against all virus strains evaluated. Data from these studies have been submitted for peer review and are available ahead of publication via the preprint server on bioRxiv. We expect to initiate clinical evaluation of rS-B.1.351 in the fall of 2021.

In one study, thirty randomly selected human serum samples from Phase 2 clinical trial participants after their second dose of NVX-CoV2373 were assayed and analyzed for their ability to neutralize Alpha (B.1.1.7) and Beta (B.1.351) variant strains. The trial participants’ sera demonstrated a neutralizing capacity of the Alpha (B.1.1.7) variant strain equal to NVX-CoV2373, with a modest reduction in neutralizing capacity again the Beta (B.1.351) variant strain. These findings support the initial development and evaluation of a B.1.351-directed vaccine as a booster or in a combination vaccine approach.

In an additional preclinical study, mice were immunized with NVX-CoV2373 or rS-B.1.351 alone, in combination, or as a heterologous prime boost. Preclinical data from this study demonstrated that rS-B.1.351 was highly immunogenic and produced neutralizing antibodies.

In another preclinical study, non-human primates (“NHPs”) that were originally immunized with NVX-CoV2373 were boosted approximately one year later with one or two doses of rS-B.1.351. Preclinical data from this study showed that NHPs

22

boosted with rS-B.1.351 induced strong neutralizing immune responses to the original COVID-19 strain, as well as Alpha (B.1.1.7) and Beta (B.1.351) variant strains. Data from this preclinical study builds upon initial data announced in May 2021.

NVX-CoV2373 Regulatory and Licensure

As of August 2021, we continue to work to complete various Chemistry, Manufacturing and Controls ("CMC") requirements, which ensure that our manufacturing processes are in accordance with regulatory standards (see further discussion of our manufacturing activities below under the heading "NVX-CoV2373 Manufacturing and Supply"). Below is a summary and status of our regulatory processes through the date of filing this Form 10-Q.

In August 2021, we filed regulatory submissions in partnership with SIIPL for emergency use authorization ("EUA") in multiple markets. Regulatory submissions were filed with the Drugs Controller General of India ("DCGI"), as well as regulatory agencies in Indonesia and the Philippines. In addition to these filings, we expect to file a submission to the WHO for emergency use listing ("EUL") in August of 2021.

In April 2021, SK bioscience Ltd. ("SK bioscience") initiated the regulatory submission process in collaboration with Novavax to the MFDS for authorization of NVX-CoV2373.