|

|

Exhibit 99.1 |

FIRST QUARTER 2018

EARNINGS RELEASE

| ROYAL BANK OF CANADA REPORTS FIRST QUARTER 2018 RESULTS |

All amounts are in Canadian dollars and are based on financial statements prepared in compliance with International Accounting Standard 34 Interim Financial Reporting, unless otherwise noted. Effective November 1, 2017, we adopted IFRS 9 Financial Instruments. Prior period amounts are in accordance with IAS 39 Financial Instruments: Recognition and Measurement. Our Q1 2018 Report to Shareholders and Supplementary Financial Information are available at: http://www.rbc.com/investorrelations.

TORONTO, February 23, 2018 — Royal Bank of Canada (RY on TSX and NYSE) today reported net income of $3,012 million for the first quarter ended January 31, 2018, which includes the impact of the U.S. Tax Reform(1) of $178 million, or $0.12 per share, primarily related to the write-down of net deferred tax assets. Net income was down $15 million from a year ago and diluted EPS(2) of $2.01 was up 2%. Excluding last year’s specified item related to the gain on sale of the U.S. operations of Moneris(3), net income was up 7% and EPS was up 10% from a year ago.

Results in the quarter were driven by strong earnings in Personal & Commercial Banking, Capital Markets, Wealth Management, and Investor & Treasury Services. This quarter’s strong performance also reflects stable credit quality, with a provision for credit losses (PCL) on impaired loans ratio of 23 basis points (bps) compared to 22 bps a year ago, and a total PCL ratio of 24 bps this quarter.

Compared to last quarter, net income was up $175 million or 6%, mainly reflecting higher earnings in Capital Markets, Personal & Commercial Banking, Wealth Management and Investor & Treasury Services, partially offset by lower earnings in Insurance and the write-down associated with the U.S. Tax Reform(1).

“Strong client activity and volume growth across most businesses drove our first quarter earnings of $3 billion while we absorbed the write-down related to the U.S. Tax Reform. We invested in our businesses to support clients, and repurchased over $920 million of common shares. In addition, I am pleased to announce a 3% increase to our quarterly dividend,” said Dave McKay, RBC President and Chief Executive Officer. “Our strategy for sustainable growth is built on prudently managing risks and effectively deploying capital for strong returns through the cycle. We will continue to invest smartly and work hard to earn the trust of our clients, employees and communities.”

|

• Net income of $3,012 million • Diluted EPS of $2.01 • ROE(4) of 17.4% • CET1(5) ratio of 11.0% |

g 0% h 2% i 60 bps g 0% |

Excluding specified item(3): • Net income of $3,012 million • Diluted EPS of $2.01 • ROE of 17.4% |

h 7% h 10% h 70 bps | ||||||

|

|

• Net income of $3,012 million • Diluted EPS of $2.01 • ROE of 17.4% • CET1 ratio of 11.0% |

h 6% h 7% h 80 bps h 10 bps |

Q1 2018 Business Segment Performance

| Personal & Commercial Banking |

Net income of $1,521 million decreased $71 million or 4% from last year as the prior year included our share of the gain related to the sale of the U.S. operations of Moneris of $212 million (before- and after-tax). Excluding our share of the gain, net income increased $141 million or 10%(3), mainly due to average volume growth of 6%, higher spreads, higher fee-based revenue in Canadian Banking, and a gain related to the reorganization of Interac this quarter. These factors were partially offset by higher PCL and higher costs in support of business growth in Canadian Banking. The prior year also included an impairment related to properties held for sale in Caribbean Banking.

| (1) | In December 2017, the U.S. H.R. 1 (U.S. Tax Reform) was passed into law. |

| (2) | Earnings per share (EPS). |

| (3) | The specified item reflects our share of a gain in Q1 2017 related to the sale of the U.S. operations of Moneris Solutions Corporation (Moneris) to Vantiv, Inc., which was $212 million (before- and after-tax). Results and measures excluding the specified item are non-GAAP measures. For further information, including a reconciliation, refer to the Non-GAAP Measures section on page 3 of this Earnings Release. |

| (4) | Return on Equity (ROE). This measure does not have a standardized meaning under GAAP. For further information, refer to the Key performance and non-GAAP measures section of our Q1 2018 Report to Shareholders. |

| (5) | Common Equity Tier 1 (CET1) ratio. |

- 1 -

Compared to last quarter, Personal & Commercial Banking net income increased $117 million or 8%, largely reflecting higher fee-based revenue, a gain related to the reorganization of Interac this quarter, average volume growth of 1% and higher spreads. Seasonally lower marketing costs also contributed to the increase. These factors were partially offset by higher PCL.

| Wealth Management |

Net income of $597 million increased $167 million or 39% from a year ago, largely reflecting higher average fee-based assets, an increase in net interest income, and a lower effective tax rate reflecting benefits from the U.S. Tax Reform. These factors were partially offset by higher variable compensation on improved results, increased costs in support of business growth, and the impact of foreign exchange translation.

Compared to last quarter, net income increased $106 million or 22%, primarily reflecting higher average fee-based assets, a lower effective tax rate reflecting benefits from the U.S. Tax Reform, and increased transaction volumes. A favourable accounting adjustment related to City National Bank and higher net interest income also contributed to the increase. These factors were partially offset by increased costs in support of business growth and higher variable compensation on improved results.

| Insurance |

Net income of $127 million decreased $7 million or 5% from a year ago, primarily reflecting favourable updates in the prior year related to premium and mortality experience, and higher claims volumes in International Insurance. These factors were partially offset by higher investment-related gains and the impact of a new longevity reinsurance contract.

Compared to last quarter, net income decreased $138 million or 52% driven by favourable annual actuarial assumption updates in the prior quarter, and higher claims volumes.

| Investor & Treasury Services |

Net income of $219 million increased $5 million or 2% from a year ago, primarily due to growth in client deposits, increased revenue from our asset services business, the impact of foreign exchange translation, as well as higher funding and liquidity earnings. These factors were largely offset by higher investment in technology initiatives.

Compared to last quarter, net income increased $63 million or 40%, primarily due to higher funding and liquidity earnings and increased revenue from our asset services business.

| Capital Markets |

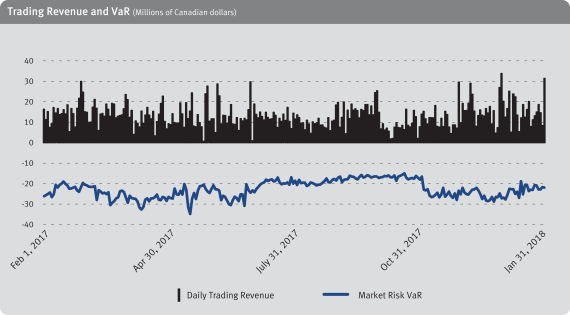

Net income of $748 million increased $86 million or 13% from a year ago, primarily due to a lower effective tax rate including the benefits from the U.S. Tax Reform and higher results in Corporate and Investment Banking and Global Markets. These factors were partially offset by increased costs due to higher variable compensation on improved results, litigation recoveries reducing costs in the prior year, higher regulatory spend and the impact of foreign exchange translation.

Compared to last quarter, net income increased $164 million or 28%, primarily due to higher results in Global Markets and a lower effective tax rate reflecting the benefits from the U.S. Tax Reform. These factors were partially offset by higher PCL and softer results in Municipal Banking.

| Corporate Support |

Net loss was $200 million in the current quarter, largely due to the impact of the U.S. Tax Reform of $178 million which was primarily related to the write-down of net deferred tax assets. Net loss in the prior quarter was $63 million, largely reflecting net unfavourable tax adjustments, severance and related charges, and charges associated with our real estate portfolio. Net loss was $5 million in the prior year, largely reflecting asset/liability management activities.

| Other Highlights |

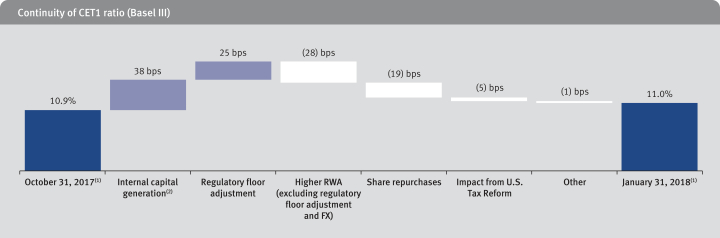

Capital – As at January 31, 2018, our CET1 ratio was 11.0%, up 10 bps from last quarter, mainly reflecting internal capital generation and a lower regulatory floor, partially offset by higher risk-weighted assets due to business growth and share repurchases.

Credit Quality – Total PCL of $334 million increased $40 million or 14% from a year ago, mainly due to higher provisions in Personal & Commercial Banking which were partially offset by lower provisions in Wealth Management and Capital Markets. PCL on loans also reflects the adoption of IFRS 9 on November 1, 2017. The PCL ratio on loans of 24 bps increased by 2 bps.

Compared to last quarter, PCL increased $100 million or 43%, mainly due to higher provisions in Capital Markets and Personal & Commercial Banking. PCL on loans also reflects the adoption of IFRS 9, as noted above. The PCL ratio on loans increased 7 bps.

- 2 -

Non-GAAP Measures

Results and measures excluding the specified item outlined below are non-GAAP measures:

| • | For the three months ended January 31, 2017, our share of a gain related to the sale by our payment processing joint venture Moneris of its U.S. operations to Vantiv, Inc., which was $212 million (before- and after-tax) and recorded in Personal & Commercial Banking. |

Given the nature and purpose of our management reporting framework, we use and report certain non-GAAP financial measures, which are not defined, do not have a standardized meaning under GAAP, and may not be comparable with similar information disclosed by other financial institutions. We believe that excluding these specified items from our results is more reflective of our ongoing operating results, will provide readers with a better understanding of management’s perspective on our performance, and will enhance the comparability of our comparative periods. For further information, refer to the Key performance and non-GAAP measures section of our Q1 2018 Report to Shareholders.

| Net Income, excluding specified item |

||||||||||||

| For the three months ended January 31, 2017 | ||||||||||||

| (Millions of Canadian dollars, except per share and percentage amounts) | Reported | |

Gain related to the sale by Moneris(1) |

|

Adjusted | |||||||

| Net income |

$ | 3,027 | ($212) | $ | 2,815 | |||||||

| Basic earnings per share |

$ | 1.98 | ($0.14) | $ | 1.84 | |||||||

| Diluted earnings per share |

$ | 1.97 | ($0.14) | $ | 1.83 | |||||||

| ROE |

18.0% | 16.7% | ||||||||||

|

Personal & Commercial Banking net income, excluding specified item |

||||||||||||

| For the three months ended January 31, 2017 | ||||||||||||

| (Millions of Canadian dollars) | Reported | |

Gain related to the sale by Moneris(1) |

|

Adjusted | |||||||

| Net income |

$ | 1,592 | ($212) | $ | 1,380 | |||||||

| (1) | Includes foreign currency translation. |

- 3 -

| CAUTION REGARDING FORWARD-LOOKING STATEMENTS |

From time to time, we make written or oral forward-looking statements within the meaning of certain securities laws, including the “safe harbour” provisions of the United States Private Securities Litigation Reform Act of 1995 and any applicable Canadian securities legislation. We may make forward-looking statements in this Earnings Release, in filings with Canadian regulators or the U.S. Securities and Exchange Commission (SEC), in reports to shareholders and in other communications. Forward-looking statements include, but are not limited to, statements relating to our financial performance objectives, vision and strategic goals, and include our President and Chief Executive Officer’s statements. The forward-looking information contained in this Earnings Release is presented for the purpose of assisting the holders of our securities and financial analysts in understanding our financial position and results of operations as at and for the periods ended on the dates presented, our financial performance objectives, vision and strategic goals, and may not be appropriate for other purposes. Forward-looking statements are typically identified by words such as “believe”, “expect”, “foresee”, “forecast”, “anticipate”, “intend”, “estimate”, “goal”, “plan” and “project” and similar expressions of future or conditional verbs such as “will”, “may”, “should”, “could” or “would”.

By their very nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties, which give rise to the possibility that our predictions, forecasts, projections, expectations or conclusions will not prove to be accurate, that our assumptions may not be correct and that our financial performance objectives, vision and strategic goals will not be achieved. We caution readers not to place undue reliance on these statements as a number of risk factors could cause our actual results to differ materially from the expectations expressed in such forward-looking statements. These factors – many of which are beyond our control and the effects of which can be difficult to predict – include: credit, market, liquidity and funding, insurance, operational, regulatory compliance, strategic, reputation, legal and regulatory environment, competitive and systemic risks and other risks discussed in the risks sections of our 2017 Annual Report and the Risk management section of our Q1 2018 Report to Shareholder; including global uncertainty and volatility, elevated Canadian housing prices and household indebtedness, information technology and cyber risk, including the risk of cyber-attacks or other information security events at or impacting our service providers or other third parties with whom we interact, regulatory change, technological innovation and non-traditional competitors, global environmental policy and climate change, changes in consumer behaviour, the end of quantitative easing, the business and economic conditions in the geographic regions in which we operate, the effects of changes in government fiscal, monetary and other policies, tax risk and transparency and environmental and social risk.

We caution that the foregoing list of risk factors is not exhaustive and other factors could also adversely affect our results. When relying on our forward-looking statements to make decisions with respect to us, investors and others should carefully consider the foregoing factors and other uncertainties and potential events. Material economic assumptions underlying the forward looking-statements contained in this Earnings Release are set out in the Economic, market and regulatory review and outlook section and for each business segment under the Strategic priorities and Outlook headings in our 2017 Annual Report, as updated by the Economic, market and regulatory review and outlook section of our Q1 2018 Report to Shareholders. Except as required by law, we do not undertake to update any forward-looking statement, whether written or oral, that may be made from time to time by us or on our behalf.

Additional information about these and other factors can be found in the risks sections of our 2017 Annual Report and the Risk management section of our Q1 2018 Report to Shareholders.

Information contained in or otherwise accessible through the websites mentioned does not form part of this Earnings Release. All references in this Earnings Release to websites are inactive textual references and are for your information only.

ACCESS TO QUARTERLY RESULTS MATERIALS

Interested investors, the media and others may review this quarterly Earnings Release, quarterly results slides, supplementary financial information and our Q1 2018 Report to Shareholders on our website at rbc.com/investorrelations.

Quarterly conference call and webcast presentation

Our quarterly conference call is scheduled for Friday, February 23, 2018 at 8:00 a.m. (EST) and will feature a presentation about our first quarter results by RBC executives. It will be followed by a question and answer period with analysts.

Interested parties can access the call live on a listen-only basis at: www.rbc.com/investorrelations/ir_events_presentations.html or by telephone (416-340-2217, 866-696-5910, passcode 9222187#). Please call between 7:50 a.m. and 7:55 a.m. (EST).

Management’s comments on results will be posted on RBC’s website shortly following the call. A recording will be available by 5:00 p.m. (EST) from Friday, February 23, 2018 until May 23, 2018 at rbc.com/investorrelations/quarterly-financial-statements.html or by telephone (905-694-9451 or 800-408-3053, passcode 8783009#).

Media Relations Contacts

Tanis Feasby, Vice President, Communications, Wealth Management, Insurance & Finance, tanis.feasby@rbc.com, 416-955-5172

Maria McGee, Manager, Financial Communications, maria.mcgee@rbc.com, 416-974-2789

Investor Relations Contacts

Dave Mun, SVP & Head, Investor Relations, dave.mun@rbc.com, 416-974-4924

Asim Imran, Senior Director, Investor Relations, asim.imran@rbc.com, 416-955-7804

Jennifer Nugent, Senior Director, Investor Relations, jennifer.nugent@rbc.com, 416-955-7805

ABOUT RBC

Royal Bank of Canada is a global financial institution with a purpose-driven, principles-led approach to delivering leading performance. Our success comes from the 81,000+ employees who bring our vision, values and strategy to life so we can help our clients thrive and communities prosper. As Canada’s biggest bank, and one of the largest in the world based on market capitalization, we have a diversified business model with a focus on innovation and providing exceptional experiences to our 16 million clients in Canada, the U.S. and 34 other countries. Learn more at rbc.com.

We are proud to support a broad range of community initiatives through donations, community investments and employee volunteer activities. See how at http://www.rbc.com/community-sustainability/.

Trademarks used in this Earnings Release include the LION & GLOBE Symbol, ROYAL BANK OF CANADA and RBC which are trademarks of Royal Bank of Canada used by Royal Bank of Canada and/or by its subsidiaries under license. All other trademarks mentioned in this Earnings Release, which are not the property of Royal Bank of Canada, are owned by their respective holders.

- 4 -